Embed Size (px)

Citation preview

FEATURING Amundi Alternative Investments // Deutsche Bank Fund Services // HedgeMark // Innocap // Lyxor Asset Management // Man FRM // Morgan Stanley // Permal Group

CUSTOMISATION Providing tailored solutions

GROWTHSecuring the future of the platform

COMPLIANCE Meeting regulatory standards

MANAGED ACCOUNTS PLATFORMS 2 0 1 5

WEEKHFMS P E C I A L R E P O R T

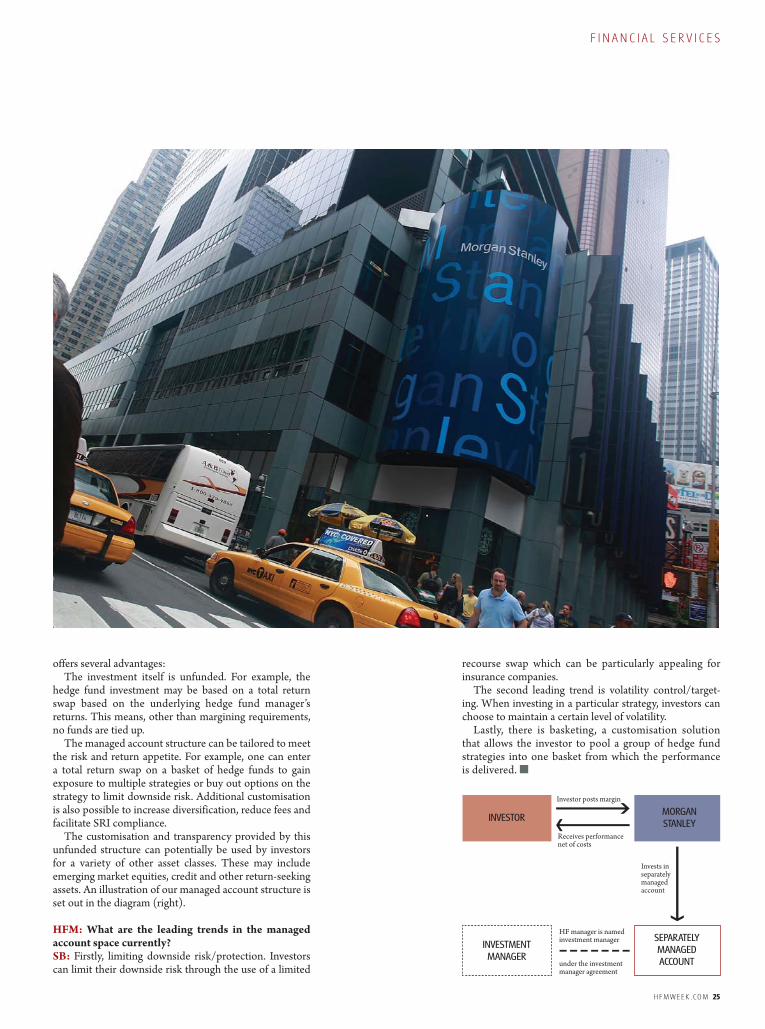

FundLogic Alternatives PlatformLiquidity. Access. Oversight.The UCITS-compliant FundLogic Alternatives Platform offers investors the potential for alpha, via access to third party alternative managers selected by Morgan Stanley.

provides several advantages. Liquidity is enhanced. Investment strategies are diverse. Risk management is robust. Plus, clients gain the professional oversight and rigorous due diligence that comes from working with Morgan Stanley.

The FundLogic Alternatives Platform is another

www.fundlogic.com

FundLogic Alternatives Platform refers to FundLogic Alternatives plc, an open-ended investment company with variable capital and segregated liability between sub-funds established as an umbrella fund authorised by the Central Bank of Ireland. This document is issued and approved by Morgan Stanley & Co. International plc (25 Cabot Square, Canary Wharf, London E14 4QA), authorised in the United Kingdom by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This document is intended exclusively for use by and is directed to Eligible Counterparties and Professional Clients. This document has been prepared solely for informational purposes and is not an offer to buy or sell any financial instrument or participate in any trading strategy. This material was not prepared by the Morgan Stanley research department. Morgan Stanley is not acting as your advisor (municipal, financial, or otherwise) and is not acting in a fiduciary capacity.

© 2015 Morgan Stanley. All rights reserved.

H F M W E E K . CO M 3

Published by Pageant Media Ltd LONDONThird Floor, Thavies Inn House, 3-4 Holborn Circus, London, EC1N 2HAT +44 (0) 20 7832 6500 NEW YORK 200 Park Avenue South Suite 1603, NY 10003T +1 646 891 2110

his year’s update on managed account platforms provides unique and crucial perspectives from some of the industry’s key players. The report considers just how relevant the managed account platform has become, the potential for its growth in the years ahead and what is required of the industry to secure this growth.

Perhaps now more than ever, responding to the needs of clients and to trends in investor behaviour is crucial. We offer discussion of the importance of providing a tailored offering to clients in an ever more demanding environment.

The language of managed account platforms is rich and varied, and it is clear that how industry members communicate is vital for the success of the platform. From managers to clients, if we begin to talk at cross purposes we limit the platform’s potential for growth. Some of the discussion in this report looks to overcome the obstacle of poor communication, and attempts to clear up some inconsistencies in industry jargon.

HFMWeek Managed Account Platforms Report 2015-2016 provides an insight into the combined experience and technical know-how of some of the industry’s most knowledgeable members. HFMWeek is hopeful that this year’s edition will assist in building yet another successful year for the managed account platform.

Mike SheenReport editor

T

REPORT EDITOR Mike Sheen T: +44 (0) 20 7832 6628 [email protected] HFMWEEK HEAD OF CONTENT Paul McMillan T: +1 646 891 2118 [email protected] HEAD OF PRODUCTION Claudia Honerjager SUB-EDITORS Luke Tuchscherer, Mary Cooch, Alice Burton CEO Charlie Kerr GROUP COMMERCIAL MANAGER Lucy Churchill T: +44 (0) 20 7832 6615 [email protected] SENIOR PUBLISHING ACCOUNT MANAGER Tara Nolan +44 (0) 20 7832 6612, [email protected] PUBLISHING ACCOUNT MANAGERS Amy Reed T: +44 (0) 20 7832 6618 [email protected]; ; Alex Roper T: +44 (0) 20 7832 6594 [email protected] CONTENT SALES Tel: +44 (0) 20 7832 6511 [email protected] CIRCULATION MANAGER Fay Muddle T: +44 (0) 20 7832 6524 [email protected]

HFMWeek is published weekly by Pageant Media Ltd ISSN 1748-5894 Printed by The Manson Group © 2015 all rights reserved. No part of this publication may be reproduced or used without the prior permission from the publisher

I N T R O D U C T I O NM A N A G E D A C C O U N T S 2 0 1 5

4 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5 C O N T E N T S

will drive the managed accounts assets’ growth in the short to midterms.

DEFINING PLATFORMS Andrew Lapkin and Josh Kestler, CEO and President & COO of HedgeMark respectively, discuss dedicated managed account solutions and clear up some marketplace misconceptions.

SYNERGIES OF IN-HOUSE LEGAL COUNSELPoseidon Retsinas, legal counsel at Innocap, discusses the firm’s customised managed accounts offering and the importance of its dedicated in-house legal counsel

THE ADVANTAGE OF MANAGED ACCOUNT PLATFORMS Stephane Berthet, executive director at Morgan Stanley, talks to HFMWeek about his take on managed account platforms

TACTICS FOR WINNING THE HEDGE FUND GAMEOmar Kodmani, CEO of the Permal Group, describes seven areas that he believes investors in hedge funds should consider in order to help them achieve highly effective results

MOVING FORWARD WITH MANAGED ACCOUNTSKristin Castellanos, director of Deutsche Bank Fund Services, discusses the development of managed accounts and their potential for future growth

AHEAD OF THE CURVEDaniele Spada, head of managed account platform at Lyxor Asset Management, discusses developments in the firm’s offering in response to industry trends

MANAGED ACCOUNT SOLUTIONS FOR INVESTORS Michael Turner, chief operating officer at Man FRM, talks about providing managed account solutions to investors

BESPOKE SOLUTIONSMichael Hart, deputy CEO at Amundi Alternative Investments, discusses how capabilities in customisation and structuration

05

19

22

08

11

14

24

17

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 5

With hedge funds becoming increas-ingly mainstream, the bar has been raised significantly for investors in these funds to add greater value in their approach. The last few years have seen increased availability and

accessibility of hedge funds in institutional and private wealth circles, the rise of direct programs from insti-tutional investors, as well as the growth of advisory or ‘assisted-direct’ propositions from consultants and other intermediaries. Many of the original professional alloca-tors to hedge funds, namely the multi-manager investment firms, have had to redefine their raison-d’être and make the transition from allocator to investor.

