Embed Size (px)

Citation preview

Small Business & Agricultural Advisory Board

Federal Reserve Bank of New York

33 Liberty Street

10F, Paul Volcker Boardroom

Tuesday, November 15, 2016

AGENDA

10:30am

10:35am

Welcome, Claire Kramer Mills, AVP

Introductory Remarks, Kausar Hamdani, Senior Vice President

10:40am-11:10am

The National Economy, Richard Peach, Senior Vice President

11:10am-11:40am

International Update, Matthew Higgins, Vice President

11:40am-12:00pm

Regional Update, Jason Bram, Officer

12:00pm

12:15pm

12:15pm-1:55pm

Adjourn to NWC Room-10F

Lunch

Round Table Discussion with William Dudley, President and Michael

Strine, First Vice President

Your experience and that of your customers and suppliers can give us

insight into current economic conditions.

Questions for discussion with President Dudley:

1. Has your firm’s sales volume increased, decreased, or stayed the

same in the second half of 2016?

2. Do you expect your firm’s sales to increase, decrease, or stay

the same in the first quarter of 2017?

3. Do you plan to increase investment in your firm (plant &

equipment) in the first half of 2017?

4. Has your firm faced any recent shortage of labor that has limited

your ability to meet demand?

5. Do you plan to increase employment in 2017? Why or why not?

6. Do you expect input prices to increase in 2017? Do you expect

prices of products/services sold to increase?

7. Over the past two quarters, have you made any recent changes to

your firm’s financing? How have the terms and conditions for

obtaining financing changed (tightened, eased, not changed)?

2:00 pm Adjourn

Small Business & Agricultural Advisory Council Federal Reserve Bank of New York

33 Liberty Street New York, NY

Tuesday, November 15 2016

ATTENDEE LIST Council Members Michael Arnoff President Arnoff Moving & Storage Adenah Bayoh Co-Founder Kapwood, LLC Eric Caslow President Acme Smoked Fish Corporation Kevin Ellis Chief Executive Officer Cayuga Milk Industries

Charles Feit President and Founder OnForce Solar Gabriel Hernández Co-Founder and Head of Tax Division BDO Puerto Rico Deborah Leo President Retail Solutions, Inc.

Federal Reserve Bank of New York

William Dudley Michael Strine Richard Peach Kausar Hamdani Matthew Higgins Anand Marri Claire Kramer Mills Jason Bram Luis Uranga Javier Silva Edison Reyes Angela Sun

President First Vice President SVP, Research & Statistics SVP, Communications & Outreach VP, Integrated Policy Analysis VP, Outreach & Education AVP, Outreach & Education Officer, Research & Statistics Officer, Chief of Staff’s Office Senior Associate, Outreach & Education Associate, Outreach & Education Associate, Legal

US Macro Overview Richard Peach, Senior Vice President

November 15, 2016

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014 2016

Growth of Real GDP

Four Quarter Percent Change Four Quarter Percent Change

Source: Bureau of Economic Analysis

Note: Shading shows NBER recessions.

Series 1

(Left Axis)

Series 2

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

1

80

90

100

110

120

130

140

0

200

400

600

800

1000

1200

1400

1600

1800

2011 2012 2013 2014 2015

Broad Trade-Weighted Exchange Value of US $ (right axis)

Nominal Trade-Weighted Value of US$ and Rig Count

Active Oil Rigs Index

Source: Federal Reserve Board and Baker

Hughes

Series 1

(Left Axis)

Series 2

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

Rig Count (left axis)

2

Manufacturing Output and Real I/S Ratio

Quarterly Growth (Annualized) Real I/S Ratio

Source: Federal Reserve Board and Bureau

of Economic Analysis via Haver Analytics

Series 1

(Left Axis)

Series 2

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

3

1.3

1.35

1.4

1.45

1.5

1.55

1.6

-25

-20

-15

-10

-5

0

5

10

15

1985 1990 1995 2000 2005 2010 2015

-1

0

1

2

3

4

5

6

-1

0

1

2

3

4

5

6

2012 2013 2014 2015 2016

Aggregate Weekly Hours Worked

Y/Y % Change Y/Y % Change

Source: Bureau of Labor Statistics

Goods-Producing

Industries

Private

Service-Providing

Industries Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

4

0

2

4

6

8

10

12

56

58

60

62

64

66

68

2000 2002 2004 2006 2008 2010 2012 2014 2016

Percent Percent

Source: Bureau of Labor Statistics,

via Haver Analytics Note: Shading shows NBER recessions.

Labor Force

Participation Rate

(Left Axis)

Unemployment

Rate

(Right Axis)

Employment-Population

Ratio

(Left Axis)

Labor Market Indicators

5

170

190

210

230

250

5

5.3

5.6

5.9

6.2

6.5

2014 2015 2016

Personal Saving Rate and Energy Price Index Energy Price Index Personal Saving Rate

Sources: Bureau of Economic Analysis and Bureau of Labor Statistics via Haver Analytics

Personal Saving Rate

(left axis)

Energy Price Index

(right axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

12-month Change

(left axis)

Monthly Change

(right axis)

12-month Percent Change Monthly Percent Change (Annualized) Real Personal Consumption Expenditures

6

-4

-2

0

2

4

6

8

10

00.5

11.5

22.5

33.5

44.5

2014 2015 2016

-15

-10

-5

0

5

10

15

20

25

30

-15

-10

-5

0

5

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012 2014 2016

> 803

754 - 803

688 - 753

606-687

< 606

Consumer Debt by Credit Score

% Change – Year to Year % Change – Year to Year

Source: FRBNY Consumer Credit Panel

1st Quintile

(Highest)

2nd Quintile

3rd Quintile 4th

Quintile

5th Quintile

(Lowest)

