Embed Size (px)

Citation preview

Strategic Treasury Management

WelcomeCharles MayoPartnerSimmons & Simmons

The Association of Corporate Treasurers

An introduction

John Grout, Policy and Technical Director, The Association of Corporate Treasurers November 2011

Origins of the ACT

• We came together in 1979 as a group of individuals – FDsand treasurers of FTSE 100 companies mostly

– used to meet regularly in the London Treasurers Club (a dining club) but we wanted to go further

• Formed a membership association as a not-for-profit company

• “To encourage and promote the study and practice of corporate treasury management and related subjects and

the education and training of those engaged therein”

• ... A new financial professional body

ACT mission

ACT professional network – the route to treasury excellence

The Association of Corporate Treasurers (ACT) qualifies, supports and represents professionals working in treasury, risk and corporate finance

28/09/2011 4

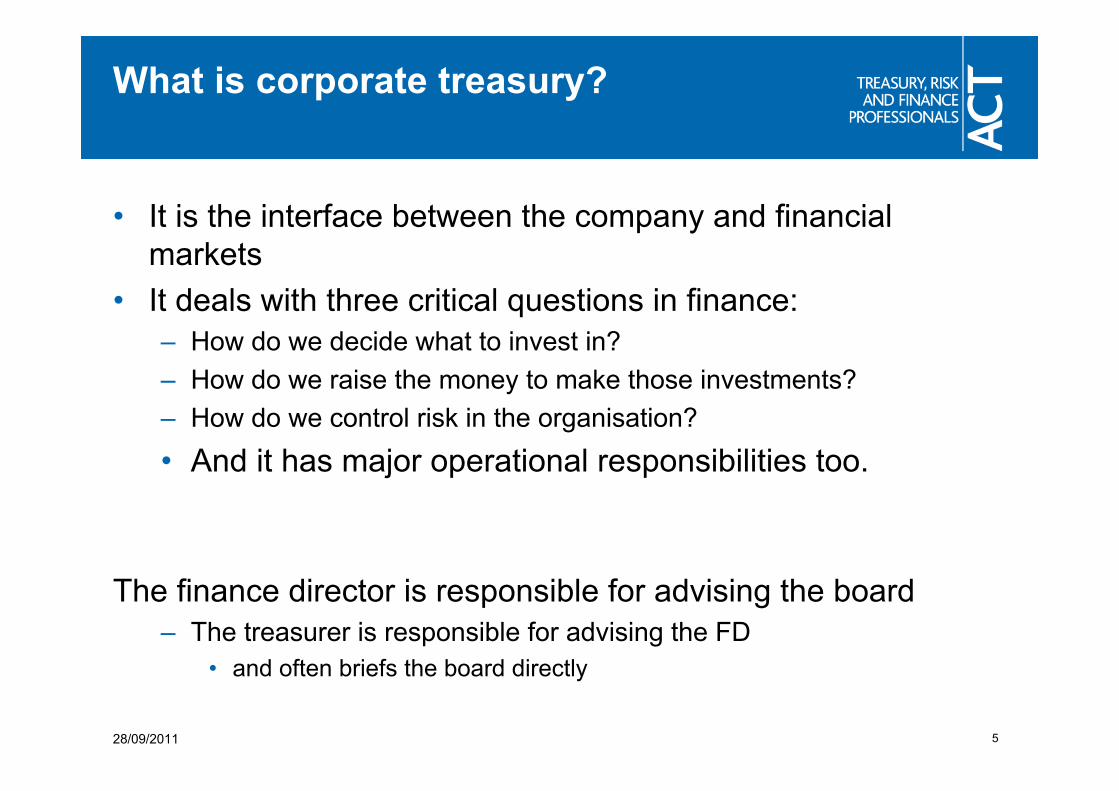

What is corporate treasury?

• It is the interface between the company and financial markets

• It deals with three critical questions in finance:– How do we decide what to invest in?

– How do we raise the money to make those investments?

– How do we control risk in the organisation?

• And it has major operational responsibilities too.

The finance director is responsible for advising the board– The treasurer is responsible for advising the FD

• and often briefs the board directly

528/09/2011

• There is never a “right” answer

– though some answers may be better than others.

– Just an endless series of judgements (as the business and the environment and the management change)

– Different companies make different judgements6

Treasury: 3 critical questionsThe treasurer’s job is among the most interesting in a company

Some key data

• Established suite of qualifications

• Membership –

• Individual by examination or

• Corporate (enables nominated individuals to to take part without becoming members)

• Activities

− Global standard in treasury education and qualification

− Events, training and publishing.

