Embed Size (px)

DESCRIPTION

Â

Citation preview

www.staplesrodway.co.nz

A STAPLES RODWAY PUBLICATIONNo 25 SUMMER 2012

www.staplesrodway.co.nzStaples Rodway is an independent member of Baker Tilly International

No 25 SUMMER 2012

DISCLAIMER No liability is assumed by Staples Rodway for any losses suffered by any person relying directly or indirectly upon any article within this document. It is recommended that you consult your advisor before acting on this information.

DIRECTORSAUCKLAND Roger Thompson (09) 309 0463

HAMILTON Rosanna Baird (07) 834 6800

TAURANGA Chris Downey (07) 578 2989

HAWKES BAY Stuart Signal (06) 878 7004

TARANAKI Chris Lynch (06) 757 3155

CHRISTCHURCH Ross Erskine (03) 343 0599

As we head towards the Christmas season and the summer break it’s worth reflecting on what has been another challenging year for you, our clients, as well as for Staples Rodway and our staff.

The fallout from the global financial crisis is ongoing, with many commentators predicting 5-7 year time frames before the world’s economies finally shake off recession. The Christchurch rebuild has yet to really kick-in and give the New Zealand economy the boost many have been expecting, confirmed by the recently announced retail and employment data.

Against that background it is good to be able to report on a few positives at Staples Rodway.

In the past year we’ve invested in new offices in Tauranga and Hamilton making better work environments for our people and our clients. Additionally, we’ve also completed a refresh of our website to make that more functional for both clients and staff.

The business environment continues to be turbulent. Against this we’re putting a renewed effort into both existing and new clients with an expanded range of services in this changing market (a couple of stories in this magazine highlight those efforts).

I thank our long-term clients for their continued support and welcome our new clients to the fold.

The team at Staples Rodway wish you all a Merry Christmas with your family and friends and a great break over the summer. Let’s take the time to recharge and refresh for a more successful and brighter 2013.

Merry Christmas and a Happy New Year.

Peter Guise CHAIRMAN, STAPLES RODWAY NEW ZEALAND

A MESSAGE FROM PETER GUISE

IN THIS ISSUE4 Hamilton & Tauranga get extreme makeovers

8 A balancing act

10 Succession planning in the dairy industry

12 Staples Rodway Cape Kidnappers Challenge

13 Sopers Ltd: Opening doors to a new way of working

14 Tax pooling

16 Electing into the FIF rules

16 Taranaki scaling new heights

18 The Fine Wine Delivery Company: The glass is half full

20 Directors’ duties under the spotlight

22 Walking with lions

24 The inbetween investor

25 The 7 year itch

26 Financial literacy in NZ

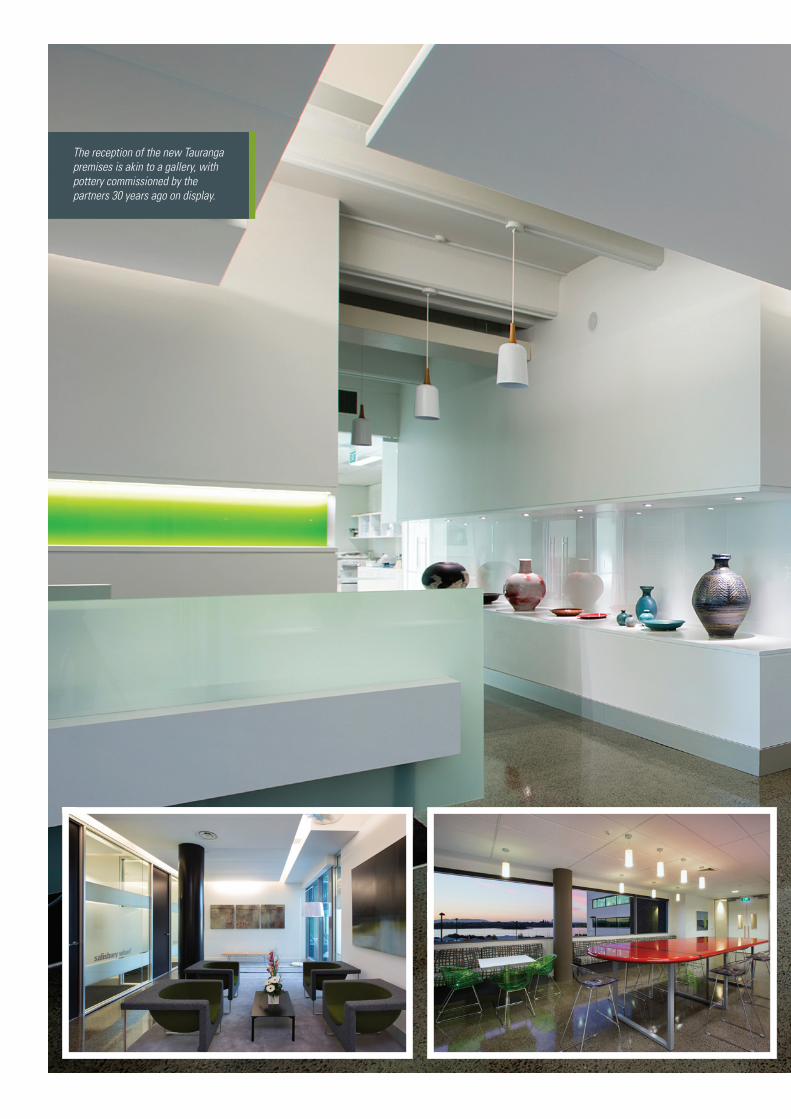

The colour scheme of the Hamilton office, inspired by the Staples Rodway logo, won a NZ Institute of Architects saward.

&GET EXTREME MAKEOVERS

T HE NEW 1000M2 PREMISES FOR the Staples Rodway Hamilton office has provided the previously separate local teams with a fresh and con-

temporary work environment and won awards for design company Chow:Hill. Chow:Hill’s design objective was to take a human-centric perspective

to the new fit-out and focus on creating an environment that was fresh and reflected the wider Waikato landscape. They also wanted to connect the busi-ness teams and support a range of working styles and individual needs.

In developing the concept for the new workplace, Chow:Hill Associate Jane Hill said, “we wanted to create an environment that encouraged different modes of working with spaces that fostered both individual and collaborative work.”

“Equal consideration was also given to the design and comfort of social and quiet breakout spaces. One of our key objectives was to maximise the easy flow between work-space, team-space and social-space, while allowing flexibility for business growth.”

The textures and colour palette were inspired by local context and environ-ment, and reflect both the new riverside location and the Waikato landscape.

Chow:Hill received a New Zealand Institute of Architects (NZIA) Award award. the NZIA Resene Colour Award, for the bold yet considered use of colour within the project – inspired by the Staples Rodway Logo.

Rosanna Baird, Managing Director of Staples Rodway Hamilton is happy with the final result. “Its great to have all the team together in the new space. It looks fantastic.”

HAMILTON TAURANGA

The Staples Rodway offices in Hamilton and Tauranga recently underwent transformations, creating stunning new work spaces.

The reception of the new Tauranga premises is akin to a gallery, with pottery commissioned by the partners 30 years ago on display.

T HE TAURANGA FIRM TURNED 65 this year, and has undergone a sig-nificant transformation, with the move to new premises within the

new ANZ Business Centre recently opened at 247 Cameron Road. We had been in our previous premises (just across the road) for some 29 years, and it was time for change.

With a move to new and modern premises, designed around what we stand for and the ideas we embrace, we have enhanced our ability to provide a productive and interactive client experience through staff development. Our architect was asked to design an environment that encompassed a stimulating working space for our staff, an environment that would enable us to offer our clients a better experience and a showcase of our rich 65 year history in The Bay. Although our firm has seen the introduction of younger partners over the past decade, it is important to us and our clients to remember we are a firm with a solid history of providing outstanding services.

The result is fantastic and we are proud of all that was achieved! Clients are greeted in our gallery-like reception with a display of stunning pottery, fea-turing items commissioned by the partners nearly 30 years ago. With names like “Fisherman’s Wharf”, “Base Track” and “Sou’East Bay” our meeting rooms, named after iconic parts of The Bay, boast new technology that allows us to work collaboratively with our clients.

We feel that staff development is essential to the delivery of high level services and solutions to our clients and there is no better way to achieve this than working alongside them. Because of this, our new premises have an open plan environment allowing staff and partners to work more closely. This new area is best described as modern and funky. Best of all, it oozes with natural light creating a far superior work environment for everybody! Our staff café encompasses a mix of the modern, funky feel of the new premises while featur-ing our iconic former boardroom table, a piece of art in itself. This allows us to embrace modern ideals while retaining some of our history that is so important to us here at Staples Rodway Tauranga.

The marketplace in the centre of our workspace has become an area that is well utilized. This encompasses a number of areas where staff can interact or work in different ways, rather than just sitting at their desks. It has also proven to be a good “gathering place” and our wax wars fundraising event for CanTeen was held here within weeks of the move!

Being part of the ANZ Business Centre is something we are proud of, and we could see the benefits of the move early on which is why we were one of the founding tenants. The building was recently officially opened by Tauranga MP Simon Bridges, who paid tribute to everyone involved, in particular investors Troop Investments, and developers CBC Construction.

