Embed Size (px)

Citation preview

02 www.hewittasia.com 01India • Volume 1 • Issue 1TotalRewards quarterly

Say on Pay: Is India Inc. Ready For It?4 Variable Pay

Mantra19Double-Digit Hikes to Continue8

India • Volume 1 • Issue 1

SpoTLighT:Variable Pay

02 www.hewittasia.com 03India • Volume 1 • Issue 1TotalRewards quarterly

It is with great excitement that I bring to you the inaugural issue of ‘Total Rewards Quarterly’. Our aim is to make this quarterly the pre-eminent repository of knowledge and exchange of ideas on performance and rewards

between you and Hewitt. Your feedback encouraged us to create this interface, presenting an opportunity to engage with our global experts and proactively present research on topical issues. Tremors of economic disorder are yet to settle globally and it will be wrong to assume that we are entirely out of the woods. In India, fortunately, we are witnessing the early signs of resurgence leading to improved strategic spending on employees, whether that is on compensation, incentives or hiring. However, organizations in this resuscitation phase are far more realistic and are striving to get the balance right between stimulus for growth and restoration of fiscal health. Conventional wisdom in pay management has concentrated heavily on best practice, benchmarking and of course budgets. Compensation is often the single largest transaction cost for an organization, yet many businesses have remained blind to the associated returns and risks. Personally, I feel the economic slowdown has had some positive outcomes. It has reset employee expectations and organizations have been forced to re-examine the quality, impact and risk of their reward programs. In this issue, we are attempting to raise and address some of these challenges for you through our cover story on variable pay and our perspectives on governance and compensation risk management. Even as we close our work on this quarterly, we are already well underway with the first phase of our Salary Increase Survey 2010-11. We look forward to bringing this and other topical research to you when we meet at our Annual Rewards Conference ‘Around the World with Total Rewards’ in November 2010. We hope you enjoy the read and we look forward to receiving your comments and feedback

Sandeep ChaudharyPrincipal | Practice Leader –

South Asia & Middle East

Compensation Consulting

Hewitt Associates

For more information, please write to us

SpoTLighT:Variable pay

CoVeR SToRy

In Hewitt’s recently concluded Variable Compensation Measurement (VCM) survey in India, 54 percent variable pay plans had an objective of improving the top line and 28 percent plans reported an objective of reduction in costs followed by 21 percent plans that had an objective of improving business cash flows.

14

what’s inside

08 11 22

Do You Know How Your Compensation Plans Stack Up? 11

Double-Digit Hikes to Continue 08

Say on Pay: Is India Inc. Ready For It? 04

Survey Calendar 24

Market Updates 22

Ask Our Expert 21

Variable Pay Mantra 19

About Us 26

Coming Up 27

editor-in-Chief

Shilpa Khanna

Tel: +91 124 4155000

Subscription

Design

CReATIve INC. (www.creative-inc.in)

Editorial, Reprints & Syndication Offices

Hewitt Tower, DLF Centre Court

Sector-42, Gurgaon, India-122002

Tel: +91 124 4155000

Fax: +91 124 4052010

Subscription Request

editorial Feedback

Total Rewards Quarterly is published four

times a year by Hewitt Associates

Copyright © 2010 Hewitt Associates

ToTAL ReWARDS QUARTeRLyIndia • volume 1 • Issue 1

www.hewittasia.com

04 www.hewittasia.com 05India • Volume 1 • Issue 1TotalRewards quarterly

Is India Inc. Ready For It?

With the passage of the Dodd Frank Bill with its concerted focus on the whole issue of ‘Say on Pay’, there

is an interesting debate in the Indian context to analyze how Indian regulators will align themselves with these global changes. While, in principle, shareholders have traditionally had their say on executive pay across different regulatory infrastructures — albeit with different levels of compliance requirements — the interest and focus on this aspect of governance has grown over the last year with shareholders increasingly expressing dissatisfaction with large payouts to top management. The Indian regulatory structure has also traditionally allowed shareholders to agree on remuneration to managers and directors, although the extent of shareholder activism on this aspect has been fairly limited. But it would be interesting to see how shareholder behavior changes if the regulatory environment encourages shareholders to vote/discuss executive compensation. A Brief Conceptual and Regulatory overview‘Say on Pay’ is based on the owner-agency dilemma in large corporations. Large corporations are typically run by professional managers on behalf of absentee owners. Since managers are not owners, they will behave in ways that maximize their own long-term interests, rather than the owner’s interests. And while incentive plan structures are aimed at aligning these interests, deciding/questioning how much compensation or incentive is paid to a professional manager should definitely be the right of the absentee owner. ‘Say on Pay’, therefore, is basically a right given to shareholders to vote on the compensation of senior executives/

directors of a company. In most western regulatory structures, ‘Say on Pay’ is largely implemented by providing shareholders a non-binding vote on executive compensation proposals. This new form of voting is most often on matters of fixed compensation increases, incentive payouts and severance proposals. Most long-term or short-term incentive plans have, however, been presented for discussion with shareholders for quite some time now. While most voting is non-binding on the organization, some regulatory structures require binding votes on some aspects of pay, e.g., Long-Term Investment Plans under UK Combined Code for Listed Companies. Globally, the history of shareholder ‘Say on Pay’ is not very long, and can be traced back to British laws, which in 2002 issued the Director Remuneration Report regulations. These regulations required companies to put up the remuneration report for shareholders to vote on at each annual general meeting of a company. Apart from cases such as GlaxoSmithKline, Vodafone, etc., where shareholders voted against either granting of shares or severance packages to the CEOs of these companies, there was very limited activism by shareholders against executive pay increases, incentives or even severance packages. This was largely on account of the fact that companies usually ensured that the more prominent shareholders were in agreement with any compensation changes before they were put up for a vote. Shareholder ‘Say on Pay’ has been encouraged and promulgated as laws across most western economies over the last five years with countries in the eU bloc as well as Australia, Canada, etc. requiring organizations to allow shareholders a non-binding vote on executive pay. US regulators

SAy on pAy:Most long-term or short-term incentive plans have, however, been presented for discussion with shareholders for quite some time now.

were reasonably slow to react to this governance driver, with the first formal legislation being passed only in 2007. Since then, with the recession biting-off large swathes of shareholder wealth, and the government becoming a significant investor into companies, there has been significantly greater activity with multiple legislations around the Troubled Asset Relief Program (TARP) and later the Shareholder Bill of Rights being passed in the Senate. The Current SituationThe interesting data that, however, has filtered out over the last proxy season in the US is that in spite of the significant amounts of data, debates and discussions around excessive compensation to executives, the response from shareholder voting records indicate that out of the 300-odd companies that voted on pay, almost 90 percent shareholders approved the compensation recommendations that were brought up for voting. While a large part of this could be on account of the fact that the Wage Bill actually came down in some of the major US corporations and CeOs across many companies took token salaries in 2008, the extent of diatribe that is seen in the US media surely did not get reflected in the voting data. The protest by shareholders against pay has been more pronounced in Europe, with quite a few prominent organizations, the likes of RBS, Shell, Valeo, etc., having to face shareholder refusal on compensation, incentive or severance proposals. It is possible that

