Embed Size (px)

Citation preview

Status: Draft

Statoil’s business area

Statoil module – Field Development - MEK4450 - 2011

Magnus Nordsveen

Status: Draft

Content 1st lecture

1st hour

• Oil & gas reserves

• Statoil’s current operations

• Statoil’s strategy

2nd hour

• Example of a field development

Status: Draft

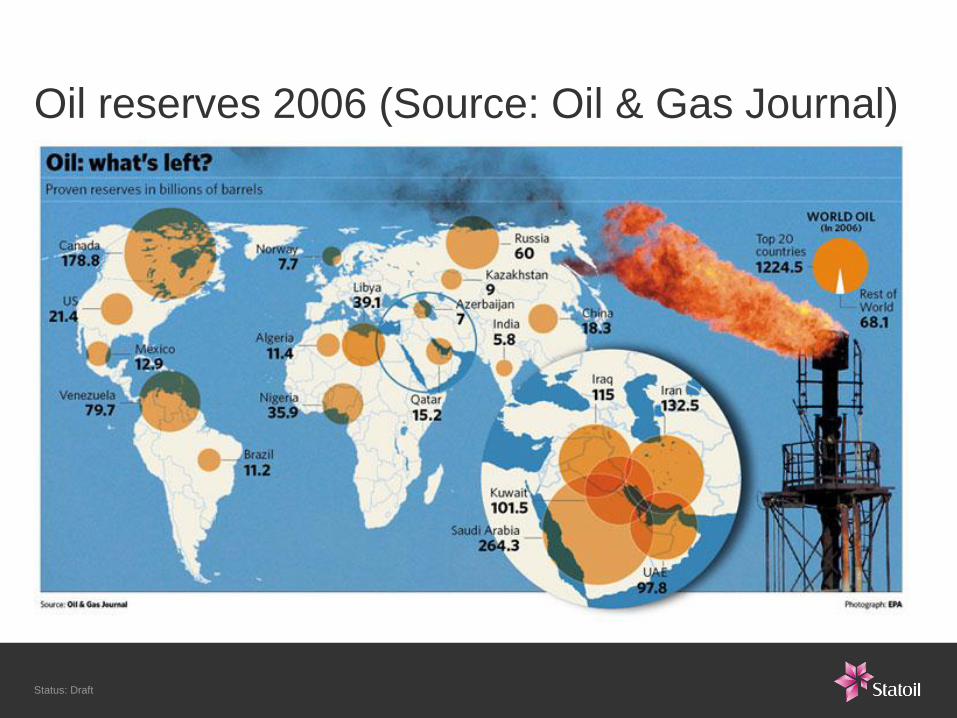

Oil reserves 2006 (Source: Oil & Gas Journal)

Status: Draft

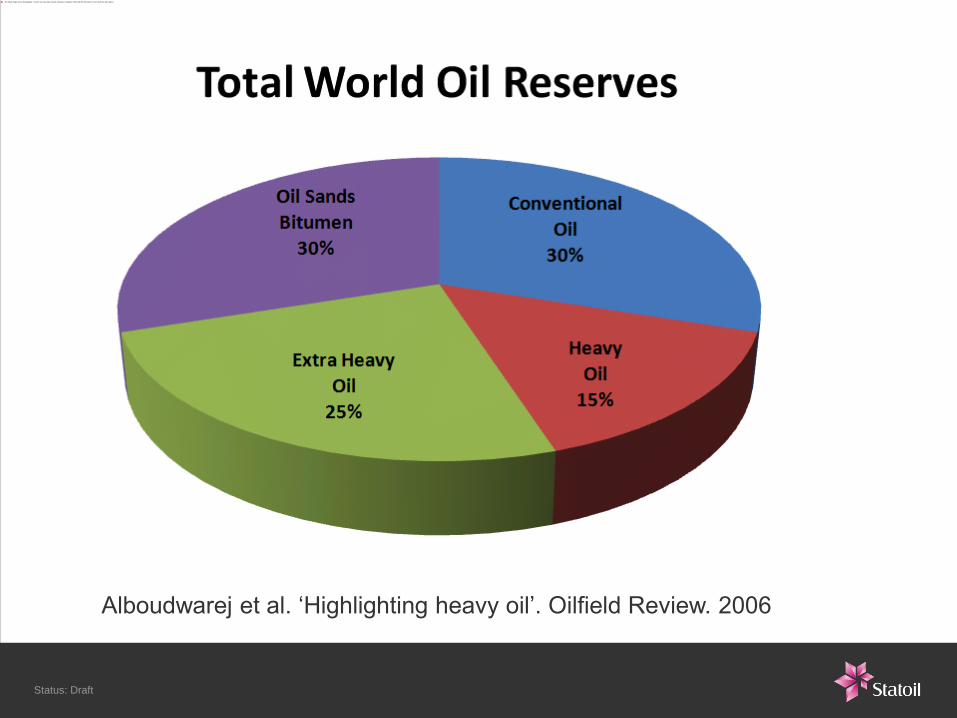

Alboudwarej et al. ‘Highlighting heavy oil’. Oilfield Review. 2006

Status: Draft

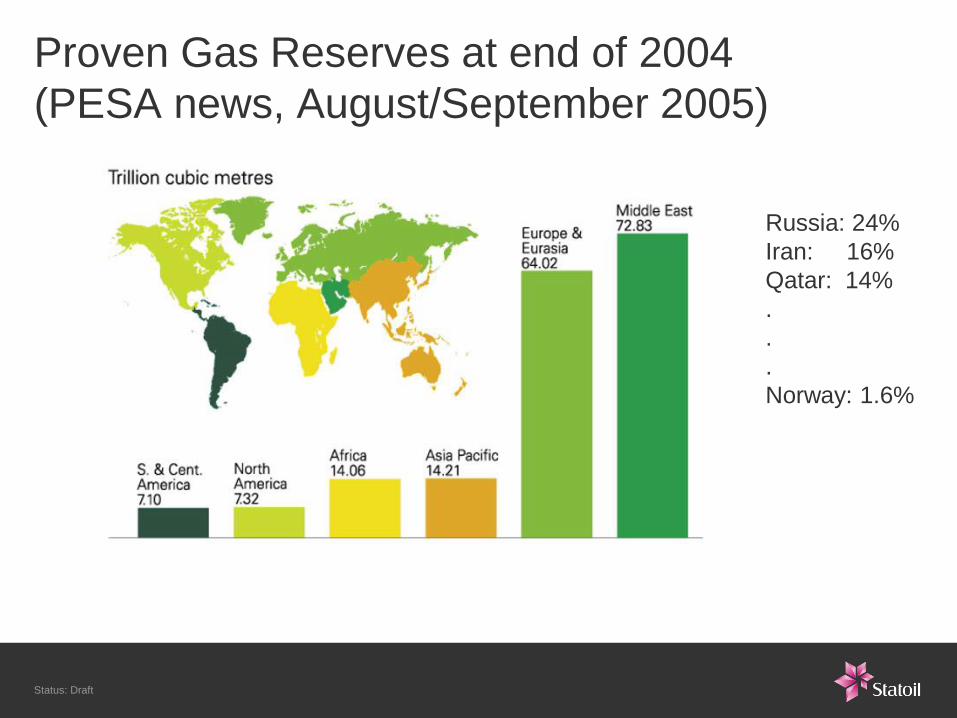

Proven Gas Reserves at end of 2004

(PESA news, August/September 2005)

Russia: 24%

Iran: 16%

Qatar: 14%

.

.

.

