Embed Size (px)

Citation preview

State Finances

NASACTSanta Fe

August 13, 2014

Scott PattisonExecutive Director

National Association of State Budget Officers444 North Capitol Street, NW, Suite 642 • Washington, DC 20001 • (202) 624-5382 • www.nasbo.org

NASBO 2

Current Economic and Fiscal Situation for States

NASBO

State Fiscal Overview

Most states -- stability and slow growth

Revenue growth less in fiscal 2014 and 2015 than fiscal 2013

Most states: budgets with spending increases

Additional spending on K-12, higher education, and healthcare

3

NASBO 4

NASBO 5

Current Fiscal Situation:

Indicators

NASBO

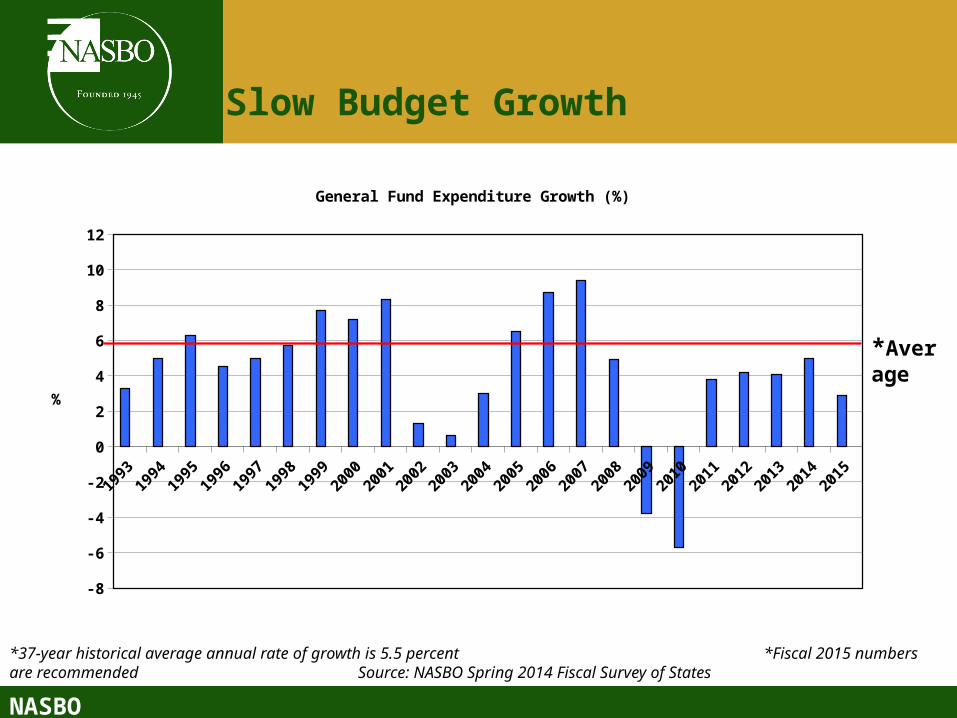

Slow Budget Growth

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

-8

-6

-4

-2

0

2

4

6

8

10

12

General Fund Expenditure Growth (%)

%

*37-year historical average annual rate of growth is 5.5 percent *Fiscal 2015 numbers are recommended Source: NASBO Spring 2014 Fiscal Survey of States

