Embed Size (px)

DESCRIPTION

STERICYCLE (SRCL). Ross Pevitz Matt Storkman Shengdong Zhu RCMP Presentation April 10, 2007. Position. May, 2001 Bought 200 Shares Purchase for $19.47 ($3,894) Current Price is $81.92 ($16,384) $12,490 Unrealized Gain 5% of Portfolio. History. 1989- Stericycle founded - PowerPoint PPT Presentation

Citation preview

STERICYCLE(SRCL)

Ross PevitzMatt StorkmanShengdong Zhu

RCMP PresentationApril 10, 2007

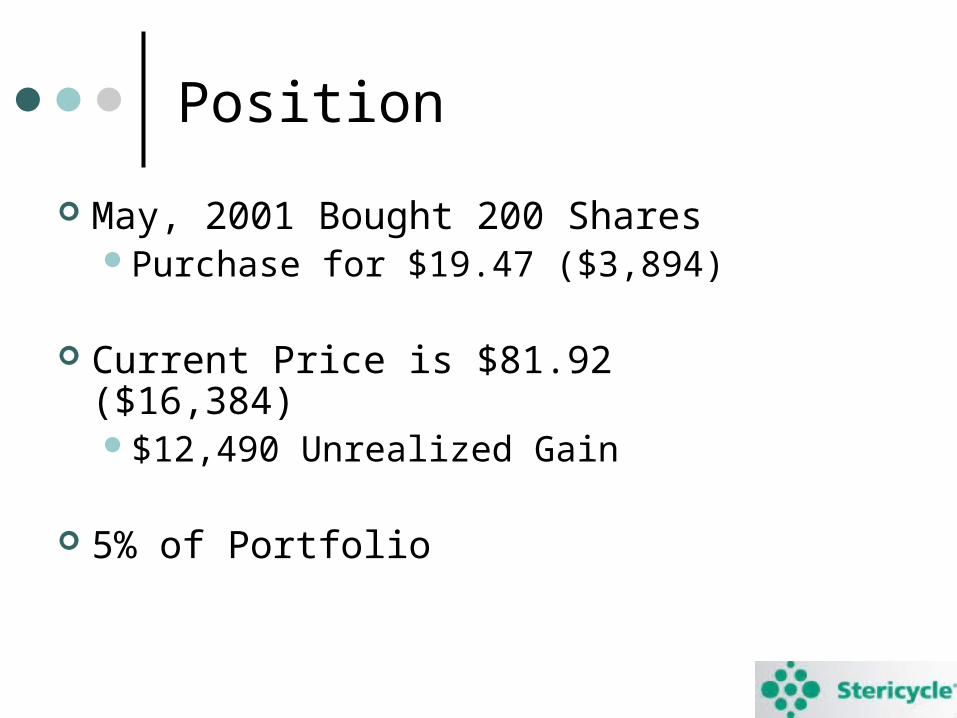

Position

May, 2001 Bought 200 SharesPurchase for $19.47 ($3,894)

Current Price is $81.92 ($16,384)$12,490 Unrealized Gain

5% of Portfolio

History

1989- Stericycle founded Medical Waste Tracking Act Strict regulations for dealing with Medical Waste Afford convenient, cost effective, and efficient solutions

1993- Acquired over 116 companies since 1993 1996- IPO 2000- North America’s Largest Provider of regulated

Medical Waste Management Services

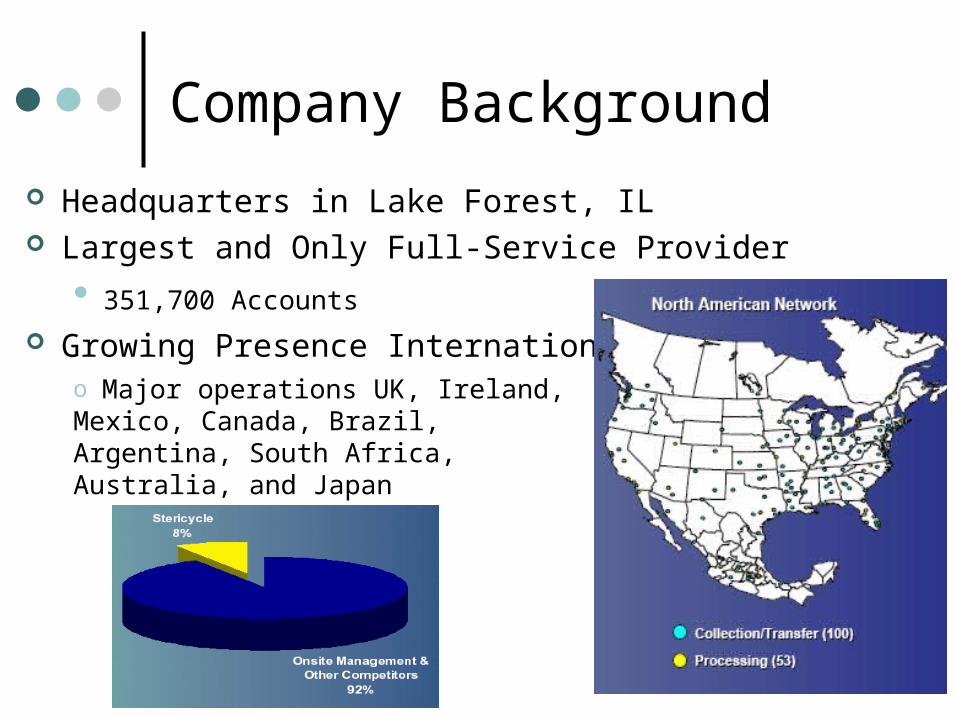

Company Background Headquarters in Lake Forest, IL Largest and Only Full-Service Provider

