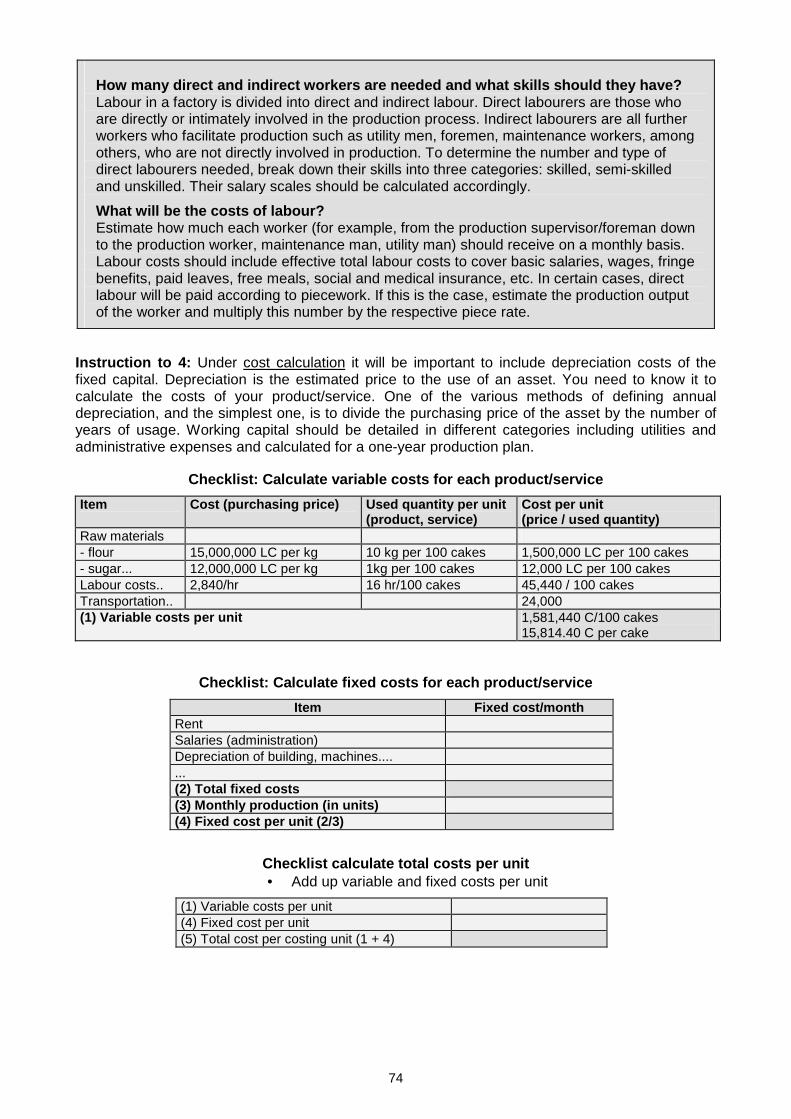

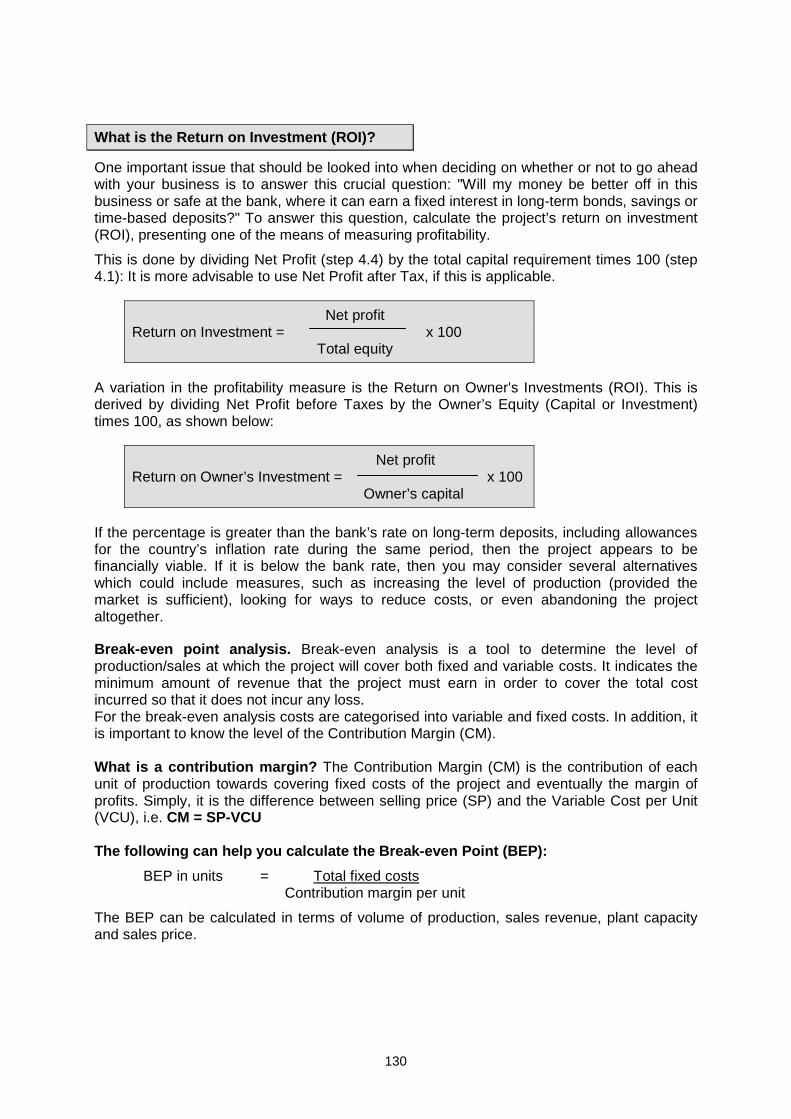

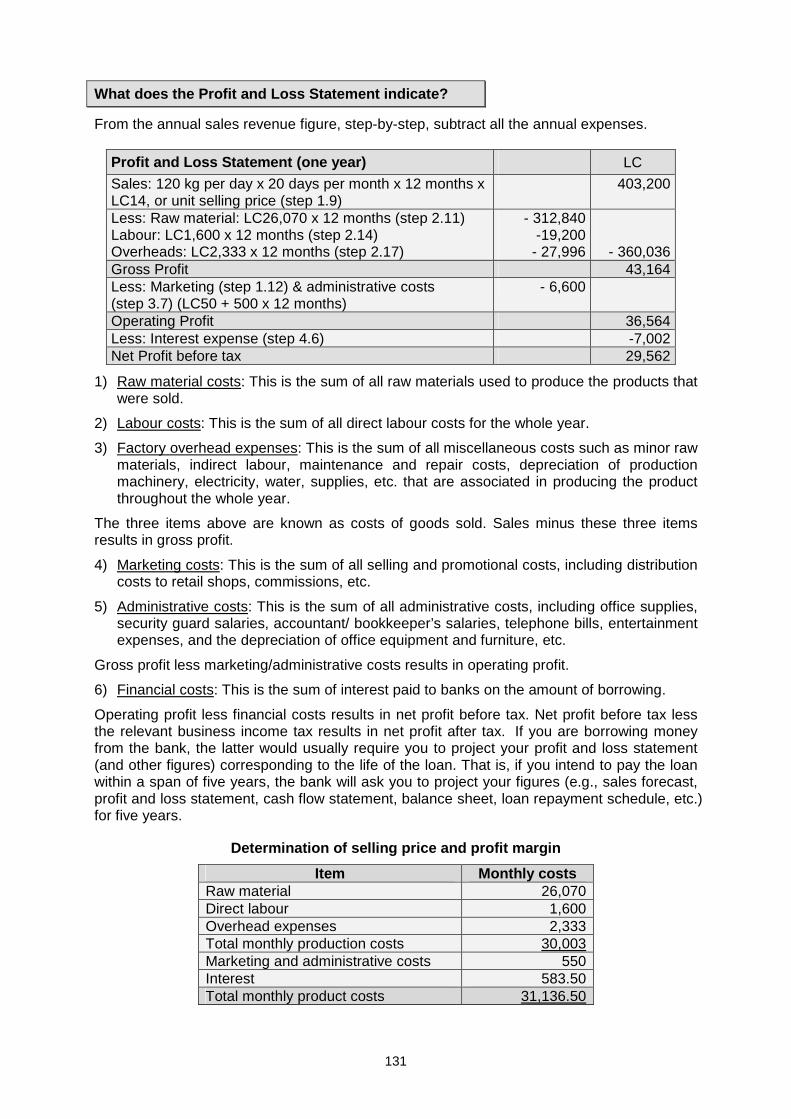

Embed Size (px)

Citation preview

Dieter Gagel

Start and Improve your Business The all-in-one business manual for start-ups and entrepreneurs in developing countries: Business idea generation, Market research, Equipment supply, Accounting and Cost calculation, Business planning, Management, Financing, Marketing, Import-Export, International trade and Tendering

Germany 2008

Business Development Services (BDS) Forum www.bds-forum.net

Production and publishing: Books on Demand GmBH, Norderstedt, www.bod.de

Original available on: ISBN 978-3-8370-5916-8

Business Development Services in Development Cooperation

www.bds-forum.net

Toolkit

Start and Improve your Business

Business idea - Market research - Equipment supply - Accounting

Business planning - Management - Financing - Marketing

Export promotion - Trade fairs - Tenders

Dieter Gagel Heidelberg, Germany 2008

Bibliographische Information der Deutschen National bibliothek Die Deutsche Nationalbibliothek verzeichnet diese Publikation in der Deutschen Nationalbibliographie; detaillierte bibilographische Daten sind im Internet über http://dnb.d-nb.de abrufbar. Bibliographic Information of the German National Li brary The German National Library registers this publication in the German National Bibliography; detailled bibliographic data are available on http://dnb.d-nb.de.

Impressum

© 2008 Dieter Gagel, author Freelance consultant [email protected] Production and publishing: Books on Demand GmBH, Norderstedt

ISBN 978-3-8370-5916-8

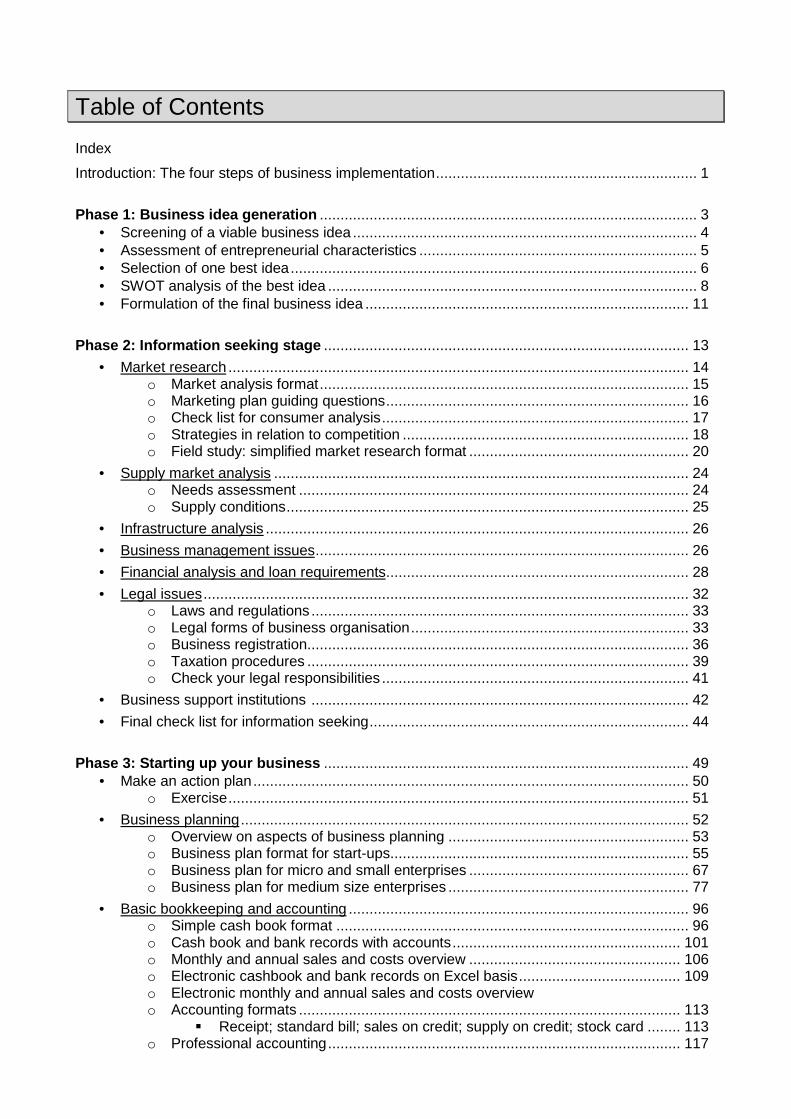

Table of Contents Index

Introduction: The four steps of business implementation............................................................... 1

Phase 1: Business idea generation ........................................................................................... 3 • Screening of a viable business idea ................................................................................... 4 • Assessment of entrepreneurial characteristics ................................................................... 5 • Selection of one best idea.................................................................................................. 6 • SWOT analysis of the best idea ......................................................................................... 8 • Formulation of the final business idea .............................................................................. 11

Phase 2: Information seeking stage ........................................................................................ 13

• Market research ............................................................................................................... 14 o Market analysis format......................................................................................... 15 o Marketing plan guiding questions......................................................................... 16 o Check list for consumer analysis.......................................................................... 17 o Strategies in relation to competition ..................................................................... 18 o Field study: simplified market research format ..................................................... 20

• Supply market analysis .................................................................................................... 24 o Needs assessment .............................................................................................. 24 o Supply conditions................................................................................................. 25

• Infrastructure analysis ...................................................................................................... 26

• Business management issues.......................................................................................... 26

• Financial analysis and loan requirements......................................................................... 28

• Legal issues..................................................................................................................... 32 o Laws and regulations ........................................................................................... 33 o Legal forms of business organisation................................................................... 33 o Business registration............................................................................................ 36 o Taxation procedures ............................................................................................ 39 o Check your legal responsibilities .......................................................................... 41

• Business support institutions ........................................................................................... 42

• Final check list for information seeking............................................................................. 44

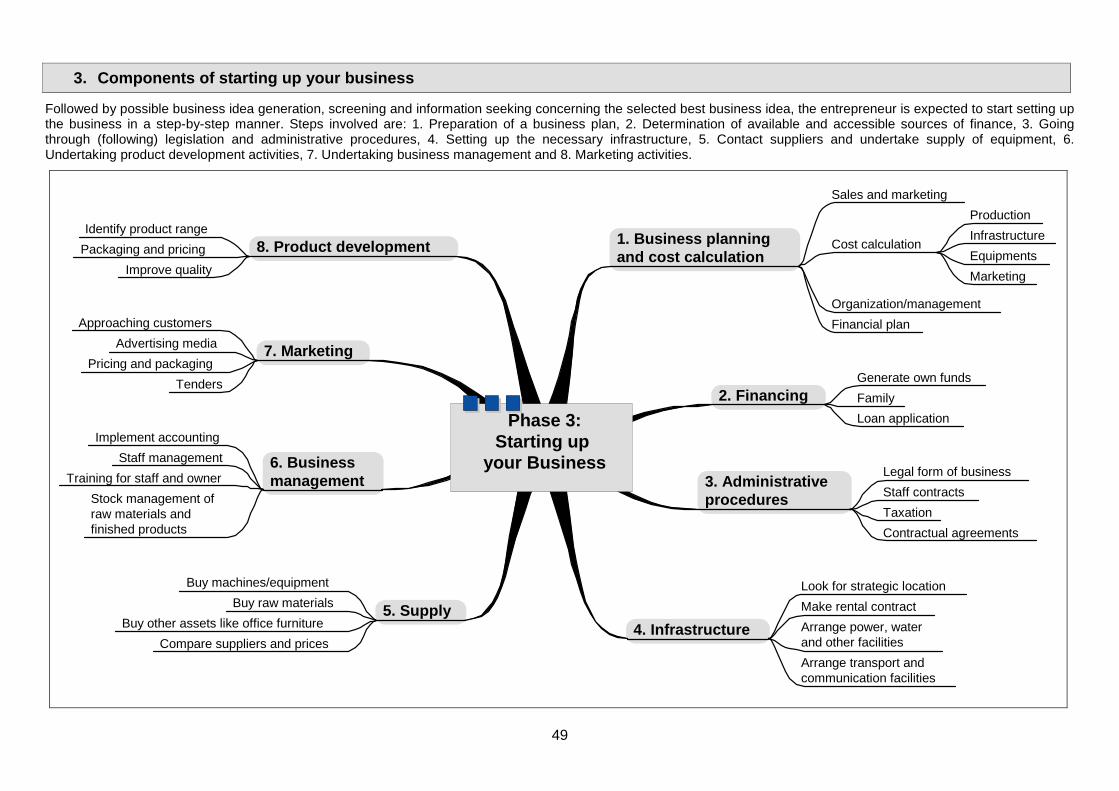

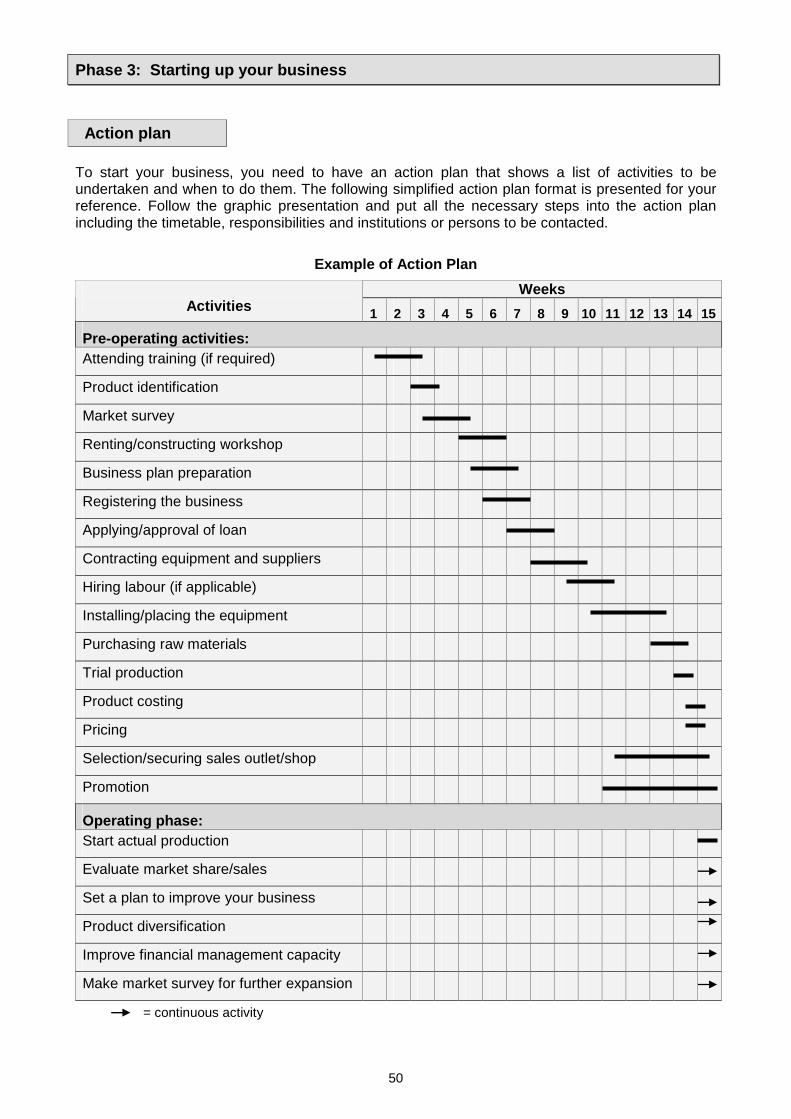

Phase 3: Starting up your business ........................................................................................ 49 • Make an action plan......................................................................................................... 50

o Exercise............................................................................................................... 51