*Average

NASBO

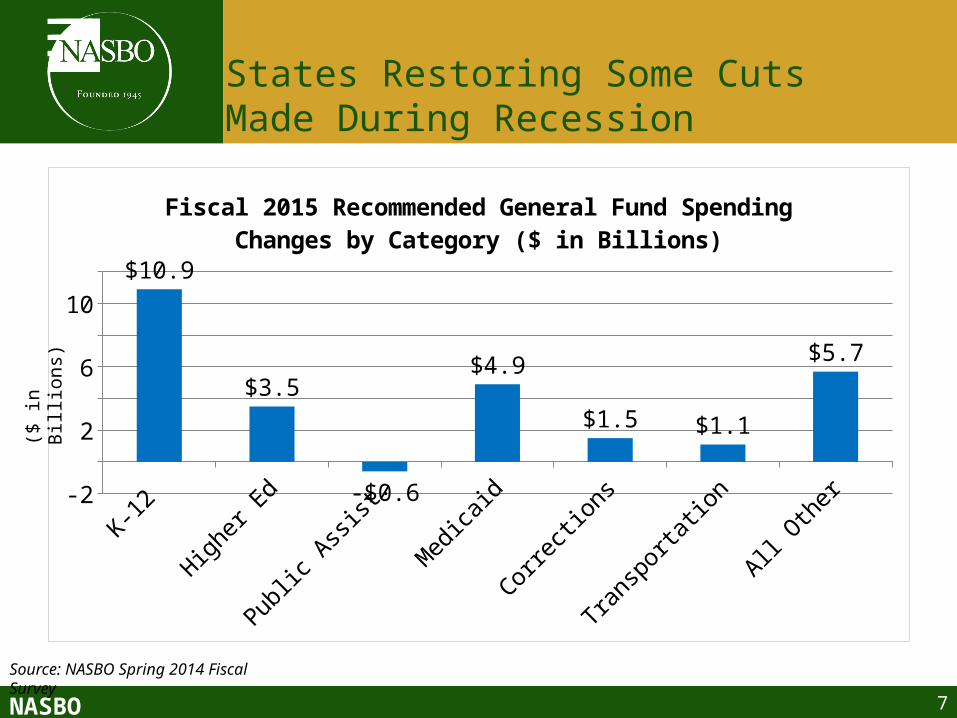

States Restoring Some CutsMade During Recession

K-12

Higher

Ed

Public

Ass

ist.

Med

icaid

Corre

ction

s

Trans

porta

tion

All Oth

er-2

0

2

4

6

8

10

12 $10.9

$3.5

-$0.6

$4.9

$1.5 $1.1

$5.7

Fiscal 2015 Recommended General Fund Spending Changes by Category ($ in Billions)

7

($ in

Bill

ions)

