Embed Size (px)

Citation preview

STATISTICALI2

3THE0RY0

Intr

oduc

tion

to

November 2021

Contents

1 Preliminaries 1

1.1 Samples and Populations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.3 Summarising data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.3.1 Tabular summaries of data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.3.2 Graphical summaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.3 Numerical summaries of data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.3.4 Shape . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2 Basic Probability 16

2.1 Randomness and probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.2 Proportion and probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.3 Terminologies, rules and axioms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.4 Probability tree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

2.5 Examples on how to approach a probability problem . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3 Univariate distributions 27

3.1 Random variables and distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.2 Discrete distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.2.1 Introduction to discrete distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.2.2 Properties of a discrete random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3.2.3 Distributions as models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3.3 Continuous distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.3.1 Introduction to continuous distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.3.2 Properties of a continuous random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

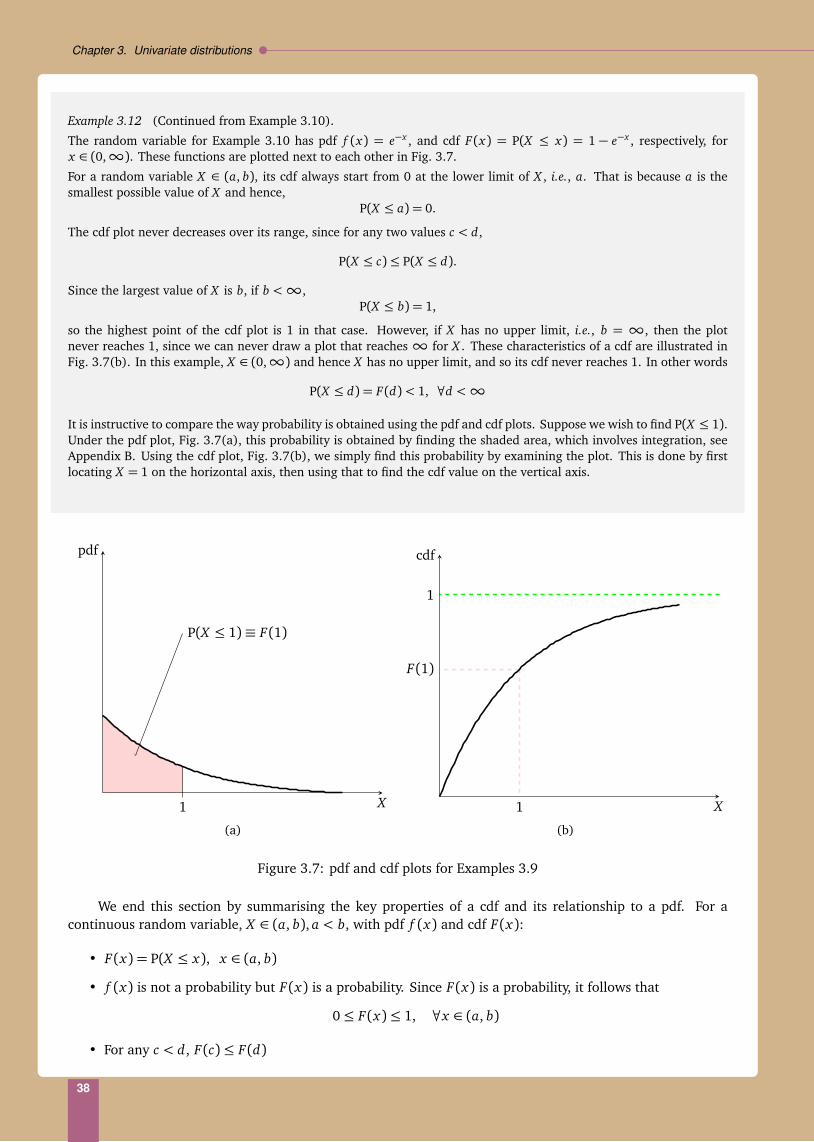

3.3.3 Cumulative distribution function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

3.3.4 A model for a continuous random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

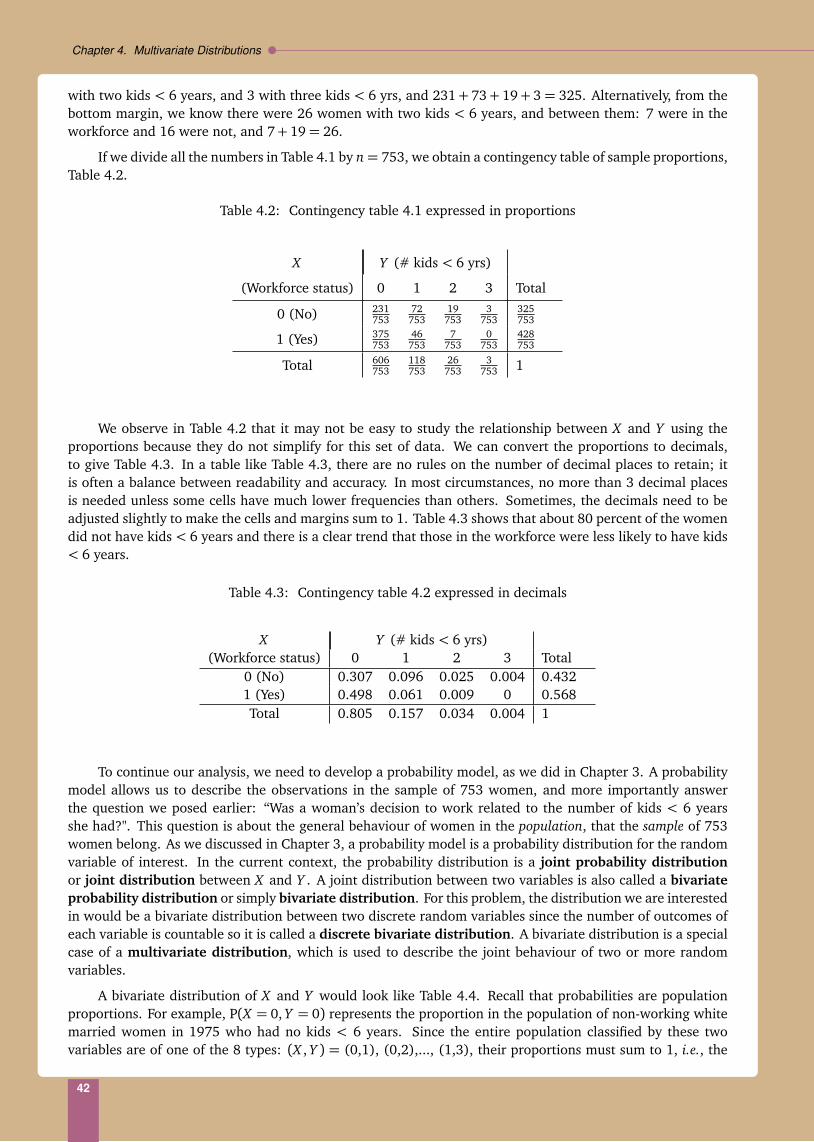

4 Multivariate Distributions 41

4.1 Discrete bivariate distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.1.1 Discrete joint distribution function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

I

Contents

4.1.2 Marginal probability distribution function . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.1.3 Conditional probability distribution function . . . . . . . . . . . . . . . . . . . . . . . . . . 46

4.1.4 Independence between discrete random variables . . . . . . . . . . . . . . . . . . . . . . . 47

4.2 Continuous bivariate distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.2.1 Marginal probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.2.2 Independence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

4.2.3 Conditional probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

5 Expectation, Variance and Covariance 57

5.1 Expectation and variance of a discrete random variable . . . . . . . . . . . . . . . . . . . . . . . . 57

5.2 Transformation of random variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5.3 Expectation and variance for a continuous random variable . . . . . . . . . . . . . . . . . . . . . . 61

5.4 Mean and variance of combinations of random variables . . . . . . . . . . . . . . . . . . . . . . . 63

6 Special Distributions 66

6.1 Bernoulli trials and binomial distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

6.2 Poisson distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.3 Exponential distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

