Embed Size (px)

Citation preview

Slide 1.1

NATURE OF A PARTNERSHIP

Being a sole trader means

a) being in control of the business

b) being responsible for all the decision making

c) being entitled to all the profits of the business or having to suffer all losses.

• A sole trader can be restrictive in two main ways as follows

a) Limited time available (i.e. hours put in by the sole trader himself)

b) Limited resources available (i.e. capital contributed by the sole trader, although loans etc. may be available).

Slide 1.2

NATURE OF A PARTNERSHIP CONTINUED • Forming a partnership may lift these restrictions in

that:

a) More man hours and capital become available

b) It may also become easier to obtain a loan.

• However, in a partnership no one person has total

control nor a right to all the profits.

• Partnerships are commonly found in:

a) In family businesses

b) Where two or more sole traders have come

together to form a partnership.

c) In professional firms such as lawyers , accountants

and doctors

Slide 1.3

REASONS FOR FORMING PARTNERSHIPS

The capital required is more than one

person can provide.

The experience or ability required to

manage the business cannot be found in

one person alone.

Many people want to share management

instead of doing everything on their own.

Very often the partners will be members of

the same family.

Slide 1.4

NATURE OF A PARTNERSHIP

A partnership has the following characteristics:

a) It is formed to make profits.

b) It must obey the law as given in the Partnership Act

of 1890,if there is a limited partner it must also

comply with the limited Partnership Act of 1907.

c) Normally there can be a minimum of two partners

and a maximum of twenty partners. Exception are

banks where there cannot be more than ten partners,

and there is no maximum for firms of accountants,

solicitors ,stock exchange members, surveyors

,auctioneers ,valuers ,estate agents, land agents

,estate managers or insurance brokers

Slide 1.5

NATURE OF A PARTNERSHIP

d) Each partner (except for limited partners)

must pay their share of any debts that the

partnership could not pay. If necessary they

could be forced to sell all their private

possessions to pay their share of the debts.

This can be said to be unlimited liability.

e) Partners who are not limited partners are

known as general partners.

Slide 1.6

DEFINITION OF A PARTNERSHIP The partnership Act of 1890 defines a partnership as

follows:

“The relation which subsists between persons carrying on a business in common with a view to profit.”

• In keeping with this definition the essential elements of a partnership are as follows:

a) There must be a business. Under the term we include trades of all kinds and professions.

b) The business must be carried on in common.

c) The partners must carry on the business with the object of gain. There are many associations of persons where operations in common are carried on, but as they are not carried on with the view to profit they are not to be considered as partnerships, e.g. a sports club.

Slide 1.7

TYPES OF PARTNERSHIPS There are two types of partnership as follows:

a) Ordinary or general partnership:

• in this type of partnership, each partner

contributes an agreed amount of capital,

• is entitled to take part in the running of the

business (but is not entitled to a salary for so

doing, unless specially agreed)

• is also entitled to receive a specified share of

the profits or losses.

• Each partner is jointly liable to the extent of his

full estate for all the debts of the partnership.

Slide 1.8

TYPES OF PARTNERSHIPS CONTINUED

b) Limited partnerships:

• Limited partnerships were introduced by the

Limited partnership Act 1907.

Slide 1.9

LIMITED PARTNERSHIPS Limited liability partnerships are partnerships containing

one or more limited partners. Limited partners are not

liable for the debts of the partnership.

They have the following characteristics and restrictions

on their role in the partnership:

a) Their liability for the debts of the partnership is limited

to the capital they have put in. They can lose that

capital but they cannot be asked for any money to pay

the debts unless they contravene the regulations

relating to their involvement in the partnership.

b) They are not allowed to take out or receive back any

part of their contributions to the partnership during its

lifetime.

Slide 1.10

LIMITED PARTNERSHIPS

c) They are not allowed to take part in the management

of the partnership or to have the power to make the

partnership take a decision. If they do, they become

liable for all the debts and obligations of the

partnership up to the amount taken out or received

back or incurred while they were taking part in the

management of the partnership.

d) All the partners cannot be limited partners, so there

must be at least one general partner with unlimited

liability.

