Embed Size (px)

Citation preview

2 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Washington, DC / London / Paris

Date June 12/13, 2012

Presented by:

Wes Henderek & Emma Mohr-McClune Consumer Services US/ Europe

Smartphones: The Death of Subsidies? A cross-regional view of carrier moves surrounding device subsidies

3 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Agenda

US • High level historical view of U.S. postpaid subsidy trends • Postpaid & Prepaid subsidy models • Key takeaways and trends

EUROPE • A year of change • Device financing: Three Models • Pros/ Cons • Emerging trends

4 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

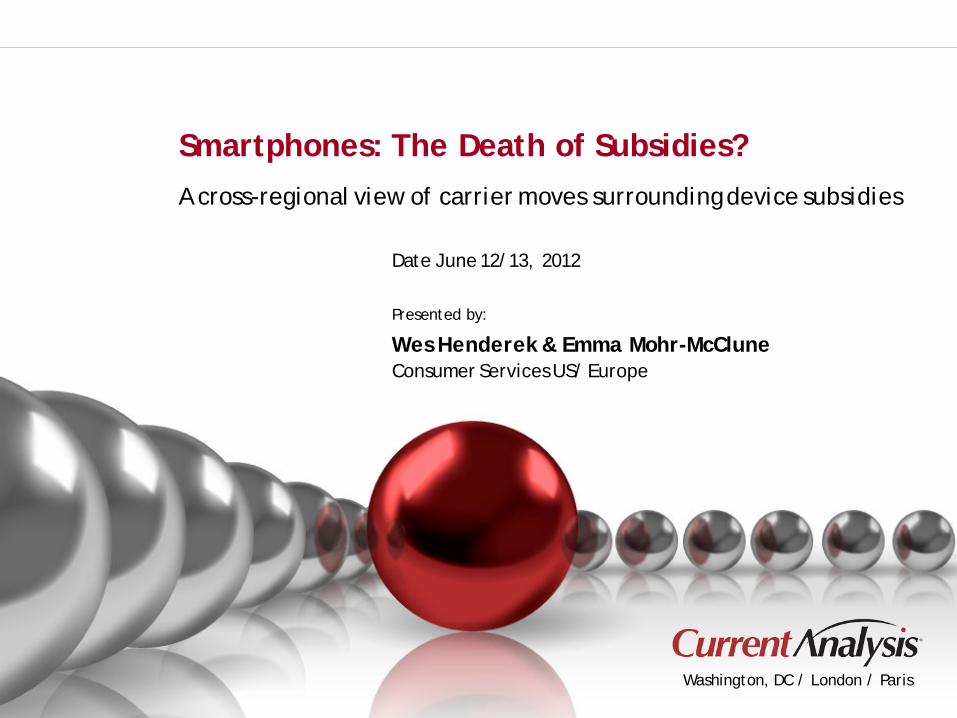

U.S. Subsidy Trends According to Current Analysis Retail Data

Over Time View of Full Retail vs. Subsidized Handset Costs

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

May

-10

Jun-

10

Jul-

10

Aug

-10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-

11

Aug

-11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Full Retail Price

Average Postpaid Savings

Subsidized Postpaid Price

Average U.S. Postpaid Handset Savings Compared to Full Retail Price is up $90 in

the Last Two Years!

5 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

U.S. Postpaid and Prepaid Device Market Today

All major national postpaid carriers engage in aggressive postpaid subsidies – Subsidies can vary by carrier

• T-Mobile USA is least aggressive on subsidies by far

Subsidies still dominant, device financing rare

Subsidies becoming increasingly commonplace and aggressive in the prepaid market due to the strong emergence of Smartphones and aggressive competition

• Regional Unlimited Providers, National Carriers, Carrier sub-brands, and MVNO’s

6 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Current U.S. Postpaid Models – Subsidy, Finance, & Rewards