Norway: 1.6%

Status: Draft

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

R

ussia

Ir

an

Q

atar

S

audi A

rabia

U

nite

d Sta

tes

A

bu-D

habi

Nig

eria

V

enezu

ela

A

lgeria

In

donesi

a

Ir

aq

A

ustra

lia

C

hina

T

urkm

enist

an

N

orway

M

alays

ia

E

gypt

K

azak

hstan

K

uwai

t

U

zbeki

stan

C

anada

Libya

A

zerb

aijan

N

ethe

rlands

In

dia

U

krai

ne

P

akista

n

B

olivia

O

man

R

omani

a

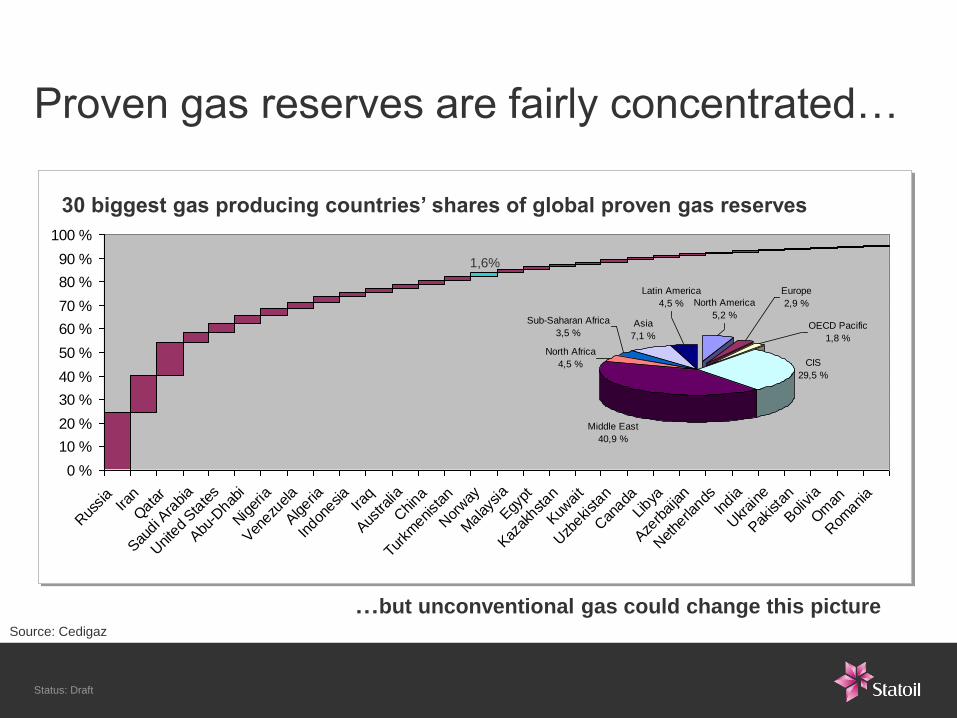

Proven gas reserves are fairly concentrated…

Source: Cedigaz

CIS

29,5 %

Middle East

40,9 %

North Africa

4,5 %

Sub-Saharan Africa

3,5 %Asia

7,1 %

Latin America

4,5 % North America

5,2 %

Europe

2,9 %

OECD Pacific

1,8 %

…but unconventional gas could change this picture

1,6%

30 biggest gas producing countries’ shares of global proven gas reserves

Status: Draft

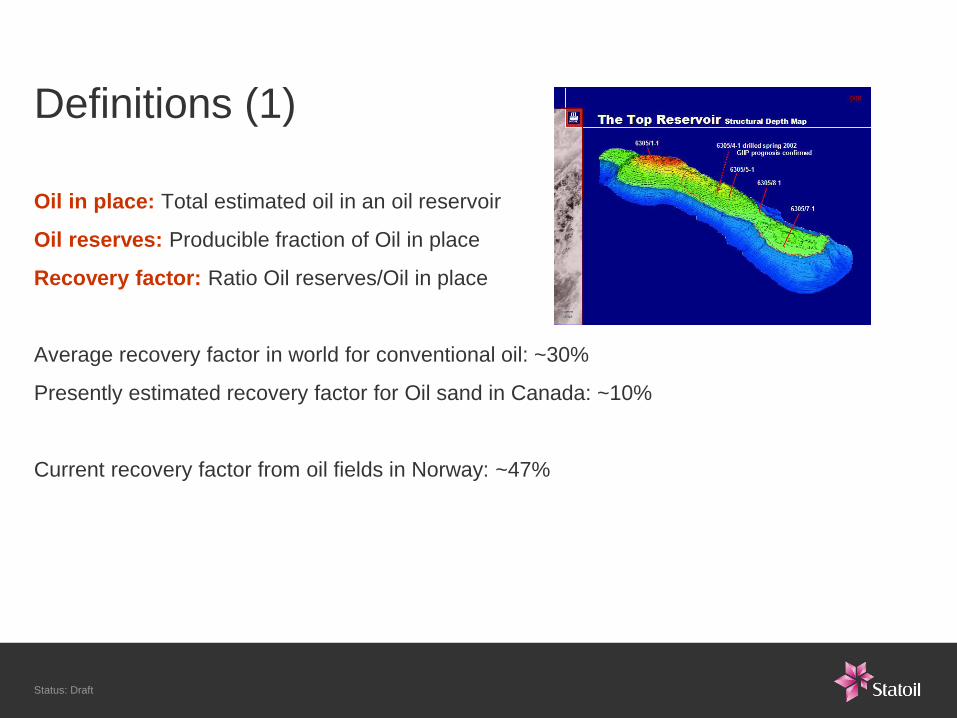

Definitions (1)

Oil in place: Total estimated oil in an oil reservoir

Oil reserves: Producible fraction of Oil in place

Recovery factor: Ratio Oil reserves/Oil in place

Average recovery factor in world for conventional oil: ~30%

Presently estimated recovery factor for Oil sand in Canada: ~10%

Current recovery factor from oil fields in Norway: ~47%

Status: Draft

Definitions (2)

Barrel of oil equivalent (boe):

• Energy released by burning one barrel of crude oil: ~1.7 MWh

( 1 barrel ~ 159 litres = 0.159 m3)

• Corresponds to about 165 m3 natural gas: ~1000 barrels

Status: Draft

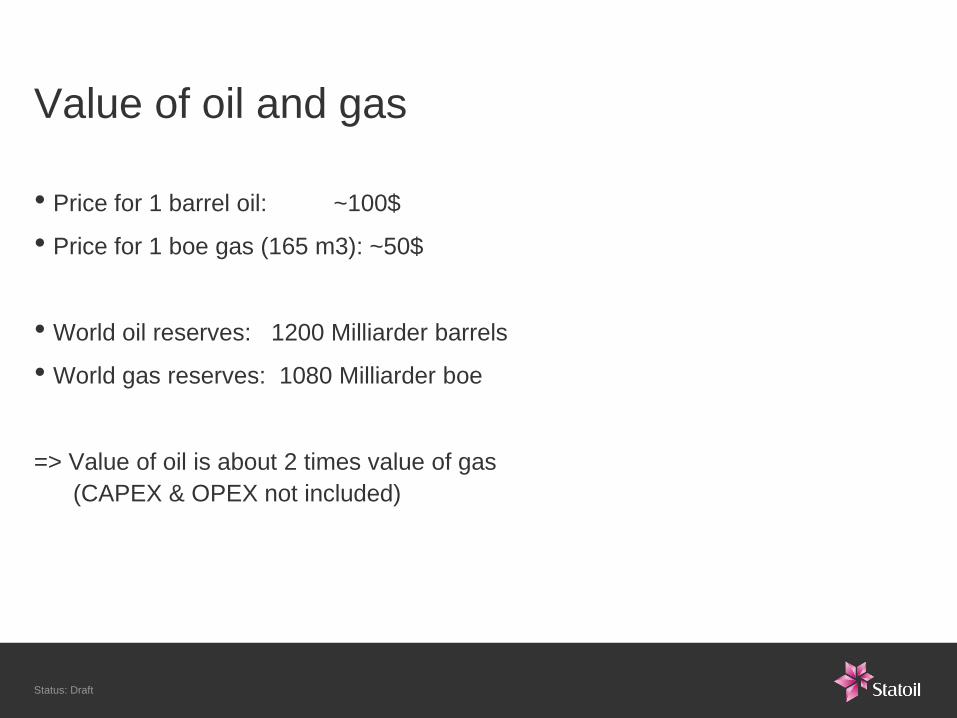

Value of oil and gas

• Price for 1 barrel oil: ~100$

• Price for 1 boe gas (165 m3): ~50$

• World oil reserves: 1200 Milliarder barrels

• World gas reserves: 1080 Milliarder boe

=> Value of oil is about 2 times value of gas

(CAPEX & OPEX not included)

