Embed Size (px)

Citation preview

Stock Code: BSE : 500303 NSE : ABIRLANUVO Reuters : ABRL.BO / ABRL.NS / IRYN.LU Bloomberg : ABNL IN / IRIG LX

2

Key Highlights 3 – 12

Business-wise Performance

13 – 28

Going Forward 29

Financials and other Annexure 30 – 52

Contents

Note 1 : The financial results of ABNL are consolidated financials unless otherwise specified

Note 2 : The financial figures in this presentation have been rounded off to the nearest ` 1 Crore

Note 3 : 1 USD : INR 60

Glossary

CY : Current Year

FY : Financial Year (April-March)

PY – Corresponding period in Previous Financial Year

PQ – Previous Quarter

Q1– April-June

Q4– January-March

YTD – Year to date

ROACE : Return on Avg. Operating Capital Employed based on EBIT

VAS – Value Added Services

EBO – Exclusive Brand Outlet

MBO – Multi Brand Outlet

TPA – Tons per annum

AAUM – Average Assets under Management

L2L – Like to Like

3

Indian Economy

India’s GDP is estimated to grow at 7.4% in FY15 compared to 6.9% in the previous year

(Source : Ministry of Finance, at constant 2011-12 market prices)

As per IMF, India’s GDP is expected to grow at 7.5% in 2015 & 2016 outpacing China

Controlled inflation propelled RBI for rate cuts

WPI inflation at -2.33% is lowest in 9 years & CPI inflation eased to 5.17% in Mar’15

IIP grew y-o-y by 5% in Feb’15. Cumulative growth in Apr-Feb’15 at 2.8% vis-à-vis -0.1% in previous year

RBI cut repo rate in Jan’15 & Mar’15 by 25 bps each on easing inflation and to push economic growth

Reforms for economic development continue to remain high on Government’s agenda

FDI / FII limit in Insurance sector increased from 26% to 49%

Government met its fiscal deficit target through auctions

Consumer confidence index has risen to its highest since Apr’11

Business confidence index continues to remain high

However, consumption and investment growth on the ground is yet to pick up

4

Aditya Birla Nuvo : Progressing in line with its vision

Investing in the Promising Sectors

Invested USD 2 billion over past 15 years to fund the growth of its businesses leading to

transformation from a manufacturing company to a premium conglomerate

2000 2001 2003

2005/06 2005-2011

2012

2013

2014

2015

Created India’s largest online money management platform MyUniverse

Added New Superfine Yarn capacity in Rayon

Expanded Linen Yarn and Fabric Capacities

Commenced Housing Finance operations

Applied for Payments bank license in a 51:49 stake with Idea

Signed MoU with MMI Holdings to enter health insurance sector in India

Enhanced strategic stake in Telecom through Idea

Expanded Financial Services portfolio by merger of

AMC & NBFC and entry in broking, private equity etc.

Augmented Fashion offerings through acquisition of

Pantaloons, a top 3 big box apparel retailer

Entered Fashion business through

acquisition of Madura

Forayed in Life Insurance business

through JV with Sun Life, Canada

Entry into IT-ITeS Business

5

Earnings before Tax

USD 141 million

(` 849 Crore : 17%↑ y-o-y)

Diversified Portfolio

Having 10 lines

of businesses

Retail Network

1869 Stores (4.8 mn sq. ft.)

Largest in fashion space

Customers Base

A large 10.8 million

loyalty customers base

EBITDA

USD 89 million

(` 532 Crore : 32%↑ y-o-y)

Building Leadership Position across its businesses

Note 1 : Includes AUM of Life Insurance, Private Equity and quarterly AAUM of Asset Management business

Market Positioning

Among the top 5 fund

managers in India

Market Positioning

#1 branded menswear &

womenswear player in India

Aditya Birla Financial Services

Fashion & Lifestyle (Madura & Pantaloons)

Scale

Selling two branded

apparels every second

Revenue

USD 1.3 billion

(` 7,926 Crore : 19%↑ y-o-y)

Revenue

USD 910 million

(` 5,450 Crore : 15%↑ y-o-y)

AUM

USD 27.5 billion1

(` 164,995 Crore : 35%↑ y-o-y)

NBFC Lending Book

USD 3 billion

(` 17,550 Crore : 52%↑ y-o-y)

6

Revenue

USD 901 million

(` 5,405 Crore : 9%↑ y-o-y)

EBITDA

USD 102 million

(` 615 Crore : 11%↑ y-o-y)

Cash profit (post tax)

USD 1.4 billion

(` 8,482 Crore : 32%↑ y-o-y )

Divisions (Jaya Shree, Indo-Gulf fertilisers, Indian Rayon, Aditya Birla Insulators)

Market Positioning

6th largest1 in the world

3rd largest2 in India

Outperforming Industry

Revenue share grew y-o-y

from 16.1% to 17.5%2

Note 1 : In terms of subscribers and based on operations in a single country (Source : GSMA, Dec’14) Note 2 : Based on gross revenue for UAS & Mobile licenses only for Oct-Dec14, as released by TRAI

Building Leadership Position across its businesses

Market Positioning

Leading manufacturer of

Linen, Urea, VFY & Insulators in India

Strong Balance sheet

Net Debt to EBITDA : 1.31x

(Standalone)

Free Cash Flow (pre-tax)

USD 52 million

(` 314 Crore : 36%↑ y-o-y)

Telecom (Idea Cellular)

Outlook

Expanding linen yarn capacity to tap sector growth

Long term anti-dumping duty to benefit Insulators sector

Gas pooling policy to benefit urea sector

EBITDA

USD 1.9 billion

(` 11,281 Crore : 32%↑ y-o-y )

Revenue

USD 5.3 billion

(` 31,527 Crore : 19%↑ y-o-y)

7

A platform to drive synergy of resources

Standalone Ratios

Standalone balance sheet has been the growth engine for ABNL & a platform to drive synergy of capital resource

Invested ~USD 1 billion to fund the growth capital requirements of its businesses over past six years

Healthy financial position : Net Debt to EBITDA at 3x & Net Debt to Equity at 0.42x as on 31st Mar’15

Contributed by strong cash flow from operations, dividend income, proceeds from divestment of sub-scale

businesses and capital support from the promoters

Received dividend of ` 89 Cr. in FY15 (~` 600 Cr. over past 6 years)

306 676 1,193

3591 3854

3584

Mar'09 Mar'12 Mar'15

Standalone Net Debt

( ` Crore)

5.8

3.7

3.0 0.87

0.68

0.42

Mar'09 Mar'12 Mar'15

Net Debt/annualised EBITDA Net Debt/Equity

O/s

Fertilisers

Subsidy

8

Exit from sub scale businesses to achieve greater focus on other businesses

Supported ABNL’s growth plans &

strengthened balance sheet

Greater focus on core businesses

Note : Refer slide 50 for transaction details

Delivering best value to all the stakeholders …

Consolidation of Branded Apparels Businesses to unlock value for the shareholders

Creating India’s largest pure-play fashion & lifestyle company

Presence across entire spectrum of fashion through India’s leading fashion brands

Unlocking value for shareholders by giving them direct holding in a best-in-class fashion powerhouse

Largest retail network in fashion space in India

Sound Balance sheet to act as a strong enabler for growth

Aditya Birla Fashion & Retail Ltd.

