Embed Size (px)

Citation preview

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 1/31

Initiating Coverage on

Bearings Sector

October 2011

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 2/31

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 3/31

Snapshot of Views on Stocks

Company

Businessanalysisoutcome View Rating

SKF India Rank: 4 Growth to be driven by auto OEM demand and capital formation led industrial demand for the next two years Variablized cost structure and diversified customer base to help withstand cyclical downturns Unorganized players and counterfeits to continue impacting after-market growth, but competitive position on supplies to OEMs is expected to

remain strong Estimate topline CAGR of 19% from CY10-CY12E and PAT CAGR of 20% for the same period

ADD

OUTPERFORM

TP: Rs 727

Bearings Sector

Sector Outlook Positive

Initiating Coverage

NRBBearings

Rank: 8 Dominant market position to sustain in needle roller bearings Domestic revenues to be inline with OEM growth Export revenues to drive overall growth Capital requirements to be high given the company’s backward integration Estimate topline CAGR of 16% from FY11-FY13E and PAT CAGR of 13% over the same period leading to a FY13E PAT of Rs. 669mn

NOT RATED

FAGBearings

Rank: 1 Growth to be driven by industrial capacity addition and automotive sector growth High cost structure variablization similar to SKF Substantial presence in roller bearings presents a lower threat from counterfeits relative to SKF, and stronger after-market growth

Strong free cash flow generation to enable the company to remain debt free Estimate topline CAGR of 18.6% for CY10-12E and PAT CAGR of 20% over the same period leading to a CY12E PAT of Rs. 1.96bn

NOT RATED

2

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 4/31

Valuation Matrix

Bearings Sector

Sector Outlook Positive

Initiating Coverage

Company

Sales (Rs. mn) EBITDA (Rs. mn) PAT (Rs. mn) EPS (Rs.) EBITDA Margin

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

SKF India 20,932 25,781 29,644 2,794 3,451 4,015 1,770 2,190 2,556 33.6 41.5 48.5 13.3% 13.4% 13.5%

FAG Bearings 10,486 12,283 14,738 1,887 2,425 2,924 1,215 1,638 1,961 73.1 98.5 118.0 18.0% 19.7% 19.8%

Note: CY financial year end for FAG and SKF and March FY ended for NRB

, , , , , , . . . . . .

Company

P/E EV/EBITDA EV/Sales

CMP (Rs)

Mkt Cap Target Rating

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

CY10/FY11

CY11E/FY12E

CY12E/FY13E

(Rs. mn) P/E Price Absolute Relative

SKF India 20.0x 16.2x 13.8x 11.9x 9.3x 7.5x 1.6x 1.2x 1.0x 671 35,384 15x 727Add OPF

FAG Bearings 16.0x 11.8x 9.9x 8.8x 6.3x 4.4x 1.6x 1.2x 0.9x 1,167 19,396 NA NANR NR

NRB Bearings 8.7x 8.1x 6.8x 5.3x 5.0x 4.3x 1.2x 1.1x 0.9x 47 4,555 NA NANR NR

3

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 5/31

Table of Contents Sector Outlook Positive

Initiating Coverage

Section Page

Industry Scenario

Bearings Industry Overview 6

Business and Financial Analysis

Bearings Sector

ompara ve na ys s o u o omponen overage n verse

Limited differentiation among bearing companies 11

SKF scores in non-auto exposure 13

FAG outperforms in cash flow generation 15

Wabco, SKF and FAG have the least leverage 17

SKF and FAG have variable cost structure but lower margins compared to NRB 20

Company Section

SKF India 24

NRB Bearings 26

FAG Bearings 28

4

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 6/31

Industry Scenario

5

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 7/31

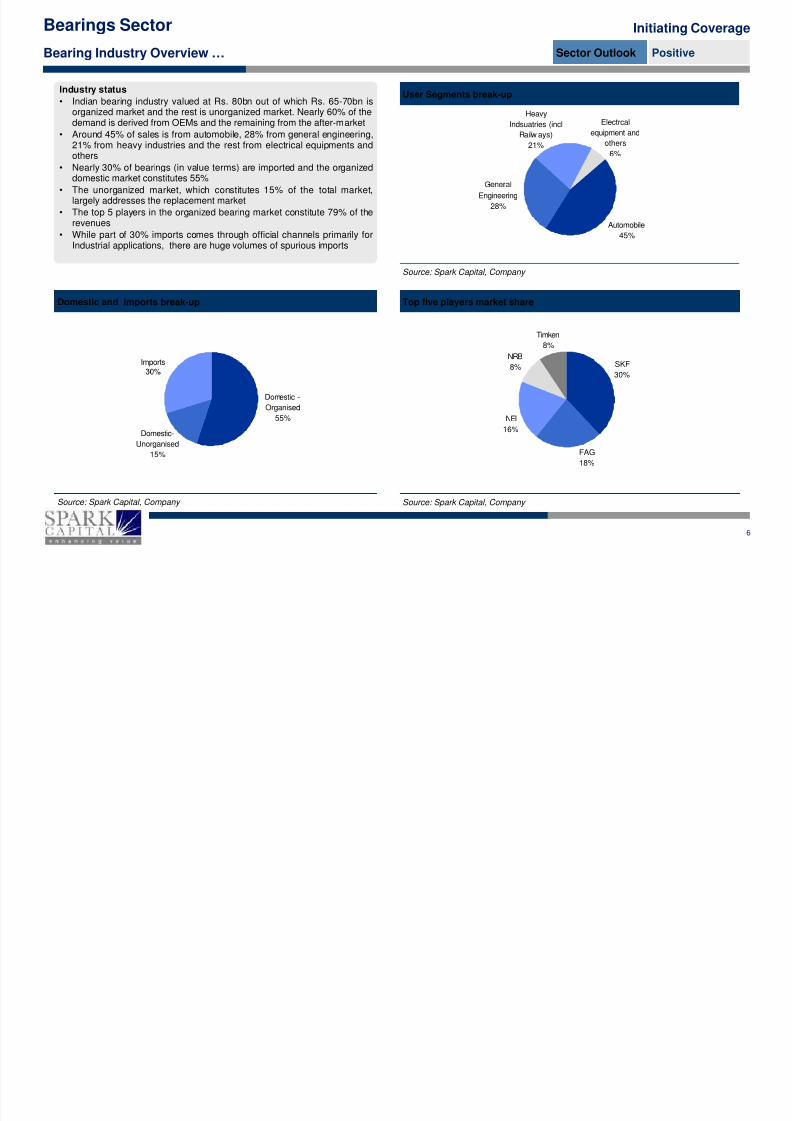

Bearing Industry Overview …

Industry status

• Indian bearing industry valued at Rs. 80bn out of which Rs. 65-70bn isorganized market and the rest is unorganized market. Nearly 60% of thedemand is derived from OEMs and the remaining from the after-market