perspective

06 www.hewittasia.com 07India • Volume 1 • Issue 1TotalRewards quarterly

norm for both incentives and increases, ignoring any secular growth trends in the compensation data over multiple periods. Also, most compensation data increases are driven by specific policies that organizations and Boards agree on; shareholders will only see and vote on the output of the policy, it is the organization or the Board that needs to influence that policy and ensure that it is aligned with the appropriate governance standards. Thirdly, while shareholders as owners should have a point of view on compensation of their managers, the line between management or Board decision-making and shareholder opinion gradually starts thinning beyond a point. A manager or the Board, as representatives of the shareholders, with far greater information or experience at their command, should have the right to determine how much to reward specific individuals given the nature of skills or capabilities they bring to the organization. To draw a parallel with the way governments function, members of parliament usually represent the voice of their constituents, and except for rare and special circumstances (such as the vote for eU membership) it usually depends on the parliamentarians to determine what is correct for the larger good. Finally, the vote is usually non-binding. Consequently, there is no express requirement for the company to act on shareholder response to a compensation proposal. And so, while it has the potential of making managers/directors extremely uncomfortable at their compensation data not being accepted by their shareholders, it need not exactly reduce or affect the compensation that they receive. From a purely Indian perspective, it gets even more complicated when one considers the fact that the situation with executive compensation actually isn’t

given the long history of ‘Say on Pay’ vote in these countries, shareholders are more organized in voting on these issues.

The indian RealityThe Companies Act in India and the various Corporate Governance Committees that have submitted their reports over the last decade all point towards the basic objective of ensuring full accountability and transparency of compensation for senior executives and directors of a company. While the Companies Act does not provide any specific requirement for shareholders to vote on executive compensation data/programs, it requires that the remuneration payable to executives and directors be determined by the Board in accordance with, and subject to the provisions of Section 198 of the Companies Act and passed by a resolution in the annual shareholder meeting. various Corporate Governance Committees, starting with the Desirable Corporate Governance Code by CII (1998), mandated the disclosure of each director’s remuneration and commission as a part of the director’s report. It also allowed commission and stock options for non-executive directors, subject to

the attendance being presented before shareholders. The Kumar Mangalam Birla Committee in its report included a non-mandatory requirement to constitute a Remuneration Committee to determine the company’s policy on specific remuneration packages including pension for directors. It also required compulsory remuneration-related disclosures to be made in the section on corporate governance in the annual report. Presently, under the revised Clause 49, all fees/compensation, if any, paid to non-executive directors including independent directors, are to be fixed by the Board of Directors and requires prior approval of shareholders in a general meeting. The shareholders’ resolution is to specify the limits for the maximum number of stock options that can be granted to non-executive directors, including independent directors, in any financial year and in aggregate. The proposed Companies Bill 2009 (yet to be passed) does not make any specific references to shareholder voting on executive compensation. Thus, while the regulatory environment expressly provides shareholders the opportunity to approve or disapprove any recommendations on

compensation of executives or directors, it does not provide any specific guideline to define a voting event on executive pay recommendations. The onus for approving the compensation of executives primarily lies with the Board as representatives of the shareholders, who for all practical purposes themselves merely ratify the decisions.

The Big Questions that need to be AnsweredWhile theoretically, from a governance point of view, there are clear benefits of shareholders, as absentee owners, being allowed a say on the compensation of professionals running the business on their behalf, the complexities this throws up are numerous. Firstly, does the individual shareholder care to invest the time and effort to understand the specific dimensions of a role, the corresponding data, and the parameters that guide the compensation setting for a role, considering there will be almost no difference to the effective returns that the same individual shareholder will generate? Consequently, shareholders will usually choose not to bother about the proposals and rely on the greater information that directors possess and go with their judgment. That probably explains the almost total acceptance of compensation proposals brought forward in US corporations. This can potentially also have definite negative results if minority shareholders decide to go with majority shareholders with vested interests in such voting. Secondly, voting of this nature is usually reactive to large changes in compensation data, ignoring incremental modifications to compensation or incentive data for managers. This effectively implies that even if shareholders exercise their ‘Say on Pay’ rights, they might end up only looking for significant variances from the

Anandorup ghose

Solution Lead – Executive Compensation and Governance, Hewitt Associates, India

For more information, please write to us at [email protected]

executives and managers. Even the proposed Companies Bill 2009, which mandates Remuneration Committees, mandates the need to have only one independent director in the committee. Indian organizations, in many cases, are opaque about their processes for appointing independent directors, and very often are criticized for appointing individuals who end up being completely controlled by the managers or owners. The other complex and potentially debatable consideration that Indian policymakers need to think about when introducing complex governance mechanisms is the kind of impact it might have on the way organizations need to operate to retain their growth momentum. India Inc. has managed to generate better than average growth even when global corporations were bleeding heavily and has managed to jump-start the growth engine much sooner as compared to its global peers. All of this has been achieved without any major compensation excesses or compensation – performance gaps being identified. So, do we stand the risk of introducing potentially limiting and interfering governance mechanisms that can stifle the growth of organizations, when in the first place simpler fixes are sufficient to prevent possible issues in the future? The new draft code released by CII on corporate governance is possibly a strong step in correcting some of the existing anomalies in the current regulatory structure. Our governance framework needs these fixes before we address evolved issues such as ‘Say on Pay’

all that bad. Executives and directors in India are paid much less (even after adjusting for currency, tax, etc.) than their peers abroad. More often than not, compensation for Indian executives seem to display a strong correlation with organizational performance. The other fact that one needs to consider is that India has had very little history of shareholder activism with respect to governance and management effectiveness issues. The Future in the indian ContextLike anywhere else in the world, any regulation around ‘Say on Pay’ needs to be accompanied by detailed guidelines on what the shareholders have ‘a say’ on. Will it be on the actual compensation or incremental value, or even the extent to which these are being aligned to the performance of the organization? These guidelines, if promulgated, need to clearly provide details on the data that organizations will need to provide shareholders before they are required to vote on compensation. Globally, severance packages have been a matter of significant interest and protest by shareholders, and in many cases have been reduced or cancelled on account of shareholder voting. India on the other hand, has very few examples of severance structures for top executives. Clearly, India Inc. and regulators have a lot more to do before introducing mechanisms which are as evolved and rely so much on shareholder maturity as ‘Say on Pay’. India does not yet has basic regulations such as mandatory remuneration committees to decide on compensation for

perspective

08 www.hewittasia.com 09India • Volume 1 • Issue 1TotalRewards quarterly

Double-Digit If 2009 was the year of recession, marred by the gloom of salary cuts, salary freezes, lay-offs and hiring freezes, 2010 is finally celebration time for employees at India Inc. India, Asia’s largest economy after Japan and China, is

