Embed Size (px)

Citation preview

Sonoma County Community Development Commission

Sonoma County Housing Authority 1440 Guerneville Road, Santa Rosa, CA 95403-4107

Dear Applicant:

Thank you for your interest in the Housing Rehabilitation Loan Program sponsored by the Sonoma County Community Development Commission (“Commission”). An application is enclosed.

The Commission offers low-interest loans for the rehabilitation of existing residential properties. Loans of up to $50,000 are available to eligible owner-occupied households and to investor owners. The current interest rate is 3%. The loan term is up to 30 years. There are no monthly payments for deferred loans.

Regarding the application: 1. Please complete ALL pages of the application and sign and date all pages

where indicated. 2. Section IV on page 4 lists the necessary documents to verify the information in

your application. Only you can provide this information. Your application cannot be processed without these documents.

3. Be sure to sign the bottom of Section VII on page 4, “Certification.” 4. Complete the “Smoke Detector Certification,” “The Housing Financial

Discrimination Act of 1977,” and “Protect Your Family from Lead in Your Home” receipt and return along with your application.

5. Mobile home owners only: If you do not have a Certificate of Title and/or Registration Card, please indicate this on a separate piece of paper.

If you have any questions, or need further information, please contact me at (707) 565-7522.

Regards,

Nina Bellucci, Senior Community Development Specialist Sonoma County Community Development Commission

Enclosures

S:\Rehab\Applications\HRLP Application Package\Cover letter.docx

Telephone (707) 565-7500 FAX (707) 565-7583 ● TDD (707) 565-7555

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

1440 Guerneville Road Santa Rosa, CA 95403 (707) 565-7500

REHABILITATION LOAN PROGRAM

Date:

Name:

Address: City: Zip:

Assessor’s Parcel Number (APN) APN is found on your property tax bill. It is a 12 digit number.

Home Phone: Work Phone:

Email: Mobile Home Park: Do you own and currently occupy the above address? Yes_____ No_____

Do you have homeowners insurance? Yes_____ No_____

Do you have a permanent disability? Yes No _____ _____

Does anyone in the household have a known sensitivity to construction related airborne contaminants such as dust, mold, or commonly used construction chemicals and cleaners? Yes_____ No_____

Please check one of the race categories that best describes your household (Optional) American Indian or Alaska Native Asian

Black or African American Native Hawaiian or other Pacific Islander White American Indian or Alaska Native and White Asian and White Black or African American and White

American Indian or Alaska Native and Black or African American Other Is the household ethnicity Hispanic? Yes___ No___

I. HOUSEHOLD SIZE: Please complete the following for all persons residing in your home. Name Age Relationship Social Security Number

Head Number of Persons in Household:

1S:\Rehab\Applications\HRLP Application Package\Application (updated 10-29-07).docx

Name of Earner

TOTAL MONTHLY INCOME

Amount Name of income source

NAME OF INSTITUTION ADDRESS OF INSTITUTION (including zip code) ACCOUNT #

Savings & Checking

Stocks and Bonds

IRA’s/Annuities

Notes/Other Assets

REAL ESTATE (other than current residence) Assessed

Location Value Income $ $ $ $

2S:\Rehab\Applications\HRLP Application Package\Application (updated 10-29-07).docx

II. GROSS MONTHLY HOUSEHOLD INCOME: Please list all income earners and the sources of income for all persons residing in your home.

************************************************************************************************************************ III. ASSETS Please list all of the accounts you currently maintain or have an interest in. For the assets listed below, provide the name of the bank, company or institution in which the assets are held, the complete address and the account number. (Use additional sheets, if necessary.) Assets are cash on hand, checking and savings accounts, stocks, bonds, notes, cash value of

insurance, real estate, valuable collections, or trust funds. Assets are not current residence, household furniture, two automobiles (if two adults are listed in

household), jewelry, etc.

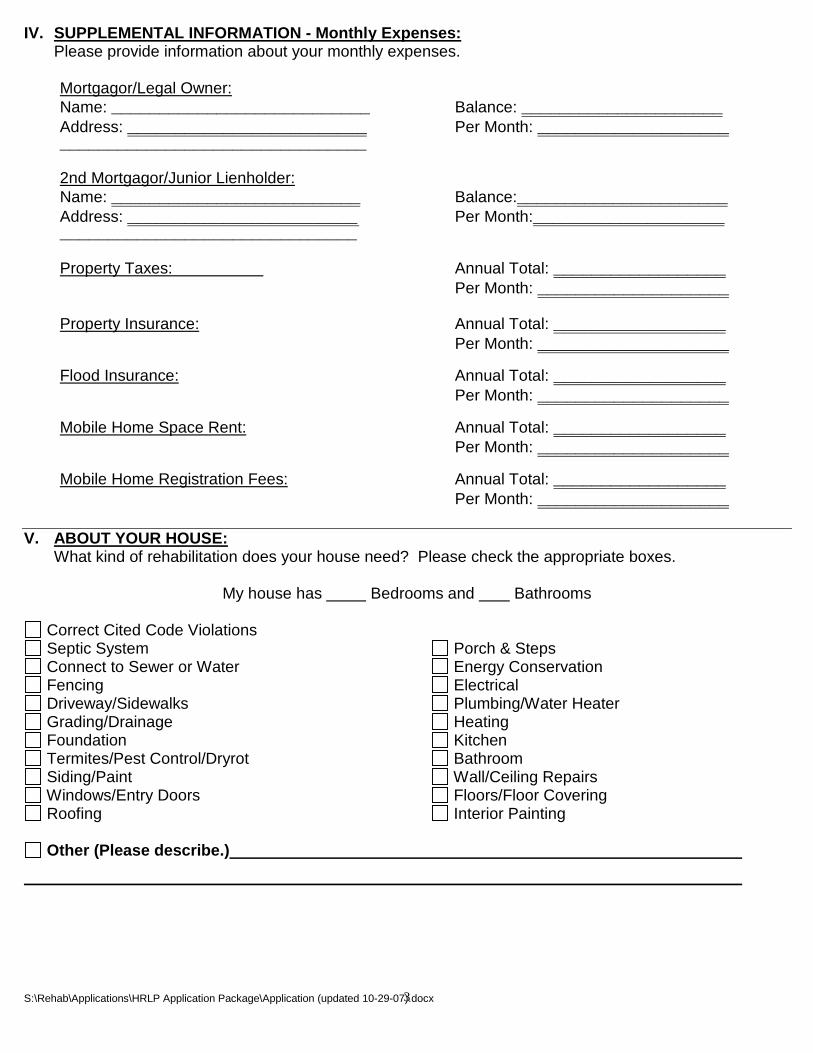

Mortgagor/Legal Owner: Name: ___________________________ Balance: _____________________ Address: _________________________ Per Month: ____________________ ________________________________

2nd Mortgagor/Junior Lienholder: Name: __________________________ Balance:______________________ Address: ________________________ Per Month:____________________ _______________________________

Property Taxes: Annual Total: __________________ Per Month: ____________________

Property Insurance: Annual Total: __________________ Per Month: ____________________

Flood Insurance: Annual Total: __________________ Per Month: ____________________

Mobile Home Space Rent: Annual Total: __________________ Per Month: ____________________

Mobile Home Registration Fees: Annual Total: __________________ Per Month: ____________________

Correct Cited Code Violations

Porch & Steps

Other (Please describe.)

Energy Conservation Electrical Plumbing/Water Heater ng KHeati

itchen Bathroom Wall/Ceiling Repairs Floors/Floor Covering Interior Painting

Septic System Connect to Sewer or Water Fencing Driveway/Sidewalks ainage Grading/Dr Foundation Termites/Pest Control/Dryrot Siding/Paint Windows/Entry Doors Roofing

My house has Bedrooms and Bathrooms

3S:\Rehab\Applications\HRLP Application Package\Application (updated 10-29-07).docx

IV. SUPPLEMENTAL INFORMATION - Monthly Expenses: Please provide information about your monthly expenses.

V. ABOUT YOUR HOUSE: What kind of rehabilitation does your house need? Please check the appropriate boxes.

4S:\Rehab\Applications\HRLP Application Package\Application (updated 10-29-07).docx

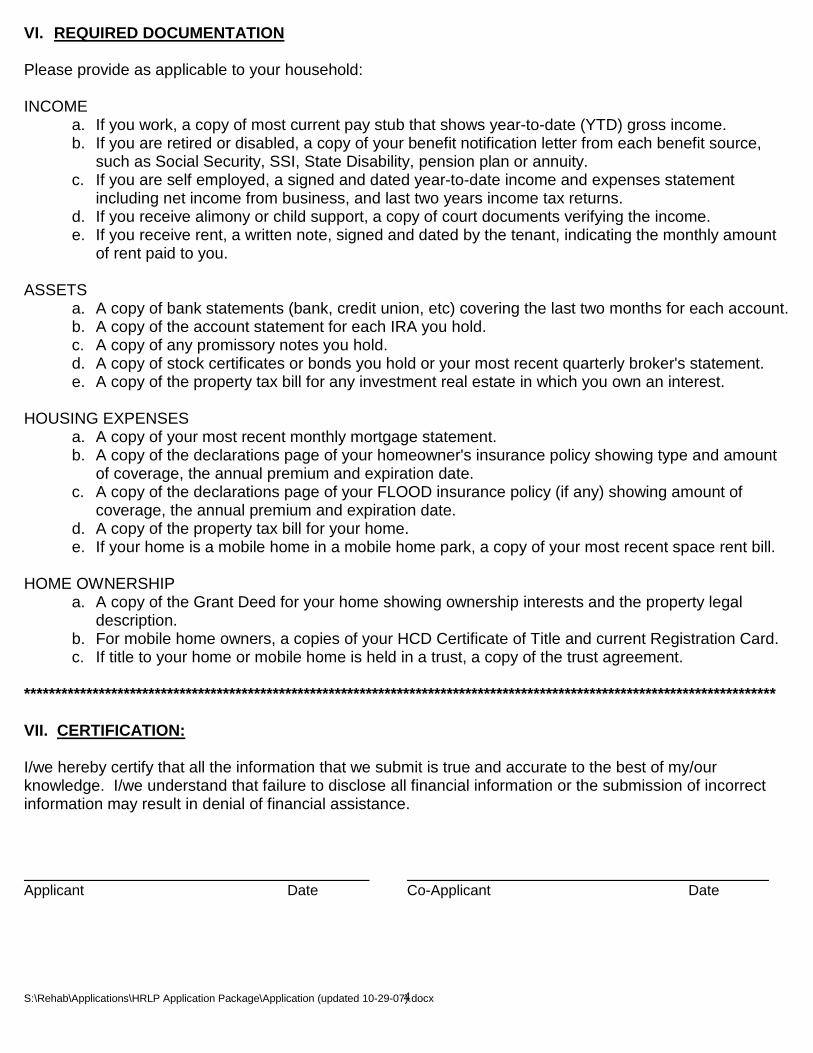

VI. REQUIRED DOCUMENTATION

Please provide as applicable to your household:

INCOME a. If you work, a copy of most current pay stub that shows year-to-date (YTD) gross income. b. If you are retired or disabled, a copy of your benefit notification letter from each benefit source,

such as Social Security, SSI, State Disability, pension plan or annuity. c. If you are self employed, a signed and dated year-to-date income and expenses statement

including net income from business, and last two years income tax returns. d. If you receive alimony or child support, a copy of court documents verifying the income. e. If you receive rent, a written note, signed and dated by the tenant, indicating the monthly amount

of rent paid to you.

