Embed Size (px)

Citation preview

SMALL DOLLAR LOAN

ONLINE CONFERENCE

HOUSEKEEPING

Please Mute Your Microphone and Turn Your Video Off

SMALL DOLLAR LOAN

ONLINE CONFERENCE

THIS PRESENTATION

FloridaProsperityPartnership.org/PRESENTATIONS

OUR FUNDERS

& YOU

NEITHER FLORIDA PROSPERITY PARTNERSHIP NOR UNIVERSITY OF FLORIDA IFAS NECESSARILY

ENDORSE ANY OF THE PRODUCTS THAT WILL BE PRESENTED TODAY,

BUT ARE PRESENTED TO YOU FOR INFORMATIONAL PURPOSES.

WE ENCOURAGE EACH OF YOU TO LEARN MORE ABOUT THEM AND OTHERS IN YOUR AREA ,

PRIOR TO USE OR REFERRAL.

HOUSEKEEPING

Please Mute Your Microphone and Turn Your Video Off

SETTING THE STAGE

What type of loans are non-bank lenders selling in Florida

Presented by Alice Vickers, Director Florida Alliance for Consumer Protection

What is a non bank “small dollar loan”

• Non-bank lenders are lenders other than banks and credit unions offering products to consumers

• Under Florida law, we have three products that non-bank lenders are able to sell if properly licensed to sell.*

*excluding pawn loans

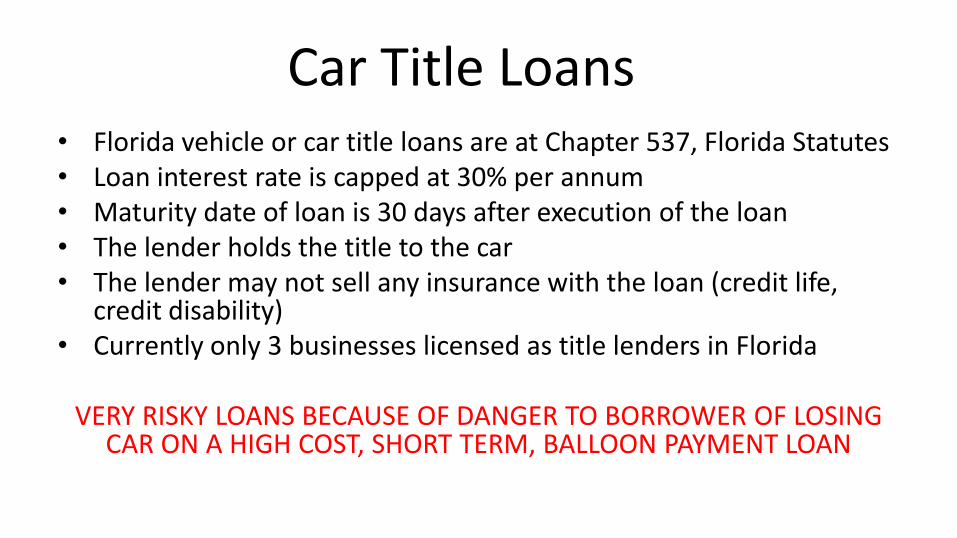

Car Title Loans • Florida vehicle or car title loans are at Chapter 537, Florida Statutes • Loan interest rate is capped at 30% per annum • Maturity date of loan is 30 days after execution of the loan • The lender holds the title to the car • The lender may not sell any insurance with the loan (credit life,

credit disability) • Currently only 3 businesses licensed as title lenders in Florida

VERY RISKY LOANS BECAUSE OF DANGER TO BORROWER OF LOSING

CAR ON A HIGH COST, SHORT TERM, BALLOON PAYMENT LOAN

Pay Day Loans • Florida Deferred Presentment loans or payday

loans are at Part IV, Chapter 560, Florida Statutes • Cost for loans is 10% of loan amount (and a $5

fee per loan) or an annual percentage rate between 280% and 500%

• Loans may be up to $500 • Loans must be paid in a lump sum between 7

days and 31 days of execution of the loan

Pay Day Loans continued • It most cases, lender has authorization to reach into borrowers

bank account for repayment • There are approximately 1100 licensees in Florida selling payday

loans (compare with McDonalds which has 868 Florida locations) • Loans closed in minutes with no determination if the borrower can

repay the loan • Loans do not build credit history for borrower VERY RISKY LOANS BECAUSE OF THE TRIPLE DIGIT APR, NO ABILITY TO REPAY DETERMINATION, LUMPSUM REPAYMENT BY ACH TRANSFER

Installment Loans

• Florida Consumer Finance Loans or installment loans are at Chapter 516, Florida Statutes

• Loans are capped at 30% per annum and may not exceed $25,000; tiers:

30% on first $3000; 24% on $3000 to $4000; 18% on amounts over $4000

Installment Loans continued • Loans must repaid in equal monthly installments

(OFR has determined that a single installment meets the requirements of the law)

• Lenders may sell insurance with the loans (credit life, credit disability, etc.)

