Embed Size (px)

Citation preview

STATEMENT OF ACCOUNTS FOR THE

YEAR ENDED 31 MARCH 2012

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

CONTENTS

P A G E

Explanatory Foreword 1 Council Approval 1 5 Statement of Responsibilities for the Statement of Accounts 1 6 Movement in Reserves Statement 1 7 Comprehensive Income and Expenditure Statement 2 0 Balance Sheet 2 1 Cash Flow Statement 2 3 Notes to the Accounts 2 4 Housing Revenue Account Income and Expenditure Statement 1 0 8 Movement on the Housing Revenue Account Statement 1 1 0 Notes to the Housing Revenue Account 1 1 1 Collection Fund 1 2 0 Notes to the Collection Fund 1 2 1 Independent Audit Opinion and Certificate 1 2 4 Glossary 1 2 7

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

E X P L A N A T O R Y F O R E W O R D The Statement of Accounts The purpose of the Accounts, which follow, is to give electors, those subject to locally levied taxes and charges, Members of the Council, employees and other interested parties clear information about the Council’s finances. The Accounts show the financial performance for 2011/12 and the financial position at 31 March 2012. The Accounts present expenditure and income incurred by the Council in the financial year 2011/12 and highlight changes in the financial position of the Council over the course of the year. The financial statements have been prepared in accordance with the Code of Practice on Local Authority Accounting in the UK (the code) published by the Chartered Institute of Public Finance and Accountancy (CIPFA). The Statement of Accounts consist of various sections and statements, which are briefly explained below: An Explanatory Foreword – this provides information on the format of this Statement of Accounts as well as a review of the financial position of the Council for the financial year. The Statement of Responsibilities – this details the responsibilities of the Council and the S151 Officer concerning the Council’s financial affairs and the actual Statement of Accounts. The Audit Opinion and Certificate – this is provided by the Audit Commission following the completion of the annual audit. The Accounting Policies – this statement explains the basis for the recognition, measurement and disclosure of transactions and other events in the accounts. The Core Financial Statements, comprising:

• The Movements in Reserves Statement – this statement shows the movement in year on the different reserves held by the Council, analysed into ‘usable’ (i.e. those that can be applied to fund expenditure or reduce local taxation) and other unusable reserves.

• The Comprehensive Income and Expenditure Statement – this statement

shows the accounting cost in the year of providing services in accordance with generally accepted accounting practices, rather than the amount funded from taxation. The Council raises taxation to cover the cost of expenditure in accordance with regulations; this may be different from the accounting cost. The taxation position is shown in the Movement in Reserves Statement.

• The Balance Sheet – the Balance Sheet shows the value as at the Balance

Sheet date of the assets and liabilities recognised by the Council. The net assets of the Council are (assets less liabilities) matched by the reserves held by the Council.

1

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

• The Cash Flow Statement – this statement shows the changes in cash and

cash equivalents of the Council during the year. It shows how the Council generates and uses cash and cash equivalents by classifying cash flows as operating, investing and financing activities.

The Supplementary Statements, comprising:

• The Housing Revenue Income and Expenditure Statement - this statement shows the economic cost in the year of providing housing services in accordance with generally accepted accounting practices, rather than the amount to be funded from rents and government grants. The Council charges rents to cover expenditure in accordance with regulations, this may be different from the accounting cost. The increase or decrease in the year, on the basis of which rents are raised, is shown in the Movement on the HRA Statement

• The Movement on the HRA Statement – this statement takes the outturn on the

HRA Income and Expenditure Statement and reconciles it to the surplus or deficit for the year on the HRA Balance, calculated in accordance with the requirements of the Local Government and Housing Act 1989.

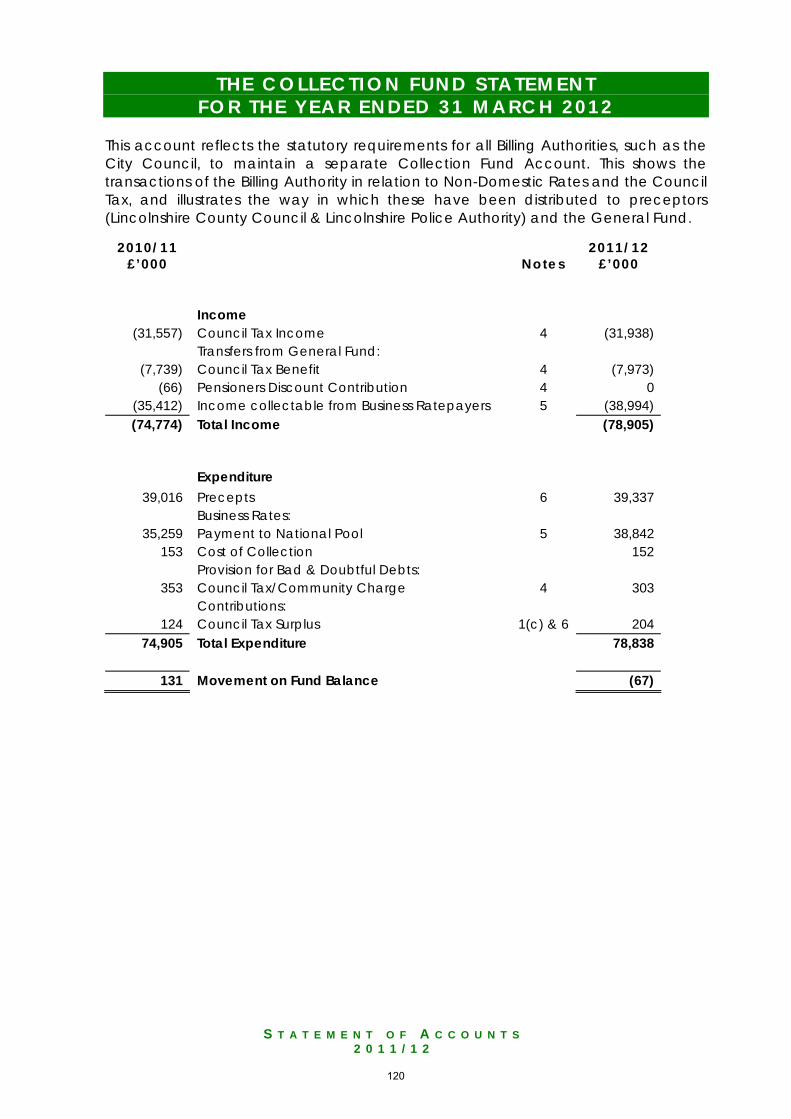

• The Collection Fund Statement- this statement is an agent’s statement that

reflects the statutory obligation for billing authorities (such as the City of Lincoln Council) to maintain a separate Collection Fund. The statement shows the transactions of the Council in relation to the collection from council tax and business rate payers and distribution to Lincolnshire County Council, Lincolnshire Police Authority and Government of council tax and national non-domestic rates.

The Notes to the Financial Statements – these provide supporting and explanatory information on the Financial Statements. Financial Summary 2011/12 2011/12 has been another challenging year financially as the economic climate remained largely unchanged from the previous and so continued to present difficult circumstances with regards to the financial management of the Council. Despite some initial encouraging signs in the UK economy during 2011, the overall recovery remains weak and continues to be affected by the financial difficulties being experienced by the Eurozone countries. The threat of a dip back into recession remains during 2012 and there have been no significant improvements to the performance of the financial and property markets. Hence, the most challenging areas continued to be treasury management, asset values and the use of, and demand for, Council services, coupled with a real terms decrease in Central Government funding. The continued difficult condition in the economy gave rise to a number of specific issues for the Council, as follows;

• The Bank of England’s policy of continuing to maintain low interest rates to combat the liquidity crisis has had a significant effect on the

2

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Council’s income from investments. In addition, the ongoing financial instability in the Eurozone has meant that the Council has limited the placing of investments to mainly short term deposits in 2011/12 to reduce risk but thereby reducing investment returns.

• Investment counterparty risk remains high. As a result there continues to be a

very limited range of counterparties available to the Council for investment purposes.

• Although the property market has continued to show poor performance in

2011/12, the overall market value of the Council’s property holdings increased by £1.76m. This was mainly due to revaluations of previously unrecognised land holdings which have been brought into use, either for rental or for development purposes. There were also net downwards revaluations and impairments of £1.657m in 2011/12 charged to the Comprehensive Income and Expenditure Statement.

• The poor performance of the property market has also reduced the Council’s

ability to generate capital receipts affecting the affordability of the General Fund Investment Programme with the financing of schemes being heavily reliant on the sales of Council assets.

• Demand for services such as Council tax and Housing Benefits has continued

to increase, with currently 12,171 household (28%) in the City in receipt of Housing and/or Council Tax Benefit. Services including Council Housing and Customer Services are also continuing to experience high levels of demand.

• Income has continued to remain at historically low levels in a number of areas

e.g. planning regulation fees, local land charges and car parking. In spite of the challenges the Council has faced it has maintained sound financial management and has delivered spending within budget in both the General Fund and the Housing Revenue Account, whilst over achieving its target for the delivery of revenue savings; and has delivered over £35.9m of capital investment, of which £24.931m relates a payment to Central Government to buy out of the Housing Revenue Account subsidy system and to become a ‘self financed’ Housing Authority from 1 April 2012. Revenue Income and Expenditure General Fund The General Fund account covers all net spending by the Council on services other than those accounted for in the Housing Revenue Account. General Fund services are partly paid for by Government Grants and contributions from Business Rates, with the balance being funded from Council Tax.

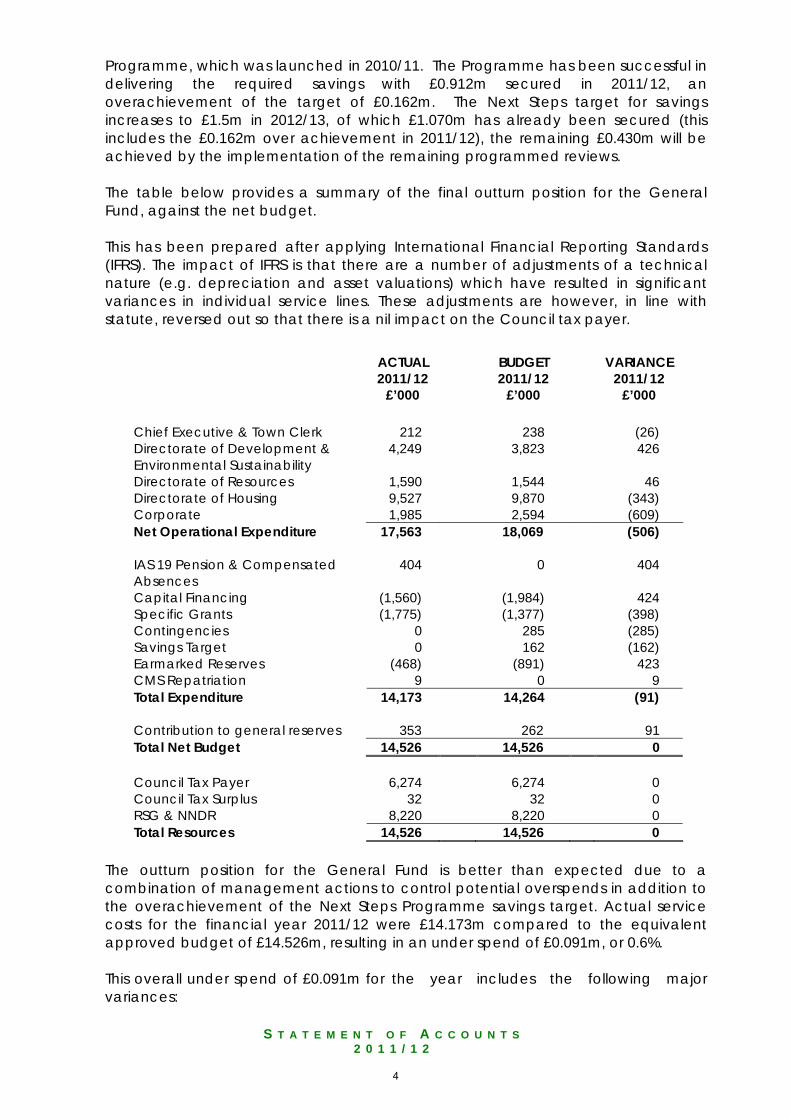

For 2011/12, the approved net expenditure budget for General Fund services was £14.264m. After allowing for planned contributions of £0.262m to non-earmarked general reserves the total Net General Fund Budget for 2011/12 was £14.526m. The Net General Fund Budget of £14.526m assumed the achievement of a £0.750m savings target to be delivered as part of the Council’s Next Steps

3

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Programme, which was launched in 2010/11. The Programme has been successful in delivering the required savings with £0.912m secured in 2011/12, an overachievement of the target of £0.162m. The Next Steps target for savings increases to £1.5m in 2012/13, of which £1.070m has already been secured (this includes the £0.162m over achievement in 2011/12), the remaining £0.430m will be achieved by the implementation of the remaining programmed reviews. The table below provides a summary of the final outturn position for the General Fund, against the net budget. This has been prepared after applying International Financial Reporting Standards (IFRS). The impact of IFRS is that there are a number of adjustments of a technical nature (e.g. depreciation and asset valuations) which have resulted in significant variances in individual service lines. These adjustments are however, in line with statute, reversed out so that there is a nil impact on the Council tax payer.

ACTUAL 2011/12

£’000

BUDGET 2011/12

£’000

VARIANCE 2011/12

£’000 Chief Executive & Town Clerk 212 238 (26) Directorate of Development & Environmental Sustainability

4,249 3,823 426

Directorate of Resources 1,590 1,544 46 Directorate of Housing 9,527 9,870 (343) Corporate 1,985 2,594 (609) Net Operational Expenditure 17,563 18,069 (506) IAS 19 Pension & Compensated Absences

404 0 404

Capital Financing (1,560) (1,984) 424 Specific Grants (1,775) (1,377) (398) Contingencies 0 285 (285) Savings Target 0 162 (162) Earmarked Reserves (468) (891) 423 CMS Repatriation 9 0 9 Total Expenditure 14,173 14,264 (91) Contribution to general reserves 353 262 91 Total Net Budget 14,526 14,526 0 Council Tax Payer 6,274 6,274 0 Council Tax Surplus 32 32 0 RSG & NNDR 8,220 8,220 0 Total Resources 14,526 14,526 0

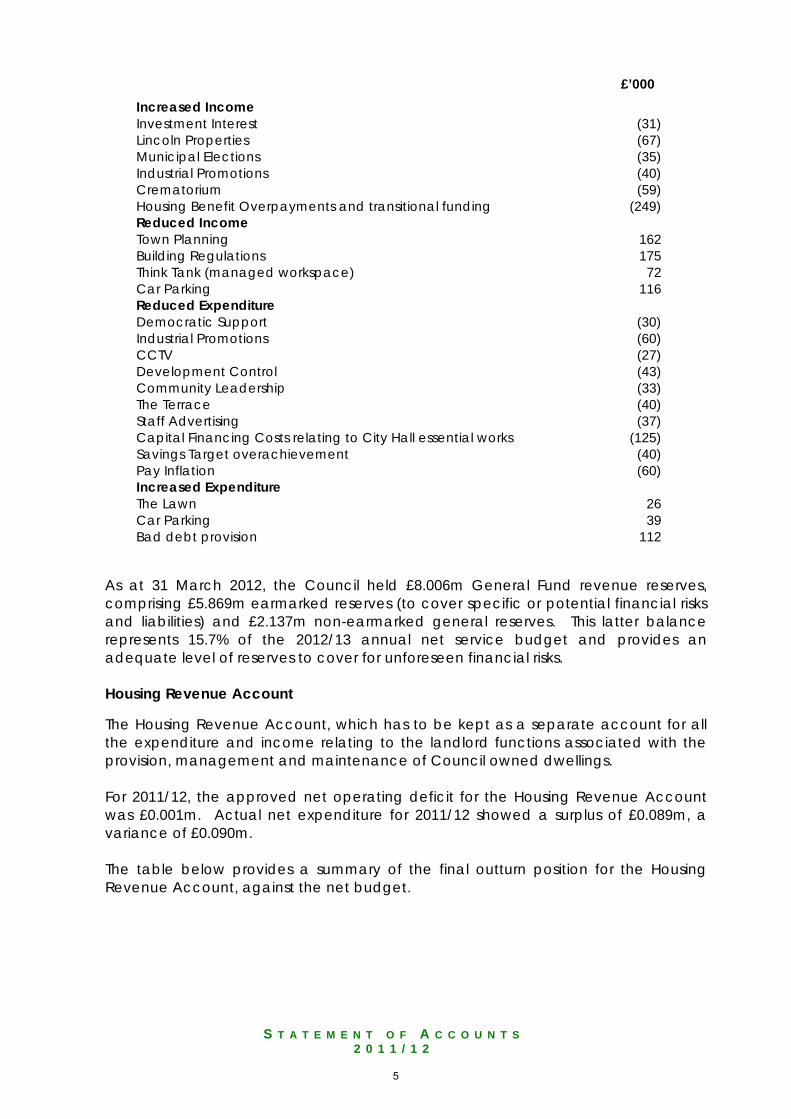

The outturn position for the General Fund is better than expected due to a combination of management actions to control potential overspends in addition to the overachievement of the Next Steps Programme savings target. Actual service costs for the financial year 2011/12 were £14.173m compared to the equivalent approved budget of £14.526m, resulting in an under spend of £0.091m, or 0.6%. This overall under spend of £0.091m for the year includes the following major variances:

4

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

£’000 Increased Income Investment Interest (31) Lincoln Properties (67) Municipal Elections (35) Industrial Promotions (40) Crematorium (59) Housing Benefit Overpayments and transitional funding (249) Reduced Income Town Planning 162 Building Regulations 175 Think Tank (managed workspace) 72 Car Parking 116 Reduced Expenditure Democratic Support (30) Industrial Promotions (60) CCTV (27) Development Control (43) Community Leadership (33) The Terrace (40) Staff Advertising (37) Capital Financing Costs relating to City Hall essential works (125) Savings Target overachievement (40) Pay Inflation (60) Increased Expenditure The Lawn 26 Car Parking 39 Bad debt provision 112

As at 31 March 2012, the Council held £8.006m General Fund revenue reserves, comprising £5.869m earmarked reserves (to cover specific or potential financial risks and liabilities) and £2.137m non-earmarked general reserves. This latter balance represents 15.7% of the 2012/13 annual net service budget and provides an adequate level of reserves to cover for unforeseen financial risks. Housing Revenue Account

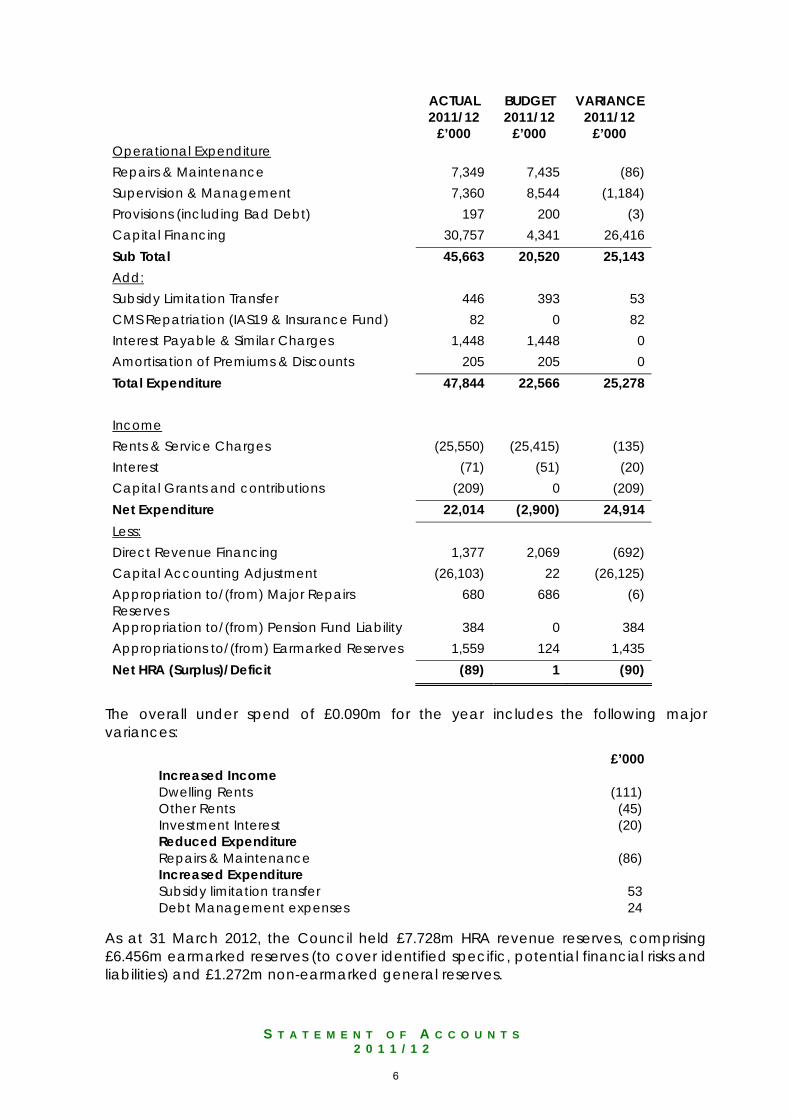

The Housing Revenue Account, which has to be kept as a separate account for all the expenditure and income relating to the landlord functions associated with the provision, management and maintenance of Council owned dwellings. For 2011/12, the approved net operating deficit for the Housing Revenue Account was £0.001m. Actual net expenditure for 2011/12 showed a surplus of £0.089m, a variance of £0.090m. The table below provides a summary of the final outturn position for the Housing Revenue Account, against the net budget.

5

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

ACTUAL

2011/12 £’000

BUDGET 2011/12

£’000

VARIANCE 2011/12

£’000 Operational Expenditure Repairs & Maintenance 7,349 7,435 (86) Supervision & Management 7,360 8,544 (1,184) Provisions (including Bad Debt) 197 200 (3) Capital Financing 30,757 4,341 26,416 Sub Total 45,663 20,520 25,143 Add: Subsidy Limitation Transfer 446 393 53 CMS Repatriation (IAS19 & Insurance Fund) 82 0 82 Interest Payable & Similar Charges 1,448 1,448 0 Amortisation of Premiums & Discounts 205 205 0 Total Expenditure 47,844 22,566 25,278 Income Rents & Service Charges (25,550) (25,415) (135) Interest (71) (51) (20) Capital Grants and contributions (209) 0 (209) Net Expenditure 22,014 (2,900) 24,914 Less: Direct Revenue Financing 1,377 2,069 (692) Capital Accounting Adjustment (26,103) 22 (26,125) Appropriation to/(from) Major Repairs Reserves

680 686 (6)

Appropriation to/(from) Pension Fund Liability 384 0 384 Appropriations to/(from) Earmarked Reserves 1,559 124 1,435 Net HRA (Surplus)/Deficit (89) 1 (90)

The overall under spend of £0.090m for the year includes the following major variances:

£’000 Increased Income Dwelling Rents (111) Other Rents (45) Investment Interest (20) Reduced Expenditure Repairs & Maintenance (86) Increased Expenditure Subsidy limitation transfer 53 Debt Management expenses 24

As at 31 March 2012, the Council held £7.728m HRA revenue reserves, comprising £6.456m earmarked reserves (to cover identified specific, potential financial risks and liabilities) and £1.272m non-earmarked general reserves.

6

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

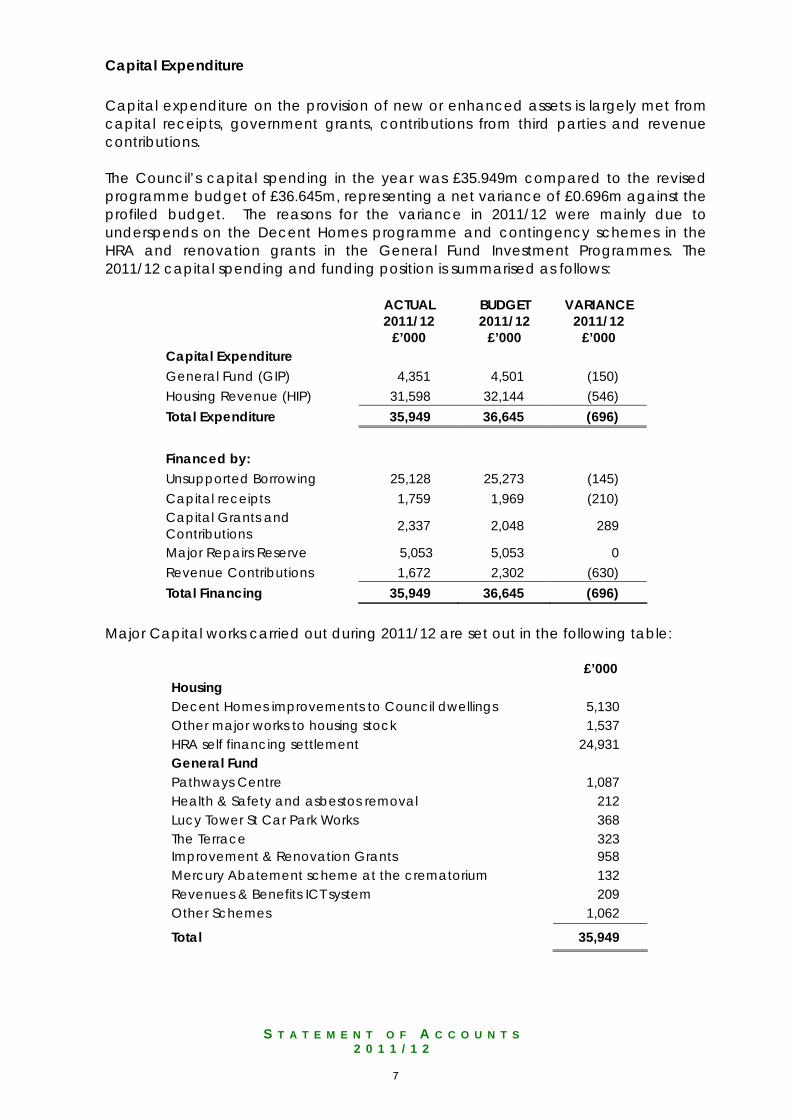

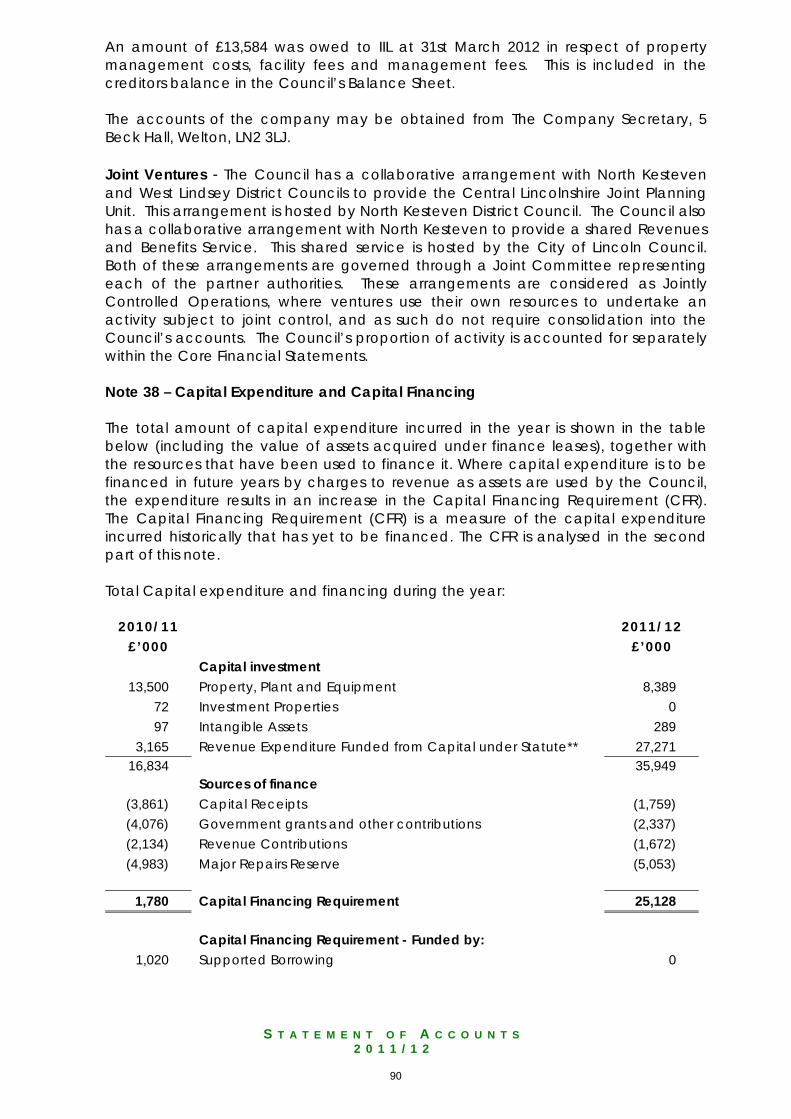

Capital Expenditure Capital expenditure on the provision of new or enhanced assets is largely met from capital receipts, government grants, contributions from third parties and revenue contributions. The Council’s capital spending in the year was £35.949m compared to the revised programme budget of £36.645m, representing a net variance of £0.696m against the profiled budget. The reasons for the variance in 2011/12 were mainly due to underspends on the Decent Homes programme and contingency schemes in the HRA and renovation grants in the General Fund Investment Programmes. The 2011/12 capital spending and funding position is summarised as follows:

ACTUAL 2011/12

£’000

BUDGET 2011/12

£’000

VARIANCE 2011/12

£’000 Capital Expenditure General Fund (GIP) 4,351 4,501 (150) Housing Revenue (HIP) 31,598 32,144 (546) Total Expenditure 35,949 36,645 (696) Financed by: Unsupported Borrowing 25,128 25,273 (145) Capital receipts 1,759 1,969 (210) Capital Grants and Contributions 2,337 2,048 289

Major Repairs Reserve 5,053 5,053 0 Revenue Contributions 1,672 2,302 (630) Total Financing 35,949 36,645 (696)

Major Capital works carried out during 2011/12 are set out in the following table:

£’000 Housing Decent Homes improvements to Council dwellings 5,130 Other major works to housing stock 1,537 HRA self financing settlement 24,931 General Fund Pathways Centre 1,087 Health & Safety and asbestos removal 212 Lucy Tower St Car Park Works 368 The Terrace 323 Improvement & Renovation Grants 958 Mercury Abatement scheme at the crematorium 132 Revenues & Benefits ICT system 209 Other Schemes 1,062

Total 35,949

7

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

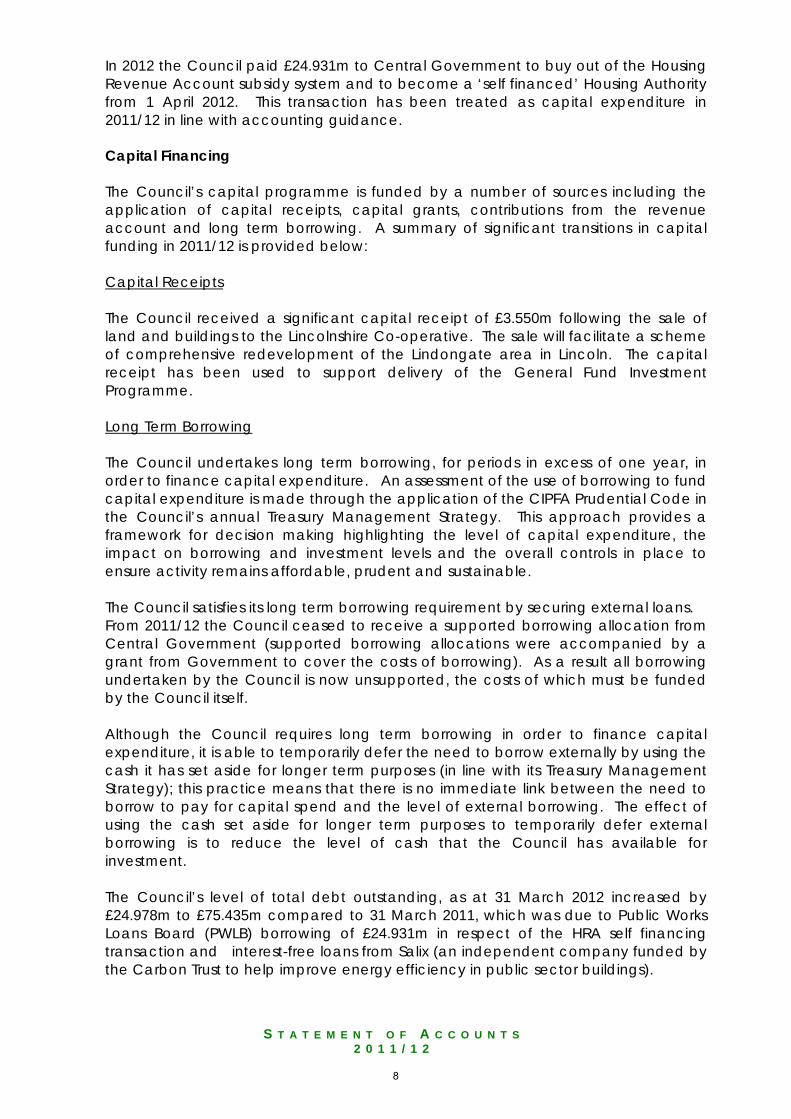

In 2012 the Council paid £24.931m to Central Government to buy out of the Housing Revenue Account subsidy system and to become a ‘self financed’ Housing Authority from 1 April 2012. This transaction has been treated as capital expenditure in 2011/12 in line with accounting guidance. Capital Financing The Council’s capital programme is funded by a number of sources including the application of capital receipts, capital grants, contributions from the revenue account and long term borrowing. A summary of significant transitions in capital funding in 2011/12 is provided below: Capital Receipts The Council received a significant capital receipt of £3.550m following the sale of land and buildings to the Lincolnshire Co-operative. The sale will facilitate a scheme of comprehensive redevelopment of the Lindongate area in Lincoln. The capital receipt has been used to support delivery of the General Fund Investment Programme. Long Term Borrowing

The Council undertakes long term borrowing, for periods in excess of one year, in order to finance capital expenditure. An assessment of the use of borrowing to fund capital expenditure is made through the application of the CIPFA Prudential Code in the Council’s annual Treasury Management Strategy. This approach provides a framework for decision making highlighting the level of capital expenditure, the impact on borrowing and investment levels and the overall controls in place to ensure activity remains affordable, prudent and sustainable. The Council satisfies its long term borrowing requirement by securing external loans. From 2011/12 the Council ceased to receive a supported borrowing allocation from Central Government (supported borrowing allocations were accompanied by a grant from Government to cover the costs of borrowing). As a result all borrowing undertaken by the Council is now unsupported, the costs of which must be funded by the Council itself. Although the Council requires long term borrowing in order to finance capital expenditure, it is able to temporarily defer the need to borrow externally by using the cash it has set aside for longer term purposes (in line with its Treasury Management Strategy); this practice means that there is no immediate link between the need to borrow to pay for capital spend and the level of external borrowing. The effect of using the cash set aside for longer term purposes to temporarily defer external borrowing is to reduce the level of cash that the Council has available for investment. The Council’s level of total debt outstanding, as at 31 March 2012 increased by £24.978m to £75.435m compared to 31 March 2011, which was due to Public Works Loans Board (PWLB) borrowing of £24.931m in respect of the HRA self financing transaction and interest-free loans from Salix (an independent company funded by the Carbon Trust to help improve energy efficiency in public sector buildings).