• Around 45% of sales is from automobile, 28% from general engineering,21% from heavy industries and the rest from electrical equipments andothers

• Nearly 30% of bearings (in value terms) are imported and the organizeddomestic market constitutes 55%

Bearings Sector Initiating Coverage

Sector Outlook Positive

User Segments break-up

Electrcal

equipment and

others

6%

Heavy

Indsuatries (incl

Railw ays)

21%

• The unorganized market, which constitutes 15% of the total market,largely addresses the replacement market

• The top 5 players in the organized bearing market constitute 79% of therevenues

• While part of 30% imports comes through official channels primarily forIndustrial applications, there are huge volumes of spurious imports

Top five players market shareDomestic and imports break-up

Source: Spark Capital, Company

Automobile

45%

Engineering28%

Imports SKFNRB

8%

Timken

8%

6

Source: Spark Capital, Company Source: Spark Capital, Company

Domestic -

Organised

55%

Domestic-

Unorganised

15%

30%

FAG

18%

NEI

16%

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 8/31

Types of bearings and its applications

Bearing Industry Overview …

Types of bearings Applications

Deep groove ball bearing Wide applications in two-wheelers, four-wheelers,

three-wheelers (Used in wheel, axles)

Spherical roller bearing Car suspension, drive shaft, heavy machinery

Types of bearings and market share

ManufacturerTypes of bearingsproduced Market share

SKF India Deep groove ball bearing 65-70%

FAG India Spherical and cylindrical

roller bearing 45%

Sector Outlook Positive

Initiating CoverageBearings Sector

Source: Spark Capital, Company

Cylindrical roller bearing Machine tools, transmissions, wheel-set bearings for

railway applications

Tapered roller bearing Wide application in commercial vehicles

Needle roller bearing Niche application in engine, gearbox. With less load

and thrust

Source: Spark Capital, Company

INA - (FAG's subsidiary) Needle Roller bearing 30%

Timken Taper Roller bearing 40-50%

NRB Bearings Needle Roller bearing 70%

Organised market size – Product-wise

Bearing Market – Rs. 65-70bn

• The organized market is estimated to be between Rs 65-70bn with over55% of the market dominated by ball bearing (primarily deep groove ballbearing)

• The competitive intensity among organized players is low given thateach la er is dominant in one of the roduct se ments

7

Source: Spark Capital, Company

Ball bearingRs 35-40bn

Spherical andcylindrical roller

bearing: Rs 10-15bn

Needle roller bearing – Rs.5bn

Tapered roller bearing – Rs. 10bn

• Large spurious and illegal import of bearing (esp. deep groove ballbearing) is an evergreen threat to the industry

• Competitive intensity to increase in the needle roller bearing market andtaper rolling bearing in the next 2-3 years with INA and Timken settingup capacities respectively

• Unorganized players will continue to impact the deep groove ballbearing market

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 9/31

Business & Financial Analysis

8

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 10/31

Identifying Critical Success Factors (CSFs)

Our CSF matrix compares the nine auto-component companies with eight critical success factors and eight financial parameters.

Parameters Definition

OEM’s dependence Dependence of the OEM, for the components. The relative criticality of a component in the vehicle (for the OEM).

Technology/R&D/Patents Technology, R&D barrier created by the company

Sector Outlook Positive

Initiating CoverageBearings Sector

Criticalsuccessfactors

Replacement Market/distribution network Proportion of revenues from replacement market (aftermarket)

Risk of JV divorce Dependency on JV partner

Customer concentration Large share of revenue coming from few key customers

Non-Auto exposure Proportion of revenue from non-automotive business (related diversification)

Competitive Landscape Market share, competitive positioning in the industry segment

Impact of govt. policies/external factors Favourable/un-favourable implication of changes in govt. policies/external factors

Revenue growth (CAGR FY11 - 13E)

PAT growth (CAGR FY12 - 13E)

EBITDA margin (%)

9

Financialparameters

(FY12E)

Total assets turnover (x)

Working Capital turnover (x)

RoCE (%)

Debt/Equity (x)

OCF/Revenue (%)

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 11/31

CSF & Financial Parameter Ranking

Scoring of coverage universe: Scale: 1 – 9 with 9 being the best

CRITICAL SUCCESS FACTORAmara Raja

Batt. Apollo Tyres Bharat Forge Exide Inds.Motherson

Sumi WABCO-TVS SKF India FAG BearingsNRB Bearings

OEM's dependence 7 5 9 7 8 9 6 6 6

Technology / R&D / Patents 6 4 8 6 7 9 5 5 5

Replacement/After - market 7 9 2 6 2 4 3 6 5

Risk of divorce of JV 7 9 8 7 7 9 9 9 9

Bearings Sector Initiating Coverage

Sector Outlook Positive

Customer concentration 4 9 4 7 5 3 8 8 8

Non-Auto Business 9 3 7 8 4 3 9 8 4

Competitive Landscape 6 3 9 7 7 8 4 4 5

Impact of govt. policy / external factors 7 3 6 7 6 7 4 4 5

Financials (FY13E/CY12E)Revenue growth (CAGR CY10/FY11 -CY12E/FY13E)

9 8 2 1 7 3 6 5 4

PAT growth (CAGR FY11 - 13E/ CY10-12E) 5 4 6 2 9 3 7 8 1

EBITDA margin (%) 3 1 5 5 2 9 4 7 8

Total assets turnover (x) 9 3 2 5 4 8 6 7 1

Working Capital turnover (x) 1 7 4 6 9 2 5 8 3

RoCE % 6 1 2 5 4 9 7 8 3

10

WABCO-TVS scores highon EBITDA margin, RoCE.And scores secondhighest on asset turnover.

