Embed Size (px)

DESCRIPTION

Smile Brands 2010 Decision Guide

Citation preview

2010 Benefits Decision Guide

www.SmileBrandsBenefits.com 1-877-263-2363

A Message from Beth Goldstein Senior Vice President, Human Resources, Smile Brands Inc.

One way Smile Brands cre-ates Smiles for Everyone!

is offering you a benefits program that is part of a competitive total rewards package. Our goal is to offer health and welfare plans that provide eligible participants a variety of cover-age choices that match your needs at a cost that is affordable for both you and the company.

The high cost of healthcare in our country continues to be on everyone’s mind. At Smile Brands, we remain committed to offering a great plan and we assertively look for ways to balance the cost of healthcare and other total rewards programs.

The availability of company-provided healthcare requires a part-nership between the company and you. The company’s responsi-bility is to annually negotiate the lowest cost and highest quality plans on your behalf – and to monitor provider and carrier costs as well as performance. The company also contributes a meaning-ful portion of the costs associated with the plans.

Your responsibility is to take an active role in learning about and understanding the benefits offered, to elect coverage that is right for you and your family and to be a responsible healthcare consumer. Because our plans are self-insured, you can hold down future cost increases by taking care of yourself so that you stay healthy, making smart benefit choices during Open Enrollment, and then using those benefits wisely throughout the year.

Last year we made significant benefit plan changes that have proven to be very beneficial to our employees, affiliates and the company. As projected, switching to the Blue Cross network en-abled deeper discounts for health services which translated into lower out-of-pocket costs for our employees, affiliates and their eligible dependents with no decrease in the quality of service. Because of our ability to hold costs down there are minimal plan design changes and next year’s self insured plan premiums will be affected as follows:

There has been a modest 4.7% increase to the Open Access Plan with some tiers experiencing no increase at all. This increase com-

pares extremely favorably to the projected national increase trend of 9.2%

The costs for the Basic Choice Plan will decrease a significant 20.1%. Many eligible employees selected the Basic Choice Plan, introduced last year, which provides basic medical services at a very affordable cost per paycheck. Basic Choice allows for six doctor visits, two urgent care visits and a comprehensive prescription plan. Affordability is achieved by having a high deductible for most other costs. If you want a plan with low monthly costs, you do not visit the doctor often, and you are looking for coverage primarily to stay well and for protection in the event of a major accident or illness, the Basic Choice Plan is now even more compelling.

Kaiser (which is only available in California) is a fully insured plan and all decisions regarding coverage and costs are made by Kaiser. Unfortunately, Kaiser has increased their premiums and made adjustments to their hospital co-pays which are out-lined in this guide. With the addition of “Employee + Children”, Kaiser now has four tiers of coverage, which is consistent with our other plans. Although Smile Brands contributes the same dollars per employee for the Kaiser Plan as it does the self-insured plans, the Kaiser increase is significant enough that it will have a meaningful impact on employee premiums.

After reading about the benefit offerings for 2010 and their new premium costs, if you do not wish to make any changes, you do not have to re-enroll. With the exception of Flexible Spending Accounts (FSAs), your current plan se-lections will automatically roll over for use next year. FSAs, however, do not automatically renew. You must re-elect an amount to contribute to your FSA every year.

Medical coverage is a very personal decision and you should review your options carefully before making a decision. We invite you to read this Benefits Decision Guide thoroughly because the choices you make will be your coverage for the next year and cannot be changed mid-year (unless you experience a Qualifying Status Event [see page 5, When Can You Change Your Benefits?]). If you need assistance, please call a benefits specialist at our Benefits Service Center at 1-877-263-2363.

2www.SmileBrandsBenefits.com 1-877-263-2363

www.SmileBrandsBenefits.com 1-877-263-2363

for 2010Here’s What’s New

Kaiser Plan ChangesKaiser has increased the co-payments required on certain ser-vices:• Hospital admission co-payment is now $500• Well child and pre-natal visits are increasing to $15 each. • Outpatient surgery procedure co-payment will increase to $100• Ambulance services will increase to $100 per trip.

Kaiser is also increasing the cost of name brand prescriptions to $35 for a 30-day supply or $70 for a 100-day supply.

A New Network for our Vision PlanWe have added the Blue Cross vision care network to our vision plan. This change will provide access to 44,000 vision care providers nationwide. These providers include thousands of independent providers, as well as retail chain providers such as LensCrafters, Target Optical, J.C. Penney Optical, Sears Optical and Pearle Vision.

Lastly, Kaiser will be changing to four-tier coverage:• Employee Only• Employee plus Spouse (formerly Employee plus 1)• Employee plus Children (new)• Employee plus Family

These changes will make Kaiser more consistent with our other medical plans.

Aside from changes in employee premiums, there are very few changes to our health and welfare plans for 2010.

Table of Contents

Here’s What’s New for 2010 …...................... 3 Eligibility ............................……................. 4 When Can You Change Your Benefits ............. 5

The Healthcare Partnership .........…….......... 6

Be a Responsible Partner in Controlling Healthcare Costs ........................................... 7 Save Money Stay In-Network .......….…........ 8 Comparison of 2010 Medical Plans …........ 10 Medical Services & Contributions .…............ 11 Dental Services ..............................……..... 12 Vision Services & Contributions ................... 13

Life & Disability Insurance ...................…..... 15 Common Medical Plan & Insurance Terms ........ 16

Flexible Spending Account ......................…... 17 Employee Perks ...........................……….... 21 Enrollment Instructions ..................…….. 22

Who is Eligible to Participate in the Smile Brands Benefit Plans?

Employees and Affiliates: All full-time, regular new hires are eligible for coverage on the first day of the month follow-ing 90 consecutive days of full-time employment.

Spouse: The employee’s or affiliate’s legal spouse is eligible for coverage; a marriage certificate, recognized in your state of residence, must be provided when requested.

Domestic Partners: There are specific criteria that must be met for Domestic Partners to be eligible. Please refer to the eligibility rules on the Benefits website www.SmileBrandsBen-efits.com or contact the Benefit Service Center at 1-877-263-2363.

Children: An unmarried child of the employee or spouse/do-mestic partner must meet one of the following criteria:• Under age 19• Under age 25, if they are a full-time student and depend on the employee for support• Has reached the age of 19 and is unable to work because of a mental or physical handicap.

