Embed Size (px)

Citation preview

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109 ISSN 2152-1034

Strategic Philanthropy and Maximization of Shareholder

Investment through Ethical and Values-Based Leadership in a Post

Enron/Anderson Debacle

Hopeton Morrison, Doctoral Candidate, Nova Southeastern University Bahaudin G. Mujtaba, Nova Southeastern University

Abstract

This paper discusses the relationship between strategic philanthropy and the maximization of

shareholder value. It highlights such key concepts as ethics, values, corporate social

responsibility (CSR), corporate social performance (CSP), corporate financial performance

(CFP), organization citizenship and strategic philanthropy. It is posited that unethical behavior

by firms result in three levels of costs that can ultimately leads to the firm’s demise. Finally,

reflections and discussions are provided to assess if there is an optimal level of strategic

philanthropy for maximizing shareholder value. The conclusion is that increasing shareholder

wealth is positively correlated to CSR and that a firm’s investment in CSR is a function of the

collective ethics and value set of the firm’s leaders and followers.

Key terms: Ethics, morality, values-based leadership, philanthropy, value maximization, and shareholder value.

Introduction: Ethics and Morality in Business

Ethics and morality are integral part of successful leadership and business. Business ethics is a study in personal moral norms and how these apply to an organization’s goals and activities (Nash, 1990). Because ethics is norm-based it is not built on its own separate moral standard but speaks to the concept of relativism. Weiss (2003) speaks to ethical relativism as holding no universal standards or rules to either guide or evaluate whether an act is moral or immoral. He argues that an individual’s ethical responses are a product of one’s own value system. Weiss further extends the concept to cultural relativism which speaks to the philosophy of imitating the behavior of Romans when in Rome. Different cultures apply different criteria for judging right and wrong largely on the basis of customs, value systems and belief systems. Within these diverse systems individuals, business professionals and top executives must craft a value system for themselves and their organizations that while relevant, to the cultural nuances of its host environment must remain faithful to their core value systems.

Due to socialization in the society, most managers and leaders probably have had a good amount of reading on the basics of ethics, leadership, stewardship, morality, and social

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 95

responsibility (Mujtaba, 2006). As such, they have formed a good understanding of them based on their experiences and thoughts. However, most people do not really take the time to understand the true meaning of values, ethics and morality because of their busy schedules. Understanding business ethics should start with the basics by differentiating between values, ethics and morals (Mujtaba, 1997a; Mujtaba, 2006; and Cavico and Mujtaba, 2009). Values are core beliefs or desires that guide or motivate our attitude and actions. What one values drives his/her behavior. Some people value honesty or truthfulness in all situations while others may value loyalty to a higher degree in certain situations. Ethics is the branch of philosophy that theoretically, logically, and rationally determines right from wrong, good from bad, moral from immoral, and just from unjust actions, conducts, and behavior (Mujtaba, 1997b). Some people define ethics simply as doing what you say you would do or walking the talk. Overall, ethics establishes the rules and standards that govern the moral behavior of individuals and groups. It also distinguishes between right and wrong conducts. It involves honest consideration to underlying motive, to possible potential harm, and to congruency with established values and rules. Applied ethics refers to moral conclusions based on rules, standards, code of ethics, and models that help guide decisions. There are many subdivisions in the field of ethics and some of the common ones are descriptive, normative, and comparative ethics. Business ethic, more specifically, deals with the creation and application of moral standards in the business environment. Morals are judgments, standards, and rules of good conduct in the society. They guide people toward permissible behavior with regard to basic values. Understanding values, ethics and morals while using ethical principles, each organization can form a framework for effective decision-making with formalized strategies. The willingness to add ethical principles to the decision-making structure indicates a desire to promote fairness, as well as prevent potential ethical problems from occurring. Corporate ethics programs are part of organizational life and organizations can use such sessions to further discuss the meaning of values, ethics and morals in the context of their businesses (Mujtaba, 2006; and Cavico and Mujtaba, 2009). Their organizational codes of ethics should protect individuals and address the moral values of the firm in the decision-making processes. This also will increase personal commitment of employees to their companies because people do take pride in the integrity of their corporate culture. Velasquez (2002) argues that although ethics is the study of morality, it is not the same as morality as, while ethics investigates morality and both the subject matter and the results are important, morality is actually the subject matter that is being investigated. He speaks to moral standards as including those norms that define right and wrong actions as well as right and wrong value systems. Velasquez identifies five characteristics that define moral standards. First, moral standards can either seriously benefit or seriously harm human beings. Second, moral standards are validated by reasons that are sufficiently adequate to support and justify them. Third, moral standards should override all other non moral values especially self interest. Fourth, moral standards are based only on the moral or right point of view and are indifferent to all else except impartial moral considerations. Fifth, moral standards associate strong emotions such as guilt, shame or remorse when breached by oneself or resentment, indignation and disgust to others when they breach these standards. Within that broader definition of morality, Velasquez (2002) offers a wider definition of ethics as a discipline that analyzes one’s individual moral standards and/or the moral standards of the wider society. Hence the ultimate aim of ethics becomes one of developing a body of moral standards.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 96