# 1 Menswear player # 1 Womenswear player

Enterprise Value

USD 260 million

Effective Date

9th May 2014

Effective Date

1st April 2013

Enterprise Value

USD 240 million

Divestment of

IT-ITeS business

Divestment of

Carbon Black business

9

4,227

10,723

21,654

Mar'09 Mar'12 Mar'15

Market Capitalisation (Rs. Crore)

-436

890

1,416

FY09 FY12 FY15

Consolidated Net Profit (Rs. Crore)

… and driving strong earnings growth

867

3,247

5,798

FY09 FY12 FY15

14,331

21,840

26,516

FY09 FY12 FY15

Branded Apparels Financials Services, Telecom & Divisions

Consolidated Revenue (Rs. Crore)

Consolidated EBITDA (Rs. Crore)

10

Performance highlights : 2014-15

11

Consolidated earnings growth

Revenue

( ` Crore)

7,111

25,892

7,073

26,516

-1%

2%

FY 14 FY 15 FY 14 FY 15

Quarter 4 Full Year

EBITDA

( ` Crore)

1,263

4,927

1,527

5,798

21%

FY 14 FY 15 FY 14 FY 15

Quarter 4 Full Year

18%

Net Profit

( ` Crore)

176

1,143

332

1,416

88%

24%

FY 14 FY 15 FY 14 FY 15

Quarter 4 Full Year

Ex-IT-ITeS business

(divested w.e.f 9th

May’14), L2L revenue

growth is 11% in Q4 &

14% in FY15

Ex-IT-ITeS business, L2L

EBITDA growth is 29% in

Q4 & 25% in FY15

Ex-IT-ITeS business and

before one-off items, L2L

Net Profit growth is 36%

in Q4 & 39% in FY15

12

Consolidated Earnings Mix – FY15

Financial Services

30%

Telecom 28%

Fashion & Lifestyle

21%

Divisions 21%

Financial Services

28%

Telecom 46%

Fashion & Lifestyle

9%

Divisions 17%

Segment Revenue1 Segment EBIT1

Note 1 : Revenue and EBIT Mix are excluding IT-ITeS business which was divested w.e.f. 9th May 2014

13

Aditya Birla Financial Services

Performance highlights : 2014-15

A significant non-bank financial services group

14

Vision : To be a leader & role model in a broad based

& integrated financial services business

A significant non-bank financial services group

Ranks among top 5 fund managers in India (excl. LIC)

Diversified portfolio with 10 lines of businesses

AUM at ` 164,995 Cr. (35%↑ y-o-y)

NBFC Lending book at ` 17,550 Cr. (52%↑ y-o-y)

Entering strategic partnerships & investing in promising sectors

Forayed into Housing Finance business in Oct’14

Acquired mutual fund schemes & portfolio accounts from ING in Sep’14

IFC became strategic financial investor in MyUniverse in Dec’14

Signed MoU with MMI Holdings in Oct’14 to enter health insurance sector

1

( ` Crore)

Assets under Management

Aditya Birla Financial Services : Progressing as envisioned

Note 1 : Includes AUM of Life Insurance, Private Equity and quarterly AAUM of Asset Management business

43,104

88,309 88,393 1,07,539

1,22,362

1,21,891

Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

Non

Equity

26%↑ y-o-y

Equity

68%↑ y-o-y

164,995

6304 6542 6378 6637

7926

FY11 FY12 FY13 FY14 FY15

( ` Crore) Revenue

368

600 761 727

849

FY11 FY12 FY13 FY14 FY15

( ` Crore)

Earnings before Tax

15

Aditya Birla Finance Limited (ABFL) - NBFC

Aditya Birla Financial Services

1,850 3,425

8,000 11,550

17,550

Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

Lending book

(` Crore)

10.2% 11.4%

14.3% 13.1%

14.6%

FY11 FY12 FY13 FY14 FY15

ROE

39%

35% 36%

31% 29%

FY11 FY12 FY13 FY14 FY15

Opex to NII

37 56 100

166

271

FY11 FY12 FY13 FY14 FY15

Net Profit

(` Crore)

196 348

715

1,201

1,776

FY11 FY12 FY13 FY14 FY15

Revenue

(` Crore)

Lending book reached USD 3 billion mark (52%↑ y-o-y)

Well diversified portfolio for sustainable growth

Growth accompanied by robust credit appraisal

and risk management practices

Gross NPA at 0.90% (PY: 1.29%)

Net NPA at 0.32% (PY: 0.58%)

Equity support and internal accruals funding growth

Net worth expanded to ` 2,585 Cr. (46%↑ y-o-y)

Infusion of ` 545 Cr. in FY15 (` 1,720 Cr. in 5 years)

Improved return ratios

ROE enhanced to 14.6% (150 bps↑ y-o-y)

ROA at 2.0% (15 bps↑ y-o-y)

Revenue at ` 1,776 Cr. (48%↑ y-o-y)

EBT at ` 411 Cr. (63%↑ y-o-y)

16

Birla Sun Life Insurance (BSLI)

Aditya Birla Financial Services

AUM crossed ` 30,000 Cr. (22%↑ y-o-y)

Ranks 6th in India with new business market share of 7.6% (in private sector)

#1 in Group new business premium @ ` 1,177 Cr. (44%↑ y-o-y)

Individual life new business premium @ ` 761 Cr. (13%↓ y-o-y)

Improved quality of business

Opex ratio at 16.6% (240 bps↓ y-o-y)

Surrender as a % of average AUM reduced y-o-y by 165 bps

Ranks 4th in India with domestic AAUM market share at 10.09% (PY: 9.85%)

Total AAUM rose to ` 1,33,689 Cr. (39%↑ y-o-y)

Strong focus on scaling up equity and offshore assets

Domestic Equity AAUM more than doubled y-o-y to ` 25,904 Cr.

# 5 in terms of equity AAUM with market share at 6.92% (PY : 5.78%)

Offshore AAUM reached USD 2 billion (103%↑ y-o-y)

Birla Sun Life Asset Management (BSAMC)

67,668 66,082

83,451

96,429

1,33,689

Q4FY11 Q4FY12 Q4FY13 Q4FY14 Q4FY15

AAUM

(` Crore)

19,760 21,110

22,929 24,775

30,185

FY11 FY12 FY13 FY14 FY15

AUM

(` Crore)

17

Aditya Birla Housing Finance (ABHFL)

Lending book as on 31st Mar’15 is ` 142 Cr.

Targeting to expand footprint from currently 15 cities to 30 cities next year

Aditya Birla Insurance Brokers (ABIBL: General Insurance Advisory)

In FY15, ABIBL’s premium placement rose y-o-y by 26% to ` 1,132 Cr. while industry premium grew by 9%

Market share increased to 1.33% (PY 1.16%)

Aditya Birla Private Equity (ABPE) : Invested more than 90% of net deployable corpus.