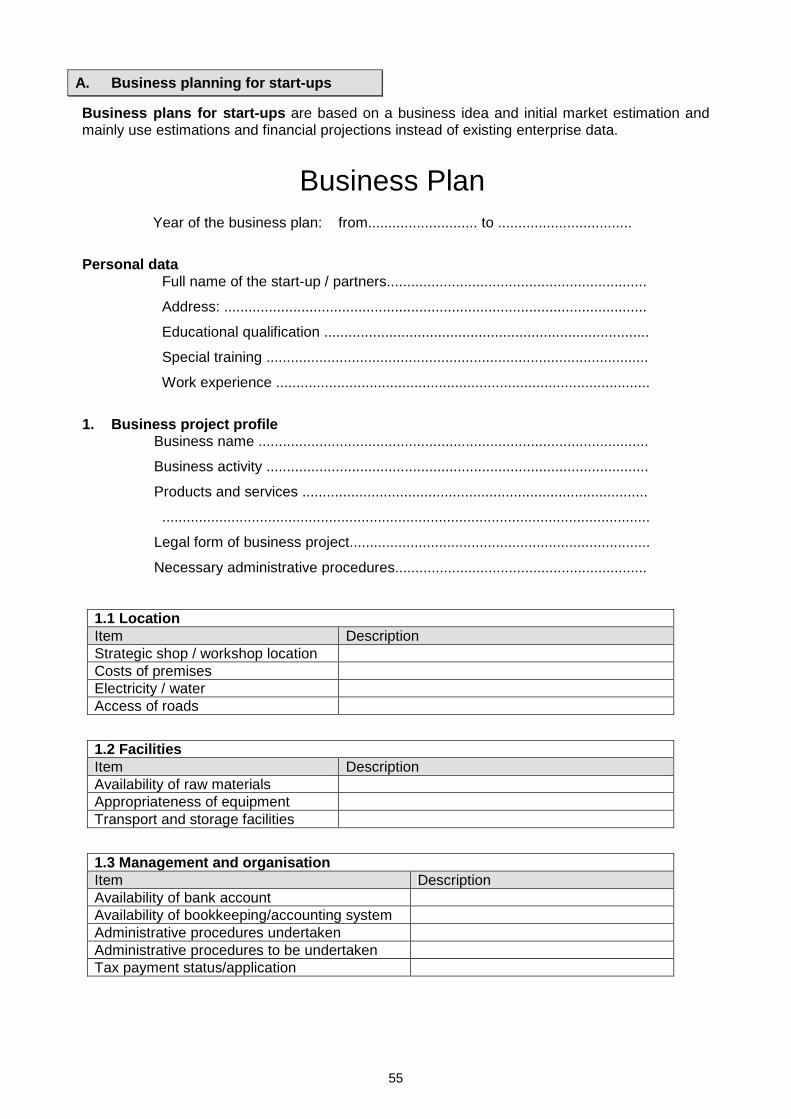

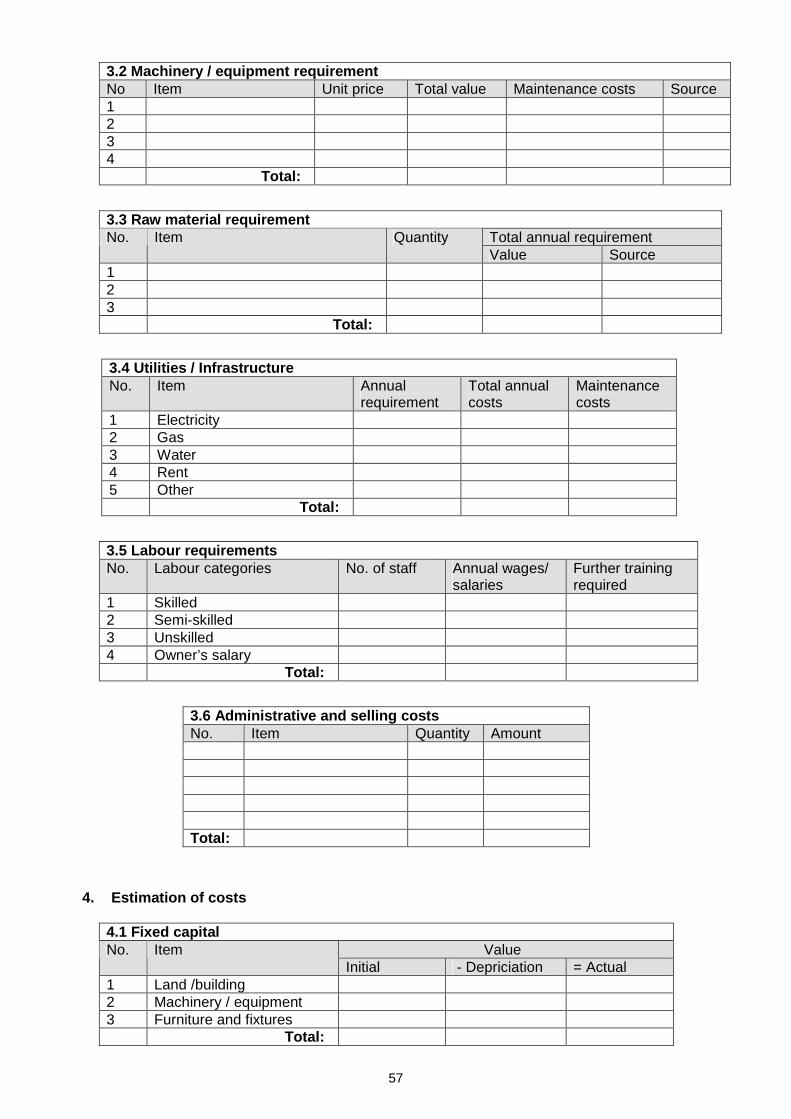

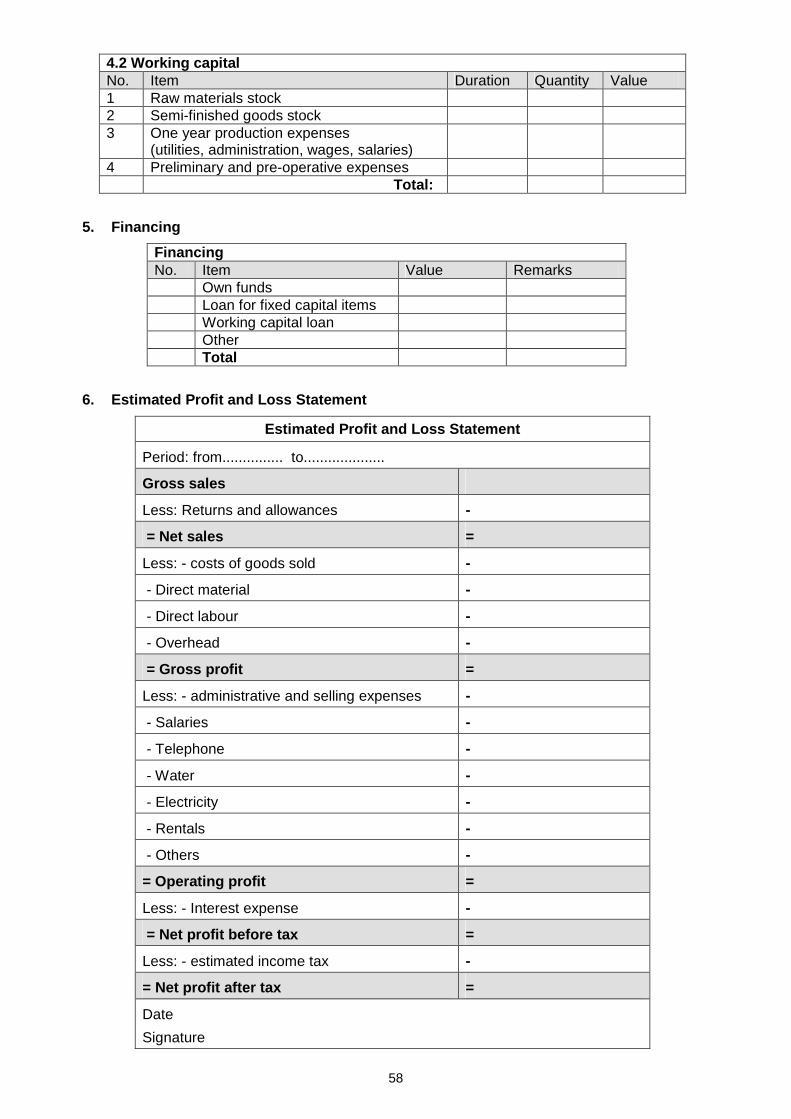

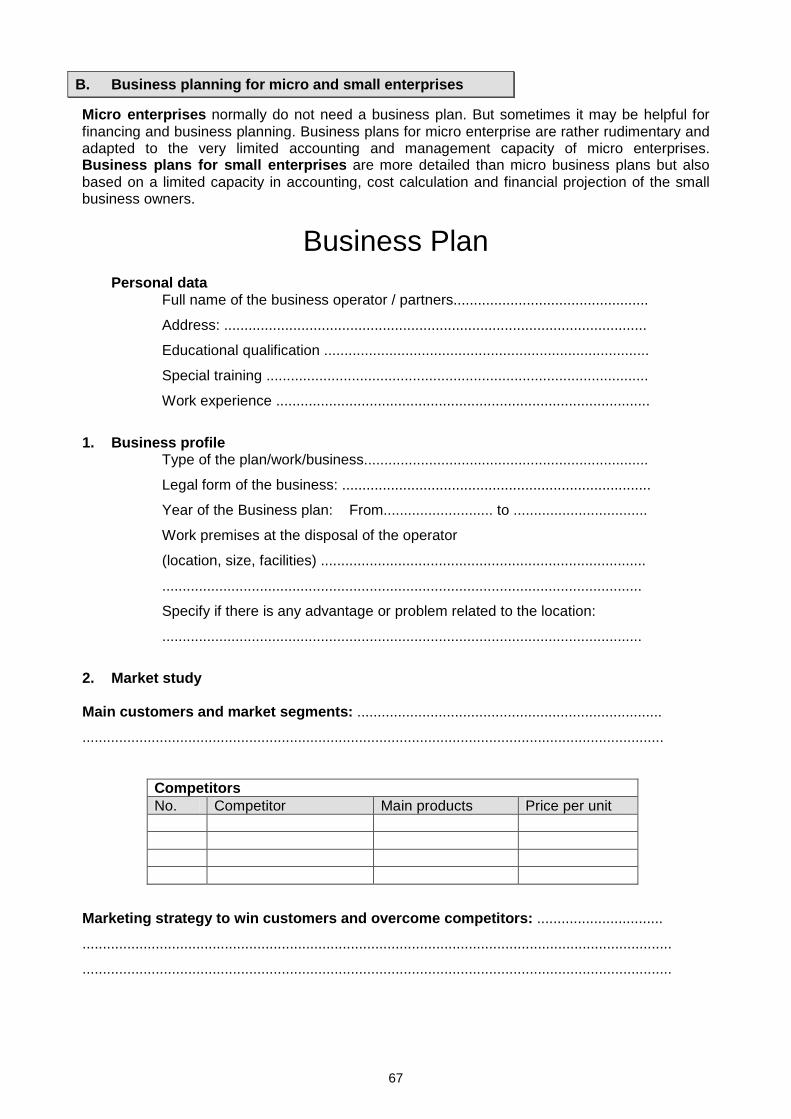

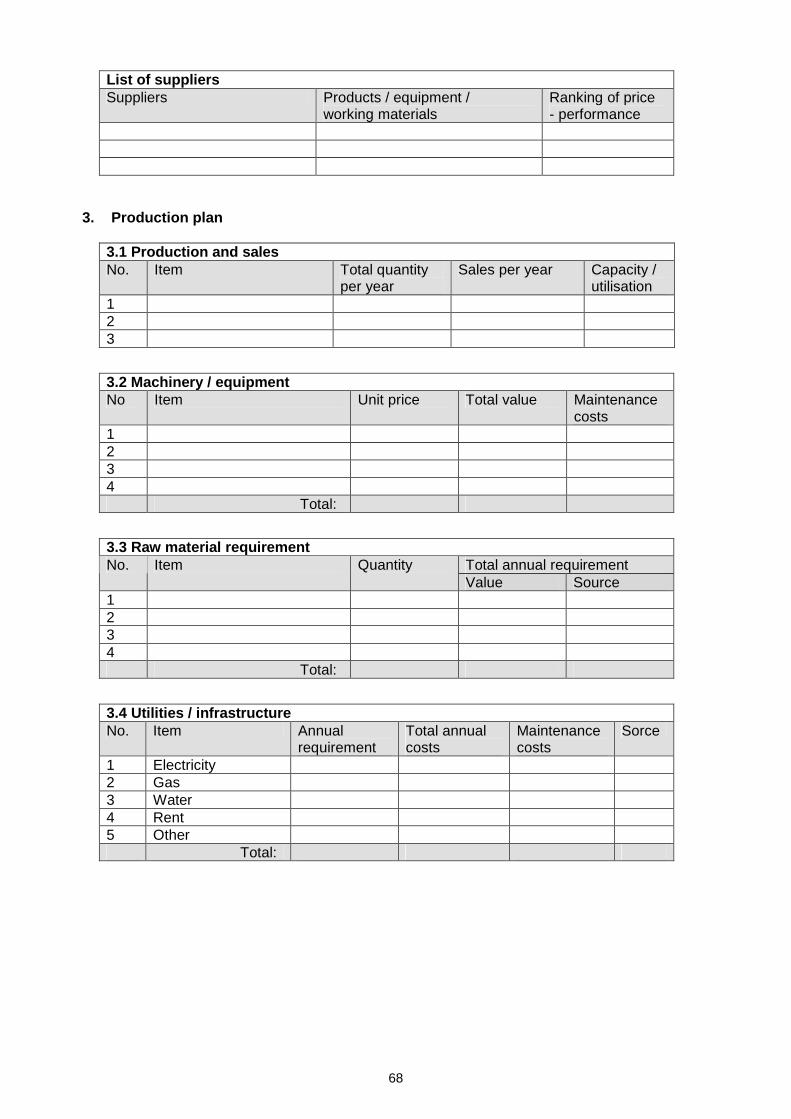

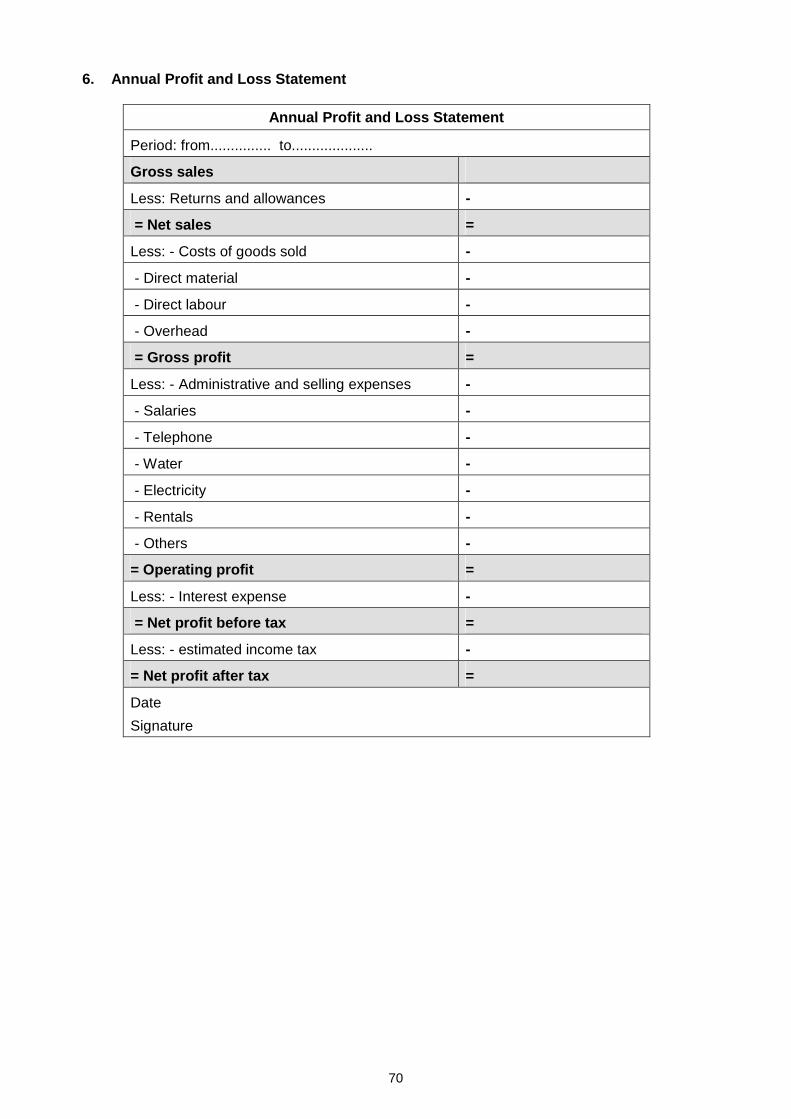

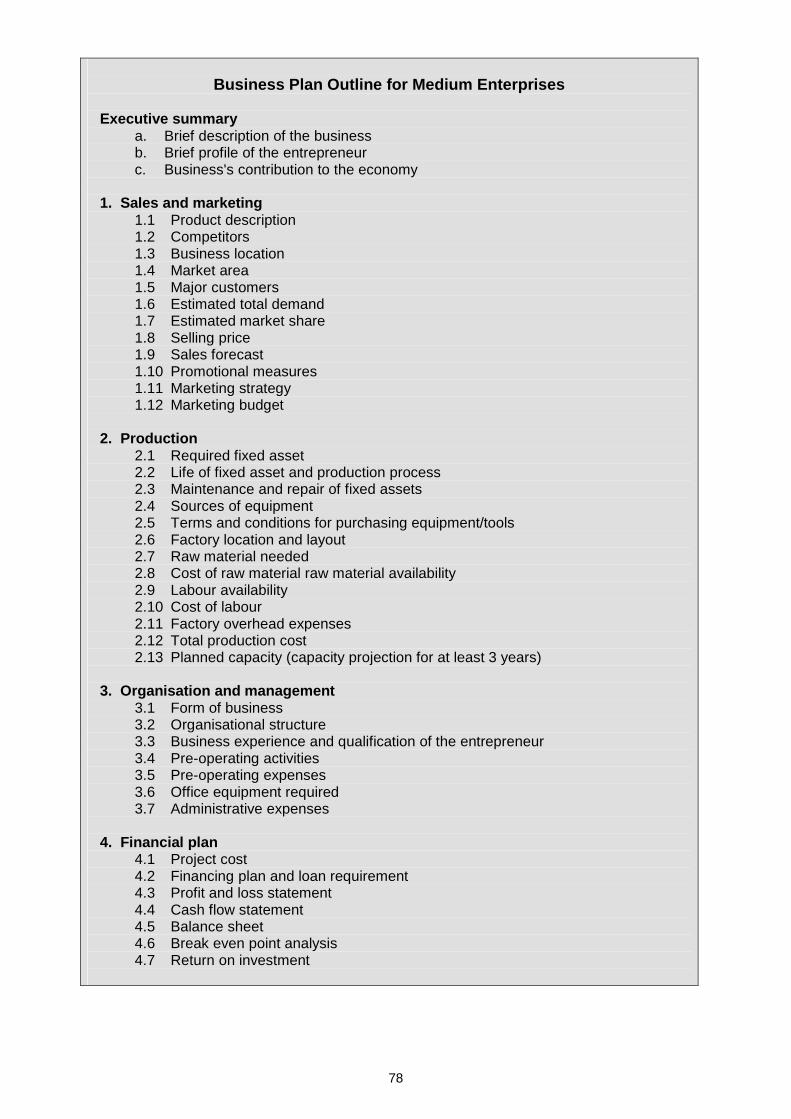

• Business planning............................................................................................................ 52 o Overview on aspects of business planning .......................................................... 53 o Business plan format for start-ups........................................................................ 55 o Business plan for micro and small enterprises ..................................................... 67 o Business plan for medium size enterprises .......................................................... 77

