Embed Size (px)

Citation preview

i

State Taxation Acts (Taxation Reform Implementation) Act 2001

Act No. 48/2001

TABLE OF PROVISIONS

Section Page

PART 1—PRELIMINARY 1

1. Purpose 1 2. Commencement 2

PART 2—HEALTH BENEFIT LEVY 3

3. Casino Control Act 1991 3 4. Gaming Machine Control Act 1991 4

PART 3—DUTIES ACT 2000 6

5. Abolition of lease duty 6 6. Abolition of duty on unquoted marketable securities and

associated duties from July 2003 6 7. New section 148A inserted 7

148A. Mortgage duty abolished from July 2004 7 8. Transitional provision consequent on the repeal of lease duty 7

PART 4—LAND TAX ACT 1958 9

9. Increase in land tax threshold 9

PART 5—PAY-ROLL TAX ACT 1971 11

10. Pre-January 1996 accrued leave 11 11. Eligible termination payments 11 12. Reduction in pay-roll tax rate 12 13. Increase in pay-roll tax threshold from 2003 12 14. Fringe benefits tax gross-up 15

Section Page

ii

PART 6—STAMPS ACT 1958 18

15. Abolition of lease duty 18 ═══════════════

ENDNOTES 20

1

State Taxation Acts (Taxation Reform Implementation) Act 2001†

[Assented to 27 June 2001]

The Parliament of Victoria enacts as follows:

PART 1—PRELIMINARY

1. Purpose

The purpose of this Act is to amend the Casino Control Act 1991, the Duties Act 2000, the Gaming Machine Control Act 1991, the Land Tax Act 1958, the Pay-roll Tax Act 1971 and the Stamps Act 1958 to implement the reform of State taxes.

Victoria

No. 48 of 2001

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

2

2. Commencement

(1) This Part and Part 4 come into operation on the day on which this Act receives the Royal Assent.

(2) Part 6 is deemed to have come into operation on 26 April 2001.

(3) Parts 2, 3 (other than section 6(4)) and 5 come into operation on 1 July 2001.

(4) Section 6(4) comes into operation on 1 July 2003.

_______________

s. 2

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

3

PART 2—HEALTH BENEFIT LEVY

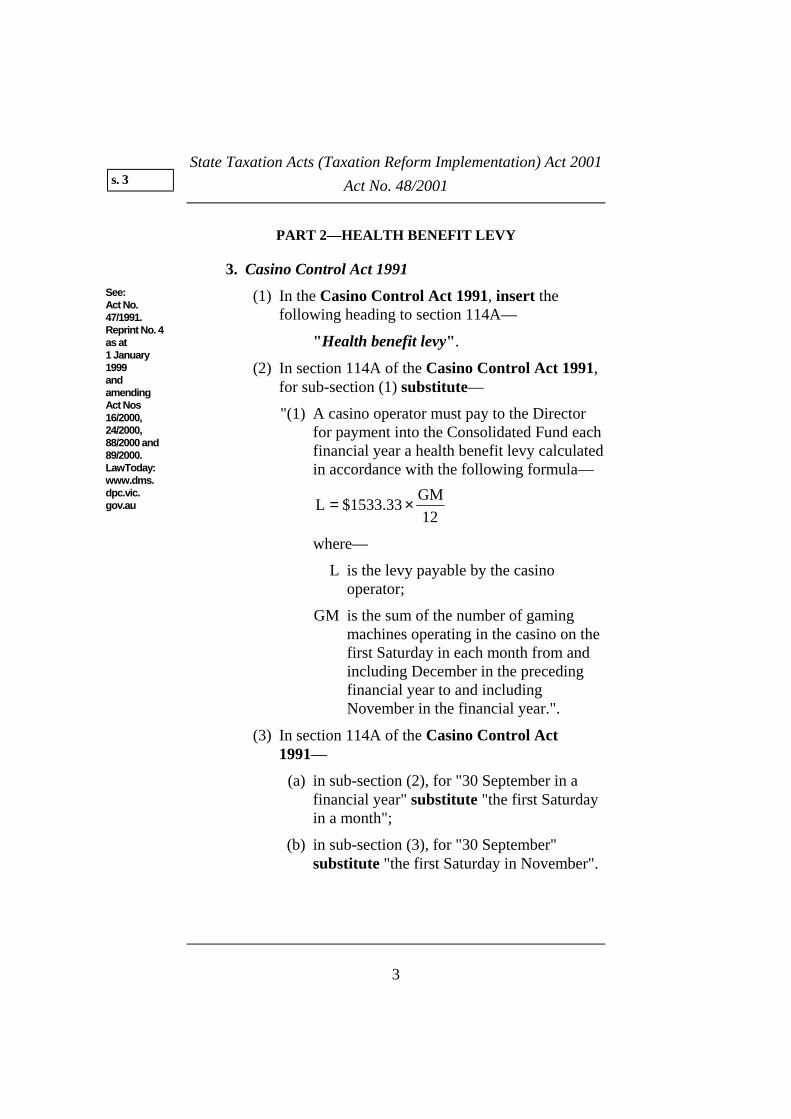

3. Casino Control Act 1991

(1) In the Casino Control Act 1991, insert the following heading to section 114A—

"Health benefit levy".

(2) In section 114A of the Casino Control Act 1991, for sub-section (1) substitute—

"(1) A casino operator must pay to the Director for payment into the Consolidated Fund each financial year a health benefit levy calculated in accordance with the following formula—

L $1533.33 GM12

= ×

where—

L is the levy payable by the casino operator;

GM is the sum of the number of gaming machines operating in the casino on the first Saturday in each month from and including December in the preceding financial year to and including November in the financial year.".

