Embed Size (px)

Citation preview

Directions for deductibility of finance (costs) in GermanyCBT Summer Conference 10/11 July 2009

Ute WittCorporate Tax Partner - Head of Tax Thought Leadership GSAErnst & Young GmbH, Berlin Office

Page 211 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyAgenda

► Introduction► General economic theory ► Specific factors influencing interest deduction in Germany► Situational analysis of the German corporate environment► Interest deduction prior to the 2008 Business Tax Reform► Basic idea of the 2008 Business Tax Reform► Aims pursued in introducing the interest limitation► Brief description of the law on interest limitation► Comparison with similar regulations abroad► Effect of the German interest limitation during the crisis ► Assessment of the interest limitation► Conclusion

Page 311 July 2009 Directions for deductibility of finance in Germany

Historical development of taxation2900 BC: Taxes as a proportion of the harvest (wheat tithe, oil tithe, cattle tithe, fruit tithe)500 AD: Poll taxes, land taxes and “portaticum, pontaticum, ripaticum, rotaticum,

pedaticum”1650: Fire taxes, later substituted by window taxes19th century: Income tax according to the source theory, which for the first time took into

account a person’s ability to pay taxFrom 1891: Prussian income tax law: taxation according to the accretion theory

(Schanz-Haig-Simons approach)From 1945: The significance of excise taxes and taxes on capital declined

Move towards income and turnover taxation2008: 2008 Business Tax Reform

► Cut in corporate income tax rate► Broadening of the tax base

► Introduction of a general limitation on deducting interest expenses► New regulations on trade tax add-backs

Directions for deductibility of finance in GermanyIntroduction

Page 411 July 2009 Directions for deductibility of finance in Germany

}‘Production efficiency theorem’ (Diamond / Mirrless):Distortion free taxation in the business sector

Directions for deductibility of finance in GermanyGeneral economic theory

► Tax system must not trigger any harmful avoidance tactics in business decisions

► Distorted free taxation of profit automatically prevents a search for alternative structures (taxation based on performance parameters)

► Import duties as well as the taxation on the means of production or intermediate products should be avoided

► Taxation of net profit ensures neutrality in investing and financing

► Strict compliance with the principle of net income taxation

Page 511 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in Germany General economic theory: Example

Exampleof a gross proceeds taxation of different industries in an identical profit situation

Company B:

Company A:

Industry: Trading operations Revenue: 1,000 Cost of goods: 700 Personnel costs: 100 Rent: 100

à Tax assessment base: 1,000

Industry: Marketing of intangible assets Revenue: 101 OPEX: 1

à Tax assessment base: 101

à Profit: 100

à Profit: 100

à Tax: 30.3

à Tax: 300 (> profit)

Page 611 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanySpecific influencing factors

Specific factors influencing the deductibility of interest

► German Constitution requires taxation being linked to the ability to pay

► Principle of horizontal tax fairness► Consistent taxation (taxation of the net proceeds)

► Principle of vertical tax fairness► Tax exemption up to the subsistence level► Progressive tax tariff thereafter

► Stable state revenue► In boom times, tax revenues are plentiful, while social transfers decrease► In times of economic crisis, the situation is reversed