8

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

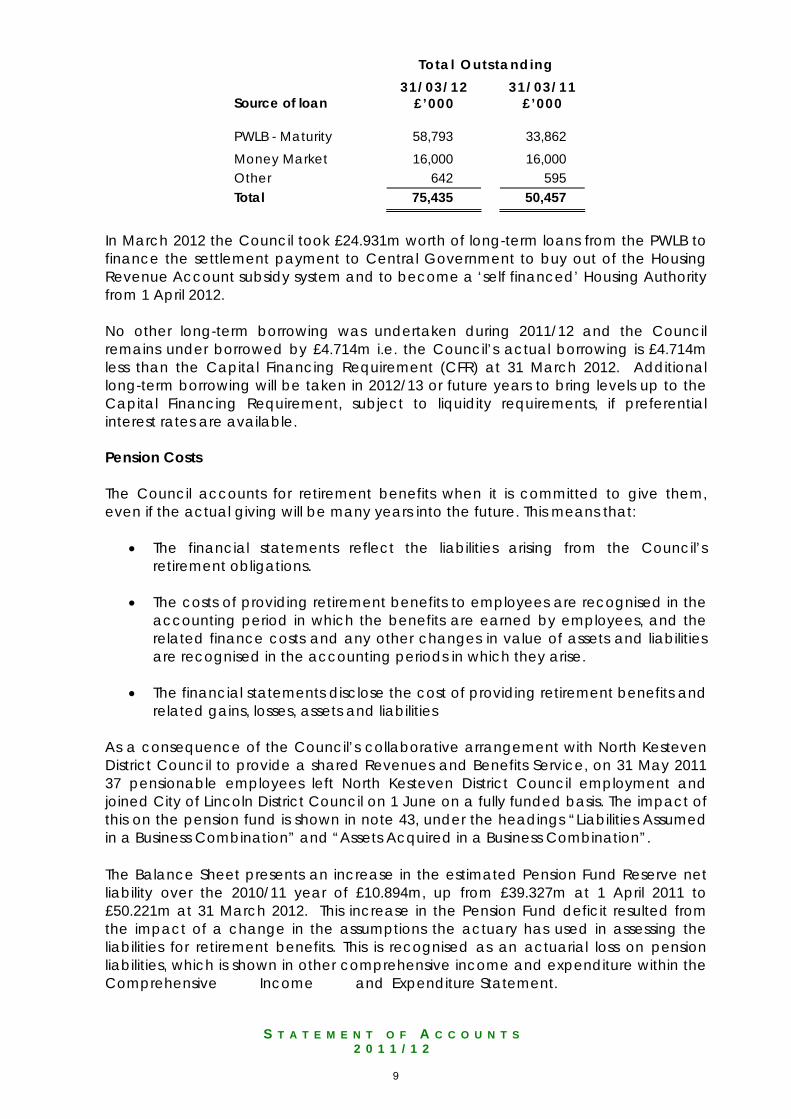

Total Outstanding

Source of loan 31/03/12

£’000

31/03/11 £’000

PWLB - Maturity 58,793 33,862 Money Market 16,000 16,000 Other 642 595 Total 75,435 50,457

In March 2012 the Council took £24.931m worth of long-term loans from the PWLB to finance the settlement payment to Central Government to buy out of the Housing Revenue Account subsidy system and to become a ‘self financed’ Housing Authority from 1 April 2012. No other long-term borrowing was undertaken during 2011/12 and the Council remains under borrowed by £4.714m i.e. the Council’s actual borrowing is £4.714m less than the Capital Financing Requirement (CFR) at 31 March 2012. Additional long-term borrowing will be taken in 2012/13 or future years to bring levels up to the Capital Financing Requirement, subject to liquidity requirements, if preferential interest rates are available. Pension Costs The Council accounts for retirement benefits when it is committed to give them, even if the actual giving will be many years into the future. This means that:

• The financial statements reflect the liabilities arising from the Council’s retirement obligations.

• The costs of providing retirement benefits to employees are recognised in the

accounting period in which the benefits are earned by employees, and the related finance costs and any other changes in value of assets and liabilities are recognised in the accounting periods in which they arise.

• The financial statements disclose the cost of providing retirement benefits and

related gains, losses, assets and liabilities As a consequence of the Council’s collaborative arrangement with North Kesteven District Council to provide a shared Revenues and Benefits Service, on 31 May 2011 37 pensionable employees left North Kesteven District Council employment and joined City of Lincoln District Council on 1 June on a fully funded basis. The impact of this on the pension fund is shown in note 43, under the headings “Liabilities Assumed in a Business Combination” and “Assets Acquired in a Business Combination”. The Balance Sheet presents an increase in the estimated Pension Fund Reserve net liability over the 2010/11 year of £10.894m, up from £39.327m at 1 April 2011 to £50.221m at 31 March 2012. This increase in the Pension Fund deficit resulted from the impact of a change in the assumptions the actuary has used in assessing the liabilities for retirement benefits. This is recognised as an actuarial loss on pension liabilities, which is shown in other comprehensive income and expenditure within the Comprehensive Income and Expenditure Statement.

9

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

The statutory arrangements for funding the remaining liability of £50.221m means that this deficit will be made good by the increased level of annual employer contributions payable to the Pension Fund over the remaining estimated average working life of our employees in the Pension Scheme. The latest triennial review of the Pension Fund was completed as at 31 March 2010 and although the results identified that there had been a deterioration in the funding position from a 83% funding level to 72%, this review did not indicate that any immediate changes in the annual contributions were required. The next triennial review is due as at 31 March 2013, when a stabilisation approach will be implemented so that in any three year period rates will only be increased or decreased by a maximum of 1%, thus avoiding any unaffordable increases in employer contributions. Any changes identified as a result of the next triennial review will be effective from 1 April 2014. Future Plans General Fund The Council, along with all other public sector bodies, will continue to face an unprecedented, and extremely challenging short and medium term financial environment as it responds to; the Coalition Government’s Spending Review, announced in October 2010; existing financial pressures, principally the current economic climate; and the publication of a large number of Government White Papers, consultation documents and statutory instruments including:

• The Local Government Resource Review proposals for business rate retention by Councils.

• Council Tax Benefit Reform containing proposals for Councils to take

responsibility for their own schemes. • Proposals to radically overhaul national welfare services, in particular to take

housing benefit services away from local government.

• The Localism Act and its implications for governance, housing and planning arrangements within local government.

• The Open Public Services White Paper that considers, amongst other ideas,

the concept that public services should not necessarily be delivered by the public sector.

As a result of significant grant reductions imposed by the Coalition Government (the Council’s grant funding was reduced by 24.4% over the period 2011/12 to 2012/13) the Council faces a significant challenge if it is to continue to deliver services to the public and remain within a severely reduced funding envelope. The Council’s Medium Term Financial Strategy for 2012-17 is based on a reduction of annual revenue spending of £1.500m in 2012/13, increasing annually to £2.750m by 2015/16. This challenge is not new to the Council and it has in recent years already become accustomed to working within tight budgets and has demonstrated excellent progress in the delivery of its Service Review and Next Steps Programmes, already securing £3.3m annual savings to the revenue budget. The Council’s Next Steps Programme continues to be the most fundamental

10

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

element of the Council’s response to the financial and policy environment. The programme brings together into a co-ordinated programme a single unified approach focusing on four core strands:

• Lean Systems Interventions • Collaborative Working • Income Generation • Cost Reductions

It will remain important to maintain the pace and extent of changes that can be delivered from the programme as the Council moves into the completion of phase one and delivery of phase two. The scale of external changes facing the Council means that further radical change will be required for the foreseeable future. In response the Council will seek to continue to make changes across the whole range of activity including how it delivers its services, the organisational structures of these services, relationships with key partners and its human resources policies. It will aim to ensure that the services the Council provides are ‘lean and fit’, achieving the standards agreed with customers and delivering the best possible value for money to the taxpayer. Housing Revenue Account (HRA) With effect from 1 April 2012 the Council’s Housing Revenue Account (HRA) is self financing following its ‘buy out’ of the former housing subsidy system. Under the old system the Council had been paying over £2m per year to the Government in negative subsidy, to be redistributed nationally. The new self financing regime will give the Council as landlord the resources, incentives and flexibility needed to manage its housing stock for the long-term and to drive up quality and efficiency. The regime allows greater certainty about future income as the Council will no longer be subject to annual funding decisions by Central Government. This will support the development of long-term plans and reinvestment of income in the Council’s housing stock. The Council will have greater flexibility to manage its stock in the way that best suits local need and will provide more opportunity for tenants to have a real say in setting priorities looking to the longer term. However, self financing also transfers significant risks from Central Government to local authorities. The Council will bear the responsibility for the long term security and viability of council housing in Lincoln. The Council will have to fund all activity related to council housing from the income generated from rents through long term business planning. The Council will be more exposed to changes in interest rates, high inflation and the financial impact of falling stock numbers and it will also need to factor in the impact of changes in government policy e.g. the impacts of the forthcoming welfare reform on income recovery. In order to optimise its resources for council housing over the short, medium and long term the Council has developed a 30 year HRA business plan. A robust business minded approach is being taken to ensure that the Council is in a position to optimise the benefits of its new responsibilities and to minimise the impact of the additional risks that self financing brings. Ultimately the business plan aims to ensure that the Council is in a position to continue to enhance the housing stock,

11

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

and provide quality, affordable services to tenants. Capital Expenditure The Council’s capital programmes will deliver projects to the value of £75.7m over the next five years, with £17.7m estimated to be spent in 2012/13. This includes significant investment and improvement to Council dwellings, and Council buildings, housing assistance grant aid, a mortgage indemnity scheme to support first time buyers and the provision of a new burial site. Capital resources for the next five years include capital receipts, government grants, contributions from third parties and revenue contributions. The General Fund element of the programme is heavily reliant upon capital receipts with a target of £10.375m over the period, 74% of the overall programme. The continued poor performance of property markets increases the risk to the Council of not generating the required level of capital receipts. In response to this the Council’s Asset Management Plan includes a major review programme of assets to identify potential disposals. Additionally, ongoing capital commitments will be reviewed regularly to ensure that the capital programme remains affordable. This will require strong integration of the Council’s Capital Strategy, Asset Management Plan, Treasury Management Strategy and balancing the impact of any changes on the revenue position. The Housing element of the capital programme is predominantly reliant upon revenue contributions from the Housing Revenue Account (HRA). This places enormous pressure on the revenue budget and is a fundamental consideration in the development of the 30 year HRA business plan. In the first 10 years of the Housing Business Plan the majority of revenue resources will be fully committed to support the capital investment required in the existing stock. Given the level of revenue support required, and increased dependency on this as the primary source of capital funding, it is recognised that it is critical that there is robust budget management of the HRA and that opportunities to achieve efficiencies and maintain/maximise income streams are actively pursued. Summary Despite the challenging financial environment the Council has continued to maintain sound, prudent financial management and remains in a good financial position, balances remain at prudent levels and the necessary provisions have been set aside for future liabilities or losses. However due to the level of uncertainty and risks facing the Council, particularly the significant reductions in Central Government funding, it needs to continue to respond positively to these challenges and continue to manage its affairs in such a way as to ensure the economic, efficient and effective use of its resources, and to safeguard its assets for the future. The Council is committed to its vision to improve the quality of life for its residents and that will be paramount to every decision it makes.

Group Accounts The increasing scope and scale of local authorities moving away from traditional ways of providing services makes it increasingly difficult for the Council’s own

12

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

financial statements to present fairly all the aspects of control over service provision and accountability for all resources and exposure to risks that the Council has taken on. A consolidated set of group accounts can make a vital contribution towards giving users a full picture of the Council’s sphere of control and influence. The Council has identified that the interest that it holds in Investors in Lincoln Ltd meets the test of ‘joint control’ and as such should be accounted for as a Joint Venture. However, after assessing the criteria for materiality, has concluded that the amounts are not material to the fair presentation of the financial position and transactions of the Council and to the understanding of the Statement of Accounts by a reader. Investors in Lincoln Ltd has therefore not been consolidated into the Council’s accounts. Details of transactions and relevant balances with Investors in Lincoln Ltd can be found in note 37 (related parties). The Council has a collaborative arrangement with North Kesteven and West Lindsey District Councils to provide the Central Lincolnshire Joint Planning Unit. This arrangement is hosted by North Kesteven District Council. The Council also has a collaborative arrangement with North Kesteven to provide a shared Revenues and Benefits Service. This shared service is hosted by the City of Lincoln Council. Both of these arrangements are governed through a Joint Committee representing each of the partner authorities. These arrangements are considered as Jointly Controlled Operations, where ventures use their own resources to undertake an activity subject to joint control, and as such do not require consolidation into the Council’s accounts. The Council’s proportion of activity is accounted for separately within the Core Financial Statements.

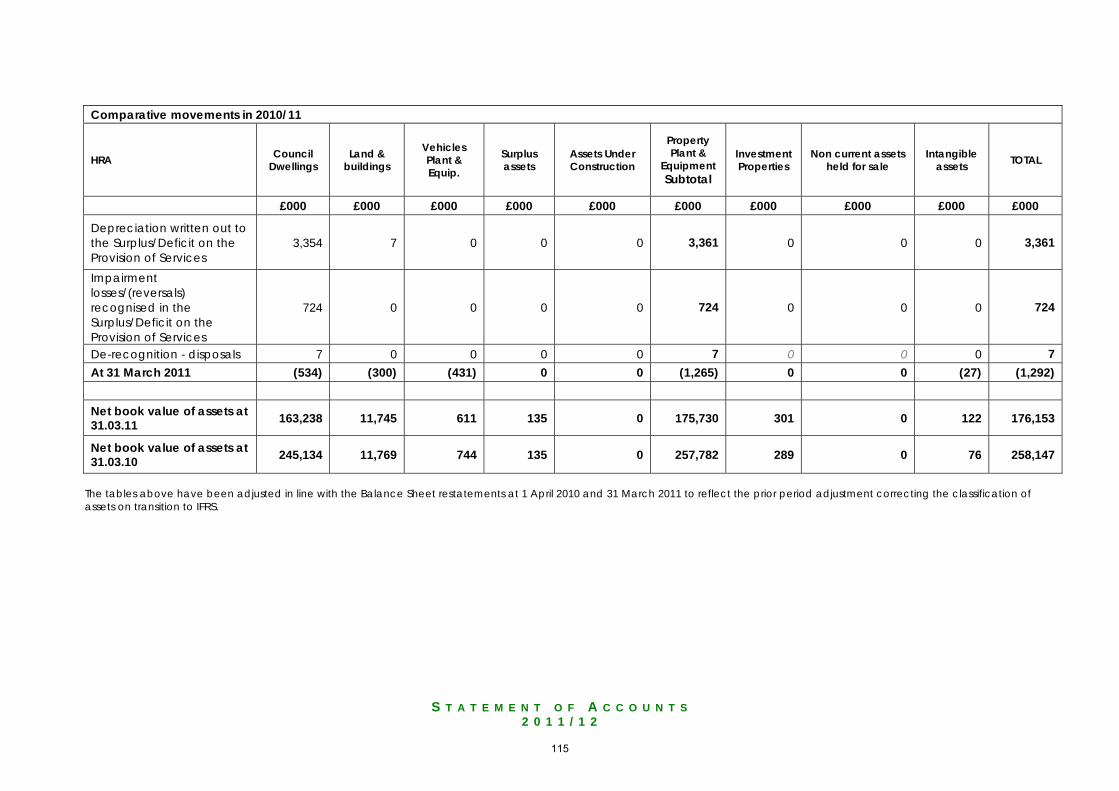

Changes in Accounting Policies In 2011/12 the code introduced a change to the accounting treatment for heritage assets held by the Council. Heritage assets are now required to be carried in the Council’s Balance Sheet at valuation. Previously these assets had been recorded as community assets in property, plant and equipment at historic (usually de-minimis) cost . The net effect of the change in accounting policy in 2011/12 has been that heritage assets are recognised at £4.667m in the Balance Sheet resulting in an increase to the Revaluation Reserve of £4.652m. These assets had not been previously recognised in the Balance Sheet. Further details on the effect of the new accounting policy can be found in note 48 (Heritage Assets: Change in Accounting Policy Required by the code). Prior Period Adjustment The financial statements for the previous year were the first to be prepared under International Financial Reporting Standards (IFRS). This included classifying all property assets held by the Council as either Investment Properties (IP) or Property, Plant & Equipment (PPE), according to strict criteria set out in the code. In preparing the financial statements for 2011/12, a review of this classification was undertaken in the light of additional information available. The result of this review is that property and land to the value of £13.797m, which was classified as

13

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

investment property in the previous year’s financial statements, do not fully meet the criteria and should therefore, have been classified under property, plant and equipment. A prior period adjustment has been made to the financial statements to correct the original misclassification. The Balance Sheet at 1 April 2010 and 31 March 2011 has been restated to reflect the required changes. Further Information Further information about the accounts is available on request from the Directorate of Resources, City Hall, Beaumont Fee Lincoln LN1 1DB. In addition, local electors have a statutory right to inspect the accounts before the audit is completed. The availability of the accounts for inspection is advertised in the local press and on the Council’s website.

