Embed Size (px)

Citation preview

Sponsored by

T H E D E F I N I T I V E G U I D E T OT H E D E F I N I T I V E G U I D E T O

d

d

Small Business Sourcebooks for Successful SmallBusinesses and EntrepreneursFebruary 2003

RBC_84395 Text 3/14/06 11:01 AM Page 1

WE MAKE LETTING YOUR SALES FORCE KNOW THEY’RE APPRECIATED EASY.Reward them with the Chrysler Intrepid and you’ll be giving them luxury, power and space all in a single package. And while they enjoy the fruits of their labour, you’ll enjoy a car covered by our new 7 yr/115,000 km powertrain warranty and 24 hour roadside assistance. For more information about our fleet operations andaggressive programs, contact your DaimlerChrysler Fleet dealer or call 1-800-463-3600.

It’s like giving every member of your sales force their very own corner office.

www.fleet.daimlerchrysler.ca

2003 Intrepid

RBC_84395 Text 3/14/06 11:01 AM Page 2

The Definitive Guide to Small Business Financing in Canada 3

The Art & Science ofSmall Business Lending

Dispelling myths.

The Niche Lenders

Custom-tailored financing.

Financing & Assistance Directory

Financing options andresources.

Government Help

SME financing options.

To Market, To Market...

Debt isn’t always the answer.

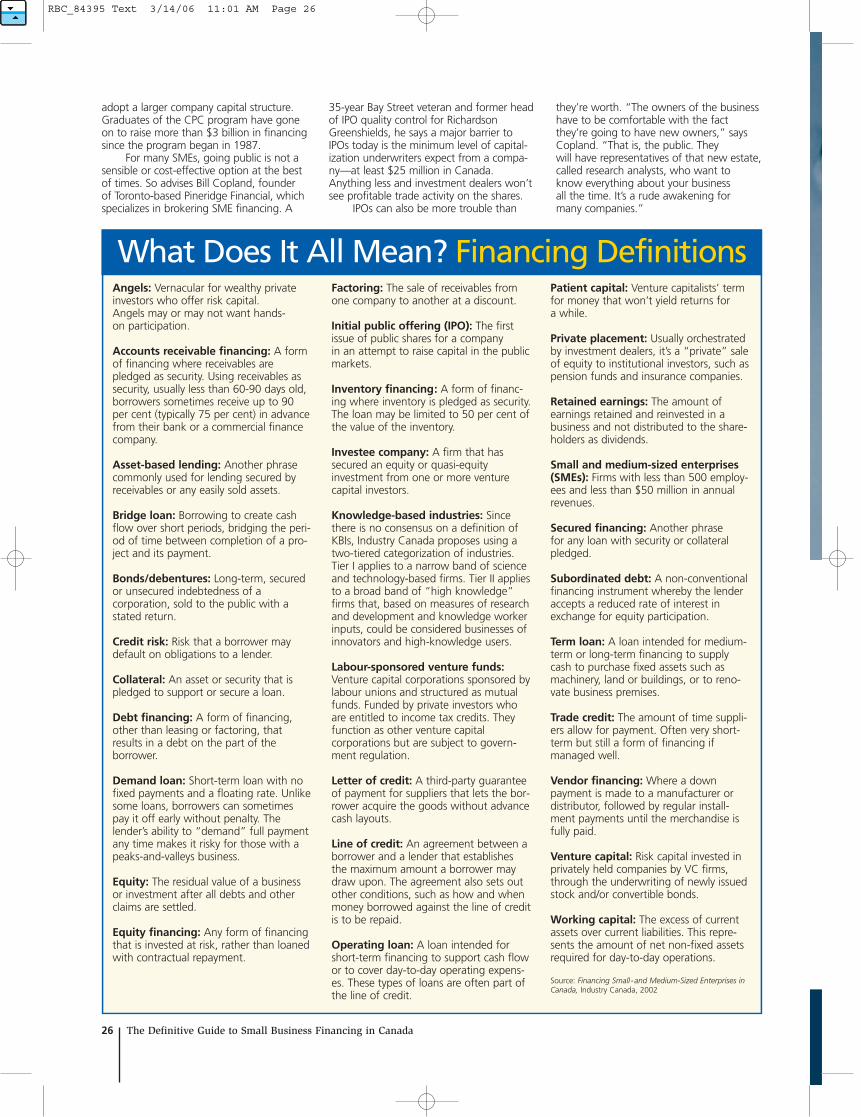

What’s it all Mean?

Financing definitions.

7

12

16

20

21

26“The Definitive Guide to Small Business Financing in Canada”is sponsored by Royal Bank of Canada. | Published by GeneralContent Corporation, 112 Adelaide Street East, Suite 400,Toronto, Ontario M5C 1K9 416-601-9247. President: Kirk KellyWriter: Charles Killin | Design & Production: Roger McFarlin Ad sales: Deb Houghting and Darlene Wang | Copy editing:Shannon Greenlaw | Photography: Getty Images | Masterfile IComstock. ©2003 General Content Corporation. No part ofthis guide can be reproduced without the written permissionof General Content Corporation. ® Registered trademark ofRoyal Bank of Canada. ™ Trademark of Royal Bank of Canada.RBC and Royal Bank are registered trademarks of Royal Bankof Canada. * Registered trade-mark of Visa InternationalService Association. Used under license.

All information provided in this Guide is, to the best of ourknowledge, current at the time of writing. As well, all infor-mation provided in this Guide is for informational purposesonly and is not intended to provide specific financial, invest-ment, tax, legal or accounting advice for you and should notbe relied upon in that regard. Royal Bank of Canada is notresponsible and will not be liable to you or anyone else for anydamages whatsoever arising out of or in connection with youruse of the information in this Guide or any action or decisionmade by you or anyone else in reliance on the information inthis Guide or any unauthorized use or reproduction of suchinformation, even if Royal Bank of Canada has been advisedof the possibility of these damages. The information in thisGuide applies to Canadian business only and may not beappropriate or correct outside of Canada. You should not actor rely on any information in this Guide without seeking theadvice of a professional.

The Changing Face of Small Business FinancingWhat a difference a few years can make! Until two years ago, it seemedthat lenders and investors were eager to finance start-ups and existingsmall businesses. Then the new economy, based on the growth of theInternet, came tumbling down. How does that affect your ability to financeor refinance your small business?

By the late 1990s, Canada was aggressively supplementing its traditionaleconomy with a dynamic high-tech sector. The emergence of the Internet as anengine of growth was awe-inspiring, and seemed to have limitless potential.

Many of Canada’s high-tech companies were small to medium-sized enter-prises (SMEs). Many drew support from venture capital companies in Canada andthe U.S., because small high-tech enterprises were either excellent acquisition tar-gets for multinational corporations, or excellent prospects for a successful initialpublic offering (IPO). Capital that had all but dried up in the recession years of theearly 90s came flooding out, from financial institutions, government agencies,labour-sponsored venture capital funds, and private investors.

T H E D E F I N I T I V E G U I D E T OT H E D E F I N I T I V E G U I D E T O

d

d

Small Business

RBC_84395 Text 3/14/06 11:01 AM Page 3

Ask for Microsoft®

Office XP on your new PC.

It costs less.*

For details, contact your

preferred computer dealer.

Or visit: www.microsoft.ca/NewPC

*An independent survey of 100 computer retailers in January 2003 indicates that Microsoft Office XP Professional costs less when loaded on a new PC than when purchased off-the-shelf as full packaged product.

©2003 Microsoft Corporation. All rights reserved. Microsoft and the Office logo are either registered trademarks or trademarks of Microsoft Corporation in the United States and/or other countries.

RBC_84395 Text 3/14/06 11:01 AM Page 4

The Definitive Guide to Small Business Financing in Canada 5

In the summer of 2000, after eightyears of steady economic and marketgrowth stimulated by low inflation and lowinterest rates, the rosy economic outlookbegan to darken.

Investors began to grow wary of theInternet business model that burned cashand spewed promises. Since even the bestof the young high-tech enterprises wereattracting investors on the strength offuture earnings—earnings that were yearsaway—investors started to pull back. Then, when general corporate earnings

began showing signs of faltering, stockprices plummeted and technology compa-nies suffered most. The dot-com bubblehad burst.

In the ensuing two years, investorsfrom pension funds to entrepreneurs tofamilies have felt the pain of collapsingmarkets. But time is a great healer andeven two years is enough time to digestevents and learn lessons. What are the cur-rent prospects for financing or refinancinga small business in Canada?

One caveat: while this guide presentsan overview of the general financing climate, actual financing is done on a case-by-case basis. Many successful entrepre-neurs are not embraced by the first lenderor investor they approach. In the end, per-sistence, confidence and discipline can be

as important to obtaining financing asunderstanding general conditions in thefinancing market.

With that in mind, it’s also safe to saythat the general conditions for financingare different than they were even a fewyears ago. Some sources are intact, butothers are not.

For example, the market for initialpublic offerings has all but dried up for thepresent time. “The IPO market is dead,”admitted venture capitalist David Fergusonof Vengrowth in a July 2002 interview with

the Financial Post, adding that it could beyears before that window re-opens. Whenit does, Ferguson believes, the only compa-nies that make it through will be profitableones with viable business models.

