Embed Size (px)

Citation preview

EUROPE’S(LOW+CARBON(TRANSITION:(UNDERSTANDING(THE(CHALLENGES(AND(OPPORTUNITIES(FOR(THE(CHEMICAL(SECTOR(

Spring(2014(

Contents(

▪ MoEvaEon(of(the(project(

▪ Competitiveness of the European chemical industry!

▪ What could be done to reduce emissions while maintaining or increasing competitiveness?!

▪ Implications and next steps!

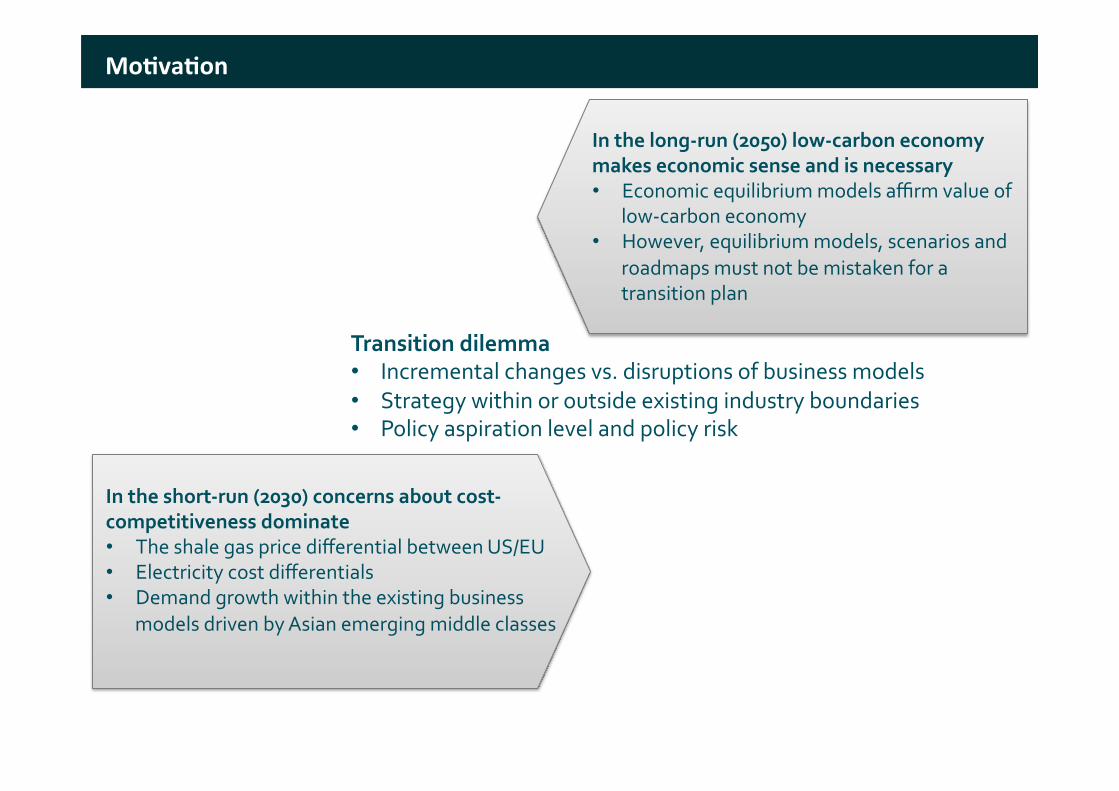

MoEvaEon(

In#the#long*run#(2050)#low*carbon#economy#makes#economic#sense#and#is#necessary#• Economic'equilibrium'models'affirm'value'of'

low5carbon'economy''• However,'equilibrium'models,'scenarios'and'

roadmaps'must'not'be'mistaken'for'a'transition'plan'

In#the#short*run#(2030)#concerns#ab0ut#cost*competitiveness#dominate#• The'shale'gas'price'differential'between'US/EU'• Electricity'cost'differentials'• Demand'growth'within'the'existing'business'

models'driven'by'Asian'emerging'middle'classes'

Transition#dilemma#• Incremental'changes'vs.'disruptions'of'business'models'• Strategy'within'or'outside'existing'industry'boundaries'• Policy'aspiration'level'and'policy'risk''

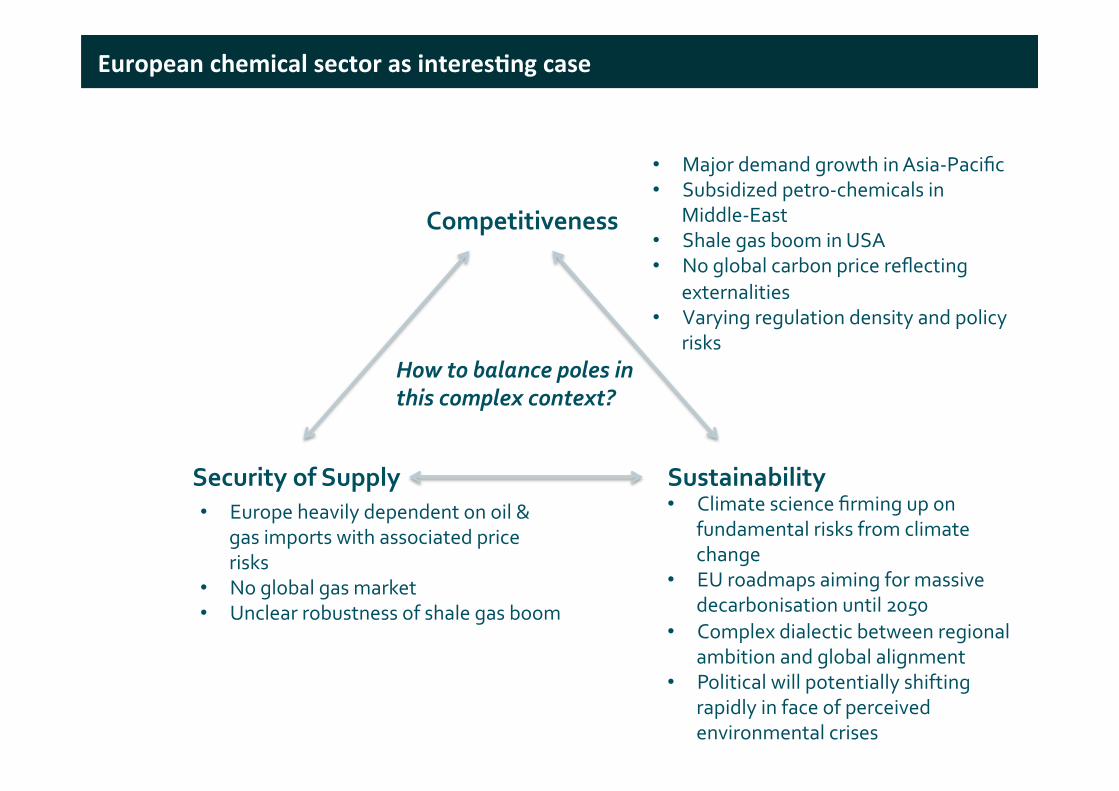

European(chemical(sector(as(interesEng(case(

Competitiveness#

Security#of#Supply# Sustainability#

• Major'demand'growth'in'Asia5Pacific'• Subsidized'petro5chemicals'in'

Middle5East'• Shale'gas'boom'in'USA'• No'global'carbon'price'reflecting'

externalities'• Varying'regulation'density'and'policy'

risks'

• Climate'science'firming'up'on'fundamental'risks'from'climate'change'

• EU'roadmaps'aiming'for'massive'decarbonisation'until'2050'

• Complex'dialectic'between'regional'ambition'and'global'alignment'

• Political'will'potentially'shifting'rapidly'in'face'of'perceived'environmental'crises'

• Europe'heavily'dependent'on'oil'&'gas'imports'with'associated'price'risks'

• No'global'gas'market'• Unclear'robustness'of'shale'gas'boom'

How$to$balance$poles$in$this$complex$context?$

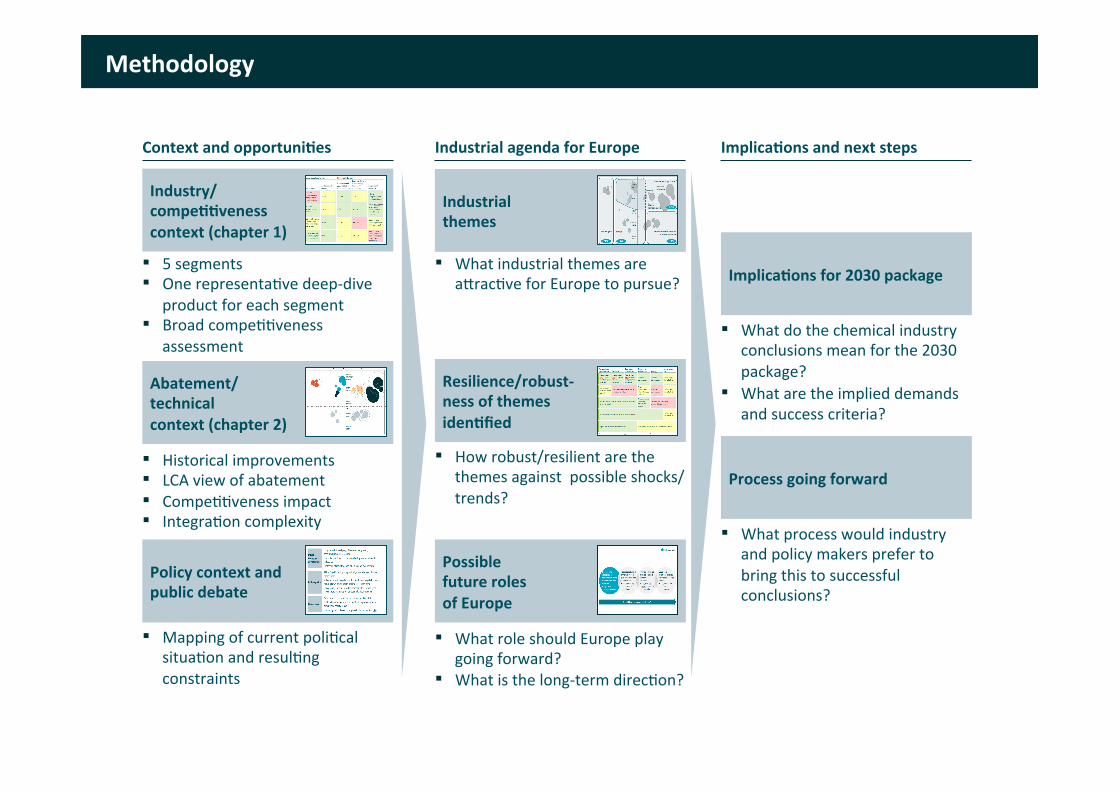

Methodology(

ImplicaEons(and(next(steps(Context(and(opportuniEes(

Policy(context(and(public(debate(

▪ Mapping!of!current!poli0cal!situa0on!and!resul0ng!constraints!

▪ 5!segments!▪ One!representa0ve!deep7dive!

product!for!each!segment!▪ Broad!compe00veness!

assessment!

Industry/(compeEEveness(context((chapter(1)(

▪ Historical!improvements!▪ LCA!view!of!abatement!!▪ Compe00veness!impact!▪ Integra0on!complexity!

Abatement/(technical(context((chapter(2)(

Industrial(agenda(for(Europe(

ImplicaEons(for(2030(package(

▪ What!do!the!chemical!industry!conclusions!mean!for!the!2030!package?!

▪ What!are!the!implied!demands!and!success!criteria?!

Process(going(forward(

▪ What!process!would!industry!and!policy!makers!prefer!to!bring!this!to!successful!conclusions?!

Industrial(themes(

▪ What!industrial!themes!are!aIrac0ve!for!Europe!to!pursue?!

Possible(future(roles(of(Europe(

▪ What!role!should!Europe!play!going!forward?!

▪ What!is!the!long7term!direc0on?!

Resilience/robust+(ness(of(themes(idenEfied(

▪ How!robust/resilient!are!the!themes!against!!possible!shocks/trends?!!

Contents(

▪ Mo0va0on!of!the!project!

▪ Competitiveness of the Europeanchemical industry(

▪ What could be done to reduce emissions while maintaining or increasing competitiveness?!

▪ Implications and next steps!

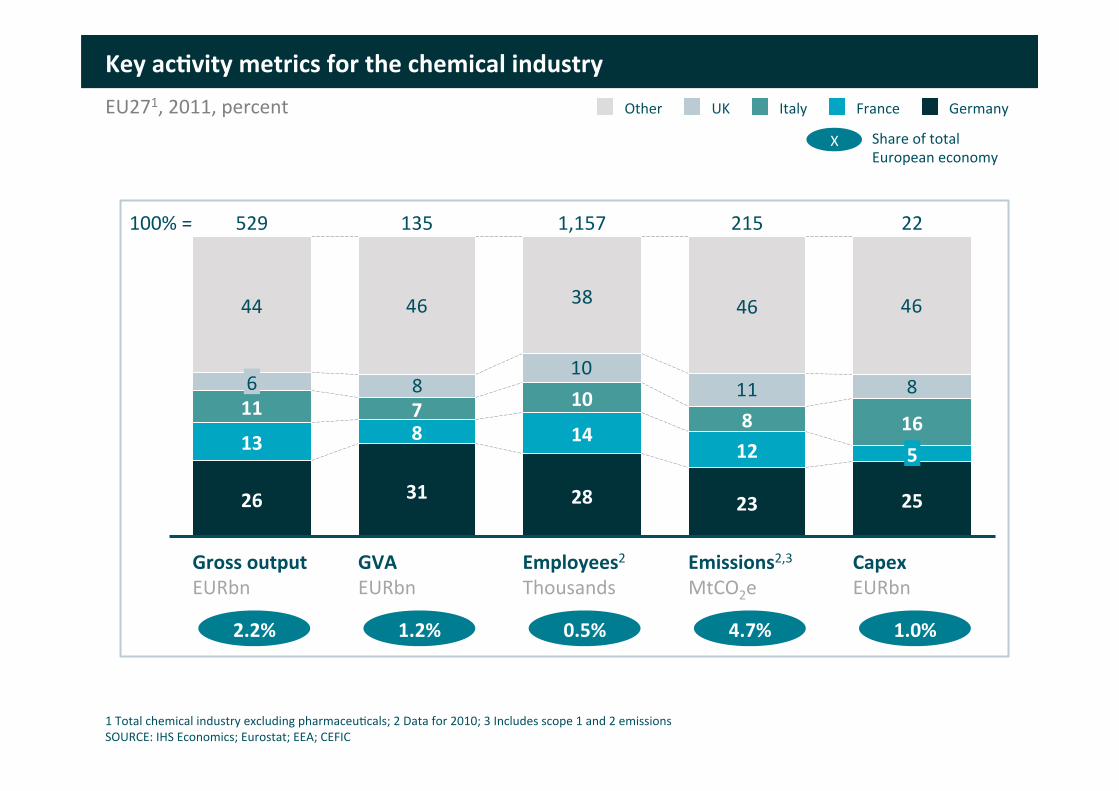

Key(acEvity(metrics(for(the(chemical(industry(

810

11 8

4646

GVA(EURbn!