• Industry says average loan is $3000; consumers use these loans to purchase cars, mobile homes but also as unsecured loans

Installment Loans continued

• Industry reports that proprietary underwriting requirements are used and credit reporting

• There are approximately 322 licensees in Florida

HIGH TO MODERATE RISK LOANS DEPENDING ON LENDER UNDERWRITING, TERM OF LOAN, AND

SALES OF ANCILLARY PRODUCTS WITH LOAN

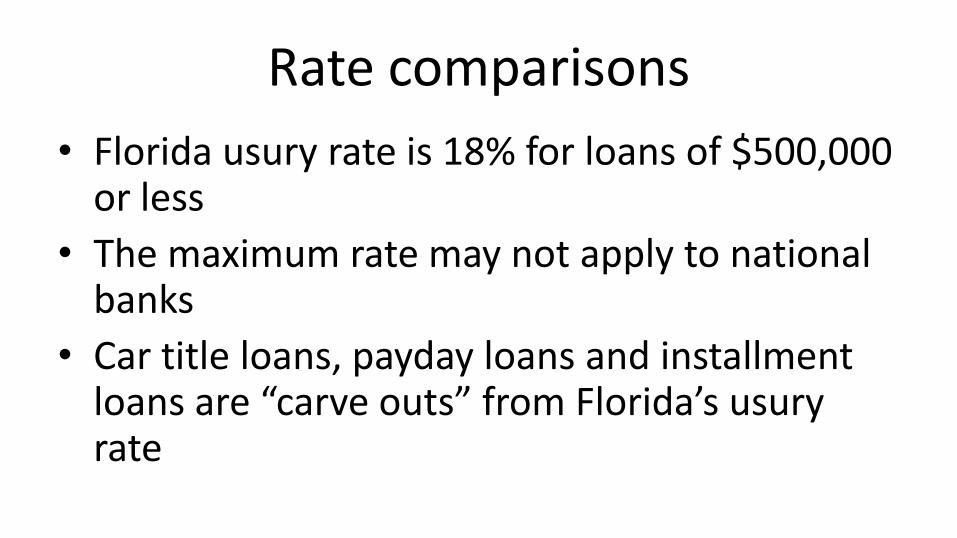

Rate comparisons

• Florida usury rate is 18% for loans of $500,000 or less

• The maximum rate may not apply to national banks

• Car title loans, payday loans and installment loans are “carve outs” from Florida’s usury rate

2017 Florida Legislative Session

• We anticipate that the Florida Legislature may see legislation to address the rate of payday loans

• It is also anticipated that the Florida Legislature may see legislation to create a new small dollar loan lending product

Questions and Contact Alice Vickers

Florida Alliance for Consumer Protection [email protected]

www.flacp.org www.stopthedebttrapflorida.org

FDIC’S SMALL-DOLLAR LOAN PILOT PROGRAM

Presented by: April A. Atkins Community Affairs Specialist

20

The purpose of this presentation is for informational purposes only.

The Federal Deposit Insurance Corporation’s participation with this online conference is not an endorsement of the organizations or presenters listed on the agenda.

21

April A. Atkins, AICP Community Affairs Specialist

Federal Deposit Insurance Corporation [email protected]

LENDING CIRCLES

AGENDA

• Introductions

• Catalyst Miami and Mission Asset Fund

• What are Lending Circles and How do they Work

• Lending Circles Program Process

• Lending Circles Important Information

• Lending Circles in Miami

• Questions

INTRODUCTION

WHAT ARE INFORMAL LENDING CIRCLES

mabati

kutu

It’s a global practice

People come

together

To lend and borrow

money to each other

Lending Circle Basics

LENDING CIRCLES

BENEFITS OF LENDING CIRCLES

Access a 0% interest social loan

Establish and build your credit

Increase your financial knowledge

Know your money is safe

Meet new people, and save together

READY TO APPLY

FOR DEFERRED

ACTION BUT DON’T

HAVE

$465?

READY TO APPLY

FOR CITIZENSHIP

BUT DON’T HAVE

$680?

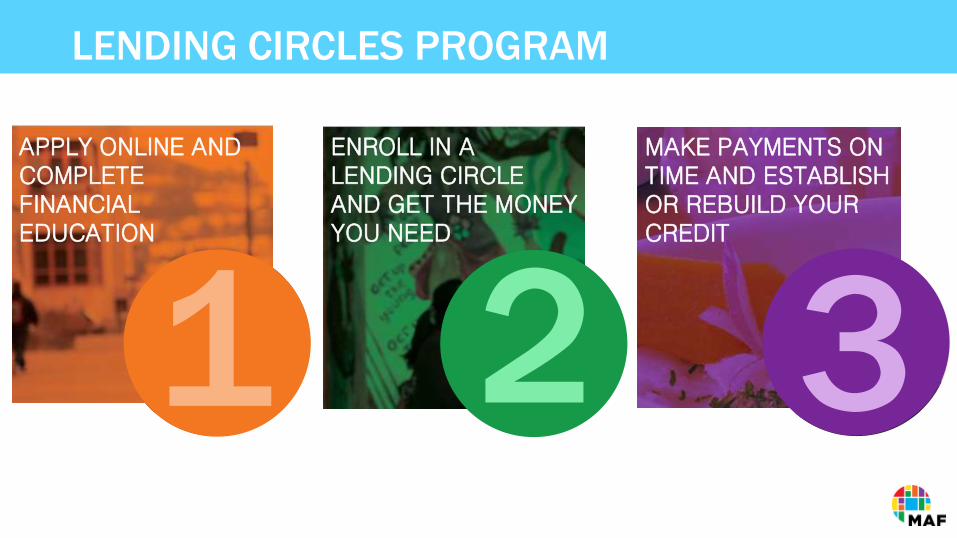

LENDING CIRCLES PROGRAM

WANT TO IMPROVE

YOUR CREDIT?