IPOs suffer in bear markets, and havealways returned with the bulls. In the near-term, however, the IPO slump makesthe capital markets an unlikely source offinancing for small business–and claps arestraint on venture capital financing aswell. Venture capitalists make their moneywhen their interests in an enterprise arepurchased by a larger corporation throughan acquisition, or by the capital marketsthrough an IPO. This is known in the ven-ture capital business as an exit strategy.

The recent slide in IPOs has been par-alleled by a similar skid in corporate acqui-

sitions, which has temporarily blocked bothclassic venture capital exit strategies. In arecent Morningstar Canada web column,analyst Iain Giles noted, “As public compa-nies have halted their shopping sprees andIPOs have become few and far between,deal flow has dramatically slowed, particu-larly in the technology space.”

The good news is that venture capitalcompanies are still out there doing whatthey’ve always done; the bad news is thatthey’re somewhat dormant these days,waiting for a high-tech revival.

If you’re not in a technology-basedindustry, some evidence suggests that ven-ture capital may not be as important foryour business. A Statistics Canada survey ofmature small businesses (10+ years) acrossall industries found that, on average, ven-ture capital accounted for less than 1 percent of all funding. Retained earnings andbank loans constituted the major sourcesof funding within these businesses. In fact,equity from retained earnings accountedfor an average 40 per cent of total workingcapital. It is interesting to note that thissurvey was released in May 2000, at thepeak of the high-tech boom.

This evidence is both encouraging andtroubling at the same time. On one hand,it shows that many successful small busi-nesses in Canada are quite self-sufficientwhen it comes to financing. On the otherhand, financing from retained earningsrelies on profitability. Have hard economictimes, as experienced over the past twoyears, pushed small businesses into greaterreliance on debt financing?

Investors began to grow wary of the Internet businessmodel that burned cash and spewed promises.

RBC_84395 Text 3/14/06 11:01 AM Page 5

Undoubtedly so. Lending institutions,while certainly more cautious than theywere a few years ago, are operating busi-ness as usual. Canada’s major banks wererecently forced to write down loan losses,but most of these losses have been gener-ated by larger corporations rather thanSMEs. In many ways, lenders favour a creditportfolio that distributes smaller amounts tomany borrowers, because it spreads out therisk and offers the institution a range ofinterest rates depending on the specifics ofeach case.

Most financial institutions across thecountry that began SME divisions in the1990s still maintain them. “We are a smallbusiness country; 40 per cent of the busi-ness loans we make are to customers whoborrow less than $25,000,” advises JimHamilton, vice-president, small business andagriculture at RBC Royal Bank. “Indeed, theaverage RBC Royal Bank business loanbelow $1 million is $65,000.”

In spite of these reasonable amounts,institutions still tend to be more cautious incircumstances like general economic down-turns. Has this caution constrained the debtcapital markets? The answer appears to beno. This seems to be the conclusionreached by both the Statistics Canada sur-vey cited above, as well as a more recentsurvey, The Path to Prosperity, co-sponsoredby the Canadian Federation of IndependentBusiness, Canadian Manufacturers &Exporters, and the companies under RBCFinancial Group. This survey, released inOctober 2002, found that financial institu-tions must address account managerturnover, provide convenient access to ser-vices, and enhance the quality of advice.

However, the report goes on to saythat the Canadian financial services industryis a world leader in many aspects of busi-ness financing.

For example, the spread between typi-cal lending and deposit rates in Canada isthe fourth-lowest among 75 countries.Canadian businesses, and SMEs in particu-lar, get a far better deal on financing coststhan American SMEs do at their banks.Small business banking fees are also lowerin Canada.

Loan approval rates for CanadianSMEs range between 79 and 94 per cent,depending upon size of company. Althoughsome Canadian entrepreneurs are ambiva-lent about financial institutions, the report

concludes; “the hard evidence on thismatter speaks for itself.”

To underscore its commitment toSMEs, the Canadian Bankers Associationreleased the Model Code of Conduct forBank Relations with Small-Medium-SizedBusinesses in 2002. In its preamble, theCode states, “Canada’s chartered banksrecognize that they have an important andunique role to play in fostering the growthof SMEs in Canada.” As a minimum stan-dard to be adopted by banks, the Codeoutlines a fair credit process that dealswith application, approval, disclosure, andchanging circumstances in the credit rela-tionship. Among the important provisionsare complaint handling, and recourse tothe Financial Consumer Agency ofCanada.

Further reassurance about the credit-worthiness of Canada’s SME sector comesfrom Business Development Bank’sPresident and CEO Michel Vennat. InBDC’s 2002 Annual Report, Vennat says,“Despite the slowing economy, small andmedium-sized enterprises continued toshow good results.”

A good example of lending institu-tions developing resources to help entre-preneurs run their businesses is theOne-Stop Business Resource Centre inRegina, Saskatchewan. RBC Royal Bankhelped create the Centre, a non-profitconsulting service to individuals interestedin setting up a business.

“Getting started can be very diffi-cult,” says Hamilton. “That’s why we’vealigned with other professionals, such asaccountants and lawyers, to provide a freesounding board for start-ups. The objec-tive is to provide a solid foundation so thatstart-ups can grow and prosper.”

In summary, while financing for smalland medium-sized businesses in Canada,has a different profile than it did a fewyears ago, it has almost as many possibili-ties. Low inflation and low interest rateshave persisted, and Canada’s economy hasbeen outperforming the economies ofmany other industrialized nations.

While financing from the capital mar-kets and venture capital sources hasdecreased significantly, this will most likelyaffect high-tech startups more than anyother SME segment. Government and pri-vate debt financing sources have main-tained their confidence in small business,

and have not been overly sensitive to thesluggish economy.

One final but important note forstartup enterprises: every type of financingcomes with costs as well as obligations.Financial institutions will lend you a dollarfor every dollar of equity you invest, or willotherwise seek to lower their risk throughother assets you may own. You must keepup your payments and provide regularfinancial reports to your lender.

Private equity investors, such as ven-ture capital companies, are in the businessof accepting risk. The tradeoff, however, isthat they will want to protect their invest-ment by helping you manage your busi-ness in a hands-on way. They also look fora much larger return on their investmentthan a secured lender. Friends and familywho invest equity in your business mayfeel the same way.

With knowledge of financing comesthe power to build your business.

6 The Definitive Guide to Small Business Financing in Canada

Loan Authorization Rates by Size of Company

Number of employees % of loans appoved

1–4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79%

5–19 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85%

20–99 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87%

100–499 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94%

Sources: Financing of Small and Medium-Sized Enterprises, Statistics Canada 2000

What’s A SME?Under Industry Canada’s definition, theterm “SME” (for small or medium-sizedenterprise) represents all companieswith up to 500 employees.

How Many SMEs?

Statistics Canada says there were about2.2 million Canadian SMEs at December2001, including self-employed individu-als. About half of these SMEs haveemployees, and 59 per cent of thosehave fewer than five.

How Big?

Two-thirds (66 per cent) of SMEs haveannual sales less than $500,000, includ-ing almost half (49 per cent) that reportsales less than $250,000. Seventy-nineper cent report annual sales less thanone million.

SMEs and banks

Canada’s banks have relationships withover 1.6 million small businesses. As ofJune 2001, the seven major banksauthorized $71 billion in debt financingto over 819,000 SME customers inCanada. That’s an increase of almost $5billion in capital, and a 17 per centincrease in the number of customerssince 1996.

Sources: Financing of Small and Medium-SizedEnterprises, Statistics Canada 2000; Key Small BusinessStatistics, Industry Canada July 2002; Small- AndMedium-Sized Businesses In Canada: An OngoingPerspective of Their Needs, Expectations and Satisfactionwith Financial Institutions, 1998 Thompson Lightstone &Company Limited; The Canadian Bankers Association.

RBC_84395 Text 3/14/06 11:01 AM Page 6

What does a lender really need to know? It may seem like a mysterious art, but lending is actually based on soundbusiness principles.

&BusinessArt Science of

Lending

The Definitive Guide to Small Business Financing in Canada 7

RBC_84395 Text 3/14/06 11:01 AM Page 7

8 The Definitive Guide to Small Business Financing in Canada

Understanding what makes banks andother lenders tick was once a major chal-lenge for SME owners and managers.However, that’s changing.

“It’s our job to understand the busi-ness owner’s point of view,” says JimHamilton, RBC Royal Bank vice president,small business and agriculture. “Bankershave traditionally been highly analytic,dealing only with numbers, and mostentrepreneurs are visionaries—concept-and action-oriented. The best bankers arethose who can bridge that gap and trulyunderstand the entrepreneur.”

That said, there is basic informationany lender needs to decide whether a loanto a start-up or existing business is feasible.The first issue both a lender and borrowerneed to think about is how much money is needed.

“Somebody coming in the door whois starting their business and looking for$500,000 of loan financing may have unre-alistic expectations and be taking on tooheavy a debt load,” says Hamilton. “Butmost businesses starting today are lookingfor less than $50,000. Thanks to technolo-gy, many are starting from their home orsmall offices, with much lower overhead.”

