Embed Size (px)

Citation preview

Statistics of Income: A By-Productof the U.S. Tax System

By Robert A. Wilson*

U.S. Government statistics are the product of a decen-tralized statistical system that involves over 70 FederalGovernment organizations, one of which is the Statistics ofIncome Division of the Internal Revenue Service (IRS) in theDepartment of the Treasury [11. Another characteristic of theU.S. system is that statistics are often a by-product of anadministrative function and are based on an administrativerecord. In the case of the Statistics of Income Division, theeconomic, financial, and tax statistics it produces are aby-product of tax returns that are processed in administer-ing the tax laws. The report series in which the data arereleased is called Statistics of Income (SOI).

This paper reviews the relationships between processingfor tax administration and processing for statistics throughabout 1985. It begins with a description of some of the SOIprograms and their uses. It then reviews IRS and SOIprocessing and their limitations and some of the improve-ments in SOI processing now under consideration. Theseimprovements will help the Statistics of Income Division tooperate more efficiently and effectively in meeting theneeds of its major users and to adjust to the continuingclimate of reduced budgets for statistics.

THE STATISTICS OF INCOME PROGRAM

The SOI series came into being after the adoption of theSixteenth Amendment to the Constitution and the subse-quent enactment of the first modern U.S. income tax law,the Revenue Act of 1916. This Act specifically called for theannual publication of statistics. The wording contained inthe 1916 Act has been repeated, with practically nochange, in each major rewrite of the tax statute since thattime. It is currently contained in the Internal Revenue Codeof 1986, which is the basis for the present tax law [2].

SOI data from the very beginning (1913) have been usedextensively for tax research and for estimating revenue,especially by officials in the Office of the Secretary of theTreasury. At the start, the reports were almost entirelydesigned to meet these needs. With the growth of researchgroups both within and outside the Federal Governmentand with the increased needs of the tax planners andrevenue estimators, new types of data soon were alsorequired. At the same time, the tax returns were expanded

* Coordination and Publications Staff. Reprinted (with minorrevisions) from the Multi-National Tax Modelling Proceedings, RevenueCanada Taxation, September 1985.

to reflect the growing number of new provisions of the law,thus providing a ready source of data with which to fulfillthese needs.

By the close of World War 11, most of the population wassubject to the income tax. At about the same time, theeconomies of using existing administrative files as thesource of data for a wide variety of Government statisticshad become more and more apparent. Each of theseevents made the tax return a valuable source of economicas well as tax information. While the tax definitions of dataitems presented some obstacles, the obstacles were faroutweighed by the likelihood that taxpayers' response tothe tax return tended to be more accurate than theirresponse to special surveys. Moreover, with experience,users learned how to adjust the tax data for these definitionsin order to meet their own particular needs. Meanwhile, SOIprocessing methods contributed by making some of theadjustments for the maj

.or users in the course of "editing"

the tax return data for the statistics [3].

The upshot of all these developments was an SOIincreasingly different in its orientation from the early SOLSeveral multi-purpose reports replaced the single tax-oriented report. While tax data continued to be included (allthe more so as the tax law expanded both in scope and incomplexity), the emphasis changed to include more gen-eral purpose statistics that would assist economists andfinancial analysts [4].

The main emphasis of the annual statistics has alwaysbeen individual and corporation income tax return data.Other studies based on other types of returns for whichdata have been tabulated either annually or periodically arepartnerships, estates and gifts, fidu

*ciaries, farmers' coop-

eratives, private foundations and other tax-exempt organi-zations, and employee plans. Schedules attached to someof the returns became the subject of separate SOI pro-grams. The sole proprietorship schedules attached to indi-vidual income tax returns were a relatively early source ofstatistics which, when taken together with data from part-nership returns, helped shed light on unincorporated busi-ness activity.

Another development in the growth of SOI has been theincreasing tendency for new provisions of the tax law torequire separate reports to Congress by Treasury's Office ofTax Analysis (OTA). These reports have required statistics onsuch topics as individuals with high income who arenontaxable, capital gains taxation, international boycott

103

104 Statistics of Income: A By-Product of the U.S. Tax System

participation, taxation of corporate income from U.S. Pos-sessions, and income of citizens working abroad.

Today, information obtained from the. SOI program isused extensively throughout the Federal Government for avariety of purposes. Besides OTA and the congressionalJoint Committee on Taxation, there is a third major Federaluser of SOI, the Bureau of Economic Analysis in theDepartment of Commerce. Profits data for corporations inthe National Income and Product Accounts are bench-marked to the SOI profits obtained from corporation incometax returns, which are then adjusted for conceptual differ-ences and extrapolated to more current years based onmore fragmentary data from other sources [5). Returns ofunincorporated businesses, i.e., sole proprietorships andpartnerships, are also used for the National Accounts; theyconstitute the only complete and reliable source of financialstatistics for this segment of the economy. Investmentincome reported on individual income tax returns is alsoused for the National Accounts.

THE STATISTICS OF INCOME DIVISION

The -1916 Act - that first called for -the publication ofStatistics of Income necessitated the creation of a statisticalorganization within IRS to carry out this mandate. Thepresent successor to that original organization is the Statis-tics of Income Division in the National Office in Washington,D.C. The Division is part of the Office of Taxpayer Serviceand Returns Processing under the Deputy Commissioner(Operations) which is charged with the responsibility forprocessing tax returns.

