Embed Size (px)

Citation preview

Social Class and Commercial

Bank Credit Card Usage

H. LEE MATHEWS

and

JOHN W . SLOCUM, JR.

Relationships between anindividual's social class andhis purchasing behavior inusing a connnnercial bankcredit card are described inthis article. Important card-use patterns with market seg-mentation implications werefound. Membership in asocial class influences pat-terns of credit card usage.Convenience and installmentuse of cards tend to vary bysocial class in a manner con-sistent with previous studiesof social class behavior pat-terns.

Journal of Markettng. Vol. 33 (Jmniuur.1M9). pp. 71-78.

/CONSUMER behavior models virtually always emphasize social^-^ class and income as variables affecting purchases.^ PierreMartineau suggested that social class is often more important thanincome in influencing purchasing behavior:

While income has generally been the most widely used be-havioral indicator in marketing, social class membership pro-vides a richer dimension of meaning. The individual's con-sumption pattern actually s.vmbolizes his class position, a moresignificant determinant of his buying behavior than justincome.-Recently, the concept of consumer credit has been expanded.' As

the consumer has become a more sophisticated shopper, credit hasplayed an increasing role in facilitating the acquisition of goodsand services. Similarly, a greater number of retail and financialinstitutions are realizing that providing credit service is a meansof reaching new market segments. Yet, social class membershiphas not been the subject of detailed analysis in understanding con-sumer credit. This study examines how a consumer's social classmembership affects his use of one type of credit instrument—thecommercial bank credit card. Implications of the study may gobeyond credit cards to other applications of the marketing of creditservice. For example, promotional materials can be better directedtowards appropriate market segments utilizing the convenience-installment classification suggested in this article.

Research

The results of a mail questionnaire study conducted in a largeeastern metropolitan area follow. A random sample of 4,316 credit

' See, for example, John A. Howard, Marketing Management: Analysisand Planning, Revised Edition (Homewood, Illinois: Richard D. Irwin,Inc., 1963) and "A Theory of Buyer Behavior" (unpublished manu-script, 1968) ; Francesco Nicosia, Consumer Decision Processes(Englewood Cliffs, New Jersey: Prentice-Hall, Inc., 1966); PhilipKotler, "Behavioral Model for Analyzing Buyers," JOURNAL OF MAR-KETING. Vol. 29 (October, 1965), pp. 37-45, and "Mathematical Modelsof Individual Buyer Behavior," Behavioral Science, Vol. 13 (July,1968), pp. 274-278.

- Pierre Martineau, "Social Classes and Spending Behavior," JOTTRNALOF MARKETING, Vol. 23 (October, 1958), p. 121.

3 Robert Bartels, "Credit Management as a Marketing Function,"JOURNAL OF MARKETING, Vol. 28 (July, 1964), pp. 59-61, and PhilipKlein and Geoffrey Moore, Quality of Consumer Installment Crectit(New York: National Bureau of Economic Research, Studies inConsumer Installment Financing, 1967).

71

72 Journal of Marketing, January, 1969

card holders was drawn from the files of a largecommercial bank and a questionnaire mailed to eachbank credit card holder. Of the 2,187 returnedquestionnaires, a total of 1,896 were usable. Theinitial questionnaire resulted in 1,615 returns, whilethe follow-up letter and questionnaire resulted in anadditional 572 questionnaires. A chi-square analysisindicated that the two samples were not significantlydifferent at the .025 level.

A two-factor index of social position combiningoccupation and education was used in this study tomeasure an individual's social class membership.^Occupation is presumed to reflect the skill and powerindividuals possess as they perform the many main-tenance functions in society. Education is be-lieved to reflect not only knowledge but also culturaltastes. This instrument, therefore, measures socialclass without taking income into consideration.

Major Concepts and DefinitionsThe two-factor social position index divides so-

ciety into five status structures. The hierarchyranges from the low status evaluation of unskilledphysical labor to the more prestigious use of skilland the manipulation of men.

Lower Class and Lower Middle Class

The lower social classes tend to be oriented locallyin outlook and emphasize relatively short horizonsand considerations. Immediate gratifications andreadiness-to-express impulses are observed. Occu-pations require little skill and education, forexample, taxi drivers, car washers, and janitors.

Middle Class

The middle class is oriented to a functional andpragmatic view. This gives them a larger per-spective than found in the lower class and rein-forces the importance of deferring gratificationsin favor of long-range goals. Included are book-keepers, small business owners, and minor pro-fessionals.

Upper Middle Class and Upper Class

The upper classes embody the intellectual, profes-sional, and managerial personnel, for example,executives, lawyers, and doctors. They tend tointegrate a variety of means to satisfy their aims,and concern themselves with individuality andachievement. Such people are highly trained andare responsible for decisions affecting otherpersons.Card use was studied by analyzing the bank's

credit card records over a 28-month period be-ginning in 1966. Two classifications of card usewere developed. A card holder who elected to pay

an amount less than the balance and pay interestcharges on the unpaid balance was classified as aninstallment user. A card holder who paid his balancewithin the billing cycle was considered to beusing the card in lieu of cash as a convenience fi-nance instrument, and these card holders have beendefined as convenience users.