Organizations and Values-Based Leadership

Maierhofer, Rafferty and Kabanoff (2003) argue as to when and why values are important in organizations. They refer to Rokeach (1973) who defines value as an enduring belief where a definite mode of conduct or certain end state existence is preferred over an opposite mode of conduct or end state existence. Some theorists are of the view that values occur based on a hierarchy measured by their relative importance to individuals (Ravlin & Meglino, 1989; Rokeach, 1973) while others accept that values are independent of each other (Kluckhohn, 1951). Maierhofer, et al. (2003) differentiate between measuring values using ipsative assessment and normative assessment. Whereas the ipsative construct requires forced choices between values normative assessments examine values separately using rating scales. They argue that broadly the values construct applies to many levels among them cultural, societal, organizational, group, and the individual. In the management lexicon it is individual values that have traditionally dominated as it was felt for some time that the power holders in organizations including chief executive officers (CEOs) wielded disproportionate value influence. Hofstede (1998), however, argues against the values of the powerful translating into shared beliefs among other members including those in the lower ranks of the organization. Maierhofer et al. (2003) state that values enter three temporal conditions. The first condition is value acquisition and they argue that entry into an organization is important for individual value acquisition. The second condition addresses value maintenance. And the third condition is values during a time of organizational change. Across this a framework is developed across the interrelationship of individual, group and organizational values resulting in nine conditions. The first and most important of these nine conditions speaks to the individual’s value acquisition process. The authors arrive at a conclusion that it is at the time of organizational entry that the firm is best able to influence an individual’s value system within that organization. They also argue against a commonly held theoretical assumption among some that individual values influence behavior but in fact the empirical evidence does not support this theory. Maierhofer et al. (2003) draw reference to Boxx, Odom and Dunn (1991) who examine individual-organizational value congruence. Boxx et al. inferred that those persons who worked in organizations where there was congruence with their own individual values were more satisfied workers than those who did not. When changes are occurring, this type of congruence becomes a frame of reference for maintaining the organization’s value systems. Some ethical breaches occur in organizations when a change in the culture occurs with the employment of a new CEO or there are wholesale changes in top management or policy directions. Moving from a conservative, risk averse, affiliation oriented culture to one of innovation, risk orientation, and aggression sometimes create anxiety and resistance in some individuals and sometimes create opportunity for individual value shifts away from those associated with the organization thus creating a propensity for negative congruence and, hence, ethical lapses. Values play a pivotal role in the emergence of an organizational culture. Among the several definitions of organizational culture, Rosseau (1990) defines this as grouped cognitions that reflect values, beliefs, understandings and expectations and that these are acquired and shared by most or all members of an organization. This culture is built on the basis of learning from the social unit that is the organization. It is important that the point is reinforced however that it is easier to influence an organizational value culture at the acquisition stage rather than at

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 97

the maintenance stage or when there are organizational changes imminent. As it is in the case of individuals so it is in the case where organizations are being founded or merged. Establish the value systems at the outset. So important is values in culture and culture in the organization that Harrison and Carroll (1991) put forward the position that a strong culture becomes an alternative to the formal structure. Maierhofer et al. (2003) argue that there is empirical evidence to support the notion that supportive, people oriented value cultures associate more with positive affective outcomes than aggressive, non supportive and task oriented cultures.

Hambrick and Mason (1984) argue in their upper echelons theory that organizations’ top management teams (TMT) drive the culture of organizations and this is generally accepted within the broad field of business ethics. It is within this context that we consider the discussion around values based leadership versus ethical based leadership. Brown and Treviño (2003) argue that value-based leadership is built around the leaders’ ability to motivate followers to achieve exceptional performance. Values-based leadership has been cited for restoring corporate reputations (Pellet, 2002) and even building companies that last for generations (Collins & Porras, 1994). The 1990s has been riddled with a series of corporate failures with perhaps none being more spectacular than Enron where a Darwinian culture overtook a veritable institution that once prided itself as among the most ethical in corporate America. Brown and Treviño argue that values-based leadership is different from ethical leadership and seek to build on empirical studies to further this claim. They draw on the work of Rokeach (1973) which differentiates between terminal values that focus on the end states achievements such as accomplishments and friendships and instrumental values that become the mode to end state or terminal values. Schwartz (1996) forwarded the position that values can be either compatible such as where power and achievement are the driving factors or conflicting such as where they lie at divergent ends of a values continuum. In their analysis of the empirical data Brown and Treviño (2003) state that one of the conclusions drawn so far was that American managers were strongly oriented to pragmatism as against ethicality and in this they draw on England (1967) whose Personal Values Questionnaire (PVQ) has attracted some interest among academics. Values based leadership is by no means new however as nearly 70 years ago Barnard (1938) advocated value driven leadership. This theme has been developed by Selznick (1957) and within the last two decades by modern management thinkers such as Chappell (1999) and Collins and Porras (1994). Brown and Treviño (2003) state that much of the literature on values-based leadership is mired in confusion. They argue that it is more than the transmission of moral and ideological values as suggested by House (1996) or transformational leadership as espoused by Burns (1978). If values-based leadership is accepted as an influencing process the leader then becomes the influencing agent. Kelman (1958) spoke to identification, internalization and compliance as three of the most powerful tools used by leaders to influence their direct reports. Of the three the most potent influencer is values internalization which takes place when followers adopt and take ownership of their leaders values. They engage these values inside and outside of the workplace, irrespective of the context of the job to be done and even beyond the leader-subordinate relationship. Selznik (1957) proffered the view that internalization can lead to exceptional follower commitment. Nonetheless Brown and Treviño bemoan the paucity of existing empirical research to help us understand how the process works. Compliance is a weaker influencer than internalization as leaders are relying less on affective influencers and more on transactional processes including legitimacy, reward and/or