Slide 1.11

TYPES OF PARTNERS There are four types of partners as follows:

a) Active partner: one who takes an active

part in the business.

b) Dormant or sleeping partner: one who

retires from active participation in the

business but who leaves capital in the

business and receives a reduced share of

the profits.

Slide 1.12

TYPES OF PARTNERS CONTINUED

c) Quasi-partner: One who retires and leaves

capital in the business as a loan.Interest,based

on a proportion is credited to the retired partner's

account each year and debited as an expense to

profit and loss account. This type of partner

would be more accurately described as a

deferred creditor ,i.e. one who receives payment

after all other creditors.

d) Limited partner: one who is excluded from

active participation and who is liable only up to

the amount he has contributed as capital.

Slide 1.13

PARTNERSHIP AGREEMENT To show the terms of that partnership (Smith V

Jeyes).

Where the terms of the partnership are embodied in writing, they may be varied by consent of all the partners.

They need not be in writing.

However, it is better if a written agreement is drawn up by a lawyer or Accountant.

A written agreement will mean fewer problems between partners.

It also means less confusion about what has been agreed.

Slide 1.14

PARTNERSHIP AGREEMENT

CONTINUED

It is not necessary for a partnership contract to be in any special form.

In practice,however,the terms of the partnership are normally drawn up in writing(usually under seal) though an unsigned document drawn up by one of the partners and acted upon by the others has been held to constitute the terms of the partnership (Baxter VS West ).

Where no written document sets out the terms of the partnership, the method of dealing which the partners adopt is admissible in evidence.

USUAL PROVISIONS OF THE

PARTNERSHIP AGREEMENT

•A properly drawn partnership agreement would

normally contain the following provisions:

1. Nature of the business to be carried on by the

firm.

2.Capital and property of the partnership, and

the respective capitals of each partner.

3.How the profits should be divided between the

partners, and how the losses should be shared.

4. Payment of interest on capital, and the

drawings rights of the partners if any.

Slide 1.16

USUAL PROVISIONS OF THE PARTNERSHIP

AGREEMENT

5. Keeping of accounts and how they should be

audited.

6. Powers of partners

7.Provision for dissolution of the partnership.

8.How the value of goodwill should be determined

upon the retirement or death of a partner.

9. Method to be employed in computing the

amount payable to an out-going partner, or to the

representatives of a deceased partner

Slide 1.17

USUAL PROVISIONS OF THE PARTNERSHIP

AGREEMENT CONTINUED

10. Right of the majority of partners to expel one

their members.

11.A clause to the effect that disputes to be

submitted to arbitration.

WHERE NO PARTNERSHIP AGREEMENT EXISTS

If no prior agreement exists then section 24 of the

1890 Partnership Act will apply and it states that:

1. Profits and losses are to be shared equally.

2. There is to be no interest allowed on capital.

3. No interest is to be charged on drawings.

4. Salaries are not allowed.

5. Partners are entitled to 5% interest on any

contributions in excess of the agreed capital

contributions.

Slide 1.19

CAPITAL CONTRIBUTIONS AND

SHARING OF PROFITS

a) Capital contributions:

• partners need not contribute equal amounts of

capital.

• What matters is how much capital each partner

agrees to contribute.

• It is not unusual for partners to increase the

amount of capital they have invested in the

partnership.

Slide 1.20

CAPITAL CONTRIBUTIONS AND SHARING

OF PROFITS

b) Partners can agree to share profits in any ratio

or any way that they may wish.

• However, it is often thought by students profits

should be shared in the same ratio as that in

which capital is contributed.

c) If work to be done by each partner is of equal

value but the capital contributed is unequal, it

is reasonable to pay interest on the partner ‘s

capital out of partnership profits.

Slide 1.21

INTEREST ON CAPITAL • This interest is treated as deduction prior to the

calculation of profits and their distribution

among the partners according to the profit

sharing ratio.