FAG, WABCO and Exide are the top 3companies ranked in that order. FAGscores high on customer concentration,non-auto exposure, revenue and earnings

growth, and working capital management

D/E (x) 5 1 2 6 3 6 6 6 4

OCF/Revenue (%) 1 2 5 7 3 6 4 9 8

FINAL RANK 5 9 7 3 6 2 4 1 8

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 12/31

#1 OEM’s Dependence #2 Technology, R&D, Patents

HighComponentcriticality

Hightechnology,R&D,patents

Highbarriersto entry

Highswitchingcosts forOEMs

Highbargainingpower forACMs

Bearings Sector

Sector Outlook Positive

Initiating Coverage

Brakingsystems

WABCO-TVS

Forged parts

BHARAT FORGE

Impeccable Function-ality is a hygiene factor.High impact on OEMsreputation

‘Building Blocks’of the vehicle

Parent acquired 166new patents in 2009

Owns process patents

OEM’sdependence Score

WABCO-TVS 9

Bharat Forge 9

Motherson Sumi 8

Amara Raja 7

Apollo Tyres 5

Technology,R&D, Patents Score

WABCO-TVS 9

Bharat Forge 8

Motherson Sumi 7

Amara Raja 6

Apollo Tyres 4

11

Wiring harness,

mirrors

MOTHERSON SUMI

Tyres, Battery, Bearings

NRB, SKF, FAG, APOLLOTYRES / AMARA RAJA /

EXIDE INDUSTRIES

Limiteddifferentiationamongvendors

Predominantly

addressingfunctionality ofperipherals

Know-how in manufac-

turing key components(Fuse, connectors etc.).SMR owns 600 patents.

Technologyinvestment primarilyto survive anddifferentiate

Exide Industries 7

SKF India 6

FAG Bearings 6

NRB Bearings 6

Exide Industries 6

SKF india 5

FAG Bearings 5

NRB Bearings 5

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 13/31

#3 Replacement Market #4 Customer Concentration

Apollo TyresHigh Low customer concentration

APOLLO TYRES

EXIDE INDUSTRIES

r e

Replacement market revenues as a % of total revenues

50 - 60%

> 70%

Aftermarket Score FAG, SKF, NRB

Sector Outlook Positive

Initiating CoverageBearings Sector

Exide Industries

Amara Raja, FAG

WABCO-TVS, NRB,SKF

BHARAT FORGE

HighLow Market share

High customer concentration

WABCO-TVS

AMARA RAJA,

MOTHERSON SUMI

A f t e r m a r k e t e x p o

s u

10 - 20%

20 - 30%

30 - 40%

40 - 50%Apollo Tyres 9

Exide Industries 6

Amara Raja 7

WABCO-TVS 4

Bharat Forge 2

Motherson Sumi 2

SKF India 3

FAG Bearings 6

12

Motherson Sumi,Bharat Forge,

High after marketexposure

High marketshare+ = Low customer

concentration

Aftermarketexposure

Pricingpower

Volumecyclicality

< 10%

NRB Bearings 5

Customerconcentration

ApolloTyres Exide Inds.

AmaraRaja

Motherson Sumi

WABCO-TVS

BharatForge

SKFIndia

FAGBearing

s

NRBBearing

s

Score 9 7 4 5 3 4 8 8 8

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 14/31

#5 Non-auto Exposure #6 Risk of JV Divorce

Non-auto revenues as a % of total revenues (relateddiversification

40 - 50%

> 50%

Amara Raja, SKF

Details of key JVs/technology partners

COMPANY JV / TECHNOLOGY PARTNER DETAILSAmara RajaBatteries Johnson Controls

Equal equity stake of 26%, Technology provider for autobatteries

Exide IndustriesFurukawa Batteries, Shin-KobeElectric Machinery Automotive and VRLA Lead Acid Storage Batteries

Motherson Sumi(MSSL) Sumitomo Wiring

Sumitomo wiring has 25% equity stake (technology providerfor wiring harness business), MSSL has six other key JVs

Bharat Forge NTPC, Alstom For foray into power equipment business

Non-autoexposure Score

Initiating Coverage

Sector Outlook Positive

Bearings Sector

5 - 10%

10 - 20%

20 - 30%

30 - 40%

Motherson Sumi,NRB

Bharat Forge

Exide Industries,FAG

Apollo Tyres - -

WABCO-TVS - -

SKF India - Global SKF provides technology know-how

FAG Bearings - Schafeller group provides technological know-how

NRB Bearings -

Inherited the technology from Nadella during its initialtie-up and now are internally capable to manufactureneedle roller bearing

Company Presence of JVImpact ofdivorce

Dependencefor technology

Historical issues withpartner

Amara Raja Batteries High High

Exide Industries High High

Motherson Sumi High High

Bharat Forge Low Low

Apollo Tyres - - -

WABCO-TVS - - -

Amara Raja 9

Exide Industries 8

Bharat Forge 7

Motherson-Sumi 4

WABCO-TVS 3

Apollo Tyres 3

SKF india 9

13

< 5% WABCO-TVS,Apollo Tyres

Dependenceon JV partner

Risk in theevent ofdivorce

Volumecyclicality

Non-autoexposure

SKF India - - -

FAG Bearings - - -

NRB Bearings - - -

Risk of JVdivorce Apollo Tyres

WABCO-TVS

BharatForge

AmaraRaja

ExideInds.