• Major Tier 1 and Tier 2 Postpaid carriers • Handset includes full device subsidy which can vary by carrier and device • Select carriers actively using higher subsidy/plan promotions to push LTE upgrades • LTE handsets seeing increased marketing & advertising • The hidden subsidy war – The carrier exclusivity push and pressure on OEMs • Subsidies stabilizing in last several months • SIM activation not actively promoted by GSM based carriers (except T-Mobile USA)

1. Postpaid – Standard Subsidy Model

• T-Mobile USA Value Plans • Proposition is a bundle of Plan + Device monthly payments • Payments positioned as SEPARATE LINE ITEMS, on the same monthly invoice • Device repayment values linked to device type, not plan value • Can include other bundled VAS (inclusive handset insurance) • SIM activation with unlocked handset is also actively promoted

2. Postpaid – Device Finance & SIM Model

• US Cellular Belief Project – Still includes standard device subsidy component • Redeem loyalty rewards for faster device upgrades, accessories, downloads, etc. • Rewards escalate depending on spend and loyalty • Two-year contract is eliminated after first 24 months – devices still fully subsidized

3. Postpaid - Rewards

7 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: Verizon Wireless Double Data Promotion Pushes LTE Smartphone Sales

This postpaid promotion was in place for more than six months

8 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: T-Mobile Value Plans is only Major U.S. Postpaid Device Financing

Value plan postpaid handsets are purchased on a 20 month agreement

SIM

onl

y Va

lue

plan

s ar

e ac

tive

ly

prom

oted

9 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: US Cellular Belief Project – Subsidy Model with Rewards