351,700 Accounts Growing Presence Internationally

o Major operations UK, Ireland, Mexico, Canada, Brazil, Argentina, South Africa, Australia, and Japan

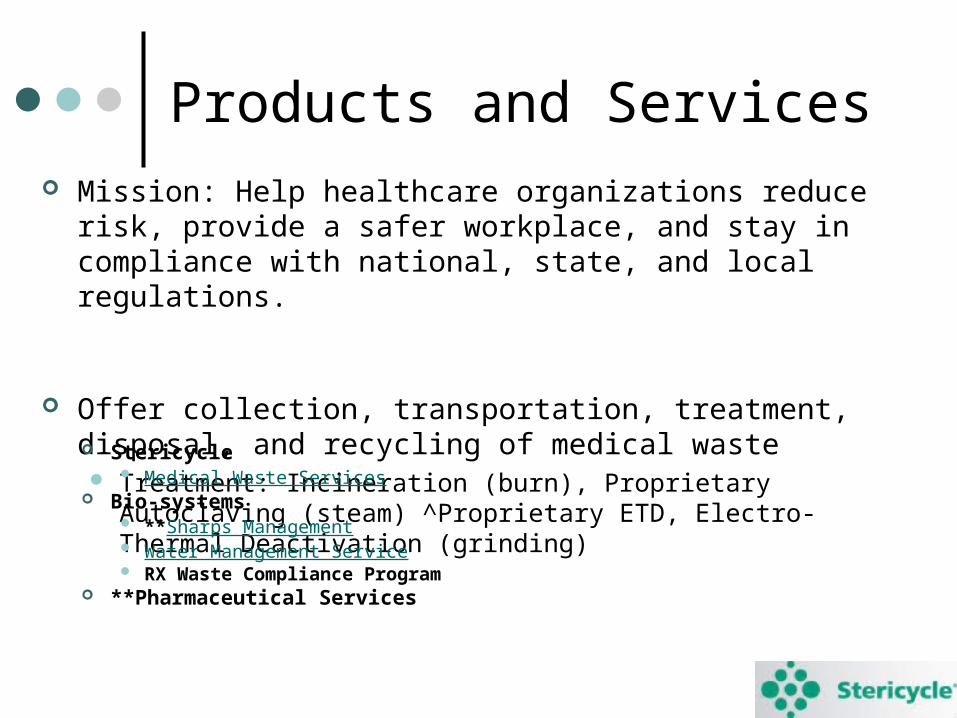

Products and Services Mission: Help healthcare organizations reduce risk, provide a

safer workplace, and stay in compliance with national, state, and local regulations.

Offer collection, transportation, treatment, disposal, and recycling of medical waste Treatment: Incineration (burn), Proprietary Autoclaving (steam)

^Proprietary ETD, Electro-Thermal Deactivation (grinding) Stericycle Medical Waste Services

Bio-systems **Sharps Management Water Management Service RX Waste Compliance Program

**Pharmaceutical Services

Products and Services

Offer training, educational, consulting, and documentation services

(Steri-Safe) OSHA and HIPPA Compliance– Occupational Safety and Health

Administration, Health Insurance Portability and Accountability Act

Product Sales

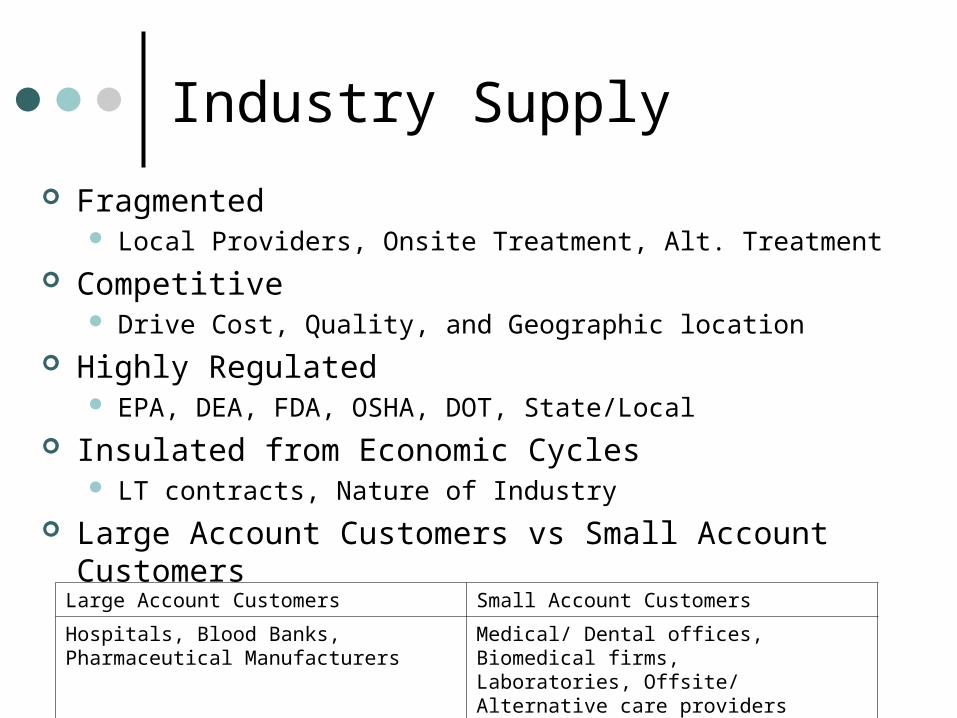

Industry Supply Fragmented

Local Providers, Onsite Treatment, Alt. Treatment Competitive

Drive Cost, Quality, and Geographic location Highly Regulated

EPA, DEA, FDA, OSHA, DOT, State/Local Insulated from Economic Cycles

LT contracts, Nature of Industry Large Account Customers vs Small Account Customers