14

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

C O U N C I L A P P R O V A L

The Statement of Accounts for the year 1 April 2011 to 31 March 2012 has been prepared and I confirm that these Accounts were approved by the City of Lincoln Council, at the meeting held on 25 September 2012. Karen Lee Councillor Karen Lee Chairman of Council Date: 25 September 2012

15

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

E M E N T O F R E S P O N S I B I L I T I E S F O R T H E S T A T E M E N T O F A C C O U N T S

The Authority’s Responsibilities

The Authority is required:

• to make arrangements for the proper administration of its financial affairs and to ensure that one of its officers has the responsibility for the administration of those affairs. In this Authority, that officer is the Director of Resources;

• to manage its affairs to ensure economic, efficient and effective use of resources and safeguard its assets;

• to approve the Statement of Accounts. The Director of Resources Responsibilities The Director of Resources is responsible for the preparation of the Authority’s Statement of Accounts in accordance with proper practices as set out in the Code of Practice on Local Authority Accounting in the UK (‘the code ’). In preparing this Statement of Accounts, the Director of Resources has:

• selected suitable accounting policies and then applied them consistently;

• made judgements and estimates that were reasonable and prudent;

• complied with the Code of Practice. The Director of Resources has also:

• kept proper accounting records which were up to date;

• taken reasonable steps for the prevention and detection of fraud and other irregularities.

The Accounts present a true and fair view of the financial position of the Authority at 31 March 2012 and its income and expenditure for the year ended on that date. ANGELA ANDREWS A ANDREWS, CPFA, Director of Resources DATE: 25 September 2012

16

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

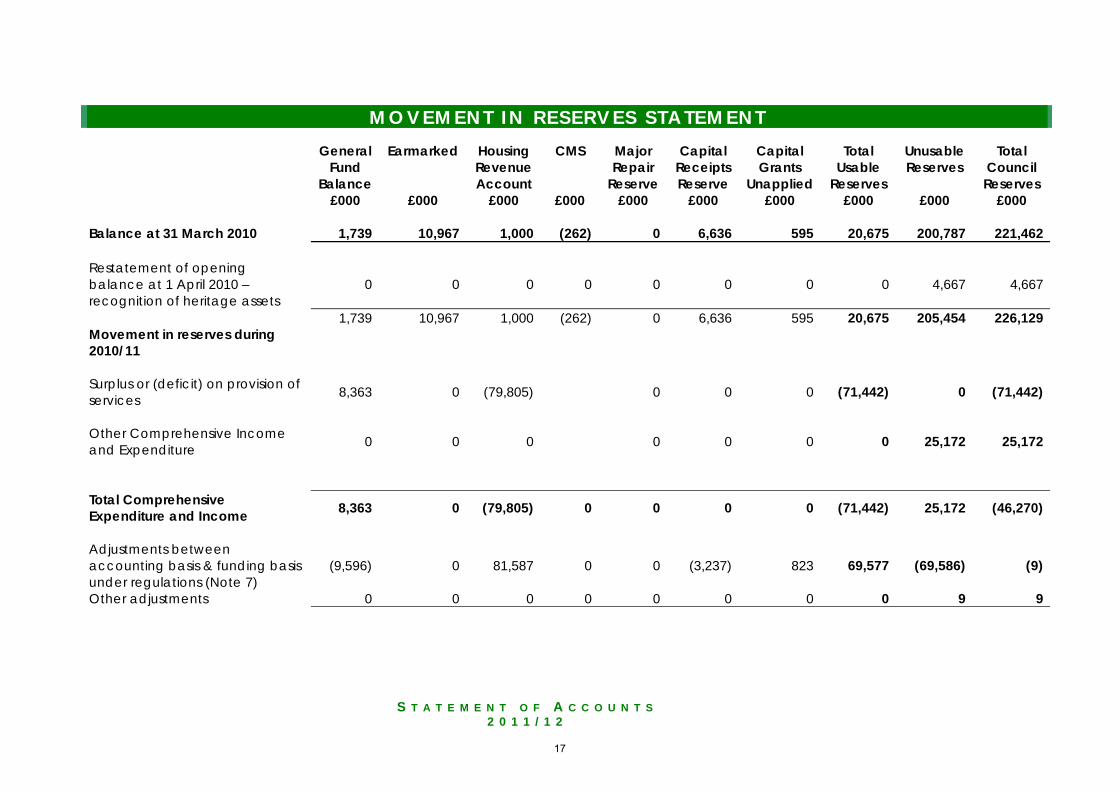

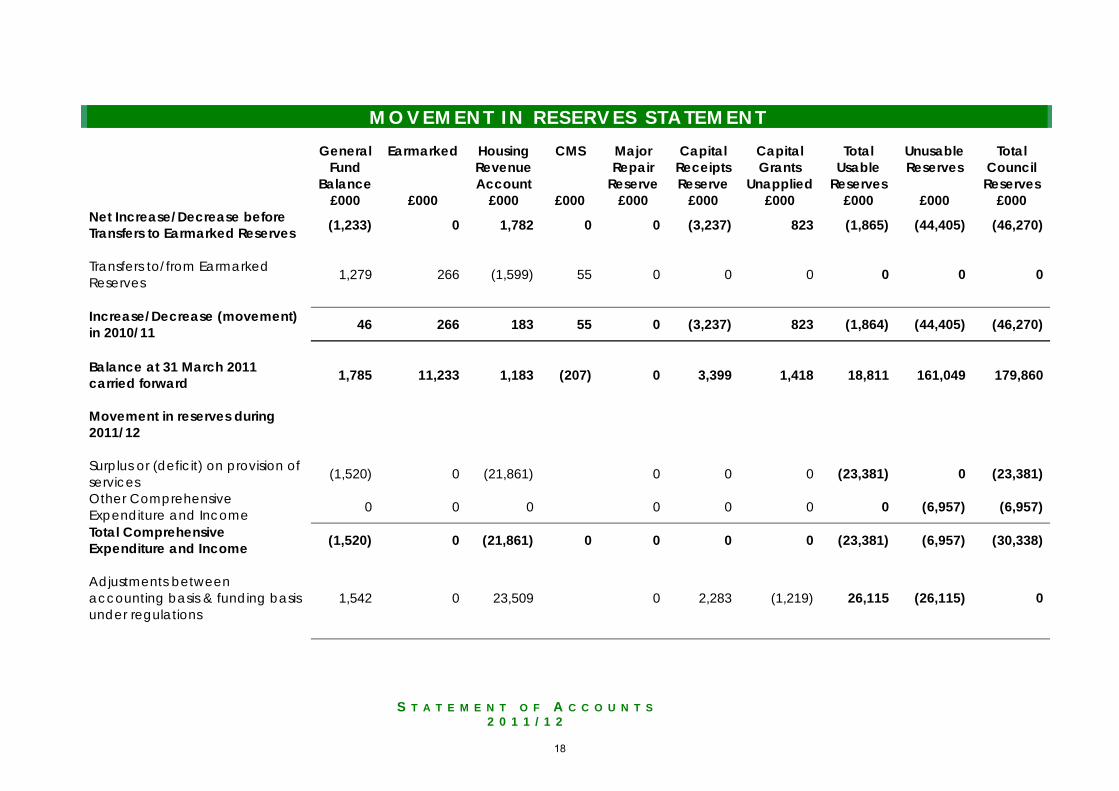

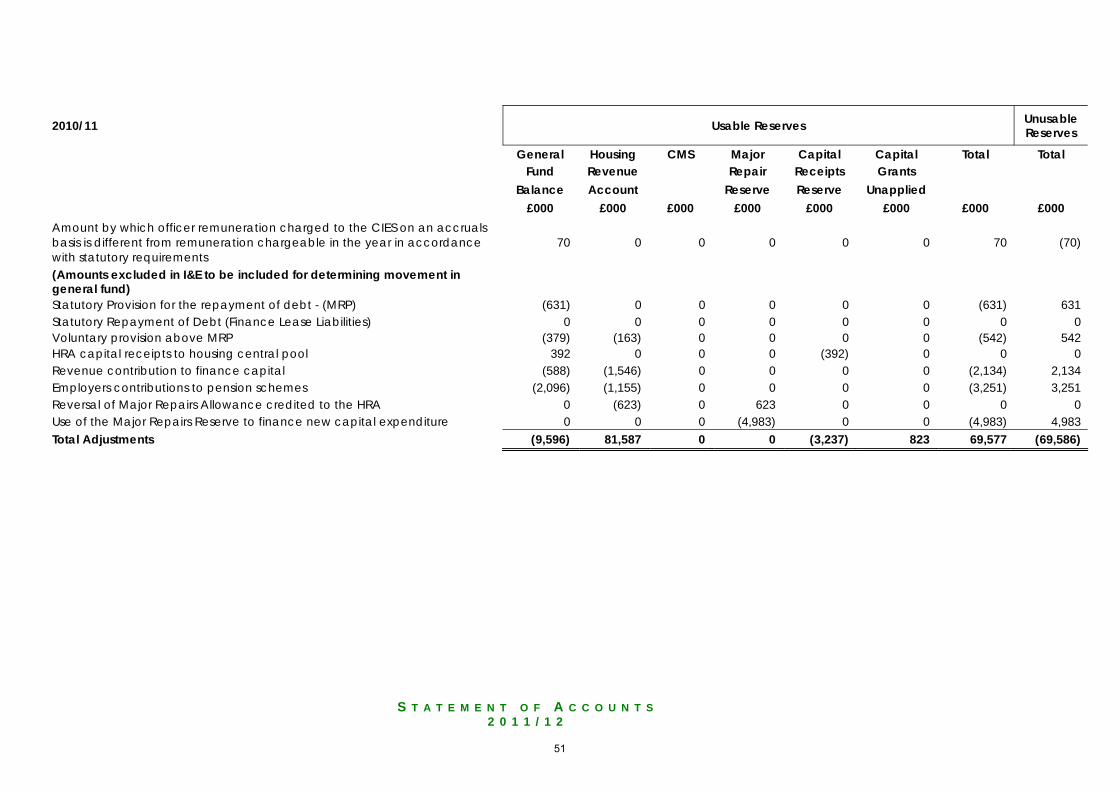

M O V E M E N T I N R E S E R V E S S T A T E M E N T

General Earmarked Housing CMS Major Capital Capital Total Unusable Total Fund Revenue Repair Receipts Grants Usable Reserves Council Balance Account Reserve Reserve Unapplied Reserves Reserves £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 Balance at 31 March 2010 1,739 10,967 1,000 (262) 0 6,636 595 20,675 200,787 221,462 Restatement of opening balance at 1 April 2010 – recognition of heritage assets

0 0 0 0 0 0 0 0 4,667 4,667

1,739 10,967 1,000 (262) 0 6,636 595 20,675 205,454 226,129 Movement in reserves during 2010/11

Surplus or (deficit) on provision of services 8,363 0 (79,805) 0 0 0 (71,442) 0 (71,442)

Other Comprehensive Income and Expenditure 0 0 0 0 0 0 0 25,172 25,172

Total Comprehensive Expenditure and Income 8,363 0 (79,805) 0 0 0 0 (71,442) 25,172 (46,270)

Adjustments between accounting basis & funding basis under regulations (Note 7)

(9,596) 0 81,587 0 0 (3,237) 823 69,577 (69,586) (9)

Other adjustments 0 0 0 0 0 0 0 0 9 9

17

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

M O V E M E N T I N R E S E R V E S S T A T E M E N T

General Earmarked Housing CMS Major Capital Capital Total Unusable Total Fund Revenue Repair Receipts Grants Usable Reserves Council Balance Account Reserve Reserve Unapplied Reserves Reserves £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 Net Increase/Decrease before Transfers to Earmarked Reserves (1,233) 0 1,782 0 0 (3,237) 823 (1,865) (44,405) (46,270)

Transfers to/from Earmarked Reserves 1,279 266 (1,599) 55 0 0 0 0 0 0

Increase/Decrease (movement) in 2010/11 46 266 183 55 0 (3,237) 823 (1,864) (44,405) (46,270)

Balance at 31 March 2011 carried forward 1,785 11,233 1,183 (207) 0 3,399 1,418 18,811 161,049 179,860

Movement in reserves during 2011/12

Surplus or (deficit) on provision of services (1,520) 0 (21,861) 0 0 0 (23,381) 0 (23,381)

Other Comprehensive Expenditure and Income 0 0 0 0 0 0 0 (6,957) (6,957)

Total Comprehensive Expenditure and Income (1,520) 0 (21,861) 0 0 0 0 (23,381) (6,957) (30,338)

Adjustments between accounting basis & funding basis under regulations

1,542 0 23,509 0 2,283 (1,219) 26,115 (26,115) 0

18

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

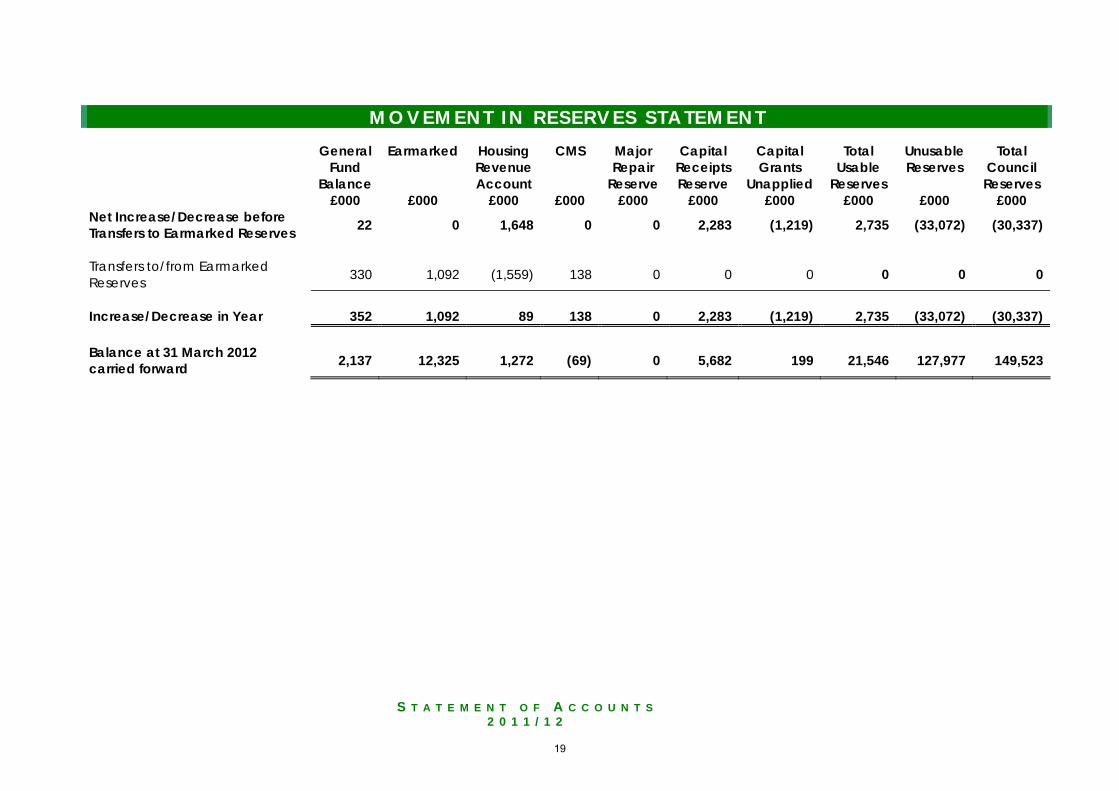

M O V E M E N T I N R E S E R V E S S T A T E M E N T

General Earmarked Housing CMS Major Capital Capital Total Unusable Total Fund Revenue Repair Receipts Grants Usable Reserves Council Balance Account Reserve Reserve Unapplied Reserves Reserves £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 Net Increase/Decrease before Transfers to Earmarked Reserves 22 0 1,648 0 0 2,283 (1,219) 2,735 (33,072) (30,337)

Transfers to/from Earmarked Reserves 330 1,092 (1,559) 138 0 0 0 0 0 0

Increase/Decrease in Year 352 1,092 89 138 0 2,283 (1,219) 2,735 (33,072) (30,337) Balance at 31 March 2012 carried forward 2,137 12,325 1,272 (69) 0 5,682 199 21,546 127,977 149,523