• The rate of interest is a matter of agreement

between the partners.

• Often it will be based upon the return which

they would have received if they had invested

the capital elsewhere.

Slide 1.22

INTEREST ON DRAWINGS It is in the best interest of the partnership if cash is

withdrawn from it by the partners in accordance with the two basic principles

a) As little as possible

b) As late as possible.

• The more the cash is left in the partnership, the more expansion can be financed, the greater the economies of having ample cash to take advantage of bargains and of not missing cash discounts because cash is not available.

• To deter the partners from taking out cash unnecessarily the concept can be used of charging the partners interest on each withdrawal ,calculated from the date of withdrawal to the end of the financial year.

Slide 1.23

INTEREST ON DRAWINGS

The amount charged to them helps swell the

profits divisible between the partners. The

rate of interest should be sufficient to

achieve this without being to harsh.

Allen and Beet are in partnership and have

decided to charge interest on drawings at 5

percent per annum, and their year end was

31 December .Calculate interest on

drawings chargeable to each partner for the

Year ended 31 December 2012.

Slide 1.24

SOLUTION EXAMPLE INTEREST ON DRAWINGS

ALLEN

Drawings Interest

Date £ Calculation of interest £

1 January 2,000

£2,000 x 5% x 12 months/12

months 100

1 March 4,800

£4,800 x 5% x 10 months/12

months 200

1 MAY 2,400 £2,400 x 5% x 8 months/12 months 80

1 July 4,800 £4,800 x 5% x 6 months/12 months 120

1 October 1,600 £1,600 x 5% x 3 months/12 months 20

Interest charged to Allen 520

BEET

Drawings Interest

Date £ Calculation of interest £

1 January 1,200 £1,200 x 5% x 12 months/12 months 60

1 August 9,600 £9,600 x 5% x 5months/12 months 200

1 December 4,800 £4,800 x 5% x 1 months/12 months 20

Interest charged to Beet 280

Slide 1.25

PARTNERSHIP SALARIES AND PERFROAMNEC

RELATED BONUSES

Partnership salaries: One partner may have more

responsibility or tasks than the others. A reward for this,

rather than change the profit and loss sharing ratio, the

partner may have a partnership salary which is

deducted before sharing the balance of profits.

Performance related payments to partners:

partners may agree that commissions or performance

related bonuses be payable to some or all of the

partners linked to their individual performance. As with

salaries ,these would be deducted before sharing the

balance of profits.

Slide 1.26

INCOME STATEMENT ,AND APPROPRIATION

ACCOUNT In the case of a partnership, the income statement (profit

and loss account)is really in two sections.

a) The first section is drawn up as already indicated

earlier like for a sole trader and is debited with the net

profit made (or credited with the net loss).

To complete the double entry, the amount of net profit is

then carried down as an ordinary balance and credited to

the second section of the income statement. (N.B. a net

loss would be carried down to the debit side of this

section.) It is this second section that shows how the net

profit is allocated to the various partners, and it is called

the profit and loss appropriation account, or just the

appropriation account.

Slide 1.27

DOUBLE ENTRY FOR THE APPROPRIATION

ACCOUNT The appropriation account starts with profits from the

profit and loss account or income which is accounted for as follows:

If net profit

Dr Profit and loss account or income statement

Cr Appropriation account

If a net loss

Dr Appropriation account

Cr Profit and loss account or income statement

• The interest on drawings is transferred to the appropriation account as follows;

Dr Drawings account

Cr appropriation account

Slide 1.28

DOUBLE ENTRY FOR THE APPROPRIATION

ACCOUNT

Then all the appropriations or share of profits and

debited to the appropriation account as follows:

a) Salary payable to the any of the partners

Dr appropriation account

Cr Current account

b) Interest on capital payable to the partners

Dr appropriation account

Cr Current account

c) The balancing figure in the appropriation account is

the balance of net profit to be shared or net loss to be

shared in the profit and loss sharing ratio.

