Embed Size (px)

Citation preview

Standing Committee of the Whole AgendaJune 13, 2016/Page 1

File No.:B06

STANDING COMMITTEE OF THE WHOLE

AGENDA REPORT

Subject: ANNUAL REVIEW OF FINANCIAL POLICIES Recommendation(s) 1. That Standing Committee of the Whole recommend to Council that City Council

Policy C-FS-01, Financial Reserves be amended by substituting City Council Policy C-FS-01, Financial Reserves, included as Attachment 1 to the agenda report "Annual Review of Financial Policies" dated June 13, 2016.

2. That Standing Committee of the Whole recommend to Council that City Council Policy C-FS-05, Budget and Taxation Guiding Principles be amended by substituting City Council Policy C-FS-05, Budget and Taxation Guiding Principles, included as Attachment 3 to the agenda report "Annual Review of Financial Policies" dated June 13, 2016.

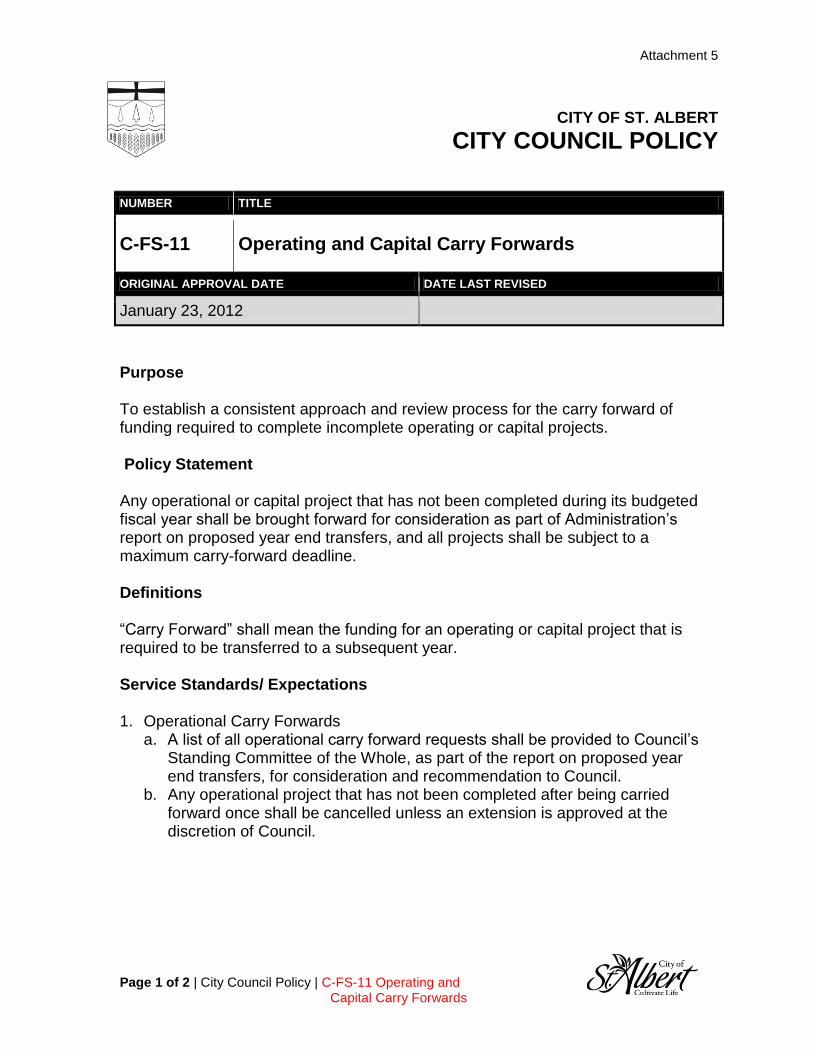

3. That Standing Committee of the Whole recommend to Council that City Council Policy C-FS-11, Operating and Capital Carry Forwards be amended by substituting City Council Policy C-FS-11, Operating and Capital Carry Forwards, included as Attachment 5 to the agenda report "Annual Review of Financial Policies" dated June 13, 2016.

Purpose of Report The purpose of the report is to provide recommendations for Committee consideration relating to suggested amendments as a result of the Annual Review of Financial Policies. Council (and/or Committee) Direction There are seven financial polices that require an annual review be conducted by Administration, with any changes to be recommended to Council for approval.

Standing Committee of the Whole AgendaJune 13, 2016/Page 2

File No.:B06

Background and Discussion Each year Administration performs a review of the following seven financial policies:

1. C-FS-01 Financial Reserves 2. C-FS-02 Investment Policy 3. C-FS-03 Debt Management 4. C-FS-04 Cash Management 5. C-FS-05 Budget and Taxation Guiding Principles 6. C-FS-11 Operating and Capital Carry Forwards 7. C-FS-14 Utility Fiscal Policy

In preparation for the 2017-2019 Budget Process, Administration has reviewed these policies to ensure that they continue to support Council’s decision making process. The financial policies with recommended amendments are C-FS-01, Financial Reserves, C-FS-05 Budget and Taxation Guiding Principles and C-FS-11 Operating and Capital Carry Forwards. Recommendations regarding amendments to C-FS-03 Debt Management and C-FS-14 Utility Fiscal Policy will be tabled later in 2016 once Council has made final decisions related to the long term debt financing of the North Interceptor (Project 9) and the Stormwater rate model changes. No changes are recommended within C-FS-02 Investment or C-FS-04 Cash Management. A summary of the key changes within each policy are described below: C-FS-02 Financial Reserves

Conversion to new format. Added to old standard 4 (New Service Standards/expectations 2) “or

as approved by Council.” to reflect current practice. Reserve Schedule O1 – Stabilization. Added statement under

Application to clarify that capital projects/equipment are not eligible. Reserve Schedule O2 – Growth Stabilization. This schedule requires

major modifications to conform with previous council motions. Re-categorized to a capital reserve C7 and restricted to funding growth capital projects.

Reserve schedule O7 – Children’s Festival Fund. Minor wording changes.

Reserve schedule O9 – Safety Enhancement Reserve. In the 2015 revision of this policy there were several “Application” details that were inadvertently removed. Adding back in this version.

Reserve Schedule C3 – Offsite Levy Recoveries. No changes recommended at this time. Finance will be bringing forward a separate policy or major amendments to this schedule to reflect the use of these dollars for debt servicing of the debenture for project 9.

Standing Committee of the Whole AgendaJune 13, 2016/Page 3

File No.:B06

Reserve Schedule OA2 – Outside agency Capital. Added 4. Library Computer Replacement. This reserve has always existed but was never listed in the policy. Also change to state that the Board and Council approve application of funds.

C-FS-05 Budget and Taxation Guiding Principles

Conversion to new format. Added policy statement (moved text from 3rd paragraph of old section

10 Capital Planning) solidifying existing practice of funding RMR and operations prior to growth to ensure we are able to maintain our existing assets and services prior to adding new ones.

Added policy statement related to the desired 80/20 taxation split. Moved the 1st paragraph under Taxation guiding principles 1. to a

policy statement at the beginning. Budget guiding principle 4. New programs and changes in service

levels, amended to add reference to collective agreements. Update to Cross references. Capital Planning section renamed to Capital Budget. Added statement under Capital Budget section to indicate that a

facility predictive model will be utilized to inform growth capital decisions.

C-FS-11 Operating and Capital Carry Forwards

Conversion to new format. Change all references to Standing Committee on Finance to

Standing Committee of the Whole. Update to Cross References.

Implications of Recommendation(s) a) Financial:

None at this time

b) Legal / Risk: None at this time

c) Program or Service: None at this time

d) Organizational:

None at this time

Standing Committee of the Whole AgendaJune 13, 2016/Page 4

File No.:B06

Alternatives and Implications Considered If Committee does not wish to support the recommendation, the following alternatives could be considered:

a) Alternative 1. Establish a date upon which Council could provide feedback to Administration for revisions to the proposed policies and direct Administration to bring back a revised version for consideration. Significant changes proposed by Council members should be brought forward in the form of a motion.

b) Alternative 2. Do nothing. Do not approve proposed amendments in any one or all policies.

Attachment(s) 1. City Council Policy C-FS-01 Financial Reserves (with proposed amendments

incorporated) 2. City Council Policy C-FS-01 Financial Reserves (with proposed amendments

highlighted) presented under new template 3. City Council Policy C-FS-05 Budget and Taxation Guiding Principles (with

proposed amendments incorporated) 4. City Council Policy C-FS-05 Budget and Taxation Guiding Principles (with

proposed amendments highlighted) presented under new template 5. City Council Policy C-FS-11 Operating and Capital Carry Forwards (with

proposed amendments incorporated) 6. City Council Policy C-FS-11 Operating and Capital Carry Forwards (with

proposed amendments highlighted) presented under new template Originating Department(s): Financial Services Author(s): General Manager Approval:

Diane McMordie, Director of Finance & Utilities Mike Dion, GM & CFO

City Manager Signature:

Date:

Attachment 1

Page 1 of 25 | City Council Policy | C-FS-01 Financial Reserves

CITY OF ST. ALBERT

CITY COUNCIL POLICY NUMBER TITLE

C-FS-01 Financial Reserves

ORIGINAL APPROVAL DATE DATE LAST REVISED

March 17, 2003 September 14, 2015

Purpose – To set aside funds for the establishment of specific reserves to provide for emergent financial needs, stabilize tax rates, to set aside funds for the replacement of existing equipment, facilities and future projects and to minimize the debt financing needs of the Corporation. Policy Statement – The City of St. Albert recognizes that the ongoing commitment of funds to specific reserves provides for property tax stabilization, contingency funding, and reduces the need for debt financing. Responsibilities 1. The establishment of, contributions to, and withdrawals from, a specific reserve

shall be approved by City Council through resolution or bylaw in accordance with the Municipal Government Act or as otherwise stated in the specified schedule.

2. Administration of all reserves will be carried out by the City Manager or his designate.

Service Standards/ Expectations 1. Transfers to/from reserves will be restricted as outlined in each specific

reserve schedule.

2. Interest earnings are intended to be applied to reserves if there are external

requirements based on legislation or agreements, or as approved by Council, and will be added to reserves according to the schedule. The interest will be applied monthly based on the net weighted average of the reserve balance relative to all interest earned by the City’s investment portfolio.

Attachment 1

Page 2 of 25 | City Council Policy | C-FS-01 Financial Reserves

3. Where appropriate, each reserve will be supported by a 10-year projection for receipt and disbursement of funds. These projections will be updated annually as part of the budget process.

4. Reserves are assumed to be ongoing unless otherwise stated in the specified schedule.

5. Reserves are assumed to have no ceiling unless otherwise stated in the specified schedule.

6. Reserve reporting will form a part of the quarterly and annual financial statements and significant transactions affecting these will be highlighted in the comments.

7. This policy along with the approved reserve schedules and balances will be reviewed by Administration annually.

Operating Reserve Schedules O1 Stabilization O3 Operating Programs O4 Risk Management O5 Automated Traffic Enforcement Technology – Speed on Green O6 LRT/BRT Reserve O7 Children’s Festival Fund O8 RCMP Contract Expense Reserve O9 Safety Enhancement Program O10 Election and Census Reserve

Capital Reserve Schedules C1 Internal Financing C2 Major Recreational Lands & Facilities

1. Major Recreational Facilities Fund – City Wide 2. Major Recreational Facilities Fund – Neighbourhood

Attachment 1

Page 3 of 25 | City Council Policy | C-FS-01 Financial Reserves

3. Parkland Fund 4. Dog License Fund

C3 Offsite levy recoveries 1. General Transportation Fund 2. Offsite levy reimbursed Funds C4 Lifecycle

1. Mobile Equipment 2. Emergency Services Equipment 3. Office Systems 4. Arden Theatre 5. Servus Credit Union Place 6. Aquatics Facility 7. Public Art 8. Fire Buildings 9. City Playground 10. Public Transit 11. Infrastructure

C5 Municipal Land & Facilities Reserve C6 Capital Fund C7 Growth Stabilization

Utility Reserve Schedule UC1 Utilities Fund

1. Water 2. Wastewater 3. Solid Waste 4. Storm water

Outside Agency Reserve Schedule

OA1 Outside Agency Operating OA2 Outside Agency Capital

1. Library Book Collection 2. Library Facilities 3. NABI Building Fund

Attachment 1

Page 4 of 25 | City Council Policy | C-FS-01 Financial Reserves

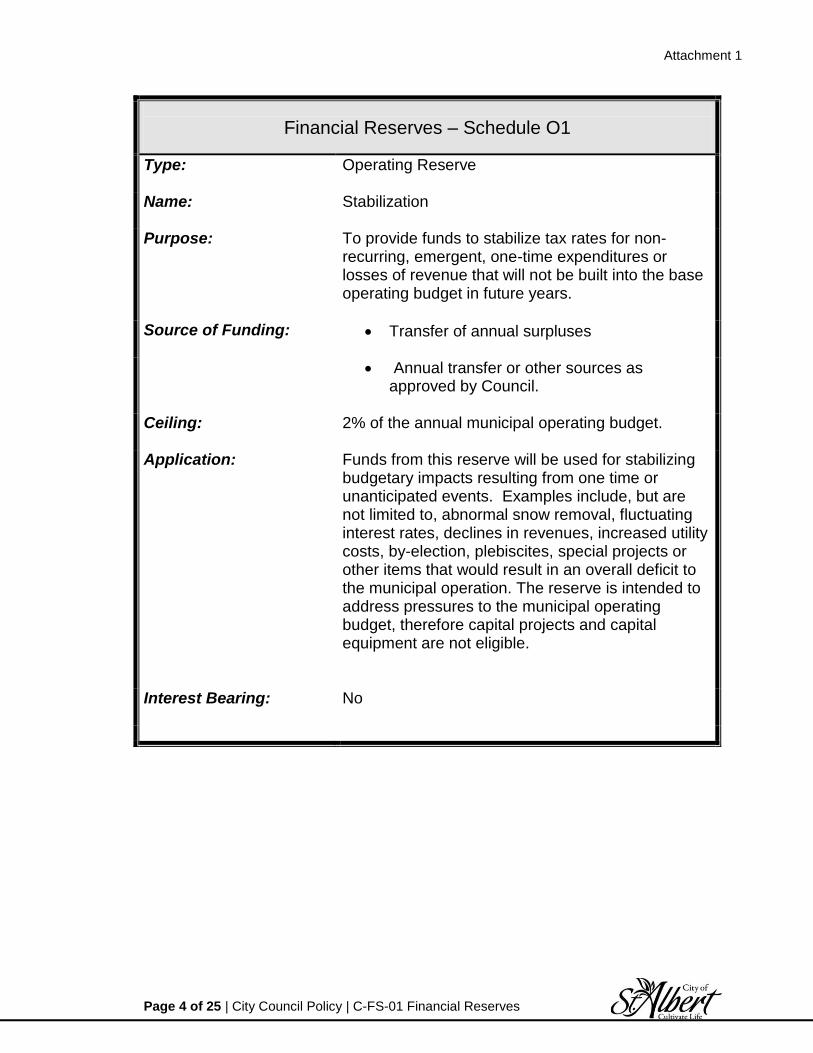

Financial Reserves – Schedule O1

Type:

Operating Reserve

Name:

Stabilization

Purpose:

To provide funds to stabilize tax rates for non-recurring, emergent, one-time expenditures or losses of revenue that will not be built into the base operating budget in future years.

Source of Funding:

Transfer of annual surpluses

Annual transfer or other sources as approved by Council.

Ceiling:

2% of the annual municipal operating budget.

Application:

Funds from this reserve will be used for stabilizing budgetary impacts resulting from one time or unanticipated events. Examples include, but are not limited to, abnormal snow removal, fluctuating interest rates, declines in revenues, increased utility costs, by-election, plebiscites, special projects or other items that would result in an overall deficit to the municipal operation. The reserve is intended to address pressures to the municipal operating budget, therefore capital projects and capital equipment are not eligible.

Interest Bearing:

No

Attachment 1

Page 5 of 25 | City Council Policy | C-FS-01 Financial Reserves

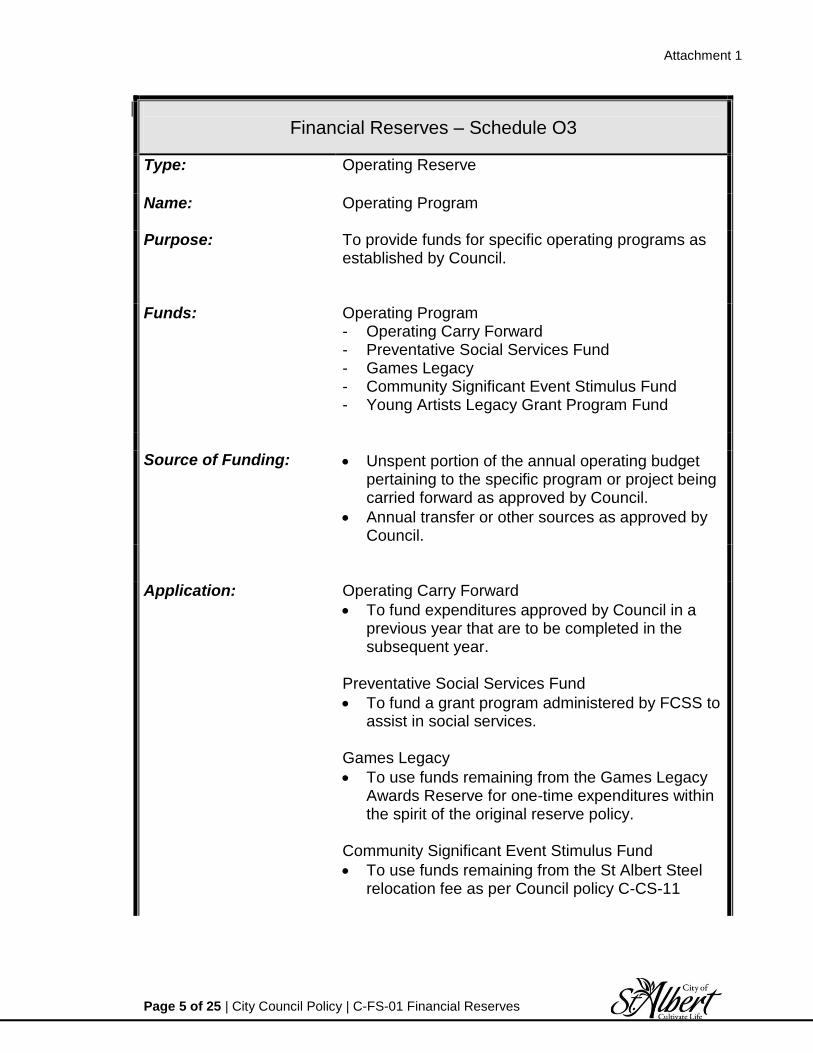

Financial Reserves – Schedule O3

Type:

Operating Reserve

Name:

Operating Program

Purpose:

To provide funds for specific operating programs as established by Council.

Funds: Operating Program - Operating Carry Forward - Preventative Social Services Fund - Games Legacy - Community Significant Event Stimulus Fund - Young Artists Legacy Grant Program Fund

Source of Funding:

Unspent portion of the annual operating budget pertaining to the specific program or project being carried forward as approved by Council.

Annual transfer or other sources as approved by Council.

Application:

Operating Carry Forward

To fund expenditures approved by Council in a previous year that are to be completed in the subsequent year.

Preventative Social Services Fund

To fund a grant program administered by FCSS to assist in social services.

Games Legacy

To use funds remaining from the Games Legacy Awards Reserve for one-time expenditures within the spirit of the original reserve policy.

Community Significant Event Stimulus Fund

To use funds remaining from the St Albert Steel relocation fee as per Council policy C-CS-11

Attachment 1

Page 6 of 25 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O3

Young Artists Legacy Grant Program

Interest earned in the Young Artists Legacy Grant Program are to be used specifically for the program and be treated as an endowment.

Interest Bearing:

No, with the exception of Young Artists Legacy Grant Program

Attachment 1

Page 7 of 25 | City Council Policy | C-FS-01 Financial Reserves

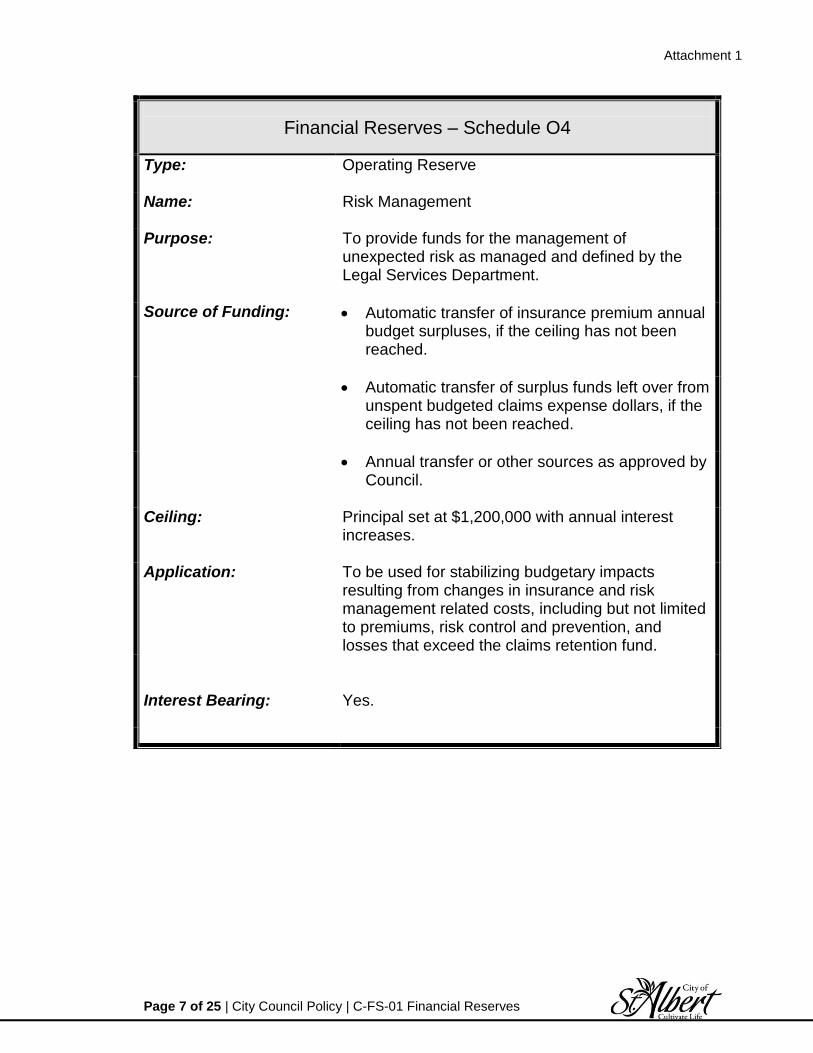

Financial Reserves – Schedule O4

Type:

Operating Reserve

Name:

Risk Management

Purpose:

To provide funds for the management of unexpected risk as managed and defined by the Legal Services Department.

