Embed Size (px)

Citation preview

Volume 1 Issue 1 2008 Hyderabad Pages 32 July

Spurt in Crude Oil Prices - Reasons & Repercussions

Spurt in Crude Oil Prices - Reasons & Repercussions

Karvy Comtrade's Invest and Harvest

A C o m p r e h e n s i v e E n g l i s h M o n t h l y M a g a z i n e o n C o m m o d i t y F u t u r e s

Article - ATF

Article - Monsoon

Bullion & Metals Review

Agri Market Review & Outlook

National Spot Exchange

Article - ATF

National Spot Exchange

Article - Monsoon

Bullion & Metals Review

Agri Market Review & Outlook

Editorial |

Dear Reader,

With the Crude Oil prices on NYMEX hitting all time high of $145.85 a barrel, the attraction of global economies has turned to find solutions to this price rally. Since most of the countries are dependant on import of petroleum products to meet their demand and is forming large chunk of expenditure of the government. In the recent past, Crude Oil has become an investment avenue following turmoil in global equity market. Since commodity market is inversely related to equity market, the global equity investors including major hedge funds have started diverting their funds into commodity market to get rid of turbulence in equity market. The Cover Story Spurt in Crude Oil Prices - Reasons & Repercussions attempts to find reasons for rally in crude oil prices, supply demand dynamics and how crude oil has emerged as a new investment avenue.

Re-launching of Commodity futures trading in 2003 opened one more investment avenue for Indian investors. Apart from normal investor, commodity market also opened the door for physical traders and corporate houses related to commodities either directly or indirectly. Success of futures trading in commodities attracted attention for setting up of National Spot Exchange on the same lines. The concept of National Spot Exchange emerged to provide single platform for commodities trading expiring on daily basis and contracts culminating into delivery upon expiry of the contract. The article on National Spot Exchange throws light on importance of setting up of National Spot Exchange, its benefits and operational mechanism.

The rally in Crude Oil prices has left no room for airline companies from its adversities because these companies are using Aviation Turbine Fuel to run their aircrafts. Of the total operational cost, expenditure on fuel is around 40% of it. With the operational cost increasing manifold most of the airline companies are cutting flights and postponing plans for fleet acquisition due to lower revenues. The best medicine available to protect the companies from rising oil prices in hedging. In an article Hedging- A Life Saving Drug for Aviation Companies we have discussed importance of hedging.

With much awaited South West Monsoon setting over Indian mainland and its good performance in the month of June has resulted into gearing up of kharif sowing across the country. The article on monsoon throws light on performance of monsoon and sowing progress across the country.

In other segments like Class Room section on Technical Analysis, we will take the readers' through construction of Point and Figure charting technique; its basics, construction and commandments behind such construction. Apart from this, monthly commodity review will update the recent happenings in each of the commodity segments; factors influenced the market and outlook for the coming days.

Ashok MittalEditor

July 2008 | 03

Editor

Ashok Mittal

Research Team

Amand Rajalaxmi

Aurobinda Prasad Gayan

Bhavana Glory

Bitupan Majumdar

Chowdareddy M V

Harish Galipelli

Mithun Maity

Vamsikrishna Kona

Veeresh Hiremath

Vishal Maniyar

Designer

Kumaraswamy B.

Corporate Office

Karvy Comtrade Ltd.

Karvy Centre,

#46, Avenue 4, Street 1

Banjara Hills

Hyderabad - 500 034

Visit Us:

www.karvycomtrade.com

Mail Us:

Printed & Published by S. Gopichand on behalf of Karvy Consultants Limited, Karvy House, 46, Avenue 4, Street No. 1, Banjara Hills, Hyderabad-500 034, A. P. Printed at Harshita Printers, 6-2-985, Yousuf Building, Adj. Railway Gate, Khairatabad, Hyderabad-500 004, A. P. Published at Hyderabad, Editor: Ashok Mittal

Invest & Harvest March 2008 15| “Karvy Centre”, 46, Avenue 4, Street No.1, Banjara Hills, Hyderabad - 500 034.Tel: 040-23388707/23431569/23440653, Fax : 040 - 6625 9955.

An ISO 9001:2000 company

When you trade with Karvy, you trade with a trusted name in the Commodities Market.

Visit us at: www.karvycomtrade.com, email: [email protected]

It’s all about turning the right opportunity into gold

COMTRADE LIMITED

Karvy Comtrade's Invest and Harvest

The Karvy Advantages

Member of NCDEX and MCXNational networkPersonalized servicesBacked by researchSMS alertsDealing facility during night sessionsSingle access number anywhere in India

Editorial |

Dear Reader,

With the Crude Oil prices on NYMEX hitting all time high of $145.85 a barrel, the attraction of global economies has turned to find solutions to this price rally. Since most of the countries are dependant on import of petroleum products to meet their demand and is forming large chunk of expenditure of the government. In the recent past, Crude Oil has become an investment avenue following turmoil in global equity market. Since commodity market is inversely related to equity market, the global equity investors including major hedge funds have started diverting their funds into commodity market to get rid of turbulence in equity market. The Cover Story Spurt in Crude Oil Prices - Reasons & Repercussions attempts to find reasons for rally in crude oil prices, supply demand dynamics and how crude oil has emerged as a new investment avenue.

Re-launching of Commodity futures trading in 2003 opened one more investment avenue for Indian investors. Apart from normal investor, commodity market also opened the door for physical traders and corporate houses related to commodities either directly or indirectly. Success of futures trading in commodities attracted attention for setting up of National Spot Exchange on the same lines. The concept of National Spot Exchange emerged to provide single platform for commodities trading expiring on daily basis and contracts culminating into delivery upon expiry of the contract. The article on National Spot Exchange throws light on importance of setting up of National Spot Exchange, its benefits and operational mechanism.

The rally in Crude Oil prices has left no room for airline companies from its adversities because these companies are using Aviation Turbine Fuel to run their aircrafts. Of the total operational cost, expenditure on fuel is around 40% of it. With the operational cost increasing manifold most of the airline companies are cutting flights and postponing plans for fleet acquisition due to lower revenues. The best medicine available to protect the companies from rising oil prices in hedging. In an article Hedging- A Life Saving Drug for Aviation Companies we have discussed importance of hedging.

With much awaited South West Monsoon setting over Indian mainland and its good performance in the month of June has resulted into gearing up of kharif sowing across the country. The article on monsoon throws light on performance of monsoon and sowing progress across the country.

In other segments like Class Room section on Technical Analysis, we will take the readers' through construction of Point and Figure charting technique; its basics, construction and commandments behind such construction. Apart from this, monthly commodity review will update the recent happenings in each of the commodity segments; factors influenced the market and outlook for the coming days.

Ashok MittalEditor

July 2008 | 03

Editor

Ashok Mittal

Research Team

Amand Rajalaxmi

Aurobinda Prasad Gayan

Bhavana Glory

Bitupan Majumdar

Chowdareddy M V

Harish Galipelli

Mithun Maity

Vamsikrishna Kona

Veeresh Hiremath

Vishal Maniyar

Designer

Kumaraswamy B.

Corporate Office

Karvy Comtrade Ltd.

Karvy Centre,

#46, Avenue 4, Street 1

Banjara Hills

Hyderabad - 500 034

Visit Us:

www.karvycomtrade.com

Mail Us:

Printed & Published by S. Gopichand on behalf of Karvy Consultants Limited, Karvy House, 46, Avenue 4, Street No. 1, Banjara Hills, Hyderabad-500 034, A. P. Printed at Harshita Printers, 6-2-985, Yousuf Building, Adj. Railway Gate, Khairatabad, Hyderabad-500 004, A. P. Published at Hyderabad, Editor: Ashok Mittal

Invest & Harvest March 2008 15| “Karvy Centre”, 46, Avenue 4, Street No.1, Banjara Hills, Hyderabad - 500 034.Tel: 040-23388707/23431569/23440653, Fax : 040 - 6625 9955.

An ISO 9001:2000 company

When you trade with Karvy, you trade with a trusted name in the Commodities Market.

Visit us at: www.karvycomtrade.com, email: [email protected]

It’s all about turning the right opportunity into gold

COMTRADE LIMITED

Karvy Comtrade's Invest and Harvest

The Karvy Advantages

Member of NCDEX and MCXNational networkPersonalized servicesBacked by researchSMS alertsDealing facility during night sessionsSingle access number anywhere in India

Cover Story |

July 02008 5|

Spurt in Crude Oil Prices - Reasons & Repercussions

uman beings are selfish by Nature. According Hto Adam Smith, founder of Capitalism, if each

and every individual tries to maximize their welfare,

then the social welfare will be maximized. Few of us

may not agree with this view as we still believe in a

socialist action. The recent oil price spike explains

basic human behavior - profit motive or in social

term - welfare. From a country perspective, we need

energy resources to sustain in a globalized world.