Drawing inspiration from the famous self-improvement book by Stephen Covey, The 7 Habits of Highly Effective People, we have listed seven key areas that investors in hedge funds should consider in order to help them achieve highly effective results. Conveniently these fall under the acronym ‘TACTICS’.

T: THEMATICThematic investing is the concept of constructing port-folios around particular investment themes rather than the more traditional approach of utilising managers as building blocks. With this approach, the investor takes a more concentrated bet on specific market moves, with the potential for greater upside, as well as the chance of greater

downside. In a multi-manager portfolio, such changes can make a significant change to the portfolio’s returns, but at the same time the diversification in a multi-manager portfolio can help weather the increased risk should an investment turn sour.

Themes are investment ideas that are likely to drive changes in markets in the short-to-medium term. Idea generation comes from investors themselves, since they have a top-down open-architecture vantage point, based on discussions with not only managers, but also independ-ent research firms, and other sources in their network.

Once a view has been formed, the search then starts for the optimal ways to express that view, which may well include a generic off-the-shelf investment with a man-ager or something that is more customised and tailored to the investor’s individual requirements. These custom-ised solutions are typically structured in consultation with the underlying manager, while execution is often through multiple-managers.

A: ACTIVEA buy-and-hold, or index approach, to hedge funds can potentially leave a lot of money on the table given the flux in global markets, as well as changes inside hedge funds themselves. An investor should be active in adjusting man-agers, as well as strategy weightings.

At the strategy level, investment themes and market cycles have an impact on which strategies work. For exam-

M A N A G E D A C C O U N T S 2 0 1 5

OMAR KODMANI, CEO OF THE PERMAL GROUP, DESCRIBES SEVEN AREAS THAT HE BELIEVES INVESTORS IN HEDGE FUNDS SHOULD CONSIDER IN ORDER TO HELP THEM ACHIEVE HIGHLY EFFECTIVE RESULTS

Omar Kodmaniis chief executive of Permal Group. Before joining Permal in 2000, Mr. Kodmani spent seven years with Scudder Investments in London and New York where he developed the firm’s international mutual fund business.

TACTICS FOR WINNING THE HEDGE FUND GAME

6 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

ple, if you look at the four broad hedge fund strategies as defined by Hedge Fund Research (equity long/short, macro, relative value, event driven) the range or difference between the best performing strategy and the worst per-forming strategy is, on average, about 14% a year.

This figure hides the true picture, for it is just focusing on broad strategies. Once such descriptions were the case, but today hedge fund strategies have become far more focused and specialised. Long/short funds are no longer the generalists of old, but vary based on sub-sectors, such as technology or healthcare; they also vary between long-biased, variable bias or market neutral; and they vary by region. Event driven has similar specialities, with some funds activist, others distressed, and others merger arbi-trage. Macro funds can be discretionary, systematic or commodity focused. So rather than looking at the broad level, when you focus on the sub-strategy level, the range of returns becomes significantly wider, with an average difference of 53.3%.

So being active at the strategy level, whether making short-term tactical or more long-term strategic changes, really does matter.

Actively changing managers is also helpful in achieving better returns. The typical hedge funds goes through a cycle from emerging/ start up, to a growth phase (if per-formance is good) to maturity, and finally - for many - the period of decline. In fact, the average life of a hedge fund is between three and five years. Looking for such signs as a fund moves through these stages is critical.

Various quantitative tools allow us to deconstruct returns of a hedge fund portfolio to show the alpha that comes from manager selection, strategic (long-term) asset allocation shifts, and tactical (shorter-term) asset alloca-tion. Historically, hedge fund investment portfolios relied heavily on manager selection, while strategic shifts were slightly additive, and tactical allocations detracted from performance. Today the more successful portfolios derive their value added from multiple sources, including tactical investment.

C: CUSTOMISEDHedge fund managers are generally running lower risk portfolios as they seek to cater to institutional clients. The consequences have become diluted returns, overly diversified portfolios and a greater overlap with peers. To be more effective, investors in hedge funds should start thinking about customising investments to correct for this. Consequently, customisation often means directing managers to a more focused mandate, either specific sub-sector where they have an edge, or a higher conviction portfolio with fewer names. It can also mean structuring mandates with higher target volatility, or perhaps sizing one particular investment in a co-investment structure. The value-added from customisation can be measured by calculating the alpha of the customised mandate relative to the manager’s flagship strategy. This annualised alpha can potentially average 2-3%.

T: TRANSPARENTPosition-level transparency in portfolios was generally not available a few years ago. Today, by having the ability to look through a portfolio on a daily basis, and having the

tools that enable you do so efficiently, allows for a far more robust risk management. At the manager level, this enables granular monitoring for style drift and particular exposures. At the portfolio level, you can take an inte-grated portfolio level view of risk exposures and liquidity. It also gives an investor a far greater degree of confidence of where they should be rebalancing a portfolio, as well as understanding areas where they can implement thematic investments or customised mandates without unduly skewing the mandate. Additionally, through more concen-trated mandates, you can better manage potential overlaps in manager positioning. Transparency, when it is achieved through managed accounts, also provides the opportunity to intervene in a crisis situation.

I: INCUBATEThere is a longstanding debate on whether emerging managers offer superior risk-adjusted returns over estab-lished hedge funds. Both have merits, but a new fund is clearly out to make their name, and is therefore prone to take more risk, as well as having an untested infrastruc-ture, while an established manager is already proven, but because of their size may well have reduced their risk. It does not have to be an either-or decision. With appropri-ate operational due diligence, proper oversight and robust managed account infrastructures, one can ‘incubate’ or invest with emerging talent in a secure operational envi-ronment. This opens the door to newer potentially higher performing investment talent while mitigating their opera-tional risk, a reason often cited as a major cause of failure amongst small hedge funds.

C: CONCENTRATEConcentrate in this instance is about building portfolios with fewer managers. With greater control of underly-ing investments through thematic portfolio construction and customisation of mandates, as well as full transpar-ency - all traits of managed accounts - investors can afford to take more concentration risk with particular manag-ers. Idiosyncratic risks (i.e. manager specific/operational issues) are mitigated via the operational safeguards of managed accounts. Systematic risks (market-related) can also be managed more closely and effectively from the top-down.

S: SAVE Negotiating lower fees where possible is clearly a source of value added, not just at the manager level, but for all service provider costs. One of the many advantages of managed accounts is that each account’s fees are individu-ally negotiated with the underlying managers. Investors can use their scale and infrastructure economies to help deliver enhanced returns through cost savings.

Each of the seven TACTICS provides the potential for higher returns from hedge fund investing. While some investors may have success in implementing one or two TACTICS, the greatest impact comes from being able to engage in all seven. This requires substantial investment and operational experience, resources, as well as global presence and infrastructure (especially related to risk man-agement systems). A sophisticated managed account plat-form is also a key attribute to effective implementation.

F I N A N C I A L S E R V I C E S

This material is for information purposes only and it is not intended to be a solicitation or invitation to invest. This is proprietary information of Man Investments Limited and its

affi liates and may not be reproduced or otherwise disseminated in whole or in part without prior consent from Man Investments Limited. Alternative investments can involve

signifi cant risks and the value of an investment may go down as well as up. Past performance is not indicative of future results. For information on Man, its products and

services, please refer to man.com and/or contact a qualifi ed fi nancial adviser.

This material is communicated by Man Investments Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

In the United States this material is presented by Man Investments Inc. (‘Man Investments’). Man Investments is registered as a broker-dealer with the US Securities and

Exchange Commission (‘SEC’) and is a member of the Financial Industry Regulatory Authority (‘FINRA’). Man Investments is also a member of Securities Investor Protection

Corporation (‘SIPC’). Man Investments is a member of the Man Investments division of Man Group plc. (‘Man Group’). The registrations and memberships in no way imply that

the SEC, FINRA or SIPC have endorsed Man Investments. In the US, Man Investments can be contacted at 452 Fifth Avenue, 27th fl oor, New York, NY 10018, Telephone: (212)

649-6600. Australia: To the extent this material is distributed in Australia it is communicated by Man Investments Australia Limited ABN 47 002 747 480 AFSL 240581, which is

regulated by the Australian Securities & Investments Commission (ASIC). This is general advice only. This information has been prepared without taking into account anyone’s

objectives, fi nancial situation or needs. Germany: To the extent this material is distributed in Germany it is communicated by Man (Europe) AG, which is authorised and

regulated by the Liechtenstein Financial Market Authority (FMA). Hong Kong: To the extent this material is distributed in Hong Kong it is communicated by Man Investments

(Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong. This material can only be communicated to intermediaries, and

professional clients who are within one of the professional investors exemptions contained in the Securities and Futures Ordinance and must not be relied upon by any other

person(s). Singapore: To the extent this material is distributed in Singapore it is for information purposes only and does not constitute any investment advice or research of any

kind. This material can only be communicated to Institutional investors (as defi ned in Section 4A of the Securities and Futures Act, Chapter 289) and distributors/ ntermediaries

and should not be relied upon by any other person(s). Switzerland: To the extent the material is distributed in Switzerland it is communicated by Man Investments AG, which is

regulated by the Swiss Financial Market Supervisory Authority. CH/14/1133-P

ENTREPRENEURIALASSET MANAGEMENT

INSTITUTIONAL FRAMEWORK.