Large Account Customers Small Account Customers

Hospitals, Blood Banks, Pharmaceutical Manufacturers

Medical/ Dental offices, Biomedical firms,Laboratories, Offsite/ Alternative care providers

Industry Demand Pressure to Reduce Healthcare Costs Aging Population

Baby Boomers Better Health Care

Stricter Environmental and Safety Regulations Larger Fines and Unaware market

Economic Risks

Interest Rate, Inflation, GDP, Competition Energy Costs

Transportation and Treatment

Foreign Exchange Risk Changing Government Regulations!!! Patent and Trademark Expiration Liabilities and Insurance

Clean up costs, personal injury, ect.

Competitive Advantages

Established Brand Name and Market Leader Strong Management Team Low Cost Operator

Economies of Scale Full Service Provider

Vertically Integrated, growing Horizontally Loyal and Diverse Customers

Revenue retention >95% Largest customers <2% of Revenues LT contracts with automatic renewal and price ↑ provisions

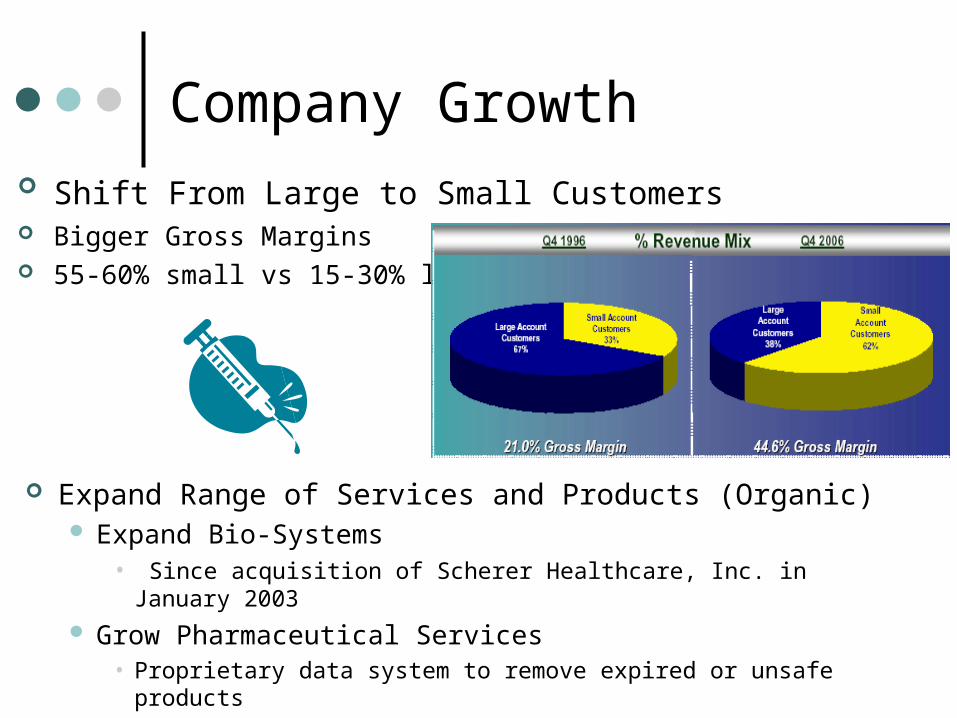

Company Growth Shift From Large to Small Customers Bigger Gross Margins 55-60% small vs 15-30% large

Expand Range of Services and Products (Organic) Expand Bio-Systems

• Since acquisition of Scherer Healthcare, Inc. in January 2003 Grow Pharmaceutical Services

• Proprietary data system to remove expired or unsafe products

Company Growth Continue Acquisitions

Focus on strategic “tuck in” Proven Integrator ~ 116 acquisitions since 1993

Mainly Asset Purchases Price determined by multiples of EBITDA and quality of asset