Motherson Sumi

SKFIndia

FAGBearings

NRBBearings

Score 9 9 8 7 7 7 9 9 9

NRB Bearings 4

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 15/31

#7 Competitive Landscape

Company Market Share Competitive Scenario

Bharat Forge 90% Sole supplier to most CV OEMs

WABCO-TVS 80% Duopoly (Knorr-Bremse second largest)

Exide Industries ~70% Duopoly (Amara Raja second largest)

Motherson Sumi 65% Duopoly (Tata Yazaki second largest)

Apollo Tyres ~30% Highly competitive market (top 5 players account for ~90%)

Amara Raja ~30% Duopoly (Exide Industries is the largest)

Competitive landscape Score

Bharat Forge 9

WABCO-TVS 8

Exide Inds. 7

Motherson Sumi 7

Amara Raja Batt. 6

Sector Outlook Positive

Initiating CoverageBearings Sector

#8 Impact of government policies/external factors

SKF India 65-70% / 30%

- % mar et s are n eep groove a ear ng an % nv overa

organized bearing market

FAG Bearings 18-20%Second leading player in the overall organized market with strongpresence in the cylindrical and spherical ball bearings

NRB Bearings 70% / 12%Leader in the needle roller bearing market with 70% share and 12% sharein the overall organized market

Apollo Tyres 3

SKF india 4

FAG Bearings 4

NRB Bearings 5

Company Impact of govt. policies / external factors Details

Apollo Tyres NEGATIVE Policy on import of tyres and rubber, movement to radials

Amara Raja POSITIVE Policy on disposal of used batteries, movement to VRLA

batteries

Impact of govt. policy Score

WABCO 7

Apollo Tyres 3

14

Exide Industries POSITIVE Policy on disposal of used batteries, movement to VRLA

batteries

WABCO-TVS POSITIVE Policy on mandatory ABS in certain CVs

Motherson Sumi NEUTRAL -

Bharat Forge NEUTRAL -

SKF India NEGATIVE Policy on spurious bearings and import duty

FAG Bearings NEGATIVE Policy on import duty

NRB Bearings NEGATIVE Policy on import duty

.

Bharat Forge 6

Exide Inds. 7

Motherson Sumi 6

SKF india 4

FAG Bearings 4

NRB Bearings 5

B i S t

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 16/31

10%

15%

20%

20%

30%

40%

50%

OCF/sales – FAG scores highest while Amara scores the lowestRoE - WABCO scores highest while Apollo scores the lowest

#9 Capital Efficiency #10 Cash Flow

6 1 2 4 8 9 1 2 5 7 3 63 5 7 4 9 8

Initiating Coverage

Sector Outlook Positive

Bearings Sector

10%

15%

0%

5%

ARBL APTY BHFC EIL MSSL W TVS SKF FAG NRB

FY11 FY12E FY13E

30%

40%

0%

10%

ARBL APTY BHFC EIL MSSL WTVS SKF FAG NRB

FY11 FY12E FY13E

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

6 1 2 5 4 9 1 3 4 7 2 87 8 3 6 9 5

RoACE – WABCO scores the highest while Apollo scores the lowest FCF/sales – FAG scores the highest and Amara scores the lowest

-10%

-5%

0%

5%

ARBL APTY BHFC EIL MSSL WTVS SKF FAG NRB

FY11 FY12E FY13E

0%

10%

20%

ARBL APTY BHFC EIL MSSL W TVS SKF FAG NRB

FY11 FY12E FY13E

15

Source: Spark Capital, Company. . Note: CY for FAG and SKF and FY for NRB Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB Note: ARBL – Amara Raja Batteries, APTY. Apollo Tyres, BHFC – Bharat Forge, EIL – Exide Industries, MSSL-Motherson Sumi, WTVS-WABCO TVS