Source: NASBO Spring 2014 Fiscal Survey

NASBO

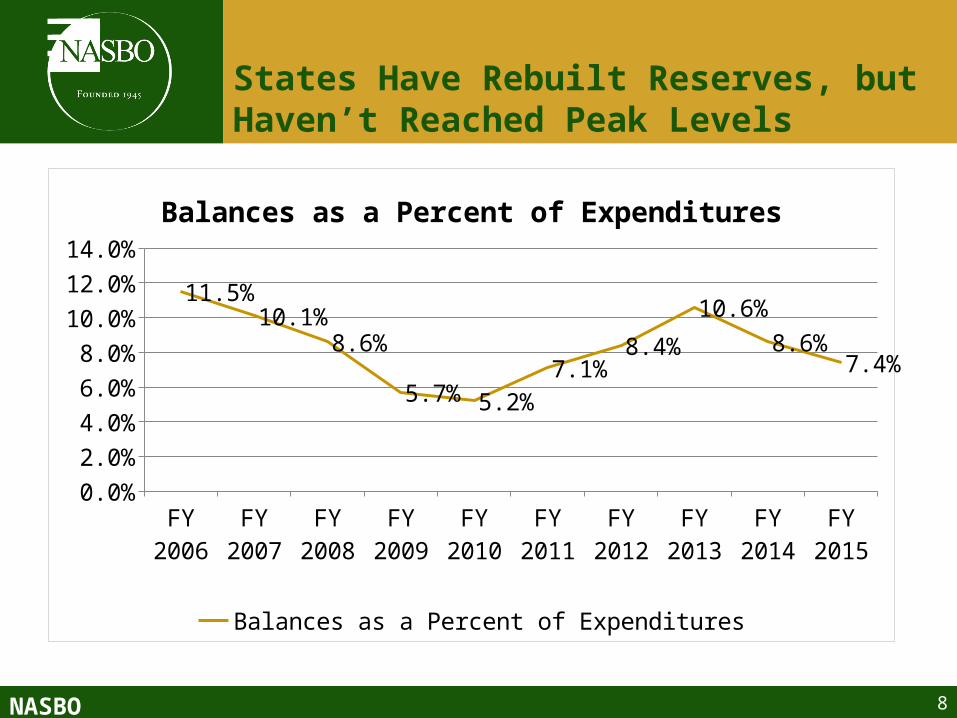

States Have Rebuilt Reserves, but Haven’t Reached Peak Levels

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

FY 2015

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

11.5%10.1%

8.6%

5.7% 5.2%

7.1%8.4%

10.6%

8.6%7.4%

Balances as a Percent of Expenditures

Balances as a Percent of Expenditures

8

NASBO

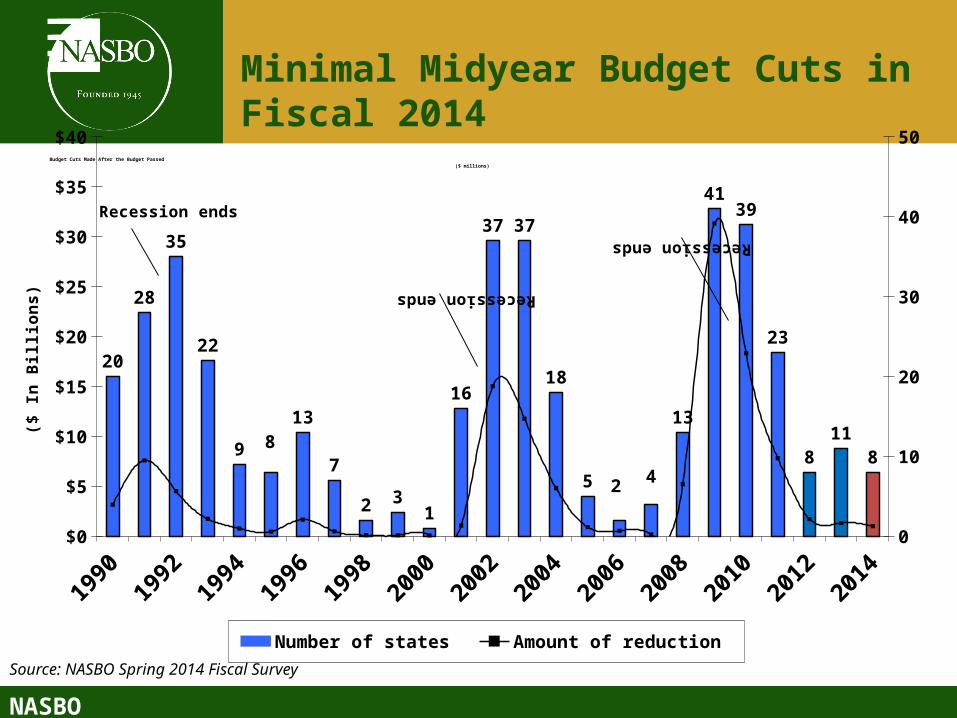

Budget Cuts Made After the Budget Passed ($ millions)

Source: NASBO Spring 2014 Fiscal Survey

Minimal Midyear Budget Cuts in Fiscal 2014

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

$0

$5

$10

$15

$20

$25

$30

$35

$40

0

10

20

30

40

50

20

28

35

22

9 813

7

2 31

16

37 37

18

5 2 4

13

4139

23

811

8

Number of states Amount of reduction

Recession ends

Recession ends

Recession ends

($ I

n B

illio

ns)

