Embed Size (px)

Citation preview

1

SSTTAATTEE OOFF AAGGRRIICCUULLTTUURREE IINN MMAANNIITTOOBBAA

2

Manitoba’s agricultural industry is built on the fact that Manitoba has a land base capable of virtually endless sustained farm production. Crop and livestock commodities are produced in: - an environment recognized worldwide for its pollution free quality, - a research network that is clearly focused on future development of the end-product, - a producer knowledge base that is both innovative and aggressive, - policies that are supportive to the growth of the industry, - an infrastructure that facilitates an effective market strategy; and - a cooperative spirit within industry and government that is committed to growth and

prosperity for the province. As the world demand for food continues to increase, opportunities for growth are significant for all sectors of agricultural production in Manitoba. Continued success of agricultural sectors in Manitoba and Canada is to a degree contingent on the ability to establish recognizable standards and regulations for both production, processing and marketing the commodity. These regulations have to be in balance with the economics of production, the realities of provable health claims from utilization and the marketing factors that are characteristic of the industry. It is paramount to recognize the fact that specialty commodities, while rooted in a long history in many parts of the world, are very much in their relative infancy in the North American marketplace and as such, extensive changes can be expected as the industry develops. There must be sufficient speed and flexibility in the regulatory aspects of the industry and the marketing mechanisms to allow for inevitable change in the industry. Manitoba has the opportunity to become a center for new crop production in Canada and North America and the potential to become a major world player in the international marketplace. Success in this sector is dependent on the willingness to be progressive and take action to combine and coordinate research efforts across the Prairies, thus enabling faster development of new new products in the western provinces. Now is the time for industry, government, research, producers, to function and operate as a single force targeting the development of new opportunities in Manitoba.

3

Real GDP (% Change)

MANITOBA’S ECONOMY: DIVERSE, DEVELOPED AND DYNAMIC The Manitoba economy is mature and well balanced, with a variety of industries ranging from resource-based enterprises to leading-edge technology and business services. This wide range of industries shields the economy from boom-and-bust cycles that disrupt less diversified regions. It also means that businesses can count on a full-spectrum economy with all the services needed to succeed. While the Manitoba economy is well developed, it is also dynamic and growing. The provincial economy continues to expand at a stable and modest pace. Despite a sharp decrease in agricultural production, due to wet weather conditions, Manitoba’s real GDP increased by 2.2% in 2011 according to projections from the Manitoba Bureau of Statistics. Statistics Canada estimated that Manitoba’s real GDP increased by 2.4% in 2010, following a 0.3% contraction in 2009; Manitoba has also led all provinces in average annual growth over the last fiveyears (2005‐2010). Manitoba’s economic growth is expected to improve slightly over the next two years. The Manitoba Finance survey of economic forecasters conducted in February 2012, projects that Manitoba’s real GDP will expand 2.3% in 2012, above the national increase of 2.0%. In 2013, Manitoba’s real GDP is expected to increase 2.5%, also above the projected national increase of 2.4%. Despite the steady outlook for Manitoba, the current global economic circumstances remain fragile, with significant downside risks in several key regions of the world. While the employment situation is improving in the U.S., the precarious fiscal austerity measures and financial markets in Europe are weighing down on near-term global demand for goods and services. For Manitoba, the challenges also include the strengthening Canadian dollar and soil moisture conditions for agriculture and related industries. The Manitoba economy was built on resource sectors such as agriculture, forestry, mining and transportation. These traditional resource sectors will continue to play a fundamental role in the economy as they begin to diversify exports and process more commodity goods in the province. The agriculture sector, in particular, is in the midst of dynamic change. Traditionally focussed on the production of grain for export, it is rapidly shifting toward more production of livestock, particularly hogs. The sector is also diversifying into many new commodities such as buffalo, elk and non-traditional crops. While primary agriculture accounts for a small share of the total economy, it is at the heart of the agriculture and agri-food system. Any changes in commodity markets can have impacts on the performance of the primary agriculture industry and the whole supply chain.

4

CONTRIBUTION OF AGRICULTURE In Manitoba, the agricultural industry is a key driver of productivity and prosperity. The diversity of agriculture in the province plays an important role in maintaining economic strength and generating socio-economic stability.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

500

1000

1500

2000

2500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% o

f M

an

ito

ba

GD

P

MIL

LIO

NS

OF

DO

LL

AR

S

YEAR

GDP - Agricultural Sector - Manitoba2002 - 2011

Crop and Animal Production Percent of Provincial GDP

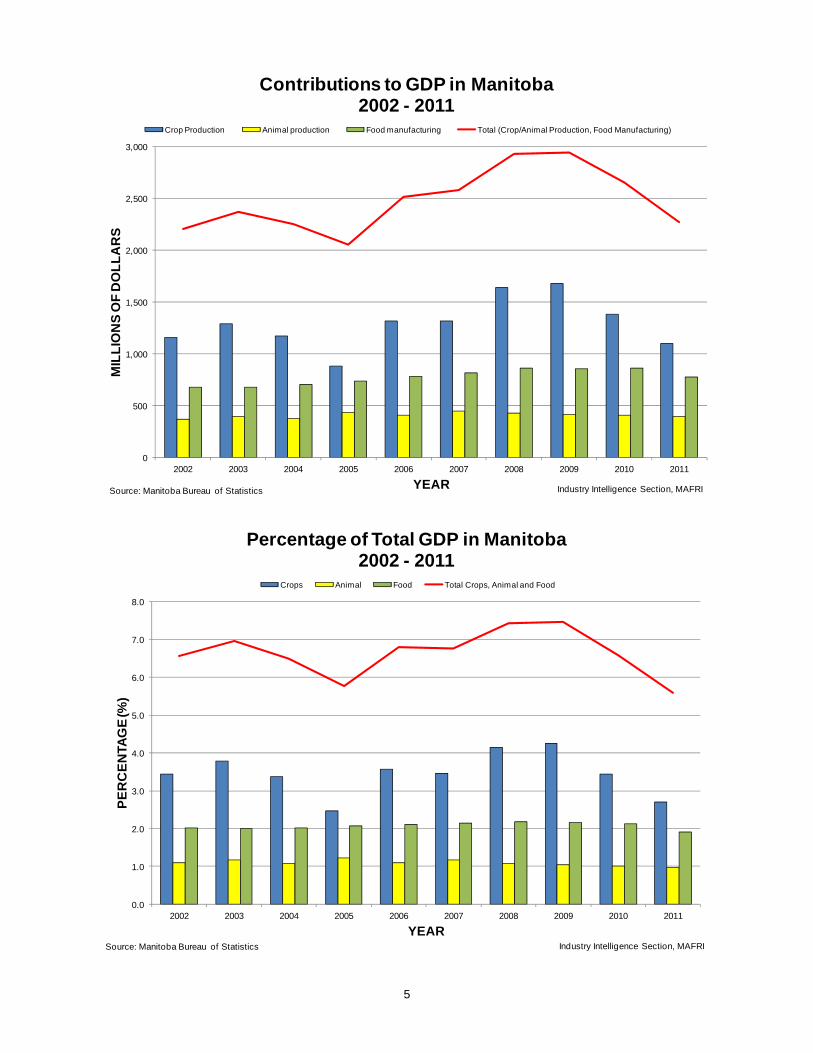

Industry Intelligence Section, MAFRISource: Manitoba Bureau of Statistics Agriculture contributes to Manitoba’s Gross Domestic Product (GDP) through net profilts and incomes including wages, depreciation and investment income. Improvements in GDP can be attributed to improved crop prices and production. Historically, agriculture’s direct and indirect contribution to GDP ranges between 4.4% and 4.8%. Food processing represents close to one-quarter of the total manufacturing output and with approximately $4 billion of foods processed, contributes an additional 2 to 4% to provincial GDP. Agriculture supports growth and employment in the rural economy by providing a market for services needed by the industry. Agriculture-connected industries, including food and beverage processing, supply inputs to agriculture, as well as wholesale, retail and other service sector components which supply services to farmers and other agriculture-related workers. When agri-food's indirect contribution to the GDP is added to its direct contribution, an estimated 9% of Manitoba's GDP is attributed to agriculture in 2011. It is estimated that when tierciary level contributions are included, the total impact on GDP may be closer to 12%.

5

0

500

1,000

1,500

2,000

2,500

3,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

NS

OF

DO

LL

AR

S

YEAR

Contributions to GDP in Manitoba2002 - 2011

Crop Production Animal production Food manufacturing Total (Crop/Animal Production, Food Manufacturing)

Industry Intelligence Section, MAFRISource: Manitoba Bureau of Statistics

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

PE

RC

EN

TAG

E (%

)

YEAR

Percentage of Total GDP in Manitoba2002 - 2011

Crops Animal Food Total Crops, Animal and Food

Industry Intelligence Section, MAFRISource: Manitoba Bureau of Statistics

6

Farms contribute directly to the economy by employing people and paying wages and salaries. In Manitoba 36.7% of all farms in the province reported paid labour for the year 2010. The census counted 19,827 paid employees, of whom 44.6% worked year-round in a full or part-time capacity. Business-to-business transactions include purchases from suppliers such as feed, fertilizer, seed and chemicals, veterinary services, trucking services, electricity, insurance, farm and equipment repairs and maintenance, etc. Farm income is spent at retail outlets, pay mortgages or rent, buy vehicles, purchase property insurance, incur medical, financial, legal and other expenses. The economic activity supported by agriculture also supports tax revenues used to fund public services. It is estimated that between 1 in 10 jobs depends on direct and indirect spin-offs from agriculture. In agriculture, GDP growth is a valuable economic indicator to measure progress in terms of the rate of expansion in the economy's capacity of the industry to produce goods and services. Economic growth occurs from accumulating knowledge and skills, investing in buildings, machinery and equipment, and the implementation of new technologies in the production process.

0 5 10 15 20 25 30

Other Services

Trade

Manufacturing

Finance, Insur & Real Estate

Government

Transportation & Warehousing

Construction

Agriculture

Utilities

Info, Culture, Arts, Rec.

