Embed Size (px)

Citation preview

12/05/2015

1

China Metallurgical Industry Planning and Research Institute

PLAN FOR FUTURE STUDY FOR DEVELOPMENT

May, 2015

Steel Market in China

Li Xinchuang

2

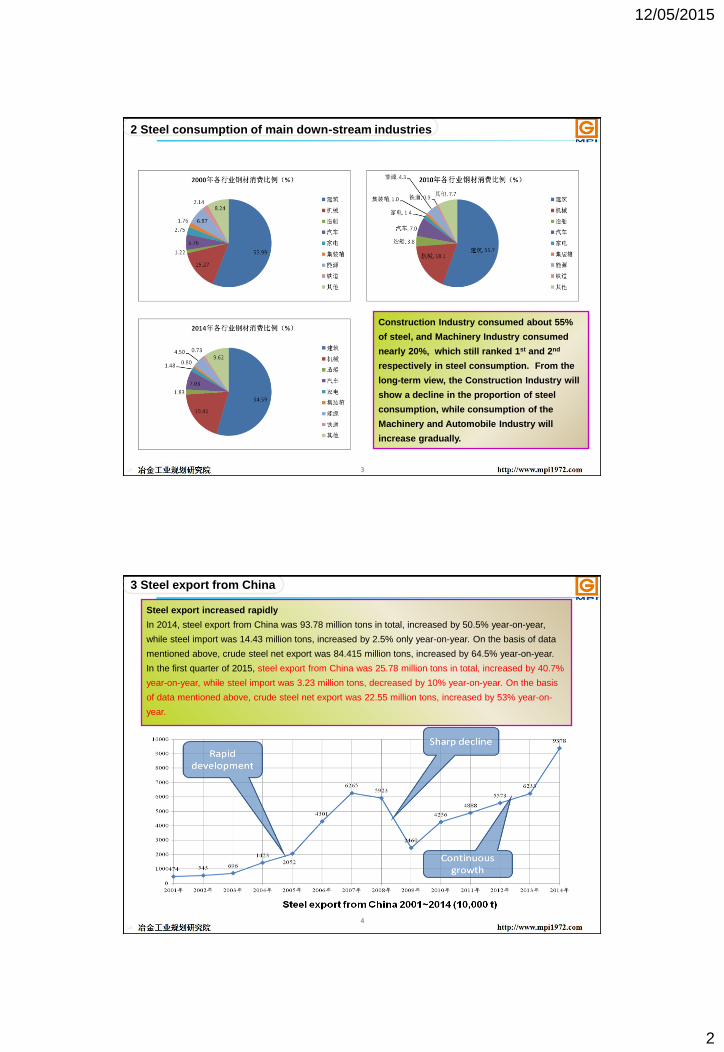

1 Actual steel consumption

★ Actual steel consumption increased by leaps and

bounds, but growth rate declined

With development of national economy especially for rapid

growth of fixed asset investment, steel consumption in China

increased dramatically. In 2014, steel produt consumption in

China was about 702 million tons, which was 23 times of 32

million tons in 1970’s, and the consumption per capita has

also went beyond 500 kg. Due to New Normal of economic

development and strategic adjustment of economic

structure, the growth of domestic actual steel consumption

decreased significantly in recent years.

12/05/2015

2

3

Construction Industry consumed about 55%

of steel, and Machinery Industry consumed

nearly 20%, which still ranked 1st and 2nd

respectively in steel consumption. From the

long-term view, the Construction Industry will

show a decline in the proportion of steel

consumption, while consumption of the

Machinery and Automobile Industry will

increase gradually.

2 Steel consumption of main down-stream industries

4

Steel export increased rapidly

In 2014, steel export from China was 93.78 million tons in total, increased by 50.5% year-on-year,

while steel import was 14.43 million tons, increased by 2.5% only year-on-year. On the basis of data

mentioned above, crude steel net export was 84.415 million tons, increased by 64.5% year-on-year.

In the first quarter of 2015, steel export from China was 25.78 million tons in total, increased by 40.7%

year-on-year, while steel import was 3.23 million tons, decreased by 10% year-on-year. On the basis

of data mentioned above, crude steel net export was 22.55 million tons, increased by 53% year-on-

year.