If you are a start-up, the lender will tryto assess whether you have the businesssavvy to make it a go. “We look for peoplestarting businesses who are coming from aplace of experience,” she says. “If youworked for an engineering firm and decid-ed to set up your own engineering consult-ing firm, I would say that’s good. If youworked in an engineering firm and wantedto start up an ad agency, I might not feelas comfortable.”

A good credit history is also impor-tant, even if it’s just responsible handling ofa credit card. A major concern of businessborrowers is often the lender’s request fora personal guarantee, something Hamiltonsays is hard to avoid.

“For start-ups, realistically you mustgive a guarantee. The banker needs toknow that the entrepreneur believes in hisor her business.”

You may also need to offer security orcollateral, but bankers are aware of thecriticisms that they sometimes ask for too much. Recently, many major banks and other financial institutions have takena lot of the pain out of getting smallerloans. For instance, RBC Royal Bank VISA*CreditLine for small business™ is a creditcard with a $50,000 limit that requires no business plan, no security and only a per-sonal guarantee.

Resources to help SMEs learn aboutloan requirements are plentiful. Detailedguides are available in most bank branchesand some even provide software to help.

RBC Royal Bank for example, has free software called “The Big Idea” which isavailable on the bank’s Web site. It includesa SME start-up guide, examples of businessplans, loan applications, and descriptions oftheir business services.

If you’re after a larger amount ofmoney, a lender will likely need moredetails on your business. Requirements forwritten business plans when applying forfinancing will vary across financial institutions, however, a business plan can

be helpful for both the lender and borrower. There are lots of good books and even software you can buy to help create a full-fledged business plan, buthere is an approach that may be a good starting point:

Introductory letter A professional cour-tesy in some regard, it briefly states whythe plan has been written and highlights itsmajor features.

Title page, contents & executive summary This will help a lender get a feelfor the breakdown of information. The

summary is important. Don’t assume peo-ple will read your plan cover-to-cover.Succinctly state what the business is about,what will make it successful, and howmuch you will need from the lender to getthere. If you or others already have moneyinvested in the business, outline how muchand how it was spent. If you have securityor collateral to offer, this is a good place tohighlight it. As well, explain the financialhealth of the business.

Business summary & history This provides an overall picture, from the time the business was started to its future objectives.

The industry This provides a snapshot ofcurrent market conditions for the industry,consumer demand and a brief analysis ofthe competition. The lender will often wantto know how large the industry sector isand why it may be different from others,such as seasonal cycles. When discussingyour competition, it may be helpful to giveas much information as you can abouttheir size, sales, strengths and weaknesses.Also, it may be able to describe the trendsthat are shaping your industry over thenext five to 10 years.

Services/products This is a key compo-nent of the plan, where you describe whatis unique about your products and services,

Understanding what makes banks and other lenders tick was once a major challenge for SME

owners and managers.

RBC_84395 Text 3/14/06 11:01 AM Page 8

130,000 Canadiansmall businesses

fail every year 1

Give yourself every advantage.Choose QuickBooks – the #1 best sellingaccounting software for small business.2

Don’t worry. You don’t need any accountingknowledge to use QuickBooks. The accountinggoes on behind the scenes. You work with familiarcheques and forms.

It’s easy to use. Set it up exactly the way youneed it for your own business. Chequing, invoicing,PST/GST, budgeting, reporting… and so muchmore! There’s a FREE 34-topic tutorial with everyproduct.

Incredible reporting. You don’t need to knowhow to set up financial reports to get an instantsnapshot of your business. More than 100QuickBooks reports are all just a click away.

Don’t wait for the end of the year to worry aboutthe books. Get QuickBooks on it now.

Pick up QuickBooks along with all your otherbusiness essentials.

It’s risk free. If you are not 100% delighted,return to us for a refund!

Not sure which product’s right for you?QuickBooks experts are waiting for your call. They’llhelp you select the QuickBooks solution that’sright for your business.

Designed for small business…“I have used QuickBooks for years andI have found this product superior toall others on the market.

It is a very user friendly product.Its editing features, inventory module,and accounts receivable module workvery well in today's changingmarketplace. I would highlyrecommend this product for allsmall businesses.”

Carmen Loxamsmall business owner

Recommended by accountants…“I am constantly called upon tohelp clients choose an accountingprogram that best suits their needs.

Since the first time I used QuickBooks,I was blown away by the product'sversatility. I have never found a clientwhose needs have not been satisfiedby this product.

QuickBooks is dedicated to progressand seems to anticipate the nextgrowth steps of my clients.”

Virginia Smithaccounting technicianfor small business

Call now toll-free 1-888-333-8580 or shop online at www.intuit.ca

BUYQUICKBOOKS

NOW and get aFREE ElectronicTraining Guide

Act now whilequantities last.

Quote Priority Code 1168-868 when you call or visit our Web site.We’ll include a FREE electronic training guide with your order.

The Training Guide will help you master the fundamentals ofQuickBooks – then learn how to do more! Sample files, how-toinstruction, comprehensive and easy-to-follow lessons, handoutsfor quick review… all FREE when you order now!

Make sure you get off to the right start!Stay on top of your finances with QuickBooks!

1. CIBC World Markets, 2002; 2. North American, PC Data and ACNielsen’s Computer Product Index, 2001

2003Designed for small business.Recommended by accountants.

RBC_84395 Text 4/3/06 9:50 AM Page 9

and how this differentiates you from your competition.

Management The background, responsi-bilities and qualifications of key personnel,as well as any references. The lender willoften want to know how much key peopleare paid.

Marketing plan Who is the target market,how big is it and how will the businessgenerate its sales? Here, you may want toexplain costs and pricing policies, as well asdistribution and promotional plans.

Capital equipment If you own or needland, buildings or equipment, it may beuseful to explain what it’s worth or costs,how it is to be financed and why it is vitalto the success of the business.

Operations An important part of anymanufacturer’s proposal, this brieflyexplains the mechanics of your business’work flow, inventory controls, personnelrequirements and production schedules.

Financial plan Profit-and-loss, balancesheet, projected income, sales and, mostimportant, cash flow statements are vital.

Risks This is where you demonstrate yourbusiness savvy and backup plans. Forexample, you may want to explain theworst-case scenarios for your business,what steps you are taking to avoid thoserisks and what you can do to minimizetheir impact if they were to happen.

Conclusion This is where you can restatethe goals and objectives for your business,the financing you’re seeking, and why youbelieve you are a qualified applicant.

That’s the written plan, but it’s alsooften wise to emphasize certain points dur-ing face-to-face discussions with lenders.The fact that you have equity or personalcapital at risk is often important. Credit his-tory, particularly if it is with that lender, isoften important, as are your references andpersonal reputation.

If your cash flow is strong enough tocover loan payments and interest, you maywant to discuss those figures and make itclear that it will not place a strain on thebusiness. You may also want to make apoint of emphasizing security or collateralyou have to offer such as receivables andinventory. If you’re using equipment orproperty as security, the lender may needvaluations and proof of insurance. Most

lenders accept real estate, equipment and personal assets such as homes, stocks and bonds, life and fire insurance as security.

Don’t expect a lender to accept 100per cent of an asset as collateral. AUniversity of Western Ontario study, Banksand Small Business Borrowers, found theliquidation value of assets was often wellbelow the market value and that the average recovery rate on collateral used for SME loans is less than 65 cents on the dollar.

Banks usually follow internal guide-lines for collateral. For example, an assign-ment of accounts receivable within 90 daysmay be valued at 50 to 75 per cent. Achattel mortgage on business equipmentor machinery may be limited to 60 to 80per cent. Inventory often isn’t given morethan 50 per cent of its value when used as collateral.

Hamilton advises, “The best time toapproach a bank is right when the business is starting. Typically there may beno borrowing requirement at this time. This allows both the banker and the business owner to get to know each other and develop a relationship as thebusiness grows.”

Are there times when a business willbe unlikely to get a loan? Yes. “If theyhave a poor credit history or have a previous bankruptcy, realistically, they arenot likely to get a loan,” says Hamilton.“Also, a time of crisis is not the best time to be looking for a new banking relationship.”

Still, he says, most lenders want toknow if a SME is experiencing difficultiesand want a chance to offer early financingsolutions or advice. Says Hamilton: “It iscritically important for a business owner tomaintain a relationship with its lender. Yourbanker should support you through toughtimes if you keep the lines of communica-tion open.”

Women & SMEsWomen Running SMEs

Forty-five per cent of all SMEs have atleast one female owner. For 34 per centof all SMEs, women hold half ownershipor more.

Size of Business

Majority female-owned businesses tendto be smaller and have fewer employ-ees, accounting for 16 per cent of SMEswith fewer than 5 employees, and 4 percent of SMEs with more than 100 employees.

Structure of Firms

Forty-four per cent of majority female-owned SMEs are incorporated, 51 percent are sole proprietorships and 5 percent are partnerships. The correspond-ing figures for majority male-ownedSMEs are 55 per cent incorporated, 47per cent sole proprietorships, 8 per centpartnerships.

Source: Survey on Financing of Small and Medium-SizedEnterprises, Statistics Canada 2000

10 The Definitive Guide to Small Business Financing in Canada

RBC_84395 Text 3/14/06 11:01 AM Page 10

There is a better way to manage your business finances.