Who is Not Eligible to Participate in the Smile Brands Benefit Plans?

Here are examples of individuals who would not be eligible under Smile Brands’s plans.• Part-time employees and affiliates working 31 hours per week or fewer• Employees and affiliates who are temporary or independent contractors• Ex-spouse• Fiancé• Boyfriend• Girlfriend• Cousin• Brother

• Sister• Parent• Grandparent• Niece• Nephew• In-laws• Aunt • Uncle• Married children• Child age 19 to 25 who is not attending an accred- ited school full time

Eligibility

4www.SmileBrandsBenefits.com 1-877-263-2363

Here is a list of the qualifying life events allowed by the IRS:

• Marriage, divorce, legal separation, or annulment

• The birth, adoption, or placement for adoption of a child

• The death of your spouse or a child

• Change in your employment status, or that of your spouse, including termination or commencement of employment; change from

an ineligible category to an eligible category (part-time to full-time) or loss of spousal coverage while on an unpaid leave

• Dependent status: ceasing to qualify due to age or student status

• Change in your work site or residence state or that of your spouse or child

• Eligibility for COBRA for your spouse or child;

• Acceptance by the Plan of a qualified medical child support order; or

• Entitlement to Medicare or Medicaid by you, your spouse, or your child.

NOTE - Financial hardship is not considered a qualifying event for cancellation or changes to coverage.

If any of these events occur and you elect to change your coverage, please notify the Smile Brands Benefits Service Center and complete a Change Form within 31 days. This 31-day eligibility period applies to any change in coverage (such as the addition of a dependent, etc.). You must supply written documentation, including a completed Change Form and the appropriate document from the Acceptable documents list at www.SmileBrandsBenefits.com (for example, a birth certificate for a new child), for any qualifying event.

When Can You Change Your Benefits?

Typically, you would only make changes to your

benefits during Open Enrollment. Otherwise, you

may change the amount of your deduction or

cancel a benefits election during a plan year only

if you have a change in family status or other

“Qualifying Life Event”.

5www.SmileBrandsBenefits.com 1-877-263-2363

6

Open Access and Basic Choice are both “self-funded” medical plans and it’s important to under-stand the fundamental difference between medical insurance issued by an insurance company and a self-funded insurance plan. The difference can be significant, especially to your wallet.

In a self-funded medical plan, the company itself provides medical coverage by paying for claims directly from company funds. In Smile Brands Inc.’s case, the plan is administered by a third party, but the claims themselves are paid directly by Smile Brands By being self-funded, Smile Brands avoids paying the high profit margin that an insurance company would tack on for being insured by them. A self-funded plan saves both you and the company this expensive and unnecessary added cost.

Here’s how this can affect your wallet. Since our plan is self-funded, the premium you pay is a per-centage of what we project the cost of the claims will be for the coming year. This projection is based on the claims paid in the prior 12 months. However, if the overall cost of claims is higher than project-ed, your portion of this higher cost will increase in 2011, which translates into higher premium deduc-tions from everyone’s paychecks. The good news is the opposite is also true. If the projected overall claims cost decreases next year, premiums in 2011 could decrease as well, lowering the cost of our plans and your payroll deductions.

The Healthcare Partnership

Emergency Room Versus Urgent Care Centers

Falling off a ladder. A pot of boiling water knocked off the stove. A severe reaction from a food that was eaten or an insect bite. Which of these situations will result in a trip to the emer-gency room? The answer, of course, depends on the severity of the injury or illness. The real question to ask is: Does the injury or illness pose an immediate threat to the victim’s life? If the answer is “No”, head to your nearest urgent care facility. Not only will the patient receive the medical attention they deserve, the $50 co-pay will be a fraction of what you would pay going to the emergency room.

www.SmileBrandsBenefits.com 1-877-263-2363

1. Make sure your doctor is in the networkGoing to a doctor that isn’t participating in the network costs both you and Smile Brands more than we need to pay for the same service. Now that we are using the vast Blue Cross network, there is an even higher likelihood your doctor will be in-network. Using a participating in-network doctor, medical group or hospital provides all of us the best value for our healthcare dollar.

2. Use generic drugs when availableThe next time you see one of those commercials for a name brand drug, ask yourself how the drug companies can afford to pay for all those ads. A month’s supply of many name brand medicines can cost you and Smile Brands $300 or more. The same generic prescription would cost a fraction of that. Generic substitutes must contain the same active ingredients and produce the same effect on the body as their brand-name counterpart. The FDA moni-tors all drugs to ensure that both the brand name and its generic equivalent meet the same requirements for quality, strength, purity and potency.

If you take maintenance prescription medications, using a mail order pharmacy is the only way to go. You can get a three-month supply for the same cost as a two-month supply from your local pharmacy. That’s like getting a month of your prescription for free!

3. Choose the proper place for healthcareAn emergency room should only be used for true emergen-cies, which are extremely serious and the health of the patient is in imminent danger. For everything else there are urgent care centers, your medical group’s walk-in center, and your own doctor’s office. Going to the emergency room for a non-immediate serious threat to your health is not only expensive, it clogs up the emergency healthcare system, driving up the overall cost of healthcare.

4. Take charge of your healthIt’s your health and well-being, so don’t take it lightly! Getting an annual physical, for example, is one of the best ways for you to keep small health issues small and big ones from becoming any bigger.

Be prepared for your visit to the doctor. Write down questions, symptoms, and any prescriptions you are currently taking. Writing these topics down ensures that you get all your ques-tions answered and the doctor has all the information needed to make a diagnosis.

Let your doctor know your family’s medical history. Informa-tion about your family history can often provide clues to aid your doctor in the early detection of some life-threatening diseases. Ask as many questions as you can; doctors are there to inform and treat you.

5. Follow your doctor’s recommendationsWhether it’s taking a prescription medication, changing your diet, getting more exercise, or quitting smoking, when you don’t follow your doctor’s instructions you have just wasted both time and money by visiting the doctor, with little or no benefit to your health and well-being.

6. Seek a second opinion for serious illnessesWhen diagnosed with a serious illness, consider getting a second opinion before undergoing treatment. Never let one serious diagnosis be your only diagnosis. You might want your doctor to send lab tests and x-rays to the second doctor so that you won’t have to repeat them.