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 98

coercion. Identification is also a weaker influencer as here followers are led more by how much they like their leader rather than because they share the leader’s values. Strong leaders wield enormous influencing power over their direct reports and other followers. Taken to one extreme value influencing leaders become transformational leaders who end up inducing followers to seek out goals that meet the values, motivations, wants, needs, aspirations, and expectations of both leader and follower (Burns, 1978). Among the theories cited by Burns was Kohlberg’s (1969) cognitive moral development theory, a widely cited theory among ethicists. Burns argued that transformational leaders jointly developed shared values with their followers as these although powerful were not manipulative. Only recently has there been any empirical study on ethical leadership (Trevino, Hartman, & Brown, 2000; Trevino, Brown & Hartman, 2003). Their studies identified an ethical leader as a person perceived as a moral person on one hand and an ethical manager on the other. To be perceived as a moral person ethical leaders are reputed to possess some personal traits including honesty and integrity. Ethical person perception also means showing concern for followers, willing to listen, and leading by example. The ethical leader should be fair, objective, and able to grasp the multiple stakeholder relationships that he or she must satisfy. These leaders are guided by an ethical value set as well as decision rules. Indeed how these leaders engage in decision making is also an important measure of their perception as a moral person. But the research conducted by Trevino, Hartman and Brown (2000) and Trevino, Brown and Hartman (2003) also concluded that a moral person perception was not enough to be perceived as an ethical leader. It was just as important to be perceived as a moral manager. Here perception is removed from the affective domain and the manager’s transactional leadership is examined. Followers react to how the manager goes about setting and communicating ethical standards. Both the moral person and moral manager construct are important and the ethical leader is perceived to be strong in both areas. James Burke, the former CEO of Johnson & Johnson, is cited by Brown and Trevino (2003) as exemplifying ethical leadership. He who turned what was a potential disaster for Johnson and Johnson following the mysterious cyanide poisoning of the Tylenol brand by not only recalling but re-branding the product as a safer product at the organization’s cost. Brown and Trevino contrasted Burke’s act with that of Al Dunlap, former Sunbeam CEO who was identified by senior executives and ethics officers from some large American corporations as an unethical leader. Among Dunlap’s misdeeds were his use of creative accounting techniques geared at distorting financial projections for short term gains at the expense of the organization’s longer term survival. Brown and Trevino (2003) seek to establish a relationship between values-based and ethical leadership. While acknowledging that both overlap, they make the point that the differences are important. Bass (1985) categorizes values based leadership as being synonymous with transformational leadership and that transformational leaders do have a strong negative side, Gandhi and Hitler represent contrasting sides of the transformational continuum. Burns (1978) argues that values-based leadership is often defined by moral values. Brown and Trevino stress further that current research in values-based leadership tends to ignore the content of the values being transferred and has focused instead on the sharing relationship between leader and follower as followers are usually more inclined to share their leaders’ values irrespective of the content of these values. It is here that the differences with ethical leadership emerge as ethical leadership focuses on the content of the values.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 99

Jack Welch was held to be a model manager as CEO at General Electric and he highlights a few key values that defined his leadership. These were profitability, success and dominance driven by GE’s mission to be at least number two in every venture entered. Welch was a values-driven leader but his record as an ethical leader and one who displayed a sense of corporate social responsibility has been questioned by some including O’Boyle (1998). A leader like Welch that achieves enormous success, influence and power is a values-driven leader and profitability and dominance will almost always guarantee the success of a firm and its leaders. And some leaders attempt to merge their success values-driven ethic with a sense of ethical leadership - such is the Schwartz (1992, 1996) mantra that good ethics is good business. In fact the communication of moral values by the ethical leader is only a small part the role set. Brown and Trevino (2003) did not find ethical leaders to be visionary or passionate in their study. They were distinguished by their propensity to set ethical standards and rewarding ethical behavior in followers. If anything, ethical leaders tended to be more transaction oriented in their leadership styles although in their concern for people they are also transformational. Standards become necessary because of the abstraction of values. Standards serve to concretize these values. Outcomes-Driven Ethical Leadership

So far we have attempted to bring a brief discussion and literature on some of the fundamentals and academic work on ethics and values. We now seek to address the proposition that ethical leaders with strong value sets will lead highly ethical firms also built on strong moral value sets. Such corporations will increase shareholder value. On the other hand unethical leaders build unethical cultures and create loose moral value sets with the firms that they lead and this will result in diminished shareholder value, and if left unchecked will ultimately destroy shareholder value. Thomas, Schermerhorn, Jr., and Dienhart (2004) argue that the creation of ethical behavior and a strong moral value set in business must be approached with the same discipline as that of profit creation, return on investment and creation of shareholder value. Paine (1994) addresses the issue from another perspective when he argues that not only does unethical business practices involve the explicit or tacit involvement of some managers but more disturbingly reflect on the value system and behavior that define the firm’s culture. Three Levels of Unethical Behavior Cost

Thomas et al. (2004) have created a model that shows three levels of costs associated with unethical behavior in businesses. Level 1 cost represents the least costs of all. These are represented by government fines and penalties that are levied when an organization first finds itself afoul of the regulators. Thomas et al. (2004) draw reference to Enron and Andersen whose ethical breaches have been well documented. Charges were levied that Anderson failed to treat Enron’s wrongdoings with the levels of objectivity and professionalism required because it was caught up in a conflict of interest. On the one hand Anderson enjoyed a privileged consulting relationship with Enron even while on the other hand it was engaged in an arm’s length relationship through its auditing function. The fine of $500,000 imposed on Anderson at its subsequent sentencing for obstruction was inconsequential to a firm that large, as at that time Anderson was worth four billion dollars. All of its stakeholders were aware of these fines which

by being imposed publicly were made obvious to them. Not so with Level 2 costs however (see Figure 1).