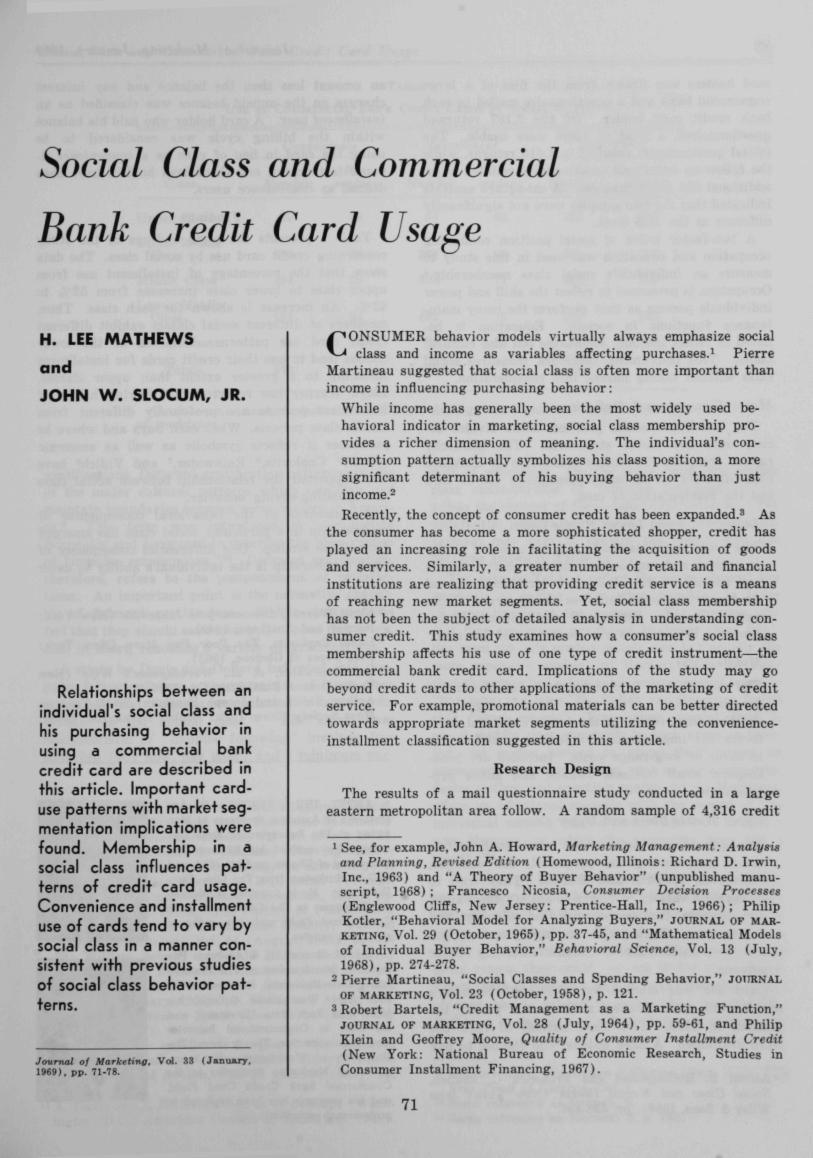

FindingsTable 1 presents the basic findings of the study

concerning credit card use by social class. The datashow that the percentage of installment use fromupper class to lower class increases from 52% to82 "Tf. An increase is shown for each class. Thus,members of different social classes exhibit difTerentcredit card use patterns. Members of the lowerclasses tend to use their credit cards for installmentfinancing to a greater extent than upper classes.Lloyd Warner has reported that buying habits oflower-class persons are profoundly different frommiddle-class persons. What each buys and where hepurchases it reflects symbolic as well as economicvalues."' Caplovitz," Rainwater," and Vidich** havealso supported the relationship between social classand spending-saving behavior.

A consensus of the behavioral consequences ofmembership in a particular social class has emergedfrom these studies. One differential consequence ofclass membership is the individual's ability to defer

^ Lloyd Warner, Democracy in JonesvUle (New York:Harper and Brothers, 1949).

"David Caplovitz, The Poor Pay More (New York:Free Press of Glencoe, 1963).

'Lee Rainwater, et al.. Work ing man'8 Wife (NewYork: Oceana Publishing Co., 1959).

>* Arthur Vidich and Joseph Bensman, Small Town inMass Society (New York: Anchor Books, Inc., 1960).

Alfred B. Hollingshead and Frederick C. Redlich,Social Cla88 and Mental Illne88 (New York: JohnWiley «St Sons, 1958), pp. 398-407.

• ABOUT THE AUTHORS. H. LeeMathews is Assistant Professor of Mar-keting at The Pennsylvania State Uni-versity. He received his BS from TheUniversity of Illinois, and his MBA andPhD in Marketing from The Ohio StateUniversity. He is coauthor ol Market-ing Strategies in The Commercial BankCredit Card Field and has authorednumerous articles.