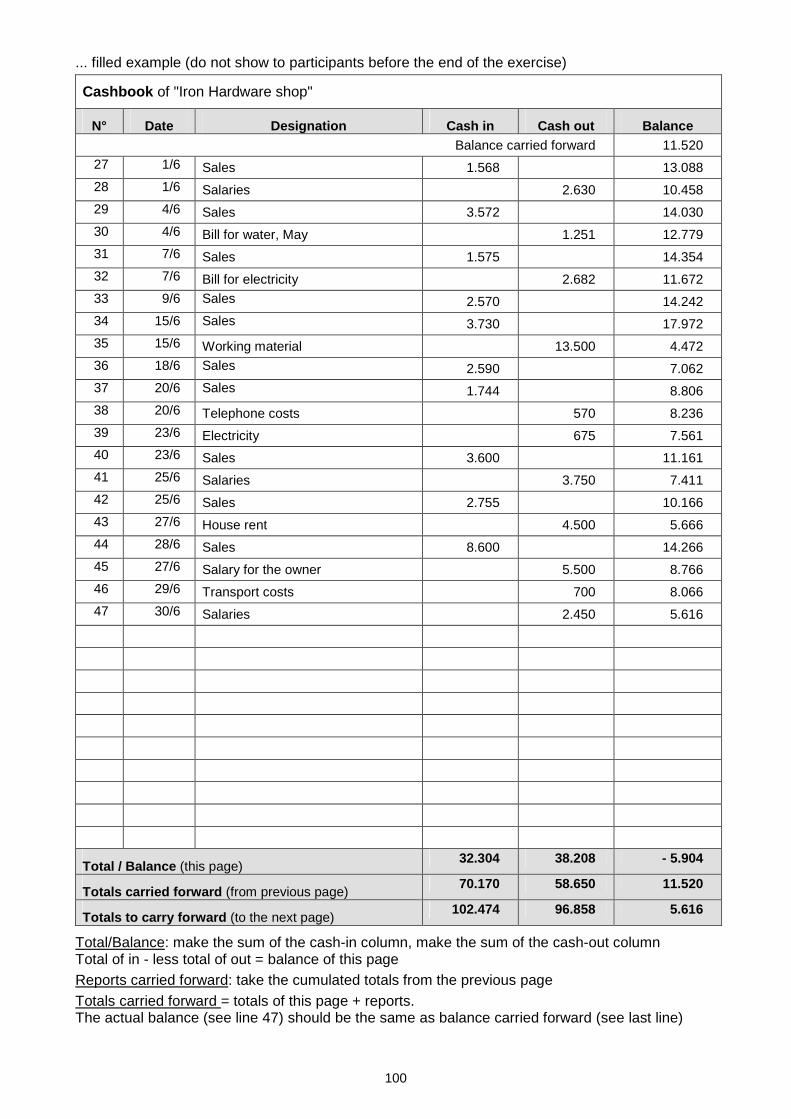

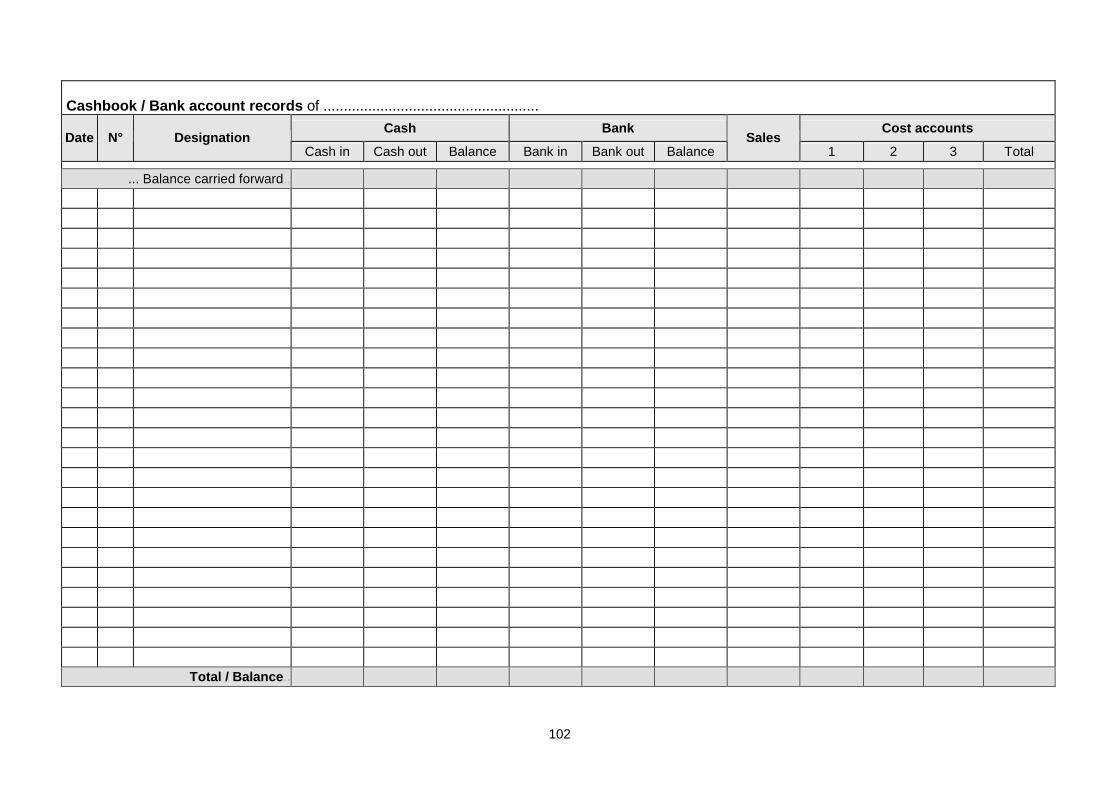

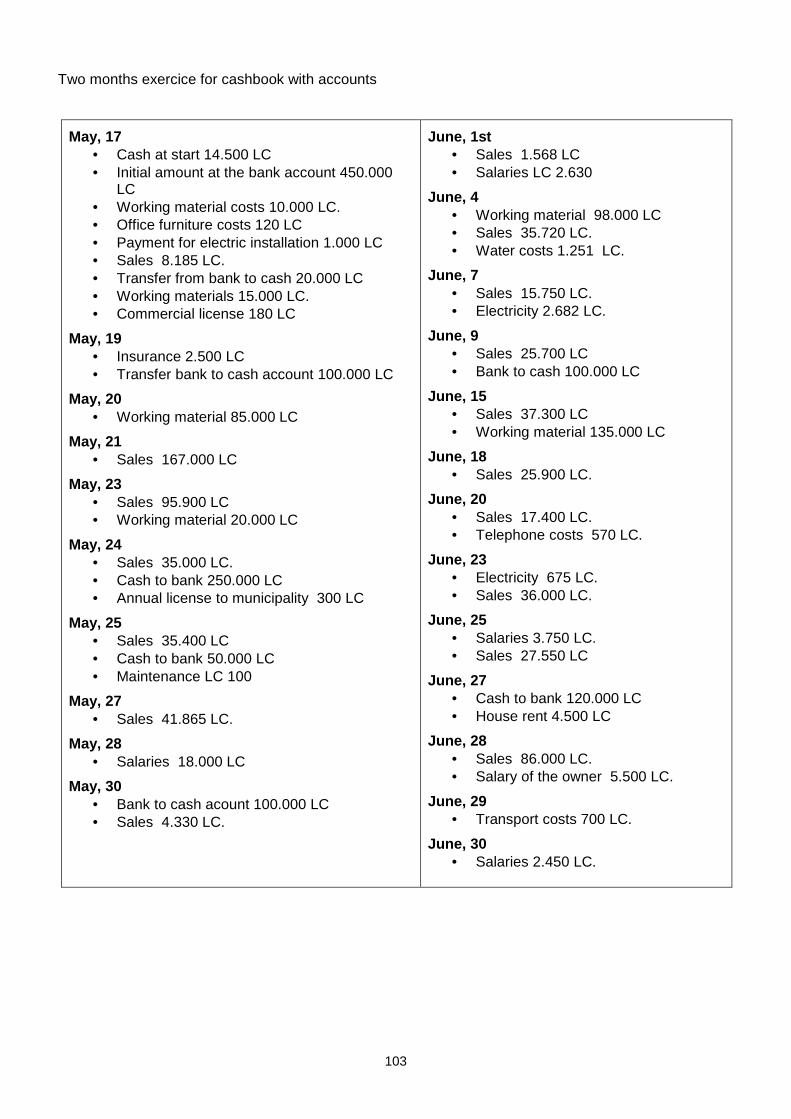

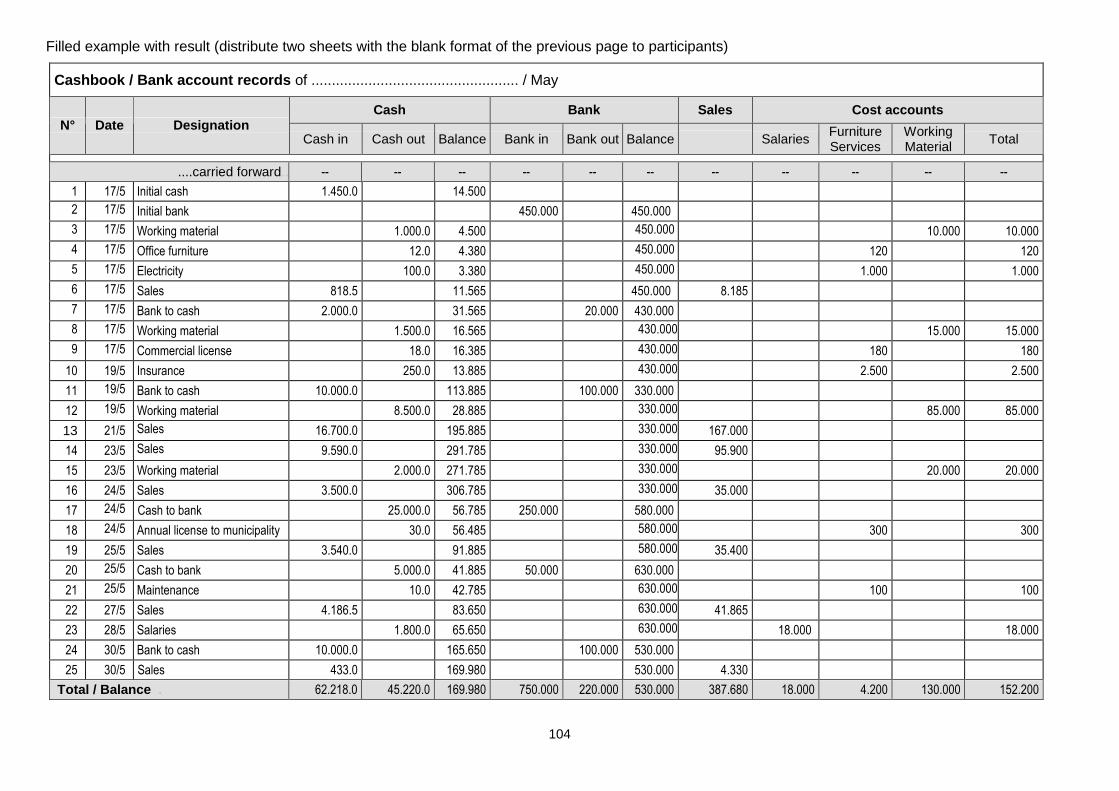

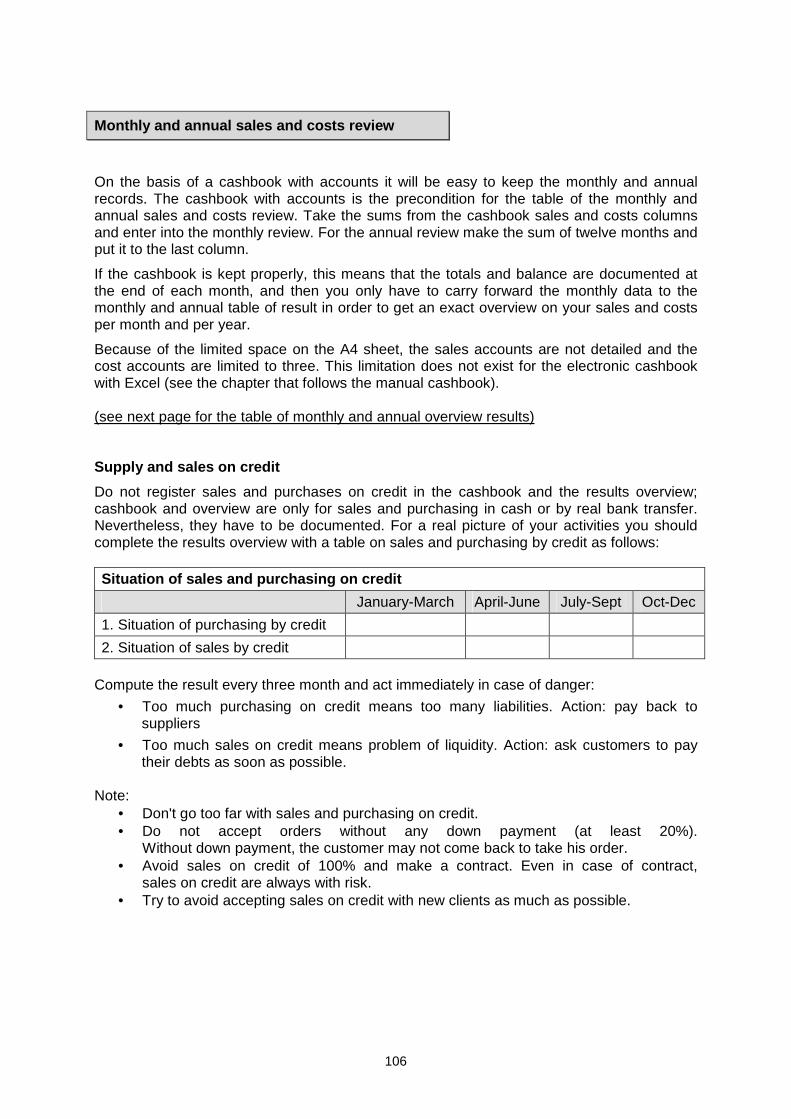

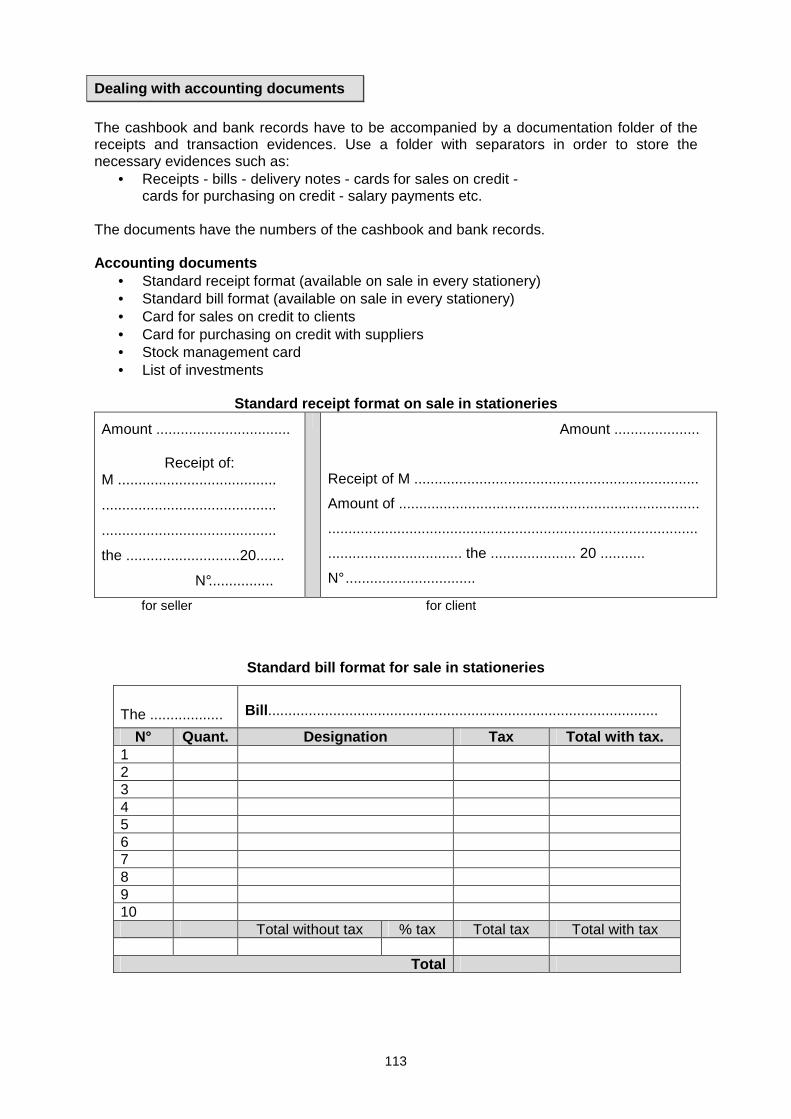

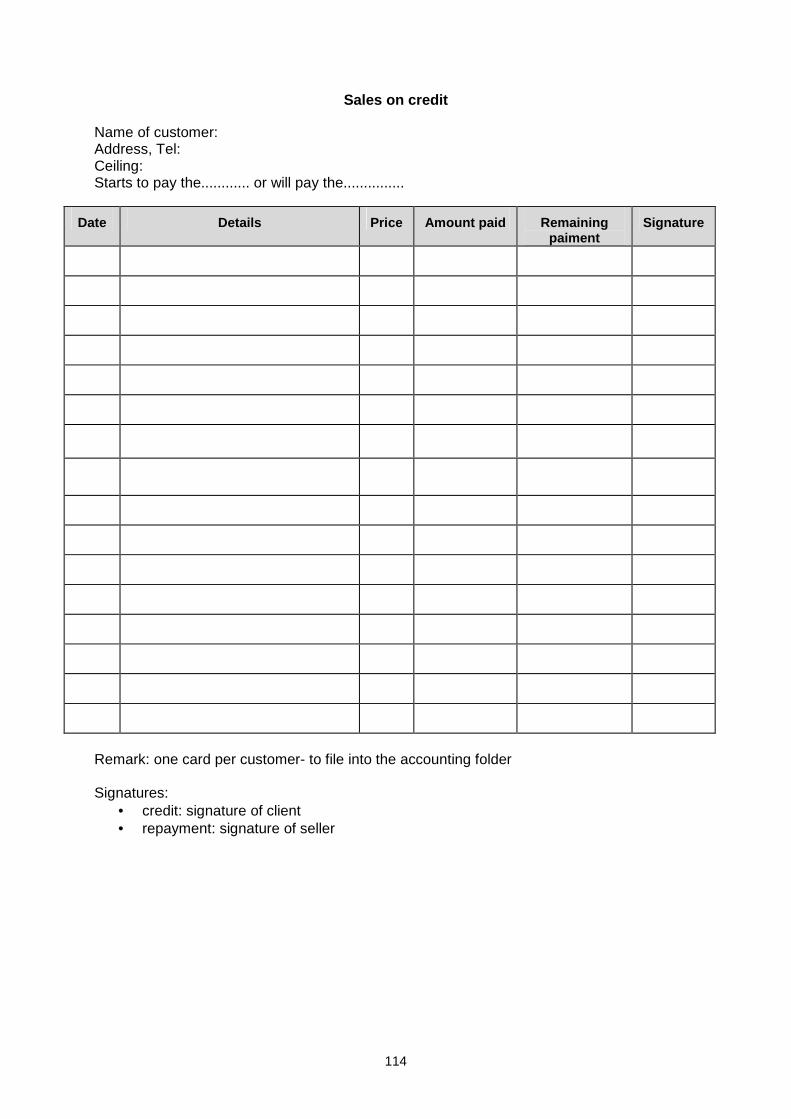

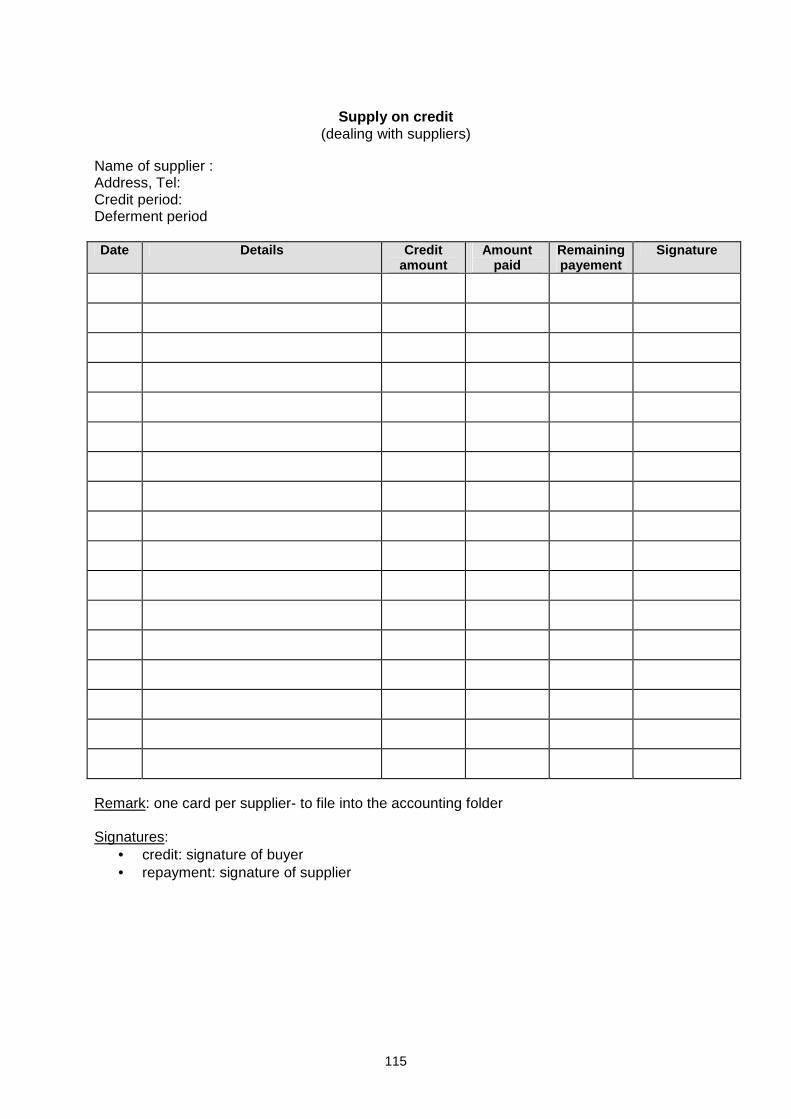

• Basic bookkeeping and accounting .................................................................................. 96 o Simple cash book format ..................................................................................... 96 o Cash book and bank records with accounts....................................................... 101 o Monthly and annual sales and costs overview ................................................... 106 o Electronic cashbook and bank records on Excel basis....................................... 109 o Electronic monthly and annual sales and costs overview o Accounting formats ............................................................................................ 113

� Receipt; standard bill; sales on credit; supply on credit; stock card ........ 113 o Professional accounting..................................................................................... 117

• Cost calculation ........................................................................................................... 118

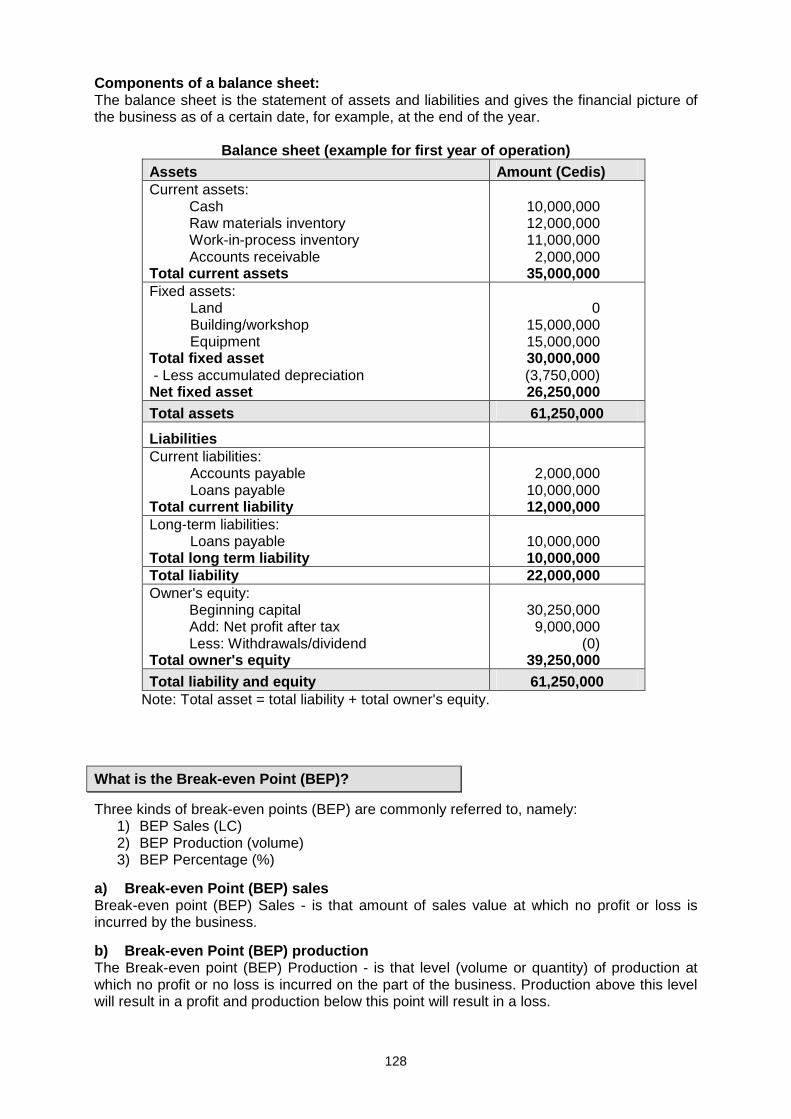

o Cost components............................................................................................... 118 o Cash flow statement .......................................................................................... 125 o Balance sheet .................................................................................................... 127 o Break even point................................................................................................ 128 o Profit and loss statement ................................................................................... 131

• Financing ....................................................................................................................... 132 o Constraints of access to finance ........................................................................ 132 o Financial records ............................................................................................... 134 o Cash flow........................................................................................................... 135 o Personal qualification......................................................................................... 135 o Costs and investments....................................................................................... 136 o Sources of finance ............................................................................................. 136 o Guide for business consultants on how to facilitate access to finance................ 138 o Loan application procedure and credit assessment............................................ 138 o Categories of financial institutions...................................................................... 142

• Administrative procedures.............................................................................................. 144 • Infrastructure (location, building, transport facilities)....................................................... 145 • Suppliers........................................................................................................................ 145 • Business management................................................................................................... 146

• Marketing strategies - the "4P Approach": Product, Price, Place, Promotion .................. 147 o Product development ......................................................................................... 148 o Managing prices ................................................................................................ 150 o Strategic location .............................................................................................. 152 o Promotion .......................................................................................................... 153

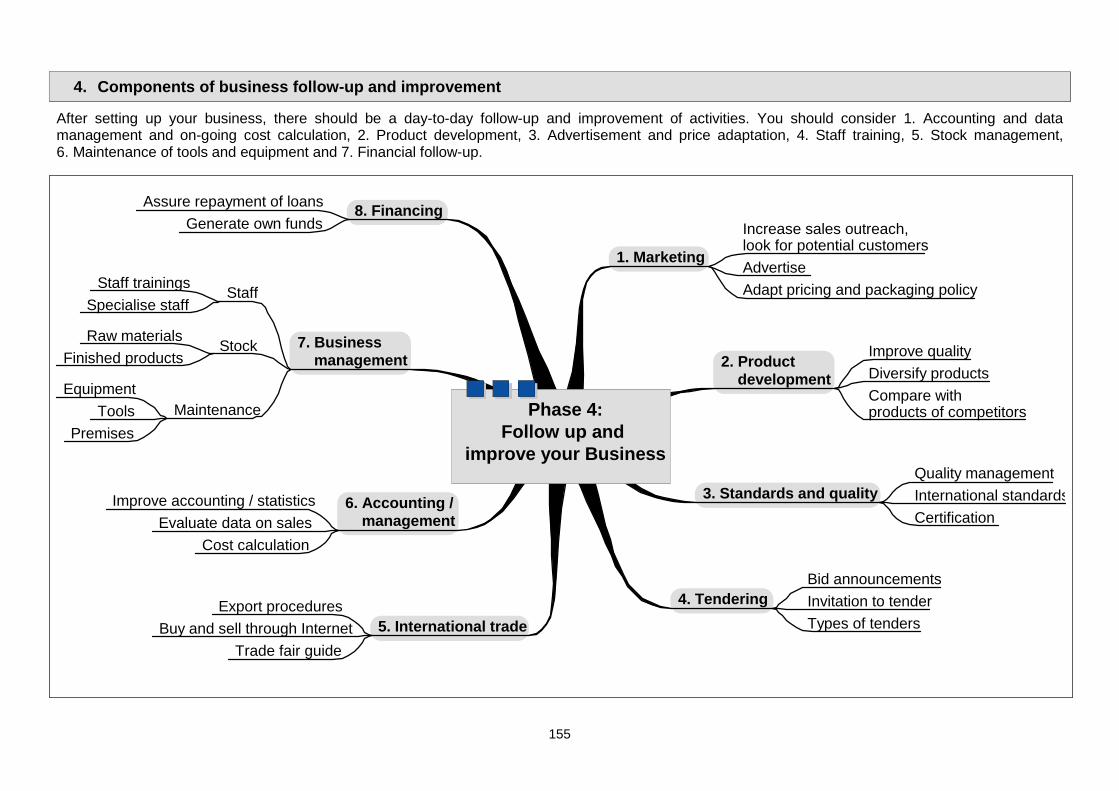

Phase 4: Follow up and improve your business ................................................................... 155

• Improve your marketing activities ................................................................................... 156 o Product development ........................................................................................ 157 o Standards and quality ........................................................................................ 160 o Participation on tenders ..................................................................................... 178 o International trade promotion ............................................................................. 191

� Exporting................................................................................................ 191 � E-commerce in Internet .......................................................................... 207 � Trade fairs and exhibitions ..................................................................... 209

• Evaluating sales and cost structure................................................................................ 216 o Check your accounting system .......................................................................... 216 o Data management ............................................................................................. 218

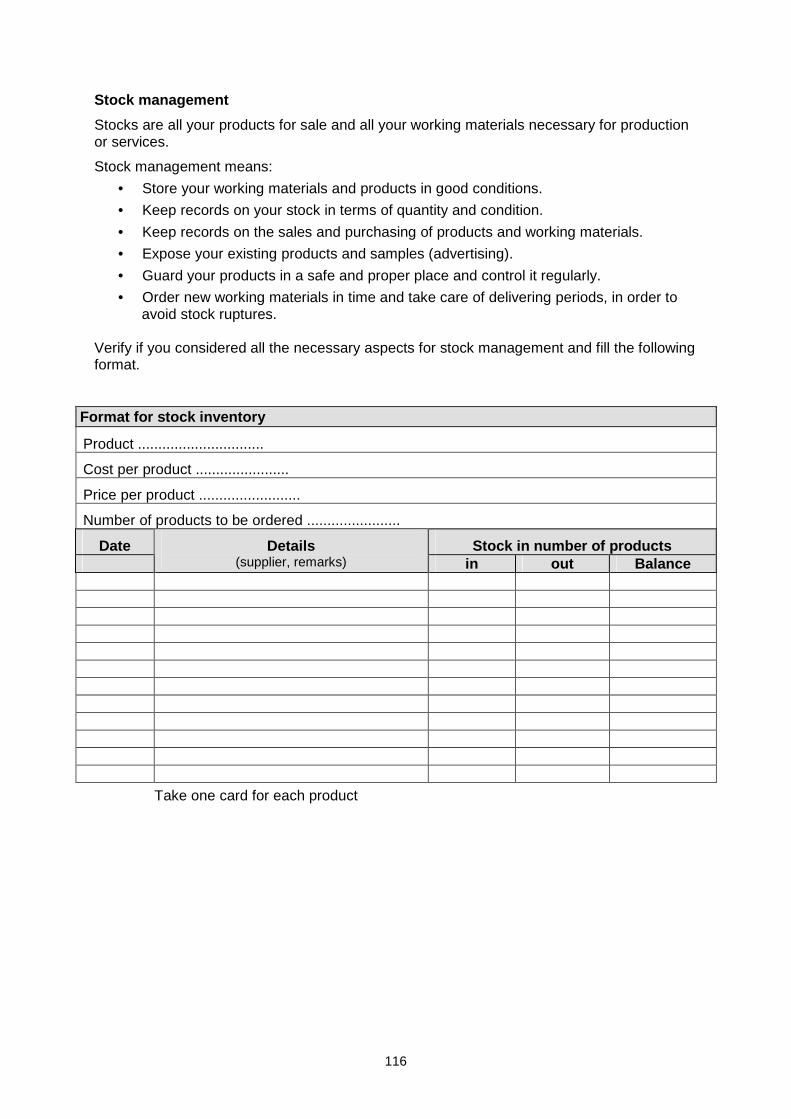

• Staff management.......................................................................................................... 219 • Stock management ........................................................................................................ 219 • Maintenance .................................................................................................................. 220 • Financing ....................................................................................................................... 221 • Check list: Summary of the follow-up phase................................................................... 222

Reformulation of your initial project idea (exercise) ............................................................. 223 Annexes

• Extended market research format • Standard loan application format • Export- and action-oriented workshop on submission to e-market places

and website publishing for export-oriented entrepreneurs • Business portals and learning platforms in Internet

1

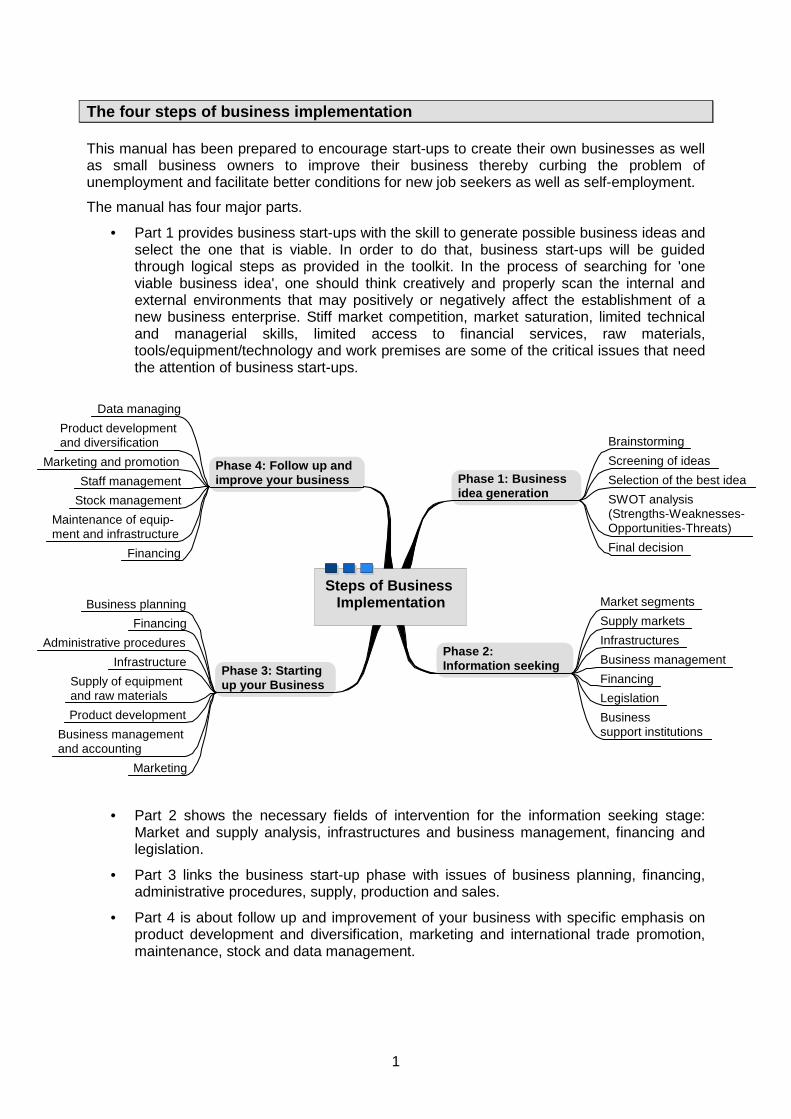

The four steps of business implementation This manual has been prepared to encourage start-ups to create their own businesses as well as small business owners to improve their business thereby curbing the problem of unemployment and facilitate better conditions for new job seekers as well as self-employment.

The manual has four major parts.

• Part 1 provides business start-ups with the skill to generate possible business ideas and select the one that is viable. In order to do that, business start-ups will be guided through logical steps as provided in the toolkit. In the process of searching for 'one viable business idea', one should think creatively and properly scan the internal and external environments that may positively or negatively affect the establishment of a new business enterprise. Stiff market competition, market saturation, limited technical and managerial skills, limited access to financial services, raw materials, tools/equipment/technology and work premises are some of the critical issues that need the attention of business start-ups.

Phase 1: Business idea generation

Phase 4: Follow up andimprove your business

Phase 2: Information seekingPhase 3: Starting

up your Business

Steps of Business Implementation

Brainstorming

Screening of ideas

Selection of the best idea

SWOT analysis (Strengths-Weaknesses-Opportunities-Threats)

Final decision

Data managing

Product development and diversification

Marketing and promotion

Staff management

Stock management

Maintenance of equip-ment and infrastructure

Financing

Market segments

Supply markets

Infrastructures

Business management

Financing

Legislation

Business support institutions

Business planning

Financing

Administrative procedures

Infrastructure

Supply of equipment and raw materials

Product development

Business management and accounting

Marketing

• Part 2 shows the necessary fields of intervention for the information seeking stage: Market and supply analysis, infrastructures and business management, financing and legislation.

• Part 3 links the business start-up phase with issues of business planning, financing, administrative procedures, supply, production and sales.

• Part 4 is about follow up and improvement of your business with specific emphasis on product development and diversification, marketing and international trade promotion, maintenance, stock and data management.

2

3

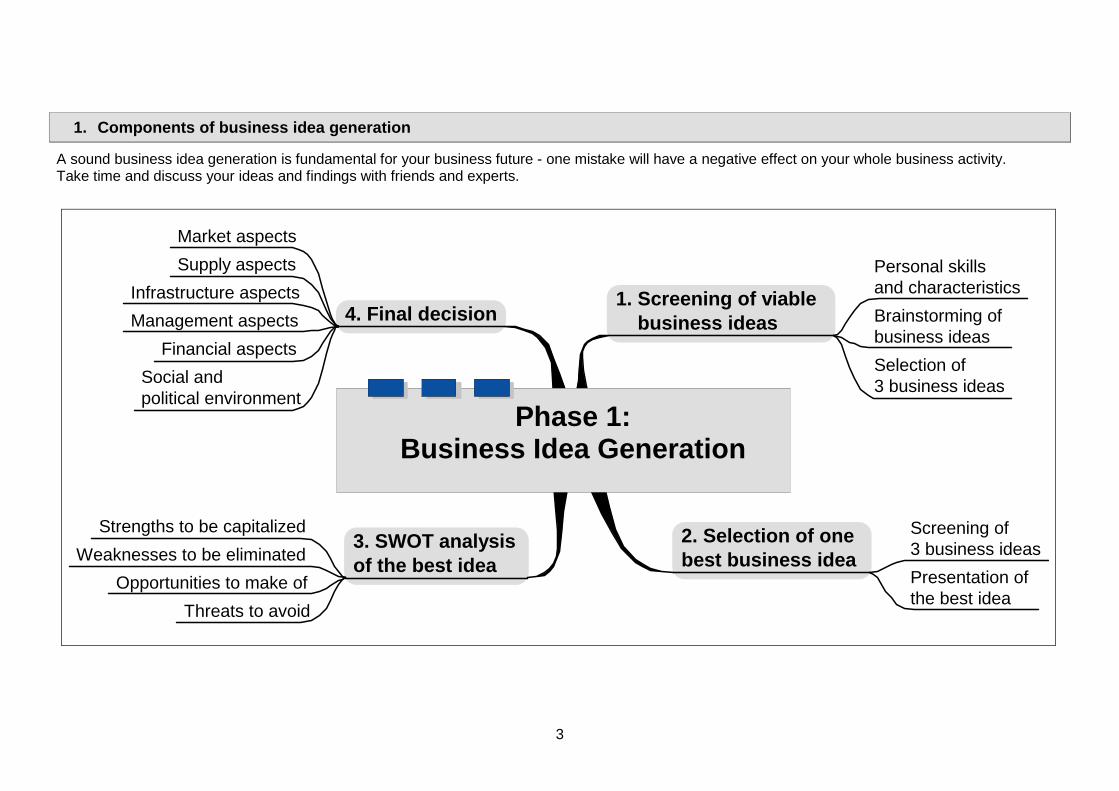

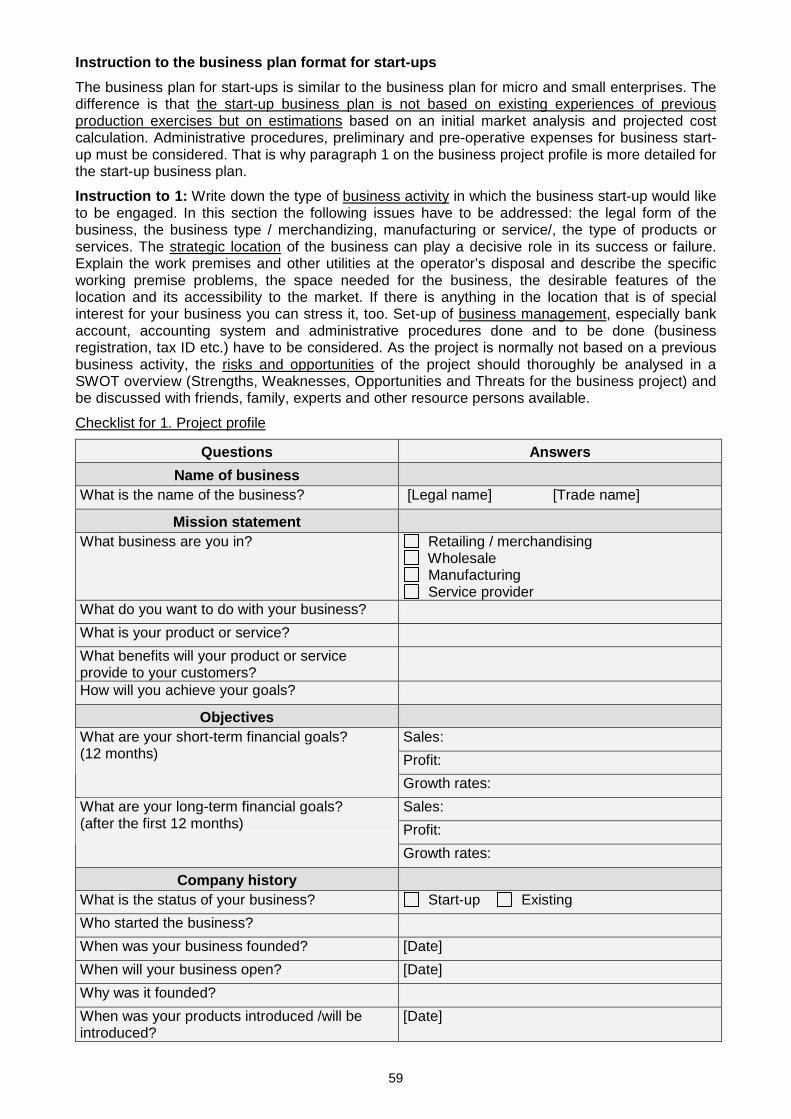

1. Components of business idea generation

A sound business idea generation is fundamental for your business future - one mistake will have a negative effect on your whole business activity. Take time and discuss your ideas and findings with friends and experts.