Source of Funding:

Automatic transfer of insurance premium annual budget surpluses, if the ceiling has not been reached.

Automatic transfer of surplus funds left over from unspent budgeted claims expense dollars, if the ceiling has not been reached.

Annual transfer or other sources as approved by

Council.

Ceiling:

Principal set at $1,200,000 with annual interest increases.

Application:

To be used for stabilizing budgetary impacts resulting from changes in insurance and risk management related costs, including but not limited to premiums, risk control and prevention, and losses that exceed the claims retention fund.

Interest Bearing:

Yes.

Attachment 1

Page 8 of 25 | City Council Policy | C-FS-01 Financial Reserves

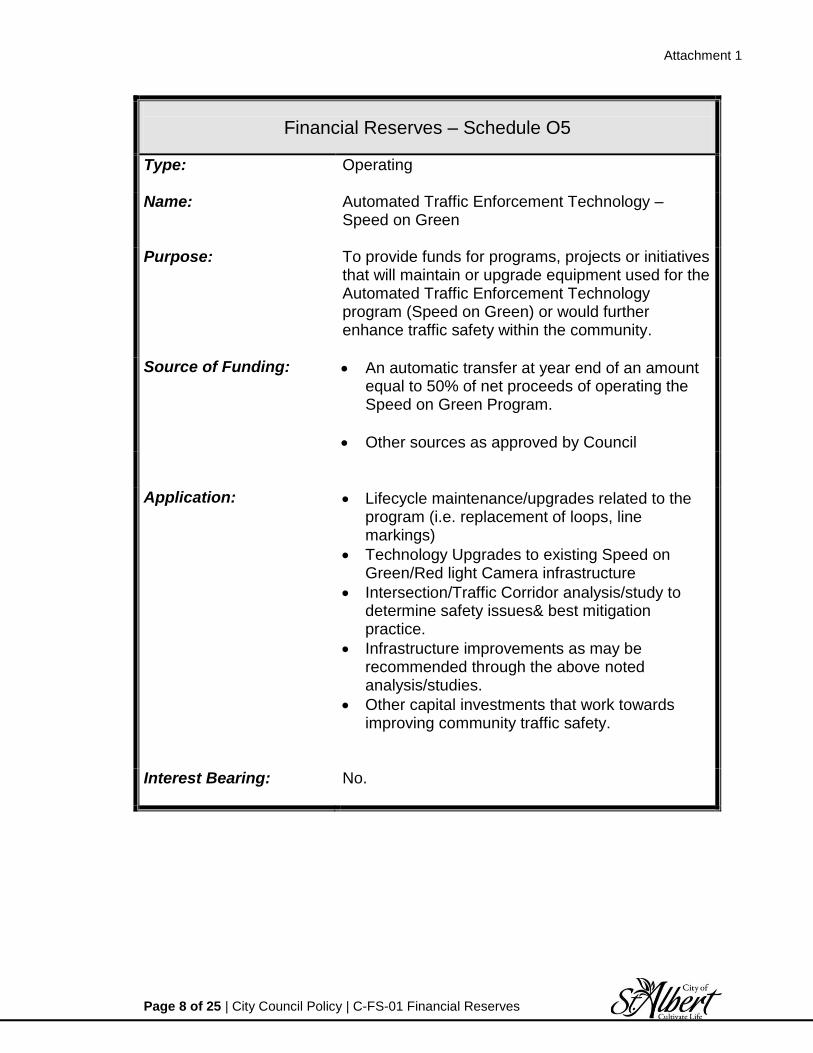

Financial Reserves – Schedule O5

Type:

Operating

Name:

Automated Traffic Enforcement Technology – Speed on Green

Purpose:

To provide funds for programs, projects or initiatives that will maintain or upgrade equipment used for the Automated Traffic Enforcement Technology program (Speed on Green) or would further enhance traffic safety within the community.

Source of Funding:

An automatic transfer at year end of an amount equal to 50% of net proceeds of operating the Speed on Green Program.

Other sources as approved by Council

Application:

Lifecycle maintenance/upgrades related to the program (i.e. replacement of loops, line markings)

Technology Upgrades to existing Speed on Green/Red light Camera infrastructure

Intersection/Traffic Corridor analysis/study to determine safety issues& best mitigation practice.

Infrastructure improvements as may be recommended through the above noted analysis/studies.

Other capital investments that work towards improving community traffic safety.

Interest Bearing:

No.

Attachment 1

Page 9 of 25 | City Council Policy | C-FS-01 Financial Reserves

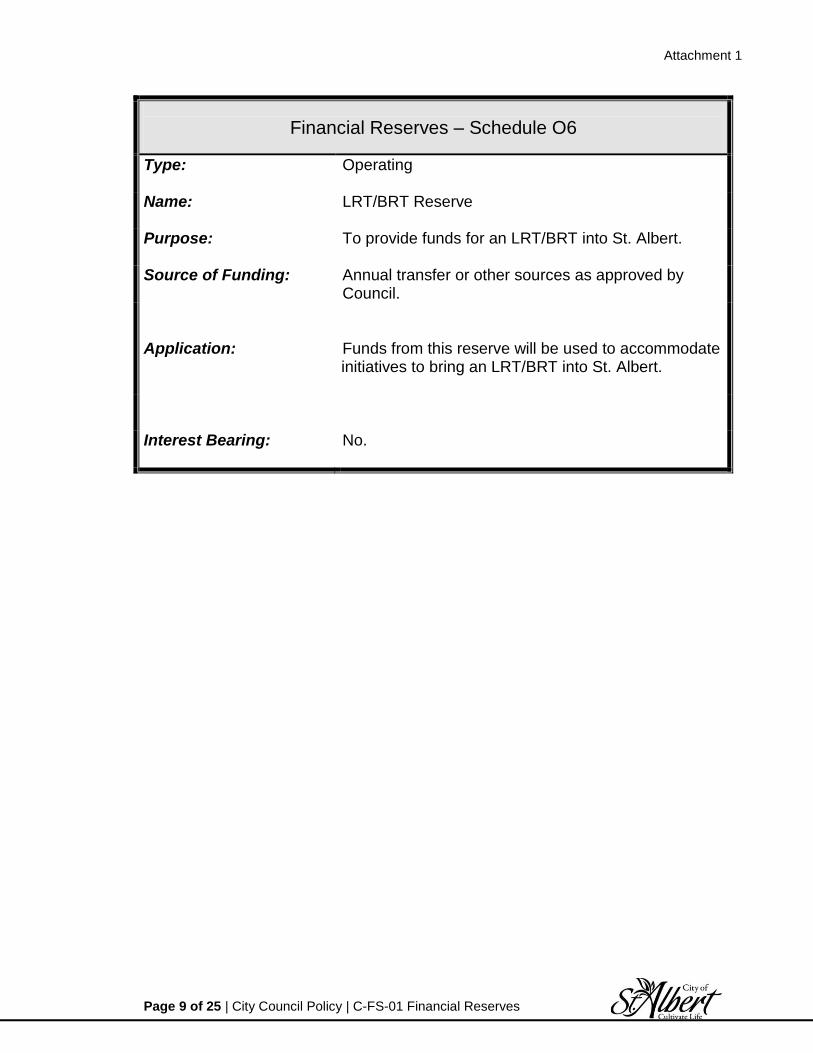

Financial Reserves – Schedule O6

Type:

Operating

Name:

LRT/BRT Reserve

Purpose:

To provide funds for an LRT/BRT into St. Albert.

Source of Funding:

Annual transfer or other sources as approved by Council.

Application:

Funds from this reserve will be used to accommodate initiatives to bring an LRT/BRT into St. Albert.

Interest Bearing:

No.

Attachment 1

Page 10 of 25 | City Council Policy | C-FS-01 Financial Reserves

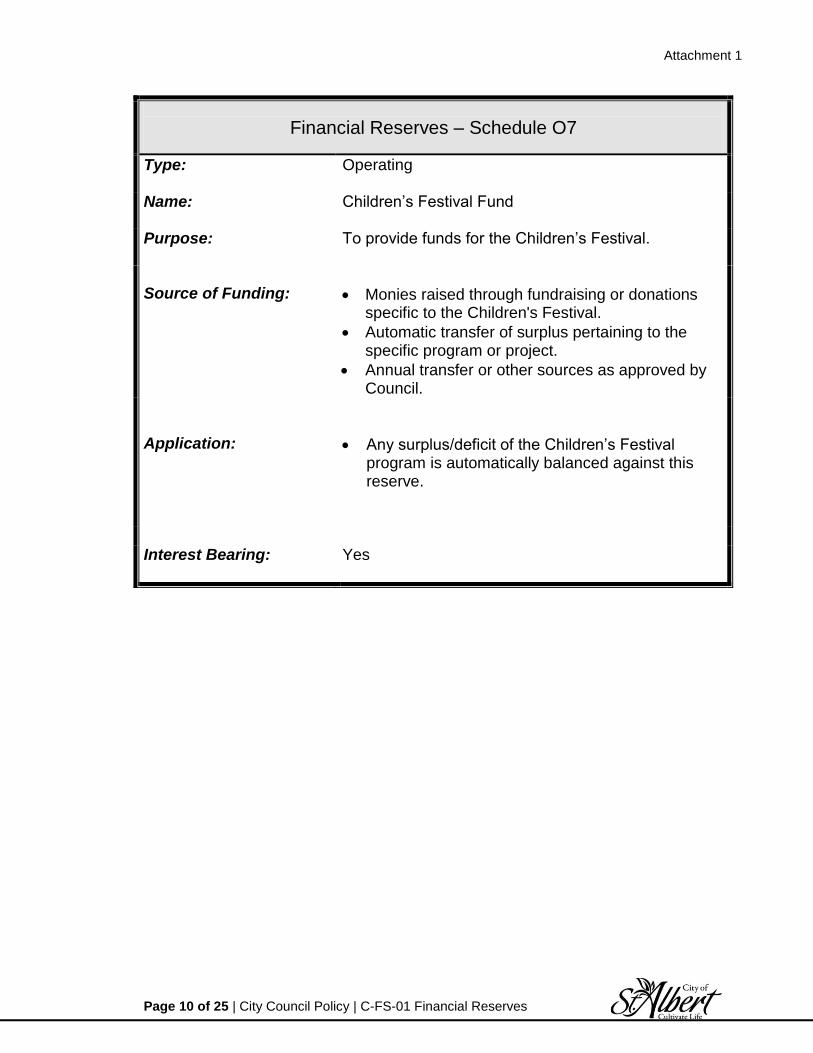

Financial Reserves – Schedule O7

Type:

Operating

Name:

Children’s Festival Fund

Purpose:

To provide funds for the Children’s Festival.

Source of Funding:

Monies raised through fundraising or donations specific to the Children's Festival.

Automatic transfer of surplus pertaining to the specific program or project.

Annual transfer or other sources as approved by Council.

Application:

Any surplus/deficit of the Children’s Festival program is automatically balanced against this reserve.

Interest Bearing:

Yes

Attachment 1

Page 11 of 25 | City Council Policy | C-FS-01 Financial Reserves

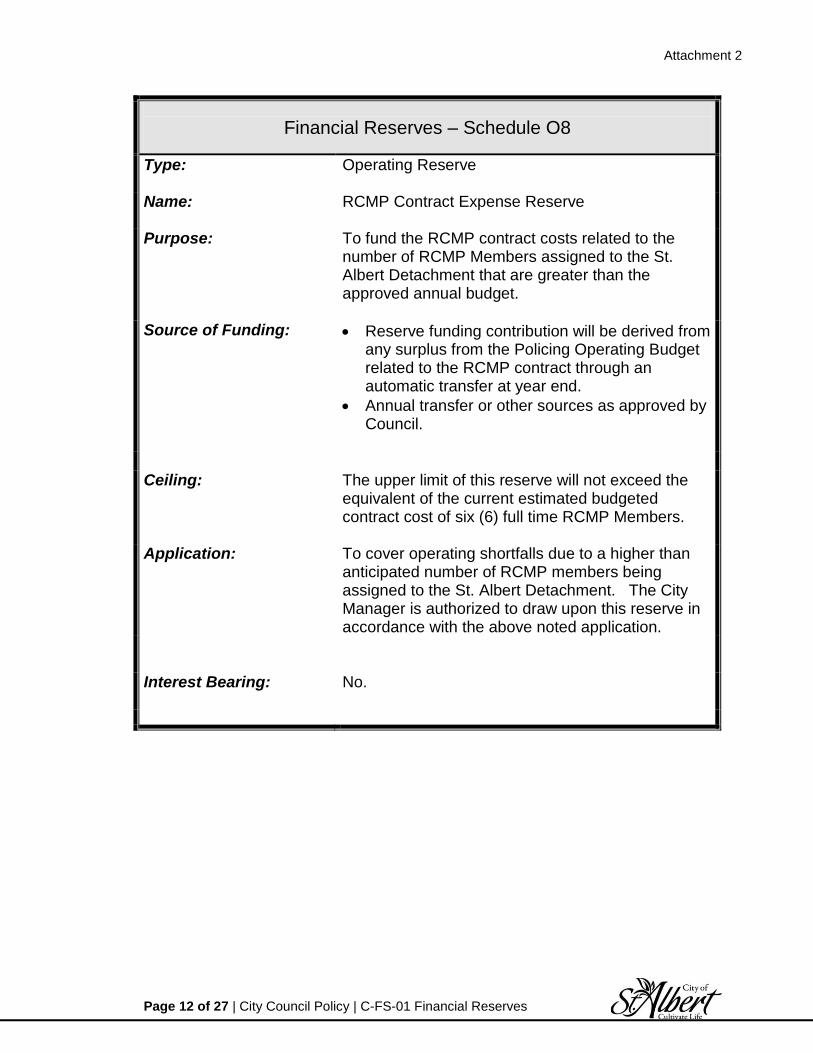

Financial Reserves – Schedule O8

Type:

Operating Reserve

Name:

RCMP Contract Expense Reserve

Purpose:

To fund the RCMP contract costs related to the number of RCMP Members assigned to the St. Albert Detachment that are greater than the approved annual budget.

Source of Funding:

Reserve funding contribution will be derived from any surplus from the Policing Operating Budget related to the RCMP contract through an automatic transfer at year end.

Annual transfer or other sources as approved by Council.

Ceiling:

The upper limit of this reserve will not exceed the equivalent of the current estimated budgeted contract cost of six (6) full time RCMP Members.

Application:

To cover operating shortfalls due to a higher than anticipated number of RCMP members being assigned to the St. Albert Detachment. The City Manager is authorized to draw upon this reserve in accordance with the above noted application.

Interest Bearing:

No.

Attachment 1

Page 12 of 25 | City Council Policy | C-FS-01 Financial Reserves

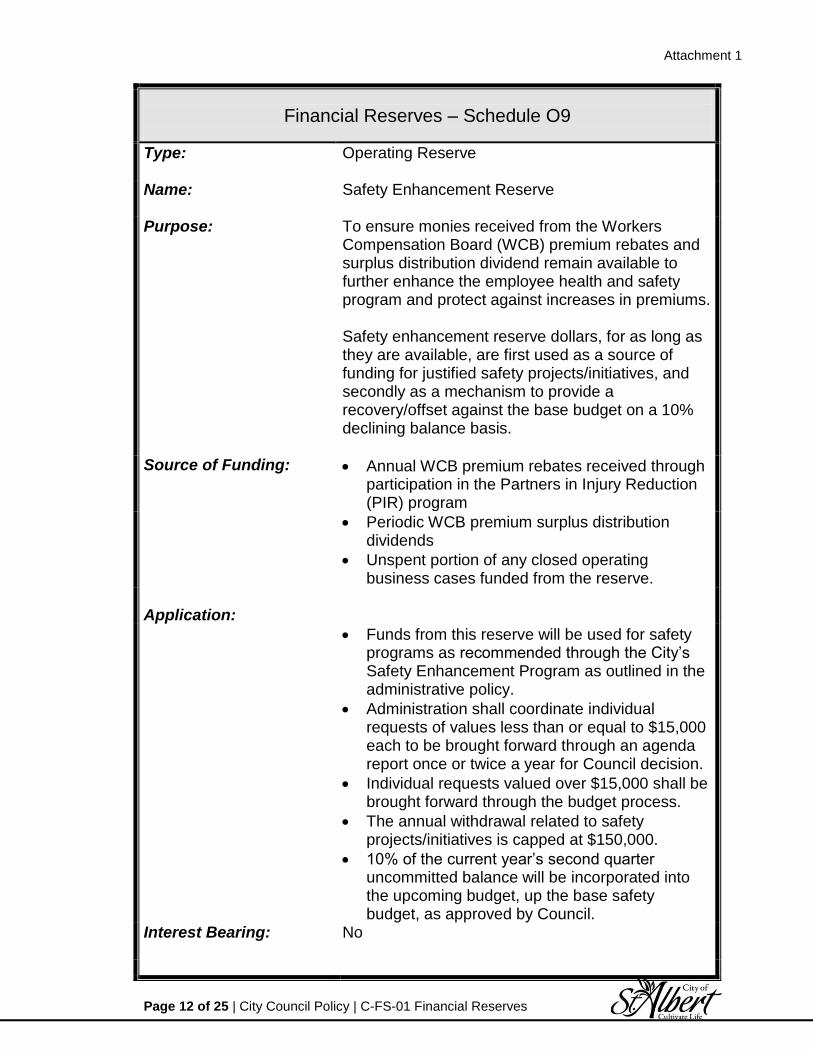

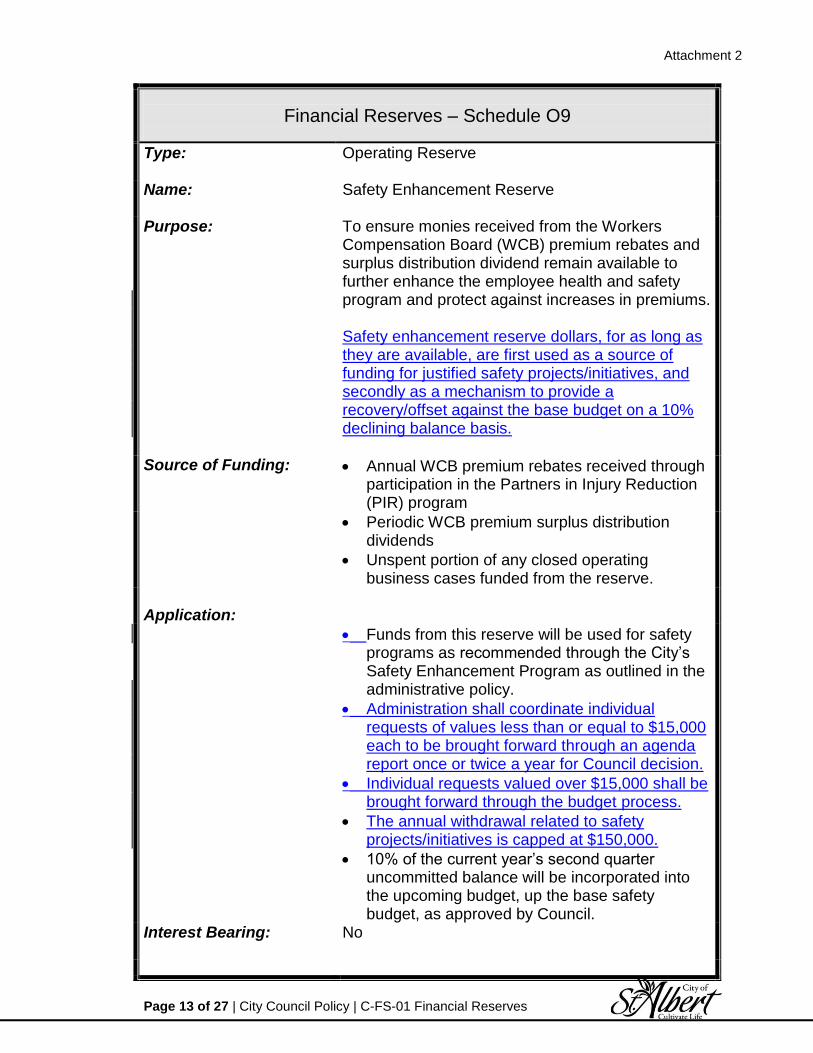

Financial Reserves – Schedule O9

Type:

Operating Reserve

Name:

Safety Enhancement Reserve

Purpose:

To ensure monies received from the Workers Compensation Board (WCB) premium rebates and surplus distribution dividend remain available to further enhance the employee health and safety program and protect against increases in premiums. Safety enhancement reserve dollars, for as long as they are available, are first used as a source of funding for justified safety projects/initiatives, and secondly as a mechanism to provide a recovery/offset against the base budget on a 10% declining balance basis.