John W. Slocum. Jr.. is Assistant Pro-fessor of Management at The Pennsyl-vania State University. He received hisBBA from Westminster College, hisMBA from Kent State University, andhis DBA in Organizational Behaviorand Administrative Theory from TheUniversity of Washington. He is co-author of AfarJcetJng Strategies in (heCommercial Bank Credit Card Field,and his research has been reported inprofessional periodicals.

Social Class and Commercial Bank Credit Card Usage 73

TABLE 1

U S E OF COMMERCIAL BANK CREDIT CARDS BY SOCIAL CLASS*

SocialClass

Upper Class

Upper MiddleClass

Middle Class

Lower MiddleClass

Lower Class

Totals

Convenience

Number

89

158

154

152

21

574

Per-centage

48

38

29

24

18

Installment

Number

97

263

381

492

89

1,322

Per-centage

52

62

71

76

82

Row

Number

186

421

636

644

110

1,896

Total

Per-centage

100

100

100

100

100

'A chi-square analysis indicates that these findings are significant at the .001 levelof confidence.

gratifications. Deferred gratification patterns are oneof the major cultural patterns which establish andmaintain boundaries between social classes in Ameri-ca.'* This term was introduced by sociologistsSchneider and Lysgaard to describe the phenomenonof "impulse renunciation.">" Deferred gratification,therefore, refers to the postponement of satisfac-tions. An important point is the normative charac-ter of deferred gratification. Middle class personsfeel that they should save money, postpone purchases,and, in short, renounce a variety of gratifications.

A study by Davis and Dollard indicated that "im-pulse following" was a characteristic of lower classpeople and that "impulse renunciation" was a charac-teristic of the middle class.'> The lower classcharacteristic of "impulse following" involves freespending (buy now, pay later) and a minimum pur-

» For example, see Murray S. Straus. "Deferred Gratifi-cation, Social Class, and the Achievement Syndrome,"American Sociological Review, Vol. 27 (June. 1962).pp. 325-335; Richard P. Coleman, "The Significanceof Social Stratification in Selling," in Marketing: AMature Discipline, Martin L. Bell, editor (Chicago,Illinois: American Marketing Association, 1961), pp.171-184; Harry Beilin, "The Pattern of Postponabili-ty and Its Relation to Social Class Mobility," Journalof Social Psychology, Vol. 44 (August, 1956), pp. 33-48; William Sewell, Archibald Haller, and MurrayStraus, "Social Status and Educational and Occupa-tional Aspiration," American Sociological Review,Vol. 22 (February, 1957), pp. 67-73; and Alfred Hol-lingshead, Elmtown's Youth (New York: John Wileyand Sons, 1949).

10 Louis Schneider and Sverre Lysgaard, "The DeferredGratification Pattern: A Preliminary Study," Ameri-can Sociological Review, Vol. 18 (March, 1953), pp.142-149.

11 A. Davis and J. Dollard, Children of Bondage (Wash-ington, D.C: American Council on Education, 1948).

suit of education. On the other hand, the middleclass characteristic of "impulse renunciation" in-volves the reverse of these behavioral patterns. Thedifferential pattern with respect to gratification de-ferment may help to explain the credit card usepatterns shown in Table 1.

The data in Table 1 reflect the lower classes' lowemphasis on saving (even when possible) in favorof expenditures at the moment. For example, thefact that appliances purchased by lower class fami-lies were not only predominately new but usually themore expensive models, led Herbert Gans to implythat this class had a low sales resistance and tends to"buy now. pay later."'- Vidich and Bensman foundthat "shack people" (lower class people) tend toreject middle class standards in such areas as hous-ing and prefer instead to spend their money onimmediate needs and fancies, such as car accessories,flashy clothes, and sporting equipment.'* Martineauoffers an additional example with the record of "anindividual earning $200 a month who . . . bought anew Mercury on which the payments were $96 amonth."'*

On the other hand, the upper classes have a great-er tendency than the lower classes toward con-venience use. This result supports the theory ofdeferred gratification. That is, while upper classeswould not use credit for installment purposes, thereis no reason they could not use it for convenience.Thus, there is certainly an indication that the natureof card use is related to social class membership.Different social classes refiect different values, and

12 Herbert Gans, The Urban Villagers (New York: TheFree Press of Glencoe, 1962).

13 Same reference as footnote 9.1* Same reference as footnote 2, p. 150.

74 Journal of Marketing, January, 1969

TYPE OF CONSUMER GOODS

I. Appliancat

2. Furnitura

3. Clothing

4 Educotion*

iff5. Gasolin*

6 SewingMachine

7. Medical^Expenses

8. Gifts*

9. Luggage*

I 0. SportingGoods^

I I. Jewelry*

12. Restaurants*

13. Boats*

14. Furs*

15. Entertoinment

16. Groceries*

17 Hobbies

18. Vacations*

19. SwimmingPool*

20 Antiques*

Dotted line signifies convenienceusers attitudes ( - - — )

Solid iinesignifies installmentusers attitudes ( )

10 20 30 40 50 60 70

Percentage Favorable80 90 100

1. Favorable attitudes toward buying consumer goods on credit.

'Attitudes differ Bignificantly by social class: upper class more favorable.

these differences are manifested in consumer buyingbehavior.