19

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

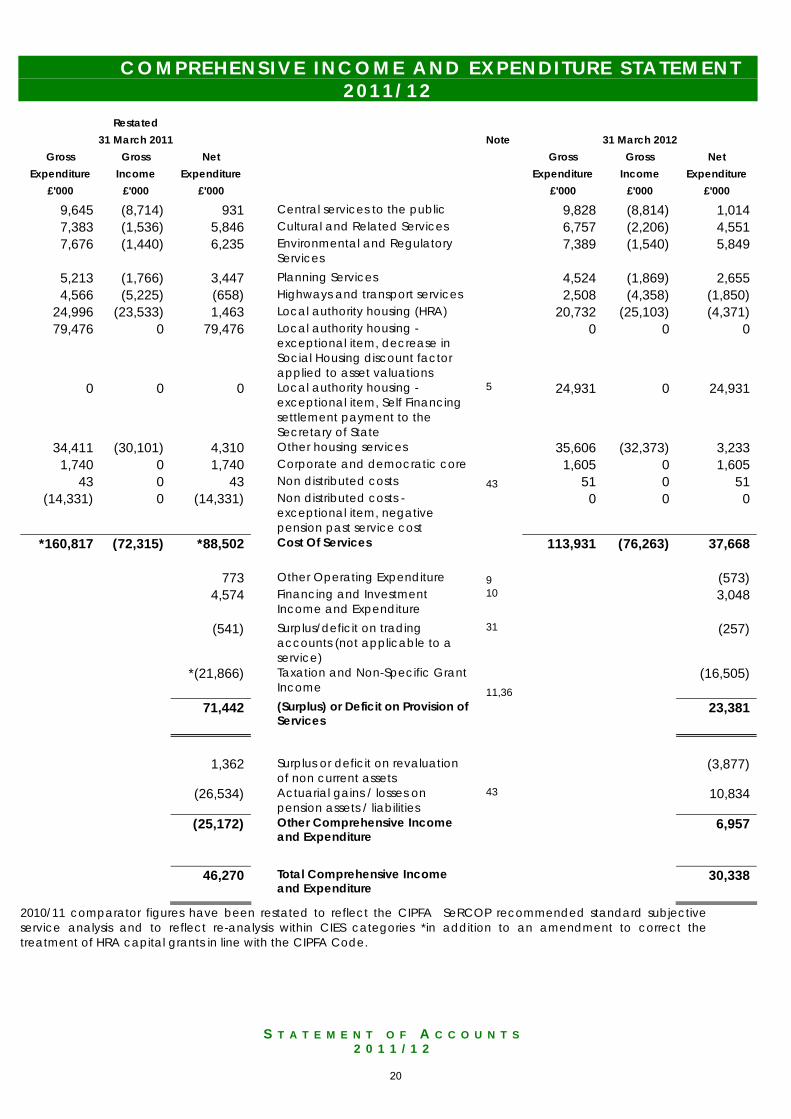

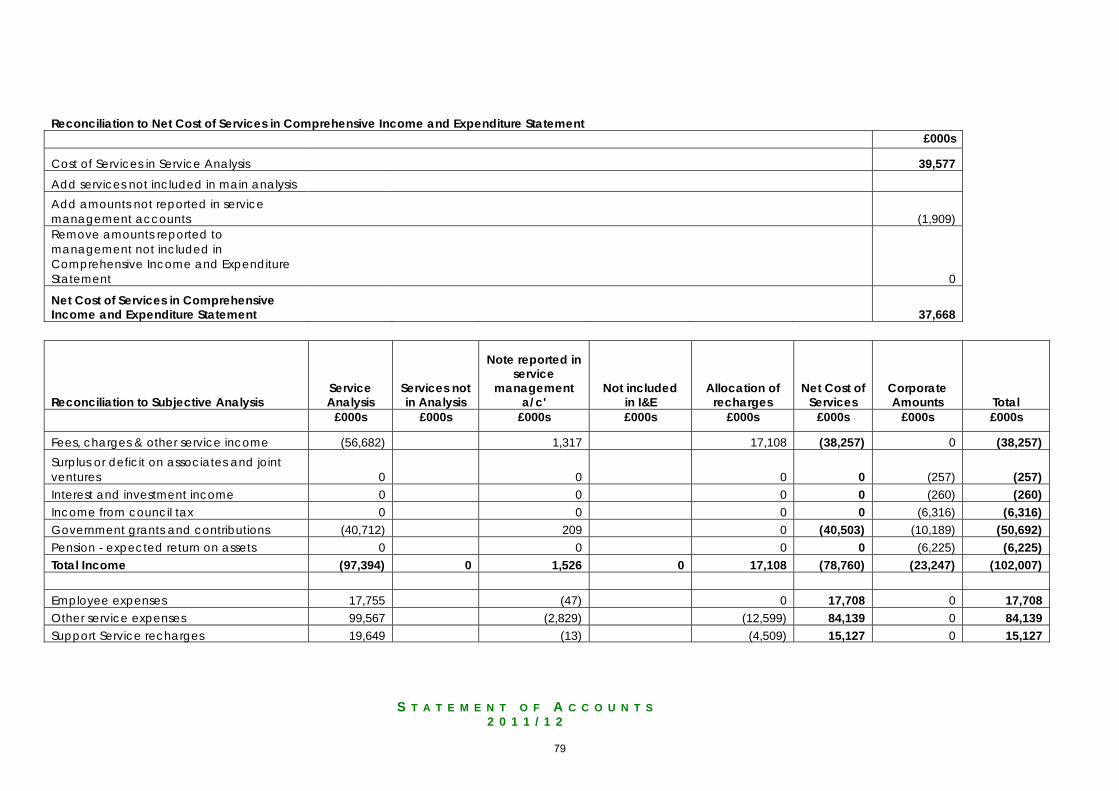

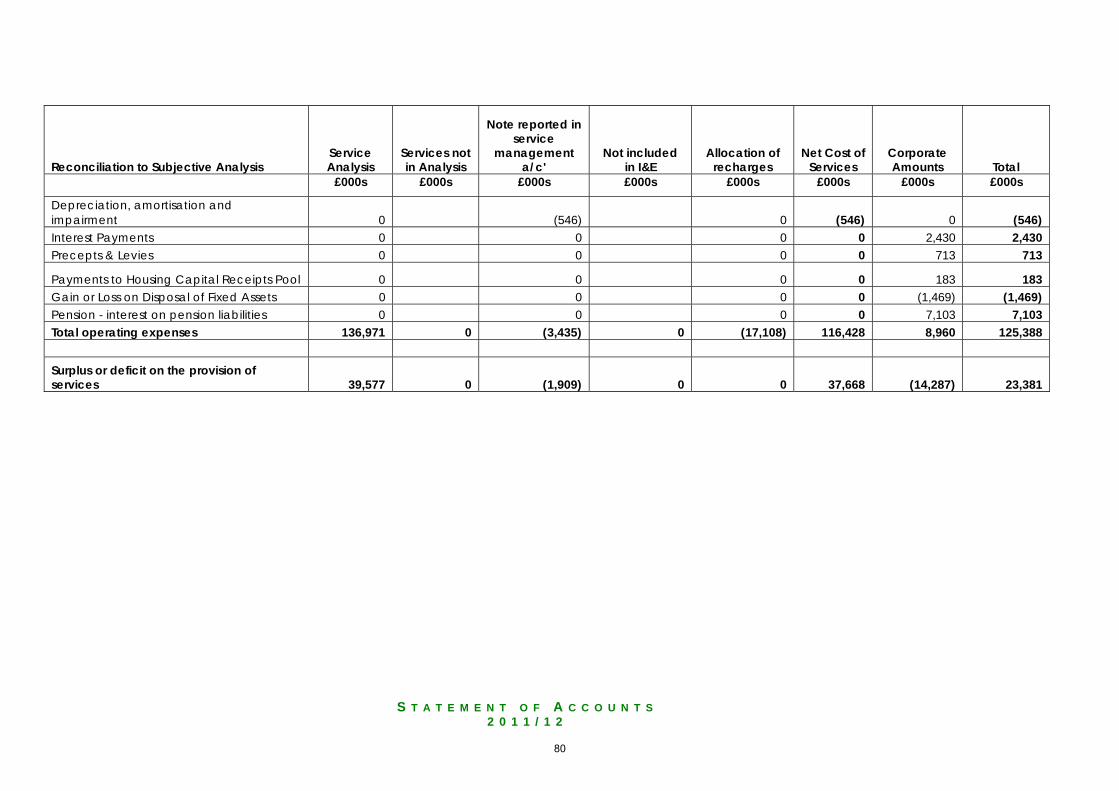

C O M P R E H E N S I V E I N C O M E A N D E X P E N D I T U R E S T A T E M E N T 2011/12

Restated

31 March 2011 Note 31 March 2012 Gross Gross Net Gross Gross Net

Expenditure Income Expenditure Expenditure Income Expenditure £'000 £'000 £'000 £'000 £'000 £'000

9,645 (8,714) 931 Central services to the public 9,828 (8,814) 1,014 7,383 (1,536) 5,846 Cultural and Related Services 6,757 (2,206) 4,551 7,676 (1,440) 6,235

Environmental and Regulatory Services

7,389 (1,540) 5,849

5,213 (1,766) 3,447 Planning Services 4,524 (1,869) 2,655 4,566 (5,225) (658) Highways and transport services 2,508 (4,358) (1,850)

24,996 (23,533) 1,463 Local authority housing (HRA) 20,732 (25,103) (4,371) 79,476 0 79,476

Local authority housing - exceptional item, decrease in Social Housing discount factor applied to asset valuations

0 0 0

0 0 0

Local authority housing - exceptional item, Self Financing settlement payment to the Secretary of State

5 24,931 0 24,931

34,411 (30,101) 4,310 Other housing services 35,606 (32,373) 3,233 1,740 0 1,740 Corporate and democratic core 1,605 0 1,605

43 0 43 Non distributed costs 43 51 0 51 (14,331) 0 (14,331)

Non distributed costs - exceptional item, negative pension past service cost

0 0 0

*160,817 (72,315) *88,502 Cost Of Services 113,931 (76,263) 37,668 773 Other Operating Expenditure 9 (573)

4,574

Financing and Investment Income and Expenditure

10 3,048

(541) Surplus/deficit on trading accounts (not applicable to a service)

31 (257)

*(21,866)

Taxation and Non-Specific Grant Income 11,36

(16,505)

71,442

(Surplus) or Deficit on Provision of Services

23,381

1,362 Surplus or deficit on revaluation

of non current assets (3,877)

(26,534) Actuarial gains / losses on

pension assets / liabilities 43 10,834

(25,172) Other Comprehensive Income

and Expenditure 6,957

46,270 Total Comprehensive Income

and Expenditure 30,338

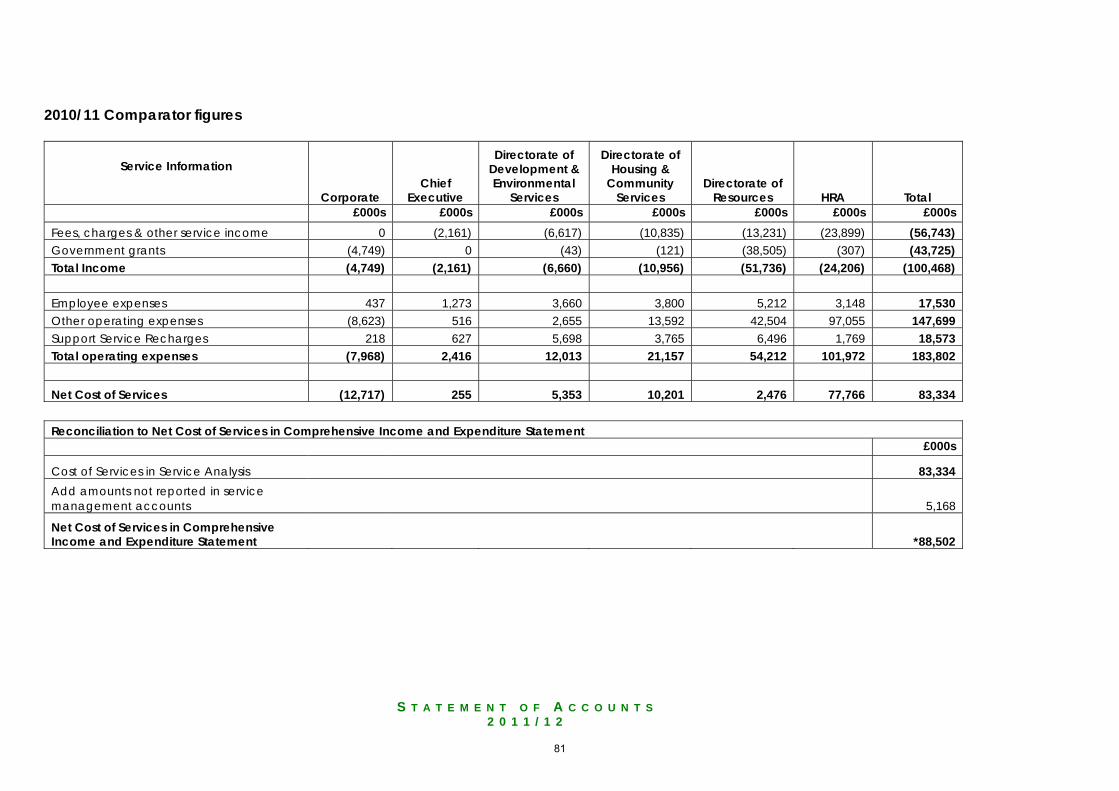

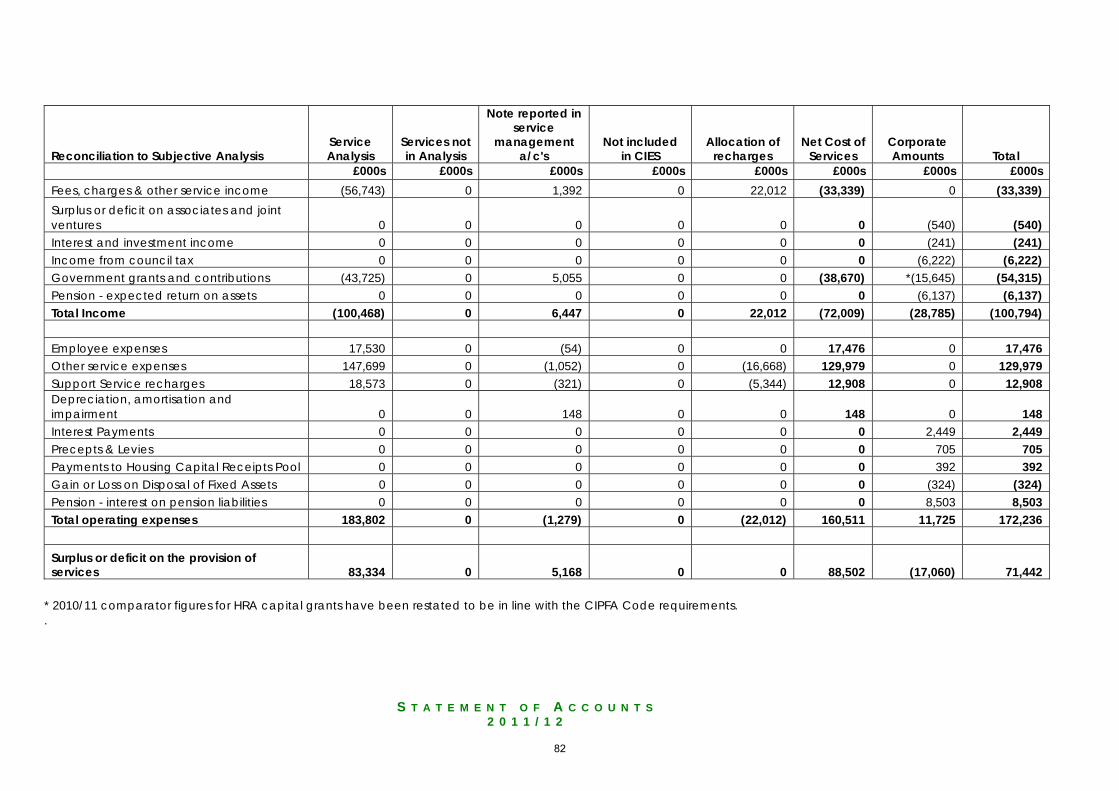

2010/11 comparator figures have been restated to reflect the CIPFA SeRCOP recommended standard subjective service analysis and to reflect re-analysis within CIES categories *in addition to an amendment to correct the treatment of HRA capital grants in line with the CIPFA Code.