1 2 3

APPLY ONLINE AND COMPLETE FINANCIAL EDUCATION

ENROLL IN A LENDING CIRCLE AND GET THE MONEY YOU NEED

MAKE PAYMENTS ON TIME AND ESTABLISH OR REBUILD YOUR CREDIT

ENROLLMENT

• Clients must complete the application for the Lending Circles at LendingCircles.org

APPLICATION

• 90 minute online class or in-house presentation

FINANCIAL

EDUCATION • You must have completed the

application, promissory note, and survey to join the Lending Circles program

SURVEY

• A personal email account is required EMAIL

PROGRAM REQUIREMENTS

• Clients will need to have a checking account in their name

CHECKING ACCOUNT

• Clients will need to have valid Email address

• Clients must provide a valid state ID/ Drivers license or government issued ID information (does not have to be a US doc)

• Clients must have Social Security Number or Tax ID Number

ID

• Clients must be over 18 years old AGE • Must have steady household income (wages,

self-employment, public benefits, etc.), and be able to afford the monthly contribution amount

INCOME

PAYMENTS

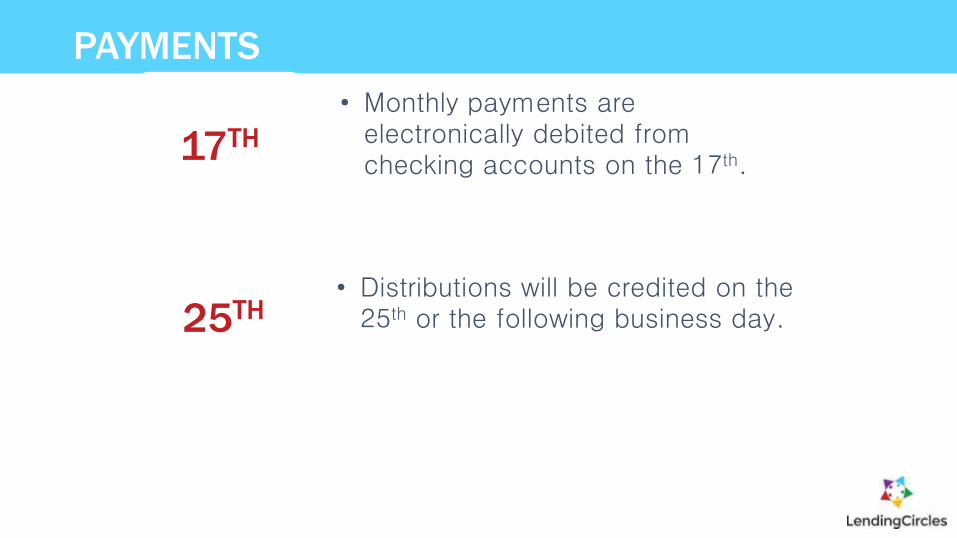

• Monthly payments are electronically debited from checking accounts on the 17th.

17TH

• Distributions will be credited on the 25th or the following business day.

25TH

MY CREDIT REPORT

Lending Circles in Miami

• Just under 100 clients enrolled in Lending Circles in two years

• Average credit score increase is ~160 points

• Engage with MAF via the LC Communities Portal

• 65% of Lending Circles clients receive Financial Coaching

Bring Lending Circles to your Community

• Visit lendingcircles.org/partners

Q&A

STAY IN TOUCH

DARREN LIDDELL SR. DIRECTOR OF COMMUNITY WEALTH

Email: [email protected]

Phone: (786) 527-2570

Office: 3000 Biscayne Blvd, Suite 210 Miami, Florida 33137

Independence is Priceless We make it Affordable

Who is FAAST?

Florida Alliance for Assistive Services and Technology

• FAAST, Inc. is a 501 (c)(3) not-for-profit organization as of October 20, 1994, funded by the U.S. Department of Health and Human Services (HHS) through the Assistive Technology Act of 2004 and through Florida General Revenue funds under §413.407, F.S. FAAST, Inc. is sponsored by the Florida Department of Education, Division of Vocational Rehabilitation

FAAST Mission

• Our Mission is to improve the quality of life for all Floridians with disabilities through advocacy and awareness activities that increase access to and acquisition of assistive services and technology.

How do we succeed at our mission:

• Six Regional Demonstration Centers: Pensacola, Tallahassee, Jacksonville, Orlando, Tampa, Miami

• Five Regional ReUse Centers: Pensacola, Tampa, Ft. Myers, Miami, Ft. Lauderdale

• Statewide Device Borrowing Program Consumers and Educators may borrow AT at no cost for 30 days to determine if the device or technology is the right fit

• New Horizon Loan Program

What is the New Horizon Loan Program? • The New Horizon Loan Program is a preferred-interest loan program

of the Florida Alliance for Assistive Services and Technology, Inc. (FAAST).

• The New Horizon Loan Program is enabled through the Assistive Technology Act of 2004, originally funded by the Rehabilitation Services Administration.

• The program offers Floridians with disabilities credit opportunities while purchasing equipment and items and associated services that will improve their overall quality of life.

• The New Horizon Loan Program offers Assistive Technology Loan and Small Business or Telework Loan Programs.