But the concern is how much oil is left to consume

and how long we can sustain the growth? Many

Capitalists write, the increased consumption in

India and China is leading to supply demand

mismatch in Crude oil. However, if we look at

figures, India and China consume 10% and 36%

respectively of what USA as a country consumes.

However, China and India are the drivers of Asian

growth story and most importantly they need

energy resources to sustain the level. But when the

energy resources are very highly priced it is difficult

for a developing country to look at its country's

balance sheet and adjust the items.

West Texas light crude oil prices rose to historic

highs of $145.85 per barrel after a series of geo-

political tensions stir up in Nigeria, Iraq, Turkey,

Iran and Venezuela and increasing investment flows

into commodities segment. Now, at a time when

entire world economy is struggling to curtail the

inflation caused by higher oil prices, it would be

important to understand the causes of this rally and

possible future course of action.

What caused the price rally? The price of any commodity is determined by

assessing the demand – supply situation and the

perception of market participants. To understand

the rally in Crude prices, we must also look at the

activity of market participants like commercials and

non commercials along with the supply-demand

dynamics. The oil supply side can be determined by

considering two cartels, The OPEC and Non

OPEC.

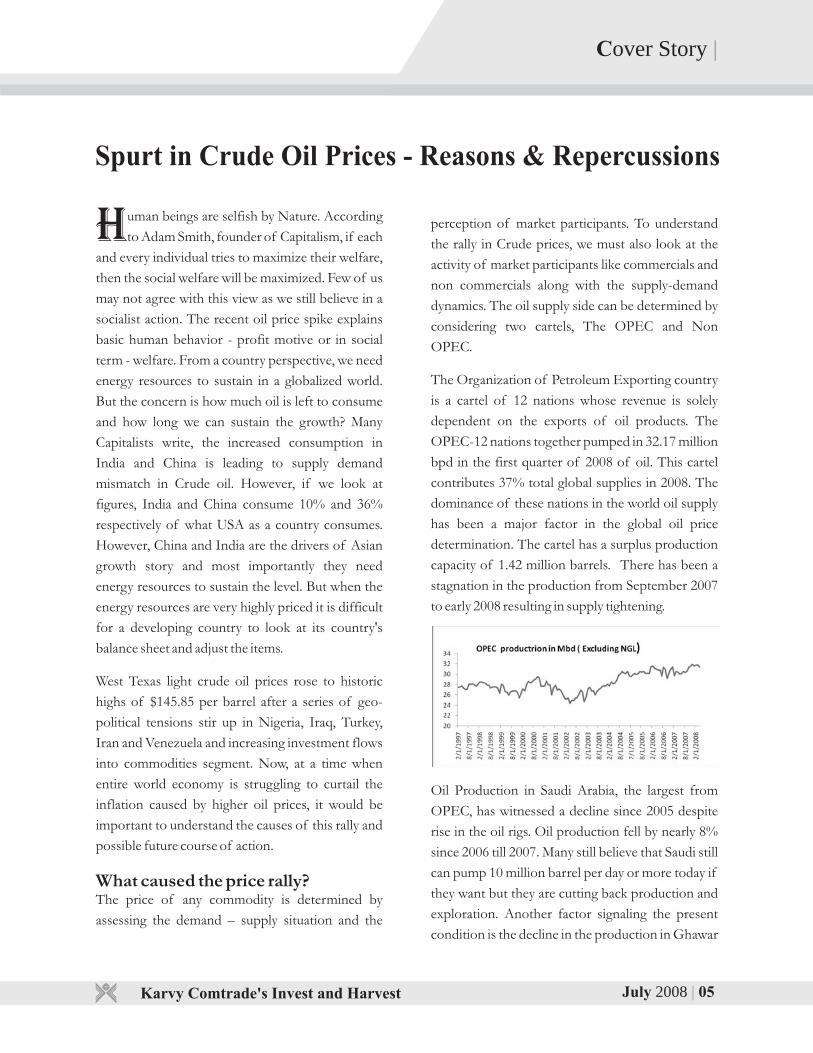

The Organization of Petroleum Exporting country

is a cartel of 12 nations whose revenue is solely

dependent on the exports of oil products. The

OPEC-12 nations together pumped in 32.17 million

bpd in the first quarter of 2008 of oil. This cartel

contributes 37% total global supplies in 2008. The

dominance of these nations in the world oil supply

has been a major factor in the global oil price

determination. The cartel has a surplus production

capacity of 1.42 million barrels. There has been a

stagnation in the production from September 2007

to early 2008 resulting in supply tightening.

Oil Production in Saudi Arabia, the largest from

OPEC, has witnessed a decline since 2005 despite

rise in the oil rigs. Oil production fell by nearly 8%

since 2006 till 2007. Many still believe that Saudi still

can pump 10 million barrel per day or more today if

they want but they are cutting back production and

exploration. Another factor signaling the present

condition is the decline in the production in Ghawar

Contents |

Spurt in Crude Oil Prices - Reasons & Repercussions 05

National Spot Exchange – An Alternate Channel for Physical Traders 11

ATF 14

Monsoon 17

Bullion & Metals Review 19

Agri Market Review & Outlook 22

Class Room 25

Economic Calendar 28

Recommendations 30

July 2008 04| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Cover Story |

July 02008 5|

Spurt in Crude Oil Prices - Reasons & Repercussions

uman beings are selfish by Nature. According Hto Adam Smith, founder of Capitalism, if each

and every individual tries to maximize their welfare,

then the social welfare will be maximized. Few of us

may not agree with this view as we still believe in a

socialist action. The recent oil price spike explains

basic human behavior - profit motive or in social

term - welfare. From a country perspective, we need

energy resources to sustain in a globalized world.

But the concern is how much oil is left to consume

and how long we can sustain the growth? Many

Capitalists write, the increased consumption in

India and China is leading to supply demand

mismatch in Crude oil. However, if we look at

figures, India and China consume 10% and 36%

respectively of what USA as a country consumes.

However, China and India are the drivers of Asian

growth story and most importantly they need

energy resources to sustain the level. But when the

energy resources are very highly priced it is difficult

for a developing country to look at its country's

balance sheet and adjust the items.

West Texas light crude oil prices rose to historic

highs of $145.85 per barrel after a series of geo-

political tensions stir up in Nigeria, Iraq, Turkey,

Iran and Venezuela and increasing investment flows

into commodities segment. Now, at a time when

entire world economy is struggling to curtail the

inflation caused by higher oil prices, it would be

important to understand the causes of this rally and

possible future course of action.

What caused the price rally? The price of any commodity is determined by

assessing the demand – supply situation and the

perception of market participants. To understand

the rally in Crude prices, we must also look at the

activity of market participants like commercials and

non commercials along with the supply-demand

dynamics. The oil supply side can be determined by

considering two cartels, The OPEC and Non

OPEC.

The Organization of Petroleum Exporting country

is a cartel of 12 nations whose revenue is solely

dependent on the exports of oil products. The

OPEC-12 nations together pumped in 32.17 million

bpd in the first quarter of 2008 of oil. This cartel

contributes 37% total global supplies in 2008. The

dominance of these nations in the world oil supply

has been a major factor in the global oil price

determination. The cartel has a surplus production

capacity of 1.42 million barrels. There has been a

stagnation in the production from September 2007

to early 2008 resulting in supply tightening.

Oil Production in Saudi Arabia, the largest from

OPEC, has witnessed a decline since 2005 despite

rise in the oil rigs. Oil production fell by nearly 8%

since 2006 till 2007. Many still believe that Saudi still

can pump 10 million barrel per day or more today if

they want but they are cutting back production and

exploration. Another factor signaling the present

condition is the decline in the production in Ghawar

Contents |

Spurt in Crude Oil Prices - Reasons & Repercussions 05

National Spot Exchange – An Alternate Channel for Physical Traders 11

ATF 14

Monsoon 17

Bullion & Metals Review 19

Agri Market Review & Outlook 22

Class Room 25

Economic Calendar 28

Recommendations 30

July 2008 04| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

July 02008 7|

Cover Story |

conditions. Reserves-to-production (R/P) ratio– If the

reserves remaining at the end of any year are divided by the

production in that year, the result is the length of time that those

remaining reserves would last if production were to continue at

that rate.

Ceteris paribus the proven conventional oil reserves

can serve the world one more century with present

production capacity. However, there can be likely

addition in the oil reserves in the coming days with

advancement of technology and rise in the prices.

And at the same time we may see a growing

popularity of other alternative sources of energy

with crude oil as a scare resource.