NASBO 10

Critical Challenges

NASBO 11

NASBO 12

NASBO

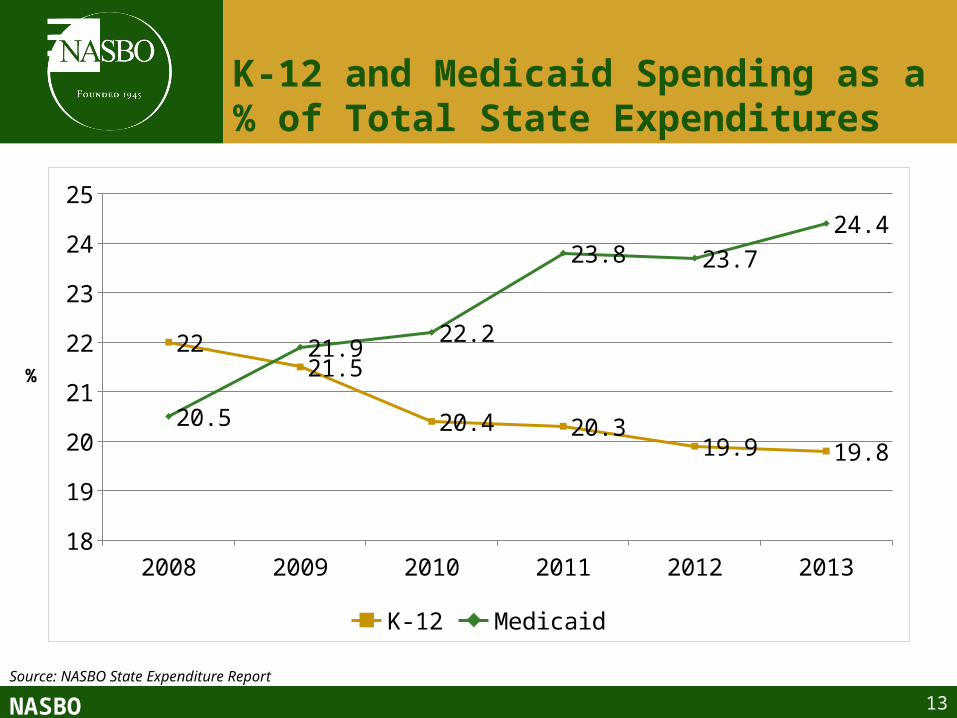

K-12 and Medicaid Spending as a % of Total State Expenditures

13

%

Source: NASBO State Expenditure Report

2008 2009 2010 2011 2012 201318

19

20

21

22

23

24

25

2221.5

20.4 20.319.9 19.8

20.5

21.922.2

23.8 23.7

24.4

K-12 Medicaid

NASBO 14

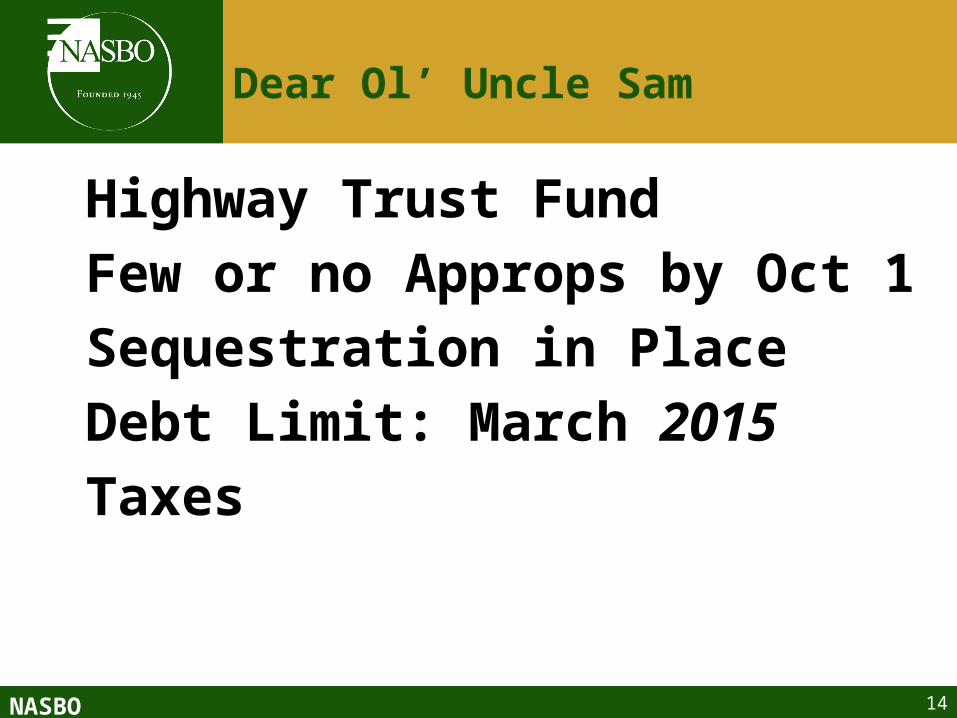