Source of Funding:

Annual WCB premium rebates received through participation in the Partners in Injury Reduction (PIR) program

Periodic WCB premium surplus distribution dividends

Unspent portion of any closed operating business cases funded from the reserve.

Application:

Funds from this reserve will be used for safety programs as recommended through the City’s Safety Enhancement Program as outlined in the administrative policy.

Administration shall coordinate individual requests of values less than or equal to $15,000 each to be brought forward through an agenda report once or twice a year for Council decision.

Individual requests valued over $15,000 shall be brought forward through the budget process.

The annual withdrawal related to safety projects/initiatives is capped at $150,000.

10% of the current year’s second quarter uncommitted balance will be incorporated into the upcoming budget, up the base safety budget, as approved by Council.

Interest Bearing:

No

Attachment 1

Page 13 of 25 | City Council Policy | C-FS-01 Financial Reserves

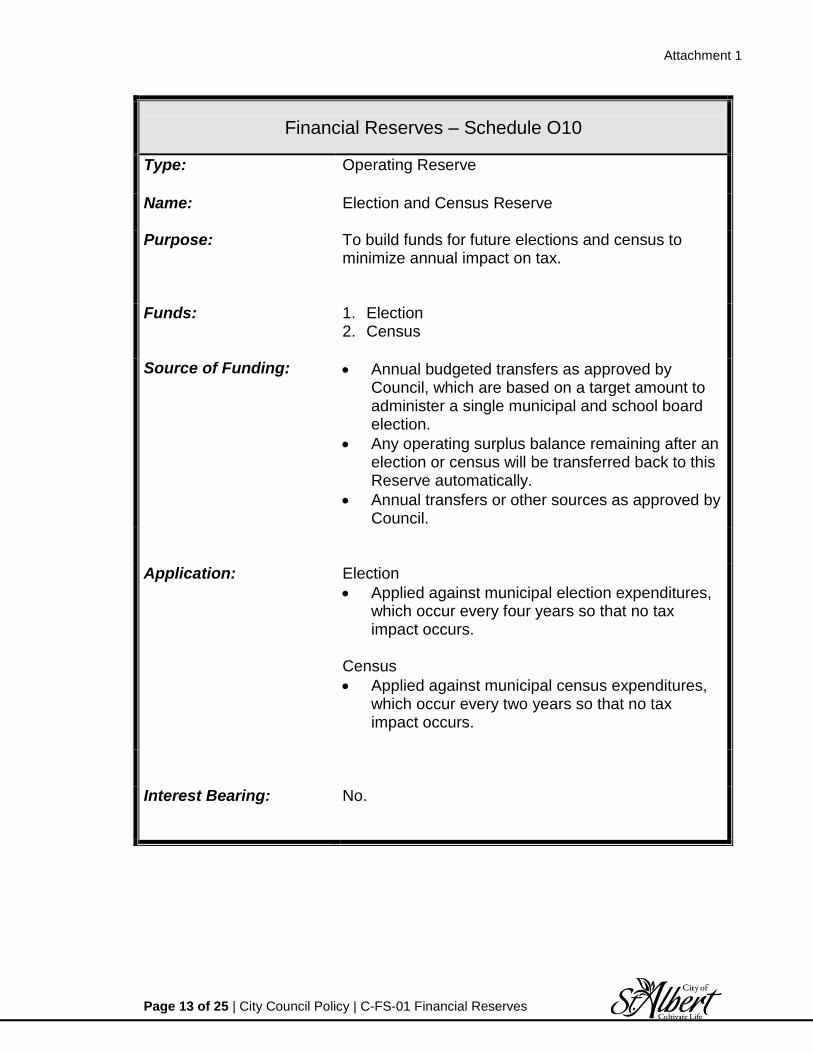

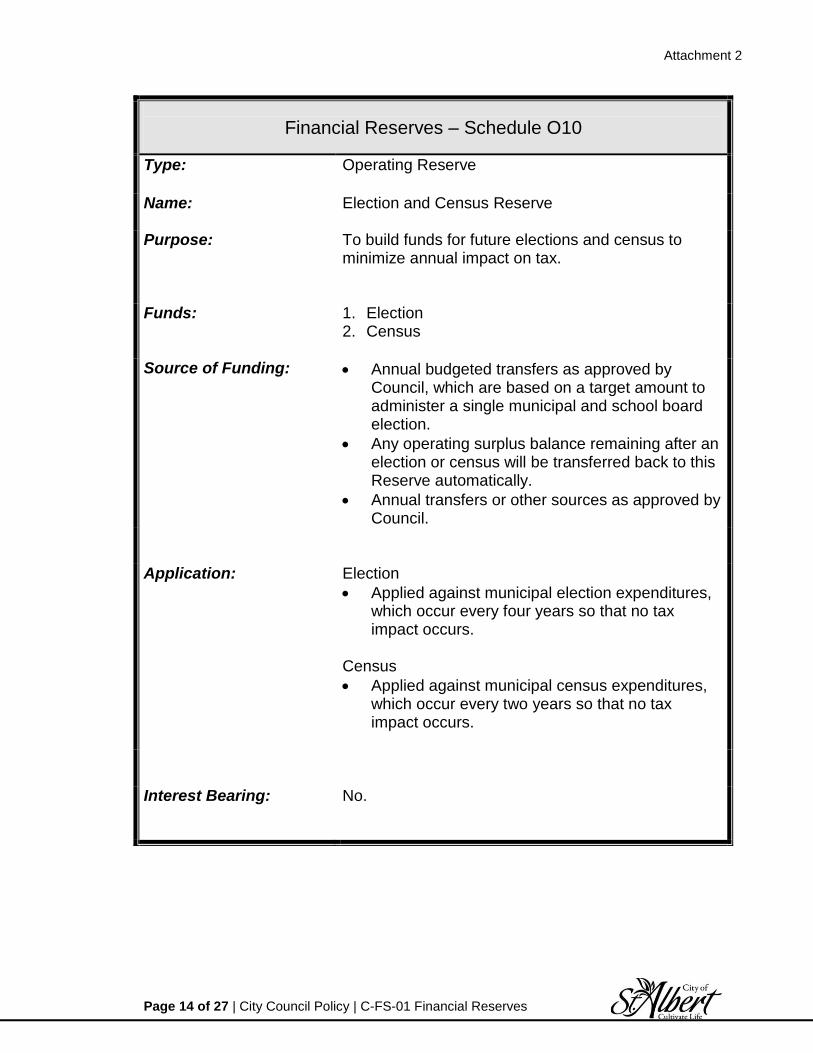

Financial Reserves – Schedule O10

Type:

Operating Reserve

Name:

Election and Census Reserve

Purpose:

To build funds for future elections and census to minimize annual impact on tax.

Funds: 1. Election 2. Census

Source of Funding:

Annual budgeted transfers as approved by Council, which are based on a target amount to administer a single municipal and school board election.

Any operating surplus balance remaining after an election or census will be transferred back to this Reserve automatically.

Annual transfers or other sources as approved by Council.

Application:

Election

Applied against municipal election expenditures, which occur every four years so that no tax impact occurs.

Census

Applied against municipal census expenditures, which occur every two years so that no tax impact occurs.

Interest Bearing:

No.

Attachment 1

Page 14 of 25 | City Council Policy | C-FS-01 Financial Reserves

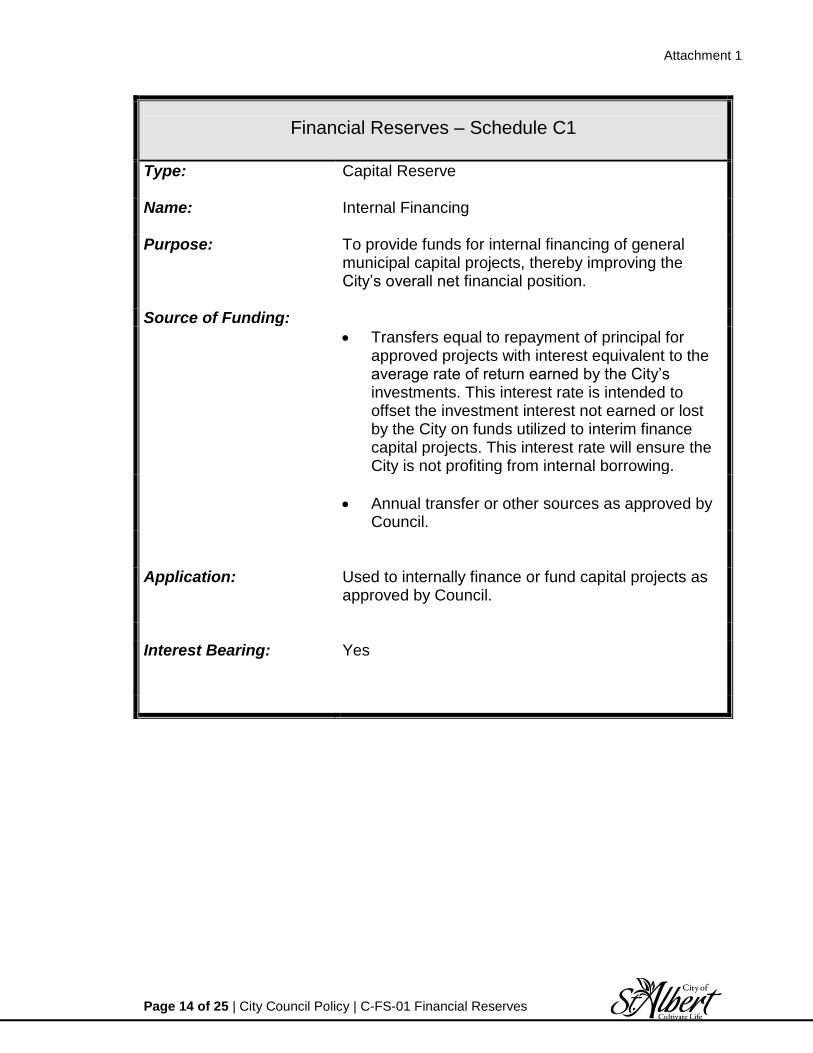

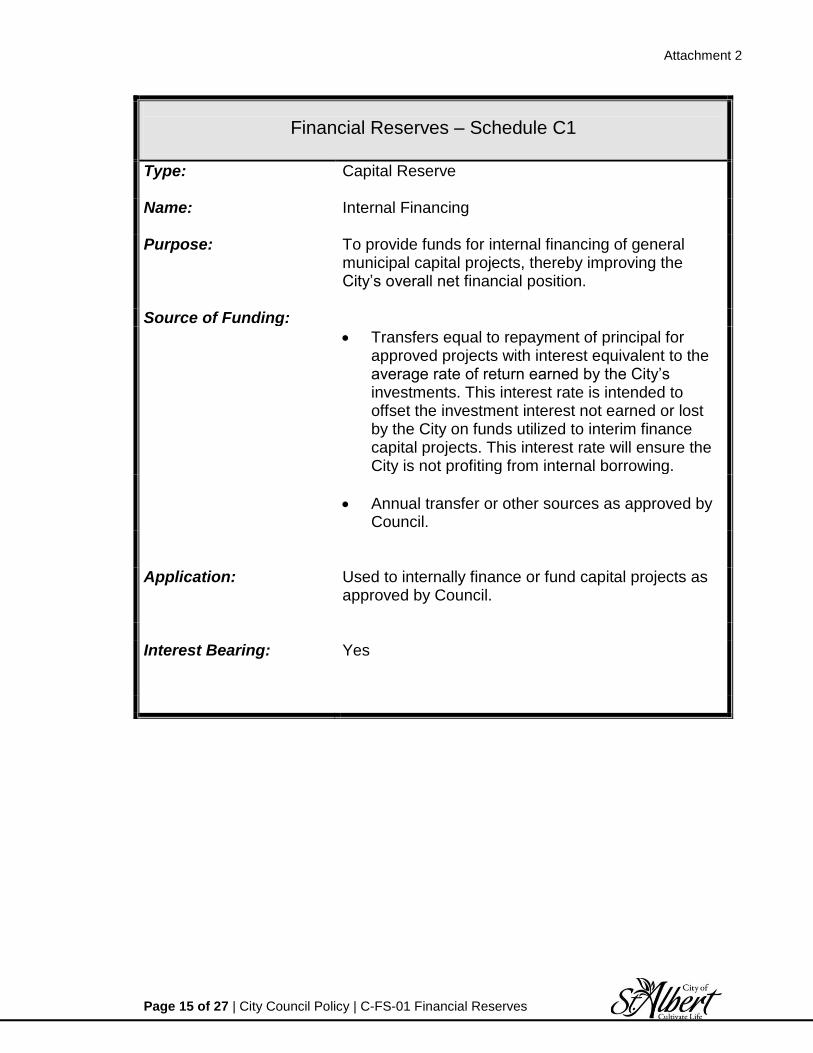

Financial Reserves – Schedule C1 Type:

Capital Reserve

Name:

Internal Financing

Purpose:

To provide funds for internal financing of general municipal capital projects, thereby improving the City’s overall net financial position.

Source of Funding:

Transfers equal to repayment of principal for approved projects with interest equivalent to the average rate of return earned by the City’s investments. This interest rate is intended to offset the investment interest not earned or lost by the City on funds utilized to interim finance capital projects. This interest rate will ensure the City is not profiting from internal borrowing.

Annual transfer or other sources as approved by Council.

Application:

Used to internally finance or fund capital projects as approved by Council.

Interest Bearing:

Yes

Attachment 1

Page 15 of 25 | City Council Policy | C-FS-01 Financial Reserves

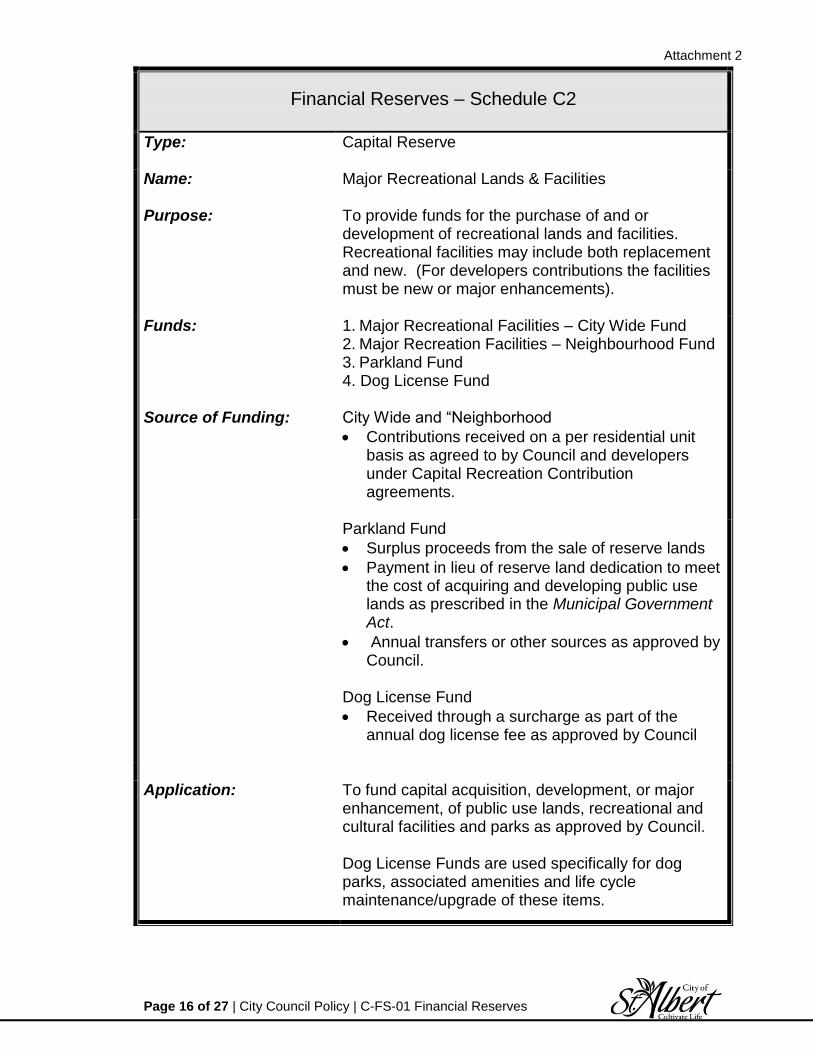

Financial Reserves – Schedule C2

Type:

Capital Reserve

Name:

Major Recreational Lands & Facilities

Purpose:

To provide funds for the purchase of and or development of recreational lands and facilities. Recreational facilities may include both replacement and new. (For developers contributions the facilities must be new or major enhancements).

Funds: 1. Major Recreational Facilities – City Wide Fund 2. Major Recreation Facilities – Neighbourhood Fund 3. Parkland Fund 4. Dog License Fund

Source of Funding:

City Wide and “Neighborhood

Contributions received on a per residential unit basis as agreed to by Council and developers under Capital Recreation Contribution agreements.

Parkland Fund

Surplus proceeds from the sale of reserve lands

Payment in lieu of reserve land dedication to meet the cost of acquiring and developing public use lands as prescribed in the Municipal Government Act.

Annual transfers or other sources as approved by Council.

Dog License Fund

Received through a surcharge as part of the annual dog license fee as approved by Council

Application:

To fund capital acquisition, development, or major enhancement, of public use lands, recreational and cultural facilities and parks as approved by Council. Dog License Funds are used specifically for dog parks, associated amenities and life cycle maintenance/upgrade of these items.

Attachment 1

Page 16 of 25 | City Council Policy | C-FS-01 Financial Reserves

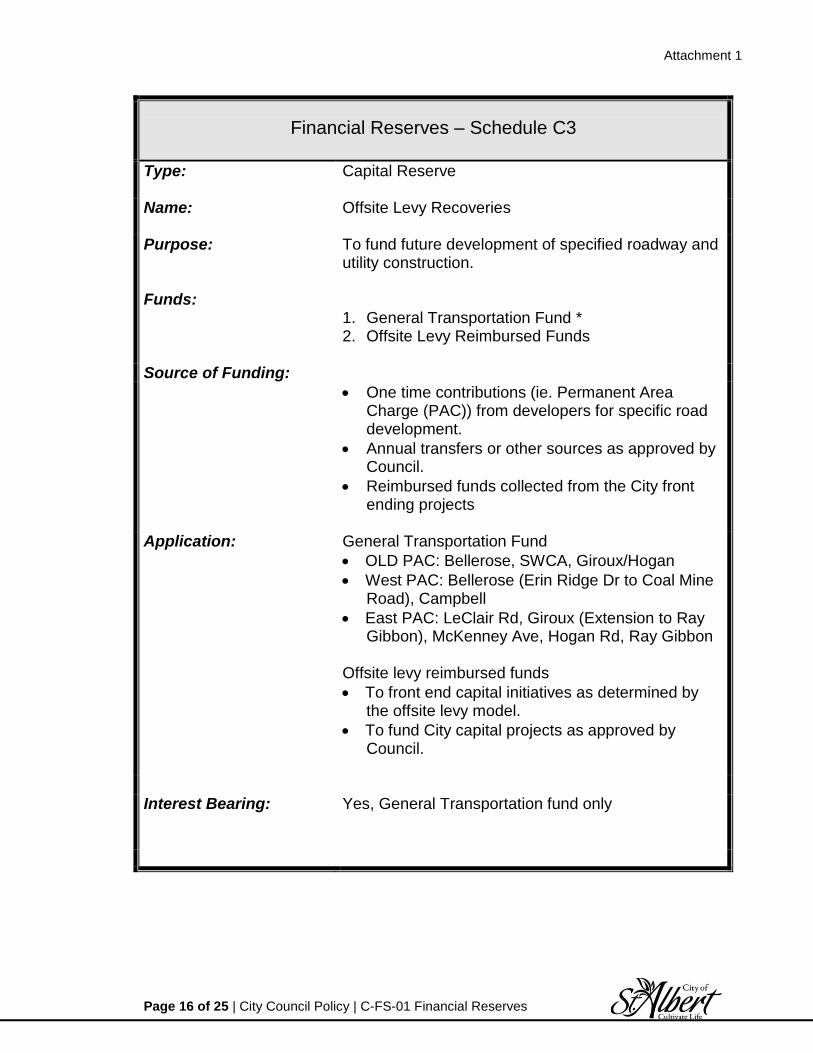

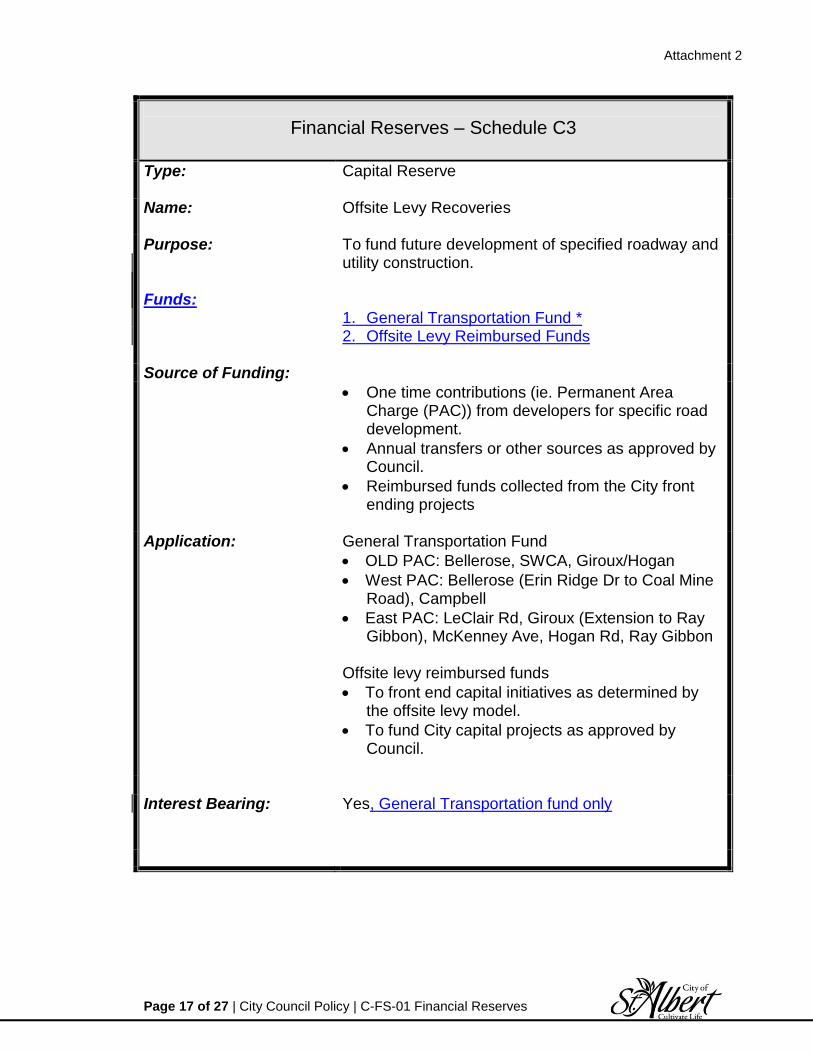

Financial Reserves – Schedule C3 Type:

Capital Reserve

Name:

Offsite Levy Recoveries

Purpose: Funds:

To fund future development of specified roadway and utility construction.

