Embed Size (px)

Citation preview

CONFIDENTIAL

www.riunit.com / www.riunit.lk

CONFIDENTIAL

www.riunit.com / www.riunit.lk

SOCIO – ECONOMIC IMPACT OF THE POTENTIAL PROHIBITION OF CHRYSOTILE IN SRI LANKA – COST EVALUATION

FINAL REPORT

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 1

Table of Contents

Executive Summary......................................................................................................…...3

1. Objective of the socio-economic evaluation ...................................................................... 5

2. Research Methodology ....................................................................................................... 7

3. Background ......................................................................................................................... 9

4. The direct costs of a potential ban ................................................................................... 14

5. Indirect economic costs .................................................................................................... 24

6. Social cost ......................................................................................................................... 32

7. The impact on the environment ....................................................................................... 43

8. Overall macro-economic impact ...................................................................................... 55

Annex A - Summary of Environmental Impact Feedback from Experts Annex B - National Housing Policy

Annex C - Methodology

Annex D - Stakeholder Agencies Annex E - Literature Review

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 2

Executive Summary Essentially the roof is the defining feature of any dwelling be it a residential, commercial or any other type of building. In this regard, any attempt to ban or restrict the most popular roofing material that Sri Lanka currently opts for will naturally have serious consequences in terms of the direct and indirect economic costs as well as the social and the environmental impacts that are more difficult to monetise but nevertheless have very serious consequences. The rationale for engaging in any discussion on a ban on the use of Chrysotile in other countries has been based on arguments that are connected to the perceived negative health impacts of Chrysotile fiber. Whilst the scope of this report does not cover any investigation of health-related aspects, it is worth noting that to date there are no medical records or statistics showing harm from the import or manufacture of Chrysotile containing roofs despite more than sixty years of use in Sri Lanka. This report begins by noting that in an international context, the countries that have banned Chrysotile are predominantly located in Europe and a few other parts of the industrialised world where the average GDP is almost ten times higher than Sri Lanka. Next, the report presents an analytical consideration of the direct costs of a potential ban based on several methods of calculation that use available government data from the Central Bank and the Department of Census and Statistics. Based on the statistical model that we have developed; the following direct costs have been presented;

Annual value of Chrysotile roofing material used in Sri Lanka is LKR 21.5 billion (US$

146.8 million)

Value of total stock of Chrysotile roofing inventory in Sri Lanka LKR 395 billion

(US$2.7 billion)

Value of existing capital investment: LKR 8-16 billion (US$55-110 million)

New investment required to produce alternatives: LKR 8-16 billion (US$55-110

million)

Loss of income and profits to the industry: LKR 14.7 billion (US$100 million)

Loss of income earned by employees (direct and indirect): LKR 17.9 billion per

annum (US$122 million)

Loss to Customs and Inland Revenue: LKR 858 million (US$5.9 million)

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 3

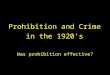

Furthermore, indirect economic costs are multifarious and include both tangible and intangible impacts that are at times difficult to monetise. Nevertheless, this report has highlighted very important concerns that in a worst case scenario may prove to be disastrous for certain domestic sectors as well as the economy as a whole. A case in point is the impact that a potential ban on Chrysotile fiber imports may have on Sri Lanka’s trade relations with Russia that are currently valued at over US$ 426 million with the balance of trade in Sri Lanka’s favour. The Russian Ambassador to Sri Lanka has already publicly voiced concerns on the government proposals to ban Chrysotile whilst the Chairman of the Sri Lanka Tea Board has also stated to the RIU research team that the potential fall-out for the domestic tea industry could be significant. The tea industry contributes over US$ 1.5 billion to the national economy and provides employment to an estimated two million workers. This report also presents the findings of our primary research on the impact of a ban on households, schools and hospitals in Sri Lanka.The findings from the household survey confirm that the impact will be somewhere between severe and damaging under scenarios where homes will not be able to replace their roofing sheets and cannot upgrade from iron sheets (takaran) because they can no longer afford a material that is a better alternative. It was also found that 25 per cent of hospitals have Chrysotile roofs with an additional 24 per cent having a mix of materials that include Chrysotile which would represent over 43,000 hospital beds. Similarly, 22 per cent of schools had Chrysotile roofs whilst a further five per cent had a mix that included Chrysotile which represents 2,368 schools and more than one million children across the island. Finally, this report presents an evaluation of the potential environmental impact of a ban on Chrysotile by looking at the likely alternatives that will fill the gap in demand for roofing materials. According to our research, clay tiles are expected to be at the frontline of those products that will be considered by home owners and developers. However, any significant increase in the production of clay tiles is not likely to be sustainable given that large portions of earth need to be excavated for this purpose. This activity is known to have serious negative impacts on the environment, including landslides, a phenomenon that Sri Lanka is now experiencing at increasing frequency. It has also been found that if the government starts to categorise Chrysotile roofing as a dangerous material, then it might follow that policies will be introduced for the safe removal and disposal of the same. Currently, there are no provisions made by the Central Environment Authority (CEA) for disposal of this material.In our research, we used the Australian model for removal and disposal and discounted the costs accordingly to represent much lower wage rates in Sri Lanka.Nevertheless, the cost of removal, transportation and disposal of all current inventory would cost the government an estimated LKR 1,653 billion (US$ 11.25 billion).

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 4

Essentially, this report has found that Chrysotile roofing is the preferred choice of material in Sri Lanka, especially for the low and mid-income groups who continue to upgrade from cheaper and less robust materials to one that is affordable and offers a huge improvement in comfort and overall material performance (thermal performance, water tightness, noise, durability, strength, aesthetic appearance and availability). Consequently, a policy that seeks to ban this important material may find that it contradicts the National Housing policy which seeks to extend affordable and decent shelter to some 100,000 people each year. Moreover, rash policy decisions in the regard also threaten to open the door for potentially harmful negative economic impacts to the specific industries as well as the macro-economy.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 5

1. Objective of the socio-economic evaluation

As part of ongoing moves by the Sri Lankan government, the Cabinet recently approved controlling the use and import of asbestos (Chrysotile) from January 2018 by adopting more “beneficial substitutes and to prepare an operational programme to prohibit asbestos related production by 2024.”1

Accordingly, a proposal made by the President Maithripala Sirisena, in his capacity as the Minister of Mahaweli Development and Environment, to control the use and import of asbestos and to prohibit asbestos related productions by 2024, was approved by the Cabinet of Ministers. However, industry commentators and economists are concerned that the government is embarking on an effort to control, restrict or ban a product that has grown in popularity due to its affordability, quality and accessibility, without having fully assessed the economic and social impact of this action.

The Research Intelligence Unit (RIU) was commissioned by the Chrysotile Information

Centre (CIC) to conduct a socio-economic cost assessment on the possible banning of

Chrysotile in Sri Lanka. Whilst the CIC has sponsored this research study, it is important to

note that the RIU has carried out the task independently and is fully responsible for the

findings of this report.

The rationale for conducting this research assignment is based on the need to grasp a better understanding of the full impact in terms of economic, environmental and social cost of any potential ban on Chrysotile products in Sri Lanka. Specifically, the objectives of the study are to address the:- “… direct, indirect and induced effects, and examine pre-existing regulations and proposed regulations – with the goal of measuring the outcomes and effects of a ban on the relevant businesses and socio-economic actors; and the outcome of this study will prove useful to policy makers and other relevant government agencies and authorities to effectively consider the cost of the situation”.

1 Source: Daily FT; http://www.ft.lk/article/566651/Asbestos-ban-in-2024--control-use-in-2018

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 6

This final report begins with a situational analysis of the country in terms of the macro-economic environment and the importance of the construction and real estate industry to the national economy. Next, this report presents a detailed description of our methodology followed by the RIU’s primary research findings which is organised as follows:- - Direct economic costs - Indirect economic costs - Social impact - Environmental costs Given the overall lack of information and material on the subject, this report represents the findings of primary research on the use of Chrysotile. This included a survey of 100 homes covering four districts, as well as a survey of 48 schools and 40 hospitals, all relevant institutions, exporters, environment experts and institutional users.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 7

2. Research Methodology

2.1 Overview

The approach, methodology and the sequence of work undertaken by the RIU team in this study are as follows;

- Desk review and study of available research materials and secondary data related to

the areas of inquiry within the scope of work; - Institutional mapping of all agencies, government and private sector organisations in

relation to where they operate in the context of the industry supply chain; - Developing databases of material, references and contacts; - Unstructured interviews with key stakeholders with a view to identify new sources of

secondary data as well as to get a sense of the knowledge and awareness levels on Chrysotile at the policy, institutional and regulatory levels.

- Finalising primary data formats for further structured meetings with stakeholders and field research covering key groups;

- Finalising survey samples for consumers, industry, stakeholders and environmentalists and conducting one-on-one interviews and meetings;

- Executing primary research at institutional and field levels with a finalised set of research tools that include one-on-one questionnaires, site observation checklists and in-depth interviews;

- Checking quality of data and data entry; - Data analysis and data modelling; - Providing the final report incorporating industry feedback with a detailed assessment

of the economic, social and environmental costs;

2.2 Information quality

At all stages of information gathering, the research team was mindful of the need for the information to be credible, accurate and relevant. In this regard, the research team filtered information of relevance while accuracy and credibility required that we continue to triangulate the information using several sources, sometimes asking the same questions from different stakeholders.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 8

2.3 Literature and secondary data review

All secondary data has been referenced and a list of references has been included in the Annexures.

