-

8/2/2019 Solving Debt Crisis

1/9

M any advanced economies, including the United Statesand various

countries in the Euro Area, face a majorcrisis due to their

accumulation of sovereign debt and

fiscal deficits. In the United Statesthe worlds biggest

economythe federal government deficit is running at

10 percent of GDP and publicly held federal debt lurched

from 36 percent of GDP in 2006 to 53 percent in 2009.

The question now is how to get out of the great debt

crisis before debt markets close.

No country can easily grow itself out of a debt crisis.

Recovery from the current episode of rapidly increasing

debt is especially difficult because a turnaround is needed

at a time when structural weaknesses have accumulated,

including a slowdown in innovation; there are increasing

shortages of human capital; and the structural reforms

needed to strengthen competitiveness and growth are not at

the top of the agenda. Country-specific solutions to restart

the engine of growth are, therefore, extraordinarily

complex.

Escaping the Sovereign-Debt CrisisProductivity-Driven Growth and

Moderate Spending May Offer a Way Out

by Stephen Sexauer and Bart van Ark

no. 339 December 2010

Sovereign debt and fiscal deficits are strangling many advanced

economies.

Policy choices are complex, but there is an escape strategy that

does not

require draconian budget cuts or risky debt-financed stimulus

spending.

The solution is based on two principal policy levers:

encouraging productivity-

driven GDP growth and keeping government spending per worker

constant.

When governments align their policies with these growth

principles, a fiscal

surplus will eventually materialize and the ratio of government

debt to GDP

will decline substantially within one to two decades.

Executive Action Series

-

8/2/2019 Solving Debt Crisis

2/9

What are the policies that help revive growth? Which

country-specific conditions call for austerity? Which

call for more stimulus? How big should government be?

What is the correct level of debt to GDP? In recessions

with deep job losses, how large is the worker safety net?

What are the incentives for workers to retool and migrate

to new jobs? What government policies will inspireconfidence in

the bond holders who are needed to fund

maturing debt and fiscal deficits until the crisis resolves?

When it comes to finding an answer to these questions

and an exit out of the debt crisis, two policy principles

appear to dominate all others: the encouragement of

productivity-driven GDP growth and restraining the

growth in government spending to at least the point

where medium-term government spending per person

remains constant until the crisis resolves. When

governments sustain such policies, a fiscal surplus will

eventually materialize and the ratio of government debt

to GDP will decline substantially. During the 1990s,

this approach worked in Sweden and Finland followingtheir crises

in the early years of the decade, as well as

in Canada, the United Kingdom, the United States,

and several Asian countries. These principles can also

help relieve todays debt crises in Greece, Ireland,

Portugal, Spain, the United Kingdom, and the United

States, as well as in other advanced economies facing

fiscal deficits and excessive debt-to-GDP levels.

2 executive action escaping the sovereign -debt crisis the

conference board

A Simple Framework for Reducing Debt

The framework used in this article is based on two factors:

productivity growth and the increase in government spending

relative to GDP growth. The use of these measures is based

on

two long-term policy goals. The first is keeping spending

growth

below GDP growth until the crisis is resolved. The default

rate

of government expenditure growth should, on average, match

the growth of population plus inflation. This will keep

average

real per person consumption of government resources close

to constant. Governments can temporarily decide to raise

government spending above the growth of population,

especially when employment falls during recessions.

However, such a rise will need to be compensated by

subsequent periods of spending growth below the rise

inemployment and inflation.

The second target that must be met is keeping the economy

growing faster than the growth in employment and inflation.

Since GDP growth equals employment growth (N) plus inflation

(I) plus productivity growth (P), productivity is the key to

both

sustained economic growth and resolving the debt-to-GDP

crisis.

Productivity growth, much more than growth in employment,

offers an avenue to reduce debt to more sustainable levels.

Without productivity growth, the only way to reduce debt is

for spending to fall below the combined growth rate of popu-

lation and inflation, which would make people worse off.

As long as the economy grows beyond population and inflation

growth, and some of the productivity-driven growth is used

for

debt reduction rather than spending increases, the

combination

of these policy principles should cause the debt-to-GDP ratio

to

fall. There are, of course, some nuances left out of this

model.

One of the most obvious is the use of tax revenue as a

source

for debt reduction. In a recovery from a recession, some

increased tax revenue may be the result of GDP growth

itself.