6.4 Normal distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

7 Sampling and sampling distribution 81

7.1 Population and Sample . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

7.2 Random Sampling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

7.3 Parameter and statistic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

7.4 Sampling error . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

7.5 Sampling distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

8 Estimation 87

8.1 Maximum likelihood estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

8.1.1 Invariance property of MLE’s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

8.1.2 Non-standard conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

8.2 Evaluating estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

8.2.1 Bias . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

8.2.2 Variance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

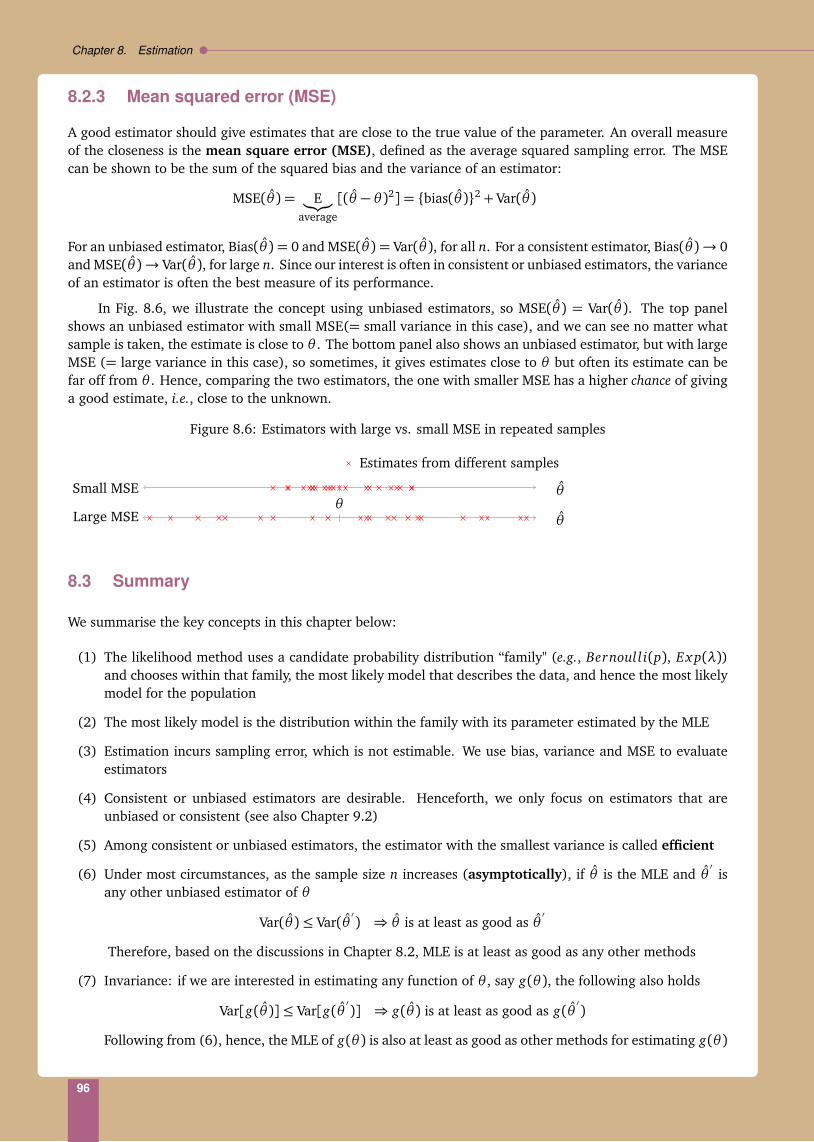

8.2.3 Mean squared error (MSE) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

8.3 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

9 Estimation 97

9.1 Large sample confidence intervals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

9.2 Large sample confidence interval for a population mean . . . . . . . . . . . . . . . . . . . . . . . . 99

II

Contents

9.3 Large sample confidence interval for a population proportion . . . . . . . . . . . . . . . . . . . . 101

9.4 Confidence interval for a normal population mean . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

10 Hypothesis Testing 104

10.1 Large sample tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

10.2 Null and alternative hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

10.3 p-value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

10.4 Type I error . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

10.5 Statistical significance and significance tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

10.6 One-sided vs. two-sided test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

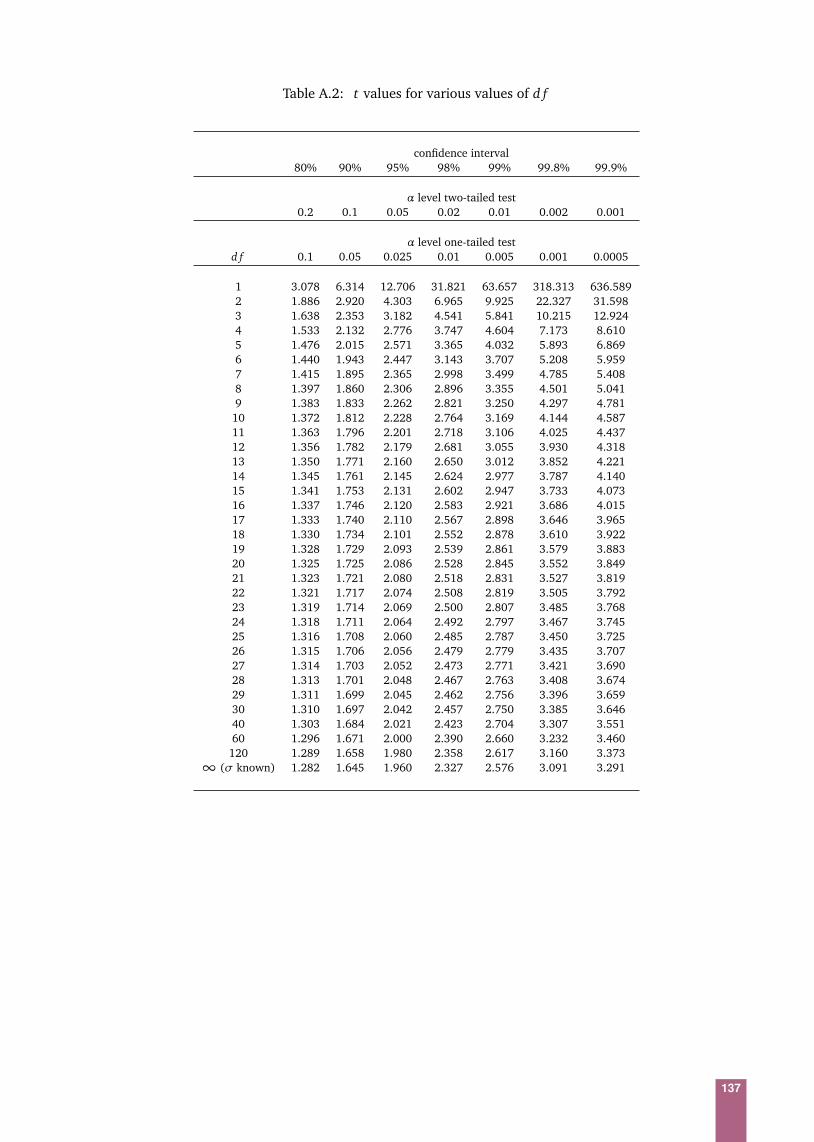

10.7 Test statistic and critical values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

10.8 Test for a normal population mean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

10.9 Other problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

10.10Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

11 Association between Quantitative Variables 116

11.1 Scatter plot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

11.2 Correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

11.3 Simple linear regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

11.3.1 Maximum likelihood and least squares solution . . . . . . . . . . . . . . . . . . . . . . . . 124

11.3.2 Residual plot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

11.3.3 Hypothesis testing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

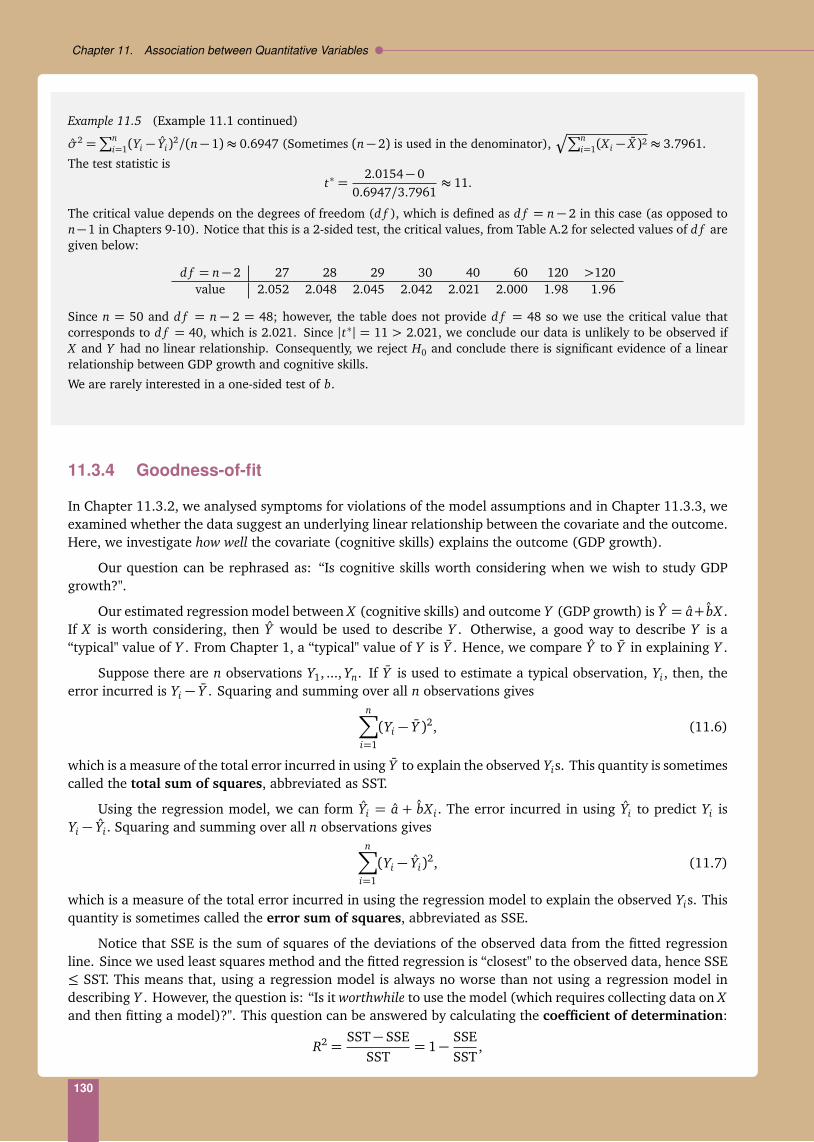

11.3.4 Goodness-of-fit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

11.3.5 Prediction using a regression model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Appendix A Statistical Tables 135

Appendix B Basic Algebra and Calculus 138

B.1 Factorials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

B.2 Significant digits & decimal places . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

B.3 The summation sign Σ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

B.4 The product sign Π . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

B.5 Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

B.6 Functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

B.7 Limits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

B.8 Derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

B.9 Integration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

Appendix C Summary of Statistical Formulae 146

C.1 Basic probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

III

Contents

C.2 Discrete and continuous distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

C.3 Expectation and variance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

C.4 Properties of some common distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

C.5 Other distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

C.6 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

C.7 Hypothesis testing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

C.8 Simple linear regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

Appendix D Notations and Symbols 154

D.1 Notations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

D.2 Greek Alphabets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 156

IV

1Preliminaries

Statistics is about solving practical problems by collecting and using information, data. The aim of this courseis to study basic statistical methods for analysing data. There are two main goals in any statistical analysis.The first goal is to make sense of the data; the second goal is to generalise what is observed in the data towhat have not observed, in a larger context. A statistical analysis takes several steps in reaching these goals.The first step is to have an informal exploration of the data. This is done by summarising the data numerically,or using figures, graphs and tables. This step is not only useful to give us a general impression of the data, italso provides guidance of what statistical methods to be used. Data invariably exhibit patterns that are hardto describe precisely. Probability theory is an important tool that helps to explain the inherent variability indata. The core ingredient to reaching the two goals of a statistical analysis is a probability model (Sometimesalso referred to as a statistical model). A probability model links the data to the general context; it explainsthe observed data and guides us in our assessment of the unobserved. A probability model also tells us theappropriate statistical methods for analysing the data.

We begin this set of notes in Chapter 1 with an introduction of data and some common methods forsummarising data. Chapter 2 reviews basic probability rules and axioms. Chapters 3 and 4 give motivation forrelating data to probability models. Chapter 5 discusses methods of summarising information in a probabilitymodel. Some commonly used probability models are given in Chapter 6. In Chapters 8-10, we learn how tochoose a probability model for a particular set of data and analyse data under the chosen model. The notesend with Chapter 11 on the topic of modeling relationships between data.

1.1 Samples and Populations

Many questions about a population, defined as all units of interest, are answered by obtaining informationfrom a subset, called a sample, of the population.a When we have a set of data, it is often assumed that thedata come from a sample selected from a population. Hence, in the future, we will use the terms sampleand data interchangeably. Earlier, we talked about the wish to apply what we learned in the data to thegeneral context. By that, we mean to use information from a sample, i.e., the data, to say something aboutthe population, i.e., the general context.

aIn general, there are two kinds of population – finite and infinite. However, as long as (1) the sample size, n, and the populationsize, N are such that n/N < 0.05 (i.e., no more than 5% of the population is sampled) or (2) the population size N so big to beconsidered infinite or (3) sampling with replacement, then there is no difference in the statistical analyses between a finite and aninfinite population. Henceforth, we assume one or more of these conditions are satisfied so we do not distinguish between the twotypes of population.

1

Chapter 1. Preliminaries

Example 1.1

Suppose we wish to find out whether a new diet can reduce weight. To answer this question, it would be impossibleto test the diet on every individual in the population. Rather, it would make more sense to test the diet on a sample ofindividuals selected from the population.

In one such study (Foster et al., New England Journal of Medicine, 2003, 2082-90), 63 individuals were selected with30 randomly given the new diet and 33 kept at the conventional diet, their average weight loss (as a percent of bodyweight) measured at different times after intervention are as follows:

Weight loss Conventional diet New dietAfter 3 months -2.7% -6.8%After 6 months -3.2% -7%

After 12 months -2.5% -4.4%

In this study, the sample consists of information from 63 individuals; these data were used to determine whether thenew diet is better than the conventional diet in reducing weight of all individuals in the population.