2.4 In-depth interviews, surveys and data modelling

This aspect of the primary research sought to add value to our understanding of the problem in an environment of limited secondary data availability. During the research, we completed the following surveys;

● Household survey: A sample of 100 households in the districts of Jaffna, Kandy, Gampaha and Colombo that currently use Chrysotile roofing material.

● Site observation checklists carried out at 40 schools and 40 hospitals in the same districts in order to identify the profile of roofing materials in key government buildings.

● One-on-one meetings with industry stakeholders, associations, business and institution leaders, environmentalists, experts on roofing materials, tea exporters and local manufacturers of Chrysotile.

● Cost calculations, particularly for the direct costs, was generated with extensive data modelling using Mini-Tab (Version 14) and SPSS.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 9

3. Background

3.1 Country overview

Sri Lanka is an island of 65,620 sq. km and a population of 21 million with literacy rates exceeding 92 per cent and has traditionally maintained human development indicators that are comparable with those of advanced countries. The economy measured in terms of per capita GDP has always led the pack among South Asian economies and the post war (2009) performance has further propelled the island economy into middle-income status. In 2015 GDP per capita stood at US$ 3,686 and Sri Lanka has had renewed support of its political reforms from all parts of the Western world as well as India. 2 Another consequence of the new political regime has been a change in the way GDP is calculated. According to the new method of National Account calculation, Sri Lanka's gross domestic product will expand to 5.8 per cent in 2016 up from 4.8 per cent in 2015 and strengthen over the medium term to achieve a higher growth target of around 7.0 per cent. The latest data from the Central Bank Annual report 2015 show:- Key Economic Indicators

● Sri Lanka’s economic growth, which slowed to 4.8 per cent in 2015, compared with a

4.9 per cent growth witnessed in 2014 is to improve by 5.8 per cent in 2016.

● Agriculture and services related activities grew by 5.5 per cent and 5.3 per cent,

respectively, while industry related activities grew at a slower pace of 3.0 per cent

during 2015.

● Inflation, as measured by the year-on-year change in the Colombo Consumers’ Price

Index (CCPI) was recorded at 2.8 per cent, compared to 2.1 per cent at the end of

2014.

● Tourist arrivals for October 2016 rose by 13.7 per cent to 150,419 according to the

Tourism Authorities. This represents a total for the year of 1.658 million a rise of 14.6

per cent from 2015. The target set for 2016 is 2.5 million visitors.

● Earnings from tourism in 2015 increased by 22.6 per cent to US$ 2,981 million,

compared to US$ 2,431 million in 2014.

2 Source: REAL ESTATE DEVELOPMENTS WITHIN A GREEN ENVIRONMENT; http://riunit.lk/wp-content/uploads/2015/03/50-51.pdf

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 10

The Human factor Along with this remarkable economic development, Sri Lanka is witnessing a positive improvement in the human development indicator which stands at 0.75 per cent.

3.2 The Western Province Contribution to National Economy

The Western Province is one of nine provinces of Sri Lanka and the first level administrative division of the country. Whilst regional disparities remain across the island in terms of growth rates and share of GDP, it is clear that the Western Province dominates the economic landscape according to the latest data.

Chart 3.1 Sri Lanka’s GDP per capita

Chart 3.2 Share of PGDP in the overall GDP Chart 3.3 Western Province contributions GDP 2015

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 11

Colombo has been changing continuously since the end of the long civil war in 2009 with increased tourism, infrastructural developments and domestic and international real estate projects.

3.3 International comparison

Despite the impressive progress in Sri Lanka’s macro-economic environment, an important point to note is that in the vast majority of cases, it is the rich industrialised countries that have embarked on a ban of Chrysotile. One of the key reasons for this phenomenon is the fact that only countries with high levels of per capita GDP will have home owners who can afford to change their roofing material to higher priced alternatives3.

3 The only exception is Mozambique which approved a ban on the production, use, import, export and trade in Asbestos and Asbestos containing products in August 2010. Since then a number of substitutes have been introduced to the market such as clay tiles, aluminum sheets and a type of straw named Palha or Caniso. Aluminum is one of the main exports of Mozambique which helped with the transition from Asbestos.Mozambique is one of the largest suppliers of aluminium in Africa.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 12

Chart 3.4 Countries that have banned

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 13

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 14

4. The direct costs of a potential ban Several approaches were used to base our estimates on the value of the Sri Lankan Chrysotile industry. The main methodologies developed in this study include the following:-

The annual value of the housing (construction) industry of which roofing material

accounts for 10 – 20 per cent;

The annual value of Chrysotile roofing as a share of new houses that have been

approved by the government;

The value of current Chrysotile inventory in use in Sri Lanka as roofing material in

homes, schools, hospitals, etc. ;

The cost of removal and disposal of existing stocks of Chrysotile inventory.

A comprehensive estimation of the direct costs will also need to take account of a wide variety of factors that include the following:-

Value of existing capital investment of the manufacturing plants and machinery for

each of the four producers;

New investment for production of alternative roofing materials;

Loss of income and profits in the industry;

Value of imports and Customs revenue.

4.1 The construction industry approach

One of the Island’s fastest growing or booming industries is the construction sector. This is witnessed by the continued growth in new housing approvals as well as in the large numbers of high-rise buildings being built in Colombo and the suburbs. According to Central Bank data, the real-estate sector grew by 9.6 per cent in 2015. This growth has been accompanied by a staggering expansion in the construction sector which has been growing at a rate of 22 per cent and contributed to 9.7 per cent of Sri Lanka’s Gross Domestic Product (GDP) in 2015.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 15

According to this method that uses Central Bank data on Housing Construction, some US$ 146 million worth of Chrysotile roofing entered the Sri Lankan economy in 2015.This figure sits well with Customs data that show Sri Lanka has imported US$ 44.9 million worth of Chrysotile fiber in 2016. It is also important to note that the cost of construction inputs have been rising steadily over recent years, including the price of Chrysotile. Therefore, the past and future values of annual Chrysotile use in Sri Lanka will vary in line with overall construction material costs.

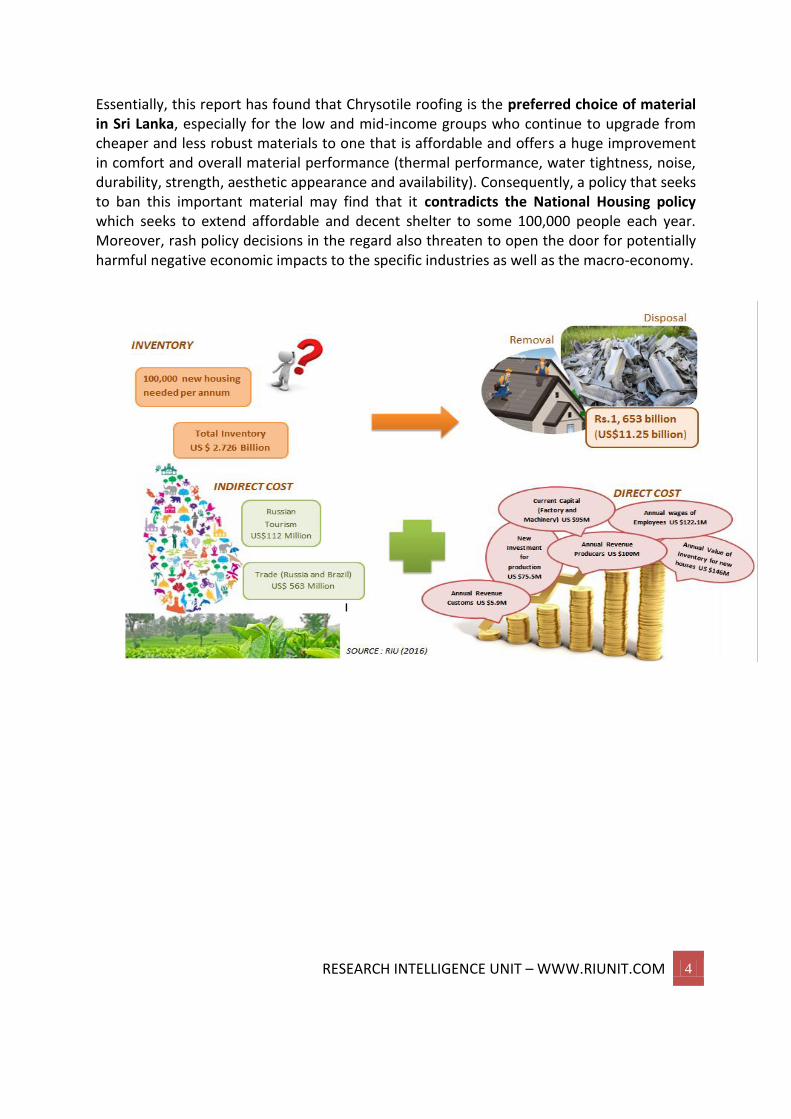

4.2 New housing approvals approach

Data released by the Central Bank of Sri Lanka indicate that the number of new houses approved over the past 12 years in Greater Colombo has tended to fluctuate at between 8000 and 16,000 units per annum. In addition, an average of 1,500 non-housing buildings are also approved each year. These contribute to the total building approvals that average 14,646 new buildings being approved per annum in Greater Colombo.