ASSETS a. A copy of bank statements (bank, credit union, etc) covering the last two months for each account. b. A copy of the account statement for each IRA you hold. c. A copy of any promissory notes you hold. d. A copy of stock certificates or bonds you hold or your most recent quarterly broker's statement. e. A copy of the property tax bill for any investment real estate in which you own an interest.

HOUSING EXPENSES a. A copy of your most recent monthly mortgage statement. b. A copy of the declarations page of your homeowner's insurance policy showing type and amount

of coverage, the annual premium and expiration date. c. A copy of the declarations page of your FLOOD insurance policy (if any) showing amount of

coverage, the annual premium and expiration date. d. A copy of the property tax bill for your home. e. If your home is a mobile home in a mobile home park, a copy of your most recent space rent bill.

HOME OWNERSHIP a. A copy of the Grant Deed for your home showing ownership interests and the property legal

description. b. For mobile home owners, a copies of your HCD Certificate of Title and current Registration Card. c. If title to your home or mobile home is held in a trust, a copy of the trust agreement.

*************************************************************************************************************************

VII. CERTIFICATION: I/we hereby certify that all the information that we submit is true and accurate to the best of my/our knowledge. I/we understand that failure to disclose all financial information or the submission of incorrect information may result in denial of financial assistance.

Applicant Date Co-Applicant Date

5S:\Rehab\Applications\HRLP Application Package\Application (updated 10-29-07).docx

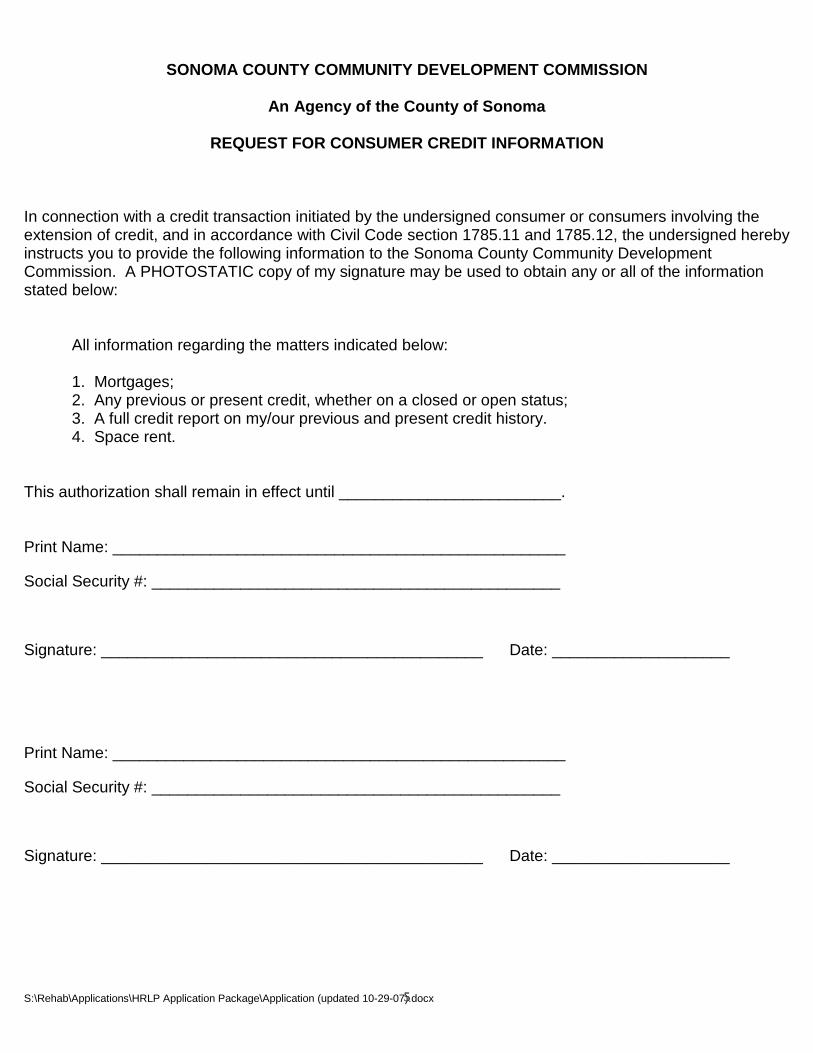

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

An Agency of the County of Sonoma

REQUEST FOR CONSUMER CREDIT INFORMATION

In connection with a credit transaction initiated by the undersigned consumer or consumers involving the extension of credit, and in accordance with Civil Code section 1785.11 and 1785.12, the undersigned hereby instructs you to provide the following information to the Sonoma County Community Development Commission. A PHOTOSTATIC copy of my signature may be used to obtain any or all of the information stated below:

All information regarding the matters indicated below:

1. Mortgages; 2. Any previous or present credit, whether on a closed or open status; 3. A full credit report on my/our previous and present credit history. 4. Space rent.

This authorization shall remain in effect until _________________________.

Print Name: ___________________________________________________

Social Security #: ______________________________________________

Signature: ___________________________________________ Date: ____________________

Print Name: ___________________________________________________

Social Security #: ______________________________________________

Signature: ___________________________________________ Date: ____________________

______________________________________________ ______________________________

______________________________________________ ______________________________

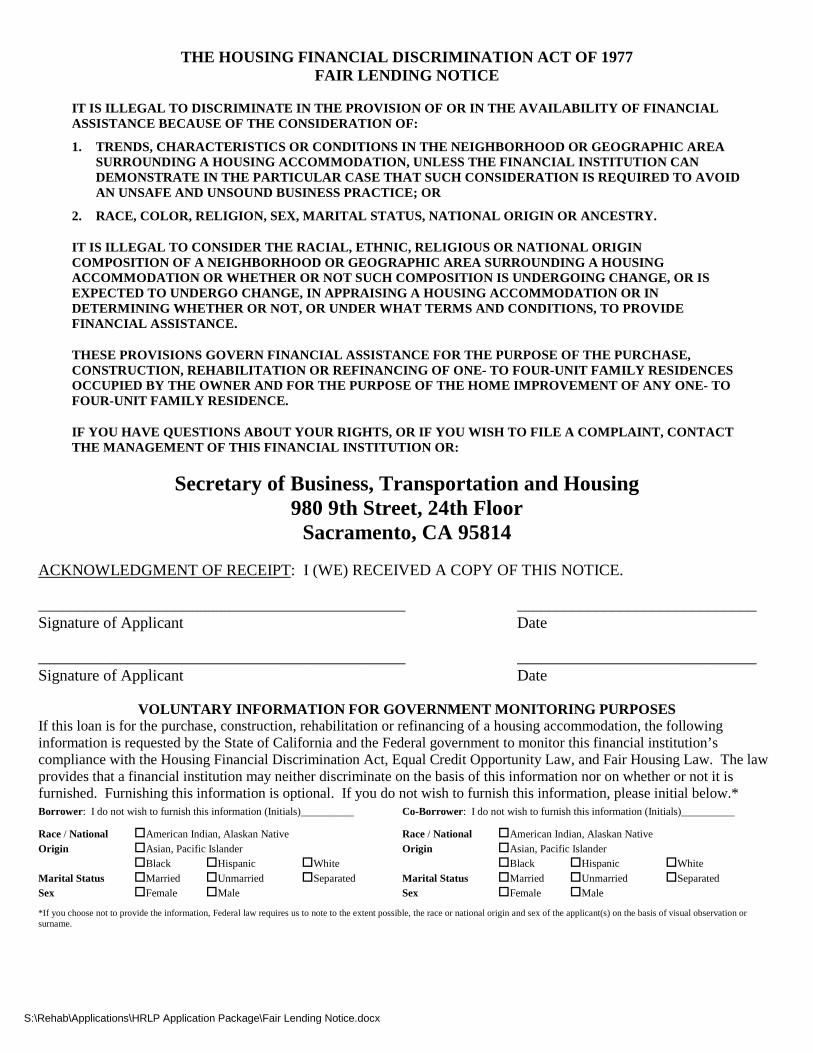

THE HOUSING FINANCIAL DISCRIMINATION ACT OF 1977 FAIR LENDING NOTICE

IT IS ILLEGAL TO DISCRIMINATE IN THE PROVISION OF OR IN THE AVAILABILITY OF FINANCIAL ASSISTANCE BECAUSE OF THE CONSIDERATION OF:

1. TRENDS, CHARACTERISTICS OR CONDITIONS IN THE NEIGHBORHOOD OR GEOGRAPHIC AREA SURROUNDING A HOUSING ACCOMMODATION, UNLESS THE FINANCIAL INSTITUTION CAN DEMONSTRATE IN THE PARTICULAR CASE THAT SUCH CONSIDERATION IS REQUIRED TO AVOID AN UNSAFE AND UNSOUND BUSINESS PRACTICE; OR

2. RACE, COLOR, RELIGION, SEX, MARITAL STATUS, NATIONAL ORIGIN OR ANCESTRY.

IT IS ILLEGAL TO CONSIDER THE RACIAL, ETHNIC, RELIGIOUS OR NATIONAL ORIGIN COMPOSITION OF A NEIGHBORHOOD OR GEOGRAPHIC AREA SURROUNDING A HOUSING ACCOMMODATION OR WHETHER OR NOT SUCH COMPOSITION IS UNDERGOING CHANGE, OR IS EXPECTED TO UNDERGO CHANGE, IN APPRAISING A HOUSING ACCOMMODATION OR IN DETERMINING WHETHER OR NOT, OR UNDER WHAT TERMS AND CONDITIONS, TO PROVIDE FINANCIAL ASSISTANCE.

THESE PROVISIONS GOVERN FINANCIAL ASSISTANCE FOR THE PURPOSE OF THE PURCHASE, CONSTRUCTION, REHABILITATION OR REFINANCING OF ONE- TO FOUR-UNIT FAMILY RESIDENCES OCCUPIED BY THE OWNER AND FOR THE PURPOSE OF THE HOME IMPROVEMENT OF ANY ONE- TO FOUR-UNIT FAMILY RESIDENCE.

IF YOU HAVE QUESTIONS ABOUT YOUR RIGHTS, OR IF YOU WISH TO FILE A COMPLAINT, CONTACT THE MANAGEMENT OF THIS FINANCIAL INSTITUTION OR:

Secretary of Business, Transportation and Housing 980 9th Street, 24th Floor

Sacramento, CA 95814

ACKNOWLEDGMENT OF RECEIPT: I (WE) RECEIVED A COPY OF THIS NOTICE.