As you can imagine, there is a lot of work behind the scenes for a move like this. Directors Mark Robinson and Brent Rogers were part of the building devel-opment team, and worked closely with the architect and developers to ensure we got the right outcome for us at the end of the day, and they can be proud of the results. There was also huge input from Director Chris Downey, and Glen Baveystock (our internal IT specialist) to ensure that the communications and computer network needs were met. It is a tribute to their efforts that the move was seamless, and we were up and running straight away.

Prior to the shift we also implemented a new records filing system, to achieve efficiency in storage of paper records. During this time we were able to donate a large number of surplus folders to community based recipients, such as Merivale Primary School, and Family Works Northern to use.

To sum up… we are proud of the 65 years of services that we have provided in the Bay of Plenty, but we aren’t sitting back resting, quite the opposite. We are energized, reinvigorated, and ready to meet the next 65 years head on!

Photography by Amanda Aitken, Living Visions Photography

INSET LEFT: The new high-tech meeting rooms are named after notable landmarks in the area. INSET RIGHT: The former boardroom table gets a new lease of life as a centrepiece in the staff café.

NUMBERS Spring 2012 • 9 www.staplesrodway.co.nz

H AVING RECENTLY ATTEMPTED A FEW days annual leave, it quickly became apparent that it is increasingly difficult to ‘switch off’.

While my husband drove, I proofed work documents on his behalf and fielded my own work calls. For the next three days, we took work calls while sight-seeing, responded to work emails while shopping and even worked while dining out. It was clear that this was not a true holiday.

The blurring of the boundaries between work and personal life has become so apparent that we can no longer really call this a work-life balance.

It is fair to say that work and life have become so integrated that there is rarely any balance between the two – possibly more of a consistent imbalance from one to the other at varying times.

We pride ourselves on being available to clients 24/7 – I’ve been known to sit in the school car park attending a conference call, construct elongated responses to emails half way round the supermarket and view my hair appointment as prime ‘work’ time to get things done.

In fairness to employers, there is a flipside, where we manage the lives of families from the comfort of a work PC and work-provided smart phones. For us fortunate ones, we are also given the flexibility to attend family activities and occasionally use that spare back office for a child care option.

New technologies have pushed this shift further and faster with email, iPhones and Blackberries major contributers to the blurring of the boundaries between work and life.

However, some organisations are now making a stand against 24-hour connectivity.

Volkswagen is one organisation that has deactivated the emails of German staff via mobile devices during out-of-office hours. Staff only receive emails half an hour before and half an hour after work. Volkswagen’s take was that “Mobile communication devices offer a great amount of freedom, but also embody the risk of no longer being able to switch off”. Other German companies have adopted a lesser policy of no mobile devices for management between Christmas and New Year unless there is an emergency.

These are interesting and significant steps in a country where burnout is blamed for almost 10 million sick days a year.

The Washington Post has also recently reported that “no after hours email” is part of a growing effort by some employers to rebuild the boundaries between work and home. Boundaries that have crumbled amid the do-more-with-less ethos that is a side effect of the economic downturn.

The Advisory Board Company in the US is one such example, asking staff to stay off email and instructing that if they can’t stay away, read but don’t reply. Their article refers to a recent survey by the Society for Human Resource Management indicating that one in four companies are creating similar rules to

Volkswagen. There is no doubt email is an important tool, but it has also worked to encroach on personal lives and contribute to work-life imbalance (not to mention encouraging passive aggressive behaviour and non-constructive confrontation).

I’m not sure we all need to go to the extent of Volkswagen and The Advisory Board Company, for many of us working in our own businesses or in SME’s to ‘switch off’ could actually jeopardise securing possible clients and projects. The one-man-band plumber is unfortunately now the receptionist, admin, and accounts person all in one.

So what does this work-life integration mean and how do we ensure that we maintain a balance? I feel quite positive about the term “integration”. Mainly because after years of trying to get a ‘balance’ and failing miserably (no matter which way the pendulum swung), I can more easily swallow the fact that the two are integrated and that this is okay.

It’s a reminder that whatever roles you are integrating, be it employee, spouse, parent, house-keeper, gardener, athlete, etc, they aren’t different hats after all, but integrated ones. There is no mythical scale of balance.

This is an interesting issue in the face of a talent shortage where employers are increasingly focused on the retention of their star performers, high potentials and critical talent.

Smart organisations are focusing on more flexible work practices that allow individuals to contribute when it suits them (day or night) and to stay and play at work. The likes of Facebook and Google are such organisations where they are catering to every lifestyle need – be it roller hockey interludes, ski holidays or gaming at work. They also handle other life considerations such as doctor and dentists visits and provide great free food and barista coffee. It results in every life need being catered for, from physical to social needs and beyond, meaning that your work can be your life.

While this points to further blurring the boundaries it may also enhance staff retention.

Director of the Career Engagement Group, Anne Fulton, says that the success of these strategies may well depend on understanding the motivators, values and career-lifestyles expectations of each employee and then tailoring the career experience to meet individuals’ unique wants and needs.

Possibly in response to the retention issue, we are also seeing many larger organisations implementing more long term career paths for their employees and in some cases lifetime career paths that follow a ‘grow from within’ approach and that allow for career breaks.

This move may either exacerbate the work-life blurring or it may work to resolve it, particularly for this next generation who are comfortable with “i-anything” area; where it is who they are.

In a world of smart phones and email, is having work-life balance asking too much, or is work-life integration the new norm?

Farm succession is an issue that can not only see many farms underperform, but at its worst, can divide families permanently. Marise James, a well-known figure in the New Zealand dairy industry as a director of a number of corporate farming businesses, steers you through the pitfalls and processes.

Article by Marise JamesSTAPLES RODWAY [email protected]

SUCCESSION PLANNINGIN THE DAIRY INDUSTRY

NUMBERS Spring 2012 • 11 www.staplesrodway.co.nz

I N MY MANY YEARS AS a dairy farmer and in governance roles in the industry I can’t think of a single issue that has plagued more dairying

families than farm succession.Lingering problems caused by mismanaging the succession process or

making the wrong decision on succession can affect farm performance and family relations adversely.

The problems come in many areas:

• Who wants the family farm and what is their expectation if they take it over?• How do you decide if more than one family member is interested?• How do you manage the inheritance issues among the non-interested

family members?• How do Mum and Dad get their money out in a timely manner?• In a larger business, are the skills there among the family to run a scaled-

up operation?• What is the intended strategy and viability for the future of the business –

to carry on paying dividends or to be sold off?• How could that business be parcelled up fairly for individual family

members to buy or inherit?• How do you ensure ongoing dividend streams to benefit all family members

– whether they have an interest in the farming business or not?

These are complex questions and many farming families are simply not equipped to address these questions. I’d go as far as to say no family-run business should attempt to solve these questions without advice. Why? It’s the emotion that is involved. Discussion around these questions is often informal, around the dinner table, or at family events.

As a result the right questions may not be asked, the best answers may not be found and the issues of succession can be left hanging, with some family members feeling intimidated and unable to express their views fairly. Various family members may be left with a different understanding of the outcome of those discussions and that can only lead to further tension during future discussions.

THE GOOD AND BADTwo recent examples I have worked with highlight the good and bad of planning for farm succession.

In the first, just about everything went wrong in a family of two sons and three daughters. One son wanted to buy the farm but never said anything and another son broke away from the family because of the debilitating effects of the personal and financial pressure. To complicate matters the in-laws became involved.

It became a complete mess with the parents and owners of the farm having to referee while trying desperately to accommodate the needs and wishes of each of their five children.

When the sale did eventually go through it was completed on a basis that was not the most tax efficient, nor did it offer the best retirement terms for the parents. Relationships were irreparably damaged.

By contrast Trevor and Harriet Hamilton, who built a $100 million dairying business from scratch, got it right when they decided to address their issues around succession planning.

The Hamiltons knew that with a business that size, they needed real exper-tise to help guide and manage the future of their business so that it would continue to grow and prosper beyond their lifetimes. They wanted it set up so the family members who wanted to be involved could find a role that fitted their skills, while other family members could derive dividends from the business to benefit education and other family orientated goals.

Trevor and Harriet are the type of people who never stop learning; they sought independent advice, outlined their goals, tweaked the resultant plan where necessary, and set up an independent board with a clear mandate to continue to maintain and grow the business. This Board has provided a non-emotional commercial forum for those family members to discuss and agree strategies and decisions that affect them all.

Four of five family members remain involved in the current eight-farm oper-ation; there is the ability to carve new farms out of the existing should a family member choose to buy and farm for themselves, and the non-involved family receive dividends that continue to benefit the whole family.

It’s a great example of turning a family business into an intergenerational, corporate business through applying good disciplines around succession planning.

WHAT TO CONSIDER?When it comes to considering farm succession there are two fundamental questions that need to be asked and one fundamental step that any dairy farming operation – small or large – should undertake before sitting down to consider those questions.

That step is to involve independent advisors. It could be your lawyer, accountant or some other expert that can provide the necessary level of inde-pendent advice that takes the sting and the emotion out of some the hard ques-tions and makes it easier to address the issues around fairness.