Revenues

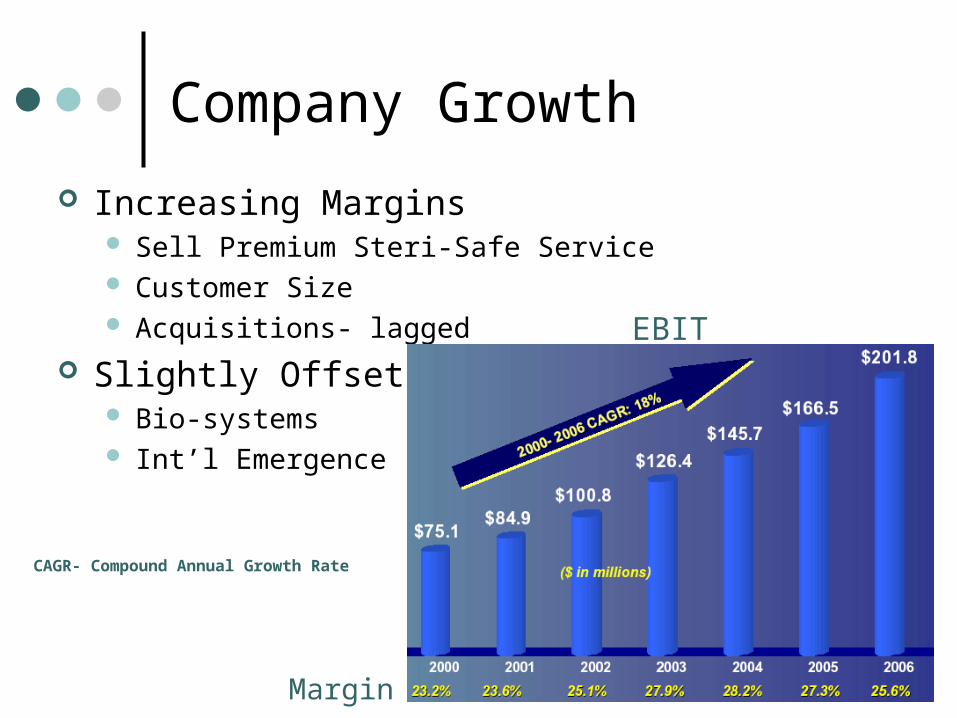

Company Growth Increasing Margins

Sell Premium Steri-Safe Service Customer Size Acquisitions- lagged

Slightly Offset Bio-systems Int’l Emergence

EBIT

Margins

CAGR- Compound Annual Growth Rate

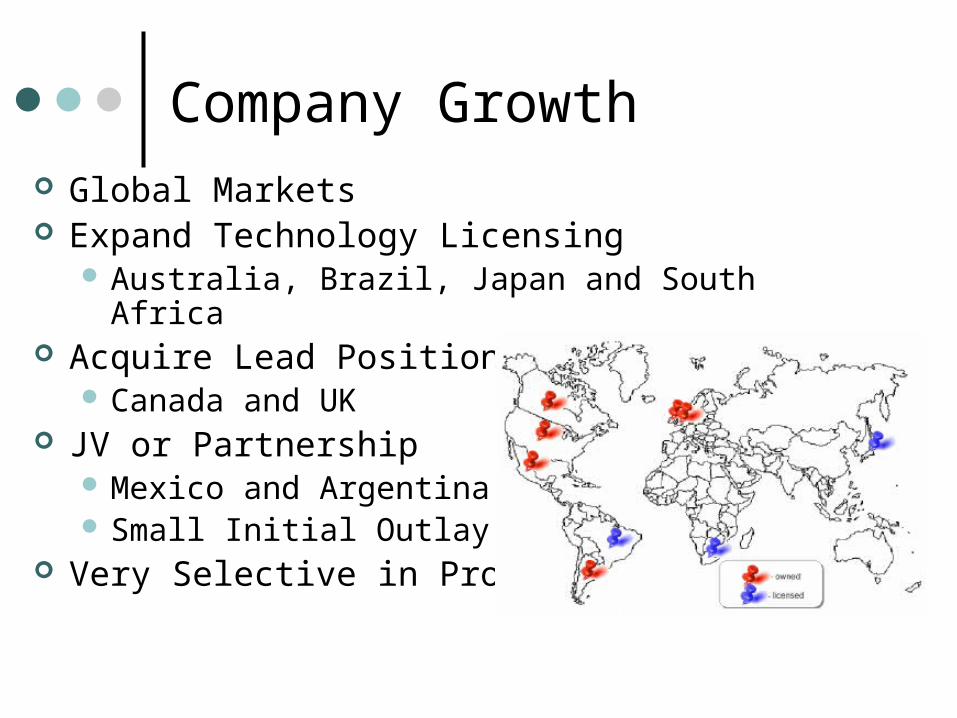

Company Growth Global Markets Expand Technology Licensing

Australia, Brazil, Japan and South Africa Acquire Lead Position

Canada and UK JV or Partnership

Mexico and Argentina Small Initial Outlay

Very Selective in Process

0

500

1,000

1,500

2,000

2,500

3,000

FY '04 FY '05 FY '06 2007 2008 2009 2010 2011 2012

US

D (

mm

)

0%

5%

10%

15%

20%

25%

30%

35%

Total operating revenues FCF Net Income EBIT Margin Net Profit Margin Revenue Growth Rate