Calculation of annual value Value of construction industry (2015) =US$ 7.985 billion Buildings1 (53.2% of total industry) =US$ 4.232 billion Roofing materials1 (10% of buildings) =US$ 423 million Chrysotile material (34.6% of roofing) =US$ 146 million (per annum in 2015)

Chart 4.1 Fluctuation of prices of construction inputs reflected by Indices

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 16

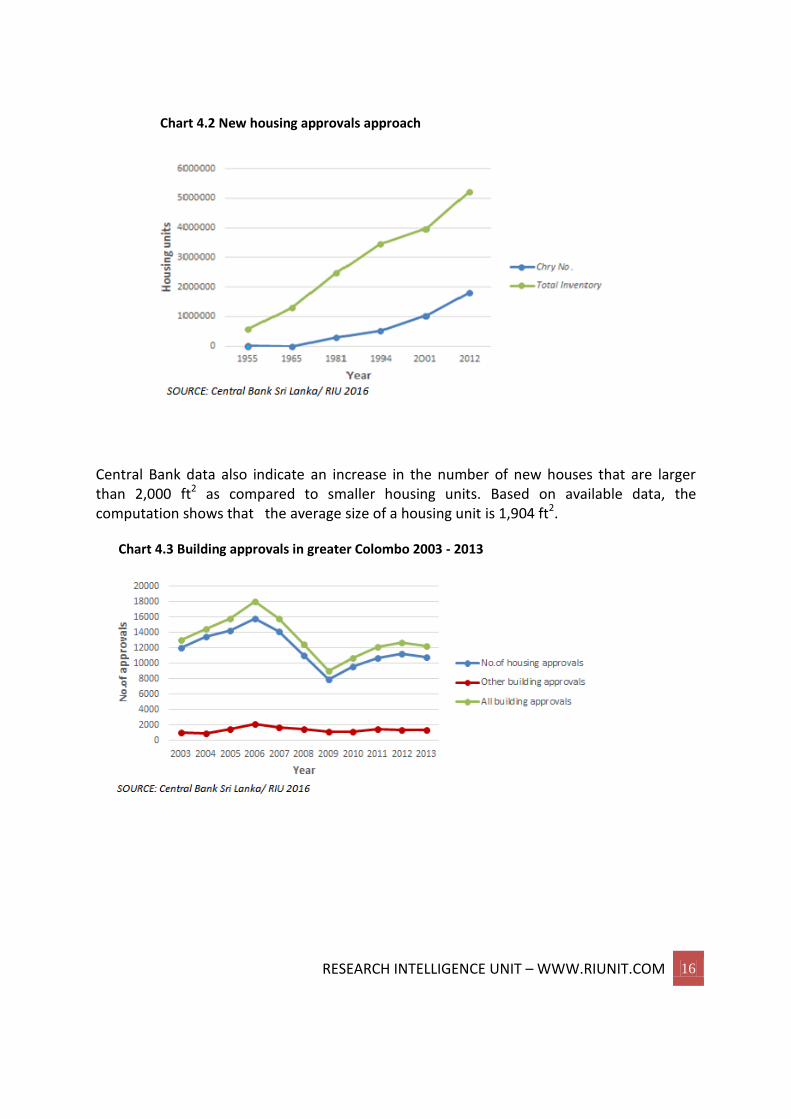

Central Bank data also indicate an increase in the number of new houses that are larger than 2,000 ft2 as compared to smaller housing units. Based on available data, the computation shows that the average size of a housing unit is 1,904 ft2.

Chart 4.2 New housing approvals approach

Chart 4.3 Building approvals in greater Colombo 2003 - 2013

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 17

According to Central Bank data when we consider every ten houses approved in Greater Colombo, there is at least one “other building approval” thus our average building unit size estimate can be revised upward4. The “other buildings” are not defined but include all non-housing buildings such as large commercial complexes and warehouses, government buildings and places of religious worship.

4 In 2010, Number of other buildings approved was 1,107

Chart 4.4 No. of housing approvals in Colombo by size of dwelling

Chart 4.5 Breakdown of building approvals in greater Colombo 2002 - 2012

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 18

As described earlier, the latest Census data has indicated that an estimated 34.6 per cent of all roofs in Sri Lanka use Chrysotile material – a total of 1,800,077 roofs. Based on available information and RIU’s data modelling, we have arrived at the following values for Chrysotile roofs per annum;

Greater Colombo5 - Total number of approved houses (2013) =10835

- Estimated average square foot of a house = 1904

- Estimated average square foot of a roof = 952

- Estimated square foot area of the roof of approved houses = 10,312,250

- Chrysotile share of roofing material1(34.6%) = 3,568,039

- Cost (Ft2 of Chrysotile roof1 = LKR 186.93

- Total value / cost of annual housing approvals = LKR 666,973,437

(US$ 4,599,817)

- Total number of approved other building units (2013) = 1422

- Estimated average square foot area of other building units = 5000

- Estimated average square foot area of a roof of other building units = 2500

- Estimated square foot area of roofs of approved other building units = 3,555,000

- Chrysotile roofing material (34.6%) = 1,230,030

- Cost (Ft2 of Chrysotile roof = LKR 186.93

- Total estimated cost of non-housing buildings = LKR 229,929,508

(US$ 1,585,721)

- TOTAL ANNUAL COST (FOR ALL BUILDINGS) = LKR 896,902,945

(US$ 6.17 million)

Island wide Population of Greater Colombo (20.07 % of total) = 4,207,876 Population of Sri Lanka = 20,966,000 TOTAL ANNUAL COST = US$ 30,819,818

(US$ 30.82 million)

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 19

4.2 Cost / value of total stock of Chrysotile roofs approach

Since 1955, Sri Lanka has used locally produced Chrysotile roofing material for home and commercial use. By 1994, Chrysotile had been gaining in popularity at a rapid pace and accounted for some 15 per cent of all roofing materials used in Sri Lanka (Demographic Survey of 1994). According to government data, the extent of Chrysotile use in the Colombo area was as high as 43 per cent. By 2012, the market penetration of Chrysotile has more than doubled and accounts for 34.6 per cent of all roofing material, including 64.6 per cent of all roofing in Colombo. This is an estimated 1.8 million houses with Chrysotile roofing material.

Total number of households with Chrysotile : 1,800,077 Estimated average size of a dwelling : 925 Total square foot area used in homes : 1,665,071,225 Estimated cost at 2015 market price (LKR 186.93 Ft2) : LKR 311,251,764,089 (US$ 2,146,563,890) Total number of other building units with Chrysotile : 180,008 Estimated average size of a dwelling : 2500 Total Ft2 area in other building units : 450,020,000 Estimated cost at 2015 market price (LKR 186.93 Ft2) : LKR 84,122,238,600 (US$ 580,153,370) TOTAL ESTIMATED VALUE OF TOTAL STOCK : LKR 395,374,002,689

(US$ 2,726,717,260)

Chart 4.6 Chrysotile Industry in Sri Lanka

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 20

4.3 Cost to manufacturers

This study confirms that there are four major organisations involved in the import of raw materials and local manufacture of Chrysotile roofing sheets in Sri Lanka. Direct employment in the industry is estimated at between 4,000 – 4,500 with up to a further 17,000 – 40,000 indirectly employed in the industry as suppliers, dealers and transport service providers. The four main players in the industry are recognised as Built Element Ltd. , Rhino Roofing (Pvt.) Ltd. , Sri Ramco (Pvt.) Ltd. and Sigiri Roofing (Pvt.) Ltd. The first operations began in 1995 when Built Element started their production plant and this was followed by Rhino in 1962. Whilst both of these firms are locally owned, Sri Ramco and Sigiri Roofing are backed by foreign investment from India.

4.3.1 Value of existing capital investment Based on the collection of primary data from all current Chrysotile producers in Sri Lanka, it is estimated that the value of current investment on capital goods is at LKR 8 – 16 billion (US$ 55 - $110 million).

4.3.2 New investment for production of alternative roofing materials It has been estimated that the production of alternative roofing materials such as galvanized

zinc and zinc aluminum will require an investment of the same magnitude as that of the

machinery and capital needed for the production of Chrysotile (US$ 55-$110 million).

4.3.3 Loss of income and profits in the industry

For reasons of confidentiality, none of the producers were willing to part with information

on their profits and revenues. However, based on available data, we have estimated

revenue in the industry at US$ 100 million per annum. According to confidential industry

sources that were accessed during our primary research, the recent trend in sales has been

steady with a slight annual increase from 30,000 – 35,000 MT tons.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 21

4.4 Loss of Customs revenue

The production of Chrysotile requires only Chrysotile fiber (imported) which amounts to around 8 per cent plus water and cement.

