Embed Size (px)

Citation preview

Slide 12.1

Share Capital, Distributable Profits and Reduction of Capital

Chapter 12

Slide 12.2

Objectives

After completing this chapter, you should be able to:• describe the reasons for the issue of shares;• describe the rights of different classes of shares;• prepare accounting entries for issue of shares;• explain the rules relating to distributable profits;• explain when capital may be reduced;• prepare accounting entries for reduction of capital;• discuss the rights of different parties on a capital reduction.

Slide 12.3

Total shareholders’ funds

• Issued share capital

• Non-distributable reserves

• Distributable reserves.

Slide 12.4

Nature of company shares and share transactions

Issues involving contributions from and distributions to company shareholders

Equity is defined as ‘... The residual interest in the assets of the

entity after deducting all its liabilities

Or, equity = assets – liabilitiesDoes this mean that equity is the result of

the activity of assets and liabilities?

Slide 12.5

Issued share capital

Ordinary Risk Residual profit

Preference Fixed rate dividend Specific prior rights

Dividend Return of capital.

Slide 12.6

Non-distributable reserves

Statutory Share premium Capital redemption

Contractual Restrictions within memorandum.

Slide 12.7

Distributable reserves

Retained profitsTreatment of unrealised profits Importance of EPS figure when deciding on

capital structure.

Slide 12.8

Reasons for share issues

Raising fundsOn acquisitionsIn lieu of dividendsDirector/Employee share option schemes.

Slide 12.9

Methods of raising equity capital

An offer for subscriptionA placingA rights issue.

Slide 12.10

Possible rights for preference shares

CumulativeNon-cumulativeParticipatingRedeemableConvertible.

Slide 12.11

Accounting for share issues

Accounting procedure Business Ventures Ltd issued a prospectus for 2

million ordinary shares. The issue is to the public at $3.00 a share, with

$0.80 per share payable on application. A further $1.20 is payable on allotment, and the

final $1.00 when called. We shall assume the company received

applications for exactly 2 million shares

Slide 12.12

Accounting for share issues

The general process is: Initial application Allotment (or issue) Calls

Slide 12.13

Accounting for share issues

Initial application investors are not entitled to any shares until the

directors make a formal allotment all share application monies must be held in a

trust account the journal entry is:

Slide 12.14

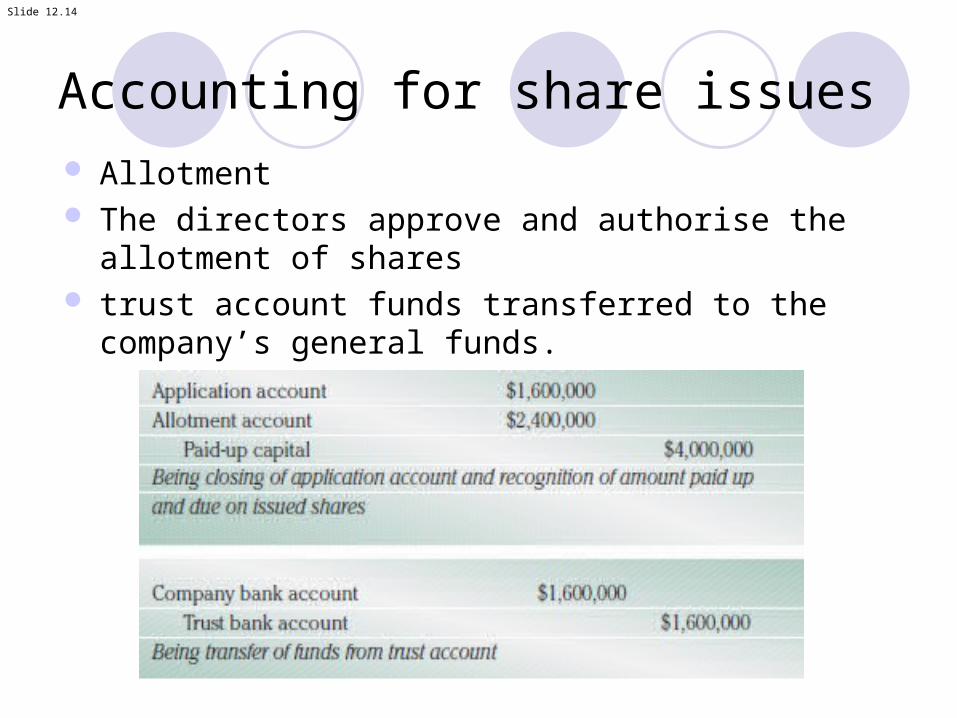

Accounting for share issues Allotment The directors approve and authorise the allotment of

shares trust account funds transferred to the company’s general

funds.