Acceptable Consumer Goods to Charge with aCommercial Bank Credit Card

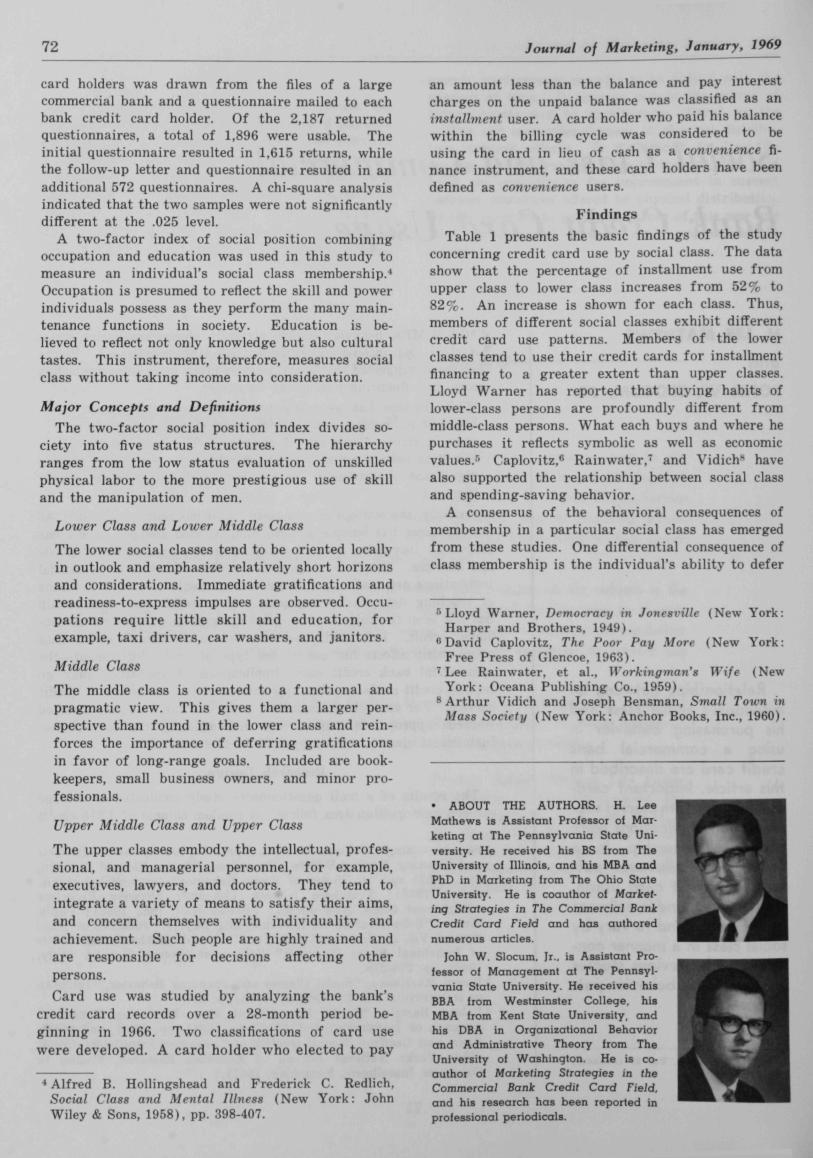

One of the most important marketing aspects of acredit service is to determine what merchandiseand or services the consumer considers chargeable.Once a group of goods has been identified as a po-tential market, the credit-granting institution has aframe of reference within which to plan and developits marketing strategies. The data pertaining towhich good (s) is acceptable to buy with credit arepresented in Figure 1. The data show that the ma-jority of card users favor purchasing goods such asappliances, furniture, clothing, and gifts on credit.

Individuals appear to feel that it is acceptable topurchase consumer durable goods, some "necessi-ties," and services, such as education and medicalexpenses, with credit. Fewer commercial bank creditcard users find it acceptable to purchase items likefurs, meals in restaurants, vacations, and antiqueson credit.

These same people do not feel that an individualneed go into debt to purchase "luxury goods." Thesefindings parallel those of George Katona at theUniversity of Michigan. Katona's research showsthat the majority of consumers in all social strataconsider credit buying a good idea; only about athird indicate that it is a "bad idea.'''^

Figure 1 also shows that some differences in ac-ceptable items to charge were found between con-