1. Screening of viable business ideas

2. Selection of one best business idea

4. Final decision

3. SWOT analysis of the best idea

Phase 1:Business Idea Generation

Personal skills and characteristics

Brainstorming of business ideas

Selection of 3 business ideas

Screening of 3 business ideas

Presentation of the best idea

Market aspects

Supply aspects

Infrastructure aspects

Management aspects

Financial aspects

Social and political environment

Strengths to be capitalized

Weaknesses to be eliminated

Opportunities to make of

Threats to avoid

4

Phase 1: Business idea generation

1.1 Screening of a viable business idea

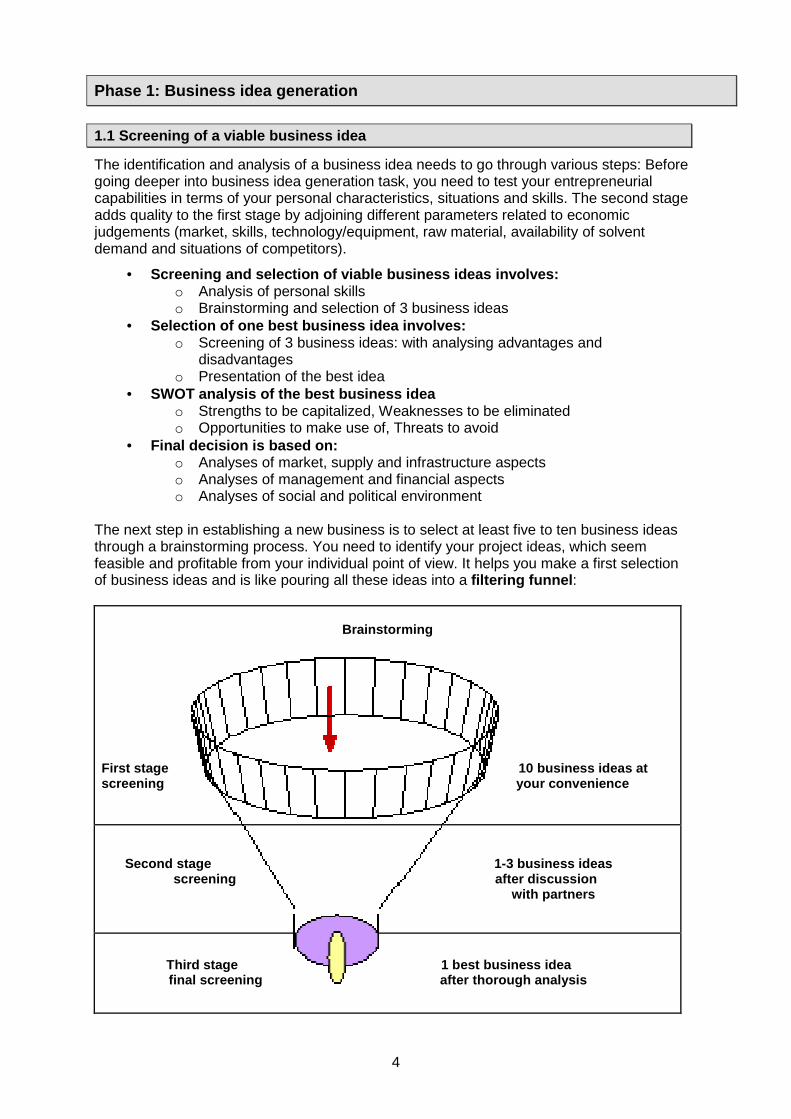

The identification and analysis of a business idea needs to go through various steps: Before going deeper into business idea generation task, you need to test your entrepreneurial capabilities in terms of your personal characteristics, situations and skills. The second stage adds quality to the first stage by adjoining different parameters related to economic judgements (market, skills, technology/equipment, raw material, availability of solvent demand and situations of competitors).

• Screening and selection of viable business ideas in volves: o Analysis of personal skills o Brainstorming and selection of 3 business ideas

• Selection of one best business idea involves: o Screening of 3 business ideas: with analysing advantages and

disadvantages o Presentation of the best idea

• SWOT analysis of the best business idea o Strengths to be capitalized, Weaknesses to be eliminated o Opportunities to make use of, Threats to avoid

• Final decision is based on: o Analyses of market, supply and infrastructure aspects o Analyses of management and financial aspects o Analyses of social and political environment

The next step in establishing a new business is to select at least five to ten business ideas through a brainstorming process. You need to identify your project ideas, which seem feasible and profitable from your individual point of view. It helps you make a first selection of business ideas and is like pouring all these ideas into a filtering funnel :

Brainstorming

First stage 10 business ideas at screening your convenience

Second stage 1-3 business ideas screening after discussi on with partners

Third stage 1 best business idea final screening after thorough analysis

5

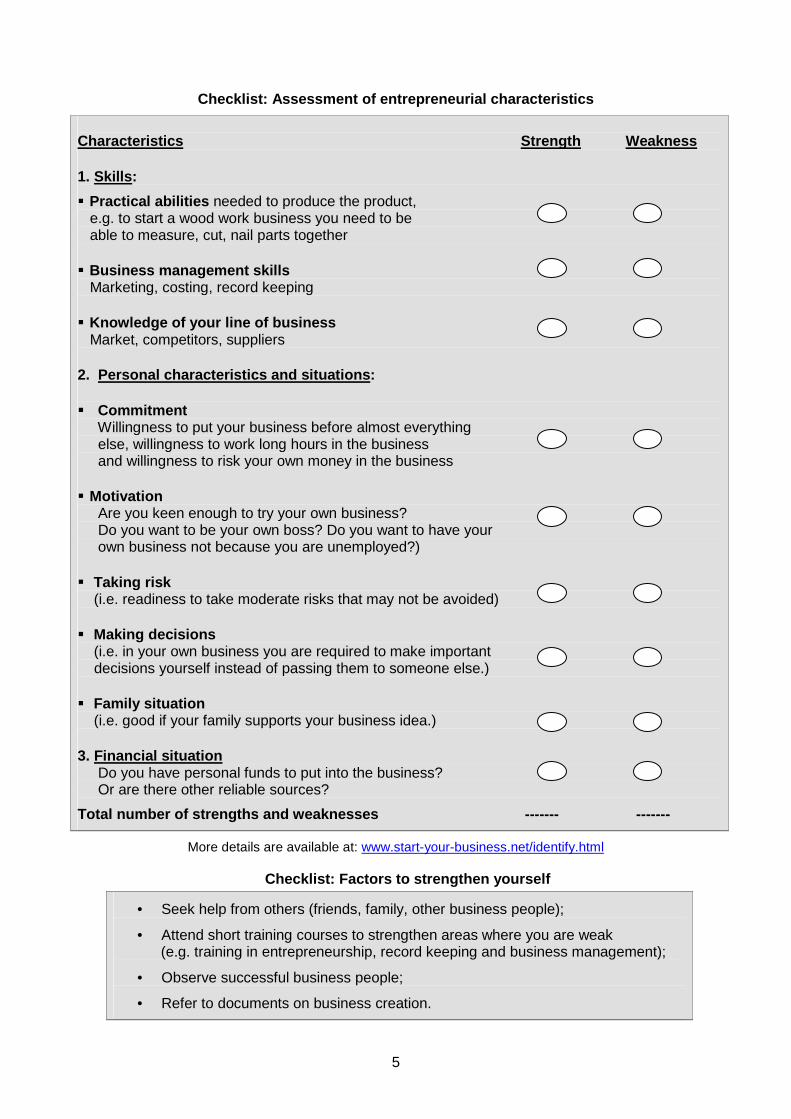

Checklist: Assessment of entrepreneurial characteri stics

Characteristics Strength Weakness

1. Skills :

� Practical abilities needed to produce the product, e.g. to start a wood work business you need to be able to measure, cut, nail parts together

� Business management skills Marketing, costing, record keeping

� Knowledge of your line of business Market, competitors, suppliers

2. Personal characteristics and situations :

� Commitment Willingness to put your business before almost everything else, willingness to work long hours in the business and willingness to risk your own money in the business

� Motivation Are you keen enough to try your own business? Do you want to be your own boss? Do you want to have your own business not because you are unemployed?)

� Taking risk (i.e. readiness to take moderate risks that may not be avoided)

� Making decisions (i.e. in your own business you are required to make important decisions yourself instead of passing them to someone else.)

� Family situation (i.e. good if your family supports your business idea.)

3. Financial situation Do you have personal funds to put into the business? Or are there other reliable sources?

Total number of strengths and weaknesses ------- -------

More details are available at: www.start-your-business.net/identify.html

Checklist: Factors to strengthen yourself

• Seek help from others (friends, family, other business people);

• Attend short training courses to strengthen areas where you are weak (e.g. training in entrepreneurship, record keeping and business management);

• Observe successful business people;

• Refer to documents on business creation.

6

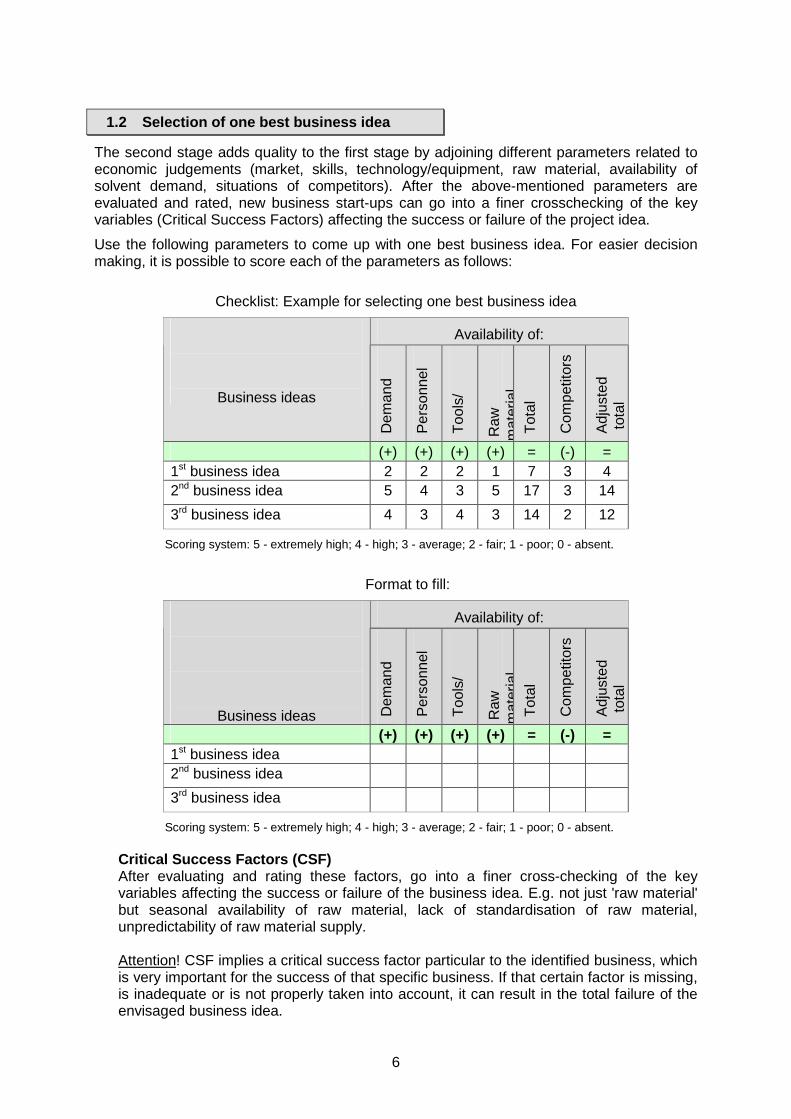

1.2 Selection of one best business idea

The second stage adds quality to the first stage by adjoining different parameters related to economic judgements (market, skills, technology/equipment, raw material, availability of solvent demand, situations of competitors). After the above-mentioned parameters are evaluated and rated, new business start-ups can go into a finer crosschecking of the key variables (Critical Success Factors) affecting the success or failure of the project idea.

Use the following parameters to come up with one best business idea. For easier decision making, it is possible to score each of the parameters as follows:

Checklist: Example for selecting one best business idea

Availability of:

Business ideas D

eman

d

Per

sonn

el

Too

ls/

Raw

m

ater

ial

Tot

al

Com

petit

ors

Adj

uste

d to

tal

(+) (+) (+) (+) = (-) = 1st business idea 2 2 2 1 7 3 4 2nd business idea 5 4 3 5 17 3 14

3rd business idea 4 3 4 3 14 2 12

Scoring system: 5 - extremely high; 4 - high; 3 - average; 2 - fair; 1 - poor; 0 - absent.

Format to fill:

Availability of:

Business ideas Dem

and

Per

sonn

el

Too

ls/

Raw

m

ater

ial

Tot

al

Com

petit

ors

Adj

uste

d to

tal

(+) (+) (+) (+) = (-) = 1st business idea 2nd business idea

3rd business idea

Scoring system: 5 - extremely high; 4 - high; 3 - average; 2 - fair; 1 - poor; 0 - absent.

Critical Success Factors (CSF) After evaluating and rating these factors, go into a finer cross-checking of the key variables affecting the success or failure of the business idea. E.g. not just 'raw material' but seasonal availability of raw material, lack of standardisation of raw material, unpredictability of raw material supply. Attention! CSF implies a critical success factor particular to the identified business, which is very important for the success of that specific business. If that certain factor is missing, is inadequate or is not properly taken into account, it can result in the total failure of the envisaged business idea.

7

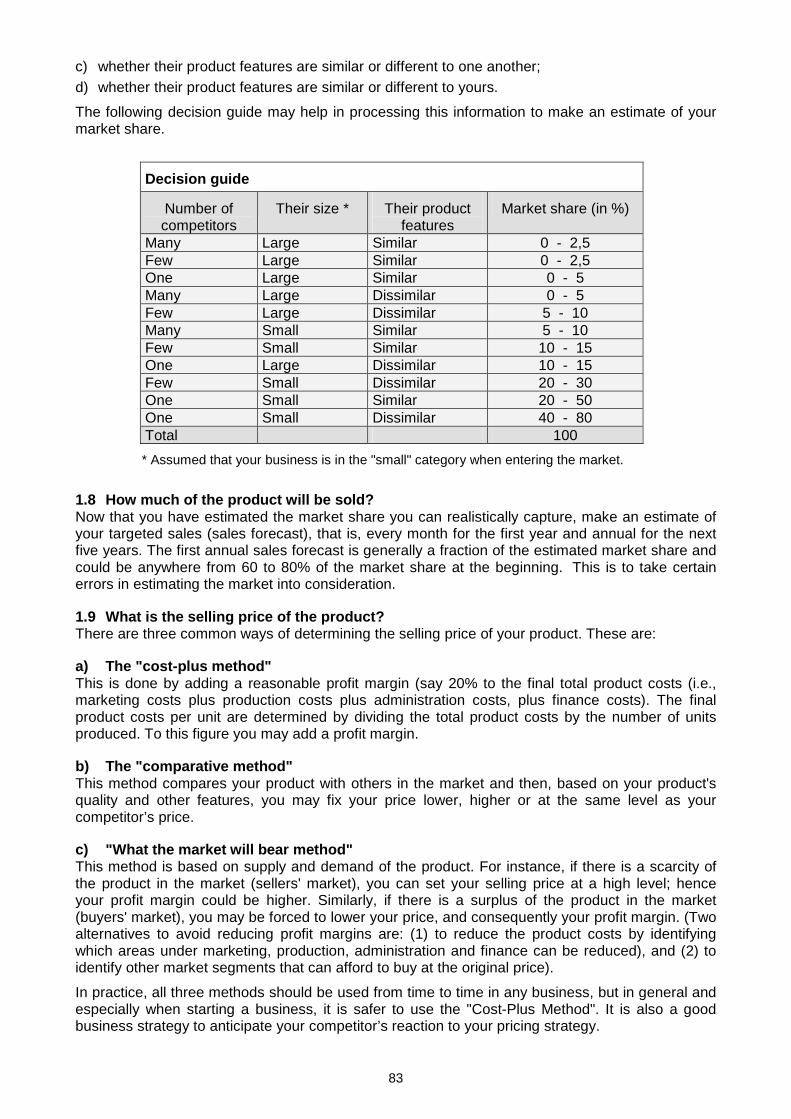

By making comparisons between the scores of the above parameters for each business idea, it is possible to choose one, which is viable. In this example, the second business idea may be the best one. It is also important to see the following additional parameters in selecting the business idea: Ease of implementation criteria:

• What are your unique competencies which give the company its competitive edge to competitors?

• Whether the business can be started within a short gestation period or reasonable preparatory period (such as three months) or not; and

• The degree to which the entrepreneur can control unforeseen difficulties and commence operations;

• The available financial and human resources. Risk exposure criteria:

• Whether the product can readily be copied or imitated if found very profitable by others;

• Competitors who have more resources and expertise may effectively retaliate if threatened by the new business;

• The envisaged business may suffer from unforeseen factors such as unavailability of raw materials.

Government priority and support criteria:

• Is the envisaged business under government's list of priorities for promotion of investment and employment generation?

• Is there a possibility of getting government support such as tax exemption or reduction, loan on reduced rate of interest or other supports such as market access, technical or advisory services?

The following format is presented as an example to show you how it is possible to generate one best business idea in a step-by-step way.

Business idea

Name of the Business: ABC Bakery

The business is to provide the following products: Loaves of bread and bread rolls

Customers are:

If your choice is to produce loaves of bread and bread rolls, then the customers could be:

• General dealers and caterers in locality ‘A’ as well as the majority of people living around that location.

The business will sell in the following way:

• Bread will be delivered to general caterers and customers.

• Other customers will buy from a shop at the bakery.

The business will satisfy the following needs of customers:

• General dealers need to sell fresh bread to their customers.

• Caterers need bread to serve with their meals.

• Private customers need a convenient place to buy bread for their households.

Fill your own template of business idea

8

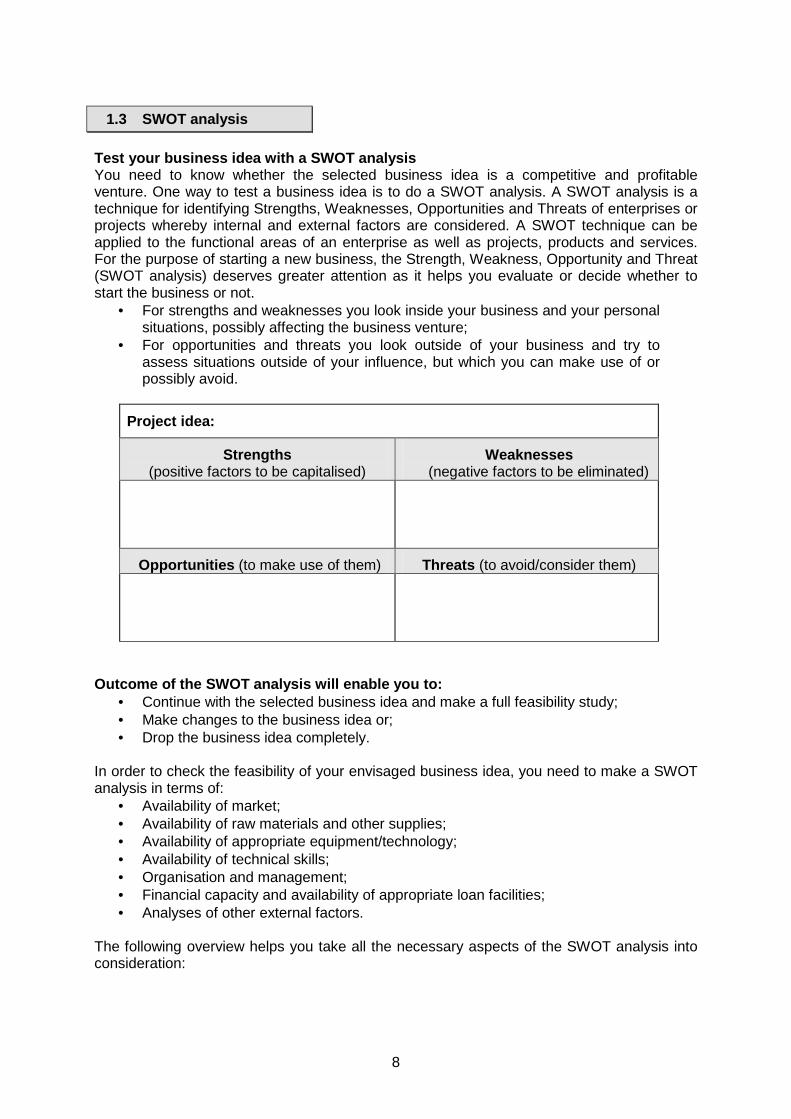

1.3 SWOT analysis

Test your business idea with a SWOT analysis You need to know whether the selected business idea is a competitive and profitable venture. One way to test a business idea is to do a SWOT analysis. A SWOT analysis is a technique for identifying Strengths, Weaknesses, Opportunities and Threats of enterprises or projects whereby internal and external factors are considered. A SWOT technique can be applied to the functional areas of an enterprise as well as projects, products and services. For the purpose of starting a new business, the Strength, Weakness, Opportunity and Threat (SWOT analysis) deserves greater attention as it helps you evaluate or decide whether to start the business or not.

• For strengths and weaknesses you look inside your business and your personal situations, possibly affecting the business venture;

• For opportunities and threats you look outside of your business and try to assess situations outside of your influence, but which you can make use of or possibly avoid.

Project idea:

Strengths (positive factors to be capitalised)

Weaknesses (negative factors to be eliminated)

Opportunities (to make use of them) Threats (to avoid/consider them)

Outcome of the SWOT analysis will enable you to:

• Continue with the selected business idea and make a full feasibility study; • Make changes to the business idea or; • Drop the business idea completely.

In order to check the feasibility of your envisaged business idea, you need to make a SWOT analysis in terms of:

• Availability of market; • Availability of raw materials and other supplies; • Availability of appropriate equipment/technology; • Availability of technical skills; • Organisation and management; • Financial capacity and availability of appropriate loan facilities; • Analyses of other external factors.

The following overview helps you take all the necessary aspects of the SWOT analysis into consideration:

9

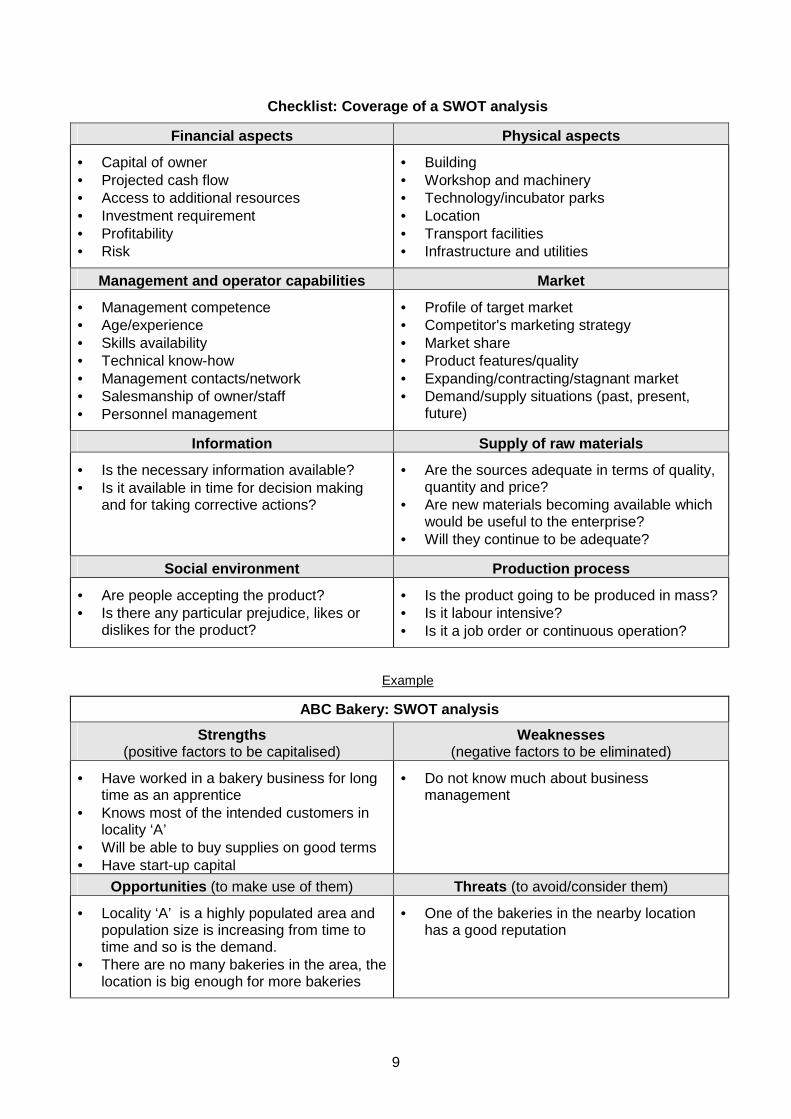

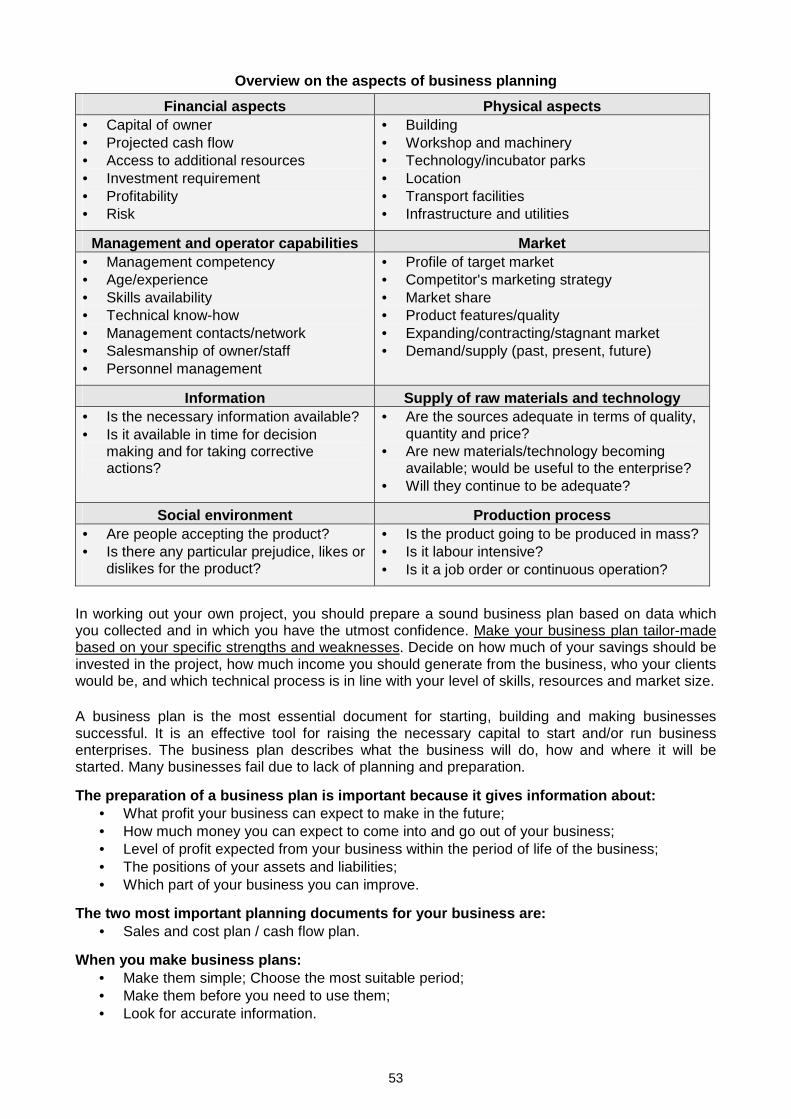

Checklist: Coverage of a SWOT analysis

Financial aspects Physical aspects

• Capital of owner • Projected cash flow • Access to additional resources • Investment requirement • Profitability • Risk

• Building • Workshop and machinery • Technology/incubator parks • Location • Transport facilities • Infrastructure and utilities

Management and operator capabilities Market

• Management competence • Age/experience • Skills availability • Technical know-how • Management contacts/network • Salesmanship of owner/staff • Personnel management

• Profile of target market • Competitor's marketing strategy • Market share • Product features/quality • Expanding/contracting/stagnant market • Demand/supply situations (past, present,

future)

Information Supply of raw materials

• Is the necessary information available? • Is it available in time for decision making

and for taking corrective actions?