Signature of Applicant Date

Signature of Applicant Date

VOLUNTARY INFORMATION FOR GOVERNMENT MONITORING PURPOSES If this loan is for the purchase, construction, rehabilitation or refinancing of a housing accommodation, the following information is requested by the State of California and the Federal government to monitor this financial institution’s compliance with the Housing Financial Discrimination Act, Equal Credit Opportunity Law, and Fair Housing Law. The law provides that a financial institution may neither discriminate on the basis of this information nor on whether or not it is furnished. Furnishing this information is optional. If you do not wish to furnish this information, please initial below.* Borrower: I do not wish to furnish this information (Initials)__________ Co-Borrower: I do not wish to furnish this information (Initials)__________

Race / National American Indian, Alaskan Native Race / National American Indian, Alaskan Native Origin Asian, Pacific Islander Origin Asian, Pacific Islander

Black Hispanic White Black Hispanic White Marital Status Married Unmarried Separated Marital Status Married Unmarried Separated Sex Female Male Sex Female Male

*If you choose not to provide the information, Federal law requires us to note to the extent possible, the race or national origin and sex of the applicant(s) on the basis of visual observation or surname.

S:\Rehab\Applications\HRLP Application Package\Fair Lending Notice.docx

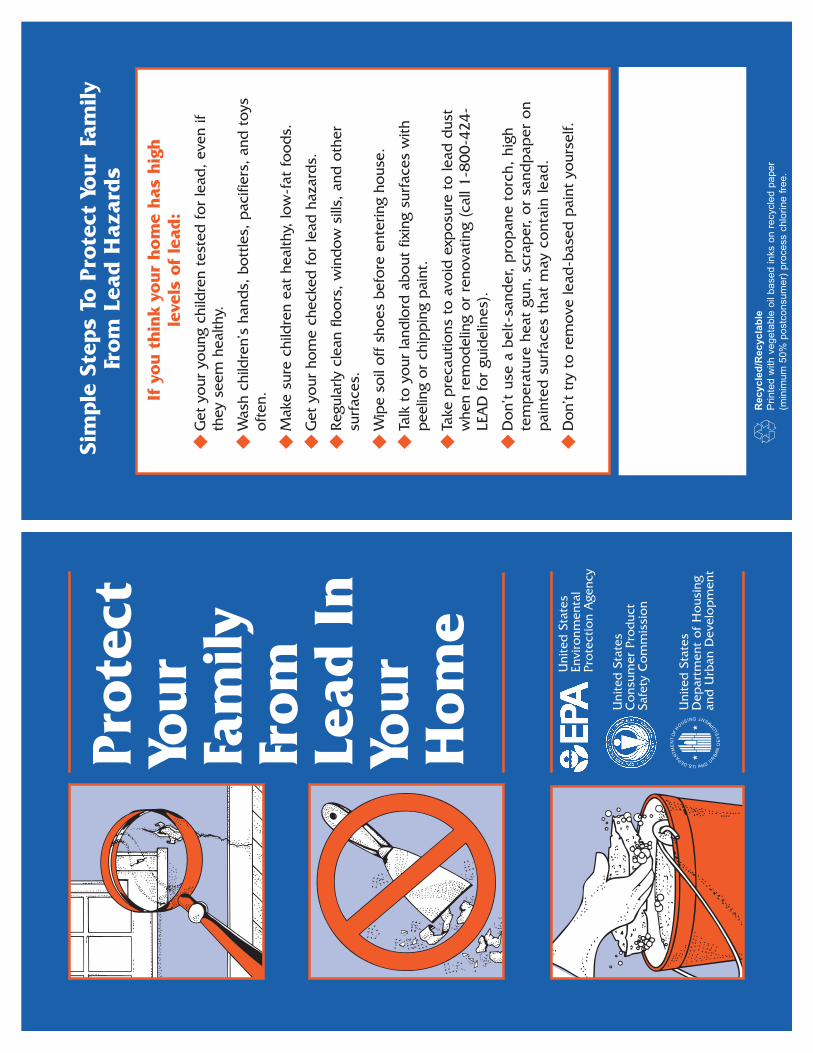

Pro

tect

Your

Fam

ily

From

Lead I

n

Your

Hom

e

United

Sta

tes

Enviro

nm

enta

l Pro

tectio

n A

gency

United

Sta

tes

Co

nsu

mer

Pro

duct

Safe

ty C

om

mis

sio

n

United

Sta

tes

Dep

art

ment

of

Ho

usi

ng

and

Urb

an D

evelo

pm

ent

Sim

ple

Ste

ps T

o P

rote

ct

Your

Fam

ily

From

Lead H

azard

s

If y

ou t

hin

k y

our

hom

e h

as h

igh

leve

ls o

f le

ad:

◆ G

et

your

young c

hild

ren t

est

ed f

or

lead,

even if

they s

eem

healthy.

◆ W

ash

child

ren’s

hands,

bott

les,

pacifie

rs,

and t

oys

oft

en.

◆ M

ake s

ure

child

ren e

at

healthy,

low

-fat

foods.

◆ G

et

your

hom

e c

hecked f

or

lead h

azard

s.

◆ R

egula

rly c

lean f

loors

, w

indow

sill

s, a

nd o

ther

surf

aces.

◆ W

ipe s

oil

off

shoes

befo

re e

nte

ring h

ouse

.

◆ T

alk

to y

our

landlo

rd a

bout

fixi

ng s

urf

aces

with

peelin

g o

r chip

pin

g p

ain

t.

◆ T

ake p

recautions

to a

void

exp

osu

re t

o lead d

ust

w

hen r

em

odelin

g o

r re

novating (

call

1-8

00-4

24

LEA

D f

or

guid

elin

es)

.

◆ D

on’t

use

a b

elt-s

and

er, p

rop

ane t

orc

h,

hig

h

tem

pera

ture

heat

gun,

scra

per, o

r sa

nd

pap

er

on

pain

ted

surf

aces

that

may c

onta

in lead

.

◆ D

on’t

try

to r

em

ove lead-b

ase

d p

ain

t yours

elf.

Recycled/R

ecyclable

ed w

ith ve

getab

le oil

base

d ink

s on r

ecyc

led pa

per

(mini

mum

50%

postc

onsu

mer)

proce

ss ch

lorine

free.

Are

You P

lannin

g T

o B

uy,

Rent,

or

Renova

te

a H

om

e B

uilt

Befo

re 1

978?

have

lead

-can

.

19

78

(c

alle

d

dust

befo

re

and

p

rop

erly

of

lead

built

o

f chip

s,

care

ap

art

ments

le

vels

p

ain

t,

taken

hig

h

fro

m

no

t if

and

co

nta

ins

Lead

hazard

s

ho

use

s th

at

pain

t).

health

any

pain

t base

d

serio

us

M po

se

OW

NER

S,

BU

YER

S,

and

REN

TER

S a

re

encoura

ged t

o c

heck

for

lead (

see p

age 6

) befo

re r

enting,

buyin

g o

r re

novating p

re

1978 h

ousi

ng.

cert

ain

re

ceiv

e

reno

vating

ind

ivid

uals

or

buyin

g,

that

renting,

req

uires

befo

re

ho

usi

ng:

law

ed

era

l in

form

atio

n

-19

78

p

reF

LA

ND

LO

RD

S h

ave t

o d

isclo

se k

now

n info

rm

ation o

n lead-b

ase

d p

ain

t and lead-b

ase

d

pain

t hazard

s befo

re lease

s ta

ke e

ffect.

Lease

s m

ust

inclu

de a

dis

clo

sure

about

lead-b

ase

d p

ain

t.

SELLER

S h

ave t

o d

isclo

se k

now

n info

rma

tion o

n lead-b

ase

d p

ain

t and lead-b

ase

d

pain

t hazard

s befo

re s

elli

ng a

house

. Sale

s contr

acts

must

inclu

de a

dis

clo

sure

about

lead-b

ase

d p

ain

t. B

uyers

have u

p t

o 1

0

days

to c

heck f

or

lead.

REN

OVATO

RS d

istu

rbin

g m

ore

than 2

square

fe

et

of

pain

ted s

urf

aces

have t

o g

ive y

ou

this

pam

phle

t befo

re s

tart

ing w

ork

.

IMPO

RTA

NT!

Lead F

rom

Pain

t, D

ust,

and

Soil C

an B

e D

angero

us I

f N

ot

M

anaged P

roperl

y

y

eht eg rn ou f

o e

y b

m ner va eh sn ea i

c b ae bru ds no a . p nx n re e or

d bda li ee h r

L c a

:

TC

AF FAC

T: Even c

hild

ren w

ho s

eem

healthy c

an

have h

igh levels

of

lead in t

heir b

odie

s. y

by rb o g

s , ne t ii s nd u i

o d atb

ndri oa

e ce

h l st g p

n n iii h w cd o

a tll ne a il at w pe s

g rr o

n o la igc o n s

e i l h g . p t nao i de t ae r a eP b e l

: TC

AF

d

g

en a

s i ac t

u b o

d - n

d e sr a i

e r l n

o , of s i s e ti

n s dao ni ct o

p t cs

o d o

y m o

n o

a gn

m

I n. i s e d sv ir a a t

h az h . ae t dl h rp t ad no a i z

e a aeP l p h

: TC

AF FAC

T: R

em

ovin

g lead-b

ase

d p

ain

t im

pro

perly

can incre

ase

the d

anger

to y

our

fam

ily.

If y

ou t

hin

k y

our

hom

e m

ight

have lead

hazard

s, r

ead t

his

pam

phle

t to

learn

som

e

sim

ple

ste

ps

to p

rote

ct

your

fam

ily.

1

s

ya

W y

na

M ni

yd

oB

eht

ni st

eG

da

eL

:y

eht f d

uring

i mo

uth

s.

y

do

r pain

ted

their

co

nta

ins

b obje

cts

i in

e that

h (esp

ecia

lly

t n

dis

turb

oth

er

dust

soil

id d

ust

or

ae le

ad

or

l t lead

th

at

eg in

hand

s

l

reno

vatio

ns

with

chip

s

n

ac th

eir

po su

rfaces)

.