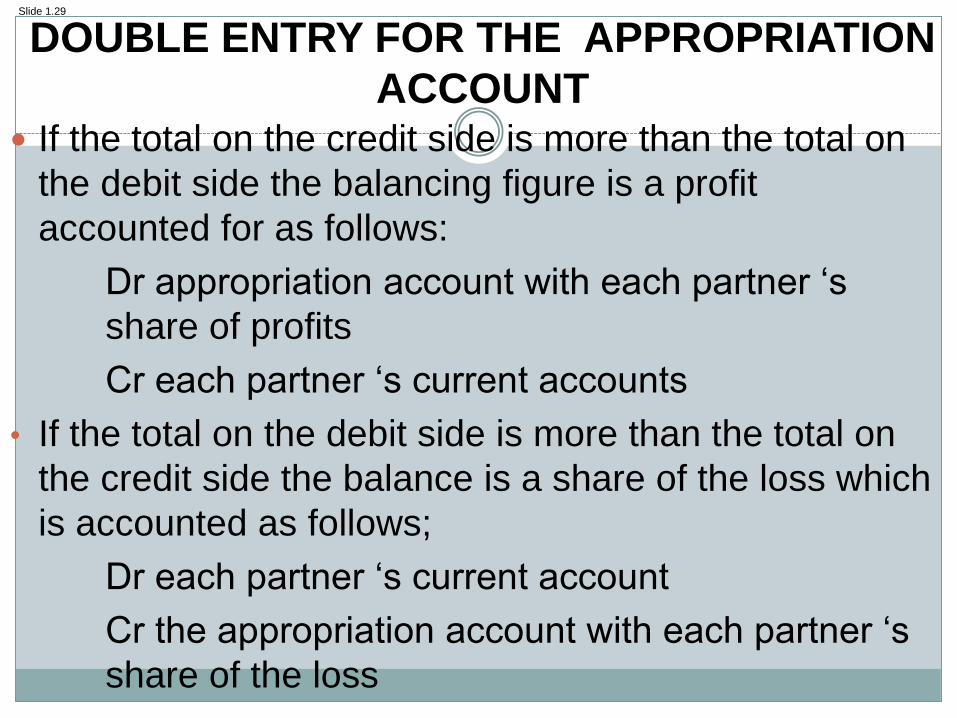

Slide 1.29

DOUBLE ENTRY FOR THE APPROPRIATION

ACCOUNT If the total on the credit side is more than the total on

the debit side the balancing figure is a profit

accounted for as follows:

Dr appropriation account with each partner ‘s

share of profits

Cr each partner ‘s current accounts

• If the total on the debit side is more than the total on

the credit side the balance is a share of the loss which

is accounted as follows;

Dr each partner ‘s current account

Cr the appropriation account with each partner ‘s

share of the loss

Slide 1.30

EXAMPLE APPROPRIATION ACCOUNT Taylor and Clarke have been in partnership for one year

sharing profits and losses in the ratio of 3 to 2

respectively.

They are entitled to 5 percent per annum interest on

capitals, Taylor having $20,000 capital and Clarke

$60,000.

Cash drawings during the year amounted to Taylor

$15,000 and Clarke $26,000.

Clarke is to have a salary of $15,000.

They charge interest on drawings , Taylor being charged

$500 and Clarke $1,000.

The net profit before any distribution to the partners

amounted to $50,000 for the year ended 31 December

2013.

Slide 1.31

APPROPRIATION ACCOUNT AS PART OF

FINANCIAL STATEMENTS

The appropriation account of a partnership is prepared as an extension to the income when preparing financial statements.

This means the income statement of a partnership will be dawn the normal like in sole trader business but for the partnership an extra section called the appropriation section is shown.

So for exam purpose you prepare an appropriation account as a continuation from where the net profit of the income statement is calculated adding the interest on drawings and subtracting the partner’s salary and the interest on capital.

The remaining profits or losses are shared according to the profit and loss sharing ratios.