20

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

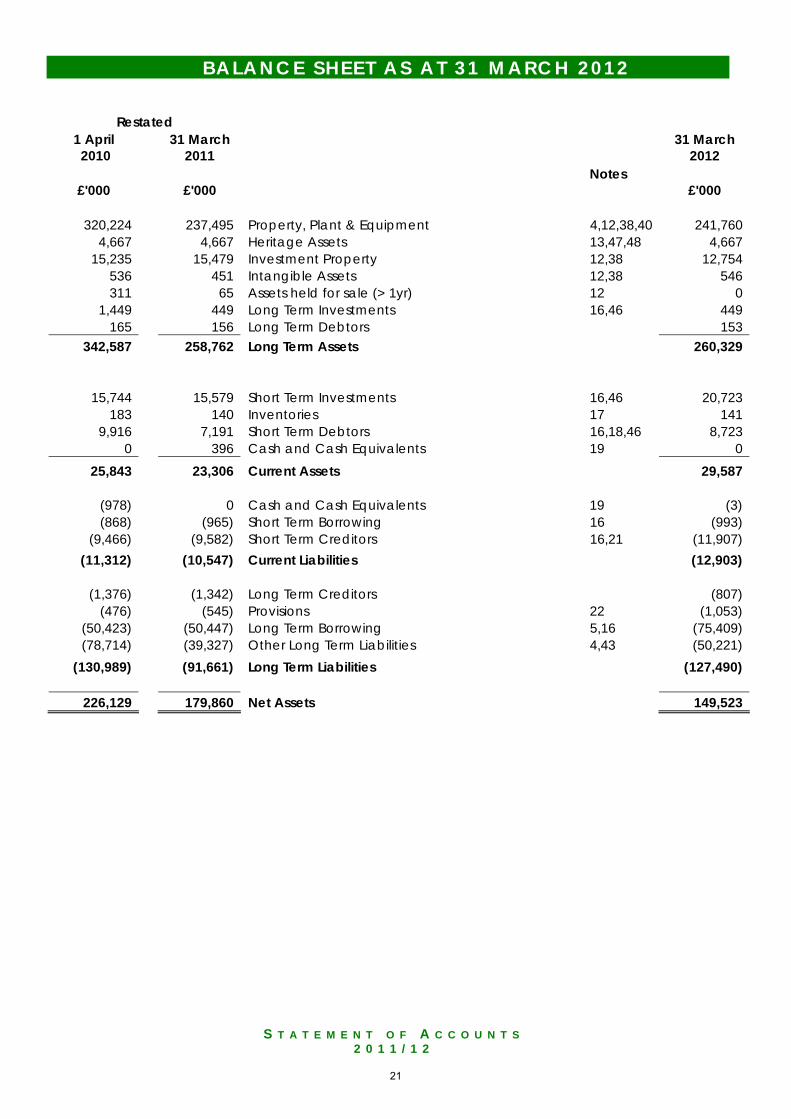

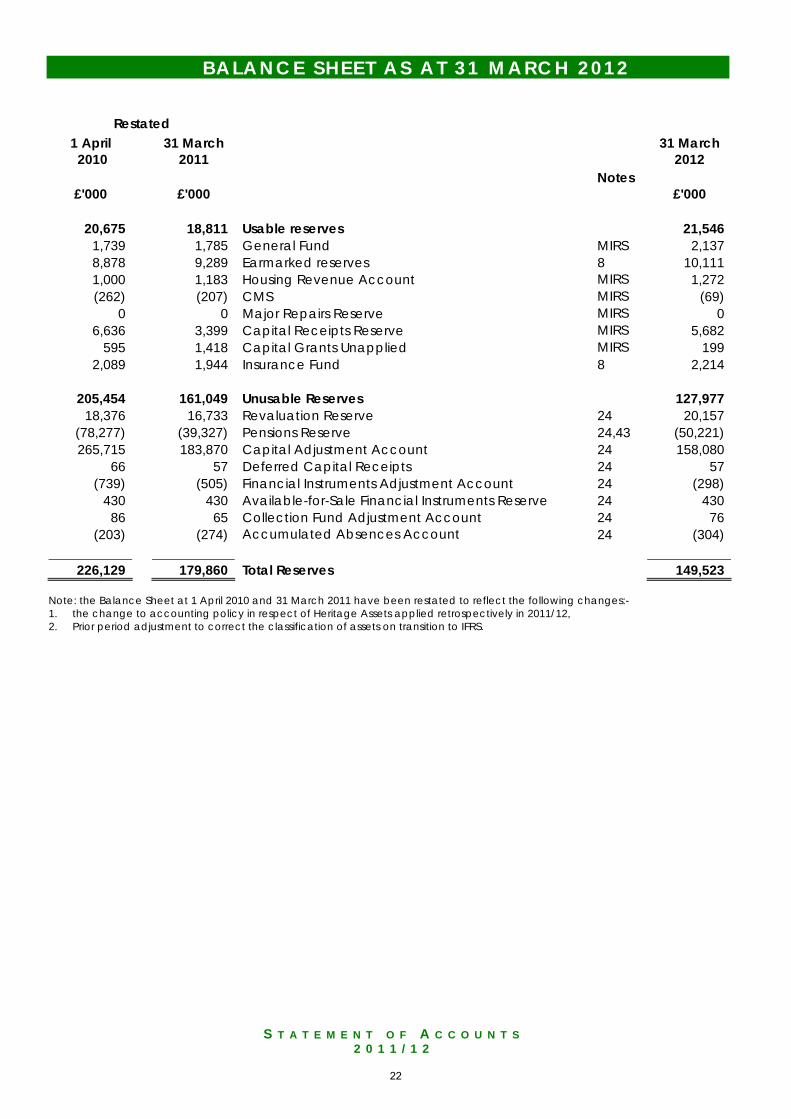

B A L A N C E S H E E T A S A T 3 1 M A R C H 2 0 1 2

Restated

1 April 2010

31 March 2011

Notes

31 March 2012

£'000 £'000 £'000

320,224 237,495 Property, Plant & Equipment 4,12,38,40 241,760 4,667 4,667 Heritage Assets 13,47,48 4,667

15,235 15,479 Investment Property 12,38 12,754 536 451 Intangible Assets 12,38 546 311 65 Assets held for sale (> 1yr) 12 0

1,449 449 Long Term Investments 16,46 449 165 156 Long Term Debtors 153

342,587 258,762 Long Term Assets 260,329

15,744 15,579 Short Term Investments 16,46 20,723

183 140 Inventories 17 141 9,916 7,191 Short Term Debtors 16,18,46 8,723

0 396 Cash and Cash Equivalents 19 0 25,843 23,306 Current Assets 29,587

(978) 0 Cash and Cash Equivalents 19 (3) (868) (965) Short Term Borrowing 16 (993)

(9,466) (9,582) Short Term Creditors 16,21 (11,907) (11,312) (10,547) Current Liabilities (12,903)

(1,376) (1,342) Long Term Creditors (807)

(476) (545) Provisions 22 (1,053) (50,423) (50,447) Long Term Borrowing 5,16 (75,409) (78,714) (39,327) Other Long Term Liabilities 4,43 (50,221)

(130,989) (91,661) Long Term Liabilities (127,490)

226,129 179,860 Net Assets 149,523

21

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

B A L A N C E S H E E T A S A T 3 1 M A R C H 2 0 1 2

Restated 1 April 2010

31 March 2011

Notes

31 March 2012

£'000 £'000 £'000

20,675 18,811 Usable reserves 21,546 1,739 1,785 General Fund MIRS 2,137 8,878 9,289 Earmarked reserves 8 10,111 1,000 1,183 Housing Revenue Account MIRS 1,272 (262) (207) CMS MIRS (69)

0 0 Major Repairs Reserve MIRS 0 6,636 3,399 Capital Receipts Reserve MIRS 5,682

595 1,418 Capital Grants Unapplied MIRS 199 2,089 1,944 Insurance Fund 8 2,214

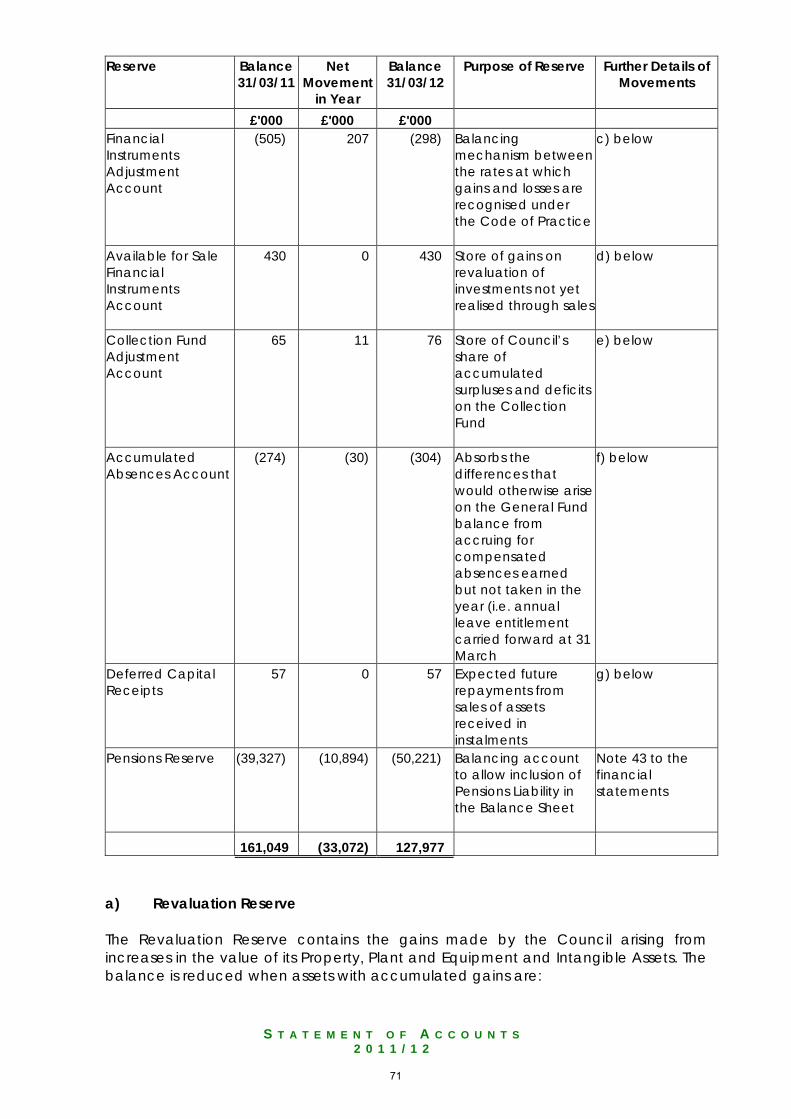

205,454 161,049 Unusable Reserves 127,977

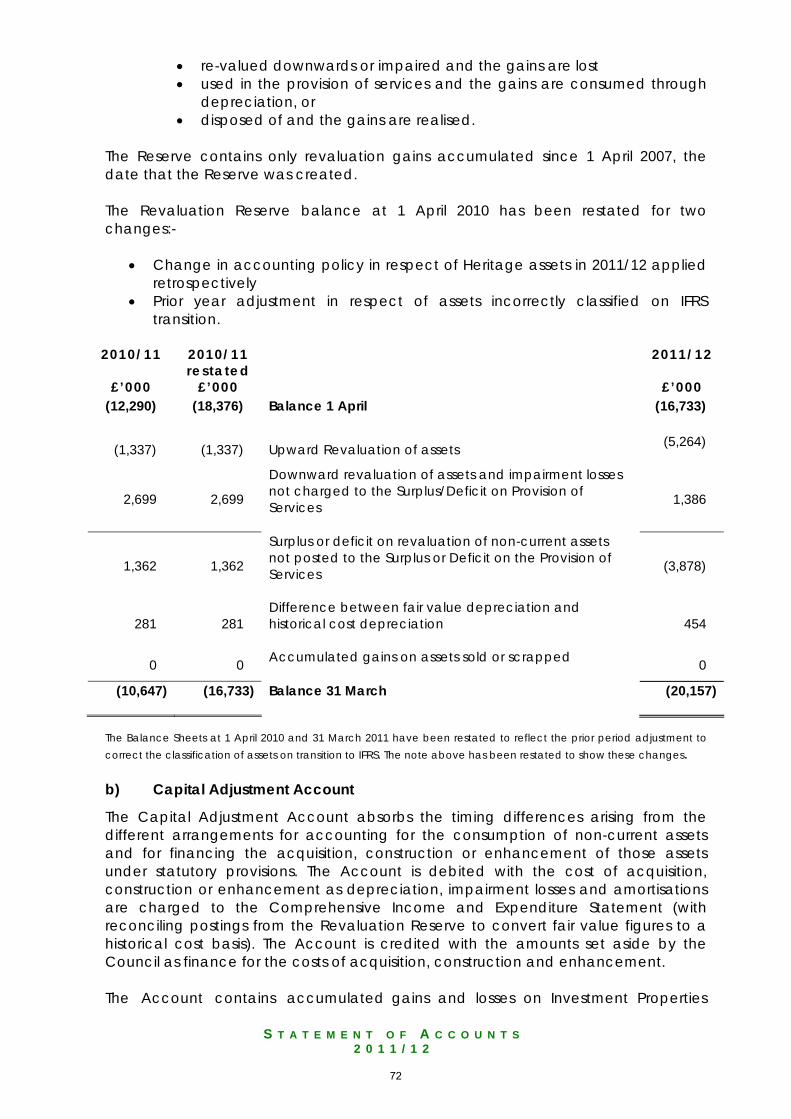

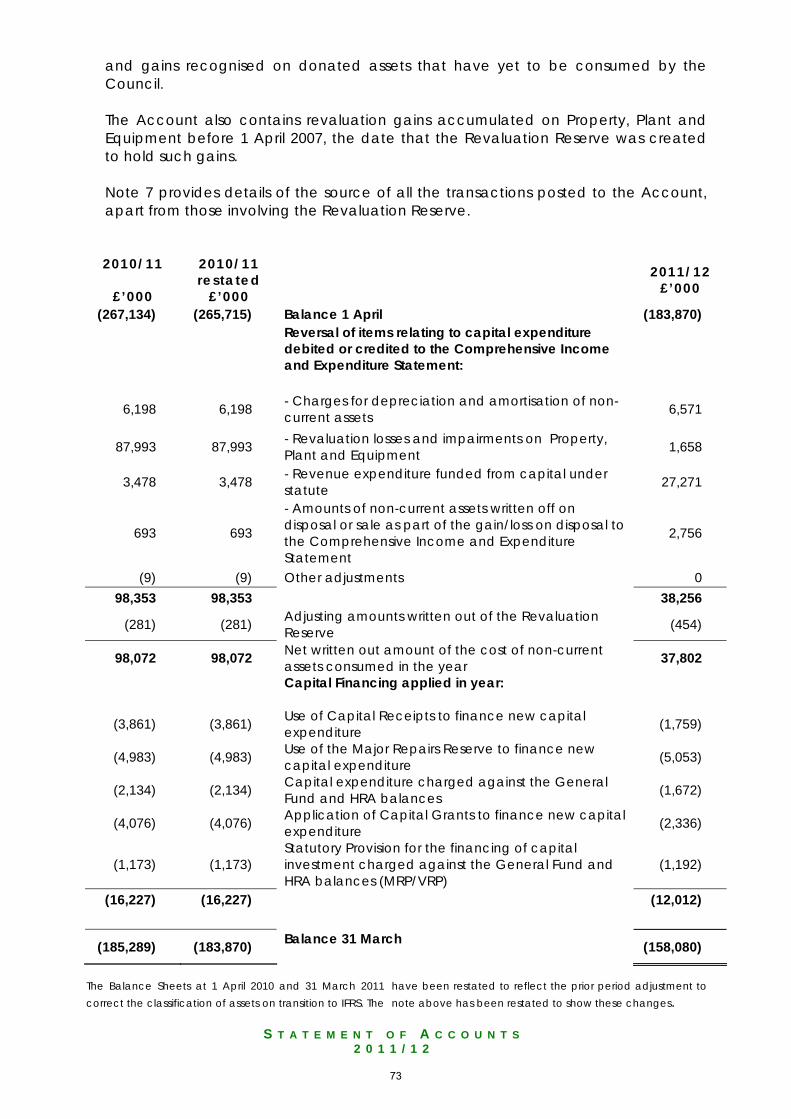

18,376 16,733 Revaluation Reserve 24 20,157 (78,277) (39,327) Pensions Reserve 24,43 (50,221) 265,715 183,870 Capital Adjustment Account 24 158,080

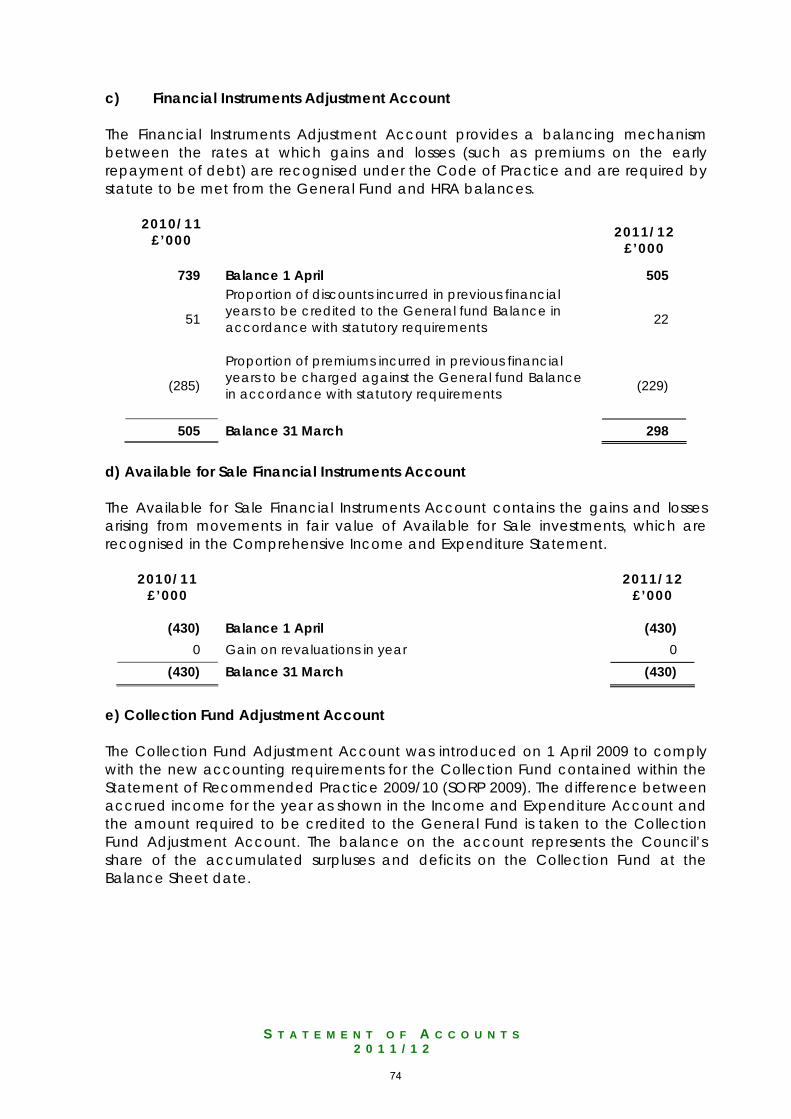

66 57 Deferred Capital Receipts 24 57 (739) (505) Financial Instruments Adjustment Account 24 (298)

430 430 Available-for-Sale Financial Instruments Reserve 24 430 86 65 Collection Fund Adjustment Account 24 76

(203) (274) Accumulated Absences Account 24 (304)

226,129 179,860 Total Reserves 149,523

Note: the Balance Sheet at 1 April 2010 and 31 March 2011 have been restated to reflect the following changes:- 1. the change to accounting policy in respect of Heritage Assets applied retrospectively in 2011/12, 2. Prior period adjustment to correct the classification of assets on transition to IFRS.