Aditya Birla Money (Broking, Wealth Management & Online Money Management)

Broking (ABML) : Market share improved in retail F&O and commodities segments

Higher average daily brokerage (67%↑ y-o-y) drove earnings growth

Wealth Management (ABMM) : Assets under Advisory at ~ ` 9,000 Cr. (as on 31st Mar’15)

MyUniverse is India’s #1 online personal finance management platform

Enjoying trust of > 1.5 million registered users & helping customers manage > ` 15,400 Cr. of money as on date

IFC has become a strategic financial investor in the venture

Health Insurance

Signed MoU with MMI Holdings Ltd. (a leading South African insurance-based financial services group) to enter health insurance

business in India. Final agreement is being negotiated post which application to IRDA will be made.

Aditya Birla Financial Services

18

Revenue at ` 7,926 Cr. (19%↑ y-o-y)

Earnings before Tax at ` 849 Cr. (17%↑ y-o-y)

Aditya Birla Financial Services

Revenue

FY14 FY15 ∆% (` Crore)

EBT FY14 FY15 ∆%

Remarks on profitability

1,201 1,776 48% ABFL 251 411 63% Expanded lending book (52%↑ y-o-y)

4,702 5,267 12%

BSLI 371 285 23% Lower new business sales and in-force book

502 596 19% BSAMC 140 182 29% Growth in total AUM (39%↑ y-o-y)

82 73 11% ABIBL 21 27 26% Higher premium placement (26%↑ y-o-y)

75 119 58% ABML (12) 6 n.a. Higher average daily brokerage (67%↑ y-o-y)

66 86 30% ABMM (6) 6 n.a. Increase in business volumes

9 8 Others (net of elim.) (39) (67) Scaling up MyUniverse

6,637 7,926 19% Total 727 849 17%

19

India’s #1 Menswear Player India’s #1 Womenswear Retailer

Fashion & Lifestyle

Performance highlights : 2014-15

20

Largest fashion retail presence serving 10.8 million loyalty customers

Presence across entire spectrum of Fashion with leading brands

Expanding market presence with addition of retail stores as well as

scaling up its own online presence through

Revenue at ` 5,450 Cr. (15%↑ y-o-y) & EBITDA at ` 532 Cr. (32%↑ y-o-y)

Fashion & Lifestyle

Madura 66%

Pantaloons 34%

Revenue mix FY15

1,811 2,239

3,802 4,759

5,450

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

136 196

312 401

532

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

Retail Network

895 1,129

1,367

1,648 1,869

Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

1.3 1.6

3.6 4.2

4.8

Carpet Area

(Million Sq. Ft.) EBOs / Stores

Note 1 : Excluding one-time investment income

1

21

Madura Fashion & Lifestyle1

Powerhouse of India’s leading fashion brands

Louis Philippe, Van Heusen, Allen Solly, Peter England

Extensive reach through multi-channel distribution network

1735 retail EBOs & 6000+ additional points of sale

Robust supply chain, strong in-house design & product

development capabilities

Posted strong earnings growth in FY15 despite weak customer

footfalls & higher promotions / discounting across the industry

Revenue at ` 3,735 Cr. (16%↑ y-o-y)

Retail channel sales (EBOs) : 14%↑ y-o-y led by stores expansion

L2L sales growth was flat. Added (net) 194 EBOs in FY15

Wholesale channel sales (Department Stores & MBOs) : 20%↑ y-o-y

EBITDA at ` 463 Cr. (19%↑ y-o-y)

Margins and ROACE expanded y-o-y to 12.4% & 72%

1,811 2,239

2,523

3,226

3,735

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

136 196

245

388 463

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

FY 11 FY 12 FY 13 FY 14 FY 15

EBITDA % 7.5% 8.8% 9.7% 12.0% 12.4%

ROACE % 11% 20% 29% 64% 72%

Note 1 : Includes Madura Fashion, a division of ABNL and Madura Lifestyle, a subsidiary of ABNL. Madura Fashion owns and retails India’s leading apparel brands such as Louis Philippe, Van Heusen, Allen Solly,

Peter England and People. Madura Lifestyle retails international luxury brands under the retail format ‘The Collective’ and It also retails Madura Fashion brands under the retail format ‘Planet Fashion’

22

Pantaloons Fashion & Retail Ltd.

Strategic initiatives taken since acquisition … Launched 39 new stores in past 2 years on a base of 69 stores

43 stores renovated and 100% store re-layouts accomplished

Created 7 new private brands, added 15 external brands

Created a stronger vendor network with pan India capability

… are yielding results

Customer reach scaled to 104 Stores & 30 factory outlets across 2.3 million sq. ft.

Share of Private brands & Madura brands enhanced from 46% to 62%

Voted amongst India’s top most trusted retailer brands in “Brand Equity Survey 2014”

In FY15, posted revenue at ` 1,851 Cr. (11%↑ y-o-y)

Driven by L2L growth of 5.5% and stores expansion

Added 25 pantaloons stores & 6 factory outlets in FY15

Driven by portfolio enrichment, gross margin increased to 45% (340 bps↑ y-o-y)

EBITDA almost doubled from ` 39 Cr. to ` 75 Cr.

EBITDA margin expanded to 4.1% (180 bps↑ y-o-y)

Higher accelerated depreciation on account of stores renovation & planned stores

closures impacted bottom-line

Men 35%

Women 42%

Kids 9%

Non-Apps 14%

Revenue Mix (FY15)

2.3%

4.1%

39

75

FY14 FY15

EBITDA (` Crore)

EBITDA %

1,661

1,851

FY14 FY15

Revenue (` Crore)

23

Telecom

Performance highlights : 2014-15

3rd largest Cellular Operator in India

24

Robust performance across key metrics2 driving earnings growth

Solid foundation for business growth laid for the next 20 years

Won 79.4 MHz spectrum in Mar’15 auctions for ~USD 5 billion

Idea grew at 1.8 times the wireless industry in Calendar Year 2014

FY15 revenue at ` 31,527 Cr. (19%↑ y-o-y) & EBITDA at ` 11,281 Cr. (32%↑ y-o-y)

Strong cash flows & funds raised supporting balance sheet2 & growth plans

Net debt to EBITDA2

at 1.31x (PY: 2.61x)

Generated post tax cash profit2 of ` 8,482 Cr. in FY15 (32% y-o-y growth)

Raised equity capital of ` 3,750 Cr. (through QIP & Preferential allotment)

Proposed dividend @ 6% of share capital [Outlay of ` 260 Cr. incl. DDT]

FY14 FY15 Δ%

Minutes of Use (billion) 588 683 +16.3%

Average Realisation per minute (`) 0.442 0.455 + 3.0%

Cost per minute (`) 0.325 0.319 -2.0%

Data Volume (billion Mega Bytes) 79.4 172.5 +117.3%

Consolidated Net Profit (` Crore) 1,968 3,193 +62.3%

Telecom : Idea Cellular

13.3% 14.4% 14.8%

16.1% 17.5%

Q3FY11 Q3FY12 Q3FY13 Q3FY14 Q3FY15

Revenue Market Share 1

1Based on gross revenue for UAS & Mobile licenses only, as released by TRAI 2Standalone = Idea and its 100% subsidiaries

15,438

19,489 22,407

26,432

31,527

FY11 FY12 FY13 FY14 FY15

Consolidated Revenue (` Crore)

3,910 5,085

6,071 8,519

11,281

FY11 FY12 FY13 FY14 FY15

Consolidated EBITDA (` Crore)

25

Divisions

Performance highlights : 2014-15

Leading manufacturer of Linen, Urea, VFY and Insulators in India

26

Divisions

Led by rising popularity of Linen as comfort & style fabric, its demand has grown at a strong pace.