However, a crisis is resolved by the compounding of relative

growth rates government revenues that grow faster than

outlays over a sustained period that can last up to 20

years.

It is reasonable to assume that tax revenues will not grow

faster

than GDP over the long term, but revenue growth can go

moderately beyond the growth in GDP in the short term.

How fast the level of debt to GDP falls can also depend on

specific policy choices. For example, governments need to

carefully time their policy decisions on spending and

productivity

enhancement. The productivity bonus that is created can be

used to reduce debt or create further productivity-driven

growth,

which serves to strengthen the mechanism itself. Governmentsalso

need to raise their own (public) productivity levels, as

lower productivity rates of government service will either

increase the pressure on the private sector for productivity

increases or require further spending cuts.

While it may seem that many policy elements are missing

from this framework, short-term interest rates, tax

structures,

multipliers, trade, regulation, long-term target debt-to-GDP

ratios,

and governments active role in economic enterprise are

implicit

in the model. For each country, the sum total of the effects

of

these policy decisions results in the four key growth rates:

GDP, productivity, expenditures, and revenues. Any

combination

of policies policies unique to an individual

countryscircumstance will work if they result in (1)

productivity-driven

GDP growth and (2) government expenditure growth that

matches the level of employment growth and inflation.

An appendix, which contains a full overview of the model and

some historical examples and projections for different

countries,

is available on request from The Conference Board Business

Information Service ([email protected]).

-

8/2/2019 Solving Debt Crisis

3/9

Lessons from HistoryThere are several examples from recent

history that show

how the combination of strong productivity-driven GDP

growth and an increase in government expenditure that

stays below the rise of GDP can cause a debt crisis to

melt away. In 1995, the Canadian government saw its

debt-to-GDP level rise to 71 percent. The Canadiangovernments

response was a multiyear effort to get its

own house in order.1 Canada set a benchmark for GDP

growth, fiscal deficits turned to surpluses, and the level

of debt to GDP fell rapidly. This occurred in the relatively

short time frame between 1995 and 2006 (Chart 1).

It is important to note that everythinggrew during this

period. Although government spending grew by 3.2 percent

per year, the Canadian economy grew at 5.4 percent per year

(Chart 2). The 2.2 percent difference between government-

spending growth and GDP growth came partly from

productivity growth and partly from slowing growth ingovernment

expenditures that was below the growth of

employment (N) plus inflation (I). It should be noted,

however, that the focus was on measures that reduced the

growth in spending rather than on deep cuts. In addition,

revenues grew by 4.9 percent, a rate that was slower than

GDP, but faster than expenditures. Employment grew at

a swift 2 percent per year, but work was also done more

productively at 1.4 percent per year.

The sum total of Canadas successful policy decisions

is summarized in Chart 1. By 2008, Canadas level of

federal debt to GDP had fallen to 22 percent. As a result

of the end of the 20082009 recession, Canada has seen

some rise in its debt-to-GDP ratio. The country, however,

appears to be on track to grow its GDP and to further

decrease its debt-to-GDP ratio, provided it can grow

productivity beyond the moderate 1.5 percent it has

recently experienced.

To be sure, certain environmental factors led to Canadas

success during the late 1990s and early 2000s. The gov-

ernments efforts to grow the nations economy while

reducing its ratio of debt to GDP were undoubtedly

blessed by the rapid growth of the global economy.

The country also managed to raise employment at a

growth rate2 percent per yearwell above the growthrate of the

population. So how does Canadas successful

application of the model compare to that of other countries?

A look at some other economies through the prism of

growth-driven reductions in debt to GDP reveals that

the results in Canada are not that unique. In Sweden,

a fall in the debt-to-GDP ratio from 83 percent to under

50 percent was driven by 2.3 percent per year productivity

growth and 0.9 percent labor growth from 1996 to 2008.

During the same period in Finland, productivity grew

2 percent per year and debt to GDP fell from 57 percent

to 34 percent. The United Kingdom experienced a similardecline

in both the late 1980s and the 1990s. Asian

economies that made policy changes in response to the

regions debt crisisIndonesia, the Philippines, and

Thailandalso saw similar declines in their levels of

debt to GDP in the early 2000s.

1 Budget in Brief, Department of Finance, Canada, 1995, p. 4

(www.fin.gc.ca/

budget95/binb/brief.pdf).