Example 1.2

In 1950, two British researchers, Richard Doll (1912-2005) and Austin Bradford Hill (1897-1991), carried out a studyto examine the association between cigarette smoking and the development of lung cancer. They used data from 1298men (649 lung cancer patients and 649 healthy individuals) and obtained each man’s smoking history. The data aregiven below:

Lung Cancer Patients Healthy IndividualsSmokers 647 622

Non-smokers 2 27

In this study, the interest is in the relationship between smoking and lung cancer in the male population. The data comefrom a sample of 1298 men. The goal is to use the observed data to answer questions such as: Is lung cancer associatedwith cigarette smoking in the population?

1.2 Data

Data appear in many forms. In Examples 1.1 and 1.2, the data have been processed and presented in waysfor ease of analyses and interpretation. These are examples of summary statistics or more simply statistics.Raw data, on the other hand, refer to information as they are collected, without any processing. Raw data arecollections of observations. On each observation, there may be information on a number of characteristicsthat are collected. Each characteristic is called a variable.

Consider the following dataset obtained from records in a group of student.

Example 1.3

Student Status Gender Age School Course Course CumulativeGPA Grade GPA

1 Singaporean Male 23 SOE 3.7 A- 2.992 Foreign Female 23 SIS 3.7 A- 3.92

2

1.2. Data

3 Singaporean Female 19 SOA 2.7 B- 3.334 Singaporean Female 20 SOA 4.0 A 3.155 Singaporean Female 36 SOB 4.3 A+ 3.666 Foreign Male 27 SOB 3.3 B+ 2.677 Singaporean Female 23 SOS 3.3 B+ 2.988 Foreign Male 25 SOB 2.3 C+ 2.359 Singaporean Male 22 SOB 3.7 A- 3.23

10 Singaporean Female 19 SOE 3.0 B 3.7211 Foreign Male 19 SOB 3.3 B+ 3.7712 Singaporean Male 19 SOA 1.7 C- 2.1713 Foreign Female 18 SOB 4.0 A 3.4214 Singaporean Female 19 SOS 1.7 C- 2.1715 Singaporean Female 18 SOS 4.0 A 3.4216 Singaporean Female 19 SOL 1.7 C- 2.1717 Singaporean Female 18 SOL 4.0 A 3.42

In the dataset in Example 1.3, there are 17 observations. For each observation, there are seven variables(characteristics) recorded (excluding “Student", which is a dummy identifier). When working with a set ofdata, we often use lower case letter n to represent the number of observations in a set of data. Hence, inExample 1.3, n= 17. Furthermore, capital letters such X , Y, Z , etc., can be used to represent variables. If X isused to denote a particular variable, then a set of n observations of X is written as X1, ..., Xn. For example, inExample 1.3, if we use X to represent gender, then X1 = Male, X2 = Female,..., X17 = Female.

A variable can either be quantitative or qualitative. A quantitative variable is a variable that is measuredon a numeric or quantitative scale, e.g., age, weight, height, salary, number of cars in a family, number ofcustomers arriving at a restaurant. A qualitative variable is a variable that is not quantitative, e.g., gender,race, color. A quantitative variable can further be subdivided into a discrete or continuous variable. Adiscrete variable can assume only a countable number of values, e.g., number of cars in a family, number ofcustomers arriving at a restaurant. A continuous variable can assume any value in a range, e.g., age, weightand height (assuming not rounded to nearest year, kg or cm). Sometimes, a variable such as income, whichhas a sufficiently large number of possible countable values, can also be considered continuous. A qualitativevariable is always discrete and sometimes also called a categorical variable.

Example 1.4 (Continued from Example 1.3)

The following is a summary of the characteristics of the seven variables:

Variable Type Range or Possible ValuesStatus Qualitative Singaporean, ForeignerGender Qualitative Male, Female

Age Quantitative (Continuous) 18− 100School Qualitative SOE, SOB, SOA, SIS, SOS, SOL

Course Grade Qualitative A,B, C, ...Course GPA Quantitative (Discrete) 0, 1.0, 1.5,...,4.3

Cumulative GPA Quantitative (Continuous) 0− 4.3

In this example, age is considered continuous because age technically can assume any value in a range.

Sometimes, especially in social sciences, variables are also classified by their scale of measurement.

3

Chapter 1. Preliminaries

There are four scales of measurement: nominal, ordinal, interval and ratio. The scale of measurementdetermines the type of analysis that is appropriate for a variable.

Gender (Female, Male) and race (Chinese, Malay, Indian, Caucasian) are examples of variables that aremeasured on a nominal scale. On a nominal scale, no ordering is implied between different values of thescale, e.g., there is no natural ordering between Male and Female. Occasionally, a nominal scale variable maybe recoded in numeric values: For instance, gender may be coded as Female=1, Male=2. Even so, there isstill no ordering because “1" and “2" are just artificial codes. Regardless of whether a nominal scale has beenrecoded as numeric or not, arithmetic operations, e.g., addition, subtraction, multiplication, division, etc., areinappropriate.

An ordinal scale is a set of ordered values. However, the distance between values is meaningless. Forexample, if we are interested in the service of a restaurant and service is rated as: Very Poor, Poor, Average,Good, Very Good, then service is measured on an ordinal scale. We can assign numerical values to an ordinalscale, e.g., 1 for "Very Good" 2 for "Good", etc., but the difference between a score of 1 and 2 may not meanthe same thing as the difference between a score of 2 and 3.

Temperature is an example of a variable measured on interval scale. Interval scales are numerical scalesin which intervals have the same interpretation throughout, e.g., the difference between 20 degrees and 40degrees represents the same temperature difference as the difference between 45 degrees and 65 degrees.Addition and subtraction of interval scales have meaning but there is no meaning to the ratio of two values,e.g., it does not make sense to say that 40 degrees is twice as hot as 20 degrees. Interval scale values do nothave a true zero point, e.g., 0 degree is an artificial number on the temperature scale.

A ratio scale is an interval scale with a true zero point and in which an interval of a particular length hasthe same interpretation on the entire scale. Weight is a ratio scale. Therefore it is meaningful to say that a200 pound person weighs twice as much as a 100 pound person.

The characteristics of the four scales can be summarised in Table 1.1.

Table 1.1: Characteristics of Four Scales

Scale Characteristics Example 1.3Nominal Can only say whether Status, Gender, School

observations are different

Ordinal Observations can be Course Graderanked + all characteristics

of a nominal scale

Interval Differences between observations Course GPA, Cumulative GPAhave meanings + all characteristics

of an ordinal scale

Ratio Ratios between observations Agehave meanings + all characteristics

of an interval scale

Example 1.5 (Continued from Example 1.3)Gender is measured in nominal scale. For example, Student 1 is Male and Student 2 is Female. Therefore:

a. The gender of Student 1 and Student 2 are different.b. (Male > Female) and (Female > Male) are both meaningless because being Male does not imply “better" (or

“worse") than being Female.

4

1.3. Summarising data

c. (Male − Female) is meaningless

d. (Male/Female) is meaningless

Example 1.6 (Continued from Example 1.3)

Course grade is measured in ordinal scale. For example, Student 1’s course grade is A- and Student 3’s course grade isB-. Therefore:

a. The grades of Student 1 and 3 are different

b. The grade of Student 1 is higher than Student 3

c. (“A-" − “B-") is meaningless

d. (“A-"/“B-") is meaningless

Example 1.7 (Continued from Example 1.3)

Cumulative GPA is measured in interval scale. For example, Student 11’s cumulative GPA is 3.77 and Student 6’scumulative is 2.67. Therefore:

a. The cumulative GPA of Student 11 and 6 are different

b. The cumulative GPA of Student 11 is higher than Student 6

c. The cumulative GPA of Student 11 is 1.1 higher than Student 6 (3.77−2.67=1.1)

d. (3.77/2.67=1.41) is meaningless because Student 11 is not 41% better than Student 6

Example 1.8 (Continued from Example 1.3)

A ratio scale has all the characteristics of the other three scales: age is a ratio scale, Student 5’s age is 36 and student13’s age is 18. Therefore:

a. The ages of Student 5 and 13 are different (36 6= 18)

b. Student 5 is older than Student 13 (36>18)

c. Student 5 is 18 years older (36-18=18)

d. Student 5 is twice as old as Student 13 (36/18=2)

1.3 Summarising data

A key step in a statistical analysis is to summarise the available data. Examples 1.1 and 1.2 give two examplesof how data can be summarised. There are many ways of summarising data, and which method to use dependson many factors, that include, the number of observations, the type of data (type of variable), purpose of thestudy, etc.. In general, there are three ways of summarising data: tabular, graphical and numerical summaries.Tabular and graphical summaries of data are useful to give a quick overall impression of the data. On theother hand, numerical summaries are useful for analysis purposes.

5

Chapter 1. Preliminaries

1.3.1 Tabular summaries of data

A useful tabular method is a table of the frequency distribution of the data. A frequency distribution simplygives the number of observations that fall within each of a number of categories or intervals of a variable.

Example 1.9

A university offers six subject majors: Finance (F), Marketing (M), Accountancy (A), Economics (E), Social Sciences(S) and Information systems (I). Suppose we are interested in students’ choice of majors, and a sample of 80 studentsare approached and their majors recorded. Then the data may look like: F, F, M, S, E, E, S, S, S, I, F, F, .... It may bedifficult to interpret the (raw) data as they are recorded. However, the frequency distribution of the subject majors canbe represented in a table, as follows:

Major n percentFinance 15 18.75%

Marketing 26 32.5%Accountancy 14 17.5%Economics 15 18.75%

Social Sciences 3 3.75%Information Systems 7 8.75%

Total 80 100%

The table tells us quickly that the highest number of students take Marketing, followed by Finance and Economics. Inaddition, Social Sciences is chosen by the smallest number of students as a major.

Example 1.10Suppose we have data on 50 students’ final score in a subject:50 50 50 51 52 52 53 53 54 54 60 60 60 62 65 65 65 68 68 70 70 70 70 71 7174 74 74 74 80 80 81 81 81 83 83 83 86 86 87 87 88 88 90 91 91 91 94 95 95The frequency distribution would look something like this:

Final score n percent50 3 6%51 1 2%52 2 4%53 2 4%54 2 4%60 3 6%62 1 2%65 3 6%68 2 4%70 4 8%71 2 4%74 4 8%80 2 4%81 3 6%83 3 6%86 2 4%87 2 4%88 2 4%90 1 2%91 3 6%94 1 2%95 2 4%

Total 50 100%

6

1.3. Summarising data

This frequency distribution table is not that useful as it is not too different from the raw data. One way to solve thisproblem is to group the raw data into intervals. For example, the frequency distribution can be presented in intervals of10, as follows:

Final score n percent50-59 10 20%60-69 9 18%70-79 10 20%80-89 14 28%

90-100 7 14%Total 50 100%

A frequency distribution table is useful if there are not more than, say 10 groups. Categorical data can also be groupedin the manner like this example as long as there are only a few categories or if some of the categories can naturally begrouped together.

1.3.2 Graphical summaries

If a variable is categorical (qualitative), then one way to summarise the data is to use a pie chart.

Example 1.11 (Continued from Example 1.9)In a pie chart, the size of each “slice" of the pie is proportional to the frequency of the corresponding category and thesum of all the slices give the pie (Fig. 1.1).