► Prevention of tax abuse

Page 711 July 2009 Directions for deductibility of finance in Germany

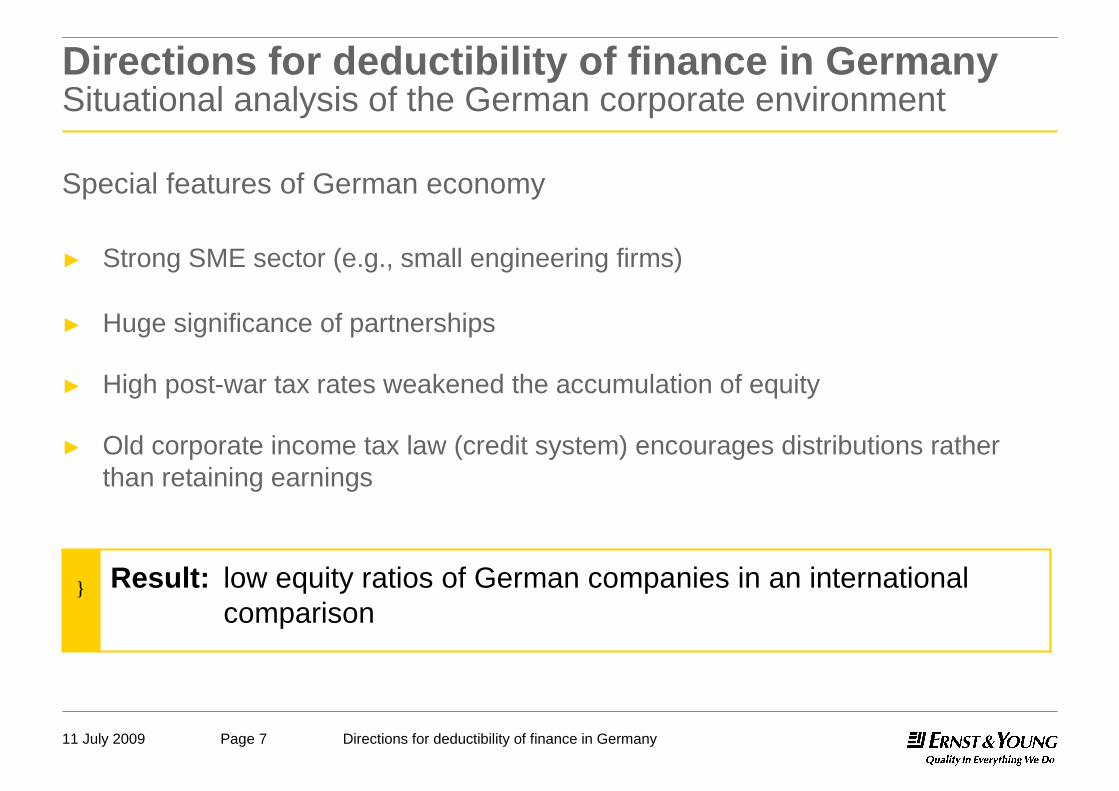

} Result: low equity ratios of German companies in an international comparison

Directions for deductibility of finance in GermanySituational analysis of the German corporate environment

Special features of German economy

► Strong SME sector (e.g., small engineering firms)

► Huge significance of partnerships

► High post-war tax rates weakened the accumulation of equity

► Old corporate income tax law (credit system) encourages distributions rather than retaining earnings

Page 811 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanySituational analysis of the German corporate environment: Equity ratios

Equity ratios of SMEs in an international comparison

Belgium, Germany, France, Japan, Netherlands, Austria, USASource BACH Database a. Creditreform

Page 911 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyInterest deduction prior to the 2008 Business Tax Reform

Trade tax

► Trade tax on capital applicable until 1997 included add backs for specific debt financing

► Interest and rent/ lease payments etc. added back in specific cases

► No neutrality between equity and debt financing

Corporate income tax

► Reclassification of interest expenses to hidden profit distribution if the remuneration is caused by company affiliations

► Safe haven for thin capitalization (1.5 : 1)

Page 1011 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyBasic idea of the 2008 Business Tax Reform

► Positive signal by decreasing the corporate income tax rate: 25% to 15%

► Broadening of tax base to ‘counter-finance’ the tax cut

► Introduction of a general interest deduction limitation rule► Expansion of trade tax add-backs► Tightening of provisions on the forfeiture of tax losses► Tightening transfer pricing regulations / introduction of

new taxation rules of function transfers► Abolition of declining-balance depreciation method, etc.► Minimum taxation (already in place since 2004)

► Downside of the reform: drafted in good times, harmful in the current crisis (Citizen Relief Act already reacted with adjustments)

► Most parties already declared a need for revision of certain regulations of the 2008 reform after the parliamentary elections in Germany (Sept. 2009)

Page 1111 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyInterest limitation (1)