3 executive action escaping the sovereign -debt crisis the

conference board

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Canadas Federal Debt-to-GDP Ratio: 1990-2008

Chart 1

0

1

2

3

4

5

6%

Nominal GDP

growth (N+I+P)

Employment (N) +

Inflation (I) +

productivity (P)

growth

Government

expenditure

growth (e)

Government

revenue

growth (r)

N

I

P

g

The Sources of Canadas GDP Growth

and Debt Reduction: 1995-2006

Chart 2

g 5.4% = Nominal GDP growth = N + I + P

r 4.9% = revenue growth

e 3.2% = expense growth

0.78 = ratio government growth to N + I =

0.90 = ratio revenue growth to GDP (N + I +P)

N 2.0% = employment growth

I 2.1% = inflation (GDP deflator)

P 1.4% = productivity (GDP - N - I)

e

r

-

8/2/2019 Solving Debt Crisis

4/9

The Euro Area has not adopted a balanced-budget policy,

but the Stability and Growth Pact (SGP) does require

members of the euro zone to keep fiscal deficits within the

range of 3 percent and a debt-to-GDP ratio of 60 percent.2

As in the United States, the agreements were largely not

adhered to, especially during the most recent crisis when

member states were allowed to temporarily increase theirbudget

deficits beyond 3 percent. During the 20082009

recession, these budget rules were temporarily shifted

aside, and the debt-to-GDP ratios began to increase to

unsustainable levels in a number of countries, although

there are large differences between them. At the same

time, and just as important, productivity growth in the

Euro Area was dismaljust over 1 percent for the

19952008 period. These low rates of productivity

growth will make the resolution of the debt-to-GDP crisis

in the Euro Area countries long, difficult, and uncertain.

Applying the Productivity and Spending

Framework to the United States

From the late 1980s through the 1990s, the United States

achieved results similar to those of Canada. In 1985,

the Gramm-Rudman-Hollings Balanced Budget Act was

adopted to create spending caps on all federal budget items

and, thereby, reduce the deficit and produce a balanced

budget. From 1985 to 1999, GDP grew 5.9 percent per year,

productivity grew 1.7 percent per year, and the growth of

U.S. spending was 4.3 percent per year (about the same as

the increase in the working population plus inflation).

This put the United States on a path to a budget surplus.

By 1998, the accumulated policy decisions of both

Democratic and Republican administrations had produced

sustained economic growthand a budget surplus from

1998 to 2001. If the Gramm-Rudman-Hollings spending

controls had been maintained into the 2000s, the U.S.debt-to-GDP

ratio would have been much lower when

the most recent recession began in 2008.3

A manipulation of the framework assumptions can high-

light alternative paths to the achievement of a beneficial

debt-to-GDP ratio. Chart 3, for example, provides the his-

torical record of the relevant variables for the United

States

from 1995 to 2006. It shows that the growth of government

expenditure in the United States exceeded employment plus

inflation growth. Chart 4 compares the actual debt-to-GDP

ratio (the solid line) with two calculations. The first (=1)

is based on a growth rate of government expenditurethat equals

the growth rate of employment and inflation.

In this case, the difference between government expenditure

and GDP growth would have been exactly the same as

productivity growth, and the debt-to-GDP ratio would

have fallen to 27 percent by 2006 instead of the actual

level

of 36 percent. The second (=.78) alternative calculation

uses the Canadian 19962006 ratio of expenditure growth to

employment plus inflation growth (compare with Chart 1).

In this projection, debt to GDP in 2006 might have been

as low as 20 percent.

4 executive action escaping the sovereign -debt crisis the

conference board

0

1

2

3

4

5

6%

Nominal GDP

growth (N+I+P)

Employment (N) +

inflation (I) +productivity (P)

growth

Government

expendituregrowth (e)

Government

revenuegrowth (r)

I

P

g

g 5.5% = Nominal GDP growth = N + I + P

r 5.4% = revenue growth

e 5.2% = expense growth

1.46 = ratio government growth to N + I =

0.97 = ratio revenue growth to GDP (N + I +P)

N 1.4% = employment growth

I 2.2% = inflation (GDP deflator)

P 1.9% = productivity (GDP - N - I)

The Sources of U.S. GDP Growth

and Debt Reduction: 1995-2006

Chart 3

N

e r

0

0.1

0.2

0.3

0.4

0.5

0.6

Actual With =1 With =.78

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

U.S. Federal Debt-to-GDP Ratio: 1990-2006

Chart 4

2 For more on the SGP, visit the European Commission Economic

and Financial

Affairs website

(ec.europa.eu/economy_finance/sgp/index_en.htm).