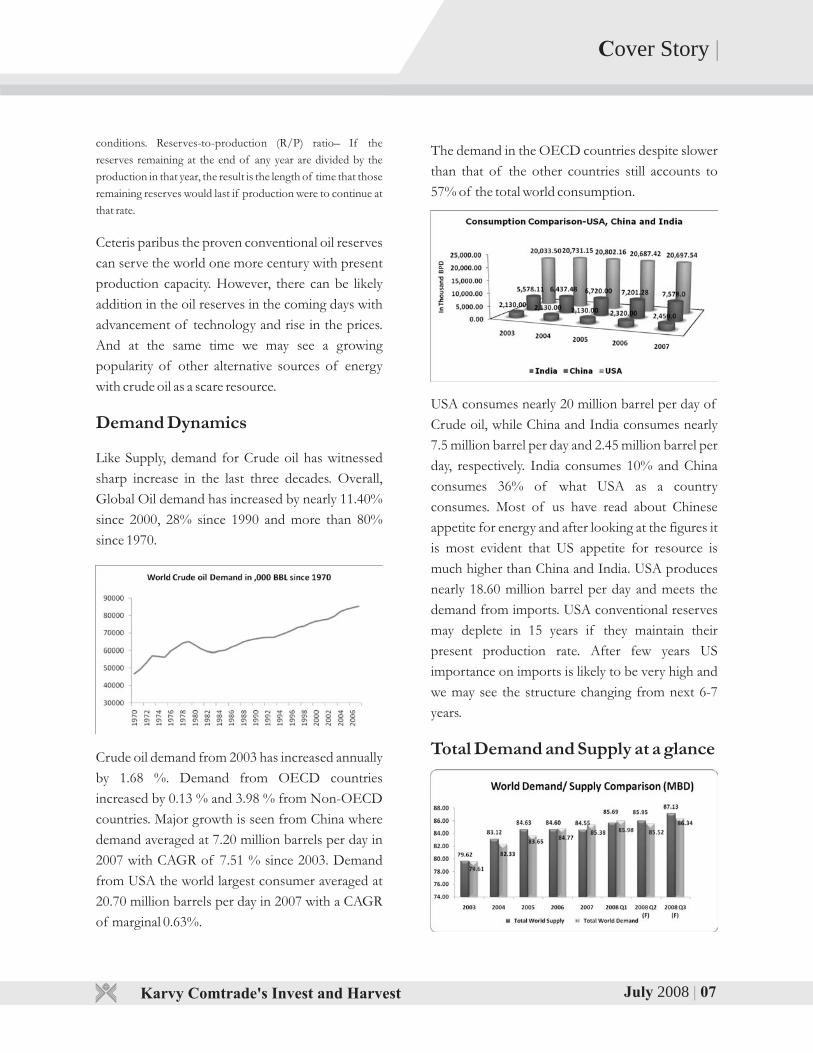

Demand Dynamics

Like Supply, demand for Crude oil has witnessed

sharp increase in the last three decades. Overall,

Global Oil demand has increased by nearly 11.40%

since 2000, 28% since 1990 and more than 80%

since 1970.

Crude oil demand from 2003 has increased annually

by 1.68 %. Demand from OECD countries

increased by 0.13 % and 3.98 % from Non-OECD

countries. Major growth is seen from China where

demand averaged at 7.20 million barrels per day in

2007 with CAGR of 7.51 % since 2003. Demand

from USA the world largest consumer averaged at

20.70 million barrels per day in 2007 with a CAGR

of marginal 0.63%.

The demand in the OECD countries despite slower

than that of the other countries still accounts to

57% of the total world consumption.

USA consumes nearly 20 million barrel per day of

Crude oil, while China and India consumes nearly

7.5 million barrel per day and 2.45 million barrel per

day, respectively. India consumes 10% and China

consumes 36% of what USA as a country

consumes. Most of us have read about Chinese

appetite for energy and after looking at the figures it

is most evident that US appetite for resource is

much higher than China and India. USA produces

nearly 18.60 million barrel per day and meets the

demand from imports. USA conventional reserves

may deplete in 15 years if they maintain their

present production rate. After few years US

importance on imports is likely to be very high and

we may see the structure changing from next 6-7

years.

Total Demand and Supply at a glance

Cover Story |

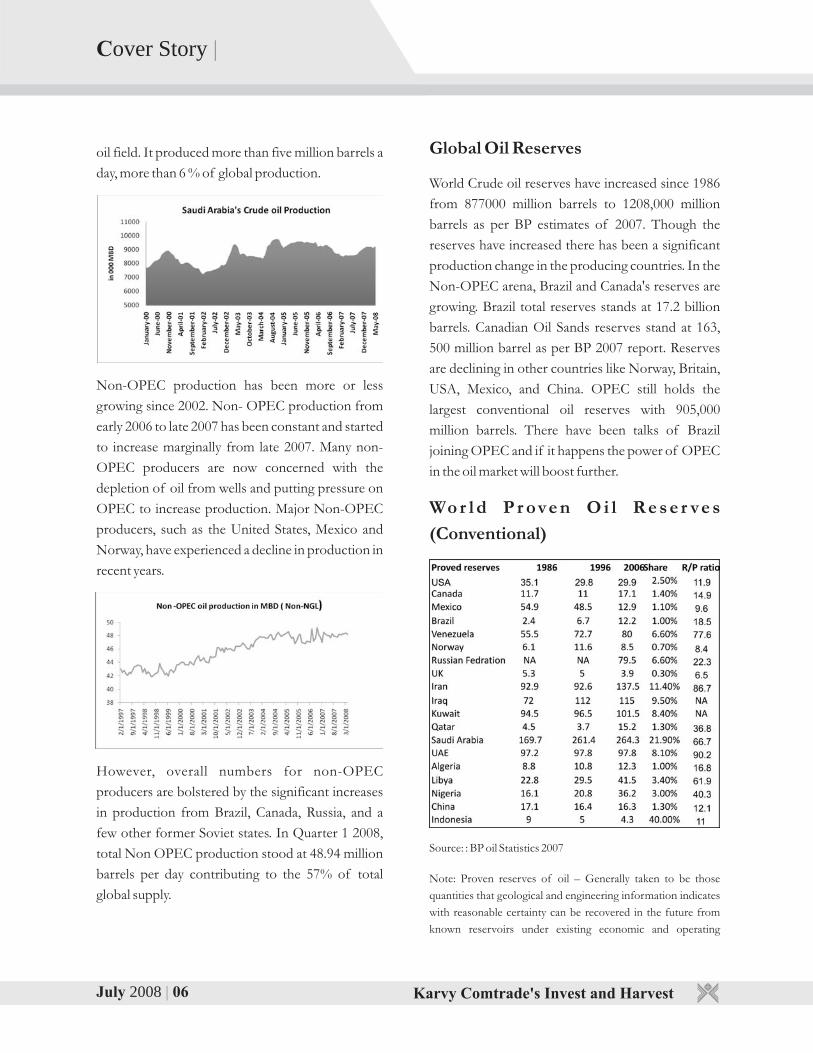

oil field. It produced more than five million barrels a

day, more than 6 % of global production.

Non-OPEC production has been more or less

growing since 2002. Non- OPEC production from

early 2006 to late 2007 has been constant and started

to increase marginally from late 2007. Many non-

OPEC producers are now concerned with the

depletion of oil from wells and putting pressure on

OPEC to increase production. Major Non-OPEC

producers, such as the United States, Mexico and

Norway, have experienced a decline in production in

recent years.

However, overall numbers for non-OPEC

producers are bolstered by the significant increases

in production from Brazil, Canada, Russia, and a

few other former Soviet states. In Quarter 1 2008,

total Non OPEC production stood at 48.94 million

barrels per day contributing to the 57% of total

global supply.

Global Oil Reserves

World Crude oil reserves have increased since 1986

from 877000 million barrels to 1208,000 million

barrels as per BP estimates of 2007. Though the

reserves have increased there has been a significant

production change in the producing countries. In the

Non-OPEC arena, Brazil and Canada's reserves are

growing. Brazil total reserves stands at 17.2 billion

barrels. Canadian Oil Sands reserves stand at 163,

500 million barrel as per BP 2007 report. Reserves

are declining in other countries like Norway, Britain,

USA, Mexico, and China. OPEC still holds the

largest conventional oil reserves with 905,000

million barrels. There have been talks of Brazil

joining OPEC and if it happens the power of OPEC

in the oil market will boost further.

Wo r l d P r ove n O i l Re s e r ve s

(Conventional)

Source:

Note: Proven reserves of oil – Generally taken to be those

quantities that geological and engineering information indicates

with reasonable certainty can be recovered in the future from

known reservoirs under existing economic and operating

: BP oil Statistics 2007

July 2008 06| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

July 02008 7|

Cover Story |

conditions. Reserves-to-production (R/P) ratio– If the

reserves remaining at the end of any year are divided by the

production in that year, the result is the length of time that those

remaining reserves would last if production were to continue at

that rate.

Ceteris paribus the proven conventional oil reserves

can serve the world one more century with present

production capacity. However, there can be likely

addition in the oil reserves in the coming days with

advancement of technology and rise in the prices.