Then you’ve got two questions to consider:Are you looking at succession from an ongoing management point of view?

orAre you looking at succession from an inheritance point of view? They are quite different proposals.When you look at the first question, you then have to ask if you want the

family farming business to be run under management for the ongoing benefit of the family and whether there is a member of the family who is capable and/or interested in that option.

If the answer is no, or you decide you want to cash up, then the discussion becomes fairly straight forward around how you divide the inheritance from selling the farming operation.

Having that independent advice on hand means all parties affected by the discussion can articulate their views and the decision can be made on a purely commercial basis; the emotion is can be taken out of those tougher decisions.

However, if the answers are yes and the decision is to continue the busi-ness longer term and involve the family, things become more complex.

First, there should be no expectation that the farms will pass to a family member as of right – they must have the skills and capability to manage the operation, not just have it passed to them, or worse, dumped on them. This is especially important if the farming business is to continue to provide dividends for other members of the family.

If the view is the interested family members will develop the necessary skills, then the appropriate structures and resources need to be put around them to ensure they continue to learn and pick up those skills before taking over the operation.

Those structures will also be very important in to the continued success of the business and to ensuring the sustainability of dividends over an extended period of time.

They also separate out any possibility of future resentment developing among family members and when it is time to leave, the current managers/owners have a clear exit path and access to the cash they need for their retirement lifestyle.

The keys to successful succession planning are:

• Independent advisors• Structured, non-emotional and robust discussions that involve all parties• Proper business structures• Managed and understood planning for the future• Managed exit strategies where everyone understands and agrees the out-

comes well in advance

Staples Rodway provides specialist succession planning advice to over-come the many issues and pitfalls of failing to plan for farm succession.

12 • NUMBERS Spring

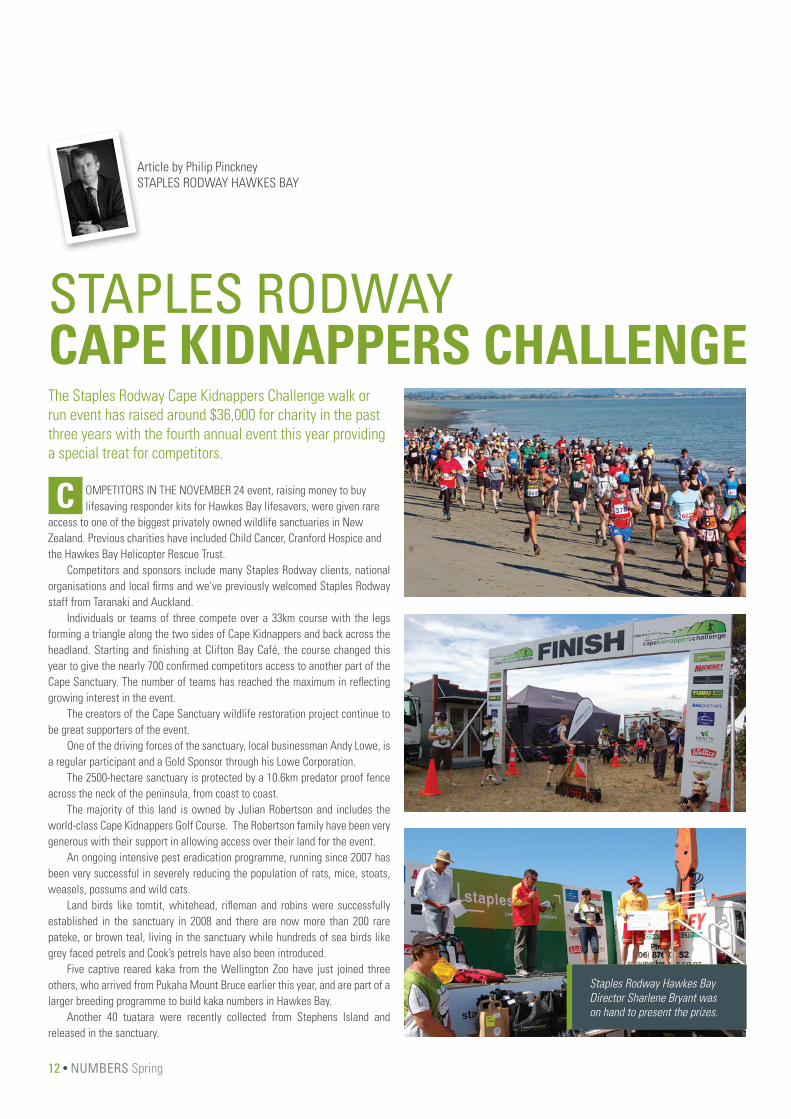

STAPLES RODWAY CAPE KIDNAPPERS CHALLENGE

C OMPETITORS IN THE NOVEMBER 24 event, raising money to buy lifesaving responder kits for Hawkes Bay lifesavers, were given rare

access to one of the biggest privately owned wildlife sanctuaries in New Zealand. Previous charities have included Child Cancer, Cranford Hospice and the Hawkes Bay Helicopter Rescue Trust.

Competitors and sponsors include many Staples Rodway clients, national organisations and local firms and we’ve previously welcomed Staples Rodway staff from Taranaki and Auckland.

Individuals or teams of three compete over a 33km course with the legs forming a triangle along the two sides of Cape Kidnappers and back across the headland. Starting and finishing at Clifton Bay Café, the course changed this year to give the nearly 700 confirmed competitors access to another part of the Cape Sanctuary. The number of teams has reached the maximum in reflecting growing interest in the event.

The creators of the Cape Sanctuary wildlife restoration project continue to be great supporters of the event.

One of the driving forces of the sanctuary, local businessman Andy Lowe, is a regular participant and a Gold Sponsor through his Lowe Corporation.

The 2500-hectare sanctuary is protected by a 10.6km predator proof fence across the neck of the peninsula, from coast to coast.

The majority of this land is owned by Julian Robertson and includes the world-class Cape Kidnappers Golf Course. The Robertson family have been very generous with their support in allowing access over their land for the event.

An ongoing intensive pest eradication programme, running since 2007 has been very successful in severely reducing the population of rats, mice, stoats, weasels, possums and wild cats.

Land birds like tomtit, whitehead, rifleman and robins were successfully established in the sanctuary in 2008 and there are now more than 200 rare pateke, or brown teal, living in the sanctuary while hundreds of sea birds like grey faced petrels and Cook’s petrels have also been introduced.

Five captive reared kaka from the Wellington Zoo have just joined three others, who arrived from Pukaha Mount Bruce earlier this year, and are part of a larger breeding programme to build kaka numbers in Hawkes Bay.

Another 40 tuatara were recently collected from Stephens Island and released in the sanctuary.

Article by Philip PinckneySTAPLES RODWAY HAWKES BAY

The Staples Rodway Cape Kidnappers Challenge walk or run event has raised around $36,000 for charity in the past three years with the fourth annual event this year providing a special treat for competitors.

Staples Rodway Hawkes Bay Director Sharlene Bryant was on hand to present the prizes.

NUMBERS Spring 2012 • 13 www.staplesrodway.co.nz

STAPLES RODWAY CAPE KIDNAPPERS CHALLENGE

S TAPLES RODWAY’S PHIL HANSER HAS been working with the family-owned business, headquartered in New Plymouth but with offices in

Christchurch, Wellington and Auckland, for about 14 years, advising on their computing and accountancy packages.

But when the company in-house accountant retired, Sopers decided to utilise the wider range of skills available from our Taranaki office to fill the gap in the business.

Business owner Rex Soper and CEO Kerry Forsyth were originally looking at replacing like for like and recruiting another in-house appointment to replace their previous, highly trusted accountant.

“It was actually my father we were looking to replace,” says Kerry Forsyth “and as he had been such a long-term, trusted part of the firm we thought we’d look for a similar in-house person.

“But when we looked at the services we needed and the expertise avail-able to us from Staples Rodway — who we already enjoyed a good relation-ship with — we decided on the additional expertise in various areas that Staples Rodway could provide.”

Kerry says that in the past 10-12 months or so the advantages of that deci-sion have been in the flexibility Staples Rodway can provide.

“The Human Resources and Audit teams have come in to look at our systems, see how we do things, and advise on little changes that help the business.

“With the team of Phil Hanser, Daimon Stewart and Abbey Tito we have access to a pool of varied expertise that we might not otherwise find in one person. They can come in, or find the right expertise we need, for however long is needed to solve a particular issue and get the best answer for our business.

“It has helped that they already knew us and we have quickly built up a good level of trust. Staples Rodway also audit themselves so we know we can rely on and trust the work they are doing for us.”

Rex Soper echoes Kerry’s comments in recognising the benefits of bringing in Daimon and Abbey who have the experience of working alongside other clients in their businesses. He says that this experience brings solutions that have worked elsewhere that can be applied to Sopers. Rex is also quick to point out the success of their new CRM Database which Phil and his team have

spent significant time in developing; it has allowed Sopers to better utilise technology and gain efficiencies.

Sopers has 54 staff based in four locations all working on providing the company’s door hardware including locks and closers, to both the residential and commercial property sectors.

The business is moving into hi-tech fields such as fingerprint locks with the renowned Kaba brand and in residential security has a product called Schlage Link that allows home owners to open and lock their properties through an iPhone or iPad app. Through security cameras a home owner can also use iPhones and iPads to see who is at the door.