To start enjoying the NEW Online Banking for Business now, visit www.rbcroyalbank.com/online or call us at 1-800-ROYAL® 7-0 (1-800-769-2570).

TM Trade-mark of Royal Bank of Canada. RBC and Royal Bank are registered trade-marks of Royal Bank of Canada.†Registered trade-mark of Visa International Service Association. Used under license.

Account Statements

Bills

Payroll

GST Remittances

• Make bill payments• Research other products and services

or rates• Copy activity from business accounts

loans and VISA† files to many popularaccounting software packages.

• View all your accounts(Canadian and US Dollar)

• Transfer funds between accounts• File your taxes, GST payments and

payroll source deduction remittances24 hours a day

RBC Royal Bank™ Online Banking has made it easier than ever for you to manageyour banking and financial needs. You can go online to view your entire financialpicture at a glance, as well as make a wide variety of transactions.Now you can:

RBC_84395 Text 3/14/06 11:01 AM Page 11

The NichLenders

Custom-Tailored Financing:

12 The Definitive Guide to Small Business Financing in Canada

Depending on what you need money for,there’s a broad range of alternative andnew financing options available to SMEs.

RBC_84395 Text 3/14/06 11:01 AM Page 12

The Definitive Guide to Small Business Financing in Canada 13

For fast-growing, highly leveragedcompanies, efficient collection of accountsreceivable is the first strategy for easingcash flow bottlenecks. However, gettingcash against receivables is just one of themany alternatives SMEs can use to easecash flow, raise money for an expansion orto secure long-term loans. Banks offer amuch wider range of financial servicesthan they did in the past. As well, thereare some niche financial services players inthe marketplace worth considering.

Private term lenders, merchant banks,insurance companies, pension funds,bridge financiers, leasing and factoringfirms are some of the options. Each isgeared to lending money for specific usesand, depending on your needs, may beable to offer financing at a cost that doesn’t impair your credit rating or giveaway equity.

For example, traditional lenders typically don’t like long-term debt on their books. This exposure makes somelenders nervous, and low interest rateguarantees beyond a few years simply

aren’t as profitable as floating rates orshorter terms.

For some SMEs, however, the natureof their businesses or the capital equip-ment they’re buying may require a 5 to 10year term, with amortizations of 10 to 25years to make payments affordable. Theymay even need an unusual payment pat-tern if it’s a seasonal business or project-based firm.

Lenders for long-term opportunitiestypically require borrowers to have a prof-itable track record and, if they don’t havemuch cash on hand, to have good assetssuch as a plant or equipment to use assecurity. Even intellectual property, such as

a well-known brand name with licensingpotential, can satisfy the lender’s need for security.

Long-term lenders also require fre-quent reporting on the health of theirinvestments, to the point where they maytake an active role advising borrowersabout managing their operations. Note thesimilarity here to risk capital investors.

THE FACTORS OF BUSINESS LIFE

Customers who don’t pay on time orbecome “collections nightmares” are SMEcash flow killers. Even SMEs with reliableaccounts may have a project or expansionin mind with immediate cash require-ments. What to do?

Some business owners may not beaware that some finance companies spe-cialize in outright purchases of accountsreceivable for cash—a service traditionallyknown as factoring. In years past, factor-ing companies were considered a last

resort because the customer would be toldto pay the factor directly. This sent a signalto the customer that the supplier wasfinancially unstable.

Today, factoring companies offer arange of services, often working transpar-ently. Some even operate as an outsourcedaccounts receivable department, sendingout your invoices and tracking collections.

Here’s how they work: the factoringcompany pays you about 70 to 80 percent of the value of your receivables assoon as a sale is made. When the cus-tomer pays in full, you get the rest of themoney less the factor’s fee and any inter-est charges. Some factors may agree to

che

Private term lenders, merchant banks, insurance companies, pension funds, bridge financiers, leasing

and factoring firms are some of the options.

RBC_84395 Text 3/14/06 11:01 AM Page 13

14 The Definitive Guide to Small Business Financing in Canada

non-recourse deals, which means theyassume the risk for bad debts. Many will accept the risk without a personal guarantee.

Factors look for a good credit historyin companies and their customers. They’llalso expect you to deal with customer com-plaints, service calls and warranty claims.

Using your assets

If you don’t want to sell youraccounts receivable outright, a viablealternative can be asset-based financing.Asset-based financing uses the inherentvalue in your company’s accounts receiv-able and inventory as security for debt

capital. Under the asset-based financingmodel, a bank can lend more money tocompanies that might not qualify for con-ventional bank financing.

Claude Alexander, Senior Manager,Portfolio & Risk for RBC Royal Bank’sAsset-Based Financing division, says thatasset-based financing was developed over20 years ago by American investmentbankers to acquire companies by leverag-ing their assets. Now it can also functionas a mechanism to finance general work-ing capital requirements, taking the formof a revolving line of credit with a limitthat floats with the value of a company’sworking capital assets: accounts receivableand inventory.

“As a company increases sales, itgrows accounts receivable and inventory,”says Alexander. “Then the credit limit willgrow by the same amount. Since financ-ing is directly related to assets, balancesheet and income statement covenantsare not as important when compared toconventional bank financing. This meansasset-based financing may be able to pro-vide larger overall operating lines of creditcompared to covenant-based facilities.”

From a business perspective—whether it’s long-term secured borrowing, factoring, asset-based financing, or otheremerging forms of financing such as leasing—alternative financing sources can help keep your traditional debt under control.

V A R I E T Y I S T H E S P I C E O F B U S I N E S S

Rank & Company Year Industry Location Revenue Revenue Growth Profit Profit Source of Founded 1996 2001 % 1996 2001 Financing

1 CryptoLogic Inc 1995 Internet-casino software and services Toronto, ON $256,672 $67,455,000 26,181% ($722,887) 28,001,000 1,12,13

2 Pivotal Corp. 1994 CRM software and services North Vancouver, BC $399,000 $95,290,000 23,782% ($1,261,000) ($32,455,000) 10,11,13,15

3 Phonetime International Inc. 1995 Prepaid long-distance phone cards Mississauga, ON $130,876 $20,148,708 15,295% ($86,548) $769,000 2,4 8,11,13,14,15

4 Intrinsyc Software Inc. 1992 “Embedded systems” hardware & software Vancouver, BC. $82,472 $10,940,424 13,166% ($602,928) ($3,734,165) 1,7,8,9,11,12,13

5 DreamCatcher Interactive Inc. 1996 Video-game publisher Toronto, ON. $283,308 $30,001,043 10,490% ($542,134) $3,424,210 4,11,12

6 Hi-Alta Capital Inc. 1995 Western Canada insurance brokers High River, AB $230,311 $22,449,174 9,647% ($75,476) $991,820 3,4,5,67,8,10,11,13,14

7 Sylogist Inc. 1993 Enterprise and mobile-workforce software Calgary, AB $215,775 $14,933,070 6,821% ($206,818) ($183,367) 6,8,11,13,15

8 Hydrogenics Corp. 1995 Fuel cells for cars and power generation Mississauga, ON $168,094 $11,490,000 6,735% $8,758 ($4,632,000) 7,9,11,13,15

9 Whitehill Technologies Inc. 1994 E-document software for law firms Moncton, NB $116,639 $7,829,973 6,613% $5,073 $903,282 1,4,8,9,11,15

10 JDS Uniphase 1981 Fibre-optics components mfr. Ottawa, ON $74,833,000 $4,911,300,000 6,463% $12,941,000 ($85,260,400,000) 7,11,13

11 Iamgold Corp. 1990 Gold mining and exploration Markham, ON $1,259,000 $81,665,000 6,386% $3,972,000 $10,948,000 4,6,7,8,10,11,12,13,15

12 Proprietary Industries Inc. 1993 Real estate, oil & gas, mining Calgary, AB $934,829 $58,108,626 6,116% $215,767 $16,789,454 4,7,11,13

13 BCE Emergis Inc. 1988 Online insurance-claim Montreal, QC $11,025,479 $656,400,000 5,853% ($614,880) ($414,400,000) 11,13and bank-transaction processing

14 Bridges.com Inc. 1994 Interactive career-planning software Kelowna, BC $336,339 $19,524,945 5,705% ($570,244) ($1,180,732) 4,8,11,13

15 Edge Entertainment Inc. 1994 Movie and TV production Saskatoon, SK $121,237 $6,490,379 5,253% ($3,053) $182,885 4,8,11,12,15

Source: PROFIT: Your Guide to Business Success, “The PROFIT 100 ranking of Canada’s Fastest-Growing Companies” June 2002.

Continuing a trend from previous years, entrepreneurs runningsome of the fastest-growing small and medium-sized business-es in Canada use a wide variety of financing sources. Almost alldip into their own pocket, public stock issues being the next

most common source of financing. Chartered banks andfriends and relatives were slightly ahead of venture capital, followed then by a diverse range of other financiers includingangels or even suppliers and customers.