► Counter-financing of the cut in corporate income tax rate (main objective)/ problem: cut most likely undone by the interest deduction limitation

► Compliance of new regulations with EU law► Constitutional requirements of taxation according to the ability to pay taxes to be

adhered to► Avoiding tax abusive financing structures (see examples below)

Aims pursued in introducing the interest deduction limitation

P

S P P

SSForeignDomestic

Shift of income

Downstream inbound financing

Debt

Upstream inbound financing

EquityDebt

EquityDebt

Externally financed outbound financing

Shift of income

Shift of income

Page 1211 July 2009 Directions for deductibility of finance in Germany

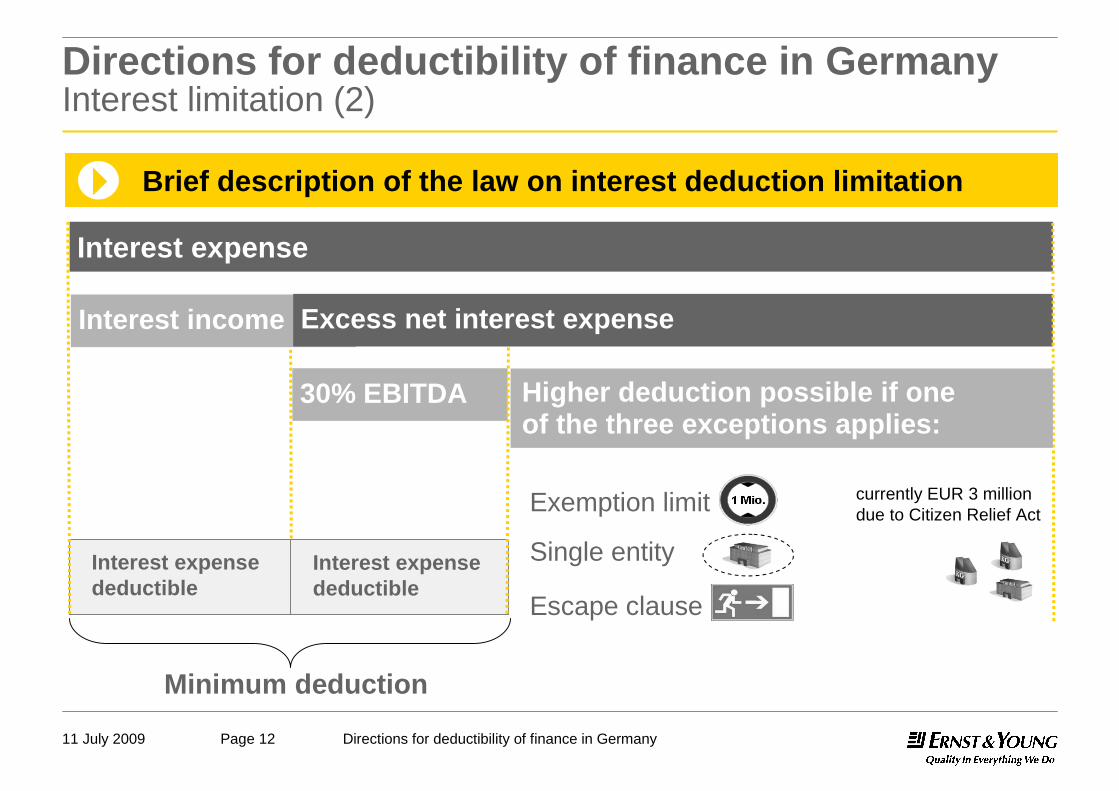

30% EBITDA

Interest expense

Interest income Excess net interest expense

Interest expense deductible

Interest expense deductible

Minimum deduction

Exemption limit

Single entity

Escape clause

Higher deduction possible if one of the three exceptions applies:

Directions for deductibility of finance in GermanyInterest limitation (2)