Status: Draft

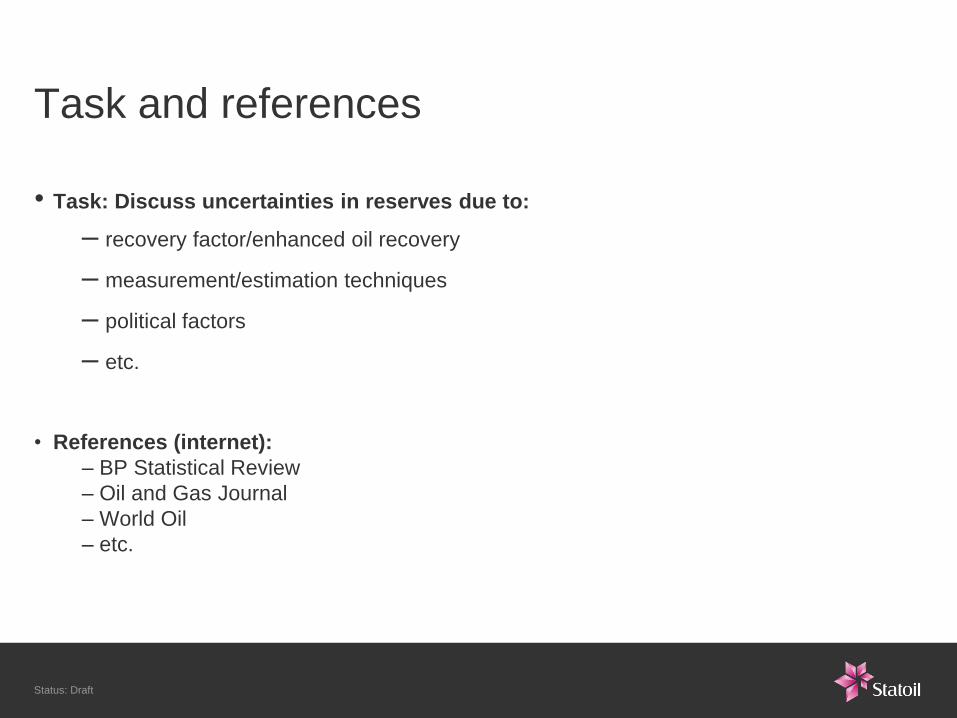

Task and references

• Task: Discuss uncertainties in reserves due to:

– recovery factor/enhanced oil recovery

– measurement/estimation techniques

– political factors

– etc.

• References (internet):

– BP Statistical Review

– Oil and Gas Journal

– World Oil

– etc.

Status: Draft

Content 1st lecture

1st hour

• Oil & gas reserves

• Statoil’s current operations

• Statoil’s strategy

2nd hour

• Example of a field development

Status: Draft

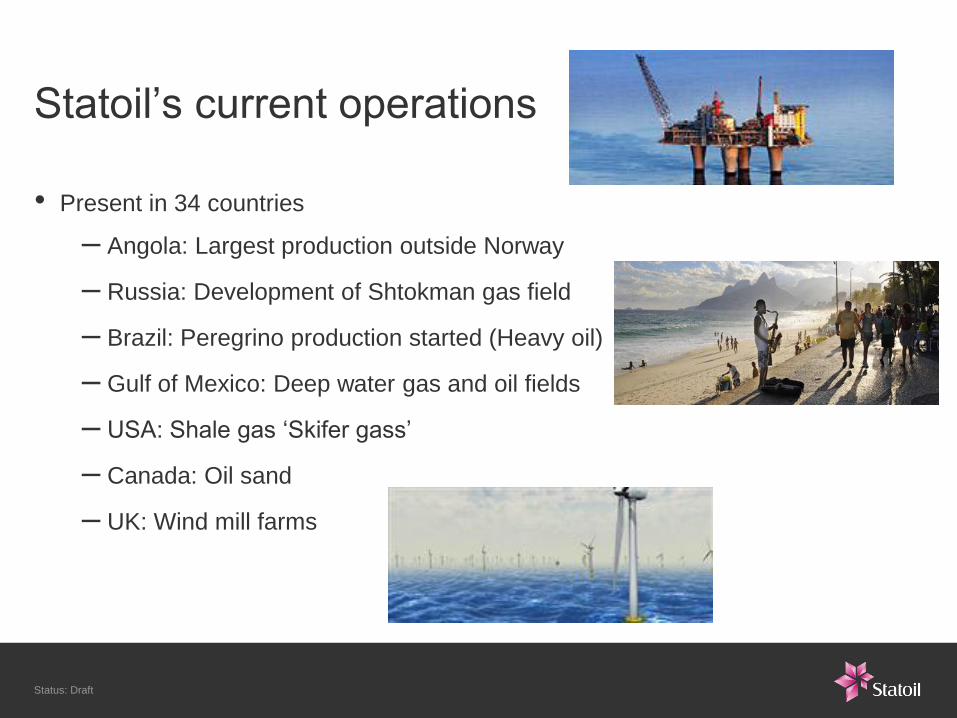

Statoil’s current operations

• Present in 34 countries

– Angola: Largest production outside Norway

– Russia: Development of Shtokman gas field

– Brazil: Peregrino production started (Heavy oil)

– Gulf of Mexico: Deep water gas and oil fields

– USA: Shale gas ‘Skifer gass’

– Canada: Oil sand

– UK: Wind mill farms

Status: Draft

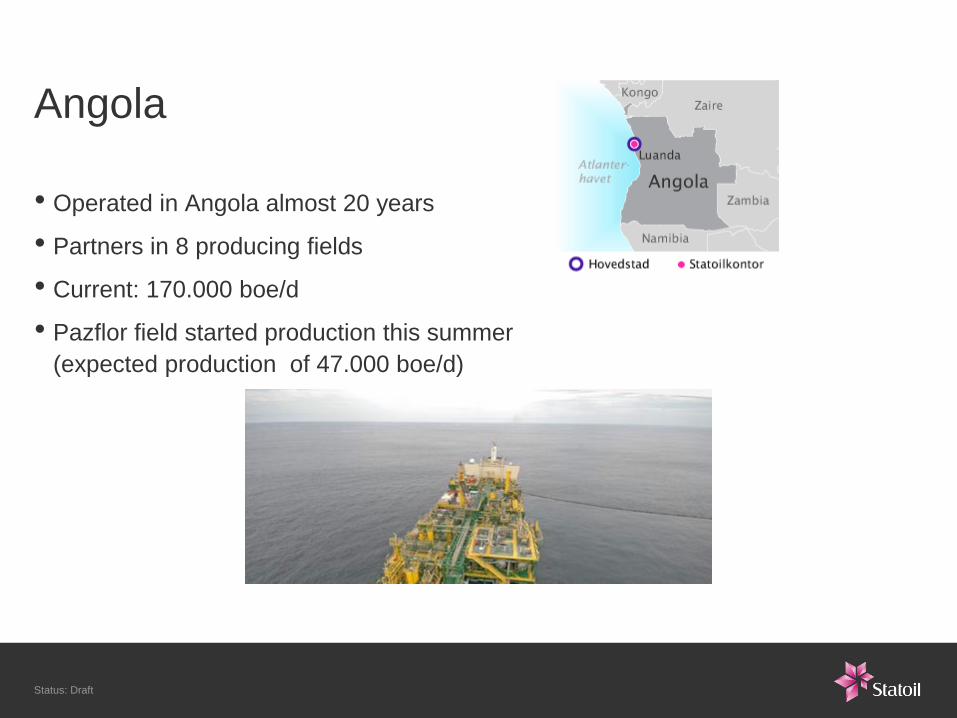

Angola

• Operated in Angola almost 20 years

• Partners in 8 producing fields

• Current: 170.000 boe/d

• Pazflor field started production this summer

(expected production of 47.000 boe/d)

Status: Draft

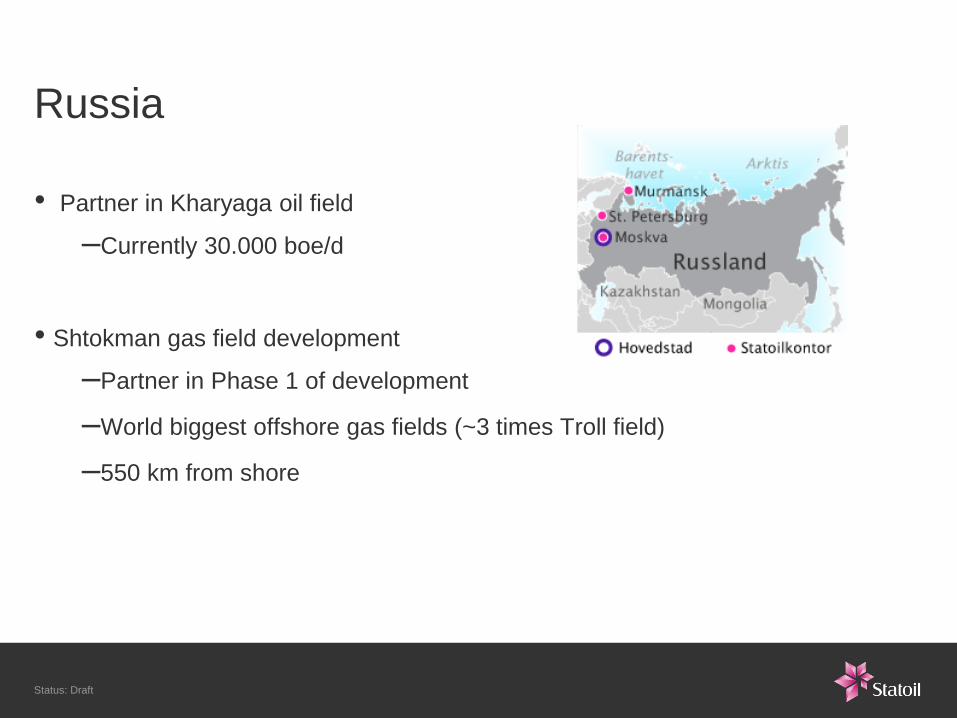

Russia

• Partner in Kharyaga oil field

–Currently 30.000 boe/d

• Shtokman gas field development

–Partner in Phase 1 of development

–World biggest offshore gas fields (~3 times Troll field)