Put

Bre

ath

e

co

vere

d

pain

t

e

Eat

lead

.

eP ◆ ◆ ◆

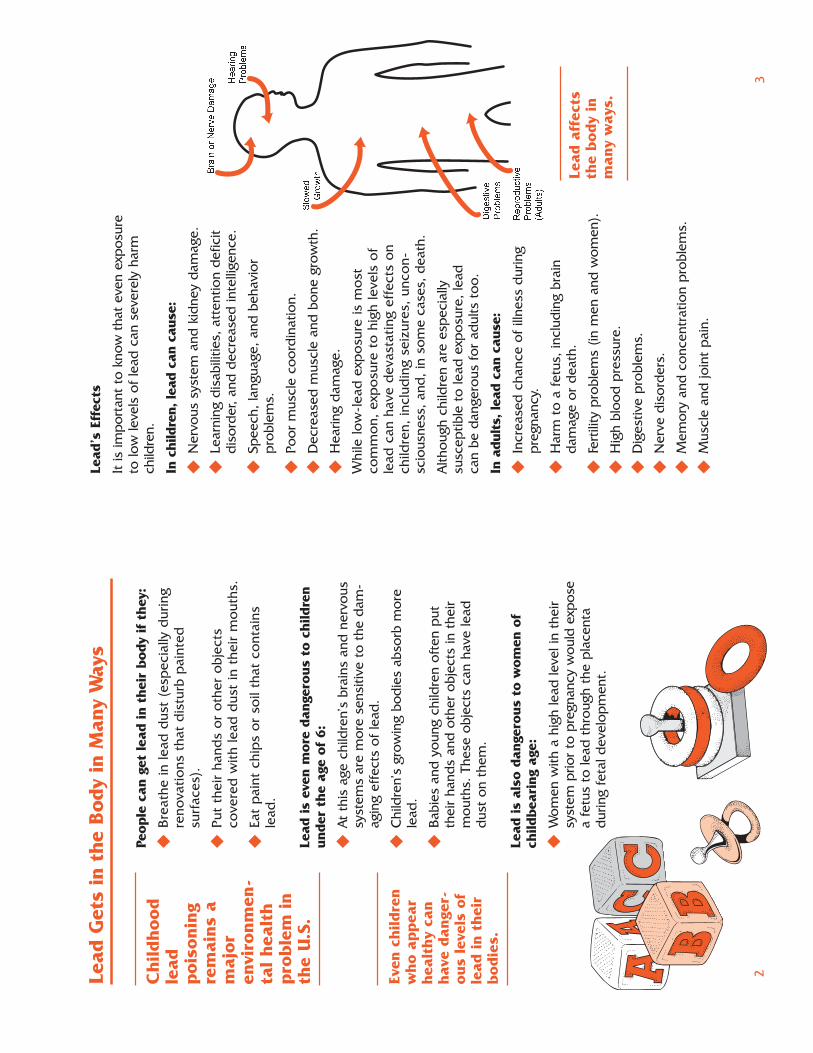

Ch

ild

ho

od

lead

p

ois

onin

g are

main

s

majo

r envir

onm

en

healt

h inta

l p

rob

lem

.

S.U

the

s -n ue o m err a o rv i dd r d m

t e al ui e h en e ph t l bh

c n ed rt n o e vo n i

o s t at a st b f ho t s s a c e e nu n v n j

o i si a

a t ee br i r cr is o

e b d d

g n s

. o li r t

s e h e cn ’ d bs c h ea n a g j t

d e e e g b: l o r r n n oe 6 d o if w u d

r lf i o e o n .

o h m oo ss a

m c r yt g e me ee r h c d se g T he dn a sga nf ’ n t

e a s n a . f v nee ee s m

a s

sr h hi o h . ee g hs t d t i r tt l i u t ns i di br i e o s

t g h a ay ud e A e hs a C l B m da d t

e n

L u ◆ ◆ ◆

ch

ild

ren

ap

pear

can

danger- of

their

levels

Even

wh

o

healt

hy

in

have

ou

s

lead

b

od

ies.

� �

e .)r .

u . n. s. e tsm

i ee h .

g c mo i c t h

p r f n w ga e l

x e o of t ma

on e

a on bh m

d re o r a g y i il

g

m

ost

le

vels

eff

ects

unco

n

e

i w

n od d

r . u i

d n a r

n ll v

e e o , a d

y e o r pe e da sy ni t l l b

v r t n ae n . e l oh s nee n o ts a s ge , ov : n i n

is e ne b b a i s e it e e d d o c r n tt i

a t s i c ei e ns t ue : d k d

lt d uh l

a sa e p eu l

n s i s u m .

t nn s o da d , a n l

a

seiz

ure

s,

a

hig

h

to m e u fp ac i n

w a cn s e oc r , d o x r a n i

e e (

o a i c e . c . r l en s r e o eo

i

d hc sn tak a c m

i e g e a n

,f c s tli sd a o g n e e b c u a i d ns a

au e m l u

xp

osu

re

e a

devast

ating

n ad a m u

m

ed

art. nne i. ar s e

u c p

s m . n ts e sl o nrb c i

e e r e oo tt c d ,g e l o jt f s s ea l o h e d p d d

n r f bo l ry c s n r nt n d . dt e i a pa . d r o d l s d ca d o ro r an a l e y oa a ns c s l s de

-lead

xp

osu

re

have

inclu

din

g

i t d o sa ,l e as g r

m u ge , e c

, s e i, h pt e n e g e n

m

l e o yn e d f n s o v r u h ca s r

n l , a t g y l i ef v e i e s bo o c e b t d a s an t or e l

E e i sp . v r h i m ce l r e d n a l t e i

n d rr b ro tas e o c low

n g

o p l gr a r r m

e l e e m

li h e v s

m

t

w g r

i u’ e s e s u u c g ea r ee i

d r h N

ii p r o e can

ri e au b d o d p D o n eL d S P H c I p H d F H D Na s l l c i

e i t o h nL I t c I ◆ ◆ ◆ ◆ ◆ ◆ While

co

mm

on,

lead

child

ren,

M Mo h ai s nt

c l u a ns A s c I ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆

sori p af e x

h e t

o t n d en n l ce i

m

u al o l

e p

o v w e

w el y . h c t

d t no n et a a h e n gs l mg uu ph e oo g r r o

r li p h ee h t vg : o

a t d en e a da g h r e

d a ti o ll i a g w r to o

n p t es n f

m il r sa e ga u m e ns e tti e i

b o s r

d l W

fyd u

s a da i

e hL c ◆

eaff

ects

in

ways.

bo

dy

Lead

th

e

many

2

3

Where

Lead-B

ased

Pain

t Is

Found

Id

enti

fyin

g L

ead

Hazard

s

In g

enera

l,

the o

lder

your

hom

e,

the

more

lik

ely

it

has lead-

based

pain

t.

. - s d s

d p

e ) ba n n u .

n r c sae ri u l , k ru a g

e b

e s c ot v un e i c

e p s v n i s n

a e s e . m . r

n r i

u e

h s o o a s m

g e

n so h

8 u , h u cn h i at y sr s

o l o7

m r y g

l u e i t ti r 9 i ho o d

v n S o e1 o o hu m e

e r d

af e o h d

f c t g : (

d t . ar l p c - i nt l f en i eo a n p , e b ai o lrf u ya o

l u m f ee t go p

p e o t i n r odb p s f c et

s e i sf d d h o

i i e

s r sl e d

e

, a

b ne e h t i e us t t au n st u d

th a

b aT t na n e t o n x

t e s s b s. c i e

s a d u

e a- oe t m pd d v ne rni a m

i m

m

ta

m

r a ar o s

e p e l a r

pl e a ao o L o p h i f

d

h S o h

y d

d

d

. t i . h a se r c

e n 8 i n s

e n o n n a uen s 7 I I b I In ll s

a r a a 9

M

a

b b 1 e ◆ ◆ ◆ ◆

Checkin

g Y

our

Fam

ily f

or

Lead

. f n ri t l ) n I a r ,

d u d o a

. u o g sa s ew n i r t t , a n q i gr n n

o a eez le a go d e oa t r et

h t n n eo e m t t d t

i a a

a eo w

n

m

p a n

m

( d e hun t

po

rches.

t a a i tt r s t on r d

o h n n a fi r t i o i . e o nn e

e d n : t r s

k v w a c a g

y se li p e , ll d

e e l iil . o . at nt m e s s, i h sa g a r rn d

a h k w h h

e eu l e ea c c c w e t c u g ms a r s u m, sr a g d

oa q i i

u e a

n rf e r s n

s d a in s r s s b c a , n r

o di d l w a

i u r f a - , z c r

s e y i

e t e ed a n a r bt i

n f gv e w

d b h e o , an e n n p

i e

d

n o l

a i h m

%

e ti e o s-k a r gd n do d

l

5 d

dp l t tc y a g

a n e l

c d naa i n i.

d

d i r n a b ae 0 h h s l

n ir b g i c -

e t d f l ai c w ao o r r r

h li n t s d l a , r s a o , o o ae t li m

a r a s g ea h a d r sg t o rn w z hbn i

- if 0 n t i w ar y t onc e

i s f i o a

d a . h a e o D

ti t pe

a s n ti 1 r p Wpi d o i a

e m

Se

o c t

e at m s s t L p t D

ai m

h oi i c i I f l ◆ ◆ ◆

Lead

fro

m

pain

t chip

s,

whic

h y

ou

can s

ee,

and

le

ad

dust,

w

hic

h y

ou

can’t

alw

ays

see,

can b

oth

be s

eri

ous

hazard

s.

Get

your

childre

n a

nd

hom

e t

este

d

if y

ou

thin

k

your

hom

e

has h

igh

lev

els

of

lead.

e . . d s . t te s, e

a n l

n v a

e

d i . g e

o ua . ed a se e n h l dpa m a r l r er h r an i f p e

e o c g

y n r eo t w o dl f n a s g

s a s t dh , a t s

o i n n s e e a s s r f ea o e c

m

r l u it eb o e

g e e nt h t t et ue

e t t n

o n

u s bs d

e

d l d a v

o m e e e e

e

r y f u o h mi h e

nu o tn e

t o

l r b

b y h t

e c

d

s 2. e s t

e s o m e s l o c t v h o l

s to s i o l g a i

a s

t

h m v B i h

p r d l t d o :

x h

and

h t ha y

. e wl

wr e n

4 a l r li o be u b d a w g

, a v oo r a m

o e t e d n n

's d

e y d z e 2 f e ill hoa i tl a

f n m d

o f d

l d

l f sk h 2

t r 1

d u p f ee

ages

a r o a ll c i ei a doe y a

y 1 m s p o e c t

n o hh e 8

o i n t s h on x

h sc l l 1 so c t p

d e l e e

l l rc a ar x

d i r

x

t o e o

t A o t eu i

c o 6

d n

o

a v m o

at hi r a

o d . il n mi e f o l k r en m o w e c f y h p n d

l eu

b m

a o e h

n

n t r a i

e c e r es o o

n co g e e t o b d

r e c y ec p r r( a r i s

r

's

d t n l f c nt h r d d r u u , o i

t l ll e

oe y h y av ud o d

o r u c i i) d

oo

l t c l he e h ay 8 d d d s r l

l e C n

h C r r t p i at y a7 i n u

o s p t n u C

hild

ren

he u eoe n 9 a o ee s oT g t i 1 C r t C y d u ◆ ◆ ◆ Y m

e .