7. Make wellness a way of lifeTake time to focus on your own health and wellness. Your doctor can guide you about how to be as fit as you can be. Take time to exercise regularly, get enough sleep, stay within a few pounds of your recommended weight, drink moderately and don’t smoke. Staying healthy is good for both you and your wallet!

Be a Responsible Partner InControlling Healthcare CostsThere are many factors beyond our control that contribute to the escalating cost of healthcare, but there are also many things all of us can do to keep our costs as low as possible. The best way to accomplish this is to think of yourself as the person in charge of next year’s cost – because for a large portion of the overall cost, you truly are! Here are some ideas that will help you stay in control of your medical costs.

7www.SmileBrandsBenefits.com 1-877-263-2363

In-Network Amount

Allergy shot $100

Network discount -$40

Balance $60

Insurance coverage at 80% -$48

Patient responsibility $12

Plan participants on the Open Access plan can choose any healthcare provider they wish, whether or not the doctor or hospital is des-ignated by Blue Cross as being “In-Network”. This is one of the primary differences between Open Access and the Basic Choice plans. (Basic Choice does not cover healthcare provided by out-of–network providers at all.) But just be-cause you are able to use out-of-network pro-viders, doesn’t mean you should! If you elect Open Access, paying attention to whether or not your healthcare providers are in the Blue Cross Network is an excellent way to save money. While in-network and out-of-network terminology may sound confusing, the follow-ing may help you understand the impact of using the Blue Cross Network.

What Does It Mean to be In-Network?Blue Cross/Anthem (Blue Cross) has contracted with a vast number of providers on your behalf to get services at discounted rates. In turn, these healthcare providers get higher volumes of patients and a consistent flow of insured patients. Blue Cross designates these providers as being “in-network” because of their pre-selection to provide quality care at a contracted rate. The main advantage for you in using an in-network provider is that you receive this negotiated discounted rate for their services. As an added incentive, our Open Access plan will pick up a larger portion of the bill than it would with an out-of-network provider.

An example: An in-network Blue Cross doctor may regularly charge $100 for an allergy shot at the doctor’s office. Blue Cross, however, has contracted with them to discount this visit to $60. In addition, our plan covers 80% of this reduced cost with Open Access, so the patient’s responsibility would only be $12.

Compare this to an out-of-network physician who also charges $100 for an allergy shot at the doctor’s office. Without the negotiated rate from Blue Cross, your cost will remain $100. For out-of-network providers, the Open Access plan covers 60%, making your patient responsibility $40 – over three times more than the cost of using an in-network provider!

Save Money!Stay “In-Network”

Out-of-Network Amount

Allergy shot $100

Network discount $0

Balance $100

Insurance coverage at 60% -$60

Patient responsibility $40

8www.SmileBrandsBenefits.com 1-877-263-2363

How Do I Find Out Who’s In-Network?

Doctors, medical groups, and other healthcare providers move in and out of a network. The best way to determine if a doctor or hospital is in-network is to check with the provider before making an appointment. Another way is to go to our benefits website and click on Quick Links, then the Provider Search. You can also call our Benefits Service Center at 1-877-263-2363. They will be happy to assist you.

Out-of-Network Service Provided Through an In-Network Provider

In rare cases, it is possible that you could go to an in-network provider and receive ancillary services from a provider who is out-of-network. An example of this might be going to a physician for a checkup and having lab work done by a company that may be out-of-network. A less common example is that the hospital where a surgery is performed may be in-network but the anesthesiologist is out-of-network. If you are concerned that this may happen to you, check with your healthcare provider to ensure that all ancillary service providers are also affiliated with Blue Cross.

Using an Out-of-Network Provider

As you have read, going to an out-of-network provider tends to be more expensive, but sometimes it is unavoidable. Here are some tips to make this situation as inexpensive as possible:

• Be up front with the provider. Tell them you know they are out of your insurance’s network and that you would like to receive the in-network negotiated rate if possible. They will need to know data about your insurance, such as your group number. All of this information can be found on your Open Access medical ID card.

• Contact the benefits service center at 1-877-263-2363 and make them aware of the situation and enlist their help in sorting out what an in-network price should have been. They will have leverage with the providers that you may not. Get that from them in advance and in writing to save yourself countless hours of headache and expense later.

• Awareness that this could happen is the first step to prevention. When you are verifying an appointment of this nature, be sure to ask network questions. If you specifically asked and were not told ahead of time that you were receiving services from an out-of-network provider, the out-of-network provider may be more likely to provide in-network pricing.

• Be aware that your payments may not be applied to your deductible. Once you’ve met your deductible, out-of-network expenses may be your responsibility to pay either in full or a substantially larger portion.

• It’s a good idea to check with your plan or the Benefits Service Center to make sure you understand your plan specifics. Being aware of the potential exposure and knowing the appropriate questions to ask will help you to navigate the system.

9www.SmileBrandsBenefits.com 1-877-263-2363

Comparison of 2010 Medical Plans and User Characteristics

Open Access

• Coverage for any provider, in and out of network, although cost is lower in-network

• Higher per-paycheck premiums, but with lower deductibles and therefore can have a lower cost overall

• Flexibility and freedom to choose doctors without needing a referral from a primary care physician

• Wants a plan with traditional deductibles and out of pocket costs

• Plans on using specialists on a regular basis

• Expects to see the doctor frequently throughout the year

• Willing to pay more per month for maximum flexibility and choice

Basic Choice

• Offers affordable choice with low per-paycheck premiums

• Emphasis on preventive care

• $35 co-pay for first 6 office visits

• Lab fees and x-rays covered in full to $500 before deductible has to be met

• No coverage for out-of-network providers

• $10 for generic prescriptions, otherwise a one-time $100 deductible must first be met for formulary name brand drugs or a one-time $300 for non-formulary

• Wants a basic plan with low monthly cost

• Does not visit the doctor often

• Wants coverage primarily for wellness (annual check up and tests) and for protection against a major accident or illness

• Uses generic drugs whenever possible

Kaiser HMO

(CA Only)

• Moderate employee contributions

• Low out-of-pocket maximums

• No annual deductible

• Choice of providers limited to those in their network

• No coverage for out-of-network providers

• No coverage for non-formulary drugs

• Little or no paperwork

• Wants to predict their medical costs

• Not sure how often they will need to see a doctor

• Is willing to give up choice of providers (doctors, hospitals, etc.) to achieve lower overall cost