1. 1. General Transportation Fund * 2. Offsite Levy Reimbursed Funds

Source of Funding:

One time contributions (ie. Permanent Area Charge (PAC)) from developers for specific road development.

Annual transfers or other sources as approved by Council.

Reimbursed funds collected from the City front ending projects

Application:

General Transportation Fund

OLD PAC: Bellerose, SWCA, Giroux/Hogan

West PAC: Bellerose (Erin Ridge Dr to Coal Mine Road), Campbell

East PAC: LeClair Rd, Giroux (Extension to Ray Gibbon), McKenney Ave, Hogan Rd, Ray Gibbon

Offsite levy reimbursed funds

To front end capital initiatives as determined by the offsite levy model.

To fund City capital projects as approved by Council.

Interest Bearing:

Yes, General Transportation fund only

Attachment 1

Page 17 of 25 | City Council Policy | C-FS-01 Financial Reserves

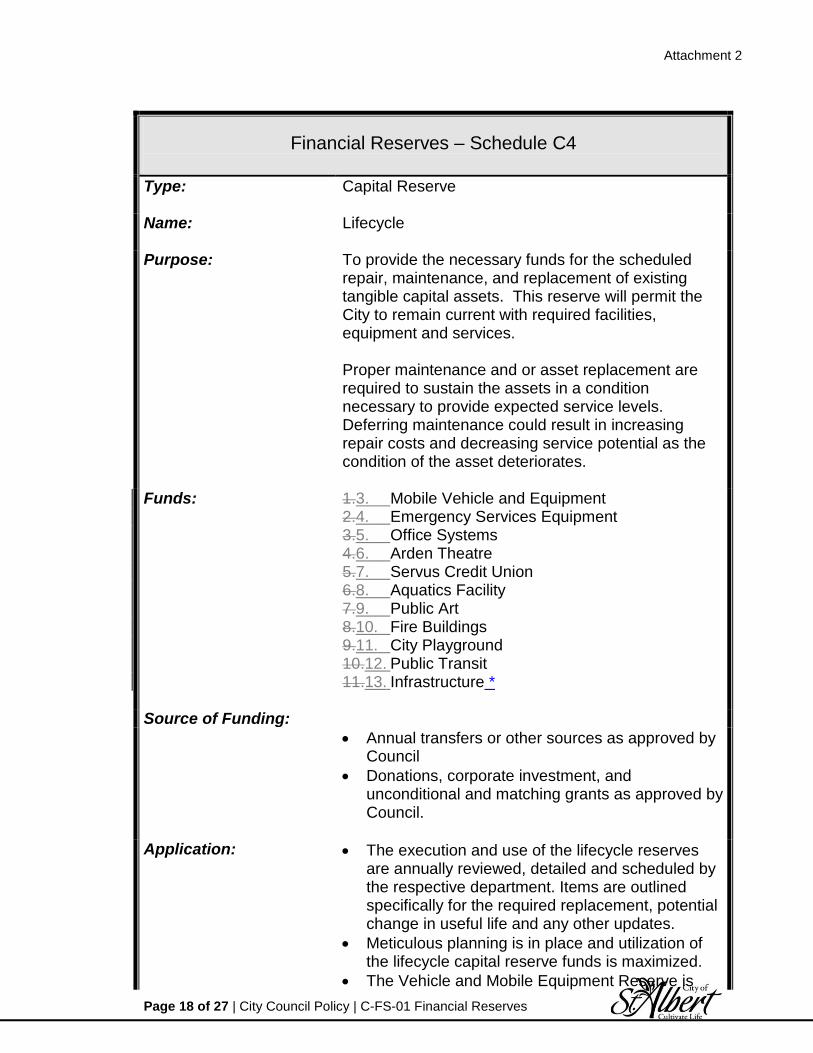

Financial Reserves – Schedule C4 Type:

Capital Reserve

Name:

Lifecycle

Purpose:

To provide the necessary funds for the scheduled repair, maintenance, and replacement of existing tangible capital assets. This reserve will permit the City to remain current with required facilities, equipment and services. Proper maintenance and or asset replacement are required to sustain the assets in a condition necessary to provide expected service levels. Deferring maintenance could result in increasing repair costs and decreasing service potential as the condition of the asset deteriorates.

Funds: 3. Mobile Vehicle and Equipment 4. Emergency Services Equipment 5. Office Systems 6. Arden Theatre 7. Servus Credit Union 8. Aquatics Facility 9. Public Art 10. Fire Buildings 11. City Playground 12. Public Transit 13. Infrastructure *

Source of Funding:

Annual transfers or other sources as approved by Council

Donations, corporate investment, and unconditional and matching grants as approved by Council.

Application:

The execution and use of the lifecycle reserves are annually reviewed, detailed and scheduled by the respective department. Items are outlined specifically for the required replacement, potential change in useful life and any other updates.

Meticulous planning is in place and utilization of the lifecycle capital reserve funds is maximized.

The Vehicle and Mobile Equipment Reserve is

Attachment 1

Page 18 of 25 | City Council Policy | C-FS-01 Financial Reserves

subject to the conditions of Administrative Policy A-P&E-04 Mobile Vehicle and Equipment Replacement.

Interest Bearing:

Yes, with the exception of Infrastructure

Attachment 1

Page 19 of 25 | City Council Policy | C-FS-01 Financial Reserves

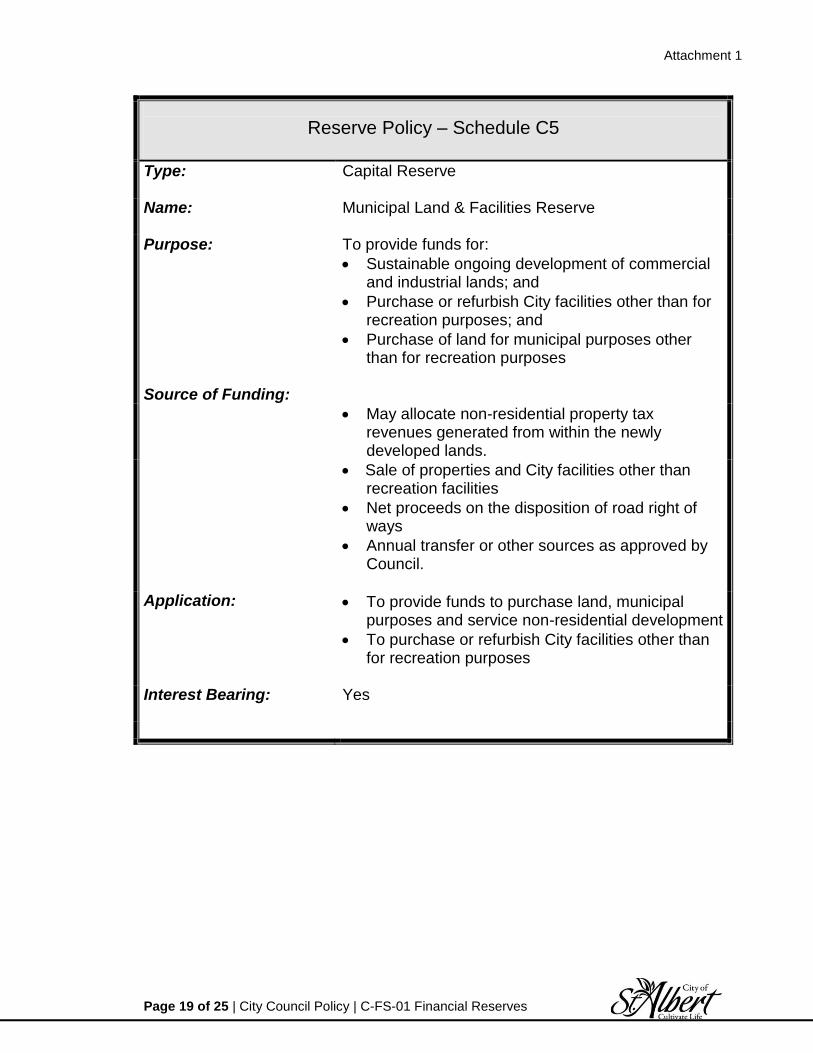

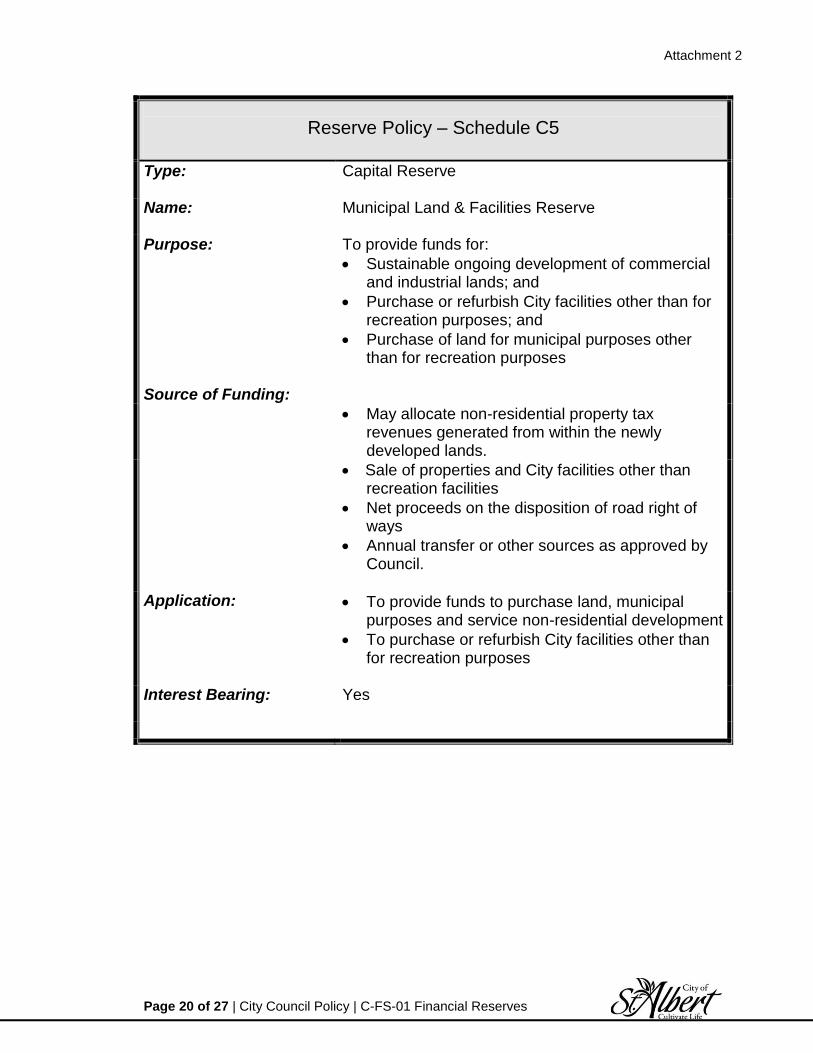

Reserve Policy – Schedule C5 Type:

Capital Reserve

Name:

Municipal Land & Facilities Reserve

Purpose:

To provide funds for:

Sustainable ongoing development of commercial and industrial lands; and

Purchase or refurbish City facilities other than for recreation purposes; and

Purchase of land for municipal purposes other than for recreation purposes

Source of Funding:

May allocate non-residential property tax revenues generated from within the newly developed lands.

Sale of properties and City facilities other than recreation facilities

Net proceeds on the disposition of road right of ways

Annual transfer or other sources as approved by Council.

Application:

To provide funds to purchase land, municipal purposes and service non-residential development

To purchase or refurbish City facilities other than for recreation purposes

Interest Bearing:

Yes

Attachment 1

Page 20 of 25 | City Council Policy | C-FS-01 Financial Reserves

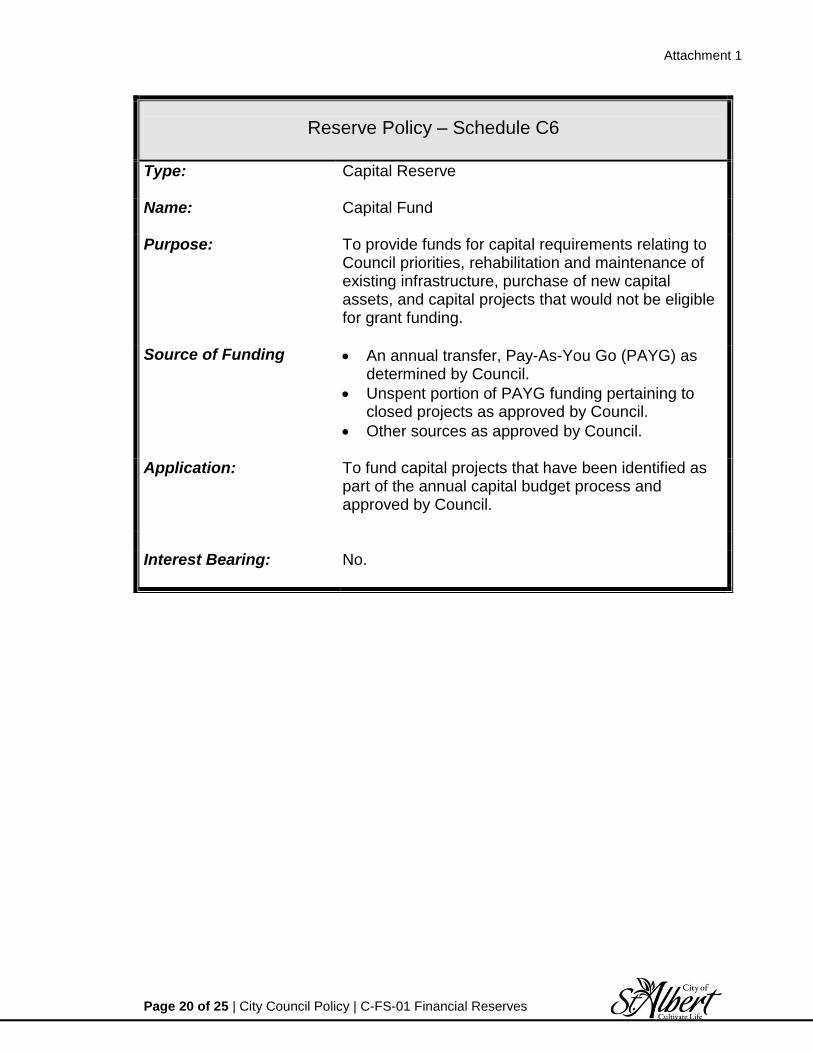

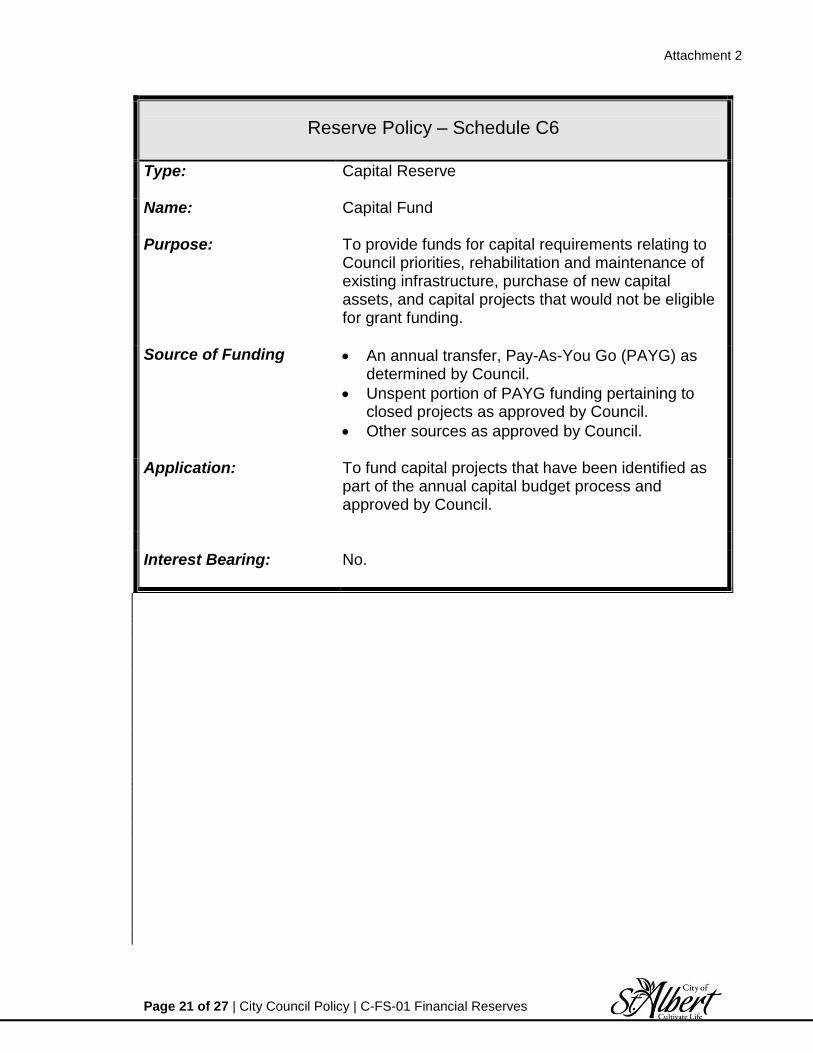

Reserve Policy – Schedule C6 Type:

Capital Reserve

Name:

Capital Fund

Purpose:

To provide funds for capital requirements relating to Council priorities, rehabilitation and maintenance of existing infrastructure, purchase of new capital assets, and capital projects that would not be eligible for grant funding.

Source of Funding

An annual transfer, Pay-As-You Go (PAYG) as determined by Council.

Unspent portion of PAYG funding pertaining to closed projects as approved by Council.

Other sources as approved by Council.

Application:

To fund capital projects that have been identified as part of the annual capital budget process and approved by Council.

Interest Bearing:

No.

Attachment 1

Page 21 of 25 | City Council Policy | C-FS-01 Financial Reserves

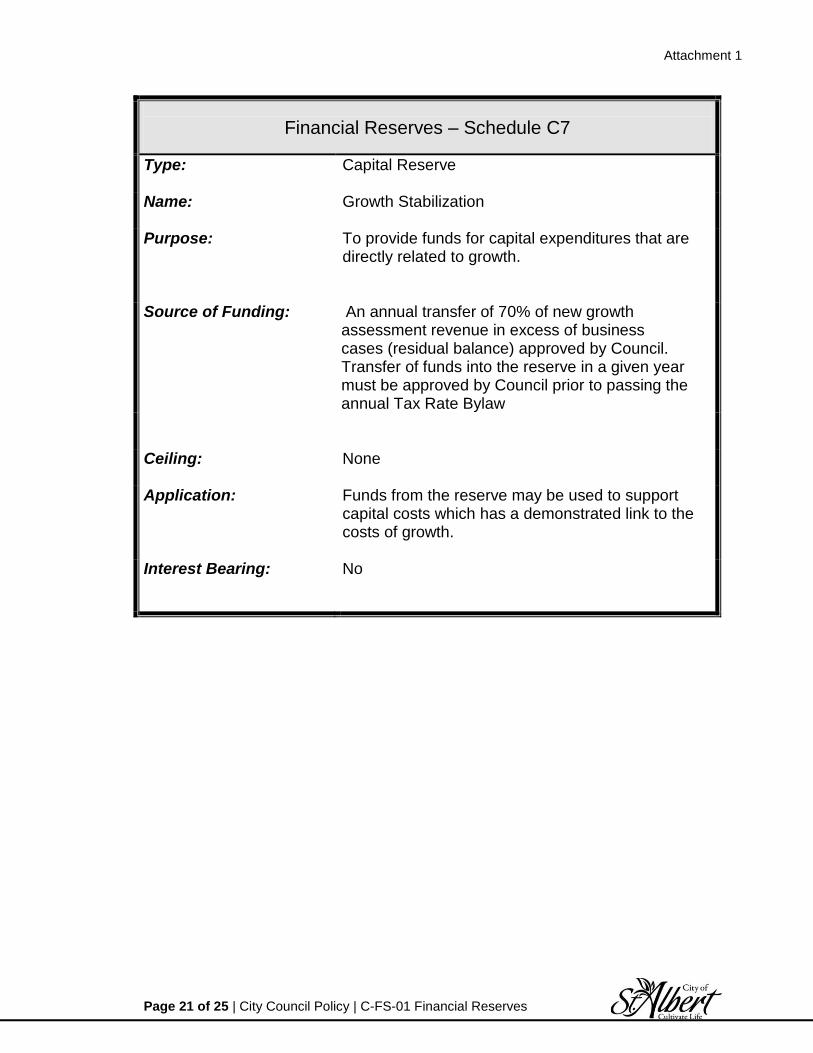

Financial Reserves – Schedule C7

Type:

Capital Reserve

Name:

Growth Stabilization

Purpose:

To provide funds for capital expenditures that are directly related to growth.