And at the same time we may see a growing

popularity of other alternative sources of energy

with crude oil as a scare resource.

Demand Dynamics

Like Supply, demand for Crude oil has witnessed

sharp increase in the last three decades. Overall,

Global Oil demand has increased by nearly 11.40%

since 2000, 28% since 1990 and more than 80%

since 1970.

Crude oil demand from 2003 has increased annually

by 1.68 %. Demand from OECD countries

increased by 0.13 % and 3.98 % from Non-OECD

countries. Major growth is seen from China where

demand averaged at 7.20 million barrels per day in

2007 with CAGR of 7.51 % since 2003. Demand

from USA the world largest consumer averaged at

20.70 million barrels per day in 2007 with a CAGR

of marginal 0.63%.

The demand in the OECD countries despite slower

than that of the other countries still accounts to

57% of the total world consumption.

USA consumes nearly 20 million barrel per day of

Crude oil, while China and India consumes nearly

7.5 million barrel per day and 2.45 million barrel per

day, respectively. India consumes 10% and China

consumes 36% of what USA as a country

consumes. Most of us have read about Chinese

appetite for energy and after looking at the figures it

is most evident that US appetite for resource is

much higher than China and India. USA produces

nearly 18.60 million barrel per day and meets the

demand from imports. USA conventional reserves

may deplete in 15 years if they maintain their

present production rate. After few years US

importance on imports is likely to be very high and

we may see the structure changing from next 6-7

years.

Total Demand and Supply at a glance

Cover Story |

oil field. It produced more than five million barrels a

day, more than 6 % of global production.

Non-OPEC production has been more or less

growing since 2002. Non- OPEC production from

early 2006 to late 2007 has been constant and started

to increase marginally from late 2007. Many non-

OPEC producers are now concerned with the

depletion of oil from wells and putting pressure on

OPEC to increase production. Major Non-OPEC

producers, such as the United States, Mexico and

Norway, have experienced a decline in production in

recent years.

However, overall numbers for non-OPEC

producers are bolstered by the significant increases

in production from Brazil, Canada, Russia, and a

few other former Soviet states. In Quarter 1 2008,

total Non OPEC production stood at 48.94 million

barrels per day contributing to the 57% of total

global supply.

Global Oil Reserves

World Crude oil reserves have increased since 1986

from 877000 million barrels to 1208,000 million

barrels as per BP estimates of 2007. Though the

reserves have increased there has been a significant

production change in the producing countries. In the

Non-OPEC arena, Brazil and Canada's reserves are

growing. Brazil total reserves stands at 17.2 billion

barrels. Canadian Oil Sands reserves stand at 163,

500 million barrel as per BP 2007 report. Reserves

are declining in other countries like Norway, Britain,

USA, Mexico, and China. OPEC still holds the

largest conventional oil reserves with 905,000

million barrels. There have been talks of Brazil

joining OPEC and if it happens the power of OPEC

in the oil market will boost further.

Wo r l d P r ove n O i l Re s e r ve s

(Conventional)

Source:

Note: Proven reserves of oil – Generally taken to be those

quantities that geological and engineering information indicates

with reasonable certainty can be recovered in the future from

known reservoirs under existing economic and operating

: BP oil Statistics 2007

July 2008 06| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

July 02008 9| July 2008 08|

Cover Story |

Inspite of demand crunch experienced in the

OECD countries the total demand for oil still

exceeds the supply supporting the higher oil prices.

In Q1 2008 the demand outpaced supply by 0.29

million barrels per day. Hence any supply disrutpion

to the existing sources is likely to cause an uptrend

in prices.

Investment Demand

Commodities as an asset class have returns

independent to the other asset classes. They are

positively correlated with inflation unlike equities

being negatively correlated. Hence, a completely

new dimension to the fundamentals of

commodities prices has evolved. Apart from the

demand and supply being neck on neck, the factors

like flow of investment into commodities by large

hedge funds, pension funds have given a new

dimension to the market. This has majorly

accounted to the surge in prices apart from the usual

demand and supply dynamics. The poor

performance of the equity markets has resulted in

the transfer of funds into the commodity complex.

The S&P GSCI commodity index, which takes into

account the 24 commodities with the major

component comprising of the Energy sector, has

outperformed the equity index. For the period of

Jan 1 2008 to June 26th 2008, the returns in the

GSCI index stood at 31% against the negative

returns of the Dow Industrial Average index of

13%. This shows that the participation in the

commodity index has been seen as an investment

opportunity yielding positive returns.

Geopolitical Tension

The decline in the oil production in the Mexico and

the recent political tiff with the Venezuela have

posed a significant threat to the US energy security.

Any political disputes from Venezuela may create

significant disturbance in the trade flows for US and

may see a sharp rally in the oil prices. Venezuela

pumps 2.15 million barrel per day and nearly 1.35

million barrel per day goes US refineries.

Iran's Standoff against West on

Nuclear Issue

Iran's nuclear program started in 1950's and

continued into the 1970s with the support,

encouragement and participation of the United

States and Western European governments. After

the Iranian Revolution in 1979, the Iranian

government temporarily disbanded elements of the

program, and then revived it with less Western

assistance than during the pre-revolution era. On 31

July 2006, the United Nations Security Council

demanded Iran to suspend all enrichment and

reprocessing related activities. In December 2006, it

imposed a series of sanctions on Iran for its non-

compliance with the earlier Security Council

resolution deciding that Iran suspends enrichment-

related activities without delay. These sanctions were

primarily targeted against the transfer of nuclear and

ballistic missile technologies and, in response to

concerns of China and Russia, were lighter than that

sought by the United States. The sanctions were

further extended in March 2008 to cover additional

financial institutions, restrict travel of additional

Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

persons, and bar exports of nuclear- and missile-

related dual-use goods to Iran.

The recent political comment from the western

leaders and most recently from Israel is creating

nervous market sentiments. Iran is the fourth largest

producer and also ranks fourth in world's oil reserve.

Iran is producing nearly 3.8 million barrels per day

which is near to 5% of the world oil production. Any

possible attack on Iran may lead to shortage of

crude oil in the world energy market.

Nigerian Oil crisis

The extraction and drilling of petroleum in Nigeria

is the largest industry and main generator of GDP in

the West Africa. Nigeria holds nearly 3.6 billion

barrels of crude oil which makes it the tenth most

petroleum-rich nation. Most of the country's

reserves are concentrated in and around the delta of

the Niger River. The Nigerian government, along

with foreign oil companies, has reaped enormous

profits over the years from the sale of oil and gas

reserves, while the residents of the Niger Delta live

in abject poverty. This has resulted in agitation by

the MEND against the oil fields. Successive military

dictatorships have been accused by Nigeria's anti-

corruption commission of embezzling $400bn in

oil windfalls. According to the Berlin-based anti-

corruption watchdog Transparency International,

Nigeria is one of the most corrupt countries in the

world - where graft is seen as "rampant". Political

instability and attack on oil facilities by the Nigerian

rebels has resulted significant disruption of Crude

oil last year. The frequent attacks of rebels had sent

25 % of oil production offline last year. The

continuing geopolitical tensions in the Niger belt

have resulted in Angola taking its position as the

largest producing African nation.

Weakness of American Dollar

US dollar has depreciated significantly against all

other major European and Asian currencies. The

housing woes, Credit market turmoil, rising

unemployment led the US dollar to depreciate to

historic lows against Euro, 11 years low against JPY

and near 7 years low against GBP. Crude oil is priced

in Dollar in major international trading and volatility

in the USD rates may cause considerable effect on

prices. Recent surge in oil prices is also attributed to

the decline in the USD apart from ongoing geo-

political tensions. In 2008, Light sweet oil prices in

Dollar terms went up by 40.81 % while it has

declined in euro terms by nearly 5.85 % and rose

nearly 34 % in terms of JPY.

Conclusion

The geo-political tension and falling dollar is

guiding string of fund based investment in the

commodities market. There has not been actual

deficiency in the oil supply and market players are

betting on the potential supply disruption which is

creating risk premium to the prices. However,

whether the price is justified or not but it is causing

serious consequences to the global economy. In the

futures market, Crude oil prices are trading above

$140 dollar a barrel and market players are betting

on $200 a barrel in the near future is having its

serious repercussion on the global growth rate. With

the majority of nation's dependant on imports for

their energy uses the continuous rise in prices is

burdening these governments in order to meet their

needs. It seems unbearable for oil importing

countries like USA, Japan, China, and India to bear

such a high prices. It leads to high consumer

inflation with trickle down effect. The increase in

price to $140 levels are on back of the geopolitical

Cover Story |

July 02008 9| July 2008 08|

Cover Story |

Inspite of demand crunch experienced in the

OECD countries the total demand for oil still

exceeds the supply supporting the higher oil prices.

In Q1 2008 the demand outpaced supply by 0.29

million barrels per day. Hence any supply disrutpion

to the existing sources is likely to cause an uptrend

in prices.