− Policy and technical

7

ACT – today

28/09/2011

ACT in 2011

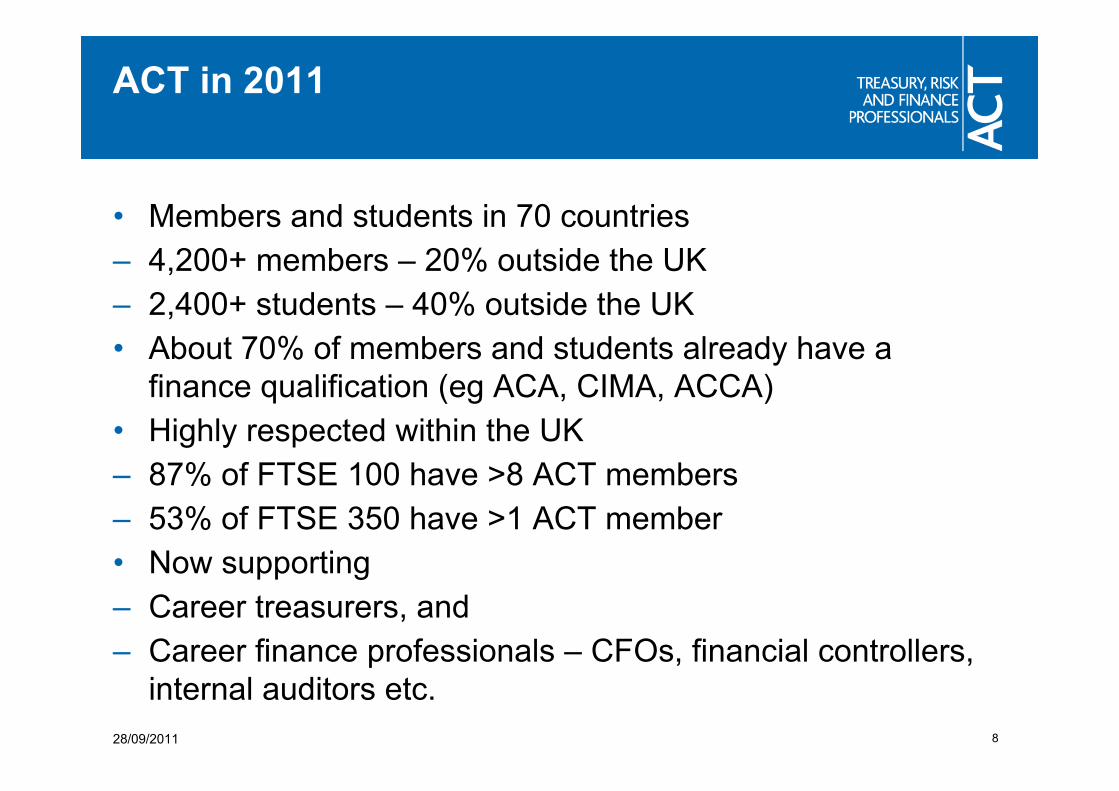

• Members and students in 70 countries

– 4,200+ members – 20% outside the UK

– 2,400+ students – 40% outside the UK

• About 70% of members and students already have a finance qualification (eg ACA, CIMA, ACCA)

• Highly respected within the UK

– 87% of FTSE 100 have >8 ACT members

– 53% of FTSE 350 have >1 ACT member

• Now supporting

– Career treasurers, and

– Career finance professionals – CFOs, financial controllers, internal auditors etc.