Man is one of the largest independent alternative investment managers in liquid, alpha investment strategies. With our clients’ needs at our

core, we offer a comprehensive suite of absolute return and long-only funds through our performance-driven investment engines. We believe

that the key to alpha generation from capital markets is to provide an institutional framework for our entrepreneurial asset managers to operate

in, allowing them to focus solely on alpha generation and research.

www.man.com

8 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

HFMWeek (HFM): You could say that managed accounts really put Deutsche Bank Fund Services on the global stage in terms of large, institutional man-dates. How has this impacted your business? What changes have you seen since you started servicing managed accounts?Kristin Castellanos (KC): Absolutely; shortly after we formed DB Fund Services we became the administra-tor of one of the largest managed account platforms in the world. Because we needed to deliver T+1 indica-tive NAVs from the beginning, we had to invest heavily in a robust technology platform and develop a ‘follow the sun’ operating model so that the risk managers in Europe had reconciled position reports by London’s open. Operating a daily environment taught us to be extremely disciplined and has had a big impact in terms of our development roadmap.

In terms of changes, we have seen managed accounts morph from a single, well under-stood model into a number of different structures. I think that managed accounts used to be defined as a very specific account vehicle which has evolved; the term ‘managed account’ now seems to be almost as amorphous as ‘hedge fund’.

HFM: What kinds of changes have you seen to managed accounts and managed account platforms?KC: Well, to go back in time a bit, in the 2000s a managed account was generally a separate trading account at a prime broker man-aged pari-passu to a hedge fund manager’s core strategy. This was a time when many hedge fund managers used a single prime bro-ker. Generally, they were owned by a single institutional investor that did not want to invest in a manager’s commingled vehicle for a variety of reasons such as transparency, control or better liquidity terms. For the manager, it would only make sense if the size of the account and corresponding fees were large enough to compensate for the additional operational burden of managing a side by side portfolio.

If you take a look at managed accounts now, they can mean different things to different people, usually based on the driver of why an investor does not want to invest in a manager’s commingled portfolio.

A managed account can be a customised portfolio solution managed by a fund of hedge funds (FoHF) manager; a FoHF manager may offer access to individ-ual hedge funds through feeder vehicles thereby allow-ing investors to help guide the investment allocation of their portfolio. This gives the investor three distinct advantages: oversight by a professional investor, access to hedge funds through a feeder which requires a much lower minimum investment and asset allocation control to prevent being over or underweight on specific strate-gies based on their overall investment platform.

A managed account can also be a separate trading account at one or more prime brokers that is ‘managed’ by a third party platform. These platforms generally serve as

the manager of a fund in the sense that they arrange for the structur-ing, incorporation and administra-tion of the managed account as a commingled investment fund. But also delegate portfolio manage-ment to a ‘trading advisor’ (i.e., the hedge fund manager to which the investor seeks access). These platforms provide investors with access to world-class hedge fund managers with many of the same benefits as the FoHF customised portfolio solutions but can also include better liquidity terms and even more control. Many of these managed accounts give the platform the ability to shut a fund down immediately (permit closing orders only) in the event that they wish to terminate the account.

HFM: There has been a great deal of discussion that the alter-

native investment industry may double in size over the next 10 years; do you think the growth of man-aged accounts will keep pace?KC: I do. There are a number of trends we are observing in the alternative investment industry that I think will support the growth of managed accounts. Two of which are an influx of investments from accredited investors

THERE ARE A NUMBER OF TRENDS WE ARE OBSERVING IN THE

ALTERNATIVE INVESTMENT INDUSTRY THAT I THINK

WILL SUPPORT THE GROWTH OF MANAGED

ACCOUNTS

”

KRISTIN CASTELLANOS, DIRECTOR OF DEUTSCHE BANK FUND SERVICES, DISCUSSES THE DEVELOPMENTOF MANAGED ACCOUNTS AND THEIR POTENTIAL FOR FUTURE GROWTH

Kristin Castellanos is the global head of Deutsche Bank Regulatory Fund Services and is responsible for the design and delivery of products that help alternative investment managers address their regulatory reporting requirements. She is an alternative investments industry specialist with over 18 years’ experience in hedge funds, private equity and funds of funds, the last 7 of which have been spent at Deutsche Bank .

MOVING FORWARD WITH MANAGED ACCOUNTS

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 9

and increased sophistication of multi manager/FoHF investors.

As hedge funds have become more accessible to retail investors through liquid alternative funds, there has been also been increased interest from individual investors who, while they are accredited and can purchased 3(c)1 shares, may not be able to directly invest in a diversi-fied portfolio of hedge funds because of the minimum investment amounts. Managed account platforms are beginning to recognise this growing market and offer managed account solutions through private banks and investment advisers which provide access to this large universe of investors.

Also, as foundations, endowments and other natural buyers of FoHFs become more sophisticated on the investment characteristics of asset classes and types of hedge funds, they seek to have greater input in their manager selection and allocation. By working with a seasoned FoHF manager, they can help devise a custom-ised managed account of hedge funds that follows their investment parameters more closely in terms of diversi-fication and liquidity.

HFM: By their definition, managed accounts are gen-erally specific to an investor; from a servicing side, does that mean that you have to customise the admin-istration for every managed account? Does this get operationally difficult?KC: Managed accounts are either specific to an investor or, in cases of some managed account platforms, specific to a hedge fund manager. Although some will present challenges in terms of bespoke requirements, if you have

a scalable technology platform and a high degree of auto-mation and straight through processing of data, the cus-tomisation should be a onetime configuration exercise rather than a departure from a standard operating model. As we built our technology platform to be extremely flex-ible, we have been able to provide customised reporting based on our standard servicing model which has made a big difference.

HFM: What advice do you have for managers that are considering managed accounts? KC: Understand the drivers of your investors and how this relates to your investment strategies. Are they look-ing for greater control over the asset allocation, and why? Will they be validating your investment decisions or do they need to ensure that your investment strategy will not under or over weight investments in the context of their overall investment program? Are they looking for greater transparency, and why? Does this pose a risk if your portfolio is concentrated in thinly traded or illiquid securities? Are they looking for greater liquidity, and why? If your positions are fairly illiquid, how will that impact your trading? Will it impact the way you manage your portfolio?

From a servicing standpoint, make sure that your service providers have the necessary infrastructure and technology platform to support whatever complexities the managed account may pose and also understand how this will impact your regulatory reporting. Managed accounts can be a great way to deliver value to your inves-tors but thinking through the operational considerations from the start is critical.