“On the commercial side of the business we’ve worked extensively with Auckland Hospital and we’re currently working with Waikato, Wellington and Rotorua Hospitals as well as aged care providers Ryman and Somerset.

“We need to be sure of our systems and information to support our wide-spread network of offices and customers,” says Kerry, “and the Staples Rodway team work well with us in supporting the variety of services we need.”

Article by Phil Hanser & Damon StewartSTAPLES RODWAY TARANAKI

A long-term relationship in one area of business has led to a much closer partnership between national locksmith and door hardware business Sopers (NZ) Ltd and Staples Rodway Taranaki.

OPENING DOORSACCESS TO WIDE RANGE OF SERVICES BENEFITS LOCAL BUSINESS WITH NATIONAL FOOTPRINT

TO A NEW WAY OF WORKING

14 • NUMBERS Spring

T AX POOLING WAS INTRODUCED BY Inland Revenue in 2003. It enables people who have overpaid tax to trade their overpayment with

someone who has underpaid, giving both parties a better result in respect of interest and potential penalties. This is a result of the arbitrage opportunities offered by the difference between the current credit rate of use of money inter-est offered by Inland Revenue of 1.75% and the current debit rate of 8.4%.

The following are all potential uses of the tax pooling regime:

BUYING TAXIf a taxpayer underpays or does not pay a provisional tax or terminal tax liability, they can purchase tax (at the appropriate date) via a tax pooling intermedi-ary. They will pay the intermediary interest but at a rate lower than the Inland Revenue’s rate (between 2% and 3%). By making the purchase they will also mitigate or remove any late payment penalties that would have been charged by Inland Revenue, as from Inland Revenue’s perspective the tax was paid in full and on time.

DEPOSITING TAXIf a taxpayer regularly pays provisional tax they may choose to make the pay-ments to a tax pooling intermediary rather than Inland Revenue. All payments to a tax intermediary will be held in trust and the taxpayer can request that they be refunded to them or transferred to Inland Revenue at any time.

Once the taxpayer’s liability for the year has been calculated and their return filed they can then ask the tax pooling intermediary to transfer the required tax to their Inland Revenue account. Any surplus tax over and above their liability can then be sold to other taxpayers via the tax pooling intermediary. This will maximise their credit interest.

Any taxpayers who regularly overpay their provisional tax should consider using a tax pooling intermediary. Their payments will be held safely on trust until they need them and they will obtain a greater rate of return on any overpayments.

FINANCING TAX PURCHASESTax financing is essentially the payment of an amount of interest in order

to secure the right to buy tax at some future date. Taxpayers benefit from increased cash retained whilst having guaranteed access to the tax needed, at the dates it is needed.

When tax is financed the tax pooling intermediary borrows the amount of tax the taxpayer wishes to finance, and deposits this in the tax pool. This creates the credit for the taxpayer. The tax credit is then held on trust for the taxpayer until the maturity date of the finance arrangement, at which point the taxpayer pays for the tax in full and it is transferred to their Inland Revenue account.

This is a particularly useful option for taxpayers who know they have a tax liability but do not have the means to pay at that point in time. By financing the tax they can ensure that they will have access to the tax they need at the dates needed once they are able to pay for it.

TAX INVESTIGATIONS AND VOLUNTARY DISCLOSURESIf Inland Revenue reassess your tax liability, as a result of an investigation or a taxpayer voluntary disclosure, tax pooling can be used to pay any resulting tax liability and reduce the interest charged. In these situations it is possible to use tax pooling for all tax types (such as GST and FBT) and not just income tax.

TAX TREATMENT OF INTERESTAny interest paid or received in connection with tax pooling will be treated in the same way as use of money interest paid to or received from Inland Revenue and will be deductible or taxable.

CHOOSING A TAX POOLING INTERMEDIARYThere are several tax pooling intermediaries available, all of which are approved by Inland Revenue. The choice of intermediary will depend on how you wish to use tax pooling and what features you are looking for. At Staples Rodway we have contacts at all the main intermediaries and understand their points of dif-ference and can work with you to determine which one best meets your needs.

If you have any queries about how tax pooling may benefit your business, please do not hesitate to contact your usual Staples Rodway advisor.

Article by Philip HampsonSTAPLES RODWAY [email protected]

Tax pooling can free up capital, reduce your interest exposure, and ultimately be a lifesaver for your bottom line.

TAX POOLINGA SMARTER WAY TO PAY TAX

T HERE IS A $50,000 THRESHOLD where you can effectively opt out of the FIF Rules. So it’s surprising to learn that taxpayers have success-

fully lobbied the Government to allow individuals with investments below this threshold to elect into the FIF Rules.

Traditionally, most New Zealanders have invested in companies resident in the grey list countries: in particular Australia, Canada, the UK and the USA. Investments in these countries received favourable treatment because their tax systems were thought to be ostensibly the same as New Zealand’s system. Thus, if New Zealand taxed the income, a foreign tax credit would probably have been available to offset the tax so payable.

Prior to 1 April 2007, if the investments were in companies resident in the grey list countries, the Kiwi investor was only taxed on dividends received. All that has changed and most investors are applying the Fair Dividend Rate (“FDR”) method, which is based on 5% of the market value of the investment.

Broadly speaking, the FDR method taxes individual investors and family trusts on their portfolio investments on the lesser of 5% of their opening market value and the actual gain produced by the shares during the year. The actual gain is the sum of dividends paid plus any increase in the value of the investment.

THE PAY-OFF Why would people elect into the FIF rules?

The benefit of the FIF rules is that the FDR Tax cost is a one-time cost. You don’t pay tax on actual dividends or on the gains made on the sale of the invest-ment to the extent they have exceeded 5% of the opening value of the investment.

Consequently, these rules are ideal for growth stocks and for stocks with a high dividend yield. So what’s the catch? Once you elect in you are practically locked into the FIF rules for the foreseeable future.

It is possible to get back under the $50,000 exemption, and pay tax only on your dividends. However, in order to achieve that you would have to sell all your overseas shares, and not hold any for four years in a row. This is to prevent people from cherry picking the best method on a year-by-year basis.

So, even if you have a relatively small portfolio of offshore shares, maybe you should be talking to your Staples Rodway advisor about using the FIF Rules to your advantage.

For more information please contact either Spencer or Sybrand in our Christchurch office on 03 343 0599.

Most accountants dread the Foreign Investment Fund (FIF) rules which apply to selected offshore investments (generally shares and super-schemes, but not interest-bearing loans). So why are many opting into the rules when they don’t have to?

Article by Spencer Smith & Sybrand van SchalkwykSTAPLES RODWAY [email protected] [email protected]

ELECTING INTO THE FIF RULES?CRAZY OR CANNY?

NUMBERS Spring 2012 • 17 www.staplesrodway.co.nz

O VER THE LAST FIVE YEARS, Taranaki has been home to the nation’s best performing district. According to economists BERL, New Plym-

outh topped rankings for economic growth, business unit growth and employ-ment between 2006 and 2011. In the June 2012 quarter this trend continued, with Taranaki posting 3 per cent growth, well ahead of second placed Waikato on 1.2 per cent and a national average of just 0.6 per cent.

These positive results have been underpinned by strongly performing oil and gas and export sectors and are built on a strong foundation of innovative thinking for which Taranaki is quietly renowned.

This innovation dates back to the region’s pioneering days, perhaps epito-mised by the Taranaki Gate – where the nation’s early farmers saw a problem, the inventive Taranaki farmer saw a simple solution.

These days that spirit of innovation manifests itself right around Taranaki’s picture-perfect mountain. Everything from the world’s best super yachts to the fastest windsurf boards, to the most comfortable hospital beds to stunning sculptures. They’re exporting digital technologies developed for the oil and gas sector to Houston Texas, engineering solutions for projects all around the world, and producing the components of some of the globe’s most popular burgers.

Taranaki’s business landscape is open to driving that innovation – the regional development agency Venture Taranaki last year facilitated 38 research and development grants to Taranaki businesses worth a total of $1,093,380, and delivered 210 Capability Development Vouchers with a total value of $240,108. Between July and September this year, Venture Taranaki enabled a further $1.16 million in R&D investment into Taranaki businesses.

But the region faces a challenge to maintaining this momentum. A recent Petroleum Skills Association survey found that the region’s top ten companies in the oil and gas industry anticipate 230 job vacancies between them over the next year. The strong Australian mining sector has lured many of the region’s skilled workforce over the ditch – Australia counts for 31 per cent of the region’s long-term arrivals and 73 per cent of departures.

Finding the right skilled people to fill the gaps in the oil and gas and other industries is critical not only to the region’s prosperity, but to its economic sur-vival. The region has a population target of 135,000 by 2035 just to keep its share of national population-based funding models. Latest estimates have the regional population at just over 110,000 people - it will require many more to reach its growth aspirations.

One of the many activities to attract more people to and back to the region’s legendary lifestyle is the Swap Sides campaign. Initially developed around the Rugby World Cup, it has been responsible for attracting some of the 30,595 RWC 2011 related visitors back here for permanent jobs.

The campaign has recently been bolstered with the launch of an online video that acts as a humorous reminder of the region’s charms. Fronted by former Taranaki comedian Ben Hurley, it’s available at the www.swapsides.co.nz website, and is supported by an extensive social media campaign.