Investment Demand

Commodities as an asset class have returns

independent to the other asset classes. They are

positively correlated with inflation unlike equities

being negatively correlated. Hence, a completely

new dimension to the fundamentals of

commodities prices has evolved. Apart from the

demand and supply being neck on neck, the factors

like flow of investment into commodities by large

hedge funds, pension funds have given a new

dimension to the market. This has majorly

accounted to the surge in prices apart from the usual

demand and supply dynamics. The poor

performance of the equity markets has resulted in

the transfer of funds into the commodity complex.

The S&P GSCI commodity index, which takes into

account the 24 commodities with the major

component comprising of the Energy sector, has

outperformed the equity index. For the period of

Jan 1 2008 to June 26th 2008, the returns in the

GSCI index stood at 31% against the negative

returns of the Dow Industrial Average index of

13%. This shows that the participation in the

commodity index has been seen as an investment

opportunity yielding positive returns.

Geopolitical Tension

The decline in the oil production in the Mexico and

the recent political tiff with the Venezuela have

posed a significant threat to the US energy security.

Any political disputes from Venezuela may create

significant disturbance in the trade flows for US and

may see a sharp rally in the oil prices. Venezuela

pumps 2.15 million barrel per day and nearly 1.35

million barrel per day goes US refineries.

Iran's Standoff against West on

Nuclear Issue

Iran's nuclear program started in 1950's and

continued into the 1970s with the support,

encouragement and participation of the United

States and Western European governments. After

the Iranian Revolution in 1979, the Iranian

government temporarily disbanded elements of the

program, and then revived it with less Western

assistance than during the pre-revolution era. On 31

July 2006, the United Nations Security Council

demanded Iran to suspend all enrichment and

reprocessing related activities. In December 2006, it

imposed a series of sanctions on Iran for its non-

compliance with the earlier Security Council

resolution deciding that Iran suspends enrichment-

related activities without delay. These sanctions were

primarily targeted against the transfer of nuclear and

ballistic missile technologies and, in response to

concerns of China and Russia, were lighter than that

sought by the United States. The sanctions were

further extended in March 2008 to cover additional

financial institutions, restrict travel of additional

Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

persons, and bar exports of nuclear- and missile-

related dual-use goods to Iran.

The recent political comment from the western

leaders and most recently from Israel is creating

nervous market sentiments. Iran is the fourth largest

producer and also ranks fourth in world's oil reserve.

Iran is producing nearly 3.8 million barrels per day

which is near to 5% of the world oil production. Any

possible attack on Iran may lead to shortage of

crude oil in the world energy market.

Nigerian Oil crisis

The extraction and drilling of petroleum in Nigeria

is the largest industry and main generator of GDP in

the West Africa. Nigeria holds nearly 3.6 billion

barrels of crude oil which makes it the tenth most

petroleum-rich nation. Most of the country's

reserves are concentrated in and around the delta of

the Niger River. The Nigerian government, along

with foreign oil companies, has reaped enormous

profits over the years from the sale of oil and gas

reserves, while the residents of the Niger Delta live

in abject poverty. This has resulted in agitation by

the MEND against the oil fields. Successive military

dictatorships have been accused by Nigeria's anti-

corruption commission of embezzling $400bn in

oil windfalls. According to the Berlin-based anti-

corruption watchdog Transparency International,

Nigeria is one of the most corrupt countries in the

world - where graft is seen as "rampant". Political

instability and attack on oil facilities by the Nigerian

rebels has resulted significant disruption of Crude

oil last year. The frequent attacks of rebels had sent

25 % of oil production offline last year. The

continuing geopolitical tensions in the Niger belt

have resulted in Angola taking its position as the

largest producing African nation.

Weakness of American Dollar

US dollar has depreciated significantly against all

other major European and Asian currencies. The

housing woes, Credit market turmoil, rising

unemployment led the US dollar to depreciate to

historic lows against Euro, 11 years low against JPY

and near 7 years low against GBP. Crude oil is priced

in Dollar in major international trading and volatility

in the USD rates may cause considerable effect on

prices. Recent surge in oil prices is also attributed to

the decline in the USD apart from ongoing geo-

political tensions. In 2008, Light sweet oil prices in

Dollar terms went up by 40.81 % while it has

declined in euro terms by nearly 5.85 % and rose

nearly 34 % in terms of JPY.

Conclusion

The geo-political tension and falling dollar is

guiding string of fund based investment in the

commodities market. There has not been actual

deficiency in the oil supply and market players are

betting on the potential supply disruption which is

creating risk premium to the prices. However,

whether the price is justified or not but it is causing

serious consequences to the global economy. In the

futures market, Crude oil prices are trading above

$140 dollar a barrel and market players are betting

on $200 a barrel in the near future is having its

serious repercussion on the global growth rate. With

the majority of nation's dependant on imports for

their energy uses the continuous rise in prices is

burdening these governments in order to meet their

needs. It seems unbearable for oil importing

countries like USA, Japan, China, and India to bear

such a high prices. It leads to high consumer

inflation with trickle down effect. The increase in

price to $140 levels are on back of the geopolitical

Cover Story |

July 2008 11| July 2008 10| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Focus |

Re-launching of Commodity futures trading in 2003

opened one more investment avenue for Indian

investors. Apart from normal investor, commodity

market also opened the door for physical traders and

corporate houses related to commodities either

directly or indirectly. Success of futures trading in

commodities attracted attention for setting up of

National Spot Exchange on the same lines.

The concept of National Spot Exchange emerged

to provide single platform for commodities trading

expiring on daily basis and contracts culminating

into delivery upon expiry of the contract. This

concept is intended to meet needs of physical

traders. It is national level institutionalized,

electronic and transparent exchange. It is a state-of

the-art unique market place providing customized

solutions to various problems faced by the farmers,

traders, processors, exporters, importers,

arbitrageurs, investors and the general mass.

Promoters

The National Spot Exchange is promoted by Multi

Commodity Exchange of India, Financial

Technologies India Ltd. and National Agricultural

Cooperative Marketing Federation of India Ltd.

MCX (Multi Commodity Exchange of India

Limited), the leading commodity exchange in India,

provides futures trading in more than 70

commodities. It is also amongst the top three

Exchanges in the world in bullion futures.

FTIL (Financial Technologies India Limited) is

among the very few companies globally that offers

exhaustive solutions library for Exchanges, provides

technology solutions to financial markets and

facilitates expansion of stock broking terminals.

NAFED (National Agricultural Cooperative

Marketing Federation of India Limited), the leading

Government agency, engages in food procurement,

distribution and storage activities.

Objectives

1. To develop a Common Indian Market, by

setting up a national level electronic spot

market and providing a state of art trading,

delivery and settlement facilities in various

commodities, which can be accessed from

across the country.

2. To provide an effective method of spot price

discovery in various commodities, in a

transparent manner from across the country.

3. To create a market where farmers can sell their

produce and realize sale proceeds at the best

prevailing price.

4. To create a market where the processors, end

users, exporters, corporates (both private and

government) and other upcountry traders can

procure agricultural produces at the most

competitive price, without any counter party

and quality risk.

5. To create a transparent market where financiers,

investors and arbitrageurs can invest money in

buying various commodities across the country

without going through the hassles of physical

market.

6. To provide authentic spot price of various

commodities that can be used by the futures

market as the benchmark price for settlement

of their contracts on the date of expiry.

National Spot Exchange – An Alternate Channel for Physical Traders

Subscribe for commodity alerts

through SMS

Logon to www.karvycomtrade.com

tension in the oil exporting nations thereby spurting

the supply concerns. In tune it's leading to the rise in

fuel costs across the world hence impacting the

growth rates by increasing inflationary pressures.

A global standoff on the higher oil prices is likely to

come by if there is a continued increase in prices.

This might lead to use of alternatives or discover

the new sources of energy. Will this hold ahead a

future for innovation or substitution of oil for the

energy consumption is yet to be discovered.

Cover Story |

July 2008 11| July 2008 10| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Focus |

Re-launching of Commodity futures trading in 2003

opened one more investment avenue for Indian

investors. Apart from normal investor, commodity

market also opened the door for physical traders and

corporate houses related to commodities either

directly or indirectly. Success of futures trading in

commodities attracted attention for setting up of

National Spot Exchange on the same lines.

The concept of National Spot Exchange emerged

to provide single platform for commodities trading

expiring on daily basis and contracts culminating

into delivery upon expiry of the contract. This

concept is intended to meet needs of physical

traders. It is national level institutionalized,

electronic and transparent exchange. It is a state-of

the-art unique market place providing customized

solutions to various problems faced by the farmers,

traders, processors, exporters, importers,

arbitrageurs, investors and the general mass.

Promoters

The National Spot Exchange is promoted by Multi

Commodity Exchange of India, Financial

Technologies India Ltd. and National Agricultural

Cooperative Marketing Federation of India Ltd.