Slide 12.15

Accounting for share issues

trust bank account can now be closed Net revenue earned on the application monies is

used to defray preliminary expenses Applicants are now shareholders, and are liable to

pay the second instalment of $1.20 per share. The allotment account entry anticipates receipt of this instalment. Journal entry is:

Slide 12.16

Accounting for share issues

Why are share issues not always fully paid allotment? Company may not require all funds immediately eg.

an expansion plan which may unfold over an extended period of time

Investors holding shares that are not fully paid have a liability for the uncalled capital

Calls If an investor sells partly paid shares the liability for

the uncalled capital passes to the purchaser Instalments subsequent to allotment are termed calls

Slide 12.17

Accounting for share issues

When a call is made, the journal entry is:

When the monies are received, the entry is:

Slide 12.18

Capital maintenance

Rules to protect creditors Directors’ discretion on dividend policy Effect of non-distributable status.

Slide 12.19

Creditor protection – why necessary?

Unincorporated businesses Unlimited liability

Limited liability companies Restricted rights against shareholders.

Slide 12.20

Creditor risks

Business risk Protection against fraud No protection against normal commercial risk

Risk of shareholders being paid ahead of creditors Rules requiring minimum share capital Rules giving criteria for distributable profits.

Slide 12.21

Distributable profits – private companies

UK Companies Act definition Unrealised profits cannot be distributed No difference between realised revenue and

realised capital profits Realised losses must be taken into account.

Slide 12.22

Maintain permanent capital as at end of the previous year

Distributable Retained realised profit brought forward Adjusted for net realised current year profit.

Distributable profits – private companies (Continued)

Slide 12.23

Undistributable reserves are Share capital Statutory undistributable reserves Contractual undistributable reserves Excess of accumulated unrealised profit over

accumulated unrealised losses.

Distributable profits – public companies

Slide 12.24

The solvency test

In New Zealand, before making any distribution to shareholders, section 52 of the Companies Act 1993 requires the directors to test the solvency of the company

The solvency test is conducted on the assumption that the distribution has been made. If the company cannot meet the solvency test on this assumption, the distribution must not be made.

There are two parts to the solvency test: a test of liquidity, and a test of financial position.

Slide 12.25

The solvency test

Liquidity test Can the company pay its debts as they fall due in its

normal business operations? The directors must ensure that the necessary cash flow is available, as the company’s creditors always take precedence over shareholders.

It is not enough that a company has a lot of assets. It must be able to fund in cash any liability as it falls due in the normal course of business.

The liquidity test looks at the assets that can be turned to cash in the normal course of business – current assets, eg. accounts receivable, inventory, and call deposits – and the robustness of its revenue stream(s).

Slide 12.26

The solvency test

Here is part of Company A’s Balance Sheet. Can it pay $200,000 of dividends to shareholders?

Slide 12.27

The solvency test

The directors have proposed a distribution of $200,000. Can it pass the liquidity test?

Immediately after the distribution was made, the company would have liquid assets of $173,000 ($373,000 – $200,000 = $173,000) to meet liabilities of $140,000.

It passes the liquidity test.

Slide 12.28

The solvency test

Financial position test Part 2 of the solvency test looks at? The overall financial structure of the company. It is a valuation exercise to establish that the

company’s assets exceed its liabilities as at the date of the distribution.

If Company A has the following additional non-current assets and liabilities, does it still meet the solvency test?