Mining & Other Primary

PERCENT

SE

CT

OR

S

Industrial Shares of Manitoba GDP in 2011

Industry Intelligence Section, MAFRISource: Manitoba Bureau of Statistics

7

Overview of Manitoba’s Agriculture Industry

8

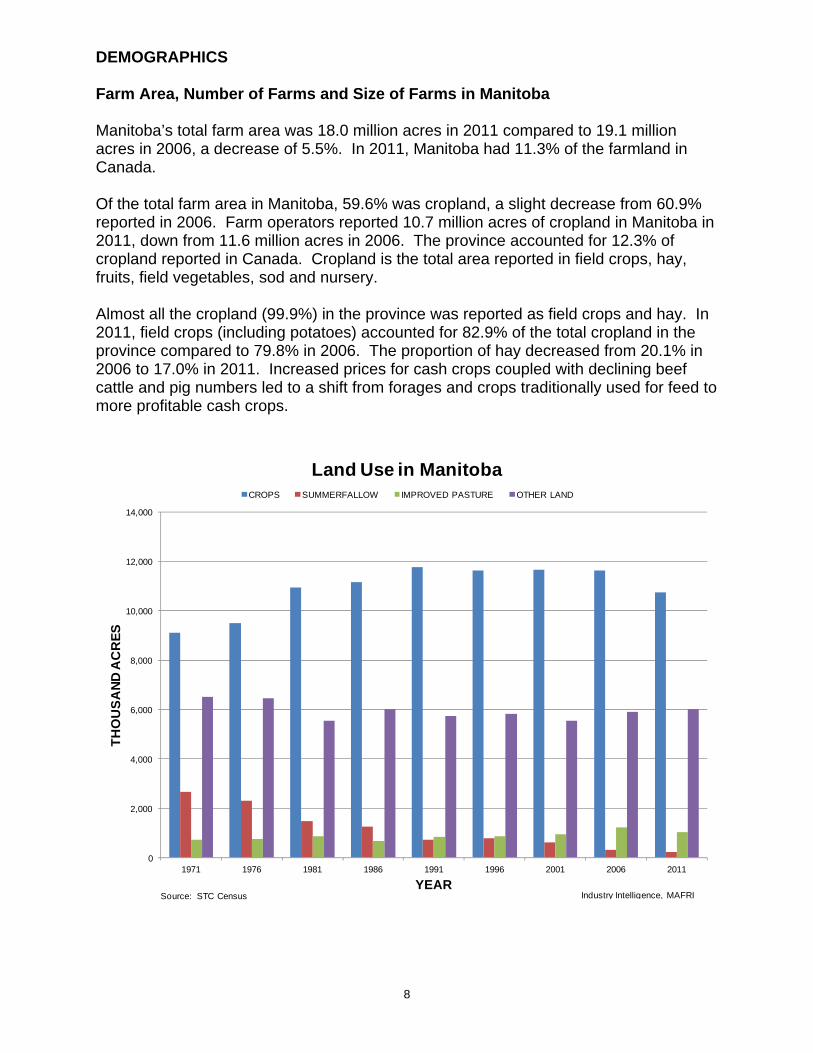

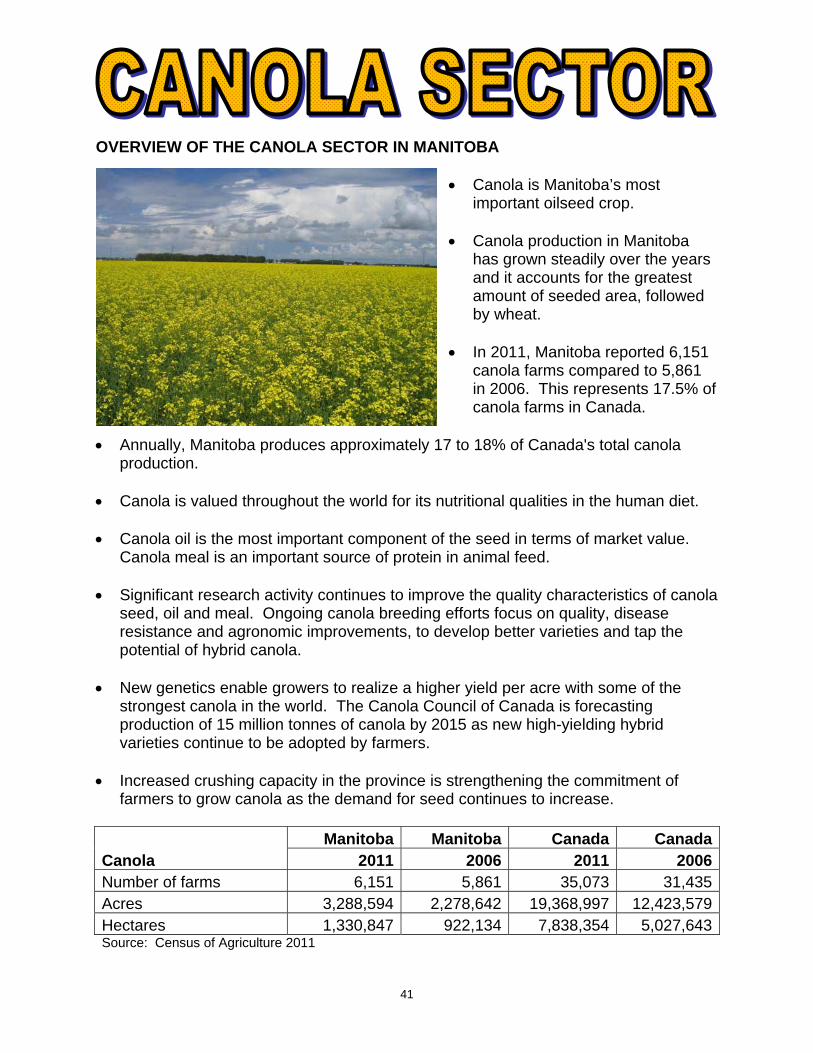

DEMOGRAPHICS Farm Area, Number of Farms and Size of Farms in Manitoba Manitoba’s total farm area was 18.0 million acres in 2011 compared to 19.1 million acres in 2006, a decrease of 5.5%. In 2011, Manitoba had 11.3% of the farmland in Canada. Of the total farm area in Manitoba, 59.6% was cropland, a slight decrease from 60.9% reported in 2006. Farm operators reported 10.7 million acres of cropland in Manitoba in 2011, down from 11.6 million acres in 2006. The province accounted for 12.3% of cropland reported in Canada. Cropland is the total area reported in field crops, hay, fruits, field vegetables, sod and nursery. Almost all the cropland (99.9%) in the province was reported as field crops and hay. In 2011, field crops (including potatoes) accounted for 82.9% of the total cropland in the province compared to 79.8% in 2006. The proportion of hay decreased from 20.1% in 2006 to 17.0% in 2011. Increased prices for cash crops coupled with declining beef cattle and pig numbers led to a shift from forages and crops traditionally used for feed to more profitable cash crops.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1971 1976 1981 1986 1991 1996 2001 2006 2011

TH

OU

SA

ND

AC

RE

S

YEAR

Land Use in ManitobaCROPS SUMMERFALLOW IMPROVED PASTURE OTHER LAND

Industry Intelligence, MAFRISource: STC Census

9

The proportion of pasture (tame or seeded pasture and natural land for pasture), summerfallow and woodlands in total farm area decreased while the proportion of other land increased to 5.7% in 2011 from 2.4% in 2006. Manitoba experienced severe flooding in the spring and summer of 2011 and land reported to the 2011 Census of Agriculture as “too wet to seed” has been categorized as “other land” and not cropland or summerfallow; this land could shift back to cropland when conditions improve. The 2011 Census of Agriculture counted 15,877 census farms in Manitoba, a 16.7% decrease since 2006. This compares to a 10.3% decrease at the national level and reflects the continued out-migration of farm operators, farm consolidation and farm retirements. A census farm is an agricultural operation that produces agricultural products intended for sale. Manitoba accounted for 7.7% of Canada’s 205,730 farms in 2011, lower than its 8.3% share in 2006.

0

200

400

600

800

1,000

1,200

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1881

1886

1891

1896

1901

1906

1911

1916

1921

1926

1931

1936

1941

1946

1951

1956

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

AV

ER

AG

E F

AR

M S

IZE

(ac

res

)N

UM

BE

R O

F F

AR

MS

CENSUS YEAR

FARM NUMBERS AND SIZE IN MANITOBA1881- 2011

NUMBER OF FARMS AVERAGE FARM SIZE (acres)

Industry Intelligence, MAFRISource: Statistics Canada While the overall number of farms in Manitoba has been declining and despite the decrease in total farm area, average area per farm has increased. The average Manitoba farm was 1,001 acres in 2006, up 12.3 % from 891 acres in 2001.

10

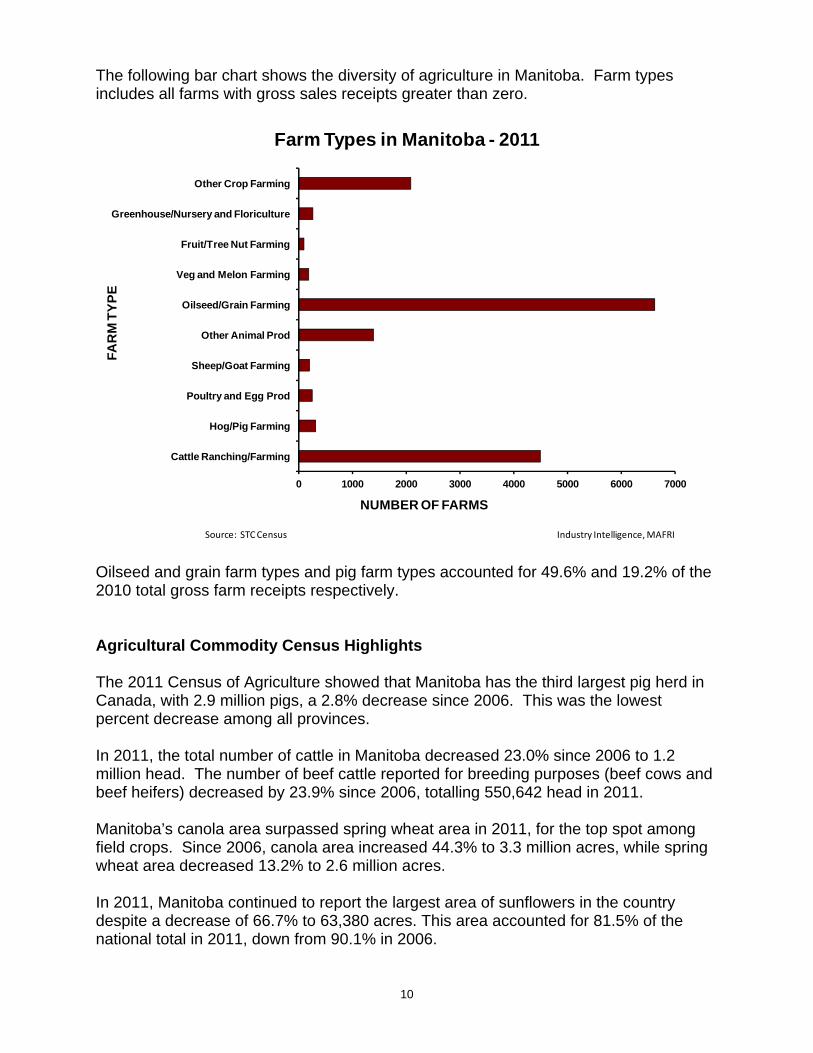

The following bar chart shows the diversity of agriculture in Manitoba. Farm types includes all farms with gross sales receipts greater than zero.

0 1000 2000 3000 4000 5000 6000 7000

Cattle Ranching/Farming

Hog/Pig Farming

Poultry and Egg Prod

Sheep/Goat Farming

Other Animal Prod

Oilseed/Grain Farming

Veg and Melon Farming

Fruit/Tree Nut Farming

Greenhouse/Nursery and Floriculture

Other Crop Farming

NUMBER OF FARMS

FA

RM

TY

PE

Farm Types in Manitoba - 2011

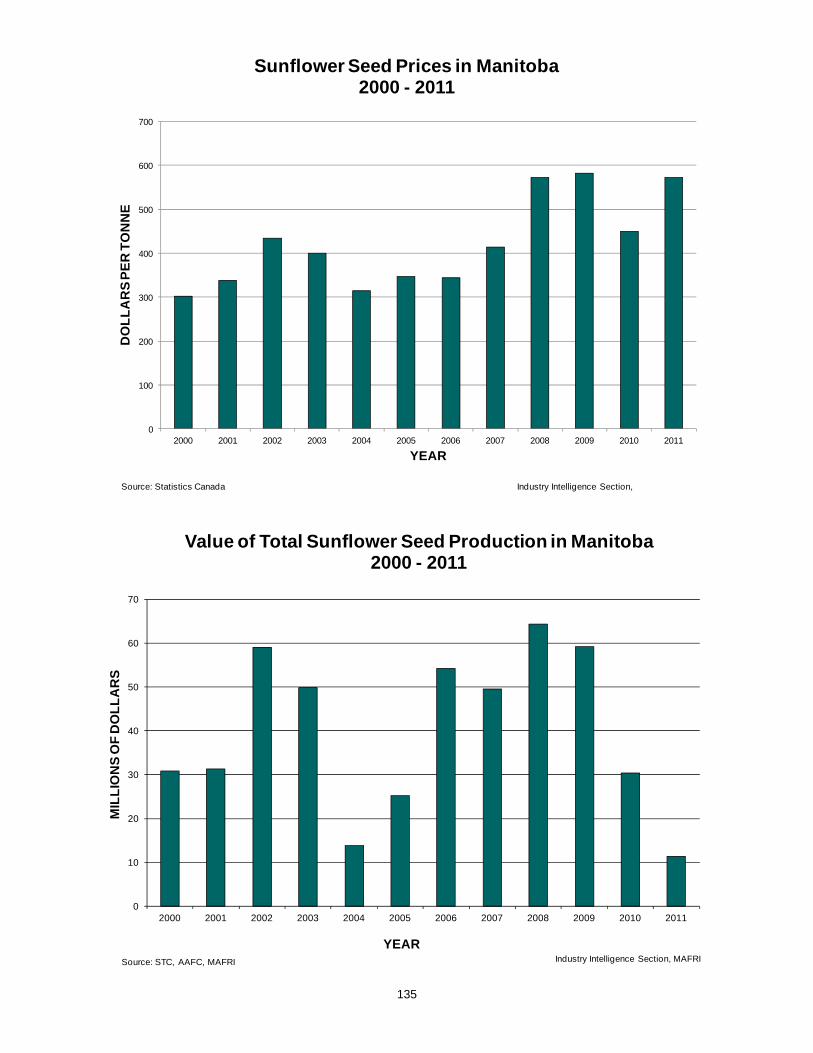

Industry Intelligence, MAFRISource: STC Census Oilseed and grain farm types and pig farm types accounted for 49.6% and 19.2% of the 2010 total gross farm receipts respectively. Agricultural Commodity Census Highlights The 2011 Census of Agriculture showed that Manitoba has the third largest pig herd in Canada, with 2.9 million pigs, a 2.8% decrease since 2006. This was the lowest percent decrease among all provinces. In 2011, the total number of cattle in Manitoba decreased 23.0% since 2006 to 1.2 million head. The number of beef cattle reported for breeding purposes (beef cows and beef heifers) decreased by 23.9% since 2006, totalling 550,642 head in 2011. Manitoba’s canola area surpassed spring wheat area in 2011, for the top spot among field crops. Since 2006, canola area increased 44.3% to 3.3 million acres, while spring wheat area decreased 13.2% to 2.6 million acres. In 2011, Manitoba continued to report the largest area of sunflowers in the country despite a decrease of 66.7% to 63,380 acres. This area accounted for 81.5% of the national total in 2011, down from 90.1% in 2006.