3 For a more detailed analysis, please see the appendix of this

report, which

is available on request from The Conference Board Business

Information

Service ([email protected]).

-

8/2/2019 Solving Debt Crisis

5/9

The framework can also be used to calculate how many

years it will approximately take an economy to grow out

of a debt crisis. Chart 5a shows an aggressive future growth

scenario for the United States. This scenario assumes that

the growth in government expenditure will, at least for a

significant period, be reduced to 0.8 of employment plus

inflation growth, productivity will increase by 3 percent,

employment will grow at 1 percent, and inflation will rise

by 2 percent. This projection also assumes that tax revenue

can rise faster than GDP (1.1 times), as GDP growth itself

provides a major impetus to more tax revenues. Under this

aggressive scenario, U.S. debt will increase to 59 percent

of GDP by 2012, drop to 50 percent by 2017, and, if sus-

tained, even drop to 30 percent by 2021 (Chart 6).

Chart 5b envisions a much more pessimistic, slow-growth

scenario. In this projection, productivity only grows by

2 percent, as the potential for innovation and growth

weakens; employment growth reaches only 0.5 percent,

assuming the unemployment rate will remain high;

and inflation will be only 1 percent due to deflationary

pressures. The growth in government expenditure in

this scenario cannot be easily reduced below employ-

ment plus inflation growth, and revenues are set to grow

at the same rate as GDP. In this pessimistic scenario,

as can be seen in Chart 6, the federal debt-to-GDP ratio

increases to 73 percent by 2019, drops to 50 percent

by 2026, and then reaches 30 percent by 2035.

The dramatic differences in terms of the size and the pace

of

the reduction in debt-to-GDP ratios between the aggressive

and slow-growth scenarios may come as a surprise, given

the small differences in the assumptions in the scenarios.

These differences, however, are the result of compounding

critical variables at different rates for a long time.

Small differences in growth rates can produce markedly

different outcomes if GDP and revenues grow faster than

expenditures. The good news is that a commitment to the

principles outlined here, slower expenditure growth, and

productivity increases will pay off surprisingly fast once

revenue growth overtakes expenditure growth.

5 executive action escaping the sovereign -debt cris is the

conference board

The sources of U.S. GDP growth and debt reduction from 2009

onward

5a Aggressive growth scenario 5b Slow growth scenario

0

1

2

3

4

5

6

7%

g

P

I

Ne

r

Nominal

GDP growth

(N+I+P)

Employment

growth (N) +

inflation (I) +

productivity (P)

growth

Government

expenditure

growth (e)

Government

revenue

growth (r)

g

P

I

N

e

r

Nominal

GDP growth

(N+I+P)

Employment

growth (N) +

inflation (I) +

productivity (P)

growth

Government

expenditure

growth (e)

Government

revenue

growth (r)

0

1

2

3

4

5

6

7%

Note: These scenarios use revenue- to-GDP ratios of .18. The

revenue-to-GDP ratio is rapidly rebounding from its extreme

cyclical low

of 14.8 percent in 2009, rising to 16.3 percent in the second

quarter of 2010.

Different growth scenarios may have very different

implications for the reduction of the debt-to-GDP ratio

Chart 5

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Actual Slow growth Aggressive

1990

1994

1998

2002

2006

2010

2014

2018

2022

2026

2022

Scenarios for the level of U.S. debt to GDP

Chart 6

2026

2030

-

8/2/2019 Solving Debt Crisis

6/9

As the economy assumes a sustained dynamic through

productivity growth, revenues will catch up quickly with

expenditures, which have accrued more slowly, and the

total debt relative to an ever-increasing level of GDP will

begin to shrink.4

These results demonstrate the importance of a well-established

framework for fiscal policy anchored in

these two principles. Under a focused productivity and

spending policy framework, the United States could grow

itself out of its debt-to-GDP crisis within one or two

decades if it adopts policies that support productivity

growth while reducing expenditure growth below the

growth of GDP. This does not mean that these goals are

easy to achieve or that they will not require difficult

choices. The results do suggest, however, that the

reduction of debt can happen without such drastic

measures as across-the-board cuts in total government

expenditures or difficult-to-reach growth targets (as highas 4

or 5 percent) for sustained productivity growth.