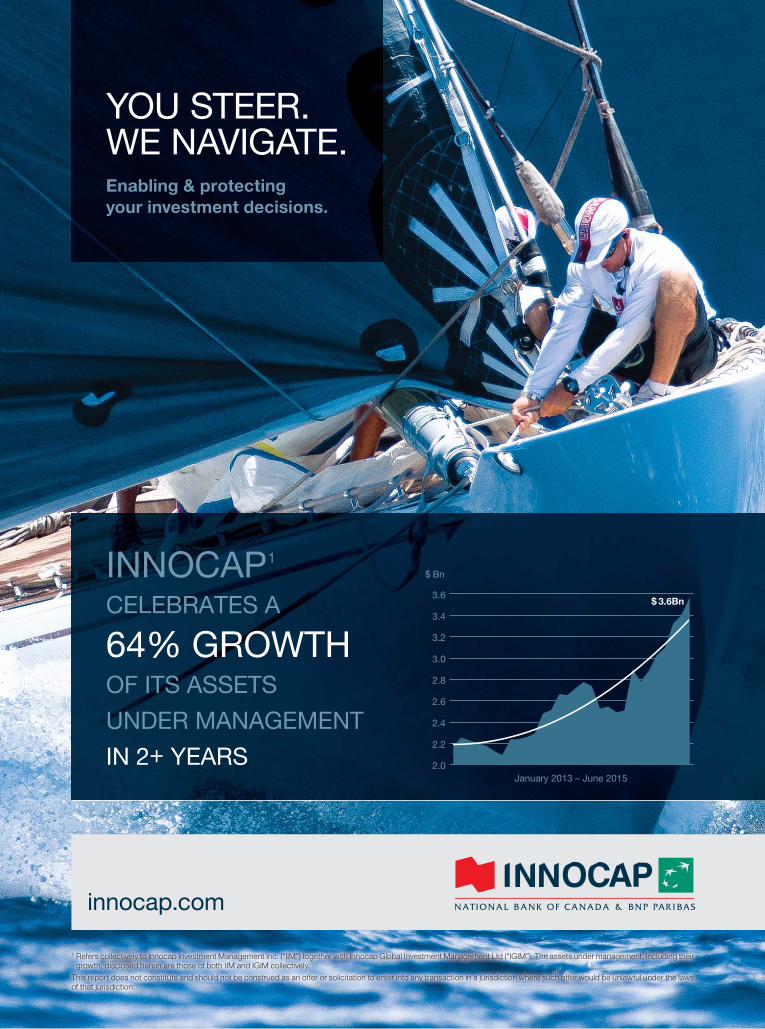

YOU STEER.WE NAVIGATE.Enabling & protecting your investment decisions.

1 Refers collectively to Innocap Investment Management Inc. (“IIM”) together with Innocap Global Investment Management Ltd (“IGIM”). The assets under management, including their growth, disclosed herein are those of both IIM and IGIM collectively.

This report does not constitute and should not be construed as an offer or solicitation to enter into any transaction in a jurisdiction where such offer would be unlawful under the laws of that jurisdiction.

innocap.com

INNOCAP1 CELEBRATES A 64% GROWTH OF ITS ASSETS

UNDER MANAGEMENT

IN 2+ YEARS 2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

$ Bn

$ 3.6Bn

January 2013 – June 2015

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 11

M A N A G E D A C C O U N T S 2 0 1 5

HFMWeek (HFM): How has Lyxor’s managed account off ering evolved in the past year? Daniele Spada (DS): First, we expanded our existing off ering of managed accounts by adding new Ucits and AIFMD managers.

Ucits funds have raised a lot of assets in the past 12 months, and we have responded to this trend by launch-ing three new Ucits funds. We aim at building a compre-hensive investment platform rather than just distributing funds. Th is means we prefer quality over quantity and are strongly focused on providing access to a small number of the highest-quality managers, running strategies that our clients are asking us about and that make sense in the current market environment.

Our strategy is to fi nd managers and strategies that you would not be able to fi nd on other platforms. In the Ucits universe, you will see a majority of multi-asset funds or long-short equity managers mainly focusing on Europe while our new Ucits launches, for instance, include a long-short credit strategy, a long-short US equities and a long-short emerging markets equities. In the fall we will be launching a US special situations manager. We want our platform to be fully representative of both the invest-ment universe and the strategies that our investors need, and all accessible in a Ucits or AIFM format.

We have also launched three AIFMD managers on the Lyxor platform. Th is regulation is currently less popular

than Ucits, but we do have a number of clients who want to invest in regulated alternative funds that are not neces-sarily constrained by Ucits regulation.

Th e second major thing we have done is to be inno-vative in the way we propose our services and range of expertise. Our platform and the expertise we can off er to our investors now go beyond alternatives.

Over the past couple of years, more and more of our clients have been asking for broader support than sim-ply providing managed accounts. So we have adapted our organisation and off ering to meet this request. We now have a manager selection team of 30 analysts, comprising 20 covering hedge funds and ten covering mutual funds, and we have put all of them together, even those not covering funds on our managed account platform. Th is means that we can now give investors the option to in-vest not only via our platform (both in a commingled or dedicated framework), but if they want to invest direct in other managers we can help them select the right one for them and follow up on their investment on their behalf. And if they need long-only rather than or in addition to alternative exposure, that is something that we now can advise with too. Our information systems are also well designed to off er comprehensive and transparent invest-ment and risk reports to investors with diversifi ed alloca-tions in mutual and hedge funds and answer to all recent regulatory requirements.

DANIELE SPADA, HEAD OF MANAGED ACCOUNT PLATFORM AT LYXOR ASSET MANAGEMENT, DISCUSSES DEVELOPMENTS IN THE FIRM’S OFFERING IN RESPONSE TO INDUSTRY TRENDS

Daniele Spada is head of managed account platform at Lyxor, where he is in charge of the development and management of the platform, including hedge fund and mutual fund selection, due diligence, and customized infrastructure services.

AHEAD OF THE CURVE

F I N A N C I A L S E R V I C E S

1 2 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

We have particularly played on the convergence be-tween alternative and traditional investments by trying to anticipate those future needs. It is all about capi-talising on the long and solid history of our managed account platform and adding new expertise that we believe investors want in the current environment and that is essential for us to diversify our offering.

HFM: What new industry trends are you having to react to and what new challenges do they represent? DS: Well, another clear trend that we are seeing is an in-creasing number of institutional investors that go down the route of “CIO outsourcing”. Such clients do this because they want a unique platform provider that is able to provide them with all of their investment needs from A to Z – helping them select the right managers (both alternative and long-only), run the investment and operational due diligence, risk modelling and man-agement tailored to all of their individual investments, provide with aggregated reporting for all of their invest-ments, and also guaranteeing that all their underlying investments are valued by the same administrator with the same pricing policy.

This is precisely what we have been working towards at Lyxor for the past 15 years, and with the recent changes we have made to our organi-sation we are even more equipped to meet these new needs. To be successful in this respect it is not only about performance, it is about selecting the right managers, managing risk, providing the right customised operational set-up and advising investors over time. We need to be able to offer an integrated, but modular, front to back set of ser-vices and expertise, so that our clients can pick and choose what they need. We have to ensure we provide the right set of management, infra-structure, selection and advisory services that can meet the demands of some very sophisticated institutional investors.

HFM: Of the three major EU regulatory de-velopments of the moment (the AIFMD, Ucits and Solvency II), which is causing you the most concern and why? DS: These regulatory developments are not necessarily “challenges” for Lyxor, because we already have the systems and processes in place to comply with them. Rather, we see them as an opportunity.

Ucits is an area of great interest to both our institutional and distribution clients, so we have been developing our offering in this field for some time. We launched our first Alternative Ucits fund back in 2013 and experienced great success last year with a merger arbitrage fund in particular, raising a large amount of capital. We are still working to bring new managers to our Ucits platform, focusing on launching a small number of high-quality managers rather than a large volume. By the end of this year we should have a comprehensive Ucits range with around ten funds that should enable our investors to build a diversified and performing allocation.

We have not made so many adaptations to our infra-structure or offering on the AIFMD side, mainly be-cause the operational set-up of our managed account platform was already compliant with the level of trans-parency required by this regulation. It is just a matter of setting up a new platform in a different jurisdiction, which obviously takes some time.

Solvency II is all about providing transparency in terms of risk – both at the aggregate level and on all underlying investments. Again, we have been doing this since before the regulation came in. What we have done is developing specific reporting for some investors on our platform (mainly insurers) to help them monitor and reduce significantly their Solvency Capital Ratio consumption associated to their alternative invest-ments. This has proved quite effective. What is crucial here is the technology needed to process all the data at the fund level and produce transparent, detailed or aggregated reporting, but again that is nothing new for Lyxor. We have been doing it for a long time.

Our aim is always to maintain standards that surpass what current regulation requires, and this means that

these regulations have not led to any hurdles for us to get over. But of course we are always on the lookout for new ways to improve our pro-cesses ahead of new requirements.

HFM: What new innovations are in Lyxor’s pipeline for the coming year? DS: Our challenge for the next 12 months is, as ever, to identify early on the alternative invest-ment strategies that have the scope to perform well against the current backdrop, to select the best managers of those strategies, and to pack-age their products to make them available to our clients on our managed account platform. The Ucits phenomenon in particular shows no signs of slowing, and will require a lot of research and energy on our side. We will also capitalise on the new expertise in selecting mu-tual funds in order to spot managers and strate-gies that could perform very well in the current market environment.

One development of particular interest is that we are about to launch a multi-manager managed account. This is basically a managed account with different buckets, each of which is managed by a different hedge fund manager. The allocation between each pocket is either decided by our clients, or by Lyxor on behalf of each client based on their individual guidelines.

This is essentially a new and evolved version of the old fund of hedge funds. It is a way to be more reactive, providing diversification of strategies, but in a more cost-efficient way because there is only one layer of fees as it is run as a single fund.