(3) In section 114A of the Casino Control Act 1991—

(a) in sub-section (2), for "30 September in a financial year" substitute "the first Saturday in a month";

(b) in sub-section (3), for "30 September" substitute "the first Saturday in November".

s. 3

See: Act No. 47/1991. Reprint No. 4 as at 1 January 1999 and amending Act Nos 16/2000, 24/2000, 88/2000 and 89/2000. LawToday: www.dms. dpc.vic. gov.au

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

4

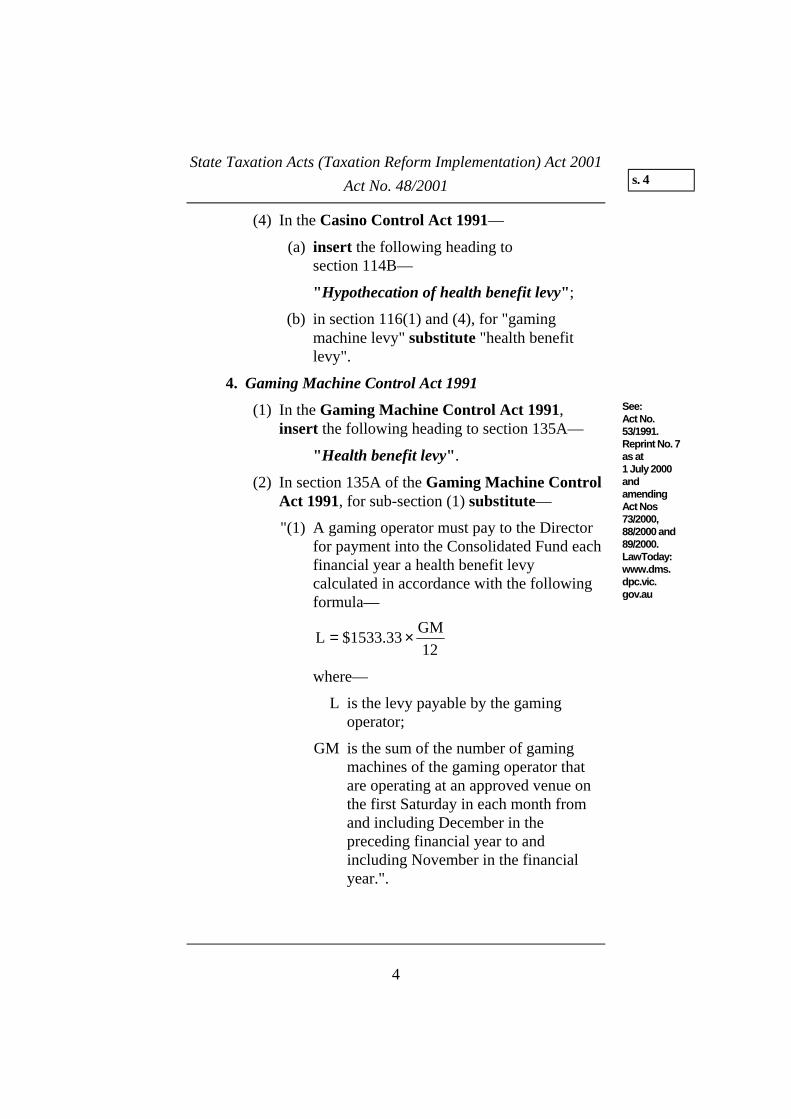

(4) In the Casino Control Act 1991—

(a) insert the following heading to section 114B—

"Hypothecation of health benefit levy";

(b) in section 116(1) and (4), for "gaming machine levy" substitute "health benefit levy".

4. Gaming Machine Control Act 1991

(1) In the Gaming Machine Control Act 1991, insert the following heading to section 135A—

"Health benefit levy".

(2) In section 135A of the Gaming Machine Control Act 1991, for sub-section (1) substitute—

"(1) A gaming operator must pay to the Director for payment into the Consolidated Fund each financial year a health benefit levy calculated in accordance with the following formula—

L $1533.33 GM12

= ×

where—

L is the levy payable by the gaming operator;

GM is the sum of the number of gaming machines of the gaming operator that are operating at an approved venue on the first Saturday in each month from and including December in the preceding financial year to and including November in the financial year.".

s. 4

See: Act No. 53/1991. Reprint No. 7 as at 1 July 2000 and amending Act Nos 73/2000, 88/2000 and 89/2000. LawToday: www.dms. dpc.vic. gov.au

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

5

(3) In section 135A of the Gaming Machine Control Act 1991—

(a) in sub-section (2), for "30 September in a financial year" substitute "the first Saturday in a month";

(b) in sub-section (3), for "30 September" substitute "the first Saturday in November".

(4) In the Gaming Machine Control Act 1991, insert the following heading to section 135B—

"Hypothecation of health benefit levy".