11

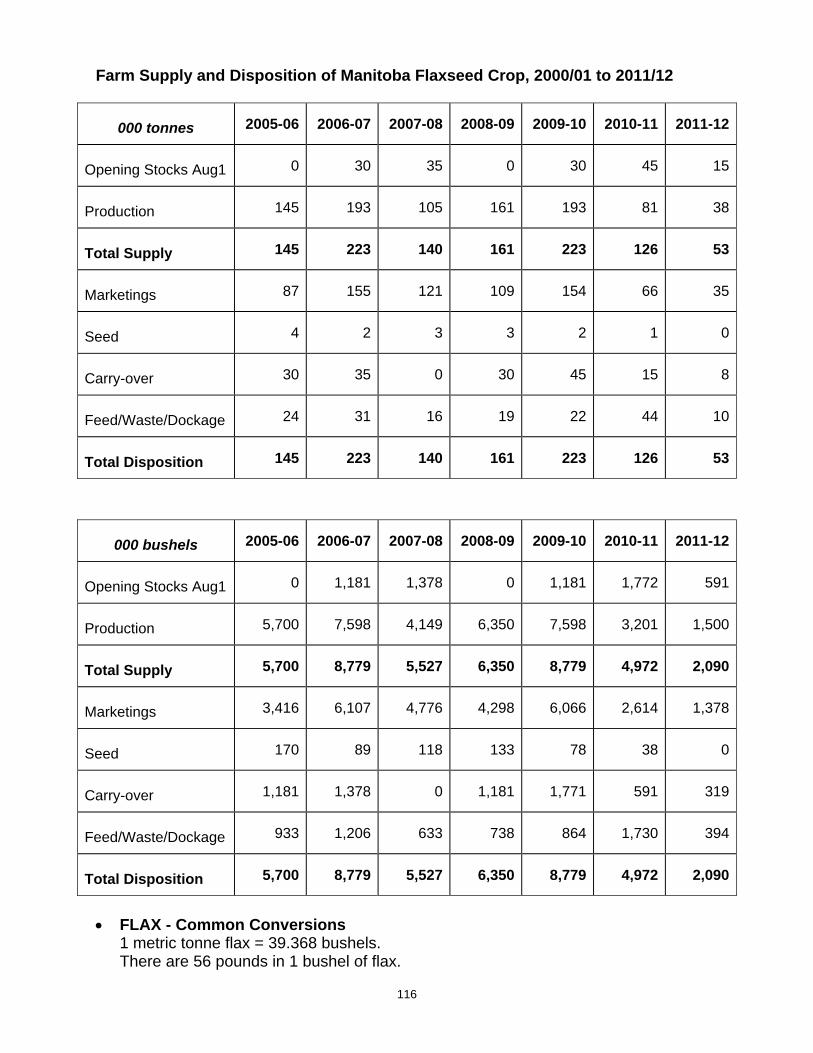

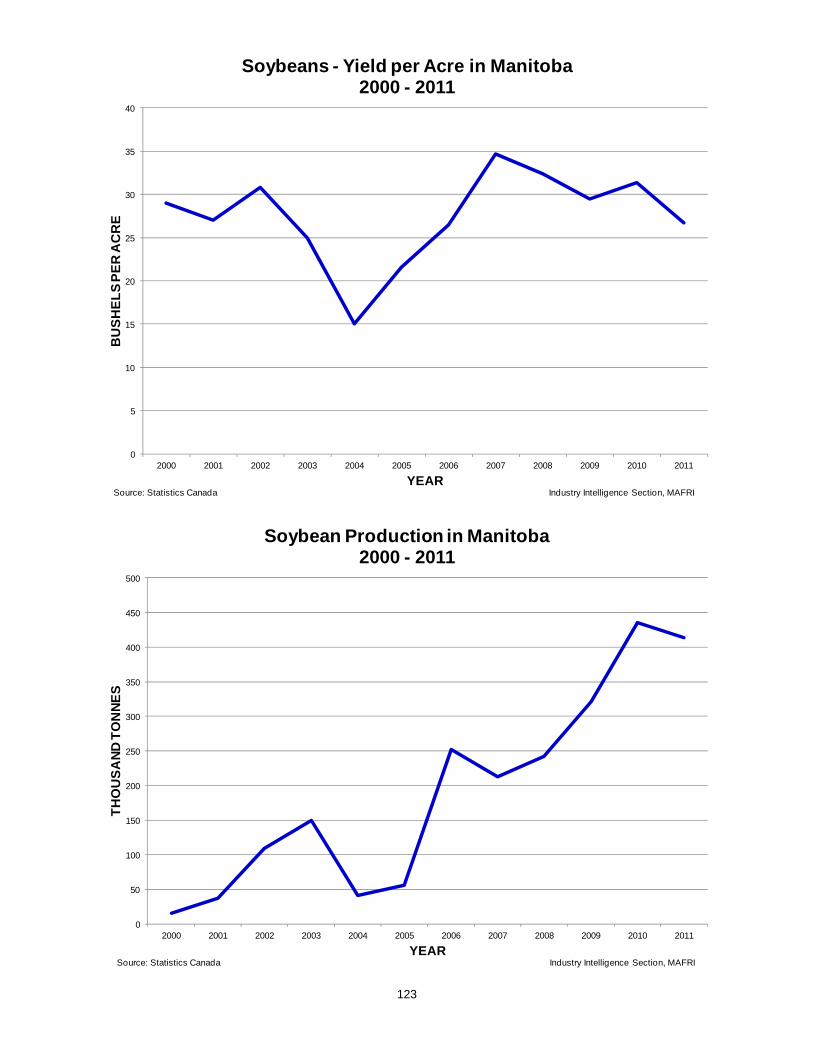

According to the 2011 Census of Agriculture, there were 180 farms with certified organic and/or transitional production in Manitoba. This represented 1.1% of all farms in the province. Nationwide, 2.0% of all farms reported certified organic and/or transitional production. The predominant category of certified organic and/or transitional products reported in Manitoba was field crops and hay and it was reported by 88.3% of the province’s 180 certified organic and/or transitional farms. Manitoba reported the second largest area of soybeans in Canada in 2011 with 705,032 acres, an increase of 101.1% since 2006. Areas reported for hay and grains traditionally used for livestock feed decreased in 2011. Hay area decreased 21.8% to 1.8 million acres in 2011. Similarly, oat area decreased 26.4% to 695,945 acres and barley area decreased 42.3% to 483,432 acres. Despite a 10.7% decrease from 2006 to 2011, Manitoba continued to report the second largest potato area in the country with 72,043 acres, behind Prince Edward Island. The total area of corn for grain increased 40.4% to 211,148 acres in 2011. Despite a 56.4% decrease in 2011, Manitoba continued to report the second largest flaxseed area in the country with 167,367 acres, behind Saskatchewan. Total vegetable area decreased 8.4% from 5,641 acres in 2006 to 5,169 acres in 2011. The largest vegetable areas in 2011 in Manitoba were sweet corn, carrots, and onions. Strawberry area decreased 26.4% to 304 acres in 2011, down from 413 acres reported in Manitoba in 2006. The area in saskatoons decreased 27.8% to 267 acres in 2011, down from 370 acres in 2006. The number of pollinating bees (excluding honeybees) decreased by 50.4% to 37,343 gallons in 2011, down from 75,332 gallons in 2006. There were 75,847 honeybee colonies reported in 2011, up from 73,411 colonies in 2006. In Manitoba, no-till methods were used on 24.0% of the land prepared for seeding in 2011, up from 21.3% in 2006. Conventional tillage decreased to 38.3% of land prepared for seeding, from 43.4% five years earlier. Conservation tillage was used on 37.7% of the land prepared for seeding, compared to 35.2% in 2006. The 2011 Census marked the first time farm operators were asked to report the area from which crop residue was baled for bedding or sale. In 2010, crop residue was baled from 747,146 acres in Manitoba.

12

Manitoba Farm Population Within Manitoba’s total population of 1,208,268 inhabitants in 2011, the farm population continued its steady decline in numbers, dropping by 8.1% since 2001 to 62,930 in 2006 (most current data available). Provincially, 1 in 18 Manitobans live on a farm, accounting for 5.5% of Manitoba’s population in 2006 compared to 6.2% five years earlier. In comparison, 1 in 46 Canadians live on a farm, accounting for 2.2% of the national population. Although 19.7% of the total Canadian population lived in rural areas in 2006, about 90% of rural inhabitants were not on farms. Manitoba’s rural population of 327,490 people accounted for 28.5% of the total provincial population in 2006 and 18.6% of the rural population lived on a farm. Farm operators in Manitoba Following the trend in the number of farms, there were 22,315 farm operators managing Manitoba’s 15,877 farms in 2011, a decrease of 16.2% from the 26,625 farm operators managing 19,054 farms in 2006. While the majority of farm operators continued to live on the farm, 3,095 or 13.9% resided off-farm in 2011 compared to 9.9% in 2006. In 2011, 23.6% of Manitoba farm operators were women, while nationally this percentage was 27.4%. The average age of a farm operator in Manitoba in 2011 was 53.1 years compared with 51.2 years in 2006. Nationally, the average age of a farm operator was 54.0 years, up from 52.0 years in 2006. In 2010, 46.6% of all Manitoba farm operators worked more than 40 hours a week on average on their farm operations, compared to 52.6% five years earlier. At the national level this percentage was 40.1% 2010. In 2010, 46.2% of all Manitoba farm operators had an off-farm job or business, compared to 47.7% in 2005. At the national level this percentage was 46.9% in 2010. According to the Census of Agriculture, 24.5% of Manitoba operators who were under the age of 35 on census day worked off the farm for more than 40 hours a week on average in 2010, compared to 20.7% of operators aged 35 to 54, and 9.6% of operators over 55 years of age. In 2011 farm operating arrangements, included 9,041 sole proprietorships, 3,982 partnerships, 2,490 family corporations and 307 other corporate farms, and 57 institutional or other farms. This compares with 2006 which had 10,866 sole proprietorships, 5,467 partnerships, 2,301 family corporations and 361 other corporate farms, and 59 institutional or other farms. High-speed internet access was reported by 43.1% of all Manitoba farms in 2011, while the national average was 44.8%.

13

In 2006 (most current data available), 8.2% of Manitoba farm operators had university degrees, up from 7.1% in 2001, and 11.7% reported apprenticeship or trades certificates or diplomas. In the 2006 Census, about 40% of Manitoba farm operators reported their main occupation as non-agricultural compared to 35.1% in 2001, suggesting that more operators are working off the farm. 58.6% of female operators in the province reported a non-agricultural occupation versus 33.4% for males. The top non-agricultural occupations for Manitoba's male farm operators included transportation equipment operators and related work, while clerical occupations were predominantly reported for women operators. 70.1% of Manitoba's total farm population in 2006 reported English as their mother tongue, 3.4% reported French and the remaining 26.5% reported another language predominantly German followed by Ukrainian. The 2006 Census of Population counted 3,340 immigrants in Manitoba's farm population or 5.3% of the total provincial farm population. The British made up 30.8% of Manitoba's immigrant farm population, while about 15% was from the Germany and the third most common place of birth for Manitoba's immigrant farm population was the United States at 10.5%. Over the past ten years, Manitoba has more than tripled its share of national immigration. Although the province accounts for about 3% of Canada’s population, it attracts nearly 6% of immigrants, more than 15,000 in 2010. The overwhelming majority of these immigrants arrived under the provincial nominee program, which Manitoba was the first province in Canada to adopt in 1998. Manitoba’s retention rate among nominee immigrants of nearly 83% may be due in part to the fact that many immigrants are able to find an ethnic community within the province. In addition, with a median age of 28, provincial nominees tend to belong to a younger age category than those in other immigration streams. The agricultural and manufacturing belt south of Winnipeg, populated by the church-going communities of Winkler, Morden and Altona, was the fastest growing region in the country in 2010. Over the years this area has attracted thousands of newcomers from Germany and Mexico, many of them with large families of seven or more, their adjustment facilitated by local German-speaking families who came to the area in the last century. This is also a region with growing immigration from Kazakhstan and other former Soviet republics as well as Ireland and Belgium. Brandon is another area outside the city of Winnipeg which has welcomed large numbers of immigrants in the last 10 years due to labour needs associated with a major meat-packing plant which spawned a multicultural boom. There are now 57 language groups in Brandon, with workers from countries such as El Salvador, China and Colombia.

14

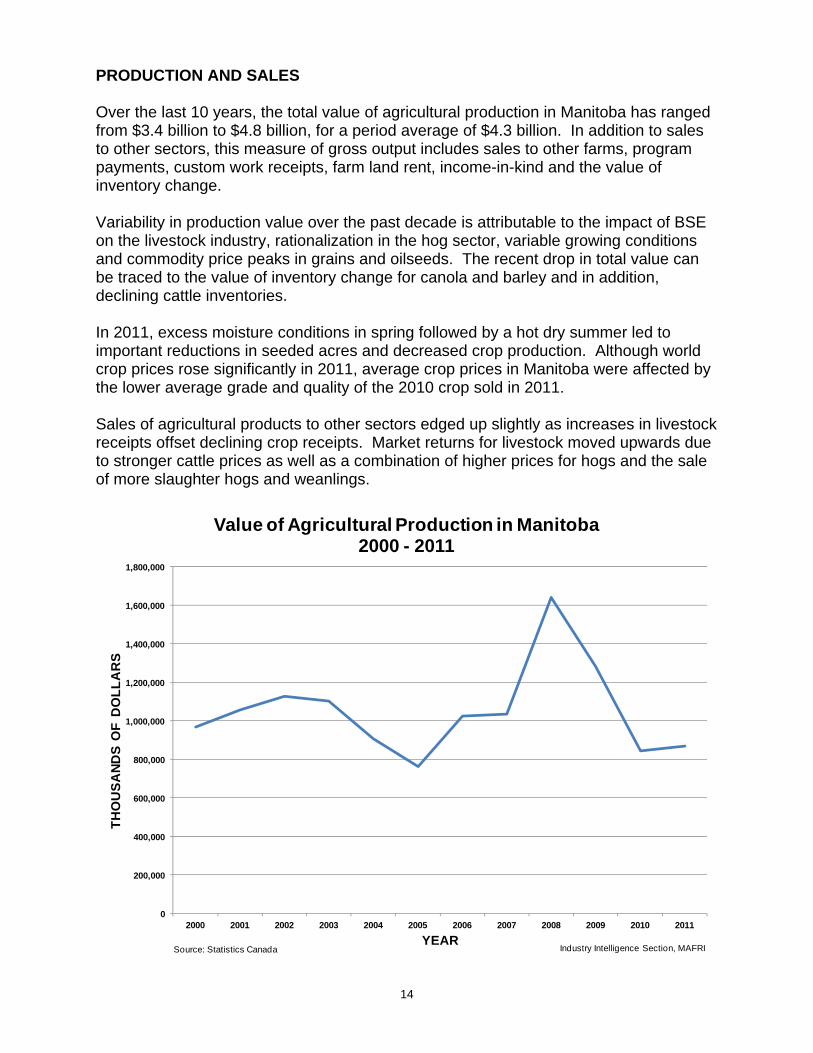

PRODUCTION AND SALES Over the last 10 years, the total value of agricultural production in Manitoba has ranged from $3.4 billion to $4.8 billion, for a period average of $4.3 billion. In addition to sales to other sectors, this measure of gross output includes sales to other farms, program payments, custom work receipts, farm land rent, income-in-kind and the value of inventory change. Variability in production value over the past decade is attributable to the impact of BSE on the livestock industry, rationalization in the hog sector, variable growing conditions and commodity price peaks in grains and oilseeds. The recent drop in total value can be traced to the value of inventory change for canola and barley and in addition, declining cattle inventories. In 2011, excess moisture conditions in spring followed by a hot dry summer led to important reductions in seeded acres and decreased crop production. Although world crop prices rose significantly in 2011, average crop prices in Manitoba were affected by the lower average grade and quality of the 2010 crop sold in 2011. Sales of agricultural products to other sectors edged up slightly as increases in livestock receipts offset declining crop receipts. Market returns for livestock moved upwards due to stronger cattle prices as well as a combination of higher prices for hogs and the sale of more slaughter hogs and weanlings.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