accelerating and could reach double-digit growth by 2013. After growing at over 9 percent in the three preceding years, India’s economic growth slipped to 6.7 percent in 2008-09. However, India achieved 7.4 percent growth rate in the last fiscal, primarily due to fiscal stimulus, easy monetary conditions and improved business sentiments as a result of recovering western economies. The Indian job market has also recovered sharply from the weaker forecasts of early 2009 and hiring prospects are strong in 2010. After a long hibernation of 18 months, head-hunters are actively out in the market as talent requirements have started trickling-in across sectors and words such as attrition and job switch are making noise yet again. After plummeting to 6.6 percent in 2009, a sharp recovery is being witnessed in salary increases in the year 2010. Due to a rapidly evolving rewards landscape witnessed in India in the recent years, Hewitt Associates initiated a mid-year dipstick research in June as a follow-on to our 14th Annual Salary Increase Survey that was commissioned in March 2010. The objective of this dipstick was to study the decisions of organizations on the actual salary increases in 2010 and analyze them in comparison with the projections for salary increases provided during the period of January-March 2010. The survey covered 151 organizations across different ownerships and across 19 industries and 26 sub-industries. The data was collected during the period of June-July 2010. The actual annual salary increase in India for 2010 ranges from 10.5 to 11.5 percent across sectors, approximately 67 percent higher than the actual increases in 2009. While most organizations have maintained the actual salary increases in 2010 very close to their earlier projections, others like Technology, Outsourcing and Financial Services organizations have paid out higher increases (1-3 percent higher) than the ones projected in the January-March quarter. It is interesting to observe that India Inc. after having braved a tempestuous storm in 2009, is now adopting deliberate, optimistic, yet slightly cautious strategies for managing rewards and performance. Organizations are willing to invest in their talent and compensate them for the sub-normal salary increases paid out or the salary freezes/cuts implemented in 2009.

Hikes to Continue

perspective

10 www.hewittasia.com

Some Key Takeaways From the Study: ▪ Technology and Outsourcing sectors

have paid out salary increases in the range of 9.5-10.5 percent in 2010 – almost double the salary increases paid out in 2009 and approximately 1 percent higher than the initial projections submitted for 2010. Buoyed by the improving business sentiments in North America and the UK, the recovery in these export-driven sectors have been largely led by the Banking and Financial Services Industry (BFSI), closely followed by Retail, Energy and Utilities. With the market opening up and hiring all set to increase post the downturn, IT/ITeS organizations are expecting to witness a turnover in the range of 18-25 percent

▪ The BFSI sector is one whose fate is directly linked to corporate India’s performance. With market sentiments being bullish across all sectors, the salary increase percentages in the BFSI sector is in the range of 13-15 percent in 2010, approximately 170 percent higher than the increases paid out in 2009. Indian Banks are leading the dream run and would soon expand their operations in overseas markets to continue the momentum they built in the last one year. Once again, the organizations in the sector are thinking in terms of ‘war for talent’ and making early moves to attract the best people in the market ahead of their competitors

▪ Automotive, FMCG and Telecommunication are among sectors that are hiking salaries in the range of 11.5-12.5 percent in 2010. Surge in consumer spending, easy availability of finance, consistent growth of rural India,

handful of recent launches in the Automotive segment and increased competition in Telecommunication has earned these industries a spot amongst the highest salary increase providing sectors in 2010

▪ The Indian Retail sector, which was hit by weak consumer sentiment, tight credit situation and unhealthy cost structures, has bounced back with salary increases in the range of 12.5-13.5 percent in 2010. Major growth drivers for the sector are the rising per capita incomes, improvements in infrastructure and the ease of certain regulatory controls. The sector is witnessing increased competition due to the entry of new and foreign players, thereby increasing the ‘war for talent’ and is also opening up to hiring from Telecommunication and FMCG organizations, which is further pushing the salaries upwards within this sector

▪ The Indian Pharmaceutical industry has shown impressive and consistent growth over the last few years and has become one of the sunrise sectors of the Indian economy. Salary increases in 2010 are in the range of 11.5-12 percent within the sector and are primarily powered by factors such as global cost advantage, availability of skilled manpower, market consolidation and the resulting churn of talent and focus on efficient healthcare in the western markets

▪ Government’s unrelenting investment and stimulus into infrastructure, and entry of many new players has strongly positioned the Engineering, Procurement & Construction (EPC) sector at a 12.5-13 percent average salary increase for 2010

The Road AheadIt is clear that the lessons learnt from the last tumultuous year will not be forgotten in a hurry as India Inc. continues to look at measured business growth and cautious compensation spending. While salary increases have witnessed a sharp rebound from 2009 levels, it will still take another 2-3 years before it reaches back to pre-recession levels. The sectors that are heavily reliant on domestic consumption have recovered sharply from recession, whereas others that are dependant on performance of global economies will gain speed during the course of 2010. India Inc. will also continue to focus on performance and productivity by reinforcing strong pay-for-performance programs as part of the rewards culture.

About hewitt’s Salary increase SurveyHewitt conducts a Salary Increase Survey bi-annually, in June and November, and typically surveys approximately 500+ organizations across ownerships and across 20 primary industries and 25 sub-industries. The study measures actual and projected salary increases, and compensation practices for six specific employee levels, namely top executive, senior management, middle management, junior manager/professional/supervisor, general staff, and manual workforce

Sandeep Chaudhary

Principal | Practice Leader –

South Asia & Middle East

Compensation Consulting

Hewitt Associates

poonam Chopra

Project Lead – Salary Increase

Survey (India), Hewitt Associates

globalperspective

The severity of the recent economic downturn has brought back to corporate America discussions

of risk and managing risk. Downturns tend to have this effect. During periods of prosperity, discussions of risk management often gets pre-empted by creating growth strategies, as if the good times will never end. Yet, how do you know if:Strong short-term financial performance is due to excellent strategy, execution, and risk governance… or comes from excessive risk taking?Often, it is difficult for the Board of Directors to know this for certain at any point in time. However, they should know, and regularly require the management to quantify, what the

fundamental sources of risk are for the enterprise (e.g., commodity price swings, markets subject to rapid change, or potential asset write-downs). They also should know whether their capital structure is too leveraged to withstand an extended earnings slump and a tougher borrowing environment. What Boards may not know today is whether the compensation programs for executives and other highly compensated contributors are aligned with the organization’s risk profile. Are they motivating the right level and type of risk taking or excessive risk taking? Evaluating compensation programs from a risk management perspective has only recently begun to emerge on the compensation committee’s radar. This perspective, however, may

lead to different conclusions than the competitive or pay-for-performance perspectives that compensation committees and their advisors have traditionally applied.

Why Take a Compensation Risk Management perspective?There is a widely held belief that compensation drives behavior. Compensation schemes have been deemed to be the contributing factors to the demise of organizations from Enron earlier this decade to the troubles with AIG and the banking industry today. The thought is that highly leveraged, short-term-oriented compensation programs coupled with generous severance packages encourage

Do yoU KnoW How Your Compensation Plans Stack Up?

perspective

For more information, please write to us

India • Volume 1 • Issue 1TotalRewards quarterly

11

12 www.hewittasia.com 13India • Volume 1 • Issue 1TotalRewards quarterly

executives to take excessive risks. One can always debate the impact of compensation on behavior. However, it must be recognized that compensation risk is derived from business risks, and not the other way around. Meanwhile, as a good governance practice, we can begin to do a better job of analyzing whether the potential to motivate excessive risk taking exists and mitigate this potential in the compensation design. There is also a distinct possibility that the government will get involved. This has already occurred for organizations that have taken TARP funds. These organizations’ compensation committees initially had 90 days to evaluate compensation plans to ensure that ‘they do not encourage taking unnecessary or excessive risks that threaten the value of the organization’. This requirement has been expanded and the reviews now need to be conducted semi-annually. The potential for expansion of government involvement in compensation risk management to all industries was introduced in a recent speech by Mary Schapiro, SeC Chairman, when she stated that in the next few months, “The commission will be considering whether greater disclosure is needed about how a company, and the company’s Board in particular, manages risk, both generally and in the context of setting compensation”. Also, Senator