_______________

s. 4

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

6

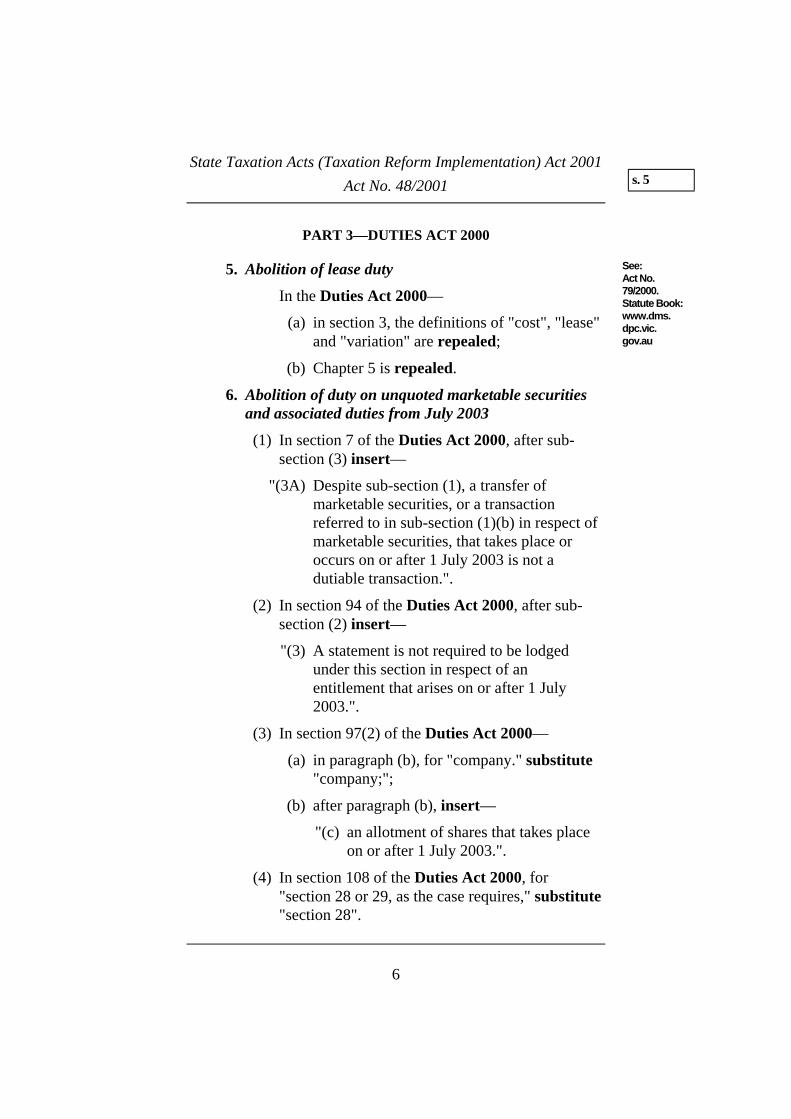

PART 3—DUTIES ACT 2000

5. Abolition of lease duty

In the Duties Act 2000—

(a) in section 3, the definitions of "cost", "lease" and "variation" are repealed;

(b) Chapter 5 is repealed.

6. Abolition of duty on unquoted marketable securities and associated duties from July 2003

(1) In section 7 of the Duties Act 2000, after sub-section (3) insert—

"(3A) Despite sub-section (1), a transfer of marketable securities, or a transaction referred to in sub-section (1)(b) in respect of marketable securities, that takes place or occurs on or after 1 July 2003 is not a dutiable transaction.".

(2) In section 94 of the Duties Act 2000, after sub-section (2) insert—

"(3) A statement is not required to be lodged under this section in respect of an entitlement that arises on or after 1 July 2003.".

(3) In section 97(2) of the Duties Act 2000—

(a) in paragraph (b), for "company." substitute "company;";

(b) after paragraph (b), insert—

"(c) an allotment of shares that takes place on or after 1 July 2003.".

(4) In section 108 of the Duties Act 2000, for "section 28 or 29, as the case requires," substitute "section 28".

See: Act No. 79/2000. Statute Book: www.dms. dpc.vic. gov.au

s. 5

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

7

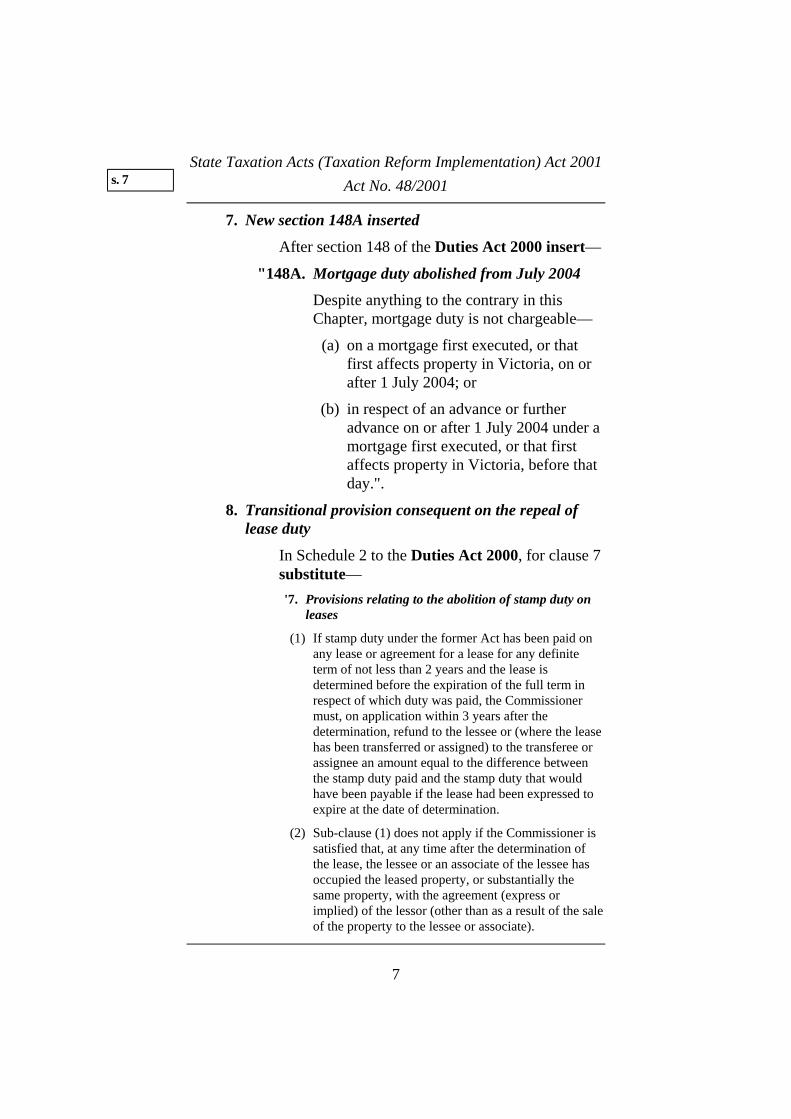

7. New section 148A inserted

After section 148 of the Duties Act 2000 insert—

"148A. Mortgage duty abolished from July 2004

Despite anything to the contrary in this Chapter, mortgage duty is not chargeable—

(a) on a mortgage first executed, or that first affects property in Victoria, on or after 1 July 2004; or

(b) in respect of an advance or further advance on or after 1 July 2004 under a mortgage first executed, or that first affects property in Victoria, before that day.".