• Likes minimal paperwork

Plan Characteristics User Characteristics

10www.SmileBrandsBenefits.com 1-877-263-2363

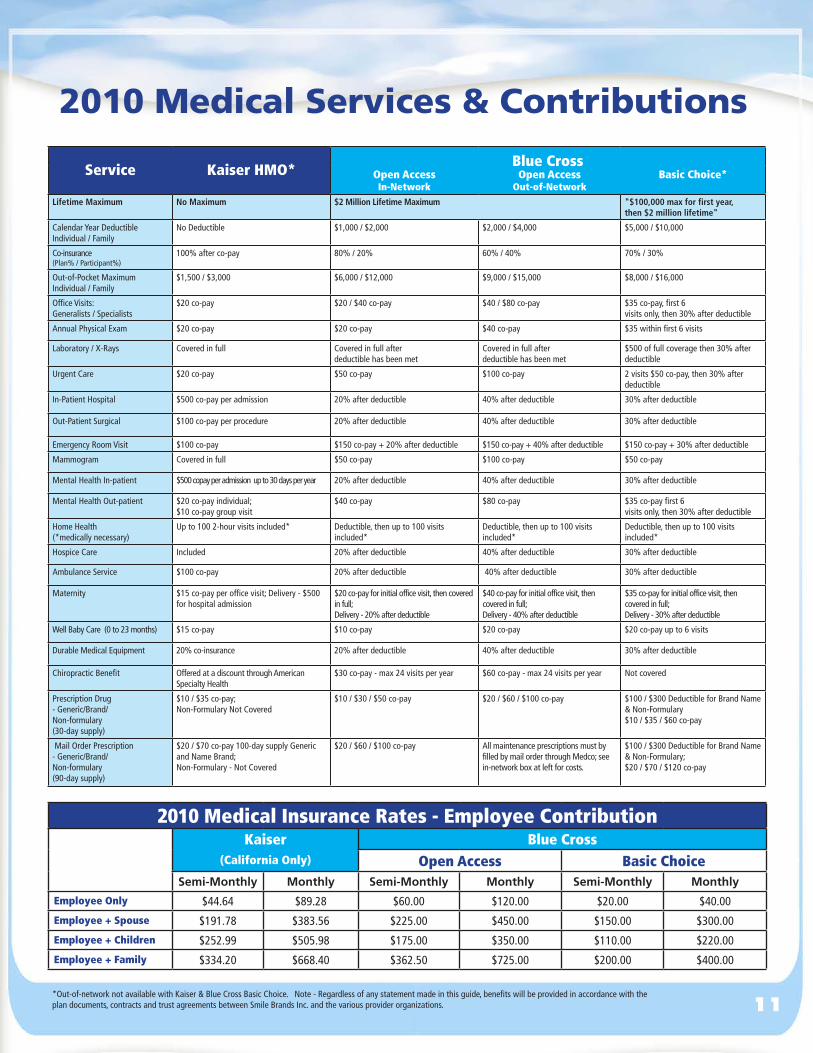

2010 Medical Insurance Rates - Employee ContributionKaiser Blue Cross

(California Only) Open Access Basic ChoiceSemi-Monthly Monthly Semi-Monthly Monthly Semi-Monthly Monthly

Employee Only $44.64 $89.28 $60.00 $120.00 $20.00 $40.00

Employee + Spouse $191.78 $383.56 $225.00 $450.00 $150.00 $300.00

Employee + Children $252.99 $505.98 $175.00 $350.00 $110.00 $220.00

Employee + Family $334.20 $668.40 $362.50 $725.00 $200.00 $400.00

Service Kaiser HMO* Blue CrossOpen Access In-Network

Open Access Out-of-Network

Basic Choice*

Lifetime Maximum No Maximum $2 Million Lifetime Maximum "$100,000 max for first year, then $2 million lifetime"

Calendar Year Deductible Individual / Family

No Deductible $1,000 / $2,000 $2,000 / $4,000 $5,000 / $10,000

Co-insurance(Plan% / Participant%)

100% after co-pay 80% / 20% 60% / 40% 70% / 30%

Out-of-Pocket Maximum Individual / Family

$1,500 / $3,000 $6,000 / $12,000 $9,000 / $15,000 $8,000 / $16,000

Office Visits: Generalists / Specialists

$20 co-pay $20 / $40 co-pay $40 / $80 co-pay $35 co-pay, first 6 visits only, then 30% after deductible

Annual Physical Exam $20 co-pay $20 co-pay $40 co-pay $35 within first 6 visits

Laboratory / X-Rays Covered in full Covered in full after deductible has been met

Covered in full after deductible has been met

$500 of full coverage then 30% after deductible

Urgent Care $20 co-pay $50 co-pay $100 co-pay 2 visits $50 co-pay, then 30% after deductible

In-Patient Hospital $500 co-pay per admission 20% after deductible 40% after deductible 30% after deductible

Out-Patient Surgical $100 co-pay per procedure 20% after deductible 40% after deductible 30% after deductible

Emergency Room Visit $100 co-pay $150 co-pay + 20% after deductible $150 co-pay + 40% after deductible $150 co-pay + 30% after deductible

Mammogram Covered in full $50 co-pay $100 co-pay $50 co-pay

Mental Health In-patient $500 copay per admission up to 30 days per year 20% after deductible 40% after deductible 30% after deductible

Mental Health Out-patient $20 co-pay individual; $10 co-pay group visit

$40 co-pay $80 co-pay $35 co-pay first 6 visits only, then 30% after deductible

Home Health (*medically necessary)

Up to 100 2-hour visits included* Deductible, then up to 100 visits included*

Deductible, then up to 100 visits included*

Deductible, then up to 100 visits included*

Hospice Care Included 20% after deductible 40% after deductible 30% after deductible

Ambulance Service $100 co-pay 20% after deductible 40% after deductible 30% after deductible

Maternity $15 co-pay per office visit; Delivery - $500 for hospital admission

$20 co-pay for initial office visit, then covered in full; Delivery - 20% after deductible

$40 co-pay for initial office visit, then covered in full; Delivery - 40% after deductible

$35 co-pay for initial office visit, then covered in full; Delivery - 30% after deductible