Slide 1.32

FORMAT APPROPRIATION SECTION OF

INCOME STATEMENT APPROPRIATION SECTION OF THE INCOME STATEMENT

£ £ £

Net profit XXX

Add:Interest on drawings

Taylor XXX

Clarke XXX

XXX

XXX

Less:

Salary :clarke XXX

Interest on capitals

Taylor XXX

Clarke XXX

XXX XXX

XXX

Balance share of profits

Taylor (3/5 x XXXX) XXXX

Clarke (2/5 x XXXX) XXXX

XXXX

Slide 1.33

FIXED ACCOUNTS AND CURRENT ACCOUNTS

The capital account for each partner remains year by

year at the figure of capital put in the partnership by

the partners.

The profits ,interest on capital and the salaries to

which the partner may be entitled are then credited to

a separate current account for the partner, and the

drawings and interest on drawings are debited to it.

The balance of the current account at the end of the

financial year will represent the amount of undrawn

(or withdrawn) profits.

A credit balance will be undrawn profits ,while a debit

balance will be drawings in excess of the profits to

which the partner was entitled.

Slide 1.34

FIXED CAPITAL ACCOUNTS AND CURRENT

ACCOUNT

Credit balance on the current account is added to

capital in the statement of financial position and

debit balance is subtracted from capital in the

statement of financial position.

For examination purposes the capital and current

accounts of the partners should be drawn in

columnar form i.e. side by side on both the debit

and the credit side.

Show the capital and current account of Taylor and

Clarke in columnar forma and prepare a statement

of financial position extract that shows how the

current accounts and capital accounts will appear.

Slide 1.35

PARTNERSHIP ACCOUNTS EXAMPLE ONE

Rush and Aldridge are in partnership sharing

profits and losses in the ratio 3:2 respectively. The

following list of balances has been extracted from

the books, of the business, for the year ended 30

November 2014.