Figure 1.1: Pie chart of data in Example 1.9

Finance

Marketing

Accountancy

Economics

Social Sciences

Information Systems

Alternatively, the same data can be summarised in a bar graph.

Example 1.12 (Continued from Example 1.9)

In a bar graph, the height of each bar is proportional to the frequency of the corresponding category (Fig. 1.2).

7

Chapter 1. Preliminaries

Figure 1.2: Bar graph of data in Example 1.9

Finance Marketing Accountancy Economics Social Sciences Information Systems

05

1015

2025

The bars in a bar graph can appear horizontally or vertically.

For a quantitative (continuous or discrete) variable, a histogram can be used.

Example 1.13

The following data were collected by the University of Michigan Panel Study of Income Dynamics. The data come fromn= 753 white married women in the US:

Woman Workforce status Hrs worked #kids Age Education Hourly wage Husband’s Experience(1=Yes, 0=No) < 6 yrs (yrs) rate wage rate (yrs)

1 1 1610 1 32 12 3.3540 4.0288 142 1 1656 0 30 12 1.3889 8.4416 53 1 1980 1 35 12 4.5455 3.5807 154 1 456 0 34 12 1.0965 3.5417 65 1 1568 1 31 14 4.5918 10.0000 76 1 2032 0 54 12 4.7421 6.7106 337 1 1440 0 37 16 8.3333 3.4277 118 1 1020 0 54 12 7.8431 2.5485 35...

......

......

......

......

750 0 0 2 31 12 0.0000 4.8638 14751 0 0 0 43 12 0.0000 1.0898 4752 0 0 0 60 12 0.0000 12.4400 15753 0 0 0 39 9 0.0000 6.0897 12

In this data set, there are eight variables. Here we focus on the 423 women who were in the workforce during 1975.We use a histogram to summarise the hourly wage rate for the 423 women, see Fig 1.3. The histogram is made upof a number of bins or intervals. The height of each bin is proportional to the frequency of observations with valuesof the variable of interest that falls within that interval. The width of an interval is called the bin size or bin width.In this example, the bins are defined by 0-2, 2-4, 4-6, etc., hence the bin size is 2. From Fig 1.3, we observe that theinterval with the highest frequency is the bin 2-4 (dollars) and most of the women have average wage below 10 dollarsan hour (Recall this data set come from 1975 and so 10 dollars is not that low). This example shows how a histogramcan effectively summarise a large amount of data.

8

1.3. Summarising data

Figure 1.3: Histogram of data in Example 1.13

Wage

Fre

quen

cy

0

50

100

150

200

0 5 10 15 20 25

Example 1.14 (Continued from Example 1.13)

The shape of the histogram changes depending on how the data are grouped. Fig. 1.4 shows student final scores groupedin intervals of 0-5, 5-10, etc. (bin size=5). If instead of using a bin size of 5, the data are grouped in bin size of 10, thenthe histogram becomes Fig 1.5, which looks very different from Fig 1.4 even though the data have not changed. This isa disadvantage of the histogram.

A histogram is not suitable for qualitative (categorical) variables. For categorical variables, a bar graph or a pie chartshould be used instead.

Figure 1.4: Histogram of data in Example 1.10 (bin size=5)

Final score

Fre

quen

cy

50 60 70 80 90 100

02

46

810

1.3.3 Numerical summaries of data

Graphical and tabular summaries are useful for giving a first impression of the data. Numerical summariesprovide alternative ways for summarising information.

9

Chapter 1. Preliminaries

Figure 1.5: Histogram of data in Example 1.10 (bin size=10)

Final score

Fre

quen

cy

50 60 70 80 90 100

02

46

810

12

Measures of location

In Statistics, location, central tendency or average, means a typical value of n observations of a variable.There are many measures of location; three popularly used measures are:

(a) arithmetic mean or sometimes simply called the sample mean – For n observations of X : X1, ..., Xn,the sample mean, is written as X and is calculated as

X =X1 + X2 + ...+ Xn

n=

1n

n∑

i=1

X i .

(b) Sample median – is the “middle" observation when the data are ranked from lowest to highest. For nobservations:

1. Order the observations, call them X(1) < X(2) < ...< X(n−1) < X(n).

2. If n is odd, then the sample median is simply the middle value. If n is even, then the sample medianis the average of the two middle values.

(c) Sample mode – The most frequently observed value in n observations of a variable.

The sample mean and sample median are only suitable for numerical data whereas the mode can be used fornumerical or categorical data.

Example 1.15

Consider the following data:

1,1,4,2,5,2,2,3,3,4.

The sample mean is:

X =

∑

X i

n=

1+ 1+ 4+ ...+ 3+ 410

= 2.7.

For the sample median, first order the data:

1,1,2,2, 2,3 ,3,4,4,5;

since n= 10, which is even, the sample median is the average of the two middle numbers:

Sample median=X(5) + X(6)

2=

2+ 32= 2.5

10

1.3. Summarising data

The most frequently observed value in the data is 2. Therefore, the sample mode is 2.

The sample mean, sample median, and sample mode are all similar in this example, but there are exceptions which willbe illustrated in the next example.

Example 1.16

Consider the dataset:

1,2,2,2,2,3,3,4,4,5.

This dataset is the same as the previous example except that one of observations with value 1 has been replaced by anobservation with a value of 2.

The sample mean becomes:

X =1+ 2+ 2+ 2+ 2+ ...+ 5

10= 2.8.

For the sample median, since n= 10, which is even, the sample median is the average of the two middle numbers:

1,2,2,2, 2,3 ,3,4,4,5.

Sample median=X(5) + X(6)

2=

2+ 32= 2.5

The most frequently observed value in the dataset is again 2. Therefore, the sample mode is 2.

In this example, only the sample mean is different from that in the last example whereas the sample mode and medianare still the same, even though the two datasets are different. This example illustrates the fact that the sample meanuses the value of every observation to form an estimate of the average, whereas the sample median uses only the twomiddle values and the sample mode uses only the most frequently observed value. Therefore, the mean uses the mostinformation from the dataset which is why it is usually the preferred method for obtaining an average of a set of data.Some exceptions are given below.

Example 1.17

Add to the dataset in the previous example an extra observation with the value 50. The dataset then becomes:

1,1,2,2,2,3,3,4,4,5,50.

The dataset now has 11 observations.

The sample mean becomes:

X =1+ 1+ 2+ ...+ 5+ 50

11= 7.7

Since n= 11, which is odd, the sample median is the middle number of the list:

1,1,2,2,2, 3 ,3,4,4,5,50.

Since the middle number is 3, the sample median is 3.

The most frequently observed value is still 2. Hence, the sample mode is 2.

In this example, the sample mode and median have not changed that much from the previous example whereas thesample mean has changed a lot because of the addition of a single value of 50 to the data. In this example, the value of50 is extremely large compared to the rest of the data. Such an observation is called an outlier, defined as observationsthat are unusual compared to the rest of the observations in a dataset. Outliers must be handled with care but themethods for handling outliers are beyond the scope in this course. This example illustrates when there are outliers, thesample mean is not an approximate measure of average.

11

Chapter 1. Preliminaries

Table 1.2: Summary of the uses of the mean, median and mode

Measure UseSample mean quantitative data with no

extreme values (outliers)

Sample median quantitative data if thereare extreme values (outliers)

Sample mode qualitative data

Example 1.18

Consider now,

1,1,2,2,2,3,3,4,4,5,> 5.

X cannot be calculated because it is not known by how much the last number is bigger than 5 . Such an observation iscalled censored. Censored data occupy an important place in statistics but are beyond the scope of this course.

The sample median and mode can still be calculated in this example with sample median=3 and sample mode=2.

Measures of spread (or dispersion, or variation)

Example 1.19

Consider the following two sets of data:

Dataset 1:-9,2,3,3,3,4,15

Dataset 2: 3,3,3,3,3,3,3

Clearly these two datasets are very different. However, for both datasets, Sample mean= sample median= samplemode=3. Using these summaries does not allow us to distinguish between the two datasets. Therefore, while averagesare useful, we also need other types of summaries to describe a set of data.

A second way of describing n observations of a variable is a measure of spread. Spread describes how thevalue of the variable changes over the n observations. As with measures of location, there are many measuresof spread. A few measures are given below:

(a) Sample range – For a numerical variable, one of the simplest measure of spread is the sample range,which is the difference between the lowest and the highest value. Suppose we have n observations ofa variable X , and X(1) < X(2) < ... < X(n−1) < X(n) are their ordered values, the sample range is simplyX(n)− X(1). The sample range is always a non-negative value. A large value of the range is indicative ofa large spread. A range of zero means all observations in the sample are identical.

(b) Sample variance (s2) – measures the average distance between observations and the mean, X :

s2 =

∑

(X i − X )2

n− 1; s =

p

s2.

If we take the (positive) square root of the sample variance, we obtain the sample standard deviation(s)s. The sample variance and sample standard deviation are exchangeable measures of spread, in the sense

12

1.3. Summarising data

that they tell us the same information about the spread of a variable, for a given set of data. For any data,

s and s2 are non-negative numbers. Sometimes, the alternative formula s2 =∑

(X i−X )2

n is used. The twoformulae give similar results unless n is very small. The two formulae can be used interchangeably. Ifs = 0 (s2 = 0), then all observations are identical. If s > 0 (s2 > 0), then at least one of the observationsmust be different from the rest. The higher the value of s or s2, the higher the spread in the dataset, i.e.,the values of the dataset are more different.

(c) Interquartile range (IQR) – The range can be adversely affected by extreme values. An alternative isthe IQR, which is defined as

IQR= upper quartile - lower quartile

where the lower quartile (also called 25-th percentile or 1-st quartile, see section on percentilesbelow) is the value such that one quarter of the observed values is less than it and the upper quartile(also called 75-th percentile or 3-rd quartile) is the value such that three quarters of the observedvalues are less than it. The calculations of the lower and upper quartiles are similar to that of themedian.The lower quartile is calculated as followsb:1. Order the observations, call them X(1) < X(2) < ...< X(n−1) < X(n)2. Calculate 1

4(n+ 1), if it is an integer then the lower quartile is X( 14 (n+1)); if it is not an integer, the

lower quartile isX(n0)+X(n1)

2 where n0, n1 are the integers that sandwich 14(n+ 1)

The upper quartile is calculated as follows:1. Order the observations, call them X(1) < X(2) < ...< X(n−1) < X(n)2. Calculate 3

4(n+ 1), if it is an integer then the upper quartile is X( 34 (n+1)); if it is not an integer, the

upper quartile isX(n0)+X(n1)

2 where n0, n1 are the integers that sandwich 34(n+ 1)

Like the range, the IQR is also non-negative. A larger value of IQR is indicative of higher spread. WhenIQR= 0, it means all observations between the first and third quartiles have the same value. However,in this case, it says nothing about the observations below the first quartile and those above the thirdquartile, c.f., the sample range.

(d) Coefficient of Variation (CV)–CV = 100

sX

%.

A CV need not be positive because X can be negative. A CV is useful for comparing the spread of twovariables that are measured on different magnitudes. A CV with a higher absolute value is indicative ofhigher spread.