3 Steel export from China

12/05/2015

3

5

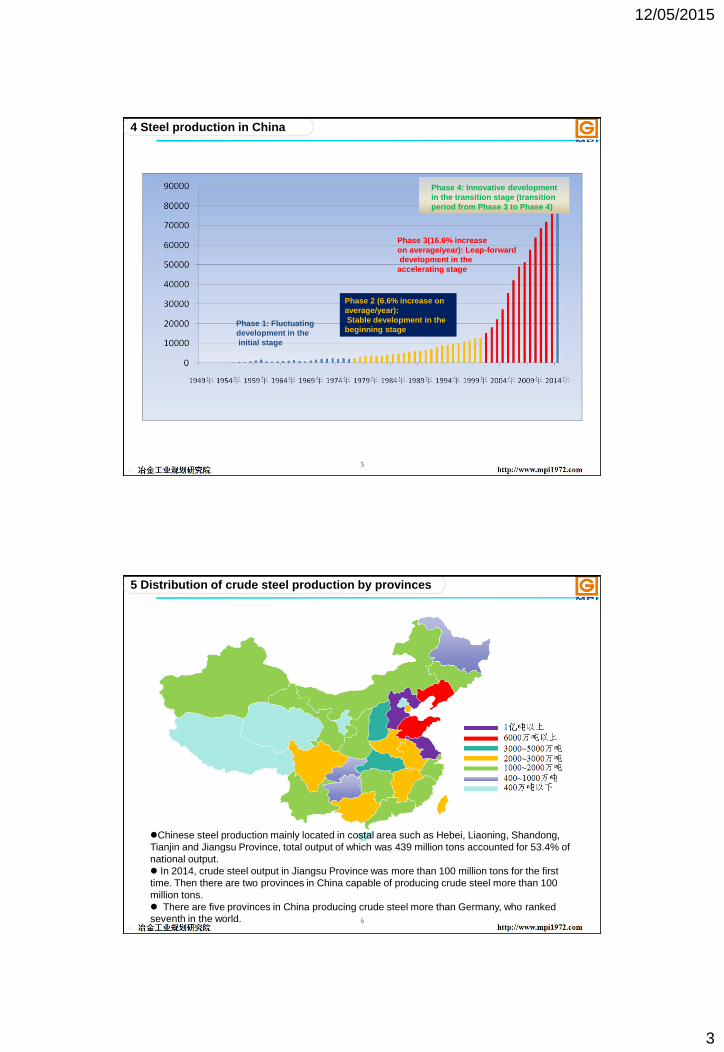

4 Steel production in China

Phase 1: Fluctuating

development in the

initial stage

Phase 2 (6.6% increase on

average/year):

Stable development in the

beginning stage

Phase 3(16.6% increase

on average/year): Leap-forward

development in the

accelerating stage

Phase 4: Innovative development

in the transition stage (transition

period from Phase 3 to Phase 4)

6

Chinese steel production mainly located in costal area such as Hebei, Liaoning, Shandong,

Tianjin and Jiangsu Province, total output of which was 439 million tons accounted for 53.4% of

national output.

In 2014, crude steel output in Jiangsu Province was more than 100 million tons for the first

time. Then there are two provinces in China capable of producing crude steel more than 100

million tons.

There are five provinces in China producing crude steel more than Germany, who ranked

seventh in the world.