• The New Horizon Loan Program offers funding through a Direct Loan Program.

History of the NHLP

Timeline

• 2002 – FAAST entered into its first contract for a lending program.

• Over $1,600,000 has been borrowed by over 125 consumers

• Began operating as a Direct Lender in 04/2015

• Will expand program to once again include a bank guarantee program in 2017

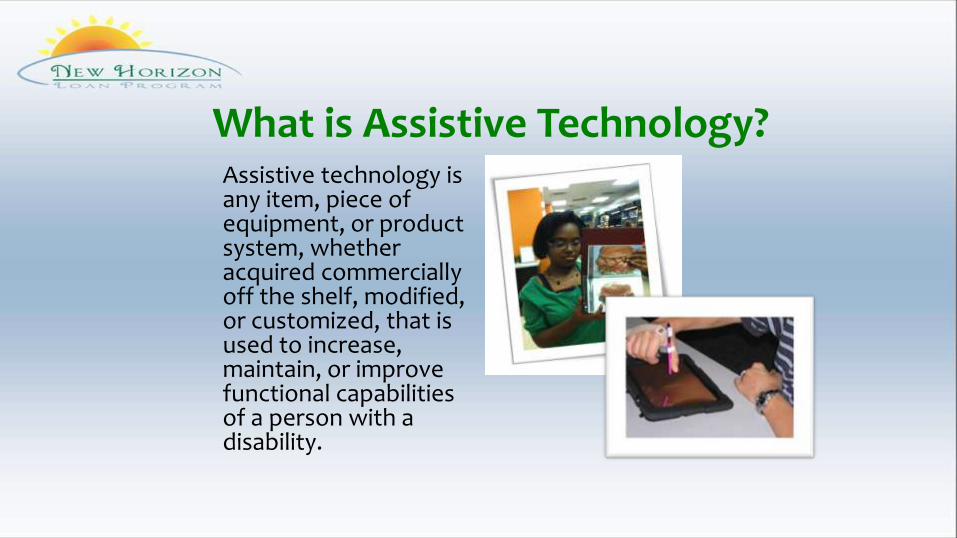

What is Assistive Technology? Assistive technology is any item, piece of equipment, or product system, whether acquired commercially off the shelf, modified, or customized, that is used to increase, maintain, or improve functional capabilities of a person with a disability.

What are some examples of AT? • Hearing Aids • Low Vision Aids • Home Modifications/Environmental Controls • Communication Devices • Adapted Computers • Modified/Accessible, Vehicles • Mobility devices and equipment • Recreational Equipment

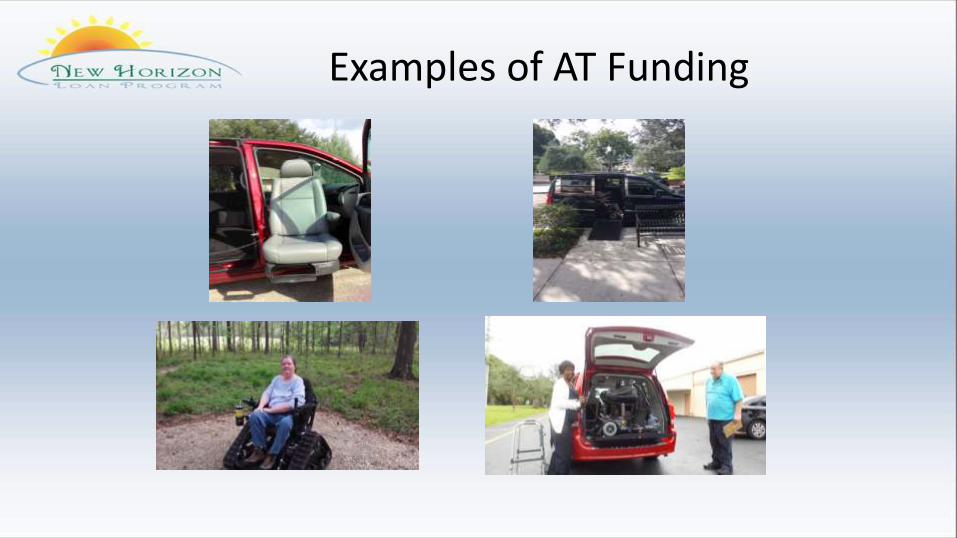

Alternative Financing Program (AFP) What can be financed?

– All types of AT can be financed under the FAAST AFP (vehicle modifications are limited to the modifications only, not the vehicle purchase at this time)

– AT services may also be financed to include trainings, fittings, leases, installations.

– FAAST has financed multiple categories of AT including: home modifications, vehicle modifications, home lift systems, hearing and vision aids, daily living, scooters and power mobility.