TH

OU

SA

ND

S O

F D

OL

LA

RS

YEAR

Value of Agricultural Production in Manitoba2000 - 2011

Industry Intelligence Section, MAFRISource: Statistics Canada

15

The farm product price index measures the prices received by farmers for commodities produced on a constant dollar basis, with 1997 as the base period. Although the total index has trended upwards since mid-2010, there has been a continual slow-down of growth since the last quarter of 2011. For most of 2011, the increase in overall livestock and animal product prices more than offset lower crop prices. Crop prices and grains in particular showed dramatic increases in the range of 30 to 50% from 2006 to 2008 and in the same time period, oilseeds mirrored the increase at a slightly lower level, ranging from 20 to 40%. This increasing trend came to an abrupt end in mid-2008 as prices returned to historical levels. More recently, grain and oilseed prices have trended upward and the International Grains Council and United States Department of Agriculture forecasted an increase in total world grain production for 2011/12. Prices received for cattle improved post-BSE but in 2007 trended downward to levels below the base period of 1997. Hog prices have remained relatively flat until 2006 where a gradual downward trend became evident in part due to weaker market conditions, Country of Origin labeling and the H1N1 issue. In 2011, advances were recorded in all livestock commodities. Lower on-farm inventories of cattle and hogs in North America and higher feed grain costs have supported the year-over-year growth trends.

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

VA

LU

E: 1

99

7=

100

YEAR

Farm Product Price Index - Manitoba 2000 - 2011

Grains Oilseeds Cattle and calves Hogs

Industry Intelligence Section, MAFRISource: Statistics Canada

16

FARM CASH RECEIPTS Gross farm receipts have been rising. Manitoba’s gross farm receipts in 2010, the year prior to the census, increased 7.8% (at 2010 constant prices) to $5.3 billion, from 2005. At the national level there was a 3.9% increase in gross farm receipts between 2005 and 2010.

0

5000

10000

15000

20000

25000

30000

35000

1981 1986 1991 1996 2001 2006 2011

NU

MB

ER

OF

FA

RM

S

YEAR

Farm Numbers by Farm Cash Receipts1981 - 2011

<$50,000 $50,000-$99,999 $100,000+

Industry Intelligence,MAFRISource: STC Census

According to the 2011 Census of Agriculture, the number of farms with $500,000 or more (at 2010 constant prices) of 2010 gross farm receipts increased by 25.7% between censuses, and those with less than $500,000 decreased by 21.6%. There were 2,490 of these larger farms in Manitoba in 2011, and while they represented 15.7% of all farms in the province, they accounted for 73.2% of total provincial gross farm receipts reported for the year 2010. The number of farms with $250,000 and $499,999 in farm cash receipts has steadily declined over the years and now represents 2,039 farms or 13% of total farms in 2011. 2,753 farms (17%) had between $100,000 and $249,999 in farm cash receipts, while 2,063 farms (13%) had between $50,000 and $100,000 in farm cash receipts. In 2011, there were 6,532 farms, or 41.1% of total farms, with less than $50,000 in farm cash receipts. While declining in numbers relative to other income categories, they still represent the single largest grouping of farms in the province. This is particularly significant as it suggests that a large number of farms in the province generate a relatively small cash flow.

17

FARMS CLASSIFIED BY TOTAL GROSS FARM RECEIPTS, 2010 Number of farms reporting

Manitoba 2006 Manitoba 2011Under $10,000 3,426 2,716$10,000 to $24,999 2,779 1,971$25,000 to $49,999 2,516 1,845$50,000 to $99,999 2,813 2,063$100,000 to $249,999 3,875 2,753$250,000 to $499,999 2,058 2,039$500,000 to $999,999 958 1,426$1,000,000 to $1,999,999 341 676$2,000,000 and over 288 388Total farms reporting 19,054 15,877

Total farm cash receipts are estimated at $4.89 billion in 2011, a rise of 0.8% from $4.85 billion in 2010. Net operating expenses after rebates (including depreciation) are estimated at $3.8 billion in 2011, up 2.9% from 2010. Government payments are estimated at $509 million, a rise of 45.8% from $349 million in 2010. The sharp rise in 2011 program payments is due to early season excess moisture which resulted in low production and triggered higher crop insurance payments and assistance under AgriRecovery.

0

1,000

2,000

3,000

4,000

5,000

6,000

MIL

LIO

NS

OF

DO

LL

AR

S

Manitoba Farm Cash Receipts1993 - 2011

CROPS LIVESTOCK DIRECT PAYMENTS

Source: Statistics Canada Industry Intelligence, MAFRI

18

763.5

989.5

848.5

465.4

792.9

494.6

Average Manitoba Farm Cash Receipts(millions of dollars)

2007 - 2011

Wheat

Canola

Other Crops

Cattle and Calves

Hogs

Other Livestock

0 200 400 600 800 1,000 1,200

Sunflower seed

Flaxseed

Dry beans

Barley

Corn

Eggs

Poultry

Oats

Soybeans

Potatoes

Dairy

Cattle/calves

Wheat

Hogs

Canola

MILLIONS OF DOLLARS

CO

MM

OD

ITY

Manitoba Farm Cash Receipts, by Commodities2009 - 2011

2011

2010

2009

Industry Intelligence Section, MAFRISource: Statistics Canada

19

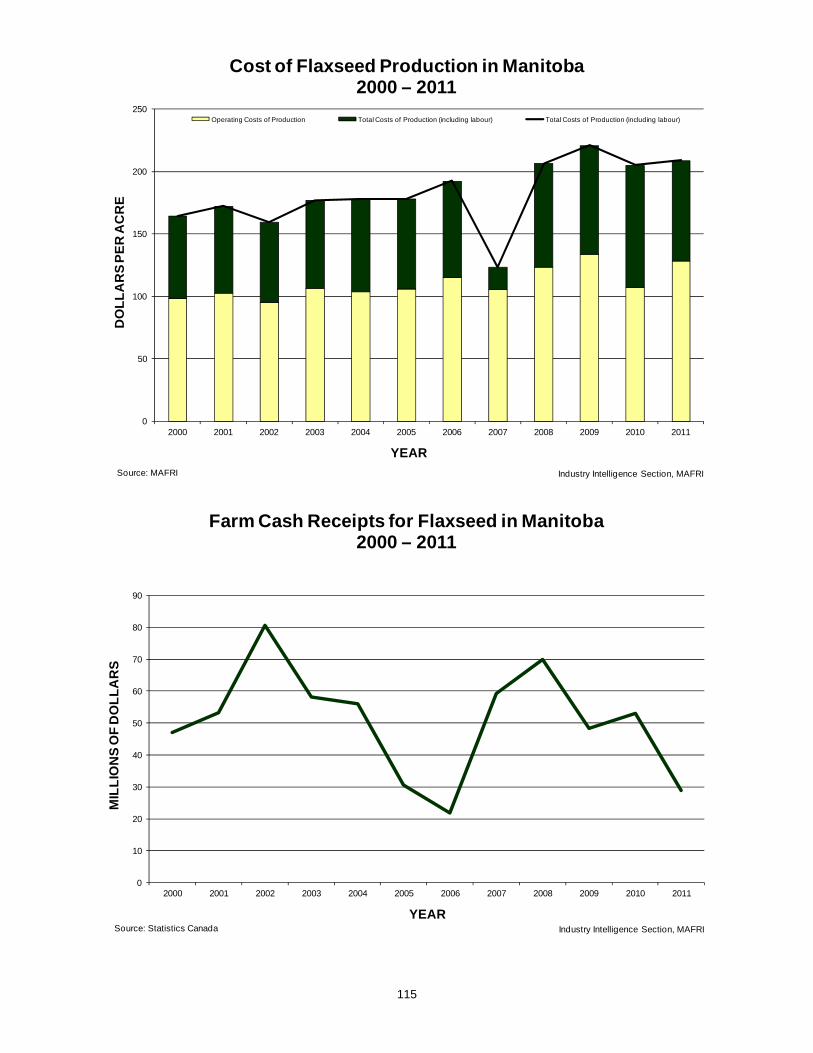

CROP MARKET RECEIPTS In 2011, crop market receipts in Manitoba were $2.5 billion, a drop of 8.9% from $2.7 billion in 2010, led by canola, wheat, soybeans and oats. Production challenges included excess moisture and delaying seeding followed by dry mid-summer conditions in several areas of the province. Tough growing conditions in both 2010 and 2011 led to production declines of more than 20% for both wheat and canola. Canola receipts were $1.02 billion in 2011, down 8.5% from 2010; all wheat receipts were $791 million in 2011, a rise of 7.7% from 2010; receipts for soybeans were $153 million in 2011, up 65.5% from 2010; and receipts for oats were 129 million, down 4.7% from 2010. Grain and oilseed prices in 2011 rose in response to tight global supply relative to use, as demand for feed and biofuels continued to rise while a drought and subsequent export restrictions in Russia and the Ukraine in 2010 constrained supplies well into 2011. Income from barley increased 15.6% to $64 million due in large measure to a 31.6% increase in barley prices. Income from corn was up 46.8% to $83 million mainly due to a 47.8% improvement in corn prices. Flax income dropped 45.6% to $29 million due to a 61.6% decrease in marketings in spite of a 25.6% improvement in flax prices. Income from potatoes was down 18.4% to $166 million primarily resulting from a 17.6% decrease in potato prices.

0

500

1,000

1,500

2,000

2,500

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

NS

OF

DO

LL

AR

S

YEAR

Farm Cash Receipts, Manitoba Principle Crops1990 - 2011

Wheat Oats Barley Flaxseed Canola

Industry Intelligence Section, MAFRISource: Statistics Canada

20

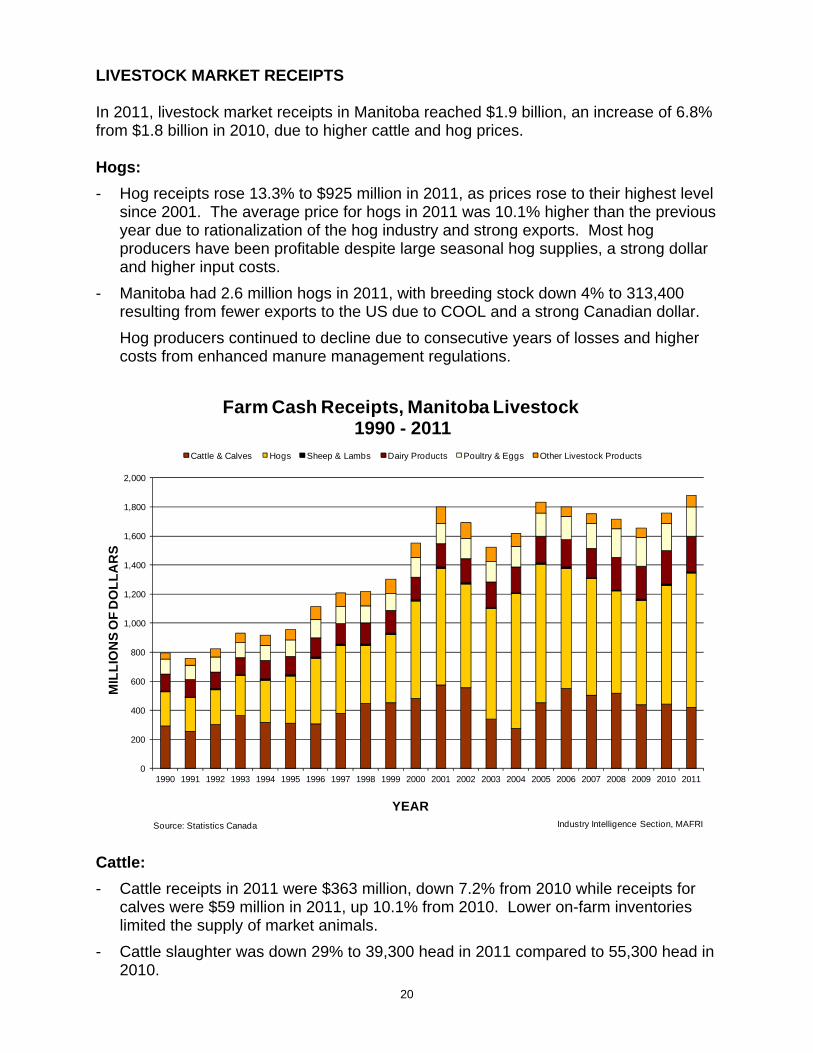

LIVESTOCK MARKET RECEIPTS In 2011, livestock market receipts in Manitoba reached $1.9 billion, an increase of 6.8% from $1.8 billion in 2010, due to higher cattle and hog prices. Hogs:

- Hog receipts rose 13.3% to $925 million in 2011, as prices rose to their highest level since 2001. The average price for hogs in 2011 was 10.1% higher than the previous year due to rationalization of the hog industry and strong exports. Most hog producers have been profitable despite large seasonal hog supplies, a strong dollar and higher input costs.