MCX (Multi Commodity Exchange of India

Limited), the leading commodity exchange in India,

provides futures trading in more than 70

commodities. It is also amongst the top three

Exchanges in the world in bullion futures.

FTIL (Financial Technologies India Limited) is

among the very few companies globally that offers

exhaustive solutions library for Exchanges, provides

technology solutions to financial markets and

facilitates expansion of stock broking terminals.

NAFED (National Agricultural Cooperative

Marketing Federation of India Limited), the leading

Government agency, engages in food procurement,

distribution and storage activities.

Objectives

1. To develop a Common Indian Market, by

setting up a national level electronic spot

market and providing a state of art trading,

delivery and settlement facilities in various

commodities, which can be accessed from

across the country.

2. To provide an effective method of spot price

discovery in various commodities, in a

transparent manner from across the country.

3. To create a market where farmers can sell their

produce and realize sale proceeds at the best

prevailing price.

4. To create a market where the processors, end

users, exporters, corporates (both private and

government) and other upcountry traders can

procure agricultural produces at the most

competitive price, without any counter party

and quality risk.

5. To create a transparent market where financiers,

investors and arbitrageurs can invest money in

buying various commodities across the country

without going through the hassles of physical

market.

6. To provide authentic spot price of various

commodities that can be used by the futures

market as the benchmark price for settlement

of their contracts on the date of expiry.

National Spot Exchange – An Alternate Channel for Physical Traders

Subscribe for commodity alerts

through SMS

Logon to www.karvycomtrade.com

tension in the oil exporting nations thereby spurting

the supply concerns. In tune it's leading to the rise in

fuel costs across the world hence impacting the

growth rates by increasing inflationary pressures.

A global standoff on the higher oil prices is likely to

come by if there is a continued increase in prices.

This might lead to use of alternatives or discover

the new sources of energy. Will this hold ahead a

future for innovation or substitution of oil for the

energy consumption is yet to be discovered.

Cover Story |

July 2008 13| July 2008 12| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Focus |

7. To help the futures exchanges, Forward

Markets Commission (FMC) and the

Government in achieving the target of

compulsory delivery in all agricultural produces

by way of creating a structured and

standardized spot market. 8. To promote grading and standardization of

agricultural produces and create a market,

where banks and money lending agencies can

provide warehouse receipt financing to farmers

and traders.

Facilities

National Spot Exchange offers electronic spot

trading facility in multiple commodities with

specific delivery centers. The exchange assures

deliver of quality produce to the buyers as it has

system of grading, quality certification and

standardization of commodities. It also facilitates

collateral financing and borrowing against

warehouse receipts. The participants in this

exchange are eligible to get customized services like

storage, transportation, logistics handling and

shipment of the produce. Through this exchange

participants can procure and dispose commodities

through online trading system.

Benefits

National Spot Exchange is beneficial for number of

participants in agri business starting from farmers

to end users. Through this exchange, farmers of the

country will come to know about prevailing price

for his crop in major trading centres at the time of

sale. Since the Indian farmers are prone to

exploitation by market middlemen, this exchange

tries to remove this system by way of guaranteeing

trade and payment. Till date, the farmer of

particular locality are selling his produce in nearby

market but with the commencement of spot

exchange he will be able to access national level

transparent market where direct selling to

processors or end users would be feasible. The

exchange increases the holding capacity due to

acceptance of warehouse receipt for financing.

Since the producer can view prevailing price for his

crop in major trading centres of the country he can

bargain best price in his nearby physical market.

On the other hand of physical trade, traders are

buyers of produce from farmers. Once the spot

exchange comes into operation, it will provide series

of benefits to traders. This exchange will provide

common platform for traders to buy and sell

commodities and there will not be counterparty risk

as the exchange assures payment in due course of

time.

Corporate houses/Exporters/Importers engaged

in agri based business can procure the produce in

bulk without counterparty risk zregarding payment

and the company will get assured quality of the

produce. Along with above mentioned facility, spot

exchange also provided storage and logistic services.

This system completely removes bottlenecks

relating to physical market operations.

The benefits of National Spot Exchange are

extended to Arbitrageurs as well by way cash futures

arbitrage on electronic platform. Arbitrageurs can

offload the deliveries received on futures market.

As an exchange, it also has few benefits like

transparent spot price for Due Date Rate

calculation. Ease of moving towards compulsory

delivery contracts through structured spot market.

Healthy growth of futures market ensured through

development of the structured spot market.

Conclusion

Exchange markets and operations will undergo a

paradigm shift in their behavior and would be

increasingly driven for providing integrated

processes and services to the trading community.

Moreover, Exchanges need to deliver highest levels

of service backed by strong technology to bring

increased participation at lowest possible cost.

National Spot Exchange gets the strategic

advantage of having Financial Technologies (India)

Ltd. as its technology partner for delivering

technologically advanced solutions to market

participants. FTIL is proven class of end-to-end

Exchange Trading technologies, addressing Trading

/ Surveillance / Clearing and Settlement

operations. It would deliver a cutting-edge to the

National Spot Exchange Trade Life Cycle i.e. Pre-

Trade, Trade and Post-Trade operations.

Online Commodity

Trading

Logon to www.karvycomtrade.com

Focus |

July 2008 13| July 2008 12| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Focus |

7. To help the futures exchanges, Forward

Markets Commission (FMC) and the

Government in achieving the target of

compulsory delivery in all agricultural produces

by way of creating a structured and

standardized spot market. 8. To promote grading and standardization of

agricultural produces and create a market,

where banks and money lending agencies can

provide warehouse receipt financing to farmers

and traders.

Facilities

National Spot Exchange offers electronic spot

trading facility in multiple commodities with

specific delivery centers. The exchange assures

deliver of quality produce to the buyers as it has

system of grading, quality certification and

standardization of commodities. It also facilitates

collateral financing and borrowing against

warehouse receipts. The participants in this

exchange are eligible to get customized services like

storage, transportation, logistics handling and

shipment of the produce. Through this exchange

participants can procure and dispose commodities

through online trading system.

Benefits

National Spot Exchange is beneficial for number of

participants in agri business starting from farmers

to end users. Through this exchange, farmers of the

country will come to know about prevailing price

for his crop in major trading centres at the time of

sale. Since the Indian farmers are prone to

exploitation by market middlemen, this exchange

tries to remove this system by way of guaranteeing

trade and payment. Till date, the farmer of

particular locality are selling his produce in nearby

market but with the commencement of spot

exchange he will be able to access national level

transparent market where direct selling to

processors or end users would be feasible. The

exchange increases the holding capacity due to

acceptance of warehouse receipt for financing.

Since the producer can view prevailing price for his

crop in major trading centres of the country he can

bargain best price in his nearby physical market.

On the other hand of physical trade, traders are

buyers of produce from farmers. Once the spot

exchange comes into operation, it will provide series

of benefits to traders. This exchange will provide

common platform for traders to buy and sell

commodities and there will not be counterparty risk

as the exchange assures payment in due course of

time.

Corporate houses/Exporters/Importers engaged

in agri based business can procure the produce in

bulk without counterparty risk zregarding payment

and the company will get assured quality of the

produce. Along with above mentioned facility, spot

exchange also provided storage and logistic services.

This system completely removes bottlenecks

relating to physical market operations.

The benefits of National Spot Exchange are

extended to Arbitrageurs as well by way cash futures

arbitrage on electronic platform. Arbitrageurs can

offload the deliveries received on futures market.

As an exchange, it also has few benefits like

transparent spot price for Due Date Rate

calculation. Ease of moving towards compulsory

delivery contracts through structured spot market.

Healthy growth of futures market ensured through

development of the structured spot market.

Conclusion

Exchange markets and operations will undergo a

paradigm shift in their behavior and would be

increasingly driven for providing integrated

processes and services to the trading community.

Moreover, Exchanges need to deliver highest levels

of service backed by strong technology to bring

increased participation at lowest possible cost.

National Spot Exchange gets the strategic

advantage of having Financial Technologies (India)

Ltd. as its technology partner for delivering

technologically advanced solutions to market

participants. FTIL is proven class of end-to-end

Exchange Trading technologies, addressing Trading

/ Surveillance / Clearing and Settlement

operations. It would deliver a cutting-edge to the

National Spot Exchange Trade Life Cycle i.e. Pre-

Trade, Trade and Post-Trade operations.

Online Commodity

Trading

Logon to www.karvycomtrade.com

Focus |

July 2008 15|

come from excellent academic background and have

vast experience. So was it a fear of accounting for

“Hedging loss” in the books of accounts? The

important point to remember here is that hedging is

a tool that neither gives profits nor makes losses but

fixes the cost and protects the margins. If they had

fixed the cost of ATF to some extent they not only

could have continued their operations with cost

almost fixed for their operations but also kept their

customers happy offering them very competitive

prices. Almost 74% of 40% that is about 30% of the

total operational cost (which is the cost of fuel)

would have been fixed and there was no need to

worry for increase/ decrease or volatility in aviation

fuel prices. Most of the other costs any way are fixed

in terms of ground handling cost, manpower cost,

lease and rentals etc.