22

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

C A S H F L O W S T A T E M E N T

31 March 2011

Notes 31 March 2012

£'000 £'000

71,442 Net (surplus) or deficit on the provision of services 23,381

(90,301) Adjustments to net surplus or deficit on the provision of services for non-cash movements 26 (12,717)

5,028 Adjustments for items included in the net surplus or deficit on the provision of services that are investing and financing activities

27 10,475

(13,831) Net cash flows from Operating Activities 25 21,139

11,974 Investing Activities 28 3,700

483 Financing Activities 29 (24,440)

(1,374) Net (increase) or decrease in cash and cash equivalents 399

(978) Cash and cash equivalents at the beginning of the reporting period 396

396 Cash and cash equivalents at the end of the reporting period 19 (3)

23

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

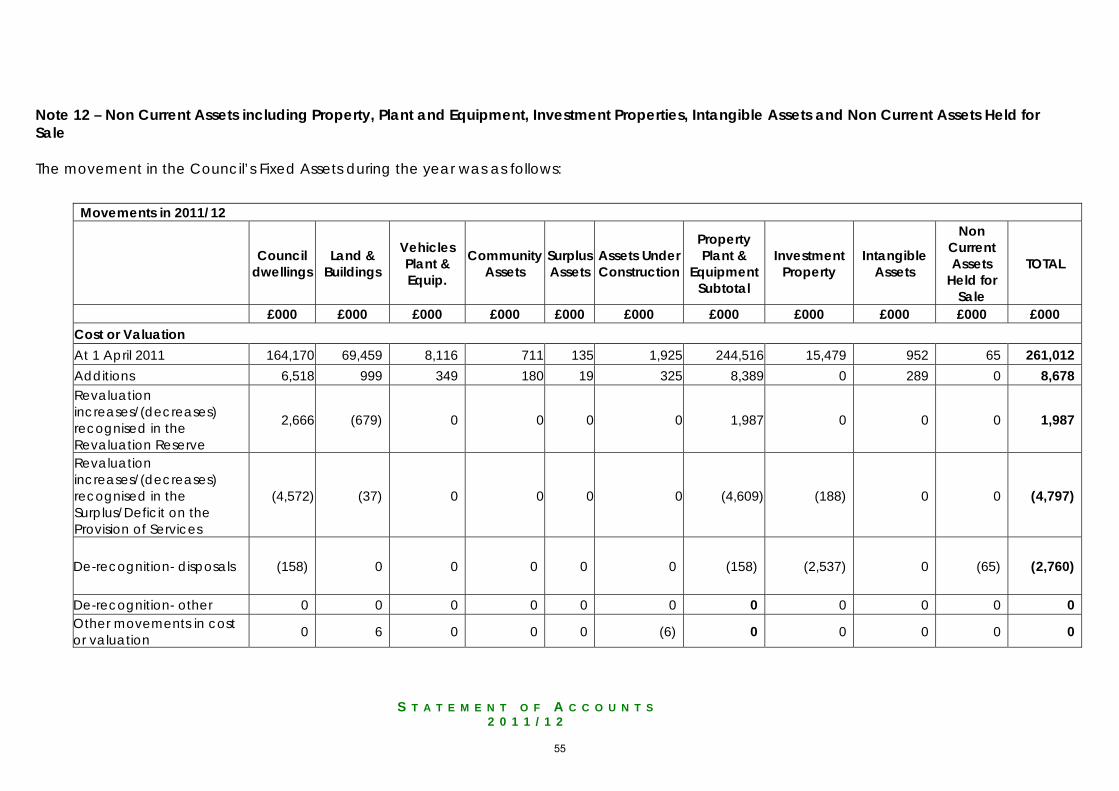

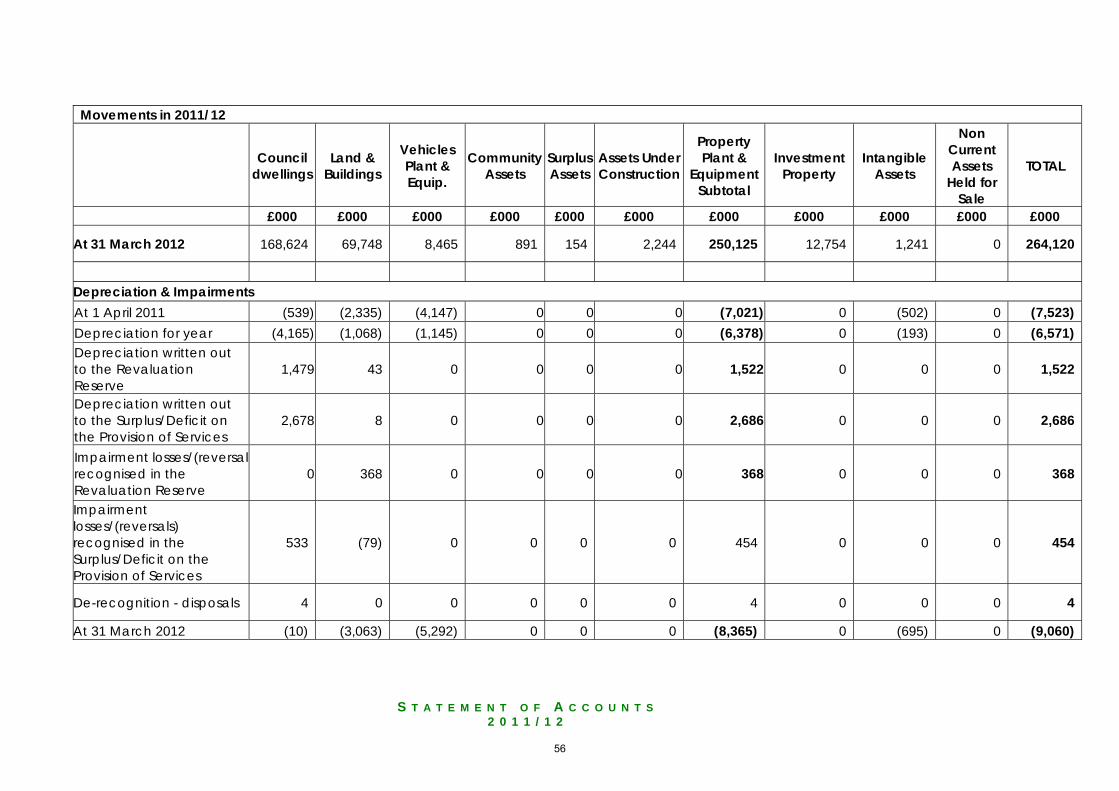

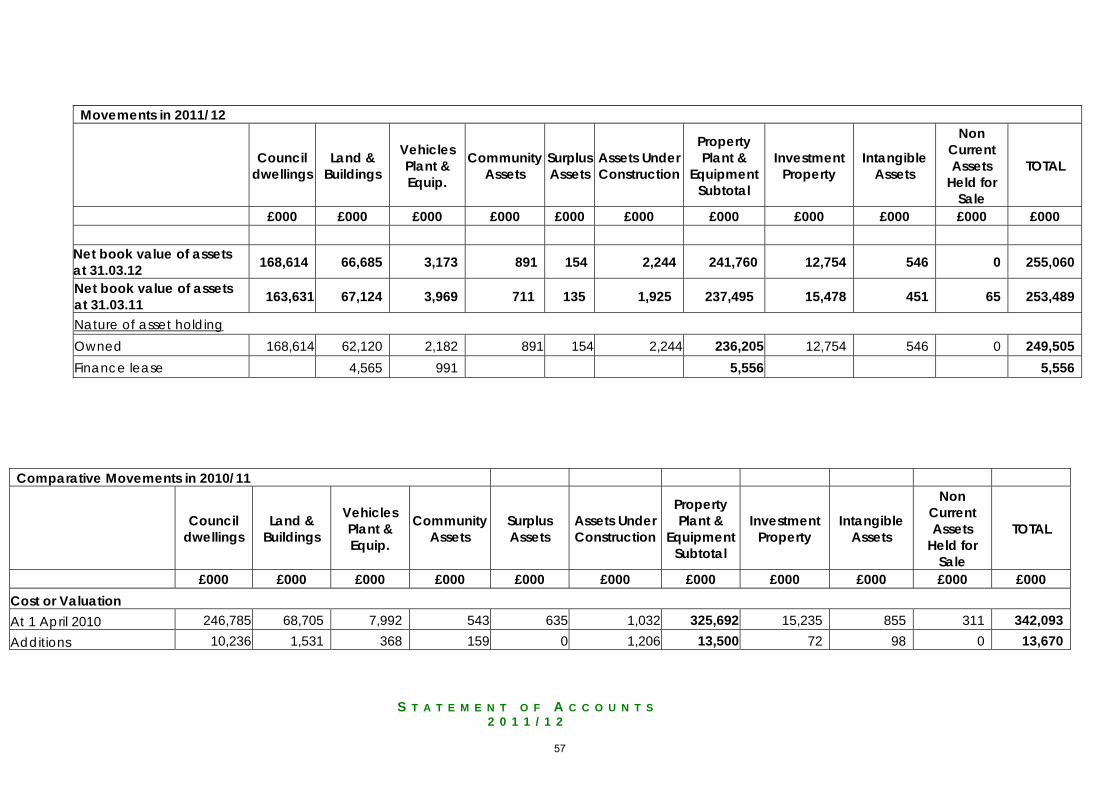

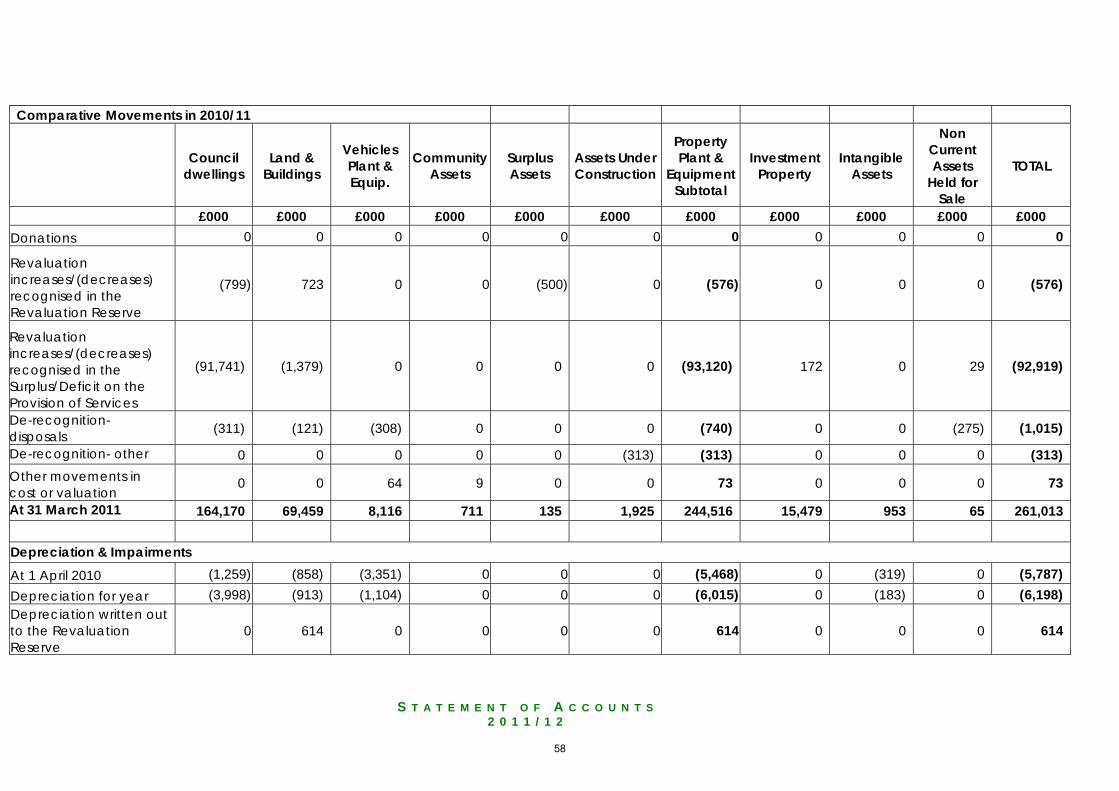

N O T E S T O T H E A C C O U N T S

Note 1 – Accounting Policies 1. General Principles The Statement of Accounts summarises the Council’s transactions for the 2011/12 financial year and its position at the year-end of 31 March 2012. The Statement of Accounts has been prepared in accordance with proper accounting practices. These practices primarily comprise the Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 (the Code) and the CIPFA Service Reporting Code of Practice 2011/12 (SeRCOP), supported by International Financial Reporting Standards (IFRS) and statutory guidance issued under section 7 of the Accounts and Audit Regulations 2011. The accounting convention adopted in the Statement of Accounts is historic cost, modified by the revaluation of certain categories of non-current assets and financial instruments. The accounts are prepared on a going concern basis which assumes that the functions of the Council will continue in operational existence for the foreseeable future. 2. Accruals of Income and Expenditure The revenue accounts of the Council are maintained on an accruals basis meaning that activity is accounted for in the year that it takes place, not simply when cash payments are made or received. In particular:

• Revenue from the sale of assets is recognised when the Council transfers the significant risks and rewards of ownership to the purchaser and it is probable that economic benefits or service potential associated with the transaction will flow to the Council.

• Revenue from the provision of services is recognised when the Council can

measure reliably the percentage of completion of the transaction and it is probable that economic benefits or service potential associated with the transaction will flow to the Council.

• Supplies are recorded as expenditure when they are consumed – where there

is a gap between the date supplies are received and their consumption they are carried as inventories on the Balance Sheet.

• Expenses in relation to services received (including services provided by

employees) are recorded as expenditure when the services are received rather than when payments are made.

• Interest receivable on investments and payable on borrowings is accounted

for respectively as income and expenditure on the basis of the effective interest rate for the relevant financial instrument rather than the cash flows fixed or determined by the contract.

24

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

• Where revenue and expenditure have been recognised but cash has not been received or paid, a debtor or creditor for the relevant amount is recorded in the Balance Sheet. Where debts may not be settled, the balance of debtors is written down and a charge made to revenue for the income that might not be collected.

3. Cash and Cash Equivalents Cash is represented by cash in hand and deposits with financial institutions repayable without penalty on notice of not more than 24 hours. Cash equivalents are investments that mature within three months or less from the date of acquisition and that are readily convertible to known amounts of cash with insignificant risk of change in value. In the Cash Flow Statement, cash and cash equivalents are shown net of bank overdrafts that are repayable on demand and form an integral part of the Council’s cash management. 4. Exceptional Items When items of income and expense are material, their nature and amount is disclosed separately, either on the face of the Comprehensive Income and Expenditure Statement or in the notes to the accounts, depending on how significant the items are to an understanding of the Council’s financial performance. 5. Prior Period Adjustments, Changes in Accounting Policies and Estimates and Errors Prior period adjustments may arise as a result of a change in accounting policies or to correct a material error. Changes in accounting estimates are accounted for prospectively i.e. in the current and future years affected by the change and do not give rise to prior period adjustment. Changes in accounting policies are only made when required by proper accounting practices or the change provides more reliable or relevant information about the effect of transactions, other events and conditions on the Council’s financial position or financial performance. Where a change is made, it is applied retrospectively (unless stated otherwise) by adjusting opening balances and comparative amounts for the prior period as if the new policy had always been applied. Material errors discovered in prior period figures are corrected retrospectively by amending opening balances and comparative amounts for the prior period. 6. Charges to Revenue for Non-Current Assets Service revenue accounts, central support services and trading accounts are charged with the following amounts to reflect the cost of holding fixed assets during the year:

• depreciation of the assets used by the service

• revaluation and impairment losses on assets used by the service

25

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

where there are no accumulated gains in the Revaluation Reserve against which losses can be written off

• amortisation of intangible fixed assets used by the service.