Source of Financing: 1 - Angels, 2 - Barter, 3 - Bond, 4 - Chartered banks, 5 - Customer, 6 - Employees, 7 - Foreign lenders /investors, 8 - Friends and relatives, 9 - Government,

10 - Other financial institutions, 11 - Owners, 12 - Private investors, 13 - Public stock, 14 - Suppliers, 15 - Venture capital

Youth & SMEsYoung Entrepreneur Help

• The Ministry of Economic Development and Trade delivers the Student Venture Loan Program in conjunction with Royal Bank of Canada. Students between the ages of 15 and 29 can borrow up to $3,000 for the purpose of owning and operating a summer business.

• Other government programs for student business loans are available, including Student Business Loans (BDC), Student Venture Capital (NB) and Youth Entrepreneurial Scholarships (NS).

• The Young Entrepreneurs Small BusinessLoan program is a First Nation and Inuit Youth initiative geared to young (34 and under) Status Indian entrepreneurs, living on reserve in N.B., N.S. and P.E.I. Joint Venture partners are Ulnooweg,

the Provinces of N.B/N.S. and ACOA, and T-D Canada Trust for N.S. and Royal Bank of Canada for N.B.

• Youth Business is a non-profit, private sector initiative designed to pro-vide mentoring and funding to young Canadian entrepreneurs. The founding members are the CIBC, Royal Bank of Canada, and Canadian Youth Foundation. Youth Business is structuredto provide loans on average of $7,500, with a maximum of $15,000 for qualifying businesses.

• The Young Entrepreneurs Association, started in 1993, promotes entrepreneur-ship and delivers seminars on a variety of business topics. It also provides peer support and networking opportunities through its corporate sponsors, such as Royal Bank of Canada.

RBC_84395 Text 3/14/06 11:01 AM Page 14

Read your customers’minds

Use the power of customer feedback to drive improvements in your company’s operations...

and grow your profits, too.

CRi™ not only tells you what your customers arethinking, it tells you how to serve them better andearn more profits while you’re doing it.

CRi is the Customer Relationship Index – a simple,cost-effective Web-based survey tool that in just 35 business days will answer seven key questions including:

• How strong are my customer relationships?• Would my customers refer me to others?• How easy is it for my customers to defect

to a competitor?

• Where exactly do I have problems in my customer relations?

• Which clients present the biggest opportunity for more business now?

• Which clients are at the greatest risk of defecting?• What can I do right now to improve my customer

relationships?

CRi. It’s priced far lower than conventional marketresearch…and designed to give you far more. Infact, for as little as $10,000, it’s customer intelli-gence that pays for itself.

Call General Content at 416-601-9247 ext 255 or visit our Web site: www.generalcontent.com/CRi

How do I get started? TM

TM Trademark of General Content Corporation

RBC_84395 Text 3/14/06 11:01 AM Page 15

General Financing Sources

RBC Royal Bankwww.rbcroyalbank.comSME financing range & avg.:$1000 to $5+ million; avg. $81,000 Avg. finance period:

12 to 60 monthsSME portfolio: $20 billionPreferred SME: No restrictionsSpecial SME programs: Widevariety of SME programs,including term financing, RoyalBusiness Overdraft Protectionof up to $5,000; RoyalBusiness OperatingLine™,offering a line of creditbetween $5,000 and $100,000(or higher, if needed); RBCRoyal Bank VISA* CreditLinefor small business™, whichoffers a line of credit of up to$50,000; asset-based financ-ing; and Canada SmallBusiness Financing (CSBF)Loan, offering up to $250,000for equipment and propertypurchases/improvements (gov-ernment guaranteed).Contact: Local BusinessBanking Centres or 1-800-ROYAL®2-0 (1-800-769-2520)

BMO Bank of Montrealwww.bmo.comFinancing range & avg.: VariesAvg. finance period:

300 month maximumPreferred SME: No restrictionsSpecial SME programs: Widevariety of SME programs,including Small Business Lineof Credit (SBLOC) offeringbetween $1,000 and $50,000,Operating Line of Credit

(OLOC) for amounts over$50,000, and US loansthrough Harris Bank.Contact: Local branches or 1-877-262-5907

CIBC Canadian Imperial Bank of Commercewww.cibc.comFinancing range & avg.:$1000 to $5+ millionPreferred SME: No restrictionsSpecial SME programs: Widevariety of SME programs.Contact: Local branches or1-800-465-CIBC.

National Bank of Canadawww.nbc.caPreferred SME: No restrictionsSpecial SME programs: Widevariety of SME programsContact: Local branches or 1-877-394-6611

Scotiabankwww.scotiabank.comFinancing range & avg.:$1000 to $5+ millionSpecial SME programs: Widevariety of SME programs.Contact: Local branches.

TD Canada Trustwww.tdcanadatrust.comFinancing range & avg.:$1000 to $500,000Avg. finance period:

12 to 180 monthsPreferred SME: No restrictionsSpecial SME programs: Widevariety of SME programs.Contact: Local branches or 1-877-247-2265.

American Capital Partners Limitedwww.financecorp.com

Financing range & avg.:$1,000,000 to $15,000,000Preferred SME: Existing compa-nies, selective start-upsSpecial SME programs:

Specializing in financialrestructuring, acquisitionfinancing and refinancing.Contact: (416) 363-3888

Canadian Western Bankwww.cwbank.comFinancing range & avg.:$250,000 to $20,000,000.Preferred SME: SMEs in western provincesSpecial SME programs:

Operating lines of credit, termloans, equipment financingand leasing, real estate andenergy lending.Contact: Offices in B.C. and Alberta.

BNP Paribas (Canada)www.bnpparibas.caFinancing range & avg.: $1 to$5 millionFees: Service charges 1 percent max.Preferred SME: No restrictionsSpecial SME programs:

Offering export financing,operating and term loans andworking capital.Contact: Regional offices or(514) 285-6000

HSBC Canada www.hsbc.caFinancing range & avg.:$250,000 to $5+ million; Avg. finance period: 12 to 120 monthsPreferred SME: Companies inBritish Columbia., Alberta,Saskatchewan, Manitoba,Ontario, Quebec, New

Brunswick, Nova Scotia andNewfoundland.Special SME programs: Widevariety of SME programsincluding term loans, lines ofcredit, and the governmentguaranteed Small BusinessImprovement Loan of up to$250,000. Contact: Local branches or(604) 641-3072

Lasalle Business Credit, (Division of ABN AMRO)www.lasallebank.comFinancing range & avg.:$5 million and overAvg. finance period:

12 to 180 monthsPreferred SME: Businesses in ITand telecommunications, man-ufacturing,medical/bio-tech-nology/chemical, services,transportation and wholesale/retail industries.Special SME programs:

Revolving credit, term loanfacilities or cash flow facilitiesContact: (416) 367-7949

Laurentian Bank of Canadawww.laurentianbank.caPreferred SME: Quebec-basedbusinessesContact: 1-800-BLC-1846

Société Général (Canada)www.socgen.comPreferred SME: Businesses inthe environment, informationtechnology and telecommuni-cations, manufacturing, min-ing/petroleum/gas, servicesand transportation industries.Special SME programs: ExportfinancingContact: (514) 841-6014

Small Business Financing Assistance Directory

Many banks, trust companies, credit unions and traditional lenders now offer much more than loans. Leasing, factoring, import and export financing and even

venture capital are among the services available. These and other listings can be found in various public sources, including the Internet and in government and trade

association guidebooks. For example, one of the most comprehensive and up-to-date lists of financing options can be found at the Sources of Financing section of

Industry Canada’s Strategis Web site (strategis.ic.gc.ca).

16 The Definitive Guide to Small Business Financing in Canada

RBC_84395 Text 3/14/06 11:01 AM Page 16

The Definitive Guide to Small Business Financing in Canada 17

Commercial Lenders

Typically, funds are investedon behalf of pension fundsand insurance firms and theloans are usually asset-basedin terms of collateral. Alsoincluded in this group are factoring companies.

CIT Group Inc.www.cit.comSpecial SME programs: Shortor long-term loans, leasing,asset management andfinancing, and industry-specificfinance solutions.Contact: Locations in Alberta,Ontario and Nova Scotia.

Execucor Financialwww.execucor.com Preferred SME: No restrictionsSpecial SME programs: Leasefinancing, loans, venture capital, and lines of credit.Contact: 1-888-393-2826

Penfund GroupFinancing range & avg.:$1,000,000 to $7,000,000SME portfolio: $300 millionPreferred SME: Establishedcommercial and industrialbusinesses with the exceptionof real estate and naturalresources sectors.Contact: (416) 865-0300.

Government Sources

In addition to the major programs and organizationslisted here, there are manyother federal, provincial,regional and even municipalprograms geared to serve theneeds of SMEs. Contact your local economic develop-ment authorities for moreinformation.

ATB Financialwww.atb.comFinancing range & avg.: VariesPreferred SME: Alberta-basedbusinesses.Special SME programs: Widevariety of SME programs, capital financing, operating,professional practice and government guaranteed loans,as well as the AlbertaBusinessCard MasterCard witha limit up to $50,000.Contact: Local offices or 1-800-332-8383.