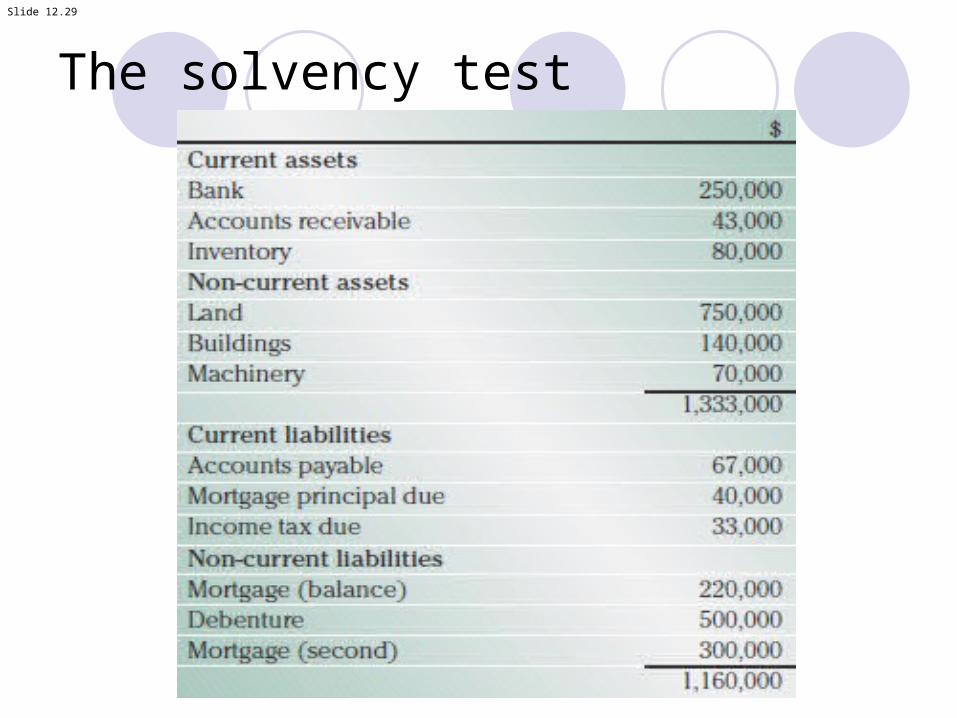

Slide 12.29

The solvency test

Slide 12.30

The solvency test

Immediately after the distribution, the company would have assets of $1,133,000 to meet liabilities of $1,160,000. It fails the financial position (Balance Sheet) test, and accordingly the distribution of $200,000 may not be made.

Would the situation change if Company A also had some internally generated intangible assets, say $300,000 of brand names and $100,000 of mastheads – making total assets $1,733,000?

No – it is unlikely that these would have value in a forced sale.

Slide 12.31

The solvency test

The solvency test is not a casual exercise. Directors cannot rely solely on the last set of audited

financial statements. They must also consider financial activities and contingencies arising after the date of the financial statements.

If a company makes a distribution and is later found not to have met the solvency test, the shareholders can be required to pay back the distribution (section 56, Companies Act 1993).

Additionally, by signing the solvency certificate, directors can be held personally liable for the company’s debts and suffer fines and other penalties.

Slide 12.32

Implications of IAS compliance on distributions

Requirement for consolidated accounts of listed companies to comply with IASs and IFRSs

These standards will affect both the disclosure and measurement of items appearing in the income statement and statement of financial position.

Slide 12.33

Disclosure changes for preference shares In the UK, preference shares are always

classified as equity rather than liabilities IAS requirement is to treat these as liabilitiesCompanies Act will require amendment so

that preference shares may be treated as liabilities.

Implications of IAS compliance on distributions (Continued)

Slide 12.34

Disclosure changes for preference shares This change will affect

The gearing ratios calculated in the balance sheet The times interest cover ratio in the income statement Loan covenant conditions or performance-related

criteria expressed in terms of either of these ratios The profit available for ordinary shareholders will

be unaffected.

Implications of IAS compliance on distributions (Continued)

Slide 12.35

Implications of IAS compliance on proposed dividends

Currently there is a statutory requirement to accrue proposed dividends and disclose them in the income statement and current liabilities

Proposed law change for disclosure of the aggregate amount of proposed dividends as a note to the accounts

This would be an improvement as dividends are payable out of distributable profits and not merely the

profit for the year.

Slide 12.36

Implications of IAS compliance

Measurement changes

Affected by the decision a company makes about the standards applied to the individual company financial statements

Choice of applying international standards or remaining with national standards.