The Power of ProductivityAn important premise of the framework

is the need for

productivity growth to account for the differences between

government revenue growth (which, in the long term, equals

GDP growth) and baseline government expenditure growth.

In other words, productivity is the most important factor

in the reduction of debt to GDP. Its power stems from its

influence on economic growth and prosperity and its ability

to create a virtuous cycle for sustainable growth.

Productivitymeasured as the growth of productivity

output over the growth in resources (labor, machinery,

etc.)has a number of underlying drivers. These include

investment in and the efficient use of new technologies

(e.g., information and communication technologies), a

better use of human capital (in particular, worker skills),

efficiency measures that smooth work processes on the

shop floor, and improvements in the supply chain and

similar trade infrastructures. Productivity is the only way

to

avoid a decline in returns on the investments by businesses

(in capital and labor), individuals (in their skills), and

the

economy as a whole (in education, infrastructure, etc.).

There are two categories of productivity growth. The first

includes the efforts of various firms to narrow the gap

in efficiency. Companies continuously adopt best practices

that help them produce at the highest possible levels of

efficiency. These practices improve the skill level of their

workers, smooth procedures, focus product portfolios to

reduce downtime, and set up more efficient productionmethods to

tailor products and services to the needs of their

clients. Governments can help these efforts by improving

conditions for efficiency gains, including the provision

of an information and communications technology

infrastructure and improving the link between skill

requirements and the educational system. Governments

can also help efficiency by focusing on incentives that

lead to reduced rigidities in the labor and product markets

and encouraging incentives to stimulate competition that

will push companies to improve or go under.

The second source of productivity growth comes frompushing the

productivity frontier. Once companies adopt

similar best practices, the next step is to invent and

innovate,

to become even better at raising output relative to the

inputs.

This type of productivity growth can come from improving

production processes, but can also come from bringing new

products and services to the market. Again, governments

can help through the provision of subsidies or tax credits

for

research and development, investment in higher education,

and efforts to establish a framework for intellectual

property

that finds a balance between protecting the inventor and

supporting an ideas diffusion.

The call for increased productivity rather than more jobs

may come as a surprise, as many see productivity as leading

to job cuts that can slow growth. A slow recovery in

employment can be the result of productivity growth in the

short run, especially in the depth of a recession. However,

in

the medium and longer term, it is productivity and its

ability

to cause the transition toward a higher skill level in the

workforce that creates growth and a higher standard of

living. Without productivity growth, additional jobs only

create as much output as the required inputs, leading to

stagnant wages and no movement toward consumption

and growth in the long term. The policies that resolve a

debt-to-GDP crisis are the same policies that create a

growing economy. Both policies promote investment in

human capital and physical capital and in technology and

innovation. Both promote more work and smarter work.

6 executive action escaping the sovereign -debt crisis the

conference board

4 Moreover, the actual starting levels of the debt-to-GDP,

revenue-to-GDP, and

expenditure-to-GDP ratios can also have a major impact on the

calculation.

For example, the U.S. example assumes a revenue-to-GDP ratio of

0.18,

which has been the average for 30 years. If the revenue-to-GDP

ratio at the

cyclical low in 2009 (0.15) is used instead, the peak in the

debt-to-GDP ratio

would not have come after three years (59 percent), but after

six (72 percent).

The 50 percent level would be reached after 15 years, not

eight.

-

8/2/2019 Solving Debt Crisis

7/9

Slowing, Not Slashing

Government SpendingAnother primary premise of the productivity

and spending

framework is that real government spending per person

needs to remain constant until the crisis resolves (i.e.,

expenditure growth equals the growth of employment plus

inflation). This is a good starting point because, on average,no

absolute cuts in government spending per person are

required, although reallocations and redistributions remain

important policy choices. The annual flow of productivity-

driven GDP above the combined growth of population

and inflation can be allocated to debt and tax reduction

or more investment in productivity-enhancing measures

that strengthen a virtuous feedback loop. A country can

spend all its productivity growth on debt reduction,

which affects the numerator of the debt-to-GDP ratio, or it

can reinvest part of it in growing the denominator (GDP)

even faster. The virtues of reinvestment as a policy are

commonly debated, and reinvestment requires carefulpolicies to

maintain sustained increases in productivity.