Figure 1 – Three Levels of Unethical Behavior Costs (Thomas et al, 2004)

Philanthropy and Shareholder Value The debate continues among academics as to whether there is any relationship between ethical leadership and improved shareholder value. The linkage between responsibility (CSR) and corporate financial performance (CFP) has been reviewed and tested for over seven decades (Griffin & Mahon, 1997; Margolis & Walsh, 2001). And whereas some have used the term corporate social responsibility (CSR) relationship with corporate financial performance (CFP), the term corporate social performance (CSP) has been used synonymously for what is essentially the same construct. In that regard although CSR will be used predominantly in this paper both terms are synonymously contextual.. Based on the absence of conclusive research in the field Godfrey (2005) was driven to reprise the simple but profound comment by Ullman (1985) that the relationship between CSR and CFP was “data in search of a theory” (p. 540). It is nonetheless entirely appropriate to define both CSR and CSP in addition to some antecedent concepts to ensure that there is congruence between both definitions. Shareholder wealth is defined by Godfrey as the value that accrues from a firm’s anticipated cash flow stream. Consistent with the Capital Asset Pricing Model (CAPM) the anticipated cash flow streams themselves accrue from the employment of the firm’s tangible and intangible assets (Godfrey goes on to posit an operational definition of philanthropy drawing from the Financial Accounting Standards Board (FASB) as “an unconditional transfer of cash or other assets to an entity or a settlement or cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner” (FASB, 1993: 2). Godfrey (2005) argues correctly in that the acid test of philanthropic activity is the nonreciprocity condition and that signsimply because not all acts of corporate giving is philanthropy. For example a corporation may

Journal of Business Studies Quarterly

2010,

100

by being imposed publicly were made obvious to them. Not so with Level 2 costs however (see

ee Levels of Unethical Behavior Costs (Thomas et al, 2004)

Philanthropy and Shareholder Value

The debate continues among academics as to whether there is any relationship between ethical leadership and improved shareholder value. The linkage between corporate social responsibility (CSR) and corporate financial performance (CFP) has been reviewed and tested for over seven decades (Griffin & Mahon, 1997; Margolis & Walsh, 2001). And whereas some have used the term corporate social responsibility (CSR) as one of the variables in measuring the relationship with corporate financial performance (CFP), the term corporate social performance (CSP) has been used synonymously for what is essentially the same construct. In that regard

edominantly in this paper both terms are synonymously contextual.Based on the absence of conclusive research in the field Godfrey (2005) was driven to

reprise the simple but profound comment by Ullman (1985) that the relationship between CSR s “data in search of a theory” (p. 540). It is nonetheless entirely appropriate to define

both CSR and CSP in addition to some antecedent concepts to ensure that there is congruence between both definitions. Shareholder wealth is defined by Godfrey as the expected discounted value that accrues from a firm’s anticipated cash flow stream. Consistent with the Capital Asset Pricing Model (CAPM) the anticipated cash flow streams themselves accrue from the employment of the firm’s tangible and intangible assets (Brealey, Myers, & Marcus, 1995). Godfrey goes on to posit an operational definition of philanthropy drawing from the Financial Accounting Standards Board (FASB) as “an unconditional transfer of cash or other assets to an

tion of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner” (FASB, 1993: 2).

Godfrey (2005) argues correctly in that the acid test of philanthropic activity is the nonreciprocity condition and that significant discretion on the part of the firm is implied in the act simply because not all acts of corporate giving is philanthropy. For example a corporation may

Business Studies Quarterly

, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010

by being imposed publicly were made obvious to them. Not so with Level 2 costs however (see

ee Levels of Unethical Behavior Costs (Thomas et al, 2004)

The debate continues among academics as to whether there is any relationship between corporate social

responsibility (CSR) and corporate financial performance (CFP) has been reviewed and tested for over seven decades (Griffin & Mahon, 1997; Margolis & Walsh, 2001). And whereas some

as one of the variables in measuring the relationship with corporate financial performance (CFP), the term corporate social performance (CSP) has been used synonymously for what is essentially the same construct. In that regard

edominantly in this paper both terms are synonymously contextual. Based on the absence of conclusive research in the field Godfrey (2005) was driven to

reprise the simple but profound comment by Ullman (1985) that the relationship between CSR s “data in search of a theory” (p. 540). It is nonetheless entirely appropriate to define

both CSR and CSP in addition to some antecedent concepts to ensure that there is congruence expected discounted

value that accrues from a firm’s anticipated cash flow stream. Consistent with the Capital Asset Pricing Model (CAPM) the anticipated cash flow streams themselves accrue from the

Brealey, Myers, & Marcus, 1995). Godfrey goes on to posit an operational definition of philanthropy drawing from the Financial Accounting Standards Board (FASB) as “an unconditional transfer of cash or other assets to an

tion of its liabilities in a voluntary nonreciprocal transfer by

Godfrey (2005) argues correctly in that the acid test of philanthropic activity is the non-ificant discretion on the part of the firm is implied in the act

simply because not all acts of corporate giving is philanthropy. For example a corporation may