828/09/2011

ACT – governance

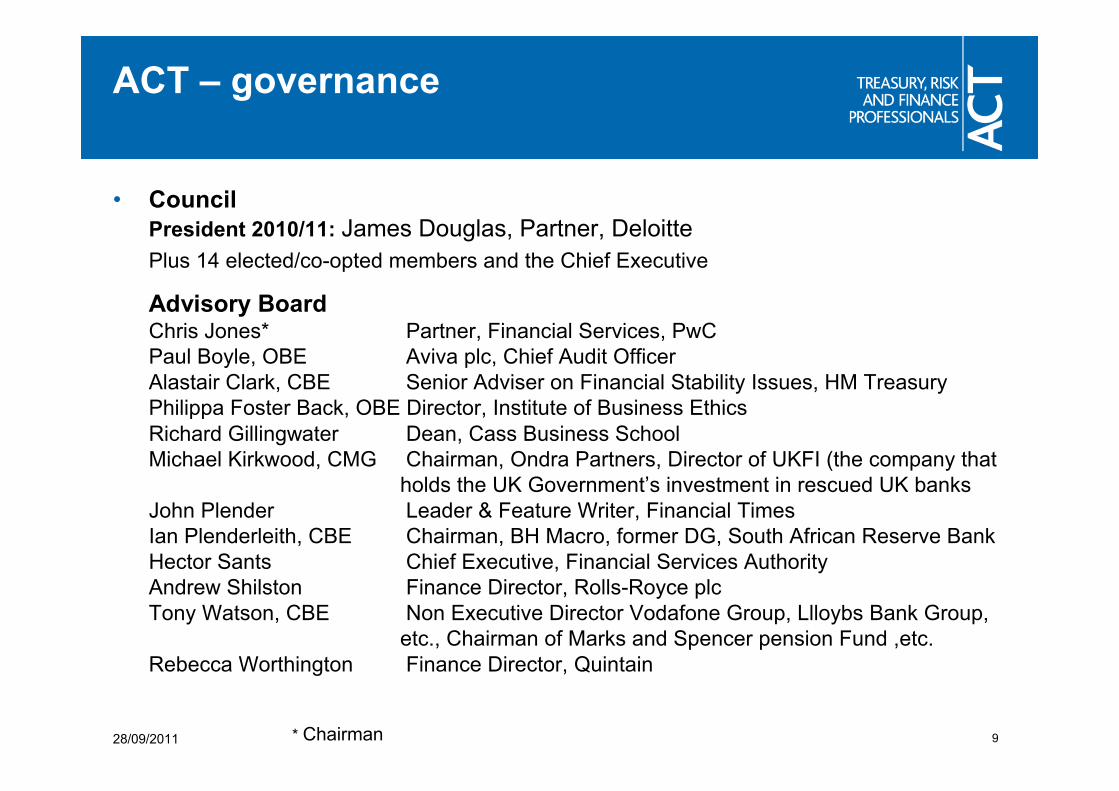

• Council President 2010/11: James Douglas, Partner, Deloitte

Plus 14 elected/co-opted members and the Chief Executive

Advisory BoardChris Jones* Partner, Financial Services, PwC Paul Boyle, OBE Aviva plc, Chief Audit OfficerAlastair Clark, CBE Senior Adviser on Financial Stability Issues, HM TreasuryPhilippa Foster Back, OBE Director, Institute of Business Ethics Richard Gillingwater Dean, Cass Business SchoolMichael Kirkwood, CMG Chairman, Ondra Partners, Director of UKFI (the company that

holds the UK Government’s investment in rescued UK banksJohn Plender Leader & Feature Writer, Financial TimesIan Plenderleith, CBE Chairman, BH Macro, former DG, South African Reserve BankHector Sants Chief Executive, Financial Services AuthorityAndrew Shilston Finance Director, Rolls-Royce plcTony Watson, CBE Non Executive Director Vodafone Group, Llloybs Bank Group,

etc., Chairman of Marks and Spencer pension Fund ,etc.Rebecca Worthington Finance Director, Quintain