So how can airlines hedge their ATF risks especially

when ATF is not traded on any commodity

exchange across the world? The answer lies in

surrogate hedging which basically means choosing

an alternate commodity which has a high degree of

price correlation with the original commodity. In

this case since ATF is unavailable, we will have to

look forwards to hedging in either crude oil or

heating oil.

The viability of surrogate hedging can be

established from the fact that there is strong

correlation between Arabian Gulf Jet Fuel Prices

(this is the basis taken by India oil marketing

companies for declaring their ATF prices) and

NYMEX WTI Crude prices. The price correlation

between these two has ranged from 0.96 to 0.98 over

the previous five years. In the case of Indian airline

companies, they should go for surrogate hedging on

MCX Crude Oil contracts, because hedging on the

NYMEX would also involve hedging foreign

currency risk thereby involving additional costing.

MCX is India's largest commodity exchange, and in

terms of liquidity is the fourth largest commodity

exchange in the world as far as volumes in crude oil

is concerned. Indian airline companies willing to

hedge on MCX Crude will be exposed to the same

volatility as NYMEX WTI Crude as the price

correlation between these two has ranged from 0.97

to 0.99 over the past three years since the launch of

crude contracts on the MCX platform.

However, before an airline undertakes a programme

of hedging or surrogate hedging as the case may be,

it has to understand that surrogate hedging in crude

will not fully cover the ATF price risk, as nearly 74

per cent of ATF price contribution is directly linked

to an international benchmark, while 19 per cent is

indirectly linked to it, as the other components are

computed as a notional %age while pricing.

So how will an Indian airline company go about

designing its hedging programme? Primarily the

company has to calculate the hedge ratio (a

statistical calculation which decides on the number

of contracts to be traded in the futures market). In

this case the hedge ratio will be based on surrogate

hedging. Once the number of contracts has been

decided, the company will have to buy an equivalent

number of MCX Crude Oil contracts to safeguard

against ATF price volatility. The day the airline

companies will get to know the monthly average

price decided by the Indian Oil Marketing

companies, they will have to square off all the future

contracts on the MCX platform.

All the above is fine in case Crude prices go up.

However if crude prices come down, there will be a

loss in the derivatives transaction and people may

worry about a “Hedge Loss” as was recently

mentioned in media in regards to Larsen & Toubro.

Hedge programme results in neither a profit nor

loss. Even if crude prices had gone up, there would

July 2008 14|

Of late airline companies in India have been crying

hoarse against rise in fuel prices and have responded

by increasing the fuel surcharge. So are the hunky-

dory days of Low Cost airlines over? That seems to

be the case with rising fuel costs forcing airlines to

increase airfares, slash discounts. Even premium

airlines are also feeling the heat. Indian airline

companies are cutting flights and postponing plans

for fleet acquisition due to lower revenues caused by

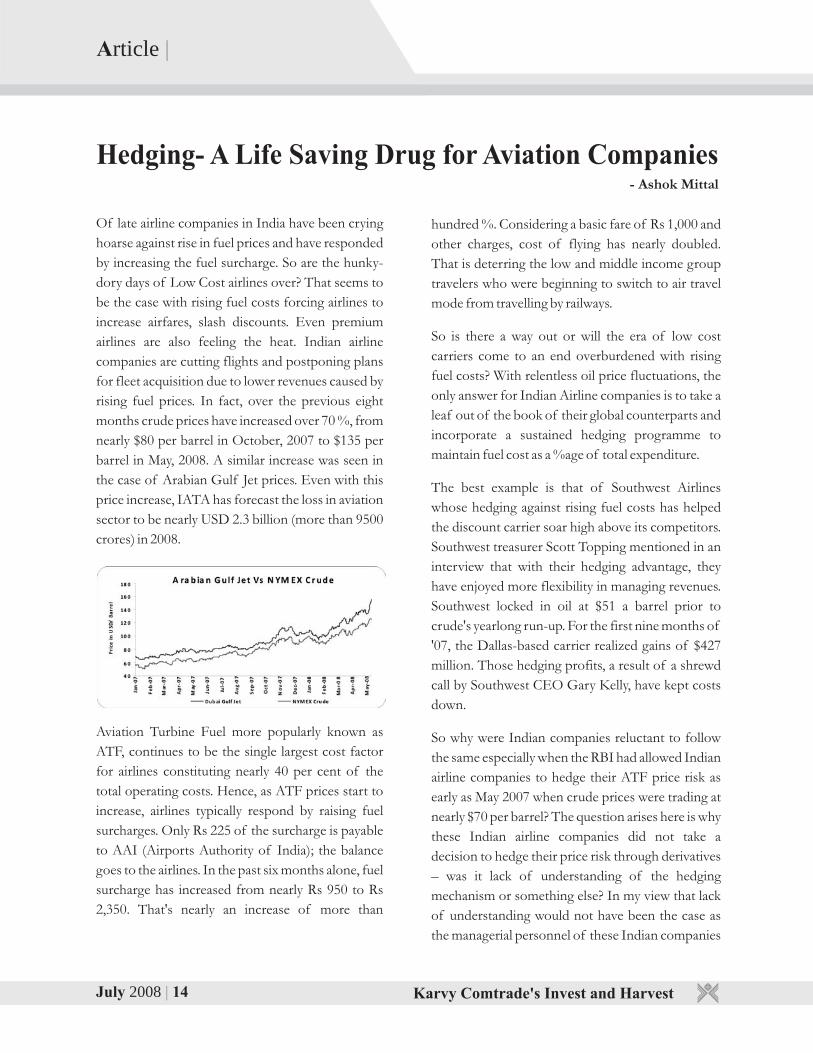

rising fuel prices. In fact, over the previous eight

months crude prices have increased over 70 %, from

nearly $80 per barrel in October, 2007 to $135 per

barrel in May, 2008. A similar increase was seen in

the case of Arabian Gulf Jet prices. Even with this

price increase, IATA has forecast the loss in aviation

sector to be nearly USD 2.3 billion (more than 9500

crores) in 2008.

Aviation Turbine Fuel more popularly known as

ATF, continues to be the single largest cost factor

for airlines constituting nearly 40 per cent of the

total operating costs. Hence, as ATF prices start to

increase, airlines typically respond by raising fuel

surcharges. Only Rs 225 of the surcharge is payable

to AAI (Airports Authority of India); the balance

goes to the airlines. In the past six months alone, fuel

surcharge has increased from nearly Rs 950 to Rs

2,350. That's nearly an increase of more than

hundred %. Considering a basic fare of Rs 1,000 and

other charges, cost of flying has nearly doubled.

That is deterring the low and middle income group

travelers who were beginning to switch to air travel

mode from travelling by railways.

So is there a way out or will the era of low cost

carriers come to an end overburdened with rising

fuel costs? With relentless oil price fluctuations, the

only answer for Indian Airline companies is to take a

leaf out of the book of their global counterparts and

incorporate a sustained hedging programme to

maintain fuel cost as a %age of total expenditure.

The best example is that of Southwest Airlines

whose hedging against rising fuel costs has helped

the discount carrier soar high above its competitors.

Southwest treasurer Scott Topping mentioned in an

interview that with their hedging advantage, they

have enjoyed more flexibility in managing revenues.

Southwest locked in oil at $51 a barrel prior to

crude's yearlong run-up. For the first nine months of

'07, the Dallas-based carrier realized gains of $427

million. Those hedging profits, a result of a shrewd

call by Southwest CEO Gary Kelly, have kept costs

down.

So why were Indian companies reluctant to follow

the same especially when the RBI had allowed Indian

airline companies to hedge their ATF price risk as

early as May 2007 when crude prices were trading at

nearly $70 per barrel? The question arises here is why

these Indian airline companies did not take a

decision to hedge their price risk through derivatives

– was it lack of understanding of the hedging

mechanism or something else? In my view that lack

of understanding would not have been the case as

the managerial personnel of these Indian companies

Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Article | Article |

Hedging- A Life Saving Drug for Aviation Companies- Ashok Mittal

July 2008 15|

come from excellent academic background and have

vast experience. So was it a fear of accounting for

“Hedging loss” in the books of accounts? The

important point to remember here is that hedging is

a tool that neither gives profits nor makes losses but

fixes the cost and protects the margins. If they had

fixed the cost of ATF to some extent they not only

could have continued their operations with cost

almost fixed for their operations but also kept their

customers happy offering them very competitive

prices. Almost 74% of 40% that is about 30% of the

total operational cost (which is the cost of fuel)

would have been fixed and there was no need to

worry for increase/ decrease or volatility in aviation

fuel prices. Most of the other costs any way are fixed

in terms of ground handling cost, manpower cost,

lease and rentals etc.