Well Baby Care (0 to 23 months) $15 co-pay $10 co-pay $20 co-pay $20 co-pay up to 6 visits

Durable Medical Equipment 20% co-insurance 20% after deductible 40% after deductible 30% after deductible

Chiropractic Benefit Offered at a discount through American Specialty Health

$30 co-pay - max 24 visits per year $60 co-pay - max 24 visits per year Not covered

Prescription Drug - Generic/Brand/ Non-formulary (30-day supply)

$10 / $35 co-pay; Non-Formulary Not Covered

$10 / $30 / $50 co-pay $20 / $60 / $100 co-pay $100 / $300 Deductible for Brand Name & Non-Formulary $10 / $35 / $60 co-pay

Mail Order Prescription - Generic/Brand/ Non-formulary (90-day supply)

$20 / $70 co-pay 100-day supply Generic and Name Brand; Non-Formulary - Not Covered

$20 / $60 / $100 co-pay All maintenance prescriptions must by filled by mail order through Medco; see in-network box at left for costs.

$100 / $300 Deductible for Brand Name & Non-Formulary; $20 / $70 / $120 co-pay

2010 Medical Services & Contributions

*Out-of-network not available with Kaiser & Blue Cross Basic Choice. Note - Regardless of any statement made in this guide, benefits will be provided in accordance with the plan documents, contracts and trust agreements between Smile Brands Inc. and the various provider organizations. 11

CoverageOur Dental Plan is easy to understand and has excellent coverage, still with no premium cost to you. All dental services are provided by a Smile Brands affiliated office.

Dental PlanThere are no employee premiums. Below are the patient’s

percentage share of the Usual & Customary Rate (UCR) schedule for these services, plus all lab fees at company cost.

Annual Maximum $10,000

Preventive Diagnostic Services - 10% of UCR - Oral Examinations - Fluoride Treatments - Prophylaxis - Oral Hygiene Instructions - X-rays, as needed - Sealants

Basic and Restorative Servcies by General Practitioners & Hygienists - 20% of UCR- Amalgam Fillings

- Composite Fillings - Temporary Crowns - Stainless Steel Crowns - Crown Build-up - Simple Tooth Extraction - Root Canals - Periodontal Procedures

Prosthodontic Services - 30% of UCR - Fixed - Crowns, Inlays & Onlays - Bridges - Removable Dentures - Partial Dentures

Specialty Services - 40% of UCR - Orthodontics- Oral Surgery - Periodontics - Endodontics - Pediatric Dentistry

Cosmetic Dentistry & Implant Services - 50% of UCR- All Porcelain and other top-tier Crowns - Veneers - Implant restorative/Prosthetics

IMPORTANT: to be eligible for coverage under the dental plan, you must elect coverage during open enrollment.

Dental Plan

12www.SmileBrandsBenefits.com 1-877-263-2363

Vision Care You asked and we listened!Smile Brands Inc. has partnered with the Blue Cross Vi-sion Network to provide one of the largest in-network provider groups for you to make a selection from. When you visit Blue Cross participating providers you pay only the co-payment for the vision examination and any amount over the plan designated allowance for materials. In most cases you will not be required to pay for these services up front. Participating physicians will invoice Blue View Vision for the covered balance and invoice you only for co-pays and balances over the covered amount.

You will now have a choice of 44,000 providers and provider locations to choose from. This includes thou-sands of independent providers, as well as retail pro-viders such as LensCrafters, Target Optical, JCPenney Optical, Sears Optical, and most Pearle Vision locations. If you choose an out-of-network provider you could be required to pay the full cost up front and then submit a claim to Blue View Vision for reimbursement.

To find a Blue View Vision Network participating provider go to www.smilebrandsbenefits.com or call 877-263-2363 and a Smile Brands Benefits Representative will be happy to search for a participating provider near you.

More on Vision Regular vision and eye examinations are important to your overall health.

Did you know that an estimated 11 million Americans have uncor-rected vision problems, ranging from refractive errors (near and far sightedness) to sight threatening disease? Whether your vision is 20/20 or less than perfect, everyone should receive regular vision care. Just like other health issues early detection of eye problems can help catch minor problems before they become major. Chances are you or a family member needs corrective eyewear.

Consider the following:• Vision problems are the second most prevalent health problem in the United States• One in four children has a vision problem that can interfere with learning• Eye diseases such as cataracts, glaucoma and macular degeneration are expected to triple in the next 30 years

13www.SmileBrandsBenefits.com 1-877-263-2363

Service Blue View Vision In-Network provider

Blue View Vision Care Out-of-Network Provider **

Frequency

Vision Exam $25 co-pay Full payment required up front for all services

Once every 12 months

Lenses Once every 12 months

Single Vision Covered in Full Up to $45 Once every 12 months

Bifocal Covered in Full Up to $ 65 Once every 12 months

Trifocal Covered in Full Up to $ 85 Once every 12 months

Lenticular Covered in Full Up to $85 Once every 12 months

Polycarbonate lenses for dependent children

Covered in Full Same as Single or Bi-focal lense benefit

Once every 12 months

Lens extras such as scratch resistant and anti-reflective coatings and progressives

Up to a 20% savings off retail price may be extended by provider

No discount

Frames Up to $120 Up to $120 Once every 24 months

Second pair (Frame Only) Up to 20% savings off retail price No coverage

Second pair (Frame and Lens)

Up to a 40% savings off retail price may be extended by provider

No discount

*Contact Lenses Up to $120 Elective / Up to $210 if visually necessary

Up to $120 Once every 12 months

* Instead of Frame and Lens benefit**An out-of-network provider is one not contracted with the vision insurance plan. Typically, if you visit a physician or other provider within the network, the amount you will be responsible for paying will be less than if you go to an out-of-network provider. Out-of-network pro-vider will also require payment up front for all services.

2010 Vision Plan Employee Rates Semi-Monthly Monthly

Employee only $4.00 $8.00 Employee + Spouse $6.35 $12.70 Employee + Children $6.48 $12.96 Employee + Family $10.46x $20.92

Vision Plan

14www.SmileBrandsBenefits.com 1-877-263-2363

Basic Life and AD&DThe company offers Basic Life and AD&D benefits at no charge to you. Both of these benefits are paid at one time your an-nual salary with a minimum of $30,000 and a maximum of $100,000. There is no enrollment needed.