5 Distribution of crude steel production by provinces

12/05/2015

4

7

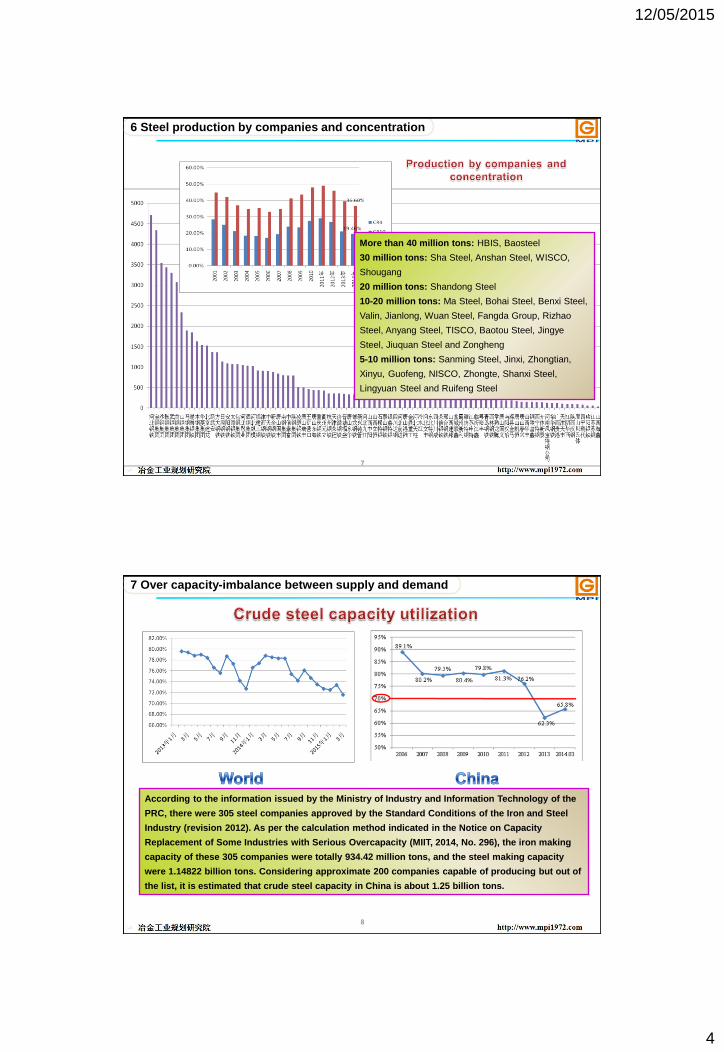

6 Steel production by companies and concentration

More than 40 million tons: HBIS, Baosteel

30 million tons: Sha Steel, Anshan Steel, WISCO,

Shougang

20 million tons: Shandong Steel

10-20 million tons: Ma Steel, Bohai Steel, Benxi Steel,

Valin, Jianlong, Wuan Steel, Fangda Group, Rizhao

Steel, Anyang Steel, TISCO, Baotou Steel, Jingye

Steel, Jiuquan Steel and Zongheng

5-10 million tons: Sanming Steel, Jinxi, Zhongtian,

Xinyu, Guofeng, NISCO, Zhongte, Shanxi Steel,

Lingyuan Steel and Ruifeng Steel

7 Over capacity-imbalance between supply and demand

8

According to the information issued by the Ministry of Industry and Information Technology of the

PRC, there were 305 steel companies approved by the Standard Conditions of the Iron and Steel

Industry (revision 2012). As per the calculation method indicated in the Notice on Capacity

Replacement of Some Industries with Serious Overcapacity (MIIT, 2014, No. 296), the iron making

capacity of these 305 companies were totally 934.42 million tons, and the steel making capacity

were 1.14822 billion tons. Considering approximate 200 companies capable of producing but out of

the list, it is estimated that crude steel capacity in China is about 1.25 billion tons.