9* Chairman28/09/2011

The rest of the world

1028/09/2011

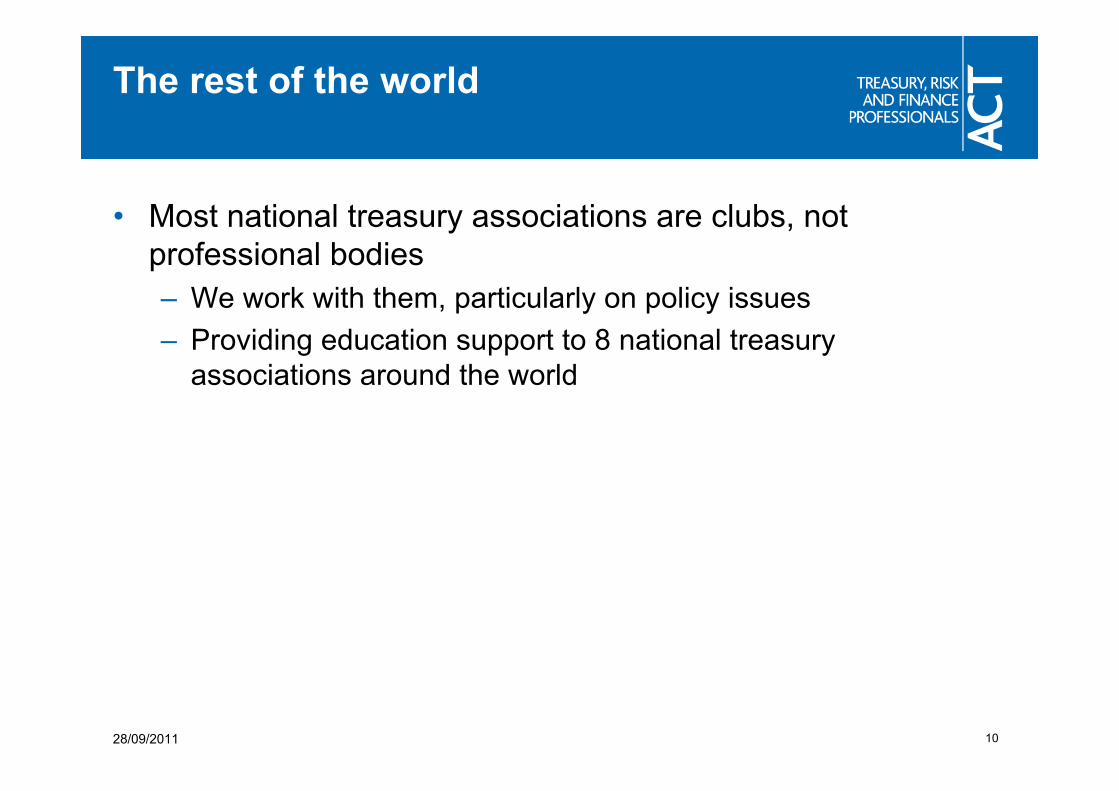

• Most national treasury associations are clubs, not professional bodies

– We work with them, particularly on policy issues

– Providing education support to 8 national treasury associations around the world

• Tuition and/or events in Germany, Hong Kong, India, Ireland, Netherlands, Russia, Singapore, South Africa, UAE and UK this year

• Active member of International and European treasury groupings (IGTA and EACT)

