Embed Size (px)

Citation preview

Revıewthe

Spring 2010

A continent gets connectedHow digital technology is solving some of Africa’s most pressing problems

NFC ticketing takes off

Fingerprint ID opens Windows

How the cellphone is reinventing social computing

Meet the man who helped secure eCommerce

�

As each year goes by, the Internet becomes more and more mobile. Mobile Network Operators can monetize the cellphone ‘screen’, with many third parties willing to sell, promote and market their goods and services. Thanks to Gemalto’s position at the heart of wireless networks for the past two decades, we are well placed to bridge these worlds with a range of solutions, services and technologies to link people’s personal, digital and mobile lives.

Bridging worlds is also one of the themes of this issue’s cover feature – in this case, introducing the digital technology that has become commonplace in the developed world to Africa, where it can have life-changing effects. Turn to page 18 to read about it.

One of the most prominent areas of convergence is social networking. On page 8, we look at some of the recent research into the spread of mobile social networking and examine the factors that are driving it forward – and those that are holding it back.

Add near field communication (NFC) technology to the cellphone and it becomes a fast, convenient and secure means of payment. On page 24, we report on the progress of a number of NFC mobile transportation ticketing trials.

Finally, as we report on page 36, Gemalto is working to reduce the environmental impact of its products. In that spirit, you may notice that the reader survey that is usually bound in to the back of this magazine has disappeared, to be replaced by an online survey. To find out how to complete it, please go to page 17.

Philippe ValléeExecutive Vice President, Telecoms Business Unit, Gemalto

Welcome

The Review

NFC

buy!

18

4

30

Cove

r im

age:

Alfre

do C

aliz/

Pano

s

Upfront

The Review is published by Gemalto Corporate Communications – www.gemalto.com© 2010 Gemalto – www.gemalto.com. All rights reserved. Gemalto, the Gemalto logo and product and/or service names are trademarks and service marks of Gemalto NV and are registered in certain countries. The views expressed by contributors and correspondents are their own. Reproduction in whole or in part without written permission is strictly prohibited. Editorial opinions expressed in this magazine are not necessarily those of Gemalto or the publisher. Neither the publisher nor Gemalto accepts responsibility for advertising content.

For further information on The Review, please email [email protected]

The Review is printed on 9Lives 55 Gloss & Silk paper. Certified as an FSC mixed sources product, 9Lives 55 is produced with 55% recycled fiber from both pre- and post-consumer sources, together with 45% FSC certified virgin fiber from well managed forests.

4 Digital Digest_What’s new in digital security

8 research_The importance of social mobilityThe combination of cellphone culture and social networking is bringing about a revolution in the way we communicate

12 the big picture_It’s good to talkBusinesses that offer access to cellphones are thriving in Africa

14 bulletin_News in focus: innovation in Asian banking; how Virgin Media is exploiting the power of the SIM card; an mHealth initiative to help new mothers in Ghana

18 society_African adventures in technologyThe introduction of digital technology is having life-changing effects across Africa. We report on how a continent got connected

24 solutions_NFC is just the ticketMobile ticketing for transportation is on the verge of breaking into the mainstream – but what factors are holding it back?

28 trenDs_The biometric evolutionWindows 7 features the first integrated approach to biometric identification and security

30 global snapshot_Significant facts and figures from around the digital world

32 innovation_Securing the futureDr Taher Elgamal, the inventor of SSL, on the current challenges facing digital security specialists

36 in brief_News updates and success stories

38 column_Identity testsGuy Clapperton on the challenge of managing your digital identities

guy clapperton

Tamsin has been writing for 18 years, specialising in computing and other high-tech areas. She has frequently worked with Microsoft on both magazines and PR.

contributorsDavey Winder

tamsin oxford

�

Contents

A prolific business and IT journalist, Guy is the author of the book This is Social Media: Tweet, Blog, Link and Post Your Way to Business Success, published in October 2009.

www.gemalto.com

A freelance technology journalist for nearly 20 years, Davey won the 2008 Information Security Journalist of the Year award. He is Contributing Editor of PC Pro magazine.

38 “It’s vital that companies respect the digital identities of their customers”Guy Clapperton

24

12

The Review is produced for Gemalto by Wardour, Walmar House, 296 Regent Street, London W1B 3AW, UK Telephone: +44 (0)20 7016 2555Website: www.wardour.co.uk

eDitor Tim Turnerconsulting eDitor Davey WinderDesign Director Ben BarrettDesigners Jeff Cochrane, Corey JacksonartWorker Mark Castro-Garcíapicture eDitor Johanna Wardpublisher Mick HurrellproDuction manager John Faulkner

your award-winning magazineThe Review was named Best business-

to-business title at the APA International Customer Publishing Awards in

November 2009. The prestigious awards recognize excellence

in customer publishingworldwide.

14

�

industry update

The Review

Digital digestE

VEN

TS C

ALE

ND

AR

Gemalto regularly participates in trade shows, seminars and events around the world. Here’s a list of those taking place over the next few months:

Date

21-24 Feb 2010

22-24 Feb 2010

1-3 Mar 2010

1-4 Mar 2010

1-5 Mar 2010

23-25 Mar 2010

13-15 Apr 2010

20-22 Apr 2010

18-20 May 2010

15-18 Jun 2010

22-23 Jun 2010

event

IBM Pulse 2010

Smart Card Alliance (SCA)Payment Summit

International Security National Resilience

HIMSS

RSA Conference

CTIA Wireless Conference

7th Security Printing Conference

WIMA2010

SCA Conference

M2M Magazine Conference

ACT Canada

location

Las Vegas, USA

Salt Lake City,USA

Abu Dhabi, UAE

Atlanta, USA

San Francisco, USA

Las Vegas, USA

Berlin, Germany

Monte Carlo, Monaco

Scottsdale, USA

Chicago, USA

Niagara Falls, Canada

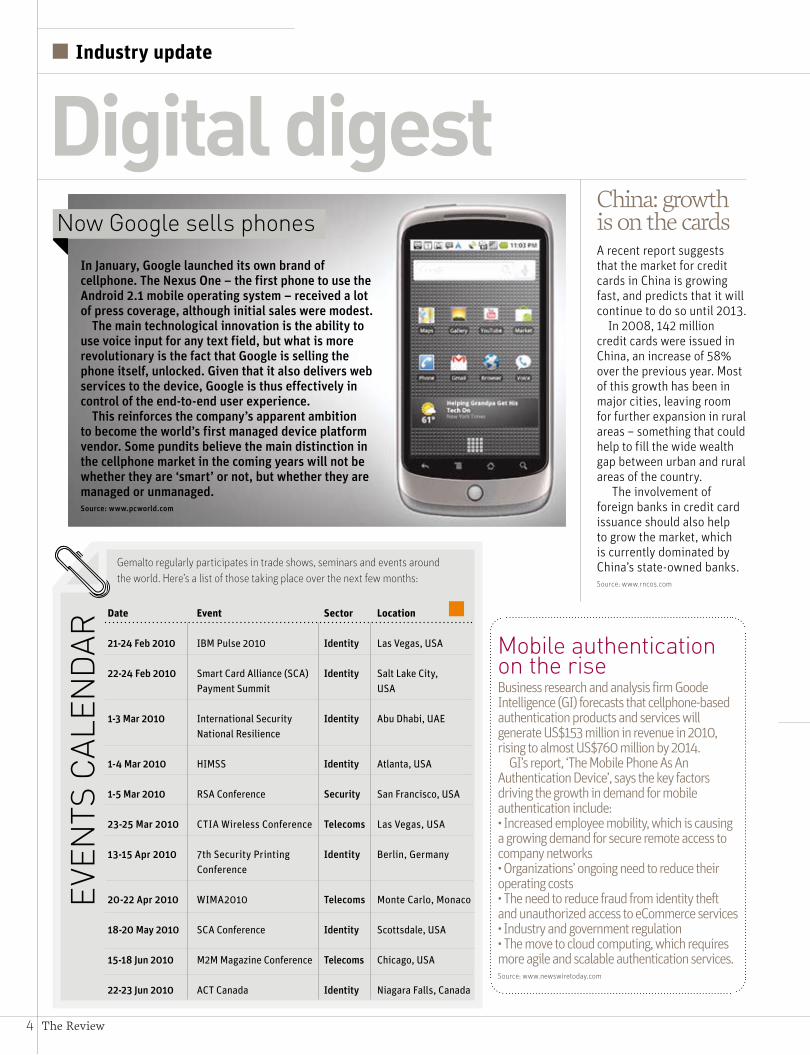

In January, Google launched its own brand of cellphone. The Nexus One – the first phone to use the Android 2.1 mobile operating system – received a lot of press coverage, although initial sales were modest.

The main technological innovation is the ability to use voice input for any text field, but what is more revolutionary is the fact that Google is selling the phone itself, unlocked. Given that it also delivers web services to the device, Google is thus effectively in control of the end-to-end user experience.

This reinforces the company’s apparent ambition to become the world’s first managed device platform vendor. Some pundits believe the main distinction in the cellphone market in the coming years will not be whether they are ‘smart’ or not, but whether they are managed or unmanaged.Source: www.pcworld.com

Now Google sells phones

Mobile authenticationon the riseBusiness research and analysis firm Goode Intelligence (GI) forecasts that cellphone-based authentication products and services will generate US$153 million in revenue in 2010, rising to almost US$760 million by 2014.

GI’s report, ‘The Mobile Phone As An Authentication Device’, says the key factors driving the growth in demand for mobile authentication include:• Increased employee mobility, which is causing a growing demand for secure remote access to company networks• Organizations’ ongoing need to reduce their operating costs• The need to reduce fraud from identity theft and unauthorized access to eCommerce services• Industry and government regulation• The move to cloud computing, which requires more agile and scalable authentication services.Source: www.newswiretoday.com

China: growth is on the cardsA recent report suggests that the market for credit cards in China is growing fast, and predicts that it will continue to do so until 2013.