12/05/2015

5

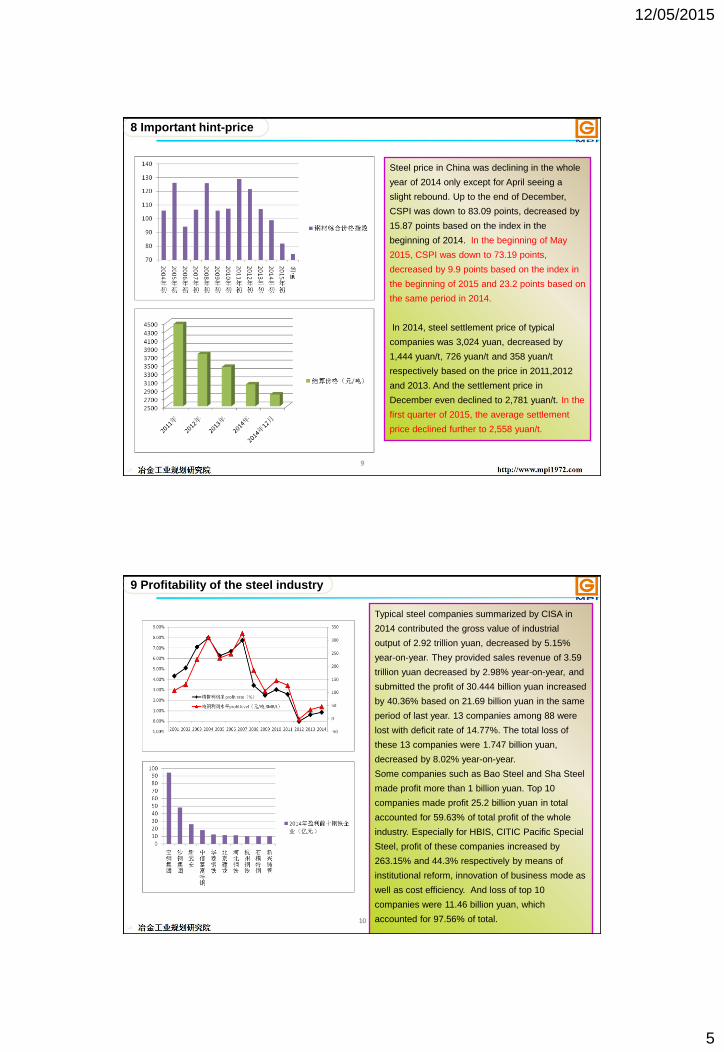

9

Steel price in China was declining in the whole

year of 2014 only except for April seeing a

slight rebound. Up to the end of December,

CSPI was down to 83.09 points, decreased by

15.87 points based on the index in the

beginning of 2014. In the beginning of May

2015, CSPI was down to 73.19 points,

decreased by 9.9 points based on the index in

the beginning of 2015 and 23.2 points based on

the same period in 2014.

In 2014, steel settlement price of typical

companies was 3,024 yuan, decreased by

1,444 yuan/t, 726 yuan/t and 358 yuan/t

respectively based on the price in 2011,2012

and 2013. And the settlement price in

December even declined to 2,781 yuan/t. In the

first quarter of 2015, the average settlement

price declined further to 2,558 yuan/t.

8 Important hint-price

10

Typical steel companies summarized by CISA in

2014 contributed the gross value of industrial

output of 2.92 trillion yuan, decreased by 5.15%

year-on-year. They provided sales revenue of 3.59

trillion yuan decreased by 2.98% year-on-year, and

submitted the profit of 30.444 billion yuan increased

by 40.36% based on 21.69 billion yuan in the same

period of last year. 13 companies among 88 were

lost with deficit rate of 14.77%. The total loss of

these 13 companies were 1.747 billion yuan,

decreased by 8.02% year-on-year.

Some companies such as Bao Steel and Sha Steel

made profit more than 1 billion yuan. Top 10

companies made profit 25.2 billion yuan in total

accounted for 59.63% of total profit of the whole

industry. Especially for HBIS, CITIC Pacific Special

Steel, profit of these companies increased by

263.15% and 44.3% respectively by means of

institutional reform, innovation of business mode as

well as cost efficiency. And loss of top 10

companies were 11.46 billion yuan, which

accounted for 97.56% of total.