8. Transitional provision consequent on the repeal of lease duty

In Schedule 2 to the Duties Act 2000, for clause 7 substitute— '7. Provisions relating to the abolition of stamp duty on

leases

(1) If stamp duty under the former Act has been paid on any lease or agreement for a lease for any definite term of not less than 2 years and the lease is determined before the expiration of the full term in respect of which duty was paid, the Commissioner must, on application within 3 years after the determination, refund to the lessee or (where the lease has been transferred or assigned) to the transferee or assignee an amount equal to the difference between the stamp duty paid and the stamp duty that would have been payable if the lease had been expressed to expire at the date of determination.

(2) Sub-clause (1) does not apply if the Commissioner is satisfied that, at any time after the determination of the lease, the lessee or an associate of the lessee has occupied the leased property, or substantially the same property, with the agreement (express or implied) of the lessor (other than as a result of the sale of the property to the lessee or associate).

s. 7

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

8

(3) An application for a refund under this clause must be accompanied by—

(a) the lease or agreement for a lease on which stamp duty was paid; and

(b) a declaration by the applicant stating that neither the lessee nor any associate of the lessee has occupied or will occupy the leased property, or substantially the same property, after the determination of the lease (other than as a result of the sale of the property to the lessee or associate).

(4) A person must not knowingly make a false declaration under sub-clause (3)(b).

Penalty: 300 penalty units in the case of a body corporate;

60 penalty units in any other case.

(5) In this section—

"determination" includes surrender and forfeiture.'.

_______________

s. 8

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

9

PART 4—LAND TAX ACT 1958

9. Increase in land tax threshold

(1) In section 7A of the Land Tax Act 1958—

(a) for "1997" substitute "2001";

(b) for "$85" substitute "$125".

(2) In the Second Schedule to the Land Tax Act 1958—

(a) insert the following heading to clause 3—

"Land Tax for 1998, 1999, 2000 and 2001";

(b) in clause 3, for "or a subsequent year" substitute ", 1999, 2000 or 2001".

(3) In the Second Schedule to the Land Tax Act 1958, after clause 3 insert—

"4. Land tax for 2002 and subsequent years

If the total unimproved value of land of an owner as assessed under this Act for 2002 or a subsequent year is not less than the amount shown in column 1 of an item in Table D and, if an amount is shown in column 2 of that item, less than the amount shown in column 2 of that item, the duty of land tax payable on the land is the amount determined in accordance with column 3 of that item.

TABLE D

Item Column 1 Column 2 Column 3

$ $

1. 0 125 000 Nil

2. 125 000 200 000 $125 and 0·1 cents for each $1 of the value that exceeds $125 000

3. 200 000 540 000 $200 and 0·2 cents for each $1 of the value that exceeds $200 000

See: Act No. 6289. Reprint No. 10 as at 14 October 1999 and amending Act Nos 69/2000 and 10/2001. LawToday: www.dms. dpc.vic. gov.au

s. 9

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

10

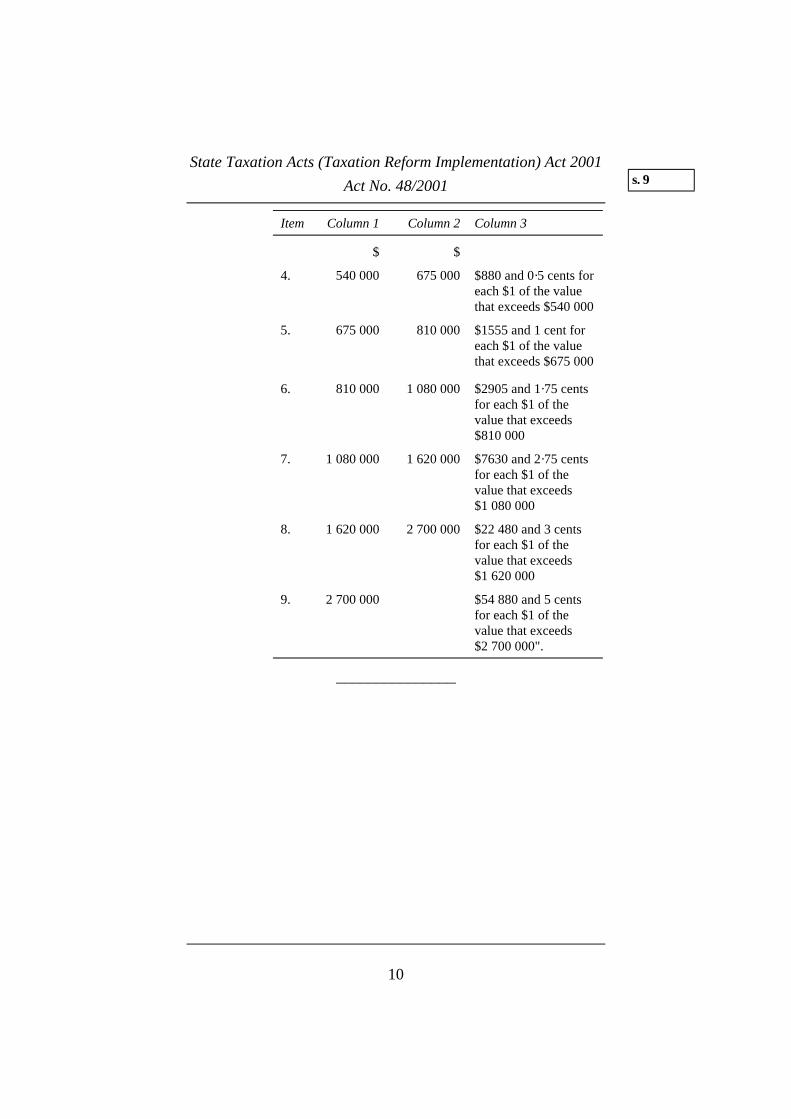

Item Column 1 Column 2 Column 3

$ $

4. 540 000 675 000 $880 and 0·5 cents for each $1 of the value that exceeds $540 000