So how can airlines hedge their ATF risks especially

when ATF is not traded on any commodity

exchange across the world? The answer lies in

surrogate hedging which basically means choosing

an alternate commodity which has a high degree of

price correlation with the original commodity. In

this case since ATF is unavailable, we will have to

look forwards to hedging in either crude oil or

heating oil.

The viability of surrogate hedging can be

established from the fact that there is strong

correlation between Arabian Gulf Jet Fuel Prices

(this is the basis taken by India oil marketing

companies for declaring their ATF prices) and

NYMEX WTI Crude prices. The price correlation

between these two has ranged from 0.96 to 0.98 over

the previous five years. In the case of Indian airline

companies, they should go for surrogate hedging on

MCX Crude Oil contracts, because hedging on the

NYMEX would also involve hedging foreign

currency risk thereby involving additional costing.

MCX is India's largest commodity exchange, and in

terms of liquidity is the fourth largest commodity

exchange in the world as far as volumes in crude oil

is concerned. Indian airline companies willing to

hedge on MCX Crude will be exposed to the same

volatility as NYMEX WTI Crude as the price

correlation between these two has ranged from 0.97

to 0.99 over the past three years since the launch of

crude contracts on the MCX platform.

However, before an airline undertakes a programme

of hedging or surrogate hedging as the case may be,

it has to understand that surrogate hedging in crude

will not fully cover the ATF price risk, as nearly 74

per cent of ATF price contribution is directly linked

to an international benchmark, while 19 per cent is

indirectly linked to it, as the other components are

computed as a notional %age while pricing.

So how will an Indian airline company go about

designing its hedging programme? Primarily the

company has to calculate the hedge ratio (a

statistical calculation which decides on the number

of contracts to be traded in the futures market). In

this case the hedge ratio will be based on surrogate

hedging. Once the number of contracts has been

decided, the company will have to buy an equivalent

number of MCX Crude Oil contracts to safeguard

against ATF price volatility. The day the airline

companies will get to know the monthly average

price decided by the Indian Oil Marketing

companies, they will have to square off all the future

contracts on the MCX platform.

All the above is fine in case Crude prices go up.

However if crude prices come down, there will be a

loss in the derivatives transaction and people may

worry about a “Hedge Loss” as was recently

mentioned in media in regards to Larsen & Toubro.

Hedge programme results in neither a profit nor

loss. Even if crude prices had gone up, there would

July 2008 14|

Of late airline companies in India have been crying

hoarse against rise in fuel prices and have responded

by increasing the fuel surcharge. So are the hunky-

dory days of Low Cost airlines over? That seems to

be the case with rising fuel costs forcing airlines to

increase airfares, slash discounts. Even premium

airlines are also feeling the heat. Indian airline

companies are cutting flights and postponing plans

for fleet acquisition due to lower revenues caused by

rising fuel prices. In fact, over the previous eight

months crude prices have increased over 70 %, from

nearly $80 per barrel in October, 2007 to $135 per

barrel in May, 2008. A similar increase was seen in

the case of Arabian Gulf Jet prices. Even with this

price increase, IATA has forecast the loss in aviation

sector to be nearly USD 2.3 billion (more than 9500

crores) in 2008.

Aviation Turbine Fuel more popularly known as

ATF, continues to be the single largest cost factor

for airlines constituting nearly 40 per cent of the

total operating costs. Hence, as ATF prices start to

increase, airlines typically respond by raising fuel

surcharges. Only Rs 225 of the surcharge is payable

to AAI (Airports Authority of India); the balance

goes to the airlines. In the past six months alone, fuel

surcharge has increased from nearly Rs 950 to Rs

2,350. That's nearly an increase of more than

hundred %. Considering a basic fare of Rs 1,000 and

other charges, cost of flying has nearly doubled.

That is deterring the low and middle income group

travelers who were beginning to switch to air travel

mode from travelling by railways.

So is there a way out or will the era of low cost

carriers come to an end overburdened with rising

fuel costs? With relentless oil price fluctuations, the

only answer for Indian Airline companies is to take a

leaf out of the book of their global counterparts and

incorporate a sustained hedging programme to

maintain fuel cost as a %age of total expenditure.

The best example is that of Southwest Airlines

whose hedging against rising fuel costs has helped

the discount carrier soar high above its competitors.

Southwest treasurer Scott Topping mentioned in an

interview that with their hedging advantage, they

have enjoyed more flexibility in managing revenues.

Southwest locked in oil at $51 a barrel prior to

crude's yearlong run-up. For the first nine months of

'07, the Dallas-based carrier realized gains of $427

million. Those hedging profits, a result of a shrewd

call by Southwest CEO Gary Kelly, have kept costs

down.

So why were Indian companies reluctant to follow

the same especially when the RBI had allowed Indian

airline companies to hedge their ATF price risk as

early as May 2007 when crude prices were trading at

nearly $70 per barrel? The question arises here is why

these Indian airline companies did not take a

decision to hedge their price risk through derivatives

– was it lack of understanding of the hedging

mechanism or something else? In my view that lack

of understanding would not have been the case as

the managerial personnel of these Indian companies

Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

Article | Article |

Hedging- A Life Saving Drug for Aviation Companies- Ashok Mittal

have been a profit in the derivatives position but a

simultaneous loss would have occurred in the Spot

market for ATF. Hence, in case crude prices comes

down, there would be a loss in the futures market

but the company will get compensated for that by

getting a benefit in the spot market as they will buy

ATF at a lesser rate. As per the recent guidelines of

the ICAI any profit/ loss on account of hedging

transactions in relation to the company's business

can be setoff against normal business profit/ loss

(AS 30). This point was also clarified by the L&T

management that losses on account of their

hedging strategy had not hit their balance sheets or

profitability.

To conclude we can say that in an era of volatile

crude prices, an airline company has no option but

to opt for a hedging programme. It is as necessary as

an insurance programme for the company's flights.

Therefore if low cost carriers - or for that matter all

the airline companies - desire to maintain

uninterrupted operations and keep the costs stable,

they must adopt a Hedging strategy after taking into

account the hedge ratio and other parameters which

will allow them to lock in the cost of ATF and then

decide their pricing policies without the fear of

uncertain fuel prices. Fixing the cost and margins

irrespective of fuel price volatility would not burden

the customer every time in the form of a fuel

surcharge. This would be a win-win situation for

everyone be it an airline company the Government

or the customer.

This article originally published in The Economic Times

dated 13th June 2008

July 2008 17| July 2008 16| Karvy Comtrade's Invest and Harvest Karvy Comtrade's Invest and Harvest

South West Monsoon – Farmers' Fortune in Thin Air

Article |

Introduction

India is the major agrarian economy growing at the

rate of 8.5% year on year basis. Its farming

community is getting ready to bet their luck on South

West Monsoon, which is lifeline of millions of

farmers. Till date, India is largely dependant on

monsoon for its large chunk of food grain

production to feed the growing population. The SW

monsoon season starts from June and continue till

September month. These four months are popularly

called as rainy season in common nomenclature,

kharif season in agriculture terminology. On an

average India receives 110-120 cm of rain in a year

and South West Monsoon alone accounts for 88-90

cm. The country witnesses two monsoons every year

namely, South West Monsoon and North East

Monsoon. Of these two monsoons, South West

brings maximum rainfall to the country than that of

other. It plays a crucial role in deciding overall

agriculture growth of the country. South West

Monsoon normally hits the Indian mainland on June

1st and covers entire India by July 15th every year.

The other North East monsoon hits India in

October and terminates in the month of December.

Northeast Monsoon season is the major period of

rainfall activity over south peninsula, particularly in

Coastal Andhra Pradesh, Rayalaseema and

Tamilnadu-Pondicherry. For Tamilnadu this is the

main rainy season accounting for about 48% of the

annual rainfall.

Monsoon 2007

In the last couple of years, South West monsoon is

hitting Indian subcontinent few days prior to normal

date of its commencement. In 2007, the monsoon

hit Kerala coast on May 28th, four days prior to

normal onset date. The country had received 105%

Long Period Average rainfall during 2007. The 2007

monsoon seasonal rainfall over the country was

more than the predicted value. Despite the adequate

rains the states like West Uttar Pradesh, Haryana,

Chandigarh and Delhi, Punjab, Himachal Pradesh

and East Madhya Pradesh experienced moderate

drought conditions (rainfall deficiency of 26% to

50%) at the end of the season. The southwest

monsoon covered the entire country on 4th July

2007. Timely arrival and well distribution of rainfall

in 2007 has resulted into bumper harvest of most of

the crops like Maize, Paddy, Sugar Cane and

Oilseeds.

Monsoon 2008

Before start of each monsoon season, the Indian

Meteorological Department, a premiere weather

forecasting agency in India, releases its rainfall