B i S t

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 17/31

15%

20%

25%

30%

15%

20%

25%

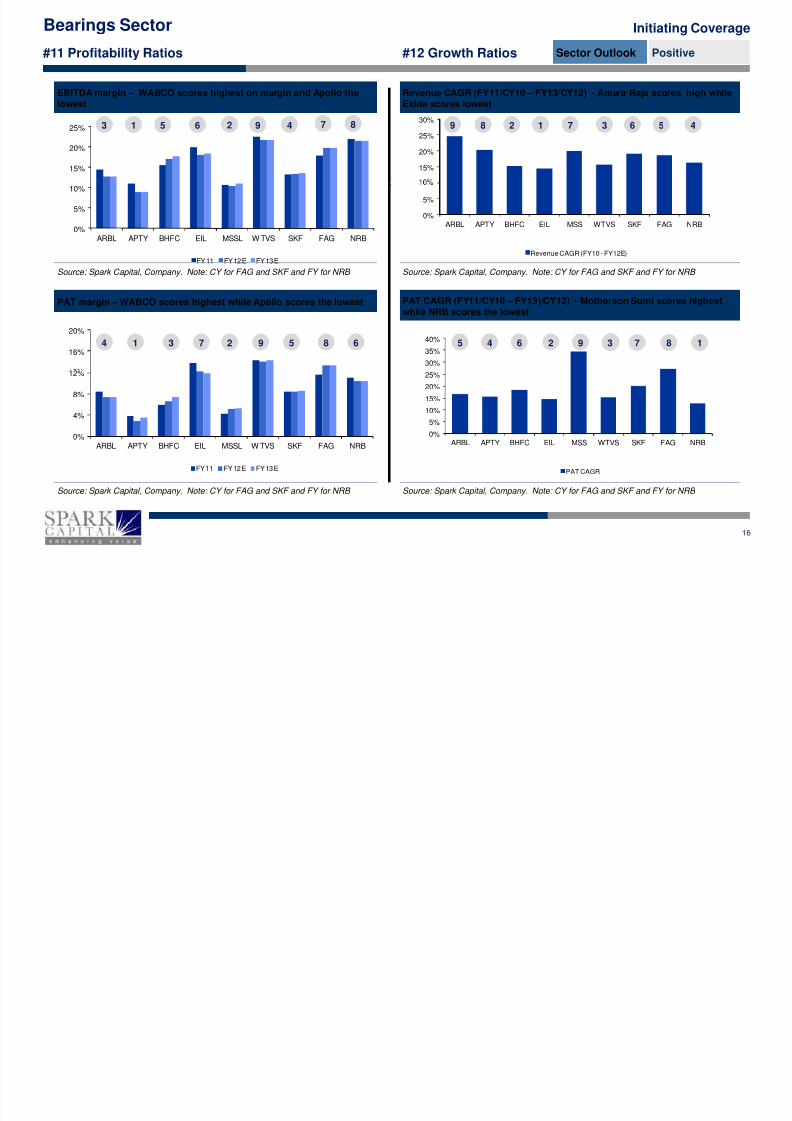

EBITDA margin – WABCO scores highest on margin and Apollo the

lowest

Revenue CAGR (FY11/CY10 – FY13/CY12) - Amara Raja scores high while

Exide scores lowest

#11 Profitability Ratios #12 Growth Ratios

3 1 5 6 2 9 9 8 2 1 7 34 7 8 6 5 4

Initiating Coverage

Sector Outlook Positive

Bearings Sector

30%

35%

40%

16%

20%

0%

5%

ARBL APTY BHFC EIL MSS WTVS SKF FAG NRB

Revenue CAGR (FY10 - FY12E)

0%

5%

10%

ARBL APTY BHFC EIL MSSL W TVS SKF FAG NRB

FY11 FY12E FY13E

PAT CAGR (FY11/CY10 – FY13)/CY12) - Motherson Sumi scores highestwhile NRB scores the lowest

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

PAT margin – WABCO scores highest while Apollo scores the lowest

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

4 1 3 7 2 9 5 4 6 2 9 55 8 6 5553 7 8 1

0%

5%

10%

15%

20%

25%

ARBL APTY BHFC EIL MSS WTVS SKF FAG NRB

PAT CAGR

0%

4%

8%

12%

ARBL APTY BHFC EIL MSSL W TVS SKF FAG NRB

FY11 FY12E FY13E

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

16

Bearings Sector

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 18/31

1.5

2.0

2.5

1.0x

1.5x

Debt / Equity – WTVS, SKF and FAG scores the highest, while Apollo the

lowestTotal asset turnover (x) – NRB scores the highest while FAG scores thelowest

#13 Turnover Ratios #14 Leverage Ratios

9 3 8 6 7 5 4 1 2 6 3 64 1 2 6 6 4

Initiating Coverage

Sector Outlook Positive

Bearings Sector

0.0

0.5

1.0

ARBL APTY BHFC EIL MSSL W TVS SKF FAG NRB

FY11 FY12E FY13E

30.0%

35.0%

40.0%

50%

60%

0.0x

0.5x

ARBL APTY BHFC EIL MSSL WTVS SKF FAG NRB

FY11 FY12E FY13E

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

Debt / Total assets – WTVS,SKF, FAG scores the highest, while Apollo thelowest

Working capital/sales - APTY scores the highest, while ARBL thelowest

2 7 4 6 9 3 5 1 2 6 3 65 8 1 6 6 4

0.0%

5.0%

10.0%

15.0%

20.0%

.

ARBL APTY BHFC EIL MSSL WTVS SKF FAG NRB

FY11 FY12E FY13E

0%

10%

20%

30%

ARBL APTY BHFC EIL MSSL WTVS SKF FAG NRB

FY11 FY12E FY13E

Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB Source: Spark Capital, Company. Note: CY for FAG and SKF and FY for NRB

17

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 19/31

Comparative analysis of bearing companies

18

I iti ti CBearings Sector

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 20/31

SKF India FAG Bearings

Revenue Profile

Revenue (CY10- Rs. 20.6bn) Revenue (CY10 - Rs. 10.4 bn)

Initiating Coverage

Sector Outlook Positive

Bearings Sector

Source: Company, Spark Capital Source: Company, Spark Capital

NRB Bearings

–

OEM – 70% After-market –

30%

– – –

OEM – 40% After-market –

60%

– –

Revenue (FY11- Rs. 4.66bn)

Revenue contribution from top two kinds of bearings (CY10/FY11)