135!

31(

8(

25(

Gross(output(EURbn!

529!

26(

13(

11(6!

44!

100%!=!

Capex(EURbn!

22!

5(16(

Emissions2,3!MtCO2e!

215!

23(

12(8(

46!

7(

Employees2!Thousands!

1,157!

28(

14(

10(

38!

Germany!France!Italy!UK!Other!EU271,!2011,!percent!

0.5%(1.2%(

X! Share!of!total!European!economy!

1.0%(4.7%(2.2%(

1!Total!chemical!industry!excluding!pharmaceu0cals;!2!Data!for!2010;!3!Includes!scope!1!and!2!emissions!SOURCE:!IHS!Economics;!Eurostat;!EEA;!CEFIC!

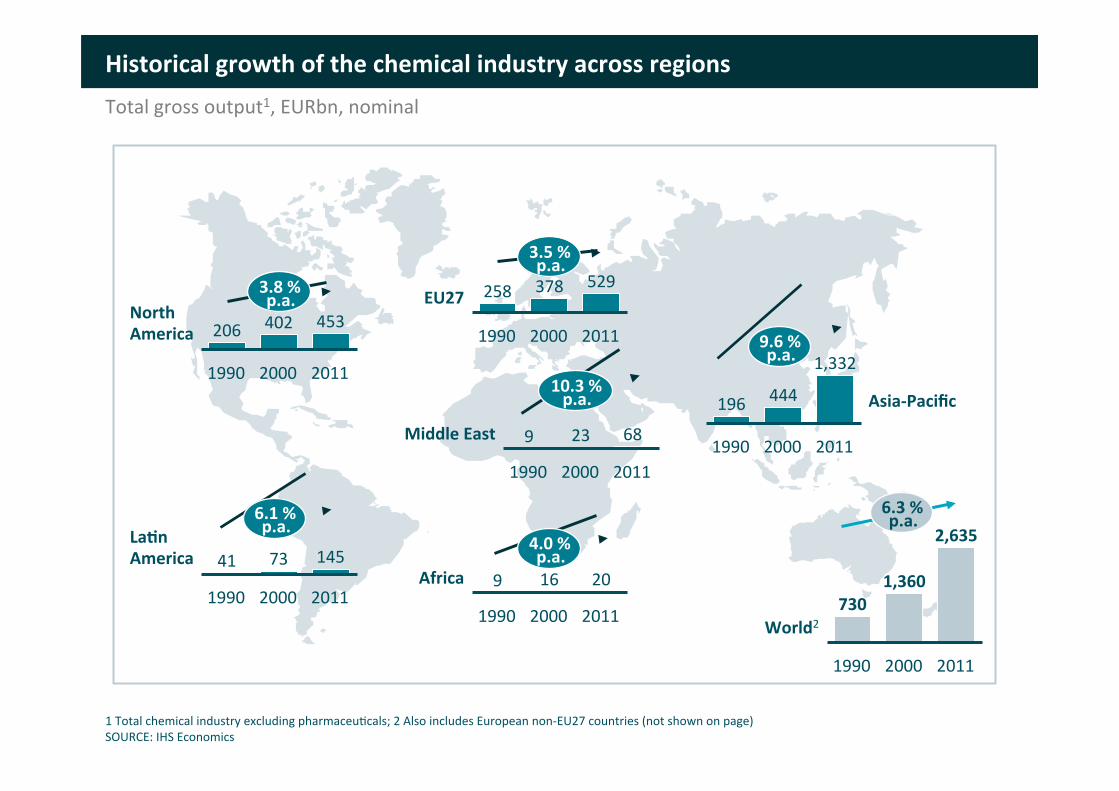

Historical(growth(of(the(chemical(industry(across(regions(

North(America

2011

453

2000

402

1990

206

LaEn(America

2011

145

2000

73

1990

41 Africa

2011

20

2000

16

1990

9

Middle(East

2011

68

2000

23

1990

9

EU27

2011

529

2000

378

1990

258

Asia+Pacific

2011

1,332

2000

444

1990

196

World2

2011

2,635

2000

1,360

1990

730

3.8(%(p.a.(

3.5(%(p.a.(

9.6(%(p.a.(

6.3(%(p.a.(

10.3(%(p.a.(

4.0(%(p.a.(

6.1(%(p.a.(

Total!gross!output1,!EURbn,!nominal!

1!Total!chemical!industry!excluding!pharmaceu0cals;!2!Also!includes!European!non7EU27!countries!(not!shown!on!page)!SOURCE:!IHS!Economics!

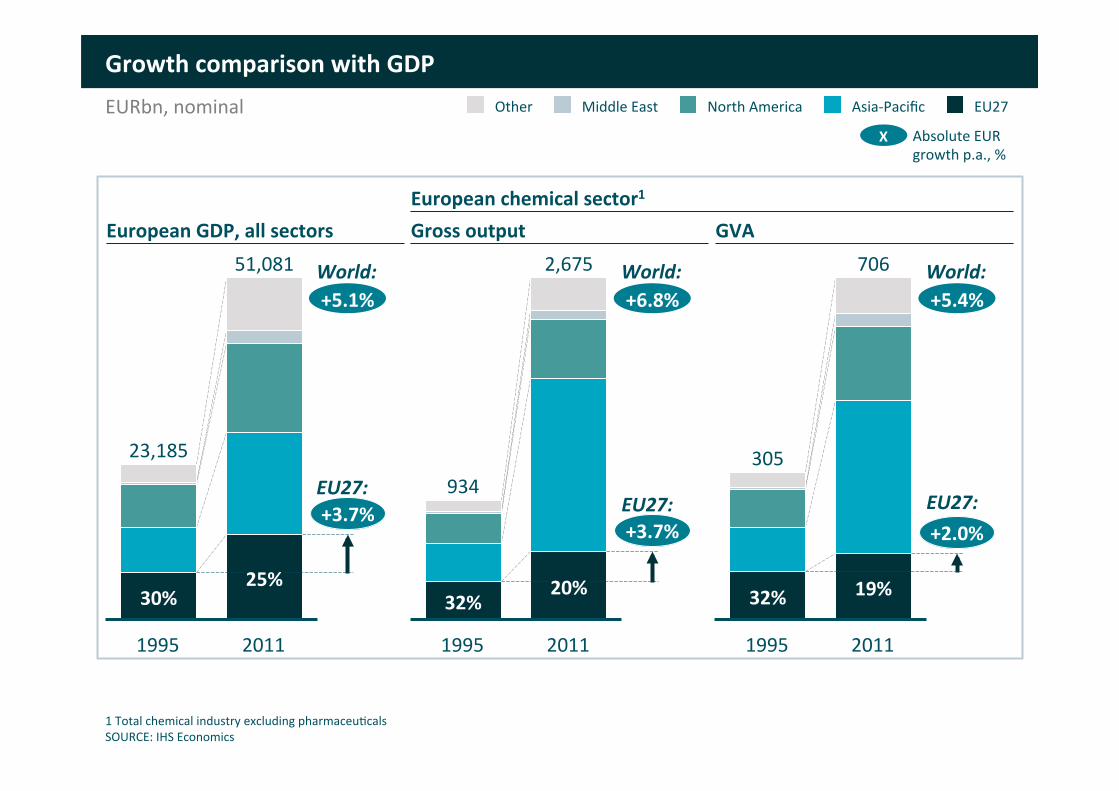

25%

1995

23,185

30%

51,081

+3.7%

2011

EU27 Asia7Pacific North!America Middle!East Other

20%

1995

934

32%

2,675

+3.7%

2011

706

+2.0%

2011

19%

1995

305

32%

Growth(comparison(with(GDP(

European(chemical(sector1(

EURbn,!nominal!

European(GDP,(all(sectors( GVA'Gross(output'

+5.1%( +6.8%( +5.4%(World:' World:' World:'

X( Absolute!EUR!growth!p.a.,!%!

EU27:'EU27:' EU27:'

1!Total!chemical!industry!excluding!pharmaceu0cals!SOURCE:!IHS!Economics!

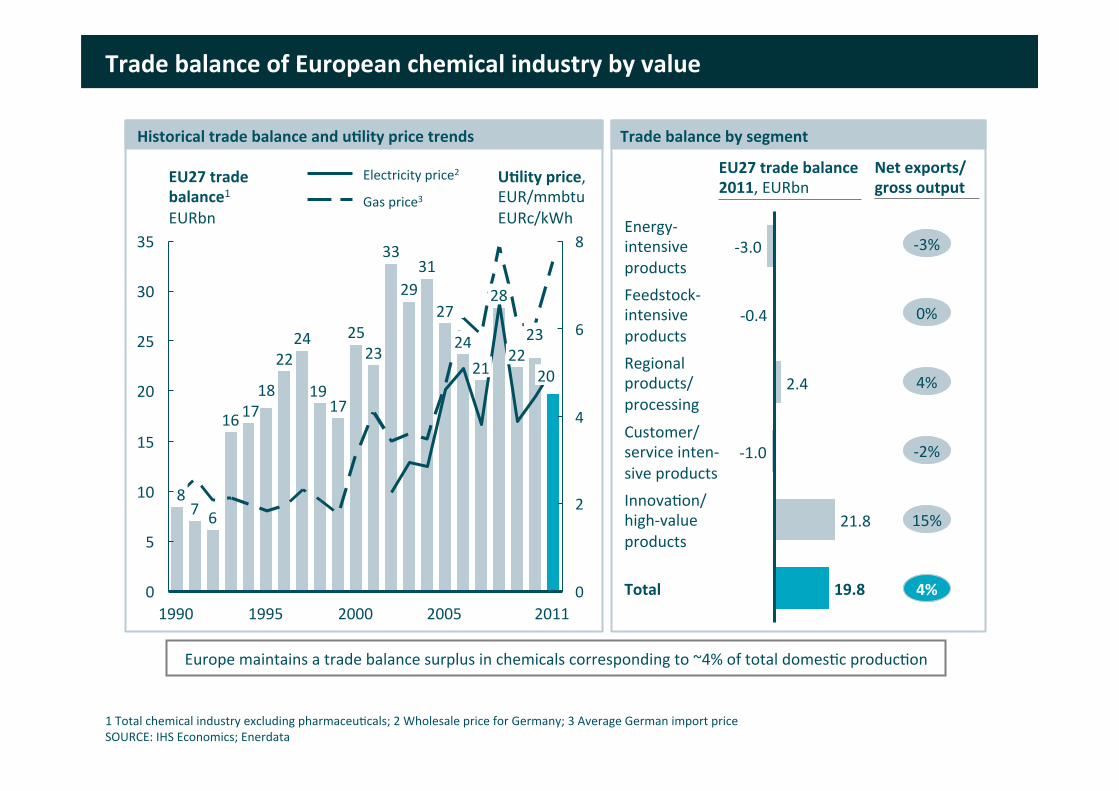

Trade(balance(of(European(chemical(industry(by(value(

Total( 19.8(

Innova0on/!high7value!products!

21.8!

Customer/!service!inten7!sive!products!

71.0!

Regional!products/!processing!

2.4!

Feedstock7!intensive!products!

70.4!

Energy7!intensive!products!

73.0! 73%!

0%!

4%!

72%!

15%!

4%(

EU27(trade(balance(2011,!EURbn(

Net(exports/(gross(output!

0

2

4

6

8

10!

5!

0!2011!

20!

23!22!

28!

21!24!

2005!

27!

31!29!

33!

23!

2000!

25!

17!19!

24!22!

1995!

18!17!16!

6!7!

35!

30!

25!

20!

15!

1990!

8!

Historical(trade(balance(and(uElity(price(trends!

EU27(trade(balance1!EURbn!

UElity(price,!!EUR/mmbtu!EURc/kWh!

Gas!price3!Electricity!price2!

Trade(balance(by(segment!

Europe!maintains!a!trade!balance!surplus!in!chemicals!corresponding!to!~4%!of!total!domes0c!produc0on!

1!Total!chemical!industry!excluding!pharmaceu0cals;!2!Wholesale!price!for!Germany;!3!Average!German!import!price!SOURCE:!IHS!Economics;!Enerdata!