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 101

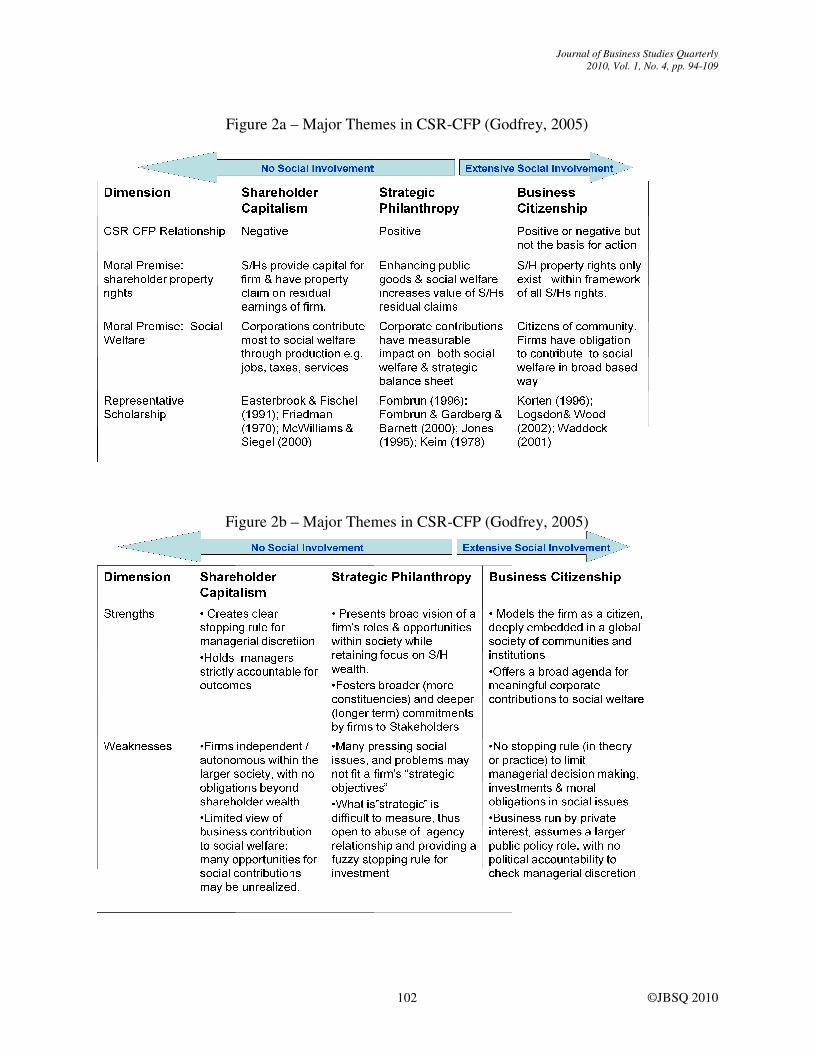

donate funds to build a new private school auditorium or on the other hand fund the construction of a large indoor sports arena that gives it exclusivity in naming rights. Although both acts constitute donations only the first would qualify as a philanthropic cause since no exchange took place. The second act would not qualify as the value given is returned in the exclusivity granted to the corporation which transfers material value. Godfrey further argues that whereas philanthropic activity or CSR sits at one end of the continuum, shareholder wealth or CFP sits at the other end. When compared against the definition by Godfrey (2005), a matching definition of corporate social performance (CSP) by Schuler and Cording (2006) seems less ethically imposing. Drawing on Griffin and Mahon (1997) and McGuire, Sundgren, and Schneeweis (1988), Schuler and Cording (2006) define CSP as a voluntary business action which results in social effects that ultimately accrue to the firm’s profitability, growth or market value. Godfrey (2005) sought to establish some core assertions one of which was that CSR could establish positive moral capital among stakeholders which capital establishes a type of insurance protection for some of the firm’s intangible assets all ultimately accruing into shareholder wealth. Godfrey assumes that all management decisions including philanthropic ones are ultimately geared at maximizing shareholder wealth. It is the stakeholders who then assess and evaluate the firm’s philanthropic activities and assign net reputational capital. Godfrey (2005) identifies in his literature review three major themes in the CSR-CFP literature. At one pole of the debate lies the proponents of strict capitalism who argue that businesses should have no role in social issues (Friedman, 1970; McWilliams & Siegel, 2000). At the other end of the pole are the proponents of business citizenship who posit the view that organizations not only have a moral responsibility but a moral duty to assist its communities and stakeholders irrespective of whether or not there are economic returns (Logsdon & Wood, 2002). The third theme, a compromise but the one accepted by Godfrey is that developed by Post and Waddock (1995) termed strategic philanthropy which holds that although a firm does not receive tangible exchange value for its acts of philanthropy major intangible strategic assets are received in return and these are best defined as reputational capital (Fombrun, Gardberg, & Barnett, 2000) (see Figure 2a and 2b).

The major intangible strategic assets incorporate employees’ trust and commitment. Godfrey (2005) argues further that the concept of strategic philanthropy has undergone significant empirical research in its theoretical development and cites the work of Fry, Keim, and Meiners (1982) in that regard. The fact that significant empirical work has been taking place in the field was also highlighted by Schuler and Cording (2006) who have cited numerous studies in their own work in the field. In spite of all of the work done in the field however there appears to be no widespread acceptance of the link between CSR-CFP. And even if unanimity were to be achieved here, what would be the optimum level of strategic donation?

Godfrey (2005) argues that strategic philanthropic activity does provide a firm with positive moral capital or reputational capital that builds intangible assets that over time builds shareholder wealth. He argues like Fombrun (1996) that reputational capital is the result of the firm’s stakeholders’ evaluation of its strategic philanthropy and that this philanthropy does have significant currency among the organization’s stakeholders irrespective of the fact that there is no tangible cash value being generated in the process. It is important to stakeholders because it finds traction with the individual value systems of stakeholders as a result of which deeper commitments and value exchanges become entrenched.

Figure 2a – Major Themes in CSR

Figure 2b – Major Themes in CSR

Journal of Business Studies Quarterly

2010,

102

Major Themes in CSR-CFP (Godfrey, 2005)

Major Themes in CSR-CFP (Godfrey, 2005)