Dear Ol’ Uncle Sam

Highway Trust Fund

Few or no Approps by Oct 1

Sequestration in Place

Debt Limit: March 2015

Taxes

NASBO 15

Revenue Issues

Income Tax/Fiscal CliffSalesGaming becoming limited

NASBO 16

Background on State Spending Trends

NASBO 17

Education Prisons

Transportation Health

NASBO

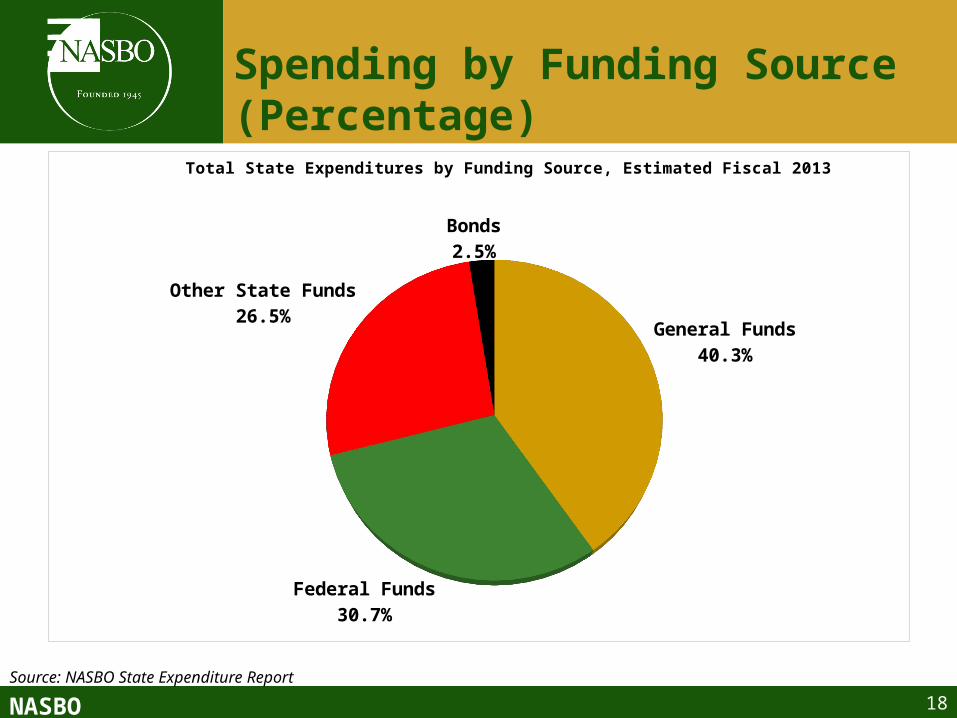

Spending by Funding Source(Percentage)