There is been a great deal of interest in this kind of so-lution from our clients. It is very attractive to distribu-tors in particular, because if you package it with a Ucits wrapper, it provides a similar level of concentration as a fund of hedge funds but in a format now available to any investor.

WE NEED TO ENSURE WE PROVIDE THE RIGHT SET OF MANAGEMENT,

INFRASTRUCTURE, SELECTION AND ADVISORY

SERVICES TO ENSURE WE CAN MEET THE DEMANDS OF SOME VERY SOPHISTICATED

INSTITUTIONAL INVESTORS

”

Amundi AI is AIFM licensed. (1) No.1 European asset manager based on global assets under management (AUM) and the main headquarters being based in Europe - Source

IPE “ Top 400 asset managers” published in June 2015 and based on AUM as at December 2014. (2) AIFMD: Alternative Investment Fund Managers Directive which came

into force on July 22, 2013. Aims to create a comprehensive regulatory framework for hedge fund managers that reconciles investors’ protection (mandatory segregation

of administration/custodian and valuation duties from fund management, new prescriptive rules aiming to prevent excessive risk taking, such as on remuneration), while

preserving the necessary fl exibility in the “performance engines” with no prescriptive constraints imposed on investment guidelines, type of instruments used, level of

leverage. Also, the AIF passport will allow to market alternative products within the EU for professionals investors, outside of the private placement regime. There is no capital

or performance guarantee. This publication cannot be reproduced or passed onto third parties, in whole or in part, without our permission. Published by Amundi Alternative

Investments, SAS - Simplifi ed Joint Stock Company with capital of €4,000,000 - Registered offi ce: 90, boulevard Pasteur, 75730 Paris Cedex 15 - Portfolio Management

Company registered with the ‘AMF’ (French Financial Markets Authority) under no. GP 01.044. Paris Register of Companies no. 439 614 553. This publication is intended for

professional investors only. The information contained in this publication is not intended to be distributed or used by any person or entity in a country or court where such

distribution or use would be contrary to legal or regulatory provisions or which would compel Amundi Alternative Investments, SAS or its affi liated companies, to comply with

the registration obligations of the said countries. The data and information contained in this publication are supplied for information purposes only. Nothing in this publication

constitutes an offer or request by any member of the Amundi Alternative Investments group, to provide advice or an investment service or to buy or sell fi nancial instruments.

The information contained in this publication is based on sources which we consider to be reliable, but we cannot guarantee that it is accurate, comprehensive, valid or relevant.

July 2015. Photo credit: Corbis. |

Amundi, the No.1 European asset manager(1)

Earningyour confi dence by being a trusted partner whatever your needs.

Alternative InvestmentsPioneering in alternative products since 1992,

Amundi reveals the power of its EU-regulated

Multi-management expertise & Managed

Account Platform.(2)

Through a bespoke consultative-approach

rather than a one size fi ts all product offering,

Amundi partners with its clients to provide

suitable alternative investment solutions.

alternatives.amundi.com

1 4 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

M anaged accounts or “MACs” aim to provide bespoke, cost-eff ective solu-tions for a number of diffi cult challeng-es faced by global hedge fund investors. For a start, MACs are designed to in-crease the effi ciency and transparency

of hedge fund investments. What is more, a MAC seeks to help an investor exercise eff ective control over their hedge fund assets as well as to understand the liquidity profi le of their investments.

Man FRM (FRM) began building MACs for its own hedge fund investments in the mid-1990s. Since then we have devel-oped a broad range of skills, which we believe may be of benefit to many different types of investors rang-ing from pension funds to insurers and other financial services provid-ers and consultants. We believe the sophistication of our in-house infra-structure and our hedge fund invest-ing skill distinguishes us from other MAC providers. We believe we are equally adept at helping investors to model and risk monitor manag-ers at either end of the complexity spectrum – ranging from complex credit and relative value strategies to managed futures and equity long long-short funds.

In this article, we want to high-light two specific ways we can pro-vide MAC solutions to investors. The first is for investors that need a broad, full-service solution. The second is for investors that want an infrastructure provider to build and run MAC solutions for them.

FULL SERVICE MAC SOLUTIONS In every mandate investors want to take advantage of FRM infrastructure, and what we believe to be industry-wide credibility, in hedge fund investing. This can result in potential cost savings on fees and provide investors with tools, which are designed to increase the performance and

value of their hedge fund investments. We can, for exam-ple, help tailor the hedge fund selection to compliment an entire investment portfolio, and over time dynamically adjust the allocation as market conditions and the client portfolio evolve.

FRM has built and run full service MACs for very dif-ferent types of clients. We have provided solutions globally for European insurers as well as Japanese and US investors and UK pension funds. We have designed specific report-ing programmes (covering, for example, SRI and Solvency II) and are well versed in working with clients to articulate

their particular data requirements (covering, for example, positions, performance and risk) and then developing customised MAC solu-tions. As part of our hedge fund investment offer, MAC clients are provided with FRM’s online risk analysis tool, Clarus. Although a highly analytical system, Clarus was designed to have an extreme-ly intuitive user interface. With Clarus, users can translate daily position level data into informa-tion clients can use to monitor and risk manage their MAC exposures within their overall portfolio.

The FRM Full Service Solution MAC platform is investment led, so we only open MACs with man-agers in whom we have confidence to invest capital. We built our MAC platform to better under-stand the managers we allocate to as hedge fund investors. Our aim

today remains the same: to construct better portfolios, exercise control of the assets and create better transpar-ency and risk analytics around hedge fund investments.

FRM continues to develop new ways to supply the MAC platform to investors. A recent example of this is the scalable and cost-effective MAC solution we built for a local government pension scheme (“LGPS”) in the UK. In this case, we developed a solution to build a diversified hedge fund portfolio customised for the particular invest-

SINCE THE FINANCIAL CRISIS, WE HAVE SEEN A

NUMBER OF SUBSTANTIAL INSTITUTIONAL INVESTORS PIVOT FROM CO-MINGLED

INVESTMENTS TO ALLOCATING TO HEDGE

FUNDS DIRECTLY

”

Michael Turneris chief operating officerof Man FRM and a member of FRM’s Management Committee. He is also responsible for investment infrastructure within FRM and oversees the teams responsible for quantitative analysis, managed account transparency and operations, and client services

MANAGED ACCOUNTSOLUTIONS FOR

INVESTORSMICHAEL TURNER, CHIEF OPERATING OFFICER AT MAN FRM, TALKS ABOUT

PROVIDING MANAGED ACCOUNT SOLUTIONS FOR INVESTORS

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 15

ment mandate and requirements of the LGPS member. At the same time, however, the program we developed allows all of the LGPS’ underlying funds using the FRM MAC platform to benefit from a sliding management fee scale based upon their collective assets. Consequently, all of the LGPS funds are treated as a single investor with regard to the pricing of the MAC programme, while each scheme is treated individually and given a customised solution.

By using an FRM MAC, each LGPS fund can exercise full ownership over its hedge fund invest-ments and have greater transparency over the underlying holdings. In addition, each LGPS fund can also benefit from the sliding management fee structure, which we believe provides a real collabo-ration opportunity for all of the LGPS funds that invest in hedge funds.

INFRASTRUCTURE MACSince the financial crisis, we have seen a number of substantial institutional investors pivot from co-mingled investments to allocating to hedge funds directly. To max-imise transparency and control these investors are increas-ingly looking to use MACs to allocate to their hedge funds. But this presents a challenge as setting up a MAC platform takes specialist skills, is complicated to do and is expensive to build. FRM’s substantial infrastructure capability with MACs is complimented by Man Group’s global infrastruc-ture, trading platforms, legal expertise and outreach.

For new sophisticated investors looking to build man-aged account platforms, FRM offers a suite of customised and innovative solutions across the MAC interface. Areas of particular expertise include:

• Legal structuring• Negotiation of trading agreements• Risk monitoring, reporting and analytics via Clarus• Portfolio optimisation • Systems development and operational integration• Project management to launch the MAC and full

lifecycle support of it.

Yet beyond this agile skill set, it is important to remember that FRM is not a service provider. Rather we bring the perspective of a hedge fund investor to MACs and our

clients receive the full firm-wide benefits of Man Group’s expertise and global scale. As investors ourselves, we very clearly understand the challenges that investors face. It also means that as investors we can share insight and per-

spective, and collaborate with clients as investors.From first contact, FRM facilitates detailed and

collaborative discussion to understand each inves-tor’s specific MAC needs. Jurisdictional require-ments are assessed as are operational, structural and other factors.