- Manitoba had 2.6 million hogs in 2011, with breeding stock down 4% to 313,400 resulting from fewer exports to the US due to COOL and a strong Canadian dollar.

Hog producers continued to decline due to consecutive years of losses and higher costs from enhanced manure management regulations.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

NS

OF

DO

LL

AR

S

YEAR

Farm Cash Receipts, Manitoba Livestock1990 - 2011

Cattle & Calves Hogs Sheep & Lambs Dairy Products Poultry & Eggs Other Livestock Products

Industry Intelligence Section, MAFRISource: Statistics Canada Cattle:

- Cattle receipts in 2011 were $363 million, down 7.2% from 2010 while receipts for calves were $59 million in 2011, up 10.1% from 2010. Lower on-farm inventories limited the supply of market animals.

- Cattle slaughter was down 29% to 39,300 head in 2011 compared to 55,300 head in 2010.

21

- 327,100 cattle and calves were exported to other provinces in 2011, up 1% from 322,900 in 2010 while 82,400 head were exported internationally, down 50% from 164,300 in 2010. This was due in part to reduced slaughter capacity in the US for Canadian hogs and the impact of COOL.

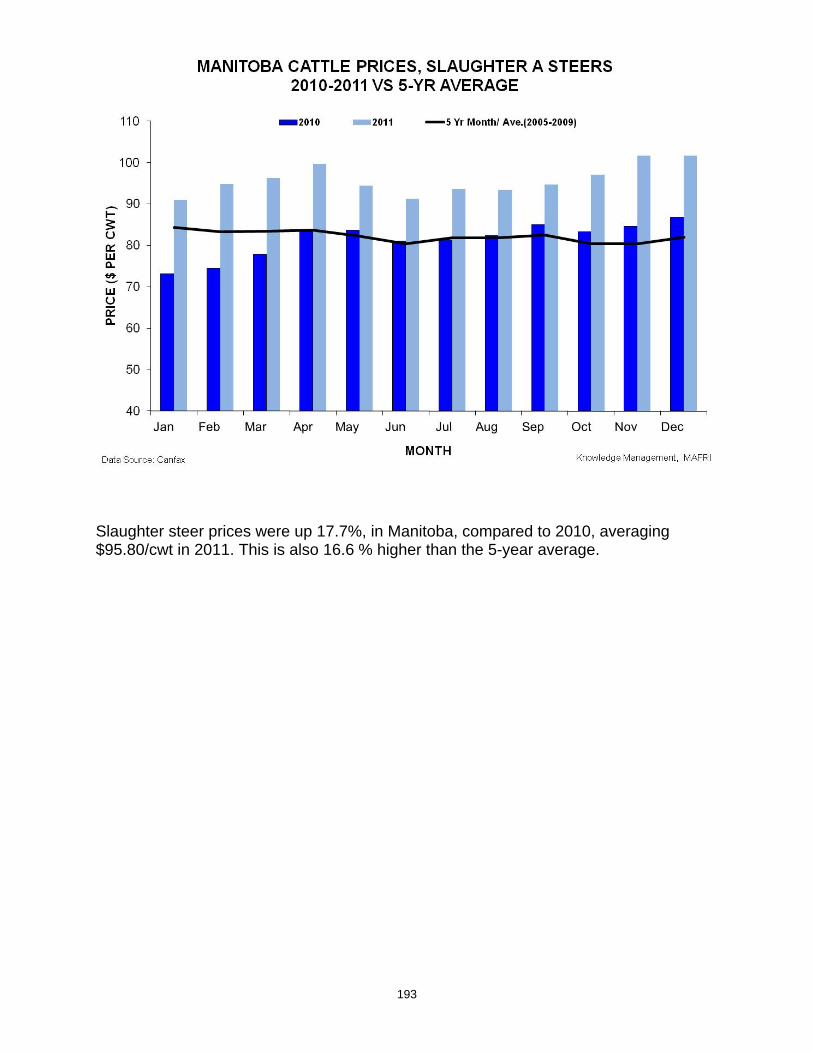

- Fed steer prices were up 18.6% at $94/cwt; feeder prices rose 24.3% to $137/cwt; and cow prices were up 26.2% at $60/cwt.

Receipts from supply-managed commodities (dairy, poultry, eggs) were $447 million in 2011, up 7.1% from 2010, mainly due to a 6.7% increase in dairy receipts and a 14.4% rise in poultry receipts as egg receipts were relatively unchanged. FARM INCOME Net cash income is estimated at $1.1 billion in 2011, a decrease of 6.0% from $1.2 billion in 2010, led by the crops sector. Realized net farm income adjusted for depreciation is estimated at $525 million in 2011, down 16.9% from one year earlier. Total net income (adjusted for depreciation and inventory change) in 2011 is estimated at $183 million compared to $56 million in 2010 due to a reduction in the value of inventory change from $-576 million in 2010 to $-342 million in 2011. FARM INCOME SUMMARY

millions of dollars 2005 2006 2007 2008 2009 2010 2011Crop Receipts 1,294 1,275 2,198 2,763 2,805 2,743 2,499Livestock Receipts 1,832 1,801 1,752 1,716 1,657 1,760 1,880Market Receipts 3,126 3,076 3,950 4,479 4,461 4,503 4,380Total Payments 699 626 413 350 386 349 509Total Cash Receipts 3,825 3,702 4,363 4,829 4,848 4,852 4,889Net Operating Expenses 3,013 3,211 3,535 3,962 3,812 3,703 3,888Net Cash Income 812 490 828 868 1,036 1,149 1,001Income-In-Kind 4 3 3 3 3 3 3Depreciation Charges 461 467 470 495 527 537 576Realized Net Income 355 27 362 376 512 616 428Value of Inventory Change -234 295 -103 501 32 -578 -445TOTAL NET INCOME 122 322 259 877 544 37 -17

Manitoba farmers have experienced considerable variation in income over the decades with realized net farm income ranging from low of $27 million in 2006 to $612 million in 2010, with an average of $356 million in the past 10 years. This value varies considerably when the value of inventory change is considered. Further, if depreciation is eliminated and cash flow is taken into consideration, net cash income over the last 10 years has averaged $833 million. In 2010 net cash income reached a record high of $1,149 million. The values highlighted indicate that depending upon the measurement selected and the time frame considered, a variety of conclusions can be reached on the economic well-being of the sector within the provincial economy. If a short term perspective is taken, the cash flow to the farm community provides a good indicator of the current financial well-being of agriculture. However, if a longer term perspective is applied, depreciation and allowances for inventory change significantly alter the overall assessment of the economic well-being of the agricultural sector.

22

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

NS

OF

DO

LL

AR

S

YEARS

Farm Income and Expenses, Manitoba 2000 - 2011

Market Receipts Total Payments Total Cash Receipts

Net Operating Expenses Realized Net Income TOTAL NET INCOME

Industry Intelligence Section, MAFRI Farmers in general are faced with a situation where they exercise only limited control on the aggregate income generated. On an individual basis, futures pricing and effective economic management can have a dramatic influence on farm earnings. As is commonly accepted, weather, changing political conditions, government policy and international exchange rates, weigh heavily on sector returns. Farm Income Terminology Farm cash receipts

----------------------------

measure gross revenue of farm businesses and include revenues from sales of crops and livestock products, program payments from government agencies and payments from private agricultural insurance programs

Market receipts

----------------------------

Include the market sales of crops and livestock products

Farm operating expenses

----------------------------

represent business costs incurred by farm businesses for goods and services used in the production of agricultural commodities

Realized net income

-- -- -- -- -- --

includes net cash income minus depreciation plus income-in-kind. It represents the cash and non-cash financial flows that are attributable to the farm business and does not include changes in stocks

Total net income

----------------------------

includes return to owner's equity, unpaid labour, management, risk and accounts for changes in the total value of inventories

Total payments

----------------------------

Includes government/producer funded program payments

23

The following chart shows average net farm operating income by farm type, defined as market receipts including program payments less operating expenses. It provides insight into sectors within agriculture in Manitoba that hold the greatest potential for profitability. Gains in the potato sector contrast with the cattle industry, the latter of which has the lowest average net operating income of all sectors. This assessment needs to be viewed in context in that the number of enterprises in each category will vary considerably as well as variability for entry into that sector by farmers.

(100,000)

-

100,000

200,000

300,000

400,000

500,000

600,000

Gra

ins

& o

ilse

eds

Po

tato

Gre

enh

ou

se

Oth

er C

rop

s

Cat

tle

Dai

ry

Ho

gs

Po

ult

ry a

nd

eg

gs

Oth

er L

ives

tock

All

farm

s

DO

LL

AR

S

FARM TYPE

Net Farm Operating Income by Farm Type(average per farm) Manitoba, 2007 - 2011

2007 2008 2009 2010 2011

Industry Intelligence Section, MAFRISource: Statistics Canada, AAFC, MAFRI The hog sector is the second most significant industry in the province when viewed on a net farm operating income basis. Within that sector, 2010 recorded considerable increase in net farm income in contrast to 2011 which shows a negative position. The grain and oilseed sector has demonstrated a relatively steady income over the last 3 year period. The high returns in some other sectors relative to grains and oilseeds is reflective of commodity prices for that particular product rather than a measure of enterprise efficiency. With improving market receipts, program payments trend downwards whereas off-farm income revenues have a slight upward trend as farm families continue to improve their economic well-being by supplementing their revenues through non-farm activities. Off-farm income, as a portion of total farm income is most significant for smaller enterprises. Seasonality of farm production also factors into the ability to generate off-farm income. The importance of program payments and non-farm income to farm operations in Manitoba is especially apparent in years when the combined revenues from both of these forms of non-farm income can exceed revenues achieved from net market receipts.

24

FARM OPERATING EXPENSES Net farm operating costs in 2011 were estimated at $3.9 billion, up 5.0% from $3.7 billion the previous year. Although interest costs remained historically low and the prime business rate charged by major banks averaged 3%, interest on debt was $251 million in 2011, up 6.4% from 236 million one year earlier. Property taxes were $85 million in 2011, an increase of 7.3% from $79 million in 2010. Farm fertilizer expenses were estimated at $622 million in 2011, an increase of 15.7% from $537 million in 2010; prices were driven upward in response to high energy costs and strong worldwide demand. Although pesticide usage levels did not change significantly, there was a general decline in pesticide expenses since glyphosate has come off patent protection and pricing reflects a more competitive market. 2011 pesticide expenditures were $263 million, down 16.3% from $314 million the previous year. Machinery and heating fuel expenses in 2011 reached $316 million, up 11.2% from $286 million in 2010. Fuel expenses rose as fuel prices went up 25% due to growing energy demand in emerging economies and slowing growth in supply. This was offset to some degree as the large area of unseeded acreage had a dampening effect on quantities purchased. Commercial feed expenses were $570 million in 2011, an increase of 15.4% from $494 million in 2010 as a result of higher grain and oilseed costs. Seed expenses were $200 million in 2011, down 2.3% from $204 million the previous year.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

TH

OU

SA

ND

S O

F D

OL

LA

RS

YEAR

Farm Operating Expenses and Depreciation, 2000 - 2011Machinery Operation & Heating Fuel Depreciation, Bldgs. & Machinery Interest on Debt

Property Taxes Cash Wages Commercial Feed

Commercial Seed Fertilizer and Lime Pesticides

Industry Intelligence Section, MAFRI

25

MANITOBA OUTLOOK 2012 Preliminary forecasts for 2012 suggest an improvement in total net income, projected to reach $521 million as Manitoba producers build up inventories. Grain and oilseed supplies are expected to be more abundant on world markets and domestic cattle and hog herds are expected to stabilize. Expenses will continue to rise, but more slowly as there are no cost spikes anticipated such as the one for fertilizer in 2011. Crop receipts are projected at $2.3 billion as better prices for grains and oilseeds are anticipated to continue in 2012. Internationally, grain and oilseed prices are expected to be lower, although historically very high, as improved harvests loosen the supply-demand situation. Domestically, crop production is expected to increase as acreage affected by excess moisture is brought back into full production. With relatively favourable growing conditions on the Prairies this year, canola will likely emerge as a $10 million crop with record output and prices in 2012-13. Record corn prices due to dry conditions in Ontario and the United States will squeeze profit margins of livestock producers in both Canada and the United States. This will limit herd rebuilding and increase consumer prices for red meat products in the second half of 2012 and first part of 2013. Livestock receipts in 2012 are forecast at $1.9 billion as strong livestock prices are expected to continue. Cattle and hog herd numbers are projected to stabilize and both sectors will continue face challenges associated with high feed costs and the strong Canadian dollar. Strong cattle demand in the U.S. is expected to carry into 2012 along with tight supplies, which will push prices up. Canadian cattle prices are projected to increase modestly given the strong dollar while marketings are expected to remain stable. Market receipts for cattle and calves, driven by price are anticipated to outpace higher expenses. As the hog sector faces the additional challenge of uncertainty surrounding future demand for pork, hog farm income is forecast to be down from 2011 and the largest factor is expected to be increase in expenses. Dairy farm average net operating income is projected to increase as increased market receipts more than offset growth in expenses. Poultry and egg farms are expected to increase from the previous year due to growth in market receipts outpacing rising expenses. Total farm operating expenses are anticipated to return to their normal historic upward trend, climbing to $4.1 billion in 2012, mainly due to costs related to field crops such as interest expenses and fertilizer. Although interest costs will remain low by historical standards, the prime business rate charged by the major banks in Canada is expected to be 3.3% on average in 2012. Fertilizer prices are forecast to climb modestly in 2012 as expected high levels of crop planting, particularly in China, India and Brazil contribute toward maintaining a tight global fertilizer supply and demand balance. Overall, the increase in operating expenses is expected to be rather broad-based, with no significant price surges for particular inputs. With regard to quantities purchased, crop-related inputs such as fertilizer, fuel, pesticides and seed are expected to return to normal levels in 2012 as the large area of unseeded acreage in 2011 returns to production.