Business Studies Quarterly

, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010

This position is contrary to that of strict capitalism which outlines a clear stopping rule to limit managerial discretion in donations to the public on the one hand (Friedman, 1970; McWilliams & Siegel, 2000) and the obligatory extargues for a duty based policy of giving since the firm is seen as a citizen of the larger community on which it imposes its own self serving ethic of profitability (Logsdon & Wood, 2002). Godfrey (2005) argues that the notion that stakeholders will impute reputational capital to strategic philanthropy is not new and in fact dates back to some of the seminal management thinkers themselves including Bernard (1938) and Selznick (1957). Godfrey posits further tha“potential economic value becomes actual when two conditions occur: (1) when stakeholders act on their dispositions, and (2) when the economic value created exceeds the cost of creating these dispositions” (p. 783). At the heart of the stakeholder’s posthe community value system with that of the firm which ultimately leads to the community’s positive moral evaluations. This imputes and results in an even deeper value construct. Philanthropy must remain discretionary or motives will be imputed by the stakeholders to be driven by some need for economic gain or the achievement of some requisite requirements to satisfy legal and maybe even moral obligations. Motives must be discretionary or the community will impute ingratiation which will accrue negative reputational capital. And these motives in turn must rest on the ethics and value systems of the managers and employees in the organization as an organization has no mind of its own. Godfrey (2005) presents a model that evaluates both the act and actor in the creation of moral capital. Where both the act (donation or positive community action for example) and actor (the firm) are perceived as positive and genuine respectively, positive moral capital wilIf the act is perceived as positive and the actor perceived as ingratiating actormoral capital will accrue. If the actor is perceived as genuine but the act perceived negatively act-based negative moral capital will result. The woand actor are perceived as negative and ingratiating respectively as this will result in both act and actor- based negative moral capital accruing (see Figure 3).

Figure 3 – Acts, Actors & Moral Capital (Godf

Journal of Business Studies Quarterly

2010,

103

This position is contrary to that of strict capitalism which outlines a clear stopping rule to limit managerial discretion in donations to the public on the one hand (Friedman, 1970; McWilliams & Siegel, 2000) and the obligatory extremity of the business citizenship model that argues for a duty based policy of giving since the firm is seen as a citizen of the larger community on which it imposes its own self serving ethic of profitability (Logsdon & Wood,

es that the notion that stakeholders will impute reputational capital to strategic philanthropy is not new and in fact dates back to some of the seminal management thinkers themselves including Bernard (1938) and Selznick (1957). Godfrey posits further tha“potential economic value becomes actual when two conditions occur: (1) when stakeholders act on their dispositions, and (2) when the economic value created exceeds the cost of creating these

At the heart of the stakeholder’s positive disposition towards a firm is the congruence of the community value system with that of the firm which ultimately leads to the community’s positive moral evaluations. This imputes and results in an even deeper value construct.

in discretionary or motives will be imputed by the stakeholders to be driven by some need for economic gain or the achievement of some requisite requirements to satisfy legal and maybe even moral obligations. Motives must be discretionary or the community will impute ingratiation which will accrue negative reputational capital. And these motives in turn must rest on the ethics and value systems of the managers and employees in the organization as an organization has no mind of its own.

sents a model that evaluates both the act and actor in the creation of moral capital. Where both the act (donation or positive community action for example) and actor (the firm) are perceived as positive and genuine respectively, positive moral capital wilIf the act is perceived as positive and the actor perceived as ingratiating actor-based negative moral capital will accrue. If the actor is perceived as genuine but the act perceived negatively

based negative moral capital will result. The worst condition of all occurs where both the act and actor are perceived as negative and ingratiating respectively as this will result in both act and

based negative moral capital accruing (see Figure 3).

Acts, Actors & Moral Capital (Godfrey, 2005)

Business Studies Quarterly

, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010

This position is contrary to that of strict capitalism which outlines a clear stopping rule to limit managerial discretion in donations to the public on the one hand (Friedman, 1970;

remity of the business citizenship model that argues for a duty based policy of giving since the firm is seen as a citizen of the larger community on which it imposes its own self serving ethic of profitability (Logsdon & Wood,

es that the notion that stakeholders will impute reputational capital to strategic philanthropy is not new and in fact dates back to some of the seminal management thinkers themselves including Bernard (1938) and Selznick (1957). Godfrey posits further that “potential economic value becomes actual when two conditions occur: (1) when stakeholders act on their dispositions, and (2) when the economic value created exceeds the cost of creating these

itive disposition towards a firm is the congruence of the community value system with that of the firm which ultimately leads to the community’s positive moral evaluations. This imputes and results in an even deeper value construct.

in discretionary or motives will be imputed by the stakeholders to be driven by some need for economic gain or the achievement of some requisite requirements to satisfy legal and maybe even moral obligations. Motives must be discretionary or the community will impute ingratiation which will accrue negative reputational capital. And these motives in turn must rest on the ethics and value systems of the managers and employees in the organization

sents a model that evaluates both the act and actor in the creation of moral capital. Where both the act (donation or positive community action for example) and actor (the firm) are perceived as positive and genuine respectively, positive moral capital will accrue.

based negative moral capital will accrue. If the actor is perceived as genuine but the act perceived negatively

rst condition of all occurs where both the act and actor are perceived as negative and ingratiating respectively as this will result in both act and

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 104

Godfrey draws reference to AT&T which in 1990 succumbed to pro-life protesters and withdrew its support to Planned Parenthood. AT&T lost support not only among pro-choice groups but even some members of pro-life groups who questioned AT&T’s sincerity and values set in its strategic philanthropy. That was a classic case of both act and actor based negative moral capital accrued and all based on an inconsistency in the value system and apparent motives of its executives. To support his theory that there was a significant positive correlation between CSR and CFP, Godfrey (2005) points to the resource based view of the firm formulated by Barney (1991) and Ghemawat (1991) which asserts that the competitive advantage built up by a firm derives from intangible assets that competitors will find very difficult to imitate and in fact become relational wealth. He further divides relational wealth into employees’ affective commitment (Meyer & Allen, 1997), legitimacy among communities and regulators (Suchman, 1995), trust among suppliers and partners (Mayer, Davis & Schoorman, 1995) and brand definition among customer stakeholders. It is the sum of these values across numerous stakeholders that create relational wealth. Conclusion