Note: Includes Student Loans 8

7

0

0.005

0.01

0.015

0.02

0.025

0.03

0

0.005

0.01

0.015

0.02

0.025

0.03

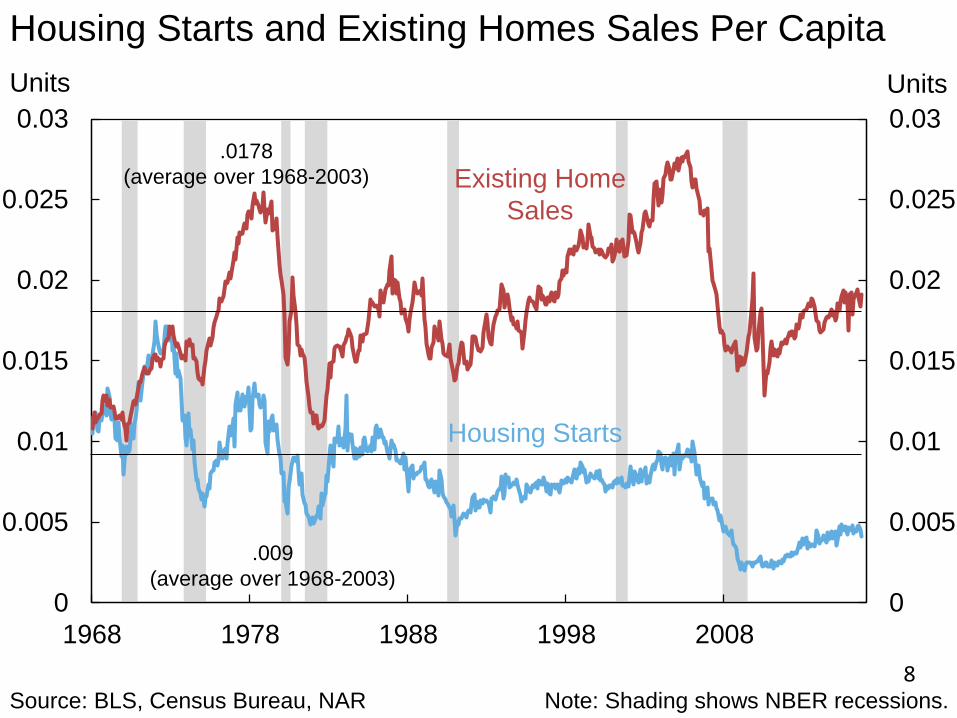

1968 1978 1988 1998 2008

Housing Starts and Existing Homes Sales Per Capita

Units Units

Source: BLS, Census Bureau, NAR

Note: Shading shows NBER recessions.

Housing Starts

Existing Home

Sales

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

.0178

(average over 1968-2003)

.009

(average over 1968-2003)

8

500

550

600

650

700

750

800

500

550

600

650

700

750

800

1999 2001 2003 2005 2007 2009 2011 2013 2015

Credit Score at Mortgage Origination: All First Mortgages

Credit Score Credit Score

Source: FRBNY / Consumer Credit Panel

Note: Shading shows NBER recessions.

Median

10th Percentile

25th Percentile

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

About 20 – 25 Million People

9

-20

-15

-10

-5

0

5

10

15

-20

-15

-10

-5

0

5

10

15

2000 2002 2004 2006 2008 2010 2012 2014 2016

Real Business Fixed Investment

4Q % Change 4Q % Change

Source: Bureau of Economic Analysis

Note: Shading shows NBER recessions.

Series 1

(Left Axis)

Series 2

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

10

-30

-20

-10

0

10

20

30

-30

-20

-10

0

10

20

30

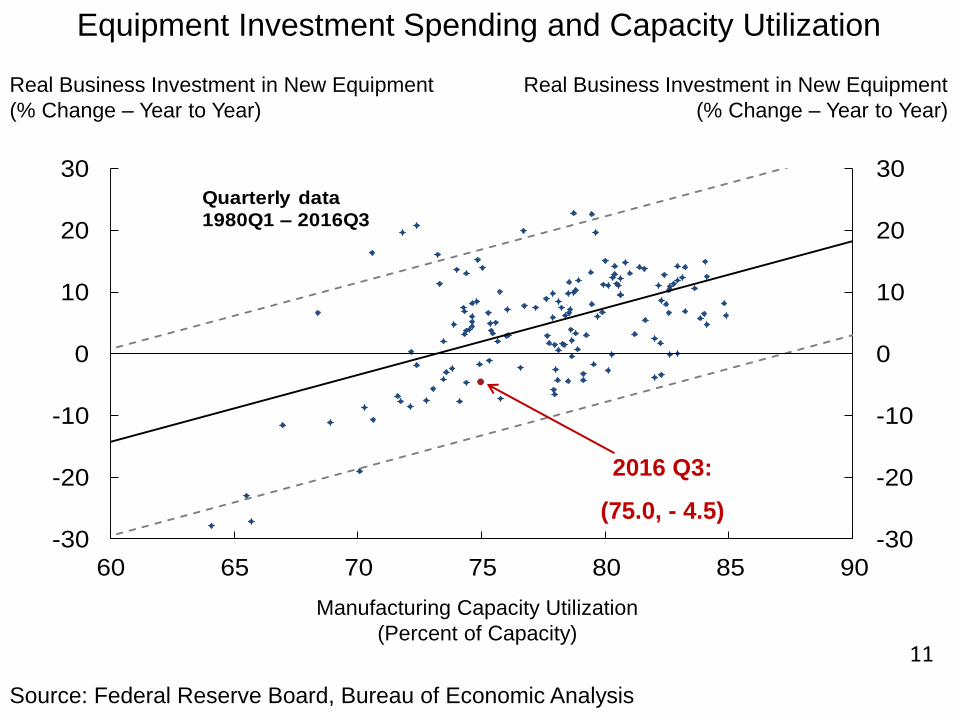

60 65 70 75 80 85 90

Quarterly data

1980Q1 – 2016Q3

Equipment Investment Spending and Capacity Utilization

Real Business Investment in New Equipment

(% Change – Year to Year)

Real Business Investment in New Equipment

(% Change – Year to Year)

Source: Federal Reserve Board, Bureau of Economic Analysis

Manufacturing Capacity Utilization

(Percent of Capacity)

2016 Q3:

(75.0, - 4.5)

11

-8

-6

-4

-2

0

2

4

6

8

10

-8

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016

Real Government Consumption and Gross Investment

4 Quarter % Change 4 Quarter % Change

Source: Bureau of Economic Analysis Note: Shading shows NBER recessions.