Source of Funding:

An annual transfer of 70% of new growth assessment revenue in excess of business cases (residual balance) approved by Council. Transfer of funds into the reserve in a given year must be approved by Council prior to passing the annual Tax Rate Bylaw

Ceiling:

None

Application:

Funds from the reserve may be used to support capital costs which has a demonstrated link to the costs of growth.

Interest Bearing:

No

Attachment 1

Page 22 of 25 | City Council Policy | C-FS-01 Financial Reserves

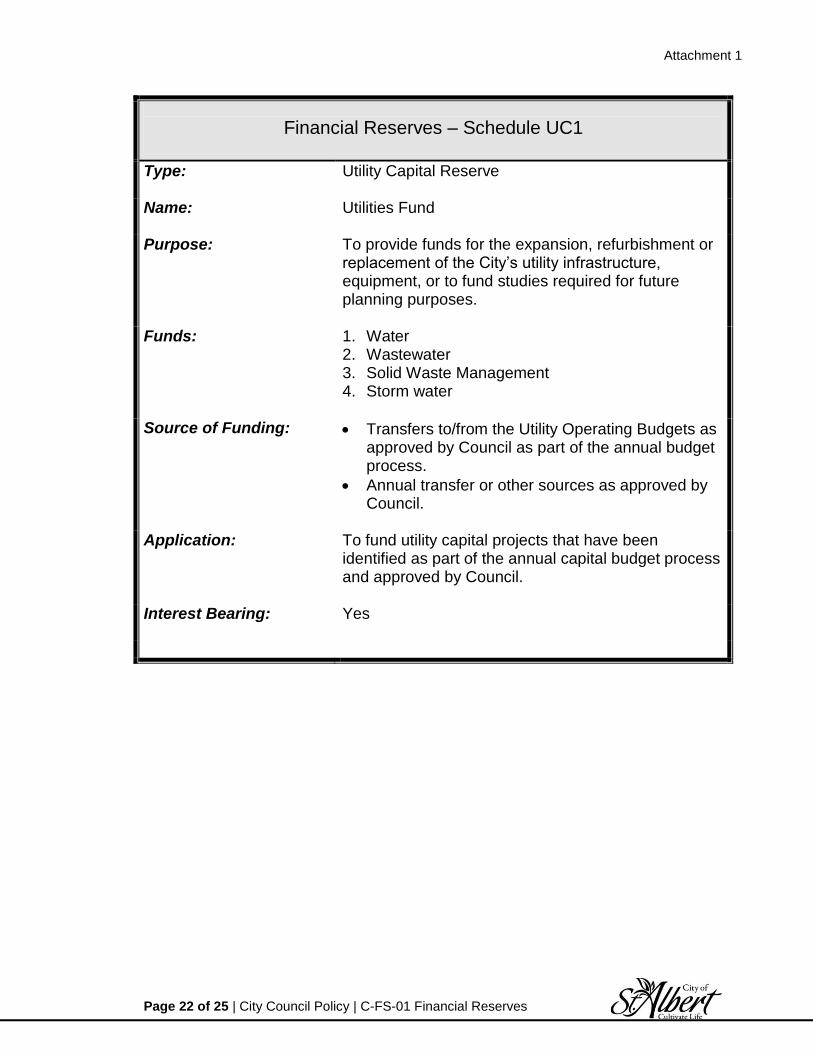

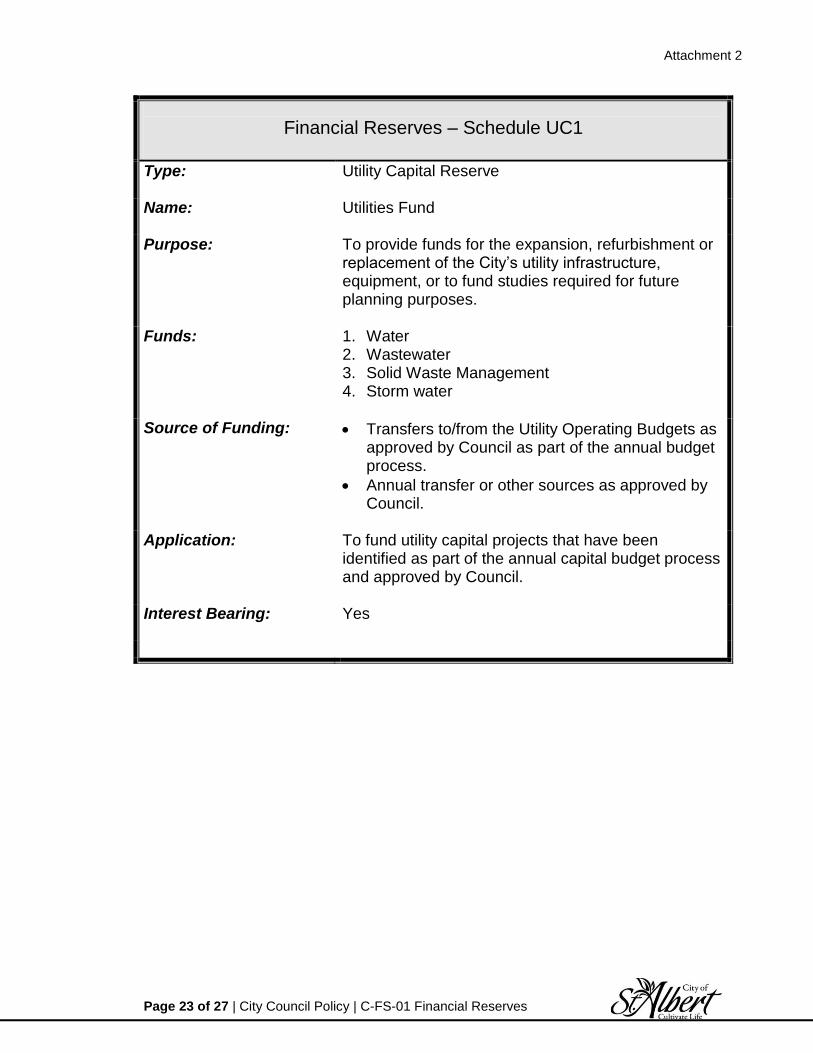

Financial Reserves – Schedule UC1 Type:

Utility Capital Reserve

Name:

Utilities Fund

Purpose:

To provide funds for the expansion, refurbishment or replacement of the City’s utility infrastructure, equipment, or to fund studies required for future planning purposes.

Funds: 1. Water 2. Wastewater 3. Solid Waste Management 4. Storm water

Source of Funding:

Transfers to/from the Utility Operating Budgets as approved by Council as part of the annual budget process.

Annual transfer or other sources as approved by Council.

Application:

To fund utility capital projects that have been identified as part of the annual capital budget process and approved by Council.

Interest Bearing:

Yes

Attachment 1

Page 23 of 25 | City Council Policy | C-FS-01 Financial Reserves

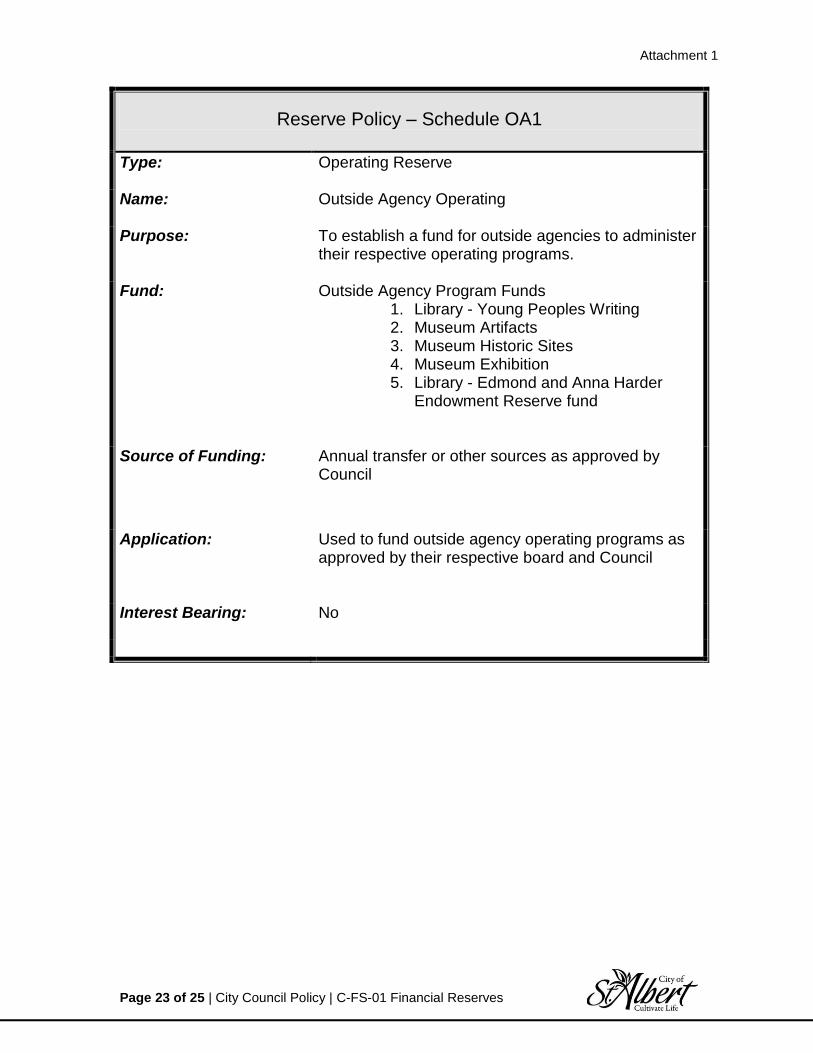

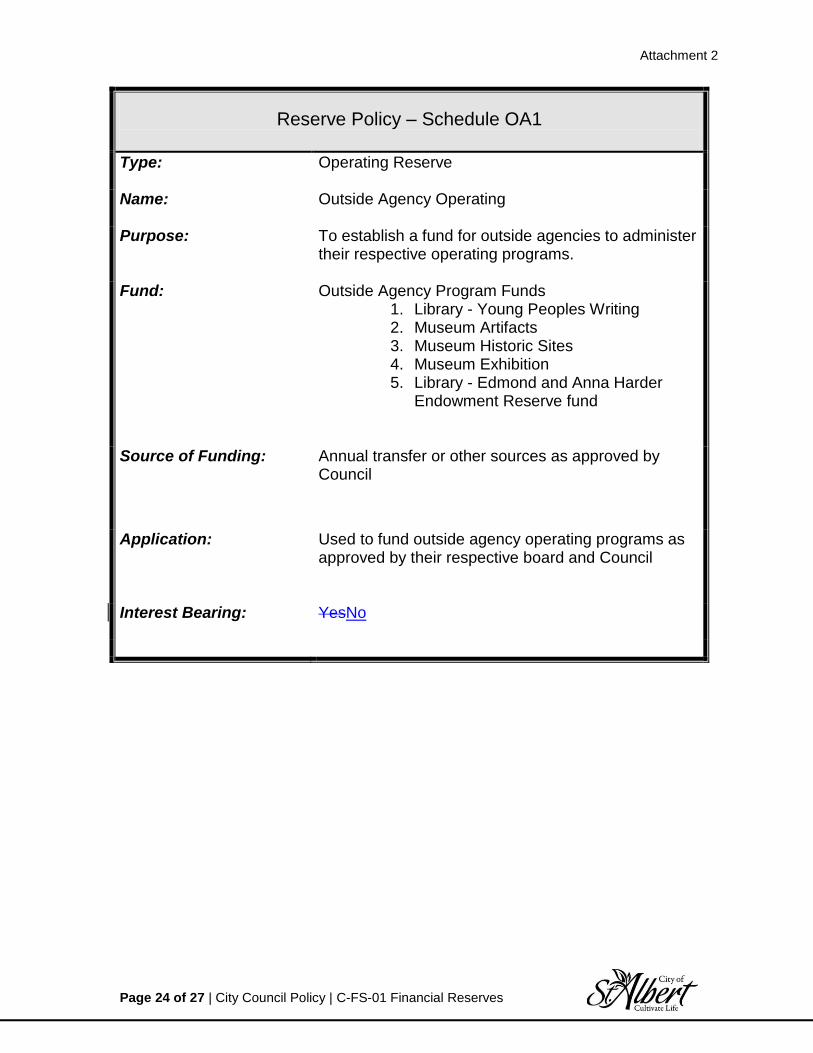

Reserve Policy – Schedule OA1 Type:

Operating Reserve

Name:

Outside Agency Operating

Purpose: To establish a fund for outside agencies to administer their respective operating programs.

Fund: Outside Agency Program Funds 1. Library - Young Peoples Writing 2. Museum Artifacts 3. Museum Historic Sites 4. Museum Exhibition 5. Library - Edmond and Anna Harder

Endowment Reserve fund

Source of Funding: Annual transfer or other sources as approved by Council

Application:

Used to fund outside agency operating programs as approved by their respective board and Council

Interest Bearing:

No

Attachment 1

Page 24 of 25 | City Council Policy | C-FS-01 Financial Reserves

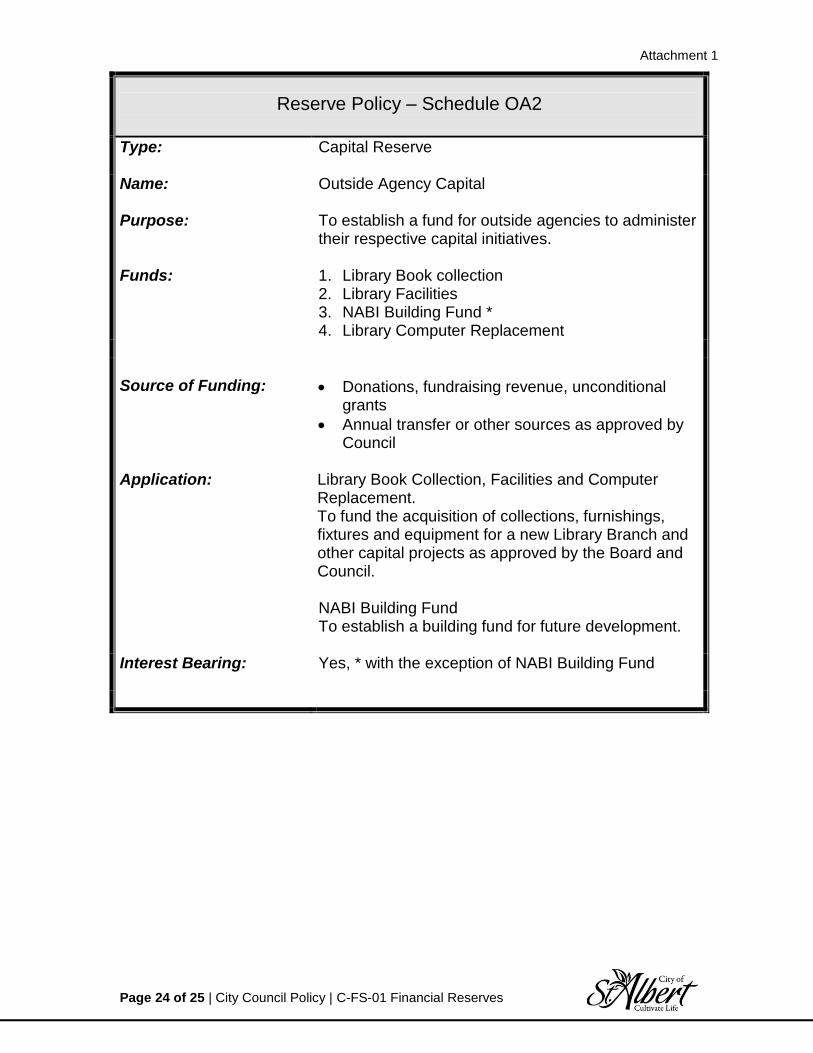

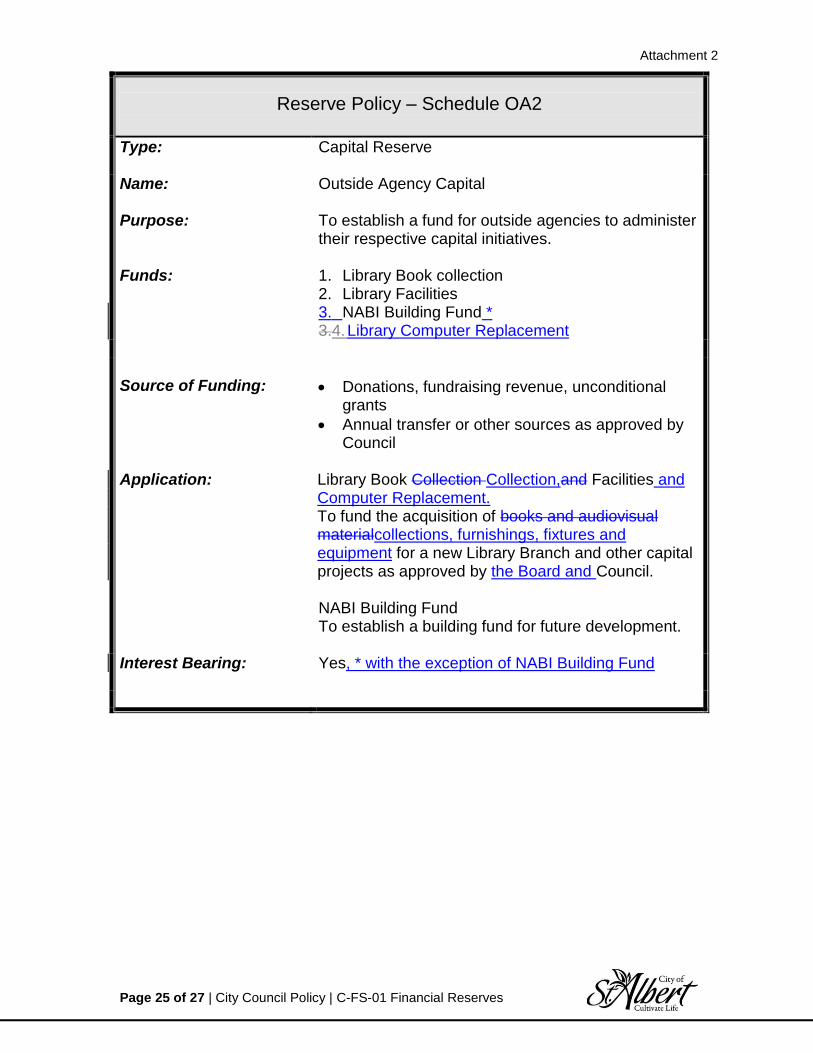

Reserve Policy – Schedule OA2 Type:

Capital Reserve

Name:

Outside Agency Capital

Purpose:

To establish a fund for outside agencies to administer their respective capital initiatives.

Funds: 1. Library Book collection 2. Library Facilities 3. NABI Building Fund * 4. Library Computer Replacement

Source of Funding:

Donations, fundraising revenue, unconditional grants

Annual transfer or other sources as approved by Council

Application:

Library Book Collection, Facilities and Computer Replacement. To fund the acquisition of collections, furnishings, fixtures and equipment for a new Library Branch and other capital projects as approved by the Board and Council. NABI Building Fund To establish a building fund for future development.