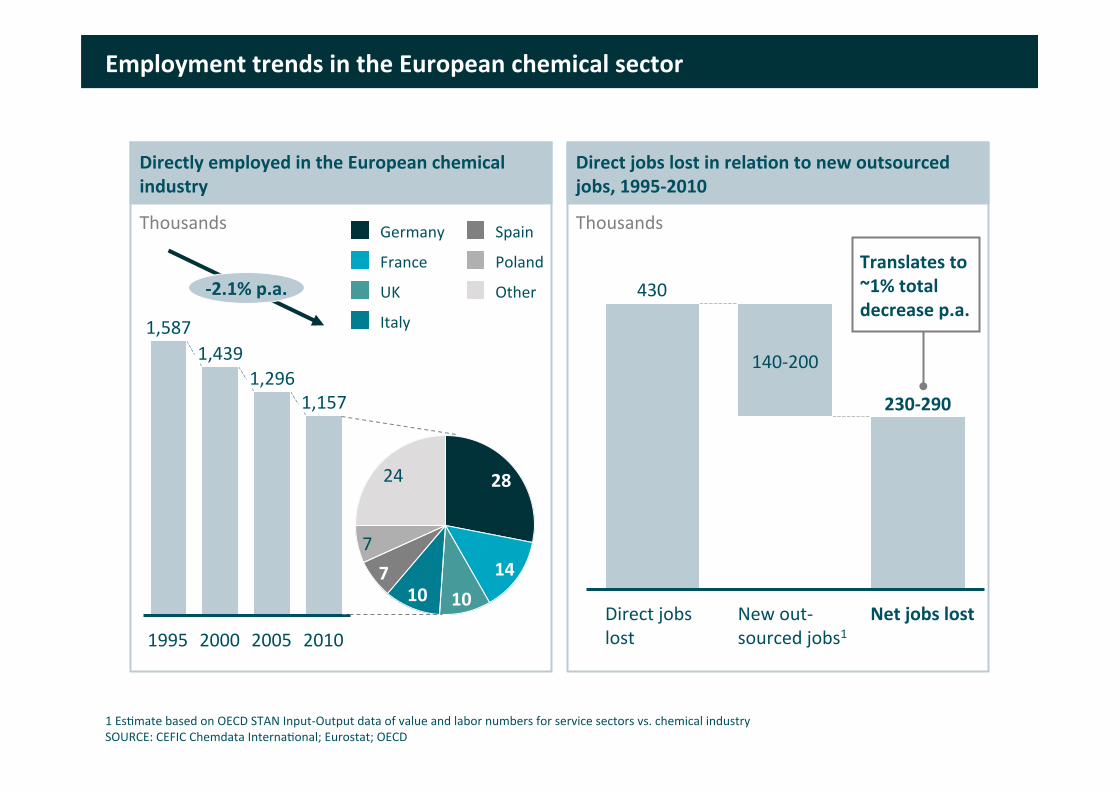

Employment(trends(in(the(European(chemical(sector(

7

24!

7(10( 10(

14(

28(

Other!

Poland!

Spain!

Italy!

UK!

France!

Germany! Thousands!Thousands!

+2.1%(p.a.(

1,157!

2010!2005!

1,296!

2000!

1,439!

1995!

1,587!

430

New!out7sourced!jobs1!

Net(jobs(lost(

230+290(

Direct!jobs!!lost!!

1407200!

Translates(to(~1%(total(decrease(p.a.(

1!Es0mate!based!on!OECD!STAN!Input7Output!data!of!value!and!labor!numbers!for!service!sectors!vs.!chemical!industry!SOURCE:!CEFIC!Chemdata!Interna0onal;!Eurostat;!OECD!

Direct(jobs(lost(in(relaEon(to(new(outsourced(jobs,(1995+2010(

Directly(employed(in(the(European(chemical(industry!!

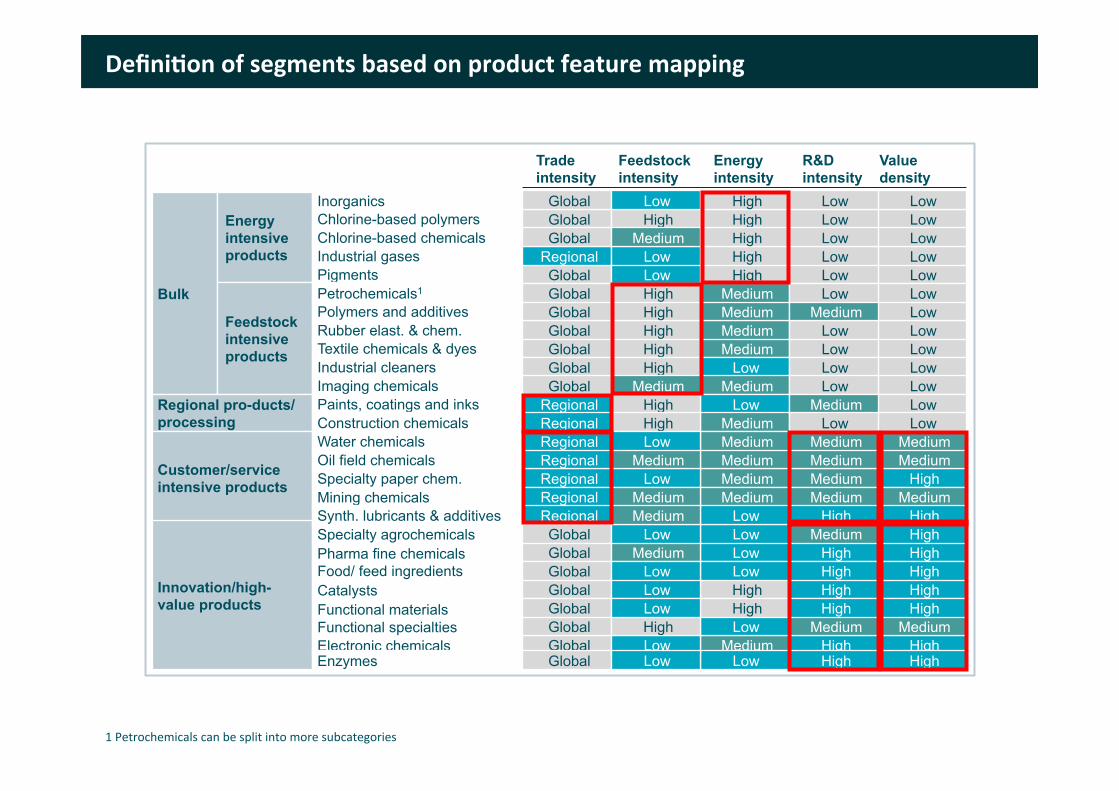

DefiniEon(of(segments(based(on(product(feature(mapping(

Bulk

Energy intensive products

Feedstock intensive products

Regional pro-ducts/processing

Customer/service intensive products

Innovation/high-value products

Pigments

Textile chemicals & dyes Industrial cleaners Imaging chemicals

Chlorine-based polymers

Industrial gases Chlorine-based chemicals

Rubber elast. & chem.

Inorganics

Polymers and additives Petrochemicals1

Pharma fine chemicals

Electronic chemicals

Specialty paper chem.

Paints, coatings and inks Construction chemicals

Oil field chemicals Water chemicals

Mining chemicals

Catalysts

Specialty agrochemicals

Enzymes

Functional specialties Functional materials

Food/ feed ingredients

Synth. lubricants & additives

High

Medium Low

Medium

High

High High

Medium

High

Medium Medium

Low

Medium

Medium

Low Medium

Medium Medium

Medium

High

Low

Low

Low High

Low

Energy intensity

Low

Global

Global Global Global

Global

Regional Global

Global

Global

Global Global

Global

Global

Regional

Regional Regional

Regional Regional

Regional

Global

Global

Global

Global Global

Global

Trade intensity

Regional

Low

Low Low Low

Low

Low Low

Low

Low

Low Low

High

High

High

Low Low

Medium Medium

Medium

High

High

High

Medium High

High

Value density

High

Low

Low Low Low

Low

Low Low

Low

Low

Medium Low

High

High

Medium

Medium Low

Medium Medium

Medium

High

Medium

High

Medium High

High

R&D intensity

High

Low

High High

Medium

High

Low Medium

High

Low

High High

Medium

Low

Low

High High

Medium Low

Medium

Low

Low

Low

High Low

Low

Feedstock intensity

Medium

1!Petrochemicals!can!be!split!into!more!subcategories!

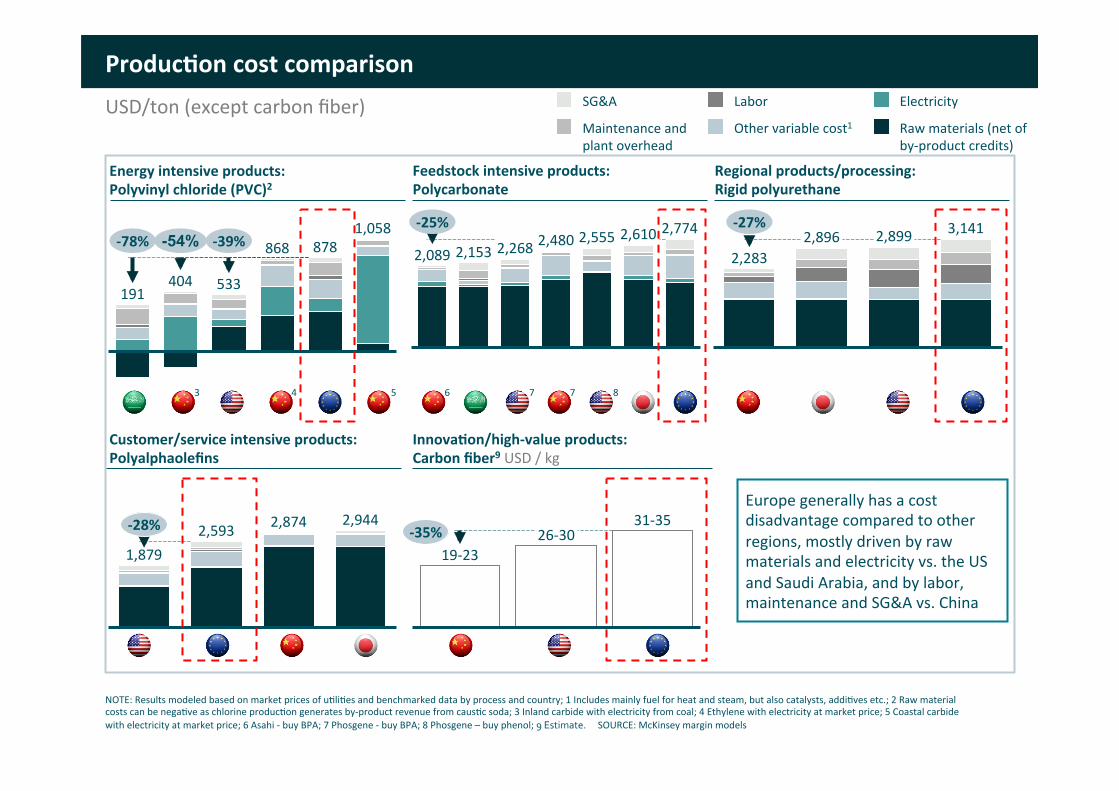

ProducEon(cost(comparison(USD/ton!(except!carbon!fiber)!

533

+39%

404

-54%

191

+78% 1,058

878 868

Raw!materials!(net!of!!by7product!credits)

Electricity

Other!variable!cost1

Labor

Maintenance!and!plant!overhead!

SG&A

2,089

+25% 2,774 2,610 2,555 2,480 2,268 2,153 2,283

+27% 3,141 2,899 2,896

1,879

+28% 2,944 2,874 2,593 19723!

31735!26730!+35%(

Energy(intensive(products:((Polyvinyl(chloride((PVC)2!(

Feedstock(intensive(products:(Polycarbonate(

Customer/service(intensive(products:(Polyalphaolefins(

Regional(products/processing:(Rigid(polyurethane(

Europe!generally!has!a!cost!disadvantage!compared!to!other!regions,!mostly!driven!by!raw!materials!and!electricity!vs.!the!US!and!Saudi!Arabia,!and!by!labor,!maintenance!and!SG&A!vs.!China!

InnovaEon/high+value(products:((Carbon(fiber9!USD!/!kg!

3! 4! 5! 6! 7!7! 8!

NOTE:!Results!modeled!based!on!market!prices!of!u0li0es!and!benchmarked!data!by!process!and!country;!1!Includes!mainly!fuel!for!heat!and!steam,!but!also!catalysts,!addi0ves!etc.;!2!Raw!material!costs!can!be!nega0ve!as!chlorine!produc0on!generates!by7product!revenue!from!caus0c!soda;!3!Inland!carbide!with!electricity!from!coal;!4!Ethylene!with!electricity!at!market!price;!5!Coastal!carbide!with!electricity!at!market!price;!6!Asahi!7!buy!BPA;!7!Phosgene!7!buy!BPA;!8!Phosgene!–!buy!phenol;!9'Estimate.'!!!!SOURCE:!McKinsey!margin!models!

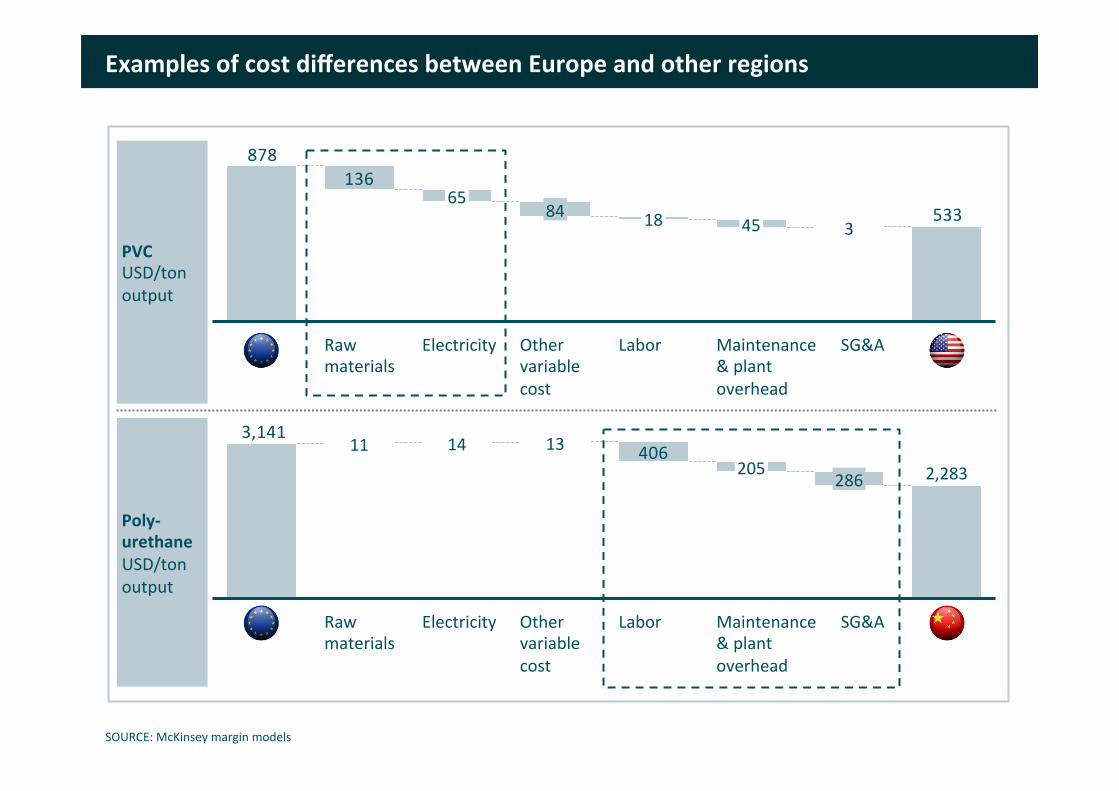

4063,141

2,283!