SKF India NRB Bearings FAG Bearings

19

Source: Company, Spark Capital

Exports – 10%

OEM – 78% After-market –

22%

Industrial – 8%Auto – 82%

Source: Company, Spark Capital

Deep grooveball bearing

35%

Taper rollerbearing

18%

Needle rollerbearing

58%

Cylindricalbearing

16%

Cylindricalbearing

35%

Sphericalbearing

25%

Initiating CoverageBearings Sector

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 21/31

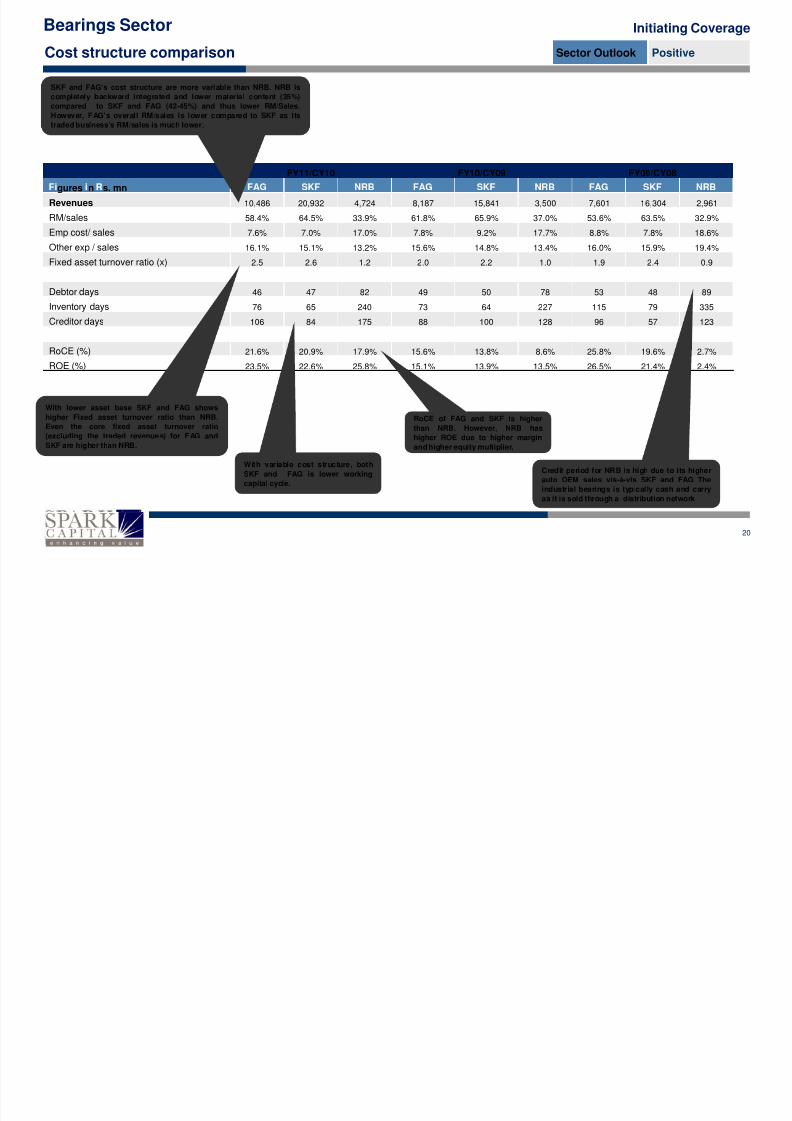

Cost structure comparison

FY11/CY10 FY10/CY09 FY09/CY08

SKF and FAG‘s cost structure are more variable than NRB. NRB is

completely backward integrated and lower material content (35%)

compared to SKF and FAG (42-45%) and thus lower RM/Sales.

However, FAG’s overall RM/sales is lower compared to SKF as its

traded business’s RM/sales is much lower.

Initiating Coverage

Sector Outlook Positive

Bearings Sector

gures n s. mn

Revenues 10,486 20,932 4,724 8,187 15,841 3,500 7,601 16,304 2,961

RM/sales 58.4% 64.5% 33.9% 61.8% 65.9% 37.0% 53.6% 63.5% 32.9%

Emp cost/ sales 7.6% 7.0% 17.0% 7.8% 9.2% 17.7% 8.8% 7.8% 18.6%

Other exp / sales 16.1% 15.1% 13.2% 15.6% 14.8% 13.4% 16.0% 15.9% 19.4%

Fixed asset turnover ratio (x) 2.5 2.6 1.2 2.0 2.2 1.0 1.9 2.4 0.9

Debtor days 46 47 82 49 50 78 53 48 89

Inventory days 76 65 240 73 64 227 115 79 335

Creditor days 106 84 175 88 100 128 96 57 123

RoCE (%) 21.6% 20.9% 17.9% 15.6% 13.8% 8.6% 25.8% 19.6% 2.7%

ROE (%) 23.5% 22.6% 25.8% 15.1% 13.9% 13.5% 26.5% 21.4% 2.4%

20

With lower asset base SKF and FAG shows

higher Fixed asset turnover ratio than NRB.

Even the core fixed asset turnover ratio

(excluding the traded revenues) for FAG and

SKF are higher than NRB.

With variable cost structure, both

SKF and FAG is lower working

capital cycle.

RoCE of FAG and SKF is higher

than NRB. However, NRB has

higher ROE due to higher margin

and higher equity multiplier.

Credit period for NRB is high due to its higher

auto OEM sales vis-à-vis SKF and FAG The

industrial bearings is typically cash and carryas it is sold through a distribution network

Initiating CoverageBearings Sector

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 22/31

FAG scores high on free cash flow generation

FAG historically has demonstrated higher

growth, better working capital management

which is expected to lead to higher FCF

generation.

FAG (Rs. mn) FY10/CY09 FY11/CY10 FY12E/CY11E FY13E/CY12E

Operating Cash Flow 1,634 1,320 1,684 1,980

Capex (78) (197) (225) (275)

Free Cash Flow 1,556 1,123 1,459 1,705

OCF yield (%) 8.45% 6.83% 8.71% 10.24%

Initiating Coverage

Sector Outlook Positive

Bearings Sector

Better working capital management to be the

key driver for NRB’s improvement in

operating cash flow and therefore leading to

hi her ield. The com an will continue to

FCF yield (%) 8.04% 5.81% 7.54% 8.81%

D/E (x) 0 0 0 0

SKF (Rs. mn) FY10/CY09 FY11/CY10 FY12E/CY11E FY13E/CY12E

Operating Cash Flow 2,275 1,147 2,121 2,634

Capex (629) (1160) (1000) (500)

Free Cash Flow 1,646 -13 1,121 2,134

OCF yield (%) 6.80% 3.40% 6.08% 7.54%

FCF yield (%) 4.90% 0.00% 3.21% 6.11%

D/E (x) 0 0 0 0

NRB (Rs. mn) FY10/CY09 FY11/CY10 FY12E/CY11E FY13E/CY12E

Strong growth in operating cash flow and

reduction in capex to lead to improvement

in free cash flow yield by CY12E.

21

have debt, however we believe the existing

financial leverage will be maintained.