Charles Schumer is soliciting support for a ‘Shareholder Bill of Rights Act’ that addresses risk management oversight at the Board level as one of the several components.

how to Approach a Compensation Risk Management Review?We foresee a time when the risk management perspective will be integrated into a comprehensive review of executive compensation and corporate governance practices. However, the initial review might be better approached as a stand-alone process. For one, it requires new people to be involved – such as the organization’s chief risk officer. Second, risk management – of the organization, not the compensation – is the Board’s responsibility. The compensation review should be linked to any overall analysis of risks being undertaken. We believe that organizations should start with a few key principles:▪ Fundamentally, this is a Board/

committee-driven process working closely with the management

▪ Link the review of the risk to the organization’s risk profile and business strategy by identifying the key sources of risk, the potential magnitude of the performance impact, and the time frame of the risks

▪ Review each feature of compensation individually, but

establish evaluation process

Objectives

Participants and Roles

Time Frame for Completion

Scope

Affirm Material Business Risks

evaluate Total Compensation for

potential incentive to excessive RiskSources of Risk

Areas of Risk

Performance Measurement/Planning

Mitigating Risk

Areas of Potential Concern

Mitigating Factors

Philosophy Issues

complete profitability picture is known?

▪ Do we pay out too soon given the time frame of the risks taken?

▪ How closely is compensation opportunity linked directly to the shareholder experience?

– Percentage of payment denominated in shares

– Vesting/ownership guidelines/ holding requirements

▪ Do the performance measures we use motivate long-term, value-creating actions and decisions?

▪ Are the performance goals, not only at target, but also at threshold and superior levels, established at levels that encourage the right level of risk taking? Are they linked to the potential impact of these risks on planned performance?

▪ Are the compensation levels earned consistent with the performances delivered?

▪ Is executive severance so high as to take away the fear of failure?

▪ Do the compensation plans overall motivate the right level of risk (neither too high nor too low) for our organization?

While these questions should be applied to each material feature of annual and long-term incentive design,conclusions should be made in the context of total compensation including related programs such as retirement plans, severance, and ownership guidelines. Wherever possible, quantitative analysis should supplement qualitative evaluations. Be wary of approaches that solely focus on comparing to peer organizations’ pay practices. If an entire industry has it wrong, being the upper quartile does not matter – think ‘financial services’ in 2008. However, because the risk management focus is new, there will be few existing standards. Normative as well as

An executive compensation structure consisting solely of base salary plus restricted stock that must be held until retirement should not encourage excessive risk taking.

draw conclusions based on the total compensation program

▪ Establish or review, the list of objectives for total compensation of which risk management is one

▪ Address compensation programs for all high-risk positions. Executives are, and should be the primary focus of attention. However, some organizations have other positions that have the ability to put the organization at risk and have highly leveraged incentive compensation schemes (e.g., traders)

Consider a three-phase process that begins with good governance and an understanding of the organization’srisk factors before addressing the compensation plans.

What to Address in the process?Establishing the evaluation process determines who is involved and what group is ultimately accountable.Also, since compensation plan changes generally start with the fiscal year, it is important to begin soon and establish a time frame that is integrated with the compensation committee schedule. Then, move on to confirm the business risk profile. Sources of business risk include, but are not limited to:▪ Potential Write-Downs of Long-Term

Assets/Investments – Examples include buildings, plant and equipment, acquisitions, financial

instruments, investment portfolios, or intangible assets

▪ Recovery of Upfront expenses – Examples include R&D, material marketing expenses (new product launch), or inventory build up

▪ Commodity Prices Volatility – Examples include both buyers and sellers of commodities such as natural resources

▪ Speculative Risk – examples include trading of energy, financial instruments, or stocks

▪ Financial Structure/Cash Flow – Examples include the organization’s ability to re-finance short and long-term debt, whether cash flow can cover interest payments and whether there is adequate equity as a percentage of total capital

▪ Currency Risk – FX on its own is often not a material risk but in combination with others can lead to material total risk

▪ Country Risk – Examples include potential for nationalization of assets, limits on moving cash and political or civil unrest

▪ Regulatory Risk – Examples include environmental and anti-trust

▪ Reputation Risk – Impact of trust on sales and transactions

The review of total compensation in light of your organization’s specific business risks should address the following questions:▪ Do the incentive plans allow for

substantial payment before the

comparative standards will need to be developed. Ultimately, the compensation committee will need to apply judgment to determine what, if any, changes are required. As stated earlier, a risk management perspective should not be the sole perspective when determining compensation design. An executive compensation structure consisting solely of base salary plus restricted stock that must be held until retirement should not encourage excessive risk taking. However, this approach may fail to achieve other critical compensation objectives.

What Might Change?What should a compensation committee and management expect from a risk management review of compensation? While the answers should be organization-specific, we expect that a risk management perspective may change the way committees think about:▪ The mix of annual and

long-term compensation▪ The forms of long-term

incentive used▪ The definition of incentive plan

performance measures and the approach for setting goals

▪ The degree of leverage in the compensation plan

▪ The length of equity vesting schedules and/or holding periods

▪ The amount of guaranteed severance and the definitions of termination without severance

However, you will not know whether these will change for your organization until you take the necessary steps of reviewing and stress-testing your program

globalperspective

The article has been authored by Hewitt Associates’ Executive Compensation Group.For more information, please write to us at [email protected]

14 www.hewittasia.com 15India • Volume 1 • Issue 1TotalRewards quarterly

coverstory

Variable PaySPOTLIGHT:

Well-articulated objectives help in designing an effective plan, since the outcomes of the plan are known and expectations are clear at every level.

Variable pay is simply defined as ‘pay at risk’. This three-word definition holds true for an employee and for the organization, but does it mean anything else? It is a powerful tool to link the employee rewards with the overall objectives of

the organization – both for the short and long run. A well-designed plan which is aligned to the organization goals and is well-understood by employees helps the organization effectively mobilize its employee population towards a common set of objectives. For a plan to be successful, it is important to lay down the objectives of the plan clearly. Well-articulated objectives help in designing an effective plan, since the outcomes of the plan are known and expectations are clear at every level. The objectives of the plan vary from organization to organization although most organizations do have a financial goal as a primary objective of a plan. In Hewitt’s recently concluded Variable Compensation Measurement (VCM) survey in India, 54 percent plans had an objective of improving the top line and 28 percent plans reported an objective of reduction in costs followed by 21 percent plans that had an objective of improving business

cash flows. These financial objectives are supplemented by other objectives which are, to an extent, behavioral in nature but are important in growing the organization. Examples of such objectives are rewarding individual excellence, increasing productivity and inclusive growth. Once the objectives of the plan are clearly laid out, it is important that each element of the variable design is approached very cautiously and is aligned with the overall objectives of the plan. The following document highlights some of the findings from this study, and provides an overview of how organizations in India are thinking about their variable pay plans.