SG&A

286!

Maintenance!&!plant!overhead!

205!

Labor Other!variable!cost!

13!

Electricity

14!

Raw!materials

11!

Examples(of(cost(differences(between(Europe(and(other(regions(

533

136878

3!

SG&A Maintenance!&!plant!overhead!

45!

Labor

18!

Other!variable!cost

84!

Electricity

65!

Raw!materials

Poly+urethane(USD/ton!output(

PVC(USD/ton!output!

SOURCE:!McKinsey!margin!models!

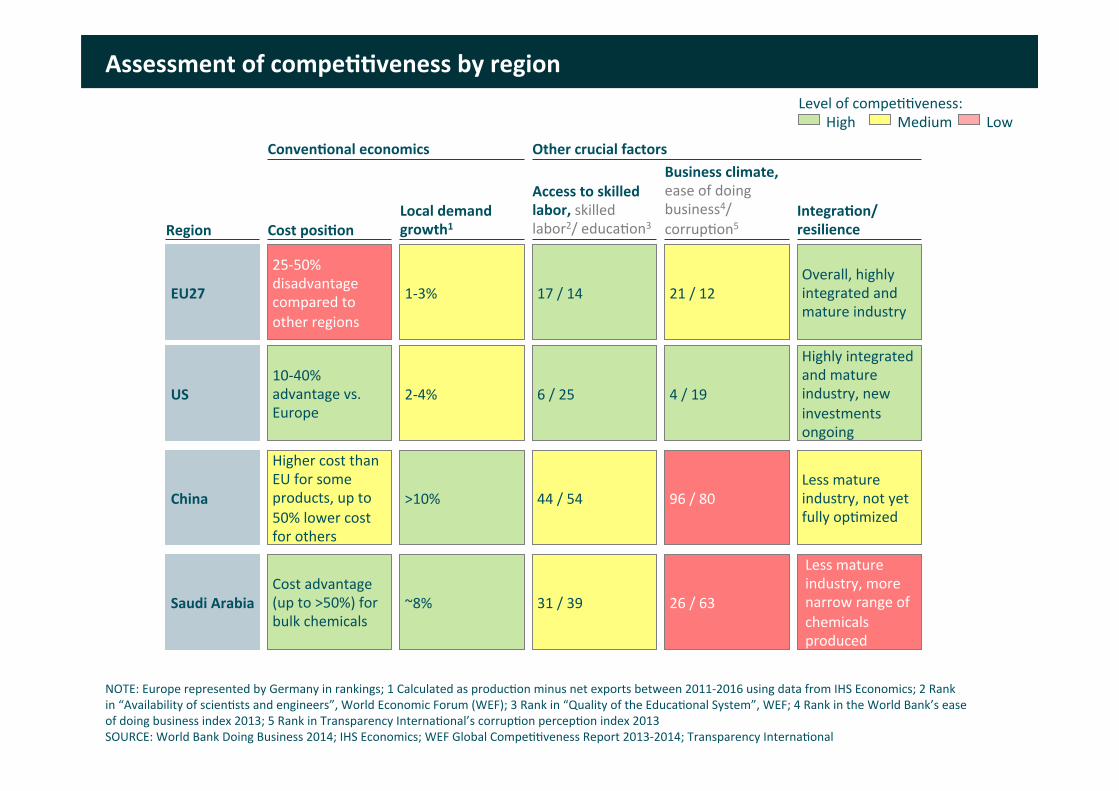

Assessment(of(compeEEveness(by(region(

Other(crucial(factors(

Region(Local(demand(growth1(Cost(posiEon(

Business(climate,((ease!of!doing!business4/!corrup0on5(

EU27(

US(

China(

Saudi(Arabia(

25750%!disadvantage!compared!to!other!regions!

21!/!12!

274%!10740%!advantage!vs.!Europe!

4!/!19!

>10%!

Higher!cost!than!EU!for!some!products,!up!to!50%!lower!cost!for!others!

96!/!80!

~8%!Cost!advantage!(up!to!>50%)!for!bulk!chemicals!

IntegraEon/(resilience(

Overall,!highly!integrated!and!mature!industry!

Highly!integrated!and!mature!industry,!new!investments!ongoing!

Less!mature!industry,!not!yet!fully!op0mized!!

Less!mature!industry,!more!narrow!range!of!chemicals!produced!

26!/!63!

Access(to(skilled(labor,(skilled!labor2/!educa0on3!

17!/!14!

6!/!25!

44!/!54!

31!/!39!

ConvenEonal(economics(

173%!

High! Medium! Low!Level!of!compe00veness:!

NOTE:!Europe!represented!by!Germany!in!rankings;!1!Calculated!as!produc0on!minus!net!exports!between!201172016!using!data!from!IHS!Economics;!2!Rank!in!“Availability!of!scien0sts!and!engineers”,!World!Economic!Forum!(WEF);!3!Rank!in!“Quality!of!the!Educa0onal!System”,!WEF;!4!Rank!in!the!World!Bank’s!ease!of!doing!business!index!2013;!5!Rank!in!Transparency!Interna0onal’s!corrup0on!percep0on!index!2013!SOURCE:!World!Bank!Doing!Business!2014;!IHS!Economics;!WEF!Global!Compe00veness!Report!201372014;!Transparency!Interna0onal!

0

50

100

150

200

250

2020!2016!2012!2008!2004!2000!

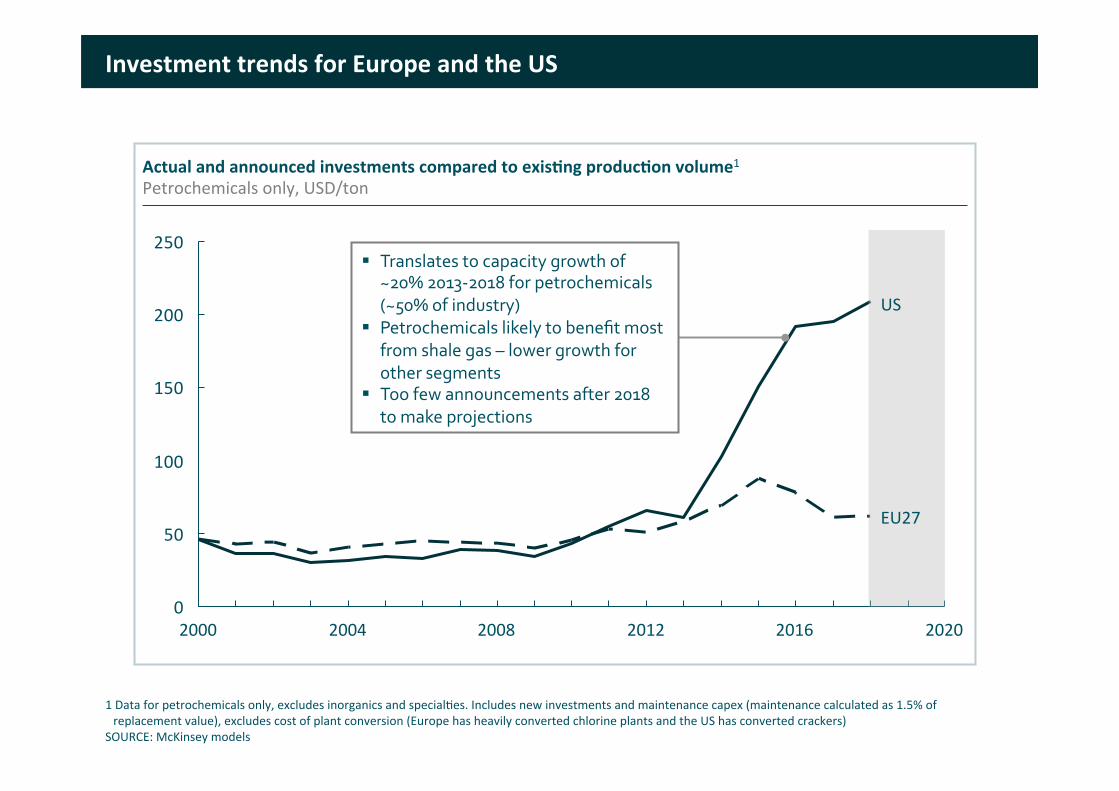

Investment(trends(for(Europe(and(the(US(

Actual(and(announced(investments(compared(to(exisEng(producEon(volume1!Petrochemicals!only,!USD/ton!

! Translates'to'capacity'growth'of'~20%'201352018'for'petrochemicals'(~50%'of'industry)'

! Petrochemicals'likely'to'benefit'most'from'shale'gas'–'lower'growth'for'other'segments'

! Too'few'announcements'after'2018'to'make'projections''

US!

EU27!

1!Data!for!petrochemicals!only,!excludes!inorganics!and!special0es.!Includes!new!investments!and!maintenance!capex!(maintenance!calculated!as!1.5%!of!replacement!value),!excludes!cost!of!plant!conversion!(Europe!has!heavily!converted!chlorine!plants!and!the!US!has!converted!crackers)!

SOURCE:!McKinsey!models!

Contents(

▪ Mo0va0on!of!the!project!

▪ Competitiveness of the European chemical industry!

▪ What could be done to reduce emissions while maintaining or increasing competitiveness?(

▪ Implications and next steps!

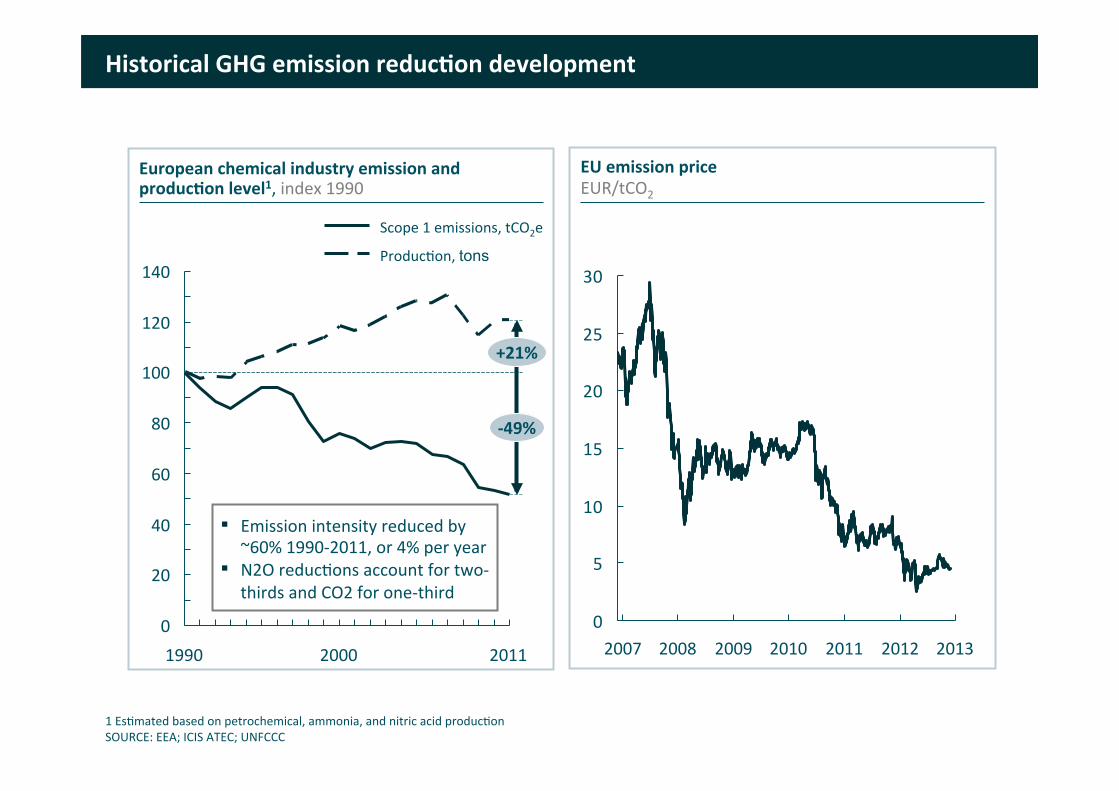

European(chemical(industry(emission(and(producEon(level1,(index!1990!

Historical(GHG(emission(reducEon(development(

140!

120!

100!

80!

60!

40!

20!

0!

+21%

+49%

2011 2000 1990

Produc0on,!tons

Scope!1!emissions,!tCO2e!

EU(emission(price!EUR/tCO2!

0

5

10

15

20

25

30

2013!2012!2011!2010!2009!2008!2007!

▪ Emission!intensity!reduced!by!~60%!199072011,!or!4%!per!year!

▪ N2O!reduc0ons!account!for!two7!thirds!and!CO2!for!one7third!

1!Es0mated!based!on!petrochemical,!ammonia,!and!nitric!acid!produc0on!!SOURCE:!EEA;!ICIS!ATEC;!UNFCCC!