• Middle East network launched in 2008 www.actmiddleeast.org

ACT – international presenceHas been demand led

1128/09/2011

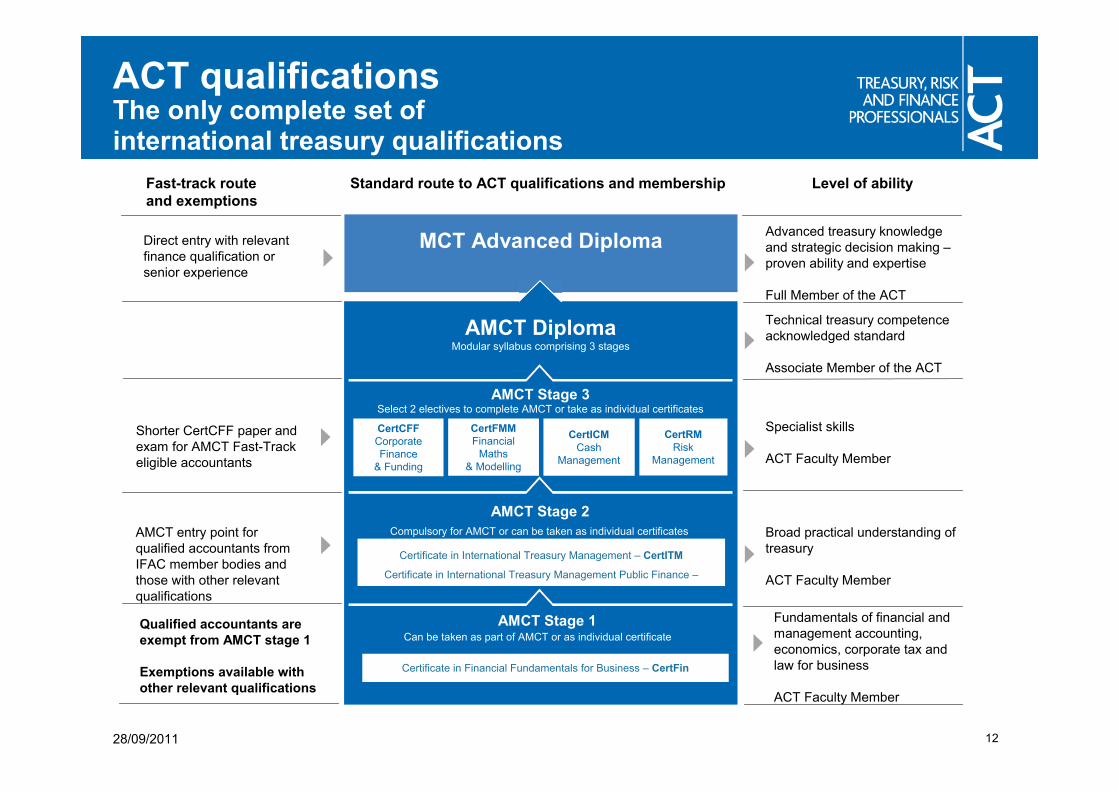

ACT qualificationsThe only complete set of international treasury qualifications

AMCT DiplomaModular syllabus comprising 3 stages

MCT Advanced Diploma

Select 2 electives to complete AMCT or take as individual certificatesAMCT Stage 3

Compulsory for AMCT or can be taken as individual certificates

AMCT Stage 2

Certificate in International Treasury Management – CertITM

Certificate in International Treasury Management Public Finance –

CertITM-PF

Advanced treasury knowledge and strategic decision making –proven ability and expertise

Full Member of the ACT

Technical treasury competenceacknowledged standard

Associate Member of the ACT

Specialist skills

ACT Faculty Member

Broad practical understanding of treasury

ACT Faculty Member

Standard route to ACT qualifications and membershipFast-track route and exemptions

Shorter CertCFF paper and exam for AMCT Fast-Track eligible accountants

AMCT entry point for qualified accountants from IFAC member bodies and those with other relevant qualifications

Direct entry with relevant finance qualification or senior experience

Level of ability

12

AMCT Stage 1

CertICMCash

Management

CertRMRisk

Management

CertCFFCorporate Finance

& Funding

CertFMMFinancial

Maths& Modelling

28/09/2011

Certificate in Financial Fundamentals for Business – CertFin

Can be taken as part of AMCT or as individual certificate

Fundamentals of financial and management accounting, economics, corporate tax and law for business

ACT Faculty Member

Qualified accountants are exempt from AMCT stage 1

Exemptions available with other relevant qualifications

ACT qualificationsMembership

AMCT DiplomaModular syllabus

comprising 3 stages

MCT Advanced Diploma

AMCT Stage 3

Advanced treasury knowledge and

strategic decision making – proven

ability and expertise.Full Memberof the ACT

Technical treasury competence;