The aim of all this is to set the client up to focus on the investment decision making. FRM puts in place the technology and processes to facili-tate the operational heavy lifting in setting up the MAC solution. Our collaborative approach and commitment to facilitating client requirements is designed to provide a major boost in end-investor capabilities and control.

We believe the benefits of these synergies to investors are often considerable. Indeed, we

believe that an investor that opts to set up an infrastructure MAC could see a positive impact on performance largely due to anticipated savings from negotiating lower man-agement and performance fees. Furthermore, we believe that annual operational fee reductions obtained through a MAC can produce additional savings for an investor.

THE OUTLOOK FOR MACs Many investors may be attracted to the long-term benefit of building partnerships around terms, strategy develop-ment, implementation and ideas sharing. Others may be looking for a pure, cost-effective infrastructure solution. We think the hedge fund market place shows that MACs are playing an increasing role at either end of the complex-ity spectrum.

We believe MACs may offer a compelling solution for virtually any type of investor. They can provide customised Solvency II reporting for insurers and through enhanced analytics capabilities aid pension funds to improve asset allocations by selecting more granular return-drivers.

At FRM, we work with clients to design and create MAC solutions. We aim to empower investors with the tools and operating expertise they need to achieve better risk adjusted returns from their hedge fund investments.

WE BELIEVE MACs MAY OFFER A COMPELLING

SOLUTION FOR VIRTUALLY ANY TYPE OF INVESTOR

”

Deutsche Bank Global Transaction Banking

This advertisement is for information purposes only and is designed to serve as a general overview regarding the services of Deutsche Bank AG and any of its branches and affiliates. The general description in this advertisement relates to services offered by Deutsche Bank AG Global Transaction Banking and any of its branches and affiliates to customers as of July 2015, which may be subject to change in the future. This advertisement and the general description of the services are in their nature only illustrative, do neither explicitly nor implicitly make an offer and therefore do not contain or cannot result in any contractual or non-contractual obligation or liability of Deutsche Bank AG or any of its branches or affiliates. Deutsche Bank AG is authorised under German Banking Law (competent authority: German Banking Supervision Authority (BaFin)) and, in the United Kingdom, by the Prudential Regulation Authority. It is subject to supervision by the European Central Bank and by BaFin, Germany’s Federal Financial Supervisory Authority, and is subject to limited regulation in the United Kingdom by the Prudential Regulation Authority and Financial Conduct Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available on request. Copyright © July Deutsche Bank AG. All rights reserved.

Award winning fund services from a trusted partnerWe provide end-to-end fund administration; regulatory,

that support an array of assets, strategies and vehicles.

Your complex fund services needs met – with global connectivity, bank-wide collaboration and long-term commitment.

Visit db.com/gtb, email [email protected] or follow us on Twitter @talkgtb for more.

Hedge Fund Administrator of the Year Global Investor/ISF Investment Excellence Awards, 2015

Winner of seven fund administration awards The Asset Triple A Asset Servicing, Investor and Fund Management Awards, 2015

Most Innovative Fund Administrator – over USD 30 billion HFM Week European Service Awards, 2015

Administrator Hedgeweek Global Service Awards, 2015

Best Fund Administrator – Mutual Funds, three consecutive years MENA Fund Managers Fund Services Awards, 2015

Fund Administrator of the Year –

Global Investor/ISF Middle East Awards, 2014

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 17

M A N A G E D A C C O U N T S 2 0 1 5

HFMWeek (HFM): Is there a possibility of the ris-ing trend of Ucits funds being the demise of the managed account platform? Michael Hart (MH): It is true that regulatory changes in the last four to five years have forced some hedge funds to go down the route of Ucits. The result of this growing regulated offering in the industry is that the key advantages of managed account platforms may be seen as less appealing.

But it seems unlikely that this marks the demise of the managed account platform. They are two complete-ly different animals. Obviously the biggest advantage you have with a managed account platform rather than going with Ucits is you have the additional safety net.

Managed account platform providers and special-ists such as Amundi Alternative Investments must of-fer ‘something else’ to clients. We have to go beyond

the traditional advantages of liquidity, transparency and control. Obviously this must begin with being ex-tremely competitive in terms of platform fee and prov-ing out capabilities in negotiating fees with hedge fund managers.

HFM: You say the future of MAP businesses is not simply replicating and distributing products. What should be done? MH: Amundi Alternative Investment’s culture is asset management and that is the reason we believe the future of the managed account platform business is not simply replicating and distributing products. The future of the business is structuring and customizing the hedge fund portfolios we have selected to work for our platform.

In terms of investment strategy, we tend to look ahead 12 to 24 months. If you become part of this rising

MICHAEL HART, DEPUTY CEO AT AMUNDI ALTERNATIVE INVESTMENTS, DISCUSSES THE ADVANTAGESOF MANAGED ACCOUNT PLATFORMS AND HOW THEY ARE HOLDING THEIR OWN DESPITE

THE RISING TREND FOR USING UCITS FUNDS

Michael Hartis deputy chief executive officer and global head of business development at Amundi Alternative Investments. He is also a member of the Executive Committee, the New Product Committee, the Compliance Committee, and the Risk Committee. Michael has more than 20 years of experience in the alternative investment space.

BESPOKE SOLUTIONS

F I N A N C I A L S E R V I C E S

1 8 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

trend of Ucits, you are just going in to an existing strat-egy. Whereas what we are putting together for clients is a customised solution, which is something you will not get with Ucits.

Hedge funds should never be looked at in isolation. Especially with how the markets are going at the mo-ment. For example, the biggest risk to pension plans is the impact of changes in US monetary policy, Eu-ropean stability and what has been happening in the Chinese stock market.

If you look at fixed income returns, what has happened in the past is that investors have be-come accustomed to looking into equities for growth. Now they need to lock in some of these gains. This is where we can address those con-cerns with our managed accounts platform, and help them reduce the volatility of their overall pension fund.

Pension funds need to close the funding gap. But they need to do that while staying within their respective risk tolerances. At the moment they are fi nding their asset values falling while their liabili-ties are rising. So they need to look for uncorre-lated, or relatively market neutral, products. What is going to provide that in the safest possible envi-ronment is a managed accounts platform.

HFM: How you would you define your man-aged account offering? How is it different from a ‘rent-a-platform’ style product? Our managed account platform differentiates it-self from others because it was developed from the clients’ perspective and for the clients’ ben-efit. So unlike many others, we are not just a dis-tribution platform.

Our fund managers go through a very stringent due diligence. This is because we principally launch managed accounts for our existing client use. This is what clients and potential clients really like about us. We are investing alongside our existing clients, which means our interests fully align with theirs.

What this also means is that our manager turnover is

relatively low, because it takes a great deal for a manager to get on to our platform. Not only from an investment risk point of view, but from an operational business risk point of view. As a result we have never had any issues with any existing managers.

Where we differ from rent-a-platform is we are offer-ing investment solutions rather than simply plug-and-

play. This could be through direct access to the managed account platform, a simple advisory solution, or a dedicated mandate.

We can be all things to all people, because what we offer is far more flexible and modular. Whereas with a rent-a-platform you are very limited. We are not simply selling managed ac-counts, we are partnering with our institutional clients and we are positioning ourselves as an extension of their in-house teams. We accom-pany our clients not only on the operational aspects of a managed account platform, but also on investment aspects

HFM: How can non-EU hedge fund manag-ers leverage your MAP tool?MH: The realities of entering Europe have be-come increasingly onerous. The advantage for some American managers, particularly emerg-ing to mid-size managers, is that the prohibi-tive costs can be reduced by working with our managed account platform and partnering with us. They can then access large central European clients in a cost-effective and timely manner.

The European market is growing, so it is a market non-EU managers do not want to ig-nore. But the regulatory realities can be off-putting. It is our job to make it is as painless as it possibly can be.

Non-EU managers can partner with Amundi in order to leverage off our AIFMD-compliant managed account platform in Ireland, or our Luxembourg Ucits platform. This partnership for those managers is a way of access-ing products which fit marketing rules in the European market quickly, easily and cheaply.

MANAGED ACCOUNT PLATFORM PROVIDERS AND SPECIALISTS SUCH

AS AMUNDI ALTERNATIVE INVESTMENTS MUST OFFER

‘SOMETHING ELSE’ TO CLIENTS. WE HAVE TO GO BEYOND THE TRADITIONAL ADVANTAGES OF LIQUIDITY,

TRANSPARENCY AND CONTROL

”

WE CAN BE ALL THINGS TO ALL PEOPLE, BECAUSE WHAT WE OFFER IS FAR MORE FLEXIBLE

AND MODULAR

”

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 19

M A N A G E D A C C O U N T S 2 0 1 5

HFMWeek (HFM): What is a hedge fund dedicated managed account? Andrew Lapkin (AL): Dedicated managed accounts (DMAs) are typically single-investor hedge funds estab-lished for the exclusive use of, and owned and controlled by, an institutional investor, such as a public or private pension plan.