Brief description of the law on interest deduction limitation

currently EUR 3 million due to Citizen Relief Act

Page 1311 July 2009 Directions for deductibility of finance in Germany

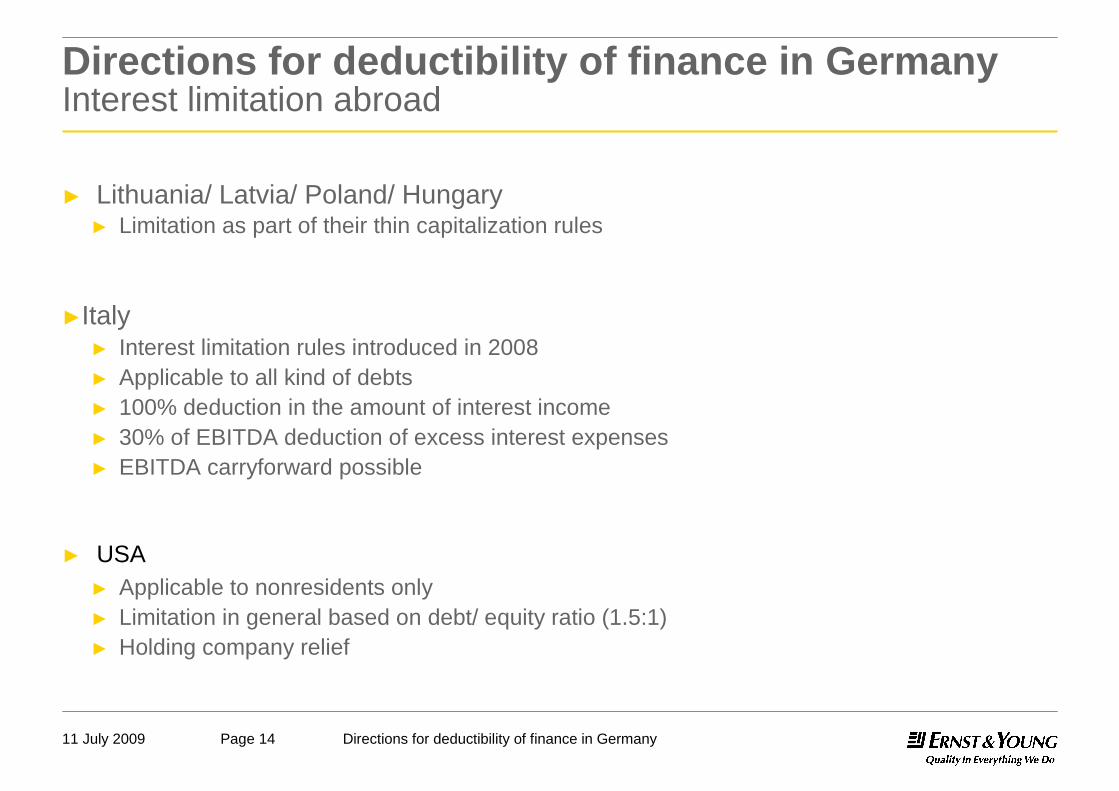

Directions for deductibility of finance in Germany Interest limitation abroad

Comparable provisions in other countries

► European trend► Limitation of interest deduction ► In general: broadening of tax base

► France/ UK► Before introduction: reclassification into hidden profit distribution► Now: limitation► Current UK development : worldwide debt cap provision

► Denmark/ Netherlands► Before introduction: no thin capitalization rules► Now: limitation

Page 1411 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in Germany Interest limitation abroad

► Lithuania/ Latvia/ Poland/ Hungary► Limitation as part of their thin capitalization rules

►Italy► Interest limitation rules introduced in 2008► Applicable to all kind of debts► 100% deduction in the amount of interest income► 30% of EBITDA deduction of excess interest expenses► EBITDA carryforward possible

► USA► Applicable to nonresidents only► Limitation in general based on debt/ equity ratio (1.5:1)► Holding company relief