plan eligibilityThe plan eligibility defines who in the organization will participate in the plan. Eligibility has to be viewed in line with the stated objectives, e.g. if the plan has to foster teamwork and inclusive growth, generally a larger population will be covered. Impact on performance measures is another important consideration, i.e. do the participants have a ‘line of sight’ to the set performance goals, if not, should they be included in the plan? From our survey findings, we found that 34 percent

organizations have all their employees participate in the plan and others cut-off the eligibility primarily by grade/level.

plan FundingThe critical question when structuring an incentive plan is to determine how these payouts get funded. The answer varies and depends on the business lifecycle stage of an organization. Organizations in the start-up stage typically follow a budgeted approach, i.e. an amount is earmarked at the beginning of the year and is modified on a quarterly/ half-yearly basis for expected payouts. As organizations move on to growth/maturity stage, they generally follow a self-funding approach where the amount available for variable pay disbursement is linked to one or the other profitability metrics. The formula ensures that the variable pay pool is funded by incremental profits. Many organizations also use a hybrid approach where the target variable pay pool is available at a target level of performance and any level of over-achievement in profitability increases the available pool generally subject to a maximum. 73 percent plans covered in our survey reported of having a budgeted approach to funding.

16 www.hewittasia.com 17India • Volume 1 • Issue 1TotalRewards quarterly

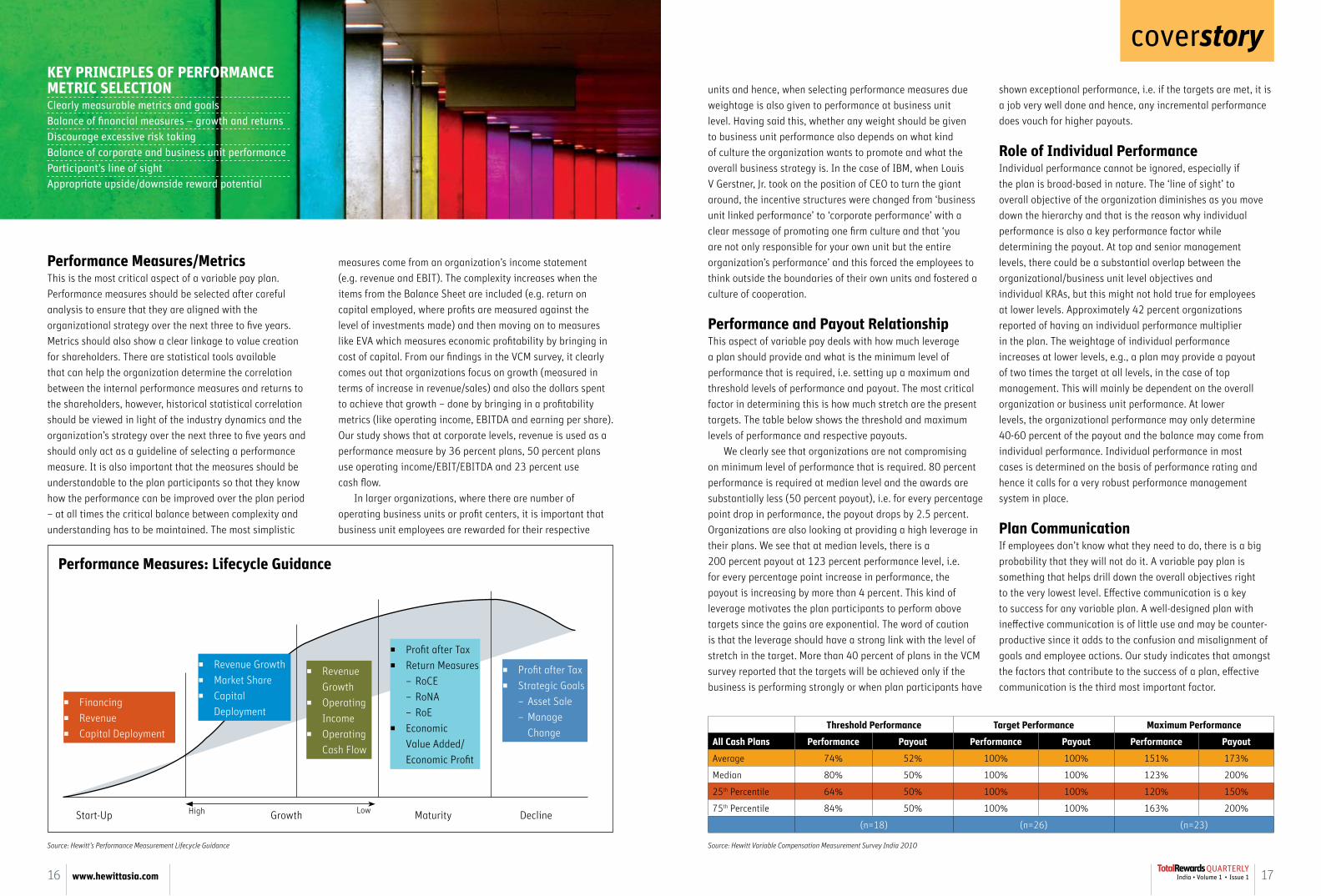

units and hence, when selecting performance measures due weightage is also given to performance at business unit level. Having said this, whether any weight should be given to business unit performance also depends on what kind of culture the organization wants to promote and what the overall business strategy is. In the case of IBM, when Louis v Gerstner, Jr. took on the position of CeO to turn the giant around, the incentive structures were changed from ‘business unit linked performance’ to ‘corporate performance’ with a clear message of promoting one firm culture and that ‘you are not only responsible for your own unit but the entire organization’s performance’ and this forced the employees to think outside the boundaries of their own units and fostered a culture of cooperation.

performance and payout RelationshipThis aspect of variable pay deals with how much leverage a plan should provide and what is the minimum level of performance that is required, i.e. setting up a maximum and threshold levels of performance and payout. The most critical factor in determining this is how much stretch are the present targets. The table below shows the threshold and maximum levels of performance and respective payouts. We clearly see that organizations are not compromising on minimum level of performance that is required. 80 percent performance is required at median level and the awards are substantially less (50 percent payout), i.e. for every percentage point drop in performance, the payout drops by 2.5 percent. Organizations are also looking at providing a high leverage in their plans. We see that at median levels, there is a 200 percent payout at 123 percent performance level, i.e. for every percentage point increase in performance, the payout is increasing by more than 4 percent. This kind of leverage motivates the plan participants to perform above targets since the gains are exponential. The word of caution is that the leverage should have a strong link with the level of stretch in the target. More than 40 percent of plans in the VCM survey reported that the targets will be achieved only if the business is performing strongly or when plan participants have