The term ‘managed account’ is the source of significant confusion in the hedge fund space. Investors often think of this term in the context of traditional investments where it means giving a manager trading authority over a broker-age or custody account. In the hedge fund context, we are almost always referring to a fund or other special-purpose vehicle when discussing a managed account. The use of leverage and short-selling by hedge fund managers can result in liabilities that exceed the amount of investment. As a result, a limited liability vehicle is typically used to house hedge fund managed account investments.

HFM: What is the difference between a commingled managed account and a DMA?Josh Kestler ( JK): A commingled managed account (CMA) is a pooled vehicle generally set up by a managed account provider who is offering a range of individual managed accounts covering multiple hedge fund strate-gies to institutional and high-net-worth investors. These vehicles or ‘funds’ are sponsored and controlled by the platform provider who is responsible for oversight of the funds.

A DMA is typically set up by a platform provider for a

single institutional investor who ultimately owns and con-trols the account. A DMA removes co-investor risk, pro-vides the investor with much more control than a CMA and allows the investor to customise the account structure, service providers and investment strategy. AL: While DMAs provide a number of advantages over a CMA, DMAs require a significant investment per fund, often $100m or more. As such, many investors will seek the benefits of managed accounts by investing in a spon-sored CMA.

HFM: Is a ‘fund of one’ the same thing as a managed account?AL: No; a ‘fund of one’ generally refers to a fund created and controlled by a hedge fund manager for a single inves-tor. In a fund of one structure, the manager rather than the investor typically controls the service provider relation-ships such as the administrator and auditor used for the fund. The manager would continue to have authority over key operational functions such as the ability to move cash and to value securities. While a fund of one can remove co-investor risk, it does not achieve all of the benefits of a managed account, including limiting the manager’s authority to trading authority only.

HFM: Is a fund of funds managed account a type of DMA? JK: No. A customised fund of funds product is often con-fused with a managed account. A custom fund of funds is a dedicated vehicle whereby a fund of funds manager invests

ANDREW LAPKIN AND JOSH KESTLER, CEO AND PRESIDENT & COO OF HEDGEMARK RESPECTIVELY, DISCUSS DEDICATED MANAGED ACCOUNT SOLUTIONS AND CLEAR UP SOME MARKETPLACE MISCONCEPTIONS

Joshua Kestleris chief operating officer, overseeing all departments associated with legal/compliance, operations and business development. Prior to joining HedgeMark in 2012, Kestler was a director of Deutsche Bank’s X-Markets Hedge Fund Platform and head of managed account platform operations in the United States.

Andrew Lapkinis chief executive officer and is responsible for overall management of the firm. Prior to joining HedgeMark in 2011, Lapkin was the co-founder, president, and chief operating officer of Measurisk , a JP Morgan company that was formerly affiliated with The Bear Stearns Companies.

DEFINING PLATFORMS

F I N A N C I A L S E R V I C E S

2 0 H F M W E E K . CO M

M A N A G E D A C C O U N T S 2 0 1 5

in several different underlying manager-sponsored hedge funds on behalf of a single investor. This structure does not typically provide any of the tradition-al benefits of managed accounts – transparency, liquidity, governance or control. A custom fund of funds is equivalent to an investor making direct investments into traditional hedge funds under an advisor’s guidance.AL: We are, however, seeing a new trend where-by fund of funds managers are using managed accounts as the building blocks for client port-folios. Fund of funds managers are beginning to understand the additional value that they can pro-vide to clients by having position-level transpar-ency, applying investment guidelines and main-taining control over the underlying assets.

The use of managed accounts by these managers changes and enhances the value proposition that fund of funds can offer clients including the crea-tion of unique products that may meet investors’ demands for liquidity, asset control and transpar-ency. It seems reasonable to expect that an advi-sor can substantially improve their investment and risk management processes with complete daily position-level information as opposed to limited exposure level information on a monthly lag.

HFM: Can you discuss the different types of hedge fund managed account platform providers and wheth-er they all offer the same services?AL: The hedge fund managed account industry has evolved significantly in the last several years and we believe that it will continue to mature. Unfortunately, there remains a great deal of confusion in the industry gen-erally regarding the different types of managed account providers and the services that they each offer. Currently, every different type of provider seems to get lumped into the same category and compared on an apples-to-apples basis when in reality the comparison is often apples to oranges. JK: There is not currently one industry standard service model. There are several types of provid-ers: the most well-known providers are historically the CMA platforms, which effectively select and distribute hedge funds in a managed account for-mat. This model was really the first phase of the hedge fund managed account industry and persists today. Many of the CMA Platforms have now also delved into the DMA space as the demand for customised, dedicated accounts has been a growth trend.

Pure play DMA providers such as HedgeMark exclusively support institutional investors in the structuring, operational oversight and risk moni-toring of custom, private managed account plat-forms. Some providers do not offer structuring services which tends to be critical for many insti-tutional investors who do not have the expertise to perform these functions internally and hiring external counsel is not a complete solution. This component of the DMA service offering tends to be critical for many institutional investors who do

not have the expertise to perform these functions inter-nally, and hiring external counsel is not a com-plete solution. There are providers that do not offer all of the operational support necessary to run anything other than the simplest hedge fund strategies, leaving these functions with either the investor or hedge fund manager which defeats the purpose of having a DMA.

We have found that certain providers hold themselves out as DMA providers, but in reality their services are limited to processing data and delivering some risk reporting. We believe that institutional investors are looking for substantially more from their providers than this. The ability for investors to differentiate among providers with barely any publicly available information regard-ing the specific services offered or an industry standard service model remains a major struggle for the managed account industry.

There are several fund of funds businesses that have developed their own internal managed account platforms. Most of these platforms are used by the fund of funds as building blocks for various products and advisory portfolios. These platforms are typically commingled from the

investor’s perspective and the underlying funds are gener-ally not offered on a stand-alone basis, but rather as a part of a broader product or portfolio. The fund of funds plat-forms are offering investment advisory products and solu-tions; whereas most of the pure managed account provid-ers are offering a utility or service to facilitate investment management by the investor or its advisor.

HFM: Is an administrator a type of managed account platform provider? AL: No. Unfortunately, we have found this to be a source of major confusion and misinformation in the marketplace.

Managed account services and fund administra-tion services are different. These services are com-plementary rather than competitive. Since a hedge fund managed account is almost always structured in a fund format, every managed account requires a fund administrator to calculate an NAV, maintain the fund’s books and records, produce financial statements etc.

A managed account provider performs various non-investment functions that would have been performed by the hedge fund manager, not the fund administrator, in a commingled, manager-sponsored fund structure. The managed account platform provider is typically responsible for co-ordinating fund set-up; co-ordinating counterpar-ty agreement negotiations and account openings; overseeing the administrator including reconcili-ation reviews, review and approval of the NAV produced by the administrator, cash movements for trade-related payments, expense payments and margin movements; co-ordinating the audit pro-cess; and risk analytics and performance report-ing. Most administrators either do not have the expertise or the willingness to perform many of these services.

A DMA REMOVES CO-INVESTOR RISK,

PROVIDES THE INVESTOR WITH MUCH MORE

CONTROL THAN A CMA AND ALLOWS THE

INVESTOR TO CUSTOMISE THE ACCOUNT STRUCTURE, SERVICE PROVIDERS AND INVESTMENT STRATEGY

”

UNFORTUNATELY, THERE REMAINS A GREAT DEAL OF CONFUSION IN THE INDUSTRY GENERALLY

REGARDING THE DIFFERENT TYPES OF MANAGED

ACCOUNT PROVIDERS AND THE SERVICES THAT THEY

EACH OFFER

”

EVERY WEEK YOU WILL RECEIVE More exclusive stories than any other hedge fund publication All the latest searches and investment news Exclusive data on launches and performance Investment strategy analysis Topical comment from leading industry figures

Exclusive research surveys Regulatory developments People on the move

As a subscriber, you will also receive full registration to www.hfmweek.com, where you can access:

Daily updated performance data Exclusive research Daily news alerts Industry events information Service directory listings and much more...

vF O R M O R E I N F O R M A T I O N P L E A S E C O N T A C TThe Membership Team at +44 (0)207 832 6511 OR email sales@hfmweek .com O R V I S I T H F M W E E K . C O M F O R D E T A I L S

THE BEST READ IN THE HEDGE FUND INDUSTRY

SUBSCRIBE TO

www.hfmweek .com

NEW MEXICO Educational

Retirement Board (NMERB)

has dropped hedge funds as an

asset class and is pulling most

of its investments in the sector

following an asset allocation

review.