Earn rewards based on total spend and loyalty with full device subsidy

Rew

ards

cus

tom

ers

only

hav

e to

sig

n on

e tw

o-ye

ar c

ontr

act

10 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

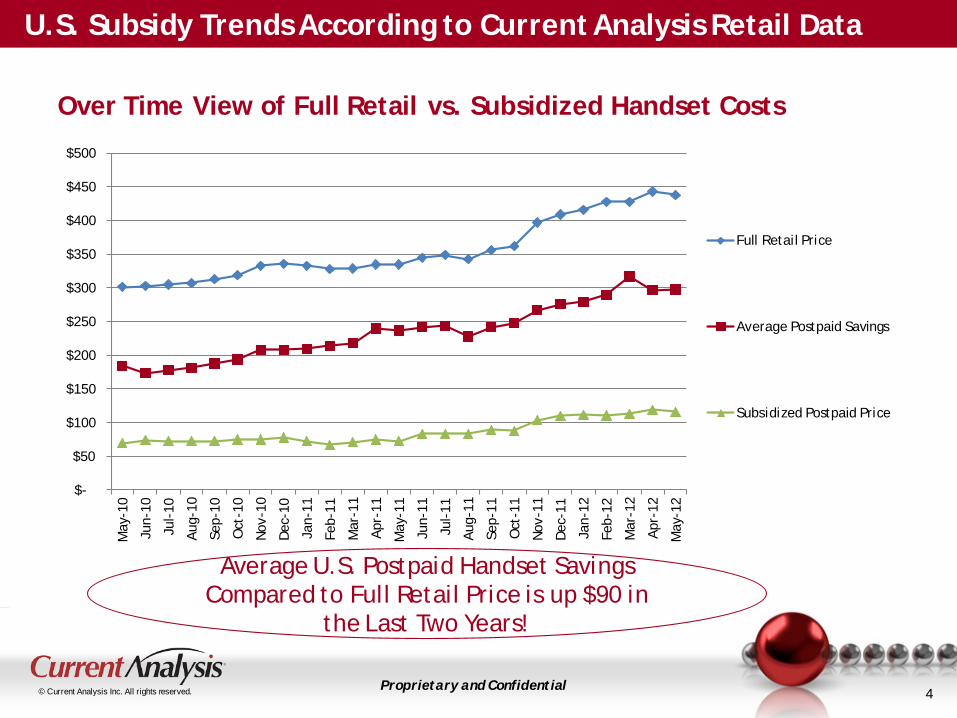

Current U.S. Prepaid Models – Subsidy (Monthly Prepaid), No Subsidy & SIM

• National Carriers, Carrier sub-brands, Regional Carriers • Subsidies on monthly prepaid plans have been increasing over the last two years • Smartphones and competition are the big driver behind increased subsidies • Providers looking to migrate feature phone customers to Smartphones (Leap Stats) • Prepaid Android Smartphones have dropped as low as $50 to $60 • High-end Smartphones increasingly common – iPhone 4 and 4S at Leap and Virgin

1. Prepaid (Monthly) – Subsidy Model (Increasing)

• MVNOs and providers offering PAYGO products • MVNOs looking to keep cost structure down and innovate on business model • Examples of Republic Wireless and Ting

2. Prepaid – Full Price Devices (Mostly)

• MVNO aligned with GSM technology – Simple Mobile & H20 • Relatively aggressive monthly pricing due to low costs • Link to third party vendor for devices with plans – Simple Mobile with Expansys

3. Prepaid – SIM only

11 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

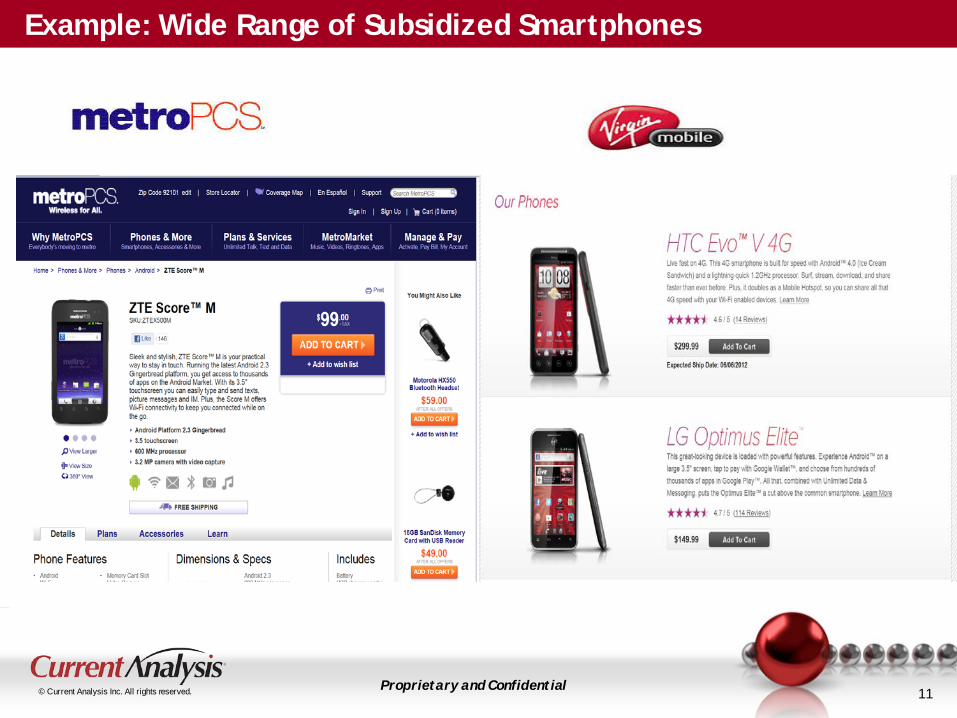

Example: Wide Range of Subsidized Smartphones

12 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: Limited Subsidy MVNO with innovative model

13 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: SIM Model

14 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Key Takeaways & Trends in the U.S. Postpaid & Prepaid Device Markets

Postpaid providers still heavily entrenched in subsidies • Subsidy and Promotional variation happening around LTE devices • Subsidies have increased for Smartphones but stabilizing • Rewards programs appearing but limited • SIM/unlocked device model not actively promoted