Federal

(Left Axis)

State & Local

(Right Axis)

12

-2

-1

0

1

2

3

4

5

-2

-1

0

1

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014 2016

12 Month % Change 12 Month % Change

Source: Bureau of Economic Analysis,

via Haver Analytics Note: Shading shows NBER recessions.

Total PCE

Core PCE

FOMC Objective

PCE Deflator

13

-3

-2

-1

0

1

2

3

4

5

-3

-2

-1

0

1

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014 2016

CPI Inflation: Core Goods and Core Services

12 Month % Change 12 Month % Change

Source: Bureau of Labor Statistics

Note: Shading shows NBER recessions.

Core Goods

Core Services

Total Core CPI

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

14

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

2000 2002 2004 2006 2008 2010 2012 2014 2016

Rental Vacancy Rate and Rent of Primary Residence

Percent 12 Month % Change

Source: Census Bureau, BLS Note: Shading shows NBER recessions.

Rental

Vacancy Rate

(Left Axis)

Rent of Primary

Residence

(Right Axis)

15

-10

-8

-6

-4

-2

0

2

4

6

8

10

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012 2014 2016

Dollar Exchange Rate and Nonoil Import Prices

12 Month % Change 12 Month % Change

Note: Shading shows NBER recession and

dollar is Board’s trade-weighted measure.

Dollar

(Left Axis)

Nonoil Import

Prices

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

Source: Federal Reserve Board, Bureau of

Labor Statistics via Haver Analytics

16

Reference Charts

17

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Personal Consumption Expenditures: Health Care Price

Index 12 Month % Change 12 Month % Change

Source: Bureau of Economic Analysis Note: Shading shows NBER recessions.

17% of total PCE deflator

19% of core PCE deflator

18

-25

-20

-15

-10

-5

0

5

10

15

20

25

-25

-20

-15

-10

-5

0

5

10

15

20

25

2005 2007 2009 2011 2013 2015

Bank Assets: Domestically and Foreign Chartered Banks

% Change Year-to-Year % Change Year-to-Year

Source: Federal Reserve Board Note: Shading shows NBER recessions.

Commercial and

Industrial Loans

(Left Axis)

Residential Real

Estate Loans

(Right Axis)

Commercial Real

Estate Loans

(Left Axis)

Series 4

(Right Axis)

19

0

2

4

6

8

10

12

60

62

64

66

68

70

195

5

195

9

196

3

196

7

197

1

197

5

197

9

198

3

1987

199

1

199

5

1999

200

3

200

7

201

1

201

5

Labor Share of National Income and Unemployment Rate

Percent Rate

Source: Bureau of Economic Analysis,

Bureau of Labor Statistics Note: Shading shows NBER recessions.

Labor Share of

National

Income

(Left Axis)

Unemployment

Rate

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

20

-1000

-500

0

500

1000

1500

2000

-1000

-500

0

500

1000

1500

2000

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Household Formations

2 Year Avg. Change 2 Year Avg. Change

Source: Bureau of the Census Note: Shading shows NBER recessions.

Total

(Left Axis) Renter

(Left Axis)

Owner

(Right Axis)

21

60

62

64

66

68

70

1965 1971 1977 1983 1989 1995 2001 2007 2013

60

62

64

66

68

70Percent Percent

Source: Census Bureau

Aggregate Homeownership Rate*

*Owner-occupied housing units divided by total occupied housing units.

Contribution to Decline by Age of Household Head: Under 35: 23.7% 35 to 44: 35.4% 45 to 54: 29.1% 55 to 64: 11.7% 65 plus: -0.9%

22

-500

0

500

1000

1500

2000

2500

3000

3500

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

-500

0

500

1000

1500

2000

2500

3000

3500

Excess Supply of Housing

Source: US Bureau of the Census, Housing Vacancy Survey, and author’s calculations.

Note: Shading represents NBER recessions.

Owner (For Sale)

Held Off Market

Renter (For

Rent)

Excess Units: Total

Thousands of Units Thousands of Units

23

Single Family Housing Market

3

4

5

6

7

8

9

10

11

12

13

-20

-15

-10

-5

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012 2014 2016

12 Month % Change Months

Source: CoreLogic, National Association of

Realtors, via Haver Analytics Note: Shading shows NBER recessions.

Single Family

House Price Index

(Left Axis)

Months’

Supply

(Right Axis)

“Normal” Range for

Months’ Supply

24

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0

10

20

30

40

50

60

Transition of Mortgage Accounts from 30-60 Days Late Percent Percent

Source: FRBNY Consumer Credit Panel

To Current

To 90+ Days Late

25

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

60 65 70 75 80 85 90 95

Data from 2015Q1 to 2016Q3 are in red.

Dashed lines represent 95% CI of predicted values.

2001Q1

2001Q3

2001Q4

2001Q2

Unemp. Rate – CBO NAIRU vs. Capacity Utilization PPT Difference (Unemp. Rate – NAIRU)

Source: BLS, CBO, Federal Reserve Board

Series 1

(Left Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

PPT Difference

Capacity Utilization: Manufacturing (Percent)

Note: Data spans from 1950Q1 to 2016Q3.