General Funds40.3%

Federal Funds30.7%

Other State Funds26.5%

Bonds2.5%

Total State Expenditures by Funding Source, Estimated Fiscal 2013

18

Source: NASBO State Expenditure Report

NASBO

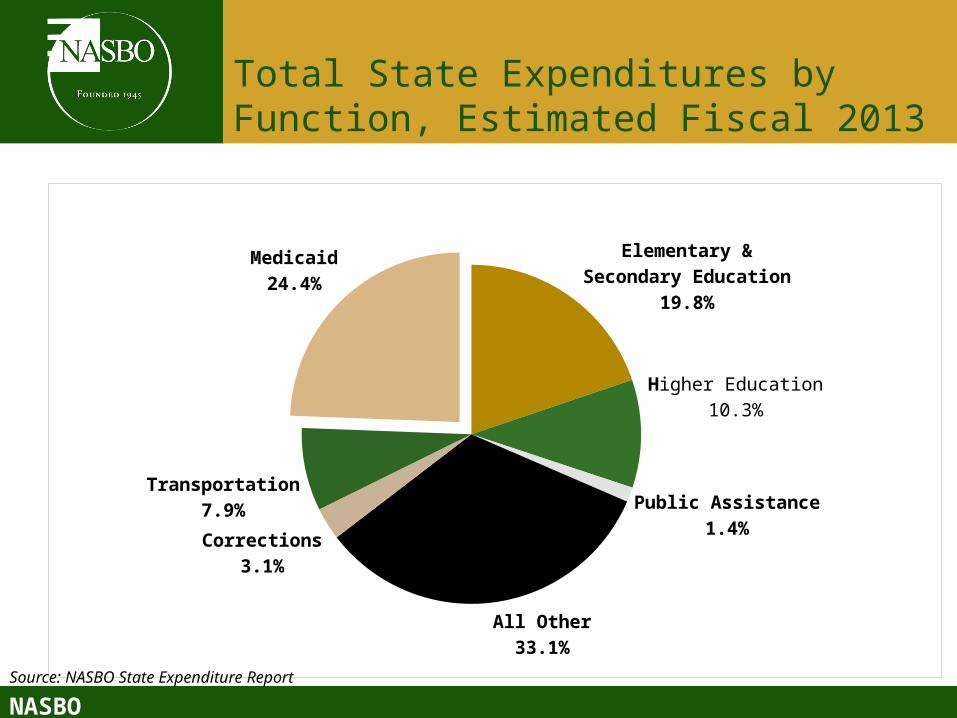

Total State Expenditures by Function, Estimated Fiscal 2013

Elementary & Secondary Education

19.8%

Higher Education10.3%

Public Assistance1.4%

All Other33.1%

Corrections3.1%

Transportation7.9%

Medicaid24.4%

Source: NASBO State Expenditure Report

NASBO

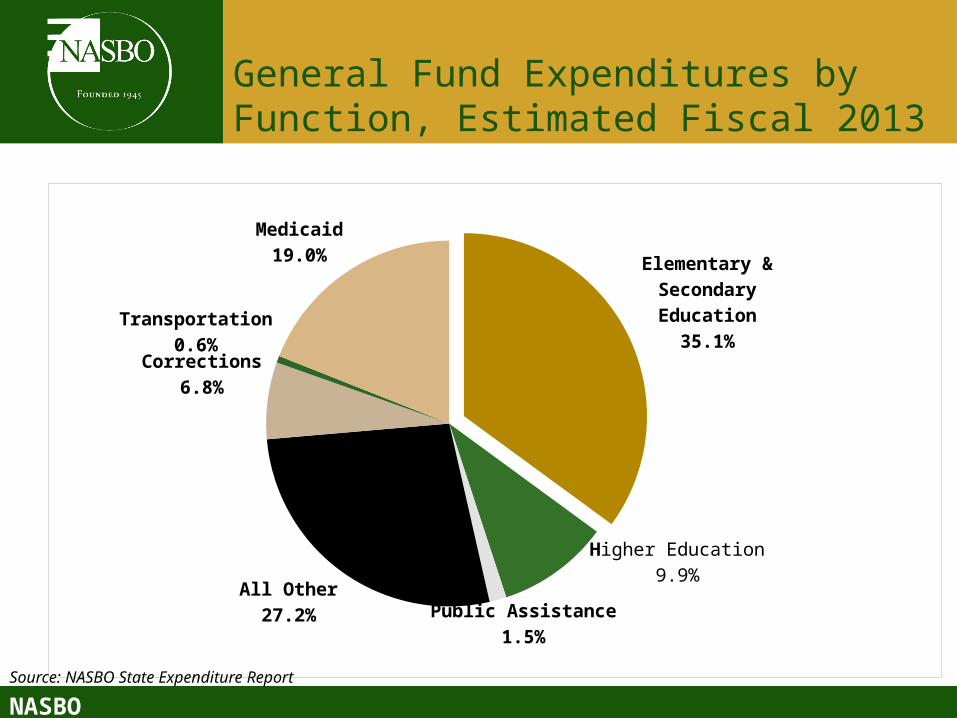

General Fund Expenditures by Function, Estimated Fiscal 2013

Elementary & Secondary Educa-