Key pRinCipLeS oF peRFoRMAnCe MeTRiC SeLeCTionClearly measurable metrics and goalsBalance of financial measures – growth and returnsDiscourage excessive risk taking Balance of corporate and business unit performanceParticipant’s line of sightAppropriate upside/downside reward potential

performance Measures/MetricsThis is the most critical aspect of a variable pay plan. Performance measures should be selected after careful analysis to ensure that they are aligned with the organizational strategy over the next three to five years. Metrics should also show a clear linkage to value creation for shareholders. There are statistical tools available that can help the organization determine the correlation between the internal performance measures and returns to the shareholders, however, historical statistical correlation should be viewed in light of the industry dynamics and the organization’s strategy over the next three to five years and should only act as a guideline of selecting a performance measure. It is also important that the measures should be understandable to the plan participants so that they know how the performance can be improved over the plan period – at all times the critical balance between complexity and understanding has to be maintained. The most simplistic

measures come from an organization’s income statement (e.g. revenue and EBIT). The complexity increases when the items from the Balance Sheet are included (e.g. return on capital employed, where profits are measured against the level of investments made) and then moving on to measures like evA which measures economic profitability by bringing in cost of capital. From our findings in the vCM survey, it clearly comes out that organizations focus on growth (measured in terms of increase in revenue/sales) and also the dollars spent to achieve that growth – done by bringing in a profitability metrics (like operating income, EBITDA and earning per share). Our study shows that at corporate levels, revenue is used as a performance measure by 36 percent plans, 50 percent plans use operating income/EBIT/EBITDA and 23 percent use cash flow. In larger organizations, where there are number of operating business units or profit centers, it is important that business unit employees are rewarded for their respective

shown exceptional performance, i.e. if the targets are met, it is a job very well done and hence, any incremental performance does vouch for higher payouts.

Role of individual performanceIndividual performance cannot be ignored, especially if the plan is broad-based in nature. The ‘line of sight’ to overall objective of the organization diminishes as you move down the hierarchy and that is the reason why individual performance is also a key performance factor while determining the payout. At top and senior management levels, there could be a substantial overlap between the organizational/business unit level objectives and individual KRAs, but this might not hold true for employees at lower levels. Approximately 42 percent organizations reported of having an individual performance multiplier in the plan. The weightage of individual performance increases at lower levels, e.g., a plan may provide a payout of two times the target at all levels, in the case of top management. This will mainly be dependent on the overall organization or business unit performance. At lower levels, the organizational performance may only determine 40-60 percent of the payout and the balance may come from individual performance. Individual performance in most cases is determined on the basis of performance rating and hence it calls for a very robust performance management system in place.

plan CommunicationIf employees don’t know what they need to do, there is a big probability that they will not do it. A variable pay plan is something that helps drill down the overall objectives right to the very lowest level. effective communication is a key to success for any variable plan. A well-designed plan with ineffective communication is of little use and may be counter-productive since it adds to the confusion and misalignment of goals and employee actions. Our study indicates that amongst the factors that contribute to the success of a plan, effective communication is the third most important factor.

▪ Financing▪ Revenue▪ Capital Deployment

Start-Up High Growth Maturity DeclineLow

Threshold performance Target performance Maximum performance

All Cash plans performance payout performance payout performance payout

Average 74% 52% 100% 100% 151% 173%

Median 80% 50% 100% 100% 123% 200%

25th Percentile 64% 50% 100% 100% 120% 150%

75th Percentile 84% 50% 100% 100% 163% 200%

(n=18) (n=26) (n=23)

coverstory

performance Measures: Lifecycle guidance

▪ Revenue Growth▪ Market Share▪ Capital

Deployment

▪ Revenue Growth▪ Operating Income▪ Operating Cash Flow

▪ Profit after Tax▪ Return Measures – RoCE – RoNA – RoE▪ economic Value Added/ economic Profit

▪ Profit after Tax▪ Strategic Goals – Asset Sale – Manage

Change

Source: Hewitt Variable Compensation Measurement Survey India 2010Source: Hewitt’s Performance Measurement Lifecycle Guidance

18 www.hewittasia.com 19India • Volume 1 • Issue 1TotalRewards quarterly

coverstory

The success of a plan is evaluated on the basis of achievement of stated plan objectives. Hence, the very foundation of the plan has to be critically debated even before one starts designing a plan. A plan can be very well-designed, but if the objectives are not in strategic alignment, there is a great possibility that the plan might fall flat. It is like climbing up a tall building and after reaching the top realizing that it is the wrong building. A well-designed, communicated and well-supported plan can bring together the efforts and energies of all employees towards the achievement of short-term objectives, which is a stepping stone to an organization’s long-term goals and strategy. Variable pay plans play a very important role in today’s dynamic economic environment. Many organizations in India are looking at revisiting the variable pay program to ensure that the plan is driving the right objectives and is in line with any changes that were made in the organization’s strategy in the wake of the recent economic turmoil.

Percentages will total more than 100 percent due to more than one response by some participants. Source: Hewitt Variable Compensation Measurement Survey India 2010

Factors Contributing to the Success of the Plan Percent of Plans

Appropriate Award Size 35%

effective Communication of Plan 47%

Employee Ability to Impact Results 18%

employee Understanding of Plan Objectives 32%

Realistic Goals/Targets 59%

Support of executives/Management 76%

Others 3%

About Variable Compensation Measurement Study ▪ Conducted for nearly 15 years, Hewitt’s variable

Compensation Measurement (VCM) survey is the only annual broad-based study capturing unique plan characteristics for cash and special recognition

▪ Areas evaluated include: Plan Objectives, Plan eligibility, Funding, Design, Plan effectiveness

Available Variable Compensation Measurement MarketseuropeAustria, Czech Republic, France, Germany, Italy, Netherlands, Poland, Sweden, Switzerland, United KingdomMiddle eastBahrain, egypt, Qatar, Saudi Arabia, United Arab emiratesAsia PacificAustralia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, ThailandThe AmericasCanada, United States

Anubhav gupta

Senior Consultant – Executive Compensation and

Governance, Hewitt Associates, India

For more information, please write to us

ViSTy BAnAjiFormer Executive Director & President (HR & Corporate Affairs), Godrej Industries Limited. He has also worked in France and India for ALSTOM. His earlier career started as a TAS Officer with Tata and he left the group as Corporate HR Head for Telco (now Tata Motors). He recently founded a boutique strategic HR consulting firm.

Q What are the three most critical things that an organization should keep in mind while designing a broad-based variable pay program?Four (sorry, I couldn’t limit it to three) fundamental questions the design must address:1 How does this pay-off design align with the EVP, cultural pillars and strategic agenda the organization is trying to drive? 2 How can the program design reinforce (or at least not dissipate) intrinsic motivators? 3 How can all or most of the critical delivery expectations, for all positions covered under the program, be captured and evaluated with an accepted degree of validity within the time span of the program period?4 How is target difficulty/evaluation fairness ensured between individuals/units/teams and what does this choice do to internal teamwork?

Q Do you think variable pay changes its definition as we move down the management hierarchy i.e., is it viewed more as an entitlement at lower levels? Regardless of level, the perception of entitlement has more to do with the manner in which the program is sold (at the time of recruitment), communicated and administered.