The Council is not required to raise Council Tax to fund depreciation, revaluation and impairment losses or amortisation. However, it is required to make an annual contribution from revenue towards the reduction in its overall borrowing requirement equal to an amount calculated on a prudent basis determined by the Council in accordance with statutory guidance. This is referred to as the Minimum Revenue Provision (MRP) and Voluntary Revenue Provision (VRP). The Council’s policy on MRP is:

• For capital expenditure incurred before 1 April 2009, or which from 1 April 2009 is supported borrowing, the MRP is based on 4% of the opening capital financing requirement (with adjustments allowed for in DCLG Regulations).

• For all unsupported borrowing from 1 April 2009, the MRP is based on the

estimated life of the asset which the borrowing has been used to fund.

• VRP will be charged if considered prudent for individual asset financing. Depreciation, revaluation and impairment losses and amortisation are replaced by the MRP and VRP, by way of an adjusting transaction between the Capital Adjustment Account and the General Fund Balance in the Movement in Reserves Statement, for the differences between the two. 7. Employee Benefits Benefits payable during employment Short-term employee benefits are those due to be settled within 12 months of the year-end. They include such benefits as wages and salaries, paid annual leave and paid sick leave, bonuses and non-monetary benefits (e.g. cars) for current employees and are recognised as an expense for services in the year in which employees render service to the Council. An accrual is made for the cost of holiday entitlements or time off in lieu, earned by employees but not taken before the year-end, which employees can carry forward into the next financial year. The accrual is made at the wage and salary rates applicable in the following accounting year, being the period in which employee take the benefit. The accrual is charged to Surplus or Deficit on the Provision of Services, but then reversed out through the Movement in Reserves Statement so that holiday benefits are charged to revenue in the financial year in which the holiday absence occurs. Termination benefits Termination benefits are amounts payable as a result of a decision by the Council to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy and are charged on an accruals basis to the appropriate service line in the Comprehensive Income and Expenditure Statement when the Council is demonstrably committed to the termination of the

26

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

employment of an officer or group of officers or making an offer to encourage voluntary redundancy. Where termination benefits involve the enhancement of pensions, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the pension fund or pensioner in the year, not the amount calculated according to relevant accounting standards. In the Movement in Reserves Statement, transfers are required to and from the Pensions Reserve to remove notional debits and credits for pension enhancement termination benefits and replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year-end. Post Employment Benefits Employees of the Council are members of the Local Government Pension Scheme, administered by Lincolnshire County Council. This scheme provides defined benefits to members (retirement lump sums and pensions), earned as employees worked for the Council. The Local Government Pension Scheme The Local Government Scheme is accounted for as a defined benefits scheme: The liabilities of the Lincolnshire County Council pension fund attributable to the Council are included in the Balance Sheet on an actuarial basis using the protected unit method – i.e. an assessment of the future payments that will be made in relation to retirement benefits earned to date by employees, based on assumptions about mortality rates, employee turnover rates, etc, and forecasts of projected earnings for current employees. Liabilities are discounted to their value at current prices, using a discount rate of 4.7% (provisional) (based on the indicative rate of return on high quality corporate bond (iBoxx Sterling Corporates AA over 15 year Index). The assets of the Lincolnshire County Council pension fund attributable to the Council are included in the Balance Sheet at their fair value:

• Quoted securities – current bid price • Unquoted securities – professional estimate • Unitised securities – current bid price • Property – market value.

The change in the net pensions liability is analysed into seven components:

• Current service cost – the increase in liabilities as a result of years of service earned this year – allocated in the Comprehensive Income and Expenditure Statement to the services for which the employees worked

• Past service cost – the increase in liabilities arising from current year decisions

whose effect relates to years of service earned in earlier years – debited to the Surplus or Deficit on the Provision of Services in the Comprehensive

27

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Income and Expenditure Statement as part of Non Distributed Costs

• Interest cost – the expected increase in the present value of liabilities during the year as they move one year closer to being paid – debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement

• Expected return on assets – the annual investment return on the fund assets

attributable to the Council, based on an average of the expected long-term return – credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement

• Gains or losses on settlements and curtailments – the result of actions to

relieve the Council of liabilities or events that reduce the expected future service or accrual of benefits of employees – debited or credited to the Surplus or Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs

• Actuarial gains and losses – changes in the net pensions liability that arise

because events have not coincided with assumptions made at the last actuarial valuation or because the actuaries have updated their assumptions – debited to the Pensions Reserve

• Contributions paid to the Lincolnshire County Council pension fund – cash

paid as employer’s contributions to the pension fund in settlement of liabilities; not accounted for as an expense.

In relation to retirement benefits, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the pension fund or directly to pensioners in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, this means that there are transfers to and from the Pensions Reserve to remove the notional debits and credits for retirement benefits and replace them with debits for the cash paid to the pension fund and pensioners and any such amounts payable but unpaid at the year-end. The negative balance that arises on the Pension Reserve thereby measures the beneficial impact to the General Fund of being required to account for retirement benefits on the basis of cash flows rather than as benefits are earned by employees. Discretionary Benefits The Council also has restricted powers to make discretionary awards of retirement benefits in the event of early retirements. Any liabilities estimated to arise as a result of an award to any member of staff are accrued in the year of decision to make the award and accounted for using the same policies as are applied to the Local Government Pension Scheme. 8. Events After the Balance Sheet Date Events after the Balance Sheet date are those events, both favourable and unfavourable, that occur between the end of the reporting period and the date

28

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

when the Statement of Accounts is authorised for issue. Two types of events can be identified:

• Those that provide evidence of conditions that existed at the end of the reporting period – the Statement of Accounts is adjusted to reflect such events

• Those that are indicative of conditions that arose after the reporting period –

the Statement of Accounts is not adjusted to reflect such events, but where category of events would have a material effect, disclosure is made in the notes of the nature of the events and their estimated financial effect.

Events taking place after the date of authorisation for issue are not reflected in the Statement of Accounts. 9. Financial Instruments Financial Liabilities Financial liabilities are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument. They are initially measured at fair value and carried at their amortised cost. Annual charges for interest payable are shown in the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, and are based on the carrying amount of the liability, multiplied by the effective rate of interest for the instrument. The effective interest rate is the rate that exactly discounts estimated future cash payments over the life of the instrument to the amount at which it was originally recognised. For most of the borrowings that the Council has, this means that the amount presented in the Balance Sheet is the outstanding principal repayable, with accrued interest due within one year shown under short term borrowings; and interest charged to the Comprehensive Income and Expenditure Statement is the amount payable for the year according to the loan agreement. Gains and losses on the repurchase or early settlement of borrowing are credited and debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement in the year of repurchase/settlement. However, where repurchase has taken place as part of a restructuring of the loan portfolio that involves the modification or exchange of existing instruments, any premium or discount is respectively deducted from or added to the amortised cost of the new or modified loan and the write-down to the Comprehensive Income and Expenditure Statement is spread over the life of the loan by an adjustment to the effective interest rate. Where premiums and discounts have been charged to the Comprehensive Income and Expenditure Statement, regulations allow the impact on the General Fund Balance to be spread over future years. The Council has a policy of spreading the gain or loss over the unexpired life of the original loan. The reconciliation of amounts charged to the Comprehensive Income and Expenditure Statement to the net charge required against the General Fund Balance is managed by a transfer to or

29

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

from the Financial Instruments Adjustment Account in the Movement in Reserves Statement. Financial Assets Financial assets are classified into two types:

• Loans and receivables – assets that have fixed or determinable payments but are not quoted in an active market

• Available for sale assets – assets that have a quoted market price and/or do

not have fixed or determinable payments. Loans and receivables Loans and receivables are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument. They are initially measured at fair value and carried at their amortised cost. Annual credits to the Financing and Investment and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are based on the carrying amount of the asset multiplied by the effective rate of interest for the instrument. For most of the loans that the Council has made, this means that the amount presented in the Balance Sheet is the outstanding principal receivable, with interest receivable within one year shown under short term investments and interest credited to the Comprehensive Income and Expenditure Statement is the amount receivable for the year in the loan agreement. However, occasionally the Council may make loans to other parties (e.g. voluntary organisations) at less than market rates (soft loans). When soft loans are made, a loss is recorded in the Comprehensive Income and Expenditure Statement for the present value of the interest that will be foregone over the life of the instrument, resulting in a lower amortised cost than the outstanding principal. Interest is credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement at a marginally higher effective rate of interest than the rate receivable, with the difference serving to increase the amortised cost of the loan in the Balance Sheet. Statutory provisions require that the impact of soft loans on the General Fund Balance is the interest receivable for the financial year – the reconciliation of amounts debited and credited to the Comprehensive Income and Expenditure Statement to the net gain required against the General Fund Balance as managed by a transfer to or from the Financial Instruments Adjustment Account in the Movement in the Reserves Statement. Where assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. The impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. Any gains and losses that arise on the de-recognition of an asset are credited or debited to the Financial and Investment Income Expenditure line in the

30

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Comprehensive Income and Expenditure Statement. Available-for-Sale Assets Available-for-sale assets are recognised on the Balance Sheet when the Council becomes a party to the contractual provisions of a financial instrument and are initially measured and carried at fair value. Where the asset has fixed or determinable payments, annual credits to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement for interest receivable are based on the amortised cost of the asset multiplied by the effective rate of interest for the instrument. Where there are no fixed or determinable payments, income (e.g. dividends) is credited to the Comprehensive Income and Expenditure Statement when it becomes receivable by the Council. Assets are maintained in the Balance Sheet at fair value. Values are based on the following principles:

• Instruments with quoted market prices – the market price

• Other instruments with fixed and determinable payments – discounted cash flow analysis

• Equity shares with no quoted market prices – independent appraisal of

company valuation or most recent price at which the shares changed hands. Changes in fair value are balanced by an entry in the Available-for-Sale Reserve and the gain/loss is recognised in the Surplus or Deficit on Revaluation of Available for Sale Financial Assets. The exception is where impairment losses have been incurred – these are debited to the Financial and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any net gain or loss for the asset accumulated in the Available-for-Sale Reserve. Where assets are identified as impaired because of a likelihood arising from a past event that payments due under the contract will not be made (fixed or determinable payments) or fair value falls below cost, the asset is written down and a charge made to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. If the asset has fixed or determinable payments, the impairment loss is measured as the difference between the carrying amount and the present value of the revised future cash flows discounted at the asset’s original effective interest rate. Otherwise, the impairment loss is measured as any shortfall of fair value against the acquisition cost of the instrument (net of any principal repayment and amortisation). Any gains and losses that arise on de-recognition of the asset are credited or debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement, along with any accumulated gains or losses previously recognised in the Available-for-Sale Reserve. Where fair value cannot be measured reliably, the instrument is carried at cost (less any impairment losses). 10. Foreign Currency Translation

31

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Where the Council has entered into a transaction denominated in a foreign currency, the transaction is converted into sterling at the exchange rate applicable on the date the transaction was effective. Where material amounts in foreign currency are outstanding at the year-end, they are reconverted at the spot exchange rate at 31 March. Resulting gains or losses, if material, are recognised in the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. 11. Government Grants and Contributions Whether paid on account, by instalments or in arrears, government grants and the third party contributions and donations are recognised as due to the Council when there is reasonable assurance that:

• The Council will comply with the conditions attached to the payments and • The grants or contributions will be received.

Amounts recognised as due to the Council are not credited to the Comprehensive Income and Expenditure Statement until conditions attached to the grant or contribution have been satisfied. Conditions are stipulations that specify that the future economic benefits or service potential embodied in the asset acquired using the grant or contribution are required to be consumed by the recipient as specified, or future economic benefits or service potential must be returned to the transferor. Monies advanced as grants and contributions for which conditions have not been satisfied are carried in the Balance Sheet as creditors. When conditions are satisfied, the grant or contribution is credited to the relevant service line (attributable revenue grants and contributions) or Taxation and Non-Specific Grant Income (non ring-fenced revenue grants and all capital grants) in the Comprehensive Income and Expenditure Statement. Where capital grants are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance in the Movement in Reserves Statement. Where the grant has yet to be used to finance capital expenditure, it is posted to the Capital Grants Unapplied reserve. Where it has been applied, it is posted to the Capital Adjustment Account. Amounts in the Capital Grants Unapplied reserve are transferred to the Capital Adjustment Account once they have been applied to fund capital expenditure. Area Based Grant Area Based Grant (ABG) is a general grant allocated by central government directly to local authorities as additional revenue funding. ABG is non-ringfenced and is credited to Taxation and Non-Specific Grant Income in the Comprehensive Income and Expenditure Statement. Business Improvement Districts A Business Improvement District (BID) scheme applies across the whole of the Council. The scheme is funded by BID levy paid by non-domestic ratepayers. The Council acts as a principal under the scheme, and accounts for income received

32

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

and expenditure incurred (including contributions to the BID project) within the relevant services within the Comprehensive Income and Expenditure Statement. 12. Intangible Assets Intangible assets are assets that do not have physical substance but are identifiable and controlled by the Council (e.g. software licences). Expenditure on intangible assets is capitalised when it is expected that future economic benefits or service potential will flow from the intangible asset to the Council for a period of more than one year. Internally generated intangible assets are capitalised where it is demonstrable that the project is technically feasible and is intended to be completed and the Council will be able to generate future economic benefits or deliver service potential by being able to sell or use the asset. Expenditure is capitalised where it can be measured reliably as attributable to the asset and is restricted to that incurred during the development phase (research expenditure cannot be capitalised). Expenditure on the development of the Council’s website is not capitalised as the website is primarily intended to promote or advertise the Council’s services. Intangible assets are measured initially at cost. Amounts are only re-valued where the fair value of the assets can be determined by reference to an active market. In practice, no intangible asset held by the Council meets this criterion, and they are therefore carried at amortised cost. Intangible assets are amortised over their useful life and charged to the relevant service lines in the Comprehensive Income and Expenditure Statement and are subject to impairment reviews. Any gain or loss arising on the disposal or abandonment of an intangible asset is posted to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement. Where expenditure on intangible assets qualifies as capital expenditure for statutory purposes, amortisation, impairment losses and disposal gains and losses are not permitted to have an impact on the General Fund Balance. The gains and losses are therefore reversed out of the General Fund Balance in the Movement in Reserves Statement and posted to the Capital Adjustment Account and (for any sale proceeds greater than £10,000) the Capital Receipts Reserve. 13. Interests in Companies and other Entities Councils are required to produce Group Accounts to include services offered to Council Tax payers by organisations other than the Council itself but in which the Council has an interest. There are a number of criteria set out by which the Council must determine whether the value of the company and the Council’s interest is significant enough for Group Accounts to be produced. The Council has complied with the Code of Practice on Local Authority Accounting, and while it has identified a company over which it has joint control, it has concluded that the company does not meet the criteria that would require consolidation into the Council’s accounts. 14. Inventories and Long Term Contracts

33

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2

Inventories are included in the Balance Sheet at the lower of cost and net realisable value. The cost of inventories is assigned using either the FIFO or weighted average costing formula. Long term contracts are accounted for on the basis of charging the Surplus and Deficit on the Provision of Services with the value of works and services received under the contract during the financial year. 15. Investment Property Investment properties are those that are used solely to earn rentals and/or for capital appreciation. The definition is not met if the property is used in any way to facilitate the delivery of services or is held for sale. Investment properties are measured initially at cost and subsequently at fair value, based on the amount at which the asset could be exchanged between knowledgeable parties at arm’s-length. Properties are not depreciated but are re-valued annually according to market conditions at year-end. Gains and losses on revaluation are posted to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. The same treatment is applied to gains and losses on disposal. Rentals received in relation to investment properties are credited to the Financing and Investment Income line and result in a gain for the General Fund Balance. However, revaluation and disposal gains and losses are not permitted by statutory arrangements to have an impact on the General Fund Balance. The gains and losses are therefore reversed out of the General Fund Balance in the Movement in Reserves Statement and posted to the Capital Adjustment Account and (for any sale proceeds greater than £10,000) the Capital Receipts Reserve. 16. Jointly Controlled Operations and Jointly Controlled Assets Jointly controlled operations are activities undertaken by the Council in conjunction with other ventures that involve the use of the assets and resources of the ventures rather than the establishment of a separate entity. If and when these exist the Council recognises on its Balance Sheet the assets that it controls and the liabilities that it incurs and debits and credits the Comprehensive Income and Expenditure Statement with the expenditure it incurs and the share of income it earns from the activity of the operation. Jointly controlled assets are items of property, plant or equipment that are jointly controlled by the Council and other ventures, with the assets being used to obtain benefits for the ventures. The joint venture does not involve the establishment of a separate entity. The Council accounts for only its share of the jointly controlled assets, the liabilities and expenses that it incurs on its own behalf or jointly with others in respect of its interest in the joint venture and income that it earns from the venture. 17. Leases Leases are classified as finance leases where the terms of the lease transfer

34

S T A T E M E N T O F A C C O U N T S

2 0 1 1 / 1 2