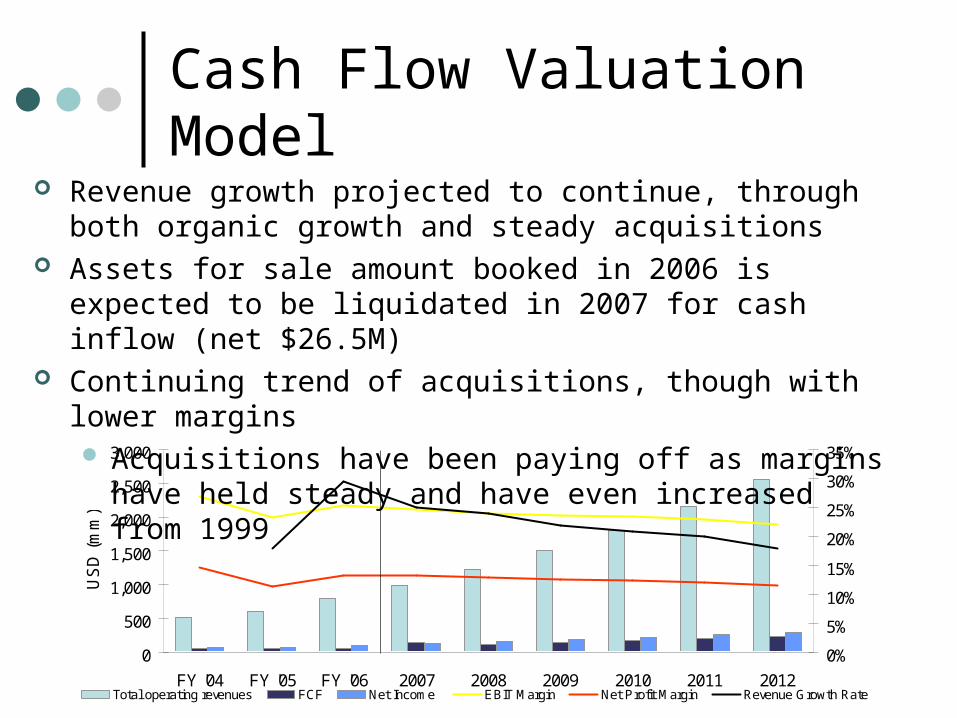

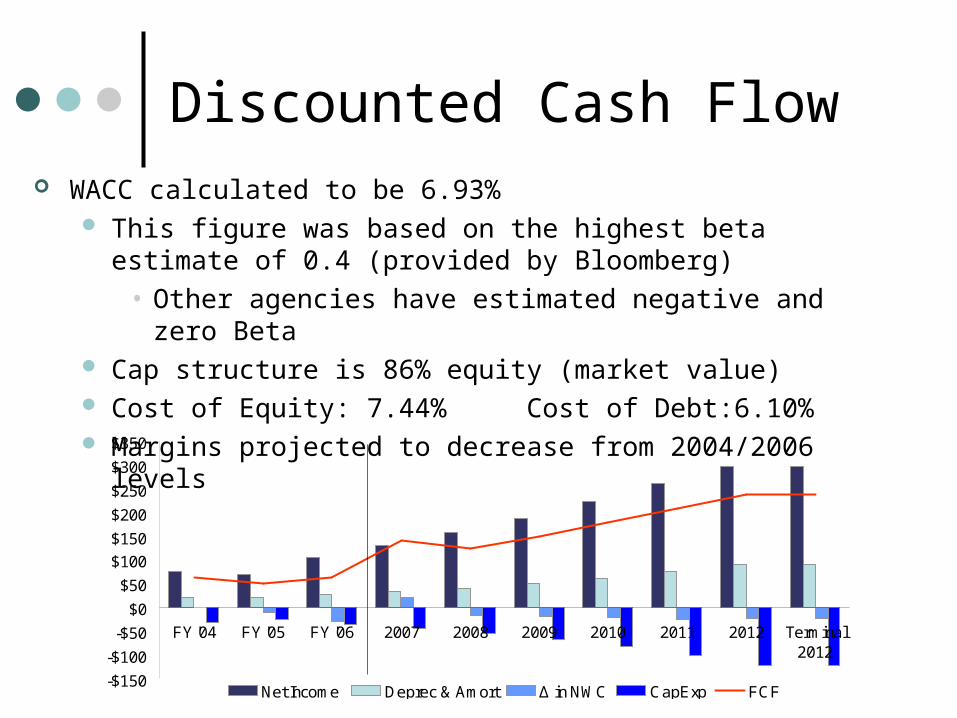

Cash Flow Valuation Model Revenue growth projected to continue, through both organic

growth and steady acquisitions Assets for sale amount booked in 2006 is expected to be

liquidated in 2007 for cash inflow (net $26.5M) Continuing trend of acquisitions, though with lower margins

Acquisitions have been paying off as margins have held steady and have even increased from 1999

-$150-$100

-$50$0

$50$100$150$200$250$300$350

FY '04 FY '05 FY '06 2007 2008 2009 2010 2011 2012 Terminal2012

Net Income Deprec & Amort Δ in NWC CapExp FCF

Discounted Cash Flow WACC calculated to be 6.93%

This figure was based on the highest beta estimate of 0.4 (provided by Bloomberg)

• Other agencies have estimated negative and zero Beta Cap structure is 86% equity (market value) Cost of Equity: 7.44% Cost of Debt:6.10% Margins projected to decrease from 2004/2006 levels