Currently ~70% of linen yarn demand is met through imports reflecting expansion opportunity.

Jaya Shree is a leading player in Linen & Wool segments in India

Focusing on retail expansion & brand promotion to fortify ‘Linen Club’ fabric brand

Retailing linen fabric through 115 EBOs and 3,500+ MBOs

Expanded linen capacities contributing to profitable growth

Targeting to further expand Linen Yarn capacity from 3,400 TPA to

6,400 TPA at a capex of ~` 220 Cr. in 2016, to tap sector growth

Operating at a sound ROACE of 53% p.a.

Acute deficit of urea in India – Approx. 1/4th of the urea demand is imported

Government’s gas pooling policy will be beneficial for the sector as it aims to improve plants efficiency & reduce subsidy outgo

Indo-Gulf is the 8th largest & one of the most energy efficient urea plants in India

Strong ‘Birla Shaktiman’ brand is preferred choice of farmers

Indo-Gulf is a complete agri-solutions provider

Offering fertilisers, seeds and agro-chemicals

Improved energy efficiency augmented earnings y-o-y

Jaya Shree

Indo-Gulf Fertilisers

53%47%

39%61%

FY11

FY15Wool Linen

99

141154

172 175

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

774

1,0461,144

1,3001,435

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

Jaya Shree : Revenue Mix

1,244

2,107

2,924

2,3132,558

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

176

211197

77

148

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

27

Divisions

VFY is a niche market globally – premium is driven by quality & value added yarns

Indian Rayon is India’s 2nd largest manufacturer and largest exporter of VFY

Integrated facilities : 34.5 MW captive power plant & caustic soda operations

In FY15, VFY segment posted higher profitability led by expanded new

superfine yarn capacity. In Chemicals Segment, maintenance shutdown

in Caustic Soda plant & lower ECU realisation impacted earnings

Operating at an ROACE of 21% p.a.

Cheaper Chinese imports had adversely impacted domestic players and the industry had appealed for anti-dumping duty

The Ministry of Finance, on 16th Sep’14, imposed an interim anti-dumping duty on imports of insulators from China and on

11th Apr’15, extended the duty till 15th Sep’19 to create a level playing field for the domestic manufacturers

Aditya Birla Insulators is India’s largest & world’s 4th largest manufacturer

In FY15, profitability improved y-o-y led by higher volumes &

realisation in the substation segment

ROACE improved to 17% p.a.

Indian Rayon

Aditya Birla Insulators

Indian Rayon : Revenue Mix

81%

19%

FY15

ChemicalsVFY

565680

777860 865

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

110128

189222

197

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

518468 454 505

548

FY11 FY12 FY13 FY14 FY15

Revenue (` Crore)

134

67 6183

95

FY11 FY12 FY13 FY14 FY15

EBITDA (` Crore)

28

Revenue at ` 5,405 Cr. (9%↑ y-o-y)

EBITDA at ` 615 Cr. (11%↑ y-o-y)

ROACE improved y-o-y from 14% p.a. to 16% p.a.

Revenue

FY14 FY15 ∆% (` Crore)

EBITDA

FY14 FY15 ∆% Remarks on profitability

1,300 1,435 10% Jaya Shree 172 175 2% Higher profitability in Linen segment offset by lower wool

combing volumes

2,313 2,558 11% Agri 77 148 90% Improved energy efficiency, higher fixed cost reimbursement

as per Government policy and increased sales of pesticides

860 865 ↔ Rayon 222 197 11% Profitable growth in VFY segment offset by lower caustic

volumes & ECU realisation

505 548 8% Insulators 83 95 14% Higher sales volume & realisation in substation segment

4.979 5,405 9% Total 554 615 11%

Divisions (Jaya Shree, Indo-Gulf Fertilisers, Indian Rayon & Aditya Birla Insulators)

29

Going Forward

Financial Services

Gaining market share in the Life Insurance business through good quality sales driven by an efficient

distribution network with acceptable expense levels

Growing profitable assets while maintaining fund performance in the Asset Management business

Expanding book size in the NBFC business while keeping risk under control

Growing the Housing Finance business

Foray into the Health Insurance business

Driving profitable growth in other businesses

Capitalising on brand !DEA, strong cash flows and expanding spectrum profile & infrastructure in the Telecom

business to capture opportunities in voice, emerging wireless broadband business & mobile banking segments

Driving profitable expansion by tapping emerging markets in tier 2/3 cities, entering new product categories,

enriching product mix and focusing on omni-channel strategy in the Fashion & Lifestyle business

Expanding linen capacity, capturing sector growth opportunities & improving operating efficiency in the divisions

30

31

Consolidated Revenue ( ` Crore)

* Include Asset Management, NBFC, Housing Finance, Private Equity, Broking, Wealth Management, online money management & General Insurance Broking businesses

@ Idea is consolidated at ~25.3% till 10th June 2014, at 23.63% till 23rd July 2014 and at 23.29% thereafter

^ Divested w.e.f 9th May 2014

Quarter - 3 Revenue

2014-15

(PQ)

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

1,913 2,271 2,585 Aditya Birla Financial Services 6,637 7,926

1,223 1,740 1,825 Life Insurance 4,702 5,267

691 533 762 Other Financial Services* 1,946 2,666

(2) (1) (2) Elimination (11) (7)

1,865 1,752 1,955 Telecom (Nuvo's share) @ 6,669 7,467

1,349 1,243 1,403 Fashion & Lifestyle 4,759 5,450

- 724 - IT-ITeS^ 2,898 283

1,522 1,134 1,134 Divisions 4,979 5,405

336 345 374 Jaya Shree 1,300 1,435

835 408 381 Agri 2,313 2,558

204 223 216 Rayon 860 865

147 159 163 Insulators 505 548

(9) (13) (3) Inter-segment Elimination (50) (16)

6,640 7,111 7,073 Consolidated Revenue 25,892 26,516

Quarter 4 Full Year

32

Segment EBIT ( ` Crore)

* Other Financial Services include Asset Management, NBFC, Housing Finance, Private Equity, Broking, Wealth Management, online money management & General

Insurance Broking businesses. Interest cost of NBFC business, being an operating expense as per AS 17, is deducted from Segment EBIT

@ Idea is consolidated at ~25.3% till 10th June 2014, at 23.63% till 23rd July 2014 and at 23.29% thereafter

^ Divested w.e.f 9th May 2014

Quarter - 3 EBIT

2014-15

(PQ)

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

197 170 182 Aditya Birla Financial Services 725 814

60 80 45 Life Insurance 371 285

136 89 137 Other Financial Services* 354 529

296 274 367 Telecom (Nuvo's share) @ 952 1,305

68 36 73 Fashion & Lifestyle 199 261

- 53 - IT-ITeS^ 181 (16)

146 74 71 Divisions 430 494

28 37 38 Jaya Shree 141 146

62 (30) (28) Agri 56 116

31 45 35 Rayon 172 156

25 23 26 Insulators 61 76

706 607 693 Segment EBIT 2,487 2,857

Quarter 4 Full Year

33

Consolidated Profit & Loss ( ` Crore)

One-off items:

In FY15, profit is lower by ` 36 Cr. on account of net loss of ` 23 Cr. from operations of Minacs for the period from 1st Apr’14 to 8th May’14 & exceptional loss of ` 13 Cr. pertaining to the

divestment of Minacs. This loss is without considering deferred grant of ` 42 Cr. receivable over next 3 years, which will be accounted for on actual receipt basis.