Atlantic CanadaOpportunities Agency(ACOA)www.acoa.caFinancing range & avg.: VariesPreferred SME: All AtlanticCanadian-based SMEs exceptthose in retail/wholesale, realestate, government services orpersonal/social services.Special SME programs: Widerange of SME programs,including the interest-freeBusiness DevelopmentProgram, and the YoungEntrepreneurs ConneXion with loans up to $15,000(ages 18-29 yrs.)Contact: Local offices or (506) 851-2271

Business DevelopmentBank of Canada (BDC)www.bdc.caFinancing range & avg.: Up to$100,000 for start-upsAvg. finance period:

Up to six yearsPreferred SME: Start-ups orwithin first year of sales.Special SME programs: Longterm financing to provideworking capital, fixed assets,marketing/start-up fees or theability to purchase a franchise.Contact: Local branches or 1-877-BDC-BANX.

Ministry of Enterprise,Opportunity & Innovationwww.ontariocanada.comFinancing range & avg.:$3,000 to $15,000Preferred SME: Ontario-basedsummer entrepreneurs and startups.Special SME programs:

Summer Company Programfor students aged 15-29 yrs.My Company Program foryoung people aged 18-29 yrs.Contact: Local Small BusinessEnterprise Centre or BusinessSelf-Help Office.

Saskatchewan Industry and ResourcesFinancing range & avg.: up to$10,000Avg. finance period: Five yearsFees: $30 administration feePreferred SME: SMEs based inSaskatchewan, except those indirect farming, exploration(such as mining and oil extrac-tion), residential real estate,multi-level marketing or chari-table organizations. Farmingoperations eligible for fundingfrom Saskatchewan

Agriculture, Food and RuralRevitalization.Special SME programs:

Small Business LoansAssociation (SBLA) Programfor startup and non-traditionalentrepreneurs. Contact: (306) 787-7154.

Leasing

RBC Royal Bankwww.rbcroyalbank.comRoyal Business Lease™ orRoyal Business Leaseline™ Financing range & avg.:$50,000 and upContact: Local branches/busi-ness centres for applications or1-800-ROYAL®2-0.

ABN Amro LeasingFinancing range & avg.:$50,000 to $5+ million; Avg. finance period: 12 to 72 monthsFees: $400 processing feePreferred SME: Businesses inforestry, construction, manufacturing,mining, petro-leum/gas or transportationindustries.Special SME programs: Leasingand financing construction,materials handling, productionand transportation equipment. Contact: (905) 331-2011

GE Capital CanadaEquipment Financingwww.gecapitalcanada.comFinancing range & avg.:$25,000 to $5+ million; Avg. finance period:

24 to 120 monthsPreferred SME: Businesses inagriculture, construction,forestry, manufacturing, min-ing/petroleum/gas, and whole-sale/retail sectors.Contact: (514) 397-5300

HSBC Canada Leasingwww.hsbc.caFinancing range & avg.:$250,000 to $5+ million; Avg. finance period: 36 to 120monthsPreferred SME: Companies inB.C., Alberta, Saskatchewan,Manitoba, Ontario, Quebec,New Brunswick, Nova Scotiaand Newfoundland.Special SME programs:

Specializes in providing custom tailor lease or financearrangements on the full

range of capital assets.Contact: (604) 641-1990

IBM Canada Ltd.www.can.ibm.comFinancing range & avg.: VariesSpecial SME programs:

SuccessLease* programfinancing up to $100,000;TOTAL Solution Financingincluding Total UsageFinancing.Contact: 1-800-426-2255extension 710.

TD Asset Finance Corp.www.tdcommercial-banking.comFinancing range & avg.:$100,000 to $5 million +Avg. finance period:

36 to 120 monthsPreferred SME: No restrictionsSpecial SME programs: Capitaland operating leases, condi-tional sales contracts and saleand leasebacks.Contact: 1-888-983-8323

Venture Capital

A full listing of active venturecapital corporations can beobtained from the CanadianVenture Capital Association in Toronto.

RBC Capital Partnerswww.rbcap.comFinancing range & avg.:$5 million and upAvg. finance period: VariesPreferred SME: Dependant onapplicable financing product.Special SME programs: Venturecapital and private equityinvestments, mezzanine debt,primarily in the energy, tech-nology, life sciences and telecom industries inNorth America.Contact: (416) 842-4077

RBC Technology Ventures Inc.www.rbcroyalbank.com/rbcvPreferred SME: No start-ups;market-ready companies inselected high growth emerg-ing sectors in North America.Special SME programs: SmallBusiness Venture Fund.Contact: (416) 974-6097

Access Capital Corp.www.accesscapital.comFinancing range & avg.:$500,000 and up.

RBC_84395 Text 3/14/06 11:01 AM Page 17

18 The Definitive Guide to Small Business Financing in Canada

Preferred SME: Informationtechnology and telecommunications.Contact: (416) 366-4820

Accés Capitalwww.accescapital.lacaisse.comFinancing range & avg.:$50,000 to $750,000. Preferred SME: Specializing inQuebec and New Brunswick-based start-ups, excluding real estate.Contact: (514) 847-2611

ACF Equity Atlantic Inc.www.acf.caFinancing range & avg.:$100,000 to $5 millionSME portfolio: $30 millionPreferred SME: Market-readycompanies in Atlantic Canadawith strong managementteam and products with aunique, competitive sustain-able advantage, excluding realestate and retail.Special SME programs: Workwith various chartered banks,credit unions, regional andfederal governments to securequasi-capital and venture capital funding.Contact: Toll-free in AtlanticCanada 1-800-251-5331;(902) 492-5164

Acorn Ventures Inc.www.acorn-ventures.comFinancing range & avg.:$250,000 to $5 millionSME portfolio: $70 millionPreferred SME: Specializing ininformation technology andtelecommunications; excludingreal estate, mining, logging and fishing.Contact: (650) 994-7801

BMO Capital Corporationwww.bmo.com/bmoccFinancing range & avg.:Up to $5,000,000SME portfolio: $200 millionPreferred SME: All sectors areeligible excluding real estate.Special SME programs: BMOSmall Business CapitalProgram, BMO TechnologyInvestment Program, andBMO Early Stages CapitalProgram for youth startups.Contact: (416) 867-7247

BCE Capital Inc.www.bcecaptial.com Financing range & avg.:$500,000 to over $5 million SME portfolio: $150 millionPreferred SME: Information

technology and telecommunications.Contact: (416) 815-0920

Business DevelopmentBank of Canada (BDC)www.bdc.caFinancing range & avg.:$250,000 to $5 millionSME portfolio: $360 millionPreferred SME: All sectors areeligible excluding hotels,restaurants, night clubs, realestate, insurance and financialinstitutions.Contact: (514) 283-8059

Capital Alliance Ventures Inc.www.cavi.comFinancing range & avg.:$500,000 to over $5 millionSME portfolio: $90 millionPreferred SME: Ontario businesses in environment,information technology,telecommunications,and med-ical/ biotechnology/chemical sectors.Contact: 1-800-304-2330.

DGC EntertainmentVentures Corp.Financing range & avg.:$100,000 to $750,000Preferred SME: Canadianentertainment and communi-cations companies.Special SME programs:Expansion, capital asset, andproject financing; debt orequity refinancing.Contact: (416) 483-9637

Deventis Capitalwww.devantiscapital.com Financing range & avg.:$1 to $2 millionPreferred SME: Provide equitycapital and business development to emergingcompanies in WesternCanada, excluding start-ups,resources, real estate, retail,biotech or manufacturing.

Ensis Growth Fundwww.ensisgrowthfund.comFinancing range & avg.:$250,000 to $5 millionAvg. finance period:120 monthsPreferred SME: Manitoba busi-ness in agriculture, environment, informationtechnology and communica-tions, manufacturing, services and tourism. Contact: (204) 949-3700

Fonds de Solidarité desTravailleurs du Québec/ TheSolidarity Fund QFLwww.fondsftq.comSME portfolio: $4.4 billionPreferred SME: Quebec-based SMEs.Special SME programs:Assistance for startups, expan-sions, IPO, consolidations,mergers, acquisitions andexports.Contact: 1-800-361-5017.

Fulcrum Partnerswww.fulcrumpartners.comFinancing range & avg.:Up to $750,000Preferred SME: GreaterToronto Area-based compa-nies with annual growth ratesof over 30 per cent, specializ-ing in consumer products, ITand telecommunications.Contact: (416) 240-5000

Investments Novacap Inc.www.novacap-inc.comFinancing range & avg.:$1 million to over $5 millionAvg. finance period:60 to 120 monthsSME portfolio: $73 millionPreferred SME: Businesses inOntario, Quebec and NewBrunswick specializing in environment, informationtechnology and telecommuni-cations, manufacturing, andmedical/biotechnology/chemi-cal sectors; excluding realestate, mining and other “primary industries”.Special SME programs: Quasi-equity and venture capital.Contact: (450) 651-5000

J.L. Albright VenturePartners Inc.www.jlaventures.comFinancing range & avg.:$1 to $5 millionAvg. finance period: 2-4 yrs.SME portfolio: $170 millionPreferred SME: GreaterToronto Area-based businessesin consumer products, infor-mation technology andtelecommunications. Excludingreal estate, mining, and oiland gas.Contact: (416) 367-2440.