• Are the sources adequate in terms of quality, quantity and price?

• Are new materials becoming available which would be useful to the enterprise?

• Will they continue to be adequate?

Social environment Production process

• Are people accepting the product? • Is there any particular prejudice, likes or

dislikes for the product?

• Is the product going to be produced in mass? • Is it labour intensive? • Is it a job order or continuous operation?

Example

ABC Bakery: SWOT analysis

Strengths (positive factors to be capitalised)

Weaknesses (negative factors to be eliminated)

• Have worked in a bakery business for long time as an apprentice

• Knows most of the intended customers in locality ‘A’

• Will be able to buy supplies on good terms • Have start-up capital

• Do not know much about business management

Opportunities (to make use of them) Threats (to avoid/consider them)

• Locality ‘A’ is a highly populated area and population size is increasing from time to time and so is the demand.

• There are no many bakeries in the area, the location is big enough for more bakeries

• One of the bakeries in the nearby location has a good reputation

10

Exercise to fill based on the above example (take your business idea and analyse it)

SWOT analysis of your project

Project idea:

Strengths (positive factors to be capitalised)

Weaknesses (negative factors to be eliminated)

Opportunities (to make use of them) Threats (to avoid/consider them)

Actions to take in order to overcome the inconvenie ncies:

11

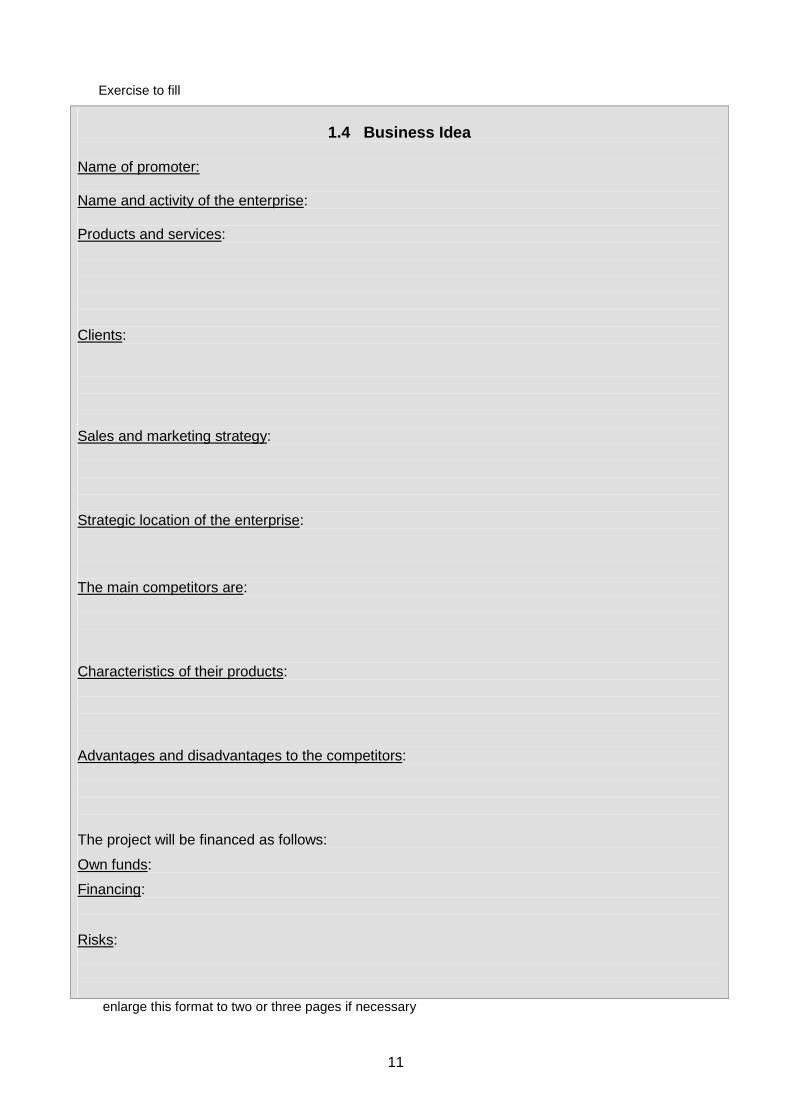

Exercise to fill

1.4 Business Idea

Name of promoter: Name and activity of the enterprise: Products and services: Clients: Sales and marketing strategy: Strategic location of the enterprise: The main competitors are: Characteristics of their products: Advantages and disadvantages to the competitors: The project will be financed as follows:

Own funds:

Financing: Risks:

enlarge this format to two or three pages if necessary

12

13

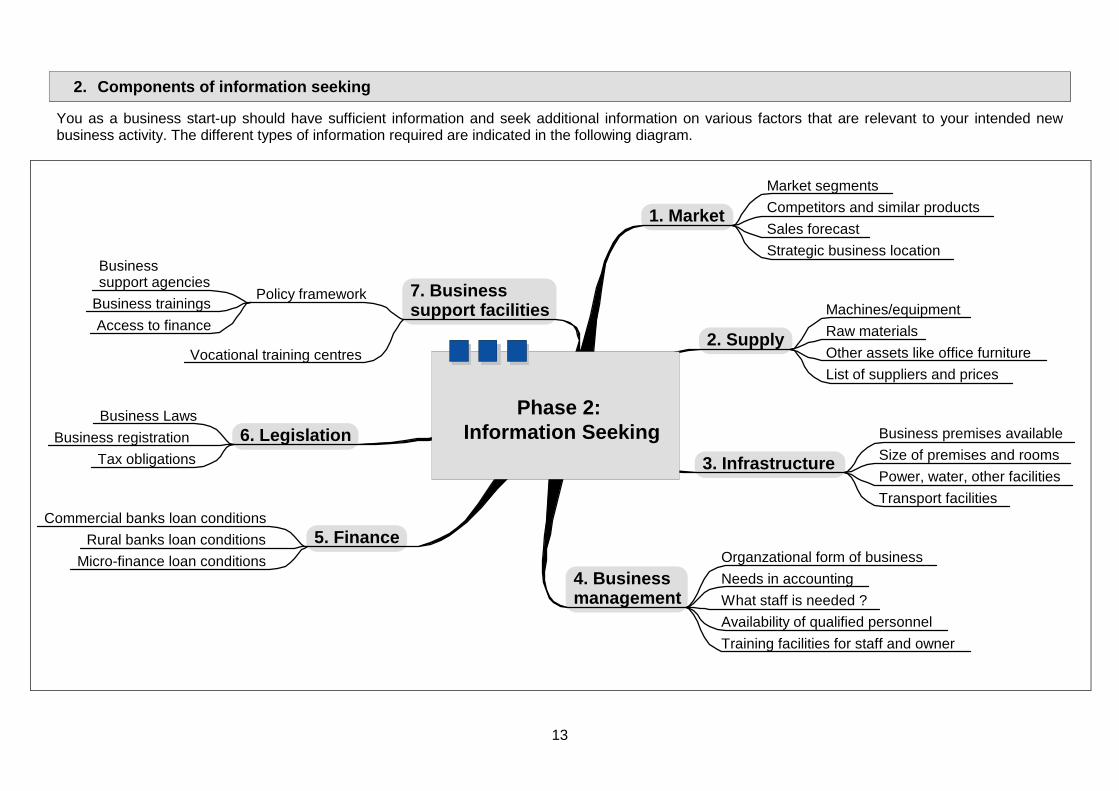

2. Components of information seeking

You as a business start-up should have sufficient information and seek additional information on various factors that are relevant to your intended new business activity. The different types of information required are indicated in the following diagram.

1. Market

2. Supply

3. Infrastructure

5. Finance

6. Legislation

4. Business management

7. Business support facilities

Phase 2: Information Seeking

Market segments

Competitors and similar products

Sales forecast

Strategic business location

Machines/equipment

Raw materials

Other assets like office furniture

List of suppliers and prices

Business premises available

Size of premises and rooms

Power, water, other facilities

Transport facilitiesCommercial banks loan conditions

Rural banks loan conditions

Micro-finance loan conditions

Business Laws

Business registration

Tax obligations

Organzational form of business

Needs in accounting

What staff is needed ?

Availability of qualified personnel

Training facilities for staff and owner

Policy framework

Business support agencies

Business trainings

Access to finance

Vocational training centres

14

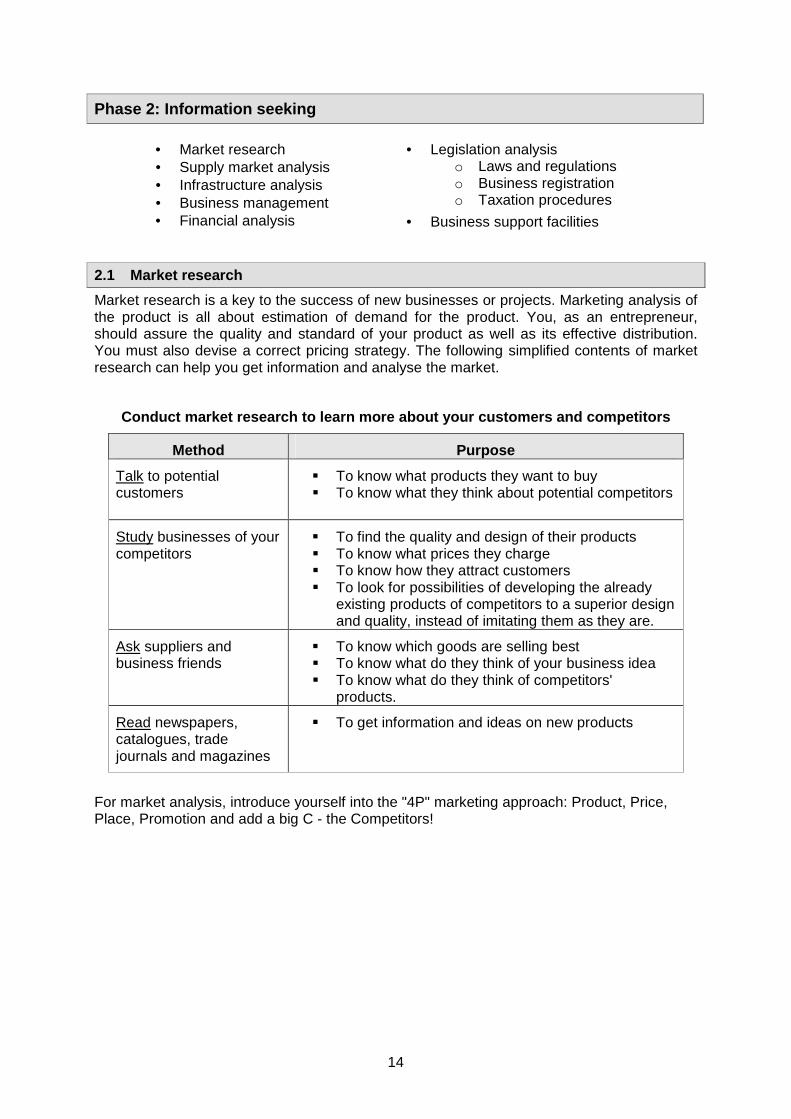

Phase 2: Information seeking

• Market research • Supply market analysis • Infrastructure analysis • Business management • Financial analysis

• Legislation analysis o Laws and regulations o Business registration o Taxation procedures

• Business support facilities

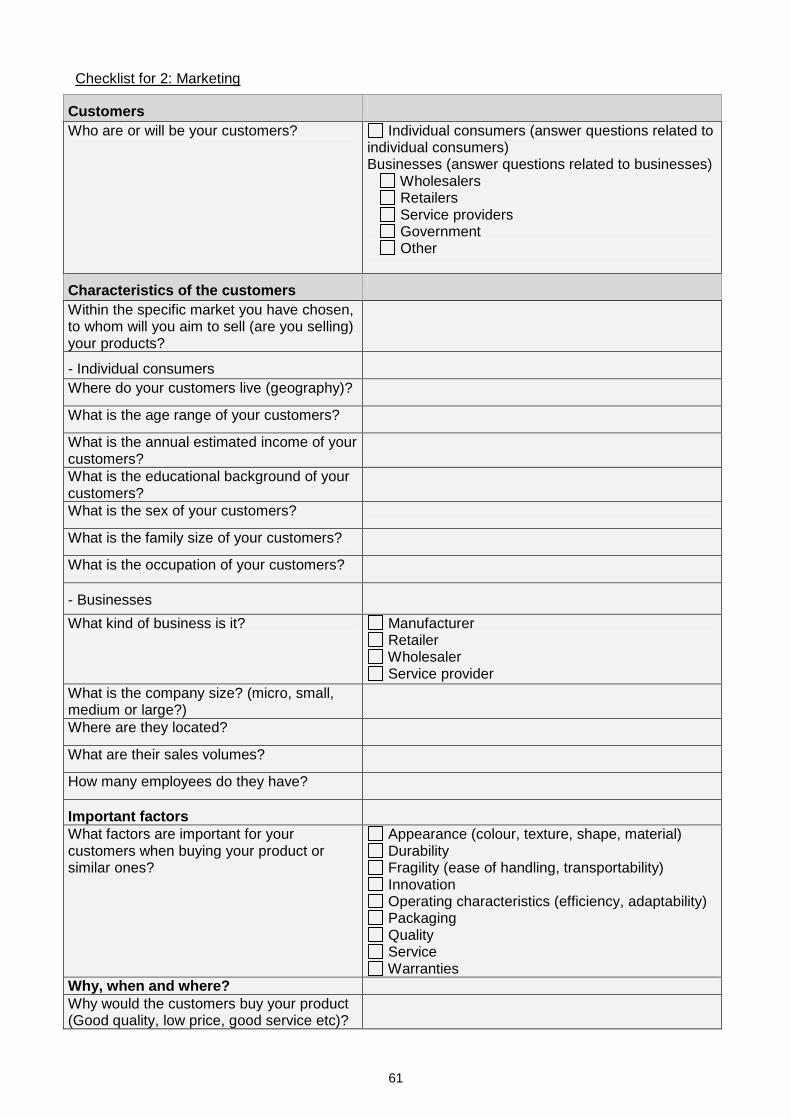

2.1 Market research

Market research is a key to the success of new businesses or projects. Marketing analysis of the product is all about estimation of demand for the product. You, as an entrepreneur, should assure the quality and standard of your product as well as its effective distribution. You must also devise a correct pricing strategy. The following simplified contents of market research can help you get information and analyse the market.

Conduct market research to learn more about your cu stomers and competitors

Method Purpose

Talk to potential customers

� To know what products they want to buy � To know what they think about potential competitors

Study businesses of your competitors

� To find the quality and design of their products � To know what prices they charge � To know how they attract customers � To look for possibilities of developing the already

existing products of competitors to a superior design and quality, instead of imitating them as they are.

Ask suppliers and business friends

� To know which goods are selling best � To know what do they think of your business idea � To know what do they think of competitors'

products.

Read newspapers, catalogues, trade journals and magazines

� To get information and ideas on new products

For market analysis, introduce yourself into the "4P" marketing approach: Product, Price, Place, Promotion and add a big C - the Competitors!

15

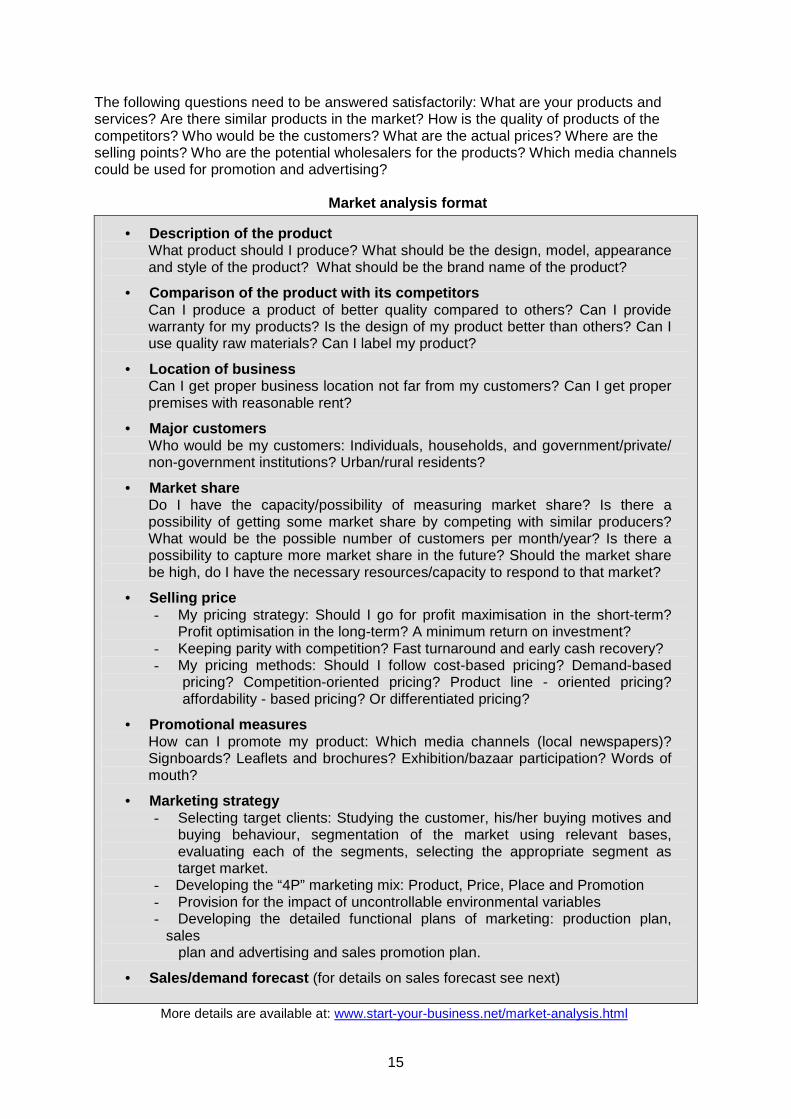

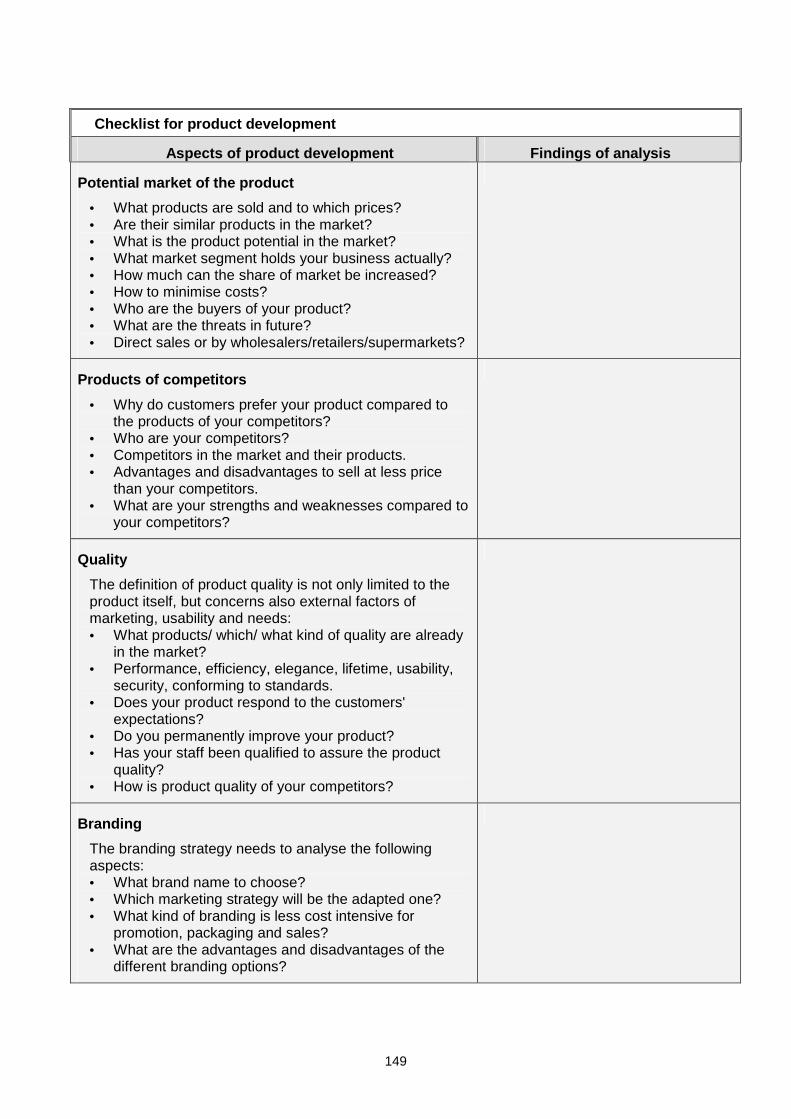

The following questions need to be answered satisfactorily: What are your products and services? Are there similar products in the market? How is the quality of products of the competitors? Who would be the customers? What are the actual prices? Where are the selling points? Who are the potential wholesalers for the products? Which media channels could be used for promotion and advertising?

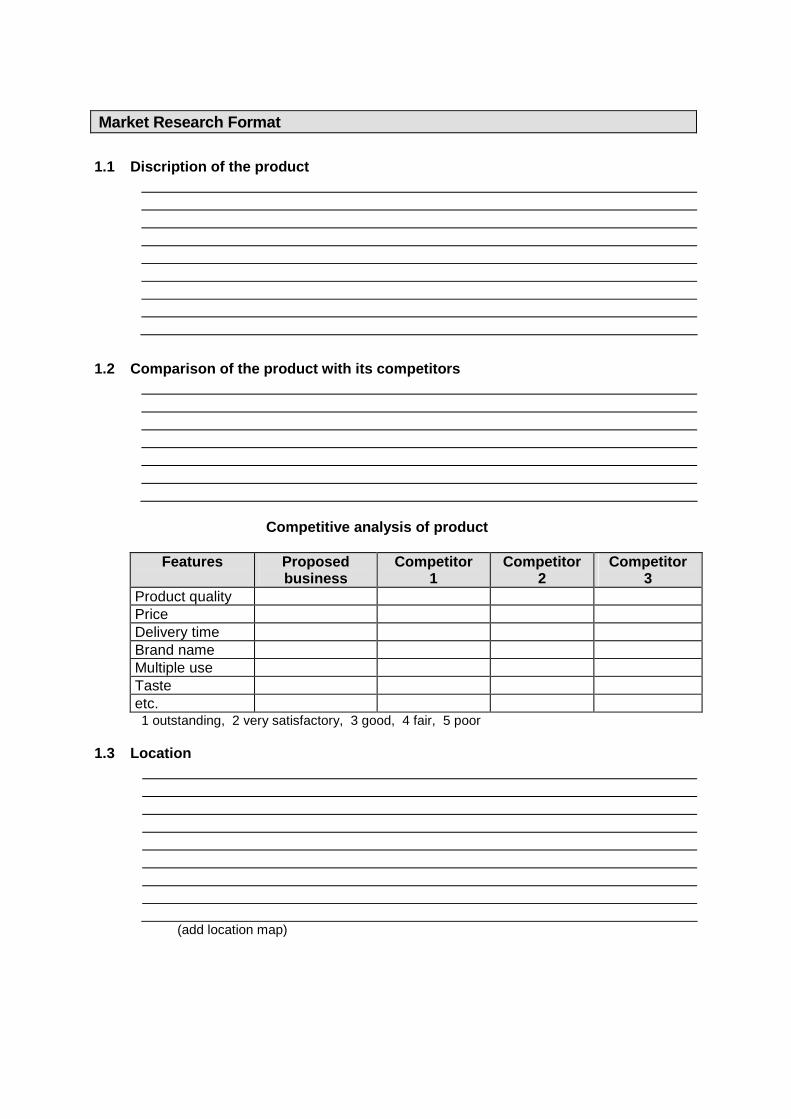

Market analysis format

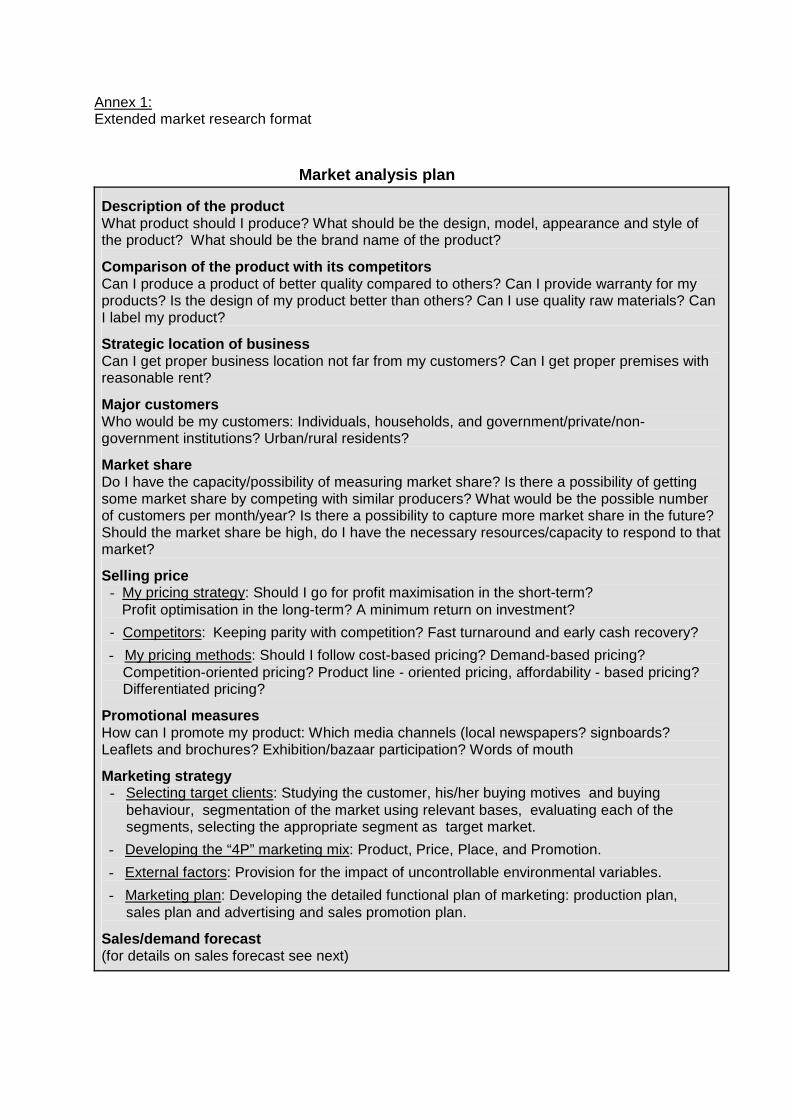

• Description of the product What product should I produce? What should be the design, model, appearance and style of the product? What should be the brand name of the product?