In 2008, 142 million credit cards were issued in China, an increase of 58% over the previous year. Most of this growth has been in major cities, leaving room for further expansion in rural areas – something that could help to fill the wide wealth gap between urban and rural areas of the country.

The involvement of foreign banks in credit card issuance should also help to grow the market, which is currently dominated by China’s state-owned banks.Source: www.rncos.com

sector

Identity

Identity

Identity

Identity

Security

Telecoms

Identity

Telecoms

Identity

Telecoms

Identity

www.gemalto.com �

continues >by ThE NuMbERS

450 millionThere were more than 450 million mobile Internet users worldwide in 2009, and that number is expected to more than double by the end of 2013. Market intelligence firm IDC predicts that the number of mobile devices accessing the Internet will pass the one billion mark in that time.Source: www.cellular-news.com

1.7 billionThe number of people in Africa, Latin America and Asia who don’t have a bank account but do have a cellphone is set to grow from 1 billion today to 1.7 billion by 2012. A report from think tank CGAP says that branchless banking, mainly using cellphones, will grow in most developing countries over the next 10 years, but that investment – both public and private – is vital if the potential of mobile banking to bring financial services to the world’s poor is to be fully realized.Source: www.finextra.com

4-5 billionThe mobile money market in western Europe is set to grow to between 4 and 5 billion Euros by 2013, according to a forecast by Frost & Sullivan. The report notes that, until near field communication technology becomes cheaper and more widely available, it will be SMS-based services that drive growth in this area.Source: www.nearfieldcommunicationsworld.com

The EU’s cyber security agency, ENISA, has published a report called ‘Cloud Computing: Benefits, risks and recommendations for information security’.

ENISA started by asking businesses their main concerns about moving into the cloud. “The picture we got back from the survey was clear,” says Giles Hogben, editor of the report. “The business case for cloud computing is obvious, but the number one issue holding many people back is security: how can I know if it’s safe to trust the cloud provider with my data and,

in some cases, my entire business infrastructure?”

The report lists 35 key security risks of cloud computing, but also highlights the benefits. “The scale and flexibility of cloud computing gives the providers a security edge,” says Dr Udo Helmbrecht, ENISA’s Executive Director. “For example, providers can instantly call on extra defensive resources like filtering and re-routing. They can also roll out new security patches more efficiently and keep more comprehensive evidence for diagnostics.”Source: www.enisa.europa.eu

Pros and cons of the cloud

What’s new?M86 Security has published a report outlining the web and messaging-based threats it expects to be combating in the coming year. It highlights the increasing sophistication of traditional threats, but also foresees a number of new ones, including:• SEO poisoning – the use of Search Engine Optimization (SEO) techniques to drive users to web pages hosting malicious code, in order to ensure a steady supply of victims• International domain name abuse – last year, ICANN (the Internet Corporation for Assigned Names and Numbers) approved the use of non-Latin characters in domain

names. This may lead to a rise in phishing attacks, as cybercriminals can register phony websites with URLs that are all but indistinguishable from legitimate ones• Attacking APIs – social networks publish

their application programming interfaces (APIs) to encourage third-party developers to use them. This sharing comes with an

implicit level of trust, granting developers access to user profiles and data, so the threats that target them are likely to increase• Targeting URL shortening services – these services, which reduce the number of characters needed to parse a link, enable cybercriminals to spread spam and malware by hiding the true destination of links.Source: www.m86security.com

>

password denied

� The Review

Imag

es: C

orey

Jack

son

industry update

NFC

buy!

Mobile applications – the top 10

A recent report from Gartner lists what they believe will be the top 10 consumer mobile applications in 2012. The 10 applications are:

1.MOBILE MONEY

TRANSFER

2: LOCATION-BASED

SERVICES

3: MOBILE SEARCH

4: MOBILE BROWSING

5: MOBILE HEALTH

MONITORING

6: MOBILE PAYMENT

7: NEAR FIELD COMMUNICATION SERVICES

8: MOBILE ADVERTISING

9: MOBILE INSTANT MESSAGING

10: MOBILE MUSIC

MOBILE SOCIAL NETWORKING IS MENTIONED AS AN ‘APP TO WATCH’Source: ‘Gartner Dataquest Insight: The Top 10 Consumer Mobile Applications in 2012’, published October 2009

It’s been revealed that microblogging site Twitter has a list of 370 passwords it will automatically reject for being too obvious. The list includes generic terms, including numerical sequences such as ‘123456’; the unimaginative ‘password’; and names of popular cars and soccer teams.

The banned list also reveals the influence of science fiction on password choices. It includes ‘NCC1701’ (the registry number of the USS Enterprise in Star Trek) and ‘trustno1’ (Agent Mulder’s computer password in The X-Files).

Research published in 2009 by insurance company CPP in the UK identified other common – and thus easily guessed – passwords. One in five people use their pets’ names; one in eight choose memorable dates, such as birthdays; and one in 10 select their children’s names.Source: www.siliconindia.com

Mobile money comes to the US It looks as if 2010 will be the year that mobile money transfer takes off in the United States, with four systems set to launch soon.

“Mobile P2P transfers are more important than desktop transfers,” says John Schulte, a Senior Vice President at Mercantile Bank of Michigan. “People live through their phones, and this seems like a natural progression.”

However, there are diverging views about whether consumers will be prepared to pay for this.

Josh Peirez, MasterCard’s Group Executive of Innovative Platforms, says: “We see it as a revenue opportunity, both for us and for banks. When [people] see the convenience of mobile transfers, they’ll be willing to pay.” But Mercantile rejected the idea of charging for its service. “We didn’t want any barriers to adoption,” says Schulte. “P2P payments can, and should, be free.”Source: www.americanbanker.com

1474_p08-11_research.indd 8-9 2/2/10 16:34:11

The latest research into mobile social networking suggests that it is taking

off – but only among the younger generation. So what factors are preventing its wider adoption?

The importance of social mobility

author DAVEY WINDER

1474_p08-11_research.indd 8-9 2/2/10 16:34:11

Both cellphone use and social technology participation have been embraced by ‘Generation Next’, the first wave of consumers to be totally immersed in cellphone culture and to truly ‘get’ social networking and applications. Combine the two and you end up with a revolution in social computing.

According to the ‘Smartphone Future 2010–2014’ report from Portio Research, smartphones accounted for 13.8% of all handsets shipped during 2009. That’s set to increase to 24.9% by the end of 2014, with huge growth expectations for emerging markets such as India and Nigeria. This fast-expanding sector of the market is having a knock-on effect in terms of the adoption of social computing, with consumers eager to soak up the culture of social networking and media sharing via their high-end handsets.

Indeed, ComScore reckons that, of the 1.1 billion people who actively use the Internet around the globe, 738 million are regular users of social networking sites – about 67%. If you add in regular users of other social computing activities such as blogging, the figure rises to 76%. Some 42% of consumer online time is now spent using social networking services, but it is the online access methodology that is most interesting of all.

A recent survey of social networking users in Japan by Mobile Marketing Data Labs makes for fascinating reading. It reveals that 75.4% of Japanese consumers only ever access their social computing services using their cellphones. That compares with just 2% who said they only ever access these services via their PC. This is a trend that is being followed in the developing world.

More people in these regions have access to cellphones than they do to computers, and so they have been quick to embrace emerging social networking services.

In Europe, according to a recent Forrester report, ‘Why Mobile Could Reinvent Social Computing’ (October 2009), on average, 7% of 16-24-year-olds already access social networking sites from their cellphones, compared with 3% of all European online consumers. Similarly, a report from the JRC Institute for Prospective Technological Studies, ‘The Impact of Social Computing on the EU Information Society and Economy’, reveals that, by the end of 2008, 41% of Internet users in the EU were engaged in social computing activities, a figure that rose to 64% if you only looked at users under the age of 24.

According to the same Forrester report, “mobile phones have the potential to become the hub of Social Computing activities”. This is hardly surprising, given that both technologies exist to enhance communication. Just think of YouTube for an example of the perfect marriage between a video camera-equipped cellphone and online sharing culture. So successful has this marriage been that if YouTube were a country, it would be the third most populous in the world. Which just goes to show that all you need to kick-start a revolution is the right catalyst.

For years, people have dreamed about an ‘always on’ society in which a combination of Wi-Fi networks and broadband would deliver the Internet all day, no matter where you

research_ Mobile social networking

www.gemalto.com �

10 The Review

were. For most, the reality has been one of ‘not always on when you need it most’. As Generation Next is proving, however, that doesn’t have to be the case if you’re prepared to make the leap from static to mobile broadband.

The newly published ‘Mobile Broadband Study’ by CCS Insight suggests that mobile broadband in Europe will explode this year, with subscriber and revenue numbers set to double by 2011. Elsewhere, that explosion has already gone off. According to Alexei Poliakov, an analyst with a particular interest in the Japanese mobile market, 3G mobile broadband penetration in Japan has already reached 95% of the market, and 84.3% of mobile consumers are using 3G data plans.

The kind of 3G penetration found in Japan fosters the early development of

a localized social networking culture. Twitter has about half a million Japanese users and Facebook 1.5 million, but homegrown network Mixi has a staggering 17 million. These networks appeal to the gaming culture that is so strong in Japan – and they aren’t afraid to charge for premium content.

making it payThe big question on the lips of everyone in the business of mobile social computing is how you make it profitable. Indeed, some might even ask if it is possible to make it pay at all. As the Japanese experience reveals, however, monetization is not an issue when consumers are already used to paying for services and goods using cellphone-based billing systems.