Ensuring Taranaki can continue to lead the nation over the next five years and beyond will require every one of the region’s agencies, businesses and resi-dents to share in the twin goals of population attraction and economic growth.

Taranaki’s growth will be built on innovation and skills.

TARANAKISCALING NEW HEIGHTS

Article by Antony RhodesCOMMUNICATIONS MANAGER, VENTURE TARANAKI

18 • NUMBERS Spring

O N THEIR RETURN TO NEW Zealand in 1997 after a number of years working for iconic wine producer Penfolds in Australia Jeff Poole

and his wife Virginia recognised a gap in the local wine retail market. They saw an opportunity to deliver high quality wines to the New Zealand wine drinker at reasonable prices.

They launched a new business called the Fine Wine Delivery Company from a spare room in their Torbay home and that is where the journey began. They are now New Zealand’s largest single-store premium wine retailer and most successful internet wine reseller with 15 full time employees.

This is the quintessential Kiwi family business success story with Jeff and Virgina’s son Richard and daughter Tracey taking active and essential roles in the company and contributing to its history.

However, the business has not been without challenges and after several years of unrivalled success, which saw them move into large commercial prem-ises in Auckland’s CBD, in 2007 they decided to venture further afield into a significant retail operation on Riccarton Road in Christchurch.

That move was predicated on large growth achieved in the company’s South Island customer base via the internet site and a perceived need for a retail store in Christchurch to continue the growth momentum in the southern customer base.

Unfortunately the Christchurch venture failed to deliver the desired result and the Auckland operation was put under financial strain with the family having to consider the implications of insolvent trading.

In November 2008, they were introduced to the Business Recovery team at Staples Rodway and the team quickly determined the company was an ideal candidate for the newly-introduced Voluntary Administration regime.

After many long nights at the office, numerous meetings with the company’s bankers and trade creditors and umpteen revised profit forecast models, a Deed of Company Arrangement was put in place whereby the debts of the company would be repaid over a period of time while still trading with suppliers and customers.

Now more than $2 million has been repaid and the company is well on the way to repaying the old debt.

It remains current with all providers and has since purchased tens of millions of dollars of wines from supporting suppliers providing a critically important route to the retail market for a great many New Zealand wine pro-ducers. The company has also been able to assist a number of wineries to clear cancelled export orders and excess stocks while ensuring the integrity of their brands is maintained.

Through the dedication, passion and tenacity of the Poole family and the team at the Fine Wine Delivery Company, together with the assistance of the Staples Rodway Business Recovery team the business has survived and pro-vides a great buying experience to anyone who enjoys a glass of fine wine.

The principal point of difference is that the skilled and knowledgeable team tastes every wine before it goes on sale, ensuring that the customers are delivered only the best wine buying options with offers tailored to suit cus-tomers’ preferred drinking habits, based on their carefully maintained buying history for each customer.

As the name of the company suggests, the focus has always been on fine, quality wines which represent great wine buying value. To avoid excluding the more price conscious customer, the company also has an online-only offering known as www.bestwinebuys.co.nz which sells wines priced under $15.

However, there is no compromise on quality and the wines on offer rival supermarket pricing, with the point of difference being that every wine has been pre-tasted so the customer knows they can rely on that quality assurance process.

In this and future editions of Numbers, Jeff will recommend a wine or two and provide some of his vast knowledge and insight into those wines which, of course, can be purchased from the Fine Wine Delivery Company.

www.finewinedelivery.co.nz & www.bestwinebuys.co.nz

After surviving some tough times, The Fine Wine Delivery Company is toasting the future of their business.

THE GLASS IS

Article by Gareth HooleSTAPLES RODWAY AUCKLAND

NUMBERS Spring 2012 • 19

RYAN NELSEN CENTRAL OTAGO PINOT GRIS 2012

An intensely flavoursome and beautifully fresh Pinot Gris from our favourite Otago vineyards.

SMELLS: Vibrant array of blossom, stone fruit and spice aromas typical of the variety when perfectly pure and ripe.

TASTES: Succulent pear, peach and melon flavours are infused with cin-namon/nutmeg spices. The luscious, tasty palate finishes crisply with a scintillating touch of sweetness. An intensely flavoursome Pinot Gris that is at optimum now to 2016.

Raymond Chan, Wine Judge

RYAN NELSEN CENTRAL OTAGO PINOT NOIR 2011

Sweet fruits, savoury complexities and fine spice wrapped within a seductive velvety texture.

THE WINEMAKING: The wine was plunged once daily during pre-fer-mentation and twice daily during fermentation. When in harmony it was pressed off to French oak barrels to spend 10 months on lees.

SMELLS: Exudes the classical dark cherry, dried herb and spicy aromas distinctive of these estates.

TASTES: Luxurious in its mouth feel its bountiful palate is beset with dark, warm fruits beautifully con-trasted by savoury complexities and fine spice within a seductive velvety texture. The result is a very special, complex Pinot Noir to enjoy now through 2016.

Raymond Chan, Wine Judge

Available at www.finewinedelivery.co.nz

Jeff Poole THE FINE WINE DELIVERY COMPANY

WINE PICKS

Recent court cases in New Zealand and Australia have drawn attention to the duties of company directors. Jackie Russell-Green examines some of the key financial reporting matters of which directors need to be aware.

Article by Jackie Russell-GreenNATIONAL TECHNICAL [email protected]

NUMBERS Spring 2012 • 21 www.staplesrodway.co.nz

M ANAGEMENT EXPERTS CONTINUALLY EMPHASISE THE need for boards to govern and management to manage. Although that’s

extremely valuable advice, as it’s important that directors have a clear focus on strategy, New Zealand company legislation and recent New Zealand and Aus-tralian court cases make it clear that directors must understand the business in sufficient detail to fulfill their directorial obligations.

One of the clear messages from recent cases is that each individual director is responsible for the performance of all directorial duties, as the responsibility is an individual one, not a collective one.

Many boards include directors who were selected for their expertise in an area critical to the company – for example, construction firms will often have an engineer on the board, technology firms will often have an IT expert and many firms have a director who is a marketing expert.

Such subject matter experts might be inclined to think that their responsibility extends only to areas in which they have expertise, and that the members of the board with accounting and finance experience should take responsibility for the financial oversight of the business and the preparation of financial statements.

However, that conclusion is incorrect – recent Australian and New Zealand court cases have made it clear that each director is required to pay attention to all matters coming before the board, irrespective of whether those matters fall within, or outside, the director’s personal field of expertise.

These court cases also show that relatively inexperienced directors are not relieved of their individual obligations by the presence of more experienced directors. In addition, recent cases also show that directors are entitled to rely on the advice of experts, but that they must not do so uncritically – for instance, where advice is based on assumptions and estimates, directors must satisfy themselves of their appropriateness.

It’s clear directors are therefore required to be involved in the management of the company and to take all reasonable steps to be in a position to guide and monitor the company’s activities.

Those recent court cases clearly indicate that directors are only able to meet these requirements if they have a reasonable level of understanding of the company’s financial performance and position and a reasonable understanding of the business conducted by the company. For instance, the judgement in the much-discussed Australian Centro case stated that: “While directors are entitled to delegate to others the preparation of books and accounts and the carrying on of the day-to-day affairs of the company, they are still required to take a diligent and intelligent interest in the information available to them, to understand that information, and to apply an enquiring mind to their responsibilities.”

Some of the most important activities undertaken by a director relate to the preparation of financial information. The Centro case makes it clear that the responsibility of directors when reading the financial statements is not merely to correct “typographical or grammatical errors or even immaterial errors of arithmetic”, but to “ensure, as far as possible and reasonable, that the informa-tion therein is accurate” and that consequently “the scrutiny by the directors of the financial statements involves understanding their content”.

For directors to properly meet these obligations, they must have reason-

able levels of financial literacy and understand the business undertaken by the company and the risks inherent in the business.

In our experience, some of the financial reporting issues that cause the greatest problems for directors are:

Accounting for complex transactionsWhere businesses are involved in complex transactions, it is likely that the accounting treatment will also be complex. Directors need to ensure that such transactions are properly understood by those preparing the financial statements.

Complex accounting treatments often rely on assumptions about future events. Directors need to be satisfied that these assumptions are consistent with the directors’ understanding of those issues. In addition, assumptions used in preparing financial statements (such as the assumptions made when impairment testing goodwill) should be derived from the entity’s board approved business plans and strategies, which must be realistic and based on sound information and judgement. Where estimates are based on factors external to the company (such as when determining the fair value of an asset that is not traded in an active market), directors must review these estimates and be satis-fied that they are reasonable.

Classification of debt and equityMany companies enter into financing transactions involving instruments such as convertible notes. In many instances, these instruments are classified as equity, without a proper consideration of their features. The rules governing the classification of a financial instrument as debt or equity are complex, and it is important that this classification is correct, as it is likely to be relied upon by a number of external parties, including lenders.

Current and non-current classificationsDirectors should examine the classification of assets and liabilities as either current or non-current. Ordinarily, an asset is classified as a current asset where it is expected to be realised within twelve months of balance date. All other assets are classified as non-current assets. However, under New Zealand equiv-alents to International Financial Reporting Standards, the test for classifying a liability as current is different – a liability can only be classified as non-current if the company has an unconditional right to defer settlement of the liability for at least twelve months after the reporting date. Thus, where a long-term bank loan must be reviewed annually, and one of the possible consequences of the review is that the debt can be called, it must be classified as current. Similarly, if the debt covenants have been breached and the lender has not waived its right to call the debt as a result of the breach, it must also be classified as current.