r , l ll e

g

i f s h v ht p m n a o o i

o a t

e i i s t o

, h , u w t r e 5

sg e s n e ed u s r r o i

o p e r d x me c d o o ld a n e t l t d a l o n

b r o ba i i

n v a il f s a s ou h f o f a e d r t r s e er o m d

s r n r m

, s l o h e ap a mo f e

s rt T n

z

d tc o r i a

p s r a . oe e

e e s ael e b s h ch

mj p ra e dp h

b n r a t d t a r g o

r u o n

e i . i a saz oc b h y n

h

d e d sl a e l y is

d a l s s h e li a l

n l r p

s h i l m e a w f s

o n p i

d i

w o i c e

er n s o

t a

a s i n h s han e ) ttf w

i

a o r e

r i r e e e t 2

g l e d

ca d r a s u t n

d a ep n r nh bs f h f i o a d

r g g

d lt n / i oi w h e

f i n bt i

u r r ss w µ t i h se e ( r ce d r ct us n

o t u e sl t o ena i n l d: i n

o s e hb r no e a o e o t h a , de- hp t s o- f n

g

e ) t

e

d e er e u f t e i

n wn n

d i

g h i g e hea h a

e e n m

n r . b a T n r a s d t d

l po o prr e n p h

n a . i pa u f a f

w t ( a

c it s o v t ze q c n ) t x

s

i r a

t o

h d s l at e i n

e eh s l u

w m

r f hhs r u g a i o

e d h g o s u i g no

z a

m l r d u p e l

d i a

e

o s d d

o a rt h i r d

f h s e

e hn o

rr md

e d ab g

v Tho an tf e d

m n r

i

p d

n a f s i . ea l n k

a r n (

n l a ra a o

b p

a s d a ae tl r m

c ea t a l c g 2

e t

p r g l sc o t s m

y

e w tl f p . hs li i l a t

t u h o n / p rt r a p d

e i g a t r o r s D

f c w r . c o t i d µ s o r p e e 0 a o du . d

S m 0

n y y

e , e u p d 0 f

d d a .

p s lc i 0

2 e e l t

d e h 0 n s

n 5e d f se n n 0 , o ut

. L c 2e e h4a a e i

u a o : 4 1 t eli e t s he e r w e

◆

ho e

L h t s b ◆ wL t s ◆

o o d

e w ◆ T t o

4

Ch

eckin

g Y

ou

r H

om

e f

or

Lead

Just

know

ing

that

a h

om

e

has l

ead-

based p

ain

t m

ay n

ot

tell

you i

f th

ere

is

a h

azard

.

r r t t e

i d t

os D t u a o . , e

s m a f uo

n n . h s ye t . r g

y er s o li r w a l a s ) A bd eed t a n

e h r s h e

e n

1 E e i

o m d f s ,r a fr u a i m a L e od e h h rr 1

a dw

-h lr a oo z h eu n t s s r uat e z o a u be y r e 4 s

e al h a o r e m e ph

relia

ble

(XR

F)

soil m e o 2 rf g a n e r d t l t or h y s m a n uh g y a li o re 4n e s y h n f h o oo w

l n r oi e o t p - ai g C ff a h d d t n e . h t d yr r . c 0 v ea f y

d u t w a ou o m u wa s co

nd

itio

n

. e s nn o r 0 a bd a o t

e o u l ei z s r is o of

d e ho

me.

p i t 8y

and

s e l e st a s uy a o s y ts ts ap h e o

e n as y a s a dl t r y fi

range

yo

ur

pain

t

dust

, n fl g m

e t- so r t aa 1 t an C o c a ir ke sl s c t l l h l r I

d l d i e t l a u

e d s d , o t l

e f i e

e t ds t ce e y a i f a t e e

: t . dt a l it l n n t of d . oy n s r

n a

m s l i e at t c e u i cr l us a t n n l a s eo t e k b o e ay ’ s o a e a

o

i fluo

resc

ence

f

o e r hsa o c l s b n e e y i y s p t t e s c ot v r e t

h o

mn r

w

i - r d t r n d w r sa o e dn i d c rr u l a, k l a e n use

te

stin

g

-ray

when

insp

ectio

n

pain

t,

d a i f at e , o b

locatio

n.

n h nt c s n oa f ( o ot e a s s o e o t su t c t ea i z s p a x e f i s t

n p e s yo I e s yl a s tt t ya a r te e f tc i a r

s e u d e iy a of

t a l

r h l os . s n h b d ua e - will

n kn ee d m d o n o ew

ho

po

rtable

m

achin

e.

test

s sa

mp

les.

t s as t d e m r t a y wi if s l , i d d sn s n l

e tr r tf et h o a t t bt s t aa ag m

i i n ge s a n c o o o d n a h n n n b a ei k a a oe e e f n i

n e i e r r o f e t l a mc r s a o -o l l t

o p r d

eth

od

s

isual

and

Lab l n ta , t

ional t y ) a o

a i aa p u i i r r yl p t c y dr o s l a a l c 3 e nc o u n n e e vc e e n n b uA oh s r 2 yy A ec r

u v i i a A i a a l e V A

c a l m oi ◆

r

◆ ◆

◆

e oao e h l o 3 o ai nl e r 5 h eY s H s m ◆ ◆ T p r o m ( H m s r

What

You C

an D

o N

ow

To P

rote

ct

Your

Fam

ily

w a e

d a r :

e l

ee R ma t o d ns E H ai , i s w

e a f c. d p

t

U n a Y

l i B y

C e eo l n ea M

t E oy o

l p l s. l dd ts : e iw

A . s p

e y H td r c s a a namk t e E m u o il E S . r

h a T na L e e b

s , k ti m w h i s a M A dd b so r B E , e i e d rrl e G n r ge m r d ne oe w h n o d o E C r c s

D ai o g i

e a i

n an S e o ss fs o. R s a h . e . bu

m

r N t f a e ’ m w ia t m

f s

e l. I s N y r ay U f e d v s h t

om

l a s d S e t w bn r o l n r A W i

e u l a c

h ci m r a O b oe . e s

m

i g i r f aa f u sa si R f s t u o a c A R d su e n t

w e d n h e o eu a sr ds p l E ea I o d d t eu a o s w l E g nN a t c o m o i , cp o f p n a s eh r H G h e re f m do y g r ei t o n a

T s t

k d en u O N i l o ti m nsy h f m pr dy t r d

a u n ss e n c nE h i me a i f a uf cp o yt n r f i ot o i i w y A M G ea oo s r a c ra t s s a d oy p t w

l

D e v d -r e p l eo a n ’ l . a f i

h n h l

n e p gg , i ai r M O l on ay w at n i , h c A i c e ea s n rA T r h d e h un i e r ee c l m o cs r lt c p f e e u ht cc a yro

M

r a i y h m o r e do t, h p r o - c X Sc e du t i

u r o ,

p l d t i

n l I T t n eh l se d r

d t t y nl e y

M

t i l i r n w a . oo p o d s a C R f e , . e a i o r up g e l hn p

O a r d l s y g a f l h g u dy rr g u r s U r l o ns o u c n e r r n s h

u i a , a a po nu oR c en eo n ns ri , e E D F o s . f b a o c n i s i t

r h e o r ers l e d p ie io a a O a f at s i d N

l p kp s u a d l

d eV c k r n

n o s re a b d e c e t l

u y e e o a e a g e t a a il l i sr s E h e n e n u l R A ie e a l h s

o a l l r e l

p C r pC

i eI s me

np f y i

g m Pz N C T h a W l a K p r K s C e t M n s Cy ie l a

tfI h s ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆ ◆

6

7

h

tiW

em

oH

a g

nitav

on

e t R ni r a

o P g d

n eil se a

d Bo -

m dae e

R LR

ed

ucin

g L

ead

Hazard

s I

n T

he H

om

e

Rem

ovi

ng

lead

impro

perl

y

can i

ncre

ase

the h

azard

to

your

fam

ily

by s

pre

adin

g

eve

n m

ore

le

ad d

ust

aro

und t

he

house.

Alw

ays u

se a

pro

fessio

nal

who

is

tra

ined t

o

rem

ove

lead

hazard

s s

afe

ly.

d

s t s r y

e

oo d e

o . a l d

r d

o p

o ms a l l hs n g ) a g , m

s u g n a t n m

a e l pg a r e n s t n g az e a y

d e r u 2 a o

g h r n t e n w tf t d

f a d r i i td

i o a r e m g

/ ; T ;r aa e s r n yg b n e eh l de i p e n o s s i

d a p s o o n g f geee i i l r l o n . t) a l es z h a u a lf µ l fta n l i b

d ii f e” e c“ r tl a d c a e l ( ot r si t s s. i e a r e s e o n

n o i l a n rt b e t e og t e si l . hv n d w ( m a m s s ee e a t h s t l e

n l a a o w l o f s e

e h v c k e t w ci a a o u h s o p lr t ll l rt i sll dp e n rt d o ia s on r ir r a f d l ( tt . e e i a e i c y do c

m

n

m — o o t

d w

l e r n o g g ea c e s b c d u y er e a nd d m o t , s d

e o , l e e w u t l

u a l c irs n c d b

w et d n nl z e pg s c r oee ) p r s a i r n t

d e e a a a ac a a m

i e nne n s h a e t m s o d v pt o u w e c ll v f r t i t i t e r i

y r hs a i o l t e n e g a ah h i o a a n t h t l

h l e e t

y n l aa lc e g r t l q r w oi t a l e vr e

m b e i et os e p ae t bw m o a t s c

d

e h r

u c i a f o aA s o li h n s i nw o i lc o c - e t e r n at rt g d a r s a o n a r, d p d s . m p u e i

o sf n ra h r a i g r n ei cr n nt s r i

m

t m p it d n o e d i

r- y pe t p ut “ o o

i

u r i

u n o

i n on u r e a i c r d n l

o e v s d q e d s w l e l t to s w

i ii i o cd

il ey t l u y. r c v e r ea p i ai oo e a f s h s a l r

n e e i r ri ha nd ed m

tt cl h r t s n o p b m oec e i l p er w r o ol l r n a o l e do g p o r e k ay t ne f f e o i ta tt a i n d t m d n t

o k r r ii o e n r el a g b t h . sn C

n s p r t f sa e o gc a e u a , 2

st 2

it t t n t s t ti a l) s g ( u o r n or e n z s n e i s n w oo t h f fa m o .w m

tn n ac 1 se ni e a rn a i t y r / /t s

o : a p s aa w rh e s r c

h p l ei e : g av t c o ng 1i k n r ” s e t d b i

p h h m s s g i n c e r osa o t - e o o µ µt d h lt i r l i uo t d ot n u g s e e n e ac i m a p l d ft s

d t n s r n e e i mr i ti i ii u nu e n 0t u a 0 o g e sc a s y k h ta o r ae o e w 0 r g cy g 0d ti o o c 5o o e f y en m n e u i aa tc i r l s e v c o nr Y b a t a p T y n p o l oa i i J c 4 2 4 ft w s a eo v i i f l

h n t d l l p a u

◆ ◆

r a u l o

c l o

n l o w h u O o ◆ ◆ ◆

a f r nnI n A f h t q r g a i f C o p if

r o h : t e

r) g e

ur c s dry

cre

ate

pro

p

the

n r uyo n u ll

gu

n,

fum

es.