The market certainly thinks there is money in mobile social networking. Technology research company Gartner recently reported that, despite having no revenues as such, Twitter had attracted a US$100 million investment based upon a valuation of US$1 billion. But even that

pales alongside Facebook, which, at the end of 2007, persuaded Microsoft to make an investment that valued the company at an incredible US$15 billion.

Both valuations were made possible by the massive growth in user numbers the companies have enjoyed in relatively short amounts of time. In one 12-month period, for example, Twitter grew from 3 million to 30 million users, while Facebook saw monthly mobile users grow from 20 million to 65 million in just eight months. Before the dotcom bubble burst, Internet investors used to chant a mantra of ‘content is king’, but today that could usefully be replaced by something along the lines of ‘where users flock, the money follows’.

The latest forecasts suggest that total mobile service revenues will exceed US$1 trillion in 2013, while voice revenues are falling. Mark Newman, Chief Research Officer at Informa Telecoms & Media, says: “The growth in data revenues is being spurred on by the rise in take-up of more advanced technologies and mobile broadband services, as well as new handset interfaces and mobile content strategies based on application stores rather than walled gardens.”

Indeed, research company Juniper has predicted that there will be nearly 20 billion mobile application downloads a year by 2014.

According to Forrester, pioneers which “have entered the market to create ‘made for mobile’ communities in emerging

territories… [are] more likely to succeed”. This is due to these markets’ lack of PC penetration and lower awareness of the big brands that more technologically advanced countries take for granted.

Not that we can ignore the big brands when it comes to the bottom line, for it is here that we find the most activity in terms of updating sites and applications to cater for different mobile devices and platforms. Having established that numbers matter when talking monetization, it’s little wonder that handset manufacturers have been quick to partner with the big brands. Forrester predicts that market differentiation will come from “the degree of handset integration with social networking brands” – something that Hutchison Whampoa subsidiary INQ, for example, is doing by positioning itself as a social mobile handset manufacturer.

“75.4% of Japanese consumers only ever access their social computing

services using their cellphones”

If the social computing world is to revolve around mobile handsets, operators need to position themselves as enablers of trust. Consumers already hand over a large amount of trust to their mobile network operator in terms of protecting voice data, text message data, contact information and so on. It’s only a small leap of faith to place their trust in securing their digital online identities to the same people.

A question of trustPh

otos

: isto

ck/A

lamy

www.gemalto.com 11

The network operators are also jumping on this particular bandwagon, not least because (as we’ve seen) mobile social computing users tend to be heavy communicators, and that’s good for business. For instance, Orange has its Social Life service, which aggregates access to multiple social networks. Last year, the company announced that the number of users accessing social networks via the Orange mobile Internet network had nearly doubled, to a little less than a million a month.

The only firms that seem to be finding it hard to carve out a significant niche in the mobile social space are the likes of Google, Microsoft and Yahoo!, which have large shares in the webmail and IM markets but have yet to find a way to convert this reach into a social audience and don’t have any social network revenues to speak of just yet. But that will surely follow in the years to come, in the form of data and communications revenues, advertising, premium content and, perhaps most importantly of all, increased user loyalty – especially in the notoriously fickle network operator and mobile handset market, where user churn is a perennial problem.

What’s driving adoption?But there is more to social computing than social networking. Media sharing has become big news for all the wrong reasons, with tabloid tales of illegal music and movie downloading now commonplace. Yet such sharing takes on a totally different perspective when it comes to social computing: think about it more in terms of an environment where you can share your family photo albums (Flickr) or snapshots (Twitter), or even your video clips (YouTube). Some 5% of all European cellphone owners upload photos to the web directly from their cellphones,

according to Forrester.Although well-known brands

such as Facebook, Flickr, Twitter and YouTube dominate media coverage of social computing, mobility is throwing up new services and applications that are totally original. Take geosocial networking. ABI Research has estimated that location-aware mobile social networking revenue alone will account for US$3.3 billion by 2013. Location Based Services (LBS) are now

being accessed by one in three smartphone users, according to web analytics company Compete, which also found that almost 75% of the LBS applications used on the iPhone are commercial products. It would seem that LBS is already realizing the potential for monetization of mobile social computing. Compete also found that LBS users will spend more on their network contracts than others, making them a hot property for carriers.

But to truly understand the impact of mobile social computing, you need to go beyond the web-based notion of social networking – beyond even the emerging geolocation services – to focus on the core competencies of the mobile handset: voice

communication and text messaging. Mix these with everything else we know about social computing and the true power of the medium starts to emerge, courtesy of services such as Nimbuzz and eBuddy, which let you discover where your friends are, what they’re doing and which of them are available to chat (via VoIP) or text (via multiple IM chat services) right this minute.

the next big thingDespite all the hyperbole and activity mobile social computing generates, there is plenty of work still to be done to maximize the value proposition. Network operators, handset manufacturers and online services need to become more open and less protectionist with regard to the technologies they promote.

The consumer contact base is currently spread over multiple phones, platforms and services, with limited interoperability. A move towards open standards would ensure that consumers get access to their social address book no matter which network they use, and would further encourage growth. Vodafone, for one, has been dipping its toes in the waters of interoperability with the 360 initiative, which allows non-Vodafone customers to access some of their social networks via their cellphones.

Ultimately, if the convergence of the social web and mobile communications continues at the current rate, then cellphones will indeed become the center of the social computing world.

For many people, the real innovation of bringing mobility into the social computing mix has been to engage the user in breaking news around the world as never before. No longer is news something to be experienced from a distance, as a spectator. Now consumers can be part of the story by capturing the event in real time, be that by delivering still images and video of the story itself, or by being part of the discussion surrounding it. News has become truly interactive for the first time, and only mobile social computing can currently deliver this immersive media experience: to shape as well as break the news.

Engaging mobile users

“Mobility is throwing up services and applications that are truly original”

67%of the 1.1bn global Internet users regularly visit social networking websites

research_ Mobile social networking

www.gemalto.com 1�

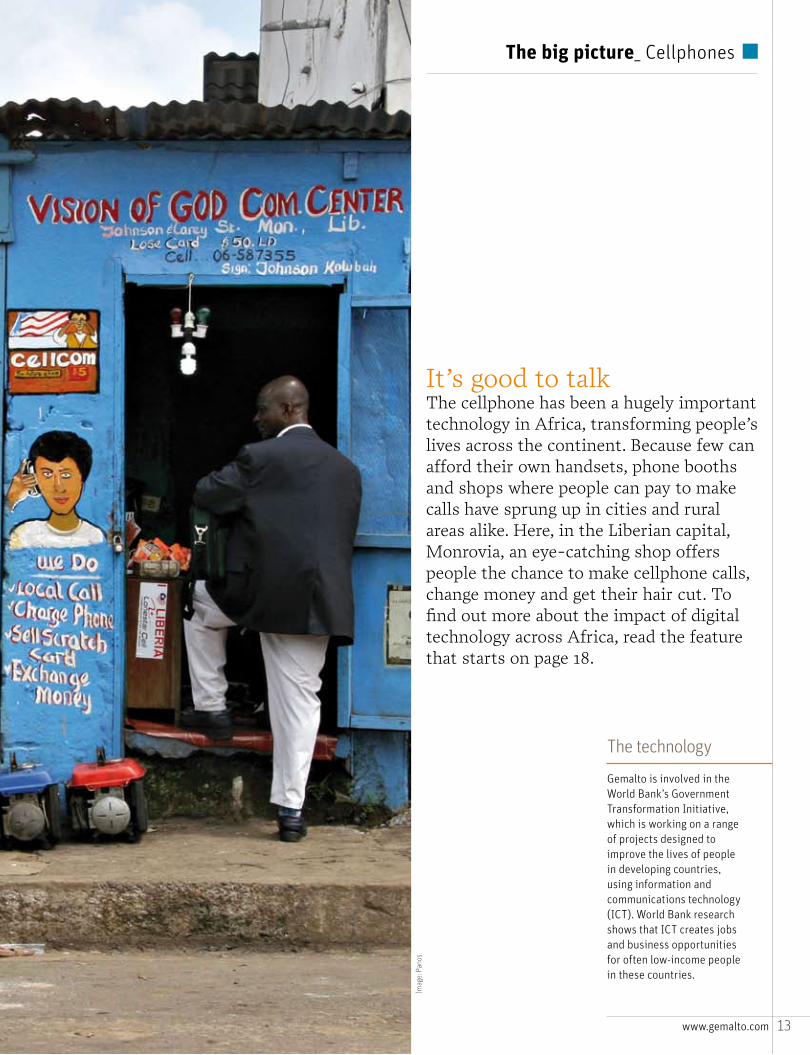

It’s good to talkThe cellphone has been a hugely important technology in Africa, transforming people’s lives across the continent. Because few can afford their own handsets, phone booths and shops where people can pay to make calls have sprung up in cities and rural areas alike. Here, in the Liberian capital, Monrovia, an eye-catching shop offers people the chance to make cellphone calls, change money and get their hair cut. To find out more about the impact of digital technology across Africa, read the feature that starts on page 18.

The technologyGemalto is involved in the World Bank’s Government Transformation Initiative, which is working on a range of projects designed to improve the lives of people in developing countries, using information and communications technology (ICT). World Bank research shows that ICT creates jobs and business opportunities for often low-income people in these countries.

the big picture_ Cellphones

Imag

e: Pa

nos

1�

news in focus

The Review

Bulletinthe 30-minute smart card

cards, and in the EZ-Link Card in Singapore. And the innovation doesn’t stop with the cards. In 2007, a national standard for smart card identification was launched in Singapore to ensure that a single device could read multiple cards. The Singapore Standard for Smart Card ID has put in place the infrastructure for next generation payments technology.