Obviously this isn’t a comprehensive list, but directors who can get on top of those issues are much better placed to provide the level of financial reporting oversight that their position demands of them.

We anticipate that the proper performance of directors’ duties will con-tinue to be a significant issue. In future issues of Numbers we’ll explore other issues that directors need to be aware of. In 2013 we’ll launch some exciting new initiatives to help directors meet their obligations – these will also be announced in Numbers.

DIRECTORS’ DUTIESUNDER THE

SPOTLIGHT

22 • NUMBERS Spring

INTO THE

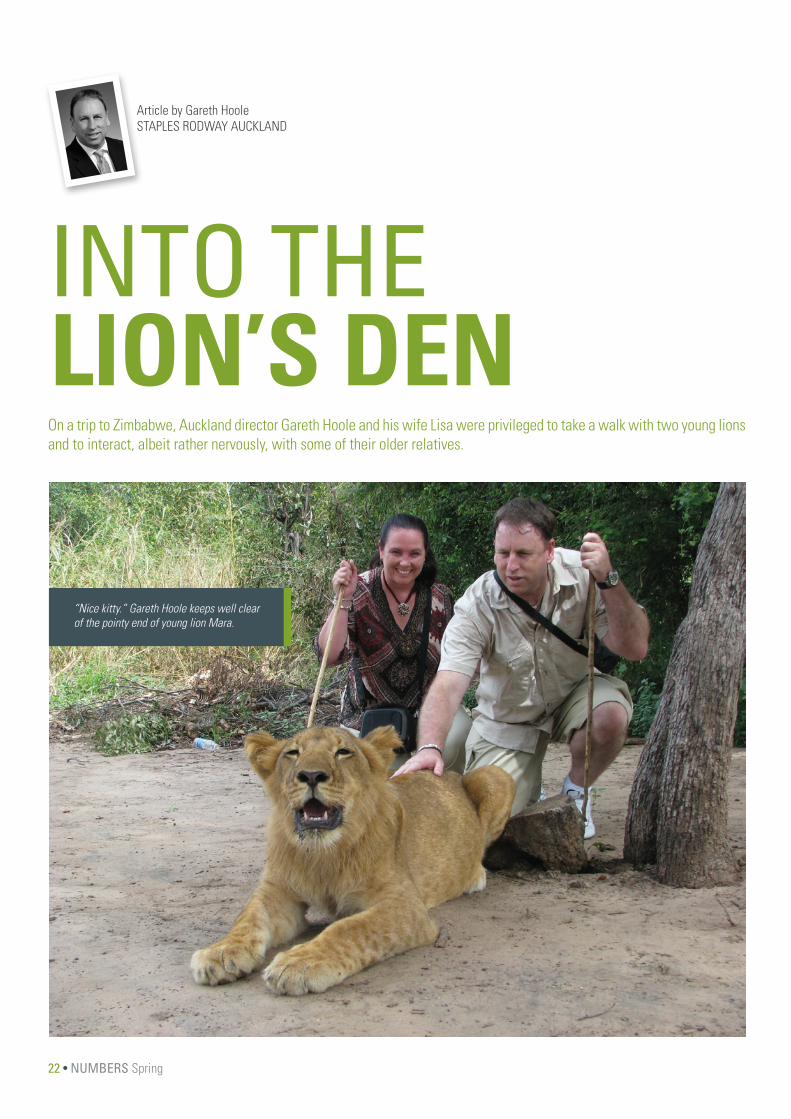

Article by Gareth Hoole STAPLES RODWAY AUCKLAND

LION’S DENOn a trip to Zimbabwe, Auckland director Gareth Hoole and his wife Lisa were privileged to take a walk with two young lions and to interact, albeit rather nervously, with some of their older relatives.

“Nice kitty.” Gareth Hoole keeps well clear of the pointy end of young lion Mara.

NUMBERS Spring 2012 • 23 www.staplesrodway.co.nz

F OR MILLENNIA THE LION HAS been an instantly recognisable symbol of courage, authority and of wisdom for cultures throughout the world.

Now, this iconic creature is in danger of losing its place as the King of Beasts.Since 1975 it is estimated that as much as 90% of the feral lion popula-

tion in Africa has been decimated by poachers, disease and encroachment into their natural habitat.

However, in Southern Africa there is a programme to preserve these beau-tiful big cats by creating in-captivity breeding programmes, ensuring proper genetic diversity, followed by rehabilitation to their natural environment where they live and do what comes naturally to them.

Just a few kilometres up the lazy grey Zambezi River from the mighty Victoria Falls, in the Matetsi safari area ALERT (African Lion Environment and Research Trust) is researching the habits and environments of the African lion and working towards restoring their population.

As part of their necessary fund raising activities they admit a small number of tourists each day to interact with the lions.

On a very hot day when the temperatures were soaring into the high 30’s two rather apprehensive but eager Kiwi tourists arrived at the Victoria Falls ALERT camp where we were given a briefing on the trust and, more importantly, how to behave around the lions. These are still wild animals even though they are accustomed to human interaction.

While being told by our guide Derek that we would be walking in a game reserve where all manner of wild animals reside, including Africa’s Big 5, we could hear the unmistakable throaty growl of juvenile lions not very far from where we were sitting, both exciting and disconcerting at the same time.

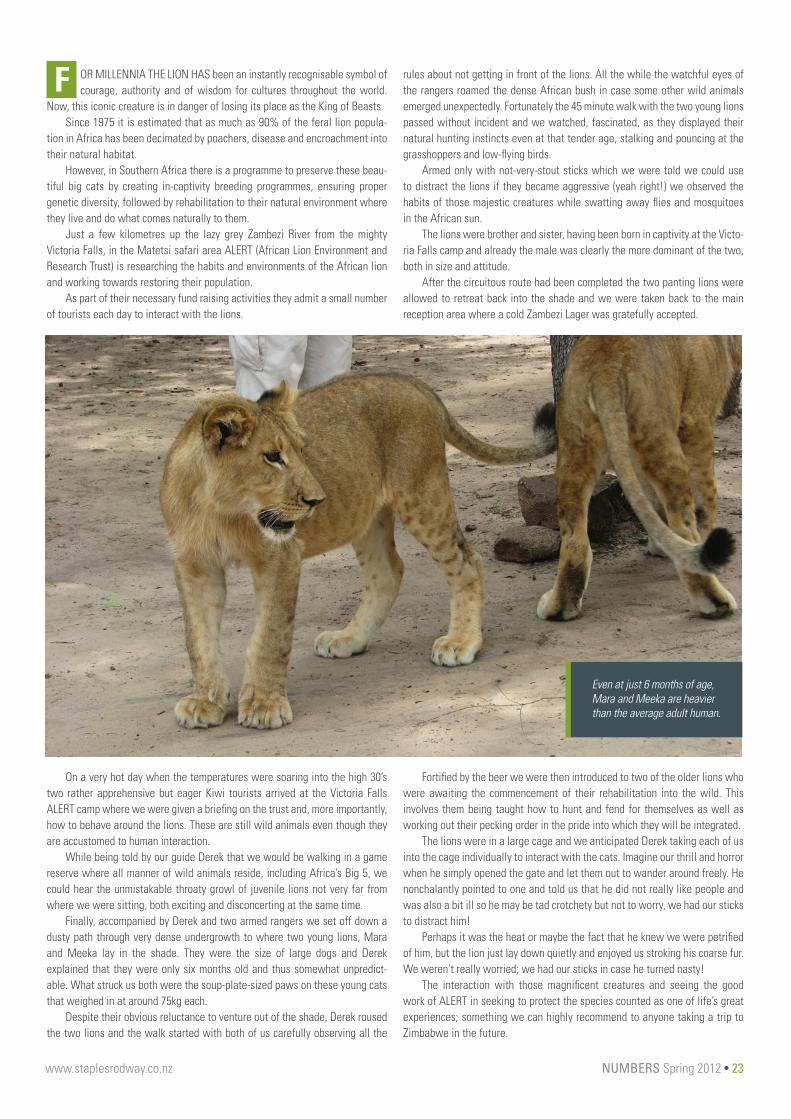

Finally, accompanied by Derek and two armed rangers we set off down a dusty path through very dense undergrowth to where two young lions, Mara and Meeka lay in the shade. They were the size of large dogs and Derek explained that they were only six months old and thus somewhat unpredict-able. What struck us both were the soup-plate-sized paws on these young cats that weighed in at around 75kg each.

Despite their obvious reluctance to venture out of the shade, Derek roused the two lions and the walk started with both of us carefully observing all the

rules about not getting in front of the lions. All the while the watchful eyes of the rangers roamed the dense African bush in case some other wild animals emerged unexpectedly. Fortunately the 45 minute walk with the two young lions passed without incident and we watched, fascinated, as they displayed their natural hunting instincts even at that tender age, stalking and pouncing at the grasshoppers and low-flying birds.

Armed only with not-very-stout sticks which we were told we could use to distract the lions if they became aggressive (yeah right!) we observed the habits of those majestic creatures while swatting away flies and mosquitoes in the African sun.