When a country is caught in a debt crisis at the same time

that it is experiencing a demographic or political cycle

of large demands for increased government spending

(e.g., because of larger entitlements), the power of the

productivity and spending growth framework is that it

focuses policy on the bottom line of government spending

growth versus GDP growth. This emphasis strongly

reinforces the view that, over time, policy decisions must

result in growth and increases in government spending

cannot exceed increases in GDP growth.

Government-spending growth can exceed the growth in

employment plus inflation for periods of time, but any such

increases in government spending can only be temporary.

If government expenditures grow at the GDP growth rate

rather than at the growth rate of employment plus inflation,

the debt-to-GDP ratio would continue to rise forever.

For a temporary period, a country can choose to be on

this path, which most countries are now following in

response to the global recession. However, at some point,

a nation must focus on keeping the expenditure growth

per employed person constant (as in the case of Chart 5b

on page 5) or (as in the case of the aggressive growth

scenario in Chart 5a on page 5) below the growth rate

of employment plus inflation, although this will make

people worse off on average. A productivity and spending-

oriented policy setup will help a country move from crisis-

level debt-to-GDP growth rates to a more self-sustaining

growth rate.

As difficult as the policy choices required to slow spending

are, the framework suggests workable solutions that do

not require deep cuts or endless deficits. For example, if

policymakers in the United States could maintain a deficit-

based stimulus at the growth of employment plus inflation

and stimulus funds could go to the growth-enhancing invest-

ments outlined above, the stimulus could result in morepeople

working more productively and initiate a virtuous

feedback loop. Similarly, a policy to reduce business and

income tax rates could also pass the test if the result was

to raise private investment in companies that grow jobs

and create productivity skills and tools. (If applied

properly,

these same principles could work in other countries.)

With these policies, the United States could get back to

a 50 percent debt-to-GDP ratio in as little as nine years.

The growth combination that leads to this result is 6

percent

nominal GDP growth, 4 percent real growth (driven by

productivity growth), and faster-than-GDP revenue growth.

While such growth rates look outside the realm of

currentpossibilities in the short term, all of these rates are

within

the history and capability of the U.S. economy.

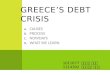

Can Greece and Spain Be Rescued by

the Productivity-Spending Framework?

These principles can also be applied to countries that face

the toughest possible environments with regard to debt and

deficit. Chart 7 shows the number of years needed to grow

out of the current debt-to-GDP crises in Greece and Spain,

which are two examples among several debt-ridden

European economies. We assume an employment growth

rate of 0.5 percent for Greece and 1 percent for Spain.

For both countries, we assume an inflation rate of 2

percent.

Productivity growth rates are 3 percent for Greece, which

still has significant catch-up potential, and 2 percent for

Spain. We also assume that revenue will grow at the rate of

GDP and the governments of Greece and Spain will grow

at 0.8 times population plus inflation. All of these growth

rates are reasonable and within historical precedent.

7 executive action escaping the sovereign -debt crisis the

conference board

0

20

40

60

80

100

120

140%

Greece actual Greece projection

Spain actual Spain projection

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

Greece and Spain Debt-to-GDP Ratios

Chart 7

-

8/2/2019 Solving Debt Crisis

8/9

When all of these factors are taken into account, Spain

would require 15 years to reduce its level of debt to GDP

to 50 percent and Greece would need 16 years to achieve

the same result.

Given the big difference in the 2009 levels of debt to

GDP in Greece (115 percent) and Spain (53 percentthe same as in

the United States), how can it be that they

both can reach a 50 percent debt-to-GDP level in the

same 1516 years? There are some straightforward

explanations for this counterintuitive result. First, Greece

is growing its GDP and revenues slightly faster than Spain.

Second, since Greece has a lower expected population

growth rate (0.50 percent) and government expenses

grow at 0.8 times population plus inflation, overall

Greek spending growth will be slightly slower than that

in Spain (2 percent versus 2.4 percent, respectively).