Q In your experience, to what extent should organizational/business unit performance be allowed to influence the quantum of reward at mid or junior management levels?Although the effect of organizational/business performance can be proportionately less at mid/junior management levels, people at these levels also expect to share the gains of a very good organizational performance and can understand why the pie is smaller when the business is doing badly.

theinterview

20 www.hewittasia.com 21India • Volume 1 • Issue 1TotalRewards quarterly

Q Target setting is usually the most contentious issue in implementing incentive plans – how have you typically driven the process of ensuring that targets are achievable while not being too easy? For individual targets, which are quantifiable, previous and comparative achievement records together with the supervisors’ intimate knowledge of the domain and essential fairness are vital for the exercise. These supervisory capabilities are even more important when majority of the targets are not easily quantifiable. In such cases, giving individuals the freedom to set their own targets and inspiring them to aim high, while the supervisor provides the moderating ‘reality check’, is the ideal approach to aim for. You will see how vital a role the supervisor plays in either case. Hence, the right attitude and training of supervisors is probably the most important variable determining the success of any variable pay program that has appraisal-based individual differentiation.

Q What is the ideal approach towards defining metrics for incentive plans? To what extent can metrics be qualitative while not losing the objectivity in the plan/payout process?The real challenge is how to give adequate weightage to result areas that are vital but difficult to measure in comparison to those that are less important but neatly quantifiable. The graveyard of incentive plans is crowded with oversmart attempts to find surrogate variables that lead to gaming and other organizationally harmful behavior. Plans that have no room for supervisory judgment and rater-ratee trust are headed for disaster when most metrics are qualitative.

Q We hear about innovations in plans like deferment of award for 2-3 years.

What according to you is driving these things? And how relevant do you think these things are in the Indian context in broad-based plans?I wouldn’t call it innovative – we designed the first such plan for Telco in the eighties. Provided such a plan diverts only a part of the gain-sharing, is limited to people who determine long-term performance (i.e. the top team) and is well-communicated, it can be a good way of encouraging long-term thinking and can act as an aid to talent retention.

Q How often do you think an organization should revisit their variable pay plans or what are the key indicators that an organization should look for to decide that its time to have a re-look? When the plans are not resulting in the performance improvement or cultural

outcome they were supposed to drive, it is time for a re-look. If they are causing dysfunctional behavior, emergency surgery is required. Q What should be kept in mind while

developing a communication strategy for variable pay? Transparency and a great respect for the intelligence of the plan participants – regardless of their level. The bottom line is that communication cannot substitute the fundamental fairness or quality of the plan design.

Q How do you determine how effective a plan is?By looking at what happens that wouldn’t have happened without the plan

theinterview

Variable pay

Mantra

askourexpert

Shekhar Purohit leads our Global Compensation

Consulting practice. Most recently, Shekhar led Hewitt’s

Executive Compensation and Corporate Governance

practice for the Asia Pacific region. He specializes in

identifying the drivers of shareholder value creation and

their relationship to performance management, strategy

execution, and total rewards.

Prior to joining Hewitt Associates, Shekhar co-founded

The Delves Group, and worked at Towers Perrin, Sibson

Consulting and SCA Consulting. Shekhar is also the

Co-founder and Vice President of a non-profit educational

organization in Boston, which focuses on providing

HIV/AIDS education for developing countries Mail your queries for Shekhar at [email protected]

SheKhAR pURohiT PRInCIPAL GLOBAL COMPEnSATIOn COnSULTInG LEADER

We bring to you ‘our expert’, Shekhar Purohit, Global Head of Rewards, at Hewitt to answer your questions related to compensation management.

For more information, please write to us

22 www.hewittasia.com 23India • Volume 1 • Issue 1TotalRewards quarterly

marketupdate

gratuity provisioningThe payment of Gratuity Act is amended with effect from May 24, 2010. The new amendment increases the upper limit of the gratuity payment from INR 350,000 to INR 1,000,000. In 2008, based on the recommendations of the government- constituted Pay Commission, the gratuity payment was enhanced for employees of the government to INR 1,000,000. This was also followed by an income tax amendment that allowed employees to receive the enhanced gratuity payment free from tax. These changes were specific to the employees of government. With this amendment, minimum Gratuity Act payments for private sector employees are now at par with government employees.

Annual income Tax Slab

Upto INR 200,000 (250,000 for senior citizen)

Nil

Between INR 200,000 to 500,000

10%

Between INR 500,000 to 1,000,000

20%

Above INR 1,000,000 30%

2 EEE (Exempt, Exempt, Exempt) method of taxation continued for popular schemes such as Government Provident Fund, Recognized Provident Fund, Public Provident Fund and Superannuation Schemes. Overall investment deduction limit of INR 100,000 applies for contribution to approved funds such as Provident Funds, Superannuation Fund, Pension and other notified funds

3 In addition to the deduction as mentioned above, an additional deduction upto the limit of INR 50,000 shall be allowed for the following:

▪ Medical insurance premium paid for self/spouse/children/ dependent parents

▪ Life insurance premium, if the premium paid during the year does not exceed 5 percent of the sum assured

▪ Tuition fees paid to any school, college or technical institute situated within India for the purpose of full-time education of any two children

The aggregate amount of additional deduction, as listed above, should not exceed INR 50,0004 Deduction for interest on housing

loan for a self-occupied house continued upto a limit of INR 150,000

5 Deduction shall be allowed for interest on loan taken for pursuing higher education by self, spouse or child

6 The exemption for Leave Travel Concession (LTC) has not been mentioned in the DTC

7 Deductions for mutual funds, eLSS,

housing loan repayment (principal) has been removed

8 Tax exemption continued for long-term capital gains from sale of listed shares. Short-term capital gain from sale of listed shares will be taxed after deduction of 50 percent

9 Corporate Tax has been capped at 30 percent (i.e. inclusive of surcharge, education cess and secondary education cess)

expatriate hiring in india On July 7, the Indian Government removed the ceiling on the number of foreigners an organization can hire as well as the cap on their annual compensation. Indian organizations had to earlier limit their foreign recruitments to 1 percent of their total workforce and pay them annual salaries upto USD 25,000. All the new applicants will, however, have to fulfill other existing conditions to get an employment visa. According to rule, the employment visa is granted to an expatriate if he or she is a ‘skilled’ and ‘qualified professional’ or a person who is being engaged or appointed by a company, organization, industry or undertaking in India on contract or employment basis at a senior level/skilled position such as technical expert, senior executive or in a managerial position. The employment visa is not granted for jobs for which large number of qualified Indians are available. Similarly, it is not granted for routine, ordinary or secretarial/ clerical jobs

MarketUpdate

The new code comes into effect from April 2012. In the proposed tax slab, exemption limit has been increased from INR 160,000 to 200,000 (INR 250,000 for senior citizens) and gender distinction removed by having a single tax slab for both male and female tax payers

For more information, please write to us

For private sector employers, the accounting impact of gratuity in the P&L Account and Balance Sheet provisioning may increase significantly for enterprises that currently have adopted gratuity plans in line with the Gratuity Act. The increase in the minimum Gratuity Act payment will also produce a higher tax deduction for the increased gratuity accrual. The increase may be recognized immediately or can be amortized over the next five years as per the provisions of the Income Tax Act.

new Direct Tax Code – What’s in it for us as employers and employees?The revised draft of the Direct Tax Code (DTC) bill was introduced in the parliament in the last week of August

and will replace the existing Income Tax Act of 1961. The code envisages promoting voluntary tax compliance and an equitable and progressive tax regime by eliminating distortions in the tax structure, introducing moderate levels of taxation, expanding the tax base and simplifying the drafting language. The implementation date has been moved to April 2012 from April 2011 to allow tax practitioners, tax payers and administrators enough time to become adequately familiar with the new provisions in DTC. The new code will completely overhaul the existing tax proposals for not only individual tax payers, but also corporate houses and foreign residents. The salient features and highlights of the DTC tabled at the parliament

pertaining specifically to employers and employees is as follows:1 The tax rates and slabs have been

modified. The proposed rates and

slabs are as follows:

24 www.hewittasia.com 25India • Volume 1 • Issue 1TotalRewards quarterly

Salary increase Survey phase i: june-September 2010phase 2: november-March 2011 One of the most exhaustive studies in the area of performance and rewards in India. The study measures actual and projected salary increases, variable pay and performance data across employee categories.

hewitt india TCM Survey 2010 March-August 2010 Hewitt’s Total Compensation Measurement™ (TCM) survey serves more than 7,000 organizations in over 40 international markets globally. The survey provides access to competitive pay data as well as plan design features for base salary, bonus, long-term incentives, benefits, and perquisites.