In FY14, profit is higher by ` 65 Cr. on account of divestment of Carbon Black business (including net tax credit of ` 41 Cr.) and interest cost is higher by one-time charge of ` 88 Cr. on

redemption of CCDs by Minacs owing to its divestment. Exceptional items in FY14 include loss of ` 19 Cr. on impairment of goodwill relating to investments in broking & wealth management

businesses and gain of ` 24 Cr. on divestment of Carbon Black business

Quarter - 3

2014-15 (PQ) 2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

6,640 7,111 7,073 Revenue 25,892 26,516

1,484 1,263 1,527 EBITDA 4,927 5,798

291 212 318 Less : NBFC Interest expenses 742 1,105

149 259 171 Less : Other Interest Expenses 809 652

1,043 792 1,037 EBDT 3,376 4,041

452 430 464 Less : Depreciation 1,609 1,703

591 362 573 Earnings before Tax (before exceptional items) 1,767 2,338

- (19) - Exceptional Gain / (Loss) 5 (13)

591 343 573 Earnings before Tax 1,772 2,325

199 160 230 Less : Provision for Taxation (Net) 550 833

24 7 11 Less : Minority Interest 79 76

368 176 332 Net Profit 1,143 1,416

Quarter 4 Full Year Consolidated

Profit & Loss Account

34

Balance Sheet ( ` Crore)

Note : 1. Standalone capex of ` 222 Cr. was incurred in FY15. Capex guidance for FY16 stands at ` 300 Cr.

2. Investments of ` 600 Cr. are planned in financial services businesses in FY16

3. Board of Directors of ABNL has recommended an equity dividend of 70% (` 7 per share) for FY15 entailing outgo of ` 109.6 Cr. (incl. DDT of ` 18.5 Cr.)

8,108 8,519 Net Worth 11,189 12,871

- - Minority Interest 778 802

3,753 3,688 Debt 10,893 11,391

- - NBFC borrowings 9,647 14,594

88 106 Deferred Tax Liabilities (Net) 504 485

11,949 12,314 Capital Employed 33,012 40,142

- -

Policyholders' funds (Incl. funds

for future appropriation) 23,557 28,839

11,949 12,314 Total Liabilities 56,569 68,981

1,845 1,859 Net Block (Incl. Capital Advances) 13,045 12,342

20 20 Goodwill 4,982 3,973

- - NBFC Lending 11,550 17,550

1,574 1,635 Net Working Capital 730 315

7,952 8,695 Long Term Investments 410 408

- - Life Insurance Investments 24,764 30,147

- - Policyholders' Investments 23,435 28,595

- - Shareholders' Investments 1,329 1,552

557 105 Cash Surplus & Current Investments 1,089 4,246

623 655 Book Value (`) 860 989

2.6 3.0 Net Debt / Annualised EBITDA (x) 2.3 1.5

0.39 0.42 Net Debt / Equity (x) 0.88 0.56

14,196 21,654 Market Capitalisation - NSE

Mar-15

Consolidated

Mar-14Mar-14 Mar-15

Standalone

Balance Sheet

35

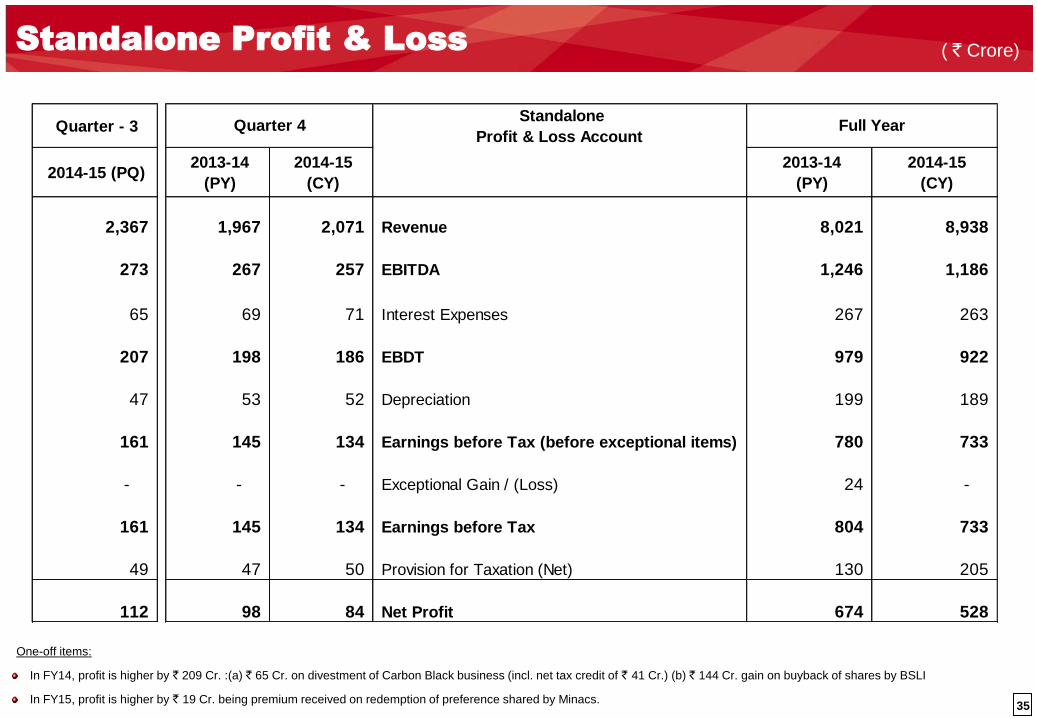

Standalone Profit & Loss ( ` Crore)

One-off items:

In FY14, profit is higher by ` 209 Cr. :(a) ` 65 Cr. on divestment of Carbon Black business (incl. net tax credit of ` 41 Cr.) (b) ` 144 Cr. gain on buyback of shares by BSLI

In FY15, profit is higher by ` 19 Cr. being premium received on redemption of preference shared by Minacs.