It was for this reason that financial services specialist Citibank Group chose Singapore to pilot its new faster card issuance program, working with the island’s metro system to get access to 1.1 million potential customers. By capturing the customer’s details digitally, Citi is able to bring a new level of speed to the market, producing cards in just 30 minutes.

In order to achieve this in such a short timeframe, additional training was needed and some changes were required to the bank’s credit and underwriting policies. But Mukesh Bubna, Regional Director, Cards Global Consumer Group (Asia Pacific) at Citi, says the biggest change needed was actually to the mindset of the management team: “It has to be a high priority of the leaders in the organisation.”

By issuing cards in the time that a typical customer spends travelling to work on the Mass Rapid Transport network, Citi saw an increase of 20-25% in card applications. The instant card programme is now being rolled out in Hong Kong, Japan, Korea, Malaysia and Thailand.

Bubna says: “Our customers have given us great feedback on these new ‘instant’ services. This is testimony that our approach is working and helps us to invest further in our strategy of ‘Instantaneity through innovation’.”

When it comes to the technology used in banking, a culture of innovation and a relative lack of legacy systems have enabled Asia to leapfrog the West in some areas. As early as 2003, the Immigration Department in Hong Kong began issuing next-generation

multi-application smart identity cards, and in 2007, Hong Kong launched the Octopus card. The contactless smart card system is now used by 95% of the population to pay for train fares, parking, fast food and groceries.

The same technology is also deployed in Japan in electronic cash

“By capturing customer details digitally, Citi can produce cards in just 30 minutes”

An instant card issuance pilot in Singapore is just one example of the culture of innovation that exists in Asian banking

1

Illus

tratio

ns: G

ary N

eill

www.gemalto.com 1�

continues >

A new contract agreement means that Virgin Media mobile customers can further exploit the SIM card’s potential

a powerful solution

“LinqUs will correctly configure each Virgin Media subscriber’s mobile handset”

Gemalto has secured a two-year exclusive agreement to supply Virgin Media with LinqUs (U)SIM cards and its hosted Device Management solution. The new and existing cards allow Virgin Media’s mobile customers to securely access and enjoy a wide range of value-added services, while the inclusion of the device management solution will automatically configure customers’ handsets for them.

In 2006, Virgin Media started using 64K Java-based cards, and this latest move to Gemalto’s state-of-the-art LinqUs (U)SIM cards will further enable Virgin Media to address its customers directly and help them access the services it offers. It will therefore be able to offer its customers a richer user experience and build a closer relationship with them.

For these and future services, Gemalto will ensure that the LinqUs Device Management solution correctly configures each Virgin Media subscriber’s mobile handset. Messages that identify the handset make and model are automatically exchanged between the card and the platform, which then automatically downloads the correct service settings to the mobile handset, leaving the customer to accept the update when prompted to do so. Once this process has been completed, customers can access Virgin Media’s web portal and other services without having to enter any settings on their phone manually.

With more than three million customers, Virgin Media is Europe’s largest Mobile Virtual Network Operator. The new contract extends an unbroken 10-year relationship between

2

Virgin Media and Gemalto. Indeed, Gemalto has supplied every SIM card used by Virgin Media subscribers.

“Gemalto has been our partner since our mobile service launched in 1999,” says Jonathan Kini, Director of Mobile at Virgin Media. “This extension to our agreement enables us to continue developing a wide range of future services for our customers, using the ever-increasing power and security inside the SIM card.”

>

1� The Review

news in focus

mothers get the message

in ghanaAn innovative scheme in

Ghana uses cellphones to improve the quantity and

quality of care for expectant mothers and newborn babies

3

One effect of the spread of cellphones in the developing world is that their use in mobile health initiatives has become increasingly popular.

In West Africa, for example, the Ghanaian government, in partnership with the Grameen Foundation (a non-profit organization that funds access to microfinance and technology for people living in poverty), is planning to use cellphones to increase the quantity and quality of antenatal and neonatal care in rural areas of the country.

The two-and-a-half-year Mobile Technology for Community Health (MoTeCH) scheme will develop a suite of services, delivered over basic cellphones, that provide relevant health information to pregnant women and encourage them to seek antenatal care from local facilities. At the same time, MoTeCH will help community health workers to identify women and newborn babies in their area who are in need of healthcare services, and automate the process of tracking patients who have received care.

Pregnant women will register by providing their phone number, the area in which they live, their estimated due date and their language preference. They will then begin to receive SMS and/or voice messages that provide information about their

pregnancy (milestones in fetal development, for example), the location of their nearest health center, and specific treatments that they should receive during their pregnancy, such as tetanus vaccinations.

Once her child is born, the mother will continue to receive messages and information about essential vaccinations for her child and how to manage critical childhood illnesses. The system will also include a facility that enables mothers to send health-related questions via SMS and receive responses by the same medium.

There will also be specific tools for community health workers, who will be able to enter data on patients into a national patient register using their cellphones. This will make daily record-keeping simpler for them, as well as enabling the Ghana Health Service to track the delivery of antenatal services and send timely and important messages to both health workers and patients.

MoTeCH, which is funded by a grant from the Bill & Melinda Gates Foundation, is a collaboration between Columbia University’s Mailman School of Public Health and the Ghana Health Service. All the parties involved hope that the end result will be a fall in infant mortality and disease across the country.

“All involved hope that the result will be a fall in infant mortality and disease across the country”

17

We hope you enjoy this issue of The Review. To help us make it even better, please take a few minutes to fill in our reader survey, which you can find at http://review.gemalto.com

You can also subscribe to the magazine at the same location. Subscriptions are free and we deliver the magazine directly to you. The first 75 people to subscribe using the online form will receive a YuuWaa – the new digital storage solution from Gemalto, with 8GB of online storage and 2GB of flash drive storage, as well as a flash drive backup.

Tell us what you think about the magazine – and subscribe for free Revıewthe

Don’t forget to tick the relevant boxes on the survey if you would like to take out a free subscription to The Review and/or our regular e-Newsletter. If you hurry, you could receive a free YuuWaa – the handy new digital storage solution from Gemalto.

http://review.gemalto.com

18 The Review

In the developing world, the application of digital technology can have life-changing effects. The Review reports on just a few of the many innovative schemes that are helping to improve people’s lives in sub-Saharan Africa

author SAMUEL MUNGADzEphotography FREDERIC COURBET

African adventures in technology

If you’re a kid in Paris or Tokyo, you’re probably surrounded by digital gadgets that make you look cool. And you probably don’t connect them with doing good.

It’s a different story if you’re in Nairobi or Accra. Across sub-Saharan Africa, the spread of digital technology has largely depended on its perceived benefits in solving some of society’s most pressing problems: education, healthcare, governance and sustainable rural development. As a result, Africa is making remarkable advances, particularly in areas that benefit human well-being.

Nkosinathi Baleni, Africa Editor at the Centre for African Journalists in Johannesburg, South Africa, says: “Digital technology has changed the way of life here. It’s no longer just for the rich and famous, but a necessity for development.

“For us in Africa, technology will go a long way in terms of meeting our goals, especially in the health sector,” he continues. “More than 80% of information technology decision-makers within the healthcare industry see mobile technologies as being more important to their organizations today than in 2008.”

a climate for investmentIn order to achieve these advances, investment is needed. Etienne Sinatambou, Deputy Speaker of the Parliament in Mauritius, says that it is up to African governments to provide a favorable investment environment for the information and communications technology (ICT) sector.

Sinatambou, the former ICT minister on the island, boasts that his country has the continent’s most investor-friendly regulations. As a result, he says, “Mauritius is now in the top three in Africa for most of the ratings on ICT, such as the ITU [International Telecommunication Union] report and the UN eGovernance report.”

Academic David Jingura, of the Global Solutions Centre based in Nairobi, Kenya, points out that alongside

its other benefits, technology can drive economic growth. “Technology has created an environment that stimulates economic activity, which translates directly into economic development,” he says. “The growth of SMEs and cooperatives will be stimulated further by the adoption of comprehensive technology policies. This will allow them to gain access to the global village, enabling them to trade their products and services on the world market.”

More broadly, as we reported in the Autumn 2009 edition of The Review, the expansion of the IT and IT-enabled services (ITES) sectors can have dramatic effects on employment prospects in developing countries, and thus on the wider economy. Experiences in India and the Philippines show that each new job created in IT and ITES results in the creation of two to four further positions in other sectors.

mobile moneyIn 2007, addressing the Connect Africa summit, Rwandan President Paul Kagame said: “In just 10 years, what was once an object of luxury and privilege, the mobile phone, has become a basic necessity in urban and rural Africa.”

Three years on, the cellphone continues to be the most important single tool that is spreading technology across sub-Saharan Africa. More people in Africa own cellphones than have bank accounts, and it is against this backdrop that leading telecoms operators across the continent are now providing mobile banking solutions. As a result, the financial services sector in Africa has been transformed, with mobile money providing a potential stepping stone to formal financial services for millions of people who lack access to savings accounts, credit and insurance.