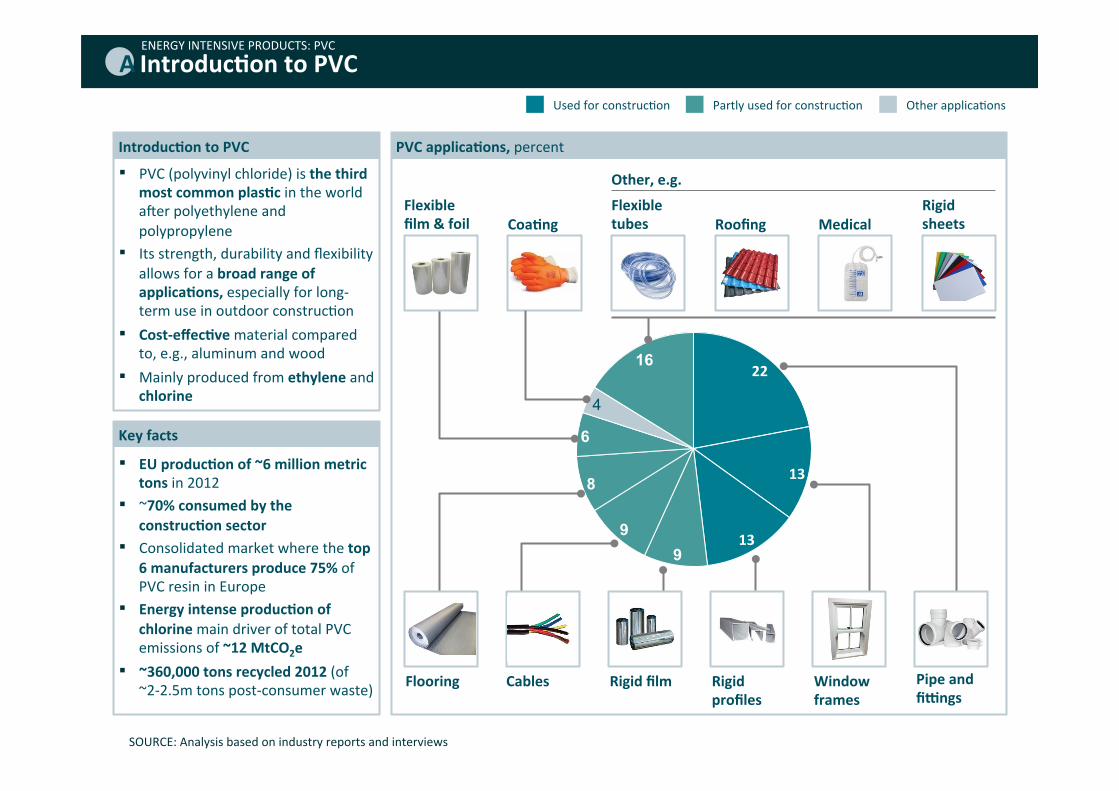

IntroducEon(to(PVC(

13

13 9

9

8

4

6

16 22

Pipe(and(fihngs((

Window(frames(

Rigid(profiles(

Rigid(film(Flooring(

Flexible(film(&(foil( CoaEng(

IntroducEon(to(PVC(

▪ PVC!(polyvinyl!chloride)!is!the(third(most(common(plasEc!in!the!world!aqer!polyethylene!and!polypropylene!

▪ Its!strength,!durability!and!flexibility!allows!for!a!broad(range(of(applicaEons,(especially!for!long7term!use!in!outdoor!construc0on(

▪ Cost+effecEve(material!compared!to,!e.g.,!aluminum!and!wood!

▪ Mainly!produced!from!ethylene!and!chlorine!

Key(facts((

▪ EU(producEon(of(~6(million(metric(tons(in!2012!

▪ ~70%(consumed(by(the(construcEon(sector(

▪ Consolidated!market!where!the!top(6(manufacturers(produce(75%(of!PVC!resin!in!Europe(

▪ Energy(intense(producEon(of(chlorine(main!driver!of!total!PVC!emissions!of!~12(MtCO2e(

▪ ~360,000(tons(recycled(2012((of!~272.5m!tons!post7consumer!waste)!

PVC(applicaEons,(percent!

Used!for!construc0on! Partly!used!for!construc0on! Other!applica0ons!

Other,(e.g.(

Cables(

Flexible(tubes( Medical(Roofing(

Rigid(sheets(

ENERGY!INTENSIVE!PRODUCTS:!PVC!

A

SOURCE:!Analysis!based!on!industry!reports!and!interviews!

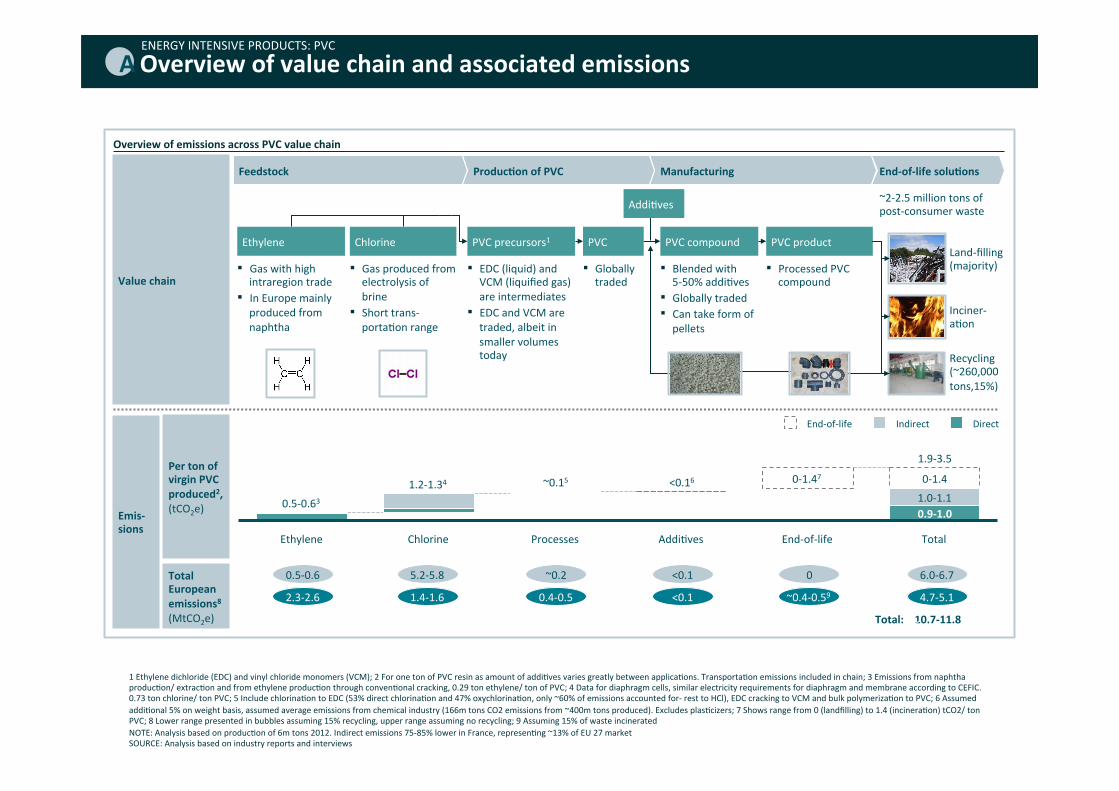

Overview(of(value(chain(and(associated(emissions(

Total!

1.973.5!

0.9+1.0(1.071.1!071.4!

End7of7life!

071.47!

Addi0ves!

<0.16!

Processes!

~0.15!

Chlorine!

1.271.34!

Ethylene!

0.570.63!

Direct!Indirect!End7of7life!

Overview(of(emissions(across(PVC(value(chain!

PVC!product!

▪ Processed!PVC!compound!

Emis+sions(

Per(ton(of(virgin(PVC(produced2,((tCO2e)!

Total(European(emissions8((MtCO2e)!

Feedstock( Manufacturing(

Value(chain(

End+of+life(soluEons(

▪ Gas!with!high!intraregion!trade!

▪ In!Europe!mainly!produced!from!naphtha(

Ethylene! Chlorine!

▪ Gas!produced!from!electrolysis!of!brine!

▪ Short!trans7porta0on!range!

PVC!

▪ Globally!traded!

▪ EDC!(liquid)!and!VCM!(liquified!gas)!are!intermediates!

▪ EDC!and!VCM!are!traded,!albeit!in!smaller!volumes!today!

PVC!precursors1!

Recycling!(~260,000!tons,15%)!

Inciner7a0on!

ProducEon(of(PVC(

PVC!compound!

▪ Blended!with!5750%!addi0ves!

▪ Globally!traded!▪ Can!take!form!of!pellets!

Land7filling!(majority)!

~272.5!million!tons!of!post7consumer!waste!Addi0ves!

2.372.6! 1.471.6! 0.470.5! <0.1! ~0.470.59!0.570.6! 5.275.8! ~0.2! <0.1! 0!

4.775.1!

6.076.7!

10.7+11.8(Total:(

AENERGY!INTENSIVE!PRODUCTS:!PVC!

1!Ethylene!dichloride!(EDC)!and!vinyl!chloride!monomers!(VCM);!2!For!one!ton!of!PVC!resin!as!amount!of!addi0ves!varies!greatly!between!applica0ons.!Transporta0on!emissions!included!in!chain;!3!Emissions!from!naphtha!produc0on/!extrac0on!and!from!ethylene!produc0on!through!conven0onal!cracking,!0.29!ton!ethylene/!ton!of!PVC;!4!Data!for!diaphragm!cells,!similar!electricity!requirements!for!diaphragm!and!membrane!according!to!CEFIC.!0.73!ton!chlorine/!ton!PVC;!5!Include!chlorina0on!to!EDC!(53%!direct!chlorina0on!and!47%!oxychlorina0on,!only!~60%!of!emissions!accounted!for7!rest!to!HCl),!EDC!cracking!to!VCM!and!bulk!polymeriza0on!to!PVC;!6!Assumed!addi0onal!5%!on!weight!basis,!assumed!average!emissions!from!chemical!industry!(166m!tons!CO2!emissions!from!~400m!tons!produced).!Excludes!plas0cizers;!7!Shows!range!from!0!(landfilling)!to!1.4!(incinera0on)!tCO2/!ton!PVC;!8!Lower!range!presented!in!bubbles!assuming!15%!recycling,!upper!range!assuming!no!recycling;!9!Assuming!15%!of!waste!incinerated!NOTE:!Analysis!based!on!produc0on!of!6m!tons!2012.!Indirect!emissions!75785%!lower!in!France,!represen0ng!~13%!of!EU!27!market!SOURCE:!Analysis!based!on!industry!reports!and!interviews!

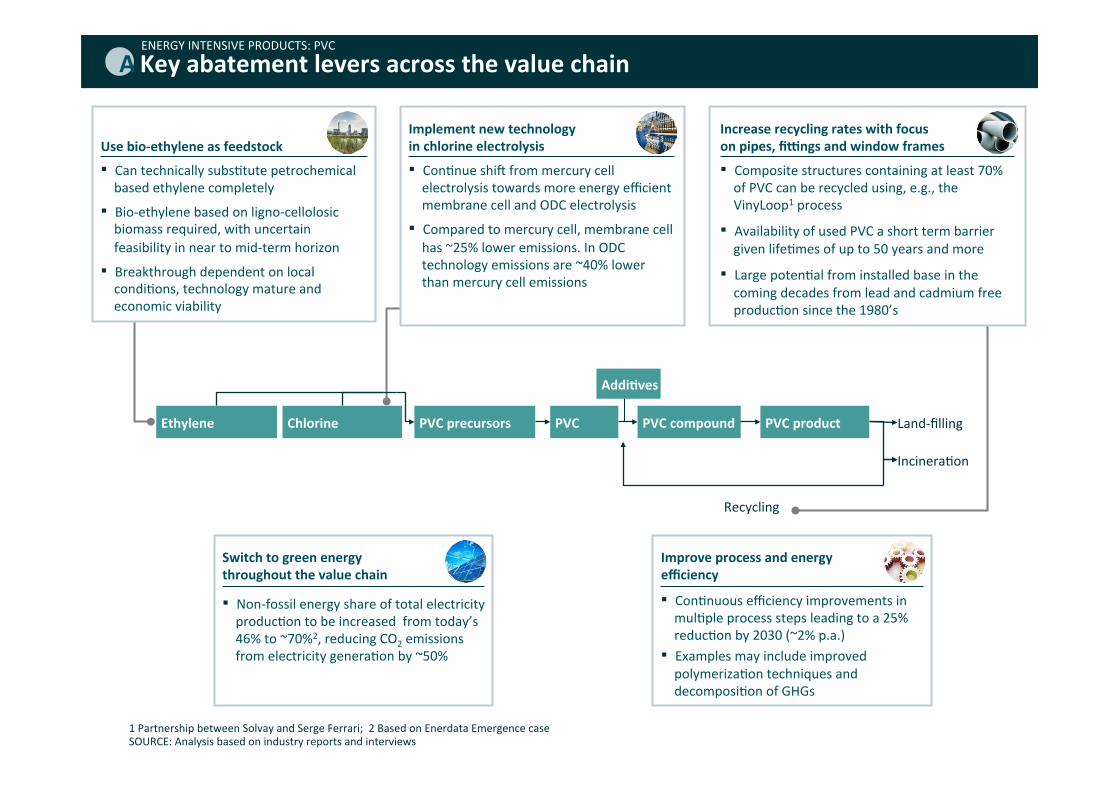

Key(abatement(levers(across(the(value(chain(

Improve(process(and(energy(efficiency(

▪ Con0nuous!efficiency!improvements!in!mul0ple!process!steps!leading!to!a!25%!reduc0on!by!2030!(~2%!p.a.)!▪ Examples!may!include!improved!polymeriza0on!techniques!and!decomposi0on!of!GHGs!

Switch(to(green(energy((throughout(the(value(chain(

▪ Non7fossil!energy!share!of!total!electricity!produc0on!to!be!increased!!from!today’s!46%!to!~70%2,!reducing!CO2!emissions!from!electricity!genera0on!by!~50%!!

Use(bio+ethylene(as(feedstock(

▪ Can!technically!subs0tute!petrochemical!based!ethylene!completely!