Interest Bearing:

Yes, * with the exception of NABI Building Fund

Attachment 1

Page 25 of 25 | City Council Policy | C-FS-01 Financial Reserves

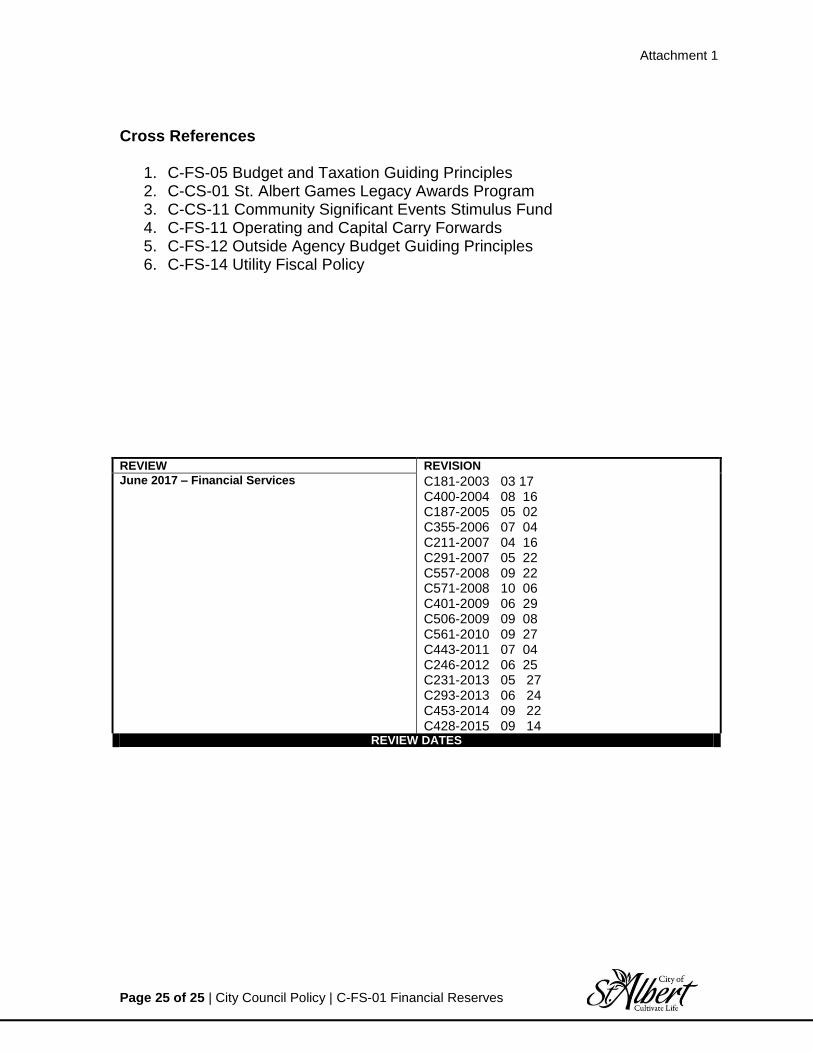

Cross References

1. C-FS-05 Budget and Taxation Guiding Principles 2. C-CS-01 St. Albert Games Legacy Awards Program 3. C-CS-11 Community Significant Events Stimulus Fund 4. C-FS-11 Operating and Capital Carry Forwards 5. C-FS-12 Outside Agency Budget Guiding Principles 6. C-FS-14 Utility Fiscal Policy

REVIEW REVISION

June 2017 – Financial Services C181-2003 03 17 C400-2004 08 16 C187-2005 05 02 C355-2006 07 04 C211-2007 04 16 C291-2007 05 22 C557-2008 09 22

C571-2008 10 06 C401-2009 06 29 C506-2009 09 08 C561-2010 09 27 C443-2011 07 04 C246-2012 06 25 C231-2013 05 27 C293-2013 06 24 C453-2014 09 22 C428-2015 09 14

REVIEW DATES

Attachment 2

Page 1 of 27 | City Council Policy | C-FS-01 Financial Reserves

CITY OF ST. ALBERT

CITY COUNCIL POLICY NUMBER TITLE

C-FS-01 Financial Reserves

ORIGINAL APPROVAL DATE DATE LAST REVISED

March 17, 2003 September 14, 2015

Purpose – To set aside funds for the establishment of specific reserves to provide for emergent financial needs, stabilize tax rates, to set aside funds for the replacement of existing equipment, facilities and future projects and to minimize the debt financing needs of the Corporation. Policy Statement – The City of St. Albert recognizes that the ongoing commitment of funds to specific reserves provides for property tax stabilization, contingency funding, and reduces the need for debt financing. Responsibilities 1. The establishment of, contributions to, and withdrawals from, a specific reserve

shall be approved by City Council through resolution or bylaw in accordance with the Municipal Government Act or as otherwise stated in the specified schedule.

2. Administration of all reserves will be carried out by the City Manager or his designate.

Service Standards/ Expectations 1. Transfers to/from reserves will be restricted as outlined in each specific

reserve schedule. 2.1.

3.2. Interest earnings are intended to be applied to reserves if there are external

requirements based on legislation or agreements, or as approved by Council, and will be added to reserves according to the schedule. The interest will be

Attachment 2

Page 2 of 27 | City Council Policy | C-FS-01 Financial Reserves

applied monthly based on the net weighted average of the reserve balance relative to all interest earned by the City’s investment portfolio.

4.3. Where appropriate, each reserve will be supported by a 10-year projection for receipt and disbursement of funds. These projections will be updated annually as part of the budget process.

5.4. Reserves are assumed to be ongoing unless otherwise stated in the specified schedule.

6.5. Reserves are assumed to have no ceiling unless otherwise stated in the specified schedule.

7.6. Reserve reporting will form a part of the quarterly and annual financial statements and significant transactions affecting these will be highlighted in the comments.

8.7. This policy along with the approved reserve schedules and balances will be reviewed by Administration annually.

Operating Reserve Schedules O1 Stabilization O2 Growth Stabilization O3 Operating Programs O4 Risk Management O5 Automated Traffic Enforcement Technology – Speed on Green O6 LRT/BRT Reserve O7 Children’s Festival Fund O8 RCMP Contract Expense Reserve O9 Safety Enhancement Program O10 Election and Census Reserve

Capital Reserve Schedules C1 Internal Financing

Attachment 2

Page 3 of 27 | City Council Policy | C-FS-01 Financial Reserves

C2 Major Recreational Lands & Facilities 1. Major Recreational Facilities Fund – City Wide 2. Major Recreational Facilities Fund – Neighbourhood 3. Parkland Fund 4. Dog License Fund

C3 Offsite levy recoveries 1. General Transportation Fund 2. Offsite levy reimbursed Funds C4 Lifecycle

1. Mobile Equipment 2. Emergency Services Equipment 3. Office Systems 4. Arden Theatre 5. Servus Credit Union Place 6. Aquatics Facility 7. Public Art 8. Fire Buildings 9. City Playground 10. Public Transit 11. Infrastructure

C5 Municipal Land & Facilities Reserve C6 Capital Fund C7O2 Growth Stabilization

Utility Reserve Schedule UC1 Utilities Fund

1. Water 2. Wastewater 3. Solid Waste 4. Storm water

Outside Agency Reserve Schedule

OA1 Outside Agency Operating OA2 Outside Agency Capital

1. Library Book Collection 2. Library Facilities 3. NABI Building Fund

Attachment 2

Page 4 of 27 | City Council Policy | C-FS-01 Financial Reserves

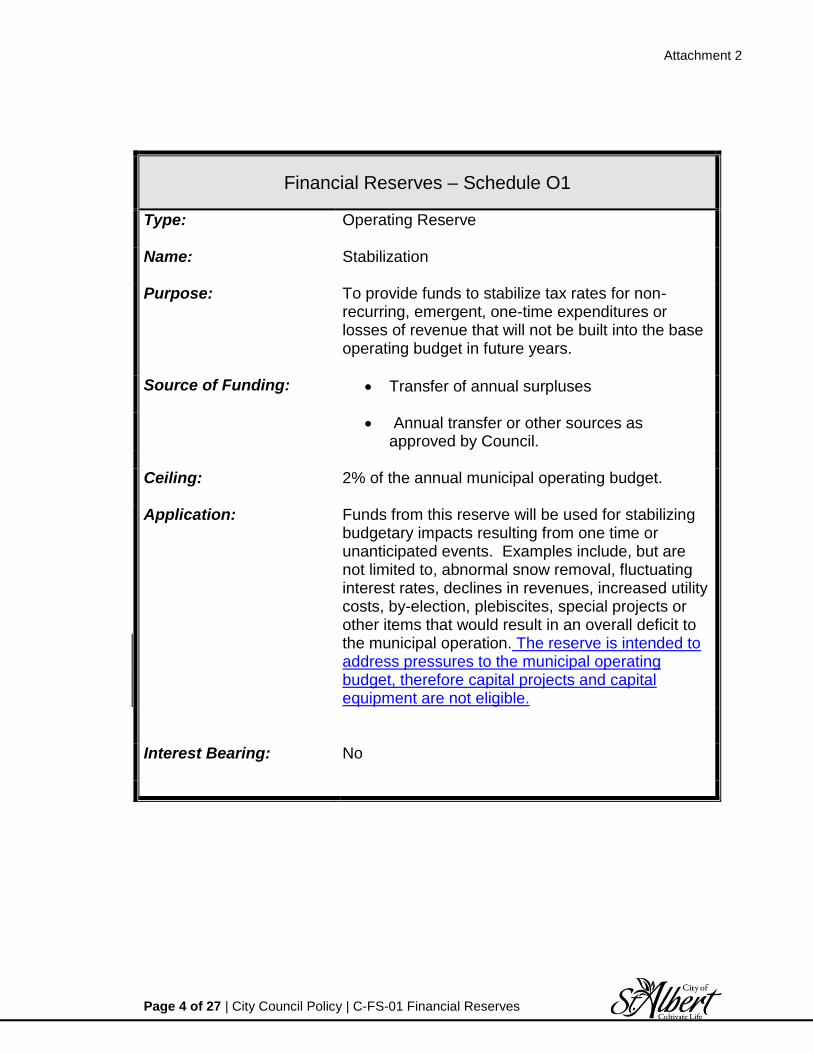

Financial Reserves – Schedule O1

Type:

Operating Reserve

Name:

Stabilization

Purpose:

To provide funds to stabilize tax rates for non-recurring, emergent, one-time expenditures or losses of revenue that will not be built into the base operating budget in future years.

Source of Funding:

Transfer of annual surpluses

Annual transfer or other sources as approved by Council.

Ceiling:

2% of the annual municipal operating budget.

Application:

Funds from this reserve will be used for stabilizing budgetary impacts resulting from one time or unanticipated events. Examples include, but are not limited to, abnormal snow removal, fluctuating interest rates, declines in revenues, increased utility costs, by-election, plebiscites, special projects or other items that would result in an overall deficit to the municipal operation. The reserve is intended to address pressures to the municipal operating budget, therefore capital projects and capital equipment are not eligible.

Interest Bearing:

No

Attachment 2

Page 5 of 27 | City Council Policy | C-FS-01 Financial Reserves

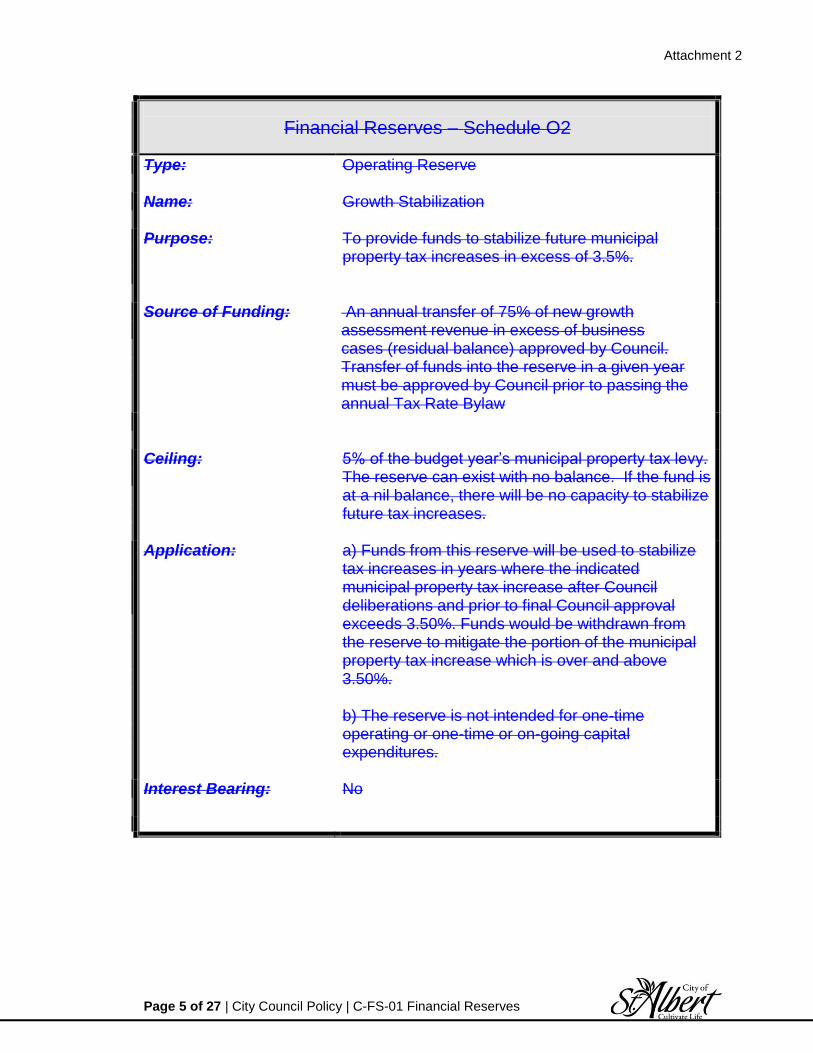

Financial Reserves – Schedule O2

Type:

Operating Reserve

Name:

Growth Stabilization

Purpose:

To provide funds to stabilize future municipal property tax increases in excess of 3.5%.

Source of Funding:

An annual transfer of 75% of new growth assessment revenue in excess of business cases (residual balance) approved by Council. Transfer of funds into the reserve in a given year must be approved by Council prior to passing the annual Tax Rate Bylaw

Ceiling:

5% of the budget year’s municipal property tax levy. The reserve can exist with no balance. If the fund is at a nil balance, there will be no capacity to stabilize future tax increases.

Application:

a) Funds from this reserve will be used to stabilize tax increases in years where the indicated municipal property tax increase after Council deliberations and prior to final Council approval exceeds 3.50%. Funds would be withdrawn from the reserve to mitigate the portion of the municipal property tax increase which is over and above 3.50%. b) The reserve is not intended for one-time operating or one-time or on-going capital expenditures.

Interest Bearing:

No

Attachment 2

Page 6 of 27 | City Council Policy | C-FS-01 Financial Reserves

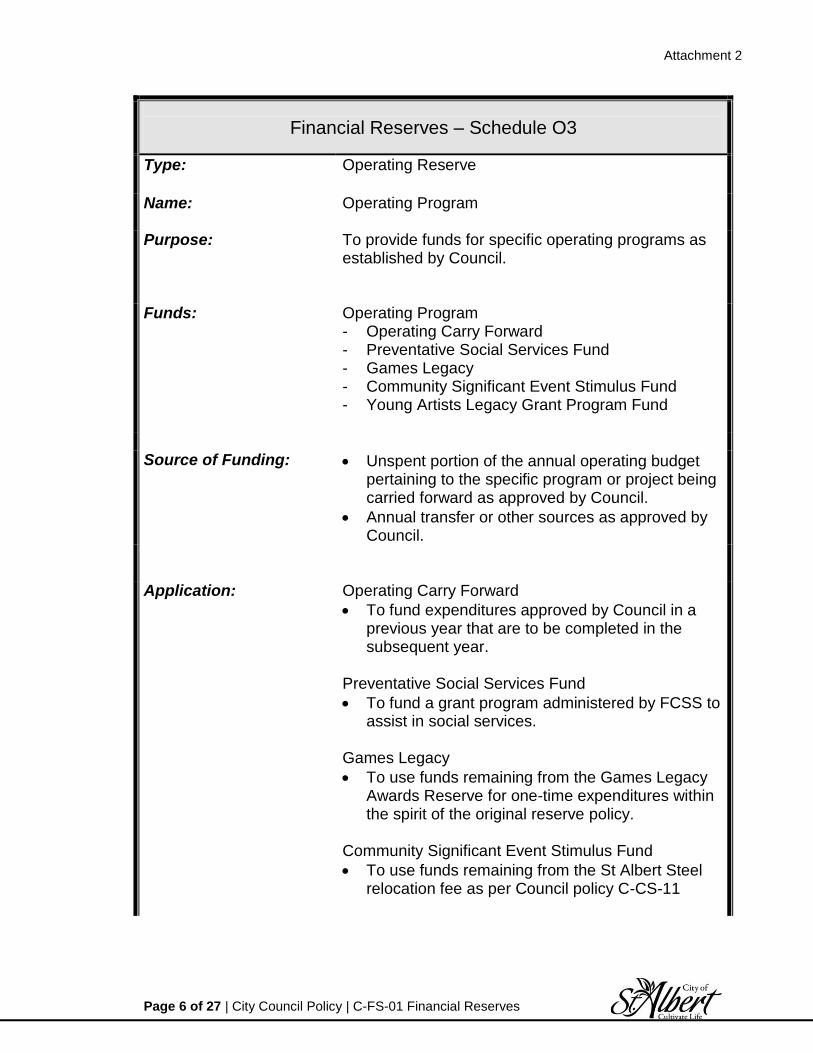

Financial Reserves – Schedule O3

Type:

Operating Reserve

Name:

Operating Program

Purpose:

To provide funds for specific operating programs as established by Council.

Funds: Operating Program - Operating Carry Forward - Preventative Social Services Fund - Games Legacy - Community Significant Event Stimulus Fund - Young Artists Legacy Grant Program Fund

Source of Funding:

Unspent portion of the annual operating budget pertaining to the specific program or project being carried forward as approved by Council.

Annual transfer or other sources as approved by Council.

Application:

Operating Carry Forward

To fund expenditures approved by Council in a previous year that are to be completed in the subsequent year.

Preventative Social Services Fund

To fund a grant program administered by FCSS to assist in social services.

Games Legacy

To use funds remaining from the Games Legacy Awards Reserve for one-time expenditures within the spirit of the original reserve policy.

Community Significant Event Stimulus Fund

To use funds remaining from the St Albert Steel relocation fee as per Council policy C-CS-11

Attachment 2

Page 7 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O3

Young Artists Legacy Grant Program

Interest earned in the Young Artists Legacy Grant Program are to be used specifically for the program and be treated as an endowment.

Interest Bearing:

No, with the exception of Young Artists Legacy Grant Program

Attachment 2

Page 8 of 27 | City Council Policy | C-FS-01 Financial Reserves

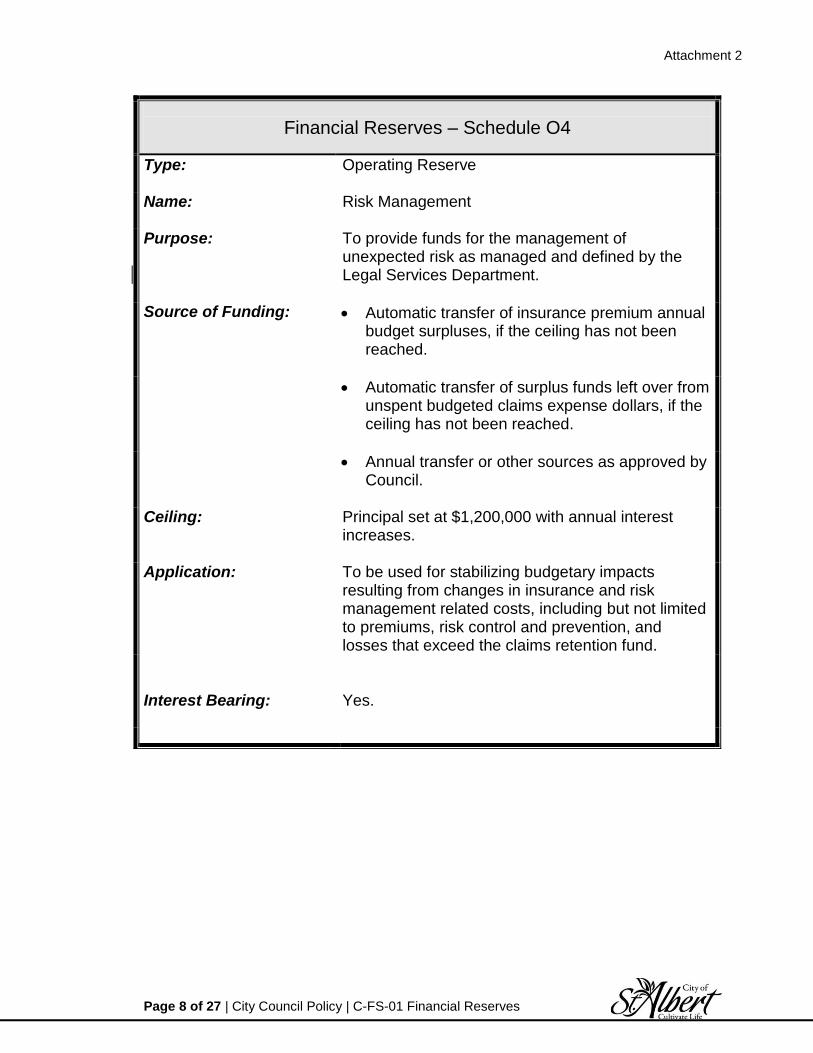

Financial Reserves – Schedule O4

Type:

Operating Reserve

Name:

Risk Management

Purpose:

To provide funds for the management of unexpected risk as managed and defined by the Legal Services Department.

Source of Funding:

Automatic transfer of insurance premium annual budget surpluses, if the ceiling has not been reached.

Automatic transfer of surplus funds left over from unspent budgeted claims expense dollars, if the ceiling has not been reached.

Annual transfer or other sources as approved by

Council.

Ceiling:

Principal set at $1,200,000 with annual interest increases.

Application:

To be used for stabilizing budgetary impacts resulting from changes in insurance and risk management related costs, including but not limited to premiums, risk control and prevention, and losses that exceed the claims retention fund.

Interest Bearing:

Yes.