New Horizon Business Loan Telework Loan

• Equipment to be used at work place or from home (your telework office)

• Vehicle or mobility necessary to get to and from the work place

• VR invaluable source

Entrepreneur Loan

• Equipment to be used at home for your own business

• Vehicle or mobility to meet clients, conduct business

• Business plan required

• VR invaluable source

Examples of AT Funding

Loan Program Details

• Loan Amounts up to $25,000

• No Income Requirements

• Target minimum credit score – 600

• Target maximum DTI – 50%

• Current Interest Rate -5.50% (subject to change)

• Terms from 6 – 60 months

• Secured and Unsecured loans

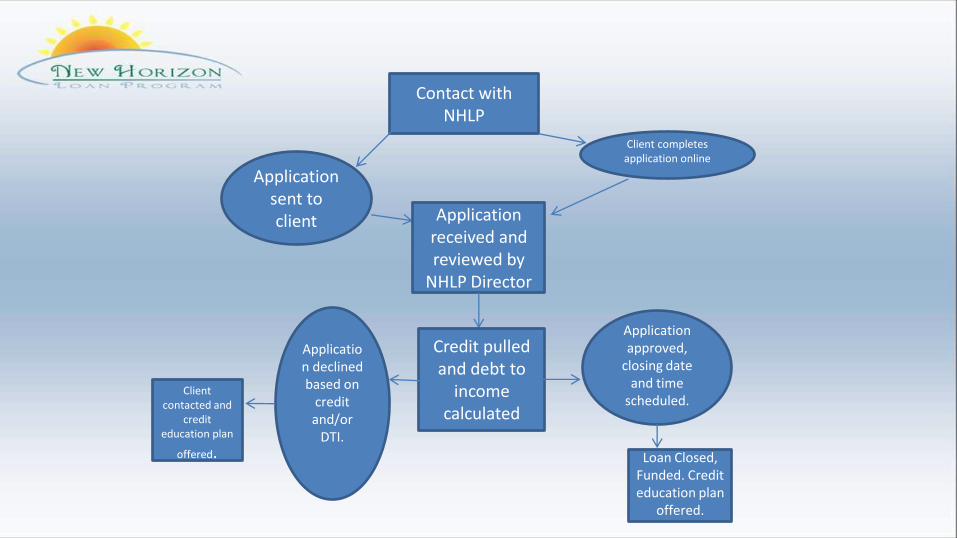

Application to Decision

How does the process work?

Contact with NHLP

Application

sent to client

Client completes

application online

Application received and reviewed by

NHLP Director

Credit pulled and debt to

income calculated

Application declined based on

credit and/or

DTI.

Client contacted and

credit education plan

offered.

Application approved,

closing date and time

scheduled.

Loan Closed, Funded. Credit education plan

offered.

Direct Loan Program Results

• First Loan – May 2015

• Forty loans approved as of 12/31/2016

• Average loan funding - $4642. Smallest loan - $100; largest loan - $20,355

• Total amount approved - $211,194 Total amount funded - $176,400

• 19 Counties served

Credit Education

• Expanding credit education in 2017

• Goal is Financial Wellness for individuals with disabilities

• Partnering with CIL’s across the state

• Look for upcoming training in your area

Bank Partnership

• Seeking bank for vehicle purchase partnership

• Guarantee loan program – FAAST provides 100% guarantee for each loan

• Allows FAAST to offer vehicle purchase loans for modified vehicles without added administrative work/cost of vehicle loan closing, title, collections.

• Allows FAAST to offer higher dollar loans while maintaining sustainability of program.

Contact Information

Eric Reed FAAST New Horizon Loan Program

3333 W. Pensacola Street Building 100, Suite 140 Tallahassee, FL 32304

(850) 487-3278 x 104 Toll Free (844) 353-2278

[email protected] www.newhorizonloanprogram.org

www.faast.org

Kiva: Crowdfunded Microloans

Kiva Loans

• LISC Small Business and Kiva are partnering to advance a shared mission: expanding financial opportunities for underserved entrepreneurs and small businesses in the U.S.

• Kiva is an online loan crowdfunding platform that enables entrepreneurs to access 0% interest small business loans up to $10,000

• Individuals lend $25 or more to borrowers through the platform

• Uses social underwriting to expand access to capital these are character-based loans – Social underwriting = character, relationships, reputation credit scores, collateral, cash flow

• All borrowers must secure a minimum number of lenders from their own networks before their loan is posted publicly on the Kiva website

• Borrowers can get endorsed by trustee organizations who vouch for their character

• All borrowers must make a $25 loan to another fundraising borrower before their loan is posted – demonstrates engagement

The Kiva Loan • Borrowers can apply for up to $10,000 – may qualify for a

lower loan amount if they are already heavily indebted

• For business purposes only

– Purchasing equipment or inventory

– Expanding product lines

– Hiring additional staff

– Marketing, advertising, improving, or creating websites

– Paying for legal fees

• 0% interest, no fees

• 2-year term for $5,000 loans; 3-year term for $10,000

loans

• Repayments begin one month after loan has disbursed

• Loans disbursed and repaid through PayPal

Kiva Borrower Eligibility

• Borrowers must be over the age of 18

• They must have a PayPal account or the ability to create one

• Borrowers cannot currently be in foreclosure or under bankruptcy

• Emphasis on entrepreneurs with household incomes under $100,000

• Borrowers must lend $25 to another fundraising borrower in support of the Kiva community

• Private fundraising period – Each borrower is required to invite a minimum number of

lenders from her own personal network before her loan is posted “live” on the website to the greater Kiva lending community

– These invited lenders can lend as little as $25

Successful Kiva borrowers have…

• A network of supporters and champions (friends, family members, and customers)

• A social media presence

• Tech savviness (comfortable using email, web, PayPal, etc.)

• Comfort marketing their business!

• Momentum coming out of the private fundraising period into public fundraising (~30% or more raised in private)

• A great photo for their campaign

Local Kiva Support: Get help from a trustee organization!