9 Profitability of the steel industry

12/05/2015

6

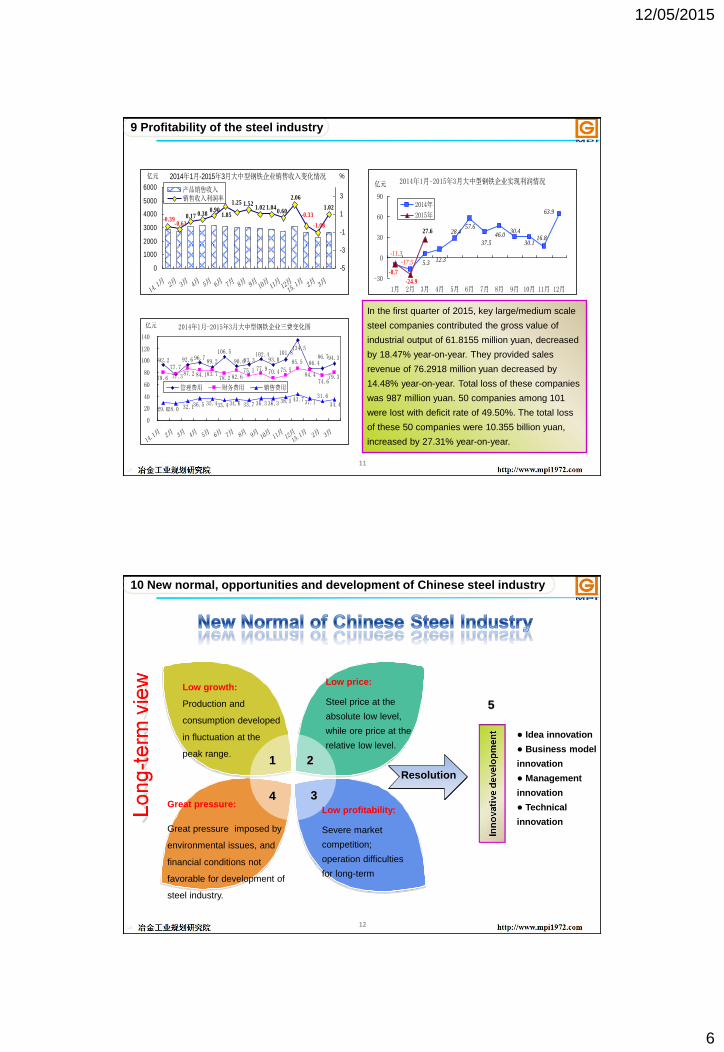

11

In the first quarter of 2015, key large/medium scale

steel companies contributed the gross value of

industrial output of 61.8155 million yuan, decreased

by 18.47% year-on-year. They provided sales

revenue of 76.2918 million yuan decreased by

14.48% year-on-year. Total loss of these companies

was 987 million yuan. 50 companies among 101

were lost with deficit rate of 49.50%. The total loss

of these 50 companies were 10.355 billion yuan,

increased by 27.31% year-on-year.

2014年1月-2015年3月大中型钢铁企业销售收入变化情况

0.601.04

0.38

-0.63 -1.08

-0.33

2.06

1.851.02

-0.390.17

0.901.25 1.52

1.02

0

1000

2000

3000

4000

5000

6000

14.1月 2月 3月 4月 5月 6月 7月 8月 9月 10

月11月12月15.1月 2月 3月

亿元

-5

-3

-1

1

3

%

产品销售收入销售收入利润率

2014年1月-2015年3月大中型钢铁企业实现利润情况

28.4

-11.3

46.030.4

30.116.8

63.9

57.6

37.5

-17.5 12.35.3

-24.9

-8.7

27.6

-30

0

30

60

90

1月 2月 3月 4月 5月 6月 7月 8月 9月 10月 11月 12月

亿元

2014年

2015年

2014年1月-2015年3月大中型钢铁企业三费变化图

92.277.7

92.6 96.7 89.2

106.5

90.693.3102.4

93.0101.8

134.5

86.486.794.3

79.6 77.387.2 84.183.7

78.2 82.675.1 77.9 70.4 75.5

85.5

84.474.679.3

29.028.0 32.136.5 35.433.4 34.6 33.7 36.3 36.3

38.5 43.737.131.6

34.4

0

20

40

60

80

100

120

140

14.1月 2月 3月 4月 5月 6月 7月 8月 9月 10

月11月12月15.1月 2月 3月

亿元

管理费用 财务费用 销售费用

9 Profitability of the steel industry

12

4 3

2

5

10 New normal, opportunities and development of Chinese steel industry

Low growth:

Production and

consumption developed

in fluctuation at the

peak range. 1

Low price:

Steel price at the

absolute low level,

while ore price at the

relative low level.