Attachment 2

Page 9 of 27 | City Council Policy | C-FS-01 Financial Reserves

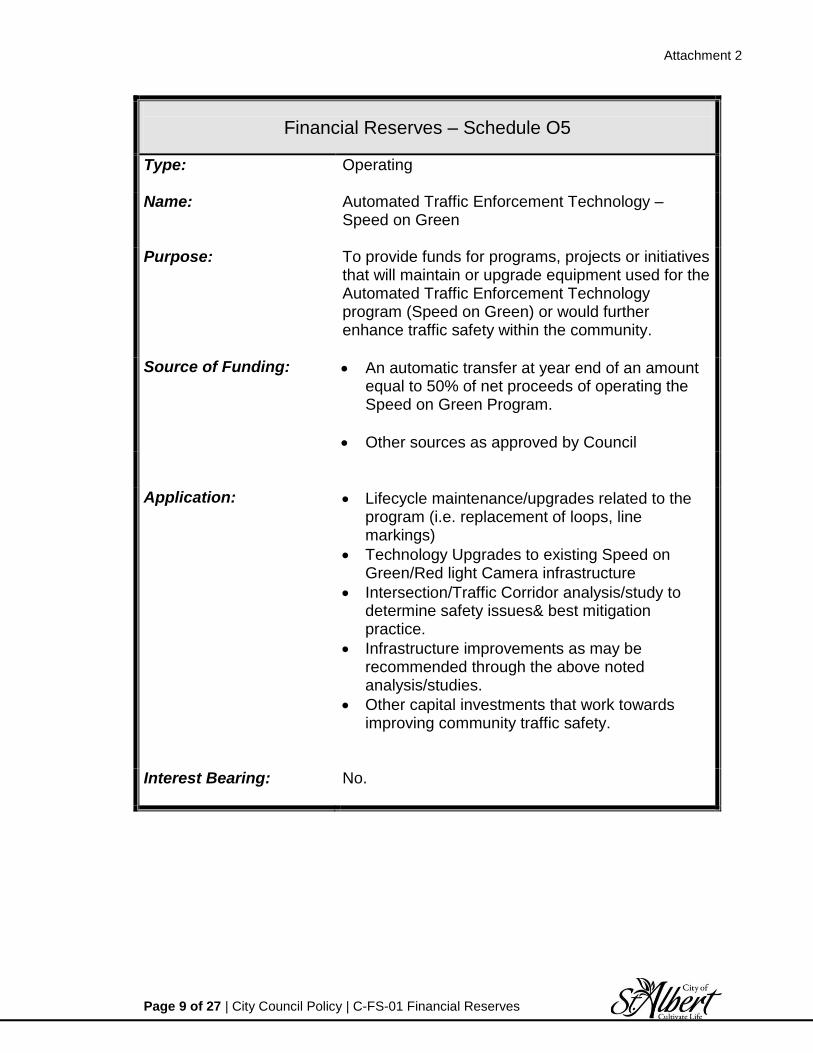

Financial Reserves – Schedule O5

Type:

Operating

Name:

Automated Traffic Enforcement Technology – Speed on Green

Purpose:

To provide funds for programs, projects or initiatives that will maintain or upgrade equipment used for the Automated Traffic Enforcement Technology program (Speed on Green) or would further enhance traffic safety within the community.

Source of Funding:

An automatic transfer at year end of an amount equal to 50% of net proceeds of operating the Speed on Green Program.

Other sources as approved by Council

Application:

Lifecycle maintenance/upgrades related to the program (i.e. replacement of loops, line markings)

Technology Upgrades to existing Speed on Green/Red light Camera infrastructure

Intersection/Traffic Corridor analysis/study to determine safety issues& best mitigation practice.

Infrastructure improvements as may be recommended through the above noted analysis/studies.

Other capital investments that work towards improving community traffic safety.

Interest Bearing:

No.

Attachment 2

Page 10 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O6

Type:

Operating

Name:

LRT/BRT Reserve

Purpose:

To provide funds for an LRT/BRT into St. Albert.

Source of Funding:

Annual transfer or other sources as approved by Council.

Application:

Funds from this reserve will be used to accommodate initiatives to bring an LRT/BRT into St. Albert.

Interest Bearing:

No.

Attachment 2

Page 11 of 27 | City Council Policy | C-FS-01 Financial Reserves

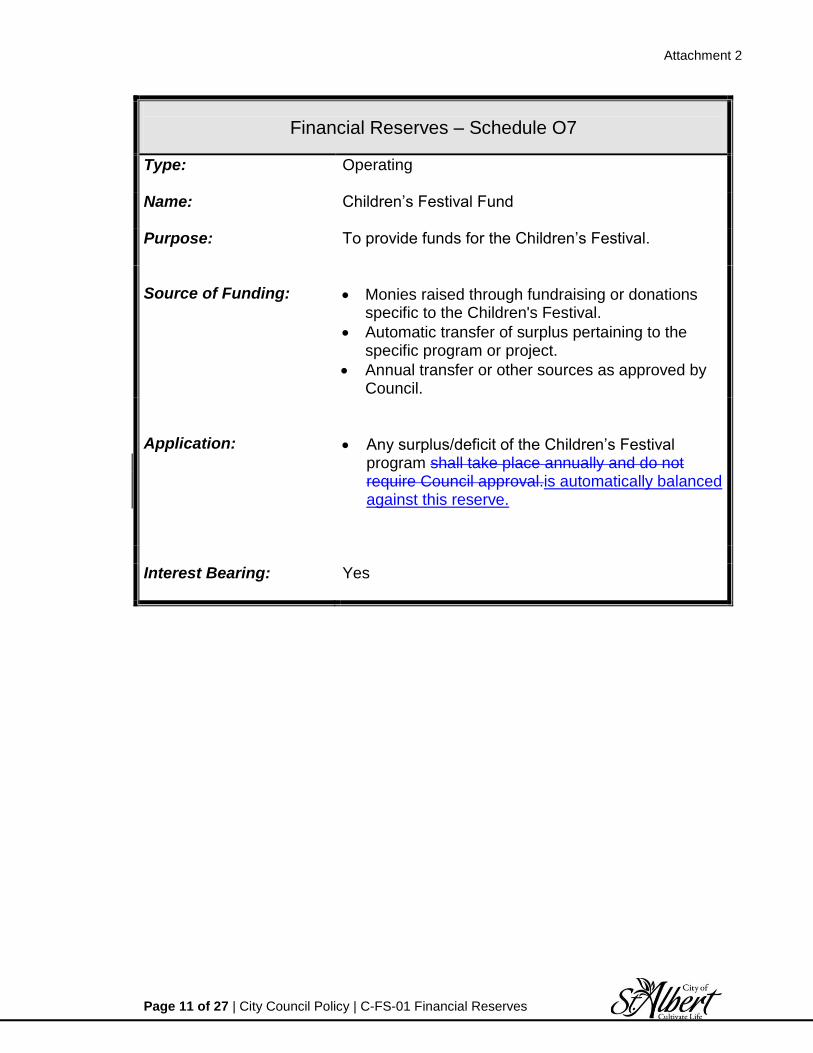

Financial Reserves – Schedule O7

Type:

Operating

Name:

Children’s Festival Fund

Purpose:

To provide funds for the Children’s Festival.

Source of Funding:

Monies raised through fundraising or donations specific to the Children's Festival.

Automatic transfer of surplus pertaining to the specific program or project.

Annual transfer or other sources as approved by Council.

Application:

Any surplus/deficit of the Children’s Festival program shall take place annually and do not require Council approval.is automatically balanced against this reserve.

Interest Bearing:

Yes

Attachment 2

Page 12 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O8

Type:

Operating Reserve

Name:

RCMP Contract Expense Reserve

Purpose:

To fund the RCMP contract costs related to the number of RCMP Members assigned to the St. Albert Detachment that are greater than the approved annual budget.

Source of Funding:

Reserve funding contribution will be derived from any surplus from the Policing Operating Budget related to the RCMP contract through an automatic transfer at year end.

Annual transfer or other sources as approved by Council.

Ceiling:

The upper limit of this reserve will not exceed the equivalent of the current estimated budgeted contract cost of six (6) full time RCMP Members.

Application:

To cover operating shortfalls due to a higher than anticipated number of RCMP members being assigned to the St. Albert Detachment. The City Manager is authorized to draw upon this reserve in accordance with the above noted application.

Interest Bearing:

No.

Attachment 2

Page 13 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O9

Type:

Operating Reserve

Name:

Safety Enhancement Reserve

Purpose:

To ensure monies received from the Workers Compensation Board (WCB) premium rebates and surplus distribution dividend remain available to further enhance the employee health and safety program and protect against increases in premiums. Safety enhancement reserve dollars, for as long as they are available, are first used as a source of funding for justified safety projects/initiatives, and secondly as a mechanism to provide a recovery/offset against the base budget on a 10% declining balance basis.

Source of Funding:

Annual WCB premium rebates received through participation in the Partners in Injury Reduction (PIR) program

Periodic WCB premium surplus distribution dividends

Unspent portion of any closed operating business cases funded from the reserve.

Application:

Funds from this reserve will be used for safety programs as recommended through the City’s Safety Enhancement Program as outlined in the administrative policy.

Administration shall coordinate individual requests of values less than or equal to $15,000 each to be brought forward through an agenda report once or twice a year for Council decision.

Individual requests valued over $15,000 shall be brought forward through the budget process.

The annual withdrawal related to safety projects/initiatives is capped at $150,000.

10% of the current year’s second quarter uncommitted balance will be incorporated into the upcoming budget, up the base safety budget, as approved by Council.

Interest Bearing:

No

Attachment 2

Page 14 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule O10

Type:

Operating Reserve

Name:

Election and Census Reserve

Purpose:

To build funds for future elections and census to minimize annual impact on tax.

Funds: 1. Election 2. Census

Source of Funding:

Annual budgeted transfers as approved by Council, which are based on a target amount to administer a single municipal and school board election.

Any operating surplus balance remaining after an election or census will be transferred back to this Reserve automatically.

Annual transfers or other sources as approved by Council.

Application:

Election

Applied against municipal election expenditures, which occur every four years so that no tax impact occurs.

Census

Applied against municipal census expenditures, which occur every two years so that no tax impact occurs.

Interest Bearing:

No.

Attachment 2

Page 15 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule C1 Type:

Capital Reserve

Name:

Internal Financing

Purpose:

To provide funds for internal financing of general municipal capital projects, thereby improving the City’s overall net financial position.

Source of Funding:

Transfers equal to repayment of principal for approved projects with interest equivalent to the average rate of return earned by the City’s investments. This interest rate is intended to offset the investment interest not earned or lost by the City on funds utilized to interim finance capital projects. This interest rate will ensure the City is not profiting from internal borrowing.

Annual transfer or other sources as approved by Council.

Application:

Used to internally finance or fund capital projects as approved by Council.

Interest Bearing:

Yes

Attachment 2

Page 16 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule C2

Type:

Capital Reserve

Name:

Major Recreational Lands & Facilities

Purpose:

To provide funds for the purchase of and or development of recreational lands and facilities. Recreational facilities may include both replacement and new. (For developers contributions the facilities must be new or major enhancements).

Funds: 1. Major Recreational Facilities – City Wide Fund 2. Major Recreation Facilities – Neighbourhood Fund 3. Parkland Fund 4. Dog License Fund

Source of Funding:

City Wide and “Neighborhood

Contributions received on a per residential unit basis as agreed to by Council and developers under Capital Recreation Contribution agreements.

Parkland Fund

Surplus proceeds from the sale of reserve lands

Payment in lieu of reserve land dedication to meet the cost of acquiring and developing public use lands as prescribed in the Municipal Government Act.

Annual transfers or other sources as approved by Council.

Dog License Fund

Received through a surcharge as part of the annual dog license fee as approved by Council

Application:

To fund capital acquisition, development, or major enhancement, of public use lands, recreational and cultural facilities and parks as approved by Council. Dog License Funds are used specifically for dog parks, associated amenities and life cycle maintenance/upgrade of these items.

Attachment 2

Page 17 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule C3 Type:

Capital Reserve

Name:

Offsite Levy Recoveries

Purpose: Funds:

To fund future development of specified roadway and utility construction.

1. 1. General Transportation Fund * 2. Offsite Levy Reimbursed Funds

Source of Funding:

One time contributions (ie. Permanent Area Charge (PAC)) from developers for specific road development.

Annual transfers or other sources as approved by Council.

Reimbursed funds collected from the City front ending projects

Application:

General Transportation Fund

OLD PAC: Bellerose, SWCA, Giroux/Hogan

West PAC: Bellerose (Erin Ridge Dr to Coal Mine Road), Campbell

East PAC: LeClair Rd, Giroux (Extension to Ray Gibbon), McKenney Ave, Hogan Rd, Ray Gibbon

Offsite levy reimbursed funds

To front end capital initiatives as determined by the offsite levy model.

To fund City capital projects as approved by Council.

Interest Bearing:

Yes, General Transportation fund only

Attachment 2

Page 18 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule C4 Type:

Capital Reserve

Name:

Lifecycle

Purpose:

To provide the necessary funds for the scheduled repair, maintenance, and replacement of existing tangible capital assets. This reserve will permit the City to remain current with required facilities, equipment and services. Proper maintenance and or asset replacement are required to sustain the assets in a condition necessary to provide expected service levels. Deferring maintenance could result in increasing repair costs and decreasing service potential as the condition of the asset deteriorates.

Funds: 1.3. Mobile Vehicle and Equipment 2.4. Emergency Services Equipment 3.5. Office Systems 4.6. Arden Theatre 5.7. Servus Credit Union 6.8. Aquatics Facility 7.9. Public Art 8.10. Fire Buildings 9.11. City Playground 10.12. Public Transit 11.13. Infrastructure *

Source of Funding:

Annual transfers or other sources as approved by Council

Donations, corporate investment, and unconditional and matching grants as approved by Council.

Application:

The execution and use of the lifecycle reserves are annually reviewed, detailed and scheduled by the respective department. Items are outlined specifically for the required replacement, potential change in useful life and any other updates.

Meticulous planning is in place and utilization of the lifecycle capital reserve funds is maximized.

The Vehicle and Mobile Equipment Reserve is

Attachment 2

Page 19 of 27 | City Council Policy | C-FS-01 Financial Reserves

subject to the conditions of Administrative Policy A-P&E-04 Mobile Vehicle and Equipment Replacement.

Interest Bearing:

Yes, with the exception of Infrastructure

Attachment 2

Page 20 of 27 | City Council Policy | C-FS-01 Financial Reserves

Reserve Policy – Schedule C5 Type:

Capital Reserve

Name:

Municipal Land & Facilities Reserve

Purpose:

To provide funds for:

Sustainable ongoing development of commercial and industrial lands; and

Purchase or refurbish City facilities other than for recreation purposes; and

Purchase of land for municipal purposes other than for recreation purposes

Source of Funding:

May allocate non-residential property tax revenues generated from within the newly developed lands.

Sale of properties and City facilities other than recreation facilities

Net proceeds on the disposition of road right of ways

Annual transfer or other sources as approved by Council.

Application:

To provide funds to purchase land, municipal purposes and service non-residential development

To purchase or refurbish City facilities other than for recreation purposes

Interest Bearing:

Yes

Attachment 2

Page 21 of 27 | City Council Policy | C-FS-01 Financial Reserves

Reserve Policy – Schedule C6 Type:

Capital Reserve

Name:

Capital Fund

Purpose:

To provide funds for capital requirements relating to Council priorities, rehabilitation and maintenance of existing infrastructure, purchase of new capital assets, and capital projects that would not be eligible for grant funding.

Source of Funding

An annual transfer, Pay-As-You Go (PAYG) as determined by Council.

Unspent portion of PAYG funding pertaining to closed projects as approved by Council.

Other sources as approved by Council.

Application:

To fund capital projects that have been identified as part of the annual capital budget process and approved by Council.

Interest Bearing:

No.

Attachment 2

Page 22 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule C7

Type:

Capital Reserve

Name:

Growth Stabilization

Purpose:

To provide funds for capital expenditures that are directly related to growth.

Source of Funding:

An annual transfer of 70% of new growth assessment revenue in excess of business cases (residual balance) approved by Council. Transfer of funds into the reserve in a given year must be approved by Council prior to passing the annual Tax Rate Bylaw

Ceiling:

None

Application:

Funds from the reserve may be used to support capital costs which has a demonstrated link to the costs of growth.

Interest Bearing:

No

Attachment 2

Page 23 of 27 | City Council Policy | C-FS-01 Financial Reserves

Financial Reserves – Schedule UC1 Type:

Utility Capital Reserve

Name:

Utilities Fund

Purpose:

To provide funds for the expansion, refurbishment or replacement of the City’s utility infrastructure, equipment, or to fund studies required for future planning purposes.

Funds: 1. Water 2. Wastewater 3. Solid Waste Management 4. Storm water

Source of Funding:

Transfers to/from the Utility Operating Budgets as approved by Council as part of the annual budget process.

Annual transfer or other sources as approved by Council.

Application:

To fund utility capital projects that have been identified as part of the annual capital budget process and approved by Council.

Interest Bearing:

Yes

Attachment 2

Page 24 of 27 | City Council Policy | C-FS-01 Financial Reserves

Reserve Policy – Schedule OA1 Type:

Operating Reserve

Name:

Outside Agency Operating

Purpose: To establish a fund for outside agencies to administer their respective operating programs.

Fund: Outside Agency Program Funds 1. Library - Young Peoples Writing 2. Museum Artifacts 3. Museum Historic Sites 4. Museum Exhibition 5. Library - Edmond and Anna Harder

Endowment Reserve fund

Source of Funding: Annual transfer or other sources as approved by Council

Application:

Used to fund outside agency operating programs as approved by their respective board and Council

Interest Bearing:

YesNo

Attachment 2

Page 25 of 27 | City Council Policy | C-FS-01 Financial Reserves

Reserve Policy – Schedule OA2 Type:

Capital Reserve

Name:

Outside Agency Capital

Purpose:

To establish a fund for outside agencies to administer their respective capital initiatives.

Funds: 1. Library Book collection 2. Library Facilities 3. NABI Building Fund * 3.4. Library Computer Replacement

Source of Funding:

Donations, fundraising revenue, unconditional grants

Annual transfer or other sources as approved by Council

Application:

Library Book Collection Collection,and Facilities and Computer Replacement. To fund the acquisition of books and audiovisual materialcollections, furnishings, fixtures and equipment for a new Library Branch and other capital projects as approved by the Board and Council. NABI Building Fund To establish a building fund for future development.

Interest Bearing:

Yes, * with the exception of NABI Building Fund

Attachment 2

Page 26 of 27 | City Council Policy | C-FS-01 Financial Reserves

Cross References

1. C-FS-05 Budget and Taxation Guiding Principles 2. C-CS-01 St. Albert Games Legacy Awards Program 3. C-CS-11 Community Significant Events Stimulus Fund 4. C-FS-11 Operating and Capital Carry Forwards 5. C-FS-12 Outside Agency Budget Guiding Principles 6. C-FS-14 Utility Fiscal Policy

REVIEW REVISION

Date – DepartmentJune 2017 – Financial Services C181-2003 03 17 C400-2004 08 16 C187-2005 05 02 C355-2006 07 04 C211-2007 04 16 C291-2007 05 22 C557-2008 09 22Date – Resolution No.

C571-2008 10 06 C401-2009 06 29 C506-2009 09 08

Attachment 2

Page 27 of 27 | City Council Policy | C-FS-01 Financial Reserves

C561-2010 09 27 C443-2011 07 04 C246-2012 06 25 C231-2013 05 27 C293-2013 06 24 C453-2014 09 22 C428-2015 09 14

REVIEW DATES

Attachment 3

Page 1 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

CITY OF ST. ALBERT

CITY COUNCIL POLICY

NUMBER TITLE

C-FS-05 Budget and Taxation Guiding Principles

ORIGINAL APPROVAL DATE DATE LAST REVISED

September 2, 2003 December 3, 2015

Purpose To establish principles for the preparation of budgets and property taxation levies in accordance with the Municipal Government Act. In some cases these principles will stand alone, while in others the principles are excerpts from separate policies established by Council. Policy Statement

1. As a component of the Strategic Framework, the corporate budget is the financial representation of the strategic plan which articulates Council’s long term outcomes, goals and strategies in support of the community vision.

2. The adoption of the City's budgets and tax/utility rate bylaws are among the

most critical functions undertaken by Council.

3. Budgets shall be developed in a consistent and planned manner and take into consideration the impacts on future years and the City's ability to fund those impacts.

4. Municipal and Utility operating budgets/forecasts shall be prepared for

Council for a rolling three (3) year period for information. Council will debate and approve year 1 of the plan.

5. Municipal and Utility capital budgets shall be prepared and approved by Council for a rolling ten (10) year period and Administration shall be given approval to execute on year one (1) of the plan.

6. The City shall maintain a fair, transparent, and competitive system in

determination of: a. Municipal property taxation, b. Utility rates,

Attachment 3

Page 2 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

while collecting the necessary revenue to meet municipal and utility program and service obligations.

7. The approved operating and capital budgets shall serve as the financial plan for the City and provide Administration with the direction and resources necessary to accomplish Council’s strategic goals, objectives and established service levels.

8. The Corporation uses a set of guidelines, principles and policies to develop

the annual budget and determine the required municipal tax and utility rates. Council approves these rates through the property tax and utility by-laws.

9. The City is committed to the preservation and long term viability of its current infrastructure and as such commits available capital dollars towards the repair, maintenance and replacement of existing assets prior to consideration of new capital growth projects and assets.

10. The City shall in principle, endeavor to decrease the reliance on residential property taxes, by enabling annual taxable assessment growth to effect change to the municipal property tax split. In addition, the City shall in principle, endeavor to strive towards a tax split goal which is comparable to other Alberta mid-sized cities. The long-term goal being defined as a 20%/80% assessment split and a 35%/65% property tax split for non-residential and residential properties respectively.

11. This policy shall be reviewed annually by Administration. Any changes shall

be recommended to Council for approval. Service Standards/ Expectations Budget Guiding Principles

1. Multi-Year Planning

The City utilizes a multi-year planning method to enhance and improve the budget process that reinforces the commitment to long-term fiscal strategies. Although the budget is approved for one year, this multi-year view communicates the short and long term plans to residents and other stakeholders.

2. Base Budget

The operating budget shall be developed based on the principle to sustain current programs and level of services. As such, the previous year is used as the starting point with various factors including inflation and other corporate adjustments.