5. 675 000 810 000 $1555 and 1 cent for each $1 of the value that exceeds $675 000

6. 810 000 1 080 000 $2905 and 1·75 cents for each $1 of the value that exceeds $810 000

7. 1 080 000 1 620 000 $7630 and 2·75 cents for each $1 of the value that exceeds $1 080 000

8. 1 620 000 2 700 000 $22 480 and 3 cents for each $1 of the value that exceeds $1 620 000

9. 2 700 000 $54 880 and 5 cents for each $1 of the value that exceeds $2 700 000".

_______________

s. 9

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

11

PART 5—PAY-ROLL TAX ACT 1971

10. Pre-January 1996 accrued leave

In section 3 of the Pay-roll Tax Act 1971—

(a) in sub-section (1), in the definition of "wages", in paragraph (e), omit "subject to sub-section (2F),";

(b) sub-section (2F) is repealed.

11. Eligible termination payments

(1) In section 3(1) of the Pay-roll Tax Act 1971, in the definition of "wages", in paragraph (e), for sub-paragraph (iii) substitute—

"(iii) so much of any eligible termination payment (within the meaning of section 27A of the Income Tax Assessment Act 1936 of the Commonwealth) paid or payable by an employer, whether or not paid to the employee or to any other person or body, that would be included in the assessable income of an employee under Subdivision AA of Division 2 of Part III of that Act if the whole of the eligible termination payment had been paid to the employee.".

(2) In section 6 of the Pay-roll Tax Act 1971, after sub-section (1AB) insert—

"(1AC) Wages referred to in paragraph (e) of the definition of "wages" in section 3(1) that are not paid in respect of services performed or rendered by an employee in a particular

See: Act No. 8154. Reprint No. 7 as at 1 September 1999 and amending Act Nos 6/2000, 42/2000, 97/2000 and 10/2001. LawToday: www.dms. dpc.vic. gov.au

s. 10

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

12

month are liable to pay-roll tax under this Act as if they were paid or payable in respect of services performed or rendered during the month in which they were paid or became payable.".

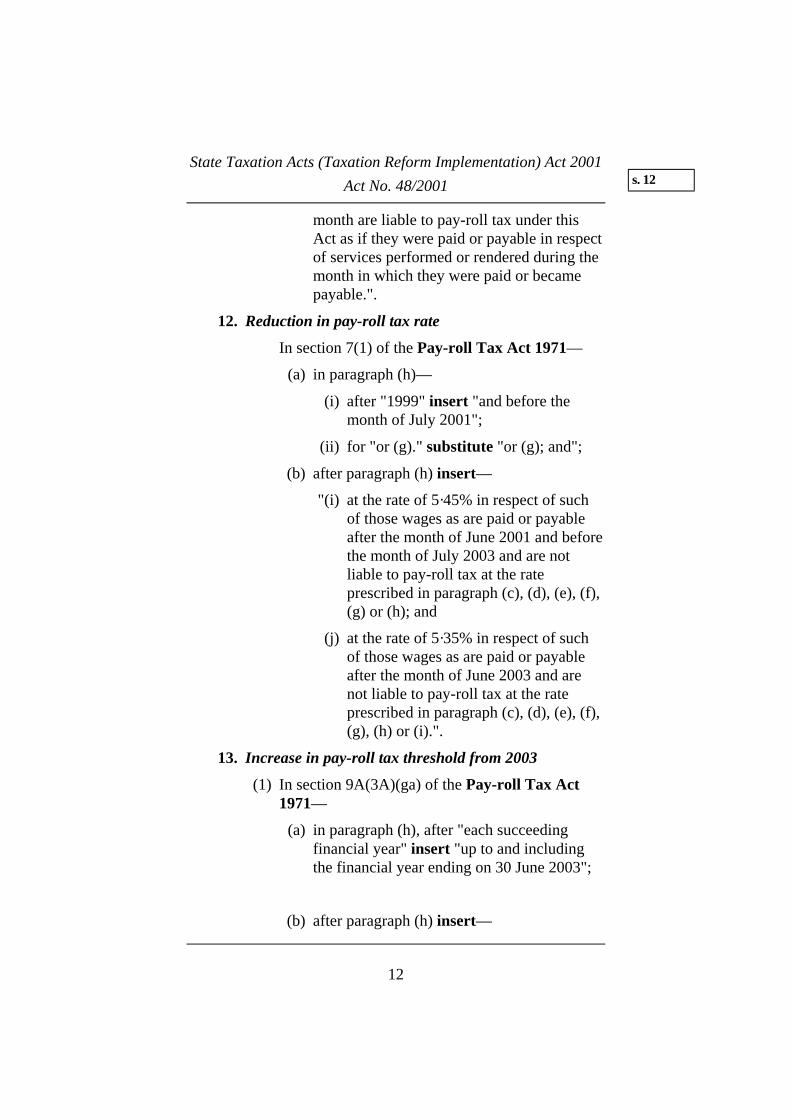

12. Reduction in pay-roll tax rate

In section 7(1) of the Pay-roll Tax Act 1971—

(a) in paragraph (h)—

(i) after "1999" insert "and before the month of July 2001";

(ii) for "or (g)." substitute "or (g); and";

(b) after paragraph (h) insert—

"(i) at the rate of 5·45% in respect of such of those wages as are paid or payable after the month of June 2001 and before the month of July 2003 and are not liable to pay-roll tax at the rate prescribed in paragraph (c), (d), (e), (f), (g) or (h); and

(j) at the rate of 5·35% in respect of such of those wages as are paid or payable after the month of June 2003 and are not liable to pay-roll tax at the rate prescribed in paragraph (c), (d), (e), (f), (g), (h) or (i).".