(esp

e

until

yo

ur o i u

off

l hh a t l ca s d ,ac ( c g

a w o on c o r n get

t i r g s rem

ove

ho

me

is

n i

n t f y re b rt bb u follo

w

this

n i u st c pro

pane

to

no e seo a and

wo

men)

a e i d reno

va

have

a r s h c v f h of

r g lead

-based

, are

a

seal

c hu e T , dust

,

r o u n

heat

actio

ns

yo

ur

fam

ily

ho

use

mo

ve

u n s i

for

sand

pap

er

do

ne.

sand

er

pre

gnant

W 7

tem

pera

ture

dust

tr es u u r” a r r

the

’t

s . or and

in

or o oo e sa oe

d

These

yo

ur

teste

d

lead

can Y a ff d e y r

t . e co

uld

ee r . r m e k a m b se o t is

and

s

n r

belt

- d m s zr o y no pain

t

test

ed

page

oo ine p

pain

t. At r ag H th

at

f a o

t on

il ni of

rem

ain

w

ork

mo

ve

yo

u

and

co

mp

lete

ly

y . H de a i co

mp

lete

d

t tf z D r

b e s a If

s d b

n o r p ea

a

dry

can

do

ne

ar

the

or a

part

ment

am

ounts

em

po

rari

ly

child

ren

cle

aned

. le

ast

e o aa f ua A da h a o t vs E

s Y t o

use

hig

h r L e

lead

-base

d a nu f

is

are

a. e do r - L gt f h ei m

the h a e 4o

dust

aft

er

the n

at g rt se i t

wo

rk e h 2 i w a

lread

y

child

ren

u , n rr d

l

g

no

t o l t

torc

h,

scra

per 4 i e

a o s e n cc n -t , e d n tfa of w i c t 0 u o i

have

rem

od

elin

g

lead

-base

d

outlin

ed

e ig pr he t ap r

Have

pain

t.

Do

larg

e

Lead

lo

ng

cia

lly

out

the

erly

fam

ilyw

ork

ao u 0 d au

d o

lll 8 e m p d or

yo

ung

b e g c o e b - R x ne step

s

u n s T F r a 1 “ R e ak

a o ih s y

ou

T f ions

ele

ase

d

our

he

rochure

.

y t a ◆ ◆ ◆ ◆ I t r y t b

If n

ot

conducte

d

pro

perl

y,

cert

ain

types

of

renova

ti

ons c

an

rele

ase l

ead

fr

om

pain

t and d

ust

into

th

e a

ir.

8

9

Oth

er

Sourc

es o

f Lead

While p

ain

t, d

ust,

and s

oil a

re t

he

most

com

mon

sourc

es o

f le

ad,

oth

er

lead

sourc

es a

lso e

xist.

t d k

s

e r

n r

l o l g

r r e u w au t n

v l

e ag g

e r w ao . a na e g

hu i s o f o t aa t n n h n cC o t t s kys u h s yr a i g u o b n d ay s e i t i t

u f y

w

a. a

m

f an i n h s at r rt k i r o d h o l soh g c e m s ee l o y t

l n ,y n yn r o e it . i r l f o n rg d u to i c , a s co i e d ri l l s i di ll r

m

r tt e r d c r r ao h e f ap a s ot s , w d e s i ea e ar o s n e l e u l r r c r d u tltr et e t e p h r

e e e u 0 e a l u n e i g l d

o c n dd e r

m m m

tt o f n3 p

w o hn u n r n u o i ea a h r au ty sr y os t a a i i

e tt u . s , so l or o e w e r i h L s nh k t d r r u, t u n m f y i , r a r b e s

e ,r w c a dn : oa o o . eo d h a ”r o p a 5 t ee u i r t i aku e r t l c n i w ne tt h y ds o r o e 1 ee f t od go n m g

ad u t n t hd o l t o y y s o t cY a t r n i d i m a o r l e d a

o u oe oh g l e. k w se . p r s od o s r o hsn f o h e al o ys tr . tl n n t d d u nn i c u e zr u h t

e y a il g aa i s

w

i he o dh n an i . e r t a e s

o n r tt at i u ce f e r i tt “a i o I l y ht if dc g y o eow

il a e t z a t

h a d q d s i

. n aw

p b e n n . f g h m o t h o i a d d e I ll i w ed l l

u v o l t r m t r n e as eS t . e ng a k o c g e og do a a e r . o i s d oc r Y n u r ac n - s

en e n l tn i e h o b . n me f v m l b s i eo a s u d

a o s s r s’ yi i o e a a s e ”b r uk t e y s a

m

l o i e .l f e er r t U ah

n e , c R b h d r p b er p j d t

o h d tl h h l i e a ebi d i ep t o tu g lu ua e t t a tf d e n k sr au d l

o i oo o me o

m

ll • • l oh rl e r ro pe li a O o e u o gD p y s w l r T c c b c f F o L r H p f F “ u ◆

◆

◆

◆

◆

◆

◆

For

More

Info

rmati

on

g t

n n . isi s ir n va do

e r ,

s a b

abo

ut

to

r agencie

s a

on

co

n

l i z eo o red

ucin

g

ae t p wt h and

)

ad

dre

ss

an

n d e

e in

pro

d

find

ing

3 da ha at:

C 2 have

t pain

t agency

local

e a

3 Mo

st

for

l e on

l aid

d

ate

.ep

a.g

ov/lead

In

form

atio

n

an 5 are

a,

m

lead

local

-i yo

ur

i 4 o info

rmatio

n

rep

ort

o

r

site

t 2

Agencie

s

ra

Ho

tlin

e

yo

u.

yo

ur

-to

f Lead

r er

f d Ho

tlin

e

ww

w

( 1-8

00

-63

8

trib

es

4

m n

o D financia

l

A lead

-base

d

n lE i

I h info

rmatio

n

L cd -

a t

e 2 ceL 4 t -l o0 1-8

00

-42

4-L

EA

D. no - v . o / n dn o e

b

o i a on

to

for

ti for

to

up

t a d el . W

m n /s ate

r

or yo

ur

and

in

at

am ar e Wr o cf d Safe

ty

pro

duct

call

i of

o a ff n f wate

r

with

for

ap

ply

firm

n i e l o

Pro

du

ct

(CPSC

)

info

rmatio

n

0 Dri

nkin

g

pro

ducts

,

CPSC

's

n 8 drinkin

g

co

nsu

mer

o - oit 1 t 1-8

00

-42

6-4

79

1

inju

ry

.cp

sc.g

ov.

4 i / d /v v

Envir

onm

enta

l st

ate

s,

Receiv

e

r ae o oel g g.a

vis

it

rule

s C

heck

law

s

info

rmatio

n

Inte

rnet

Natio

nal

the

h .r t sp o a d pro

vid

e

sourc

es

the

s p ur e or at

e h in citie

s,

o c

req

uest

and

ow

n

Safe

,

whic

h

als

o

abate

ment

hazard

s.

pho

ne

on

. . f ca w wa

N

l w l da w wo o ’s

o c

onta

ct

n

C h a Te w w A Call

lead

their

activitie

s.

T Co

mm

issio

n

lead

and

h

Co

nsu

mer

T co

nsu

mer

unsa

fe

uct-

rela

ted

2

77

2w

ww

So

me

see

po

ssib

le

EP

Healt

h

can

lead

tacts

o

r C

ente

r

fn oo i yt nama sr

o s .

f e en c rI c u l a ha cr oe t o

d rbe 9

F s 3 i

e 3 h

ht 8 t

- nl il 7 a s

c 7 r , 8 ebd -

e 0 mri 0 ua 8 n

p -m

e1 ni t og a hn i pr e

a c eie v h

h r t

ee S

h t y ar l

o eF R

10

11

3

2

t 0

c t 2

a -

t e

1 4n

) e 1r 1

oC 1

n t 4T S 2 3

d Po s 0i 7C s a g (

e e er A -

2

L 0

7R gl 0 M 3

A na 1 , o )

n P 1 nC 8

o E e o 8i . g t e t

i s 8S ne . u o (

R U S O B 1

EPA

Regio

nal

Off

ices

Your

Regio

nal EPA

Off

ice c

an p

rovid

e f

urt

her

info

rmation r

egard

in

g r

egula

tions

and

lead

pro

tection p

rogra

ms.

CPSC

Regio

nal

Off

ices

Your

Regio

nal C

PSC

Off

ice c

an p

rovid

e f

urt

her

info

rmation r

egard

in

g r

egula

tions

and

consu

mer

pro

duct

safe

ty.

, , st dt ne as lu sIh

c e

a ds os ha RM , , e

s t r

u ihe c sc iti pf cf e m

O n anl Hoa

n C w

o ( ei 1 )

g N t

e n , n

R e oo A

i ng i ma r

P e

E R Me

V

, kr 5

o e 2

Y 2

w u 9

) nt p

7ee s c o 6

N d va t 3t A S

, n -a n l y il e

o 2 7

e s g a 3s I C n 1

d 8r n

d i Mo 7i 8e r , iJ 6a g b 0

w g 9r 6i e e d

0 J -V L R oe 2 1

, l A o

N W g N

o a , 2

( 3n Pci o E i

n i 0

) n n

2

od R . 2

o g 9 l sS i i 3e 8 u do .t 7i r R U 2 B E (

g ee u

R P

, C

Dn

o, t )

d g 3

n n 3ial h C 3

t y sr a c W 01a W a 3

M

t ( 9

, n

3

, a o t 1

e i C n e 0

r n A

a ig d

eo 0r P

w

i t r , 0i a g S a 5ea V e

) L h i -l , R h 4e l a ca pD r 1i i a A

l

( n n P A e 8

3 a i n

0 d ) E

g ov . a

n r i l 5i g 5 ly V S i 1

o s t

. e 6 h 2i n R U 1 P (sg n ee eR P W

, , aai ng ilr oo r

e aG C

, h

a t )

d r t e ci o er a W

o N s t Sl s n 3

, F e 4 , i 0o, p n C n

t e 3 8

a p n

d e 0i o 9

m e rs i 3T t 9

a s a g

e e i , S

b s a Ls R h A 8-

a n 2i l tlA

i Gl y 6

M a A

, ( o s 5 n P a

4 , r ) r E ty a oi o n

n . 4k C Fg S c 1 al 0

o u h e . t 4i t t R U 6 A (

g n u

e e o

R K S

, n

agi

hc d

i ) ) r

M J a 6

n 8 v 6, i s t - eTa n c l 6u 3n o a D -

a t ( oc n 5 i 4Bd si o 0

n n

3

I W C n 6

, , 0

d oo 0s 6 0si o

ia g k i e c 6o eh a L -

n O

L R IJ 6i l ll , I a A , t 8s o( 8a n P e g

5 t o E )

o W a

n i . c 2s g S 1e e 7 i

ho . 3i n R U 7 C (

g ne i

R M

w

e r

N o

o, l

a F

n h

a ti 3

) t s 2 3i s c 1 7u a a , 2o x t

e n e -L T o 6

u 2, , n n 0s C 7

a

d e 2a o 7

m vs i 5 5a gn A 7 7o e ea -h s Lk Rl sr a X 5

o TA lk a A

6

( R , 6

O n P

6

o E . 5

s ) , n i a 44o g l

S l 1e ac . 4o i 2i R U 1 D (xg eeR M

, iru

ossM

i

t 1

, c 0as 1t

a no 7

t 6

s 6

n eC n

e S 0

a

d oK r 2i t K, a g )