Quarter - 3 Standalone

Profit & Loss Account

2014-15 (PQ) 2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

2,367 1,967 2,071 Revenue 8,021 8,938

273 267 257 EBITDA 1,246 1,186

65 69 71 Interest Expenses 267 263

207 198 186 EBDT 979 922

47 53 52 Depreciation 199 189

161 145 134 Earnings before Tax (before exceptional items) 780 733

- - - Exceptional Gain / (Loss) 24 -

161 145 134 Earnings before Tax 804 733

49 47 50 Provision for Taxation (Net) 130 205

112 98 84 Net Profit 674 528

Full YearQuarter 4

36

37

Aditya Birla Financial Services

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

Revenue

1,740 1,825 Birla Sun Life Insurance 4,702 5,267

346 504 Aditya Birla Finance 1,201 1,776

125 184 Birla Sun Life Asset Management 502 596

18 14 Aditya Birla Insurance Brokers 82 73

20 31 Aditya Birla Money 75 119

19 23 Aditya Birla Money Mart 66 86

5 5 Aditya Birla Capital Advisors (PE) 23 21

(2) (2) Others / (Elimination) (14) (13)

2,271 2,585 Revenue 6,637 7,926

155 190 Earnings before tax 727 849

122 134 Net Profit 584 638

Quarter 4

` Crore

Full Year

38

Aditya Birla Finance (ABFL)

Loan book growth continues to be robust and of good quality

More than 80% of lending book is secured

Attained growth across all the segments

Mortgages book crossed ` 5,000 Cr. (71%↑ y-o-y)

Capital Market, Infra & Corporate finance books crossed ` 4,000 Cr. each

Healthy borrowings Profile

Highest A1+ rating for short term debt

Long term debt rating upgraded to AA+ in FY15

Out of total borrowings ~75% is long term (PY: ~60%)

Capital Market

24%

Corporate Finance

23%

Infra Financing

23%

Mortgage* 29%

Others 1%

Lending book as on 31st Mar’15 : Break-up

* LAP / LRD & Construction Finance

(PY:26%)

(PY:22%)

(PY:23%)

(PY:28%)

(PY:1%)

2013-14

PY

2014-15

CY

Revenue 346 504

Earnings before tax 71 117

Net Profit / (Loss) 47 77

Revenue 1,201 1,776

Earnings before tax 251 411

Net Profit / (Loss) 166 271

Quarter 4

Full Year

` Crore

FY13 FY14 FY15

Net Interest Income (incl. fee income) (%) 5.4% 5.1% 5.0%

Return on Avg. Assets (p.a.) (%) 1.92% 1.85% 2.0%

Gross NPA (as % of total loans & advances) 1.23% 1.29% 0.90%

Net NPA (as % of total loans & advances) 0.83% 0.58% 0.32%

Net Worth (` Crore) 1,079 1,769 2,585

Borrowings (` Crore) 6,867 9,647 14,594

Leverage (x) 6.4x 5.5x 5.6x

39

Industry

In FY15, industry’s total new business de-grew by 9% while

private sector grew by 16%. In individual life new business,

industry de-grew by 10% while private sector grew by 16%

Private sector growth is driven by large bank backed players

Open architecture in bancassurance and increase of FDI / FII

limit in insurance sector from 26% to 49% will be beneficial for

the industry

Birla Sun Life Insurance

In FY15, New business premium at ` 1,938 Cr. (14%↑ y-o-y)

Renewal premium at ` 3,295 Cr. (5%↑ y-o-y)

Revenue at ` 5,267 Cr. (12%↑ y-o-y) driven by group business

EBT at ` 285 Cr. (23%↓ y-o-y)

Share of non-ULIPs in individual new business at 62% (PY: 60%)

Out of this, PAR products contributed to 42% (PY: 31%)

Birla Sun Life Insurance (BSLI)

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

726 710 New Business Premium (Gross) 1,697 1,938

297 271 Individual 879 761

429 438 Group 818 1,177

1,052 1,110 Renewal Premium (Gross) 3,136 3,295

1,018 1,065 Individual 3,010 3,156

34 45 Group 125 140

1,778 1,820 Premium Income (Gross) 4,833 5,233

(80) (79) Less : Reinsurance ceded & Service tax (307) (267)

1,699 1,741 Premium Income (Net) 4,526 4,966

41 85 Other Operating Income 176 301

1,740 1,825 Revenue 4,702 5,267

80 45 Earnings before tax 371 285

80 45 Net Profit 371 285

Assets under management 24,775 30,185

Policyholders' Investments 23,445 28,632

Shareholders' Investments 1,329 1,552

Full Year

` Crore

Quarter 4

40

Industry

Recorded its highest ever AAUM at ` 11.95 trillion (31%↑ y-o-y)

Equity AUM rose by 89% to ` 3.7 trillion contributing to more

than 60% of industry’s AUM growth in 2014-15

Birla Sun Life Asset Management

Total AAUM at ` 1,33, 689 Cr. (39%↑ y-o-y)

Equity & offshore AAUM surged by 124% and 103%

Consistently gaining market share

Equity market share is expanding year after year

Attained 10.3% share in industry’s net equity sales during 2014-15

Retail focus

Monthly SIP book size is 84%↑ y-o-y

Revenue at ` 596 Cr. (19%↑ y-o-y) & EBT at ` 182 Cr. (29%↑ y-o-y)

Recognition of strong fund performance

‘Asset Management House of the Year’ by Money Today-FPCIL Awards 2015

‘Best Fund House – Debt’ by Morningstar Awards 2015

Birla Sun Life MNC fund won ‘Best Small/Mid Cap Equity fund’ – Morning Star 2014

Birla Sun Life Asset Management (BSAMC)

` Crore

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

125 184 Revenue (Fee Income) 502 596

25 49 Earnings before tax 140 182

17 33 Net Profit 95 123

Quarter 4 Full Year

Revenues

Q4FY14

(PY)

Q3FY15

(PQ)

Q4FY15

(CY)

Domestic Equity &

Alternate Assets12,922 23,141 27,555

Domestic Fixed Income 77,586 86,673 94,128

Offshore Assets 5,921 7,675 12,006

Total AUM 96,429 1,17,489 1,33,689

` Crore

Average AUM

8.35% 9.09% 9.20% 9.45%

9.85% 10.09%

5.09% 5.45% 5.27% 5.26%

5.78%

6.92%

FY10 FY11 FY12 FY13 FY14 FY15

Domestic Market Share Equity Market Share

41

Other Financial Services

> Aditya Birla Housing Finance : Book Size at ` 142 Cr. as on 31st Mar’15

> Aditya Birla Insurance Brokers (General insurance advisory)

In FY15, premium placement grew from ` 898 Cr. to ` 1,132 Cr. (26%↑ y-o-y)

Revenue at ` 73 Cr. (11%↓ y-o-y) and EBT at ` 27 Cr. (26%↑ y-o-y)

> Aditya Birla Money (Broking, Wealth Management & Online Money Management )

Broking : Industry volumes were up by 71% in retail cash equity, up by 50% in retail F&O & lower by 36% in commodities

Market share of Aditya Birla Money improved to 2.48% (PY:1.37%) in retail F&O, 0.64% (PY:0.54%) in commodities & 0.50%

(PY: 0.29%) in currency segment while it was lower in retail cash equity segment at 1.34% (PY:1.43%)

Wealth Management: Average equity assets under advisory expanded y-o-y by 34%

Online Money Management Portal (MyUniverse) : Launched ZipSip – the smarter, easier and quicker way of doing SIP

> Aditya Birla Private Equity : Funds under management (net) at ` 1,121 Cr.