Chart 4.7 TOTAL FIBRE IMPORTS FROM 2000 to 2016

Year Total Fiber Imports (Kgs) US $

2000

22,574,922 N/A

2001

23,394,941 N/A

2002

24,140,636 N/A

2003

23,284,995 N/A

2004

33,816,710 N/A

2005

35,911,931 N/A

2006

39,444,687 N/A

2007

46,104,990 N/A

2008

58,113,000

31,426,032

2009

39,378,792

13,781,205

2010

47,875,292

29,089,988

2011

60,979,129

40,228,635

2012

64,385,051

44,037,829

2013

40,977,558

25,228,012

2014

51,340,000

38,807,247

2015 44,887,500 31,086,734

2016 44,992,500 27,416,906

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 22

Based on data on asbestos (HS Code: 25249000) from the Department of Customs, the tax rates are PAL (7.5 per cent), NBT (2 per cent) and VAT (11 per cent). The total duty earned by Customs in 2015 from this product was LKR 858, 701,483 (US$ 5.9 million) and in 2016 LKR 958, 687,826 (US$ 64, 80537) due to a higher volume of imports.

4.5 Cost to employees

According to the primary research efforts of the team, we have arrived at the following estimates for the industry workforce; The average wage of an employee in the industry is estimated at LKR 50, 000 pcm based on our findings. Thus the monthly loss of income to those directly employed in the industry is LKR 225, 000,000 (US$ 1,551,724). Those who are defined as indirectly employed include service providers, suppliers, dealers, hardware merchants, transporters and also indirect entities. Many of these workers also face the risk of unemployment in the event that the factories cease to operate. If we proceed with a conservative assumption that the effect on those employed indirectly will be impacted half as much as those employed directly, the cost will be LKR 1.25 billion (US$ 8,620,689)

Direct employees : US $1,551,724 Indirect employees : US $8,620,689 TOTAL COST (PCM) : US $10,172,413 LOSS PER ANNUM: US $122,068,965

Employees : 4,500 Indirect employees : 50,000 Dependents (indirect) : 200,000

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 23

4.6 Summary of direct economic costs

Value of total inventory (at 2016 market prices): US $2.5 - $3.0 billion Annual value of inventory for new houses: US $146 million Current capital (factory and machinery): US $55 - $110 million New investment needed for new production: US $55 - $110 million Annual revenue of producers: US $100 million Annual customs revenue: US $5.9 million

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 24

5. Indirect economic costs Consideration of indirect economic cost involves multifarious tangible and intangible impacts that are difficult to monetise with any degree of certainty. However, in this section, we highlight several key areas that are likely to feel a direct impact that will result in an indirect economic cost as a consequence of any potential ban. These include the impact on Sri Lanka’s international trade with an emphasis on tea exports, the prospect of possible litigation on the part of producers and those enterprises that stand to take a financial hit and the potential impact on the tourism industry.

5.1 International trade and importing of raw materials

Whilst the manufacture of Chrysotile is done locally, the raw material, Chrysotile fiber, has to be imported from several overseas destinations that include Russia and Brazil. The imports of raw material have steadily increased over the past 15 years, from 22.5 million kilogrammes in 2000 to 51.3 million kilogrammes in 2014. In 2014, the value of total imports is estimated at US$ 38.8 million. According to Customs data, Russia accounts for the lion share of the market, accounting for as much as 89 per cent of total Chrysotile fiber imports. Next is Brazil with an estimated 9 per cent of total raw material imports, followed by Kazakhstan, India and China who jointly account for around 2 per cent. Given the important role played by Russia in the trade, it would be important to note the significance of Russia as a trade partner with Sri Lanka.

Chart 5.1 Fiber imports

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 25

5.1.1 Trade with Russia Diplomatic relations between the Soviet Union and Sri Lanka were established on February 19, 1957 but the history of Russian – Sri Lankan relations originates much earlier. The Russian Consulate was established in Galle in 1892 and in 1959 the Friendship Society with Sri Lanka was established in Moscow. The agreements mentioned below have been entered into between Russia and Sri Lanka:-

1. Economic & Technical Corporation

2. Housing Constructions

3. Goods Exchange

4. Air Services

5. Education

According to the Export Development Board, Sri Lanka’s main export products to Russia are tea, apparel, industrial & surgical gloves of rubber, desiccated coconut, activated carbon, discharge lamps, green tea, mixed coir fiber, coir pads, coir yarn, pneumatic and retreated rubber tires and tubes. The main imports from Russia to Sri Lanka are base metal products, paper and paper products, non - metallic mineral products, chemicals and plastic products, electrical and electronic products and parts and machinery woven fabrics.

Chart 5.2 Trade between Russia and Sri Lanka

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 26

As illustrated by the composition of the main exports from Sri Lanka to Russia, tea is the standout product that is demanded by Russian consumers. Tea has traditionally played a vital role in the Sri Lanka economy and contributed US$ 1.5 billion in 2013 whilst employing some 2 million workers (direct and indirect). Sri Lanka exports its tea mainly to Russia and several Middle East countries including Iraq (31 kt), Syria (11 kt), Kuwait (9 kt), Jordan (6 kt) and Saudi Arabia (5 kt). Other significant importers in 2015 were Turkey (33 kt), Japan (8 kt) and Germany (7 kt)5. Given the volatility in some of these important markets, many of which are global trouble-spots, Sri Lanka is always exposed to unstable prices. As such, the stability that the Russian market offers is of vital importance to the local industry that has been involved in fierce competition with Kenya over recent years for the top-spot in global tea exporters. Domestically, the industry has very serious challenges from climate change and the comparatively high price of labour. Any attempts to ban the importation of Chrysotile fiber from Russia threaten to destabilise this all-important trade tie with this important trade partner. The Russian Ambassador to Sri Lanka has already appealed to the Sri Lankan Government to reconsider its proposed asbestos ban and work with stakeholders to find a mutually acceptable solution to address health issues, which it believes are overblown. At the recently held Annual General Meeting of the Sri Lanka-Russia Business Council, Russian Ambassador Alexander A. Karchava appealed to the council to intervene in the Government’s decision to ban the use of Chrysotile fibre in Sri Lanka, stating that such a move could strain relations between the two countries. (Financial Times, 21st October 2016) 5 Dr. Janaka Ratnasiri – The Island

Chart 5.3 Top 10 Sri Lankan exporters to Russia

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 27

During this research assignment, the RIU also met with Mr. Rohan Pethiyagoda, Chairman of the Sri Lanka Tea Board, to discuss the potential impact on the tea industry of any ban on Chrysotile imports from Russia. In response, the Chairman said that such a move posed significant risk to the local tea industry given the importance of the Russian market to exporters. He added that developing countries seem to suffer from a phenomenon of embarking upon drastic policy changes that are not fully thought out and the full impact of the consequences not considered. This is in contrast to the developed world that takes a long time to research the impact of implementing changes in policy, especially on an issue as important as the most popular type of roofing material in the country.

5.1.2 Trade with Brazil Bilateral relations between Brazil and Sri Lanka were established in 1960 and the Framework Agreement on Technical Cooperation, in force since 2010, is the main legal instrument for cooperation and involves the following areas:- ● Biofuels technology, production, and distribution;

● Agricultural and livestock research, production, and trading; and

● Development of social programmes.

Bilateral trade increased between 2002 and 2013, growing from US$ 24.9 million to US$ 137 million, with a surplus for Brazil. During the same period, Brazilian imports from Sri Lanka increased by a total of US$ 1.9 million to US$ 47 million.

5.1.3 Trade with Kazakhstan Kazakhstan takes 4th place in the global distribution of asbestos production in the world, following Russia, China, and Brazil. It produces about 214,000 metric tons of Chrysotile asbestos per year, which is about 10 per cent of the worldwide output yearly. Around 90 per cent is exported to other countries, whilst the rest is used locally. In 2013 Sri Lanka imported 517,675 kg of fibre by spending US$ 374,206. While there is an increase in 2014 up to 1,237,500 kg by spending US$ one million fibre imports from Kazakhstan increased up to 2.3 per cent in 2014.6

6 Source: Overview of Chrysotile Asbestos in Kazakhstan,2013

http://ibasecretariat.org/cop6_side_event_kazakhstan_2013.pdf

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 28

5.1.4 WTO and other trade agreements In the event that a ban on Chrysotile takes place, there will also be important international trade agreements and World Trade Organisation (WTO) commitments that might be negatively impacted. Sri Lanka has been a member of the WTO since 1 January 1995 and a member of the General Agreement on Tariffs and Trade (GATT) since 29 July 1948. As a founding member of the GATT, Sri Lanka remains fully committed to the WTO by pursuing an outward-oriented multilateral trade system. Therefore, any ban on the import of Chrysotile fibre could be viewed by the source countries as going against the principles of the WTO. According to the WTO, Agreement on Technical Barriers to Trade (TBT) Article 2.2: With respect to central government bodies: “Members shall ensure that technical regulations are not prepared, adopted or applied with a view to or with the effect of creating unnecessary obstacles to international trade. For this purpose, technical regulations shall not be more trade-restrictive than necessary to fulfill a legitimate objective; taking account of the risks non-fulfillment would create. Such legitimate objectives are, inter alia: national security requirements; the prevention of deceptive practices; protection of human health or safety, animal or plant life or health, or the environment. In assessing such risks, relevant elements of consideration are, inter alia: available scientific and technical information, related processing technology or intended end-uses of products." According to the WTO guidelines on sanitary and phyto-sanitary measures7, any product ban that affects international trade requires advance notification as well as documentation of local evidence and research proving harm, before trade and import can be suspended. No such procedures of local scientific or technical studies have been conducted in Sri Lanka to date (Chrysotile in Sri Lanka, CIC).