Example 1.20 (Continued from Example 1.19)

Dataset 1:

X =

∑

X i

n=−9+ 2+ ...+ 15

7= 3

⇒ s2 =

∑

(X i − X )2

n− 1=(−9− 3)2 + (2− 3)2 + ...+ (15− 3)2

7− 1= 48.333.

n= 7,14(n+ 1) =

14(8) = 2,

34(n+ 1) =

34(8) = 6,

Since these are integers, therefore,

lower quartile= X(2) = 2, upper quartile= X(6) = 4,

bThe method given here is one of at least nine different methods of calculating the upper and lower quartiles, all of which areequally valid. In practice, we will most likely compute quartiles using one of the commercially available programs so depending onthe program we use, the answer may be different. Therefore, it is more important to understand the concept of a quartile and knowits approximate value rather than trying to find its “exact" value.

13

Chapter 1. Preliminaries

andIQR= 4− 2= 2.

Range= 15− (−9) = 24.

For CV, we need to first calculate:X = 3, s =

p

48.333= 6.95,

therefore,

CV =100× 6.95

3%= 231.7%.

Dataset 2:

X =3+ 3+ ...+ 3

7= 3

⇒ s2 =

∑

(X i − X )2

n− 1=(3− 3)2 + (3− 3)2 + ...+ (3− 3)2

7− 1= 0.

Hence, the difference in the two datasets is revealed in the sample variances. Sometimes, the standard deviation ispreferred because it is in the same scale as the mean. Obviously, knowing the sample variance implies knowing thesample standard deviation and vice versa.

Since all observations are the same, clearly the first and third quartile are identical. Therefore, IQR=0.

Range= 3− 3= 0.

For CV:X = 3, s = 0,

Therefore,

CV =100× 0

3%= 0%.

Using any of the four measures of spread, we arrive at the same conclusion that there is more variation amongobservations in Dataset 1 than in Dataset 2.

Percentiles

A percentile is the ranking of a value in the dataset as compared to other values. The X-percentile of a datasetis the value that is bigger than X% of the values in the dataset. For example, if a student received a score of560 on the SAT verbal test and her score is at the 62-th percentile, then 62% of the scores are below her scoreand 38% are above her score. It is important to distinguish the difference between a percent and a percentile.A percent has a value between 0 and 100, but a percentile’s value can be anything, depending on the context.

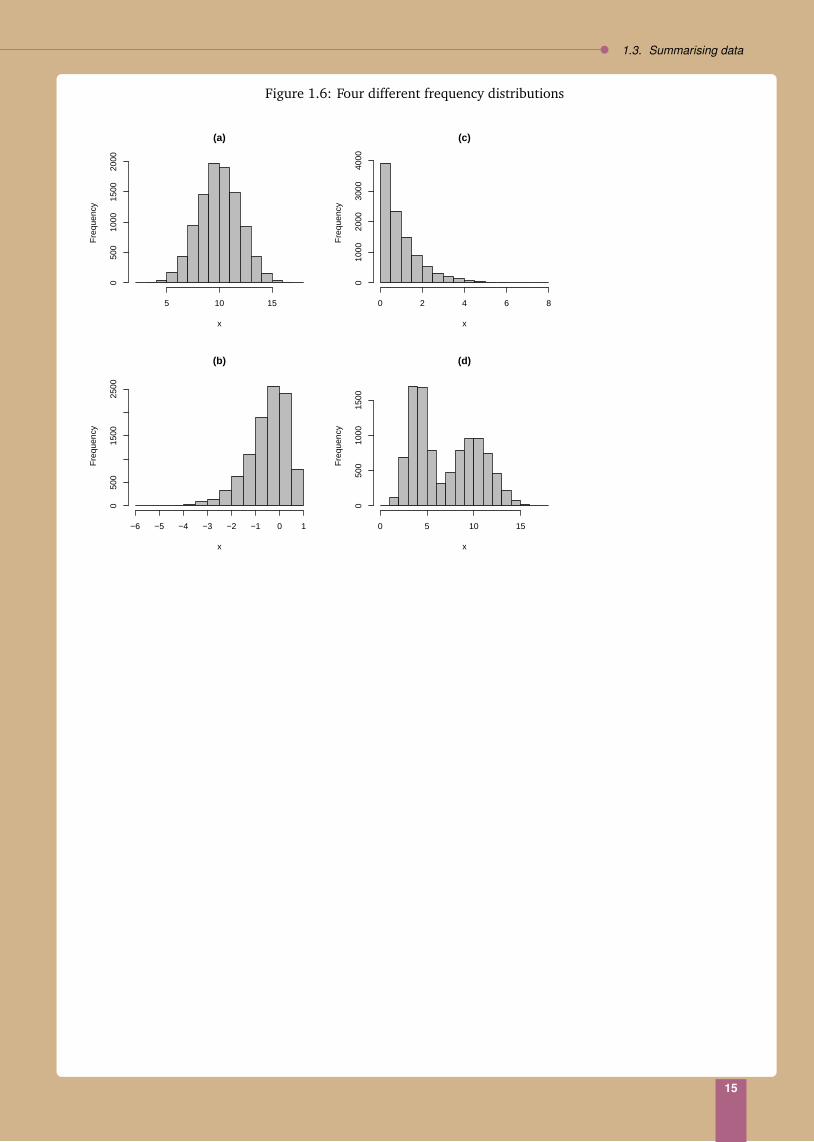

1.3.4 Shape

The histograms in Fig. 1.6 show the frequency distributions for four sets of data. We notice that for Fig. 1.6(a)-(c), there is only one “peak" or “hump". A frequency distribution that displays one peak is called a unimodaldistribution (as opposed to those with more than one peak [Fig. 1.6(d)], which are called multi-modal). Afrequency distribution that is asymmetric [Fig. 1.6 (b), (c)] is called skewed; otherwise, it is called symmetric[Fig. 1.6 (a)]. For a unimodal distribution that is symmetric, Sample mean ≈ sample mode ≈ sample median.

14

1.3. Summarising data

Figure 1.6: Four different frequency distributions

(a)

x

Fre

quen

cy

5 10 15

050

010

0015

0020

00

(b)

x

Fre

quen

cy

−6 −5 −4 −3 −2 −1 0 1

050

015

0025

00

(c)

x

Fre

quen

cy

0 2 4 6 8

010

0020

0030

0040

00(d)

x

Fre

quen

cy

0 5 10 15

050

010

0015

00

15

2Basic Probability

2.1 Randomness and probability

A pandemic is hitting a region, two different drugs, A and B, are dispatched to the region. One hundredpatients are given A and another 100 patients are given B. Out of those given A, 60 recovered. Of thosegiven B, 70 recovered. A mother is taking her affected child for treatment. Which treatment should she askfor her child? The mother in this example is one of the many situations in life when we have to deal withuncertainties. In those situations, the concept of probabilitya can be very useful in helping us to form ourdecisions.

Let us take a closer look at the pandemic example. Consider the data from those who have been treatedwith A. If we use 1 for “recovered" and 0 for “not recovered", the data would look like the following:

1 1 1 0 0 0 1 1 1 0 0 1 0 1 0 0 1 1 1 11 1 1 0 1 1 0 0 1 1 1 1 0 1 1 0 0 1 1 00 1 0 1 1 0 1 0 0 1 1 1 1 0 1 0 1 1 1 01 0 1 0 1 1 0 0 0 0 1 1 1 0 1 0 0 0 1 11 0 1 1 1 1 0 0 1 1 1 1 0 1 0 0 1 0 1 1

In total, there are 60 1’s (recovered) and 40 0’s (not recovered). We may observe that the outcome of patientsvary, some are successfully treated (1) while some are not (0). Hence, if the treatment is to be given to thechild, we could not say with certainty what the outcome would be: whether the child would get 1 (recovered),or 0 (not recovered). Similarly, for patients given B, there are 70 1’s (recovered) and 30 0’s (not recovered) thatappear in some haphazard order. We call these phenomena, that the 1’s and 0’s appear in some unpredictablemanner, random. A concept that is useful for explaining randomness is probability. This concept can beillustrated through the following example:

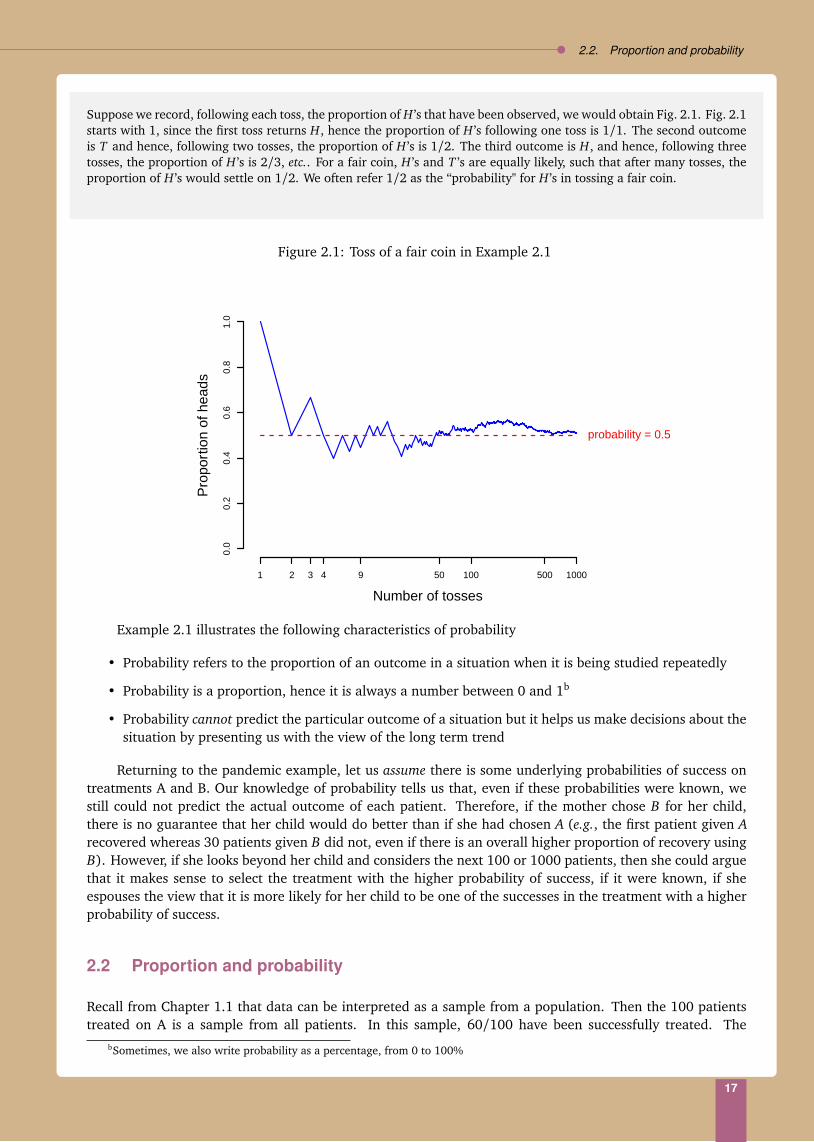

Example 2.1

Assume we have a fair coin, such that it is equally likely we would observe heads (H) or tails (T) when the coin is tossed.If we tossed this fair coin, we might observe the following outcomes in the respective tosses:

Toss 1 2 3 4 5 6 7 8 9 · · ·Outcome H T H T T H T H T · · ·

aSometimes also loosely referred to as chance

16

2.2. Proportion and probability

Suppose we record, following each toss, the proportion of H ’s that have been observed, we would obtain Fig. 2.1. Fig. 2.1starts with 1, since the first toss returns H, hence the proportion of H ’s following one toss is 1/1. The second outcomeis T and hence, following two tosses, the proportion of H ’s is 1/2. The third outcome is H, and hence, following threetosses, the proportion of H ’s is 2/3, etc.. For a fair coin, H ’s and T ’s are equally likely, such that after many tosses, theproportion of H ’s would settle on 1/2. We often refer 1/2 as the “probability" for H ’s in tossing a fair coin.