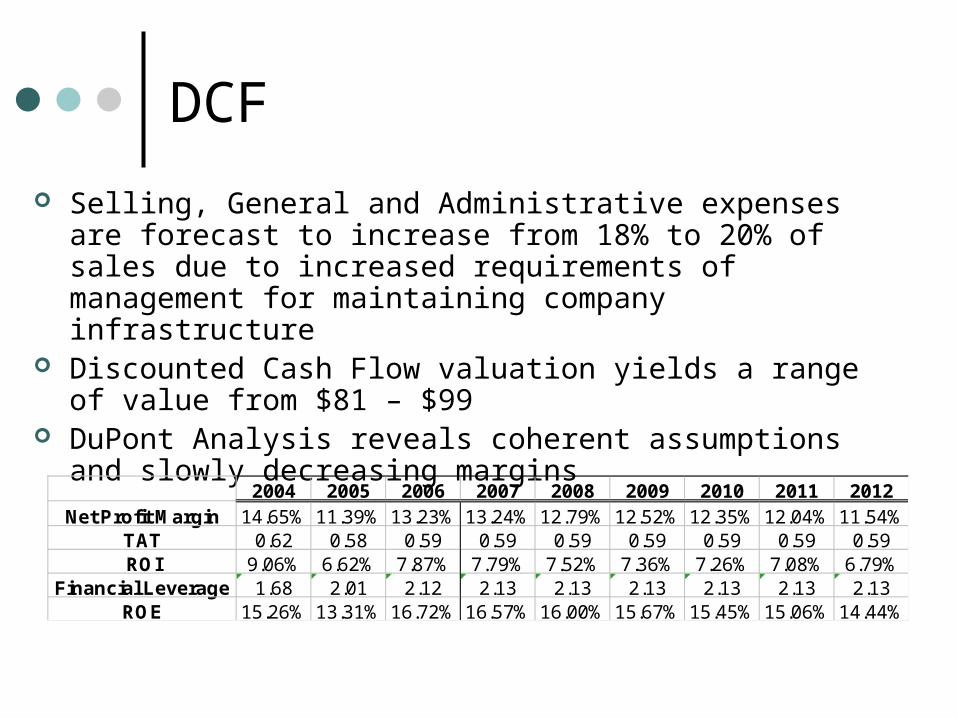

DCF Selling, General and Administrative expenses are forecast to

increase from 18% to 20% of sales due to increased requirements of management for maintaining company infrastructure

Discounted Cash Flow valuation yields a range of value from $81 – $99

DuPont Analysis reveals coherent assumptions and slowly decreasing margins

2004 2005 2006 2007 2008 2009 2010 2011 2012Net Profit Margin 14.65% 11.39% 13.23% 13.24% 12.79% 12.52% 12.35% 12.04% 11.54%

TAT 0.62 0.58 0.59 0.59 0.59 0.59 0.59 0.59 0.59ROI 9.06% 6.62% 7.87% 7.79% 7.52% 7.36% 7.26% 7.08% 6.79%

Financial Leverage 1.68 2.01 2.12 2.13 2.13 2.13 2.13 2.13 2.13ROE 15.26% 13.31% 16.72% 16.57% 16.00% 15.67% 15.45% 15.06% 14.44%

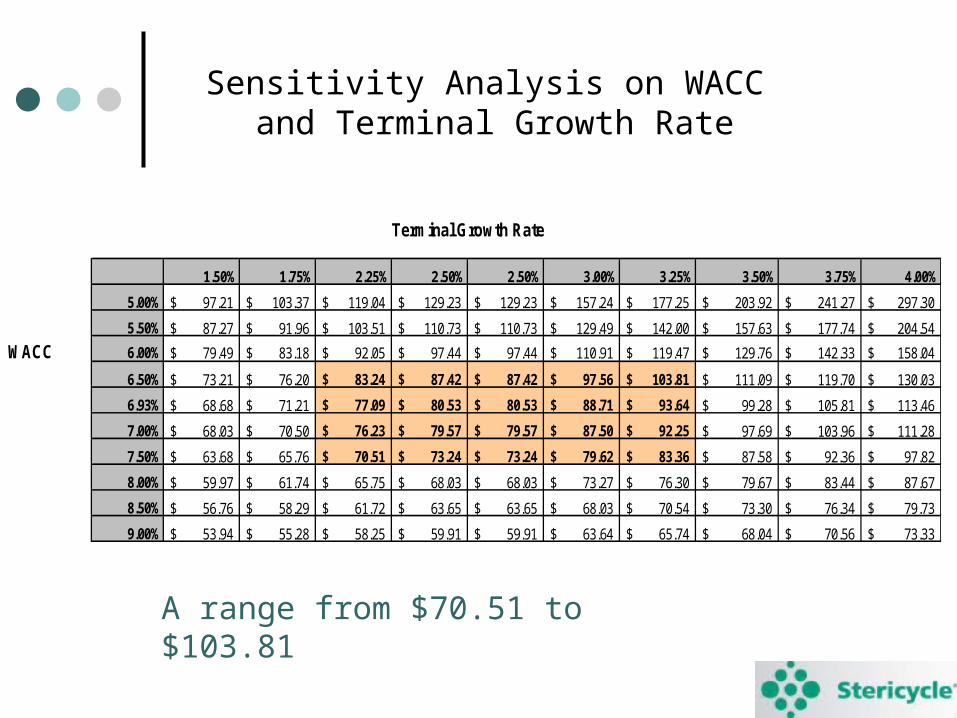

Sensitivity Analysis on WACC and Terminal Growth Rate

A range from $70.51 to $103.81

1.50% 1.75% 2.25% 2.50% 2.50% 3.00% 3.25% 3.50% 3.75% 4.00%5.00% 97.21$ 103.37$ 119.04$ 129.23$ 129.23$ 157.24$ 177.25$ 203.92$ 241.27$ 297.30$

5.50% 87.27$ 91.96$ 103.51$ 110.73$ 110.73$ 129.49$ 142.00$ 157.63$ 177.74$ 204.54$ 6.00% 79.49$ 83.18$ 92.05$ 97.44$ 97.44$ 110.91$ 119.47$ 129.76$ 142.33$ 158.04$