McLean Watson Capital Inc.www.mcleanwatson.comFinancing range & avg.:$500,000 - $5 million; Avg. finance period:24 to 60 months

SME portfolio: $160 millionPreferred SME: Software andinformation technology and telecommunications companies.Special SME programs:McLean Watson SOFTECHFund, focusing on softwarecompanies, and McLeanWatson Ventures II, focusingon information technology.Contact: (416) 363-2000

MDS Capitalwww.mdscapital.comFinancing range & avg.:$250,000 to over $5 millionAvg. finance period:24 to 120 monthsPreferred SME: Medical,biotechnology and chemicalsectors only.Contact: (416) 675-4530

Quorum FundingCorporationwww.quorum.caFinancing range & avg.:$1 million-$5 million; Avg. finance period:36-60 monthsSME portfolio: $150 millionPreferred SME: Companies ininformation technology andtelecommunications sectors,excluding startups or earlystage businesses except inexceptional circumstances.Special SME programs:Venture capital, mezzanineand other financing.Contact: (416) 971-6998.

TD Capitalwww.tdcapital.comFinancing range & avg.:$1 to $5 million +Avg. finance period:36-84 monthsFees: Program-dependentSME portfolio: $3 billionPreferred SME: growth-orient-ed middle-market companiesrequiring financing for a widerange of circumstances includ-ing buyouts, growth andexpansion, acquisitions andrecapitalizationsSpecial SME programs:Mezzanine Partners, CanadianPrivate Equity Partners, PrivateEquity Investors, TechnologyVenturesContact: (416) 308-3230

RBC_84395 Text 3/14/06 11:01 AM Page 18

® Registered trademark of Royal Bank of Canada ™Trademark of Royal Bank of Canada. RBC and Royal Bank are registered trademarks of Royal Bank of Canada. This site is owned and operated by General Content Corporation. Royal Bank of Canada receives no compensation from General Content Corporation, the course providers or their agents.

Learn online from your own homeor office, at your own speed andschedule. With valuable info on mar-keting fundamentals. Sales and sellingstrategies. Customer service.Marketing on the Internet and more.

It’s e-learning sponsored by RBCRoyal Bank® and it’s everything today’sbusiness owner or manager needs tosharpen their skills and get an edge inthe marketplace.

Many of these courses are beingmade available to individual business-people for the first time. They include:

• Writing a Marketing Plan• Guerilla Marketing• Marketing Your Business on

the Internet• Promote Yourself!• Opening Closed Doors Sales

Strategies

Use the Definitive Guides to help getyou started with valuable advice on building your business. Then check out our e-learning site atwww.definitiveguidelearning.com.

You’ll find our complete catalogueof online courses that go beyond thebasics to expand your business skills inkey areas – now available at 10-30%off normal registration fees.

Get online and get what you need to succeed. Definitive Guide e-learning.

Enhance Your Most Valuable Asset.

Knowledge you can use to help build your businessDefinitive Guide e-Learning Courses

Your Mind.

Sponsored by

RBC_84395 Text 3/14/06 11:01 AM Page 19

Many entrepreneurs aren’t aware of the many government-related financing and support programs for SMEs. Here are a few:

20 The Definitive Guide to Small Business Financing in Canada

Technocap Inc.www.technocap.comFinancing range & avg.:$500,000-$750,000Avg. finance period:60 months minimumSME portfolio: $100 millionPreferred SME: Companies inAlberta, Ontario, Quebec,New Brunswick and NovaScotia specializing in information technology andcommunications.Contact: (514) 483-6000

Vengrowth Fundswww.vengrowth.comFinancing range & avg.:$750,000 to $5+ million; Avg. $3 millionAvg. finance period:48 to 72 monthsSME portfolio: $450 millionPreferred SME: Ontario-basedestablished business in theenvironment, informationtechnology and telecommuni-cations, manufacturing, med-ical/biotechnology/chemical,services, tourism and whole-sale/retail sectors. Mining andreal estate are excluded.Contact: (416) 971-6656

Ventures WestManagement Inc.www.ventureswest.comFinancing range & avg.:$500,000-$5+ millionAvg. finance period:36 to 60 monthsSME portfolio: $400 millionPreferred SME: Companies inthe information technologyand telecommunications,medical/biotechnology/chemi-cal sectors, excluding realestate, natural resources andnon-technology.Contact: (604) 688-9495

Working VenturesCanadian Fund Inc.www.workingventures.caFinancing range & avg.:$500,000-$5+ millionAvg. finance period:48 to 84 monthsSME portfolio: $700 millionPreferred SME: Companies inSaskatchewan, Ontario, NewBrunswick, Nova Scotia andPrince Edward Island, exclud-ing real estate.Contact: (416) 934-7777

Government SME Finance Options

Canada Small Business Financing

If you’re running a for-profit business that’s not a farm or a religiousinstitution, and your annual gross revenues are less than $5 million, youmay qualify for a government-guaranteed loan from a financial institution.The Small Business Loans Act permits authorized lenders to finance up to90 per cent of expenses used to:

• purchase, install, renovate, improve or modernize new or used equipment (e.g. computers, computer software for operational purposes,manufacturing equipment, etc.);

• purchase land to operate the business; and• renovate, improve, modernize, extend, construct or purchase business

premises necessary for the operation of the business.

Eligible purchases made within the past six months can be financedwith this loan, and loans are advanced only upon receipt of eligible invoic-es. The most you can access using this program is $250,000, repaid over amaximum of 10 years.

Pricing of these loans is competitive, but the government charges a2 per cent registration fee at the beginning (usually added to the principalamount of the loan) as well as a 1.25 per cent administration fee withevery payment. These fees are used to help keep the program running.

If the business fails, the Federal government will share up to 85 percent of the loan losses with the lender. Note that personal guarantees forunsecured loans are limited to a maximum of 25 per cent of principalamount under this program.

Business Development Bank of Canada

Business Development Bank of Canada (BDC) is becoming a majorplayer in financing and refinancing SMEs, often working in partnershipwith other financial institutions. As well, BDC offers consulting, trainingand other services such as ISO 9000 certifications.

Over the past few years, BDC has become less program-oriented,and now deals more with the individual needs of entrepreneurs. BDC alsooffers start-up financing that provides term financing up to $100,000 andthe possibility of personalized management support.

BDC Venture Capital is also a major venture capital investor inCanada, active at every stage of a company's development cycle, fromstart-up through expansion. Its focus is on technology-based businesseswith high growth potential that are positioned to become dominant players in their markets.

BDC Technology Seed Investments Group provides financing for thecreation of innovative technology businesses with high-growth potential.BDC’s financing is often paired with other financial, management, or com-mercial development resources.

Other Programs

The Ottawa-based Export Development Corporation plays a uniquerole for SMEs. EDC insures foreign receivables, provides security to anexporter’s bank for any line of credit, and can even offer financing to aforeign buyer of Canadian exported products.

Microcredit funds are designed for entrepreneurs who do not haveaccess to bank credit. The purpose of these loans, which are under$25,000, is to finance the start-up of very small businesses (less than five employees and gross revenues under $500,000). The funds are managed by local economic development centres that assign security to private lending institutions. These funds often support community pro-jects that promote employment for specific groups, such as minorities andthe disabled.

Among the many regional federal government financing programs,the Atlantic Canada Opportunities Agency (ACOA) is a success story initself, providing interest-free, unsecured repayable contributions to SMEs.ACOA also operates the Young Entrepreneurs ConneXion Program thatprovides unsecured, personal loans of up to $15,000 to young entrepre-neurs between the ages of 18 and 29. Funds can be used for businessstart-up or expansion, and up to $2,000 for business counselling andtraining costs.

In Northern Ontario, The Federal Economic Development Initiative forNorthern Ontario (FedNor) supports local investment funds for the start-up, expansion, and/or stabilization of local businesses. These funds areoperated by Community Futures Development Corporations (CFDCs) thatuse volunteer boards and professionals with business experience to assessapplications for financing. CFDC investments are provided where financingavailable from personal investment, financial institutions and other sourcesis insufficient. Funds, normally up to $125,000 maximum, can be allocatedas loans, loan guarantees or share capital equity.

Western Economic Diversification Canada offers a wide range offinancing programs in partnership with financial institutions to help select-ed western industries. WD, as it is known, focuses on knowledge andgrowth businesses, information technology and telecommunications, andagriculture value-added processing, as well as small and medium-sizedB.C. companies in traditional industries.

RBC_84395 Text 3/14/06 11:01 AM Page 20

toMarket

toMarketEquity investment can be another option. While risk

capital doesn’t appear to be flowing as freely as it dida few years ago, sources such as angels and venturecapitalists still know a good deal when they see one.

Debt isn’t the only answer.

The Definitive Guide to Small Business Financing in Canada 21

RBC_84395 Text 3/14/06 11:01 AM Page 21

While most Canadian SMEs still pursueexternal financing in the form of debt, fewbusinesses can be financed by debt alone.Most businesses need a foundation of equity investment, obtained from theowner’s personal funds, re-invested earn-ings, or risk capital investments made byoutside parties who become partners in anownership group.

Risk capital financing can be partic-ularly important for businesses in theknowledge-based industries (KBIs). Thesecompanies can have high cash require-ments for research and development,deferred earnings and few tangible assetsto represent security for debt financing.Often, high-growth SMEs soon outstriptheir self-financing options, and need helpfrom outside risk capital investors.