The Statistics of Income Division is comprised of a staffmostly of statisticians and economists who work closelywith users to determine the content of each program andreport, to desig'n the statistical samples' used, and todevelop processing procedures. Complications arise fromthe fact that the processing is currently decentralized in asmany as eleven different locations throughout the country;hence there is a need for a strong coordinating role by theStatistics of Income Division, including adequate qualitycontrols to assure uniform and accurate processing.

The role of the Division has changed over the years. Untilrecent times, it had the additional responsibility of produc-ing management statistics to assist IRS in its day-to-dayoperations. However, SOI has always been the Division'smajor responsibility.

ADMINISTRATIVE VS. SOI PROCESSING: A BRIEFHISTORY. I

Within IRS, statistical processing of the tax return datahas historically been a separate off-line operation, divorcedfrom the mainline processing of tax returns for administra-

tive purposes. There were reasons that dictated this sepa-ration, some of which are still applicable:

• SOI is designed to serve tax policymakers in particularand economists in general. Consequently, it is of littleinterest to tax administrators (the role of IRS is, aboveall, tax administration) most of whom are attorneys andaccountants whose statistical needs, where they exist,are quite different from those of policymakers.

• As a corollary to the first point, SOI was and continuesto be a byproduct of the IRS tax administration system.Therefore, SOI and the processing for it have oftenbeen given a lower priority by IRS. In recent years theSOI budget has reflected this, with continued declinesin the resources set aside for statistics. As a programadministered by IRS, these budget declines mightordinarily have been steeper. However, the fact thatneeds for Treasury Department tax policymaking hadto be considered often served to mitigate the size of thedeclines.

.0 Most of the SOI programs are based on samples ofreturns and for many years these samples were man-ually designated. This sampling as- accomplishedmost effectively only after administrative processingwas completed. Moreover, after the sampled returnswere selected, they were sent to a central location, theStatistics of Income Division in Washington, for specialprocessing.

The administrative processing which preceded statisticalprocessing is and has been a decentralized operation. Untilthe 1.950's, all of this processing took place in the morethan 50 IRS district offices throughout the United Stateswhere taxpayers filed their returns. This processing was inlarge part manual, assisted, beginning in 1948, by punch-card equipment to service the larger district offices. Areaservice centers, also with punchcard equipment, werecreated in the mid-1950's to assist these same largerdistricts. Administrative processing consisted largely ofmathematical verification to assure that returns were "inbalance," plus certain other basic checks that included areview of the tax computation [6].

In contrast, statistical processing was conducted inWashington and was limited to returns selected for the SOIsamples. Compared to the administrative processing ofthese returns, it was a lengthier and more complicatedprocedure. Many more lines on the return forms wereutilized and some of the totals reported on these lines had

'to be edited for the statistics using amounts identifiedthrough examination of supporting forms and taxpayerschedules that were included as part of the return.

The advent of automatic data processing (ADP), for taxadministration purposes in the early 1960's had a profound

Statistics of Income: A By-Product of the U.S. Tax System

effect on IRS processing and statistical processing wasdirectly affected. Statistical abstracting, editing, and tran-scription, which after 1955 had begun to be decentralizedfrom Washington to the pre-ADP area service centers, werecompletely decentralized during the 1960's to the ten ADPregional service centers where returns were now filed bytaxpayers and then processed there for administrativepurposes under the new system.

However, with a view to relieving regional service centersof all processing not directly related to the administrativeprocessing of returns, a data center (now called a comput-ing center) was later established in Detroit, Michigan.Among its duties was SOI processing, especially the com-puter programming-to test and tabulate the data. TheData Center also manually resolved the errors uncoveredby these tests and, in addition, for many years was respon-sible for the initial manual abstracting, editing and transcrip-tion of data from returns for the corporation and certainother SOI programs.

While statistical processing continued to be an off-lineprocess, under the new ADP system processing was nolonger under the control of the Statistics of Income Division.The role of the Division in response to these changesevolved into one of planning, coordinating and overseeinga field operation. This was in addition to its continuing roleof meeting with users to identify their data needs and topublish the SOI reports. As a result of the transition, theStatistics of Income Division ceased to have its own manualand computer processing operation and no longer hadaccess to the computer which it had previously shared withthe Bureau of the Census. Instead, it became a "payingcustomer" for the processing services that were providedby other IRS organizational units whose principal functionswere return processing in general. The Division developedthe data "requirements" (including standards and goals forcompletion) and, at least in principle, these other organiza-tions determined the best way to carry out and meet theserequirements. The loss of control over its own processingoperation and the administrative problems that developedunder the new system have continued to this day to presentchallenges to timely, accurate, efficient and economicalprocessing for statistics.

CURRENT IRS ADMINISTRATIVE PROCESSING

The concept of a centralized Master File containing acomputerized account for each taxpayer was adopted bythe Service in the mid-1 950's. Then, in 1959, the concept ofregional centers located in each of the Internal RevenueRegions was adopted. These centers were designed as ameans of centralizing the processing that had previouslytaken place in the district offices and area centers, and ofintroducing computer processing of tax return data to

105

replace a large part of the previously-manual operation. Thefirst regional center was opened in 1961.