acknowledged standard

Associate Member of the ACT

Standard route to ACT qualifications and

membership

Fast-track route and

exemptions

Direct entry with relevant

finance qualification

or senior experience

Level of ability

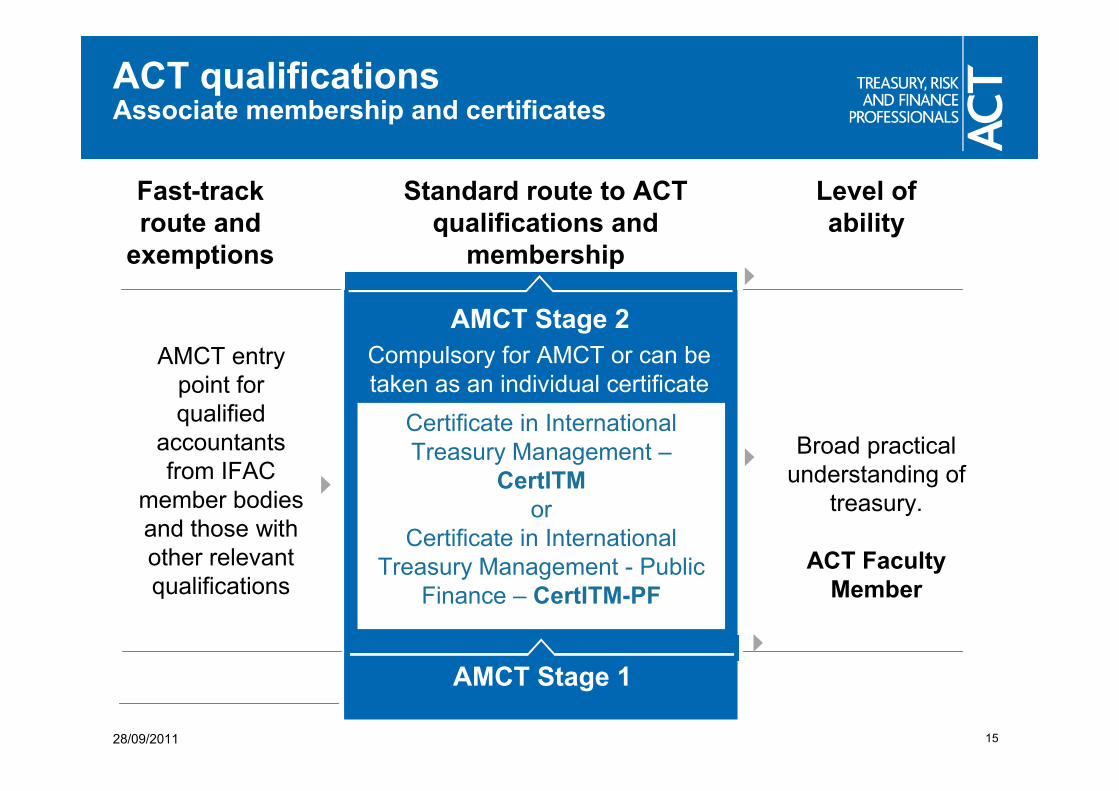

ACT qualificationsAssociate membership and certificates

Select +2 electives to complete AMCT or take as individual

certificates

AMCT Stage 3

AMCT Stage 2

Certificates:Specialist skills

ACT Faculty Member

Shorter CertCFF paper and exam for AMCT Fast-Track eligible accountants

14

CertICMInternational

CashManagement

CertRMRisk

Management

CertCFFCorporate Finance

& Funding

CertFMMFinancial

Maths& Modelling

28/09/2011

Standard route to ACT qualifications and

membership

Fast-track route and

exemptions

Level of ability

Stage 3:Technical treasury

competence;acknowledged

standardAssociate Member

of the ACT

ACT qualificationsAssociate membership and certificates

Compulsory for AMCT or can be taken as an individual certificate

AMCT Stage 2

Certificate in International Treasury Management –

CertITMor

Certificate in International Treasury Management - Public

Finance – CertITM-PF

Broad practical understanding of

treasury.

ACT Faculty Member

AMCT entry point for qualified

accountants from IFAC

member bodies and those with other relevant qualifications

1528/09/2011

Standard route to ACT qualifications and

membership

Fast-track route and

exemptions

Level of ability

AMCT Stage 1

ACT qualificationsStage 1: CertFin

16

AMCT Stage 1

28/09/2011

Certificate in Financial Fundamentals for Business

CertFin

Can be taken as part of AMCT or as individual certificate

Fundamentals of financial and management accounting,

economics, corporate tax and law for

businessACT Faculty

Member

Qualified accountants are

exempt from AMCT stage 1

Exemptions available with other relevant qualifications

Standard route to ACT qualifications and

membership

Fast-track route and

exemptions

Level of ability

Entry with no exemptions

ACT Annual ConferencePanel session

28/09/2011 17

ACT Annual ConferencePlenary

28/09/2011 18

ACT Annual ConferenceExhibition: ACT stand

28/09/2011 19

Conferences and events

• Spotlight on the Vickers report – the real world effect: Breakfast event: London

Lord Myners, Pete Hahn of the Cass Business School, Eric Anstee, former CFO of three FTSE 100 companies, and Greg Thwaites, Lead Economist on the ICB secretariat 28 Sept 2011

• ACT Corporate Funding Conference5 Oct 2011: London

• ACT Middle East Annual Conference16 Nov 2011: Dubai

28/09/2011 20

• Representing the corporate user of financial services– Lobbying

– Pre-consultation stakeholder activity

– Responses to consultations

– Presence on panels and committees, e.g. Bank of England Foreign Exchange Joint Steering Committee, FSA’s Market Abuse Practitioners Panel, etc.

– Contribution to public debate

• Issuing guidance– Topic briefing

– Through ACT events

– Through ACT publications

• Help line

2128/09/2011

The voice of corporate treasuryACT Policy and Technical

Policy and TechnicalRepresentation and Guidance

28/09/2011 22

The Association of Corporate Treasurers

ACT professional network

The route to treasury excellence

The Association of Corporate Treasurers (ACT) qualifies, supports and represents professionals working in treasury, risk and corporate finance

28/09/2011 23

The Association of Corporate Treasurers

www.treasurers.org

Strategic treasury Management:Changing capital structures

27th September 2011

John GroutPolicy & Technical Director

Theory or practice?

• We are not academics, so you would expect a strong practical bias

• Finance practitioners need to know the theoretical background

• Finance is part of management – a social science– Treasury operates at the boundary between financial theory and

human behaviour

– Usually no “right” answers, as we are dealing with complexity and incomplete knowledge. But some “answers” are better than others

• Endless judgements, changing over time, based on expectations of the future

– Be afraid of point answers

– Expect your treasurer (whatever his title) to have considered anumber of scenarios – upsides as well as stress testing.