• Trustees are organizations or individuals that recommend borrowers and endorse

them publicly on the Kiva website

• Endorse borrowers based on their character and the viability of their businesses

• Under no financial or legal liability, but…

• …Help support borrowers throughout the Kiva process

– Applying

– Fundraising

– Repaying

Why become a trustee?

• Help the entrepreneurs you work with access capital

• Gain exposure for your organization – each trustee has an online Kiva profile that links to its website and includes information about it

• Track your impact over time and showcase your work with Kiva to funders

Trustee Responsibilities • Spread the word about Kiva • Vouch for creditworthiness • Help ensure that a borrower is successful

– Kiva leans on its trustees in the application, fundraising, and repayment processes. Trustees track borrowers’ progress as they apply, provide advice and share Kiva loans to their networks during fundraising, and follow up with the borrower as necessary during the repayment process.

Loan Example: Heather, Top Shelf Cookies • Produces artisan cookies – “all about

bringing Boston a better cookie”

• Borrowed $5,000 through Kiva to create a new logo, get a wholesale license, and buy labels and packaging

• LISC Small Business matched 42 lenders, contributing $2,250 towards Heather’s loan

• First borrower endorsed by CommonWealth Kitchen in Dorchester, MA, a Boston LISC partner – business has operated out of CWK since September 2014

• Results…new logo!

“I have never felt so energized to move

forward with Top Shelf Cookies. When

you look at a list of 40 people that just

gave you money to continue to follow

your dream and take the next big step, I

kind of want to cancel my vacation and

just get to work. I have great plans for

2016 for Top Shelf Cookies.” – Heather,

Top Shelf Cookies

Next Steps….

• For more information Contact Devin Thompson [email protected]

• Apply for a loan at www.kiva.org/borrow

• Apply to be a trustee at https://www.kiva.org/trustees/apply

• Learn more at http://liscsmallbusiness.org/

Kiva: Crowdfunded Microloans

Kiva Loans

LISC Small Business and Kiva are partnering to advance a shared mission: expanding

financial opportunities for underserved entrepreneurs and small businesses in the U.S.

Kiva is an online loan crowdfunding platform that enables entrepreneurs to access 0%

interest small business loans up to $10,000

Individuals lend $25 or more to borrowers through the platform

Uses social underwriting to expand access to capital these are character-based loans

Social underwriting = character, relationships, reputation credit scores, collateral,

cash flow

All borrowers must secure a minimum number of lenders from their own

networks before their loan is posted publicly on the Kiva website

Borrowers can get endorsed by trustee organizations who vouch for their

character

All borrowers must make a $25 loan to another fundraising borrower before

their loan is posted – demonstrates engagement

The Kiva Loan Borrowers can apply for up to $10,000 – may qualify

for a lower loan amount if they are already heavily indebted

For business purposes only

Purchasing equipment or inventory

Expanding product lines

Hiring additional staff

Marketing, advertising, improving, or creating websites

Paying for legal fees

0% interest, no fees

2-year term for $5,000 loans; 3-year term for $10,000 loans

Repayments begin one month after loan has disbursed

Loans disbursed and repaid through PayPal

Kiva Borrower Eligibility

Borrowers must be over the age of 18

They must have a PayPal account or the ability to create one

Borrowers cannot currently be in foreclosure or under bankruptcy

Emphasis on entrepreneurs with household incomes under $100,000

Borrowers must lend $25 to another fundraising borrower in support of the Kiva community

Private fundraising period

Each borrower is required to invite a minimum number of lenders from her own personal network before her loan is posted “live” on the website to the greater Kiva lending community

These invited lenders can lend as little as $25

Successful Kiva borrowers have…

A network of supporters and champions (friends, family members, and customers)

A social media presence

Tech savviness (comfortable using email, web, PayPal, etc.)

Comfort marketing their business!

Momentum coming out of the private fundraising period into public fundraising (~30% or more raised in private)

A great photo for their campaign

Local Kiva Support: Get help from a trustee organization!

Trustees are organizations or individuals that recommend borrowers and

endorse them publicly on the Kiva website

Endorse borrowers based on their character and the viability of their

businesses

Under no financial or legal liability, but…

…Help support borrowers throughout the Kiva process

Applying

Fundraising

Repaying

Why become a trustee?

Help the entrepreneurs you work with access capital

Gain exposure for your organization – each trustee has an online Kiva profile that links to its website and includes information about it

Track your impact over time and showcase your work with Kiva to funders

Trustee Responsibilities Spread the word about Kiva

Vouch for creditworthiness

Help ensure that a borrower is successful

Kiva leans on its trustees in the application, fundraising, and repayment processes. Trustees

track borrowers’ progress as they apply, provide advice and share Kiva loans to their

networks during fundraising, and follow up with the borrower as necessary during the

repayment process.

Loan Example: Heather, Top Shelf Cookies

Produces artisan cookies – “all about bringing

Boston a better cookie”

Borrowed $5,000 through Kiva to create a new

logo, get a wholesale license, and buy labels and

packaging

LISC Small Business matched 42 lenders,

contributing $2,250 towards Heather’s loan

First borrower endorsed by CommonWealth

Kitchen in Dorchester, MA, a Boston LISC partner –

business has operated out of CWK since September

2014

Results…new logo!