Attachment 3

Page 3 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

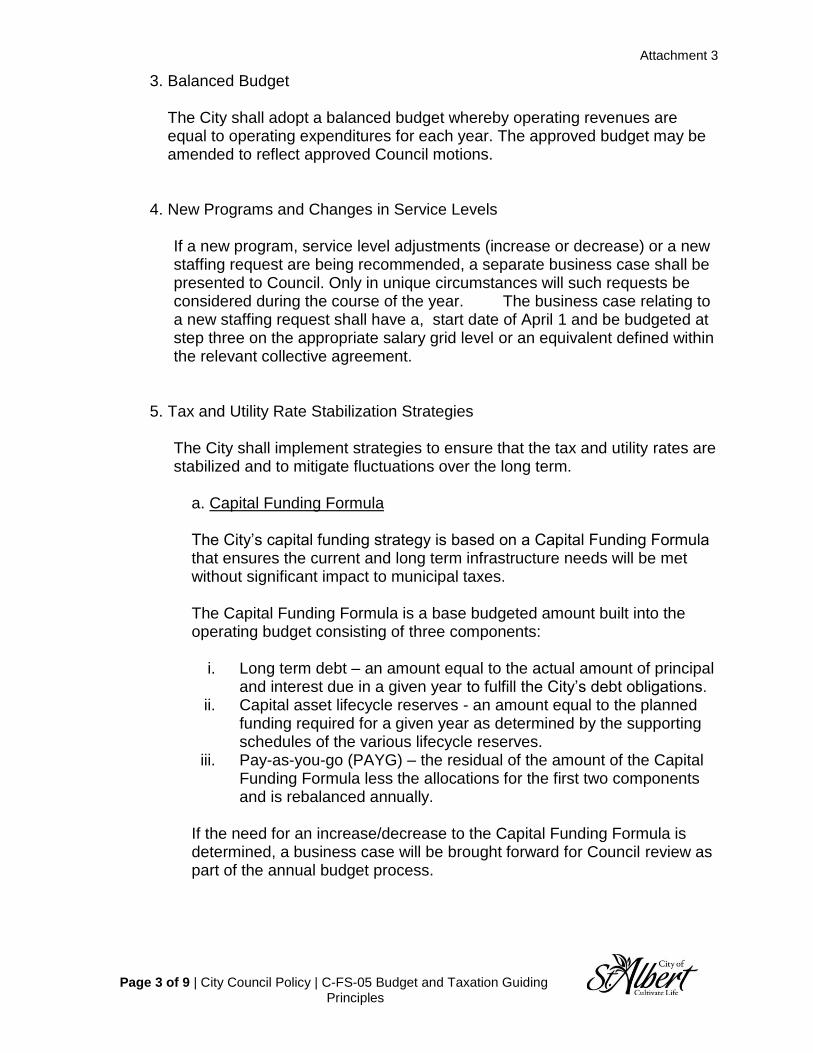

3. Balanced Budget

The City shall adopt a balanced budget whereby operating revenues are equal to operating expenditures for each year. The approved budget may be amended to reflect approved Council motions.

4. New Programs and Changes in Service Levels

If a new program, service level adjustments (increase or decrease) or a new staffing request are being recommended, a separate business case shall be presented to Council. Only in unique circumstances will such requests be considered during the course of the year. The business case relating to a new staffing request shall have a, start date of April 1 and be budgeted at step three on the appropriate salary grid level or an equivalent defined within the relevant collective agreement.

5. Tax and Utility Rate Stabilization Strategies The City shall implement strategies to ensure that the tax and utility rates are stabilized and to mitigate fluctuations over the long term.

a. Capital Funding Formula The City’s capital funding strategy is based on a Capital Funding Formula that ensures the current and long term infrastructure needs will be met without significant impact to municipal taxes.

The Capital Funding Formula is a base budgeted amount built into the operating budget consisting of three components:

i. Long term debt – an amount equal to the actual amount of principal

and interest due in a given year to fulfill the City’s debt obligations. ii. Capital asset lifecycle reserves - an amount equal to the planned

funding required for a given year as determined by the supporting schedules of the various lifecycle reserves.

iii. Pay-as-you-go (PAYG) – the residual of the amount of the Capital Funding Formula less the allocations for the first two components and is rebalanced annually.

If the need for an increase/decrease to the Capital Funding Formula is determined, a business case will be brought forward for Council review as part of the annual budget process.

Attachment 3

Page 4 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

b. New Assessment Growth

i. New assessment growth is defined as the anticipated future

property tax revenue for new residential/non residential building construction forecasted for the following budget year.

ii. The City shall apply new assessment growth revenue through a

balanced approach of 70% growth revenue to fund new initiatives (business cases and/or capital charters) and 30% to offset the base budget property tax requisition.

iii. Any portion of the 70% of growth revenue not applied to business

cases or capital charters during the budget process shall be transferred to the Growth Stabilization Reserve.

c. Reserves

i. Reserves and reserve funds are established as required and maintained in

accordance with their respective policy as determined by Council. Use of

reserves is planned and is not considered as an alternate-funding source in

place of good financial practice.

ii. The Budget will allocate an appropriate level of funds to Reserves in order

to maintain services throughout economic cycles, mitigate unexpected

events/expenditures and to stabilize tax and utility rates during periods of

growth.

6. Utility Budget

The utility budget shall be funded by user rates and achieve financial independence and sustainability in accordance with the Utility Fiscal Policy.

7. Public Engagement

Council shall engage the public through the budget process in accordance with established policies and procedures with support from the City.

8. Revenues

a. Revenue Estimates

Operating revenue projections shall be based on actual historic trends, supplemented with additional knowledge of future expectations.

Attachment 3

Page 5 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

b. Revenue Diversification

i. The City shall charge fees for services where applicable and cost effective to do so.

ii. The City shall charge fines as permitted through policy, by-law or

other legislation.

iii. The City shall strive to maximize cost recovery where it is applicable and cost effective to do so. Consideration will be given to regional competitiveness and user affordability.

iv. The City shall continuously seek new and diverse revenues so as

to limit the dependence on one or only a few sources and in order to maintain approved service levels.

c. One Time Revenues, Surpluses and Unpredictable Revenue

One time revenues and surpluses and unpredictable revenue shall not be relied upon to fund ongoing expenditures, unless otherwise noted in the Financial reserve policy/schedules. This could result in annual expenditure obligations that may not have adequate funds available for future years.

In the event of an operating surplus/deficit, funds will applied to/from:

a. Reserves, municipal and/or utility, for use in maintaining reserve levels set by Council policy; or

b. one-time expenditures; or c. repayment of outstanding debt.

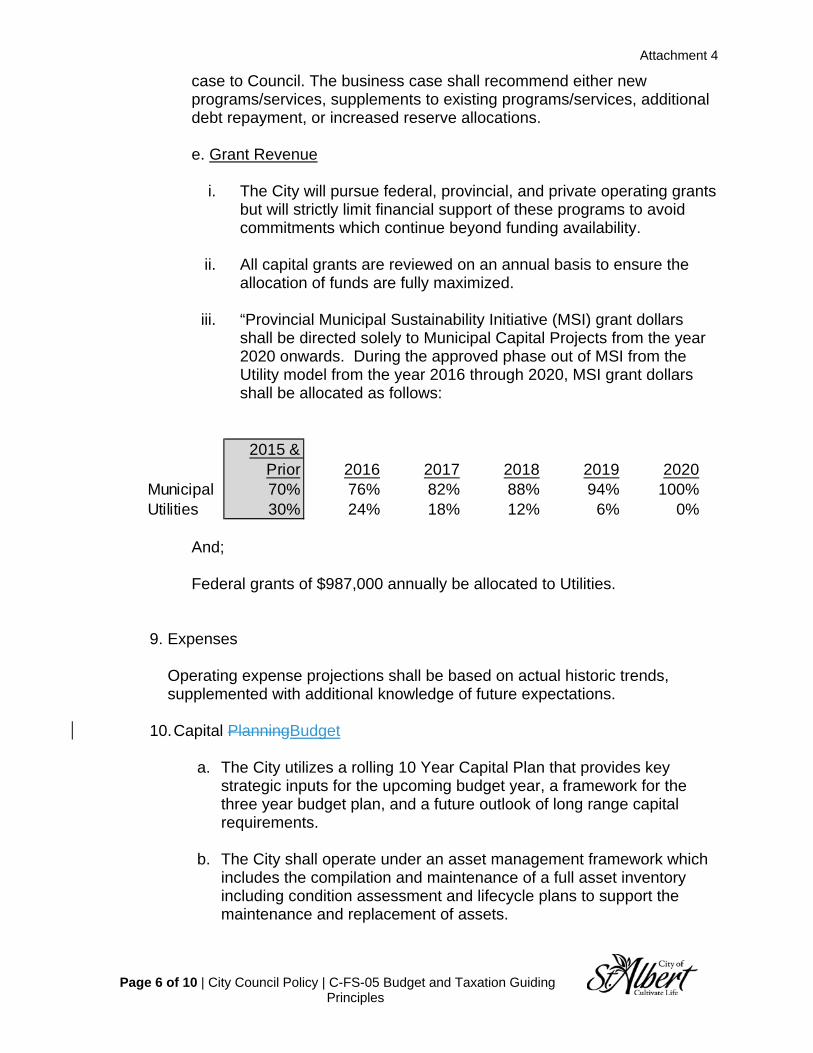

d. Unconditional New Operating Revenues

When the City creates or receives a stable, lasting and unconditional revenue source, the City Manager shall present an operating business case to Council. The business case shall recommend either new programs/services, supplements to existing programs/services, additional debt repayment, or increased reserve allocations.

e. Grant Revenue

Attachment 3

Page 6 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

i. The City will pursue federal, provincial, and private operating grants but will strictly limit financial support of these programs to avoid commitments which continue beyond funding availability.

ii. All capital grants are reviewed on an annual basis to ensure the

allocation of funds are fully maximized.

iii. “Provincial Municipal Sustainability Initiative (MSI) grant dollars shall be directed solely to Municipal Capital Projects from the year 2020 onwards. During the approved phase out of MSI from the Utility model from the year 2016 through 2020, MSI grant dollars shall be allocated as follows:

And; Federal grants of $987,000 annually be allocated to Utilities.

9. Expenses

Operating expense projections shall be based on actual historic trends, supplemented with additional knowledge of future expectations.

10. Capital Budget

a. The City utilizes a rolling 10 Year Capital Plan that provides key

strategic inputs for the upcoming budget year, a framework for the three year budget plan, and a future outlook of long range capital requirements.

b. The City shall operate under an asset management framework which

includes the compilation and maintenance of a full asset inventory including condition assessment and lifecycle plans to support the maintenance and replacement of assets.

c. The City shall utilize a facility predictive model to guide growth capital

strategies.

d. The City utilizes two categories to define its infrastructure needs:

2015 &

Prior 2016 2017 2018 2019 2020

Municipal 70% 76% 82% 88% 94% 100%

Utilities 30% 24% 18% 12% 6% 0%

Attachment 3

Page 7 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

i. Repair, Maintain, Replace (RMR) - Capital initiatives that relate to maintaining current service levels that are required by lifecycle plans and are considered a replacement or rehabilitation of existing infrastructure, facilities, and equipment.

ii. Growth - Capital initiatives that are required to meet future

demand relating to facilities, equipment, technology, and infrastructure for the development of cultivating and strengthening the community.

e. The City has several sources of financing available to be used toward

Capital Infrastructure. The funding allocations are comprised of various Provincial and Federal Grants, City Reserves, and the predetermined amount of Pay as You Go (PAYG) funds established through the Capital Funding Formula.

f. Council shall review and approve the RMR Capital Budget

approximately six months prior to the next fiscal year so that preparatory work and applications can be completed and be made available at the beginning of the next approved budget year. Expenditures relating to these RMR projects will not be incurred until final approval of the corporate business plan and budget. Complete project charters supporting the 10 year RMR capital plan will be provided to Council as part of the review process.

g. Capital projects relating to Growth will be reviewed during Council’s

deliberation of the subsequent budget year. Complete project charters supporting the 10 year Growth capital plan will be provided to Council as part of the review process.

11. Budget Amendments Additional Expenditures and or Revenues

As per the MGA (section 248.2), council authorization is required for expenditures and/or revenues that are not included in the approved budget. This includes any new services, programs or projects undertaken.

Taxation Guiding Principles

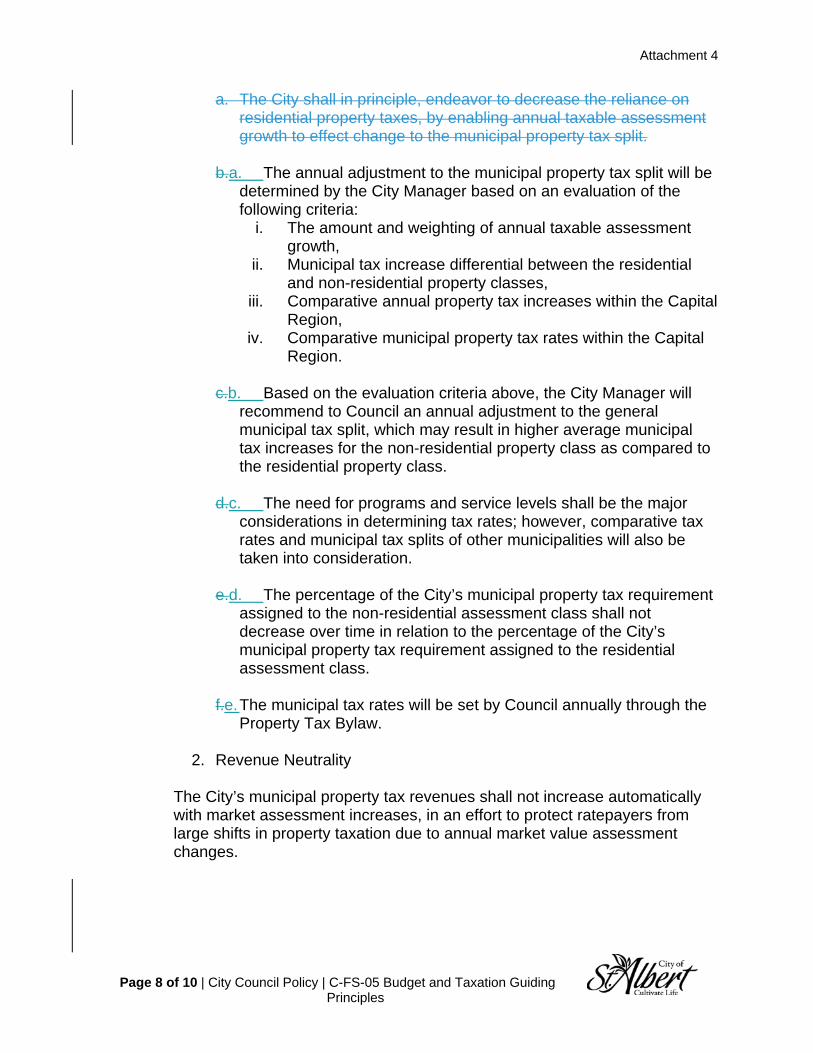

1. Municipal Property Tax Split

a. The annual adjustment to the municipal property tax split will be

determined by the City Manager based on an evaluation of the following criteria:

Attachment 3

Page 8 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

i. The amount and weighting of annual taxable assessment growth,

ii. Municipal tax increase differential between the residential and non-residential property classes,

iii. Comparative annual property tax increases within the Capital Region,

iv. Comparative municipal property tax rates within the Capital Region.

b. Based on the evaluation criteria above, the City Manager will

recommend to Council an annual adjustment to the general municipal tax split, which may result in higher average municipal tax increases for the non-residential property class as compared to the residential property class.

c. The need for programs and service levels shall be the major

considerations in determining tax rates; however, comparative tax rates and municipal tax splits of other municipalities will also be taken into consideration.

d. The percentage of the City’s municipal property tax requirement

assigned to the non-residential assessment class shall not decrease over time in relation to the percentage of the City’s municipal property tax requirement assigned to the residential assessment class.

e. The municipal tax rates will be set by Council annually through the

Property Tax Bylaw. 2. Revenue Neutrality

The City’s municipal property tax revenues shall not increase automatically with market assessment increases, in an effort to protect ratepayers from large shifts in property taxation due to annual market value assessment changes.

Attachment 3

Page 9 of 9 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

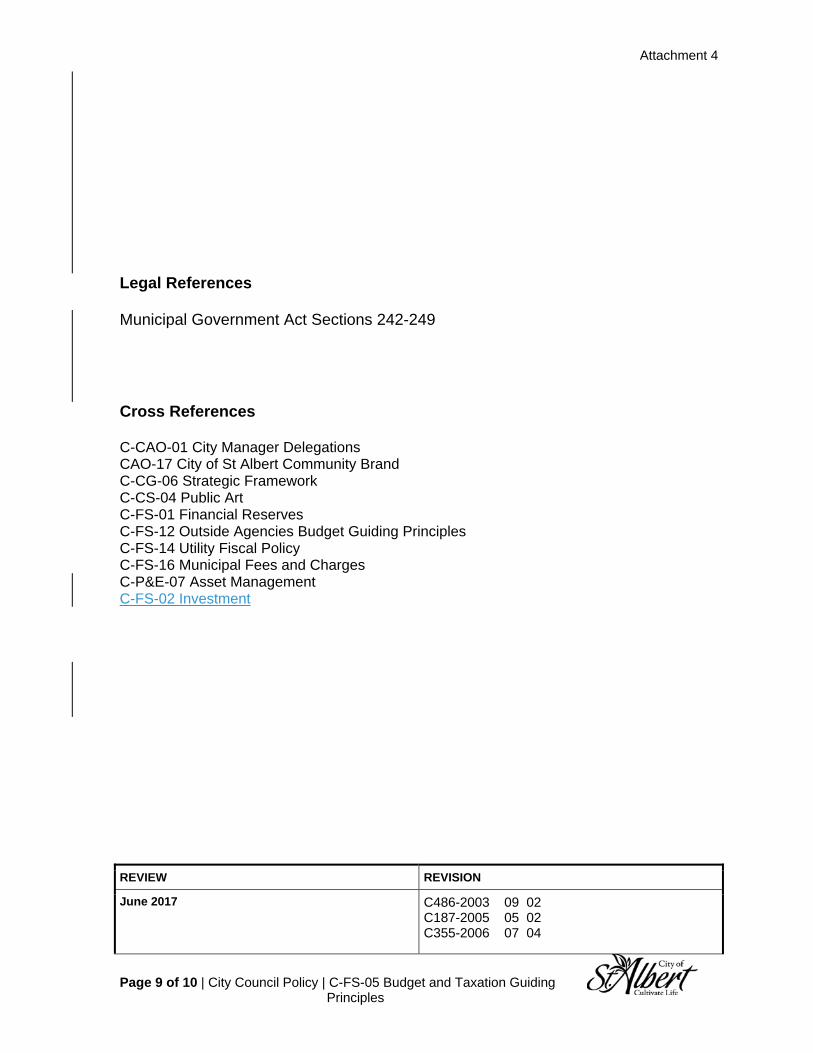

Legal References Municipal Government Act Sections 242-249 Cross References C-CAO-01 City Manager Delegations CAO-17 City of St Albert Community Brand C-CG-06 Strategic Framework C-CS-04 Public Art C-FS-01 Financial Reserves C-FS-12 Outside Agencies Budget Guiding Principles C-FS-14 Utility Fiscal Policy C-FS-16 Municipal Fees and Charges C-P&E-07 Asset Management C-FS-02 Investment

REVIEW REVISION

June 2017 C486-2003 09 02 C187-2005 05 02 C355-2006 07 04 C25-2009 01 19 C98-2010 02 16 C161-2011 03 07 C220-2012 04 16 C151-2013 04 22 C110-2014 03 03 C453-2014 09 22 C544-2014 12 01 C598-2015 12 03

REVIEW DATES

Attachment 4

Page 1 of 10 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

CITY OF ST. ALBERT

CITY COUNCIL POLICY NUMBER TITLE

C-FS-05 Budget and Taxation Guiding Principles

ORIGINAL APPROVAL DATE DATE LAST REVISED

September 2, 2003 December 3, 2015

Purpose To establish principles for the preparation of budgets and property taxation levies in accordance with the Municipal Government Act. In some cases these principles will stand alone, while in others the principles are excerpts from separate policies established by Council. Policy Statement

1. As a component of the Strategic Framework, the corporate budget is the financial representation of the strategic plan which articulates Council’s long term outcomes, goals and strategies in support of the community vision.

2. The adoption of the City's budgets and tax/utility rate bylaws are among the

most critical functions undertaken by Council.

3. Budgets shall be developed in a consistent and planned manner and take into consideration the impacts on future years and the City's ability to fund those impacts.

4. Municipal and Utility operating budgets/forecasts shall be prepared for

Council for a rolling three (3) year period for information. Council will debate and approve year 1 of the plan.

5. Municipal and Utility capital budgets shall be prepared and approved by Council for a rolling ten (10) year period and Administration shall be given approval to execute on year one (1) of the plan.

6. The City shall maintain a fair, transparent, and competitive system in

determination of: a. Municipal property taxation, b. Utility rates,

Attachment 4

Page 2 of 10 | City Council Policy | C-FS-05 Budget and Taxation Guiding Principles

while collecting the necessary revenue to meet municipal and utility program and service obligations.

7. The approved operating and capital budgets shall serve as the financial plan for the City and provide Administration with the direction and resources necessary to accomplish Council’s strategic goals, objectives and established service levels.

8. The Corporation uses a set of guidelines, principles and policies to develop

the annual budget and determine the required municipal tax and utility rates. Council approves these rates through the property tax and utility by-laws.

9. The City is committed to the preservation and long term viability of its current infrastructure and as such commits available capital dollars towards the repair, maintenance and replacement of existing assets prior to consideration of new capital growth projects and assets.

10. The City shall in principle, endeavor to decrease the reliance on residential property taxes, by enabling annual taxable assessment growth to effect change to the municipal property tax split. In addition, the City shall in principle, endeavor to strive towards a tax split goal which is comparable to other Alberta mid-sized cities. The long-term goal being defined as a 20%/80% assessment split and a 35%/65% property tax split for non-residential and residential properties respectively. .

8.11. This policy shall be reviewed annually by Administration. Any changes shall be recommended to Council for approval.

Service Standards/ Expectations Budget Guiding Principles

1. Multi-Year Planning

The City utilizes a multi-year planning method to enhance and improve the budget process that reinforces the commitment to long-term fiscal strategies. Although the budget is approved for one year, this multi-year view communicates the short and long term plans to residents and other stakeholders.

2. Base Budget