26

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0

0.2

0.4

0.6

0.8

1

1.2

1.4

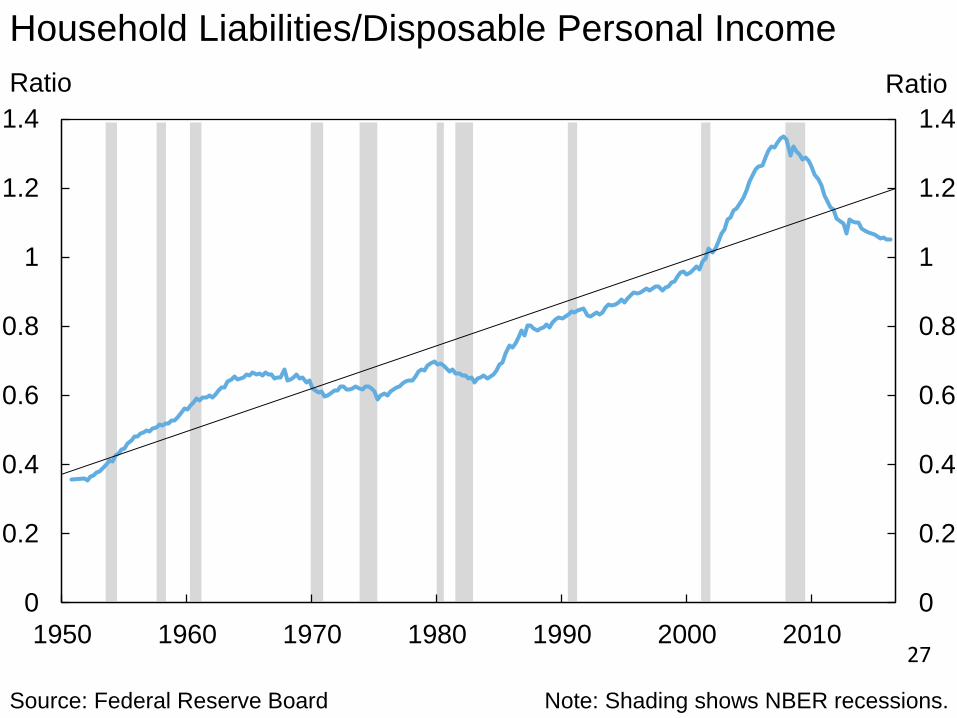

1950 1960 1970 1980 1990 2000 2010

Household Liabilities/Disposable Personal Income

Ratio Ratio

Source: Federal Reserve Board

Note: Shading shows NBER recessions.

Series 1

(Left Axis)

Series 2

(Right Axis)

Series 3

(Left Axis)

Series 4

(Right Axis)

Series 5

(Left Axis)

Series 6

(Right Axis)

27

11/14/2016

1

Global Economic Outlook

Small Business and Agricultural Advisory Council Matthew Higgins, November 2016

The views expressed here are those of the author, and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System.

Roadmap

Recent global economic performance

Foreign advanced economies’ struggle to escape“lowflation”

Capital outflows and pressures on China’sexchange rate

U.S. international trade by geography and producttype

11/14/2016

2

0

2

4

6

8

10

12

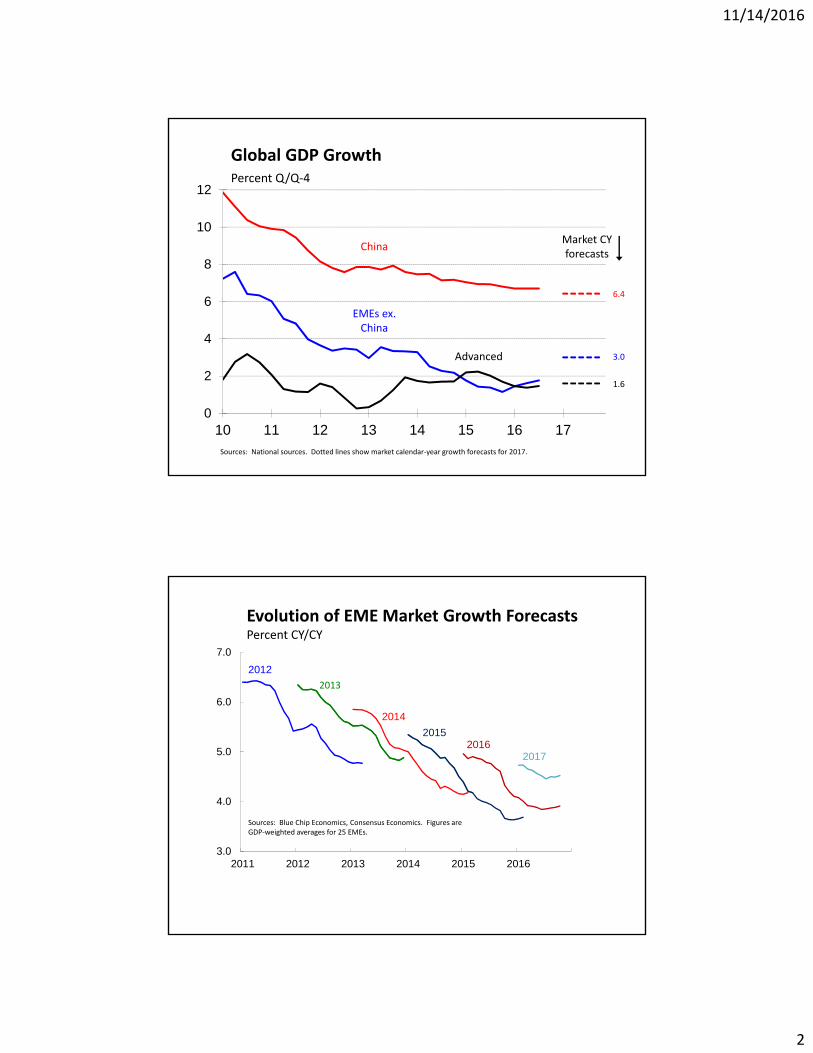

10 11 12 13 14 15 16 17

Global GDP GrowthPercent Q/Q‐4

6.4

1.6

3.0

EMEs ex. China

China

Advanced

Sources: National sources. Dotted lines show market calendar‐year growth forecasts for 2017.