–550 km from shore

Status: Draft

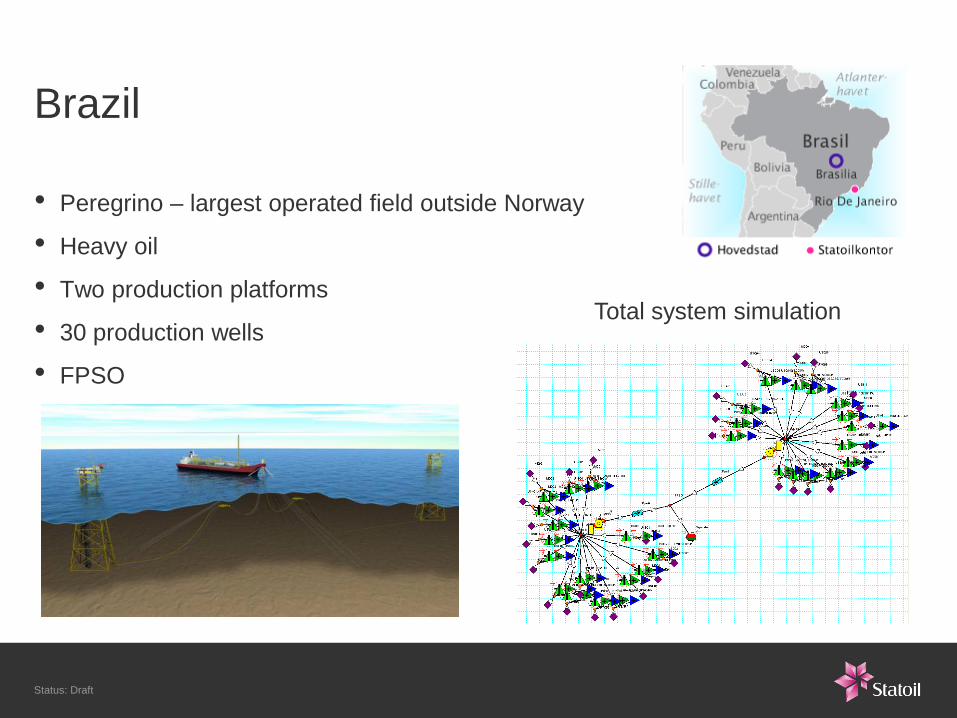

Brazil

• Peregrino – largest operated field outside Norway

• Heavy oil

• Two production platforms

• 30 production wells

• FPSO

Total system simulation

Status: Draft

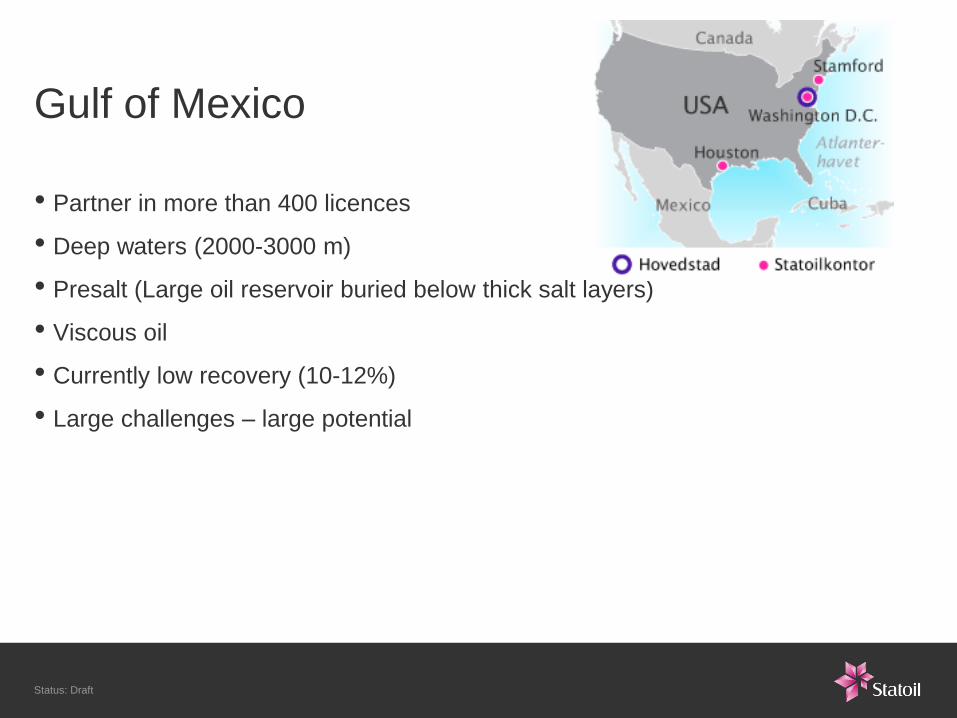

Gulf of Mexico

• Partner in more than 400 licences

• Deep waters (2000-3000 m)

• Presalt (Large oil reservoir buried below thick salt layers)

• Viscous oil

• Currently low recovery (10-12%)