Voluntary Life and AD&D These plans are underwritten by Principal. If you choose addi-tional life and AD&D benefits under this option, the premiums are your responsibility and are taken on an after-tax basis. If benefits need to be paid, they are tax free to the recipient. If you already have this coverage and do not want to make changes, you do not need to make an election. Unless other-wise changed by you, your 2009 coverage levels will automati-cally carry over to your 2010 elections.

The plan does offer a guaranteed acceptance by the carrier of three times annual salary to a maximum of $200,000. Any amount over that would need to be underwritten by the car-rier and will require evidence of insurability.

Spouse Voluntary Life and AD&D is available for up to one half of the employee’s option, to a maximum of $250,000. This plan offers a guaranteed acceptance by the carrier of $50,000; any amount over that would have to be underwritten by the car-rier and will require evidence of insurability.

Child Voluntary Life is available in two increments either $5,000 or $10,000. Both levels have guaranteed acceptance by the carrier.

Guaranteed acceptance is only available to those who are first time eligible.

Short Term Disability

This is a voluntary benefit that can help supplement your income; while disabled this plan can offer up to 60% of your pre-disability income for 90 days. The rates are based on your age and income and are deducted on an after-tax basis from your paycheck.

In states that offer a state disability program, this benefit will only supplement the state program to a total of 60% of your pre-dis-ability income and rates are reduced because of the lower benefit.

This coverage does not cover work-related injuries and must be underwritten by the carrier. Pre-existing condition clauses do apply.

If you already have this coverage and do not want to make changes, you do not need to make an election. Unless other-wise changed by you, your 2009 coverage will automatically carry over to your 2010 elections.

Long Term Disability

Basic LTD This coverage is company provided and provides a payment to you for 40% of your pre-disability income at no charge to you. No pre-existing conditions affect this coverage. The premiums for this coverage are paid for by Smile Brands.

Voluntary LTD This coverage is a voluntary supplement to the Basic LTD the company provides and allows coverage of up to 60% of your pre-disability income. The rates are based on your age and income and are deducted on an after-tax basis from your paycheck. This coverage does not cover work-related injuries and must be un-derwritten by the carrier. Pre-existing condition clauses do apply.

If you already have this coverage and do not want to make changes, you do not need to make an election. Unless other-wise changed by you, your 2009 coverage will automatically carry over to your 2010 elections.

Life & Disability Plans

15www.SmileBrandsBenefits.com 1-877-263-2363

www.SmileBrandsBenefits.com 1-877-263-2363

Some medical plan and insurance terms can be confusing. Here are some explanations of important medical benefits and insurance words and phrases. If you need further ex-planation, do not hesitate to consult with a Benefits Service Center representative at 1-877-263-2363.

Allowed Amount - Usually refers to the amount of payment a provider has agreed to accept for a service, treatment, or product under the terms of their negotiated contract with the insurance company. This can also refer to the maximum amount that Blue Cross will “allow” a provider to bill for a service, whether they are in or out-of-network.

Co-insurance – You and the medical plan share the cost of medi-cal procedures in a specified proportion after your deductible has been met. For example, after you have satisfied your deductible, you incur another medical bill for $1,000. With an 80% / 20% co-insurance, the plan will cover $800 and you will pay $200.

Co-pay(ment) – The set or fixed-dollar amount you are required to pay each time you use a particular medical service. Example: A co-payment for a doctor’s office visit would be $35 if you select the Basic Choice plan.

Deductible – The cumulative amount that you must pay annually before certain benefits will be paid by the plan. For example: Open Access has a $1,000 deductible, which means the plan will pay its portion of the co-insurance as agreed after you pay the first $1,000. Medical services that have a co-pay, such as a doctor’s office visit, are not subject to this deductible.

Exclusions – Conditions for which the medical plan will not pay; for example, cosmetic procedures are considered exclusions.

Formulary – A list of prescription drugs (both brand-name and generic medications) that are preferred by Medco, our phar-macy third-party administrator for the Basic Choice and Open Access plans. A prescription from the formulary list of medicines would be the first choice for treating a certain condition. A For-mulary may also be referred to as a Preferred Drug List.

In-Network – Providers such as private doctors, medical groups, urgent care centers, and hospitals that have contracted with an insurance company, such as Blue Cross, to provide their services at a pre-determined cost. The provider is a part of the Preferred Provider Organization or PPO.

Network Discount - The amount by which a provider’s bill is adjusted as a result of a negotiated rate covered under a negotiated contract between the provider and the insurer. The network discount term often appears on an Explanation of Benefits (EOB) statement, but it does not appear on all, since those forms vary by insurer. Insurers use many variations on this term including “Adjustment,” and others.

Common Medical Plan and Insurance Terms

Non-Formulary – Any prescription drug which is not on the current Formulary list of preferred medications. Non-Formulary prescriptions have higher co-pays than generic and name-brand drugs that are on the formulary list.

Out-of-Network – Providers who do not participate in the network used by your medical plan. Open Access plan partici-pants may still use these providers, but the co-insurance and other costs will be higher than if you use an in-network pro-vider. Basic Choice plan participants will pay for the full cost of a service if an out-of-network provider is used.

Out-of-Pocket Costs – The total you pay out of your pocket during a plan year either on an individual or family basis. These costs include the deductibles and co-insurance. Patient Responsibility - The amount that you owe the provider based on information sent from your provider to Blue Cross. This should include any co-payments, deductibles, co-insurance and/or excluded charges.

Pre-Existing Condition – A medical condition that required treatment during a fixed period of time, usually 3 to 6 months, before you purchased your insurance policy, such as Short Term Disability. For example, if you or your spouse is pregnant before you enroll for Short Term Disability, the pregnancy is considered a pre-existing condition and will not be covered.

Premium – The per-pay-period price you pay for your medical or other insurance plan.

Usual and Customary Rates (UCR) – Also called “Reasonable and Customary Charges”. This is the routine charge for a medical service performed by similar medical pro-viders in the same geographical area. You may pay an amount above the Usual and Customary charge if a provider charges more than other providers for the same service.

16

Flexible Spending Accounts (FSA)

This benefit program offers you a significant tax savings opportunity. It allows you to pay for eligible expenses using tax-free dollars – money taken from your paycheck before income and Social Security taxes have been calculated.