Operating Cash Flow 755 351 675 791

Capex (122) (391) (650) (350)

Free Cash Flow 620 23 25 441

OCF yield (%) 17.10% 8.00% 14.80% 17.36%

FCF yield (%) 14.00% 0.50% 0.54% 9.68%

D/E (x) 0.44 0.44 0.5 0.47

Initiating CoverageBearings Sector

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 23/31

SKF India

Trading History

FAG Bearings

7x

10x

13x

16x

19x

300400500600700800900

1,000

C M P ( R s . )

7x

10x

13x16x

19x

1,000

1,500

2,000

2,500

C M P ( R s . )

Initiating Coverage

Sector Outlook Positive

Bearings Sector

NRB Bearings

Source: Bloomberg, Spark Capital Source: Bloomberg, Spark Capital

Forward P/E buckets and Frequency

4x

0100

N o v - 0 6

J a n - 0 7

M a r - 0 7

M a y - 0 7

J u l - 0 7

S e p - 0 7

N o v - 0 7

J a n - 0 8

M a r - 0 8

M a y - 0 8

J u l - 0 8

S e p - 0 8

N o v - 0 8

J a n - 0 9

M a r - 0 9

M a y - 0 9

J u l - 0 9

S e p - 0 9

N o v - 0 9

J a n - 1 0

M a r - 1 0

M a y - 1 0

J u l - 1 0

S e p - 1 0

N o v - 1 0

J a n - 1 1

M a r - 1 1

M a y - 1 1

J u l - 1 1

S e p - 1 1

12M fwd P/E

13x

16x

19x

80

100

120

( R s . )

4x

0

500

O c t - 0 6

J a n - 0 7

A p r - 0 7

J u l - 0 7

O c t - 0 7

J a n - 0 8

A p r - 0 8

J u l - 0 8

O c t - 0 8

J a n - 0 9

A p r - 0 9

J u l - 0 9

O c t - 0 9

J a n - 1 0

A p r - 1 0

J u l - 1 0

O c t - 1 0

J a n - 1 1

A p r - 1 1

J u l - 1 1

12M fwd P/E

P/E Multiple Range SKF FAG NRB

Under 8 24% 28% 16%

-

Source: Bloomberg, Spark Capital

22

Source: Company, Spark Capital; TTM PE for NRB

4x

7x

10x

0

20

40

60

S e p - 0 6

N o v - 0 6

J a n - 0 7

M a r - 0 7

M a y - 0 7

J u l - 0 7

S e p - 0 7

N o v - 0 7

J a n - 0 8

M a r - 0 8

M a y - 0 8

J u l - 0 8

S e p - 0 8

N o v - 0 8

J a n - 0 9

M a r - 0 9

M a y - 0 9

J u l - 0 9

S e p - 0 9

N o v - 0 9

J a n - 1 0

M a r - 1 0

M a y - 1 0

J u l - 1 0

S e p - 1 0

N o v - 1 0

J a n - 1 1

M a r - 1 1

M a y - 1 1

J u l - 1 1

TTM P/E

C M P ( -

10 - 12x 12% 34% 23%

12 - 14x 16% 11% 6%

14 - 16x 31% 1% 8%

16 - 18x 7% 0% 7%

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 24/31

Company Section

23

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 25/31

SKF Bearings Absolute AddCMP Rs. 671

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 26/31

SKF BearingsRelative OutperformTarget Rs. 727Financial Summary

Abridged Financial Statements Key metricsRs. mn CY09 CY10 CY11E CY12E CY09 CY10 CY11E CY12E

Profit & Loss Growth ratios

Revenues 15,841 20,932 25,781 29,644 Revenues -2.8% 32.1% 23.2% 15.0%

Manufacturing & Other Expenses 14,244 18,137 22,330 25,629 EBITDA -23.2% 75.0% 23.5% 16.4%

EBITDA 1,597 2,794 3,451 4,015 PAT -26.2% 87.8% 23.7% 16.7%

Depreciation 290 333 405 456 Margins

EBIT 1,307 2,461 3,045 3,559 EBITDA 10.1% 13.35% 13.38% 13.54%

Net Interest Exp / (inc) (124) (200) (246) (283) EBIT 8.3% 11.8% 11.8% 12.0%

Profit Before Tax 1,431 2,661 3,291 3,842 PAT 5.9% 8.5% 8.5% 8.6%

Tax 489 891 1,102 1,286 Leverage & WC ratios

Adj. Net Profit 942 1,770 2,190 2,556 Debt to equity (x) 0.0 0.0 0.0 0.0

Balance Shee t (Rs. mn) Current ratio (x) 2.7 2.9 2.9 3.1

Shareholders Equity 7,147 8,487 10,144 12,079 Debtor days (Sales) 50 47 47 47

Loan funds 1 0 0 0 Inventory days (COGS) 64 65 65 65

Sources of funds 7,148 8,517 10,174 12,109 Creditor Days (COGS) 100 84 84 84

Net block 2,017 2,834 3,429 3,473 Performance & turnover ratios

Investments RoACE 13.8% 20.9% 21.7% 21.3%

Capital WIP 551 359 359 359 RoAE 13.9% 22.6% 23.5% 23.0%

Current assets, loans & advances 8,236 9,586 11,457 13,995 Total asset turnover (x) 1.0 1.2 1.3 1.3

Current liabilities & provisions 3,026 3,302 4,008 4,567 Fixed asset turnover (x) 2.3 2.7 3.0 3.2

Net Current Assets 5,210 6,284 7,449 9,428 Valuation metrics

25

Application of funds 7,148 8,517 10,174 12,109 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 53 53 53 53

Cash flows from operations 2,275 1,147 2,121 2,634 Market capitalisation (Rs. mn) 35384 35384 35384 35384

Capex 629 1,160 1,000 500 Enterprise value (Rs. mn) 32492 33295 32604 31003

Free Cash Flow 1,646 -13 1,121 2,134 EV/EBIDTA (x) 20.3 11.9 9.4 7.7

Cash flows from investments (1,037) (1,652) (1,000) (500) Adj. Per-share earnings (Rs.) 17.9 33.6 41.5 48.5

Cash flows from financing (272) (255) (430) (533) Price-earnings multiple (x) 37.5 20.0 16.2 13.8

Cash generated during the year 2,879 2,119 2,810 4,411 Dividend yield (%) 0.60% 1.04% 1.29% 1.51%

671

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 27/31

NRB Bearings Absolute Not RatedCMP Rs. 47

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 28/31

NRB BearingsRelative Not RatedTarget N.A.Standalone Financial Summary

Abridged Financial Statements Key metrics

Rs. mn FY10 FY11 FY12E FY13E FY10 FY11 FY12E FY13E

Profit & Loss Growth ratios

Revenues 3,500 4,724 5,379 6,384 Revenues 7.9% 35.0% 13.9% 18.7%

Manufacturing & Other Expenses 466 616 703 833 EBITDA 58.1% 76.9% 11.1% 18.7%

EBITDA 590 1,044 1,159 1,377 PAT 472.5% 115.0% 7.5% 18.5%

Depreciation 195 229 266 309 Margins

, . . . .