13. Increase in pay-roll tax threshold from 2003

(1) In section 9A(3A)(ga) of the Pay-roll Tax Act 1971—

(a) in paragraph (h), after "each succeeding financial year" insert "up to and including the financial year ending on 30 June 2003";

(b) after paragraph (h) insert—

s. 12

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

13

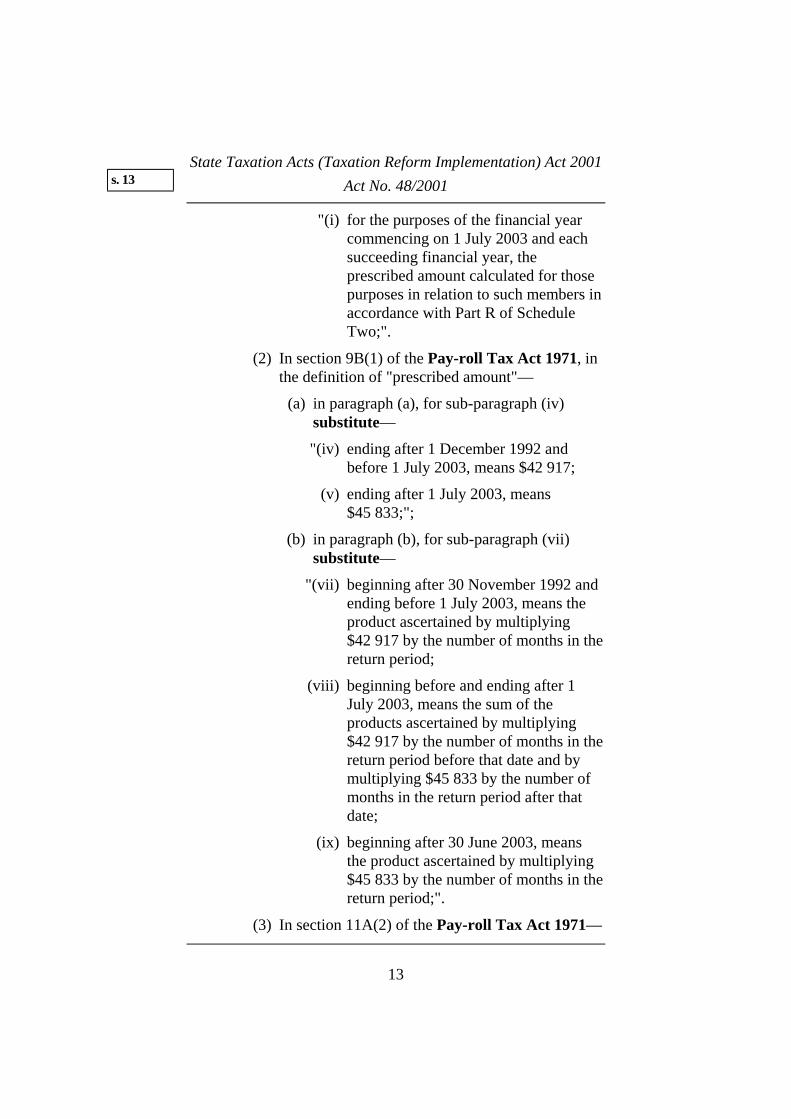

"(i) for the purposes of the financial year commencing on 1 July 2003 and each succeeding financial year, the prescribed amount calculated for those purposes in relation to such members in accordance with Part R of Schedule Two;".

(2) In section 9B(1) of the Pay-roll Tax Act 1971, in the definition of "prescribed amount"—

(a) in paragraph (a), for sub-paragraph (iv) substitute—

"(iv) ending after 1 December 1992 and before 1 July 2003, means $42 917;

(v) ending after 1 July 2003, means $45 833;";

(b) in paragraph (b), for sub-paragraph (vii) substitute—

"(vii) beginning after 30 November 1992 and ending before 1 July 2003, means the product ascertained by multiplying $42 917 by the number of months in the return period;

(viii) beginning before and ending after 1 July 2003, means the sum of the products ascertained by multiplying $42 917 by the number of months in the return period before that date and by multiplying $45 833 by the number of months in the return period after that date;

(ix) beginning after 30 June 2003, means the product ascertained by multiplying $45 833 by the number of months in the return period;".