Using individual income tax returns as the example,Figures A and B summarize the major steps (also de-scribed below) in the administrative processing system as ithas now evolved [7]:

Tax returns are received at the service centersthroughout the country where processing begins. Taxexaminers in the service centers first check the returnsreceived to be sure they are signed and meet the IRScriteria for a completed return. Returns are sorted bytype and accompanying checks compared with theamounts reported. A quick search is made for unal-lowable deductions and obvious errors and the returnsare coded for computer processing.

Information and tax data comprising nearly all of theinformation reported on the main part of the return andmuch of what is included on selected supportingschedules are transcribed for computer processing.This is accomplished by means of direct data entryonto magnetic tape, using key station terminals.

After verifying the return count per "block," the com-puter verifies the tax computation used or, if appropri-ate, computes the tax for the taxpayer [8). A number ofconsistency and validity checks are made to theinformation transcribed in order to identify certainmathematical errors made by taxpayers and mistakesmade in the actual data capture process. (However,unless errors have a direct bearing on the tax reported,they may not be corrected. The implications of this onSOI are discussed below.)

After a block of return records meets the standards foracceptability, the service center transmits it on com-puter tape to the national computing center in Martins-burg, West Virginia (MCC), for central account post-ing and "settlement." The function of MCC is to posttaxpayer transactions to the so-called Master File. Inthe process, MCC performs several functions. It ana-lyzes the data from the service centers by makingcomparisons with the prior year and generates refundand tax deficiency notices; it identifies returns forpossible audit examination; and it creates speciallistings for the centers, one of which identifies thereturns for inclusion in the S01 samples.

SOI USE OF THE TAX ADMINISTRATION SYSTEM

SOI began to piggyback directly on the tax administra-tion system soon after the Master File for individuals wasdeveloped. The Master File offered a vastly improvedsampling frame. Moreover, it could be accessed by com-

106 Statistics of Income: A By-Product of the U.S. Tax System

Figure A.-IRS Administrative Processing

V --ra. TAY PA'Y F. A. ffil

XRS SMVICECENMERS I-

RMIZN5 RECEN&D ANDCHE(q,,'ED Re COIARE-M NESS

OR

OENICCLS ERRORS

_FA X DATA

COMPUTIER

VaRi Fi r:: b

NAME)lb NO.EFXE=-M PT/oN-5

V9579999t~\Kr--Y- ENTER Gb

INNNI DUAL J~_-M

SEL.Fr

DEFFNMIM7 N~r

jEwED FbR

palmmtmmm

SPENT W4 -rApE ToMART1N5bVQ.C-rCOMPUTW& CENTE9

puter, enabling more efficient, sophisticated and effectivesample designs to be used than under manual sampling.Since, in addition, these samples were usually smaller insize, economies as well as improved data often resulted.Sampling by computer was then gradually extended to theother major SOI programs. Within a few years, nearly all of

the SOI samples were designated by computer, using

information from the Master File system.

Yet, for many years, little use was made of the actual datacaptured from the returns for tax administration purposes[9]. As a result, there appeared to be some duplicationbetween the administrative and SOI systems because, forreturns in the SOI sample, many of the same data items

were processed twice, once for tax administration and oncefor statistics. However, a number of items were processeddifferently under the two systems. On the one hand, all dataused for SOI were subject to rigorous testing and tostatistical editing when necessary. On the other hand,because of the sheer volume of returns processed by IRSsome reporting and processing errors were accepted un-der the administrative system. (The 193.2 million docu-ments processed by the Service in Fiscal Year 1987 wereabout twice the number processed in Fiscal Year 1962, atthe inception of ADP) To conserve resources, such short-cuts in administrative processing had to be taken wheneverpossible. Because the two systems served such differentpurposes, it was not without reason that the SOI Division

Statistics of Income: A By-Product of the U.S. Tax System

r

F&SI-S TAXPAYEP.7RANSACTIONS -ro

IDENTIFIE~5 RETURN5Fok AL)Drr-

Figure B.-Martinsburg Computing Center Processing

W-1

kk f__1Q

J~t00-0 ~0~REFUNI)N07 ICES

was reluctant to use administrative data.

Traditionally the emphasis in administrative processinghas been on production. To meet production standardsthe expectation is that the reporting and processing errorsthat initially are allowed * to "pass" will be caught later onif significant, through computer review. However,since this computer review generally addresses onlydata items necessary for tax administration (generallythe return entries that have a direct bearing on the tax or onthe payments reported or refund claimed), errors in otherreturn items that are important for statistics often remain inthe system. Although service centers often instituted somesort of verification system of their own design when re-sources were available, it has only been recently that IRShas begun to institute more of a balance between quantityand quality.

Despite these shortcomings in the adequacy of some ofthe administrative data for statistical use, efforts were made

I t'E r-IA:STr--R PILE

107

starting in the mid-1970's to utilize them for the SOIindividual income tax return program, but only to a limitedextent. Administrative data items that came from the sameentries on the return as those required for SOI weremanually verified or edited at the same time that additionaldata needed for the statistics, but not available from theadministrative system, were abstracted and edited for SOL(The principal economy achieved through this process wasin not having to retranscribe the administrative data thatwere accepted for the statistics.) Then, toward the end ofprocessing all of the transcribed data comprising a returnrecord were brought together and tested for internal con-sistency at the Detroit computing center. Inconsistencieswere resolved, either manually or by computer, on the basisof logical relationships among return items inasmuch as thereturns were no longer accessible for statistical purposes atthis stage.