Great pressure:

Great pressure imposed by

environmental issues, and

financial conditions not

favorable for development of

steel industry.

Low profitability:

Severe market

competition;

operation difficulties

for long-term

Resolution

● Idea innovation

● Business model

innovation

● Management

innovation

● Technical

innovation

12/05/2015

7

13

10 New normal, opportunities and development of Chinese steel industry

- New Normal is one strategic opportunity to speed up

structural adjustment, transformation and upgrading of the

steel industry.

- New Normal is one important opportunity to promote fair

competition for the steel industry.

- New Normal is one fatal opportunity to accelerate

transformation of Chinese steel industry from large to strong.

New opportunities under New Normal

New opportunities under New Normal

New opportunities under New Normal

14

思路及研究方向探讨 4 4

思路及研究方向探讨 4 4 (4)

1

5 3

4

6 2

10 New normal, opportunities and development of Chinese steel industry

Changes of Chinese steel industry over the coming years

From steel

manufacturing to

material service Coordinated competition

instead of disordered

competition; improve

industrial concentration

by means of accelerated

consolidation and

reorganization

Diversified

development instead

of single

development Extensive development

with high consumption

and emission to

sustainable development

with low carbon emission

Development driven by

innovation instead of by

investment

From domestic

development to

integrated development

home and abroad

Six

changes

12/05/2015

8

15

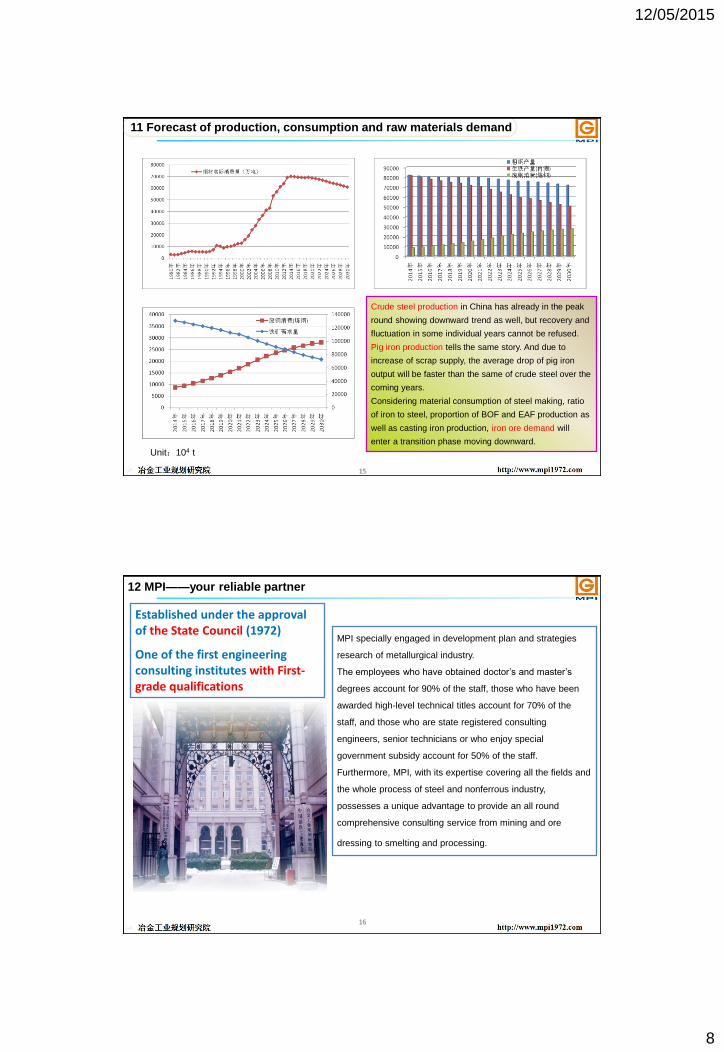

11 Forecast of production, consumption and raw materials demand

Crude steel production in China has already in the peak

round showing downward trend as well, but recovery and

fluctuation in some individual years cannot be refused.