Drawing on the doctrine of “mens rea” Godfrey (2005) speaks to the profundity of the firm’s executives value system. He draws reference to LaFave (2000, p. 225) whose translated definition of “mens rea” that “an act does not make one guilty unless his mind is guilty” lends significant support to the essential premise of this paper that increasing shareholder wealth is positively correlated to CSR and that a firm’s investment in CSR is a function of the collective ethics and value set of the firm’s leaders and followers. So then we would seek to conclude this brief analysis by enquiring if there is an optimal level of philanthropic activity. Godfrey (2005) argues that managers should target philanthropic activity as a strategy that does maximize shareholder wealth. Top management needs to rationalize relational wealth, risk and accrued moral capital to build corporate financial performance which will maximize shareholder wealth. Risk we introduce as a new variable into our discussion for the first time in this paper even as we are concluding our discourse because it is the crucial mathematical unknown and only circumscribed by what the proponents of strict capitalism define as that clear stopping rule for managerial discretion in strategic philanthropy. Stated otherwise, managers have a duty to ensure that the firm’s strategic philanthropy is consistent with a value system that is core, lasting and integral to the firm’s self-definition (Albert & Whetten, 1985), but more importantly will result in increased shareholder value. What is the optimum level of strategic philanthropy that will ensure that shareholder value is maximized? That is the risk factor, β within the CAPM scenario that will form the basis for further intervention from the finance discipline. In the absence of an optimal level of strategic philanthropy however, the empirical data outlined above justifies our proposition that the creation of ethical behavior and a strong moral value set in business must be approached with the same discipline as that of profit creation, return on investment or creation of shareholder value. And it all rests in the ethical state and value set of the organization’s leaders and followers.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 105

References

Albert, S., & Whetten, D.A. (1985). Organizational identity. Research in Organizational

Behavior, 7, 263-295. Barnard, C.I. (1938). Functions of the executive. Boston: Harvard Press. Barney, J.B. (1991). Firm resources and sustained competitive advantage. Journal of

Management, 17, 99-120. Bass, B.M. (1985). Leadership and performance beyond expectations. New York: Free Press. Brealey, R.A., myers, S.C. & Marcus, A.J. (1997). Fundamentals of corporate finance. New

York: McGraw-Hill Brown, M.E., & Treviño, L.K.(2003). Is Values Based Leadership Ethical Leadership? In S.W.

Gilliland, D.D. Steiner, & D.P. Starlicki (Eds.), Emerging perspectives on values in

organizations (pp.3-32). Connecticut: Information Age Publishing. Burns, J.M. (1978). Leadership. New York: Harper & Row. Cavico, F. J. & Mujtaba, B. G. (2009). Business Ethics: The Moral Foundation of Leadership,

Management, and Entrepreneurship (2nd

edition). Pearson Custom Publications. Boston, United States.

Chappel, T., (1999). Managing upside down: The seven intentions of values-centered leadership.

New York: W. Morrow. Collins, J.C., & Porras, J.I. (1994). Built to Last: Successful habits of visionary companies. New

York: Harper Business. England, G.W. (1967). Personal value systems of American managers. Academy of Management

Journal, 10, 53-68. Fombrun, C. (1996). Reputation. Boston, Harvard Business School Press. Fombrun, C., Gardberg, N.A., & Barnett, M.L. (2000). Opportunity platforms and safety nets:

Corporate citizenship and reputational risk. Business and Society Review, 105, 85-106. Friedman, M. (1970). The social responsibility of business is to increase its profits. New York

Times Magazine, September 13, 122-126. Fry, L.W., Keim, G.D., & Meiners, R.E. (1982). Corporate contributions: Altruistic or for-profit?

Academy of Management Journal, 25, 94-106. Ghemawat, P. (1991). Commitment. New York: Free Press

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 106

Godfrey, P.C. (2005). The relationship between corporate philanthropy and shareholder wealth:

A risk management perspective, Academy of Management Review, 30, 777-798. Griffin, J.J., & Mahon, J.F. (1997). The corporate social performances and corporate financial

performance debate: Twenty-five years of incomparable research. Business & Society, 36, 5-31.

Harrison, J.R., & Carroll, G.R. (1991). Keeping the faith: A model of cultural transmission in

formal organizations. Administrative Science Quarterly, 36, 552-582. Hofstede, G. (1998). Attitudes, values and organizational culture: Disentangling the concepts.

Organizational Studies, 19, 477-492. House, R.J.(1996). Path-goal theory of leadership: Lessons, legacy and a reformulated theory.

Leadership Quarterly, 7, 323-353. Kelman, H.C. (1958). Compliance, identification, and internalization: Three processes of attitude

change. Journal of Conflict Resolution, 2, 51-60. Kohlberg,L. (1969). Stage and sequence: The cognitive development approach to socialization.

In D.A. Goslin (Ed.), Handbook of socialization theory and research. Chicago: Rand McNally.

Kluckhohn, C. (1951). Values and value-orientations in the theory of action. In T. Parsons & E.

Shils (Eds.), Toward a general theory of action (pp. 388-433). Cambridge, MA: Harvard University Press.

LaFave, W.R. (2000). Criminal law (3 rd ed.). St. Paul: West Group. Logsdon, J.M., & Wood, D.J. (2002). Business citizenship: From domestic to global level of

analysis. Business Ethics Quarterly, 12, 155-187. Maierhofer, N.I., Rafferty, A.E., & Kabanoff, B. (2003). When and Why are values important in

organizations? In S.W. Gilliland, D.D. Steiner, & D.P. Starlicki (Eds.), Emerging

perspectives on values in organizations (pp.3-32). Connecticut: Information Age Publishing.