5.2 Tourism

Sri Lanka's tourism industry has been booming since a three-decade war ended in 2009. Earnings from tourism increased significantly in 2015 recording a 22.6 per cent increase against the previous year. In the twelve months to December, the Island has earned US$ 2,980.7 million from tourism.

The State Tourism Promotion Office states that tourist arrivals to Sri Lanka rose 11.8 per cent from a year earlier to 186,288 in August 2016, with total visitors up 16 per cent for 2016 to 1.359 million. Arrivals to Sri Lanka have also increased from 448,000 in 2009 to 1.8 million in 2015. Currently Sri Lanka shares 0.13 per cent of the total tourists’ arrivals and 0.2

7 The WTO Agreement on the Application of Sanitary and Phytosanitary Measures (SPS Agreement) http://www.wto.org/english/tratop_e/sps_e/spsagr_e.htm

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 29

per cent of the total tourist earnings of the world. According to estimates made by the World Travel and Tourism Council (WITC) the direct and total contribution to the GDP and employment by the travel and tourism sector of Sri Lanka is far better than the world and Asia Pacific averages. Nevertheless, the potential for growth lies untapped, as the travel and tourism direct and total contribution to the GDP and employment of Sri Lanka is comparatively lower than regional competitors such as Maldives, Cambodia, Thailand and Malaysia. According to the Sri Lanka Tourism Promotion Bureau, more than 2.2 million tourists are expected in 2016. In order to cater to such a high number of tourists, it is estimated that 40,000 to 50,000 rooms are required, where only around 30,000 hotel rooms are available - both in tourist hotels and supplementary establishments as at end 2015. More than 6,400 hotel rooms are expected to add on in 2016 and many new hotel projects to enhance facilities are in the pipeline.

Russian tourists are an important source of foreign exchange earnings for Sri Lanka and an estimated 69,718 Russian tourists arrived in 2014 spending an estimated US$ 112 million.

Chart 5.4 Tourist arrivals by countries of residence Jan 2015 - 2016

Chart 5.5 Tourist arrivals from Russia

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 30

5.3 Litigation Every country in the world where Chrysotile has been banned has witnessed a dramatic and immediate mushrooming of lawsuits that have cost hundreds of millions to taxpayers and businesses, notwithstanding the form of legal system. In the United States the RAND Corporation8 recently estimated the total costs of asbestos-related claims will exceed US$ 250 billion. Of the US$ 54 billion spent to date, 65 per cent of those claims have come from non-malignant cases with more than 50 per cent of costs being allocated to “transaction costs”. Outside the US, numerous cases have been initiated by the efforts of US and Australian law firms and their associations acting abroad. In the UK, more than US$ 17.7 billion of litigation expenses are estimated to have accrued. In Japan it is estimated that more than US$ 22.732 billion have been spent on litigation so far (Chrysotile in Sri Lanka, CIC). The highest levels of asbestos related litigation around the world have been in developed countries.

5.4 Summary of Indirect Economic Cost

8 http://www.rand.org/content/dam/rand/pubs/documented_briefings/2005/DB397.pdf

Chart 5.6 Annual value of Tourism

A map to show the GDP per capita around the Globe

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 31

5.4 Summary of Indirect Economic Cost

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 32

6. Social cost

6.1 Cost to the industry workers and dependents

According to primary research as presented in the previous section, the number of workers who are directly involved in working in the industry is estimated at 4,500 with an additional 50,000 workers indirectly involved at various points on the supply chain. In addition to the direct financial and psychological impact of being laid off work, there will be an estimated 18,000 family members who will also be hit with possible economic hardship or worse. Should consideration be given to those indirectly employed at various points along the supply chain, some 272,500 individuals are likely to feel a negative financial impact and this will have serious social cost implications.

6.2 The household level (End users)

As part of our primary research, a survey of 100 households that currently use Chrysotile roofing material was completed in Colombo, Jaffna, Kandy and Gampaha. The survey sampling is structured to the extent that we covered a statistically significant critical mass of urban, rural and estate community households9.

9 Allocating 30 per cent of our sample size to cover the estate community has resulted in an average dwelling size that is much smaller (in our sample) than the (national level) estimates that we have used earlier that was based on available data from the Department of Census and Statistics and the Central Bank. Nevertheless, this survey provides great insights into the micro-level issues faced by each of the three types of communities that have been defined as rural, urban and estate.

Employees: 4,500 Dependents: 18,000 Indirect employees: 50,000 Dependents (indirect) 200,000 TOTAL: 272,500

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 33

According to the survey, the largest of the dwellings were found to be those in urban areas, followed by those in rural areas with the estate community houses accounting for the smallest size dwellings.

Chart 6.1 Sample sizes from household survey

Chart 6.2 Square foot area of the houses

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 34

Chart 6.3 Houses by sector and size of dwelling

Chart 6.4 Average repair cost of household

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 35

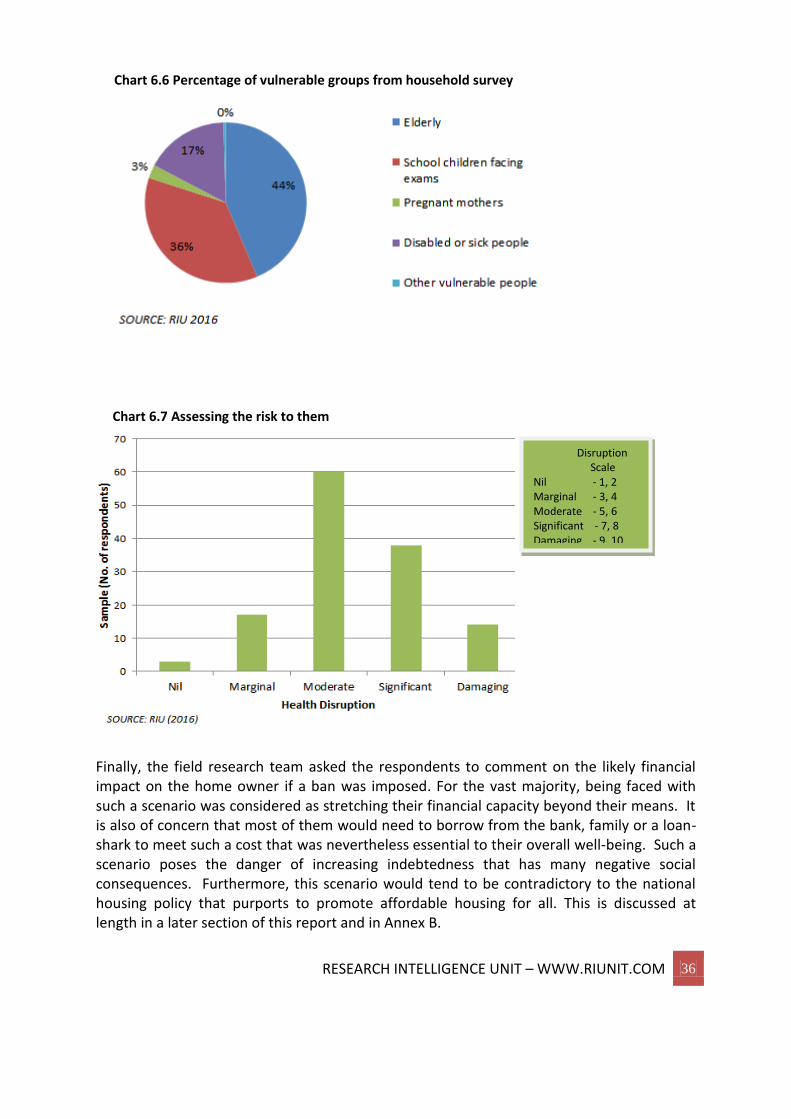

Where repair and replacement costs are concerned, the respondents to the survey (have for the most part) indicated a cost of around LKR 200,000 for a small house of between 500-1000 Ft2. However, the actual repair cost to a chrysotile roofing sheet can be as low as LKR 50. 7.3 Respondents were also asked about the potential disturbance to those living in their homes should they have to replace the entire roof arising from an immediate ban on Chrysotile. Even if the government did not introduce a ban that covered roofing that was already in use, a very likely consequence of a ban on the future sale of Chrysotile roofing sheets is that people will not have access to replacements for damaged sheets. They would then be faced with a situation of having to replace their entire roofing material. In such a situation, most people expect the disturbance to their household to be significant to severe. It is interesting to note that in the Sri Lankan cultural context, almost half of the homes surveyed had elderly people living under the same roof whilst 36 per cent of homes had children and 17 per cent had disabled or sick people residing within a family setting. As a result, the majority of people considered that there would be a significant negative health and education impact on their household from a situation where they had to undertake major changes to their roofing material.