Social Class and Commercial Bank Credit Card Usage 75

.o

ISO

140

130

120

I 10

100

90

80

70

60

50

40

30

20

10

0

Installment users =

Convenience users =

NN•A

2 4 6 8 10 12 14 16 18 20 22 24 26 28

Number of Months

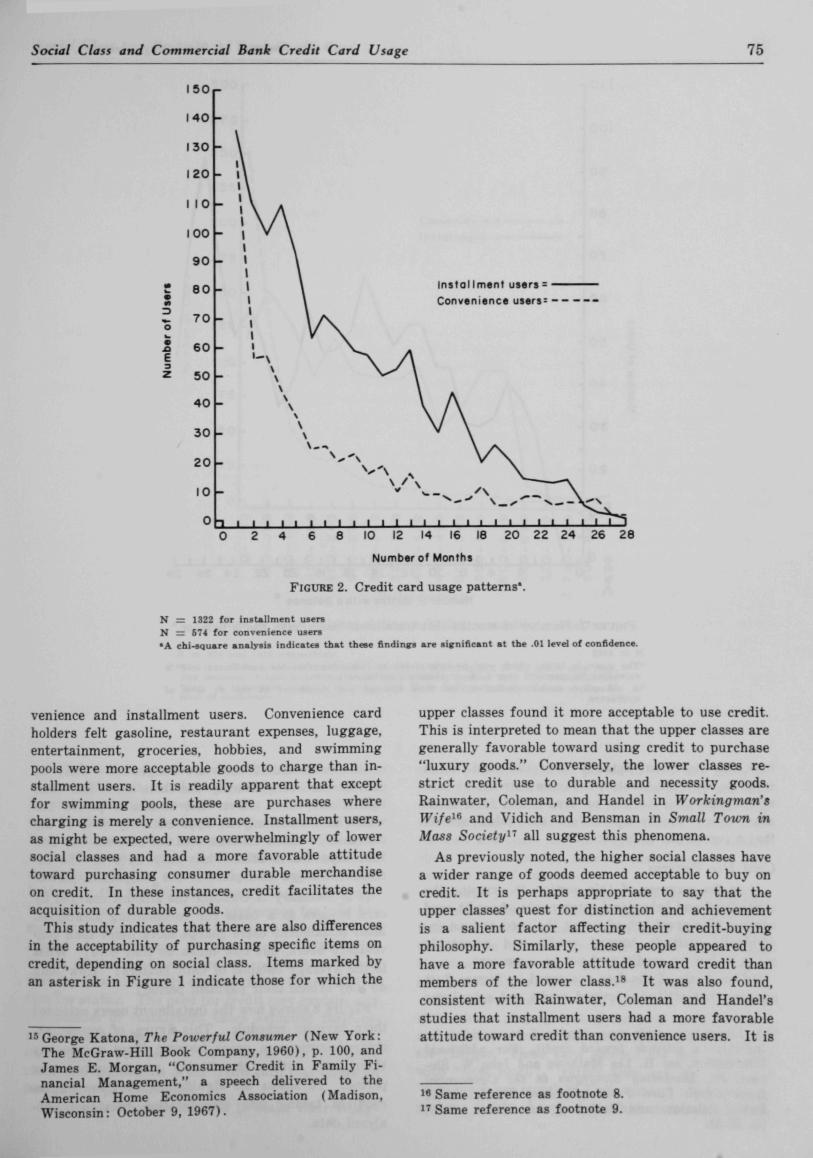

FIGURE 2. Credit card usage patterns'.

= 1322 for inaUllment usere— 674 for convenience userschi-square analysis indicates that these findings are significant at the .01 level of confidence.

venience and installment users. Convenience cardholders felt gasoline, restaurant expenses, luggage,entertainment, groceries, hobbies, and swimmingpools were more acceptable goods to charge than in-stallment users. It is readily apparent that exceptfor swimming pools, these are purchases wherecharging is merely a convenience. Installment users,as might be expected, were overwhelmingly of lowersocial classes and had a more favorable attitudetoward purchasing consumer durable merchandiseon credit. In these instances, credit facilitates theacquisition of durable goods.

This study indicates that there are also differencesin the acceptability of purchasing specific items oncredit, depending on social class. Items marked byan asterisk in Figure 1 indicate those for which the

'George Katona, The Powerful Consumer (New York:The McGraw-Hill Book Company, 1960), p. 100, andJames E. Morgan, "Consumer Credit in Family Fi-nancial Management," a speech delivered to theAmerican Home Economics Association (Madison,Wisconsin: October 9, 1967).

upper classes found it more acceptable to use credit.This is interpreted to mean that the upper classes aregenerally favorable toward using credit to purchase"luxury goods." Conversely, the lower classes re-strict credit use to durable and necessity goods.Rainwater, Coleman, and Handel in Workingman'sU'l/e'* and Vidich and Bensman in Small Tovm inMass Society^' all suggest this phenomena.

As previously noted, the higher social classes havea wider range of goods deemed acceptable to buy oncredit. It is perhaps appropriate to say that theupper classes' quest for distinction and achievementis a salient factor affecting their credit-buyingphilosophy. Similarly, these people appeared tohave a more favorable attitude toward credit thanmembers of the lower class.'* It was also found,consistent with Rainwater, Coleman and Handel'sstudies that installment users had a more favorableattitude toward credit than convenience users. It is

Same reference as footnote 8.Same reference as footnote 9.