The SOI system has since been modified. Formerly,

108 Statistics of Income: A By-Product of the U.S. Tax System

clerical tax examiners verified the administrative data forSOI and corrected or edited them as necessary. Now, alldata items from the individual income tax return are.'accepted" for the statistics as reported, unless the returnfails a computerized check for acceptability which is madein the service centers. Return records failing this check areflagged for the specific item questionable and the returnentry to be used for the statistics corrected or subjected toSOI editing while the return is still available.

This same computer-assisted editing process also iden-tifies returns for which additional data need to be obtainedfor SOI only. This identification is based on the presence ofentries in the administrative system for which the t

'axpayer

has to file supplemental or computational information,. oftenin a supporting schedule that is the source of the dataneeded for SOL This means that, at least in the case ofindividual income tax. returns, most of the computer check-ing for consistency is decentralized from the Detroit com-puting center to the service centers which are where thereturns are processed, both for administrative and statisticalpurposes. It also means that some of the additional editingof the return totals that was formerly accomplished byrecoursa-to - supplemental data in supporting schedules-may no longer be possible because the need for cdrtainadjustments formerly made in the manual edit processcannot always be determined by computer [10].

.For the sole proprietorship and partnership programs, a

more comprehensive manual statistical edit, often involvingmany more items than are available from the Master Filesystem, especially for farm data, is now being consideredfor certain future years. This special editing may coincidewith the Agricultural and Economic Censuses. for 1992,1997, and so on. Special requests for data may be. accom-modated in a like manner At the present time, thle corpo-ration program is the only major S01 program. in whichadministrative data have not yet been used.

At least in the case of individuals, little appears. to havebeen lost by the inclusion of administrative data, with nonoticeable breaks in the historical time series apparent. Thischange in the approach to return editing would

'probably

have been necessitated in any case by outside events; withthe decline in statistical budgets throughout the FederalGovernment in recent years, more economical and efficientmethods of obtaining data have become a necessity. At.thesame time, the drive to reduce respondent reporting bur,dens has also been made applicable to tax returns. As aresult, some of the return form schedules used to facilitateSOI editing may no longer be required. Changes.in themode of taxpayer filing can also be expected to makechanges in statistical processing, particularly in the dataediting. This will result, for exampl

'e,, from the filing by

computer of certain tax returns by paid tax preparers.

PRESENT STATUS OF SOI PROCESSING

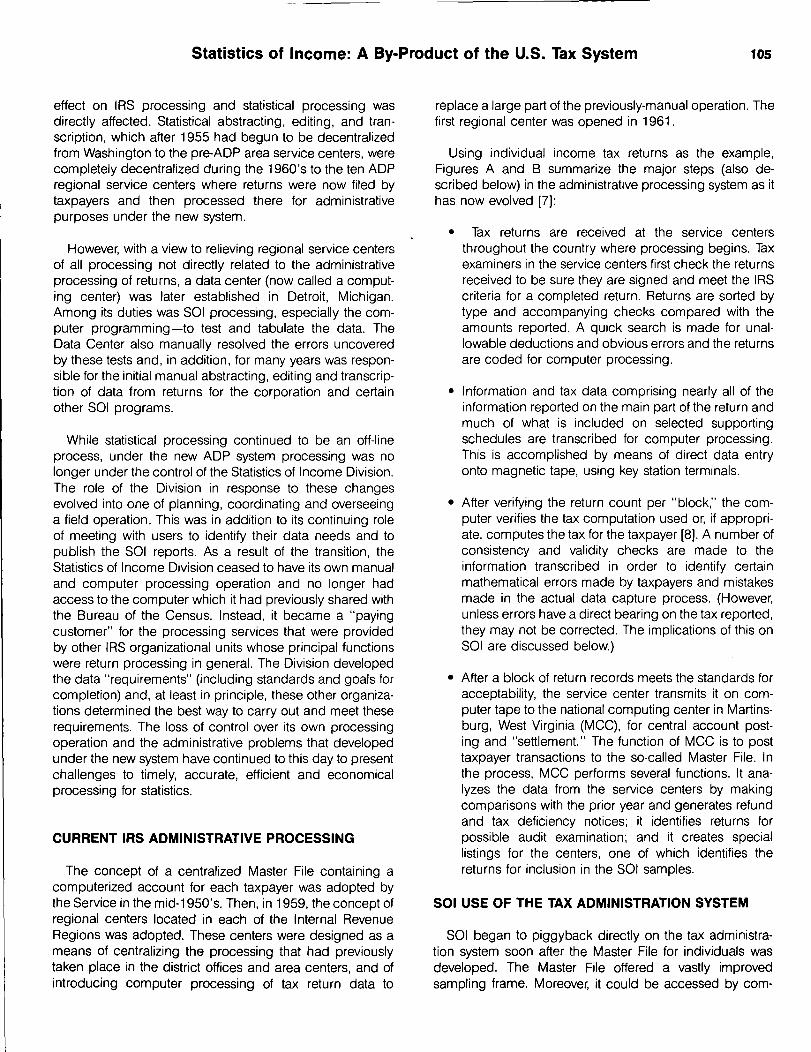

How does SOI fit into the current IRS processingscheme? Figures C and D pick up where Figure B leavesoff in showing the connection between the administrativeand SOI systems. Figure E shows this relationship in moredetail.