26

Program payments in 2012 are estimated at $424 million. The biggest factor in this forecast decline is the absence of an AgriRecovery program, such as the excess moisture payments that took place in 2011; another factor is the decline in AgriStability payments in calendar year 2012. Compared to the previous year, the outlook projected for 2012 indicates restored total net income but a reduction in net cash income to $608 million and a drop in realized net income to $21 million. Both these values reflect structural changes in the livestock sector and the associated impact on income, a return to more normal inventory volumes for grains and oilseeds, an increase in expenditures and depreciation charges. Overall long term trends include greater world-wide demand for feed grains, rising prices for crude oil, the strength of the Canadian dollar and Canada’s population growth of 1.2% per year with its implications for increased domestic food demand.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

MIL

LIO

NS

OF

DO

LL

AR

S

YEAR

Value of Farm Capital in Manitoba2000 - 2011

LAND AND BUILDINGS EQUIPMENT LIVESTOCK

Industry Intelligence Section, MAFRISource: Statistics Canada As farms become larger, their capital value moves higher. The continuous trend to fewer numbers of larger, more capital-intensive farms is driven by the need for farm operations to capture economies of specialization and size. In 2006 and 2007, farm land values recorded a dramatic increase, reflective of the overall appreciation of land values in North America. Farm land and buildings account for the largest portion of capital. Farm machinery and equipment have shown a stable, modest growth over time, driven in part by the need for larger, more technologically complex equipment.

27

Livestock values peaked in 2001 at $1.9 billion and fell dramatically in 2003 to $1.4 billion in response to the BSE issue. Livestock value trended downwards due to decreases in hog values/numbers and continued weakness in the cattle/calf sector. The total value of farm capital has increased from $14.9 billion in 2000 to and estimated $23.5 billion in 2011. On average, Manitoba farms have low debt to asset ratios reflecting the fact that a large portion of the wealth of farmers is contained in the land asset. The difficulty with this situation is that land, which has appreciated over time and represents the bulk of the wealth of producers, is not easily liquidated. This has implications in terms of the year to year operations of the farm enterprise and the constant need for debt financing of operating costs. As farms get larger, a strong asset position will become increasingly more important as it will allow producers to leverage assets to debt financing at higher levels in support to these type of enterprises. The ratio of farm equity to total assets is currently 80% and has ranged between 77 and 82% over the last 10 years. In general, highly capitalized industries such as the hog sector and the potato sector have recorded larger capital investments per farm relative to grain enterprises and cattle operations.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011f

DO

LL

AR

S P

ER

FA

RM

YEAR

Average Farm Assets, Liabilities, Net Worth in Manitoba2000 - 2011

Total Assets Net Worth Total Liabilities

Industry Intelligence Section, MAFRISource: Statistics Canada, AAFC, MAFRI The Chartered Banks continue to be the major source of debt financing for Manitoba farms accounting for $2.3 billion in 2011 while Credit Unions are the second largest lender in rural Manitoba with $2.1 billion outstanding. The current trend suggests a constriction in chartered bank lending partially in response to global and national economic conditions. In contrast, Credit Unions, which tend to be community oriented, have shown a steady increase in debt financing for Manitoba farm operations.

28

Provincial government program funding, which by nature, tends to assume a higher level of risk, remains relatively stable as the sixth largest source of funding for farm enterprises in the province. Federal government funding, the third largest funding agency in the province, has demonstrated a slow, gladual growth in outstanding farm debt.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

INS

TIT

UT

ION

YEAR

Outstanding Farm Debt, 2000 - 2011Chartered Banks Federal Gov't Agencies Provincial Gov't Agencies

Credit Unions Insurance, Trust, Loan Companies Private Individuals & Others

Advance Payment Programs

Industry Intelligence Section, MAFRISource: Statistics Canada

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011f

EQ

UIT

Y R

AT

IO

YEAR

Manitoba Farm Equity to Total Assets Ratio2000 - 2011

Industry Intelligence Section, MAFRISource: Statistics Canada, AAFC, MAFRI

29

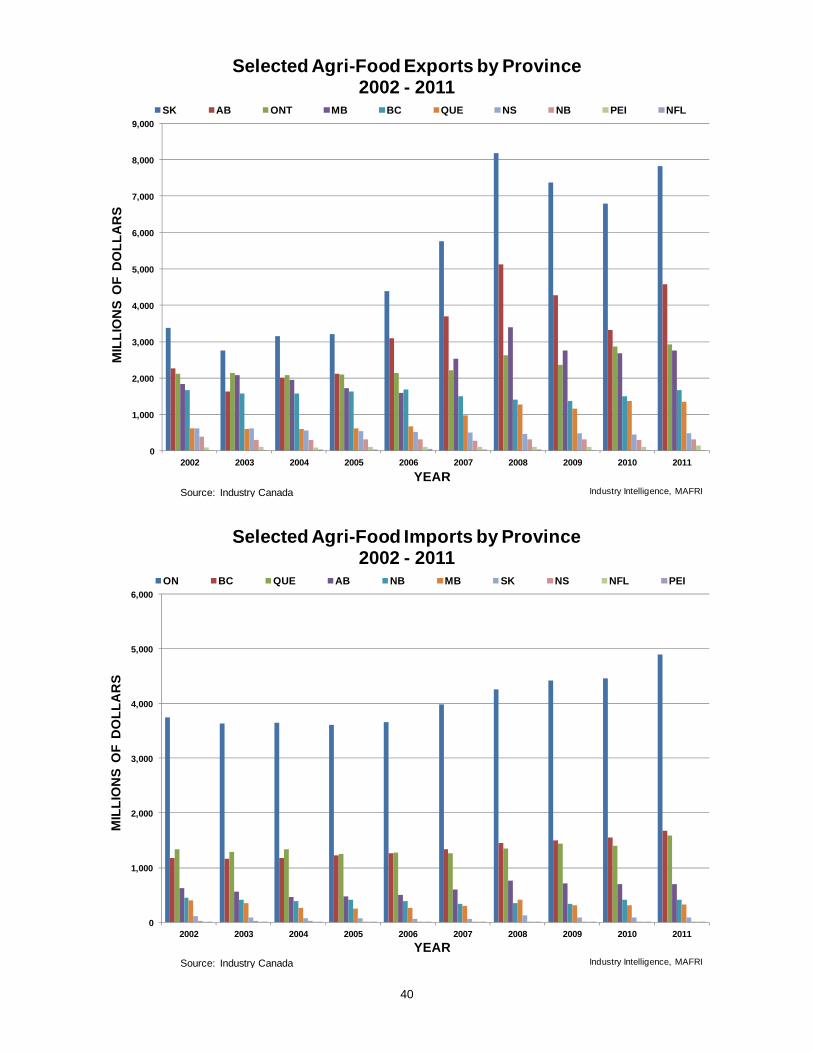

AGRI-FOOD TRADE Manitoba provides a gateway to key exports markets. Given its strategic location at the centre of North America, Manitoba is a natural transportation and distribution axis for the entire mid-continent. The province forms the northern end of a major trade corridor extending through the Midwest U.S. to Mexico, and potentially further south to the emerging markets of Latin America. Well-developed air, rail and road links make Manitoba a hub for the flow of goods destined for markets in North America, Europe and Asia. With its relatively small population, Manitoba has always looked to export markets for growth -- a tradition that stands the province in good stead as markets become more global in nature. The province is the most diversified manufacturing centre in North America, with a strong presence in industries such as farm equipment and machinery, apparel, food processing, bus manufacturing, building products and aerospace. During the past decade, Manitoba manufacturing companies have rapidly increased production and export sales. Other important industries in the province are tourism and business services. Manitoba businesses are also pursuing opportunities in knowledge-driven fields such as information technology, health care products and services, aerospace and telecommunications. Annual exports from the province in 2011 reached more than $11.8 billion, including agri-food exports of more than $4.3 billion. Manitoba acts as a "supermarket to the world," exporting agri-food products around the globe. Agri-food exports are among the largest single sources of foreign exchange earnings in Manitoba with shipments to over 180 countries. The United States is Manitoba's most important trading partner, accounting for close to $1.9 billion of agri-food products in 2011, followed by approximately $484 million of agri-food exports shipped to Japan, $241 million to Mexico and $385 million to China. Wheat is Manitoba's top agri-food export. At a minimum, the province's wheat exports account for 23 per cent of the province's agri-food and fish exports. Unprocessed wheat is exported to more than 70 countries, but the primary importers are the U.S., Iran, Japan and Mexico. Varieties of grains and pulses exported from the province include barley and oats, peas, beans, flax, lucerne (alfalfa) and grasses. Canola seed, used for oil extraction in international markets, is the province's second-largest agri-food export and represents 18 per cent of provincial exports. Following canola seed is canola oil and its fractions that account for 10 per cent of exports. The oil is used in many applications, such as margarine, and as a cooking oil or as a food ingredient or a raw material for biodiesel. Potatoes are Manitoba's fourth-largest agri-food export, and the province is Canada's second-largest potato producer after Prince Edward Island. The versatile potato finds its way into many products, including alcohol, starches, pharmaceuticals and biodegradable plastics.

30

The sole Canadian manufacturer of food-grade potato starch is in Manitoba. The company processes its starch from product recovered from local potato processing operations, to be used as a natural thickener in the production of snack foods, processed meats, baked goods, noodles, pet foods, shredded cheese, sauces, gravies and soups. Potato starches are also used as additives in cosmetics and pharmaceuticals. Manitoba’s commercial fishing industry is well-known for walleye (pickerel) and sauger, which are the most sought-after species in the province's commercial fishery and account for about 33 per cent of Canada's annual commercial catch of freshwater fish. The Manitoba fishery earns about $25 million in annual export sales. Lake Manitoba, Lake Winnipeg, and Lake Winnipegosis have the largest commercial fisheries. From the time of catch, strict quality control measures apply. The fish are packed in ice and expedited to a modern processing plant in Winnipeg. The Orthodox Union provides onsite rabbinical supervision if Kosher certification is required. The province has more than 40 private-sector companies, employing more than 2,300 people in the life-sciences industry. Manitoba has been recognized internationally as a hub of the knowledge economy and in recent years has been among the fastest-growing life-science economies in Canada. The world economy and demand for agriculture greatly impact Manitoba’s trade situation. The slow economic recovery in the United States and the instability of the European Euro in 2011 are likely to keep the Canadian dollar at par or slightly above the U.S. dollar in 2012. The Canadian dollar averaged US$1.011 in 2011, 4.1% above 2010 and its highest annual average in more than forty years. While the stronger Canadian dollar had a negative impact on agricultural product prices, it also resulted in lower costs for imported farm inputs. It is projected that interest rates in Canada are less likely to increase as long as the United States continues its low interest rate policy in 2012 and longer. In 2012, oil prices started strong and are projected to rise above the 2011 average of US$95 per barrel. U.S. corn and wheat prices were record high in 2011. Despite dampening enthusiasm for ethanol and with a small carry-over, U.S. corn prices set the trend at record levels in 2011/12. In the U.S, competition with corn for land help support soybean, barley, oat, flaxseed and canola prices. According to USDA forecasts for the next 5 years, corn prices are projected to average at or below US$4.50 per bushel due to growth in feed use, exports and demand for corn by ethanol producers. Wheat prices are expected to decline through 2013/14 due to near-term market adjustments and are projected to average about US$6 per bushel for the following 5 years. Estimated price increases for wheat in later years are more moderate than those for corn and soybeans. Current economic prospects suggest that grain prices based on normal yields will be lower in 2012, but still high historically. Given improvements in world demand for beef and pork, raising average U.S. cattle and pig prices in 2011 to record levels, livestock prices are projected to remain high in 2012.

31

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

N D

OL

LA

RS

YEAR

Total Value of Manitoba Agri-Food Trade - WorldIMPORTS EXPORTS

Industry Intelligence, MAFRISource: Industry Canada, AAFC, MAFRI

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MIL

LIO

N D

OL

LA

RS

YEAR

Total Value of Manitoba Agri-Food Trade - U.S.