76 Journal of Marketing, January, 1969

3Z

f 10

100

90

eo

70

60

50

40

30

20

10

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Number of Months with a Balance

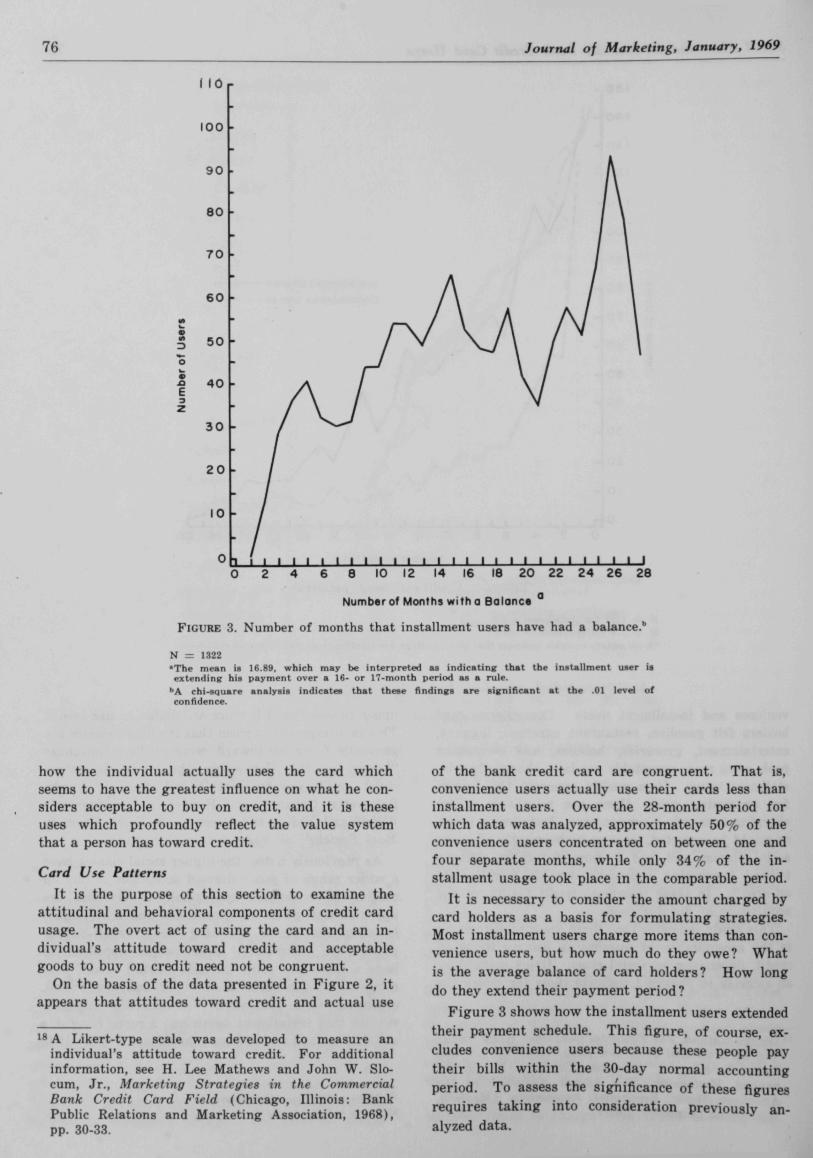

FIGURE 3. Number of months that installment users have had a balance.''

N = 1322*The mean is 16.89. which may be interpreted as indicatinK that the installment user isextending his payment over a 16- or 17-month period as a rule.

''A chi-square analysis indicates that these findings are significant at the .01 Ievei ofconfidence.

how the individual actually uses the card whichseems to have the greatest influence on what he con-siders acceptable to buy on credit, and it is theseuses which profoundly refiect the value systemthat a person has toward credit.

Card Use PatternsIt is the purpose of this section to examine the

attitudinal and behavioral components of credit cardusage. The overt act of using the card and an in-dividual's attitude toward credit and acceptablegoods to buy on credit need not be congruent.

On the basis of the data presented in Figure 2, itappears that attitudes toward credit and actual use

A Likert-type scale was developed to measure anindividual's attitude toward credit. For additionalinformation, see H. Lee Mathews and John W. Slo-cum, Jr., Marketing Strategie8 in the CommercialBank Credit Card Field (Chicago, Illinois: BankPublic Relations and Marketing Association, 1968),pp. 30-33.

of the bank credit card are congruent. That is,convenience users actually use their cards less thaninstallment users. Over the 28-month period forwhich data was analyzed, approximately 50% of theconvenience users concentrated on between one andfour separate months, while only 34% of the in-stallment usage took place in the comparable period.

It is necessary to consider the amount charged bycard holders as a basis for formulating strategies.Most installment users charge more items than con-venience users, but how much do they owe? Whatis the average balance of card holders? How longdo they extend their payment period?

Figure 3 shows how the installment users extendedtheir payment schedule. This figure, of course, ex-cludes convenience users because these people paytheir bills within the 30-day normal accountingperiod. To assess the significance of these figuresrequires taking into consideration previously an-alyzed data.