Postpaid Device Financing Option Limited to T-Mobile USA • Device financing lets T-Mobile advertise lower rate plan prices • 20 month financing plan is still very complex • T-Mobile providing interest free loans

Prepaid providers see increased subsidies with move to Smartphones • Leap now has 50% of subscriber base on Smart devices • MVNOs looking to new business models (not subsidies) to innovate • Prepaid providers could look to implement device financing on higher end

devices

Device Financing Options Limited & Subsidies “Still” the Rule

15 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Europe: ONE YEAR AGO …

Nordic players, plus Vodafone CZ and O2 DE

Subsidies dominant, device financing rare

Early 2011: European MNOs in the grip of smartphone user acquisition drive, using subsidies to migrate feature-phone users to smartphones, higher ARPU plans

16 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Roll clock forward to June 2012

Today Available In Most Markets (in one form or another…)

Device Financing Spreads Across Europe

17 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

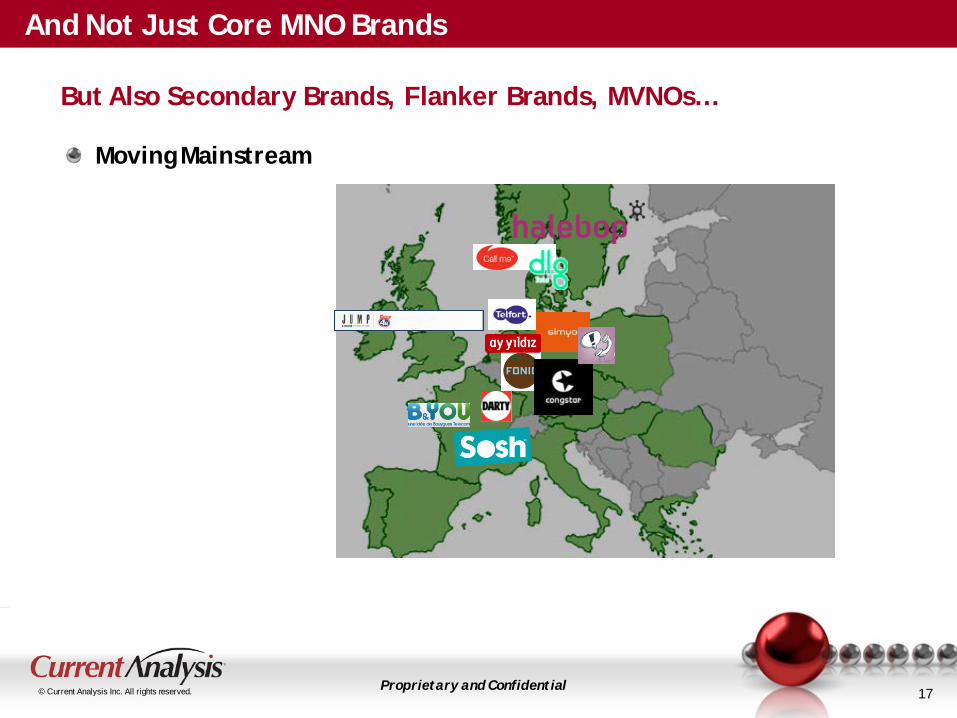

And Not Just Core MNO Brands

Moving Mainstream

But Also Secondary Brands, Flanker Brands, MVNOs…

18 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

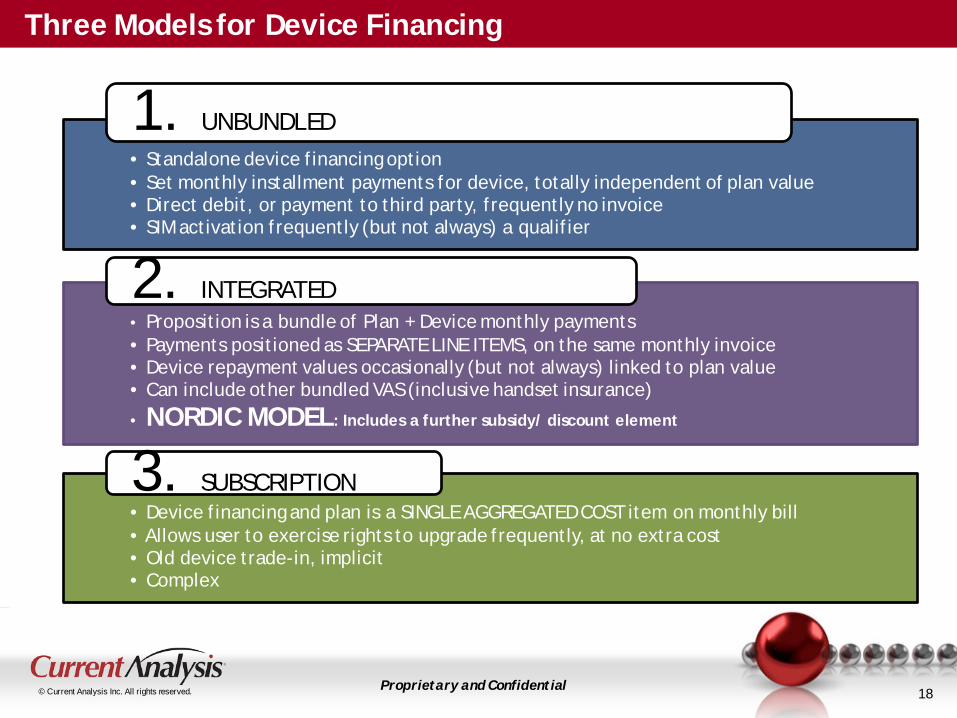

Three Models for Device Financing

• Standalone device financing option • Set monthly installment payments for device, totally independent of plan value • Direct debit, or payment to third party, frequently no invoice • SIM activation frequently (but not always) a qualifier

1. UNBUNDLED

• Proposition is a bundle of Plan + Device monthly payments • Payments positioned as SEPARATE LINE ITEMS, on the same monthly invoice • Device repayment values occasionally (but not always) linked to plan value • Can include other bundled VAS (inclusive handset insurance)

• NORDIC MODEL: Includes a further subsidy/ discount element

2. INTEGRATED

• Device financing and plan is a SINGLE AGGREGATED COST item on monthly bill • Allows user to exercise rights to upgrade frequently, at no extra cost • Old device trade-in, implicit • Complex