IMPORTS EXPORTS

Industry Intelligence, MAFRISource: Industry Canada, AAFC, MAFRI

32

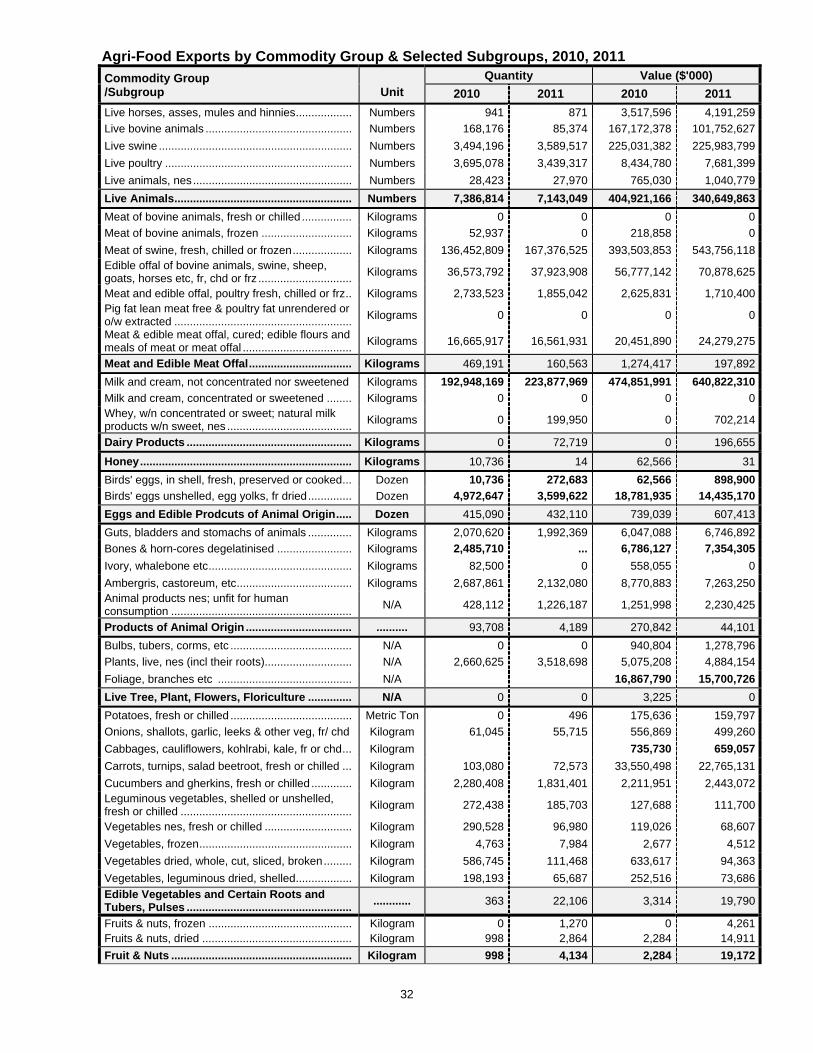

Agri-Food Exports by Commodity Group & Selected Subgroups, 2010, 2011

Commodity Group /Subgroup

Unit

Quantity Value ($'000)

2010 2011 2010 2011

Live horses, asses, mules and hinnies .................. Numbers 941 871 3,517,596 4,191,259

Live bovine animals ............................................... Numbers 168,176 85,374 167,172,378 101,752,627

Live swine .............................................................. Numbers 3,494,196 3,589,517 225,031,382 225,983,799

Live poultry ............................................................ Numbers 3,695,078 3,439,317 8,434,780 7,681,399

Live animals, nes ................................................... Numbers 28,423 27,970 765,030 1,040,779

Live Animals ......................................................... Numbers 7,386,814 7,143,049 404,921,166 340,649,863

Meat of bovine animals, fresh or chilled ................ Kilograms 0 0 0 0

Meat of bovine animals, frozen ............................. Kilograms 52,937 0 218,858 0

Meat of swine, fresh, chilled or frozen ................... Kilograms 136,452,809 167,376,525 393,503,853 543,756,118Edible offal of bovine animals, swine, sheep, goats, horses etc, fr, chd or frz ..............................

Kilograms 36,573,792 37,923,908 56,777,142 70,878,625

Meat and edible offal, poultry fresh, chilled or frz .. Kilograms 2,733,523 1,855,042 2,625,831 1,710,400Pig fat lean meat free & poultry fat unrendered or o/w extracted .........................................................

Kilograms 0 0 0 0

Meat & edible meat offal, cured; edible flours and meals of meat or meat offal ...................................

Kilograms 16,665,917 16,561,931 20,451,890 24,279,275

Meat and Edible Meat Offal ................................. Kilograms 469,191 160,563 1,274,417 197,892

Milk and cream, not concentrated nor sweetened Kilograms 192,948,169 223,877,969 474,851,991 640,822,310

Milk and cream, concentrated or sweetened ........ Kilograms 0 0 0 0Whey, w/n concentrated or sweet; natural milk products w/n sweet, nes ........................................

Kilograms 0 199,950 0 702,214

Dairy Products ..................................................... Kilograms 0 72,719 0 196,655

Honey .................................................................... Kilograms 10,736 14 62,566 31

Birds' eggs, in shell, fresh, preserved or cooked ... Dozen 10,736 272,683 62,566 898,900

Birds' eggs unshelled, egg yolks, fr dried .............. Dozen 4,972,647 3,599,622 18,781,935 14,435,170

Eggs and Edible Prodcuts of Animal Origin ..... Dozen 415,090 432,110 739,039 607,413

Guts, bladders and stomachs of animals .............. Kilograms 2,070,620 1,992,369 6,047,088 6,746,892

Bones & horn-cores degelatinised ........................ Kilograms 2,485,710 ... 6,786,127 7,354,305

Ivory, whalebone etc .............................................. Kilograms 82,500 0 558,055 0

Ambergris, castoreum, etc ..................................... Kilograms 2,687,861 2,132,080 8,770,883 7,263,250Animal products nes; unfit for human consumption ..........................................................

N/A 428,112 1,226,187 1,251,998 2,230,425

Products of Animal Origin .................................. .......... 93,708 4,189 270,842 44,101

Bulbs, tubers, corms, etc ....................................... N/A 0 0 940,804 1,278,796

Plants, live, nes (incl their roots)............................ N/A 2,660,625 3,518,698 5,075,208 4,884,154

Foliage, branches etc ........................................... N/A 16,867,790 15,700,726

Live Tree, Plant, Flowers, Floriculture .............. N/A 0 0 3,225 0

Potatoes, fresh or chilled ....................................... Metric Ton 0 496 175,636 159,797

Onions, shallots, garlic, leeks & other veg, fr/ chd Kilogram 61,045 55,715 556,869 499,260

Cabbages, cauliflowers, kohlrabi, kale, fr or chd ... Kilogram 735,730 659,057

Carrots, turnips, salad beetroot, fresh or chilled ... Kilogram 103,080 72,573 33,550,498 22,765,131

Cucumbers and gherkins, fresh or chilled ............. Kilogram 2,280,408 1,831,401 2,211,951 2,443,072Leguminous vegetables, shelled or unshelled, fresh or chilled .......................................................

Kilogram 272,438 185,703 127,688 111,700

Vegetables nes, fresh or chilled ............................ Kilogram 290,528 96,980 119,026 68,607

Vegetables, frozen ................................................. Kilogram 4,763 7,984 2,677 4,512

Vegetables dried, whole, cut, sliced, broken ......... Kilogram 586,745 111,468 633,617 94,363

Vegetables, leguminous dried, shelled .................. Kilogram 198,193 65,687 252,516 73,686

Edible Vegetables and Certain Roots and Tubers, Pulses .....................................................

............ 363 22,106 3,314 19,790

Fruits & nuts, frozen .............................................. Kilogram 0 1,270 0 4,261Fruits & nuts, dried ................................................ Kilogram 998 2,864 2,284 14,911

Fruit & Nuts .......................................................... Kilogram 998 4,134 2,284 19,172

33

Coffee w/n roast or decaff ..................................... Kilogram 1,946 2,670 18,763 41,704Seeds of anise, badian, fennel, coriander, cumin, caraway or juniper .................................................

Kilogram 437,931 521,899 954,725 969,139

Coffee, Tea, Mate and Spices ............................. Kilogram 439,877 524,569 973,488 1,010,843

Wheat and meslin .................................................. Metric Ton 3,452,529 2,681,082 886,736,957 921,194,871Rye......................................................................... Metric Ton 77,137 55,128 17,267,535 15,775,843

Barley ..................................................................... Metric Ton 189,612 127,307 45,827,520 37,403,703

Oats ....................................................................... Kilogram 513,989,721 536,613,992 111,870,705 137,578,363

Maize (corn) ........................................................... Kilogram 70,995,788 99,825,846 15,182,354 31,354,052

Rice ........................................................................ Kilogram 0 0 0 0

Grain sorghum ....................................................... Kilogram 4,536 17,010 2,534 11,744

Buckwheat, millet and canary seed; other cereals Kilogram 17,605,139 24,161,019 9,730,258 16,786,096

Grains, Bulk or Cereals ....................................... ............ 1,086,617,863 1,160,104,672

Wheat or meslin flour ............................................. Kilogram 5,287,715 4,883,473 3,947,897 3,768,857Cereal flours other than of wheat or meslin........... Kilogram 210,865 211,047 175,208 186,146

Cereal grouts, meal and pellets ............................. Kilogram 86,869,149 88,701,703 35,877,376 44,307,939

Cereal grn o/w worked (ex hulled etc) ................... Kilogram 83,944,768 81,321,936 41,968,533 47,204,349

Flour, meal & pdr of veg ........................................ Kilogram 743,958 1,128,045 825,907 1,204,743

Malt, whether or not roasted .................................. Kilogram 22,611,777 9,066,766 12,747,665 5,554,245

Starches; inulin ...................................................... Kilogram 1,600,956 1,159,085 1,101,263 760,751

Grain Products, Malt, Starches .......................... Kilogram 201,269,188 186,472,055 96,643,849 102,987,030

Soya beans, whether or not broken ...................... Kilogram 337,613,971 355,032,640 126,314,687 171,258,861Linseed, whether or not broken ............................. Kilogram 142,610,828 64,208,428 66,797,032 42,189,618

Rape or colza seeds, whether or not broken......... Kilogram 1,609,158,267 1,320,118,857 732,104,410 768,509,598

Sunflower seeds, whether or not broken ............... Kilogram 44,465,214 41,380,916 32,246,309 32,331,193

Oil seeds and oleaginous frutis nes, w/n broken ... Kilogram 20,703,405 16,335,642 21,370,638 17,869,628

Flour and meals of oil seeds or oleaginous fruits .. Kilogram 3,144,020 10,797,577 1,336,945 3,854,861

Seeds, fruit and spores, for sowing ....................... Kilogram 18,036,916 22,642,003 35,530,963 47,492,887Plants & pts (incl seeds & fruits) for perf, pharm etc, fr, dried ............................................................

Kilogram 2,732 0 12,599 0

Locust beans etc, fr,chd,frz/drd, nes ..................... Kilogram 44,876 80,631 67,362 135,678

Cereal straw & husks, unprepared ........................ Metric Ton 72 901 7,104 117,745Swedes, mangolds, fodder roots, hay, lucerne (alfalfa), clover etc, w/n pellet ................................

Metric Ton 11,237 14,259 2,054,145 2,552,712

Oilseeds, Seeds for Sowing, Fodder ................. ............ 1,017,842,194 1,086,312,781

Lac; natural gums, resins, gum-resins & oleoresins

Kilogram 6,768 0 24,466 0

Vegetable saps & extracts .................................... Kilogram 3,350,573 4,227,816 7,180,145 9,555,713

Lac; Gums, Resins, Saps & Extracts ................. Kilogram 3,357,341 4,227,816 7,204,611 9,555,713

Vegetable products, nes ........................................ N/A 0 0 24,426 35,175Vegetable Plaiting Materials; Other Products .. .......... 24,426 35,175

Pig (incl lard) & poultry fat, rendered ..................... Kilogram 2,209,364 3,934,772 1,235,346 3,495,136Soya-bean oil and its fractions, w/n refined ........... Kilogram 38,179 0 43,476 0Safflower, sunflower or cotton-seed oil & fractions, w/n refined .............................................

Kilogram 822,720 606,700 428,500 303,350

Rape, colza or mustard oil & their fract, w/n ref'd .. Kilogram 291,586,926 306,191,415 284,827,970 396,529,233

Fixed veg fats/oils (incl jojoba oil), fract, w/n ref'd . Kilogram 465,353 811,443 2,101,370 3,580,382

Animal or veg fats, oils & fract, hydrog w/n ref'd ... Kilogram 238,832 214,590 174,350 309,774Margarine; edible mx or prep of animal or veg fats & oils or fractions ...................................................

Kilogram 557,979 218,337 919,910 394,248

Waxes veg (o/t triglycerides) beeswax, insect waxes & spermaceti, w/n ref'd/col .........................

Kilogram 308,212 289,201 1,533,920 1,625,803

Animal - Veg Fats & Oils, Margarine .................. Kilogram 296,227,565 312,266,458 291,264,842 406,237,926

Sausages & sim prod, of meat, meat offal or blood; food prep of these prod...............................

Kilogram 1,845 0 7,353 0

Prepared/preserved meat, meat offal/blood, nes .. Kilogram 13,441 111,587 74,119 448,354Prepared or preserved fish; caviar & caviar subst prepared from fish eggs .........................................

Kilogram 197,627 319,650 1,828,388 2,539,554

Preparations of Meat ........................................... Kilogram 212,913 431,237 1,909,860 2,987,908

34

Sugars, nes ............................................................ Kilogram 8,673 0 4,250 0Sugar confectionery (cntg white choc), not containing cocoa ....................................................