26

Finance theory and the crisis

• Simplify and exaggerate: how we understand the world or make models

– Models may tell us something about the world over a range of circumstances

– But usually fail outside a comfort zone

• Always look at your financing and risk management arrangements in failure modes

– Will assumed correlative relationships break down?

– Will funding vanish unexpectedly?

– Etc/

• Don’t believe your model if your eyes tell you it is not working

• Prudent treasurers have always done this. Not all companies remember to do it during boom times.

• It means that you need redundancy in systems so that failure of individual parts of the system don’t stop it working overall

– So be wary of too much talk of “optimum financing” or “efficient financing”

• In the back of your pack there is a blog I wrote earlier this year that quotes Nassim Taleb of Black Swan fame, on this.

27

Corporate Strategy

28

Business strategy Financial strategy

Complex, unstable

Feedback

Corporate Strategy

29

Financial strategy

Financial Strategy

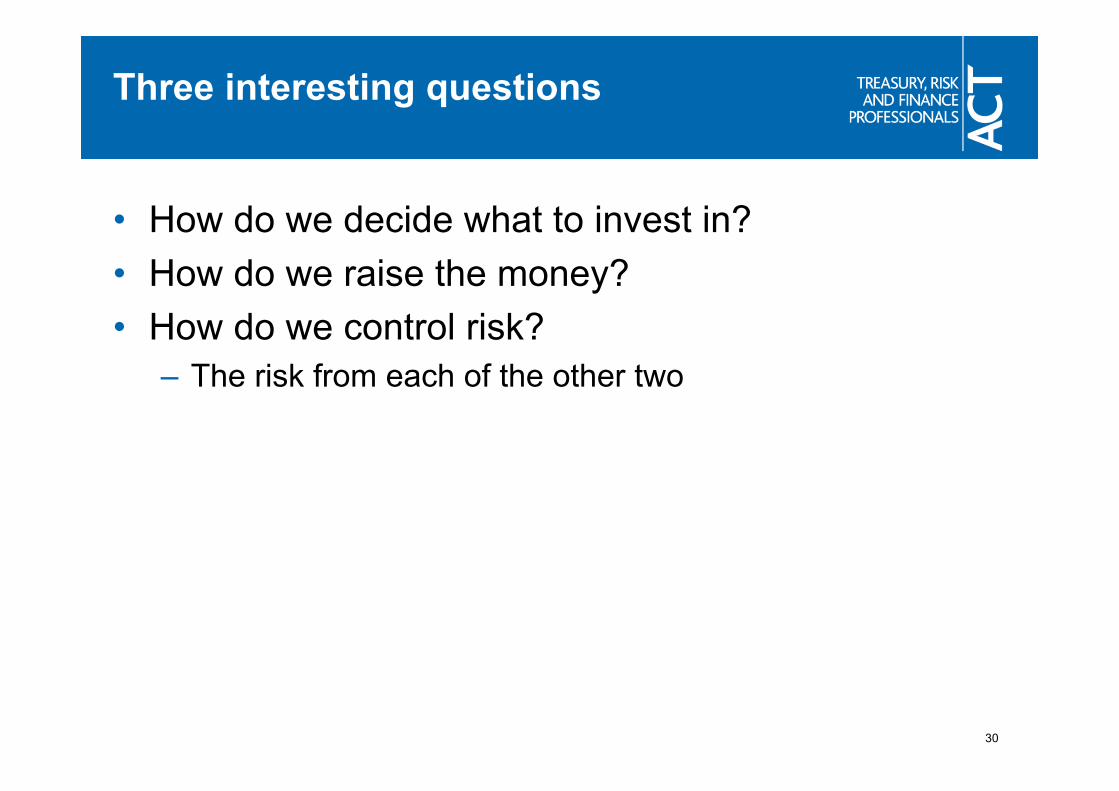

Three interesting questions:Good finance people always have them in mind

NEDs need to be comfortable with how companies handle this.

Three interesting questions

• How do we decide what to invest in?

• How do we raise the money?

• How do we control risk?

– The risk from each of the other two

30

31

Financial StrategyFeedback network

• You can’t consider any of the questions in isolation

• Every decision involves judgement

How do we decide what to invest in?

How do we raisethe money?

How do wecontrol risk?