Impact Scale Nil - 1, 2 Marginal - 3, 4 Moderate - 5, 6 Significant - 7, 8 Damaging - 9, 10

Chart 6.5 Disturbances to household

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 36

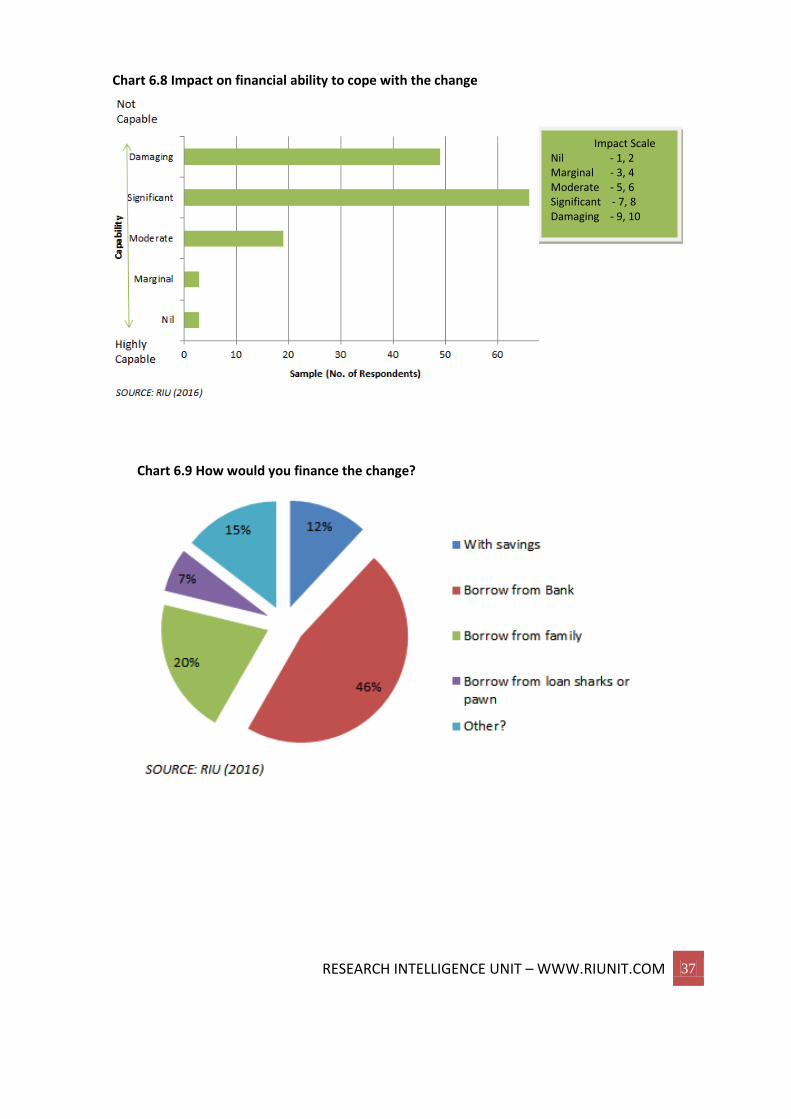

Finally, the field research team asked the respondents to comment on the likely financial impact on the home owner if a ban was imposed. For the vast majority, being faced with such a scenario was considered as stretching their financial capacity beyond their means. It is also of concern that most of them would need to borrow from the bank, family or a loan-shark to meet such a cost that was nevertheless essential to their overall well-being. Such a scenario poses the danger of increasing indebtedness that has many negative social consequences. Furthermore, this scenario would tend to be contradictory to the national housing policy that purports to promote affordable housing for all. This is discussed at length in a later section of this report and in Annex B.

Chart 6.6 Percentage of vulnerable groups from household survey

Chart 6.7 Assessing the risk to them

Disruption Scale Nil - 1, 2 Marginal - 3, 4 Moderate - 5, 6 Significant - 7, 8 Damaging - 9, 10

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 37

Chart 6.9 How would you finance the change?

Chart 6.8 Impact on financial ability to cope with the change

Impact Scale Nil - 1, 2 Marginal - 3, 4 Moderate - 5, 6 Significant - 7, 8 Damaging - 9, 10

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 38

6.3 Social infrastructure

6.3.1 Hospitals

In the government sector, the most significant in terms of buildings are schools and hospitals. These are also perhaps the most important in terms of the social impact that can affect children, the elderly and the sick. Government data indicates 9,662 operational schools in the island along with 1,085 hospitals that are under government administration.

However, due to the lack of any data available on the roofing materials of these buildings, the RIU conducted a primary research that covered 100 schools and 100 hospitals in four districts. According to the findings of this study, approximately 25 per cent of all hospital roofs in the survey had Chrysotile roofing with an additional 24 per cent having a mix of Chrysotile with clay tiles (8 per cent), concrete (8 per cent) or aluminum (8 per cent)

Chart 6.10 Total numbers of hospitals by type

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 39

Findings on hospitals10 If the above findings are extrapolated to the national level, a total of 153 hospitals will be directly impacted which represents some 29,042 beds across the island. In addition, a total of 146 hospitals use Chrysotile for part of their roofs. If we take this average as 50 per cent of the covering, it translates into 73 hospitals with 13,940 hospital beds.

6.3.2 Schools As with hospitals, there is currently no official data available on the roofing material composition of schools in Sri Lanka.

10 For the categorisation of hospitals in Sri Lanka, ten hospitals were selected under five different types - 2 District Hospitals, 2 Base Hospitals type A, 2 Base Hospitals type B, 2 Divisional General Hospital type A and 2 Divisional General Hospital type B followed by the highest number of beds in each type.

Chart 6.11 Findings on Hospitals

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 40

Findings on schools11 The research covered a sample of 48 school buildings in four districts. This research confirmed that 22 per cent had Chrysotile roofs while an additional 5 per cent had a mix of Chrysotile and clay tiles. Should these statistics be extrapolated to the national level, a total of 2126 schools will be directly impacted. This represents some 902,109 children island-wide. In addition, a total of 483 schools use Chrysotile for part of their roofs mixed with other materials. If this average is 50 per cent of the covering, it translates into 242 schools and 102,512 children.

11 The sampling methodology used in the study sought to represent the types of schools that are classified in Sri Lanka - two National Schools, two Navodya Schools, two Isuru Schools and six other schools (Private Schools) from each district.

Chart 6.12 Findings on Schools

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 41

6.4 Implications on the National Housing policy

According to government policy on housing, the main policy goal is to ensure the right to live in “adequate, stable, qualitative, affordable, sustainable, environment friendly and secure housing with services for creating a high living standard on the timely needs of the people.”

However, according to the findings of this study, there will be some contradiction between the stated goals of the government and banning Chrysotile, especially on aspects related to “stable”, “qualitative”, “affordable” and “environmentally friendly” goals as stated in the policy document given the challenge of finding suitable substitutes or alternative products.

In the meantime, the demand for affordable housing in Sri Lanka is gathering pace every year. According to the Central Bank, the estimated annual demand for new housing in Sri Lanka is estimated at between 50,000 – 100,000 units, but around two thirds of the incremental demand is not met. Consequently, the back-log continues to increase and the pent-up demand places further strain on the government as well as low income members of the population.

The twin pressure of urbanisation along with population growth trends will have the most severe impact on the urban population. According to the World Bank, Colombo, Gampaha, Kalutara and Kandy are amongst those districts that have the highest people-per-square-kilometre density.

People in the mid and lower income groups not only have the challenge of land affordability in urban areas, but also have to face the rising cost of construction material.12 Given that the National Housing Development budget (Capital Expenditure) for 2016 is LKR 6 billion (US$ 41,758,620), we can estimate the cost of the roofing component at between LKR 605 million and LKR 1.2 billion for 2016. In the event of a ban of Chrysotile, the cost of a roof could escalate by as much as 40 per cent, depending on the alternative material used by the government. Under a worst case scenario, the government would need to increase its housing budget by up to LKR 484 million in order to build the same number of houses or alternatively, reduce the total number of houses to be built by 8 per cent. Whilst the former option would take its toll on the state budget which is under considerable pressure to reduce the public debt burden, the latter would prove devastating on the people who already suffer from an affordable housing shortfall the National Housing Development

12

A World Bank report claimed that the cost of buildings has tripled from 1990 to 2010 because of the rapid increase in land prices, particularly in city areas, and also because of price increases and shortages of construction material. “Building materials that registered substantial price increases include sand (1,070 percent increase), timber (568 percent), and bricks (678 percent). Labour costs also increased by nearly 250 percent during this period,” according to the World Bank report.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 42

budget (Capital Expenditure) for 2016 is LKR 6 billion (US$ 41,758,620), we can estimate the cost of the roofing component at between LKR 605 million and LKR 1.2 billion for 2016. In the event of a ban of Chrysotile, the cost of a roof could escalate by as much as 40 per cent, depending on the alternative material used by the government. Under a worst case scenario, the government would need to increase its housing budget by up to LKR 484 million in order to build the same number of houses or alternatively, reduce the total number of houses to be built by 8 per cent. Whilst the former option would take its toll on the state budget which is under considerable pressure to reduce the public debt burden, the latter would prove devastating on the people who already suffer from an affordable housing shortfall13.