Slide 12.37

Measurement changesIf international standards are applied, then there

are measurement changes that will affect the profit available for distribution to equity shareholders

Examples are the effects of the proposed treatment of leases Leases currently treated as operating will be treated in

the same way as finance leases Even if companies decide to apply national standards

there will be subsequent impact as national standards are brought into line with the international standards, e.g. full provisioning for deferred taxation.

Implications of IAS compliance (Continued)

Slide 12.38

Discussion questions

1. What is the relevance of dividend cover if dividends are paid out of distributable

profits?

2. How can non-distributable reserves become distributable?

Slide 12.39

Reduction of issued share capital

• Companies Act permits share capital reduction subject to court

– Capital already lost and not represented by assets

– Repayment of capital – unwanted liquid resources

– Redemption of shares.

Slide 12.40

Distributable profits: effect of accumulated trading losses

Elimination affecting only equity shareholders Existing losses eliminated No need to make good in future years Distribution from future profits not diverted to

cover losses.

Slide 12.41

Distributable profits: accounting for reduction due to losses

Debit capital reduction accountCredit profit and loss accountDebit share capitalCredit capital reduction account.

Slide 12.42

Accounting for reduction due to losses

Writing off accumulated losses If a company has accumulated losses instead of retained

earnings as a component of equity, the directors may appoint new management and cancel shares with a paid-in value sufficient to write the accumulated losses off.

Is this harsh treatment for the shareholders who lose part of their investment?

If the company continues running losses, eventually the shareholders would lose all their investment. Writing off accumulated losses can be a signal that new management is positive, and if it is successful in returning the company to running surpluses, shareholders can expect to benefit.

Slide 12.43

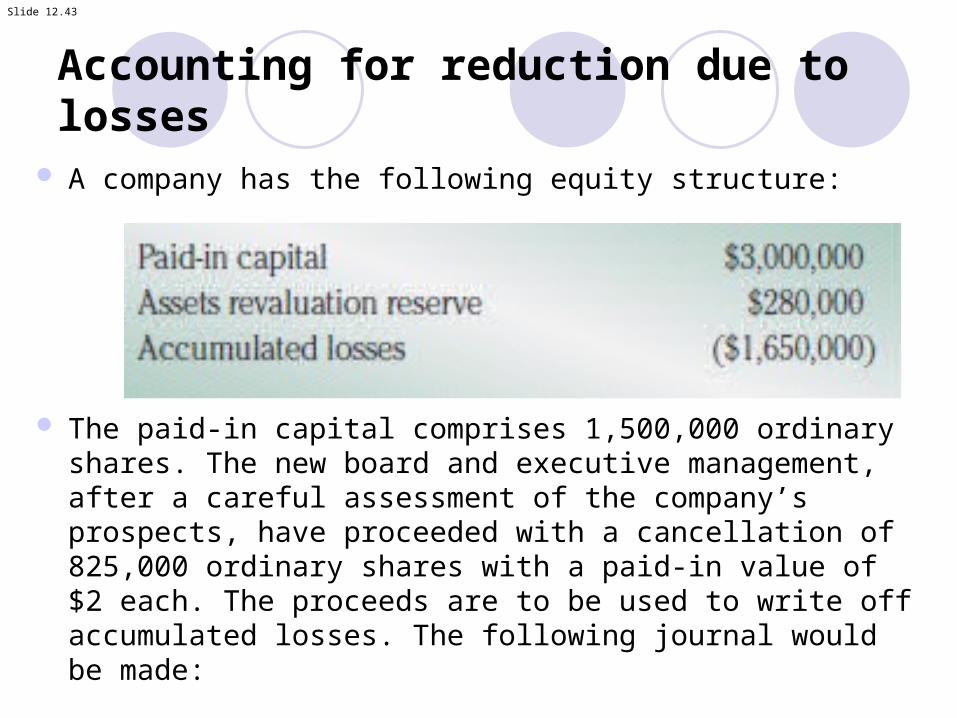

Accounting for reduction due to losses

A company has the following equity structure:

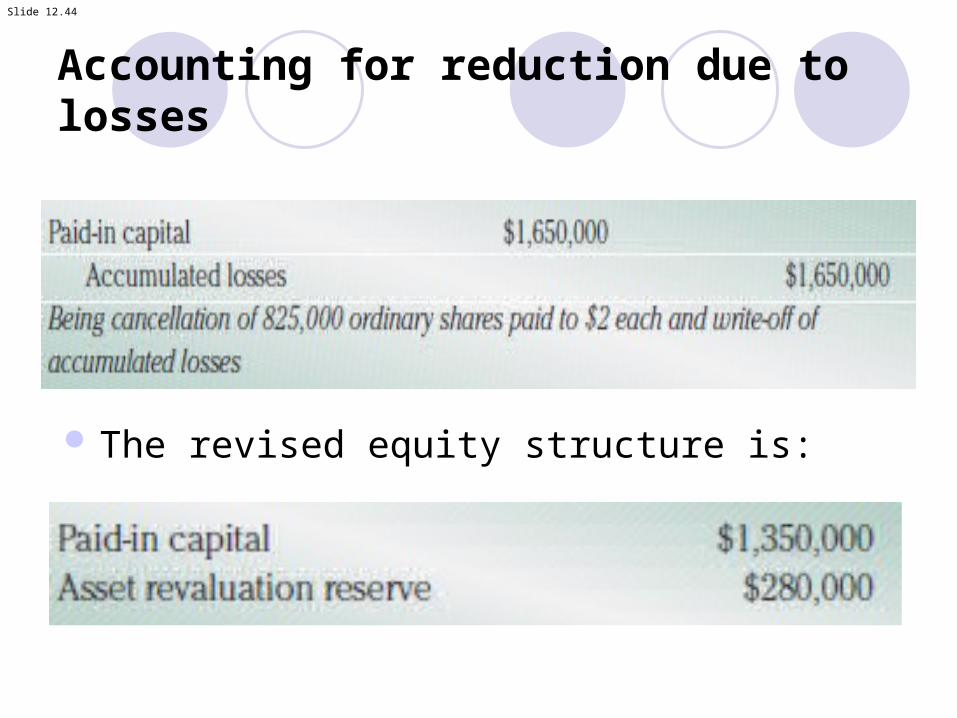

The paid-in capital comprises 1,500,000 ordinary shares. The new board and executive management, after a careful assessment of the company’s prospects, have proceeded with a cancellation of 825,000 ordinary shares with a paid-in value of $2 each. The proceeds are to be used to write off accumulated losses. The following journal would be made:

Slide 12.44

Accounting for reduction due to losses

The revised equity structure is:

Slide 12.45

Distributable profits: accounting for reduction due to trading and asset value losses. Distributable profits: accounting for reduction where losses are borne by more stakeholders

We will skip this in class as there is not enough time available to cover this part of the topic.

Slide 12.46

Discussion

What rights do loan creditors have if a company approaches them to bear part of accumulated losses?

What calculations might they make before agreeing to a proposed scheme?

Why might it be unfair to apportion the total loss pro rata across equity shareholders, preference shareholders and loan creditors?

Slide 12.47

Discussion (Continued)

It is important in any capital reduction scheme for the existing equity shareholders to retain overall control

What would a court take into account when considering whether to approve a scheme?

Slide 12.48

Buyback of own shares – treasury shares

In Europe and USA it is permissible tobuyback shares, known as treasury shares, and hold them for reissue

Two common accounting treatments – the cost method and the par value method

Most common method is the cost method.

Slide 12.49

Buyback of own shares – treasury shares

Treasury stock These are shares held by the issuing company on which

rights and obligations (e.g. voting rights and dividends) are suspended.

A company acquiring its own shares may retain up to 10% of repurchased shares as treasury stock provided the rights and obligations attaching to these shares are suspended.

The company cannot exercise voting rights, nor receive any distribution in respect of these shares.

Any other shares repurchased by the company must be cancelled immediately.