ANGELS ARE INVISIBLE

For those entrepreneurs willing toaccept a partner for the sake of growth,the first source to tap is usually an informalinvestor, also known as an angel. These areindividuals who make relatively small invest-ments in private companies with highgrowth prospects.

Information about angel investing isscarce because they operate privately andindependently. Estimates suggest thatangels in Canada invest between $1 billionand $20 billion each year, with 60 per cent

of this amount targeted at SMEs in theearly stages of growth. In the U.S., angelshave been identified as the single mostimportant source of risk capital for SMEs.

Where do angels come from? OneIndustry Canada study, Practices andPatterns of Informal Investment, found thatangels are well-educated and report consid-erable experience as investors. They tend tohold other full-time jobs, limiting the timethey can devote to their direct investments.Another survey found that 18 per cent ofbusiness owners have invested privately inother companies. High-earning profession-als such as doctors, dentists, lawyers andaccountants have traditionally invested ingrowing businesses as well.

In their book Beyond theBanks...Creative Financing for CanadianSmall Business Owners, authors Allan L.Riding and Barbara J. Orser suggest the fol-lowing ways to help you find and workwith angels:

Study your own local networks Meet asmany angel investors as possible in yourneighbourhood and get all the referrals you can.

Customize your pitch Learn about theinvestor before you approach him or her,then personalize the business plan toemphasize how your business opportunityreflects the investor’s goals.

Stress the creative elements of your project Angels want to build and cre-ate. Show the angel exciting and uniqueelements of the opportunity you offer.

Emphasize your competence as a man-ager and your integrity Angels usuallyreject 39 out of 40 opportunities, mostlybecause they lack confidence in the man-agement. In the business plan, stress yourtrack record, ability, and the honesty ofyour management team. Be honest aboutyour weaknesses.

Target lead investors Most angels preferto invest in groups. Every investor commu-nity has respected “archangels” who mar-shal informal capital by establishingsyndicates of other investors. Find out whothey are.

Get in to meet potential investorsAngels usually reject 75 per cent of opportunities before even meeting the prin-cipals. If you can get the investor’s personalattention, chances of making a dealincrease dramatically.

Be prepared to give up something toget something While most angels are notinterested in taking control of your compa-ny, they will have concrete requirements inmany areas. Since they bring a wealth ofexperience and commitment to the busi-

22 The Definitive Guide to Small Business Financing in Canada

RBC_84395 Text 3/14/06 11:01 AM Page 22

ness, it may be advisable to heed whatthey say.

Be persistent If an angel rejects your pro-ject, press for referrals to other angels andsympathetic business associates.

Angels typically invest at the earlystages of growth—either at start-up orseed stage—and approve only about 12per cent of proposals they see. What’s theleading cause of rejection? The SME is not“investor-ready” because of undevelopedknowledge or an unwillingness to share control.

THE VENTURE CAPITALADVENTURE

Some firms quickly outgrow the abili-ty of angels to provide growth capital, andmove on to the next stage in risk capitalfinancing—venture capital. You will findtwo kinds of equity providers in theCanadian market: venture capital compa-nies that typically provide capital to tech-nology-related companies at early stages,

and private equity companies that provideequity for growth for a wider variety ofbusinesses that are not necessarily technol-ogy-driven. In spite of adverse economicconditions and volatile public markets, theCanadian venture capital industry had thesecond-best year in its history in 2001 withdisbursements totaling $4.9 billion. Thisrepresents a drop of 27 per cent from theprevious year, but contrasts sharply withventure capital in the U.S., which plum-meted 65 per cent in the same period.

It should be noted that only a verysmall minority of Canadian SMEs use ven-ture capital. Out of Canada’s approximatelytwo million business establishments, only818 received venture capital financing in2001. Another source suggests thatbetween 2.5 per cent and 3 per cent ofCanadian SMEs use venture capital financ-ing, and these SMEs have annual sales ofat least $5 million.

Neuro Therapeutics Inc. typifies thekind of company that attracts venture capi-tal. NTI has developed a promising func-tional repair process for treating spinal cordinjuries. There are over 500,000 chronicspinal cord injury survivors in North

America, with 11,000 new injuries occur-ring each year. There are no therapies thatare currently available to reverse paralysis inspinal cord-injured individuals.

Milestone Medica, founded in 1998by RBC Technology Ventures Inc. andResearch Corporation Technologies (RCT),partnered with University MedicalDiscoveries Inc. to provide seed financingto NTI. As a result, NTI obtained an exclu-sive worldwide license to the lead technol-ogy from the University of British Columbiaand has obtained a Canadian patent.Worldwide patents are pending, includingsecond-generation compositions. With thesupport of Milestone Medica’s network,NTI entered into a joint venture withMedarex Inc. to develop and finance thelead therapeutic application required forboth the pre-clinical and clinical phases.“This partnership is pivotal, in that it pro-vides a commercially viable and clear pathforward for the development of NTI’s leadtechnology,” says Dr. John Steeves,President and CEO of NTI.

“Every day we hear about new andexciting medical research discoveries,” saysMilestone Medica CEO Dr. David Shindler.“Obviously, discovery is an importantbeginning, but to be successful in develop-ing new medical products takes a lot ofplanning and management. To take a newdrug from the beginning of R&D toapproval, and then to market availability,could require over $300 million. In addition

Out of Canada’s approximately two million business establishments, only 818 received venture

capital financing in 2001.

The Definitive Guide to Small Business Financing in Canada 23

RBC_84395 Text 3/14/06 11:01 AM Page 23

to providing the seed financing to put sig-nificant medical discoveries on a commer-cial development track, Milestone Medicadedicates considerable managementresources to ensure success.”

Over the last few years, venture capitalhas developed into the near-exclusive pre-serve of high-tech companies. However,according to the fourth Canadian VentureCapital Confidence Survey from Deloitte &Touche and the Canadian Venture CapitalAssociation (CVCA), weak markets are forc-ing venture capitalists to consider investingin traditional industries such as manufactur-ing. Almost two-thirds of firms surveyed in

the third quarter of 2002 would considerold-economy venture capital investments,compared to less than half in the previousquarter. This development may represent aglimmer of good news for SMEs that oper-ate traditional businesses, but the surveyalso suggests that the majority of VCs arefocussing more on managing their currentportfolios, as opposed to seeking out new investments.

Within the ailing tech sector, the sur-vey emphasized a shift away from informa-tion technology over to biotechnologyinvestments. Biotech and Medical remainthe most positively viewed investment sec-tors with 61 per cent and 57 per cent ofrespondents, respectively, expecting thenumber of transactions to increase. Theoutlook for the technology sector is lessfavourable; the majority of respondents

anticipate a decline in investment activityacross the technology spectrum. Half of VCrespondents believe investments in commu-nications and Internet will decrease in theshort-term.

Readers should note that venture capitalists often insist on providing manage-ment input with their investment. This inputusually takes the form of a seat or seats onyour board of directors, at the very least.Realistically, their experience and knowl-edge is almost always helpful—and some-times essential. However, entrepreneursmust decide how much management con-trol they are willing to share.

That being said, some common mythsexist about VC deals. Many entrepreneursbelieve VCs are in for a quick buck and sig-nificant control. It is true VCs expect a lot,from 20 per cent to as much as 60 per centin annual compounded return on a dollar.Usually, though, that’s not due until the VCexits via a buyout or an IPO—an event thatalso benefits the original owners.

As for the quick payback, it doesn’thappen often. The average VC holds aninvestment for three to eight years. And,the average VC has just 32 per cent of theequity, according to an industry survey.

While they seem to (and do) haveaccess to a lot of money, VCs are a cautiousgroup, preferring businesses with hotprospects and clear potential for a big pay-out when the business goes public or issold. In dollar terms, that means a business

capable of hitting $30-$50 million in saleswithin five years.

What VCs Really, Really Want

So, you’ve got a sense of what VCsand other risk capital investors want and you think you can dazzle them withyour opportunity. What’s in a VC-friendlyplan? Like any potential investor, VCs areimpressed by clarity of thought and profes-sionalism. The plan has to be concise andeasy to read, from its executive summarythrough to a glossary of any technicalterms. Few venture capital or private equityfirms will meet with you prior to reviewingat least a summary of your business plan.

In between those pages, the VCs needevidence of a realistic growth path in sales,earnings, assets and cash flow. Wildly stat-ed revenue forecasts or underestimates ofcosts will set off alarms. The plan shoulddescribe the company’s history, current sta-tus and prospects, as well as weaknesses.Strong candidates for equity investmentalso have a national or even global market-ing strategy.

On the financial and marketing sides,don’t try to get away with a one–or even athree-year plan. Since most VCs have along-term exit strategy, they’ll want toknow where you’re headed over the nextfive to eight years. Some signs you’re on agrowth path could be that you’ve got somebig contracts signed, major deals locked ornew products in the wings. This also sug-gests the VC needs to act quickly.

Most important is to show you have astrong management team. What makes fora strong team? Usually it means successfulexperience—owners and executives who have already made money for them-

Most VCs have a long-term exit strategy, they’ll want to know where you’re headed over the