This benefit has two components:

Healthcare Reimbursement AccountThis account allows you to set aside pre-tax dollars to pay for certain out-of-pocket healthcare expenses such as deductibles, co-insurance, co-payments and certain over the counter medications and medical supplies. The maximum amount you can contribute for the plan year of 1/1/2010 through 12/31/2010 is $2,400.

Dependent Care Reimbursement AccountThis account allows you to set aside pre-tax dollars to help pay for day care services for your eligible dependents. The maximum amount you may contribute for the plan year of 1/1/2010 through 12/31/2010 is $5,000.

www.SmileBrandsBenefits.com 1-877-263-2363 17

The accounts you sign up for now are for expenses you incur between January 1 and December 31, 2010.

A Flexible Spending Account (FSA) is an excellent way to reduce your taxes and keep more of the money you earn. It works like an expense account. You automati-cally set aside a portion of your salary, before taxes, to pay for qualified medical expenses or child/dependent care. You save money because you don’t pay taxes on the money you set aside. You can use these accounts to pay for day care and your medical care and prescription drug costs that aren’t covered by insurance, as well as some over-the-counter medicines and drugs.

Getting money from your account is simpleYou will have online access 24/7 to check your bal-ance and status of claims. With the debit card you can pay your provider directly from your account. Or you can submit expenses through fax, mail or e-mail. Once received, HealthComp, our FSA third party administrator, will process your claim and send you a check.

Health Care Flexible Spending Account Dependent Care Flexible Spending AccountIf you’re married and you file a joint return, or you file a single or head of household return, the annual IRS limit is $5,000. If you’re married and file separate returns, you can each elect $2,500 for the calendar year. To qualify, you and your spouse must be employed, or your spouse must be a full-time student.

Eligible Expenses• Prescription medicines and drugs• Hearing aids• Orthopedic goods, prosthetic devices• Doctors• Dentists, orthodontists• Osteopaths• Chiropractors• Optometrists, ophthalmologists, opticians • Chiropodists, podiatrists • Eyeglasses• Over-the-counter medicines and drugs• Nursing and personal care facilities• Hospitals• Medical and dental laboratories• Medical services and health practitioners• Ambulance services, equipment and supplies

View a full list of eligible medical expenses, and information about using the FSA debit card to pay for these expenses, at HealthComp.com.

A Dependent Care Flexible Spending Account is a simple way to save money on quality day care for your loved ones. It allows you to set aside pre-tax dollars to pay for these expenses.

If you’re married and you file a joint return, or you file a single or head of household return, the annual IRS limit is $5,000. If you’re married and file separate returns, you can each elect $2,500 for the calendar year. To qualify, you and your spouse must be employed, or your spouse must be a full-time student.

Eligible Dependents• Children under age 13 who are claimed as a dependent for tax purposes• Disabled spouse or disabled dependent of any age

Ineligible Expenses• Costs claimed as a dependent care tax credit on your tax return• Services provided by one of your dependents• Expenses for nighttime baby sitting• Baby sitting payments to your own dependents under age 19• Expenses paid for schooling, kindergarten and above

You may receive reimbursement up to the current balance in your account at the time the request is made. As additional contributions are received, eligible claim amounts not yet paid will be issued to you automatically.

Use It or Lose It!If this is your first time using an FSA, be conservative in your estimate of how much you think you’re going to spend for either medical or dependent care expenses. The IRS has a “use it or lose it” rule which states that you must forfeit any FSA balances not used by the end of the plan year. If you still have

a healthcare balance in December, move up those January appointments to the optometrist or other healthcare provider to incur the cost before the end of the year. You have 90 days following the end of the year to submit claims incurred in 2010 to HealthComp.

Keep More of Your

Money!You may be able to save 20% or more by enrolling in a Flexible Spending Account

• Lower your medical costs • Cut your income taxes

18www.SmileBrandsBenefits.com 1-877-263-2363

Estimate your Out-of-Pocket Costs for Health Care

A Flexible Spending Account is an excellent way for you to pay

for health care expenses with pre-tax dollars. This work-

sheet will assist you in estimating the out-of-pocket medical

expenses that you and your family expect to incur during the

plan year. Reviewing the expenses you had this year will give

you a good indication of what your expenses might be for the

new plan year. Also with the availability of a debit card your

funds are easier to access.

Last Year Estimated This Year

Medical deductible

Medical co-payments

Medical co-insurance

Prescription medication co-payments

Dental co-payments

Vision co-payments and dispensary costs

Hearing aid expense

Over-the-counter medications

Other eligible healthcare expenses

Total Expenses:

• Keep in mind when determining how much to contribute to your Medical Flexible Spending account that federal law requires that you forfeit any funds remaining in your account at the end of your plan year. You can access the

list of eligible medical expenses from the Benefits web-site, www.SmileBrandsBenefits.com. Find more informa-tion on FSAs on page 18.

The Hidden Tax BreakDid you know that your Smile Brands premiums for medical and

vision are deducted from your paycheck on a pre-tax basis? They

help lower the amount of your overall total taxable earnings in

much the same way as a Flexible Spending Account. The less of

your pay that the IRS sees as taxable, the more that stays in your

pocket! For a bigger tax break, consider contributing to a health

care or dependent care Flexible Spending Account.

FSA HealthcareWorksheet

19www.SmileBrandsBenefits.com 1-877-263-2363

20

?Did You Enroll for a New Flexible Spending Account? Access Your Flexible Spending Account Quickly with the FSA Debit Card!Now that you’ve decided to contribute to a Flexible Spend-ing Account (FSA) to gain a significant tax advantage on what you spend for healthcare or dependent care, the next thing to do is make it fast and easy to access this benefit. Normally, you would pay for eligible expenses, such as pre-scriptions and co-pays, at the time you make the purchase or receive service, then submit a paper FSA claim form to HealthComp to be reimbursed. For the low cost of $1 per month, which is deducted from your FSA account, you can save time and eliminate the cost of postage to mail a claim for most of your purchases.

Instead of paying first and getting reimbursed, you simply use your debit card for payment at the time of service, such as a doctor’s office visit co-payment, or when purchasing eligible over-the-counter items or prescription drugs. The payment is debited directly from your Flexible Spending Account, without you sending a paper claim form or waiting for reimbursement. You can do the same with dependent care providers, as long as they accept MasterCard and you have signed up for a Dependent Care FSA.