3. SUBSCRIPTION

19 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

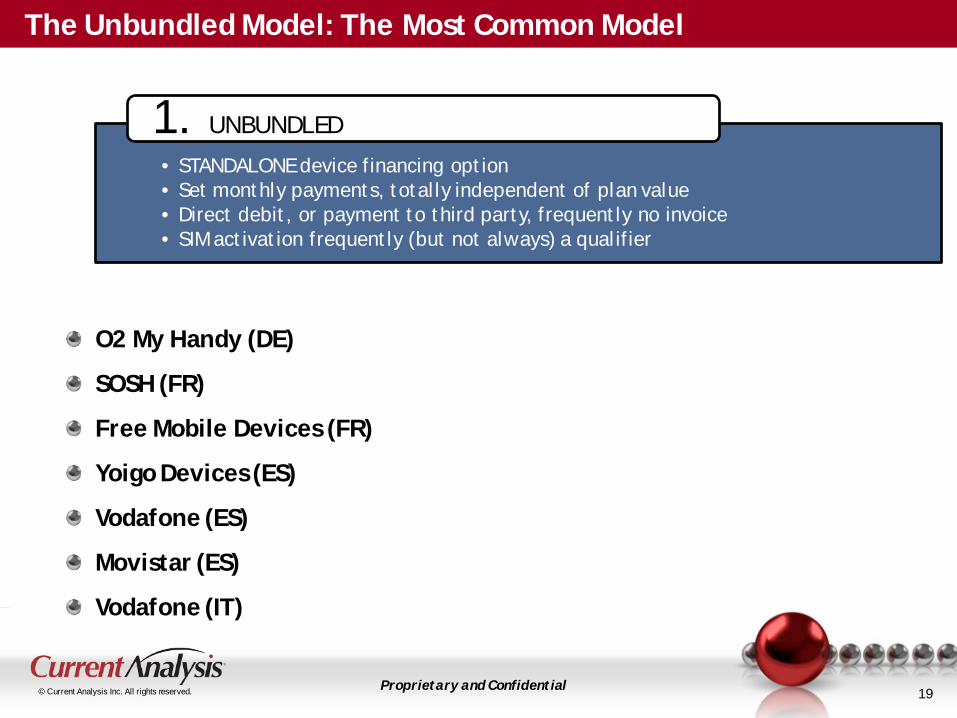

The Unbundled Model: The Most Common Model

O2 My Handy (DE)

SOSH (FR)

Free Mobile Devices (FR)

Yoigo Devices (ES)

Vodafone (ES)

Movistar (ES)

Vodafone (IT)

• STANDALONE device financing option • Set monthly payments, totally independent of plan value • Direct debit, or payment to third party, frequently no invoice • SIM activation frequently (but not always) a qualifier

1. UNBUNDLED

20 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: O2 My Handy (Telefonica Germany)

21 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

The Integrated Model (Simple)

BASE (DE)

Ay Yildiz (DE)

• Proposition is a bundle of Plan + Device monthly payments • Payments positioned as SEPARATE LINE ITEMS, on the same MNO monthly invoice • Frequently includes other bundled VAS (inclusive handset insurance)

2. INTEGRATED

22 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: BASE Germany

23 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

The Integrated Model (NORDIC MODEL)

‘TDC Rate’

‘Telenor Smart Agreement’

‘Telia Devices’

• Proposition is a bundle of Plan + Device monthly payments • Payments positioned as SEPARATE LINE ITEMS, on the same MNO monthly invoice • Frequently includes other bundled VAS (inclusive handset insurance)

2. INTEGRATED

• NORDIC MODEL: Includes a further subsidy/ discount element

All integrated models which also include a monthly discount element, linked to plan value

24 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example: TDC Rate

25 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

But if I choose a higher-value plan

My ‘TDC Rate’ (monthly device loan payments) is reduced

26 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Third Model: Subscription

JUMP in UK

Highest Level of Integration, handset financing payments and plan

• Device financing and contract plan is a SINGLE AGGREGATED COST item on monthly bill • Allows user to exercise rights to upgrade frequently, at no extra cost • Old device trade in, implicit • Complex

3. SUBSCRIPTION

27 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Pros & Cons – Unbundled Versus Integrated Models

UNBUNDLED INTEGRATED

Pros • Pricing Transparency • Easy to grasp • Applicable to post and prepaid

Cons • No clear upgrade lever • Little differentiation opportunity

Pros • Proposition creativity • Focuses on bottom-line cost • Incentivizes postpaid/ no-

contractual relationship • Upgrade lever opty (BASE)

Cons • Complex, and not as transparent as

unbundled model

28 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Six Emerging Trends In Device Financing, Europe

Self-service portals • Online self-service portal for loan status, early repayments (O2 DE)

Promotions/ launches with distinct Apple products • Guarantees attention, could include trade-in element (O2 UK, TDC)

Align with Smartphone Recycle/ Trade-In • O2 Lease, BASE Germany credit note

And Second Hand Device Online Store • O2 Outlet (Germany), Movistar Spain, B&You

Aligned with Loyalty Points, Upgrade Bonus • BASE, and Movistar Spain

Filling the ‘Loyalty’ Vacuum…

29 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Example, Movistar Spain…

Bringing Multiple Elements Together

Loyalty points bonus for upgrade

Device trade-in for credit note

Choice of repayment periods

Discount for Movistar ADSL customers

30 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Lastly… it’s not only MNOs