Social Class and Commercial Bank Credit Card Usage 77

2 7 5

2 50

2 2 5

2 0 0

1 75

150

125

100

75

5 0

25

0

11

• \

\

\

"

1\

• \

\

A

T 1

\

\ A\ V V\\\\\\\\_N

" " ^ ^ ^

1 1 1 1

Convenience =

\ / \\y \^ \\\\\1 1 1 1 1 1 r ~ i — i ~ - i - - i — 1

a>CO— — c M o j i o i o ^ ^ m i o ( 0 < o N

I I I I I I I I I I I I I I I I I

O O O O O O O O O O O O O O O O O O

Dollar Amountt ^

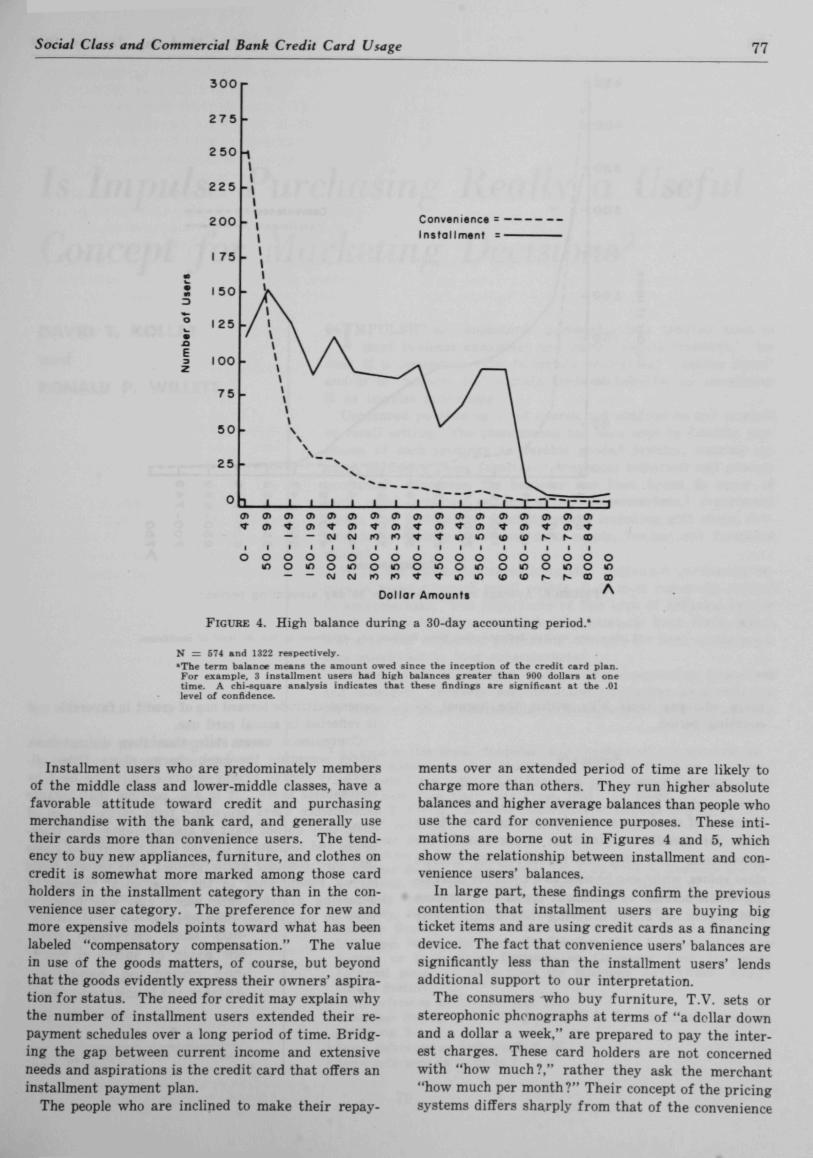

FiGimE 4. High balance during a 30-day accounting period.*

N = 574 and 1322 respectively.•The terra balance means the amount owed since the inception of the credit card plan.For example, 3 installment users had high balances greater than 900 dollars at onetime. A chi-square analysis indicates that these findings are significant at the .01level of confidence.

Installment users who are predominately membersof the middle class and lower-middle classes, have afavorable attitude toward credit and purchasingmerchandise with the bank card, and generally usetheir cards more than convenience users. The tend-ency to buy new appliances, furniture, and clothes oncredit is somewhat more marked among those cardholders in the installment category than in the con-venience user category. The preference for new andmore expensive models points toward what has beenlabeled "compensatory compensation." The valuein use of the goods matters, of course, but beyondthat the goods evidently express their owners' aspira-tion for status. The need for credit may explain whythe number of installment users extended their re-payment schedules over a long period of time. Bridg-ing the gap between current income and extensiveneeds and aspirations is the credit card that offers aninstallment payment plan.