Magnetic tape extracts containing the identification ofsampled returns are sent by MCC to each of the servicecenters where returns for SOI are selected from the files.The sampled returns in some cases may be processed forthe statistics in the same service center in which taxpayersfile them. Increasingly though, they are shipped to anotherservice center or to the computing center in Detroit forprocessing. The exact locations chosen are dependent onprior-year experience, e.g., familiarity with the SOI pro-grams and their processing requirements, the efficiency ofa center's SOI operation and the quality of its work, and thepriority it assigns the program and its ability to meetdeadlines.

As already mentioned, SOI programs increasingly utilizedata captured during administrative processing, and onlythe data not available from the administrative processingsystem are obtained directly from the returns. The latterdata are either transcribed directly or are entered ontointermediate "edit sheets" for transcription at the servicecenters or Detroit computing center The two sets of dataare then merged.

Computer testing is now in two stages. In the first stage,the administrative data are checked to assure that, at leastto start with, they can be reconciled with what is reported onthe return. It is at this stage that most of the errors leftuncorrected during administrative processing are caught.Then, after the complete record (including the additionaldata obtained solely for SOI) is on tape, it is sent to theDetroit center for the second stage of testing.

It is during this second testing stage that illogical relation-ships and internal inconsistencies are identified. Misre-ported or missing information may be imputed by theDetroit center, either manually or by computer (and theStatistics of Income Division sometimes has to make thefinal decision on how to deal with specific returns). In thecase of errors, the output, in the form of hardcopy error.registers or information listings, is sent by mail to theoriginating service center where it is associated with theactual returns. Return information is then used to helpcorrect the SOI records by annotating the error or informa-tion registers. This is a "back and forth" process betweenservice centers and the Detroit center until the file isconsidered error-free. After the second round of correctionsis made by the service centers, any remaining errors arecorrected at the Detroit center, without recourse to thereturns, in order to save time. Having arrived at this point in

Statistics of Income: A By-Product of the U.S. Tax System

Figure C.-Statisticall (SO11) Processing

AMPLE LLST`,AJ>M1t4LSTRATIVF_ &ATA

I hMly/sTmOMPUTEK- IMVF_1~4~01

CORRECTED

DMA] -54MPL-E SE~~-X_7EbI I

processing, the files are tested for duplicates and othercharacteristics including those used to evaluate the com-pleteness of the total sample. Weighting factors are thenproduced.

In addition to tabulations, either for publication or tosatisfy special user needs, analytical tables are generatedto assist in reviewing the aggregated data. Most of thisreview takes place in the Statistics of Income Division andtakes into account how the data were processed as well aswhether or not they are reasonable in light of prior-yeardata, changes in tax law and data from other statisticalseries. Disclosure in tables is dealt with mostly by comput-erized routines. Table programming is now done, not onlyat the Detroit computing center, but in the Statistics ofIncome Division or by outside contractors.

CURRENT PROBLEMS AND FUTURE PLANS

Even as SOI becomes more of a "natural" by-product ofthe administrative system there are a number of problemsthat need to be addressed. Some of them are describedbelow [11 ].

109

In this period of continuing budget constraints, limitedresources pose significant problems for SOI. The presentSOI system has developed into one that utilizes whateverresources are available and thus it still relies heavily onmanual processing. It does not take advantage of theinteractive capabilities of computer systems because theyhave not been available. To help counter the cost of manualprocessing, the Statistics of Income Division has beenattempting to adopt more sophisticated processing tech-niques, such as using specialized samples or using longi-tudinal files to assist in error resolution. However, this cannotalways be done, in part because computer programmingresources are not always available.

Because processing occurs at so many locations, there ismuch shipping of documents and data tapes. The monitor-ing of these shipments is time consuming. Significantdelays in processing result from late, missing, or misroutedshipments. Timely project completion as well as the securityof tax return information has sometimes been jeopardizedby the controlling and shipping process. Moreover, thesedelays mean that the returns are not always available whenneeded for IRS compliance activities. Competition for re-

110 Statistics of Income: A By-Product of the U.S. Tax System

Figure D.-SO1 Process!ng-(Continued)

).TESTS C0RREC7--_S DATAF:bR- L-06-Alr, , CON61-STENCY

2.1MIPUTE5FOR Mlb5ING AN[)WSREPORTED J)ATA

J. GiENE:RAFFE75 FHRR~RPE-66TERS FOR-COMPARI-SnN --FOACTLJAL- RETURNS

turns is aggravated by the length of time it takes for errorresolution. Service centers must sometimes hold returnsuntil the Detroit computing center has processed two errorresolution cycles. The competition sometimes necessitatesphotocopying. Most frequently, the competition is for thelarger returns which are sampled for SOI at the 1 00-perbentrate.