Many households in Africa rely on remittances from family members living in other, economically stronger, countries. According to the World Bank, remittances to sub-Saharan Africa accounted for just 6.2% of the

1� www.gemalto.com

“In 10 short years, what was once an object of luxury and privilege, the mobile phone, has become a basic necessity in Africa”Paul Kagame, President of Rwanda, speaking in 2007

society_ Africa

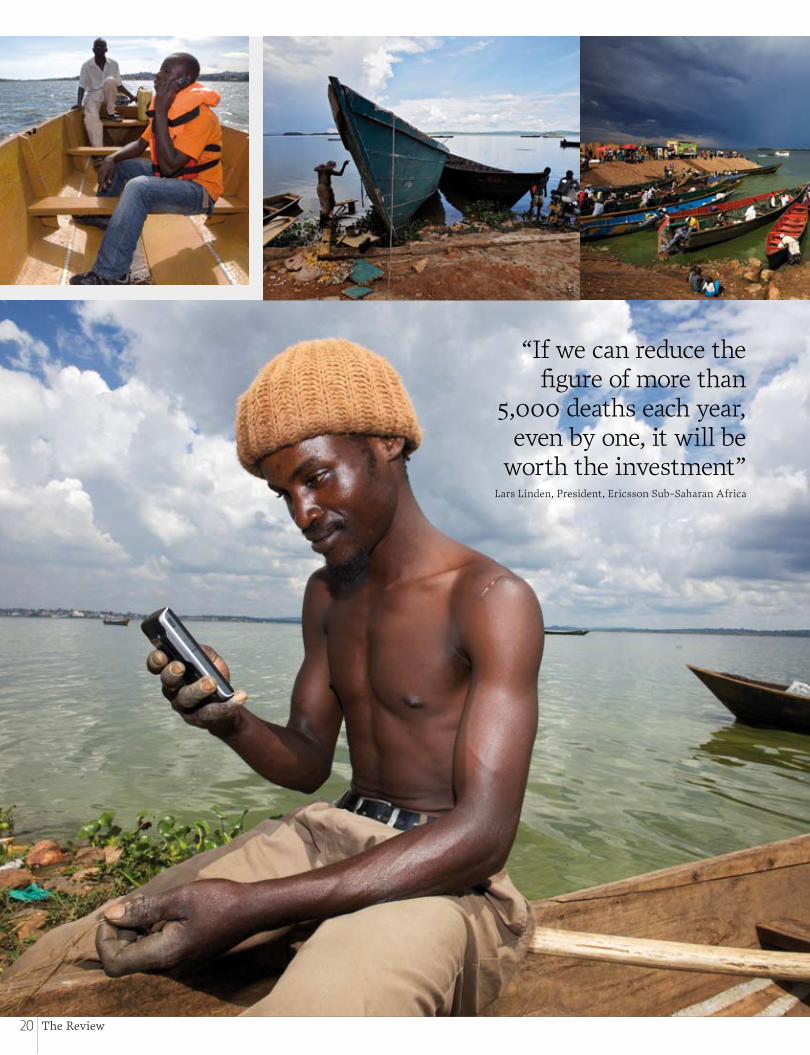

The pictures accompanying this article were taken in December 2009 by Frederic Courbet near Kampala in Uganda, on the shores of Lake Victoria, where the fishermen use cellphones to keep in touch with everything from the price of fish to the weather forecast (see p21). Courbet works for Panos, whose photographers document issues and geographical areas that are under-reported, misrepresented or ignored. Half the agency’s profits are given to the Panos Institute to further its work on issues including globalization, the environment, HIV/AIDS and conflict.

�0 The Review

“If we can reduce the figure of more than

5,000 deaths each year, even by one, it will be

worth the investment”Lars Linden, President, Ericsson Sub-Saharan Africa

�1 www.gemalto.com

US$338 billion of global remittances in 2008 – but that still equates to US$21 billion.

Kenya has taken the lead in mobile banking solutions through the M-Pesa service, launched in 2007 by Safaricom (the ‘M’ stands for ‘mobile’, while ‘pesa’ is the Swahili word for money). With M-Pesa, seven million Kenyans are now using their cellphones to pay bills and make payments for goods and services; send and receive money; withdraw cash; top up airtime accounts; and manage their bank accounts. The service gives customers security and flexibility, reducing the need to carry cash and ensuring that payments between friends and relatives remain secure. A password is needed for each transaction and the service is protected by a state-of-the-art security application provided by Microsoft.

According to a recent study, the incomes of households using M-Pesa in Kenya have increased by between 5% and 30% since they started using it. And although M-Pesa accounts don’t pay interest (for regulatory reasons), some people use the service as a savings account. Having even a small cushion of savings to fall back on allows people to deal with unexpected expenses, such as medical treatment, without having to sell a cow or take a child out of school. Many have come to realize that mobile banking is safer than storing wealth in the form of cattle (which can become diseased and die) or gold (which can be stolen), in neighborhood savings schemes (which may be fraudulent) or by stuffing banknotes into a mattress.

no account neededThe lack of widespread technological infrastructure has led to other innovations in the banking sector, too. For

example, South African bank Absa has won several international awards for its CashSend service, which allows customers to transfer cash from their own account to anyone in the country, even if they don’t have a bank card or account. The sender uses Internet or mobile banking or an Absa ATM to create a six-digit access code, which they provide to the recipient. Once the transaction has been confirmed, the CashSend system will send a unique 10-digit PIN to the recipient’s cellphone. They simply enter this PIN into any Absa ATM to instantly receive the transferred cash.

A different approach to money transfer services is typified by the Tembo Card offered by CRDB Bank in Tanzania, which is designed to take the place of both cash and checks. It consists of a plastic card embedded with a microchip that can be programmed to facilitate different functions. A Tembo Card can operate as a credit or debit card or as an e-wallet, and users (who don’t need to have an account with CRDB) can top it up at ATMs, in the bank’s branches or at point-of-sale devices in shops. Using an electronic banking system in this way makes payments faster, safer and cheaper, helping to eliminate fraud and corruption.

the small screenAnother of the key drivers of Africa’s technological revolution is mobile Internet connectivity. Across the continent, even in relatively developed South Africa, fixed broadband Internet is difficult to access, expensive and unreliable. However, the number of cellphone subscribers in Africa overtook the number using fixed-line telephony as long ago as 2001, and mobile penetration across the continent ranges from

society_ Africa

Telecoms giants zain and Ericsson have joined together in East Africa in an initiative that is being coordinated by the GSM Association. This partnership has brought development across the Lake Victoria region by providing increased mobile network coverage to the countries that border the lake – Kenya, Uganda and Tanzania – and launching a safety and security initiative that will benefit the fishermen who rely on the lake for their livelihood.

The coverage of Lake Victoria allows both voice and SMS communication. This has been touted as a catalyst for the economic and social development of the lakeside communities, and could potentially reduce the number of fishing-related deaths by providing timely warnings of the approach of storms, which can arrive rapidly out on the water and have devastating effects. zain has developed value-added services that will enable fishermen on the lake to access critical information such as fish and commodity prices, and to receive weather and safety alerts. The expanded network will also make it possible to collect data on daily catch from the more than 1,400 Beach Management Units on the lake’s shore.

Lars Linden, President of Ericsson Sub-Saharan Africa, says: “Mobile communications play an important role in helping communities to develop sustainably. Building out the mobile networks in this region is a key business interest for Ericsson, but it will also play a vital role in delivering increased safety and security, as well as improved economic viability and livelihoods.

“If we can reduce the figure of more than 5,000 deaths each year, even by one, it will be worth the investment,” he concludes.

Storm warnings on Lake Victoria

��

30% to a massive 84% in South Africa (as reported in the Africa Mobile Factbook 2008). Indeed, the total mobile subscriber base in Africa is predicted to reach 561 million (53.5%) by 2012.

Now some phone companies are taking the opportunity to offer mobile data services and Internet access. Africa is a GSM-based continent, and GPRS (General Packet Radio Service) and HSDPA (High-Speed Downlink Packet Access, sometimes called 3.5G) are the core data platforms. MTN, a South African telecoms company with 28 million subscribers across 10 African countries, is already widely offering data services.

Most phones sold in Africa have GPRS capabilities, making data access a core functionality available to cellphone users. MTN is now using HSDPA to help Internet cafés to set up in townships where fixed Internet access is just a dream.

Meanwhile, the BBC has reported that 61% of its international WAP (Wireless Application Protocol) users are in Nigeria and 19% in South Africa. Of course, this partly reflects the fact that WAP (a simplified web browser technology designed to work on cellphones) has never really taken off in Europe, but it does show that it is a viable technology in an emerging

economy where Internet access is primarily via cellphones. Thus, in Africa, digital content providers must focus on mobile delivery if they want to access anyone other than an elite handful who live in select areas and can afford to pay for fixed broadband.

So, despite its enormous economic and other problems, Africa is becoming a

showcase for the potential of the mobile Internet. This has quickly shifted from being a status symbol to an instrument for promoting economic growth.

Jose Henriques, Executive Head of Internet Services at pan-African mobile telecoms company Vodacom, says: “Cellphones are the advance guard for mobile broadband networks, and at the same time they are promoting economic benefits and providing a basic tool of education.”

This is still a fledgling sector: only 3.3% of Africans have access to the Internet via their cellphones. Nevertheless, the market continues to grow dramatically; the number of pages viewed increased by 422% between April 2008 and April 2009.

Henriques explains that countries such as Zambia, Kenya, Rwanda and Nigeria in particular are working hard to extend mobile penetration, especially in rural areas. But he warns that companies will only succeed if they provide a good user experience: “They must ensure that the Internet can be accessed from any phone, with cost-effective rates, and that users can view big websites properly on a small screen.”

the importance of identityAnother digital technology seeing steady growth in Africa is the ePassport. In 2008, Nigeria, South Africa and Senegal were joined by Côte d’Ivoire in adopting this technology. The West African nation has more than one million ordinary passports in use, and planned to update them all by the end of 2009, as well as incorporating the electronic capability in all new travel documents.

In Nigeria, the ePassport has been hailed as helping to curb fraud involving travel documents, while the South African Department of Home Affairs began rolling out

The Review

“The GSMA estimates that there are 485 million cellphone users worldwide who don’t have access to the electricity grid”

SMS technology is being used in South Africa to solve one of the most pressing problems facing the healthcare sector: ensuring people get the treatment they need.