The lions were brother and sister, having been born in captivity at the Victo-ria Falls camp and already the male was clearly the more dominant of the two, both in size and attitude.

After the circuitous route had been completed the two panting lions were allowed to retreat back into the shade and we were taken back to the main reception area where a cold Zambezi Lager was gratefully accepted.

Fortified by the beer we were then introduced to two of the older lions who were awaiting the commencement of their rehabilitation into the wild. This involves them being taught how to hunt and fend for themselves as well as working out their pecking order in the pride into which they will be integrated.

The lions were in a large cage and we anticipated Derek taking each of us into the cage individually to interact with the cats. Imagine our thrill and horror when he simply opened the gate and let them out to wander around freely. He nonchalantly pointed to one and told us that he did not really like people and was also a bit ill so he may be tad crotchety but not to worry, we had our sticks to distract him!

Perhaps it was the heat or maybe the fact that he knew we were petrified of him, but the lion just lay down quietly and enjoyed us stroking his coarse fur. We weren’t really worried; we had our sticks in case he turned nasty!

The interaction with those magnificent creatures and seeing the good work of ALERT in seeking to protect the species counted as one of life’s great experiences; something we can highly recommend to anyone taking a trip to Zimbabwe in the future.

Even at just 6 months of age, Mara and Meeka are heavier than the average adult human.

M OST PEOPLE IN BUSINESS KNOW that there are the tax rules for investors in Controlled Foreign Companies (CFCs) and there are

Foreign Investor Fund (FIF) Rules for ‘portfolio’ investors holding interests of less than 10% in a foreign company.

But what are rules for the person holding more than 10% but less than 50%? The ‘In Between’ Investor is technically called a ‘non-portfolio investor’

(abbreviated to ‘NPI’ hereon for brevity’s sake) and the investment is called a ‘non-portfolio FIF’. The NPI has a significant shareholding, but not enough to control the non-portfolio FIF; therefore it is not a CFC.

The rules that tax a NPI have recently been updated. Prior to the update the rules for NPIs were divided into 2 camps: the grey list countries (Australia, Canada, UK, USA, Japan, France and Spain) and the rest. A NPI investing in a company resident in a grey-list country was taxable only on dividends received.

THE NEW RULESThe new rules align with the FIF Rules for portfolio investors (< 10%), but with one important difference: a NPI investing in an Australian company will be taxed on dividends only i.e. the company does not have to be listed. In contrast, portfo-lio investors in Australian companies may be taxed on the dividends only, but the company must meet certain conditions, including being listed on the Australian Stock Exchange. This concession for NPIs is both convenient and sensible.

For investments in countries other than Australia, the problem in many cases is that the shares in the non-portfolio FIF will not be traded on a recog-nised exchange. Therefore, there is no readily available market value to use. Consequently, the NPI is left with rather limited options.

Generally speaking, the investor can elect either to be taxed only on their share of the passive income of the company they invested in, or they can apply a method that taxes 5% of the ‘cost’ of their investment.

As you might expect, the rules can be a minefield, but fortunately your Staples Rodway team are always on hand to guide you through.

For more information please contact either Spencer or Sybrand in our Christchurch office on 03 343 0599.

When it comes to the new Foreign Investment Fund rules, it’s no longer a case of ‘one size fits all’.

THE INBETWEEN INVESTOR

Article by Spencer Smith & Sybrand van SchalkwykSTAPLES RODWAY [email protected] [email protected]

NUMBERS Spring 2012 • 25 www.staplesrodway.co.nz

THE INBETWEEN INVESTOR

L EADING ECONOMIC COMMENTATORS SEE THE current New Zealand economy as only half way through a seven-year readjustment process

characterised by inconsistent demand, margins under threat, continued delever-aging and rebalancing of the economy and business sectors. Business owners hoping the economy will recover rapidly are likely to be disappointed.

Many businesses have survived the post GFC economic period by just cutting costs and approaching business from a ‘siege’ mentality. This response has preserved a short term trading position for some, but with increasing exter-nal pressures this approach is unlikely to create the platform to prosper in the medium or longer term. For some the lack of any realistic restructuring of their business in the face of change outside their control will lead to business failure.

Some owners have approached expense reduction advisors that offer a relatively unsophisticated cost reduction service for bulk costs such as energy, telecommunications and other regular purchases, but these items are only part of the picture.

Business optimisation and structuring is a far more strategic response that looks at a business from a holistic point of view, how that business currently operates and seeks to identify an optimal position for the future. This process typically determines the current position, market opportunities, the most effi-cient way of presenting products to market and sustainability in the future.

In many assignments we have identified the business is not viable in its current form due to contraction of the market or changing technologies. If the current business structure is not viable or making an inadequate return on the capital invested in the business, the owners must seek an alternative.

Many businesses are experiencing margin erosion and need to find ways of reducing product acquisition costs. Manufacturers may need to consider sourcing some of their products from overseas or re-equipping their facilities to match overseas competitors.

Consideration will be given to adding new products, markets or the acquisi-tion of a competitor to increase scale. In some circumstances a smaller focused business may be the solution.

By applying a top down approach available market opportunities, margins and cost structures can be effectively examined together with the funds required to support the business. These exercises look at internal and exter-nal operational efficiencies and seek to determine the best fit of ingredients to maximise profitability and the return of funds.

The management team is also a key consideration in managing a reposi-

tioning process successfully. Risk will also be factored into any recommended solution and in particular the implementation risks of transitioning a business from its current structure to a new structure for the future.

Ownership of customer relationships is even more important for business owners in the face of increasing competitive challenges. Businesses need to offer a world class service at a competitive price to remain relevant.

Business optimisation will identify the ideal position for the future and in conjunction with the leadership team plot the sequential steps required to implement the plan. Strategy advisors tend to label these steps in technical terms, our approach to use established processes to find ways to create a sus-tainable business explained in simple and understandable language. Our goal is to generate increased profits and improved cash flows.

The current economic environment has created both opportunities and challenges for people in business. Many small to medium businesses in New Zealand need to adapt to changing circumstances and increasing competitive pressure.

THEYEAR ITCH7

Article by Colin TheyersSTAPLES RODWAY [email protected]

26 • NUMBERS Spring

T EACHING YOUNG NEW ZEALANDERS FINANCIAL literacy seems to require the same approach as teaching kids about nutrition.

The fundamental principle is to recognise the difference between wants and needs and not scoff everything in front of you. The greatest demon in both cases is that familiar human trait – greed.

All the lessons in the world about budgeting and the benefits of compound interest will be a waste of time if you can’t master the basic behaviour of delayed gratification. Going without something today in order to have a better tomorrow – how hard can that be?

Very hard in fact. There’s no doubt that children struggle with this and so do adults. Some are just better at it than others.

The famous Stanford Marshmallow Experiment, a 1972 study on deferred gratification by psychologist Walter Mischel, is a great example. One by one, four-year-old children were led into a room where their treat of choice (Oreo, marshmallow or pretzel stick) was placed on a table by a chair. The children were told that they could eat the marshmallow, but if they waited 15 minutes, without giving in to temptation, they would be rewarded with a second marshmallow.

Over 600 children took part in the experiment with a minority eating the marshmallow immediately. Of those who attempted to delay, only one third deferred gratification long enough to get the second marshmallow.

However, it was the results of the follow-up study that took place many years later that surprised Mischel. Mischel discovered there existed an unex-pected correlation between the results of the marshmallow test and the success of the children many years later.

The first follow-up study, in 1988, showed that “preschool children who delayed gratification longer in the self-imposed delay paradigm were described more than 10 years later by their parents as adolescents who were “significantly more competent”. A second follow-up study, in 1990, showed that the ability to delay gratification also correlated with higher scores in academic achievement.

What I’d like to know is whether the kids who waited for the second marsh-mallow ended up as adults with a higher net worth than the other participants. Did the inherent ability to delay gratification make these kids better savers as

adults? I’d also like to know, if you carried out a similar test on 600 four-year-olds today (40 years after the original study), would you have a different per-centage of them willing or able to wait?

In addition to willpower, a person’s environment must surely play a part. The issue for our kids today is one of abundant supply. There is just so much stuff out there.

Advertisers with access to decades of observations and lessons about consumer behaviour have wrapped up their “buy” messages in a captivating mix of music, colour and special effects. Just like the poor kid stuck in an empty room in front of the marshmallow, it is nigh on impossible for children today to avoid temptation.

During the experiment in the 1970s, Mischel observed that some kids would “cover their eyes with their hands or turn around so that they couldn’t see the tray, others would start kicking the desk, or tug on their pigtails, or stroke the marshmallow as if it were a tiny stuffed animal”.

If your child owns a cell phone or an iPod or iPad, you can be sure they are receiving messages constantly about one-day deals that are not to be missed. Their willpower is being sorely tested every day.

If the spending versus saving decision is just a matter of willpower, however, why is our government so keen on raising the level of financial lit-eracy in New Zealand – and will it make any difference to improving our financial wellbeing?

The NZ Network for Financial Literacy defines “financial literacy” as: “The ability to make informed judgements and take effective decisions regarding the use and management of money throughout life.”