• Comparison of the product with its competitors Can I produce a product of better quality compared to others? Can I provide warranty for my products? Is the design of my product better than others? Can I use quality raw materials? Can I label my product?

• Location of business Can I get proper business location not far from my customers? Can I get proper premises with reasonable rent?

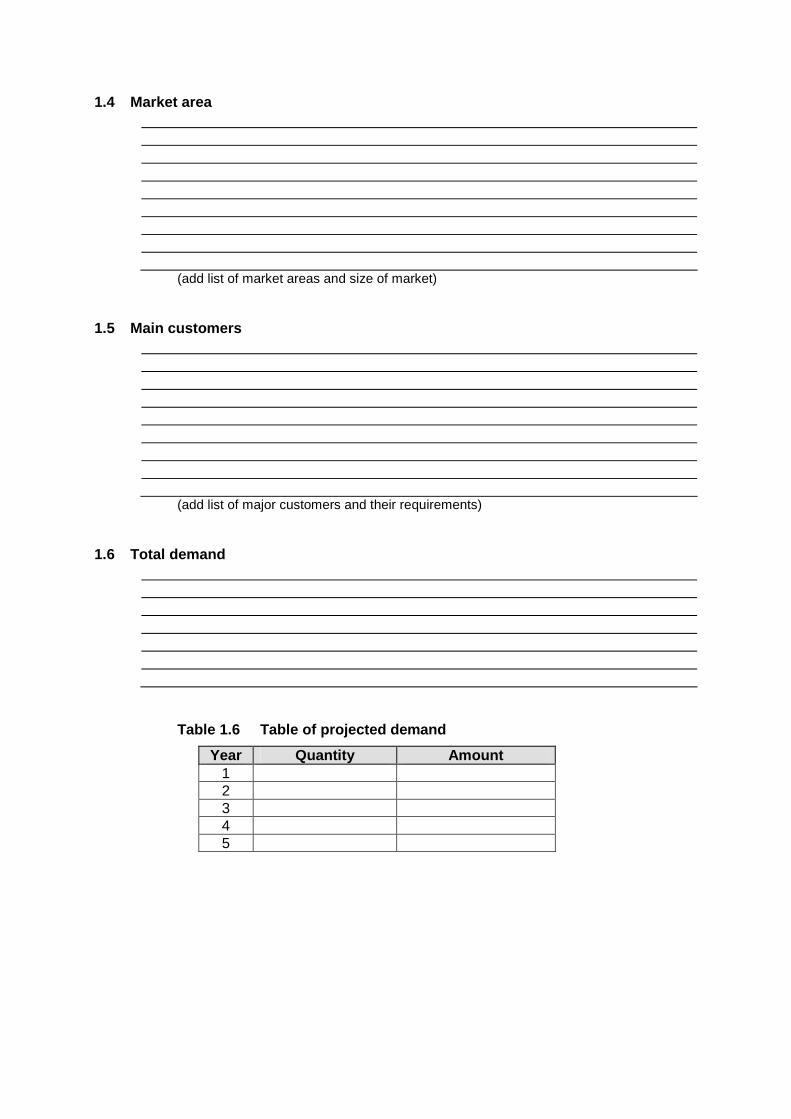

• Major customers Who would be my customers: Individuals, households, and government/private/ non-government institutions? Urban/rural residents?

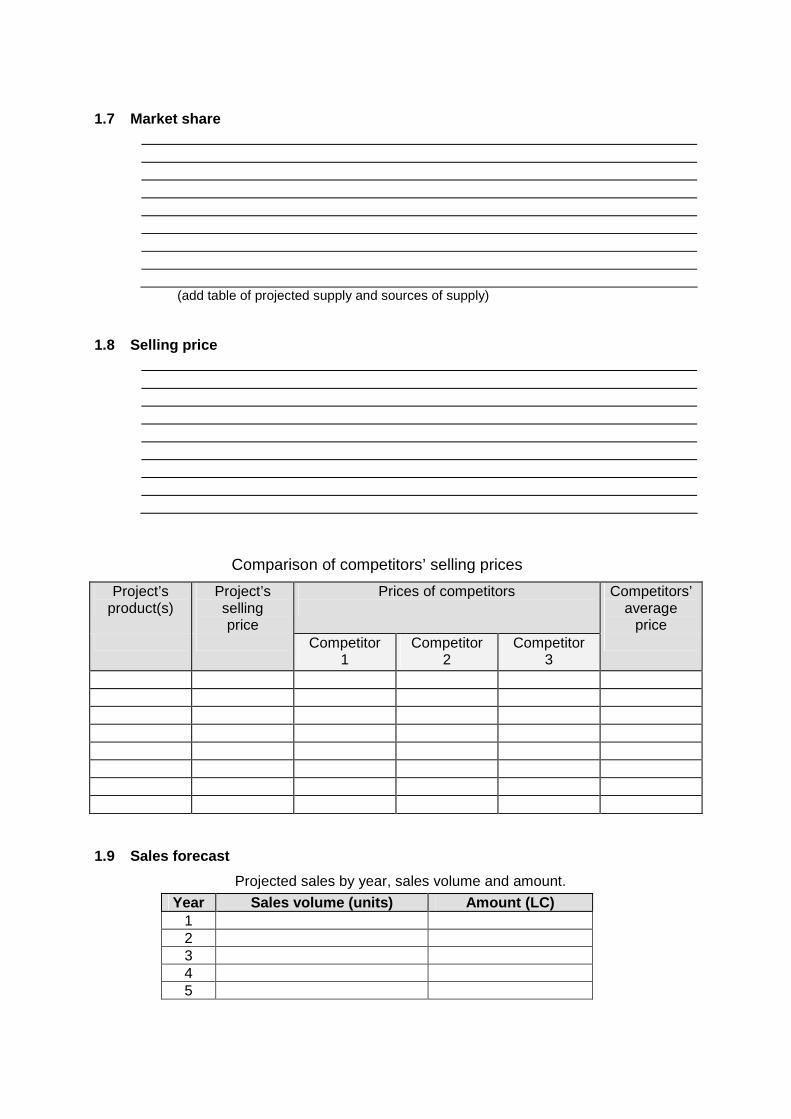

• Market share Do I have the capacity/possibility of measuring market share? Is there a possibility of getting some market share by competing with similar producers? What would be the possible number of customers per month/year? Is there a possibility to capture more market share in the future? Should the market share be high, do I have the necessary resources/capacity to respond to that market?

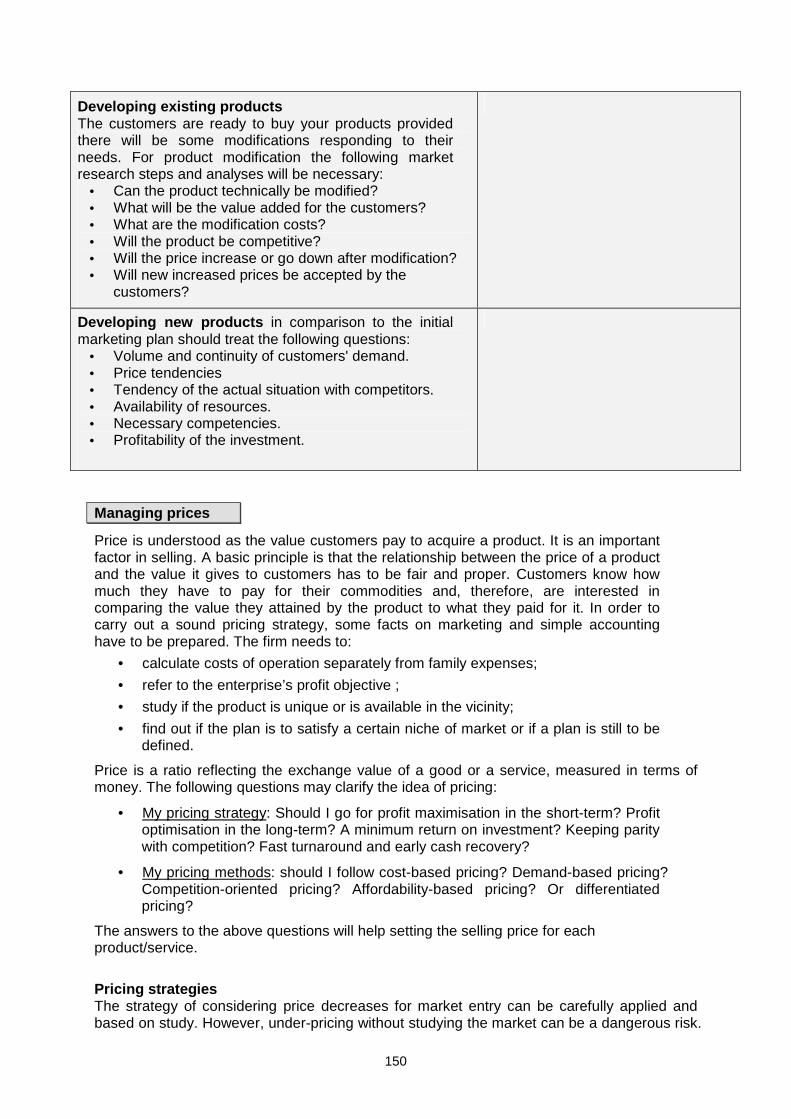

• Selling price - My pricing strategy: Should I go for profit maximisation in the short-term?

Profit optimisation in the long-term? A minimum return on investment? - Keeping parity with competition? Fast turnaround and early cash recovery? - My pricing methods: Should I follow cost-based pricing? Demand-based

pricing? Competition-oriented pricing? Product line - oriented pricing? affordability - based pricing? Or differentiated pricing?

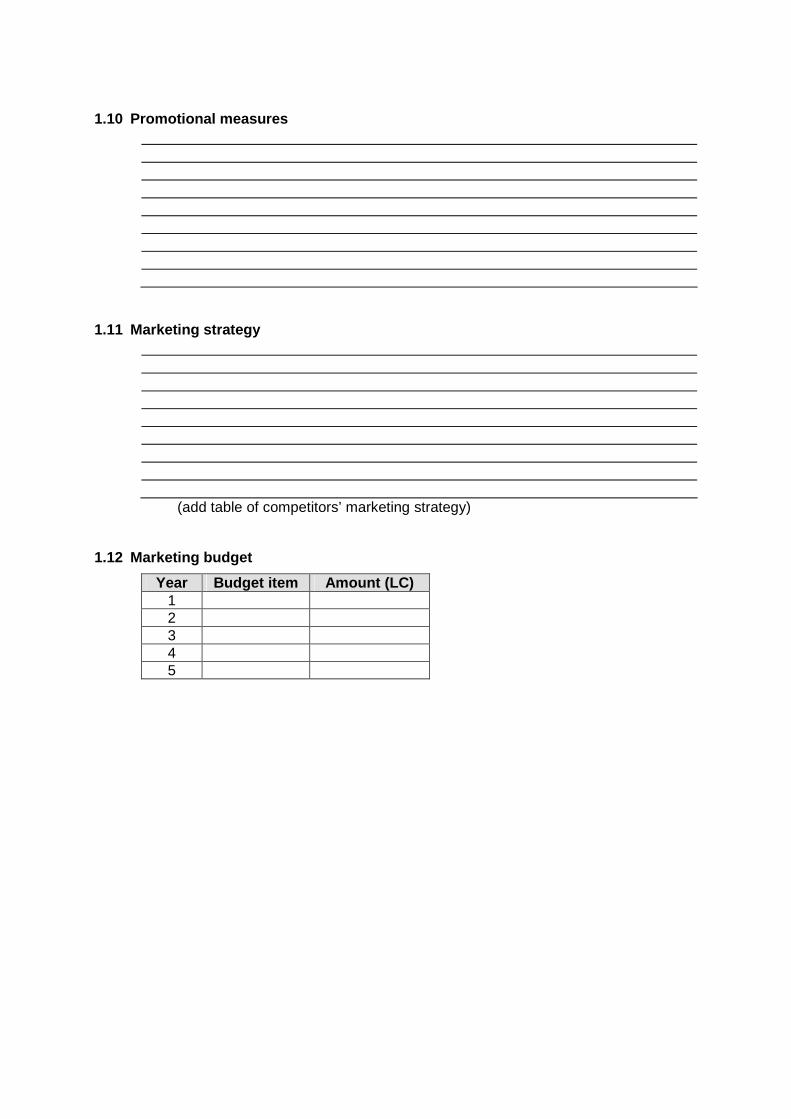

• Promotional measures How can I promote my product: Which media channels (local newspapers)? Signboards? Leaflets and brochures? Exhibition/bazaar participation? Words of mouth?

• Marketing strategy - Selecting target clients: Studying the customer, his/her buying motives and

buying behaviour, segmentation of the market using relevant bases, evaluating each of the segments, selecting the appropriate segment as target market.

- Developing the “4P” marketing mix: Product, Price, Place and Promotion - Provision for the impact of uncontrollable environmental variables - Developing the detailed functional plans of marketing: production plan,

sales plan and advertising and sales promotion plan.

• Sales/demand forecast (for details on sales forecast see next)

More details are available at: www.start-your-business.net/market-analysis.html

16

Sales/demand forecasting is required to predict or estimate a future situation. Since the future is unforeseen, no forecast can be 100% correct. However every business needs demand/ production/ sales forecast for taking decisions. In sales forecast, decisions concerning quantity, type and quality of products should be considered because production needs resources, i.e. finance, raw materials and manpower, which have to be arranged. The following steps are required to make a forecast: Foreca sting steps

• Determine the objective; • Select the period of forecast; • Select the forecasting techniques; • Collect the information to be used; • Make the forecast.

As an entrepreneur, you are required to make a study on availability of demand for the product. Demand for the product is manifested by a 'desire' backed by ability and willingness to pay. Demand for a product has always reference to price , period of time and place . The demand for a particular product can also depend on its supply. Demand forecasting for micro a nd small businesses

End-use/user expectation method

Steps:

- List the various users of the product; - Assert the individual likely demand of the product; - Consolidate the forecast for the demand.

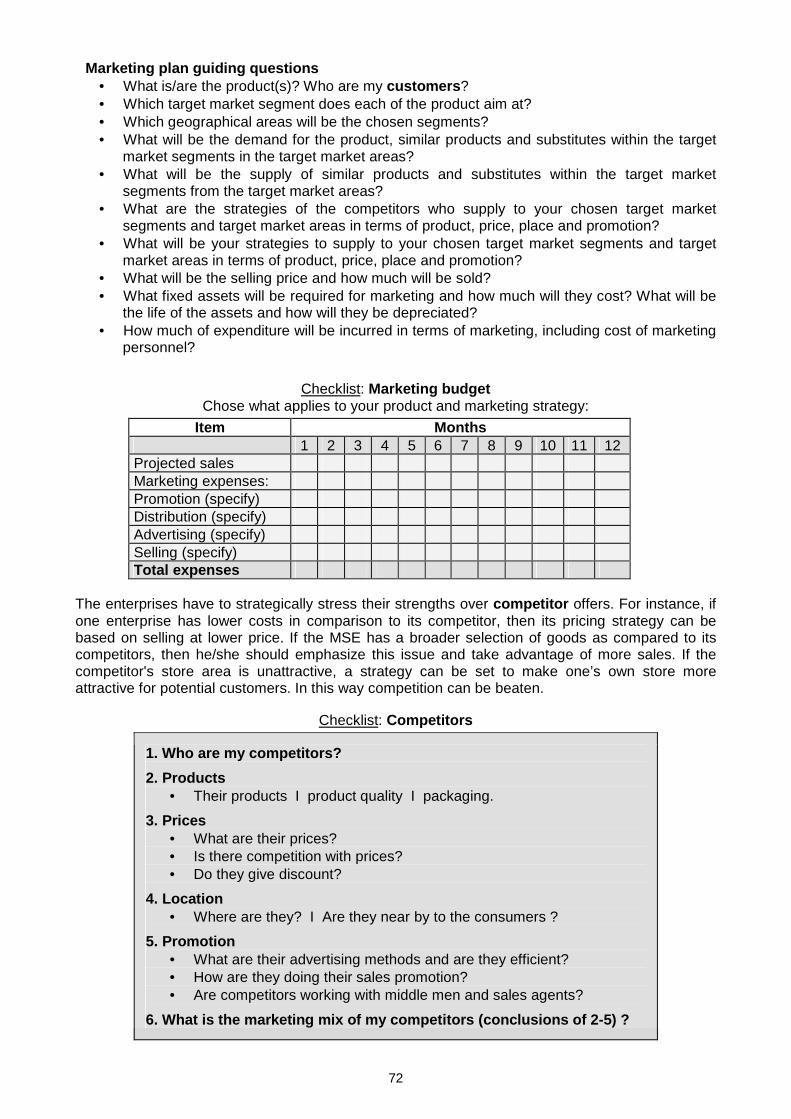

Marketing plan guiding questions • What is/are the product(s)? • Which target market segment does each of the product aim at? Or: To whom will

the business sell its products? • Which geographical areas will be the chosen segments? • What will be the demand for the product, similar products and substitutes within the

target market segments in the target market areas? • What will be the supply of similar products and substitutes within the target market

segments from the target market areas? • What are the strategies of the competitors who supply to your chosen target market

segments and target market areas in terms of product, price, place and promotion? • What will be your strategies to supply to your chosen target market segments and

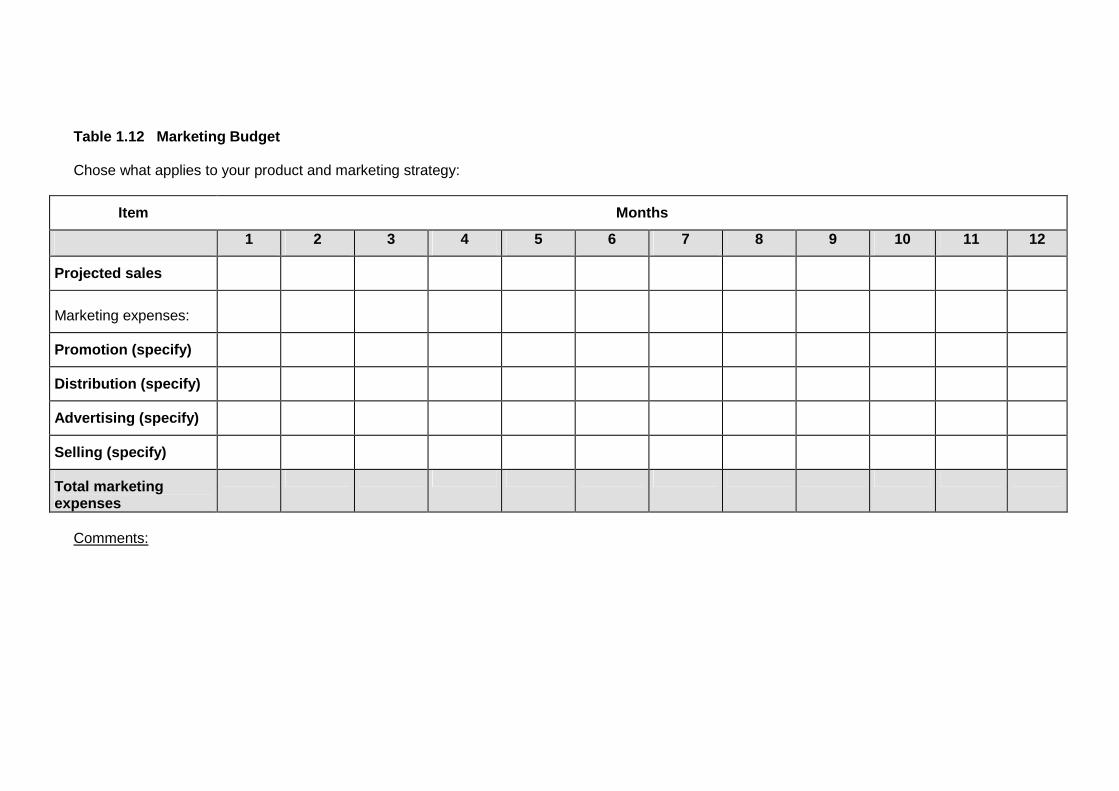

target market areas in terms of product, price, place and promotion? • What will be the selling price and how much will be sold? • What fixed assets will be required for marketing and how much will they cost? What

will be the life of the assets and how will they be depreciated? • How much of expenditure will be incurred in terms of marketing, including cost of

marketing personnel?

17

Exercise: Table to fill

Check list for consumer analysis

Step of research Result

1. How much potential customers are in the area? How much customers use similar products in this area?

2. How much customers are actually with you? What is the real selling price?

3. Who are the customers? Houswifes, families, other enterprises, shops, retailers, wholesalers? What is their financial capacity?

4. Who are the buyers? Are they also the users?

5. Where are the selling points? In the enterprise? In shops? On the market?

6. Where are the customers? In the area? Next district? Next town? etc.

7. What type of product do they like (best one, or medium with normal price) ?

8. Why do they like this product?

9. Where do they buy actually? Only with you or also with your competitors?

10. If the customers do not buy your products, what products do they buy?

11. How much do they pay for the product?

12. Are customers actually not satisfied with the existing products on the market and why not?

13. When and how much do customers buy? Once per day/week/month? In the morning, afternoon, evening or irregular?

14. How do they buy and which quantity?

15. Is market growing or going down? Are there more customers or less? Do they spend more or less? Why?

18

Strategies in relation to competition

Almost all micro and small enterprises have competitors. Therefore, the enterprises have to strategically stress their strengths over competitor offers. For instance, if one enterprise has lower costs in comparison to its competitor, then its pricing strategy can be based on selling at lower price. If the MSE has a broader selection of goods as compared to its competitors, then he/she should emphasize this issue and take advantage of more sales. If the competitor's store area is unattractive, a strategy can be set to make one’s own store more attractive for potential customers. In this way competition can be beaten. Joining chambers and trade associations is one way of interacting with competitors and learning how successful enterprises do business. If the enterprise suffers from different rivals, it could use a strategy that provides it with a competitive advantage over others as part of the sales deal.

A wiser strategy would be to try to be good in some competitive areas. MSEs need to select a few areas, in which they can excel in the competition,

since it is difficult to be good in all areas.

If competitors sell on a door-to-door basis then those who have no buyers at home can develop delivery to "x" buyer's premise. The strategy has to look into aspects that the buyer cares about.

The best strategy would be a strategy that separates micro and small sized enterprises from its competitors.

The issue of getting data and information is relevant, not only to competition, but to all other marketing mixes. Besides, information is a knowledge source of what is going on or what competitors are doing. In relation to the shortage of data and information already mentioned earlier, the service providers can play a role in establishing centres for data and information that the MSEs can effectively use in their proximity. It obviously requires a good budget, but with the assistance of some financiers the topic can be considered.

Competitors analysis Almost all micro and small enterprises have competitors. Therefore, the enterprises have to strategically stress their strengths over competitor offers. For instance, if one enterprise has lower costs in comparison to its competitor, then its pricing strategy can be based on selling at lower price. If the MSE has a broader selection of goods as compared to its competitors, then he/she should emphasize this issue and take advantage of more sales. If the competitor's store area is unattractive, a strategy can be set to make one’s own store more attractive for potential customers. In this way competition can be beaten.

1. Who are my competitors? − Local retailers? Local wholesalers? Importers of similar products?

2. Products − Their products / Product quality / Packaging.

3. Prices − What are their prices? Is there competition with prices? Do they give discount?

4. Location − Where are they? Are they near by the consumers?

5. Promotion − What are their advertising methods and are they efficient? − How are they doing their sales promotion? − Are competitors working with middlemen and sales agents?