Healthcare has advanced remarkably in recent years, especially in the area of HIV/AIDS, but the delivery of Anti-Retroviral Therapy (ART) has been problematic on the continent where the majority of those affected live.

Now Right to Care, a non-profit, non-governmental organization that provides access to ART for patients who can’t afford it, has embraced digital technology at the Themba Lethu Clinic at Helen Joseph Hospital in Johannesburg. Right to Care has led the use of Therapy Edge, a software tool specific to HIV disease

management. In 2007, in partnership with technology developers Praekelt Foundation, it launched TxtAlert, a service that sends SMS messages to remind patients of clinic visits and alert them of their laboratory results.

The initiative has been a huge success; missed appointments have dropped from 30% to 4% and lost-to-follow-ups (the proportion of new patients who fail to return) have fallen from 27% to 4%. More than 100,000 HIV patients now use TxtAlert.

The next phase of the project will monitor treatment adherence. A pilot project was due to begin in January, with 100 patients using an electronic medication monitoring device that tracks the opening and closing of medicine bottles.

HIV patients get the message

61% of international users of the BBC’s WAP service are in Nigeria

�� www.gemalto.com

society_ Africa

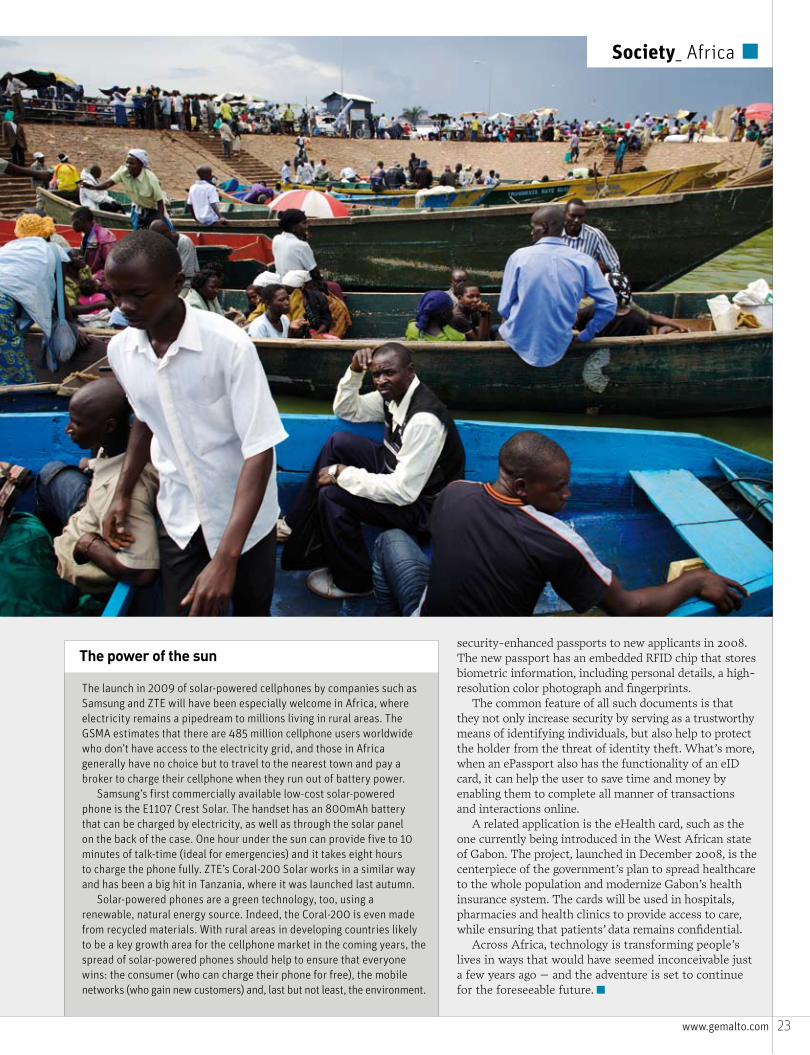

security-enhanced passports to new applicants in 2008. The new passport has an embedded RFID chip that stores biometric information, including personal details, a high-resolution color photograph and fingerprints.

The common feature of all such documents is that they not only increase security by serving as a trustworthy means of identifying individuals, but also help to protect the holder from the threat of identity theft. What’s more, when an ePassport also has the functionality of an eID card, it can help the user to save time and money by enabling them to complete all manner of transactions and interactions online.

A related application is the eHealth card, such as the one currently being introduced in the West African state of Gabon. The project, launched in December 2008, is the centerpiece of the government’s plan to spread healthcare to the whole population and modernize Gabon’s health insurance system. The cards will be used in hospitals, pharmacies and health clinics to provide access to care, while ensuring that patients’ data remains confidential.

Across Africa, technology is transforming people’s lives in ways that would have seemed inconceivable just a few years ago – and the adventure is set to continue for the foreseeable future.

The launch in 2009 of solar-powered cellphones by companies such as Samsung and zTE will have been especially welcome in Africa, where electricity remains a pipedream to millions living in rural areas. The GSMA estimates that there are 485 million cellphone users worldwide who don’t have access to the electricity grid, and those in Africa generally have no choice but to travel to the nearest town and pay a broker to charge their cellphone when they run out of battery power.

Samsung’s first commercially available low-cost solar-powered phone is the E1107 Crest Solar. The handset has an 800mAh battery that can be charged by electricity, as well as through the solar panel on the back of the case. One hour under the sun can provide five to 10 minutes of talk-time (ideal for emergencies) and it takes eight hours to charge the phone fully. zTE’s Coral-200 Solar works in a similar way and has been a big hit in Tanzania, where it was launched last autumn.

Solar-powered phones are a green technology, too, using a renewable, natural energy source. Indeed, the Coral-200 is even made from recycled materials. With rural areas in developing countries likely to be a key growth area for the cellphone market in the coming years, the spread of solar-powered phones should help to ensure that everyone wins: the consumer (who can charge their phone for free), the mobile networks (who gain new customers) and, last but not least, the environment.

The power of the sun

�� The Review

You want to catch a bus to the city center. So, before leaving home, you visit the public transit company’s website and buy a ticket, which is automatically credited to your cellphone. Then, when the bus arrives, you simply board it, wave your phone in front of a reader and you’re off.

It’s an appealing vision – and the good news is that the technology that makes it possible, based on cellphones using near field communication (NFC), is on the verge of breaking into the mainstream. Several cities and conurbations are either introducing NFC-based ticketing trials or expanding existing ones, to test out the pros and cons of the technology and understand how consumers use it.

In spring 2010, for example, the French city of Nice will begin a pre-commercial test

involving 3,000 users. Volunteers will be able to use their cellphones to pay for tram and bus tickets, find information on routes and times and access other services relating to local museums and cultural events. The French government is providing seed funding for the project, which will see Nice become a reference city for further rollouts across the rest of France, where there have already been more than 20 trials during the past two years. The Nice initiative is being led by the city council, and other participants include bus and tram operator Veolia Transport, mobile operators Orange, SFR and Bouygues Telecom and the University of Nice Sophia Antipolis.

Meanwhile, Deutsche Bahn in Germany plans to extend its Touch&Travel pilot scheme, run in

The widespread use of NFC-based cellphones for mobile ticketing is just around the corner. The Review looks at the development of a technology that consumers are eager to adopt – and the factors holding it back

NFC is just the ticket

author CATH EVERETTillustration ARMY OF TROLLS

�� www.gemalto.com

conjunction with Telfónica O2 Germany, Vodafone and T-Mobile. The program, which began in February 2008, previously included about 2,500 passengers travelling around and between major cities such as Berlin, Hanover and Frankfurt. As of January, that figure rose by 3,000 with the addition of customers in the Ruhr area, and the service is expected to be launched commercially in 2011.

NFC-based schemes such as these all work in the same way. Customers download a software application onto their phone and can then use the wallet interface to buy tickets or top them up, either from the phone itself over a GSM mobile network or by accessing their service provider’s website. This means that they no longer need to wait in line to make a transaction, and they can also check their balance, view their transaction history and check routes and times from their phone at any time.

poised for growthThis is just the beginning, according to market analysts Jupiter Research. According to its report ‘Mobile Ticketing: Transport, Sport, Entertainment & Events 2008-2013’, the number of cellphone users buying and redeeming tickets in the major world markets in three years’ time

will be 410 million, compared with just 22 million at the end of 2008. Adoption is anticipated to be particularly strong in the Far East, where 16% of cellphone users will be using mobile ticketing services within three years.

Not all cellphones used for mobile ticketing will be NFC-based, however, as countries such as Japan and South Korea introduced alternative systems before NFC technology took off. For instance, Japan Railways East (JRE) launched its Mobile Suica system with telecommunications company NTT Docomo in January 2006. This is based on Sony’s FeliCa contactless RFID integrated circuit chip.

Mobile Suica is currently used by 1.5 million commuters in the Tokyo area, who board trains by waving their cellphones over sensors in turnstiles. Although NFC-based phones can be used by customers in exactly the same way, the underlying technology is slightly different.

the appeal of nfcNFC enables two compatible devices to communicate wirelessly if they are brought within four centimeters of each other, but, unlike FeliCa, it is based on international standards. The technology is also appealing to transportation and cellphone companies

16%of cellphone users in the Far East will be using mobile ticketing services within three years

solutions_ Mobile transport ticketing

�� The Review

because its more advanced functionality gives it the potential to support a broader range of revenue-generating value-added services such as loyalty schemes, mobile coupons and personalised discounting based on travel times (which helps to manage congestion).

Another attraction for operators is the system’s ability to cut costs. Sarah Clark, Editor of online publication Near Field Communications World, explains: “On average, the cost of issuing traditional tickets accounts for about 25% of the ticket price, and you need a huge infrastructure in place to manage it.”