Market CY forecasts

Evolution of EME Market Growth ForecastsPercent CY/CY

3.0

4.0

5.0

6.0

7.0

2011 2012 2013 2014 2015 2016

2013

2014

20152016

2012

2017

Sources: Blue Chip Economics, Consensus Economics. Figures are GDP‐weighted averages for 25 EMEs.

11/14/2016

3

-40

-30

-20

-10

0

10

20

30

16:01 16:03 16:05 16:07 16:09 16:11

Percent positive or negative*

Citigroup Economic Surprise Indexes

Advanced Economies

Emerging Economies

*Weighted by series’ historical FX impact

35

40

45

50

55

60

65

-6

-4

-2

0

2

4

6

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Percent SAAR

AE GDP Growth and Composite PMI

GDP Growth

Composite PMI

Correlation = 0.85

Sources: Markit Economics, national authorities.

Oct.

11/14/2016

4

40.0

42.5

45.0

47.5

50.0

52.5

55.0

57.5

60.0

-4

-2

0

2

4

6

8

10

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Percent SAAR

EME GDP Growth and Composite PMI

GDP Growth

Composite PMI

Correlation = 0.89

Sources: Markit Economics, national sources.

Oct.

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Real GDP

EC Potential Estimate

Linear Trend, 1998‐2005

EC forecasts

Sources: Eurostat, EC CIRCA database.

2016

2017

Trillions of 2010 euros

Euro area real GDP and European Commission Forecast

11/14/2016

5

460

480

500

520

540

560

580

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Real GDP

BoJ Potential Estimate

Linear Trend, 1998‐2005

BoJ projections

Sources: Bank of Japan. Calendar‐year GDP forecast inferred from central tendency of fiscal‐year growth projections of BoJ board members. BoJ staff potential growth forecast for 2016 carried forward to 2017.

2016

2017

Trillions of 2005 yen

Japanese Real GDP and Bank of Japan Projection

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

12 13 14 15 16

Percent change from year ago

G‐3: Core Consumer Price Inflation

Japan

U.S.

Euro Area

Sources: BEA, Eurostat, BoJ. U.S. inflation measured using the PCE index.

1.7

0.8

0.2

11/14/2016

6

0

20

40

60

80

100

08 09 10 11 12 13 14 15 16 17

Percent

Central Bank Credit as a Share of GDP

Japan

United States

Euro Area

Sources: BoJ, ECB, Federal Reserve.

AE Core Inflation Performance with Negative Policy Rates

Country Date AdoptedInitial Core

InflationCurrent Core

Inflation

Japan January 2016 1.1 0.2

Sweden February 2015 1.0 0.7

Switzerland December 2014 0.4 -0.3

Denmark September 2014 0.7 0.1

Euro Area June 2014 0.8 0.8

Sources: National sources, OECD. Policy rates are as follows: Japan, marginal current account balances; Sweden, repo rate; Switzerland, 3‐mo. LIBOR target; Denmark, CD rate; Euro Area, deposit rate.

11/14/2016

7

-200

-150

-100

-50

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017

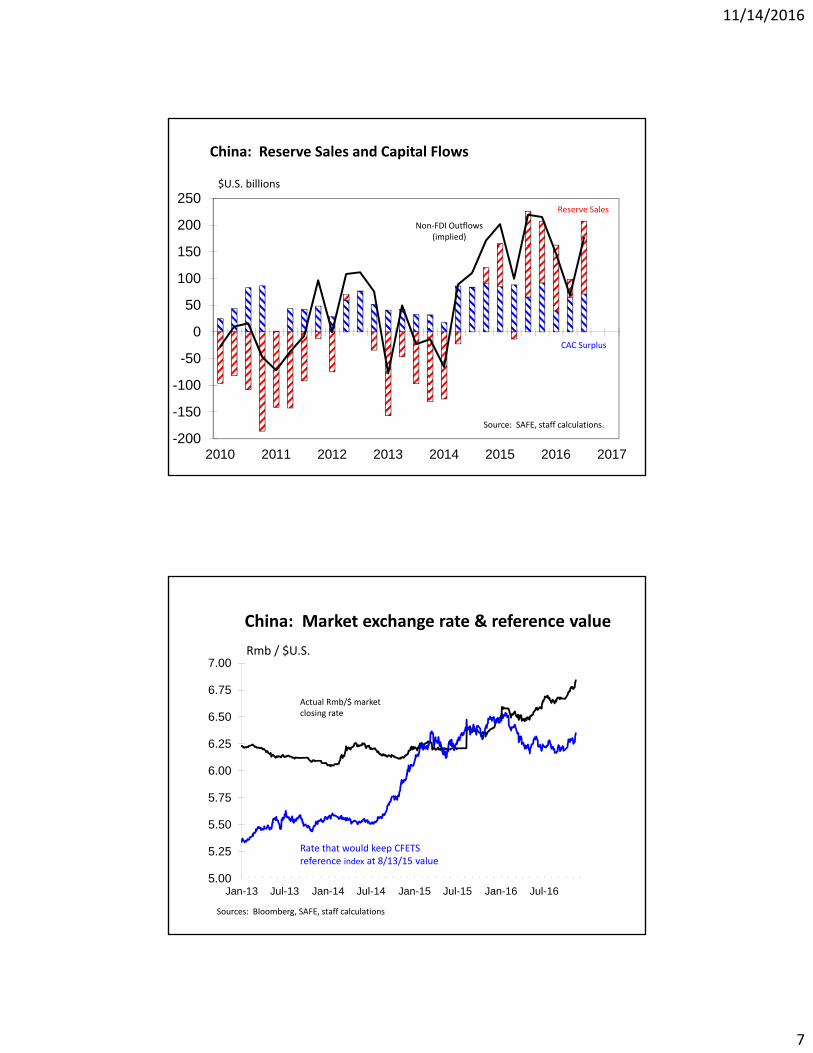

China: Reserve Sales and Capital Flows

Reserve Sales

$U.S. billions

Source: SAFE, staff calculations.

CAC Surplus

Non‐FDI Outflows (implied)

5.00

5.25

5.50

5.75

6.00

6.25

6.50

6.75

7.00

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

China: Market exchange rate & reference value

Rmb / $U.S.