Control of the sample is also complicated by the processused to merge administrative and SOI data. When dataobtained through the tax administration system are incor-porated into a project, they are included in the same returnrecord that is used for sample control. When this record ismatched with the separate record containing the additionaldata obtained for SOI, problems can arise if there aretranscription errors in the return identifiers used to effect thematch. When data from the administrative system are notused in a project, sample control is entirely manual. In theabsence of a computerized audit trail, there is always theadditional problem of returns getting lost at some stage inprocessing.

Although - the basic SOI process'

is the one alreadydescribed, there are many variations from project to project,especially in computer processing. There are two majorprojects-corporations and individuals-for which process-ing is complex and for which large computer files arenecessary. The numerous smaller projects are forced tocompete with these two major ones for available mainframe

L I F

zEx~,~_inr_-nA \AIEIC-qHTS i TABULATES,

"ERROR FOC-:F-" F:*ILE ~CREATES PUBLIC-US!E

- 1--:11 F-S

computer resources. As a result, many of the smallerprojects have had to be assigned a lower priority and,therefore, are not always produced on as timely a basis.

The Statistics of Income Division is taking steps to dealwith these and other problems that will improve SOI dataand how they are produced. A mini/micro computer systemin the service centers and in the Statistics of IncomeDivision is being installed for processing smaller SOIprojects [12]. This system will enable the Division to havemore of a voice in setting priorities for the statisticaloperation in the service centers. It will also increase itsability to monitor the costs and timeliness of its productsmore effectively. The increased SOI processing at theservice centers expected as a result will free up programdevelopment resources and computer time at the Detroitcenter for use on the two larger projects. It should alsopermit the release of SOI returns to compliance activitiessooner

Most of the savings expected through this system will beachieved by centralizing transcription and by combiningdata editing and testing into a single operation. As a result,the need for edit sheets and error registers will be elimi-nated. Since a sample return will be controlled only once, atthe point it is processed, controlling costs will also bereduced.

Shipping of paper documents will also be curtailed, thusreducing time delays. While most of the processing is now

Statistics of Income: A By-Product of the U.S. Tax System

1.

2.

3.

7.

8.

9.

Figure E.-SOI Data Source and Processing at Various Locations(individual Income Tax Returns)

Service Centers Martinsburg, West Virginia(Ten sites throughout country) Computing Center

1 Returns are received in mailfrom taxpayers and numbered

Refurns are checked-m-amu'alTy-,transcribed, computer veri-fied, and administrativeerrors are corrected

Computer tapes are producedand transmitted to the Mar-tinsburg Computing Center

tical purpose

Sampled reCords are furthercomputer tested for statis-

E-r-rorcases identified areresolved and corrections aretranscribed

items identified for manualentry are abstracted andtranscribed

4. return information isTaxposted to the IndividualMaster File

6.

Ll

II

Refund and deficiency no-tices aregenerated

T

SOI sample Alection 11and corresponding computertapes are transmitted toservice centers

10. apes are transmitted to theI --it Computing Center

I essing errors are resolved

Ne-w data items are sub-jected to testing and proc-

being decentralized from the Detroit computing center tothe service centers, not all of the service centers will beinvolved. When a center chosen is other than the one inwhich the returns were filed, the distance over whichdocuments have to be shipped will be one of the factorstaken into consideration in making the selection. Withshipping reduced,to an optimal level, security problemscaused by loss of tax return data will also be reduced.

Under the new system, it will become possible for the firsttime to accumulate totals from the SOI returns processedand to screen the returns with particular characteristics atany point in time. This will make it easier to detect problemareas noticeable only from aggregated data at an earlyenough stage so that remedial action can be taken beforethe complete tabulations are run.

Sample monitoring should be improved and it will be-come possible to determine the number of missing returnsat any time during processing. The earlier that missing

Detroit, MichiganComputing Center

t:sa are again subjected tos11. ID ting,and missing and mi

reported taxpayer intormation-is imputed

12.

13.

[ Data are wei hted

Public Use Tax Modeltap-e-TIT-t-s-and tables aregroduced

returns can be identified, the better the chances are thatthey can be located before the sample has to be closed out.

The modern design of SOI processing systems for virtu-ally all programs will incorporate some form of administra-tive data usage. With the recent redesign of the corporationSOI program to include use of administrative data for thefirst time, all major SOI programs will share the advantagesof data abstracting by electronic means. This improvementfrom manual abstracting to electronic retrieval has changedthe nature of SOI processing, which was once consideredtoo complex to be connected with administrative process-ing, but which will now use this system as the starting point.With the marriage of SOI and administrative data, manualprocessing operations which previously were the costliestto perform will be dramatically reduced. Use of administra-tive data will reduce the amount of manual editing done, aswell as the need for much of the transcribing and verifyingof data.

In the case of corporations, the savings may not be as

112Statistics of Income: A By-Product of the U.S. Tax System

dramatic as in other SOI programs because, unlike individ-uals, manual editing is expected to continue to be a majorfactor, especially for the larger returns where taxpayerreporting is more complicated and less standardized. Whilethe administrative data will be checked by computer in anycase before they are accepted (by the process alreadydescribed for individuals) and changed. when they areinconsistent with SOI definitions, in the future this may bedone only for subsamples (in the case of the smallercorporation returns) so that imputation factors can bedeveloped for the rest of the returns of similar size. A relatedcost-saving innovation may be the use of improved impu-tation techniques for erroneous or missing data [13].