Many major cities already have a contactless smart card based infrastructure in place that can support NFC-based cellphone use without any modification. In any case, the two technologies are considered to be complementary. Both are useful in reducing congestion in stations and cutting the number of costly ticket machines required, which take up valuable floor space.

NFC mobile ticketing has also proved highly popular with customers. According to a survey undertaken by Gemalto, which has been involved in about 25 pilot projects worldwide, 90% of users love its ease of use and convenience.

the handset issueHowever, despite the public appetite for NFC-based mobile ticketing, there are currently two

main barriers to its broader adoption.The first is the lack of widely available,

inexpensive NFC handsets. The Nokia 6216 already supports the NFC standard, and Malaysian manufacturer Fonelabs went into mass production with its US$120 X-Series NFC devices at the end of December 2009, with the expectation of selling two million units this year. However, there are few other commercial offerings on the market. This is due to a classic chicken-and-egg situation: manufacturers don’t want to commit resources until there is a clear volume market for NFC handsets, and such a market is unlikely to materialise until they do so.

However, interim fixes are available, in the form of MicroSD cards that can be inserted into existing phone slots and stickers that can be attached to the back of phones to upgrade them – although such solutions are, inevitably, not as elegant as devices with native NFC support, says Clark.

“These products do have potential, but they should be seen as bridging solutions and as a way to get NFC trials started,” she explains. “They’re not as good as functionality that is built into a phone from the outset. For example, users might have to orient their phone quite carefully to get it to work, rather than just wave and go.”

“ NFC’s functionality gives it the potential to support revenue-generating value-added services such as loyalty schemes and mobile coupons”

90%of people surveyed after taking part in pilot projects said that they loved the ease of use and convenience of mobile ticketing

�7 www.gemalto.com

French train operator SNCF, in conjunction with Gemalto, has built a working NFC mobile ticketing prototype as a key step towards launching a commercial service.

Ticketing experts SNCF Proximités Innovation and Technologies Pole, together with SNCF subsidiary RITMx, have already tested the system and will use it as the basis for a future pilot project. The go-ahead for full deployment is likely to be given when NFC cellphones and SIM cards start appearing on the market in volume, and when suitable business models are agreed with other participants in the Ulysse working group, which has helped to develop a standard framework for the introduction of the service. This group includes SNCF and its Keolis subsidiary; three other transport operators – RATP in Paris and the Ile-de-France, and Transdev and Veolia in Nice; and three mobile operators – Bouygues Telecom, Orange and SFR.

Joel Eppe, head of SNCF Proximités Innovation and Technologies Pole, says: “The number of participants means that business models are complicated. Everyone will have to revisit their aims before the service can be rolled out. If costs are too high for customers or service providers, it will act as a barrier to deployment.”

The working prototype, which was first demonstrated at the Cartes exhibition in Paris in November 2009, is intended to work with services provided by the other transportation operators and will enable customers

to purchase and top up different ticket options such as monthly passes or carnets. It will also enable them to check their balance, access travel news in real time, find the nearest station and purchase an hourly ticket via an interactive poster.

Over time, passengers are also expected to be able to use their NFC phones to pay for station parking spaces, access secure bike sheds and register to use free bicycles. The service will be targeted both at commuters and at occasional passengers, such as tourists, who don’t have access to contactless transit cards.

The offering is based on Gemalto’s Trusted Services Management capability. Passengers load the software onto the SIM card to create a personalised profile. It also provides a user interface in the shape of a personal wallet, which customers can use to buy and download tickets from the SNCF portal using any wireless network, after entering their credit card details into their cellphone.

“The launch of this service will reinforce SNCF’s image as a technologically innovative company,” concludes Eppe. “Beyond its practical applications, it will also encourage customer loyalty and improve the quality of service.”

“Over time, passengers are also expected to be able to use their NFC phones to pay for station parking spaces, access secure bike sheds and register to use free bicycles”

solutions_ Mobile transport ticketing

SNCF is on track in France

mutual benefitsThe second inhibitor to adoption relates to the difficulties participants in NFC mobile ticketing initiatives often encounter in devising suitable business models. Because transportation operators and cellphone providers are, in most instances, working together for the first time, it can be tricky to decide on mutually beneficial ways to share both the costs and the rewards.

“The challenge is getting agreement between the various types of companies involved,” Clark explains. “They all work in different ways and have varying business philosophies, so they see the world differently.”

Japan got round this issue because its initiative was driven and funded by one company, NTT Docomo, which subsequently invited other service providers to participate. An alternative is to turn to a trusted service provider to mediate and facilitate discussions or, as in the Nice model, to encourage government funding.

These obstacles are by no means insurmountable, as Clark concludes: “The trials should help participants to work out a clearer picture of acceptance levels and costs to help them build a business case, though one or two of the mobile operators could be about to break away and say they’ll do it themselves. Whatever happens, the early players will be looking at commercial launches in 2011.”

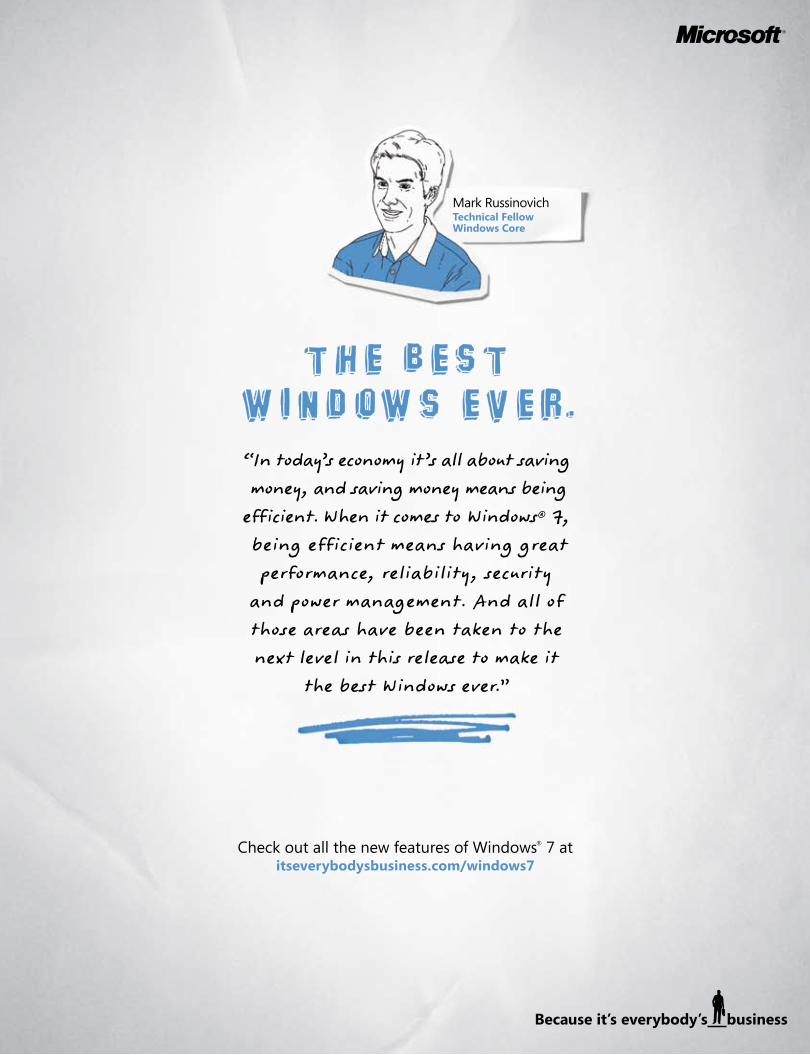

evolutionbi metricThe

Microsoft’s Windows Biometric Framework

represents the first integrated approach to

biometric identification and security

author TAMSIN OxFORd

The Review�8

Biometric technology uses an individual’s unique biological traits, such as fingerprints or facial characteristics, to determine identity. The most common form currently in use is fingerprint identification, with tens of millions of devices now shipping for PCs, laptops and peripherals.

However, until recently there wasn’t a consistent set of components upon which developers could build fingerprint biometric devices for the Windows® platform. They had to provide their own drivers, software development kits and applications, and this led to a wide variety of proprietary solutions that didn’t have common management platforms. Many devices had incompatibility issues with applications and were inconsistent in terms of reliability and quality. In a white paper published in December 2008, Microsoft also stated that “the differing nature of application stacks and driver models for biometric devices complicated servicing and maintaining these proprietary solutions”.

Windows innovationThe launch of Windows 7 in October 2009 saw Microsoft presenting a new solution that it believes will address these issues and take biometric identification and security to the next level: the Windows Biometric Framework (WBF). The

�� www.gemalto.com

trends_ Windows Biometric Framework

Microsoft Windows features such as BitLocker® Drive Encryption and DirectAccess can work in conjunction with Match-On-Card for powerful security solutions. DirectAccess offers secure mobile access to corporate networks and remote machine servicing, while BitLocker and BitLocker To Go™ help protect data on PCs and removable USB drives when the physical asset is lost or stolen.

Both work within the WSF and, alongside solutions such as Protiva .NET Bio, deliver multi-factor authentication. DirectAccess authenticates both the computer and the user, employing IPv6-over-IPsec to encrypt communications across the Internet. BitLocker and BitLocker To Go protect sensitive data from access by unauthorized users and can be set to demand passwords, a

smart card or domain user credentials to allow access.

Other Microsoft applications also contribute to strong authentication. Office 2007 uses document protection settings that enable password protection and encryption and, along with Outlook® 2007, offers the option of digital signatures. The latter places an encryption-based stamp on a macro or document, verifying that it originated from the signatory and hasn’t been altered. Internet Explorer® 8 includes features such as SmartScreen®, Cross Site Scripting Filter, Click-jacking prevention and Data Execution Prevention, adding yet more layers to the security protocols.