0S , 7a e e Ih yL -

w L R tt i 1l o A A 5 CR 5I a( . P - s 5) n

7 aa o D N ) E s

n i k . Tg R 1 3

s nS 1e ao a . 0A 9ri R U ( 9 K (

g be e

R N

) g

h nitr mo o

N y, Wa 0

, 0n 6

ha 5 6

t a t

n t c e 4

o U t 2a i -

M , tna t o 8 u 2S 0,

o , 2o C n t 1

e 0k o 2d a d

i e 8a r 0r D a g t

o eL O

6 e Sl h -

R 2o t l h

C

u a A

, 1C t r( o 8 3n P

8 eS

o E 1 ) . g 9 vi , 3

n na S 0t e 9 eo . 3i o R U 9 D (

g ke a

R D

, iia

wa

H,

a 5

i 0n t 1r c 4o t

af ei t 9l en

a ro A

C t

C S C 4

,

d 6a e

o 1n na 9 ,

o e n r c 4o s -z Li o i h 7r l i ct 4A ga( n e w n

a 9

9 a

o R r ) ) H Fn 5

n i . a g S 1d e 5

ao . 4i a R U 7 S (

g ve e

R N

, n

og

er 8 8

O 22

, t 11c 1o -ah

e -t M 1a n 0

0d 1 Co uI 1C n 5

, n

W

a d o n 8e 8v 9k i 9a g o A

s

e e i

l L h a t A 1-

R cA ) t e W 3l 5n A x( a S

0 i , P S 5o n s e ) 1 t o E lt 0

gn i c. t 6g i 0n x aS 0i e 2o eo . 2hi R U T 1 S (sg ae

R W

Co

mm

issi

on

90

3

Cente

r Safe

ty

Ro

om

R

egio

nal

Pro

duct

Str

eet,

1

00

14

NY

Easte

rn

Co

nsu

mer

Varick

York

, 6

20

-41

20

20

1

New

(2

12

)

Co

mm

issi

on

29

44

R

oo

m

Cente

r Safe

ty

Str

eet,

Regio

nal

Pro

duct

Dearb

orn

6

06

04

Centr

al

Co

nsu

mer

So

uth

IL

3

53

-82

60

23

0

Chic

ago

, (3

12

)

HU

D L

ead

Off

ice

Co

mm

issi

on

61

0-N

Cente

r Safe

ty

Regio

nal S

uite

Pro

duct

94

61

2

Str

eet,

Weste

rn

Co

nsu

mer C

A

Cla

y

63

7-4

05

0

13

01

O

akla

nd

, (5

10

)

Ple

ase

conta

ct

HU

D's

Off

ice o

f H

ealthy H

om

es

and

Lead

Hazard

C

ontr

ol fo

r in

form

ation o

n lead

regula

tions,

outr

each e

ffort

s, a

nd

le

ad

hazard

contr

ol and

rese

arc

h g

rant

pro

gra

ms.

Develo

pm

ent

Co

ntr

ol

Urb

an

Hazard

and

Lead

Ho

usin

g

and

-3

20

6

H

om

es P,

SW

of

20

41

0

Dep

art

ment

Str

eet,

H

ealthy

DC

of

Off

ice 7

55

-17

85

Seventh

.

S.

Wash

ingto

n,

U 45

1

(20

2)

This

docum

ent

is in t

he p

ublic

dom

ain

. It

may b

e r

epro

duced

by a

n indiv

idual or

org

aniz

ation w

ithout

perm

issi

on.

Info

rmation p

rovid

ed

in t

his

bookle

t is

base

d

upon c

urr

ent

scie

ntific a

nd

technic

al unders

tandin

g o

f th

e iss

ues

pre

sente

d a

nd

is

reflective o

f th

e jurisd

ictional boundaries

est

ablis

hed

by t

he s

tatu

tes

govern

ing

the c

o-a

uth

oring a

gencie

s. F

ollo

win

g t

he a

dvic

e g

iven w

ill n

ot

necess

arily

pro

vid

e c

om

ple

te p

rote

ction in a

ll si

tuations

or

again

st a

ll health h

azard

s th

at

can

be c

ause

d b

y lead

exp

osu

re.

A747

-K-99

-001

2003

EP June

2020

720

460

DC

2041

0

DC DC

ashin

gton

Wash

ington

ashin

gton

W CP

SC W A

EP HUD

U.

S.U.

S. U.

S. 12

13

After carefully reading the notice entitled, “Protect Your Family from Lead in Your Home,” please sign this receipt and return it with your application.

RECEIPT

I have received a copy of the notice entitled “Protect Your Family from Lead in Your Home.”

Print Full Name:

Signature:

Address:

Date:

Housing Rehabilitation Program Design July 2016

1 | P a g e

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

HOUSING REHABILITATION LOAN PROGRAM DESIGN

OWNER-OCCUPIED AND RENTAL PROPERTIES (1-4 UNITS)

I. INTRODUCTION

A. Purpose & Objectives:

1. The purpose of the Housing Rehabilitation Loan Program (the “Program”) is to maintain residential properties within Sonoma County (County) which are predominantly occupied by low-income households.

2. The primary objective of the Program is to provide decent, safe and

sanitary housing for low-income residents of Sonoma County through the correction of actual or potential health and safety problems in existing structures.

3. The secondary objectives of the Program are to:

a. preserve Sonoma County’s affordable housing stock;

b. mitigate hazards and correct potential health and safety problems in designated areas of special need; and

c. assist in the process of neighborhood revitalization. B. Authority:

1. The five members of the Sonoma County Board of Supervisors, acting in their capacity as Commissioners, form the governing body for the Community Development Commission (Commission). This Program Design, containing the policies which form the framework for the Housing Rehabilitation Program, has been adopted by the Commissioners. No revisions may be made hereto without the express action of the Commissioners.

2. The Executive Director of the Commission is hereby granted the authority

to make exceptions to the policies contained in this Program Design to the extent necessary to provide assistance required to correct health and safety hazards that are deemed an imminent threat to the occupants’ physical well-being.

Housing Rehabilitation Program Design July 2016

2 | P a g e

C. Program Funding:

1. Funding for this program will be from a variety of sources, including Federal Community Development Block Grant (CDBG), County Reinvestment and Revitalization Fund, Commission Low- and Moderate-Income Housing Asset Fund (LMIHAF), and other funds as designated from time to time by the Sonoma County Board of Supervisors/Sonoma County Community Development Commission.

2. The applicable regulations, priorities, and policies of each available funding source shall govern use of such funds and, in any instances of conflict with the provisions of this Program Design, the funding source regulations, priorities, and policies shall prevail.

II. ELIGIBILITY The Commission shall not discriminate in the provision of financial assistance because

of race, color, ancestry, national origin, religion, sex, marital or familial status, age, medical condition, handicap, disability, sexual orientation, domestic partnership or other prohibited basis.

A. Conflict of Interest: No member of the governing body of the County of Sonoma,

participating city, or the Community Development Commission and no other official or employee or agent of the County government, participating city, or Commission who exercises any policy decision making functions or responsibilities in connection with the planning and implementation of the Housing Rehabilitation Loan Program shall directly or indirectly be eligible for assistance under the Program.

B. Ownership & Residency: The applicant must be the legal owner of the real

property, or the registered owner of the mobile home, to be rehabilitated. 1. For owner-occupied properties, the property must be occupied by the

owner as his or her principal residence. 2. It is not required that non-occupants on title to a real property, or listed as

registered owners on a mobile home title, be named as a maker on the loan, but they must sign the related Deed of Trust or Security Agreement.

3. Applicants who occupy and control a residential property through a

revocable or irrevocable trust, a life-estate, or other similar arrangement shall be eligible for a loan if the applicant has the legal right to encumber the property. If the trust, life estate or other arrangement requires the trustee or other non-occupant on title to approve any encumbrance on the property, the trustee or other non-occupant on title will be required to co-sign the Deed of Trust or Security Agreement to secure the loan.

Housing Rehabilitation Program Design July 2016

3 | P a g e

C. Eligible Properties: Subject to funding availability, loans may be made for

improvements to mobile homes, single-family residences, and multifamily residential properties located within the unincorporated areas of the County of Sonoma or within the boundaries of the participating cities and town. 1. Mobile homes must be legally sited. For mobile homes situated in mobile

home parks, the applicant must have a valid space lease and be current on space lease payments.

2. Properties which have benefited previously through a Commission grant

or loan program may be eligible for the program upon the review and approval of the Commission Director or his/her designee and if all prior loans are fully repaid.

3. Multifamily properties may contain up to four units in one or more buildings

sited on one or more contiguous parcels under common ownership. (Note: Assistance for multifamily properties with more than four units, as defined above, is governed by the Sonoma County Community Development Commission Loan Policies.)

4. Secondary residences (e.g. summer homes, guest cottages not used as

rentals) are not eligible for the program. 5. Condominiums and co-operative units are not eligible. Townhouses and

co-housing may be eligible if permitted by regulations and policies of available funding sources.

D. Displacement: Rental property owners shall provide certification of the following:

1. The proposed rehabilitation work will not cause permanent displacement

of any of the tenants currently residing at the project.

2. No tenant has been, nor will be, forced to move from the project permanently so that the project may qualify for the Housing Rehabilitation Program.

E. Income and Asset Limits: All occupant households must demonstrate income

and asset eligibility.

1. Eligible properties shall be occupied by low-income households with incomes not to exceed 80% of area median income (AMI) adjusted for family size.

2. At least 51% of the units in a multifamily complex and one unit in a duplex must be occupied by income-eligible tenants.

3. AMI is determined by the U.S. Department of Housing and Urban

Development (HUD) or the California Department of Housing and

Housing Rehabilitation Program Design July 2016

4 | P a g e

Community Development (HCD), depending upon the funding source for the rehabilitation loan.

4. Household income is computed as defined in Section VIII. 5. There shall be a cap on the level of assets allowed for program eligibility for

owner-occupied properties.

a. Household assets cannot exceed 150% of the HUD AMI for a household of four persons* except as provided for below, regardless of funding source for loan.

b. Elderly and/or permanently disabled households may have assets not exceeding 300% of the HUD AMI for a household of four persons*, regardless of funding source for loan.

*As of May, 2015, the HUD AMI for a household of four is $75,900.