▪ Bio7ethylene!based!on!ligno7cellolosic!biomass!required,!with!uncertain!feasibility!in!near!to!mid7term!horizon!

▪ Breakthrough!dependent!on!local!condi0ons,!technology!mature!and!economic!viability!

Implement(new(technology(in(chlorine(electrolysis(

▪ Con0nue!shiq!from!mercury!cell!electrolysis!towards!more!energy!efficient!membrane!cell!and!ODC!electrolysis!

▪ Compared!to!mercury!cell,!membrane!cell!has!~25%!lower!emissions.!In!ODC!technology!emissions!are!~40%!lower!than!mercury!cell!emissions!

Increase(recycling(rates(with(focus((on(pipes,(fihngs(and(window(frames(

▪ Composite!structures!containing!at!least!70%!of!PVC!can!be!recycled!using,!e.g.,!the!VinyLoop1!process!

▪ Availability!of!used!PVC!a!short!term!barrier!given!life0mes!of!up!to!50!years!and!more!

▪ Large!poten0al!from!installed!base!in!the!coming!decades!from!lead!and!cadmium!free!produc0on!since!the!1980’s(

Recycling!

Land7filling!

Incinera0on!

PVC(product(Ethylene( Chlorine( PVC(PVC(precursors( PVC(compound(

AddiEves(

AENERGY!INTENSIVE!PRODUCTS:!PVC!

1!Partnership!between!Solvay!and!Serge!Ferrari;!!2!Based!on!Enerdata!Emergence!case!SOURCE:!Analysis!based!on!industry!reports!and!interviews!

Shik(to(renewable(feedstock(

Shik(to(green(energy(

Global(emission(reducEons(

Process(and(energy(efficiency(

Recycling/(re+use(

Frozen(technology(20302(

Total(emissions,(2030(

Go(to(more(green((energy(mix(

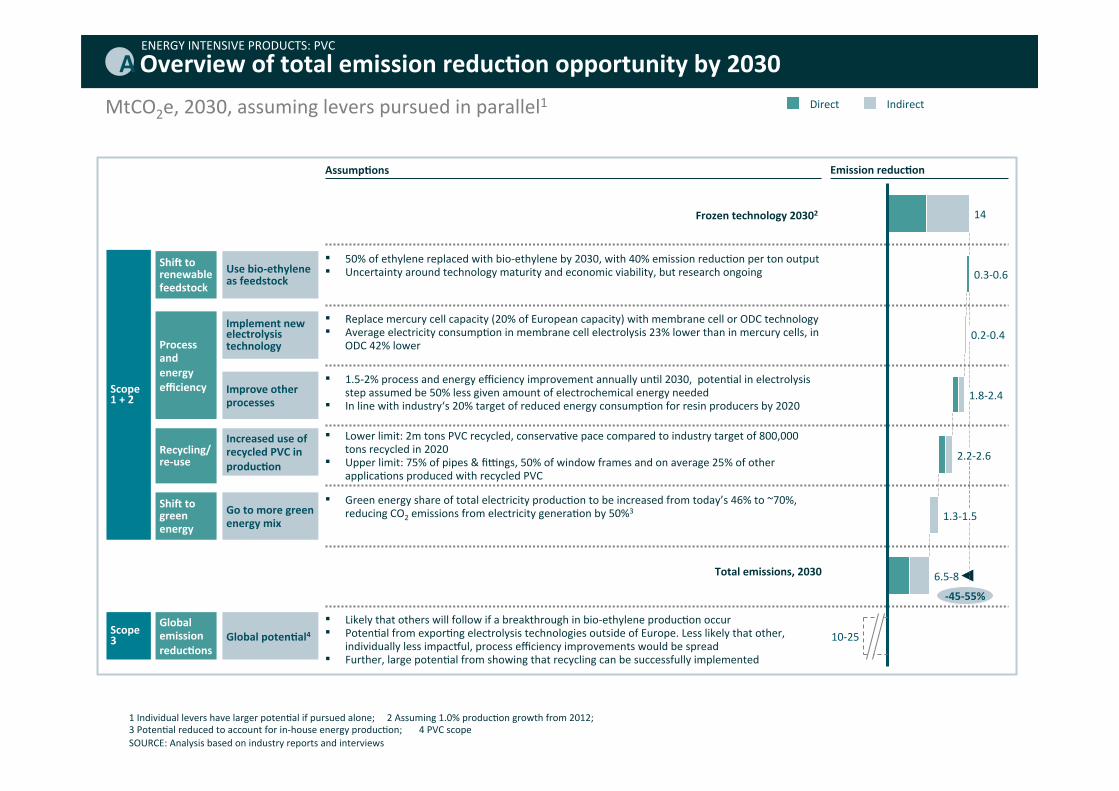

▪ Green!energy!share!of!total!electricity!produc0on!to!be!increased!from!today’s!46%!to!~70%,!reducing!CO2!emissions!from!electricity!genera0on!by!50%3!

Use(bio+ethylene(as(feedstock(

▪ 50%!of!ethylene!replaced!with!bio7ethylene!by!2030,!with!40%!emission!reduc0on!per!ton!output!▪ Uncertainty!around!technology!maturity!and!economic!viability,!but!research!ongoing!

Improve(other(processes(

▪ 1.572%!process!and!energy!efficiency!improvement!annually!un0l!2030,!!poten0al!in!electrolysis!step!assumed!be!50%!less!given!amount!of!electrochemical!energy!needed!

▪ In!line!with!industry‘s!20%!target!of!reduced!energy!consump0on!for!resin!producers!by!2020!

Implement(new(electrolysis(technology(

▪ Replace!mercury!cell!capacity!(20%!of!European!capacity)!with!membrane!cell!or!ODC!technology!▪ Average!electricity!consump0on!in!membrane!cell!electrolysis!23%!lower!than!in!mercury!cells,!in!

ODC!42%!lower!

Increased(use(of(recycled(PVC(in(producEon(

▪ Lower!limit:!2m!tons!PVC!recycled,!conserva0ve!pace!compared!to!industry!target!of!800,000!tons!recycled!in!2020!

▪ Upper!limit:!75%!of!pipes!&!fixngs,!50%!of!window!frames!and!on!average!25%!of!other!applica0ons!produced!with!recycled!PVC!

Global(potenEal4(▪ Likely!that!others!will!follow!if!a!breakthrough!in!bio7ethylene!produc0on!occur!▪ Poten0al!from!expor0ng!electrolysis!technologies!outside!of!Europe.!Less!likely!that!other,!

individually!less!impacyul,!process!efficiency!improvements!would!be!spread!▪ Further,!large!poten0al!from!showing!that!recycling!can!be!successfully!implemented!

Emission(reducEon(AssumpEons(

Overview(of(total(emission(reducEon(opportunity(by(2030(

+45+55%(

6.578!

10725!

1.371.5!

2.272.6!

1.872.4!

0.270.4!

0.370.6!

14!

Direct!! Indirect!

Scope((1(+(2(

Scope((3(

AENERGY!INTENSIVE!PRODUCTS:!PVC!

MtCO2e,!2030,!assuming!levers!pursued!in!parallel1!

1!Individual!levers!have!larger!poten0al!if!pursued!alone;!!!!!2!Assuming!1.0%!produc0on!growth!from!2012;!!!!!!!3!Poten0al!reduced!to!account!for!in7house!energy!produc0on;!!!!!!!4!PVC!scope!SOURCE:!Analysis!based!on!industry!reports!and!interviews!

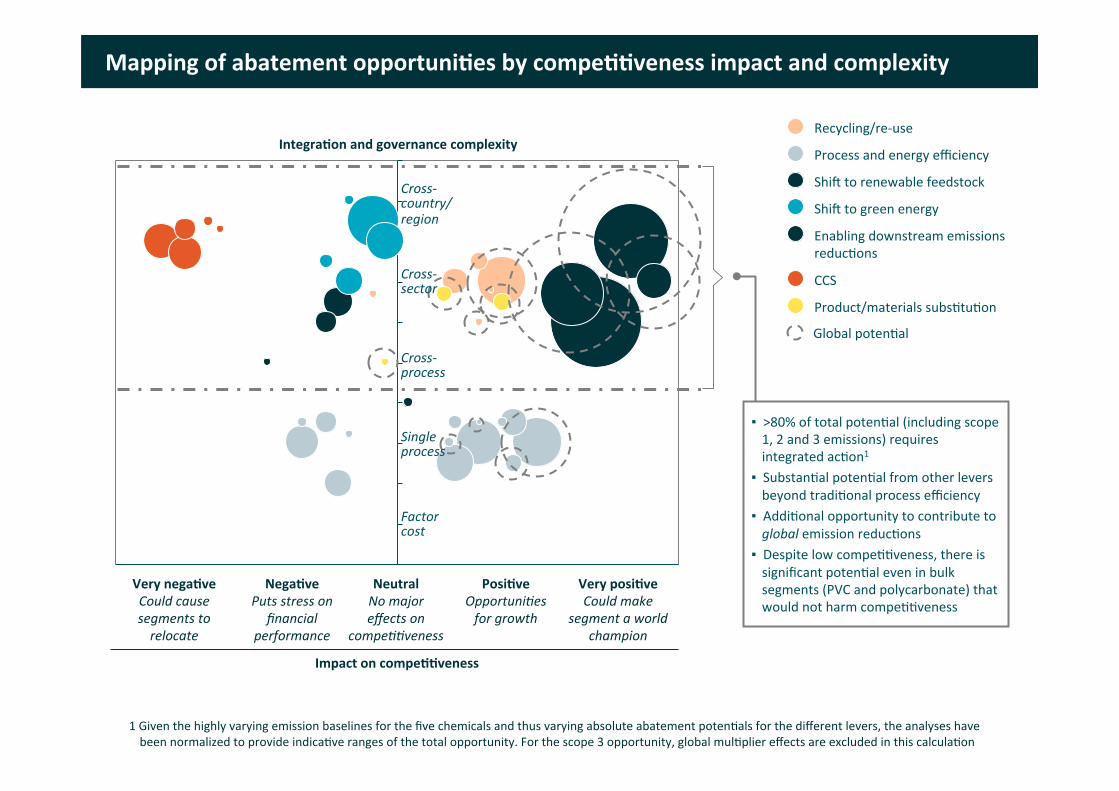

Mapping(of(abatement(opportuniEes(by(compeEEveness(impact(and(complexity(

Global!poten0al!

Product/materials!subs0tu0on

Shiq!to!green!energy

CCS

Enabling!downstream!emissions!!reduc0ons!

Shiq!to!renewable!feedstock

Process!and!energy!efficiency

Recycling/re7use IntegraEon(and(governance(complexity!

Factor'cost'

Single'process'

Cross1'process'

Cross1'country/'region'

Cross1'sector'

Impact(on(compeEEveness(

NegaEve(Puts'stress'on'

financial'performance'

PosiEve(Opportuni:es'for'growth(

Very(negaEve(Could'cause'segments'to'relocate'

Very(posiEve(Could'make'

segment'a'world'champion(

(

Neutral(No'major''effects'on'

compe::veness(

1!Given!the!highly!varying!emission!baselines!for!the!five!chemicals!and!thus!varying!absolute!abatement!poten0als!for!the!different!levers,!the!analyses!have!been!normalized!to!provide!indica0ve!ranges!of!the!total!opportunity.!For!the!scope!3!opportunity,!global!mul0plier!effects!are!excluded!in!this!calcula0on!

▪ >80%!of!total!poten0al!(including!scope!1,!2!and!3!emissions)!requires!integrated!ac0on1!▪ Substan0al!poten0al!from!other!levers!beyond!tradi0onal!process!efficiency!▪ Addi0onal!opportunity!to!contribute!to!global!emission!reduc0ons!▪ Despite!low!compe00veness,!there!is!significant!poten0al!even!in!bulk!segments!(PVC!and!polycarbonate)!that!would!not!harm!compe00veness!

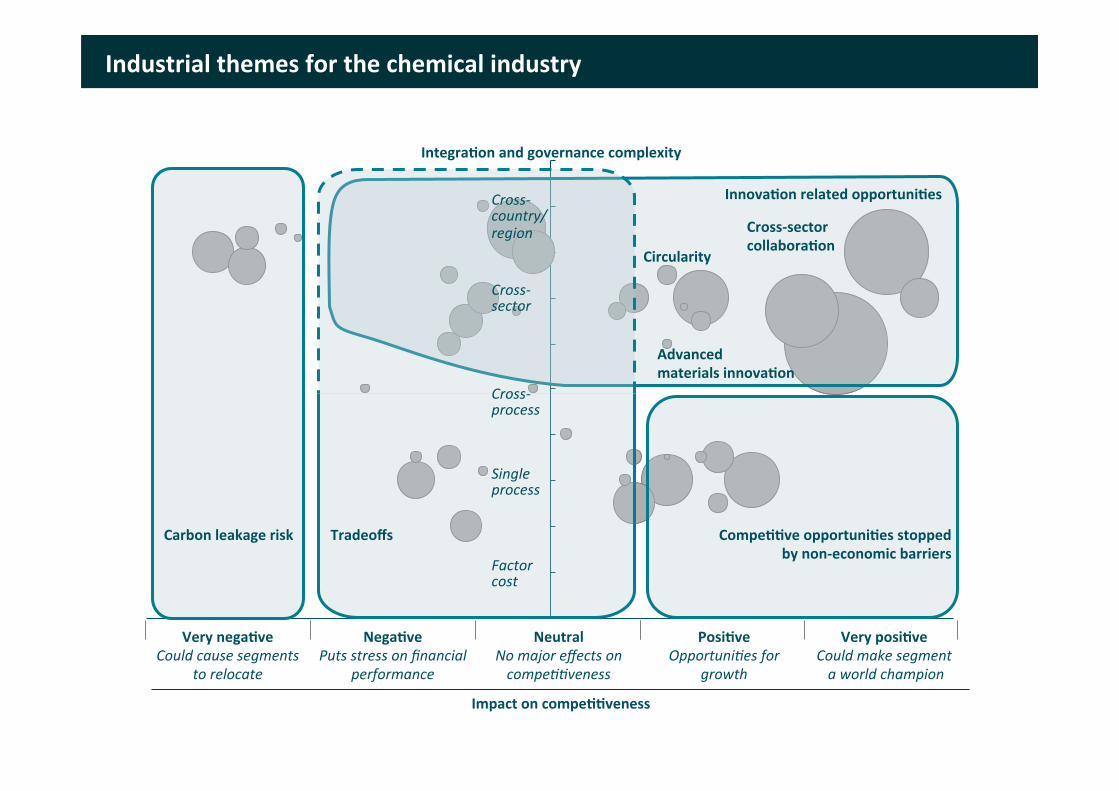

Industrial(themes(for(the(chemical(industry(

Carbon(leakage(risk!