Page 1511 July 2009 Directions for deductibility of finance in Germany

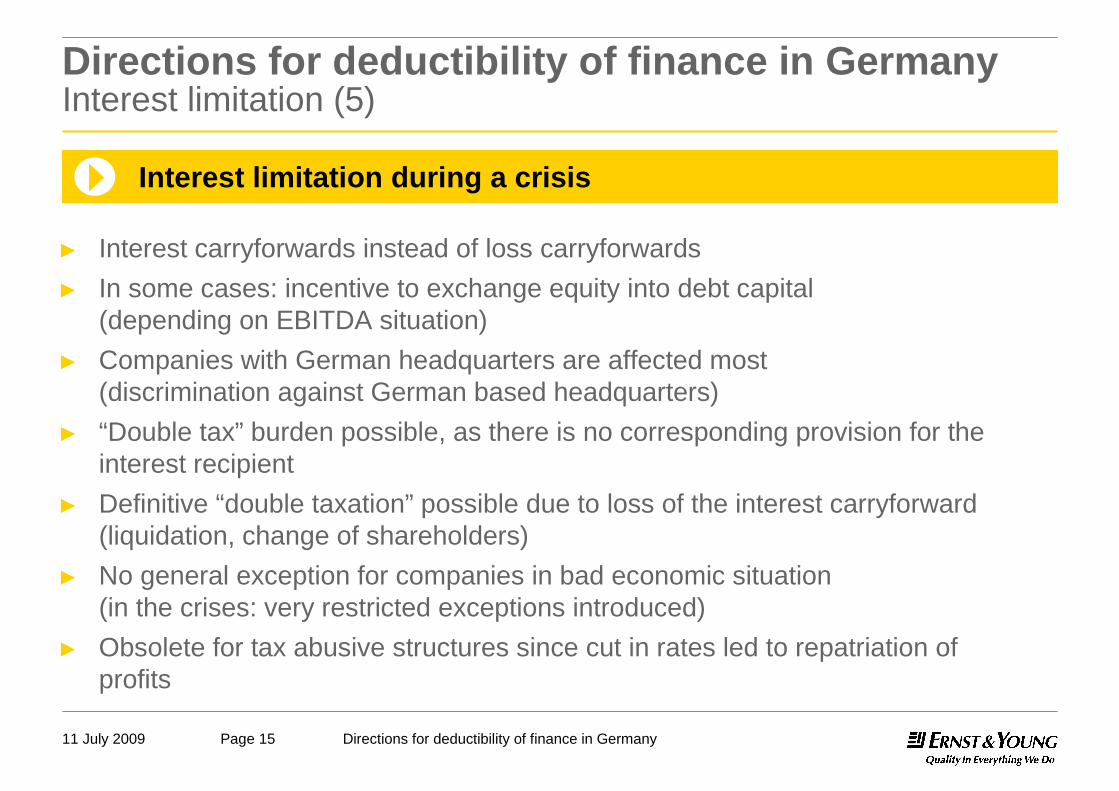

Directions for deductibility of finance in Germany Interest limitation (5)

► Interest carryforwards instead of loss carryforwards► In some cases: incentive to exchange equity into debt capital

(depending on EBITDA situation)► Companies with German headquarters are affected most

(discrimination against German based headquarters)► “Double tax” burden possible, as there is no corresponding provision for the

interest recipient ► Definitive “double taxation” possible due to loss of the interest carryforward

(liquidation, change of shareholders)► No general exception for companies in bad economic situation

(in the crises: very restricted exceptions introduced)► Obsolete for tax abusive structures since cut in rates led to repatriation of