6.5 Summary of Social Costs

13 UPDATE (10-11-2016): The proposal made by Hon. Sajith Premadasa, Minister of Housing and Construction, to accept the National Policy on Construction and its implementation mechanism prepared by the National Advisory Council on Constructions under the provisions of Construction Industries Development Act no. 33 of 2014. This with a view of providing strategic leadership for all parties in the construction field, encouraging sustainable development reforms and improvements, promoting low cost and environmental friendly building materials and systems, suitable research promotions, compilation of standards and norms and promoting construction overseas, was approved by the Cabinet of Ministers.

Chart 6.14 Summary of social costs

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 43

7. The impact on the environment

7.1 Removal and disposal In the event of a blanket ban on Chrysotile, the first challenge would be that of removal and disposal. The three main considerations that need to be factored into our model for these have been identified as follows:- - Removal of material from roofs - Transportation of the material from the dwelling to the disposal site - The actual cost of disposal and maintaining the disposal site

7.1.1 Removal and transportation Starting with the cost of removal, our estimates are based on the current market rates for construction workers in Sri Lanka. However, as there is no regulation in force, the cost of special safety equipment has not been factored in (safety equipment could and should be used). As a result, we have arrived at a very conservative rate of LKR 30, 000 per 1000 Ft

2 of Chrysotile roofing or LKR 3 Ft2. For transportation cost from the dwelling to a dump site, we have again taken the standard rate based on the average vehicle hire cost which is a function of the cost of fuel. As there are currently no dump sites operated by the Central Environment Authority (CEA) that can be used for the purpose of Chrysotile disposal, it is assumed that provisions will be made to have dump sites at each of the 25 districts in the country. Therefore, we have taken a very conservative estimate of 10 kms average travel from dwelling to dump site at a cost of LKR 30 per km. However, if a ban takes place, it would be inconceivable that a material that the government deems to be “unsafe” could be removed and transported sans any safety equipment. In the industrialised world, extensive use of safety equipment characterises the removal process and transportation of Chrysotile sheets. If Sri Lanka imposes a ban that requires the removal of the sheets, then by the same reasoning, safety measures including equipment along with regulations would be needed to guide the process of removal and transportation. Consequently, the real cost may escalate significantly.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 44

7.1.2 Disposal According to available studies and estimations, some 50000 MT (in full) of hazardous waste is generated annually in Sri Lanka. Most of this hazardous waste is disposed in a haphazard manner in unsuitable locations. These malpractices lead to severe environmental and health issues. Being a signatory of the Basel Convention of the trans-boundary movement of the hazardous waste, Sri Lanka has taken some vital actions per the obligations of the convention. All signatory countries should develop and implement necessary legal provisions for the proper management of hazardous waste in the country. Whilst there are no specific guidelines for the disposal of Chrysotile, guidelines on disposal addresses several issues related to the selection of disposal sites and advise on minimising health risks, environmental impacts, public acceptance and costs. A general listing of various factors to be considered for siting hazardous waste disposal facilities is presented below. Specific concerns that come to the fore in the event of managing the safe disposal of Chrysotile include consideration of the following:-

Chart 7.1 Removal cost

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 45

Physical Constraints ● Surface soils

● Subsurface geology and aquifers

● Topography

● Surface water and streams, flooding

Ecological Constraints ● Flora and fauna

● Conservation value

● Habitat value

Human Values ● Landscape

● Recreation

● Historical/archaeological/cultural

● Population density

● Employment opportunities

Land Use

● Agricultural value

● Extractive industry/mining

● Water supply (surface and subsurface)

● Development potential

● Transportation corridor or utility use

● Land use designation (residential/industrial, etc.)

Waste Disposal Suitability ● Proximity to users

● Transport access

● Availability to utilities and services

● Adjacent land use - zones

● Site modifications

Given the lack of information available on the potential cost of local disposal, we have taken the Australian cost model for disposal and modified it to accommodate the local market conditions. Essentially, we have noted that the cost of disposal consists of labour (40 per cent) and land and equipment (60 per cent). Keeping equipment and land costs as the same for Sri Lanka, we have adjusted the labour costs to represent prevailing domestic market rates which are estimated at around 10 per cent of the Australian labour rate.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 46

Taking the existing stock of inventory in use in Sri Lanka (1.8 million), the total removal cost will be in the staggering range of US $11.25 billion with an average household spend of US$ 6,253. According to our estimates, removing and safely disposing all of the current stock will be more than four times the cost of existing stock.

7.2 Replacement preferences One option that none of the survey respondents selected was polymer roofing14 as they were unaware of its availability. Polymer roofing is a material that is set to enter the market in the near future. Polymer sheets are set to provide an alternative to Chrysotile in terms of shape and size of the sheets. However, this material does not compete well in terms of price and durability, especially under hot conditions, when longevity will be only around half of that of Chrysotile. The breaking load of polymer roofing is also much less than that of Chrysotile and its potential environmental impact is still unknown. The RIU primary research also focused on peoples’ preferences in the event that Chrysotile was no longer available in the market. Here, most home owners expressed their preference to switch to clay or cement tiles, followed by concrete roofs.

14

Polymer roofing specifically refers to a type of roofing which has not yet entered the Sri Lankan market.

According to Introduction of Fibre-Reinforced Polymers − Polymers and Composites: Concepts, Properties and

Processes; Martin Alberto Masuelli, Polymers are different from other construction materials like ceramics and

metals, because of their macromolecular nature.

Australian disposal cost (Ft2): US$ 10.5 (Australian labour cost component: US$ 4.22) Sri Lankan disposal cost (Ft2): US$ 6.76 (Sri Lankan labour cost component: US$ 0.422)

Chart 7.2 Alternative roof preferences

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 47

Nevertheless there is a large gap between peoples’ preferences and their willingness to pay for alternative roofing materials. The survey found that 40 per cent would not be willing to pay an additional 40 per cent for alternative materials whilst 46 per cent would consider it depending on their circumstances at the time. Only 14 per cent confirmed that they would be willing to pay an extra 40 per cent. Of those that did not want to pay 40 per cent more for their roofing materials, most were willing to pay a smaller extra amount, not exceeding 10 per cent of the current Chrysotile costs. A significant number were not able to consider increasing their roofing material budgets.

7.3 Environmental implications of alternatives

Scientists and experts in the field have defined four phases in the lifecycle of a roofing product - raw materials, manufacturing, service on the roof, and the end of lifecycle. Phase one of the lifecycle is where materials are extracted and transported for manufacturing, then refined into the final product and transported to the distributor or end user. On the roof the product reacts with the environment throughout its service life. After its service has expired, it reaches the fourth and final phase - the end of the lifecycle. Most green products involve recycling the material for other purposes or introducing it to the manufacturing process a second time. Thus, the final stage would also include some dumping of the waste material. According to the weight of research, evidence based on preference choices and budgets of households, any interruption to the supply of Chrysotile roofing sheets will inevitably lead to an immediate hike in the demand for clay tiles. However, producing clay tiles involves excavating clay from the earth’s crust where cement is only added in a small percentage. The excavations can go very deep or cutting off small mounds of land. However, serious

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 48

environmental consequences of such action can cause natural disasters such as landslides which have continued to cause deadly damage to the lives and properties in Sri Lanka at an alarming rate in recent years15. Clay soil retains water, minerals and even metals that the plants need for its growth. Removing the top clay layers will cause damage to these environments as well. According to environmental experts all soils cannot be used for tile production and the country will very soon run out of clay to produce tiles. Consequently, there will be very serious issues of sustainability if clay tiles become the preferred alternative. In addition, the degradation or weathering of the final product and burning will release greenhouse gasses giving rise to global warming which will be against the Paris Agreement that Sri Lanka is also a part of. This is a long-term goal of keeping increases in the global average temperature to well below 2°C above pre-industrial levels (Annex A provides further information in this regard).

7.4 Manpower implications

Typically, Chrysotile roofing is the least demanding in terms of manpower as compared with

alternative materials for building new houses. For example, the use of wood for rafters

differs greatly between various types of roofing materials. Consequently, the demand for

labour in the construction process will increase significantly, especially for tile and concrete

roofs.

15 According to the Government of Sri Lanka Disaster Management Centre (May

2016), 301,602 people have been affected by floods and landslides in May. 104

people are known to have died and 99 people were missing. An estimated 21,484 people were still displaced as a result of the disaster and are living in camps and temporary accommodation - including schools. It is estimated that 623 houses have been destroyed and 4,414 have been damaged.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 49

In the current environment where there is a short-fall in skilled construction workers, partly due to worker migration to the Middle East where there is a much higher earning potential, any sudden hike in demand for construction labour will result in long delays for work to be completed. Such a situation would also exert upward pressure on construction workers wages which will serve to further escalate the cost of construction. As described earlier, the cost of construction as well as land prices pose a serious threat to the goal of providing affordable houses to large sections of the population.