Actual Rmb/$ market closing rate

Rate that would keep CFETS reference index at 8/13/15 value

Sources: Bloomberg, SAFE, staff calculations

11/14/2016

8

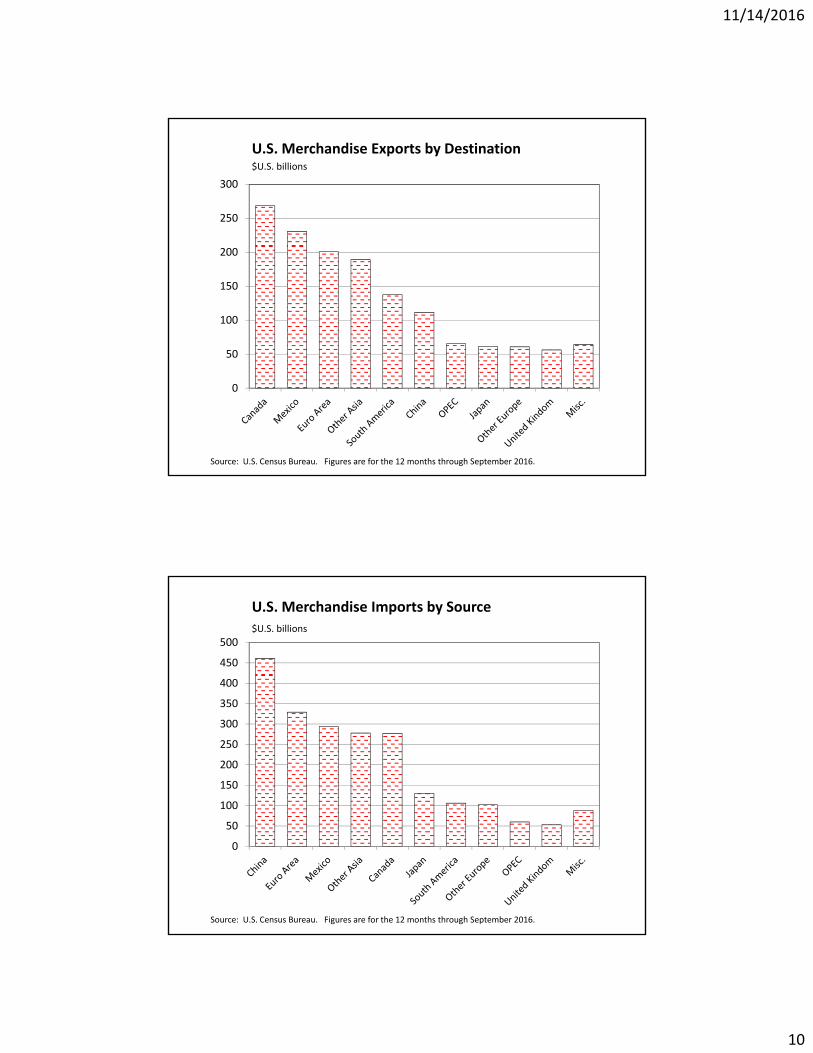

U.S. Merchandise Trade Flows ( $U.S. bn. )

Country or Region Exports Imports Balance

World 1,446 2,178 -733

Canada 269 277 -8Mexico 231 294 -63Euro area 201 329 -128Asia ex. China, Japan 189 278 -89South America 132 106 26China 112 461 -350OPEC 71 60 11Japan 61 130 -69Europe ex. EMU, UK 61 102 -41United Kingdom 56 53 3

Miscellaneous 64 88 -24

Source: U.S. Census Bureau. Figures are for the 12 months through September2016, and at customs values.

U.S. Merchandise Trade by End-Use ( $U.S. bn. )

Country or Region Exports Imports Balance

Total 1,449 2,173 -724

Capital Goods 520 583 -63Industrial Supplies 392 433 -42 Petrol. & Gas Products 92 148 -56Consumer Goods 194 583 -389Motor Vehicles & Parts 151 350 -199Food, Feeds and Bev. 132 128 3

Miscellaneous 61 96 -34

Source: U.S. Census Bureau. Figures are for the 12 months through Sep. 2016, at customs value. Consumer goods are ex. food and autos.

11/14/2016

9

0

500

1000

1500

2000

70 74 78 82 86 90 94 98 02 06 10 14

Domestic plus foreign profits

Domestic profits (net)

Q2: $682 billion

Source: BEA. Domestic profits are net of payments to foreign equity holders.

U.S. Corporate Profits by Source$U.S. billions, annual rate

Reference Charts

11/14/2016

10

Source: U.S. Census Bureau. Figures are for the 12 months through September 2016.

U.S. Merchandise Exports by Destination$U.S. billions

0

50

100

150

200

250

300

Source: U.S. Census Bureau. Figures are for the 12 months through September 2016.

U.S. Merchandise Imports by Source

$U.S. billions

0

50

100

150

200

250

300

350

400

450

500

11/14/2016

11

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2007:Q4 2016:Q2

Foreign private

Sources: U.S. Treasury, Federal Reserve Board.

U.S. private

Federal Reserve

Holdings of U.S. Treasury Securities

$U.S. billions

Foreign official

$2,243

$4,038

$2,462

$5,189

Regional Economic Outlook Presentation to the Advisory Council on Small Business and Agriculture

Jason Bram, Research Officer November 15, 2016

The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or the Federal Reserve System.

Overview of Regional Conditions

• New York City’s economy continues to lead the region in growth, led by the outer boroughs.

• While NYC’s key finance sector has been sluggish, tech (which tends to pay fairly well) has been booming.

• New Jersey’s economy continues to grow modestly.

• Job trends in much of upstate NY look much stronger than current data suggest. Upstate housing markets strengthening, especially in metro Buffalo.

• Puerto Rico’s economy remains depressed.