Pig iron production tells the same story. And due to

increase of scrap supply, the average drop of pig iron

output will be faster than the same of crude steel over the

coming years.

Considering material consumption of steel making, ratio

of iron to steel, proportion of BOF and EAF production as

well as casting iron production, iron ore demand will

enter a transition phase moving downward.

Unit:104 t

12 MPI——your reliable partner

16

Established under the approval of the State Council (1972)

One of the first engineering consulting institutes with First-grade qualifications

MPI specially engaged in development plan and strategies

research of metallurgical industry.

The employees who have obtained doctor’s and master’s

degrees account for 90% of the staff, those who have been

awarded high-level technical titles account for 70% of the

staff, and those who are state registered consulting

engineers, senior technicians or who enjoy special

government subsidy account for 50% of the staff.

Furthermore, MPI, with its expertise covering all the fields and

the whole process of steel and nonferrous industry,

possesses a unique advantage to provide an all round

comprehensive consulting service from mining and ore

dressing to smelting and processing.

12/05/2015

9

17

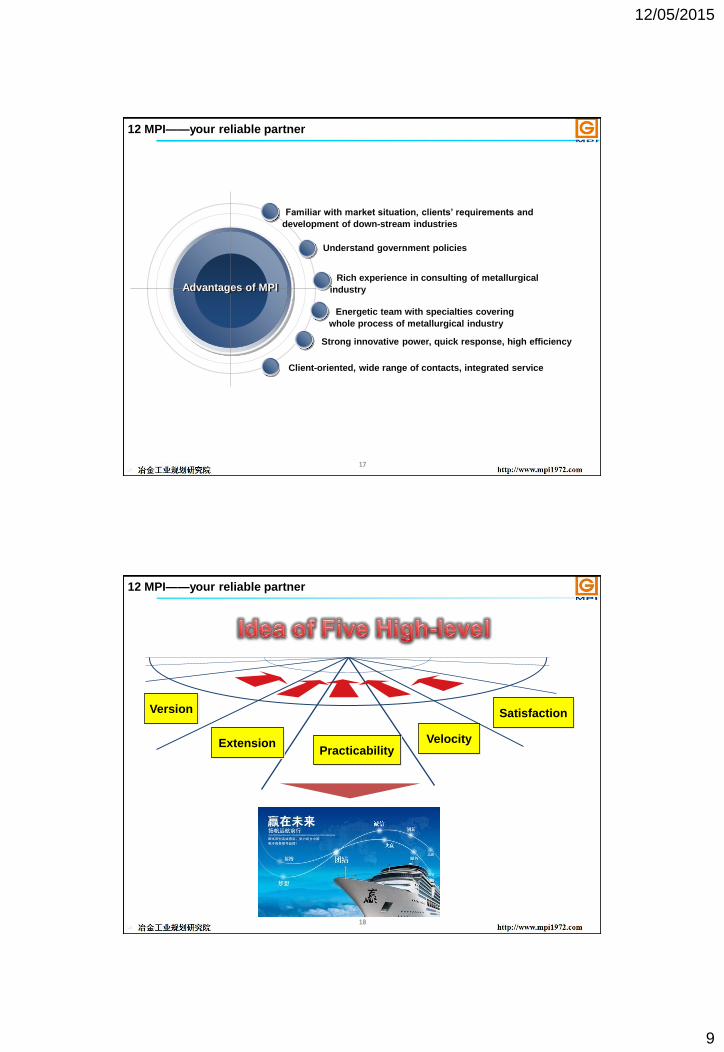

Familiar with market situation, clients’ requirements and

development of down-stream industries

Energetic team with specialties covering

whole process of metallurgical industry

Rich experience in consulting of metallurgical

industry

Client-oriented, wide range of contacts, integrated service

Advantages of MPI

Strong innovative power, quick response, high efficiency

Understand government policies

12 MPI——your reliable partner

18

Practicability Velocity

Satisfaction

Extension

Version

12 MPI——your reliable partner

12/05/2015

10

19

12 MPI——your reliable partner

20

12 MPI——your reliable partner

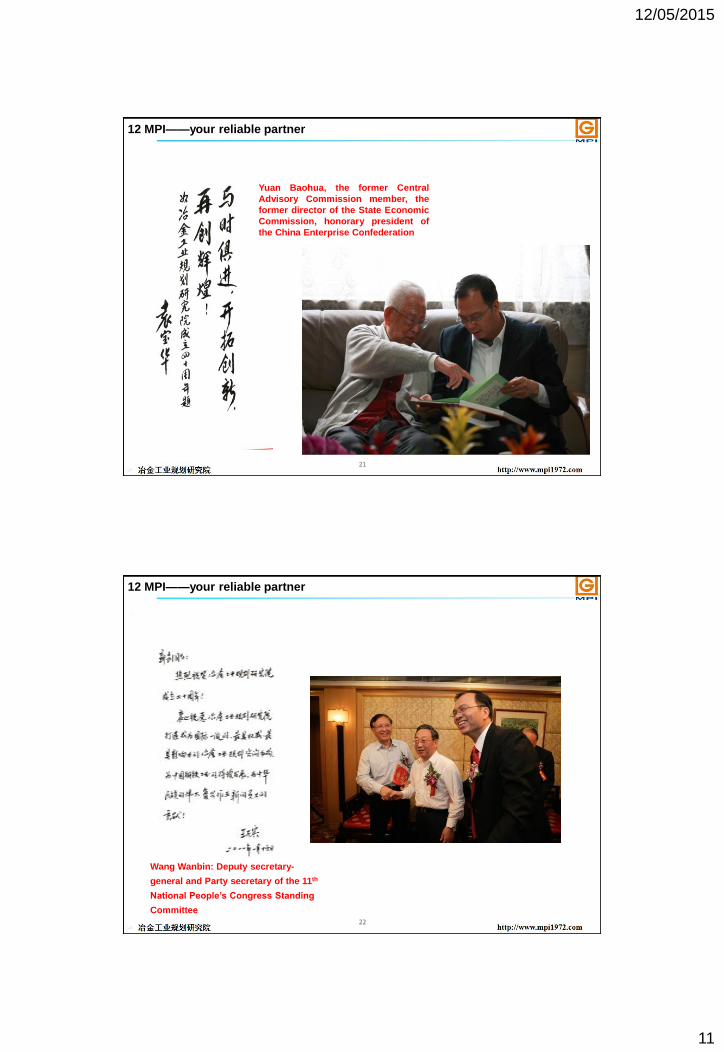

Business fields