Factor'cost'

Single'process'

Cross1'process'

Cross1'sector'

Tradeoffs! CompeEEve(opportuniEes(stopped(by(non+economic(barriers(

Circularity!

InnovaEon(related(opportuniEes(Cross1'country/'region' Cross+sector(

collaboraEon!

Advanced((materials(innovaEon!

NegaEve(Puts'stress'on'financial'

performance'

PosiEve(Opportuni:es'for'

growth(

Very(negaEve(Could'cause'segments''

to'relocate'

Very(posiEve(Could'make'segment''a'world'champion(

Neutral(No'major'effects'on'compe::veness(

Impact(on(compeEEveness!

IntegraEon(and(governance(complexity!

65775

55765 50760

20730

40750

~0

40750 35745

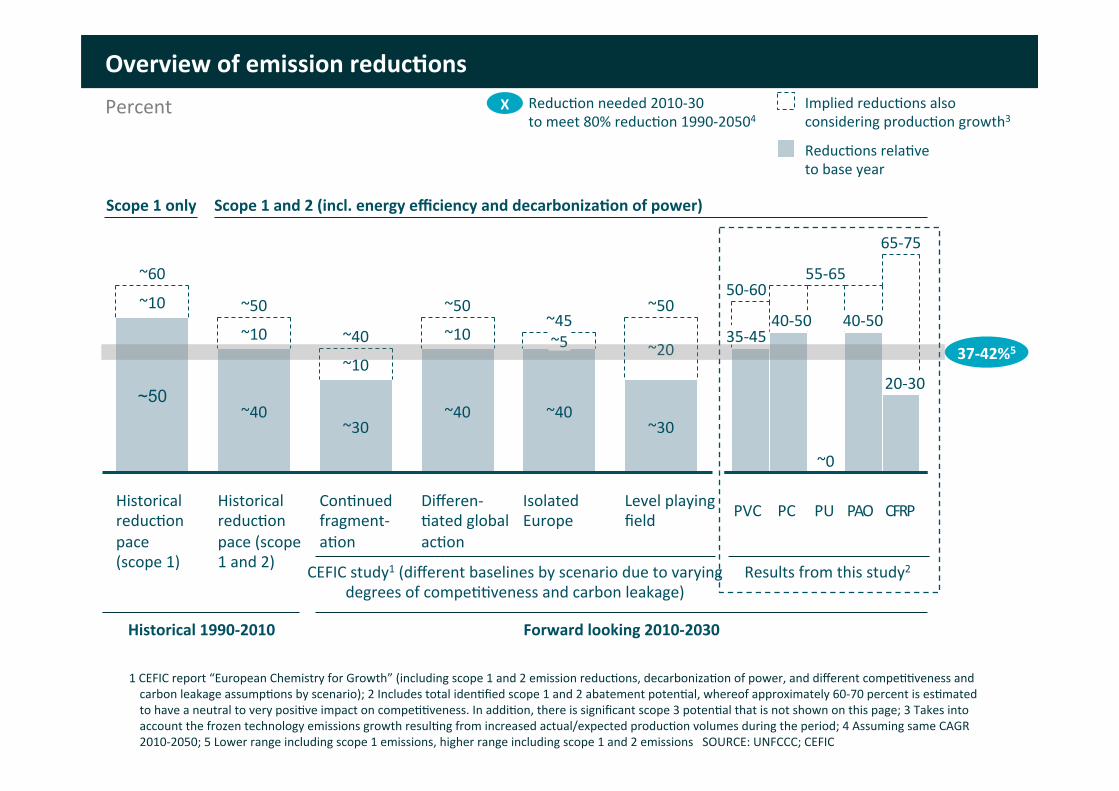

Overview(of(emission(reducEons(

~50!

~30

~20

Isolated!Europe!

~45!

~40

~5

Differen70ated!global!ac0on!!

~50!

~40

~10

Level!playing!field!

~40

~30

~10

Historical!reduc0on!!pace!(scope!1!and!2)!

~50

Con0nued!fragment7a0on!

~10

Historical!reduc0on!!pace!(scope!1)

~60

~50

~10

~40

Reduc0ons!rela0ve!to!base!year!

Implied!reduc0ons!also!considering!produc0on!growth3!

Historical(1990+2010( Forward(looking(2010+2030(

X( Reduc0on!needed!2010730!!to!meet!80%!reduc0on!1990720504!

37+42%5(

Results!from!this!study2!

Scope(1(only( Scope(1(and(2((incl.(energy(efficiency(and(decarbonizaEon(of(power)(

PVC! PC! PU! PAO! CFRP!

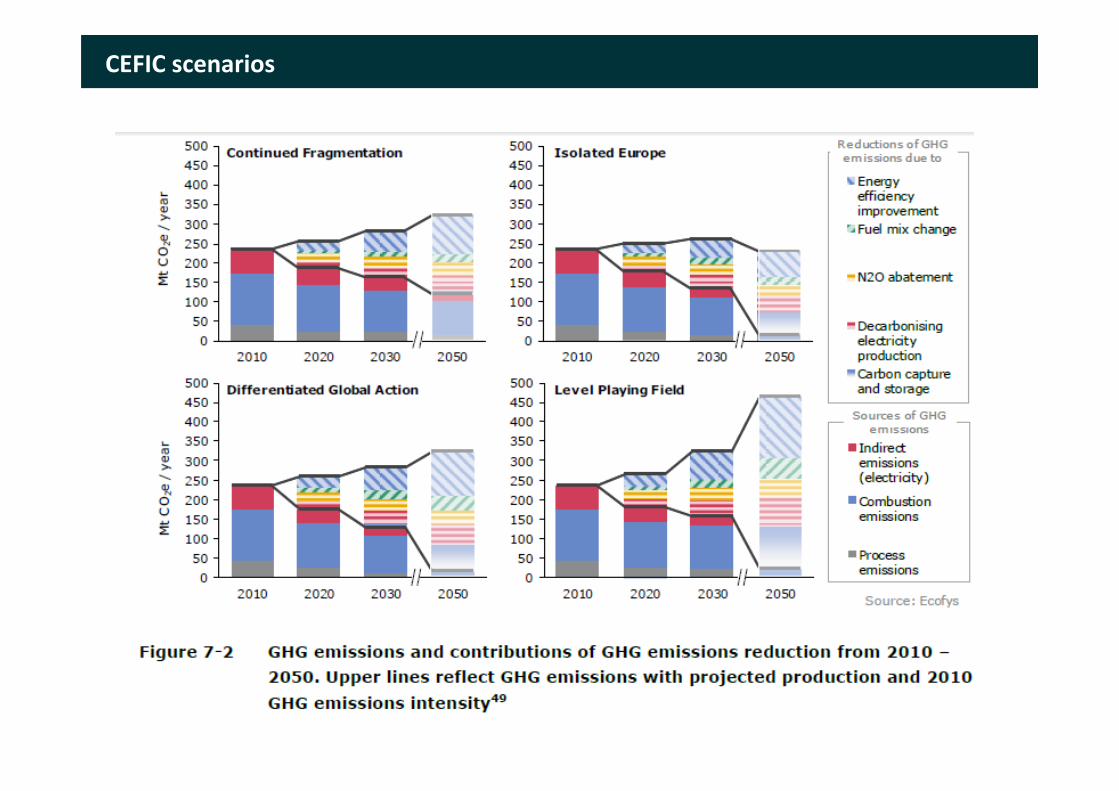

CEFIC!study1!(different!baselines!by!scenario!due!to!varying!degrees!of!compe00veness!and!carbon!leakage)!

Percent!

1!CEFIC!report!“European!Chemistry!for!Growth”!(including!scope!1!and!2!emission!reduc0ons,!decarboniza0on!of!power,!and!different!compe00veness!and!carbon!leakage!assump0ons!by!scenario);!2!Includes!total!iden0fied!scope!1!and!2!abatement!poten0al,!whereof!approximately!60770!percent!is!es0mated!to!have!a!neutral!to!very!posi0ve!impact!on!compe00veness.!In!addi0on,!there!is!significant!scope!3!poten0al!that!is!not!shown!on!this!page;!3!Takes!into!account!the!frozen!technology!emissions!growth!resul0ng!from!increased!actual/expected!produc0on!volumes!during!the!period;!4!Assuming!same!CAGR!201072050;!5!Lower!range!including!scope!1!emissions,!higher!range!including!scope!1!and!2!emissions!!!SOURCE:!UNFCCC;!CEFIC!

Contents(

▪ Mo0va0on!of!the!project!

▪ Competitiveness of the European chemical industry!

▪ What could be done to reduce emissions while maintaining or increasing competitiveness?!

▪ Implications and next steps(

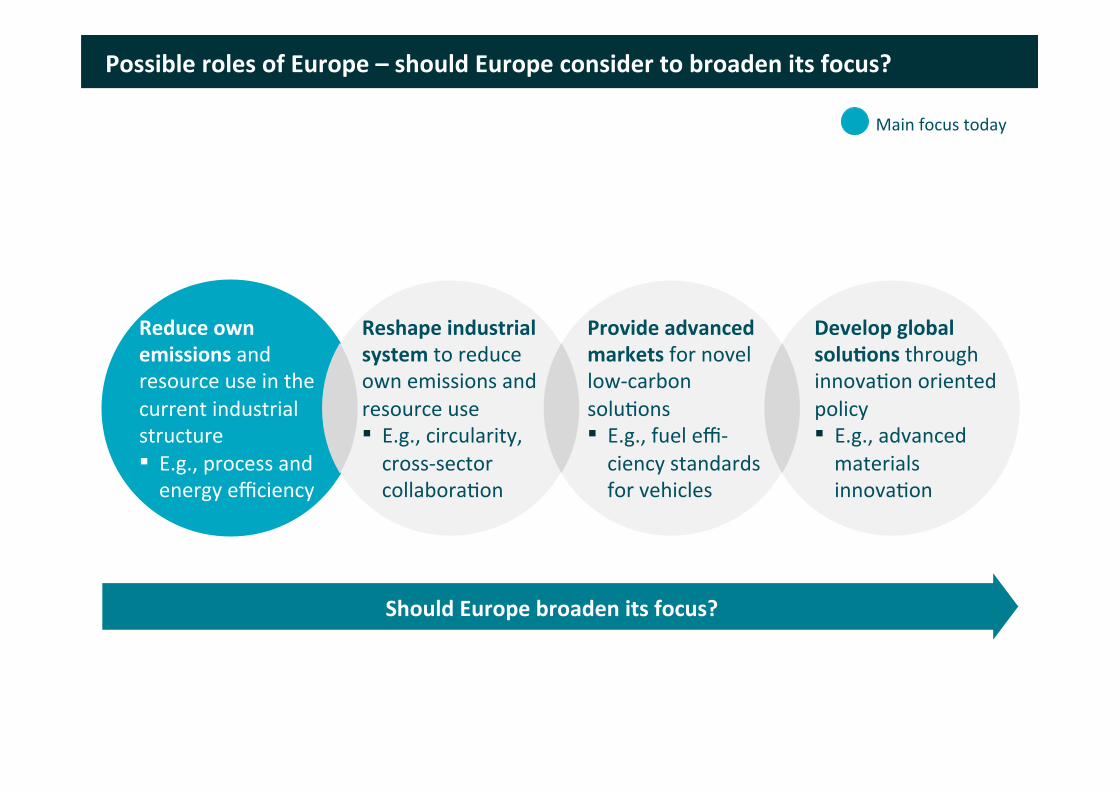

Possible(roles(of(Europe(–(should(Europe(consider(to(broaden(its(focus?(

Should(Europe(broaden(its(focus?(

Main!focus!today!

Reduce(own(emissions(and!resource!use!in!the!current!industrial!structure!▪ E.g.,!process!and!energy!efficiency!

Reshape(industrial(system(to!reduce!own!emissions!and!resource!use!▪ E.g.,!circularity,!cross7sector!collabora0on!

Provide(advanced(markets(for!novel!low7carbon!solu0ons!▪ E.g.,!fuel!effi7ciency!standards!for!vehicles!

Develop(global(soluEons(through!innova0on!oriented!policy!▪ E.g.,!advanced!materials!innova0on!