Figure 2.1: Toss of a fair coin in Example 2.1

Pro

port

ion

of h

eads

0.0

0.2

0.4

0.6

0.8

1.0

1 2 3 4 9 50 100 500 1000

probability = 0.5

Number of tosses

Example 2.1 illustrates the following characteristics of probability

• Probability refers to the proportion of an outcome in a situation when it is being studied repeatedly

• Probability is a proportion, hence it is always a number between 0 and 1b

• Probability cannot predict the particular outcome of a situation but it helps us make decisions about thesituation by presenting us with the view of the long term trend

Returning to the pandemic example, let us assume there is some underlying probabilities of success ontreatments A and B. Our knowledge of probability tells us that, even if these probabilities were known, westill could not predict the actual outcome of each patient. Therefore, if the mother chose B for her child,there is no guarantee that her child would do better than if she had chosen A (e.g., the first patient given Arecovered whereas 30 patients given B did not, even if there is an overall higher proportion of recovery usingB). However, if she looks beyond her child and considers the next 100 or 1000 patients, then she could arguethat it makes sense to select the treatment with the higher probability of success, if it were known, if sheespouses the view that it is more likely for her child to be one of the successes in the treatment with a higherprobability of success.

2.2 Proportion and probability

Recall from Chapter 1.1 that data can be interpreted as a sample from a population. Then the 100 patientstreated on A is a sample from all patients. In this sample, 60/100 have been successfully treated. The

bSometimes, we also write probability as a percentage, from 0 to 100%

17

Chapter 2. Basic Probability

number, 60/100, refers to a sample proportion, which must be distinguished from the underlying probabilityof being successfully treated on A, for all patients in the population. A probability is always associated with apopulation; it is the (population) proportion of patients who are successful treated, out of all patients in thepopulation.

Example 2.2 (Continued from Example 2.1)

If we use data from the first nine tosses of our coin, we have

Toss 1 2 3 4 5 6 7 8 9Outcome H T H T T H T H T

which gives a (sample) proportion of 4/9 of H’s. The figure P(H) = 0.5 for this coin refers to the proportion of H’s thatwould have been obtained, if the coin is tossed many times. Hence, the outcomes of the many tosses is a population ofoutcomes, whereas those of the nine tosses is a sample.

Example 2.3

A university has 143 professors and among them, 55 are female and 88 are male. If we pick a professor at random, thenthe probability of picking a female is the same as the proportion of female professors, 55/143. Similarly, the probabilityof picking a male professor is 88/143. In this case, the 143 professors represent all the professors in the university, as suchit is the population of interest. The quantities 55/143 and 88/143 are population proportions, and hence probabilities.

Suppose we randomly select 6 professors, and their gender are:

F F F M M F

Then our data come from a sample and in our sample, the (sample) proportion of female is 4/6, which is different fromthe probability of 55/143. Similarly, the sample proportion of male professors is 2/6, compared to the probability ofmale professors, which is 88/143.

In this example, we also encounter the concept of randomness, genders in the data do not seem to follow any predictablepattern, and hence, random. Furthermore, even though the probability of a female professor is lower at the university,for this particular sample of six professors, there are actually more females than males.

2.3 Terminologies, rules and axioms

For us to effectively use probability to explain randomness, it would be useful for us to learn someterminologies, rules and axioms.

In any situation we are studying, we might be interested in a particular outcome or a collection ofoutcomes. A general term for an outcome or a collection of outcomes is called an event.

Example 2.4

Suppose we have a die, marked 1, 2, 3, 4, 5, and 6. Then the possible outcomes when the tie is tossed is one of the sixnumbers. If we are interested in odd numbers, then we are interested in the event, say A, such that A= 1, 3,5. On thehand, if we are going to toss the die twice, and we are interested in obtaining two 6’s, then the event of interest wouldbe A= 6,6.

If we are interested in an event A, then we use the notation P(A) to denote the “probability that A occurs".Probabilities are numerical values. We attach numerical values to probabilities so we can

18

2.3. Terminologies, rules and axioms

• Compare the probabilities between different events, e.g., Let A = recovery given A, B = recovery givenB in the pandemic example, then P(A) = 0.6, P(B) = 0.7, therefore P(B)> P(A).

• Carry out calculations on probabilities

The following are some basic rules of probability:

Rule 1: For any event A, the probability P(A) is a number between 0 and 1. That is 0 ≤ P(A) ≤ 1. If P(A) = 0,then we mean that we are certain that A will not occur. If P(A) = 1, then we are certain that A will occur.In most cases, we are interested in events with probabilities other than these two extremes.

Example 2.5Suppose we are interested in the weather for tomorrow and the possible outcomes are: “Rain" or “No rain". Then0≤ P(Rain)≤ 1 and 0≤ P(No rain)≤ 1.

Rule 2: In any situation, if S represents the set of all possible outcomes, then P(S) = 1.

Example 2.6In Example 2.5, there are only two possible outcomes: “Rain" or “No rain", hence S= rain, no rain.P(S) = 1.

Rule 3: If A is an event, then the event A does not occur is the complement of A, denoted by Ac or A. For anyevent A with probability P(A), the probability that A does not occur is P(Ac) = 1− P(A).

Example 2.7In Example 2.5, if A=No rain, then Ac=Rain and P(No rain) = 1− P(Rain).

Rule 4: If there are two events, A and B, then the joint probability between A and B are defined as the probabilityof occurrence of both A and B, written as

P(A and B)≡ P(A∩ B).

The two events are disjoint or mutually exclusive if they cannot happen simultaneously, in which case

P(A∩ B) = 0.

Example 2.8In Example 2.5, let A=No rain and B=Rain. Since it either rains or it does not rain, A and B are mutuallyexclusive events,

P(Rain and No rain) = 0.

19

Chapter 2. Basic Probability

Rule 5: (Multiplication Rule) If A and B are two events, then

P(A and B) = P(B)× P(A|B).

Here, P(A|B) is called the conditional probability of A given B.

Example 2.9If two cards are selected at random, one at a time without replacement (the first card drawn is not put back inthe deck) from a deck of 52 cards, what is the probability that both cards will be aces?Let A=First card is an ace and B =Second card is an ace

P(Two aces) = P(A and B)= P(First card is an ace)× P(Second card is an ace|First is an ace)

=4

52×

351= 0.0045

Rule 5a: (Conditional probability) Rearranging the multiplication rule gives

P(A|B) =P(A and B)

P(B),

which is a general expression for calculating conditional probabilities.

Example 2.10In a class of 105, 40 students are female, and among the female students, 10 are foreigners. What is the probabilitythat a female student is a foreigner?Let A=Foreign and B =Female

P(Foreign|Female) = P(A|B)

=P(A and B)

P(B)

=P(Female foreign student)

P(Female)

=10/10540/105

= 0.25.

Rule 6: (Independent events) Two events A and B are independent if knowing whether A occurred does notchange the probability that B occurs, and vice versa. If two events A and B are independent, then

P(A|B) = P(A) and P(B|A) = P(B).

The above equalities make sense. For example, P(B|A)means the probability of B given A. If A and B areindependent, then knowing A does not change the probability that B happens. Therefore, the probabilityof B given A must be the same as P(B) without any knowledge of whether A occurred or not.

For independent events A and B,P(A∩ B) = P(A)P(B)

20

2.3. Terminologies, rules and axioms

Example 2.11If two cards are selected at random, one at a time with replacement (so that the first card is put back in the packbefore the second is selected) from a pack of 52 cards, what is the probability that both cards are aces?

P(Two aces) = P(First is an ace and second is an ace)= P(First is an ace)× P(Second is an ace)

=4

52×

452= 0.0059.

Since the first card is returned to the pack, the probability that the second is also an ace is exactly the same as thatfor the first card. In this case, the events, A=First card is an ace and B=Second card is an ace are independent.

Rule 7: Total Probability (Union of events):

If A and B are not disjoint, then

P(A or B)≡ P(A∪ B) = P(A) + P(B)− P(A and B).

If A and B are disjoint, then P(A and B) = 0, therefore,

P(A or B) = P(A) + P(B)

In probability, “or" means “at least one of" so A∪ B includes A, B or both A, B.

Example 2.12If a fair die (a die such that the probabilities of observing any one of the six numbers are the same, i.e., 1/6) isrolled twice, what is the probability of getting at least one 6? This is the same as asking for

P(6 on first roll or 6 on second roll or 6 on both rolls),= P(6 on first roll) + P(6 on second roll)− P(6 on both rolls)

=16+

16−

16×

16

=1136

In this example, A is the event 6 on first roll and B is the event 6 on second roll. For P(6 on both rolls), weused the multiplication law for independent events.

Example 2.13In Example 2.5, since A=Rain and B=No rain are mutually exclusive, hence P(A∩ B) = 0 and consequently,

P(Rain or No rain) = P(A∪ B) = P(A) + P(B).

Rule 8: Complementary events and the calculation of P(At least 1)

Under the complementary rule, P(A) = 1 − P(Ac). If we are interested in the event A=At least one,then the complement event is Ac=None; furthermore,

P(At least 1)= 1− P(None)

21

Chapter 2. Basic Probability

Example 2.14For families of four children, what is the probability that there will be at least one boy, assuming boys (B) andgirls (G) are equally likely and births are independent?Instead of listing the 16 outcomes BBBB, BBBG, etc., we simply use

P(At least one boy) = 1− P(No boys)= 1− P(GGGG)

= 1−12×

12×

12×

12

=1516

.

Rule 9: Often, it is given P(A|B) but the interest is in P(B|A), Bayes Theorem provides a solution:

P(A|B) =P(B|A)P(A)

P(B)

Example 2.15Among three airlines providing services between two cities, airline A has 50% of all the scheduled flights, airlineB has 30% and airline C has 20%. Their on-time departure rates are 80%, 65% and 40%, respectively. A planehas just departed on time. What is the probability that it was airline A?Let D =on time, A=airline A, B =airline B, C =airline C. Then:

P(A) = 0.5,P(B) = 0.3, P(C) = 0.2, P(D|A) = 0.8, P(D|B) = 0.65,P(D|C) = 0.4

P(D) = P(D|A)P(A) + P(D|B)P(B) + P(D|C)P(C)= 0.4+ 0.195+ 0.08= 0.675

P(A|D) =P(D|A)P(A)

P(D)=

0.40.675

= 0.593

Rule 10: Partition rule

For any A, a partition is any collection of disjoint subsets of A that together make up A; P(A) can bewritten as the sum of the probabilities of its disjoint subsets.