FEDERAL RESERVE BANK OF NEW YORK 2

Down more than 1% Down 0.6% to 1% Down 0.1% to 0.5% Unchanged Up 0.1% to 0.5% Up 0.6% to 1% Up more than 1%

3

State Coincident Indexes Three-Month Change Ending September 2016

Source: Federal Reserve Bank of Philadelphia

80

90

100

110

120

Sep

130

140

2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

New York State

New Jersey

New York City

Regional Economic Activity Index of Coincident Economic Indicators (CEI)

Index (Dec2007=100)

Source: Federal Reserve Bank of New York 4

-60

-40

-20

0

Oct

20

40

60

2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

Empire State Manufacturing Survey

Business Leaders Survey

Current Economic Conditions FRBNY Business Surveys, Current Conditions

Diffusion Index

Source: Federal Reserve Bank of New York 5

Recent Private Sector Job Trends Percent Change from September 2015 to September 2016

Source: Bureau of Labor Statistics and Moody's Economy.com

Down Flat to up 1.5% Up 1.5% to 2% Up more than 2%

6

Longer-Term Private Sector Job Trends Percent Change From Previous Peak to September 2016

Source: Bureau of Labor Statistics and Moody's Economy.com

Down more than 2% Within 2% Up 2% to 5% Up more than 5%

7

88

92

96

100

104

108

112

116

120

2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

New York State

New York City

United States

New Jersey

Puerto Rico

Private-Sector Employment Seasonally Adjusted Index

Index (Dec2007=100)

Oct

Source: Bureau of Labor Statistics and Moody's Economy.com

Sep

8

88

92

96

100

2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

Glens Falls

United States

Utica

116

112 108

Oct

104

Sep

120

Albany

Private-Sector Employment Seasonally Adjusted Index

Index (Dec2007=100)

Source: Bureau of Labor Statistics and Moody's Economy.com 9

88

92

96

100

2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

Rochester

United States

Syracuse

116

112 108

Oct

104

Sep

120

Buffalo

Private-Sector Employment Seasonally Adjusted Index

Index (Dec2007=100)

Source: Bureau of Labor Statistics and Moody's Economy.com 10

Source: U.S. Bureau of Labor Statistics, Moody’s Economy.com, and FRBNY Staff Calculations.

440

445

450

455

460

465

2012 2013 2014 2015 2016

Thousands

Preliminary

Expected Revision

Albany Employment Preliminary vs Expected Revision

11

540

545

550

555

560

565

570

2012 2013 2014 2015 2016

Thousands

Preliminary

Buffalo Employment Preliminary vs Expected Revision

Expected Revision

Source: U.S. Bureau of Labor Statistics, Moody’s Economy.com, and FRBNY Staff Calculations. 12

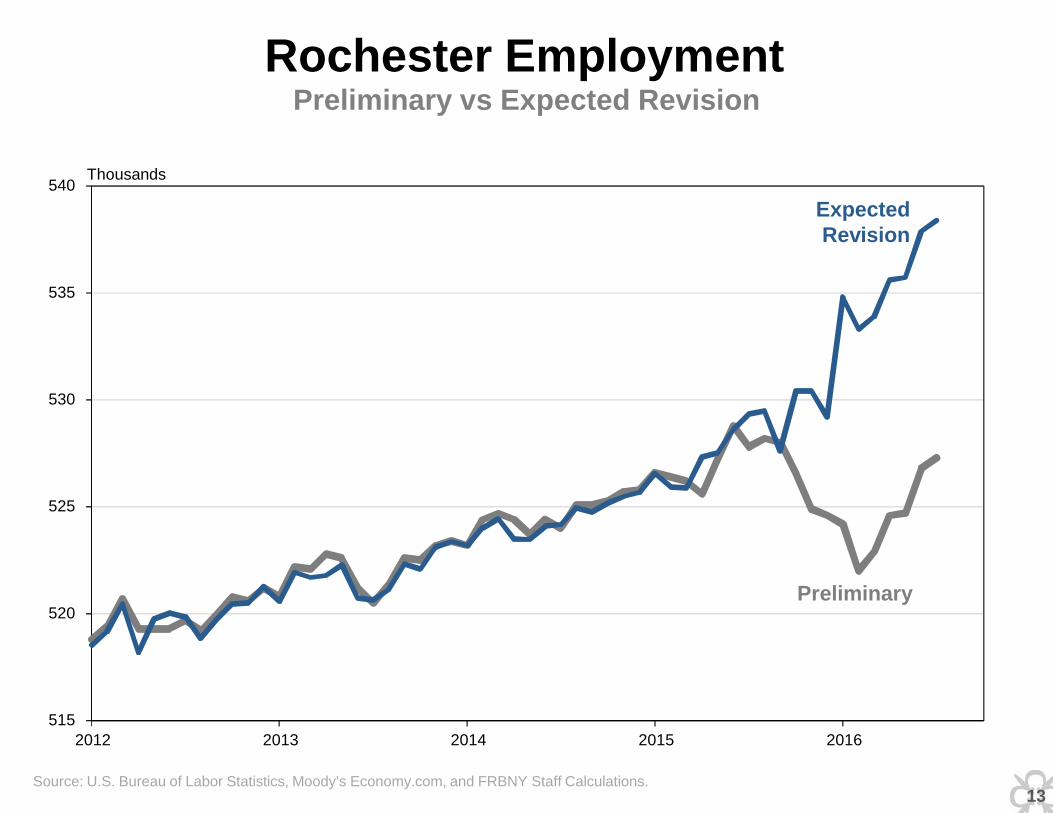

515

520

525

530

535

540

2012 2013 2014 2015 2016

Thousands

Preliminary

Rochester Employment Preliminary vs Expected Revision

Expected Revision

Source: U.S. Bureau of Labor Statistics, Moody’s Economy.com, and FRBNY Staff Calculations. 13