• Large challenges – large potential

Status: Draft

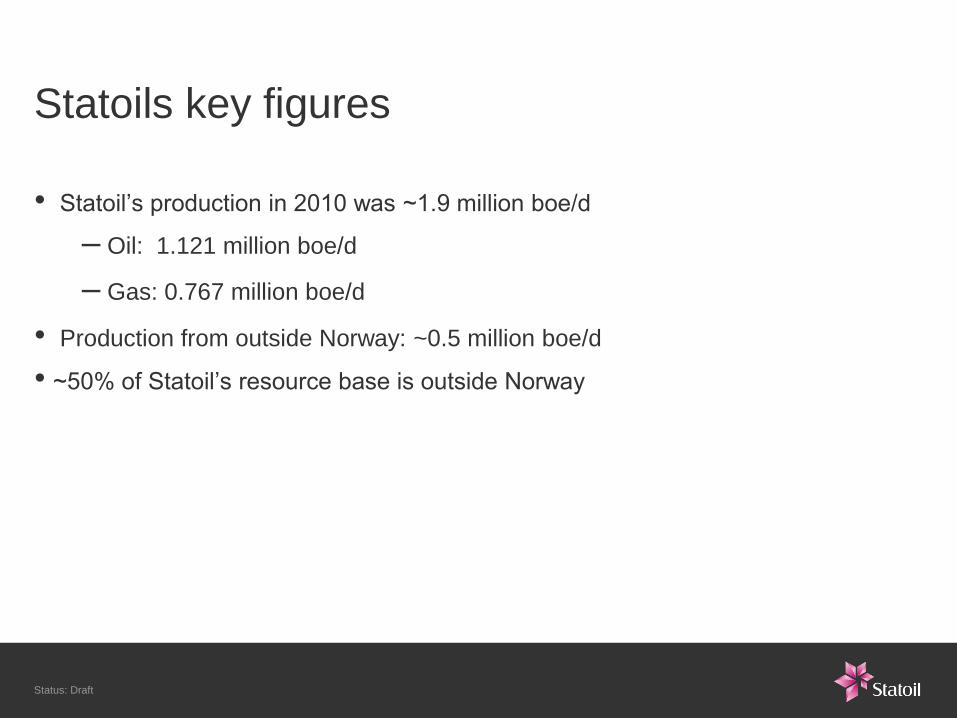

Statoils key figures

• Statoil’s production in 2010 was ~1.9 million boe/d

– Oil: 1.121 million boe/d

– Gas: 0.767 million boe/d

• Production from outside Norway: ~0.5 million boe/d

• ~50% of Statoil’s resource base is outside Norway

Status: Draft

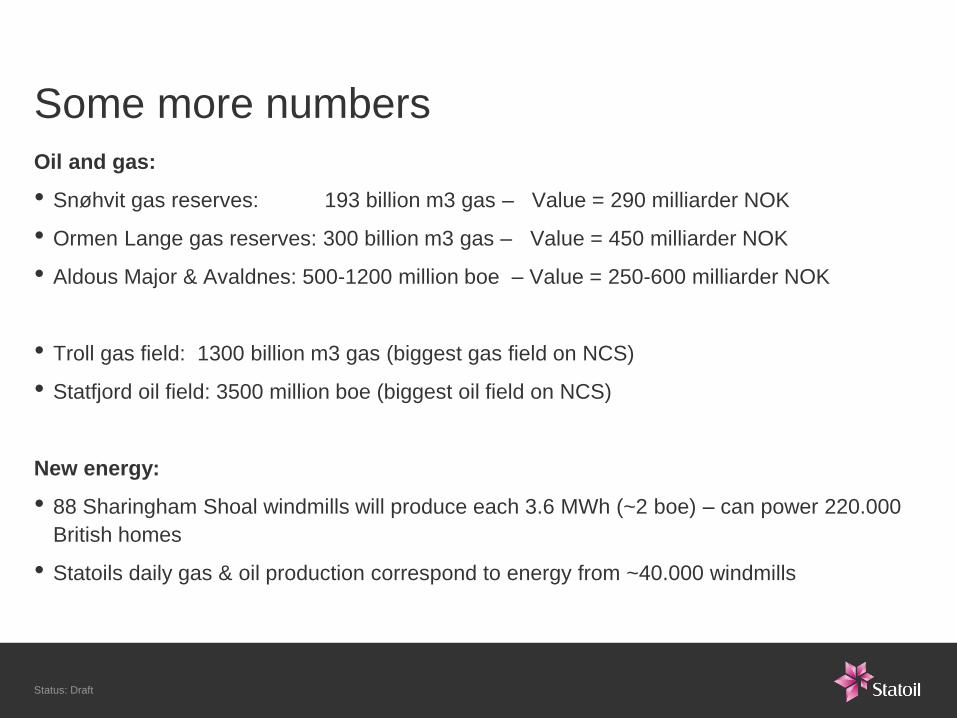

Some more numbers

Oil and gas:

• Snøhvit gas reserves: 193 billion m3 gas – Value = 290 milliarder NOK

• Ormen Lange gas reserves: 300 billion m3 gas – Value = 450 milliarder NOK

• Aldous Major & Avaldnes: 500-1200 million boe – Value = 250-600 milliarder NOK

• Troll gas field: 1300 billion m3 gas (biggest gas field on NCS)

• Statfjord oil field: 3500 million boe (biggest oil field on NCS)

New energy:

• 88 Sharingham Shoal windmills will produce each 3.6 MWh (~2 boe) – can power 220.000

British homes

• Statoils daily gas & oil production correspond to energy from ~40.000 windmills

Status: Draft

Content 1st lecture

1st hour

• Oil & gas reserves

• Statoil’s current operations

• Statoil’s strategy

2nd hour

• Example of a field development

Status: Draft

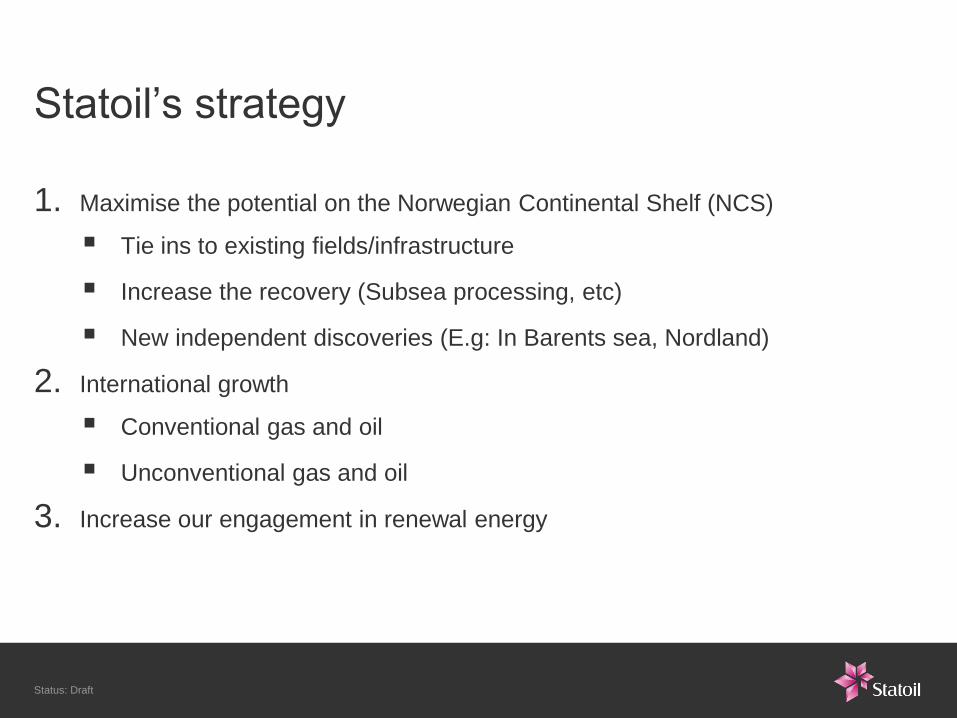

Statoil’s strategy

1. Maximise the potential on the Norwegian Continental Shelf (NCS)

Tie ins to existing fields/infrastructure

Increase the recovery (Subsea processing, etc)

New independent discoveries (E.g: In Barents sea, Nordland)

2. International growth

Conventional gas and oil

Unconventional gas and oil

3. Increase our engagement in renewal energy

Status: Draft

Challenges

• Find new oil and gas fields

• Enhanced recovery

–Smart wells (horizontal, zones, branched)

–Water/gas injection wells to maintain reservoir pressure

–ESPs (pumps in wells)

–Sub sea processing

• Transport

–Multiphase to receiving facility (floater/shore)