6.50% 73.21$ 76.20$ 83.24$ 87.42$ 87.42$ 97.56$ 103.81$ 111.09$ 119.70$ 130.03$

6.93% 68.68$ 71.21$ 77.09$ 80.53$ 80.53$ 88.71$ 93.64$ 99.28$ 105.81$ 113.46$

7.00% 68.03$ 70.50$ 76.23$ 79.57$ 79.57$ 87.50$ 92.25$ 97.69$ 103.96$ 111.28$

7.50% 63.68$ 65.76$ 70.51$ 73.24$ 73.24$ 79.62$ 83.36$ 87.58$ 92.36$ 97.82$

8.00% 59.97$ 61.74$ 65.75$ 68.03$ 68.03$ 73.27$ 76.30$ 79.67$ 83.44$ 87.67$

8.50% 56.76$ 58.29$ 61.72$ 63.65$ 63.65$ 68.03$ 70.54$ 73.30$ 76.34$ 79.73$

9.00% 53.94$ 55.28$ 58.25$ 59.91$ 59.91$ 63.64$ 65.74$ 68.04$ 70.56$ 73.33$

Terminal Growth Rate

WACC

Competitors

o Who?o American Ecology Corp (ECOL)o Microtek Medical Holdings Inc. (MTMD)o Waste Management, Inc (WMI) o Waste Management Industry

o Why?o Industry specifico Strong/Solid performerso Multiples in line with Industry

Critical Multiples Comparison

o Gross Margino Operating Margins o Enterprise Value/Revenueo Enterprise Value/EBITDAo EPS

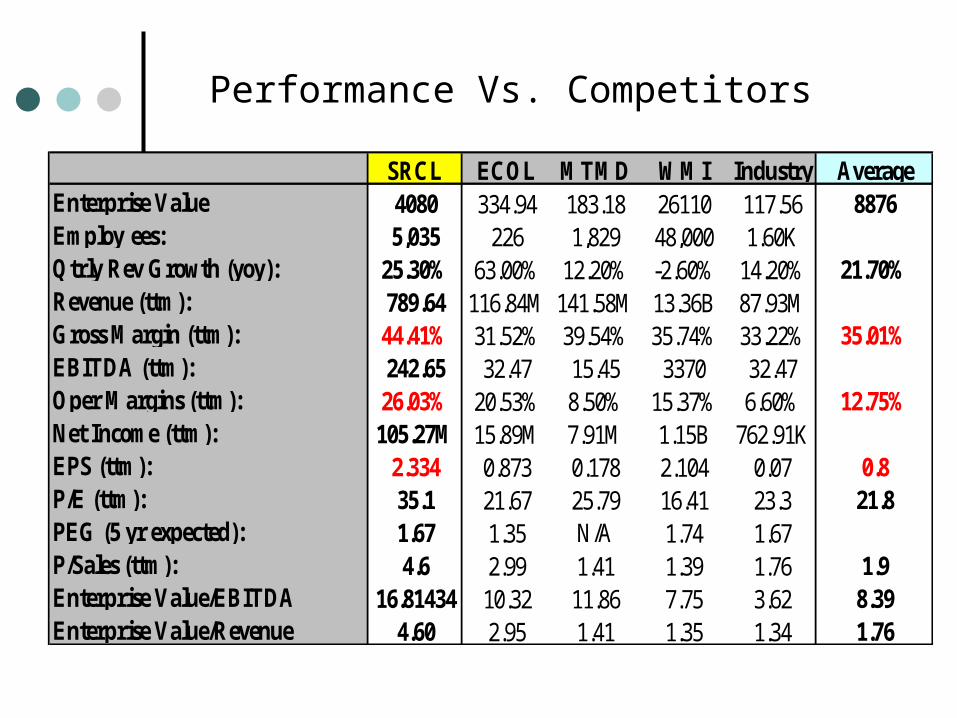

Performance Vs. Competitors

SRCL ECOL MTMD WMI Industry AverageEnterprise Value 4080 334.94 183.18 26110 117.56 8876Employ ees: 5,035 226 1,829 48,000 1.60KQtrly Rev Growth (yoy): 25.30% 63.00% 12.20% -2.60% 14.20% 21.70%Revenue (ttm): 789.64 116.84M 141.58M 13.36B 87.93MGross Margin (ttm): 44.41% 31.52% 39.54% 35.74% 33.22% 35.01%EBITDA (ttm): 242.65 32.47 15.45 3370 32.47Oper Margins (ttm): 26.03% 20.53% 8.50% 15.37% 6.60% 12.75%Net Income (ttm): 105.27M 15.89M 7.91M 1.15B 762.91KEPS (ttm): 2.334 0.873 0.178 2.104 0.07 0.8P/E (ttm): 35.1 21.67 25.79 16.41 23.3 21.8PEG (5 yr expected): 1.67 1.35 N/A 1.74 1.67P/Sales (ttm): 4.6 2.99 1.41 1.39 1.76 1.9Enterprise Value/EBITDA 16.81434 10.32 11.86 7.75 3.62 8.39Enterprise Value/Revenue 4.60 2.95 1.41 1.35 1.34 1.76