profits

Interest limitation during a crisis

Page 1611 July 2009 Directions for deductibility of finance in Germany

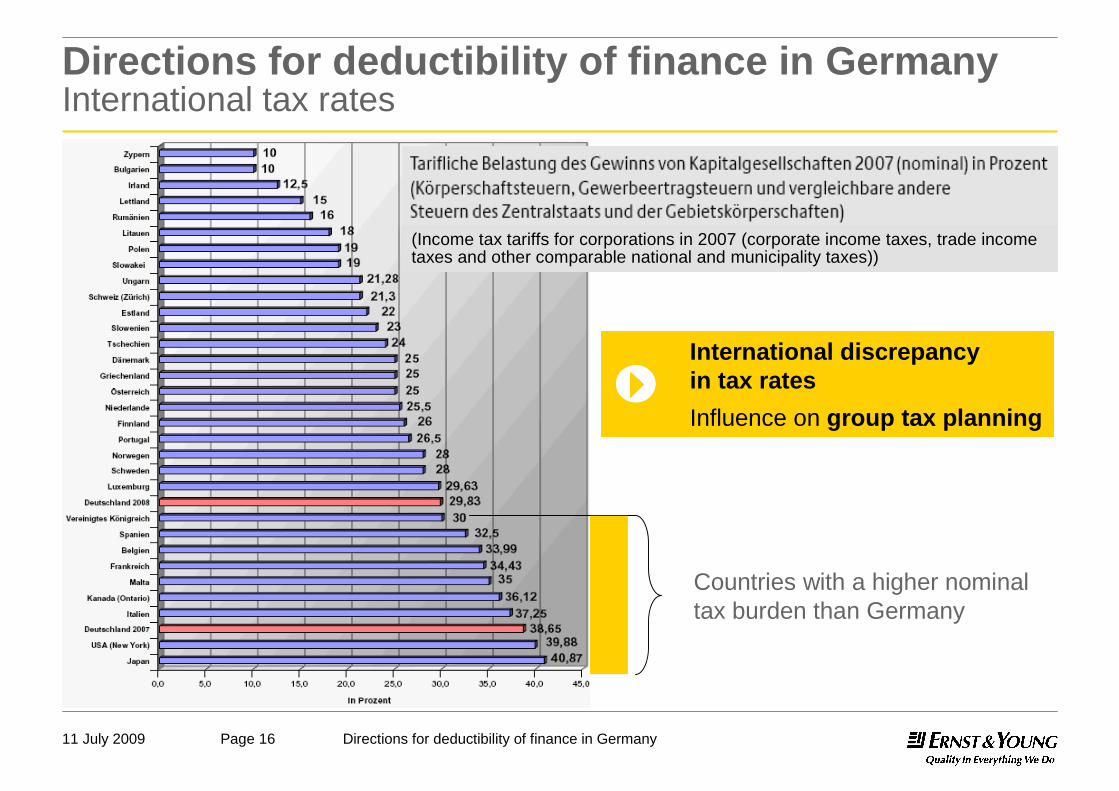

Directions for deductibility of finance in GermanyInternational tax rates

International discrepancy in tax ratesInfluence on group tax planning

Countries with a higher nominal tax burden than Germany

(Income tax tariffs for corporations in 2007 (corporate income taxes, trade income taxes and other comparable national and municipality taxes))

Page 1711 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyInterest limitation (6)

► The interaction of the interest limitation rule with other tax regulations leads to excess taxation of the business sector► Violation of the general economic call for production efficiency► Violation of neutral taxation of debt and/ or equity financing► Taxation no longer linked to the performance parameters of the entrepreneur

► Violation of the net principle taxation► Constitutional requirements concerning taxation according to the ability to pay taxes

are violated by the interest limitation ► Principle of horizontal tax fairness is violated with the interest limitation► Trade tax add-backs and minimum taxation as well as loss forfeiture rules (500

thousand millionth tax loss carryforwards) increase the problem

Assessment of the German interest limitation regulation

Page 1811 July 2009 Directions for deductibility of finance in Germany

Directions for deductibility of finance in GermanyConclusion

► Trade-off between dependence of the state revenue on economic conditions and taxation only on net results has to be resolved in favour of taxation based on performance parameters. Thus the state has to► change from governmental accounting to double entry book-keeping► introduce saving and incentive systems within public administration► transfer unused funding to subsequent budget years

► Combating tax abuse is a legitimate goal since “business goes global – taxes stay local”► But: interest limitation has to be restricted to tax abusive structures

► Move away from the net principle taxation means return to the medieval times► No steering via taxes► Back to a principle based tax regime necessary

Thank you!