88

92

96

100

104

108

112

116

120

2007 2008 2009

Shading indicates NBER recession

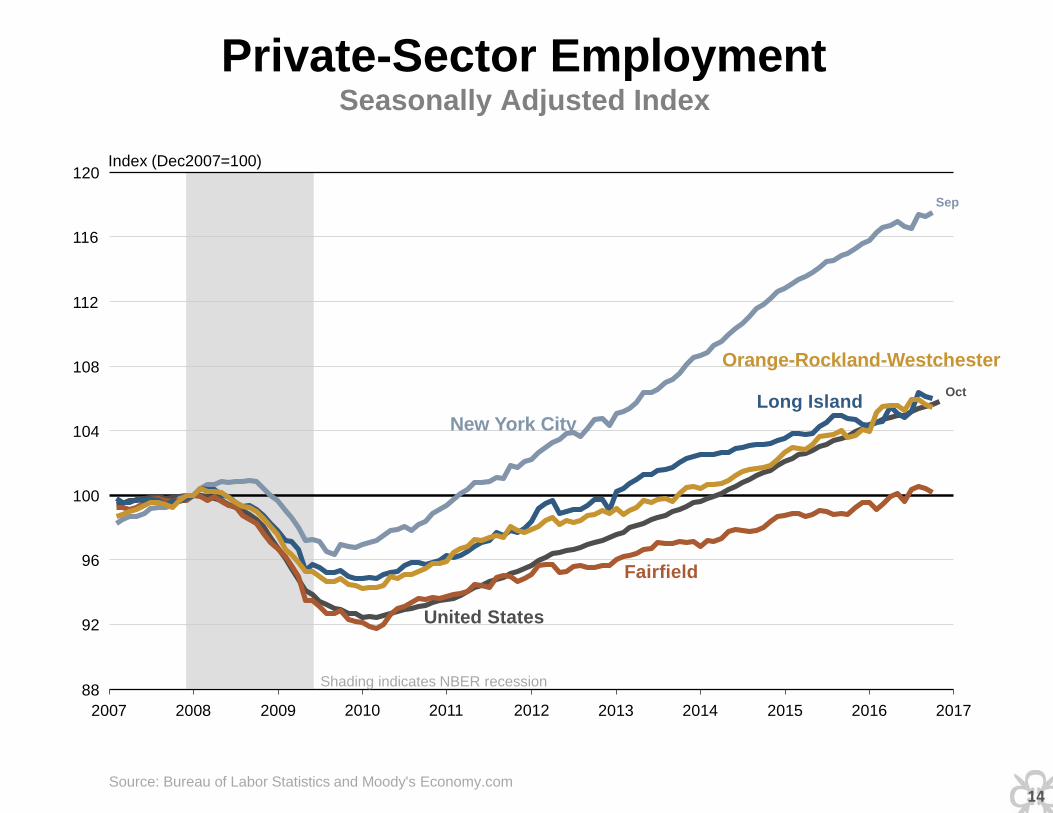

2010 2011 2012 2013 2014 2015 2016 2017

New York City Long Island

United States

Fairfield

Orange-Rockland-Westchester

Private-Sector Employment Seasonally Adjusted Index

Index (Dec2007=100)

Oct

Source: Bureau of Labor Statistics and Moody's Economy.com

Sep

14

60

90

120

150

180

210

240

270

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2,500

2,750

3,000

3,250

3,500

3,750

4,000

4,250 Shading indicates time between securities

peak and trough

Securities Employment

(left axis)

Total Employment Minus Securities

(right axis)

NYC Securities Employment Seasonally Adjusted Levels

Thousands Thousands

Sep

Source: Bureau of Labor Statistics, Moody's Economy.com, and FRBNY calculations 15

NYC Finance and Securities Sectors’ Share of NYC Employment and Earnings

Source: Bureau of Labor Statistics (QCEW). 16

0%

10%

20%

30%

40%

1972 1987 2001 2007 2015 1972 1987 2001 2007 2015

Finance Ex-Securities Securities

NYC Tech and Securities Employment Thousands of Jobs

Source: Bureau of Labor Statistics and Moody’s Economy.com.

0

50

100

150

200

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Securities Employment

Technology Employment

Thousands

+53,000

+12,000

2010 to 2015

17

Technology Employment • Computer manufacturing • Electronic shopping • Software publishing • Data processing, hosting, etc. • Internet/web search portals • Computer systems design • Scientific R&D services

Shading indicates NBER recession

60

70

80

90

100

110

120

2006 2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

United States

NYC Metro

Downstate NY

Upstate NY

New York State

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

Index (Mar2006=100)

Sep

Source: CoreLogic Home Price Index (including distressed sales) 18

60

70

80

90

100

110

120

2006 2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

United States

NYC Metro

Fairfield

Westchester

Rockland

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

Index (Mar2006=100)

Sep

Source: CoreLogic Home Price Index (including distressed sales) 19

60

70

80

90

100

110

120

2006 2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

United States

Bergen

Hudson

Passaic

Essex

Union

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

Index (Mar2006=100)

Sep

Source: CoreLogic Home Price Index (including distressed sales) HPI_5 13NOV2016 20

60

70

80

Sep

90

100

110

120

130

2006 2007 2008 2009

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

United States

Albany

Rochester

Upstate NY

Buffalo

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

Index (Mar2006=100)

Source: CoreLogic Home Price Index (including distressed sales) 21

60

80

100

120

140

160

2006 2007 2008 2009

United States

Shading indicates NBER recession

2010 2011 2012 2013 2014 2015 2016 2017

Brooklyn

Nassau County

Suffolk County

Queens

Manhattan

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

Index (Mar2006=100)

Sep

Source: CoreLogic Home Price Index (including distressed sales) 22

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Shading indicates NBER recessions

NYC Downtown

NYC Midtown

Central NJ

Northern NJ

Office Vacancy Rates Overall Vacancy Rates

Percent

Q3

Source: Cushman & Wakefield 23

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Shading indicates NBER recessions

Westchester County

Long Island

Fairfield County

Office Vacancy Rates Overall Vacancy Rates

Percent

Q3

Source: Cushman & Wakefield 24