–Single phase to market

• Deep waters, Harsh environment, Arctic

Status: Draft

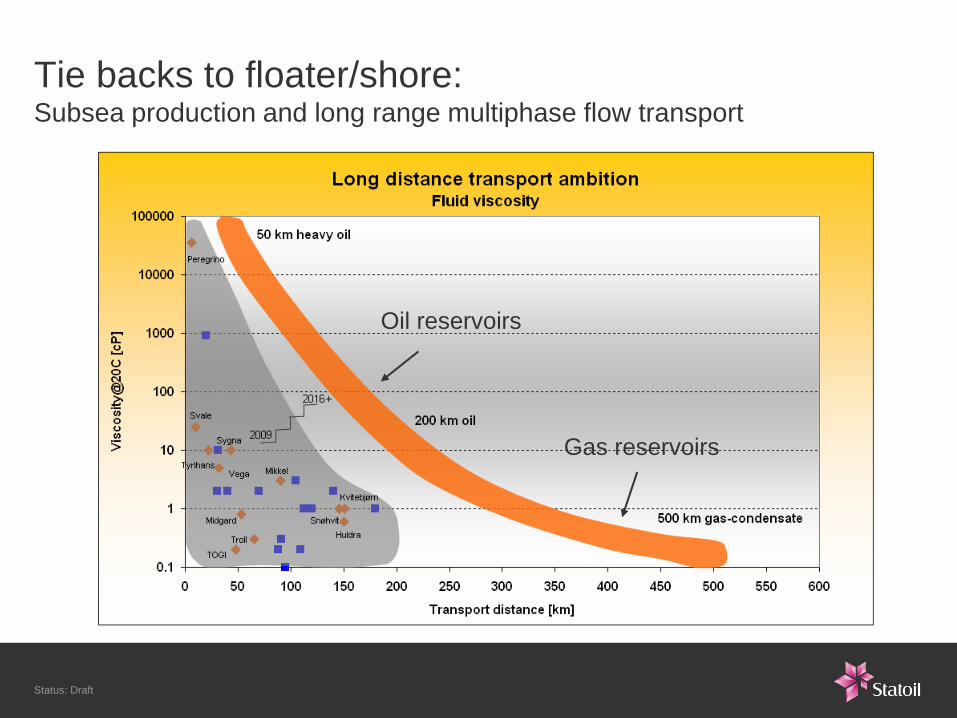

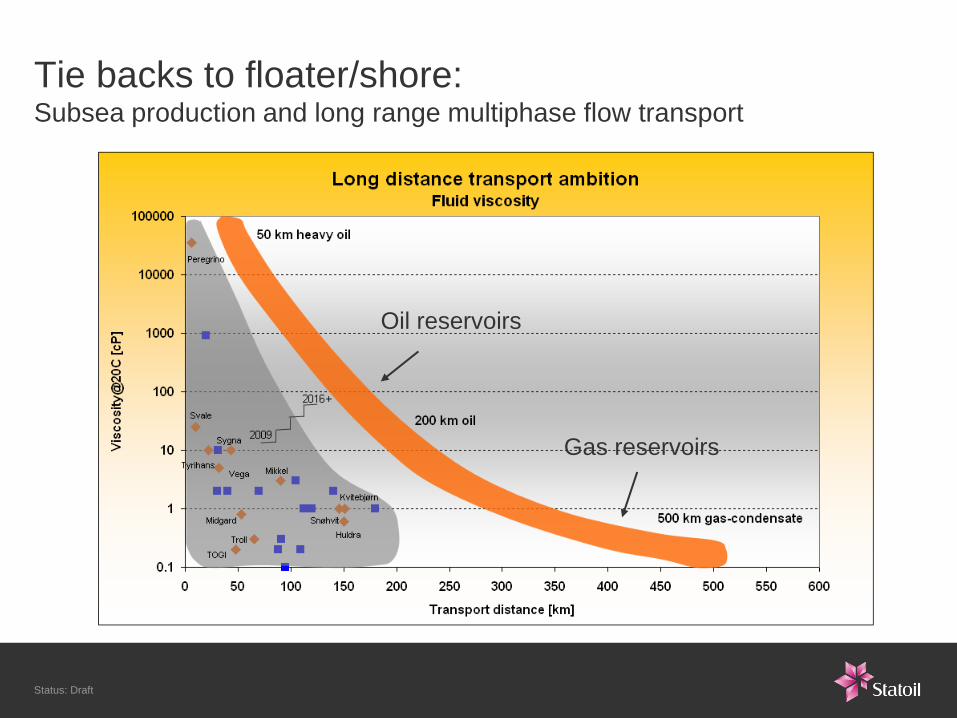

Tie backs to floater/shore: Subsea production and long range multiphase flow transport

Oil reservoirs

Gas reservoirs

Status: Draft

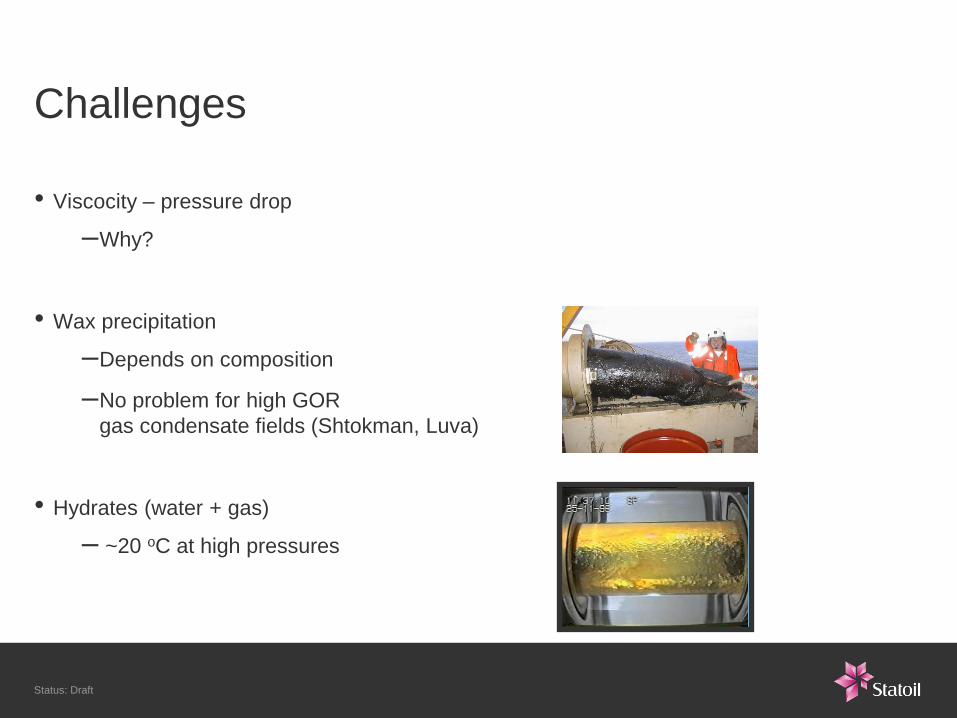

Challenges

• Viscocity – pressure drop

–Why?

• Wax precipitation

–Depends on composition

–No problem for high GOR

gas condensate fields (Shtokman, Luva)

• Hydrates (water + gas)

– ~20 oC at high pressures

Status: Draft

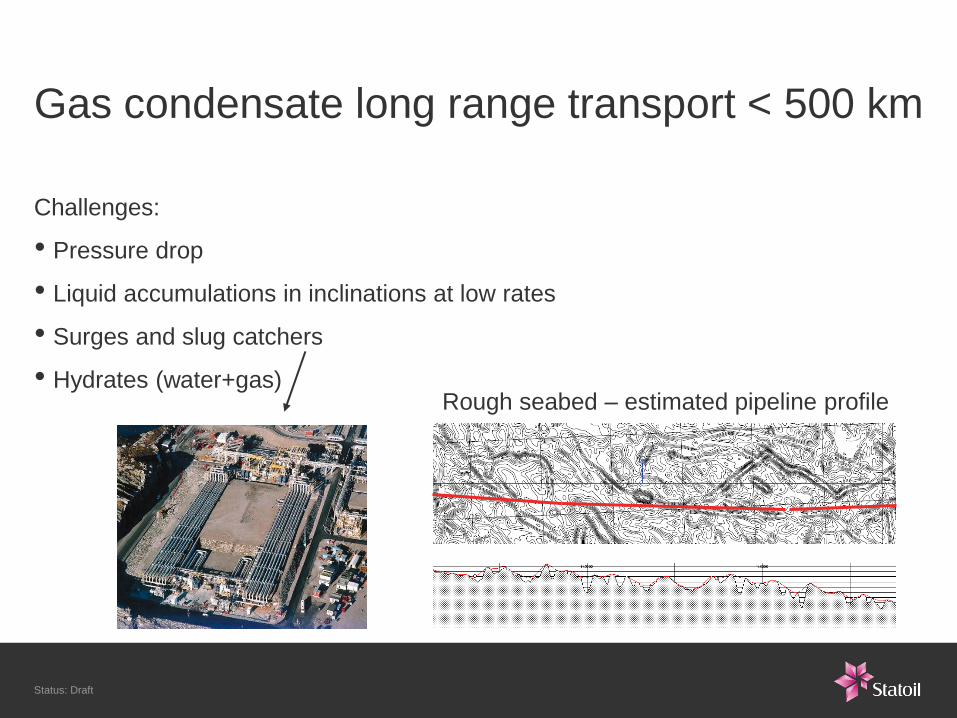

Gas condensate long range transport < 500 km

Challenges:

• Pressure drop

• Liquid accumulations in inclinations at low rates

• Surges and slug catchers

• Hydrates (water+gas) Rough seabed – estimated pipeline profile

Status: Draft

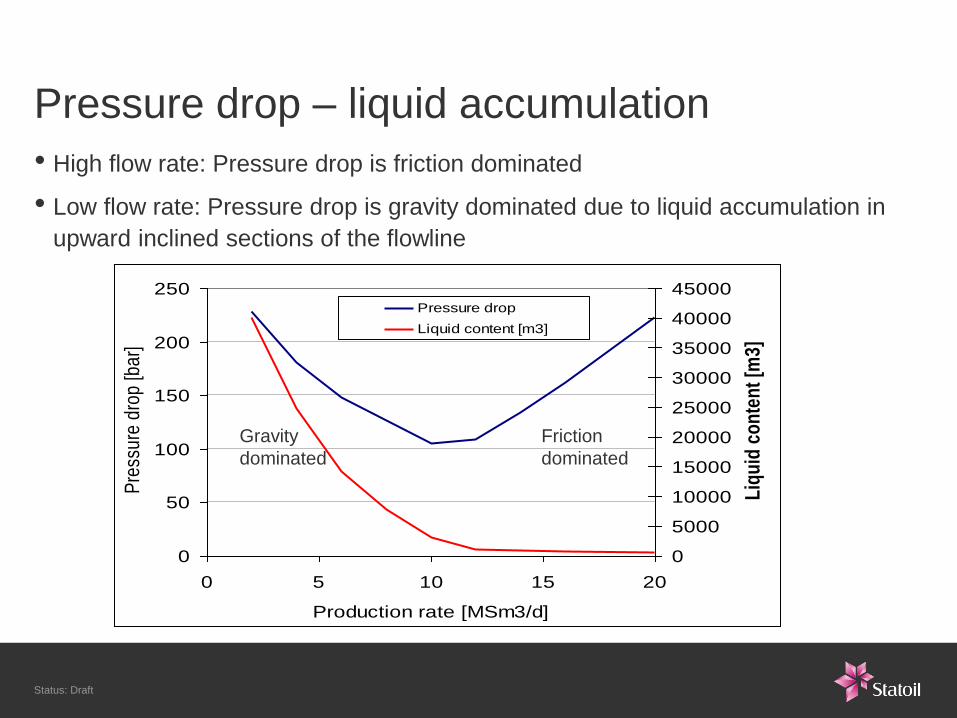

Pressure drop – liquid accumulation

• High flow rate: Pressure drop is friction dominated

• Low flow rate: Pressure drop is gravity dominated due to liquid accumulation in

upward inclined sections of the flowline

0

50

100

150

200

250

0 5 10 15 20

Production rate [MSm3/d]