The IRS Requires Verification Since there is no claim form with receipts attached when you use a debit card, how will the IRS know that the pur-chase you made on your debit card was for an eligible expense? HealthComp, our FSA administrator, will auto-matically verify transactions wherever it can. Co-payments to doctors’ offices and hospitals, for example, are usually auto-approved, as are recurring transactions that have

been previously substantiated. Pharmacies want eligible expenses made in their stores auto-approved as well. Most pharmacy chains employ an electronic data interface called Inventory Information Approval System to do just that. This system sends HealthComp information on the purchase as quickly as it prints the data onto a receipt, eliminating the need to submit receipts to HealthComp.

Despite this ability to auto-approve most transactions charged to your FSA debit card, occasionally a payment will not be auto-verified. When this occurs, HealthComp will send you a letter requesting receipts for one or more past transactions made on the card. That’s why it’s important that you keep your itemized receipts and provide a copy to HealthComp if requested. This can be mailed, faxed, or scanned and e-mailed. If a requested receipt is not submit-ted promptly, HealthComp may have to suspend the use of your card to protect the plan for other plan participants. The IRS conducts periodic audits at HealthComp to ensure their administration of the FSA benefit is in compliance with IRS regulations.

Need Help With Your New FSA? We’re Here for You!Whenever you are not sure how much is left in your ac-count, just go to our benefits website (www.SmileBrands-Benefits.com) and click on the FSA page. You will be shown how to access your individual account and check your bal-ances. Whenever you have a question regarding your FSA, contact one of our Benefits Service Center representatives at 1-877-263-2363. We will be happy to help you get the most out of your FSA benefit.

www.SmileBrandsBenefits.com 1-877-263-2363

What other Perks are Available to Employees and Affiliates?Besides a paycheck and a great place to work, we offer discounts on:

• Movie and theme park tickets through Working Advantage• Cellular service through Verizon Wireless• Personal computers directly from Dell• Office Depot office supplies• Weight loss with Weight Watchers• Will preparation services with ARAG Services• Laser Vision correction through National Lasik Network• Hearing aids through American Hearing Benefits (AHB) Inc.

More discounts are provided through Anthem/Blue Cross or Kaiser.

Please click on the My Perks tab on www.SmileBrandsBenefits.com for updates and additional discount opportunities.

Life’s Ups and Downs Employee Assistance ProgramWhether dealing with issues large or small, everyone can use a helping hand once in a while. An Employee Assistance Program (EAP) from Magellan Health Services is available for dealing with issues including family matters, divorce and stress manage-ment, as well as providing resources on parenting, safety and community services. You and your family members can call 800-450-1327 for telephonic assistance or access the Magellan website at www.MagellanHealth.com.

Tobacco CessationQuitting tobacco use can lower your risk of heart attack, lung cancer and emphysema. The American Cancer Society’s telephone-based cessation counseling program, Quitline®, connects you with a trained cessation counselor, who will send you materials to help you prepare to quit, plus learn about additional programs and resources to help. Whether you smoke or use chewing tobacco, studies have shown this service nearly doubles your chances of quitting successfully.For more information call 877-ACS-0110 and mention the Principal Life pass code: EDGE

Grief Support ServicesEveryone grieves in a unique way and coping with loss can be very difficult. Grief Support Services from Magellan Health Services offers access to licensed professionals providing confidential guidance and helpful strategies to beneficiaries needing emotional support. Legal services are also available.

Dependents and Beneficiaries can call 800-274-4529 or visit www.MagellanHealth.com.

Employee Perks

21www.SmileBrandsBenefits.com 1-877-263-2363

To enroll Online follow these steps:

Log on to the Smile Brands Benefits Service Center websiteat www.SmileBrandsBenefits.com and follow the prompts. You can also find a link to this web site on BrightNet; look in the left naviga-tion column under BN!D links.

Click on the login button. The username is: SmileBrands The password is Smiles.

Click on the “My Enrollment” tab.

When you click on “Enroll” you will see the screen below:

– Your Login ID is: BNDI + your employee ID number

– Your Password is your birth date in this format: MMDDYYYY

– After logging in, you will be prompted to change your password.

Click on the “2010 Step by Step Benefits Enrollment” link andfollow each step. You must elect or decline each line of coverage.Please check your Enrollment Confirmation carefully before exiting the online benefits system. If you see a problem or want tomake a change, simply go back to the benefits section and modifyyour election. When you are finished, print your BenefitsEnrollment Confirmation.

To enroll By Phone follow these steps:

Call 1-877-263-2363 and press option #1 to speak to a Smile Brands Service Representative. A representative will be able to take your enroll-ment elections and enroll you by phone. As verification, you will receive a confirmation of enrollment in the mail.

Watch for Your NEW Benefits ID Card

By the second week in January, you will

receive a benefits identification card from

HealthComp. If you are enrolled in Open Ac-

cess, Basic Choice, Dental or Vision. Kaiser will

not issue new cards for existing participants.

Detailed Benefits Documents Available Online The benefit descriptions found in this guide

have been prepared to help you understand

your Smile Brands Inc. benefits choices. As

summaries, these descriptions only highlight

the main characteristics of each plan. You

can find more detailed descriptions of the

plans in your Summary Plan Descriptions and

in the materials supplied by the providers.

Regardless of any statement made in this

guide, benefits will be provided in accordance

with the plan documents, contracts and trust

agreements between Smile Brands Inc. and the

various provider organizations.

There are two enrollment Options to choose from:

After reading about the benefit offerings for 2010 and their new premium costs, if you do not wish to make any changes, you do not have to do anything. With the exception of Flexible Spend-ing Accounts (FSAs), your current plan selections will automatically roll over for use next year. FSAs, however, do not automatically renew. You must re-elect an amount to contribute to your FSA every year.

![Smile Inc Dental Surgeons Pte Ltd v Lui Andrew Stewart · Smile Inc Dental Surgeons Pte Ltd v Lui Andrew Stewart [2012] SGCA 39 Case Number :Civil Appeal No 145 of 2011 Decision Date](https://img.pdfslide.net/doc/110x75/612e78591ecc51586942d589/smile-inc-dental-surgeons-pte-ltd-v-lui-andrew-stewart-smile-inc-dental-surgeons.jpg)