tion35.1%

Higher Education9.9%

Public Assistance1.5%

All Other27.2%

Corrections6.8%

Transportation0.6%

Medicaid19.0%

Source: NASBO State Expenditure Report

NASBO 21

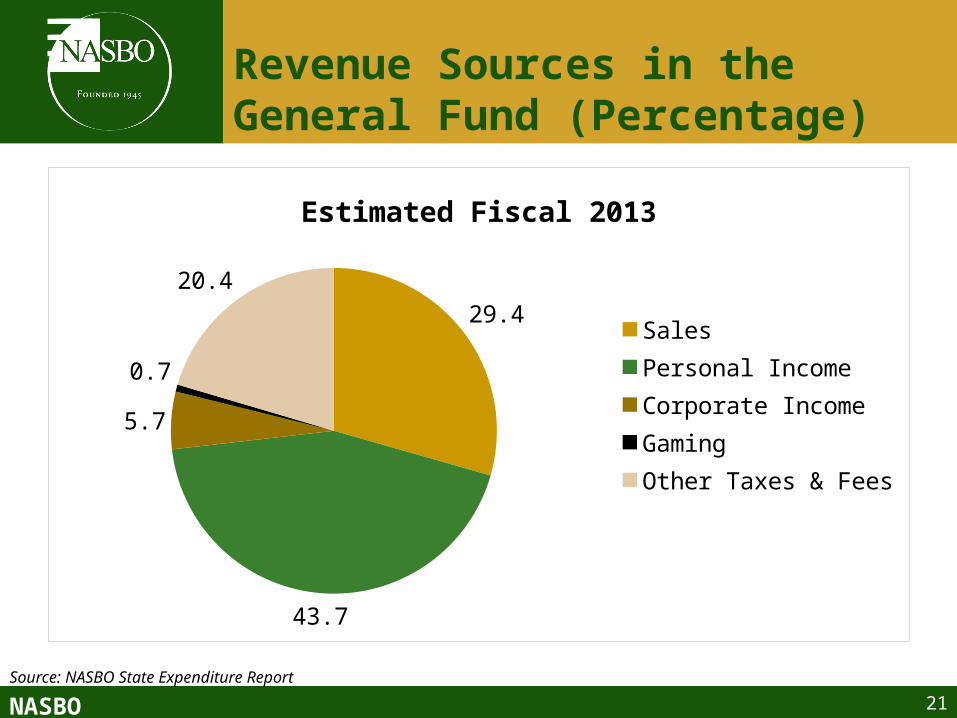

Revenue Sources in the General Fund (Percentage)

Source: NASBO State Expenditure Report

29.4

43.7

5.7

0.7

20.4

Estimated Fiscal 2013

Sales Personal IncomeCorporate IncomeGamingOther Taxes & Fees

NASBO 22

Outlook

NASBO 23

NASBO 24

State Fiscal Outlook

Slow increase in spending

Revenue growth remains slow in fiscal 2015

Challenges: infrastructure, long-term liabilities

“Crowd Out”

Federal impacts