Pre

ssur

e dr

op [b

ar]

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Liq

uid

co

nte

nt

[m3]

Pressure drop

Liquid content [m3]

Friction

dominated

Gravity

dominated

Status: Draft

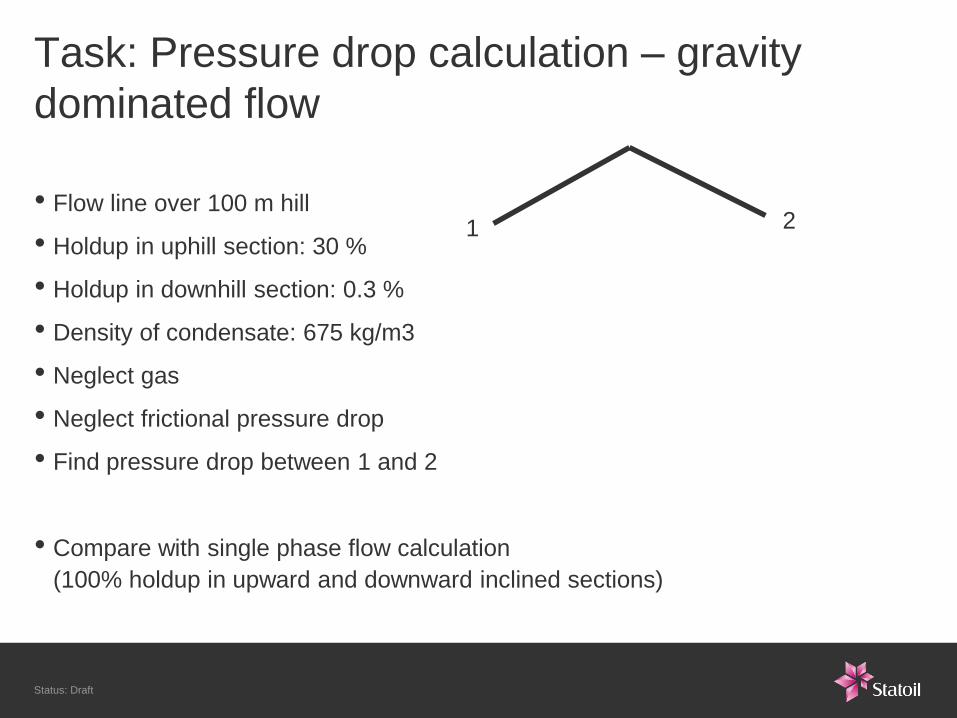

Task: Pressure drop calculation – gravity

dominated flow

• Flow line over 100 m hill

• Holdup in uphill section: 30 %

• Holdup in downhill section: 0.3 %

• Density of condensate: 675 kg/m3

• Neglect gas

• Neglect frictional pressure drop

• Find pressure drop between 1 and 2

• Compare with single phase flow calculation

(100% holdup in upward and downward inclined sections)

1 2

Status: Draft

Oil field long range transport < 200 km

• Currently < 50 km

• Challenges: Wax, hydrates

• Current solution:

–Keep temperature above hydrate temp.

(insulation or insulation + heating)

–Pigging for wax

• Future alternative: Cold flow

–Transport with particles without settling on wall/plugging

Status: Draft

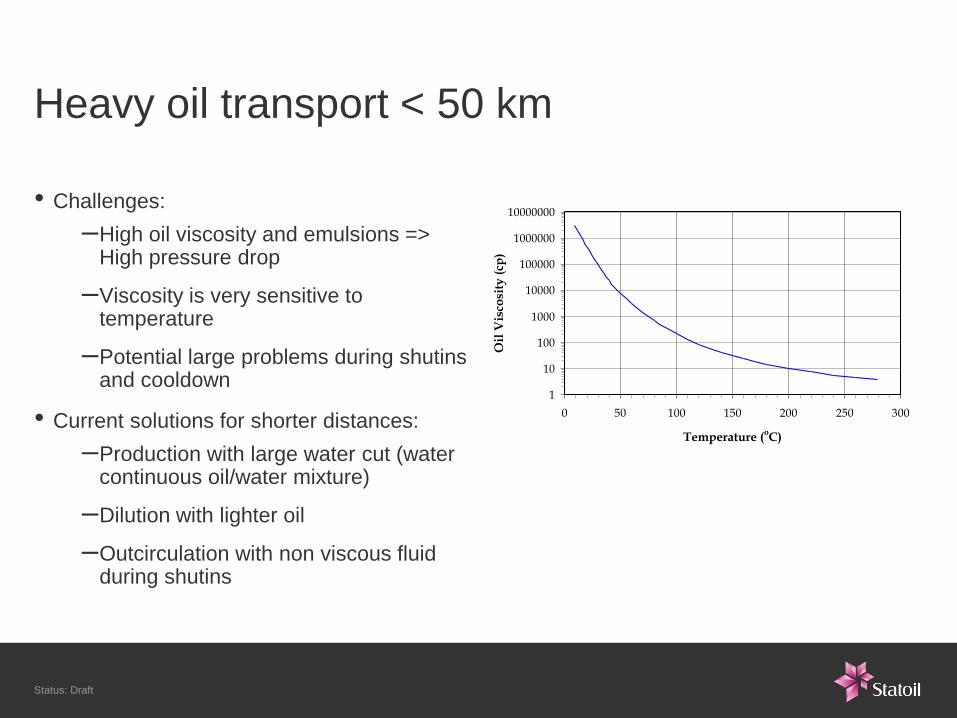

Heavy oil transport < 50 km

• Challenges:

–High oil viscosity and emulsions => High pressure drop

–Viscosity is very sensitive to temperature

–Potential large problems during shutins and cooldown

• Current solutions for shorter distances:

–Production with large water cut (water continuous oil/water mixture)

–Dilution with lighter oil

–Outcirculation with non viscous fluid during shutins

Athabasca Bitumen, Canada (8.6oAPI)

1

10

100

1000

10000

100000

1000000

10000000

0 50 100 150 200 250 300

Temperature (oC)

Oil

Vis

cosi

ty (

cp)

Status: Draft

Tie backs to floater/shore: Subsea production and long range multiphase flow transport

Oil reservoirs

Gas reservoirs

Status: Draft

Statoil New Energy

Offshore wind

Carbon capture and storage

Geothermal energy, Biofuel and Hydrogen

Status: Draft

Stepwise development of new energy platform

Our main focus is on offshore wind power where we add value by using our

extensive competence from offshore oil and gas activities

• Sheringham Shoal Offshore Wind Farm

• Dogger Bank – Asset for growth

• Hywind – Proven floating wind mill concept

Status: Draft

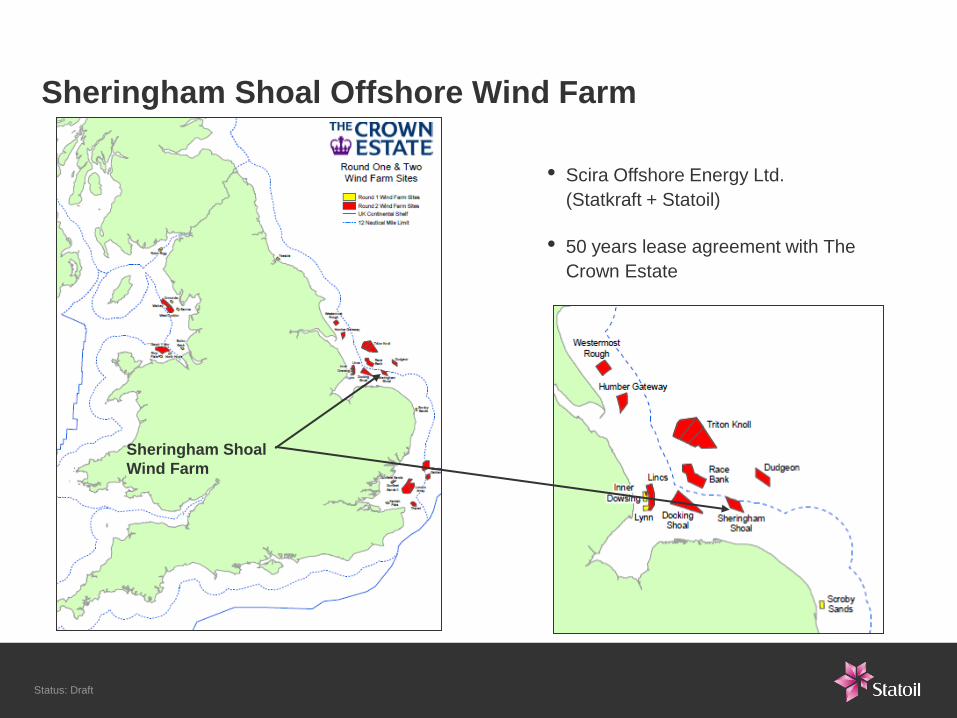

Sheringham Shoal Offshore Wind Farm

• Scira Offshore Energy Ltd.