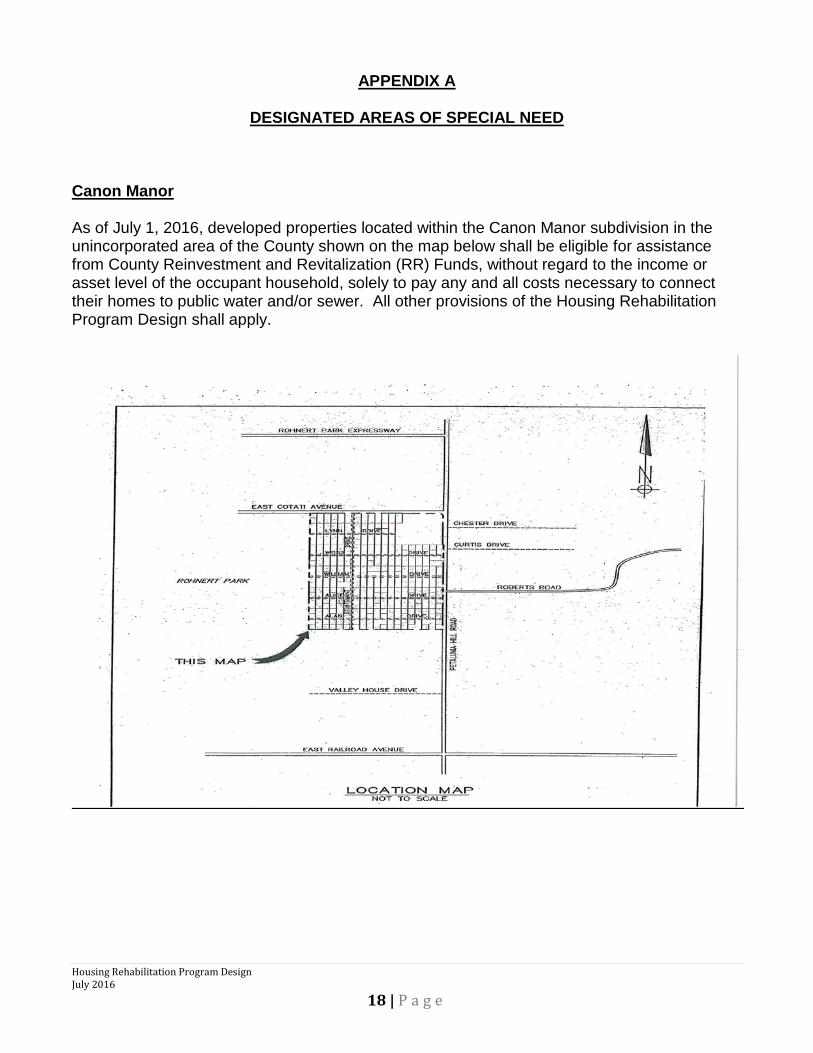

6. Notwithstanding the foregoing provisions of this Section II, properties in

areas designated in Appendix A as areas of special need for purposes of mitigating hazards or correcting potential health and safety problems are not subject to income or asset requirements to be eligible for assistance.

III. LOAN TERMS AND CONDITIONS The Commission will offer amortized and deferred-payment loans with below-market interest rates. Each of these is described in greater detail below. All property owners must provide financial documentation sufficient for Commission staff to make loan approval decisions in compliance with the following loan terms and conditions. A. All loans under this policy are non-recourse loans.

B. Amortized Loans: All loans to rental property owners shall be fully amortized loans. Loans to owner-occupants who are able to afford the regular monthly payments on the loan shall also be fully amortized. An owner-occupant household will be considered able to afford monthly payments on an amortized loan if their total monthly housing costs are less than 30% of their gross monthly income. Monthly housing costs shall be defined as the sum of all mortgage payments including the rehabilitation loan payments, property taxes, homeowner's insurance, homeowner’s association dues, and utility costs. Housing costs for mobile home owners shall also include the monthly park space rent. Utility costs shall include gas, electricity, other heating fuel, water, sewer, garbage, and shall be calculated using allowances established by the Sonoma County Housing Authority.

1. Term: All amortized loans will be for a 20-year term. Except as allowed

under Section VII B, amortized loans shall be due and payable in full prior

Housing Rehabilitation Program Design July 2016

5 | P a g e

to 20 years should one or more of the following occur: 1) the borrower dies; 2) the property or any interest therein is sold, conveyed or transferred; 3) the borrower no longer occupies the property as his or her principal residence for reasons other than medical treatment, disability, education, family matters or similar situation which the Commission Director or his/her designee approves in writing and which requires a temporary alternate residence; 4) the borrower does not make payments when due; or 5) a breach of any provision of the note or deed of trust/security instrument occurs.

a. A borrower may prepay the outstanding loan balance, or any

portion thereof, at any time without penalty. b. All payments on the amortized loan shall be applied first to the

interest due and then to the principal balance of the loan.

2. Interest: The annual interest rate for amortized loans is 3%. 3. Loan Amount: The maximum amount of an amortized loan is $50,000 for

a single-family house or mobile home on owned land; $24,000 for a mobile home on a rented space; and $25,000 per unit for multifamily units. Exceptions may be made in cases where hazard mitigation is required as a condition for the rehabilitation work.

B. Deferred-Payment Loans: The Commission shall offer loans on a deferred-

payment basis to owner-occupants who cannot afford monthly payments on an amortized loan at the time of application. The applicant household will be considered unable to afford monthly payments on an amortized loan if their monthly housing costs, as defined in Section III.A, exceed 30% of their gross monthly income.

1. Term: The loan term shall be 20 years. No payments shall be required

prior to the twentieth anniversary of the loan. However, except as allowed under Section VII B, the deferred-payment loan shall be due and payable in full prior to 20 years should one or more of the following occur: 1) the borrower dies; 2) the property or any interest therein is sold, conveyed or transferred; 3) the borrower no longer occupies the property as his or her principal residence for reasons other than medical treatment, disability, education, family matters or similar situations which Commission Director or his/her designee approves in writing and which require a temporary alternate residence; or 4) a breach of any provision of the note or deed of trust/security instrument occurs. a. At the beginning of the twenty-first year, the deferred-payment loan

is due and payable in full. b. A borrower may repay the outstanding balance of the loan, or any

portion thereof, at any time without penalty. A borrower may choose to make irregular, periodic payments on the deferred-

payment loan. All such prepayments will be credited first to the interest due and then to the principal balance of the loan.

2. Interest: Interest will be simple interest. Interest shall accrue on the unpaid principal balance from the date on which the Promissory Note is executed. The annual interest rate for deferred payment loans is 3%.

3. Loan Amount: The maximum amount of a deferred-payment loan is

$50,000 for a single-family house or mobile home on owned land and $24,000 for a mobile home on a rented space. Exceptions may be made in cases where hazard mitigation is required as a condition for the rehabilitation work.

C. Relocation Requirements: Owners of rental properties must agree to comply with

all applicable federal and state relocation laws and regulations.

1. If temporary relocation of tenants is required during rehabilitation, the borrower shall be responsible for locating comparable temporary housing which is suitable, decent, safe and sanitary.

2. The rental property owner shall be responsible for paying all reasonable

out-of-pocket expenses incurred by the tenants in connection with the temporary relocation including the cost of moving to and from the temporarily occupied housing and any increase in monthly rent and utility costs at such housing.

3. The rental property owner shall deposit sufficient funds into an approved

escrow account to fully cover the estimated temporary relocation costs of the project. The Commission shall issue payments from the escrow account to the tenants, or to the rental property owner if payment has already been made to the tenants, for reimbursement of all reasonable out-of-pocket relocation expenses incurred.

D. Affordability Restrictions: The following affordability restrictions will be required

based on whether the rehabilitation is considered to be “substantial” or “non-substantial”, as defined in Section VIII.

1. Substantial Rehabilitation:

a. For any substantial rehabilitation of rental property assisted with any source of funds, a covenant will be recorded restricting continued occupancy of the property to low- or very low-income households for fifty-five (55) years. Said covenant shall run with the land.

b. If required by the funding source for substantial rehabilitation of owner-occupied single-family properties, a covenant will be recorded restricting continued occupancy of the property to low- or very-low

Housing Rehabilitation Program Design July 2016

6 | P a g e

Housing Rehabilitation Program Design July 2016

7 | P a g e

income households for up to forty-five (45) years. Said covenant shall run with the land.

2. Non-Substantial Rehabilitation:

a. For non-substantial rehabilitation of rental properties assisted with any source of funds, a covenant will be recorded restricting continued occupancy of the units to low- and very low-income households for twenty (20) years. Said covenant shall run with the land.

b. If required by the funding source for non-substantial rehabilitation of

owner-occupied single-family properties, a purchase option will be recorded in favor of the Commission for up to fifteen (15) years. The Commission will exercise the option if (a) the owner decides to sell the property during the term of the option, (b) the Commission identifies a qualified buyer, and (c) the Commission has adequate funding to support, if needed, said buyer’s acquisition of the property at fair market value. If the Commission does not exercise the option, the seller can sell the property on the open market. The specific terms of the purchase option shall be detailed in an Option Agreement, available in template form for prospective borrowers to review.

IV. ELIGIBLE IMPROVEMENTS

A. Eligible Improvements: Improvements must be of a permanently fixed nature. Repairs and improvements should be completed in the following priority order.

1. Improvements to correct health and safety hazards, including lead hazard

removal, and to maintain the structural integrity of the building. 2. Repairs to correct cited code violations. 3. Repairs to correct other code items. 4. Repairs to correct incipient code items.

B. Ineligible Improvements:

1. Items which exceed the Commission’s “moderate quality” standards for fixtures, windows, floor coverings, finishes, and other items.

2. Improvements of a recreational nature are not eligible. 3. Luxury improvements.

C. In no event shall the Commission approve loans for work unless all identified items described in IV.A:1 and 2 are corrected as a result of the work carried out in conjunction with the Commission's loan, except as permitted in areas of special need as designated in Appendix A.

Housing Rehabilitation Program Design July 2016

8 | P a g e

D. The Commission shall not approve loans for work required to repair a condition

for which the applicant has received, or will receive, an insurance settlement or funds from another source (such as FEMA or SBA) to pay for the repair except to augment the insurance or other funds in cases where such funds are insufficient to make the required repairs in compliance with all applicable codes or ordinances.

E. All work funded in whole or in part by the Commission is subject to the permit

processes of the State, County and/or city in which the property is located.

1. All work must be done according to standards acceptable to the Sonoma County Permit and Resource Management Department, the State of California Department of Housing and Community Development, and/or the building inspection department of the city in which the property is located.

2. The proper permit(s) shall be obtained for all work which requires such

permit(s). The cost of permits may be part of the loan. F. "Self-Help" work by the owner-occupant may not be a part of the contract or loan.

No "volunteer" assistance is allowed primarily for liability reasons.

V. LOAN PROCEDURES

A. Application Process:

1. All loan applications will be processed and evaluated on a first-come, first-served basis. Completed applications will be considered for assistance based upon the order of receipt of completed applications by the Commission. An application will be considered to be complete when all required information has been supplied by the property owner(s) and tenant households.

2. All applicants will complete a pre-application and furnish Commission staff

with all required verifications. The information in the pre-application will be used to determine the applicant's initial eligibility for assistance.

3. After initial eligibility has been established, a thorough inspection of the property will be carried out by Commission staff. If necessary, additional tests and/or inspections by third parties will be conducted. A rough scope of work and cost estimate will be developed based on the inspection(s), tests and consultation with the property owner.

4. After review and acceptance of the rough scope of work by the

homeowner, Commission staff will prepare a formal loan application.

Housing Rehabilitation Program Design July 2016

9 | P a g e

B. Loan Approval: Commission staff shall exercise sound underwriting practices in all loan transactions. 1. In all instances, the Commission's underwriting standards will be