Example 2.16If A= all white women, a partition of A is A1 =all white women with wage < 3 and A2 =all white womenwith wage ≥ 3. Hence:

P(A) = P(A1) + P(A2)

22

2.4. Probability tree

Figure 2.2: Probability tree for two independent tosses of a fair coin

Toss 1

Toss 2

P(H ∩H) = 12 ·

12

H12

P(H ∩ T ) = 12 ·

12T

12

H12

Toss 2

P(T ∩H) = 12 ·

12

H12

P(T ∩ T ) = 12 ·

12T

12

T12

Figure 2.3: A typical probability tree that records conditional probabilities

Event 1

Event 2

E1

P(E1)

Event 2

Event 3

P(E1 ∩ E2 ∩ E3)

E3

P(E3|E1 ∩ E2)

P(E1 ∩ E2 ∩ E3)E3

P(E3|E1 ∩ E2)E2

P(E2|E1)E1

P(E1)

2.4 Probability tree

Probability tree is a useful way to visualize probabilities when we are dealing with combinations of events.Each branch in a probability tree represents a possible outcome. If two events are independent, the outcomeof one has no effect on the outcome of the other. For example, if we toss two coins, getting heads with thefirst coin will not affect the probability of getting heads with the second. A probability tree which representsa coin being tossed two times, assuming toss outcomes are independent looks like Fig. 2.2.

Notice the probabilities on the branches are conditional probabilities. Therefore, a probability tree is agood candidate for carrying out calculations that involve conditional probabilities. For example, from the treejust given, P(H ∩ H) = P(H in second toss|H in first toss)P(H in first toss) = (1/2)(1/2) since the two tossesare independent.

A tree can have many branches. For example, for three events, the tree would look like Fig. 2.3. Noticethat P(E1 ∩ E2 ∩ E3) = P(E1)P(E2|E1)P(E3|E1 ∩ E2). In general, if there are K events, then P(E1 ∩ · · · ∩ EK)can be evaluated by multiply all the probabilities along the path back to the root of the tree, which isP(E1)P(E2|E1) · · ·P(EK |E1 ∩ · · · ∩ EK−1).

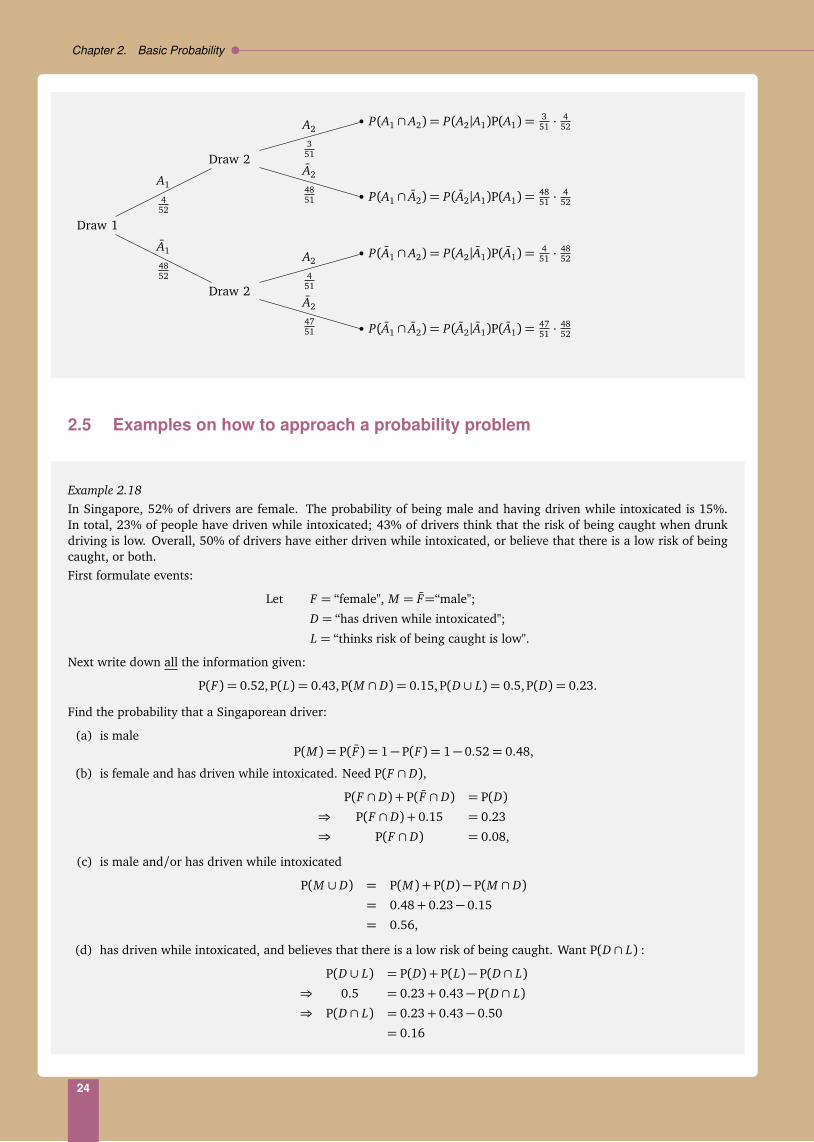

Example 2.17 (Continued from Example 2.9)

Let Ai denote "Ace is drawn" in i-th draw, i = 1,2. The two draws can be represented as:

23

Chapter 2. Basic Probability

Draw 1

Draw 2

P(A1 ∩ A2) = P(A2|A1)P(A1) =4751 ·

4852

A2

4751

P(A1 ∩ A2) = P(A2|A1)P(A1) =451 ·

4852A2

451

A1

4852

Draw 2

P(A1 ∩ A2) = P(A2|A1)P(A1) =4851 ·

452

A2

4851

P(A1 ∩ A2) = P(A2|A1)P(A1) =351 ·

452A2

351

A1

452

2.5 Examples on how to approach a probability problem

Example 2.18In Singapore, 52% of drivers are female. The probability of being male and having driven while intoxicated is 15%.In total, 23% of people have driven while intoxicated; 43% of drivers think that the risk of being caught when drunkdriving is low. Overall, 50% of drivers have either driven while intoxicated, or believe that there is a low risk of beingcaught, or both.First formulate events:

Let F = “female", M = F=“male";

D = “has driven while intoxicated";

L = “thinks risk of being caught is low".

Next write down all the information given:

P(F) = 0.52,P(L) = 0.43,P(M ∩ D) = 0.15, P(D ∪ L) = 0.5,P(D) = 0.23.

Find the probability that a Singaporean driver:

(a) is maleP(M) = P(F) = 1− P(F) = 1− 0.52= 0.48,

(b) is female and has driven while intoxicated. Need P(F ∩ D),

P(F ∩ D) + P(F ∩ D) = P(D)⇒ P(F ∩ D) + 0.15 = 0.23

⇒ P(F ∩ D) = 0.08,

(c) is male and/or has driven while intoxicated

P(M ∪ D) = P(M) + P(D)− P(M ∩ D)= 0.48+ 0.23− 0.15

= 0.56,

(d) has driven while intoxicated, and believes that there is a low risk of being caught. Want P(D ∩ L) :

P(D ∪ L) = P(D) + P(L)− P(D ∩ L)⇒ 0.5 = 0.23+ 0.43− P(D ∩ L)⇒ P(D ∩ L) = 0.23+ 0.43− 0.50

= 0.16

24

2.5. Examples on how to approach a probability problem

(e) has driven while intoxicated, and believes that the risk of being caught is not low. Want P(D ∩ L):

P(D ∩ L) + P(D ∩ L) = P(D)⇒ 0.16+ P(D ∩ L) = 0.23

⇒ P(D ∩ L) = 0.23− 0.16

= 0.07

(f) is male given the person is intoxicated. Want P(M |D):

P(M ∩ D)P(D)

=0.150.23

= 0.65.

Example 2.19

Probabilities from tables of counts. The following table gives the number of applicants to SMU in 2003, classified by sexand SAT score:

SexMale Female Total

< 800 79 13 92SAT 800-1000 772 216 988

1000-1150 1081 499 1580>1150 1795 2176 3971Total 3727 2904 6631

Let event A=“applicant is female", B=“applicant’s SAT < 800".

(a) Suppose a person is chosen at random from the table:

P(A) = P(female) =No. of female applicantsTotal no. of applicants

=29046631

= 0.44.

Notice in this case, the table represent the entire population of applicants to SMU in 2003, hence, probability is givenby the (population) proportion, see Chapter 2.2 and Example 2.3.

(b) But, if only people from those with SAT < 800 are chosen, then:

P(Applicant is female, given SAT< 800) = P(A|B)

=P(A∩ B)

P(B)

=no. female applicants with SAT< 800total no. applicants with SAT< 800

=1392= 0.14.

(c) Are A and B independent?

Two ways to prove independence: (i) A and B are independent if and only if

P(A∩ B) = P(B)P(A).

Using the table of frequencies,

P(A∩ B) =13

6631= 0.00196,

P(A) =29046631

= 0.4379,

P(B) =92

6631= 0.01387.

So,P(A)P(B) = 0.4379× 0.01387= 0.00607 6= P(A∩ B).

25

Chapter 2. Basic Probability

Not independent! (ii) A and B are independent if P(A|B) = P(A) and P(B|A) = P(B). From above P(A|B) = 0.14, butP(A) = 0.4379, therefore, P(A|B) 6= P(A). Not independent!

(d) What is the probability that the applicant is female or the applicant’s SAT is above 800?

Want P(A∪ B) = P(A) + P(B)− P(A∩ B).P(B) = 1−P(B) = 1− 92

6631 = 0.986. Since A and B are not independent, A and B are also not independent. So to obtainP(A∩ B), we must look at the entries in the table and not use P(A)P(B). P(A∩ B) = 216+499+2176

6631 = 0.436.

SoP(A∪ B) = 0.44+ 0.986− 0.436= 0.99.

Make sure all probability calculations give an answer between 0 and 1! (Rule 1)

26

3Univariate distributions

3.1 Random variables and distributions

In the pandemic example in Chapter 2, we were interested in the treatment outcome for someone affectedby a disease. We noticed that even for patients treated on the same drug, some recovered and some did not.Furthermore, the treatment outcome for future patients could not be predicted precisely. We called such aphenomenon “random". Whenever we are studying a variable, such that its value varies randomly betweenobservations, we call the variable a random variable. Hence, treatment outcome is a random variable. Thereare many other examples of random variables. In Example 1.3 of Chapter 1, we have records of seven variablesfrom a group of students. Not only the values of each variable vary over students, if we randomly select anotherstudent from the same school, it would not be possible to predict the student’s gender, GPA, etc. Hence, thevariables in Example 1.3 are random variables.

A random variable may take any value from a set of possible values. For example, in the pandemicexample, the possible values of treatment outcome are 1 (recovered) or 0 (not recovered). In Example 1.3,suppose we are interested in Course GPA, the possible values fall in the interval from 0 to 4.3. In either case,even though we know the set of all possible values of the random variable, its value could not be predictedprecisely before we observe the data. Furthermore, some values may be more likely than others to occur. Forexample, it may be more likely for a patient to recover if the patient is given treatment; it may be more likelyto see Course GPA between 2.7 and 3.0 than above 4.0, etc..