Slide 1.36

PARTNERSHIP ACCOUNTS EXAMPLE ONE

K

Land at cost 120,000

Fixtures and fittings (cost) 70,000

Fixtures and fittings (depreciation) 20,000

Creditors 17,000

Debtors 21,000

Balance at bank (cr) 7,500

Bank loan 20,000

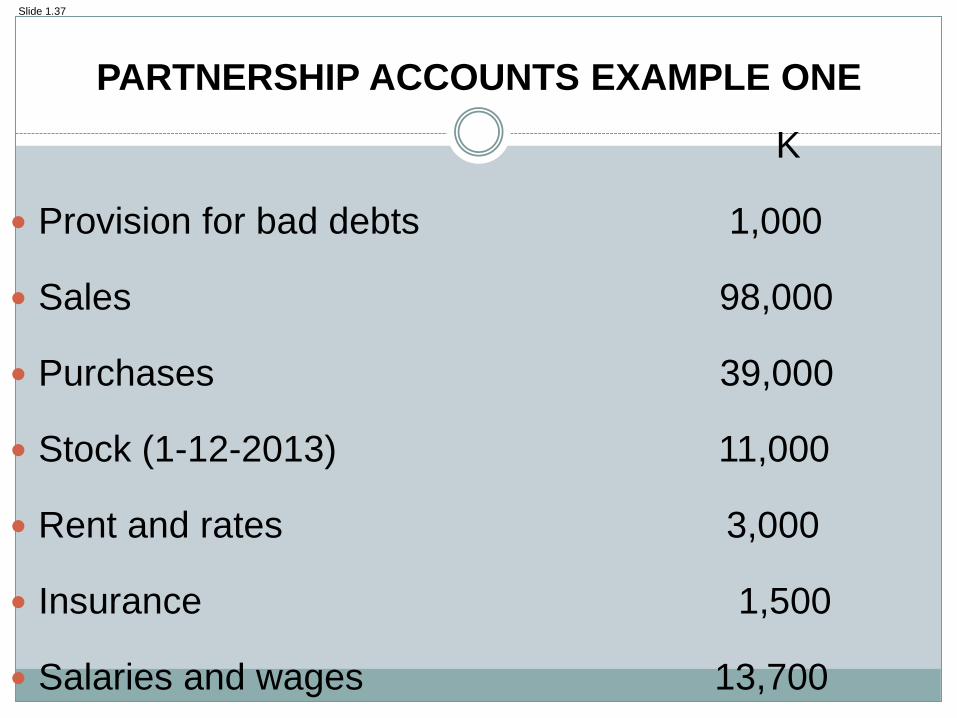

Slide 1.37

PARTNERSHIP ACCOUNTS EXAMPLE ONE

K

Provision for bad debts 1,000

Sales 98,000

Purchases 39,000

Stock (1-12-2013) 11,000

Rent and rates 3,000

Insurance 1,500

Salaries and wages 13,700

Slide 1.38

PARTNERSHIP ACCOUNTS EXAMPLE ONE K

Office expenses 2,800

Heating and lighting 1,750

Advertising 900

Capital account – Rush 80,000

– Aldridge 50,000

Current account – Rush (cr) 3,850

– Aldridge (dr) (2,000)

Drawings – Rush 3,700

– Aldridge 7,000

Slide 1.39

PARTNERSHIP ACCOUNTS EXAMPLE ONE The following information is also available:

– At 30.11.2014:

– Closing stock K13, 800

– Rent outstanding K500

– Salaries outstanding K1,120

– K80 insurance prepaid for the following year

– Provision for bad debts needs increasing to K1,150

– Interest of K2,000 on the bank loan needs to be

included in the accounts

Slide 1.40

PARTNERSHIP ACCOUNTS EXAMPLE ONE

– Fixtures and fittings are depreciated at 10% on a

reducing balance basis

– Partnership salaries are as follows:

– Rush K8,000

– Aldridge K2,000

– Interest on capital is allowed at 10%

Slide 1.41

PARTNERSHIP ACCOUNTS EXAMPLE ONE

Required:

a) From the list of balances (at 30-11-2014) prepare

the trial balance for Rush and Aldridge.

(5 marks)

b) (Prepare a trading and profit and loss account and

a balance sheet as at 30 November 2014.

(25 marks)

(Total 30 marks)

Slide 1.42

PRACTICE QUESTION

Dixon and Phillips are in partnership sharing

profits and losses in the ratio 2:1

respectively. The following trial balance has

been drawn up at 31 March 214.

Slide 1.43

DR CR

K K

Land - at cost 100,000

Buildings - at cost 126,000

Fixtures - at cost 8,000

Cumulative depreciation (at 1 April 2014)

- buildings 9,450

- fixtures 1,600

Stock (at 1 April 2014) 2,100

Debtors 4,900

Creditors 1,300

Slide 1.44

Bank overdraft 840

Sales 78,600

Purchases 31,700

Rent 1,120

Rates 2,360

Insurance 3,540

Heating 8,020

Salaries and wages 14,290

Slide 1.45

Capital - Dixon 150,000

- Phillips 75,000

Current - Dixon 1,750

- Phillips 2,650

Drawings - Dixon 4,180

- Phillips 6,180

316,790 316,790

Slide 1.46

The following information is also available:

1. Closing stock at 31 March 2009 was K4,240.

2. Rent accrued at 31 March 2009 was K400.

3. Insurance prepaid at 31 March 2009 was K720.

4. Depreciation was to be provided as follows:

- buildings at 2.5% per year on a straight line basis assuming nil

residual value.

- fixtures at 20% per year on a reducing balance basis.

5. Partnership salaries are as follows:

- Dixon K2,000 - Phillips K500

6. Interest on capital is allowed at 5% per year.

Slide 1.47

Required:

(a) Prepare the trading, profi t and loss account and

appropriation account for Dixon and

Phillips for the year ended 31 March 2014. (12

marks)

(b) Prepare a balance sheet for Dixon and Phillips at

31 March 2014. (13 marks)

(Total 25 marks)

![Greater Owensboro Life Science Partnership Slide[1]](https://img.pdfslide.net/doc/110x75/55615b62d8b42a5f4b8b4767/greater-owensboro-life-science-partnership-slide1.jpg)