7.5 Material performance and durability

According to the feedback from the residents of homes with Chrysotile roofing, we can note that the majority is moderately satisfied with Chrysotile while a significant number also complained about heat and repair costs. For many of those interviewed in the survey, a Chrysotile roof represented an upgrade from iron sheets which are still popular in the low income housing category. The overall feeling was that Chrysotile material was not perfect but was the best of what is considered as affordable.

Chart 7.4 Annual demands for occupation in the construction Industry

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 50

According to a study that was published in the Built-Environment journal of Sri Lanka, (following extensive research and testing), Chrysotile was found to be give the highest ranking material when compared to alternatives on thermal performance, strength, availability, health hazards, cost and other important parameters. The RIU’s own primary research findings which include a qualitative assessment on the performance of alternative materials are given in Annex A. 7

Chart 7.5 Summary of roofing materials

Chart 7.6 Roofing material cost per ft2

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 51

SOURCE: RIU (2016)

Assuming the lifespan of a

Chrysotile roof to be 40 to

50 years, the following is the

replacement cost

Chart 7.7 Housing Inventory using Chrysotile

Chart 7.8 Cost of replacing Chrysotile roofing material during a 40 to 50 year life cycle

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 52

As illustrated above, the long-term implications of switching to alternatives need to be considered with reference to the roof replacement schedule that is expected over the coming years as those Chrysotile roofs that are currently in use will need to be replaced in future years with more expensive alternatives. For example, the Chrysotile stock that was installed in 1970 should have been replaced by 2010, given a 40 year durability assumption. With this assumption, it is noted that replacing Chrysotile roofs with concrete will cost almost three times more than if it is replaced with new Chrysotile sheets. Consequently home-owners will experience serious challenges in a future scenario of non-Chrysotile availability.

7.6 Other Implications of switching to alternatives

From the results of the survey, it is clear that for the vast majority of people, the only options they would consider are concrete and tile roofing. However, given the difference in cost between tiles and concrete slabs, it is expected that most people will opt for tiles. At present, the production of Chrysotile requires an estimated 1500 tons of cement per day for the four local manufacturers of the Chrysotile fibre cement roofing sheets. Cement suppliers have claimed that the Chrysotile industry is their largest customer. As such, if the production of Chrysotile ceased and people switched to tiles, the impact on the cement industry would be severe. One industry expert claimed that the cement industry would collapse due to such a sudden drop in demand.

Switching to tiles would also have important environmental implications given that the demand for sand and clay would escalate beyond the resource availability of the Island. The increasing scarcity of river sand in particular is reflected in the price escalation that has taken place over recent years.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 53

7.7 Summary of environmental costs

The key findings from other countries point to a need to mitigate health and safety risks from the removal and disposal, including the release of fiber into the immediate environment. Such measures will be costly to the government. There is also a serious mismatch between preferences on alternatives and their budgets for more expensive materials. The product that people would want to switch to and their ability to finance the switch are not compatible and as a result, many people may remain in dwellings with iron. sheets.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 54

Less Chrysotile is very likely to result in more carbon emissions and increased risk from landslides due to the switch to clay tiles. There will also be related demands on construction labour which are likely to have implications on the cost of construction.

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 55

8. Overall macro-economic impact According to the findings of this study, the direct impact of a potential ban on Chrysotile in Sri Lanka is very significant. The annual value of new roofing material is estimated at around US$ 146.429.In addition, there is an estimated US$ 55-110 million worth of capital investment that could be rendered unproductive. This would lead to the loss of some US$ 122.1 million in the form of wages for workers who are either directly or indirectly dependent on the industry. Furthermore, there would be direct losses to the Department of Customs of almost US$ 2 million in addition to the losses in profit to the producers estimated at US$ 100 million per annum. It is important to note that Chrysotile has been the preferred choice of roofing material for low and mid income families as they upgrade from cheaper and less robust materials to one that they consider as sustainable and able to meet the basic needs in terms of shelter. The quality of the product and its durability has in fact made it a product of choice also for higher income households, especially in the Western Province. Consequently, we expect Chrysotile to account for an increasing share of the housing inventory in the country (in the absence of any ban).The current value of total inventory in use (at 2016 market prices) accounts for a staggering US$ 2.726 billion or 3.38 per cent of the country’s GDP.

Chart 8.1 Percentage of households using Chrysotile inventory

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 56

In addition to the direct costs, the indirect or induced costs have been presented in this report and our findings indicate some level of risk to vital industries, including tea and tourism from any possible issues regarding trade with Russia in particular. In addition, there is an un-opened “can of worms” with regard to litigation where the potential for damaging legal action remains as a threat that would lead to losses for the tax-payers. It is also important to note that the highest concentration of Chrysotile is in the Western Province where there is the highest level of economic activity and contribution to GDP. Therefore, disruptions would impact disproportionately on the most important geographic area of the Island where GDP contribution is concerned.

From an international perspective, not all countries have introduced legislation regarding the use, control and import of asbestos. Developing nations such as China, India16 and Russia have not yielded to pressure from the industrialised world’s attempts to reduce the amount of exposure to asbestos and are still using Chrysotile for materials such as corrugated asbestos roofing sheets for schools, factories and homes. There have been several attempts by third party organisations to persuade governments to take action, but so far there has not been any action taken. Instead, nations including Thailand, Vietnam and India have focused on strengthening the safe use policies for the material and thereby averted any risk of major economic loss to individuals as well as the country as a whole.

16 HISTORIC DECISION FROM INDIA’S SUPREME COURT: In a very important decision rendered on 21 January, the Supreme Court of India refused to grant the petition to ban asbestos that was filed by an NGO connected to the anti-asbestos movement. Rather, the Court ordered the national and state governments to better regulate the use of asbestos. This historic decision opens the door to the strategy proposed by Quebec chrysotile asbestos producers to export, along with the fibre, its unique expertise on safe and responsible use. • NO to the petition for a ban on all uses of asbestos • YES to better regulation • THE COURT CRITICIZED THE ANTI-ASBESTOS NGO BEHIND THE PETITION for the petition’s lack of authenticity and the failure to prove its claims ( http://www.chrysotile.com/data/inde_janvier2011_en.pdf)

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 57

ANNEX A - SUMMARY OF ENVIRONMENTAL IMPACT FEEDBACK FROM EXPERTS

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 58

Type of roofing material

Durability Cost (Ft2) Environmental Impact

Is it imported or locally produced

Other information such production, strength etc.

Polymer roofing sheets

May last within 5 to 7 years depending on the Polymer and the weather conditions

Expensive ,relative to metal

Less degradable and can accumulate in the environment if not treated well

Both Plastic does not handle extreme heat very well

Plastic tends to occasionally chip when metal will not as easily

Will provide natural lighting for indoors

If damaged during installation or in extreme weather a chip or crack can spread to ruin the entire panel

Plastic has more aesthetic appeal than metal

Sometimes needs a special kind of paint if you want to paint the plastic panels

Not as flimsy as metal and the weight is usually better for extreme weather.Commonly more water-tight than metal.

Clay tiles Clay tiles can last for as long as 100 years. However, due to small hazards like coconuts falling on the

Clay tiles cost about 30 per cent more than concrete tiles US$10 to 15 Ft2

Made from a natural earth derived material, they are easily recycled. However, increasing production can raises issues of sustainability.

Clay tiles are resistant to strong winds and cannot be destroyed in a fire. Because of the way they are shaped, Clay tiles protect the underlayment of your roof, while also creating an air pocket thereby helping to insulate and isolate any unwanted heat or cold from being transferred to your home’s attic space.

Table 8.2 Summary of Environmental Impact – Feedback from experts

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 59

roof or the presence of monkeys and other animals on the roof, regular breakage and replacement characterises clay tile roofs.

Clay roofing tiles have a water absorption of about 6 per cent. While most Clay roofing tiles weigh only 600 – 650 pounds per square. In colder climates, Clay tiles have the tendency to crack or shatter due to freezing and thawing cycles. As a result, Clay tiles are mostly found in warmer climates. Since Clay is a naturally occurring material, clay tiles maintain their original color for years despite being subjected to weather conditions.

Zinc Aluminium Sheets

Expensive Not environmentally friendly since metals are a threat to the environment

Coating composition of Aluminum 55 per cent, Zinc 43.4 per cent & Silicon 1.6 per cent, and a polyester based finish coating on both sides of the sheet to protect the material from adverse corrosive elements.

Metal Sheets17 Metal roofs have been found to last between 40 and 70 years, but it depends on the material

Expensive Metal roofs can be quite noisy in the event of heavy rain or hail compared to architectural roof shingles or tile shingles.

Metal roofs also can withstand strong winds and is a resilient roofing type. You will not have to worry about maintenance and upkeep if you go the metal roofing route. A metal roof system is an energy efficient roofing type, because it reflects solar heat and can cut back on cooling costs

17

This refers to Metal sheets in general and does not cover one type - includes Aluminium and Silicon coated steel

RESEARCH INTELLIGENCE UNIT – WWW.RIUNIT.COM 60

that you choose to make your metal from.

immensely. The metal roofing will not go up into flames in the event of a lightning strike.

Commonly quite cheap and affordable

Is wholly more durable than plastic

Constructing a roof with corrugated metal is difficult to work with in windy weather because it is light-weight

Will have to be treated for rust

Can dent in extreme weather