Random variables can generally be classified into one of two types: discrete random variables andcontinuous random variables. When the set of possible values a random variable can take is countable, thenthe variable is a discrete random variable. A continuous random variable, on the other hand, can take valuesin a set of uncountable possible values, for example, values in an interval.

Example 3.1 We reproduce the data in Example 1.3 here. In this set of data, Status, Gender, School, Course GPA, CourseGrade are all discrete random variables. Cumulative GPA is a continuous random variable. Age can be considereda discrete random variable if we age rounded to the nearest year, as shown in the table, or it may be considered acontinuous random variable if we use the exact age of each student.

Student Status Gender Age School Course Course CumulativeGPA Grade GPA

1 Singaporean Male 23 SOE 3.7 A- 2.992 Foreign Female 23 SIS 3.7 A- 3.923 Singaporean Female 19 SOA 2.7 B- 3.334 Singaporean Female 20 SOA 4.0 A 3.15

27

Chapter 3. Univariate distributions

5 Singaporean Female 36 SOB 4.3 A+ 3.666 Foreign Male 27 SOB 3.3 B+ 2.677 Singaporean Female 23 SOS 3.3 B+ 2.988 Foreign Male 25 SOB 2.3 C+ 2.359 Singaporean Male 22 SOB 3.7 A- 3.23

10 Singaporean Female 19 SOE 3.0 B 3.7211 Foreign Male 19 SOB 3.3 B+ 3.7712 Singaporean Male 19 SOA 1.7 C- 2.1713 Foreign Female 18 SOB 4.0 A 3.4214 Singaporean Female 19 SOS 1.7 C- 2.1715 Singaporean Female 18 SOS 4.0 A 3.4216 Singaporean Female 19 SOL 1.7 C- 2.1717 Singaporean Female 18 SOL 4.0 A 3.42

In Chapter 2, we discussed how probability helps us to explain randomness. When we are studying arandom variable, with possible values in a set, but some values are more likely that others to occur, we needa probability distribution. Often a probability distribution is simply referred as a distribution. A distributionrecords the probabilities for the occurrence of the different values of a random variable. In other words, adistribution is simply a collection of probabilities, one for each of the outcomes of a random variable.

There are two main types of distributions: discrete distribution and continuous distribution, for eachof the two main types of random variables.

3.2 Discrete distributions

3.2.1 Introduction to discrete distributions

When we toss a coin with two faces, if the coin is fair and the chance that the coin would land on its edgeis practically zero, then the toss outcome is a random variable, say X , with two possible values: H (heads)or T (tails). Since there are two possible values of X , hence countable, X is a discrete random variable. Theprobability of H, P(X = H) ≡ P(H) = 1/2 and the probability of T , P(X = T ) ≡ P(T ) = 1/2. In this case,we have an example of a distribution of one toss of a fair coin. A distribution tells us the probabilities of allthe outcomes in the toss of a coin. In this case, we have only two possible outcomes and each outcome has aprobability 1/2 of occurring. We can also represent the probability distribution in the form of a table

Outcome ProbabilityH (heads) 1/2T (tails) 1/2

We notice from the table that the probabilities of the two possible outcomes sum to 1.

Example 3.2Consider rolling a die with six faces: 1, 2, 3, 4, 5, 6.

distribution for the outcome of the roll of a die

Outcome 1 2 3 4 5 6

Probability 16

16

16

16

16

16

28

3.2. Discrete distributions

In this case, there are six possible outcomes, hence countable and discrete. The distribution tells us that the six outcomesare equally probable. Once again, the probabilities of all the possible outcomes sum to 1.

Example 3.3

Consider tossing a fair coin three times and counting the number of heads in the three tosses. We assume that theoutcome of each toss is independent of each other. In Chapter 2, we talked about the concept of independent events.This means, in the current context, the outcome of one toss is not dependent on the outcomes of previous (and future)tosses. Let us enumerate the different possible outcomes from three tosses of a coin. The possible outcomes are (H =heads, T = tails):

HHH, HHT, HT H, T HH, HT T, T HT, T T H, T T T

What is the probability of each of these outcomes? Let us look at the outcome HHH. Since P(H) = P(T ) = 1/2 in onetoss of a fair coin, the probability of observing the first H is 1/2. Subsequently, the probability of obtaining HH, by theindependence assumption and using the multiplication rule for independent events, P(HH) = P(H)P(H) = (1/2)(1/2).Similarly, the probability of obtaining HHH is P(HHH) = P(H)P(H)P(H) =(1/2)(1/2)(1/2) = (1/2)3.

We can use the same argument for the outcome HHT , P(HHT ) = P(H)P(H)P(T ) = (1/2)(1/2)(1/2) = (1/2)3. Theprobabilities for the other outcomes are similarly determined to be (1/2)3.

Now, we are only interested in the number of heads. If the three tosses give HHH, then the total number of heads is 3.Therefore, P(3 heads) = P(HHH) = (1/2)3 =0.125.

On the other hand, any of the three outcomes HHT , HT H, or T HH would give 2 heads. Therefore, P(2 heads) =P(HHT, HT H or T HH) = P(HHT ) + P(HT H) + P(T HH) = 3(1/2)3 = 0.375.

Similarly, any of the three outcomes HT T , T HT , T T H would give 1 head. Therefore, P(1 head)=P(HT T, T HT or T T H) = 3(1/2)3 = 0.375.

Finally, if the three tosses are T T T , then the number of heads is 0. Therefore, P(0 heads) = P(T T T ) = (1/2)3 = 0.125.

Summarizing the calculations, we have

Table 3.1: distribution for the number of heads in three tosses of a coin

Number of heads Probability0 (1/2)3 = 0.1251 3(1/2)3 = 0.3752 3(1/2)3 = 0.3753 (1/2)3 = 0.125

Once again, the probabilities of the different outcomes sum to 1.

The distribution can also be depicted in a graph, see Fig. 3.1. The graph of a discrete distribution is normalised so thatthe height of each bar is equal to its area, both of which represent probability. For example, in Fig. 3.1, the area (orheight) of each bar in the graph gives the probability of the outcome, hence, the areas (heights) of the four bars sum to1.

In this example, even though we know all the possible values of outcome, the actual outcome, is unknown until thecoins are tossed. As such, the outcome is a random variable. In addition, the random variable is discrete because thenumber of possible outcomes is countable: 0, 1, 2, or 3 heads. “The number of heads" is random because we wouldnot know its value until the coins are tossed. Nevertheless, the distribution gives us some idea of the relative chancesof the different outcomes. The situation is analogous to the example at the beginning of Chapter 2, where the motherbelieves treatment B gives a higher chance of recovery for her child, even though she would not find out whether herchild would recover until after the treatment is given. Therefore, a random variable is a term for the unknown outcomeof any situation that we may be interested in.

29

Chapter 3. Univariate distributions

Figure 3.1: distribution of the number of heads in three tosses of a fair coin

0 1 2 3

Number of heads

Pro

babi

lity

0.0

0.2

0.4

0.6

0.8

3.2.2 Properties of a discrete random variable

Based on the examples in Chapter 3.2.1, we now formally define a discrete random variable and give itsproperties.

A discrete random variable, X , is used to describe the unknown outcome of a situation if the value of Xcan only come from a countable number of possible values: a1, a2, ..., ak, where k is any positive integer ≥ 2.Some possible cases are illustrated in the following example:

Example 3.4

• Treatment outcome: X = 1 or 0 (2 possible values)

• Die: X = 1, 2, 3, 4, 5 or 6 (6 possible values)

• Three tosses of a fair coin : X = HHH, HHT, HT H, T HH, HT T, T HT, T T H, T T T (8 possible values)

• No. of infections in a large population: X = 0, 1, 2, 3,... (Large and possibly infinite but countable number ofpossible values)

P(X = ai) is called a probability distribution function (often abbreviated as pdf or PDF); it gives theprobability that X = ai . The probability distribution function, or simply distribution function, tells us howlikely the different outcomes of a discrete random variable occur. A valid distribution function must satisfythe following rules:

• P(X = ai) must be between 0 and 1, i.e., the probability of each outcome must be non-negative.Furthermore, the proportion of times an outcome appears cannot be more than 1.

• We are certain that one of the outcomes would appear:

P(X = a1 or X = a2 or ... or X = ak) = 1.

Furthermore, since X cannot assume two outcomes simultaneously, the k outcomes are mutuallyexclusive. Therefore, by the total probability rule in Chapter 2.3:

P(X = a1 or X = a2 or ... or X = ak) = P(X = a1) + P(X = a2) + ...+ P(X = ak) = 1,

30

3.2. Discrete distributions

which means the sum of the probabilities of all the outcomes is 1.

Example 3.5 (Continued from Example 3.3)

There are four distinct outcomes: 0, 1, 2, 3. Let X = “the number of heads in three tosses".

P(X = 0) = 0.125 > 0

P(X = 1) = 0.375 > 0

P(X = 2) = 0.375 > 0

P(X = 3) = 0.125 > 0

P(X = 0, 1, 2 or 3) = 0.125+ 0.375+ 0.375+ 0.125 = 1. This last statement is true, because, even though before thetosses we would not know whether 0, 1, 2, or 3 H ’s appear, it is certain one of these four outcomes must appear, hencethe probability is 1.

The distribution of a discrete random variable can be presented as a table, as in Table 3.1, or as a picture,as in Fig. 3.1. There is a third way of representing a discrete distribution that we will explore in Chapter 6.

3.2.3 Distributions as models

At the beginning of Chapter 1, we talked about the two goals of a statistical analysis, making sense of the dataand generalising what is observed in the data to the population of interest. Here, we discuss how these twogoals can simultaneously be achieved using distribution as a model for the data.

In Example 2.2, a fair coin is tossed nine times to yield a set of data. Earlier, we talked about how datacan be interpreted as sample from a population, so in this context, we have a sample of nine outcomes, outof the many outcomes if this coin were tossed many times (the population of toss outcomes). In other words,the nine outcomes is a subset of the many possible outcomes that could have been observed from repeatedtosses of the coin.

The data show that the order of H ’s and T ’s in the nine tosses seems unpredictable. We learned inChapter 2.1 we could use probability to explain such phenomenon. For a fair coin, there are only two possibleoutcomes: H or T . The probabilities for these outcomes are: P(H) = 0.5 and P(T ) = 0.5. We argued theseprobabilities can be interpreted as population proportions (see Chapter 2.2). In other words, if we tossed thecoin many times, half of the outcomes would be H ’s and the remaining T ’s. However, in any single toss, it isnot certain whether H or T would appear; this is the randomness we referred to in the nine tosses. Hence,the two probabilities P(H) = 0.5 and P(T ) = 0.5, which form a distribution (see Chapter 3.2.1) can explainthe nine tosses (the data) as well as the many tosses that have not been made (the population). In this sense,the distribution helps to explain the observation made in the data, and link the data to the population. Wecall the distribution a probability model for the outcome of a coin toss. The probability model explains theoutcomes of the nine tosses and the same model allows us to talk about the “population" of tosses that havenot been made.

Example 3.6

In the pandemic example in Chapter 2, we have data on the outcomes of 100 patients treated on drug A. The outcomesare of only two possible values: 1 (recovered) or 0 (not recovered). In the data, 60 patients are observed to haverecovered while 40 did not recover; the outcomes in these patients do not appear in any particular order.