(Statkraft + Statoil)

• 50 years lease agreement with The

Crown Estate

Sheringham Shoal

Wind Farm

Status: Draft

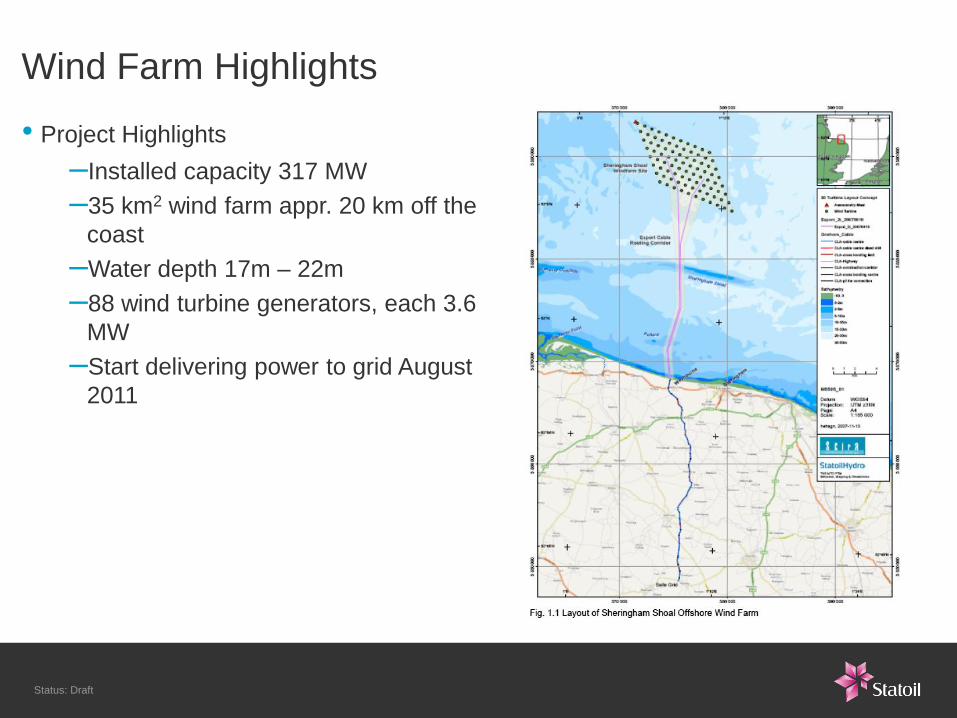

• Project Highlights

–Installed capacity 317 MW

–35 km2 wind farm appr. 20 km off the

coast

–Water depth 17m – 22m

–88 wind turbine generators, each 3.6

MW

–Start delivering power to grid August

2011

Wind Farm Highlights

Status: Draft 34 - Classification: Internal 2010-11-24

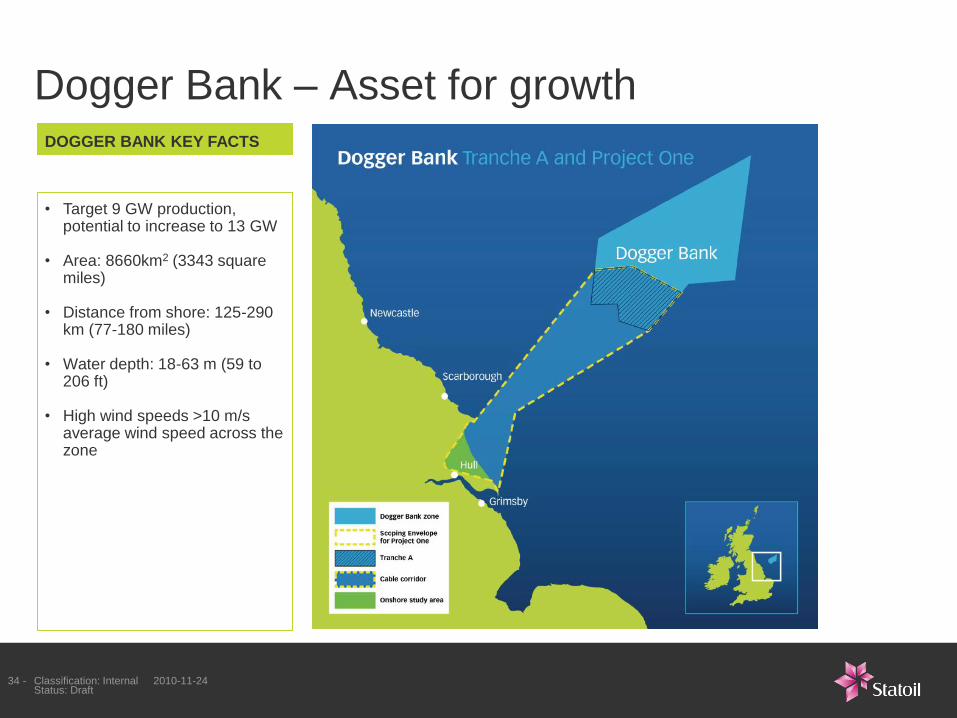

Dogger Bank – Asset for growth

• Target 9 GW production, potential to increase to 13 GW

• Area: 8660km2 (3343 square

miles)

• Distance from shore: 125-290 km (77-180 miles)

• Water depth: 18-63 m (59 to

206 ft) • High wind speeds >10 m/s

average wind speed across the zone

DOGGER BANK KEY FACTS

Status: Draft

Status: Draft

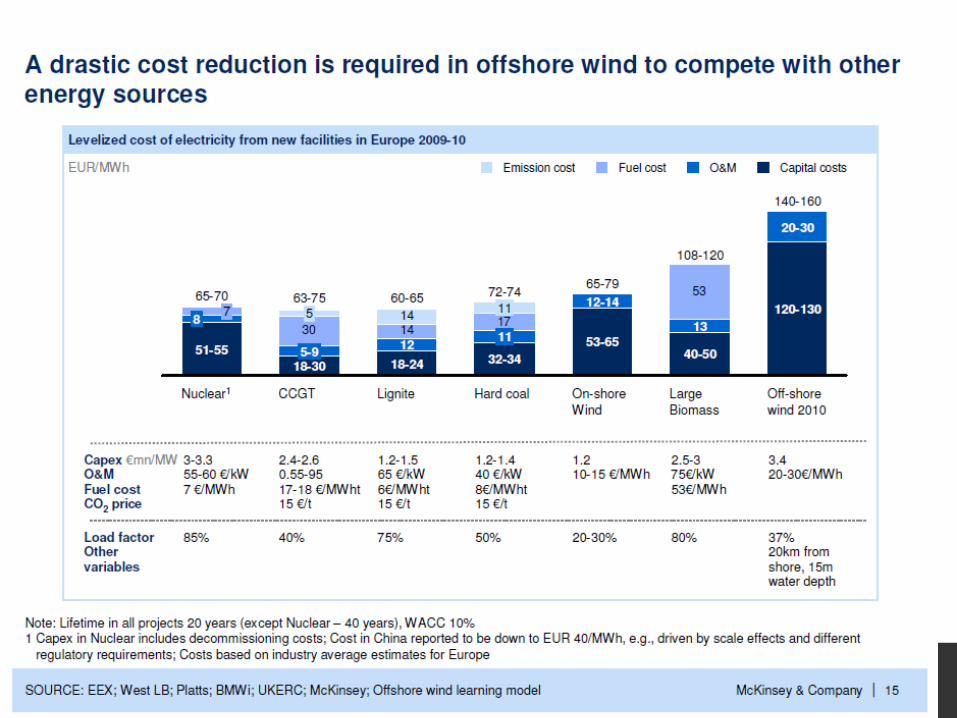

Cost of Energy could reach grid parity in high cost

electricity markets during the next decade

• Potential for further cost reduction

–Lighter / cheaper turbines

–Mass production

–Supply chain development

–Improved installation methods

Status: Draft

References for Statoil

• www.statoil.com

• Statoil in Brief: 2010/11 (brochure)

Status: Draft

Thank you