Finally, Encrypting File System in Windows Server® 2003 lets users encrypt files and directories stored on a disk.

Strong authentication with Microsoft

evolutiondowntime caused by users forgetting their PINs.

The WBF opens the market to strong authentication solutions such as ProtivaTM .NET Bio. Integrating biometrics with the Match-On-Card system (where fingerprint verification takes place on the card itself) offers enterprises a highly customizable security system with a choice of two- and three-factor authentication.

Continuing developments in biometrics and security offerings, such as WBF and Protiva, will ensure far better quality and ease of operation for both users and developers. Certainly the WBF offers enterprises and developers an additional, powerful layer of security that can be tailored to integrate with existing networks.

“We are monitoring trends in the industry and gathering feedback from our ecosystem partners to understand how we should evolve our support for biometrics in the future,” concludes Bossio. And with implementations in police forces, airports and government institutions highlighting its potential, the future of biometrics certainly looks positive.

WBF is designed to expose fingerprint readers and other biometric devices to higher-level applications in a uniform way, and offers a consistent user experience for discovering and launching fingerprint applications.

“The proliferation and increased popularity of fingerprint readers presented a great opportunity for Microsoft to invest in improving the user experience and the reliability of these devices,” says David Bossio, Lead Program Manager for Windows Security and Identity at Microsoft. “We saw that a large number of users, and the ecosystem, would benefit from a common platform for application developers who want to use fingerprint devices, while making it more convenient to log on to Windows.”

Windows 7 is Microsoft’s first operating system to offer integrated biometric support. The WBF supports fingerprint biometric devices through a set of components designed to improve the quality, reliability and consistency of the user experience. These include management components that let users and administrators configure biometric devices, either on a single computer or globally for a domain, and core platform components with driver interface definition and a client application programming interface (API).

“The WBF delivers an improved user experience, coupled with a common programming model for using fingerprint devices on Windows, independent of a specific hardware provider,” says Bossio. “The WBF and our investments in the Windows Smart Card Framework (WSF) enable users to make better use of the built-in fingerprint devices that are shipping on many laptops today.”

seamless securityThe out-of-the-box experience may well be optimized for the consumer, but it also enables multi-factor authentication for the enterprise by building on the foundation provided by the WBF and interoperability with the WSF.

“It is possible to use the WBF for [biometric PIN] implementations where the fingerprint match takes place on the smart card, or where the fingerprint template is stored on a smart card, [to authenticate the card holder as the rightful owner],” Bossio explains.

This responds neatly to the demand for security solutions that are interoperable, convenient and meet the requirements for multi-factor authentication. Users can opt to log in to the system with their fingerprint and smart card, or their fingerprint and a PIN. This offers flexibility within the security infrastructure, and may have the added advantage of limiting the

“The WBF offers enterprises and developers an additional, powerful level of security”

Imag

e shu

tterst

ock

�0

Global snapshotstatistics from the digital world

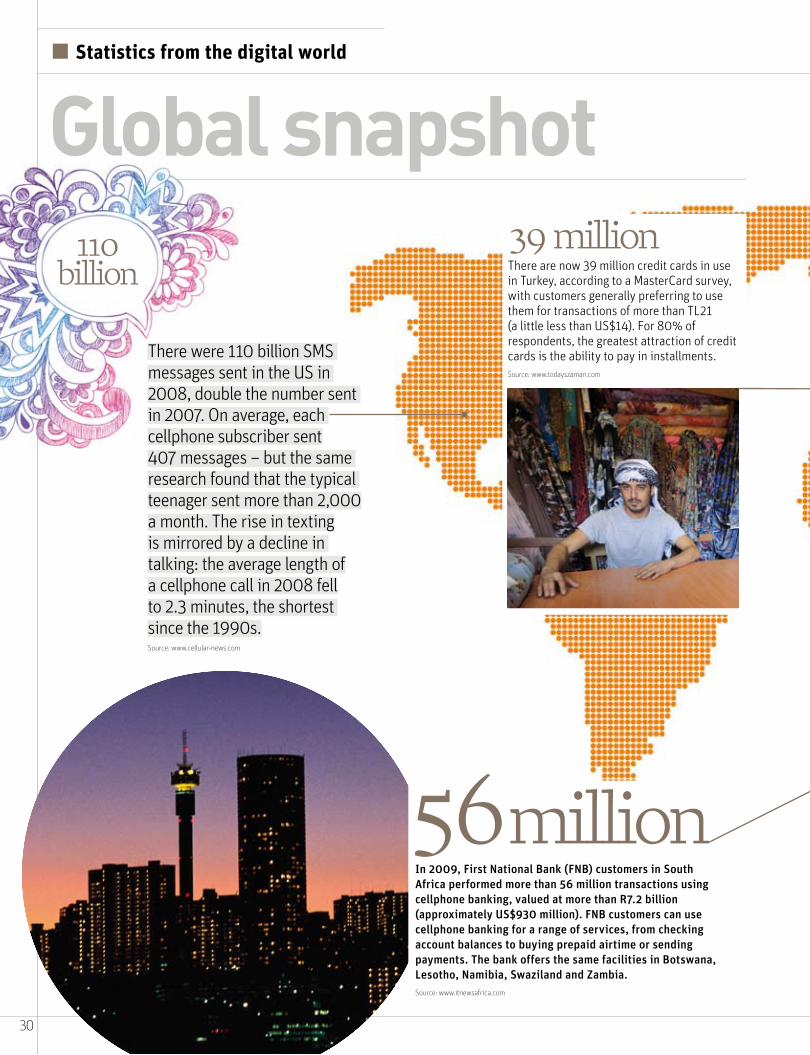

110 billion

There were 110 billion SMS messages sent in the US in 2008, double the number sent in 2007. On average, each cellphone subscriber sent 407 messages – but the same research found that the typical teenager sent more than 2,000 a month. The rise in texting is mirrored by a decline in talking: the average length of a cellphone call in 2008 fell to 2.3 minutes, the shortest since the 1990s.Source: www.cellular-news.com

39 millionThere are now 39 million credit cards in use in Turkey, according to a MasterCard survey, with customers generally preferring to use them for transactions of more than TL21 (a little less than US$14). For 80% of respondents, the greatest attraction of credit cards is the ability to pay in installments.Source: www.todayszaman.com

In 2009, First National Bank (FNB) customers in South Africa performed more than 56 million transactions using cellphone banking, valued at more than R7.2 billion (approximately US$930 million). FNB customers can use cellphone banking for a range of services, from checking account balances to buying prepaid airtime or sending payments. The bank offers the same facilities in Botswana, Lesotho, Namibia, Swaziland and Zambia.Source: www.itnewsafrica.com

56 million

�1 www.gemalto.com

4The Singaporean government is investing S$16 million (US$11.35 million) in subsidies to merchants to persuade them to install point- of-sale terminals that can accept contactless payments. The aim is to increase the installed base of contactless terminals from 5,000 to nearly 24,000 by 2011.Source: www.nearfieldcommunicationsworld.com

S$16 million

Four mobile network operators are collaborating on the development of NFC technology in Russia. VimpelCom, MegaFon, MTS and Moskovskaya Sotovaya Svyaz are working with Russia’s Infocommunication Union on proposals to introduce mass-market NFC services. The first pilot is scheduled to begin this summer.Source: www.nearfieldcommunicationsworld.com

In Australia, 1.5 million diabetics can now upload their blood glucose level to their cellphone. For $1 a day, sufferers can subscribe to the MyGlucoHealth wireless blood glucose meter. Each time they check their level, they can send the information from the meter to their cellphone, and both they and their doctor can then monitor their progress over the Internet.Source: www.theaustralian.com.au

At the end of October 2009, India had 488.4 million wireless connections, giving it the second largest number of cellphone users in the world, after China. India now has a teledensity (phone connections per 100 people) of 45%, though there is a marked disparity between urban areas, which have a teledensity of 97%, and rural ones, where the figure is 18%.Source: wirelessfederation.com

488.4m

1.5 million

The development of the Secure Socket Layer (SSL) – now superseded by the Transport Layer Security (TLS) protocols – has been pivotal in the development of the Internet as a commercial environment. Without SSL, eCommerce could not have developed, as it provided the all-important secure connection between a customer’s browser and the server of the business they wanted to buy from.

SSL inventor Dr Taher Elgamal, now Chief Security Officer at business software company Axway, Inc., is also the creator of the Elgamal Cryptosystem, the foundation for modern elliptic-curve ciphers, which is used in many commercial encryption products. In addition, he has developed numerous technologies and standards for data security and digital signature, including the cryptographic basis for the Digital Signature Standard. He also participated in the development of the SET (Secure Electronic Transaction) protocol that is used to secure credit card transactions.

Dr Elgamal was presented with a Lifetime Achievement Award in Information Security at the 2009 RSA Conference.

secure shoppingThe Review began by asking Dr Elgamal how the web has changed in terms of eCommerce transactions, compared to when

he was doing his pioneering work with SSL.“At the beginning of the eCommerce industry

in the mid-90s, we realized that the highest risk lay in the open nature of the Internet,” he says. “SSL was designed and implemented by the Netscape team [that he was part of], alongside several industry experts, to prevent unauthorized access to communications on the net.

“SSL was not in fact designed to solve all security issues, but focused on the communication aspect. In essence, eCommerce would be probably a very different industry if we were starting now.

“There is no reason to change the thinking about how SSL is designed, even today,” he continues. “But, knowing what we know today, we would have implemented SSL as a step towards achieving secure electronic transactions, rather than believing that SSL is the only measure to use.”