(3) In section 11A(2) of the Pay-roll Tax Act 1971—

s. 13

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

14

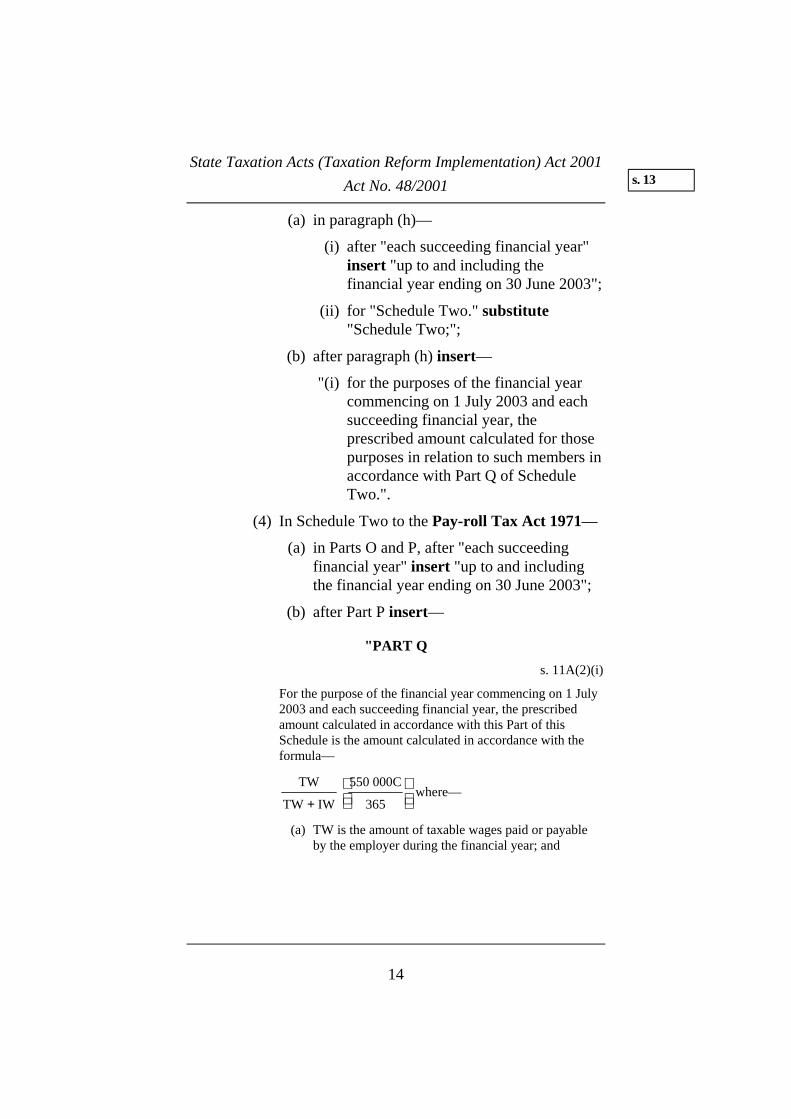

(a) in paragraph (h)—

(i) after "each succeeding financial year" insert "up to and including the financial year ending on 30 June 2003";

(ii) for "Schedule Two." substitute "Schedule Two;";

(b) after paragraph (h) insert—

"(i) for the purposes of the financial year commencing on 1 July 2003 and each succeeding financial year, the prescribed amount calculated for those purposes in relation to such members in accordance with Part Q of Schedule Two.".

(4) In Schedule Two to the Pay-roll Tax Act 1971—

(a) in Parts O and P, after "each succeeding financial year" insert "up to and including the financial year ending on 30 June 2003";

(b) after Part P insert—

"PART Q s. 11A(2)(i)

For the purpose of the financial year commencing on 1 July 2003 and each succeeding financial year, the prescribed amount calculated in accordance with this Part of this Schedule is the amount calculated in accordance with the formula—

TW

TW IW

550 000C

365+

where—

(a) TW is the amount of taxable wages paid or payable by the employer during the financial year; and

s. 13

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

15

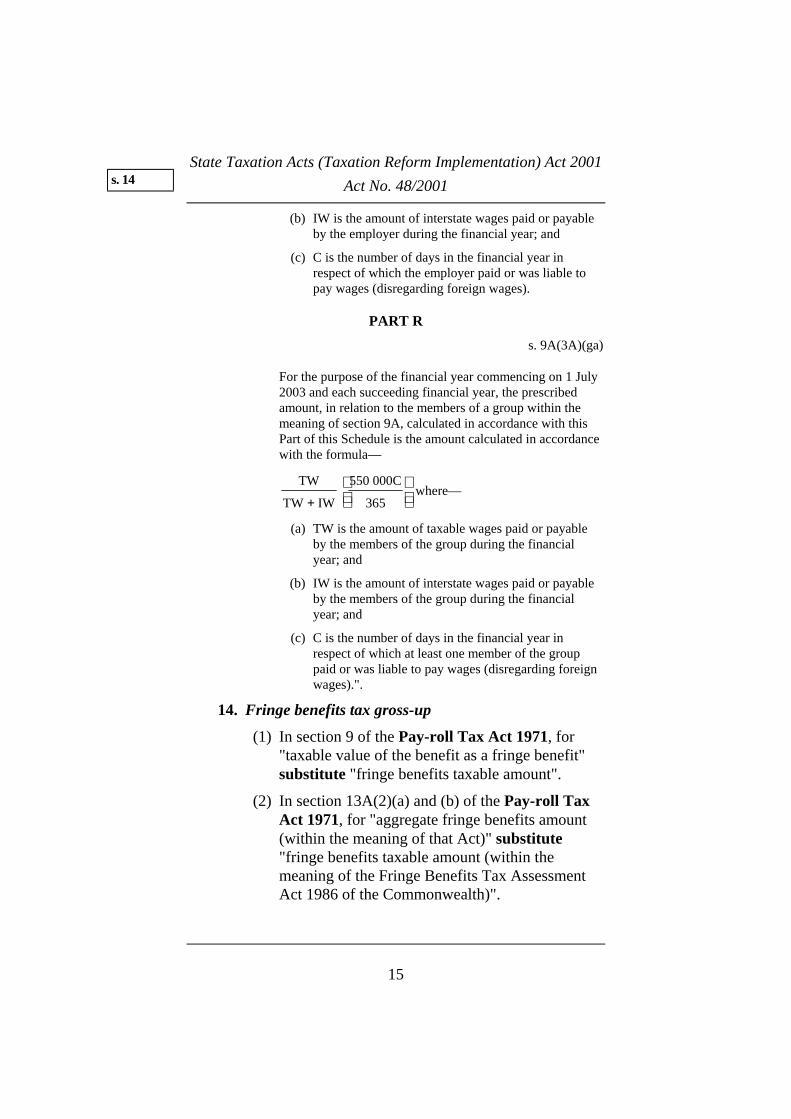

(b) IW is the amount of interstate wages paid or payable by the employer during the financial year; and

(c) C is the number of days in the financial year in respect of which the employer paid or was liable to pay wages (disregarding foreign wages).