Invested in Wonderla Holidays, City Union Bank, Indian Energy Exchange, Manpasand Beverages, CIBIL & Monte Carlo Fashions in FY15

PY CY PY CY PY CY PY CY

Revenue 18 14 20 31 19 23 5 5

Earnings before tax 1 2 (1) 1 2 2 2 0

Net Profit / (Loss) 1 1 (1) 1 2 2 1 0

Revenue 82 73 75 119 66 86 23 21

Earnings before tax 21 27 (12) 6 (6) 6 9 6

Net Profit / (Loss) 14 18 (12) 6 (6) 5 6 4

Full Year

Aditya Birla

Money Mart

(Wealth Management)

Aditya Birla Insurance

Brokers (General

Insurance Broking)

` Crore Quarter 4

Aditya Birla Money

(Equity & Commodity Broking)

Aditya Birla

Capital Advisors

(Private Equity)

42

Capex of ` 95 Cr. was incurred during FY15

Capex guidance for FY16 stands at about ` 160 Cr. mainly towards new store launches and renovation of existing stores

Madura Fashion & Lifestyle

Retail Channel

895

1,129 1,272

1,541 1,735

Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

1.3 1.6

1.9 2.2

2.5

Carpet Area (Million Sq Ft)

No. of EBOs

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

893 984 Revenue 3,226 3,735

117 138 EBITDA 388 463

93 112 Segment EBIT 299 377

457 591 Capital Employed 457 591

82 79 ROACE (Annualised) (%) 64 72

Quarter 4

` Crore

Full Year

43

Pantaloons Fashion & Retail Ltd.

Capex of ` 115 Cr. was spent during FY15

Launched 13 new stores in Q4 (25 during the year)

FY16 capex guidance stands at about ` 125 Cr. mainly

towards launch of 30-35 new stores

Customer Reach

90 95 107

134

Jun'12 Mar'13 Mar'14 Mar'15

1.6 1.7 2.0

2.3

Carpet Area (Million Sq Ft)

No. of Stores incl.

Factory Outlet ` Crore

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

410 460 Revenue 1,661 1,851

3 17 EBITDA 39 75

(46) (33) Segment EBIT (75) (110)

Quarter 4 Full Year

` Crore

As on

31st

Mar'14

As on

31st

Mar'15

Net Fixed Assets (Incl. Capital Advances) 496 422

Goodwill 1,168 1,168

Cash & Current Investments 17 7

Net Working Capital (50) 60

Net Worth 579 346

Debt 1,050 1,311

44

Base of 161 million active subscribers provides a great platform for upgrading voice customers to wireless data services in future

Currently, 33.4 million Idea subscribers use its mobile data services, contributing 16.9% of total service revenue in Q4FY15

As of Mar’15, Idea had 102.3% of reported subscribers as VLR (active) subscribers – highest in the industry

VAS as percentage of service revenue grew to 24.5% in Q4FY15 (PQ: 23.1%, PY: 16.5%)

Capex of ` 40.5 billion (excl. spectrum) incurred in FY15. Capex guidance for FY16, (excl. spectrum payout) stands at ` 50-55 billion

Idea Cellular

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

6,975 8,397 Revenue 26,432 31,527

2,273 3,251 EBITDA 8,519 11,281

1,090 1,577 Segment EBIT 3,773 5,508

590 942 Net Profit 1,968 3,193

Net Worth 16,527 23,029

Total Debt 20,635 26,859

Capital Employed 37,162 49,888

ROACE (Annualised) (%) 12 14

` Crore

(Consolidated Results)

Quarter 4 Full Year

45

Jaya Shree

Industry

Apparels & Textiles industry witnessed subdued consumer

spending during H2FY15

Jaya Shree

Revenue at ` 1,435 Cr. (10%↑ y-o-y)

Linen segment surged by 25% driven by expansion

Wool segment de-grew due to poor wool grease demand

EBITDA at ` 175 Cr. (2%↑ y-o-y)

Higher profitability in linen segment was offset by lower

wool combing volumes

Continuous focus on retail expansion and brand promotion to

fortify ‘Linen Club’ fabric brand

Opened 19 new ‘Linen Club’ EBOs during the year to reach

a total of 115 EBOs

Launched its own apparel line through ‘Linen Club Studio’

Operating at a sound ROACE of 53% p.a.

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

167 196 Linen Segment 614 765

177 178 Wool Segment 687 671

345 374 Revenue 1,300 1,435

45 46 EBITDA 172 175

37 38 Segment EBIT 141 146

317 237 Capital Employed 317 237

54 65 ROACE (Annualised) (%) 57 53

` Crore

Quarter 4 Full Year

46

Industry

Due to government policy for urea production beyond

100% quantity as permissible under Pricing mechanism,

few urea manufacturers had to take urea plant shutdown

during Q4FY15

Indo-Gulf

Indo-Gulf had to take urea plant shutdown for 35 days

starting 27th Feb’15, thereby, pulling down earnings from

normalised level. The plant resumed operations on

2nd Apr’15. During last year too, urea plant shutdown was

taken for 41 days

Revenue grew y-o-y by 11% largely due to pass through

of rise in natural gas prices & higher sales of customised fertilisers

EBITDA surged y-o-y by 90% to ` 148 Cr. led by improved energy efficiency, higher fixed cost reimbursement as per

Government policy and higher sales of pesticides

Outstanding subsidy & receivables at ` 1,207 Cr. (PQ: ` 1,109 Cr., Mar’14 : ` 1,176 Cr.)

Indo Gulf Fertilisers

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

175 176 Manufactured Urea Sales ('000 MT) 1,034 1,025

408 381 Revenue 2,313 2,558

361 348 Manufacturing(Urea, Customised Fertilisers)

1,995 2,248

47 33 Trading (Fertilisers, Seeds, Agro-Chemicals)

318 310

(25) (20) EBITDA 77 148

(30) (28) Segment EBIT 56 116

1,616 1,641 Capital Employed 1,616 1,641

(8) (7) ROACE (Annualised) (%) 3 7

Full Year

` Crore

Quarter 4

47

Industry

Indian textiles industry witnessed slowdown in H2FY15 with

steep fall in demand & prices across all major fibres & yarn.

ECU realisation declined y-o-y due to cheaper caustic imports

and lower chlorine prices. Q-o-Q, realisation has improved.

Indian Rayon

Amidst industry slowdown, Indian Rayon posted strong growth

in VFY profitability driven by new superfine yarn capacity

Total Revenue grew marginally y-o-y to ` 865 Cr.

VFY : Higher volumes led by new capacity

Chemicals : Softening of ECU realisation & lower caustic

volumes due to maintenance shutdown in power plant

EBITDA de-grew y-o-y by 11% to ` 197 Cr.

VFY : Expansion led higher volumes & realisation drove profitable growth

Chemicals : Lower ECU realisation & caustic soda volumes impacted coupled with higher power cost owing to shutdown

Operating at an ROACE of 21% p.a.