Apple Store UK, ‘AFS’ (Apple Financing Service’, together with Barclays Bank) offered at checkout

Apple Offers Its Own Device Financing Options

31 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

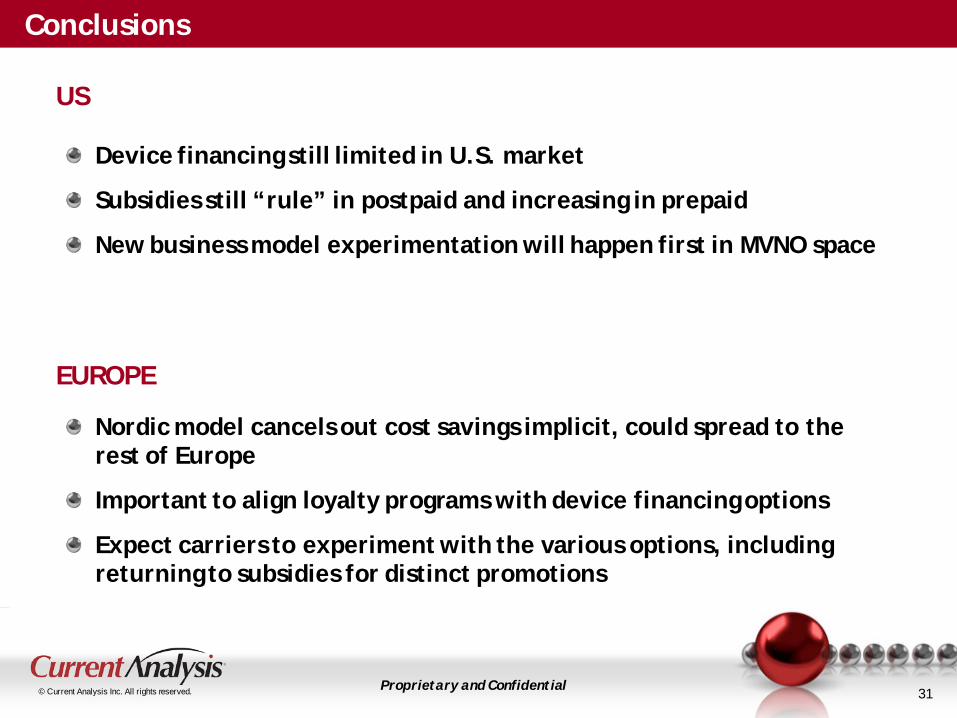

Conclusions

Device financing still limited in U.S. market

Subsidies still “rule” in postpaid and increasing in prepaid

New business model experimentation will happen first in MVNO space

US

EUROPE

Nordic model cancels out cost savings implicit, could spread to the rest of Europe

Important to align loyalty programs with device financing options

Expect carriers to experiment with the various options, including returning to subsidies for distinct promotions

32 Proprietary and Confidential © Current Analysis Inc. All rights reserved. 32 Proprietary and Confidential © Current Analysis Inc. All rights reserved.

Thank You

Weston Henderek Principal Analyst, Consumer Services U.S. Email: [email protected] Direct: +1 703-788-3606 Mobile: +1 858-925-3764

Current Analysis helps clients differentiate themselves in the marketplace and win more business by providing continuous, in-depth competitive intelligence. We enable sales teams, marketing professionals, product managers, and executives to anticipate market opportunities and quickly respond to competitor threats.

Questions? Emma Mohr-McClune Research Director, Consumer Services Europe Email: [email protected] Direct: +49 (0) 76 15 03 59 29 Mobile: +49 (0) 172 307 3208 Twitter: @EmmaMM8