Variable Compensation Measurement Study May-August 2010 Launched for the first time in India, Hewitt’s Variable Compensation Measurement survey is the only annual broad-based study capturing unique plan characteristics for cash and special recognition.

executive Compensation Study july-october 2010 A first-of-its-kind study launched in India by Hewitt. The study will provide organizations with access to rich analysis of data and practices in executive compensation.

india Banking StudyMay-october 2010 A study for all major Indian and MNC Banks to come together to share and benchmark their positions and levels across the industry.

investment Banking StudyMay-September 2010 A benchmark study conducted for large MNC and Indian Investment Banks covering 120+ positions across investment banking, institutional equities, research, debt and fixed income.

Asset Management Forumjuly-october 2010 A flagship study in the AMC sector benchmarks 100+ positions across fund management, sales and other functions.

private Banking Forumjune-September 2010 A study covering large Indian and MNC private wealth management organizations and benchmarks key roles across functions.

Microfinace Compensation SurveyDecember-March 2011 A study that measures and analyzes salary benchmarks for MFIs across India.

Life insurance Forum August-october 2010 A study of large Indian and MNC life insurance organizations covering 100+ positions across sales & distribution, actuarial services, and other functions.

Retail Broking Forumnovember-February 2011 A study covering Indian and MNC retail brokerage organizations and benchmarks 100+ positions across sales, PMS and other functions.

private equity ForumSeptember-December 2010

A study of private equity players covering key positions across fund management roles.

nBFC Forumnovember-March 2011 A study of large NBFCs covering cash and benefits data across 100+ positions.

hewitt india Telecom-infrastructure Forumoctober-December 2010 The study brings together all major telecom infrastructure organizations to share and benchmark their positions and levels across the industry.

hewitt india Telecom Forumnovember-March 2011 This is one of the flagship studies in the Telecom sector that captures cash and benefits information across 170 positions.

SiAM Forum Compensation Studyoctober-December 2010 This study looks at compensation data across levels of management and also serves as a platform for sharing best practices.

hewitt india FMCg Forum 2010-11june-September 2010 The study brings together all major MNC and Indian FMCG organizations to benchmark their positions, levels and benefits across the industry.

Clinical Research ForumAugust-December 2010 The study covers leading clinical research organizations providing robust and comprehensive information on cash compensation, benefits and industry trends.

iT industry Studyjune-September 2010 Launched in 2001, this study provides robust and comprehensive information on cash compensation, benefits and industry trends.

iTeS industry Studyjuly-october 2010 This exhaustive study covers 500+ positions across 60+ job families. The study also includes detailed benefits and compensation best practices benchmarking across the ITeS industry.

indian Semiconductor & eDA Forum (iSeF) july-october 2010 Rewards/HR managers of leading Semiconductor & EDA organizations have come together to form a rewards forum for conducting a comprehensive, co-sponsored rewards benchmarking survey

surveycalendar

For more information, please write to us at [email protected]

Upcoming inSighTS

26 www.hewittasia.com 27India • Volume 1 • Issue 1TotalRewards quarterly

In the current dynamic business environment, business objectives can change frequently, and

strategies for meeting those objectives change even more often. Employee compensation needs to support the organization’s objectives and strategies, while at the same time accomplishing the following goals related to its key talent: ▪ Attract and retain employees▪ Motivate and reward performance▪ Align rewards with the

organizational culture▪ Encourage desired behaviors and

recognize the required results▪ Focus employees on achieving the

organizational goalsAt the same time, the compensation program needs to be simple enough that employees can understand it and the human resource team can administer it. That’s a tall order. Our broad-based Compensation practice helps ensure that your organization’s pay strategy is designed and executed to meet business needs, while focusing employees on what they need to do to help the organization meet its goals.

Hewitt’s CompensationConsulting Services

aboutus

Combining Expert Consulting with Top Quality, Comprehensive Data to Ensure Effective Pay Programs

Strategic solutions for compensation: A sound strategic plan for compensation originates with an organization’s business plan. Hewitt’s Business Driver Analysis determines what your organization’s objectives are and how they should link to compensation. Compensation design solutions: Hewitt determines what type of pay programs will best support the organization’s compensation strategy. We define the jobs being performed, determine their economic value, and then make recommendations on salary structures, pay bands or grades, and applicable variable pay and recognition programs. We additionally provide consulting on pay delivery processes for merit pay, promotions, and adjustments and assist in developing administrative policies and procedures related to pay.Data-related services: Hewitt fulfills your organization’s data needs with competitive compensation data.We help organizations plan and manage compensation programs based on our analysis of this data. Our market pricing provides a valid, definitive way to determine how an organization’s pay compares to that of other organizations.

Then, if the current compensation program needs adjustment, we provide consulting on the best ways to manage the changes. We also conduct compensation audits, to review current practices and approaches, and compensation modeling, where our ‘what-if’ analyses allows you to test different assumptions. our experience: Hewitt started its compensation practice in 1940. We pull from this deep experience to offer insight and ideas that have proven to be successful.

About hewitt AssociatesFor more than 70 years, Hewitt Associates (NYSe: HeW) has provided clients with best-in-class human resources consulting and outsourcing services. Hewitt consults with more than 3,000 large and mid-size organizations around the globe to develop and implement HR business strategies covering retirement, financial, and health management; compensation and total rewards; and performance, talent, and change management. For more information, please visit www.hewitt.com

Across the world, organization heads are looking at new approaches to optimize their

Total Rewards Strategy and strike a balance between risk and rewards. They not only have the task of rewarding the right candidate in the right measure, but also have the responsibility to scale their rewards policies to meet the organizational goals and leverage them to get the desired results.

Hewitt’s ‘Around the World with Total Rewards 2010’ is designed to help you unleash the power of rewards as a winning HR tool. It is an opportunity to discuss and evaluate time-tested practices and innovative ways to solve the newer challenges of managing and rewarding talent. Launched in 2006, the conference has met with resounding success in multiple countries and will be back in

Around the World with

Total Rewards 2010M i D - n o V e M B e R 2 0 1 0 , M U M B A i

comingup

To receive updates on the conference, please send

us an email at [email protected]

India in November. Hear from Hewitt Content Leaders and Industry Experts as they share recent research, compelling success stories and emerging practices