Kilogram 477,891 415,926 2,061,587 1,850,269

Sugars and Sugar Confectionery ...................... Kilogram 2,065,837 1,850,269

Chocolate and other food preparations incl cocoa Kilogram 47,752 31,853 210,352 208,919

Cocoa and Cocoa Preparations ......................... Kilogram 210,352 208,919

Malt extract; food prep of flour ............................... Kilogram 1,273,941 1,158,909 2,881,851 3,165,750

Pasta w/n cooked/stuffed, o/w prep ...................... Kilogram 654 618 648 3,011

Bread, pastry etc w/n cntg cocoa .......................... Kilogram 1,016,550 3,953,171 3,970,660 13,043,775

Preparations of Grains, Pasta ............................ Kilogram 2,291,145 5,112,698 6,853,159 16,212,536

Vegetables nes, prep or presv, frozen .................. Kilogram 337,520,692 203,645,480 300,889,824 169,937,372

Vegetables nes, prep or presv, not frozen ............ Kilogram 167,281 245,158 704,360 1,060,301Jams, fruit jellies, marmalades, fruit or nut purée & pastes, ckd, w/n sweetened ...............................

Kilogram 0 0 0 0

Fruits, nuts & edible pts of plants o/w prep or presv w/n sweetened, nes .....................................

Kilogram 9,510 39,385 37,869 132,989

Preparatons of Vegetables, Fruit & Nuts .......... Kilogram 337,697,483 203,930,023 301,632,053 171,130,662

Sauces & prep nes ................................................ Kilogram 320,686 298,956 563,977 386,307

Soups, broths & prep thereof ................................. Kilogram 16,480 0 65,531 0

Ice cream and other edible ice w/n ctng cocoa Kilogram 55 0 213 0

Food preparations, nes .......................................... Kilogram 2,777,345 186,504 6,093,615 1,831,163

Miscellaneous Edible Preparations ................... Kilogram 3,114,566 485,460 6,723,336 2,217,470

Waters, incl nat or arti min or aerated waters........ Liter 1,752,160 3,919,000 455,034 688,717

Waters, min or aerated, sweet or flav, nonalc bev Liter 301,402 101,956 631,187 149,678

Beer made from malt ............................................. Liter 0 0 0 0

Wine of fresh grapes, incl fortified ......................... Liter 0 0 0 0

Spirits liqueurs & other spirit beverages ................ Liter 3,554,465 368,699 3,031,318 389,483

Beverages, Spirits and Vinegar ......................... Liter 5,608,027 4,389,655 4,117,539 1,227,878

Flours etc of meat, meat offal, fish, crustaceans etc unfit for human cons; greaves .........................

Kilogram 9,563,000 7,817,000 3,493,403 3,229,338

Bran, sharps etc w/n pellet .................................... Kilogram 3,609,037 5,192,131 1,447,469 1,819,461

Starch & sim residues, beet-pulp etc ..................... Kilogram 50,000 22,000 8,184 3,824

Soya-bean oil-cake and other solid residues ........ Kilogram 0 0 0 0

Oil-cake nes ........................................................... Kilogram 330,434,118 328,991,964 71,651,541 79,166,989

Vegetable mat, waste, residues & by-prod nes ..... Kilogram 507,374 1,964,428 134,086 442,224

Animal feed preparations, nes ............................... Kilogram 33,655,509 14,596,155 12,432,264 11,634,876

Food Industry Residues & Waste, Prepared Fodder ...................................................................

Kilogram 377,819,038 358,583,678 89,166,947 96,296,712

Essential Oils ....................................................... Kilogram 0 0 0 0

Albumins, albuminates & other albumin derivs ..... Kilogram 2,045,819 573,708 6,507,156 1,904,579Peptones & derivs; protein substances & derivs, nes; hide powder ...................................................

Kilogram 231,345 222,137 657,160 629,971

Dextrins & other mod starches; glues based on starches, dextrins or other mod starches ..............

Kilogram 0 0 0 0

Caseins & Albumins ............................................ Kilogram 2,277,164 795,845 7,164,316 2,534,550

Raw hides & skins of bov or equ animals .............. Number 16 26,014 696 195,428Raw hides & skins of sheep or lambs w/n with woollen or split ......................................................

Number 103 0 321 0

Raw hides & skins nes, w/n dehaired or split ....... Number 12,151 15,747 244,003 359,680

Raw Hides, Skins ................................................. Number 12,270 41,761 245,020 555,108

Raw furskins & pieces suitable for furriers’ use Number 10,803 52,694 119,981 1,211,091Furskins ................................................................ Number 10,803 52,694 119,981 1,211,091

Flax, raw or processed not spun; flax tow & waste Kilogram 17,643,712 21,352,656 8,297,275 9,975,225True hemp (Cannabis sativa L), raw or processed, not spun; tow & waste of true hemp ...

Kilogram 4,500 11,659 1,184 6,631

Other Textile Fibers ............................................. Kilogram 17,648,212 21,364,315 8,298,459 9,981,856

Fish and Crustaceans ......................................... ............ 52,795,232 51,672,663

TOTAL EXPORTS................................................. ............ 4,063,042,219 4,300,958,667

35

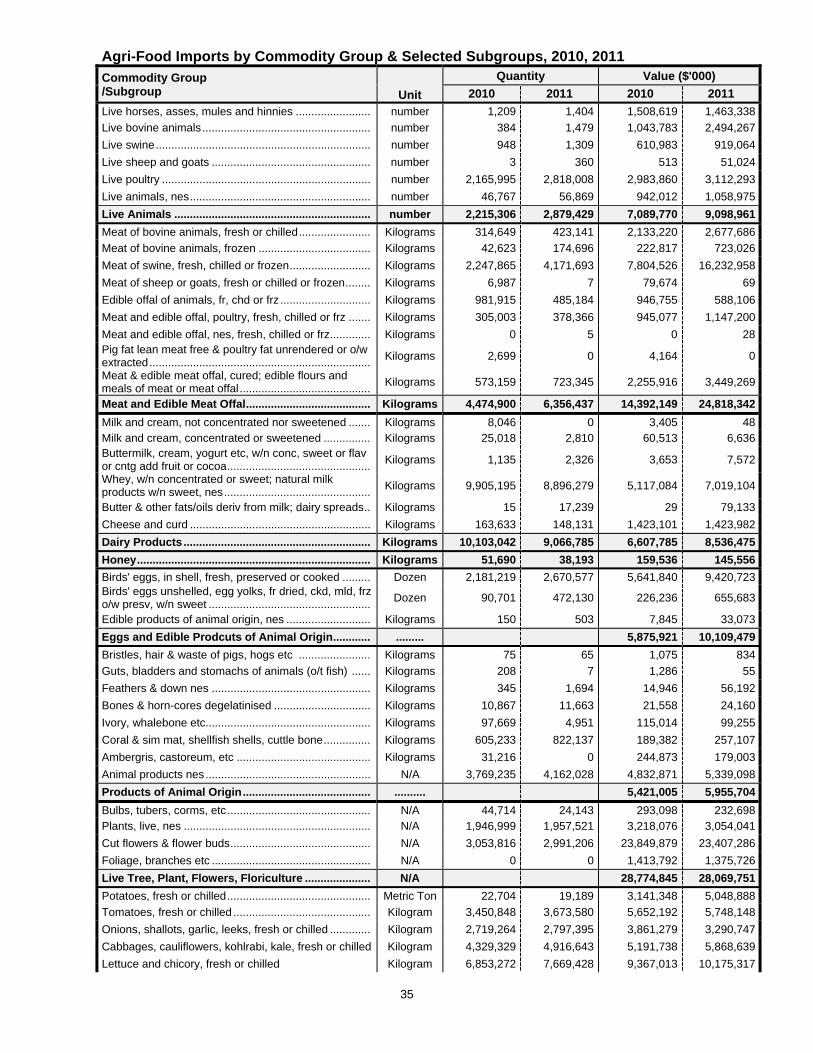

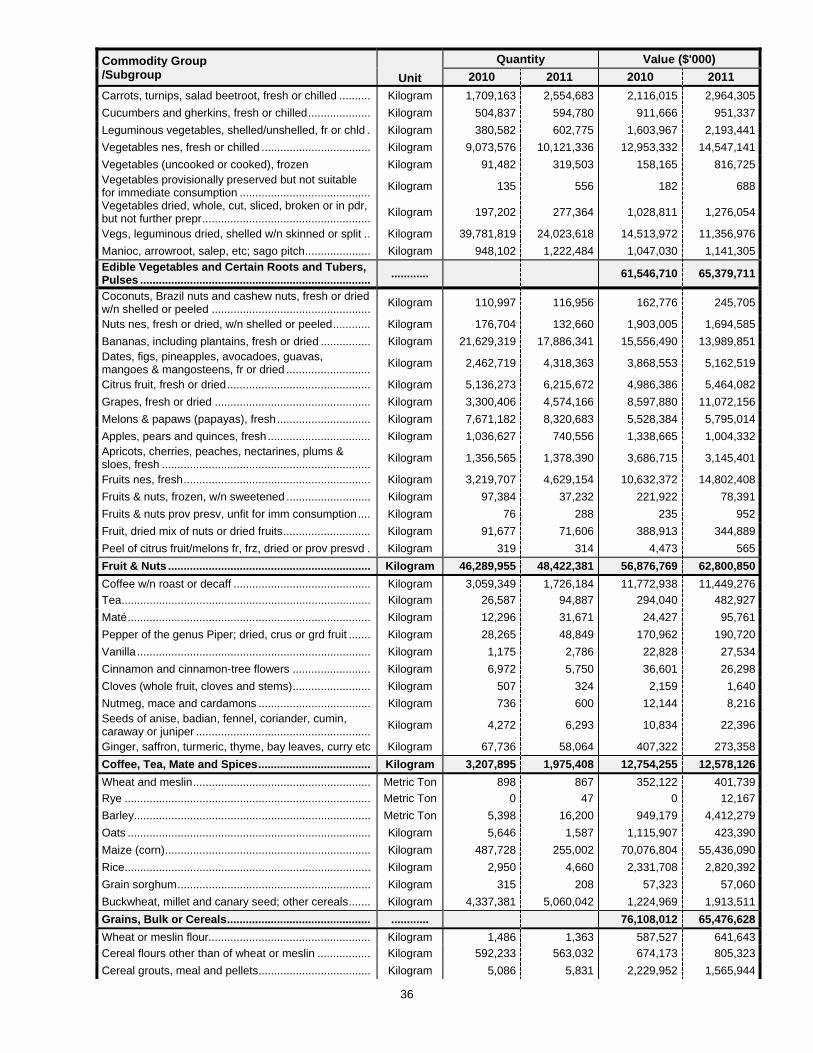

Agri-Food Imports by Commodity Group & Selected Subgroups, 2010, 2011

Commodity Group /Subgroup

Unit

Quantity Value ($'000)

2010 2011 2010 2011

Live horses, asses, mules and hinnies ........................ number 1,209 1,404 1,508,619 1,463,338

Live bovine animals ...................................................... number 384 1,479 1,043,783 2,494,267

Live swine ..................................................................... number 948 1,309 610,983 919,064

Live sheep and goats ................................................... number 3 360 513 51,024

Live poultry ................................................................... number 2,165,995 2,818,008 2,983,860 3,112,293

Live animals, nes .......................................................... number 46,767 56,869 942,012 1,058,975

Live Animals ............................................................... number 2,215,306 2,879,429 7,089,770 9,098,961

Meat of bovine animals, fresh or chilled ....................... Kilograms 314,649 423,141 2,133,220 2,677,686

Meat of bovine animals, frozen .................................... Kilograms 42,623 174,696 222,817 723,026

Meat of swine, fresh, chilled or frozen .......................... Kilograms 2,247,865 4,171,693 7,804,526 16,232,958

Meat of sheep or goats, fresh or chilled or frozen ........ Kilograms 6,987 7 79,674 69

Edible offal of animals, fr, chd or frz ............................. Kilograms 981,915 485,184 946,755 588,106

Meat and edible offal, poultry, fresh, chilled or frz ....... Kilograms 305,003 378,366 945,077 1,147,200

Meat and edible offal, nes, fresh, chilled or frz ............. Kilograms 0 5 0 28Pig fat lean meat free & poultry fat unrendered or o/w extracted .......................................................................

Kilograms 2,699 0 4,164 0

Meat & edible meat offal, cured; edible flours and meals of meat or meat offal ..........................................

Kilograms 573,159 723,345 2,255,916 3,449,269

Meat and Edible Meat Offal ........................................ Kilograms 4,474,900 6,356,437 14,392,149 24,818,342

Milk and cream, not concentrated nor sweetened ....... Kilograms 8,046 0 3,405 48Milk and cream, concentrated or sweetened ............... Kilograms 25,018 2,810 60,513 6,636Buttermilk, cream, yogurt etc, w/n conc, sweet or flav or cntg add fruit or cocoa ..............................................

Kilograms 1,135 2,326 3,653 7,572

Whey, w/n concentrated or sweet; natural milk products w/n sweet, nes ...............................................

Kilograms 9,905,195 8,896,279 5,117,084 7,019,104

Butter & other fats/oils deriv from milk; dairy spreads .. Kilograms 15 17,239 29 79,133

Cheese and curd .......................................................... Kilograms 163,633 148,131 1,423,101 1,423,982

Dairy Products ............................................................ Kilograms 10,103,042 9,066,785 6,607,785 8,536,475

Honey ........................................................................... Kilograms 51,690 38,193 159,536 145,556

Birds' eggs, in shell, fresh, preserved or cooked ......... Dozen 2,181,219 2,670,577 5,641,840 9,420,723Birds' eggs unshelled, egg yolks, fr dried, ckd, mld, frz o/w presv, w/n sweet ....................................................

Dozen 90,701 472,130 226,236 655,683

Edible products of animal origin, nes ........................... Kilograms 150 503 7,845 33,073