Net Interest Exp / (inc) 77 50 88 108 EBIT 11.3% 17.3% 16.6% 16.7%Profit Before Tax 371 782 827 980 PAT 7.0% 11.1% 10.5% 10.5%

Tax 127 257 263 312 Leverage & WC ratios

Adj. Net Profit 244 525 564 669 Debt to equity (x) 0.4 0.4 0.5 0.5

Balance Shee t (Rs. mn) Current ratio (x) 0.3 0.3 0.2 0.2

Shareholders Equity 1,876 2,190 2,496 2,875 Debtor days (Sales) 78 82 82 82

Loan funds 827 971 1,252 1,352 Inventory days (COGS) 227 240 240 240

Sources of funds 2,831 3,277 3,864 4,343 Creditor Days (COGS) 128 175 175 175

Net block 1,525 1,687 2,071 2,112 Performance & turnover ratios

Investments 179 166 166 166 RoACE 8.6% 17.9% 17.1% 17.7%

Capital WIP 13 140 140 140 RoAE 13.5% 25.8% 24.1% 24.9%

Current assets, loans & advances 244 317 317 317 Total asset turnover (x) 0.9 1.1 1.1 1.3

Current liabilities & provisions 727 1,209 1,448 1,678 Fixed asset turnover (x) 1.0 1.3 1.3 1.3

Net Current Assets 1,114 1,285 1,487 1,925 Valuation metrics

27

Application of funds 2,831 3,277 3,864 4,343 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 97 97 97 97

Cash flows from operations 755 351 675 791 Market capitalisation (Rs. mn) 4,560 4,560 4,560 4,560

Capex 122 391 650 350 Enterprise value (Rs. mn) 5,328 5,531 5,812 5,912

Free Cash Flow 620 23 25 441 EV/EBIDTA (x) 9.0 5.3 5.0 4.3

Cash flows from investments (108) (310) (650) (350) Adj. Per-share earnings (Rs.) 2.52 5.41 5.82 6.90

Cash flows from financing (642) (29) (32) (252) Price-earnings multiple (x) 18.68 8.69 8.08 6.82

Cash generated during the year 5 12 (7) 189 Dividend yield (%) 2.1% 4.3% 4.6% 5.4%

47

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 29/31

FAG Bearings Absolute Not RatedCMP Rs. 1,167

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 30/31

gRelative Not RatedTarget N.A.Financial Summary

Abridged Financial Statements Key metrics

Rs. mn CY09 CY10 CY11E CY12E CY09 CY10 CY11E CY12E

Profit & Loss Growth ratios

Revenues 8,187 10,486 12,283 14,738 Revenues 7.7% 28.1% 17.1% 20.0%

Manufacturing & Other Expenses 7,146 8,800 10,063 12,027 EBITDA -25.6% 52.0% 28.5% 20.6%

EBITDA 1,242 1,887 2,425 2,924 PAT -31.5% 85.4% 34.8% 19.7%

Depreciation 201 201 206 213 Margins

EBIT 1,041 1,686 2,220 2,711 EBITDA 15.16% 17.99% 19.75% 19.8%

Net Interest Exp / (inc) 7 9 12 13 EBIT 12.71% 16.08% 18.07% 18.39%

Profit Before Tax 996 1,819 2,434 2,936 PAT 8.0% 11.6% 13.3% 13.3%

Tax 340 604 796 975 Leverage & WC ratios

Adj. Net Profit 655 1,215 1,638 1,961 Debt to equity (x) 0 0 0 0

Balance Shee t (Rs. mn) Current ratio (x) 3.2 3.1 3.5 3.8

Shareholders Equity 4,617 5,735 7,238 9,044 Debtor days (Sales) 49 46 46 46

Loan funds 0 0 0 0 Inventory days (COGS) 73 76 76 76

Sources of funds 4,663 5,764 7,268 9,073 Creditor Days (COGS) 88 106 106 106

Net block 1,416 1,410 1,429 1,496 Performance & turnover ratios

Investments 3 3 3 3 RoACE 15.6% 21.6% 22.8% 22.2%

Capital WIP 68 86 86 86 RoAE 15.1% 23.5% 25.2% 24.1%

Current assets, loans & advances 4,609 6,276 8,030 10,196 Total asset turnover (x) 1.0 1.1 1.1 1.1

Current liabilities & provisions 1,435 2,012 2,281 2,708 Fixed asset turnover (x) 2.0 2.5 2.9 3.2

29

Net Current Assets 3,175 4,265 5,749 7,488 Valuation metrics

Application of funds 4,663 5,764 7,268 9,073 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 17 17 17 17

Cash flows from operations 1,634 1,320 1,684 1,980 Market capitalisation (Rs. mn) 19,396 19,396 19,396 19,396

Capex (78) (197) (225) (275) Enterprise value (Rs. mn) 18,760 17,665 16,515 15,153

Free Cash Flow 1,556 1,123 1,459 1,705 EV/EBIDTA (x) 15.1 9.4 6.8 5.2

Cash flows from investments (444) (74) (225) (275) Adj. Per-share earnings (Rs.) 39.4 73.1 98.5 118.0

Cash flows from financing (94) (96) (97) (134) Price-earnings multiple (x) 29.6 16.0 11.8 9.9

Cash generated during the year 1,096 1,150 1,362 1,571 Dividend yield (%) 0.4% 0.4% 0.6% 0.7%

1,167

8/10/2019 Spark - Bearings Sector Report

http://slidepdf.com/reader/full/spark-bearings-sector-report 31/31