The $10.1bn pension fund

previously held investments in

six FoHFs with most of those

relationships dating back to

2006/07. But HFMWeek has

learned it has decided to with-

draw its allocations.

It follows a review completed

by the investment committee

alongside consultants NEPC in

June this year, and marks a rap-

id change in attitude to hedge

funds by the pension fund.

NMERB had a 7% target

allocation to hedge funds as

recently as last year, but has

since dropped that target to 3%

and intends to get to zero with a

series of fresh redemptions.

So far, NMERB has with-

drawn from Austin Capital

Management, Gottex Fund

Management, TAG and Deut-

sche Bank’s Topiary Fund.

Its remaining FoHFs, GAM

and Benchmark Plus, have been

issued with redemption notices.

CIO Bob Jacksha told

HFMWeek the pension fund

retained some hedge fund

investments in other asset classes

– namely Bridgewater’s

Pure Alpha Fund and a

US state’s $10.1bn Educational

Retirement Board removes

hedge funds as asset class

BY ALEX CARDNO

03

COMMENT A WAKE-UP C ALL TO THE HEDGE FUND INDUSTRY 14

New Mexico

pension drops

hedge funds

WHEN THE

GOING GETS

TOUGH...

HOW CAN HEDGE FUNDS

BEST PREPARE FOR A

FUTURE CRISIS? FEATURE 21

The long and the short of it

ISSUE 349 7 August 2014

LAUNCH 10

EX-GRAHAM CAPITAL AND AHL PAIR PLAN LAUNCH

Simon Crooks and Lee Bostock line up London fi rm

NEWS 05

BNP PARIBAS SWOOPS FOR CREDIT SUISSE ADMIN UNIT

Latest administration deal expected to complete in H1 2015

NEWS 09

QUARTER OF DEPOSITARIES AWAITING FCA APPROVAL

Twelve out of 44 applications to regulator still pending

FE ATURE 16HFMWeek data on the top 20 admins,

auditors, custodians and prime brokers

for SEC-registered hedge funds

SNAPSH

OT

THE

ALPHAPIPE-

HFMWEEK

SERVICE PROVIDER

Q 2 : 14

s indd 1

05/08/2014 16

www.hfmweek .com

FEARS ARE GROWING

among hedge funds trading

OTC derivatives over the con-

tinued failure of trade reposi-

tory DTCC to reliably provide

crucial data required by new

European regulations. Under Emir rules, which

went live on 12 February but

only became effective on 22

July for non-EU funds as part of

the AIFMD, managers can del-

egate reporting of OTC deriva-

tives to their prime broker but

remain liable for its accuracy,

with Esma stating that manag-

ers must check the data passed

on by trade repositories.Most managers spoken to

by HFMWeek have appointed

DTCC to provide the data but

many managers have faced prob-

lems acquiring the data to check.

The issue intensified this

week when new daily valuation

and sporadic collateral report-

ing requirements kicked in,

significantly adding to the vol-

umes DTCC is dealing with.

A spokesperson for DTCC

admitted it had “experienced

challenges with some aspects of

reporting” but was working to

address the issues, while keep-

ing regulators informed.Allan Yip at Simmons &

Simmons said almost every

delegated reporting agreement he has seen

Many managers still facing

DTCC problems New requirements intensified issue on Monday

BY MAIYA KEIDAN

03

COMMENT GET T ING YOUR A IFMD ANNEX IV REPORT ING R IGHT 14

Fears mount over Emir reporting

responsibility

COST OF COMPLIANCENEW RULES MEAN NEW COSTS – BUT WHO

SHOULD PAY?

FEATURE 19

The long and the short of it

ISSUE 350 14 August 2014

LAUNCH 10

FINANCE AUTHOR LAUNCHES HEDGE FUND WITH HUSBAND

Yasmine Hayek and Nabil Kobeissi start LTW Capital Partners

NEWS 07

CITI RESTATES COMMITMENT TO ADMIN AS TRIO JUMP TO SS&C

US bank “deeply committed” to space following departures

NEWS 09

AQR HIRES FORMER WINTON CAPITAL GENERAL COUNSEL

Move comes as Arrowgrass compliance head joins CQS

K I L L I N G O F T H E F L A S H B O Y S ?

FEATURE 16

Regulators, politicians and legislators

have HFT in their sights – but what

will be the outcome? HFM investigates001_003_HFM350_News.indd 1

12/08/2014 16:50

www.hfmweek .com

HIGHBRIDGE IS RAMPING

up its European expansion

drive, with its London office

significantly increasing head-

count this year.

The $29bn US manager has

made several well-publicised

recent hires in Europe and

HFMWeek analysis of filings

underlines the scale of the

increase, finding that more than

two-fifths of its FCA-registered

London personnel were added

since January.

Its substantial growth push

is designed to capitalise on

what the firm perceives as huge

opportunities in the European

credit and private and public

equity sectors.

Fifteen of Highbridge’s 36

London-based employees reg-

istered with the FCA have been

added in 2014, with just three

departing its UK-regulated

entities.

A minority of the 15 are

existing Highbridge staff trans-

ferred from other divisions,

most notably its global head

of investment strategy Kevin

McNamara who has switched

to the private equity-focused

Principal Strategies unit.

But most have joined the

JP Morgan-owned firm from

elsewhere, including Philip

Moore who has joined

Principal Strategies

More than two-fifths of

US firm’s 36 FCA-approved

personnel are newly

registered this year

BY WILL WAINEWRIGHT

03

COMMENT D ISTR IBUT ING HEDGE FUNDS IN C ANADA

14

Highbridge’s

London hiring

spree continues

CHOOSING A

PLATFORM

HFMWEEK LOOKS AT

THE PROS AND PITFALLS

OF PARTNERING WITH A

PLATFORM FEATURE 19

The long and the short of it

ISSUE 351 21 August 2014

INVESTOR 08

ALLOCATORS WEIGH IN ON LGPS CIV PROPOSALS

Majority believe it is too early to judge the impact of CIVs

SEARCH 03

TEXAS ERS TO RAMP UP HEDGE FUND INVESTMENT

$21bn US pension fund plans two new allocations next year

NEWS 07

DEUTSCHE BANK’S PRIME CONSULTING CHIEF LEAVES

Chris Farkas departs as JP Morgan raids Barclays for talent

HFMWEEK

EXPLORES THE

50 STATES

FEATURE 16HFMWeek digs down into the current

exposure levels of public pension funds

in states across the Western seaboard

19/08/2014

www.hfmweek .com

THE LUXEMBOURG regula-tor is demanding non-EU man-

agers accessing investors using private placement comply with

tough remuneration rules far above what other European

jurisdictions are requiring, HFMWeek can reveal.The Commission de

Surveillance du Secteur Financier (CSSF) has added a

declaration in its private place-ment form that means the AIFM

will need to comply with Section XIII of Esma’s remuneration

guidelines, which includes a requirement for managers to

publicise a raft of remuneration details through annual reports

or on their website. The declaration has seen several managers halt moves

to market in the region. One lawyer, who did not wish to be

named, said three clients who had started the national private

placement process have now scrapped their plans due to the

remuneration requirements. However, sources close to

the CSSF said it is just drawing managers’ attention to the cor-

rect rules and if other regulators choose to disapply these rules it

may lead to an Esma review.Section XIII is based on 2009

recommendations that other European countries have not

applied to non-EU AIFMs. It requires

Non-EU managers scrap marketing plans due to

onerous requirementsBY MAIYA KEIDAN

03

COMMENT A RETURN TO PRE-2007 CREDIT MARKET BEHAVIOUR? 14

Luxembourg brings in tough AIFMD remuneration rules

KEEPING IT PERSONALRELATIONSHIPS, HOBBIES, EXTERNAL COMMITMENTS: HOW DO YOU ENSURE INVESTORS AREN’T PUT OFF?FEATURE 19

The long and the short of it

ISSUE 352 4 September 2014

LAUNCHES 10

EQUINOX TO DEBUT ASPECT CAPITAL MUTUAL FUND

London trend giant ’s fi rst standalone ’40 Act offering

PEOPLE MOVES 03

MAN GROUP’S SIMON WHITE RETIRES AFTER 19 YEARS

Geoff Galbraith to take on role of COO

INVESTOR 08

ARIZONA PSPRS MULLS DISTRESSED CREDIT ALLOCATION

Pension plan could invest $75m in Davidson Kempner fund

G O L D S TA R

FEATURE 16

Texas’s fund industry is booming.

HFMWeek investigates the secrets

of the Lone Star state’s success001_003_HFM352_News.indd 1