“I have never felt so energized to

move forward with Top Shelf

Cookies. When you look at a list of 40

people that just gave you money to

continue to follow your dream and

take the next big step, I kind of want

to cancel my vacation and just get to

work. I have great plans for 2016 for

Top Shelf Cookies.” – Heather, Top

Shelf Cookies

Next Steps….

For more information Contact Devin Thompson [email protected]

Apply for a loan at www.kiva.org/borrow

Apply to be a trustee at https://www.kiva.org/trustees/apply

Learn more at http://liscsmallbusiness.org/

TRUECONNECT

For Life‘s Unexpected Moments

™

Sometimes we all need a little help

Employees are dealing with financial stress Did You Know?

4 of every 10 American employees are

“one bill from disaster”

™

And that financial stress is not staying at home….

1. MetLife, Inc., 10th Annual Study of Employee Benefits Trends: Seeing Opportunity in Shifting Tides 51 (2012), available at http://www.winonaagency.com/img/~www.winonaagency.com/10th annual met life study of ee benefits trends.pdf

2. PricewaterhouseCoopers, LLC, supra note 5, at 11. 3. MetLife, Inc., supra note 12, at 3.

• 22% of employees admit that they have taken unexpected time off in the past 12 months to deal with a financial issue.1

• 39% spend at least three hours each week either thinking about or dealing with financial problems at work. 2

• 81% say financial problems have affected their productivity 3

It’s not about how well you pay employees…

TRUECONNECT

For Life‘s Unexpected Moments

™

$1000 deductible

So when life happens…

Too many employees can’t pay for this…

TRUECONNECT

For Life‘s Unexpected Moments

™

$2,500 deductible

Or this…

TRUECONNECT

For Life‘s Unexpected Moments

™

Millions of employees resort to predatory loans.

Payday loans are a WORKING CLASS issue, not an unemployed or homeless issue.

TRUECONNECT

For Life‘s Unexpected Moments

™

• Regulation • Education Safe Help

TRUECONNECT

For Life‘s Unexpected Moments

™

Solving the predatory lending problem Requires a Team Effort !!!

It’s simple. 4 small loan amounts available online.

$1000 $1500 $2000

TRUECONNECT

For Life‘s Unexpected Moments

™

$3000

• Eligibility based on income and tenure • No credit score needed • Repayment over a full year • Small, amortized payroll deductions • No more than 8% of paycheck for repayment • No more than $3000, regardless of income

Delivered as a voluntary benefit hand-in-hand with Human Resources

TRUECONNECT

For Life‘s Unexpected Moments

™

While payday loans cost hundreds of dollars a month in fees…

the monthly finance charge on a $1,000*

TrueConnect loan is about the cost of a pizza

$11.83 TRUECONNECT

For Life‘s Unexpected Moments

™

If you provide an alternative to 400% payday loans to your employees - you will help them save up to

$1,350 each time

How does that feel?

TRUECONNECT

For Life‘s Unexpected Moments

™

Other programs hide extra fees

TrueConnect hides

nothing

TRUECONNECT

For Life‘s Unexpected Moments

™

There’s no waiting

employees know right away if they can

get the emergency help they need

TRUECONNECT

For Life‘s Unexpected Moments

™

Home Login Questions For Employers Since employee payment history is reported to credit bureaus, the

effect on credit score may even be positive

TRUECONNECT

For Life‘s Unexpected Moments

™

Home Login Questions For Employers TrueConnect is offered by the social mission bank named “Best for the World Overall”……….three times

TRUECONNECT

For Life‘s Unexpected Moments

™

so you can be confident you’re entrusting this task to the right team!

“Thank you for offering me a chance at help without the instant fear of being rejected”

“This came at just the right time for me”

TRUECONNECT™

For Life’s Unexpected Moments

TrueConnect Loans made by Sunrise Banks, N.A. St. Paul, MN.

Hello! I’m Andy Posner,

Founder & CEO of Capital Good Fund

A 501(c)3 nonprofit, U.S. Treasury-certified

Community Development Financial Institution

that provides small-dollar personals loans and

financial coaching

Who We Are

• Founded in Rhode Island in 2009

• 1,400 loans totaling $1.6 million financed

• 93% all-time repayment; 96% since 2013

• $730K outstanding with 99.5% on-time

• Personal loans range from $300 - $20,000

• 21 full-time staff

• Lending throughout RI, FL, and DE

Our History

Products – Small Dollar Personal Loans Credit Builder Loan: $15 / month for 12 months. Reported to bureaus. Includes 90 minute Coaching session

Loan Examples Amount Purpose Rate Term

(Months) Monthly Payment

Total Paid Total Interest

$400 Car repair 30% + $8 closing

12 $39.77 $477.24 $77.24

$1,000 Citizenship Costs

24% 24 $52.87 $1,268.88 $268.88

$15,000 Car purchase 13% 60 $341.30 $20,478 $5,478

Points of Comparison:

1. Payday loan: 278%. Rolled over average of 8 times

2. Pawn ticket: 60%

3. Rent-to-own: $500 couch = $1,000 +

4. Title-secured loan: 100% + APR

5. Buy-here-pay-here: 18% + APR

6. Overdraft: Effective APR of 1,000% (or more!)

1. Residual ability-to-pay test

2. Banking history

3. Credit history

4. Loan Purpose

5. Other

Loan Features 1. Monthly Payments reported to all three bureaus

2. No prepayment penalty

3. Unsecured (save for car loan)

4. No minimum FICO

5. ITIN or SSN

6. For car loans:

i. Max LTV 115%

ii. $500 down

Underwriting Guidelines

Florida Expansion

Florida Plans

1. Began lending statewide October 1st, 2016

2. First in-state hire begins February 1st, 2017

3. 600 + loans in 2017

4. Three in-state staff by summer 2017

Why Florida?