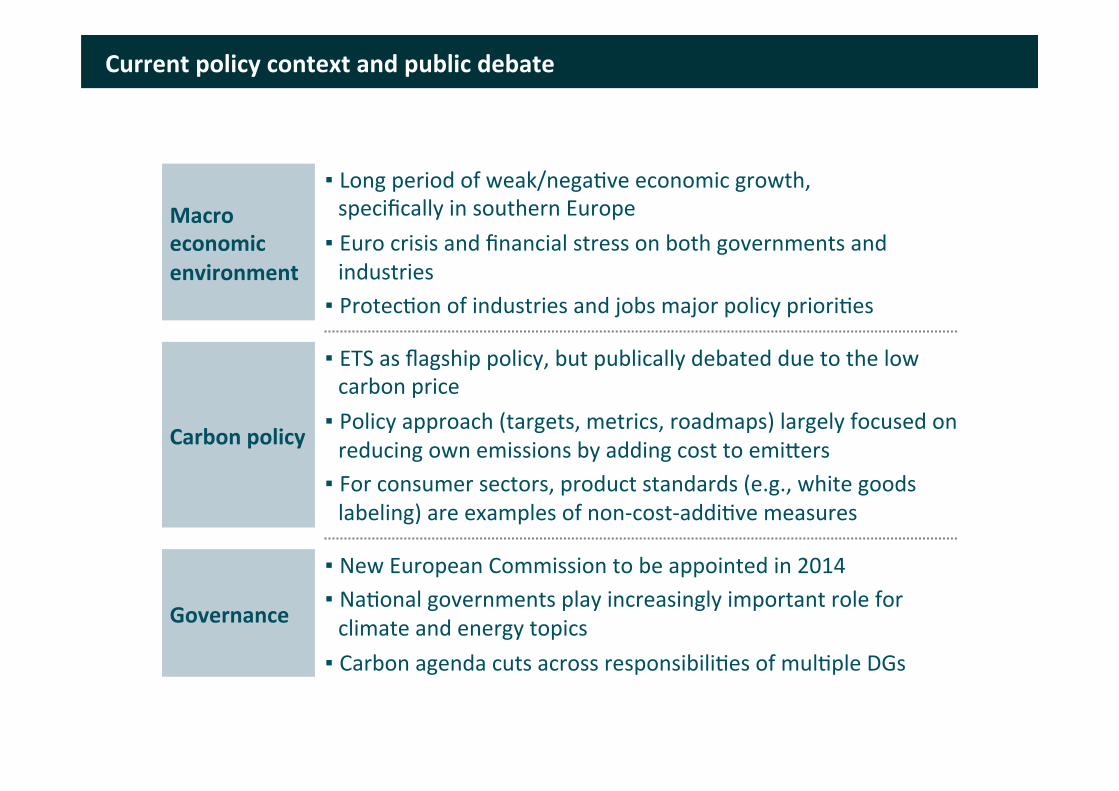

Current(policy(context(and(public(debate(

Carbon(policy(

Macro(economic(environment(

Governance(

▪ New!European!Commission!to!be!appointed!in!2014!▪ Na0onal!governments!play!increasingly!important!role!for!climate!and!energy!topics!▪ Carbon!agenda!cuts!across!responsibili0es!of!mul0ple!DGs!

▪ ETS!as!flagship!policy,!but!publically!debated!due!to!the!low!carbon!price!▪ Policy!approach!(targets,!metrics,!roadmaps)!largely!focused!on!reducing!own!emissions!by!adding!cost!to!emiIers!▪ For!consumer!sectors,!product!standards!(e.g.,!white!goods!labeling)!are!examples!of!non7cost7addi0ve!measures!

▪ Long!period!of!weak/nega0ve!economic!growth,!!specifically!in!southern!Europe!▪ Euro!crisis!and!financial!stress!on!both!governments!and!industries!▪ Protec0on!of!industries!and!jobs!major!policy!priori0es!

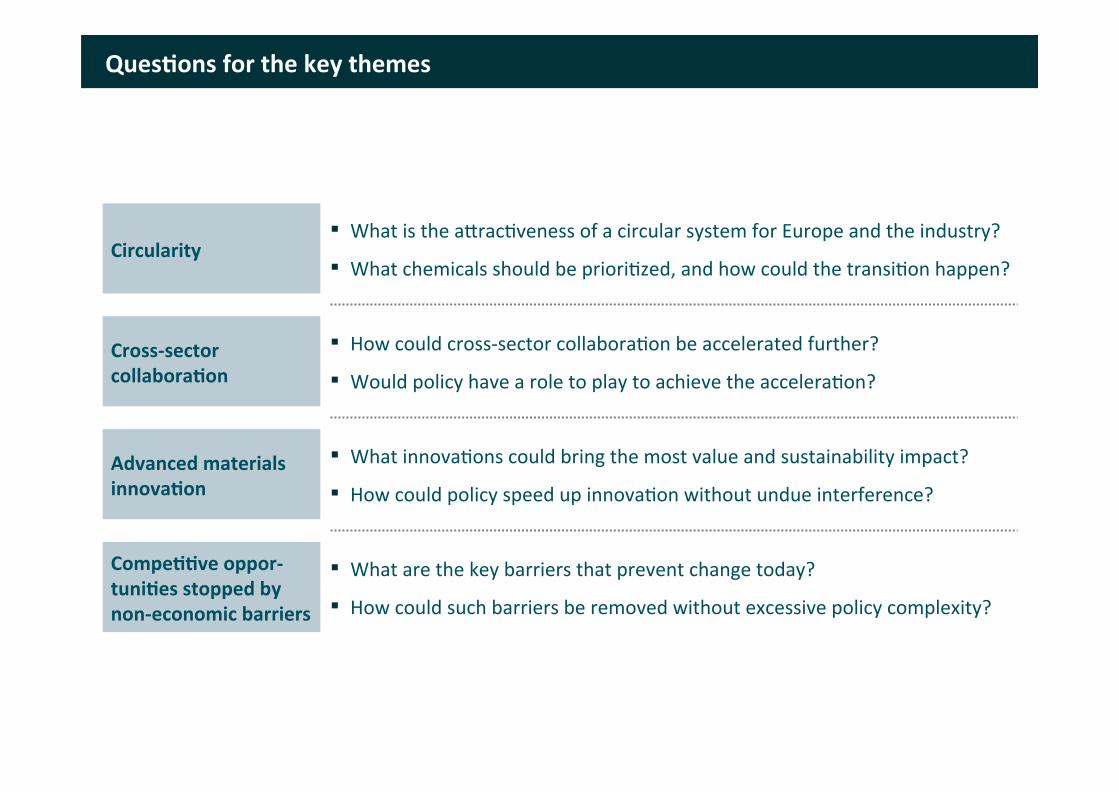

QuesEons(for(the(key(themes(

Circularity(▪ What!is!the!aIrac0veness!of!a!circular!system!for!Europe!and!the!industry?!

▪ What!chemicals!should!be!priori0zed,!and!how!could!the!transi0on!happen?!

Cross+sector(collaboraEon(

▪ How!could!cross7sector!collabora0on!be!accelerated!further?!▪ Would!policy!have!a!role!to!play!to!achieve!the!accelera0on?!

Advanced(materials(innovaEon(

▪ What!innova0ons!could!bring!the!most!value!and!sustainability!impact?!

▪ How!could!policy!speed!up!innova0on!without!undue!interference?!

CompeEEve(oppor+tuniEes(stopped(by(non+economic(barriers(

▪ What!are!the!key!barriers!that!prevent!change!today?!

▪ How!could!such!barriers!be!removed!without!excessive!policy!complexity?!

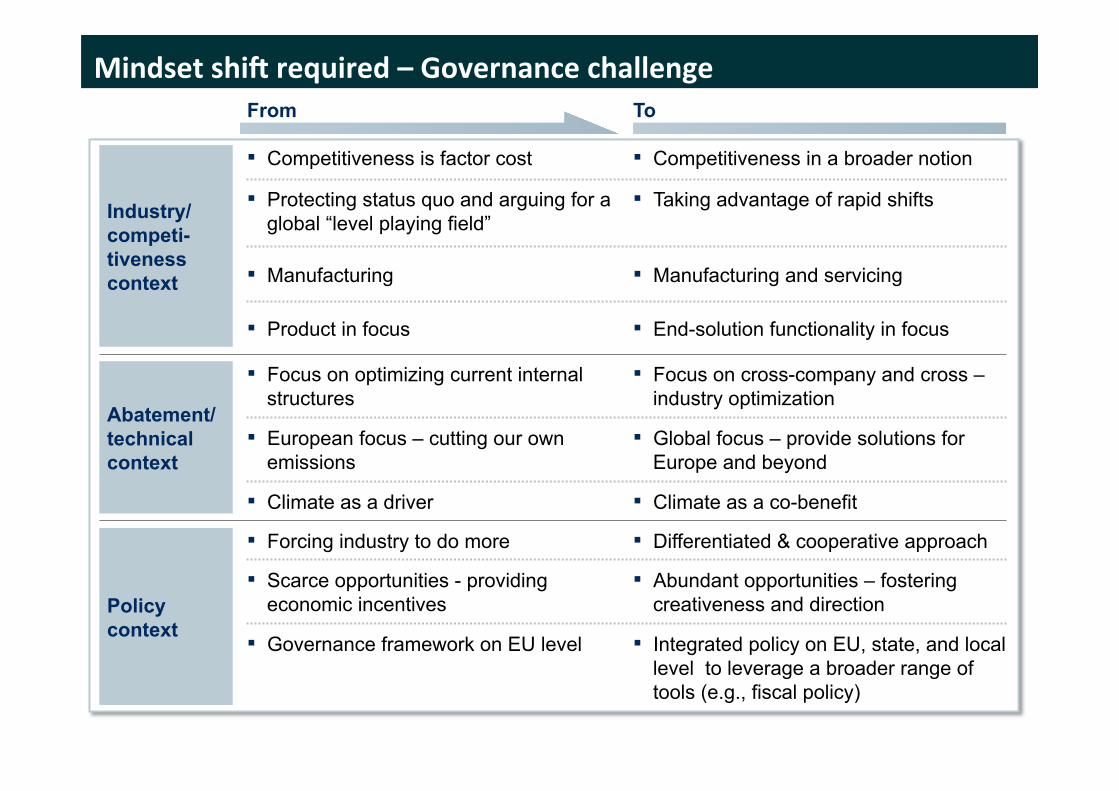

Mindset(shik(required(–(Governance(challenge(

Industry/ competi-tiveness context

Abatement/ technical context

Policy context

From To

▪ Protecting status quo and arguing for a global “level playing field”

▪ Taking advantage of rapid shifts

▪ Competitiveness is factor cost ▪ Competitiveness in a broader notion

▪ Product in focus ▪ End-solution functionality in focus

▪ European focus – cutting our own emissions

▪ Global focus – provide solutions for Europe and beyond

▪ Scarce opportunities - providing economic incentives

▪ Abundant opportunities – fostering creativeness and direction

▪ Forcing industry to do more ▪ Differentiated & cooperative approach

▪ Governance framework on EU level ▪ Integrated policy on EU, state, and local level to leverage a broader range of tools (e.g., fiscal policy)

▪ Focus on optimizing current internal structures

▪ Focus on cross-company and cross –industry optimization

▪ Climate as a driver ▪ Climate as a co-benefit

▪ Manufacturing ▪ Manufacturing and servicing

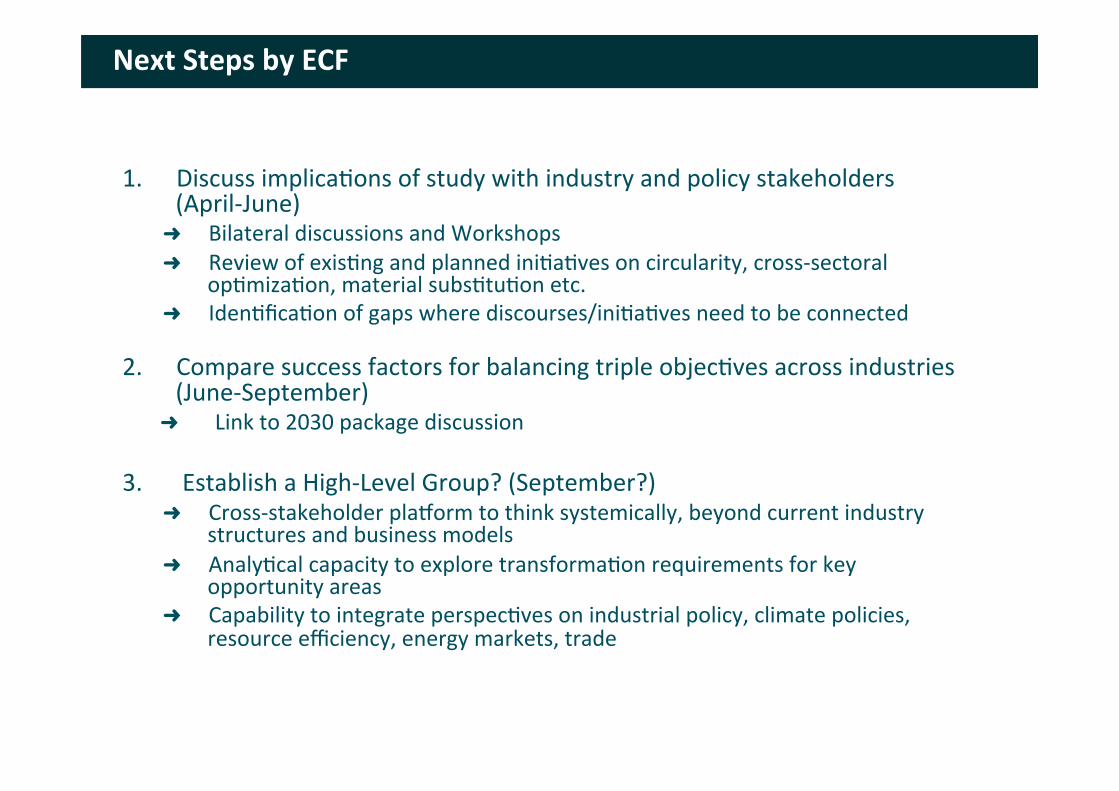

Next(Steps(by(ECF(

1. Discuss!implica0ons!of!study!with!industry!and!policy!stakeholders!(April7June)!� Bilateral!discussions!and!Workshops!!� Review!of!exis0ng!and!planned!ini0a0ves!on!circularity,!cross7sectoral!

op0miza0on,!material!subs0tu0on!etc.!!� Iden0fica0on!of!gaps!where!discourses/ini0a0ves!need!to!be!connected!

!2. Compare!success!factors!for!balancing!triple!objec0ves!across!industries!

(June7September)!� Link!to!2030!package!discussion!

3. !Establish!a!High7Level!Group?!(September?)!� Cross7stakeholder!playorm!to!think!systemically,!beyond!current!industry!

structures!and!business!models!� Analy0cal!capacity!to!explore!transforma0on!requirements!for!key!

opportunity!areas!� Capability!to!integrate!perspec0ves!on!industrial!policy,!climate!policies,!

resource!efficiency,!energy!markets,!trade!

APPENDIX!

CEFIC(scenarios(