6. What is the marketing mix of my competitors (conclusions of 2-5) ?

19

Exercise: Table to fill

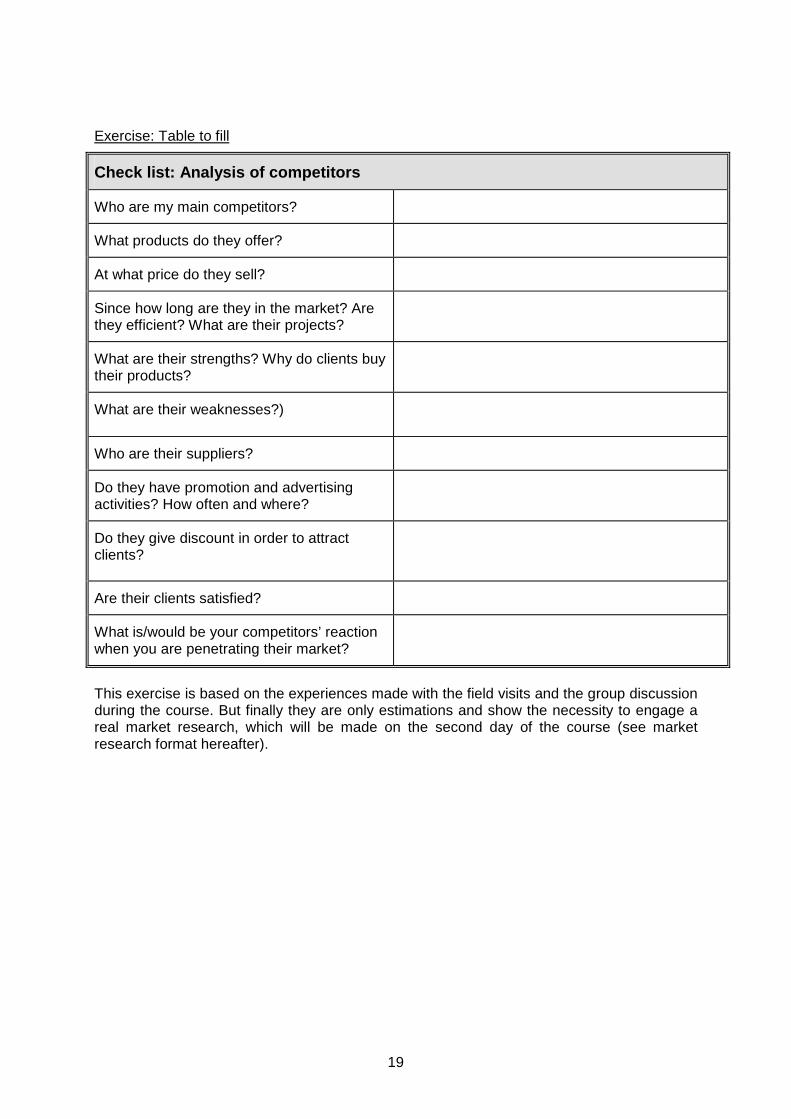

Check list: Analysis of competitors

Who are my main competitors?

What products do they offer?

At what price do they sell?

Since how long are they in the market? Are they efficient? What are their projects?

What are their strengths? Why do clients buy their products?

What are their weaknesses?)

Who are their suppliers?

Do they have promotion and advertising activities? How often and where?

Do they give discount in order to attract clients?

Are their clients satisfied?

What is/would be your competitors’ reaction when you are penetrating their market?

This exercise is based on the experiences made with the field visits and the group discussion during the course. But finally they are only estimations and show the necessity to engage a real market research, which will be made on the second day of the course (see market research format hereafter).

20

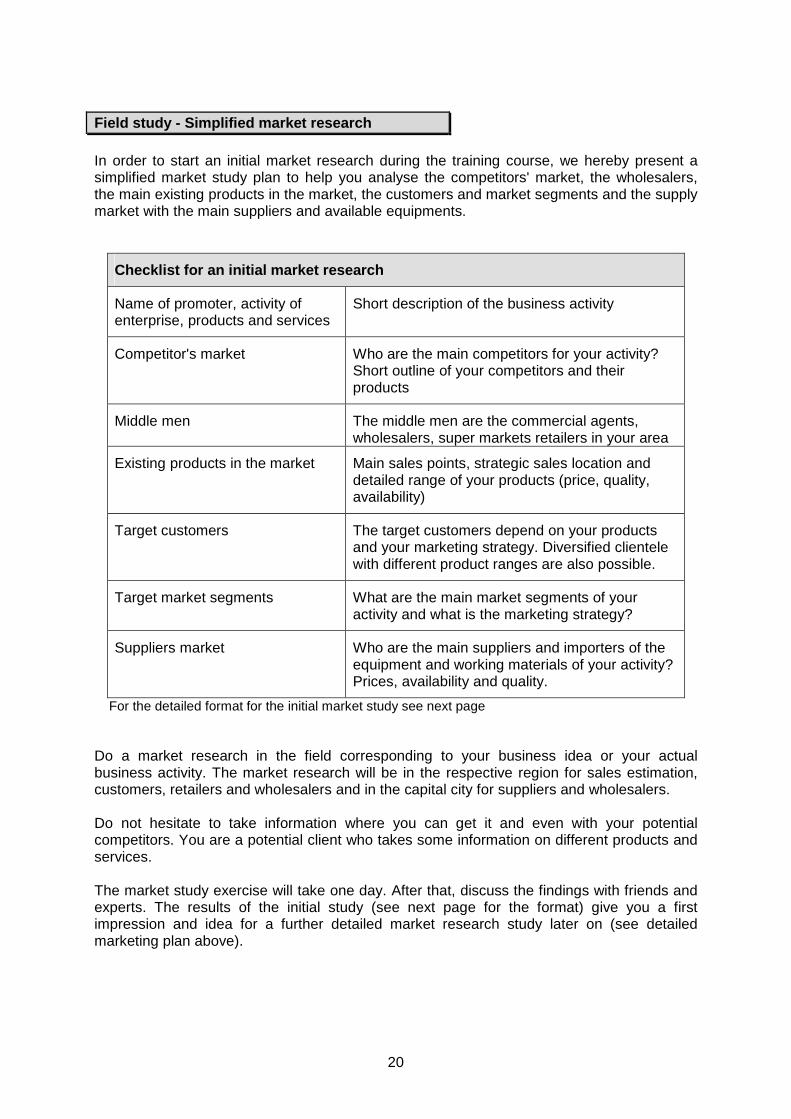

Field study - Simplified market research In order to start an initial market research during the training course, we hereby present a simplified market study plan to help you analyse the competitors' market, the wholesalers, the main existing products in the market, the customers and market segments and the supply market with the main suppliers and available equipments.

Checklist for an initial market research

Name of promoter, activity of enterprise, products and services

Short description of the business activity

Competitor's market

Who are the main competitors for your activity? Short outline of your competitors and their products

Middle men

The middle men are the commercial agents, wholesalers, super markets retailers in your area

Existing products in the market

Main sales points, strategic sales location and detailed range of your products (price, quality, availability)

Target customers

The target customers depend on your products and your marketing strategy. Diversified clientele with different product ranges are also possible.

Target market segments

What are the main market segments of your activity and what is the marketing strategy?

Suppliers market

Who are the main suppliers and importers of the equipment and working materials of your activity? Prices, availability and quality.

For the detailed format for the initial market study see next page Do a market research in the field corresponding to your business idea or your actual business activity. The market research will be in the respective region for sales estimation, customers, retailers and wholesalers and in the capital city for suppliers and wholesalers. Do not hesitate to take information where you can get it and even with your potential competitors. You are a potential client who takes some information on different products and services. The market study exercise will take one day. After that, discuss the findings with friends and experts. The results of the initial study (see next page for the format) give you a first impression and idea for a further detailed market research study later on (see detailed marketing plan above).

21

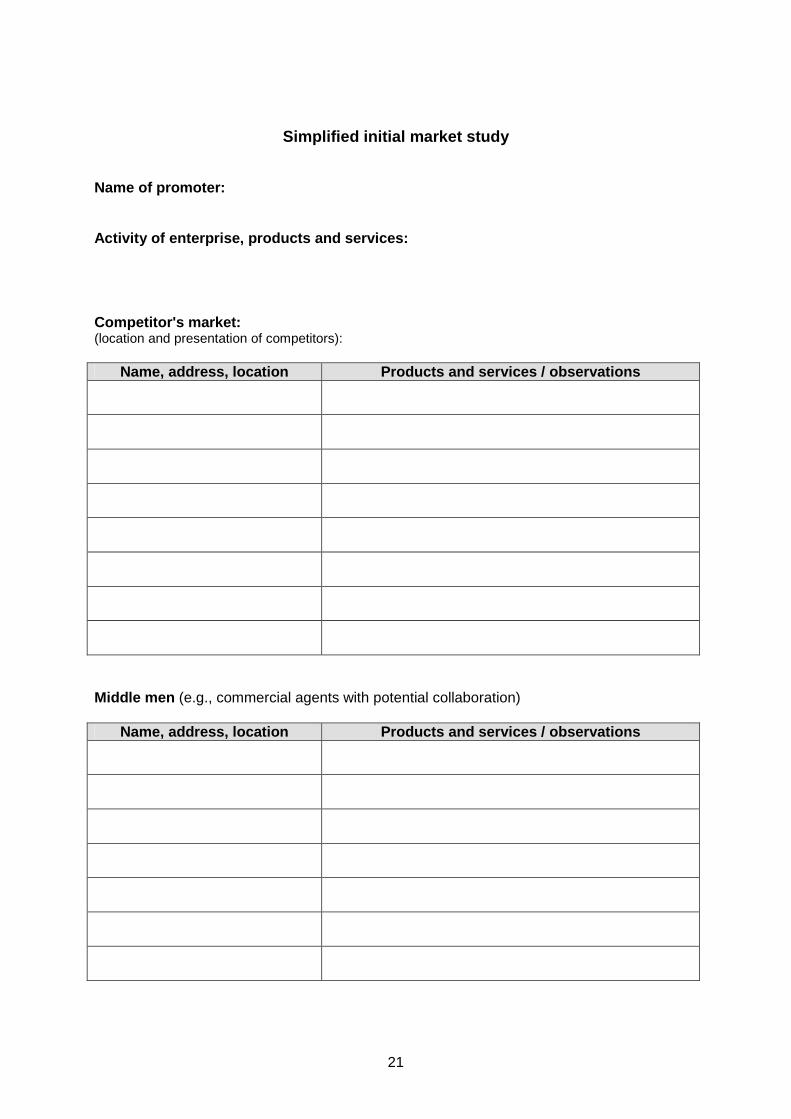

Simplified initial market study Name of promoter: Activity of enterprise, products and services: Competitor's market: (location and presentation of competitors):

Name, address, location Products and services / observations

Middle men (e.g., commercial agents with potential collaboration)

Name, address, location Products and services / observations

22

Existing products in the market: (sales points, quantity, quality, price, presentation)

Sales point Main products Quantity, quality, price Observations

Target group of customers: Target market segments:

23

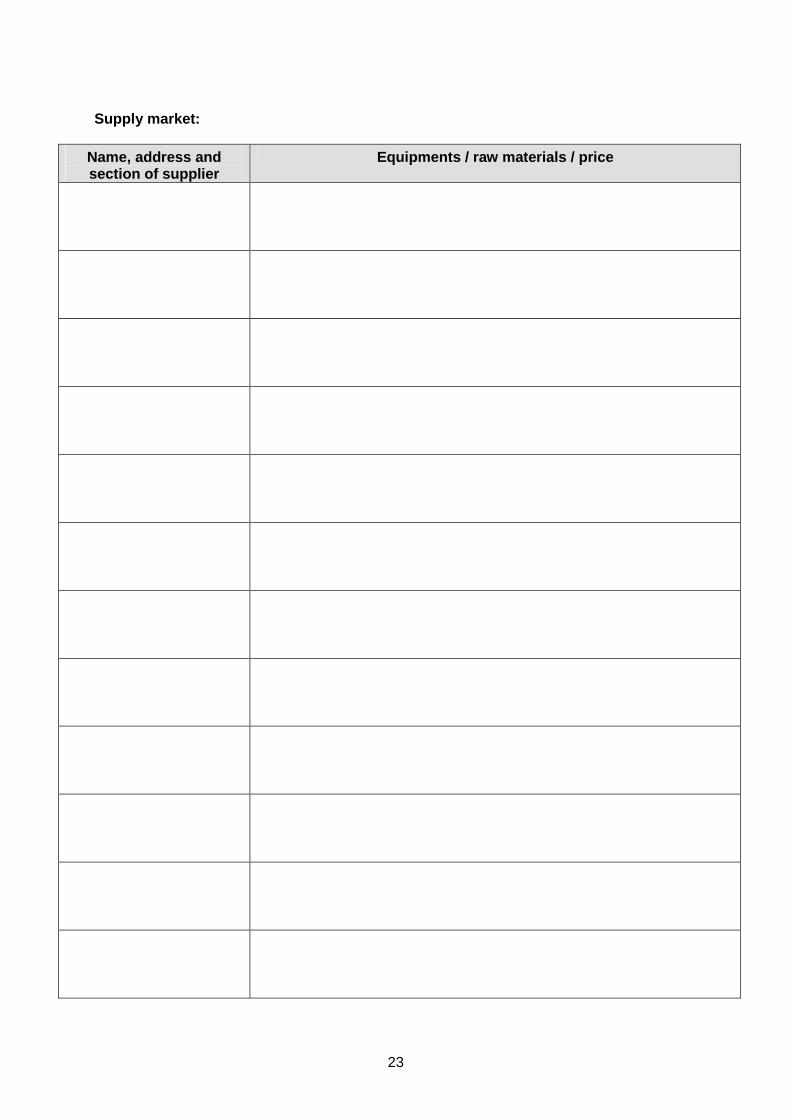

Supply market:

Name, address and section of supplier

Equipments / raw materials / price

24

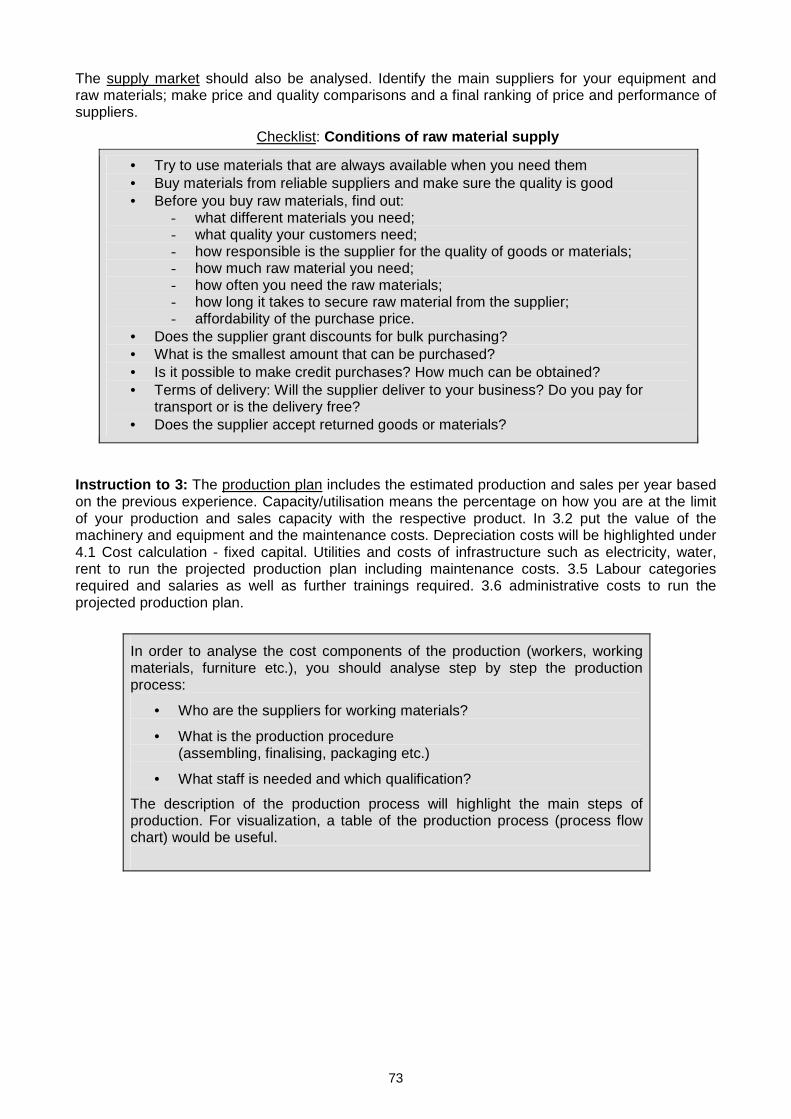

2.2 Supply market analysis Supply refers to the different types of input you need from others for production. It requires identifying the main suppliers for your equipment and raw materials and making price and quality comparisons and a final ranking of price and performance of suppliers. A sound analysis of the availability and the best prices of equipment and working materials will stabilize your business, protect you from shortages and minimize costs.

Production-oriented business owners need to buy:

• Equipment/tools; • Inputs such as raw material.

Buying equipment/tools Equipment is all the machinery, tools, workshop fittings and office furniture that your business needs. Old equipment needs to be replaced. You should check regularly to see how well your equipment works - if it still produces as much as it used to and if it still produces the quality you need. You may need to buy new equipment when it:

• becomes difficult to operate; • does inferior work; • breaks down often; • becomes old.

Important questions to ask before buying equipment/ tools

• What kind of equipment do I need? • How much will the equipment cost? • Can my business afford to buy the equipment? • Can I buy the equipment second hand? • Will the increase in profit after I buy the equipment be high enough to pay for the cost of the equipment? • How much more work does my business get now and in the future? • How big must the equipment be to do the work I expect (capacity)? • Maybe you do not need to buy equipment of your own. In that case find out if you can:

- borrow or rent equipment only when you need it; - outsource to another business that has the equipment to do the work for you.

• Is there another new kind of equipment better than existing ones? • Which equipment is the cheapest to run and easiest to operate? • Do I need special training to use the equipment? Can I get it? Is the fee affordable? • How long would the equipment last? • Does the supplier give a written guarantee? • Will the supplier install the equipment and service it? • Can I have it serviced locally? • Are the spare parts available locally? Is the cost affordable?

Buying raw materials Raw materials are all the materials and parts that go into the products you make. Example: Wood and varnish for making furniture.

25

Buying office and workshop furniture for your busin ess You have to know what type of furniture you need before the start of the business. Some of them include:

• Shelves, tables, seating; • Computer facilities, printers, photocopy machine; • Telephone, fax, Internet connection.

Conditions of raw material supply

• Try to use materials that are always available when you need them • Buy materials from reliable suppliers and make sure the quality is good

• Before you buy raw materials, find out: o what different materials you need; o what quality your customers need; o how responsible is the supplier for the quality of goods or materials; o how much raw material you need; o how often you need the raw materials; o how long it takes to secure raw material from the supplier; o affordability of the purchase price.

• Does the supplier grant discounts for bulk purchasing? • What is the smallest amount that can be purchased? • Is it possible to make credit purchases? How much can be obtained? • Terms of delivery: Will the supplier deliver to your business? Do you pay

for transport or is the delivery free? • Does the supplier accept returned goods or materials?

Get information about suppliers and compare them ba sed on the following offers:

• Lowest price; • Best credit terms; • Best terms of delivery; • Best quality of raw materials.

Institutions involved

• Contact Chamber of Commerce and “Yellow Pages” for list of raw materials, office and workshop equipment suppliers;

• Make visits to the most important commercial centres in town (including importers, if necessary);

• Contact wholesalers and retailers of supplies.

Steps to follow when you buy

• Find out what your business needs; • Buy only equipment which is really necessary for your business; • Get information about different suppliers; • Contact and choose the best suppliers for your business; • Place the order; • Check the goods immediately; • Check the invoice; • Pay.

26

2.3 Infrastructure analysis

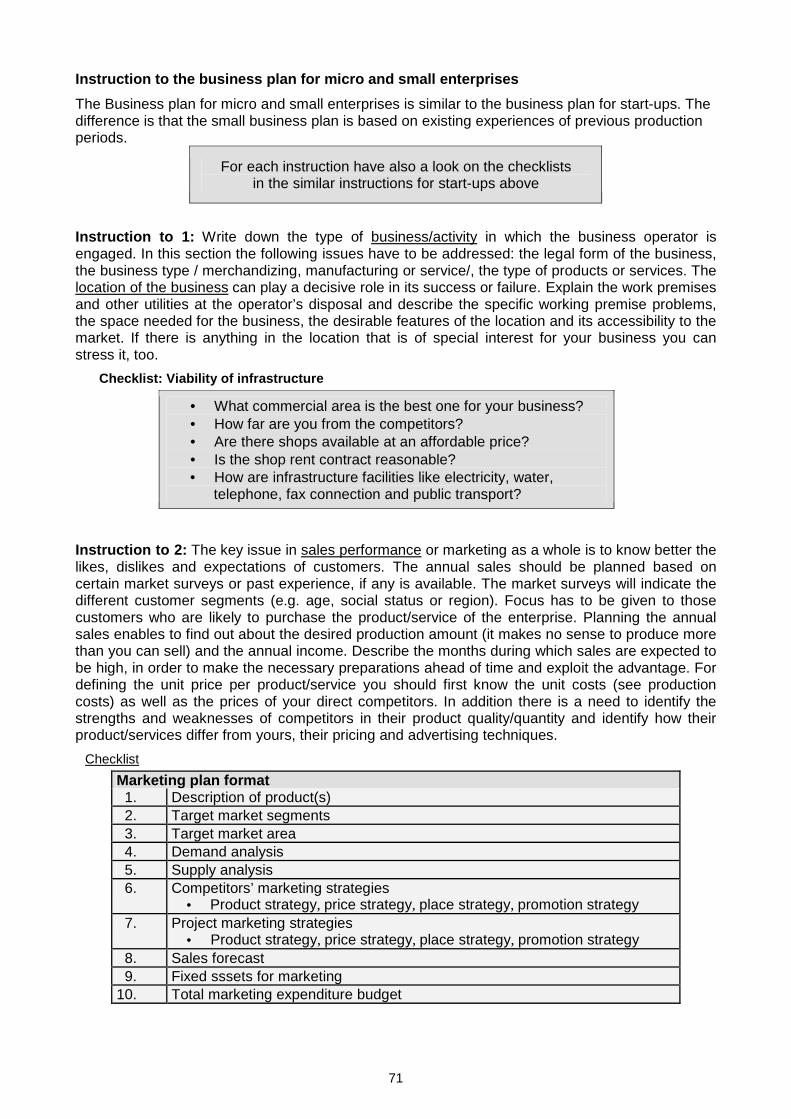

Infrastructure includes access to roads, transportation services, electric power, water supply, telephone services, storage facilities, production and marketing premises. Availability of transport facilities and electric power play great roles if you are engaged in the manufacturing and construction business sectors. You need to get a good transport facility with affordable fees to transport raw materials as well as your finished goods. If you are using power driven machines/equipment, availability and affordability of electric power will also play determinant role. In addition to the analysis of infrastructure, you also need to look for a strategic business location to reach potential customers.

Availability of infrastructure

• What commercial area is the best for your business? • How far are you from the competitors? • Are there shops available at affordable price? • Is the shop rent contract reasonable? • How are infrastructure facilities like electricity, water,

telephone, fax connection and public transport?

2.4 Business management

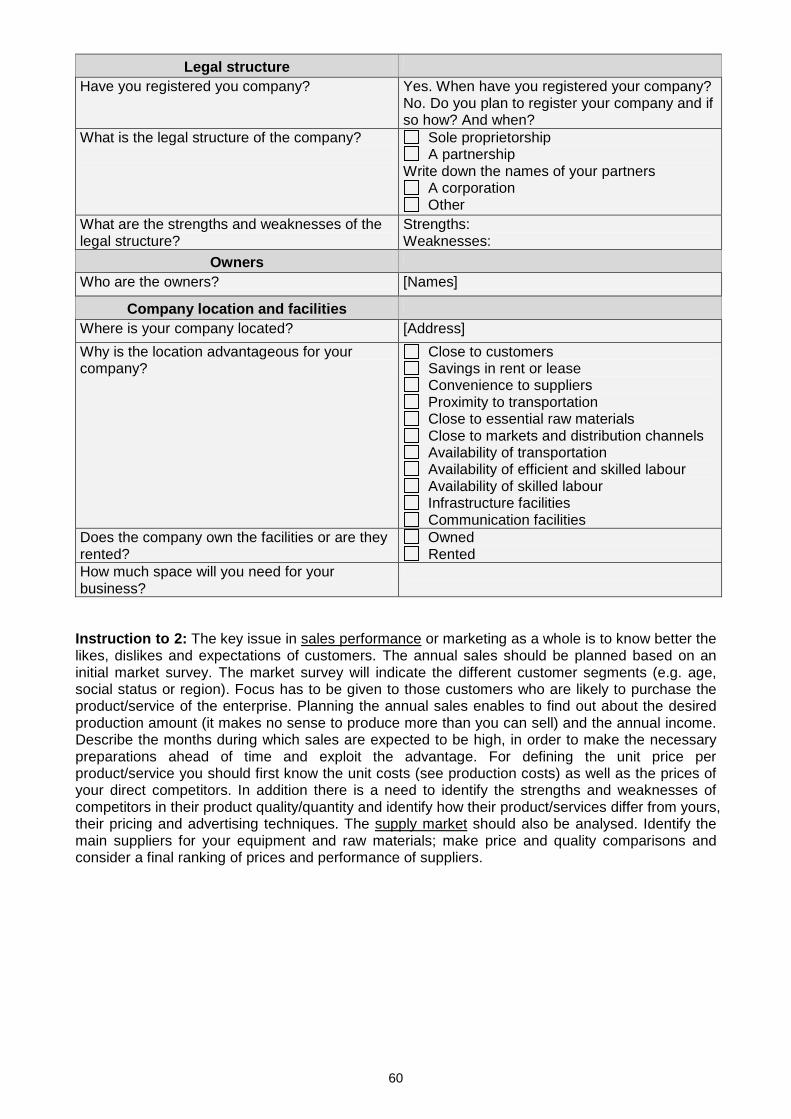

Business management aims at drawing upon effective organisation and management to achieve the entrepreneur's objectives. Business management is all about co-ordinating your meagre resources such as materials, financial and human, thereby undertaking your business activities efficiently and effectively. Having the necessary skills in the areas of marketing, costing your products and services, financial/business planning and record keeping are very crucial for you to succeed in business. You may have taken some business management courses during your school or college days, or you may not. Which ever the case may be, you need to look for opportunities to strengthen your business management skills continuously. This can be done by completing business management training courses intended for people like you. In addition, you as a business starter need to decide upon what form of business organisation you have to choose. The choice may partly be done based on the level of your investment capital as well as the commercial code of your country.

General aspects of business management

With regards to business management, you should give attention to questions such as:

• Do I have the necessary business management skills to start and run a new business? • What form of business organisation should I register in? • In case I am going to hire labour, what type of qualification do I need? • Do I have the capacity to manage my personnel issues? • What series of pre-operating activities should I perform? • What pre-operating costs am I able to bear? • Where shall I get as much information as possible pertaining to regulations, finance and

competitors?

27

Before you start operating your new business, you need to select in which organisational form you should establish your business. The choice of organisational form is important and can make a difference in:

• Cost of starting and registering the business; • Simplicity of starting the business; • Financial risk the owner of the business faces; • Possibility of having partners; • Way decisions are made in the business; • Mode of taxation of the business profit.

Qualified personnel : This indicates the analysis of the number and qualifications of the staff you need and labour organisation (production workers, administrative personnel, salespersons) and job description for your staff, labour costs and its availability (survey of labour market using newspapers and contacting the labour and social affairs bureau).