Slide 12.50

Buyback of own shares – treasury shares

On purchase The treasury shares are debited at gross cost to a

Treasury Stock account – this is deducted as a one-line entry from equity, e.g. a statement of financial position might appear as follows:

When the treasury stock was repurchased, paid-in capital was not reduced: it remained at ₤1.00 per share

Slide 12.51

Buyback of own shares – treasury shares

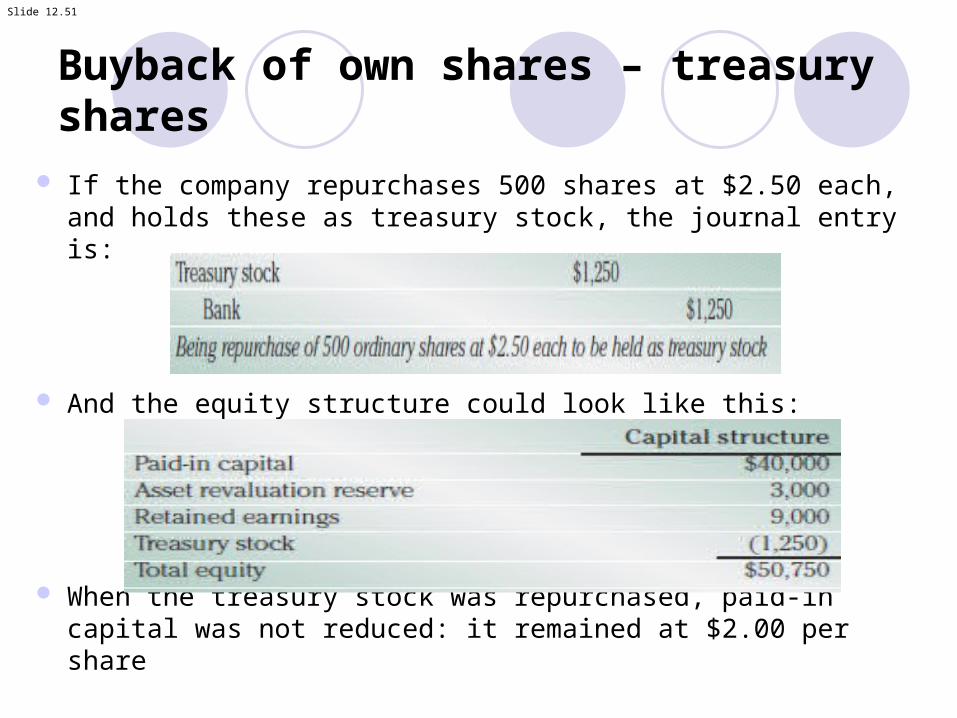

If the company repurchases 500 shares at $2.50 each, and holds these as treasury stock, the journal entry is:

And the equity structure could look like this:

When the treasury stock was repurchased, paid-in capital was not reduced: it remained at $2.00 per share

Slide 12.52

Buyback of own shares – treasury shares

Treasury stock is recorded as a negative component of equity.

It is not an asset. Why? These shares cannot produce service potential or

future economic benefits so they do not meet the definition of assets.

Slide 12.53

On resaleIf on resale the sales price is higher than the cost

price, the Treasury Stock account is credited at cost price and the excess is credited to Paid-in Capital (Treasury Stock)

If on resale the sales price is lower than the cost price, the Treasury Stock account is credited with the proceeds and the balance is debited to Paid-in Capital (Treasury Stock)

If the debit is greater than the credit balance on Paid-in Capital (Treasury Stock), the difference is deducted from retained earnings.

Buyback of own shares – treasury shares

Slide 12.54

Buyback of own shares – treasury shares

If 500 shares of treasury stock are re-issued at $4.00 per share, the journal entry would be:

The company paid $2.50 on the market and resold at $4.00. The difference of $1.50 per share is the $750 net increase in paid-in capital.

Slide 12.55

Redemption of shares

Companies may issue a separate class of share called redeemable shares.

Normally, these are a type of preference share, and redemption may be at the option of either the company or the shareholder. If the shares are redeemable at the option of the

company, all holders must be treated equally. In addition, the company must be able to satisfy the solvency test before redemption is undertaken.

Slide 12.56

Redemption of shares (Continued)

If the shares are redeemable at the option of the holder, then the company redeems only those shares where an option is exercised. However, if any shares are not redeemed by the shareholders, they become part of the company’s liabilities.

On redemption, the shares are deemed to be cancelled and so the journal entry is of the form:

Slide 12.57

Review questions

2. Why do companies reorganise their capital structure when they have accumulated losses?