PART R s. 9A(3A)(ga)

For the purpose of the financial year commencing on 1 July 2003 and each succeeding financial year, the prescribed amount, in relation to the members of a group within the meaning of section 9A, calculated in accordance with this Part of this Schedule is the amount calculated in accordance with the formula—

TW

TW IW

550 000C

365+

where—

(a) TW is the amount of taxable wages paid or payable by the members of the group during the financial year; and

(b) IW is the amount of interstate wages paid or payable by the members of the group during the financial year; and

(c) C is the number of days in the financial year in respect of which at least one member of the group paid or was liable to pay wages (disregarding foreign wages).".

14. Fringe benefits tax gross-up

(1) In section 9 of the Pay-roll Tax Act 1971, for "taxable value of the benefit as a fringe benefit" substitute "fringe benefits taxable amount".

(2) In section 13A(2)(a) and (b) of the Pay-roll Tax Act 1971, for "aggregate fringe benefits amount (within the meaning of that Act)" substitute "fringe benefits taxable amount (within the meaning of the Fringe Benefits Tax Assessment Act 1986 of the Commonwealth)".

s. 14

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

16

(3) In section 13A of the Pay-roll Tax Act 1971, after sub-section (6) insert—

'(7) If an employer is a prescribed sporting club, a reference in sub-section (2) to the fringe benefits taxable amount within the meaning of the Fringe Benefits Tax Assessment Act 1986 in relation to that employer is taken to be a reference to the sum of the type 1 aggregate fringe benefits amount and the type 2 aggregate fringe benefits amount (within the meaning of that Act) in relation to that employer.

(8) For the purposes of sub-section (7), a prescribed sporting club is a body prescribed by the regulations, being an association, club or other body—

(a) an object of which is to participate in, facilitate or promote a sporting activity; and

(b) that employs persons who play for the body in a competitive sporting activity; and

(c) that pays more than 50% of its total wages in a financial year to persons referred to in paragraph (b) in respect of services performed by those players being the playing of a sport.

(9) In this section, "competitive sporting activity" includes the playing of a sport, but does not include—

(a) the umpiring or refereeing of a sporting activity; or

s. 14

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

17

(b) the administration of a sporting activity; or

(c) the non-competitive practice of a sport.'.

_______________

s. 14

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

18

PART 6—STAMPS ACT 1958

15. Abolition of lease duty

(1) At the end of section 80 of the Stamps Act 1958 insert—

"(2) Sub-section (1) does not apply if the Comptroller is satisfied that, at any time after the surrender, forfeit or other determination of the lease, the lessee or an associate of the lessee has occupied the leased property, or substantially the same property, with the agreement (express or implied) of the lessor (other than as a result of the sale of the property to the lessee or associate).

(3) An application for a refund under this section must be accompanied by a declaration by the applicant stating that neither the lessee nor any associate of the lessee has occupied or will occupy the leased property, or substantially the same property, after the surrender, forfeit or other determination of the lease (other than as a result of the sale of the property to the lessee or associate).

(4) A person must not knowingly make a false declaration under sub-section (3).

Penalty: 300 penalty units in the case of a body corporate;

60 penalty units in any other case.".

(2) In section 83A of the Stamps Act 1958, after sub-section (6) insert—

"(6A) Sub-sections (4), (5) and (6) do not apply on or after 26 April 2001.

See: Act No. 6375. Reprint No. 16 as at 3 July 2000 and amending Act Nos 103/1993 (as amended by No. 119/1994), 34/1999, 79/2000, 10/2001 and 11/2001. LawToday: www.dms. dpc.vic. gov.au

s. 15

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

19

(6B) If, on or after 26 April 2001 but before the day on which the State Taxation Acts (Taxation Reform Implementation) Act 2001 received the Royal Assent, the Comptroller made a re-estimate under sub-section (5)—

(a) if additional stamp duty was paid under sub-section (5)(a) as a result of the re-estimate, the Comptroller must refund an amount equal to the additional duty paid;

(b) if the Comptroller refunded an amount under sub-section (5)(b) as a result of the re-estimate, that amount must be repaid to the Comptroller and the Comptroller may recover that amount from the person to whom it was paid as a debt in a court of competent jurisdiction.".

(3) In the Third Schedule to the Stamps Act 1958, in Heading VIII, after clause (4) insert— "Duty is not payable under this Heading on a lease,

assignment of lease or agreement for a lease that is made on or after 26 April 2001.".

═══════════════

s. 15

Act No. 48/2001

State Taxation Acts (Taxation Reform Implementation) Act 2001

20

ENDNOTES

† Minister's second reading speech—

Legislative Assembly: 17 May 2001

Legislative Council: 12 June 2001

The long title for the Bill for this Act was "to amend the Casino Control Act 1991, the Duties Act 2000, the Gaming Machine Control Act 1991, the Land Tax Act 1958, the Pay-roll Tax Act 1971 and the Stamps Act 1958 to implement the reform of State taxes and for other purposes."

Endnotes

![THE COMPANIES ACT 2001 Act 15/2001 - MIPA...THE COMPANIES ACT 2001 Act 15/2001 Proclaimed by [Proclamation No. 21 of 2001] w.e.f. 1st December 2001 SAVINGS 1. Please refer to schedule](https://img.pdfslide.net/doc/110x75/5f062c7a7e708231d416a9b3/the-companies-act-2001-act-152001-mipa-the-companies-act-2001-act-152001.jpg)