28

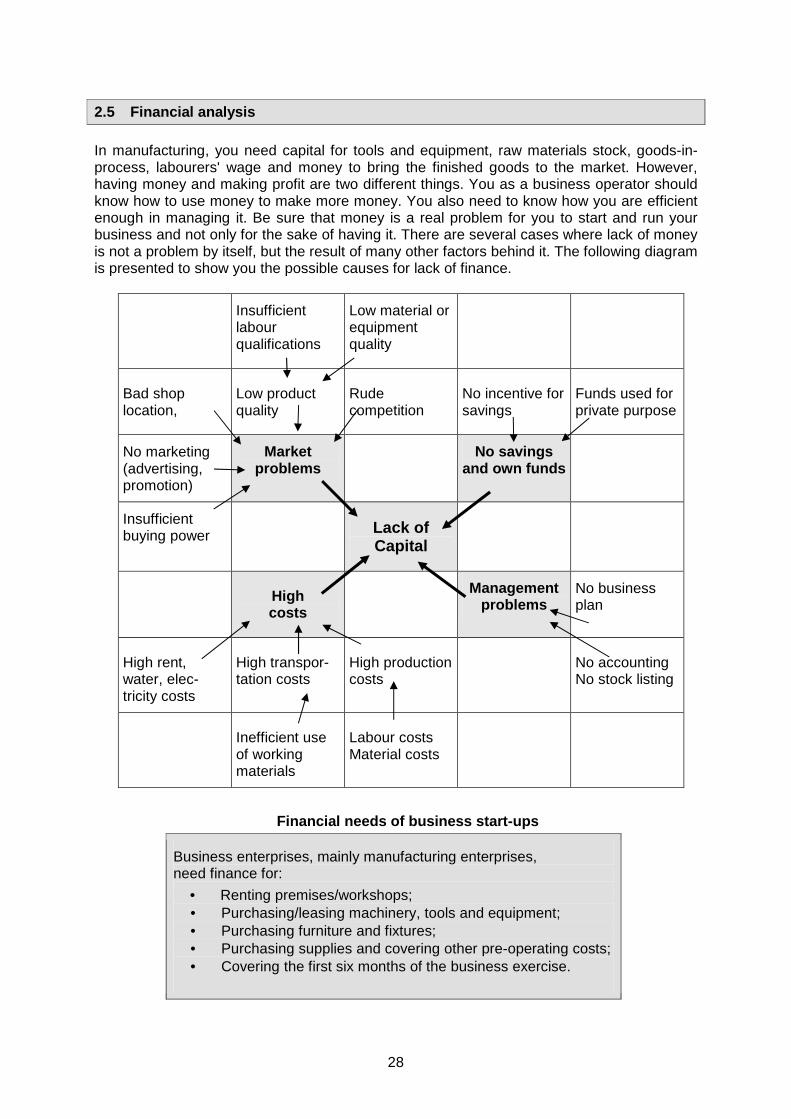

2.5 Financial analysis In manufacturing, you need capital for tools and equipment, raw materials stock, goods-in-process, labourers' wage and money to bring the finished goods to the market. However, having money and making profit are two different things. You as a business operator should know how to use money to make more money. You also need to know how you are efficient enough in managing it. Be sure that money is a real problem for you to start and run your business and not only for the sake of having it. There are several cases where lack of money is not a problem by itself, but the result of many other factors behind it. The following diagram is presented to show you the possible causes for lack of finance.

Insufficient labour qualifications

Low material or equipment quality

Bad shop location,

Low product quality

Rude competition

No incentive for savings

Funds used for private purpose

No marketing (advertising, promotion)

Market problems

No savings and own funds

Insufficient buying power

Lack of Capital

High costs

Management problems

No business plan

High rent, water, elec-tricity costs

High transpor-tation costs

High production costs

No accounting No stock listing

Inefficient use of working materials

Labour costs Material costs

Financial needs of business start-ups

Business enterprises, mainly manufacturing enterprises, need finance for:

• Renting premises/workshops; • Purchasing/leasing machinery, tools and equipment; • Purchasing furniture and fixtures; • Purchasing supplies and covering other pre-operating costs; • Covering the first six months of the business exercise.

29

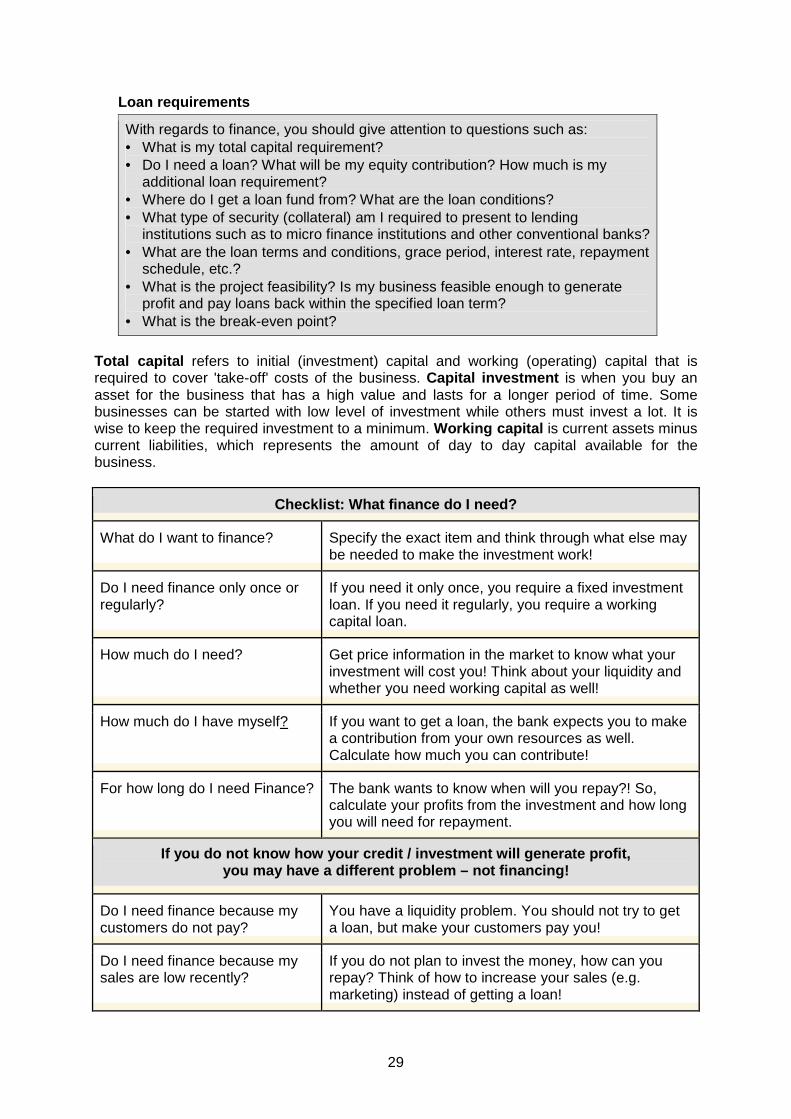

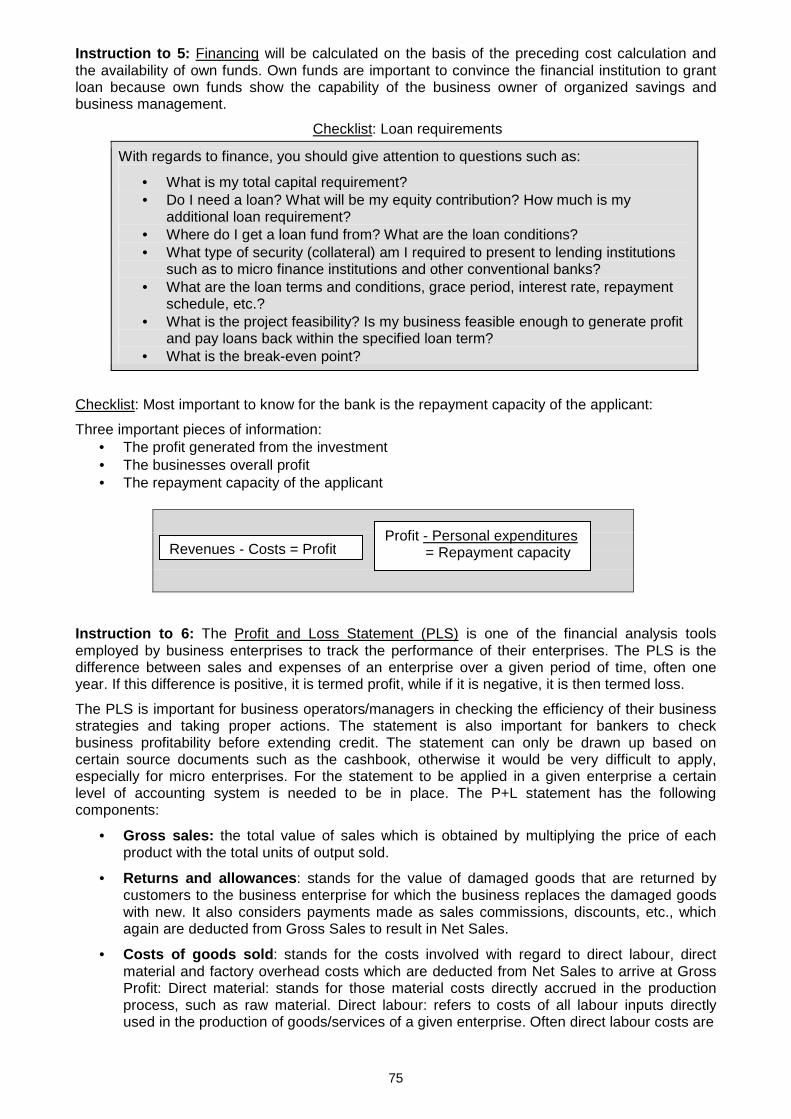

Loan requirements

With regards to finance, you should give attention to questions such as: • What is my total capital requirement? • Do I need a loan? What will be my equity contribution? How much is my

additional loan requirement? • Where do I get a loan fund from? What are the loan conditions? • What type of security (collateral) am I required to present to lending

institutions such as to micro finance institutions and other conventional banks? • What are the loan terms and conditions, grace period, interest rate, repayment

schedule, etc.? • What is the project feasibility? Is my business feasible enough to generate

profit and pay loans back within the specified loan term? • What is the break-even point?

Total capital refers to initial (investment) capital and working (operating) capital that is required to cover 'take-off' costs of the business. Capital investment is when you buy an asset for the business that has a high value and lasts for a longer period of time. Some businesses can be started with low level of investment while others must invest a lot. It is wise to keep the required investment to a minimum. Working capital is current assets minus current liabilities, which represents the amount of day to day capital available for the business.

Checklist: What finance do I need?

What do I want to finance? Specify the exact item and think through what else may be needed to make the investment work!

Do I need finance only once or regularly?

If you need it only once, you require a fixed investment loan. If you need it regularly, you require a working capital loan.

How much do I need? Get price information in the market to know what your investment will cost you! Think about your liquidity and whether you need working capital as well!

How much do I have myself? If you want to get a loan, the bank expects you to make a contribution from your own resources as well. Calculate how much you can contribute!

For how long do I need Finance? The bank wants to know when will you repay?! So, calculate your profits from the investment and how long you will need for repayment.

If you do not know how your credit / investment wil l generate profit, you may have a different problem – not financing!

Do I need finance because my customers do not pay?

You have a liquidity problem. You should not try to get a loan, but make your customers pay you!

Do I need finance because my sales are low recently?

If you do not plan to invest the money, how can you repay? Think of how to increase your sales (e.g. marketing) instead of getting a loan!

30

Research on financing conditions

Inform yourself on the loan conditions of local financial institutions, notably commercial banks, rural banks and micro finance institutions:

• Contact appropriate financial institutions until your loan request is addressed; • Identify and contact appropriate government and donor programs that assist

businesses; • Be sure that you have a financial control system that helps you keep accounts

in acceptable standards. External auditors should also audit your financial statements. Audited financial statements increase the credibility of your business. Financial institutions, in particular, are interested in looking at your financial statements before they issue loans for your business;

• In case you do not have the necessary skills to keep your accounts in good order, you should either attend short-term training in accounting or try to get assistance from others.

What are the best sources to get finance? Sources of finance for sole proprietors

• Personal savings • Loan from friends and relations • Loan from financial institutions • Credit unions

Partnerships • Contribution from partners • Loans from individuals • Loans from financial institutions • Credit facilities

Limited liability companies • Shares: Ordinary, preference (cumulative, non-cumulative and participating) • Debentures1 (ordinary and secured) • Loans from individuals • Loans from financial institutions • Credit facilities

Capital structure Short-term funds up to one year

• Trade credit • Bank borrowing • Bills of exchange • Deferred tax payment.

1 Backed only by the integrity of the borrower, not by collateral, and documented by an agreement called an indenture. One example is an unsecured bond.

31

Medium and long-term loans up to five or more years

• Mortgage debentures secured on specific assets • Floating charge debenture which only becomes a fixed charge on the assets of the

company in the event of certain contingencies. • Preference Shares which are a source of long-term or permanent finance, and are

similar in some respect of loan capital, but they carry the title of part of ownership of the business. The holders of such shares receive their fixed share of profits first and in the event of winding up they are given priority when paying back capital.

• Equity Capital. The major part of long-term business finance is provided in the form of equity capital which includes the accumulated profits over the life of the project. Equity funds are also residual claimants to earnings in that they can participate in earnings only when all creditors and other suppliers of funds have received their interest payment in full. Equity investors received only the residue of funds realized on winding up of a business after all creditors have been paid in full. Equity funds are therefore subject to the greatest risk of all forms of capital and so equity funds are forthcoming only when profit prospects are sufficiently attractive to compensate for the risk involved and this makes it the most expensive source of finance even though it is one essential source of finance. Equity shareholders are the „true“ owners of the business.

Long-term versus short-term

Long-term finance must cover the project cost of fixed investment and the estimated working capital requirements needed for normal operation. These should be procured in the form of equity and long-term credits. „Borrowing short“ to „finance long“ is not advisable. Short-term loans for financing fixed assets or working capital will burden a project’s cash balance with early and heavy principal repayments. The capital structure should be related to the earning power of the project.

Equity versus debts

The combination of equity and loans will determine a project’s debts to equity ration. Relatively heavy reliance on credit offers both advantages and disadvantages:

• Advantages o The rate of interest on loans may be lower than the rate of return on the

project, thus increasing the actual rate of return due to equity. o Since interest is charged against profits, less tax is paid and actual rate of

return due to equity is increased.

• Disadvantages o Interest charges, which are costs, are fixed and due for payment whether

profits are made or not. o Equity leaves management independent (to an extent) while creditors can

interfere with management’s programme. Note: There is no rule for an ideal debt/equity ratio. Each project or alternatives of a set of projects must be considered on their own merits.

32

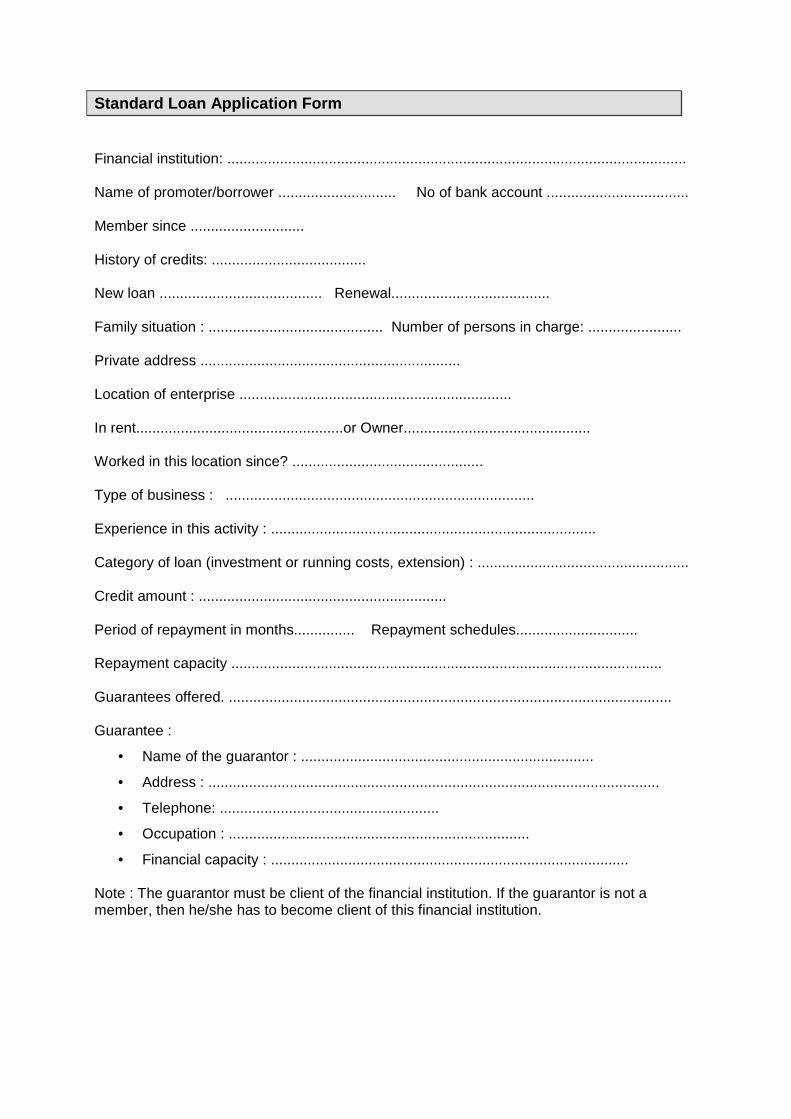

Guide for business consultants and BDS facilitators in order to facilitate access to finance

• The facilitator who deals with the operator often is confronted with operator's financial problems. In order to assess the real needs, it may be useful to get an overview of the situation of the enterprise concerned. What are the real causes for the "lack of finance"? The decisive matter of financing should be the market situation of the enterprises. If the operator meets problems in sales and clients, the facilitator should be hesitating to recommend credit activities. In general a micro or small enterprise with market problems may not be easily able to use the credit in a profitable manner.

• If the enterprise meets a shortage in investment, equipment, raw materials or wants to extend his enterprise by a normal or good sales situation, credit measures may be considered.

• In that case an analysis of the business situation and an analysis of the business projects should be undertaken by writing a business plan . The business plan should be written by the operator him/herself assisted by the facilitator.

• At the same time the operator should be urged to open a savings account and to strengthen his/her savings. Because proper funds are a good condition for a successful loan application procedure.

• Simultaneous to these preparations on operator's level, information on bank or micro-finance level should be obtained. What are the appropriate finance institutions for this kind of business? What are the loan application conditions? Individual or group collateral? Loan ceiling? The interest rates? Repayment period and conditions? Grace period?

• Finally, get the loan application form and help the operator fill out the form.

Institutions involved • Commercial banks, rural banks and micro finance institutions; • Governmental institutions with business support programs; • Donor programs involved in private sector development; • Accounting consultants; • Accounting training centres.

2.6 Legal issues (example of Ghana)

You as a business owner have a legal obligation to adhere to existing laws and regulations. These responsibilities include paying taxes, respecting regulations regarding employees, getting licenses and permits, adhering to lease and contractual agreements. Paying taxes is part of running a business and it applies to every one unless you get short-term preferential treatment from the government. It is, therefore, your responsibility to learn about the legal requirements that concern you as a business person.

Laws and regulation, legal forms of business and business registration in most cases are similar but nevertheless a country specific matter. That is why in the following we develop these issues on the example of Ghana.

33

Engage your own country specific research on the ba sis of the following outline. (personal contacts, yellow pages, Internet research)

a. Laws and regulations - example of Ghana The relevant laws that govern the formation of entities that carry on business in the country are

• the Companies Code, 1963 (Act 179), with regard to companies, • the Incorporated Private Partnerships Act, 1962 (Act 152) ("IPPA"), with regard to

partnerships, • the Statutory Corporations Act, 1964 (Act 232), with regard to statutory corporations,

and • the Registration of Business Names Act, 1962 (Act 151), with regard to

unincorporated business.

The Registrar-General's Department is the government agency responsible for registration and regulation of business entities, except statutory corporations. The labour market is governed by the Constitution, the Labour Decree, 1967 (NLCD 157), the Labour Regulations, 1969 (LI 632), the Industrial Relations Act, 1965 (Act 299) and the Workmen's Compensation Law, 1987 (PNDCL 187). The labour decree , and amendments thereto, apply only to clerical workers whose remuneration does not exceed the prescribed sum, artisans, labourers and domestic servants.

One of the main provisions of the labour decree is the requirement that contracts of employment for more than six months or which stipulate conditions of employment which differ materially from those customary in the relevant district of employment for similar work, must be in writing. Failure to reduce such contracts into writing renders them unenforceable. Furthermore, the decree requires all contracts to be submitted by the employer to the chief labour officer or a labour officer for attestation and registration Any contract which a labour officer refuses to attest, shall have no further validity. Registration is for the purposes of enabling the worker to prove the existence and the terms of the contract and to verify the terms of the contract at any time. The decree also contains detailed provisions on inter alia the termination of contracts of employment, the determination of severance pay, civil proceedings in employment matters, the employment of females, children and young persons. b. Identification of legal forms of business organi sations - example of Ghana

This refers to the determination of what form of business organisation you are going to register your business in. The various kinds of companies are as follows:

Sole proprietor business. The sole proprietor business is the most common for micro and small enterprises in Ghana. The registration procedure for a sole proprietor business is less complicated and costly than for a company limited. The sole proprietor must register at the Registrar-General's Department.

Partnership business. A partnership is an arrangement whereby two or more persons combine some or all of their resources, skills or industry with the objective of making profit which will be shared by the partners.

34

Company limited by shares. In a company limited by shares, the shareholder need not pay the whole amount of his shares to the company at once when acquiring the shares. The usual practice is that shareholders make payments when the directors make "calls" upon them to pay. The shareholder's liabilities are therefore limited to any amounts unpaid on the shares, and once a shareholder has fully paid for his shares, he is not to incur any further liabilities in respect of the company. Thus no contribution is required from any member, exceeding any amount unpaid on his shares, where the company is being wound up. However, the company may decide, by special resolution, to reserve any unpaid liability on shares until the company is being wound up.

The regulations of a company limited by shares must expressly state the fact of the limited liability of members. The last word of the name of a company limited by shares shall be "limited", or its abbreviation "ltd."

Company limited by guarantee. This is a company that has the liability of its members limited to amounts that they respectively undertake or guarantee to contribute to the assets of the company in case of liquidation. Unlike companies limited by shares, where the liability of the member may have to be implemented at any time during the existence of the company, that is, during the active life as well as during winding up, in the guarantee company, that liability need only be implemented after the commencement of the winding up of the company. The companies code provides for the total liability of members, and no further contribution shall be required from any member.

A guarantee company is not registered with shares and is not permitted to create any shares. This type of company is therefore only suitable if no initial funds are required or those funds are obtained from other sources, e.g. endowments and donations. The company is also not permitted to engage in trading. The company is not permitted to pay dividends or distribute/return any assets to members.

Whilst other companies may operate on a "one share, one vote" principle, the operating principle in respect of guarantee companies is "one member, one vote". The regulations of a guarantee company must contain the following mandatory provisions:

• That the liabilities of the members are limited • That the income and property of the company shall be applied solely towards the

promotion of its objects • That no portion of the income and property shall be paid or transferred in any manner

to the members, except payments permitted by the regulations, such as the payment of reasonable and proper remuneration to officers in return for services actually rendered, out-of-pocket expenses, interest not exceeding 6% on money lent to the company, and reasonable and proper rent for premises let to the company. Further, no director is to be appointed to any salaried office. These may be modified only with the approval of the registrar.

• That each member will contribute to the assets of the company in the event of its being wound up, to cater for the payment of the company's debts and obligations, costs of liquidation and other amounts required, up to whatever limit is prescribed by the Regulations. In respect of members, this liability extinguishes only where a person has ceased to be a member for more than a year. Note that membership of a guarantee company may end only by death, valid retirement or any other manner prescribed in the regulations.

• That upon winding up, the residue of the property shall not be distributed to members, but shall be either given to some other guarantee company with similar objects or applied to some charitable purpose. Members before the dissolution of the company shall determine the beneficiary.

Unlimited company. This company is also registered with shares, and, there is no limit on the liability of the members, e.g. they are liable to contribute whatever sums are required to pay the debts of the company in case of bankruptcy. There are not too many of such

35

companies in Ghana. The few that exist are mostly law firms and other professional establishments who may be prevented from operating as limited liability companies by professional ethics.

Public and private companies. Each of the above types of companies may be "private" or "public". A company is a private company if by its regulations, it fulfils the following conditions:

• The total number of members and debenture holders do not exceed 50 debentures are similar to bonds except there are no pledges on specific assets. This number excludes genuine employees and ex-employees of the company who became members or debenture holders during their employment, and continued to be so after their employment. The exclusion of employees is designed to enable companies to institute co-partnerships schemes without forfeiting their private status.

• The company is prohibited from making of any public invitations for the acquisition of its shares and debentures.

• The company is prohibited from making an invitation to the public to deposit money for fixed periods or payable at call, whether interest-bearing or not.

Cooperative. Membership is unrestricted but is for specific purposes such as joint purchase of raw materials and group marketing of products.

External company. Corporate bodies formed outside Ghana that seek to operate in Ghana need not automatically incorporate subsidiaries in Ghana. Such a corporate body is allowed to establish a place of business in Ghana after it has registered with the companies registry as an "external company". Which form of business should I establish? You should consider varieties of conditions before deciding which form of business to establish. Assistance of others may be needed to select and register your business. But make the selection by yourself and try to understand why you should select that form and what consequences it will have in the future.

Basis for which form of business to select

Ease of registration requirement and simplicity of the process • Registration of limited company is relatively complicated.

Cost of starting the business

• Sole partnership and co-operative forms involve low cost; • Limited company involves high cost.

Number of owners

• Sole proprietorship - only one owner; • Partnership - at least two owners; • Private limited companies - at least two owners; • Share company- 5 or more share holders; • Co-operative - at least 10 members.

Financial responsibility of the owners

• Sole proprietorship - unlimited personal liability by the owner for all debts; • Partnership - unlimited personal liability by the owners for all debts; • Limited company - no personal liability by the shareholders for the debts; • Co-operative - no personal liability by the members for the debts.

36

Decision making in the business

• Sole proprietorship - all decisions are made by the owner; • Partnership - decisions are made jointly by all owners, unless agreed

otherwise; • Limited company - shareholders appoint board of directors who in turn can

appoint managers to run the business; • Co-operative - every member has one vote, a management committee is often

appointed.

Mode of taxation • Sole proprietorship - the owner is taxed for business profits; • Partnership - the owners are taxed individually for their share of business

profits; • Limited company - the company pays tax for business profit; • Co-operative - the co-operative may pay tax for business profit or be made

exempt for a period of time.

c. Business registration

After selecting one of the above forms of business organisations, the next procedure is to register your business with the Registrar-General at the Registrar-General’s Department.

Registration procedure Application for registration of a company is made directly, or through agents or solicitors, to the Registrar-General. A company is duly registered after the company's regulations have been submitted to the registrar of companies and a certificate of incorporation issued. A specified fee is paid on presentation of the regulations. The information required includes:

• the name of the company with the word "limited" as the last word in the name; • the nature of the company's business; • a statement that the company possesses all the powers of a natural person of full

capacity; • the names of the first directors of the company; • a statement that the liability of the company is limited; • the share capital and its division into shares of no par value; • limitation on the powers of the board of directors in accordance with section 202 of

the companies code; • any other lawful provisions relating to the constitution and administration of the

company.

The requirements for a public company limited by shares are similar to those stated above, except that the public can buy shares.

Before commencing business , further information on the company must be provided. This includes the particulars of the company and a declaration of compliance. The particulars of the company are given on form no. 3 and signed by the directors and the company secretary. The information provided must include:

• name of company; • authorized business; • particulars of directors (at least two) and a secretary; • name and address of auditors; • addresses of the company's registered office and principal place of business;

37

• address at which register of members is maintained; • amount of stated capital; number of authorized and issued shares, amount paid

(other than cash), and amount due for each class.