Third, the primary goal is not to decrease the absolutelevel of

debt, but to lower the ratio of debt to GDP by

growing GDP in the first place. The drop in debt to GDP

comes from the compound growth of three different

economic flows (GDP, revenues, and expenditures) and

net changes in the stock of debt outstanding. These

variables all compound at different rates and generate

results that are immediately clear from looking at the

various moving parts in isolation.5

Putting the Framework into PracticeAccording to the productivity

and spending framework,

a government in a debt crisis can devise an escape strategy

by implementing policies that result in productivity-driven

growth and increases in government spending that are no

faster than increases in population growth plus inflation.

The government policies that accomplish this will not be

easy to implement, especially given the acute nature of

the current crisis and increasing demands on government

services by an aging population. A productivity-focused

strategy and spending approach that extends beyond

immediate recession management can provide a basis

for fiscal policies that do not require drastic cuts across

the board. These productivity and growth policies do,

however, require sustained commitment and wide political

support to guarantee continuation even when administra-

tions change. Examples of when such continuity was

achieved include Canada in the 1990s; the United States

in the 1980s and 1990s, when growth-and-deficit-reducingpolicies

persisted through multiple administrations;

and periods of sustained reductions in debt to GDP in

Sweden, Finland, and several Asian countries.

Surely one needs a bit of luck, too, when faced with a

crisis

like the current one. Some might argue that the historical

examples of Canada and other countries are unique or lucky,

in that they happened on the back of rapid global growth

at the end of the 1990s and in the early 2000s. While such

growth certainly helped, it does not affect the premise

that the combination of policies that promote growth

more people working more productivelywith moderategrowth in

spending will resolve todays debt crises.

Every policy decision in every country faces a number of

questions: Is there evidence that this policy decision will

lead to increases in productivity? Will the end result of

this policy be more people working more productively?

Will government expenditures grow slower than GDP

until the crisis is fully resolved and debt to GDP is at

the desired level?

Government policies must also create confidence in the

bond markets, which need to fund maturing debt and

fiscal deficits until the crisis resolves. Two decades may

seem like a long time, but the compounding effects of

small differences in growth rates over periods of 10 to 15

years or more are very powerful. It is the compounding

of good policy over time that resolves a crisis. When

both the country and its creditors can see that credible

policies exist to be productive, grow, and reduce debt to

GDP to sustainable levels, then the interests of the bond

holders will match those of a sovereign government.

8 executive action escaping the sovereign -debt crisis the

conference board

5 The complete debt-to-GDP reduction calculation is in the

appendix, which is

available on request from The Conference Board Business

Information Service

([email protected]).

-

8/2/2019 Solving Debt Crisis

9/9

9 executive action escaping the sovereign -debt cris is the

conference board

About the Authors

Stephen Sexauer is chief investment officer at Allianz

Global Investors Solutions.

Bart van Ark is senior vice president and chief economist

of The Conference Board.

The Conference Board creates and disseminates knowledge

about management and the marketplace to help businesses

strengthen their performance and better serve society.

Working

as a global, independent membership organization in the

public

interest,we conduct research, convene conferences, make

forecasts, assess trends, publish information and analysis,

and bring executives together to learn from one another.

The Conference Board is a not-for-profit organization andholds

501 (c) (3) tax-exempt status in the United States.

www.conferenceboard.org

The Americas

845 Third Avenue

New York, NY 10022-6600

United States

Tel +1 212 759 0900

Fax +1 212 980 7014

ASIA

China

Beijing Representative Office

7-2-72 Qijiayuan,

9 Jianwai Street

Beijing 100600 P.R. China

Tel +86 10 8532 4688

Fax +86 10 8532 5332

www.conferenceboard.cn

Hong Kong

Suite No. 2-3, 18/F, Queens Place

74 Queens Road Central

Hong Kong sar

Tel + 852 2804 1000

Fax + 852 2869 1403

India

A-701 Mahalaxmi Heights

Keshavrao Khadye Marg

Mahalaxmi (East)

Mumbai 400 011 INDIA

Tel + 91 22 23051402

Singapore

8 Eu Tong Sen Street #22-81

The Central

Singapore 059818

Tel +65 6325 3121

Fax +65 6222 4637

EuropeChausse de La Hulpe 130, box 11

B-1000 Brussels, Belgium

Tel + 32 2 675 54 05

Fax + 32 2 675 03 95

Copyright 2010 by The Conference Board, Inc. All rights

reserved.

The Conference Board and the torch logo are registered

trademarks of

The Conference Board, Inc.