1. $3 billion + payday loan market

2. Large immigrant population

3. Prevalence of title-secured and buy-here-pay-here loans

4. Low regulatory barrier-to-entry

5. National Council of La Raza Affiliates

6. Critical to five-year scaling plan

Thank You! Questions?

Small steps toward a big difference

• Consumer Finance Expertise – Manatee Community Federal Credit Union 3.5 years President 1.5 Years Exec. Vice President 5 Years Board of Directors • 2 Years Vice Chairman

• Community Development Expertise – 7 1/2 years Executive Director Bradenton Central CRA – 2 years Community Liaison for Gov. Jeb Bush’s Front Porch Initiative – 5 years Board of Directors Florida Redevelopment Association – 3 years Board of Directors Florida Prosperity Partnership – 2015 Clinton Global Initiative Attendee – Founder/Chairman Suncoast Community Capital – Founder/Co-Chairman CareerEdge Workforce

Funders Collaborative

– Founder/Interim Executive Director Central Economic Development Center

• Credit Expertise – 5 years Management at Equifax

Sherod Halliburton, President of MCFCU

Our Mission Strengthen communities, build assets, and improve lives by providing

access to affordable, high-quality financial products and related services with emphasis on the needs of low-income communities.

Small steps toward a big difference

Small steps toward a big difference

Our History

• 1958 – Founded to exclusively serve employees and family members of Tropicana Products

• 2002 – Designated as a Low-Income Credit Union

• 2005 – Charter expanded to serve all of Manatee County

• 2012 – Certified as Community Development Financial Institution (CDFI)

• 2014 – Expanded Field of Membership to include participants in poverty elimination programs

• 2016 – Wells Fargo NEXT Award Finalist

• 2016 – Launched Community Network Poverty Elimination Program

Small steps toward a big difference

Small Dollar Loans

Long-Term Solution or Crutch?

Small steps toward a big difference

Pay Day Loans

Advantages Solves an immediate cash flow challenge Easy approval Friendly staff

Disadvantages

Extremely high effective interest rates Must pay in full or it renews Must provide access to your Checking Account Timely payments don’t improve your credit score

Small steps toward a big difference

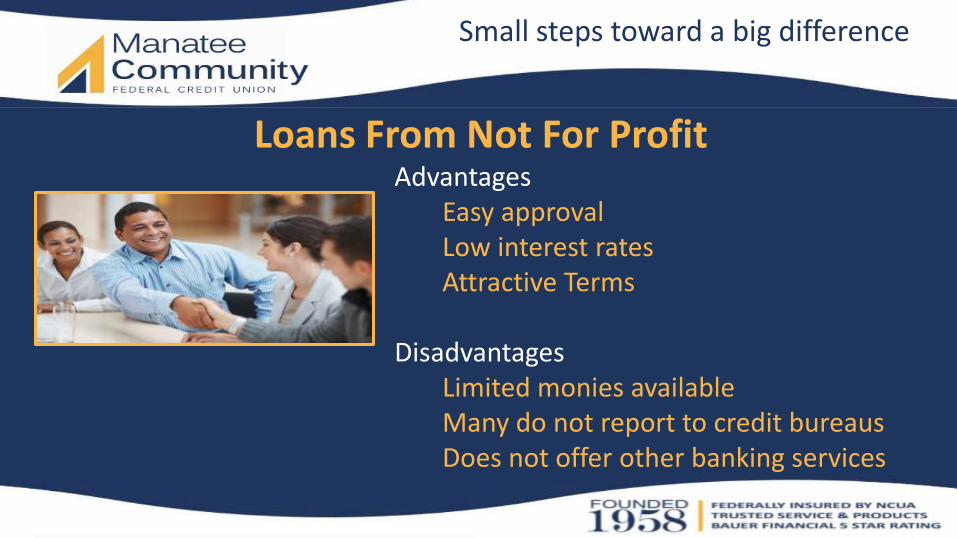

Loans From Not For Profit Advantages

Easy approval Low interest rates Attractive Terms

Disadvantages

Limited monies available Many do not report to credit bureaus Does not offer other banking services

Small steps toward a big difference

Depositories Advantages

A variety of loan and deposit options Low interest rates Unlimited Resources

Disadvantages

Must Credit Qualify Late Payments negatively impact credit

Small steps toward a big difference

Manatee Community FCU Unsecured Line of Credit

Advantages Easy Qualifications Small or Large Dollars ($200-$15,000) Timely payments grow your credit Score Increased credit limit with timely payments

Disadvantages Must Credit Qualify Revolving Debt

Small steps toward a big difference

CONTACT INFORMATION

INVENTORY OF SMALL DOLLAR LOANS

Credit Unions and CDFIs:

FloridaProsperityPartnership.org/PRESENTATIONS

JAN 2017 13 12 00

SMALL DOLLAR LOAN

ONLINE CONFERENCE