In regard to quality, steps are being taken to ensure thatevery statistical study has a formal quality assurance pro-gram which provides for a review at each stage in process-ing. Because of the observed lapses in the quality of dataduring administrative processing, the Statistics of IncomeDivision has also taken the initiative, in conjunction withother areas of the Service, to undertake an independentreview of the quality of the administrative data transcribedfrom individual income tax returns. If the Division's recom-mendations are adopted, both IRS and SOI will stand tobenefit.

Many other recent initiatives for streamlining SOI pro-cessing are ongoing or in developmental stages. A goal isto integrate SOI more fully into the administrative process-ing stream as that system is revised so that statistics canbecome more of an on-line IRS operation.

If SOI is to serve tax policymakers in a more responsivemanner and on broader issues, it will be necessary to builda data base from as many sources as. possible. Oneapproach being explored is through use of statisticalmatching with information from other sources. Another is toestablish exchange agreements with other Federal agen-cies with regard to information furnished to them by the IRSunder special provisions of the tax code (to the extentpossible, given these agencies' own confidentiality rules).

I If these efforts are successful, the new agreements wouldprovide that IRS be able to receive back a copy of theinformation it furnishes which would also include anycorrections, modifications, or enhancement% or the addi-tion of any other information prepared by the other agencyfor inclusion in, or for use with, the IRS data. Even withoutthe assistance of other agencies, much can be done toexpand the SOI data base through linkages of recordswithin IRS. For example, efforts are currently underway torelate estate tax returns to the returns of heirs for a specifiednumber of years.

Considerable research is, of course, necessary to de-velop or perfect methods of overcoming the many known

difficulties that would be encountered in trying to expandthe data base. For example, techniques would have to bedeveloped for linking employees with the employer, taxpay-ing entity, "establishment," pension plan and payroll entity,all of which may have different definitions. Such linkageswould encompass all types of employers-corporations,sole proprietorships and partnerships. A start in this direc-tion has been the linkages made between business incometax returns and related employment tax returns, betweenpartnerships and partners, and between certain smallcorporations and stockholders. In another research area,"panels" of data, representing returns of the same taxpay-ers over several-years time, are also being developed.These will enable the revenue estimators to make moreaccurate adjustments for the effects of "carrybacks" [141.

CONCLUSION

The 1980's has been a period of major changes in SOIprocessing methods. The emphasis during this time hasbeen on finding ways to reduce costs and speed upprocessing.

There are obvious ways to streamline a program, such ascutting samples, projects -and publications-, but these areonly part of the solution. Methodological and processingchanges must continue to keep pace or even lead the way.The decisions to use administrative data, to adopt comput-erized testing of data while returns are still present, and tomake more use of prior-year data in perfecting data for thecurrent year are examples of the kinds of steps that arereally needed. Some of these steps might have beenintroduced earlier, had the incentive to revise the SOIprocessing system been present. The budget reductions ofrecent years have provided that incentive.

While samples may be redesigned and better methodsfound to estimate totals, partly to help offset the reductionsin samples necessitated in recent years, further reductionsin the size of samples will now seriously compromise thereliability of the data. Therefore, future savings will have tocome from continued efforts to develop more efficientmethods of data processing. These efforts will enable theStatistics of Income Division to meet the needs for morestatistical data that are expected over the next few years,while releasing the regular SOI reports and studies on amore timely basis. They should also enable the Division todevote resources to new areas of research and to satisfy theneeds of its major users, while at the same time helping itadjust to any further budget reductions. -

NOTES AND REFERENCES

(1] See The Federal Statistical System, 1980 to 1985,Committee on Government Operations, U.S. House ofRepresentatives, 1 984, a report - prepared . for the

Statistics of Income: A By-Product of the U.S. Tax System

Congressional Research Service, Library of Congress,by the Baseline Data Corporation.

[2] See section 6103(a), Internal Revenue Code of 1986.

[3] Statistical editing involves adjusting certain taxpayerentries based on supplemental information reportedelsewhere in the return, usually in schedules thatsupport a reported total. Editing also includes theconstructing of certain totals for the statistics that arereported in a format that differs from the official taxform, using information from the taxpayer's improvisedschedules. (The Internal Revenue Service permitssome latitude on how certain information is reportedas long as it is correctly reported).

Editing is designed to help overcome some of thelimitations inherent in tax return statistics that are dueto nonstanclarclized reporting. It also helps to achievecertain statistical definitions desired by a user. Anexample of the former occurs when corporations filebalance sheets of their own design instead of usingthe balance sheet schedule that appears on the returnform; in this case, the statistical editor must attempt torecast the taxpayer's balance sheet into the officialformat of the return so that uniform statistics can beproduced. An example of the latter is when editors arerequired to examine cost of goods sold schedules forany depreciation reported there in order to augmentthe depreciation deduction on the return-an objec-tive that is of far greater interest to tax policyrnakersand national income economists than a cost of goodssold figure that may otherwise be correct from anaccounting standpoint.

While statistical editing is minimal in producing indi-vidual income tax return statistics (and, when it isnecessary, can often be accomplished through com-puterized imputations), it is a major factor in producingcorporation income tax return statistics because of thecomplexity of many of the returns, particularly those ofthe larger corporations which dominate the statistics.The need for editing accounts for a large part of SOIprocessing costs.