Indian Rayon

Note 1 : Including captive consumption and inter unit sale

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY) Net Revenue VFY

4,516 4,632 Manufactured VFY Sales Volumes (MT) 17,423 18,839

171 172 Revenue (VFY & allied chemicals) ( ` Cr.) 659 699

Chemicals

20,172 20,716 Caustic Soda Sales Volume (MT)1 86,758 80,162

51 44 Revenue ( ` Cr.) 202 166

223 216 Total Revenue 860 865

57 45 EBITDA 222 197

45 35 Segment EBIT 172 156

759 757 Capital Employed 759 757

23 19 ROACE (Annualised) (%) 24 21

Full Year

` Crore

Quarter 4

48

Aditya Birla Insulators

Industry

Insulators industry’s domestic sales volume de-grew

y-o-y by 12% during Apr’14-Jan’15 (Source : IEEMA)

Long term imposition of anti-dumping duty on imports from

China will provide sustainable relief to domestic manufacturers.

Aditya Birla Insulators

Revenue grew y-o-y by 8% to ` 548 Cr.

EBITDA rose by 14% to ` 95 Cr.

Higher volumes and increase in realisation (mainly to pass on

rise in operating costs) in the substation segment contributed

to the earnings growth

Profitability in the transmission segment was lower due to 42 days disruption / suspension of plant operations in Q1FY15

caused by stoppage of work in the plant by workers, pending long term wage settlement.

ROACE improved from 15% p.a. to 17% p.a.

2013-14

(PY)

2014-15

(CY)

2013-14

(PY)

2014-15

(CY)

11,340 11,564 Sales Volumes (MT) 36,913 38,581

159 163 Revenue 505 548

28 30 EBITDA 83 95

23 26 Segment EBIT 61 76

430 455 Capital Employed 430 455

22 24 ROACE (Annualised) (%) 15 17

Full Year Quarter 4

` Crore

49

50

Transaction Structure

ABNL

Transaction Steps

PFRL

58.3% 41.7%

27.4% 72.6% #

ABG Public

1 ABNL

MGLRCL

Madura

Lifestyle

2

100% #

Pre Transaction Post Transaction

39.84% 9.06% #

ABG Public

1

PFRL / ABFRL

Madura

Lifestyle

51.1%

Swap Ratio

# Including indirect holding

Mirror Demerger of Madura Fashion division into PFRL

Mirror Demerger of Madura Lifestyle division into PFRL

Net debt of ~Rs. 473 Cr. will be transferred along with the

businesses into PFRL. Transaction is subject to corporate &

regulatory approvals and is expected to take 6 to 9 months

1

2

26 equity shares of PFRL for every 5 equity shares of ABNL

7 equity shares of PFRL for every 500 equity shares of

MGLRCL

1 equity share of PFRL for all o/s preference shares of

MGLRCL

Shareholder holding 100 shares in ABNL will continue to hold 100 shares in ABNL & in addition will get 520 shares of PFRL

51

Transaction Details

Regulatory Body Requirement

Stock Exchange and SEBI

Scheme filing after board approval

Post court order – Allotment of shares

Approval for listing of shares

High Courts Bombay and Gujarat High Courts

Transaction is expected to be completed in next 6 - 9 months

Advisors

Transaction Advisor • Standard Chartered Bank

Independent Fairness Opinion • Axis Capital Limited

• JM Financial Institutional Securities Pvt. Ltd.

Legal Advisor • Amarchand & Mangaldas & Suresh A Shroff & Co.

Valuation Expert • Price Waterhouse & Co. LLP

• Bansi S Mehta & Co.

Key Regulatory Approvals

52

Annexure IV : Reporting Structure

Divisions

Rayon*

Agri*

Fashion &

Lifestyle

Financial

Services Telecom $ #

(23.28%)

Asset Management^

(51%) @

Life Insurance^

(74%) @

Private Equity (100%) ^

Broking (75%)^ #

Wealth management (100%) ^

General Insurance Advisory (50.01%) ̂ MyUniverse (100%)^

Insulators*

Represent Joint Ventures Represent Subsidiaries @ JV with Sun Life Financial, Canada Represent Divisions # Listed * ^ $

Leadership position in India Leader Top 3 Top 5

Pantaloons^ #

(72.62%)

Madura* Jaya Shree*

Note : Percentage figures indicated above represent ABNL’s shareholding in its subsidiaries /JV’s

NBFC & Housing Finance (100%) ^

53

Disclaimer

Certain statements made in this presentation may not be based on historical information or facts and may be “forward looking statements” including, but

not limited to, those relating to general business plans & strategy of Aditya Birla Nuvo Limited ("ABNL"), its future outlook & growth prospects, future

developments in its businesses, its competitive & regulatory environment and management's current views & assumptions which may not remain constant

due to risks and uncertainties. Actual results may differ materially from these forward-looking statements due to a number of factors, including future

changes or developments in ABNL's business, its competitive environment, its ability to implement its strategies and initiatives and respond to

technological changes and political, economic, regulatory and social conditions in the countries in which ABNL conducts business. Important factors that

could make a difference to ABNL’s operations include global and Indian demand supply conditions, finished goods prices, feed stock availability and

prices, cyclical demand and pricing in ABNL’s principal markets, changes in Government regulations, tax regimes, competitors actions, economic

developments within India and the countries within which ABNL conducts business and other factors such as litigation and labour negotiations.

This presentation does not constitute a prospectus, offering circular or offering memorandum or an offer to acquire any shares and should not be

considered as a recommendation that any investor should subscribe for or purchase any of ABNL's shares. Neither this presentation nor any other

documentation or information (or any part thereof) delivered or supplied under or in relation to the shares shall be deemed to constitute an offer of or an

invitation by or on behalf of ABNL.

ABNL, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to, the

fairness, accuracy, completeness or correctness of any information or opinions contained herein. The information contained in this presentation, unless

otherwise specified is only current as of the date of this presentation. ABNL assumes no responsibility to publicly amend, modify or revise any forward

looking statements on the basis of any subsequent developments, information or events or otherwise. Unless otherwise stated in this document, the

information contained herein is based on management information and estimates. The information contained herein is subject to change without notice and

past performance is not indicative of future results. ABNL may alter, modify or otherwise change in any manner the content of this presentation, without

obligation to notify any person of such revision or changes. This presentation may not be copied and disseminated in any manner.

INFORMATION PRESENTED HERE IS NOT AN OFFER FOR SALE OF ANY EQUITY SHARES OR ANY OTHER SECURITY OF ABNL

This presentation is not for publication or distribution, directly or indirectly, in or into the United States, Canada or Japan. These

materials are not an offer of securities for sale in or into the United States, Canada or Japan.

Aditya Birla Nuvo Limited

Corporate Identity Number L17199GJ1956PLC001107

Regd. Office: Indian Rayon Compound, Veraval – 362 266 (Gujarat)

Corporate Office: 4th Floor ‘A’ Wing, Aditya Birla Center, S.K. Ahire Marg, Worli, Mumbai – 400 030

Website: www.adityabirlanuvo.com or www.adityabirla.com Email: [email protected]