Technical Consultation: overall planning, mineral resources, steel market, energy saving & environmental protection,

general layout, diversified operation, technological economy, management consultation

Forum and information service : China Steel Report and six high-end forums

Technology promotion: de-S of sintering fume, energy resources management (power generation by surplus heat or energy,

energy saving for water pumps, coal prewetting etc), technology agent

Business

Research and analysis of industrial policy

Mineral resource exploitation and green mine planning

Technical service for sintering fume desulphurization

Research on metallurgical industry layout planning

Industry and industrial park planning

Energy resources diagnosis and energy saving

Logistics and logistics park planning

Preparation of project proposal, application report and

feasibility

Recycling economy planning

Industrial and enterprises development planning

Assets evaluation and technological estimation

Market survey, analysis and prediction

Energy saving and emission reduction and cleaning

production planning

Social security evaluation

Industrial chain extension planning

Preparation of energy saving evaluation report

Host and cooperator of industrial conferences

Consultation for new technology promotion and

application

Promotion of human resources management

Overall development strategy

Enterprises merging planning

Analysis of capitalized cost

Marketing management

Operation management

Procurement management

Payment and performance management

Lean assessment

12/05/2015

11

21

12 MPI——your reliable partner

Yuan Baohua, the former Central

Advisory Commission member, the

former director of the State Economic

Commission, honorary president of

the China Enterprise Confederation

22

12 MPI——your reliable partner

Wang Wanbin: Deputy secretary-

general and Party secretary of the 11th

National People’s Congress Standing

Committee

12/05/2015

12

Address: http://www.mpi1972.com

E-mail: [email protected]

23

Thank you for your attention!