Margolis, J.D., & Walsh, J.P. (2001). People and profits: The search for a link between a

company’s social and financial performance. Mahwah, NJ: Lawrence Erlbaum Associates.

Mayer, R.C., Davis, J.H., & Schoorman, F.D. (1995). An integrative model of organizational

trust. Academy of Management Review, 20, 709-734.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 107

McGuire, J.B., Sundgren, A., & Schneeweis, T. (1988). Corporate social responsibility and firm financial performance. Academy of Management Journal, 31, 854-872.

McWilliams, A., & Siegel, D. (2000). Corporate social responsibility: A theory of the firm

perspective. Academy of Management Review, 26, 117-127. Messick, D., & Bazerman, M. (1996). Ethical leadership and the psychology of decision making.

Sloan Management Review, 37, 9-22. Meyer, J.P., & Allen, N.J. (1997). Commitment in the workplace: Theory, research and

application. Thousand Oaks, CA: Sage. Mujtaba, B. G. (2006). Ethics and morality in business: the hard choice is usually the right

choice. SmartBusiness: The Management Journal for Corporate Growth. SmartBusiness Tampa Bay. Available on: http://broward.sbnonline.com/National/Article.aspx?CID=10417

Mujtaba, B. (1997a). Corporate Ethics Training Programs. Journal of Developments in Business

Simulation and Experiential Learning, Vol. 24, Pages 130-131. Available on: http://sbaweb.wayne.edu/~absel/bkl/vol24/24bh.pdf

Mujtaba, B. G. (1997b). Business Ethics Survey of Supermarket Managers and Employees. UMI

Dissertation Service. A Bell & Howell Company. UMI Number: 9717687. Nash, L. (1990). Good Intentions Aside: A Manager’s Guide to Resolving Ethical Problems, 5.

Boston: Harvard Business School Press. O’Boyle, T. (1998). At any cost: jack Welch, general electric and the pursuit of profit. New

York: Alfred A. Knopf. Paine, L.S. (1994). Managing for organizational integrity. Harvard Business Review, 72, 106-

117. Pellet, J. (2002). Trust in an age of doubt. Chief Executive, 180, 60-67. Post, J. E., & Waddock, S. A. (1995). Strategic philanthropy an partnerships for economic

progress. In R.F. America (Ed.), Philanthropy and economic development: 65-84. Westport, CT: Greenwood Press.

Ravlin, E.C., & Meglino, B.M. (1989). Transitivity of work values: Hierarchical performance

ordering of socially desirable stimuli. Organizational Behavior and Human Decision

Processes, 44, 508. Rokeach, M. (1973). The nature of human values. New York: Free Press.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 108

Rosseau, D.M. (1990). Quantitative assessment of organizational culture: The case for multiple measures. In B. Schneider (Ed.), Frontiers in industrial and organizational psychology (Vol. 3, pp. 153-192). San Francisco: Jossey-Bass.

Schwartz, S.H. (1992). Universals in the content and structure of values: Theoretical advances

and empirical tests in 20 countries. In M.P. Zanna (Ed.), Advances in experimental social

psychology: An International Review, (pp. 1-65). San Diego, CA: Academic. Schwartz, S.H. (1996). Value priorities and behavior: Applying a theory of integrated value

systems. In C. Seligman, J.M. Olson, & M.P. Zanna (Eds.), The psychology of values (pp. 1-24). Mahwah, NJ: Lawrence Erlbaum Associates, Inc.

Schuler, D.A., & Cording, M. (2006). A corporate social performance-corporate financial

performance behavioral model for consumers. Academy of Management Review, 31, 540-548.

Selznik, P. (1957). Leadership in administration: A sociological interpretation. New York:

Harper & Row. Suchman, M.C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of

Management Review, 20, 571-610. Thomas, T., Schermerhorn, Jr., J.R., Dienhart, J.W. (2004). Strategic leadership of ethical

Behavior in business. Academy of Management Executive, 18, 56-66. Treviño, L.K., Hartman, L.P. & Brown, M. (2000). Moran person and moral manager: How

executives develop a reputation for ethical leadership. California Management Review, 42, 128-142.

Treviño, L.K., Brown, M., & Hartman, L.P. (2003). A qualitative investigation of perceived

executive ethical leadership: Perceptions from inside and outside the executive suite. Human Relations, 56, 5-37.

Ullman, A.A. (1985). Data in search of a theory: A critical examination of the relationships

among social performance, social disclosure, and economic performance of U.S. firms. Academy of Management Review, 10, 540-557.

Weiss, J. (2003). Business Ethics: A Stakeholder and Issues Management Approach (3rd

ed.).Thomson. South-Western.

Journal of Business Studies Quarterly

2010, Vol. 1, No. 4, pp. 94-109

©JBSQ 2010 109

Author Biography:

Hopeton Morrison is currently a doctoral candidate at the Nova Southeastern

University’s H. Wayne Huizenga School of Business and Entrepreneurship in Fort Lauderdale, Florida. Morrison has been CEO of a credit union in Jamaica for the past 16 years. He has also been an adjunct lecturer in business ethics and strategy at the University of Technology, Jamaica for over 20 years in addition to being a trainer and consultant in entrepreneurship and micro finance, personal finance and ethics in business to multilateral institutions and corporations in Jamaica. Morrison can be reached through email at: [email protected].

Bahaudin G. Mujtaba is an Associate Professor of Management, Human Resources Management, and International Management at Nova Southeastern University’s H. Wayne Huizenga School of Business and Entrepreneurship in Fort Lauderdale, Florida. Bahaudin has worked as an internal consultant, trainer, and management development specialist as well as retail management in the corporate arena for over 16 years. Bahaudin is the author and co-authors of several books in the areas of management, business ethics, leadership, and international management. Bahaudin can be reached through email at: [email protected].