[4] For a more detailed history of SOI, see U.S. InternalRevenue Service, Statistics Division, Statistics of In-come, 50th year, 1916-1965, Historical Summary,-Individuals, Corporations, Partnerships, 1965, unpub-lished. A more concise history is contained in U.S.Internal Revenue Service, Statistics of Income Divi-sion, Statistics of Income Programs, 70th AnniversaryCelebration, 1913-1983, 1983, unpublished. For ahistory of the individual income tax return statisticalprogram, see Paris, David and Hilgert, Cecelia, "70thYear of Individual Income and Tax Statistics, 1913-

[5]

113

1982," Statistics of Income Bulletin, Winter 1983-84,Volume 3, Number 3. Other articles in this 75thanniversary commemorative issue should also beconsulted.

The adjustments necessary to conform corporate prof-its reported in Statistics of Income (SOI) with thecoverage and definition of corporate profits in theNational Income and Products Accounts (NIPA) aredescribed in detail in U.S. Department of Commerce,Bureau of Economic Analysis, Corporate Profits: Prof-its Before Tax, Profits Tax Liability, and Dividends,1985, Methodology Paper Series MP-2.

In brief, SOI data become available about 3 years afterthe income year to which they relate and this deter-mines the approach used in preparing the NIPAestimates. Each July, the existing estimates for a yearfor which SOI data are newly available are replacedwith estimates based on SOI. The major adjustmentsto SOI corporate profits data can be summarized asfollows:

a. An allowance is added for the underreporting ofcorporate income disclosable by Internal RevenueService (IRS) audit examination.

b. IRS deductions that are not elements of costs ofcurrent production are added back, e.g., deple-tion, amounts "expensed" currently that are inexcess of depreciation for mining exploration anddevelopment costs and for "intangible drillingcosts"; State and local profits tax accruals; and baddebt allowances in excess of actual losses.

c. Elements of costs of current production that are notIRS current deductions, are subtracted, specificallythe costs of trading or issuing corporate securities.

d. Elements of domestic income from current produc-tion that are not IRS "income" are added, e.g.,income of Federal Reserve Banks and other U.S.sponsored credit agencies; savings and loan asso-ciation profits (SOI data for this industry are notused because of discontinuities in the treatment ofbad debts); and income from credit unions (whichare tax-exempt). (Note that SOI profits includetax-exempt interest on State and local Governmentobligations which is reported on the tax return andwhich is added to taxable net income for the profitstatistics.)

e. Elements of IRS income that are not domesticincome from current production are excluded, e.g.,gain or loss from most sales of property; intercor-

114 Statistics of Income: A By-Prbduct of the U.S. Tax System

porate dividends received from domestic corpora-tions; and income or equities in foreign corpora-tions and branches.

[61 U.S. Department of the Treasury, Internal RevenueService, Annual Report of the Commissioner of Inter-nal Revenue, various fiscal years, 1945-1960. , :

[7]

181

191

Based on U.S. Internal Revenue Service, ReturnsProcessing and Accounting Division, "Overview ofReturns Processing in IRS Service Centers," 1984,unpublished.

processing, when commissions were identified bystatistical editors on the return lines in support of total'bther income", they were transferred to salaries andwages. Because the return entries in support of total"other income" are not transcribed for administrativeprocessing, the most that can now be done undercomputer-assisted editing is to identify the returns with"other income" for manual review. However, becauseof the large number of returns with "other income" andthe need-to reduce costs, only those returns with alarge amount reported for "other incomd' are nowreviewed.

Returns in each service center are assembled andnumbered in groups of 100 returns within each of thereturn processing categories used in administrativeprocessing. Each grouping of returns is known as a"block."

Initial plans to integate statistical processing into anenlarged administrative processing. system in the so-called "System of the 70's" were never implementedbecause of budget constraints which prevented theInternal Revenue Service from acquiring the newdomputer -systerffcalled for in the plan. Budget restric-_tions were further compounded by concerns in,theU.S. Congress about the privacy of taxpayer informa-tion under the new system proposed. .

[10] For example, without manually examining the individ-ual income tax return, it is not possible to determine ifthe taxpayer has reported commission income as anitem of miscellaneous income under "other income,".instead of in salaries and wages (as the. tax returninstructions request). Formerly, during manual SOI

[111 For additional information about future plans, see, forexample, Statistics of Income Division, U.S. InternalRevenue Service. (1985) Proposed Multi-year Operat-ing Plan, Statistics of Income Division, FY 1986-92,Volurne 1, Basic Operating Plan, 1986, unpublished.

[12] The setting for this new system is described in U.S.Internal Revenue Service, Statistics of Income Divi-sion, "Information Systems Requirements AnalysisReport: Statistics of Income Distributed ProcessingSystem,~' 1984, unpublished.

[13] For example, see Hinkins, Susan, "Matrix Samplingand the Effects of Using Hot Deck Imputation," 1986Proceedings of the American Statistical Association,Section on Survey Research Methods.

[1 4] The need for adjustments for carrybacks is discussedin the article by Ralph B. Bristol, Jr., "Tax Modellingand. the Policy Environment of the 1990's", alsocontained in this issue of the Statistics of IncomeBulletin. ,