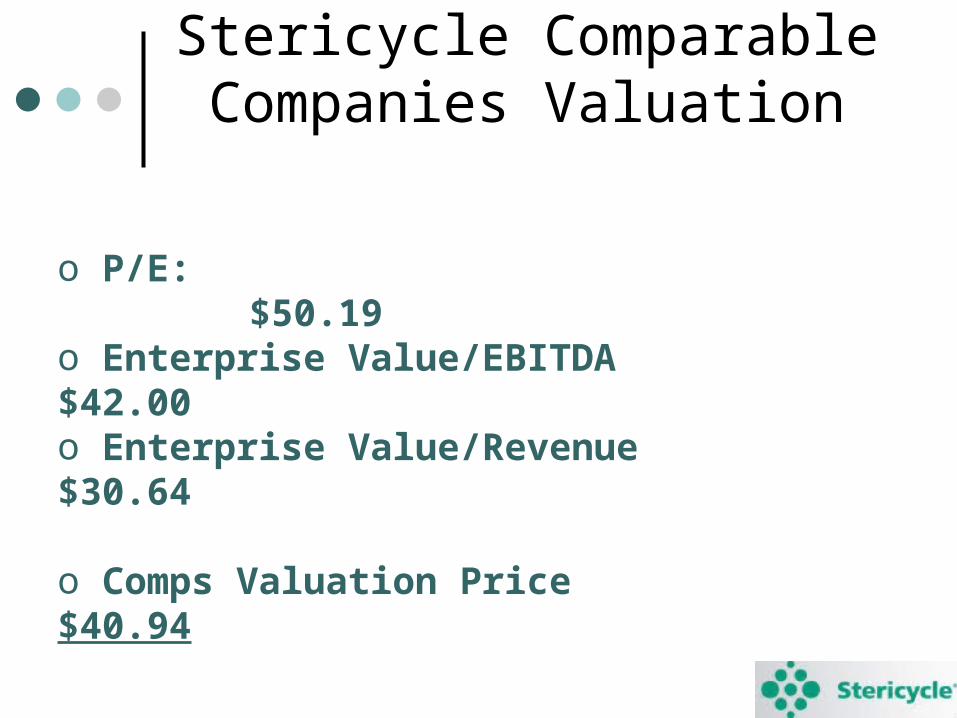

Stericycle Comparable Companies Valuation

o P/E: $50.19 o Enterprise Value/EBITDA $42.00 o Enterprise Value/Revenue $30.64

o Comps Valuation Price $40.94

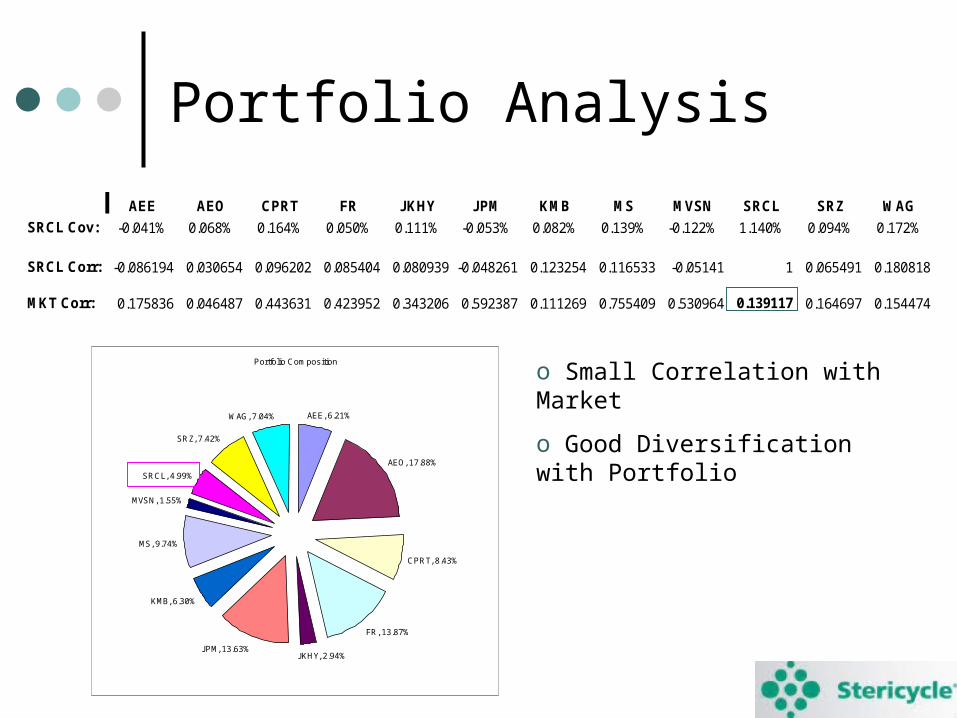

Portfolio Analysis

Portfolio Composition

AEE, 6.21%

AEO, 17.88%

CPRT, 8.43%

FR, 13.87%

JKHY, 2.94%JPM, 13.63%

KMB, 6.30%

MS, 9.74%

MVSN, 1.55%

SRCL, 4.99%

SRZ, 7.42%

WAG, 7.04%

AEE AEO CPRT FR JKHY JPM KMB MS MVSN SRCL SRZ WAGSRCL Cov: -0.041% 0.068% 0.164% 0.050% 0.111% -0.053% 0.082% 0.139% -0.122% 1.140% 0.094% 0.172%

SRCL Corr: -0.086194 0.030654 0.096202 0.085404 0.080939 -0.048261 0.123254 0.116533 -0.05141 1 0.065491 0.180818

MKT Corr: 0.175836 0.046487 0.443631 0.423952 0.343206 0.592387 0.111269 0.755409 0.530964 0.139117 0.164697 0.154474

o Small Correlation with Market

o Good Diversification with Portfolio

Valuation Discussion: Hold The low estimate of the discounted cash flow valuation

represents the current market price of SRCL $81 is also the year-high for the stock

Comparable company valuation places a much lower value on the stock SRCL is trading at a large premium compared to its

peers SRCL outperforms all of its peers in operating metrics

such as gross margin and operating margin DCF analysis and forecasting provide reasoning and

reinforce the market’s premium for SRCL Analyst Team recommends holding SRCL

Questions?

Love to Entertain!!!