Let’s think about that for a bit …Those people who lost money in failed finance companies must have

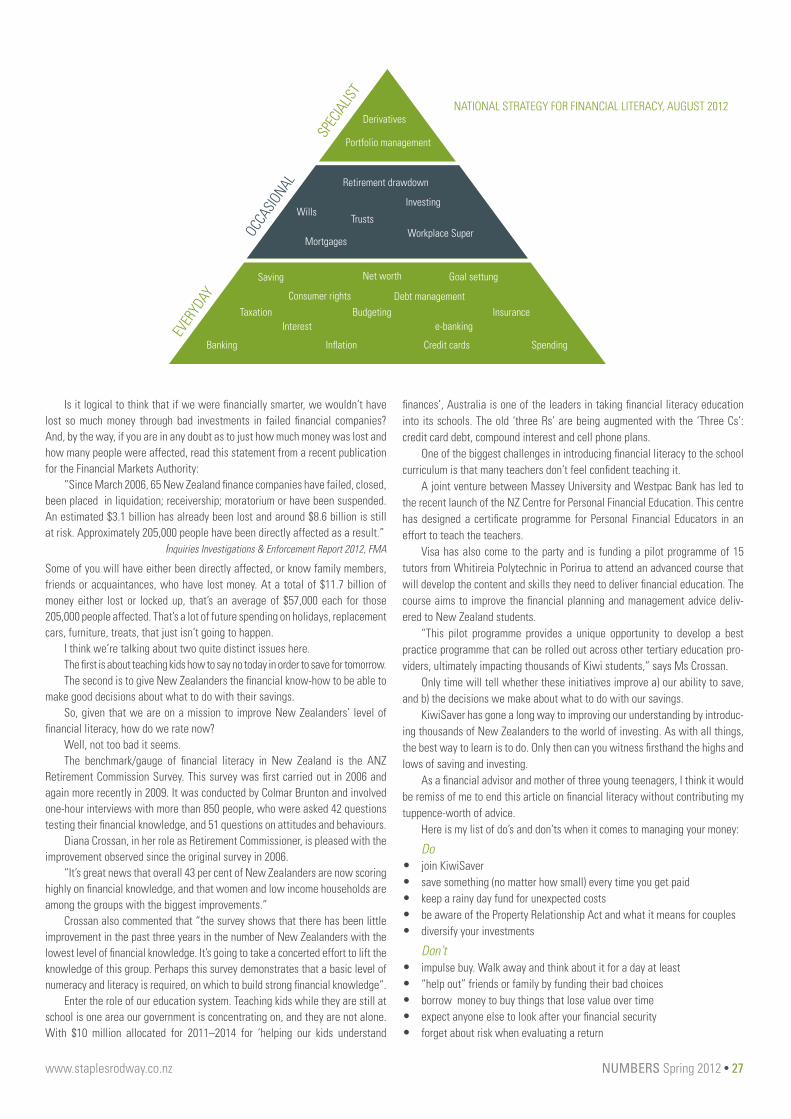

managed to save it in the first place – which means that willpower and the ability to go without was not the issue here. To be in a position to invest in anything, those individuals are likely to have progressed beyond the first layer of the diagram below, which “reflects the range of information and different levels of skill and knowledge that everyone needs to live in a modern economy”.

IN NZFINANCIAL LITERACY

Teaching financial know-how is more about mind over matter rather than a textbook approach.

Article by Louise O’BrienSTAPLES RODWAY [email protected]

NUMBERS Spring 2012 • 27 www.staplesrodway.co.nz

Is it logical to think that if we were financially smarter, we wouldn’t have lost so much money through bad investments in failed financial companies? And, by the way, if you are in any doubt as to just how much money was lost and how many people were affected, read this statement from a recent publication for the Financial Markets Authority:

“Since March 2006, 65 New Zealand finance companies have failed, closed, been placed in liquidation; receivership; moratorium or have been suspended. An estimated $3.1 billion has already been lost and around $8.6 billion is still at risk. Approximately 205,000 people have been directly affected as a result.”

Inquiries Investigations & Enforcement Report 2012, FMA

Some of you will have either been directly affected, or know family members, friends or acquaintances, who have lost money. At a total of $11.7 billion of money either lost or locked up, that’s an average of $57,000 each for those 205,000 people affected. That’s a lot of future spending on holidays, replacement cars, furniture, treats, that just isn’t going to happen.

I think we’re talking about two quite distinct issues here.The first is about teaching kids how to say no today in order to save for tomorrow.The second is to give New Zealanders the financial know-how to be able to

make good decisions about what to do with their savings.So, given that we are on a mission to improve New Zealanders’ level of

financial literacy, how do we rate now?Well, not too bad it seems. The benchmark/gauge of financial literacy in New Zealand is the ANZ

Retirement Commission Survey. This survey was first carried out in 2006 and again more recently in 2009. It was conducted by Colmar Brunton and involved one-hour interviews with more than 850 people, who were asked 42 questions testing their financial knowledge, and 51 questions on attitudes and behaviours.

Diana Crossan, in her role as Retirement Commissioner, is pleased with the improvement observed since the original survey in 2006.

“It’s great news that overall 43 per cent of New Zealanders are now scoring highly on financial knowledge, and that women and low income households are among the groups with the biggest improvements.”

Crossan also commented that “the survey shows that there has been little improvement in the past three years in the number of New Zealanders with the lowest level of financial knowledge. It’s going to take a concerted effort to lift the knowledge of this group. Perhaps this survey demonstrates that a basic level of numeracy and literacy is required, on which to build strong financial knowledge”.

Enter the role of our education system. Teaching kids while they are still at school is one area our government is concentrating on, and they are not alone. With $10 million allocated for 2011–2014 for ‘helping our kids understand

finances’, Australia is one of the leaders in taking financial literacy education into its schools. The old ‘three Rs’ are being augmented with the ‘Three Cs’: credit card debt, compound interest and cell phone plans.

One of the biggest challenges in introducing financial literacy to the school curriculum is that many teachers don’t feel confident teaching it.

A joint venture between Massey University and Westpac Bank has led to the recent launch of the NZ Centre for Personal Financial Education. This centre has designed a certificate programme for Personal Financial Educators in an effort to teach the teachers.

Visa has also come to the party and is funding a pilot programme of 15 tutors from Whitireia Polytechnic in Porirua to attend an advanced course that will develop the content and skills they need to deliver financial education. The course aims to improve the financial planning and management advice deliv-ered to New Zealand students.

“This pilot programme provides a unique opportunity to develop a best practice programme that can be rolled out across other tertiary education pro-viders, ultimately impacting thousands of Kiwi students,” says Ms Crossan.

Only time will tell whether these initiatives improve a) our ability to save, and b) the decisions we make about what to do with our savings.

KiwiSaver has gone a long way to improving our understanding by introduc-ing thousands of New Zealanders to the world of investing. As with all things, the best way to learn is to do. Only then can you witness firsthand the highs and lows of saving and investing.

As a financial advisor and mother of three young teenagers, I think it would be remiss of me to end this article on financial literacy without contributing my tuppence-worth of advice.

Here is my list of do’s and don’ts when it comes to managing your money:

Do• join KiwiSaver• save something (no matter how small) every time you get paid• keep a rainy day fund for unexpected costs• be aware of the Property Relationship Act and what it means for couples• diversify your investments

Don’t• impulse buy. Walk away and think about it for a day at least• “help out” friends or family by funding their bad choices• borrow money to buy things that lose value over time• expect anyone else to look after your financial security• forget about risk when evaluating a return

EVER

YDAY

O

CCAS

IONAL

SPEC

IALIS

T

Derivatives

Portfolio management

Retirement drawdown

WillsTrusts

Investing

MortgagesWorkplace Super

Saving Net worth Goal settung

Taxation

Debt management

InsuranceInterest

Budgetinge-banking

Banking Inflation Credit cards Spending

Consumer rights

NATIONAL STRATEGY FOR FINANCIAL LITERACY, AUGUST 2012

AUCKLANDLevel 9, Tower Centre 45 Queen St, PO Box 3899 Auckland 1140, New Zealand Phone 64 9 309 0463 Fax 64 9 309 4544 [email protected]

HAMILTON4th Floor, BNZ Building 354 Victoria Street PO Box 9159 Hamilton 3240, New Zealand Phone 64 7 834 6800 Fax 64 7 838 2881 [email protected]

TAURANGALevel 1, 247 Cameron Road PO Box 743 Tauranga 3140, New Zealand Phone 64 7 578 2989 Fax 64 7 577 6030 [email protected]

HAWKES BAYCnr. Hastings and Eastbourne Streets PO Box 46 Hastings 4156, New Zealand Phone 64 6 878 7004 Fax 64 6 878 0078 [email protected]

NEW PLYMOUTH109-113 Powderham Street PO Box 146 New Plymouth 4340, New Zealand Phone 64 6 757 3155 Fax 64 6 757 5081 [email protected]

STRATFORD78 Miranda Street PO Box 82 Stratford 4352, New Zealand Phone 64 6 765 6019 Fax 64 6 765 8342 [email protected]

CHRISTCHURCHAMI House 116 Riccarton Road, PO Box 8039 Christchurch 8440, New Zealand Phone 64 3 343 0599 Fax 64 3 348 0186 [email protected]

www.staplesrodway.co.nz