The people who are inclined to make their repay-

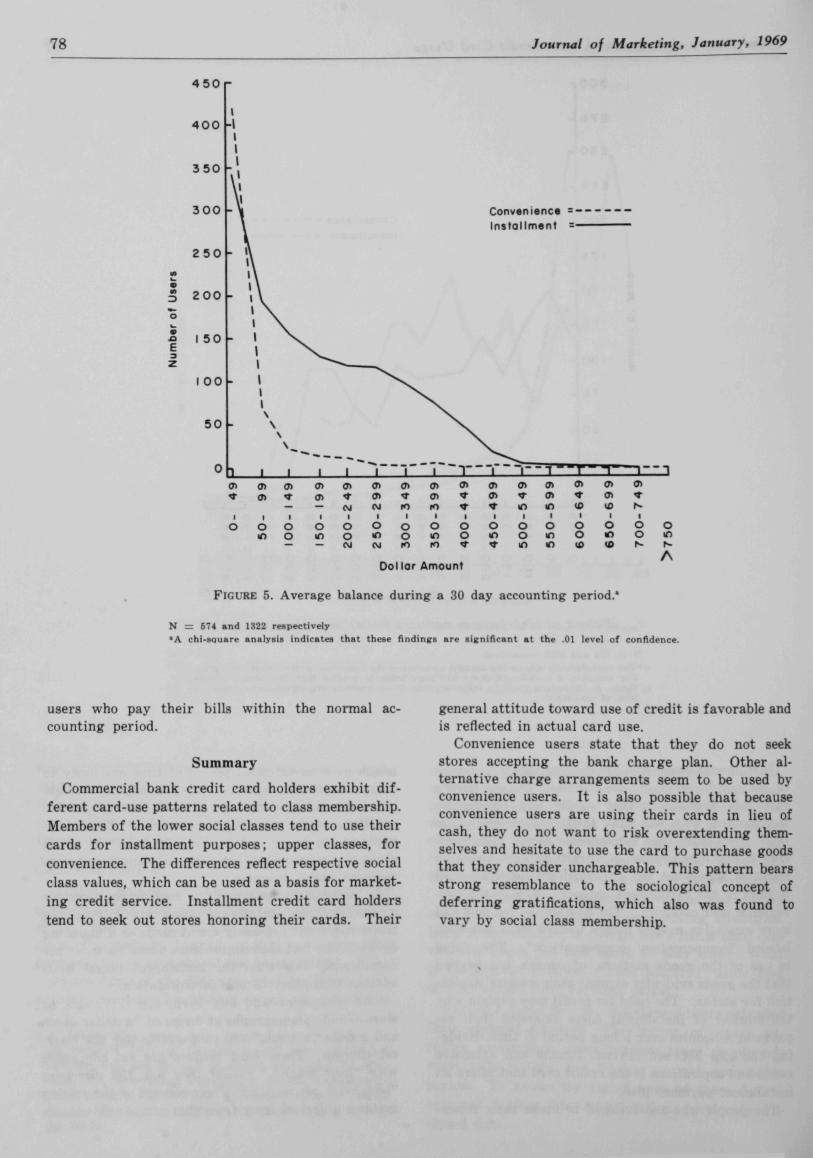

ments over an extended period of time are likely tocharge more than others. They run higher absolutebalances and higher average balances than people whouse the card for convenience purposes. These inti-mations are borne out in Figures 4 and 5, whichshow the relationship between installment and con-venience users' balances.

In large part, these findings confirm the previouscontention that installment users are buying bigticket items and are using credit cards as a financingdevice. The fact that convenience users' balances aresignificantly less than the installment users' lendsadditional support to our interpretation.

The consumers who buy furniture, T.V. sets orstereophonic phonographs at terms of "a dollar downand a dollar a week," are prepared to pay the inter-est charges. These card holders are not concernedwith "how much?," rather they ask the merchant"how much per month?" Their concept of the pricingsystems differs sharply from that of the convenience

78 Journal of Marketing, January, 1969

E3

450

400

350

300

250

200 •

Convenienc*Installment

Dollar Amount

FIGURE 5. Average balance during a 30 day accounting period.*

N = 674 «nd 1322 respectively*A chi-sguare analysis indicates that these flndincs are lignificant at the .01 level of confidence.

users who pay their bills within the normal ac-counting period.

Summary

Commercial bank credit card holders exhibit dif-ferent card-use patterns related to class membership.Members of the lower social classes tend to use theircards for installment purposes; upper classes, forconvenience. The differences reflect respective socialclass values, which can be used as a basis for market-ing credit service. Installment credit card holderstend to seek out stores honoring their cards. Their

general attitude toward use of credit is favorable andis reflected in actual card use.

Convenience users state that they do not seekstores accepting the bank charge plan. Other al-ternative charge arrangements seem to be used byconvenience users. It is also possible that becauseconvenience users are using their cards in lieu ofcash, they do not want to risk overextending them-selves and hesitate to use the card to purchase goodsthat they consider unchargeable. This pattern bearsstrong resemblance to the sociological concept ofdeferring gratifications, which also was found tovary by social class membership.