Financial strategyIf you don’t have a treasurer someone still does this

• Level of equity and debt (Static Leverage)

• Coverage ratios (Dynamic leverage)

– These two are key financial inputs to credit ratings

• Credit rating target

– Integrating business and financial risk

– Changing the target may change investors and availability

• Investment benchmarks

– Company’s cost of capital

– Required rate of return on different activities to enable NPV tools for investment allocation

• Risk management

– What business risks accepted/managed down/laid off?

– Economic cycle; shocks

Financial strategySome detail

• Leverage targets

• Sources of debt

• Credit rating target

• Debt maturity profile

• Liquidity/standby finance (group and unit)

• Financial price risks

– Commodity/Interest rate/inflation/exchange rates

• Other financial risks

– Longevity, etc. etc.

• Organisation and control

• Reporting

• Staffing

Financial price risk

34

Risk covers business strategy and financial strategy

Simplified risk diagram

Over-simplified.Risks must be seen

together. E.g.:some businesses givehigh financial liquidity

risk; a tool for strategicfx risk is location ofoperations – that

changes operating risks; etc.

Remember that if you can’t raise money, maybeyour customers and suppliers can’t either

Volatility v Leverage

Volatility of earnings

Leverage

Low High

High

Low

NO

YES

YES

YES

Risk

Risk Asset finance

-airlines

Utilities

High IP/ high

growth

No private sector AAA

companies in Europe

Beyond = High risk:

private equity,

structured financing

2x2 matrices are over

simplifications

Real option value v. LeverageCompanies create and exploit real options

Real option value

Leverage

Low High

High

Low

NO

YES

YES

YES

Risk

Risk

Utilities

High IP/ high growth

If offered a debt investment in a high tech start-up, be cautious

Boring small to mid-sized

Equity participation: film finance

or distress

FINC 6290 S.4 John Grout Webster Graduate School, Regent’s College 37

Cos

t of

cap

ital

Gearing

After-tax cost of debt

Cost of equity

Weighted averagecost of capital

100% equity;no debt Little equity;

mostly debt

Curves areintended toshow theidea, not torepresentcosts foranyparticularcompany

“Refusal”

Weighted average cost of capitalWACC

FINC 6290 S.4 John Grout Webster Graduate School, Regent’s College 38

Curves areintended toshow theidea, not torepresentcosts foranyparticularcompany

Cos

t of

cap

ital

Gearing

After-tax cost of debt

Cost of equity

Weighted averagecost of capital

100% equity;no debt Little equity;

mostly debtGearing

After-tax cost of debt

Cost of equity

Weighted averagecost of capital

100% equity;

“Refusal” “Refusal”

Some firms which would

have been funded will now fail

Downturn/credit squeeze/issues affecting an individual firm

Structural subordinationLenders are more aware of who they are lending to

39

Parent Co

OpCo 1An Integrated

OpCo

OpCo 2Uses IP licensedfrom IPHoldCo

IPHoldCoOwns IP essential

For OpCo 2

Lenders to Parent may want guarantees from all 3 subsidiariesand undertakings to limit borrowings by subsidiaries

Lenders to OpCo 1 may want a guarantee from ParentLenders to OpCo 2 may want a guarantee from Parent and

IPHoldCo and a non-disposal covenant on IPHoldCo

Corporate Finance

• Equity investors / management board require equity type returns

– These are typically around 12-20%

• Arguable that industrials are around 10%

• Banks have indicated a target of 12-15% (down from pre-crisis 15-20%)

• Private Equity looks for around 20-25%

• If the business is low risk and therefore has low yields

– High returns can only come from monopoly effects or leverage, i.e. debt.

• If business return exceeds cost of debt, leverage produces excess return

• Tendencies

– Businesses with high risk make poor borrowers (secured or structured credit)

– Businesses with low risk make good borrowers

– Businesses with low or poor assets make poor borrowers

– Businesses with high and good assets make good borrowers

• Debt of highly levered companies can behave more like equity (ortransform to it – “loan to own”). Can be attractive to, e.g., hedge funds

41

Measuring financial leverage

• Interest cover

• Fixed charge cover

• EBITDA cover

• Income to debt

• Cash flow to debt

• Debt / EBITDA

• Debt / Equity

• Debt / Debt + Equity

• Debt / Assets

• Return on capital

= Profits / Interest charge

= Adj. profits/Interest-like costs (Int.+leasing etc..)

= EBITDA / Interest charge

= Income + Depreciation / Debt

= Cash flow / Debt

= Debt / EBITDA

= Debt / book or market capitalisation

= Debt / Debt + book or market cap.

= Debt / Asset value (individual or portfolio)

= Income / Total Assets

In financial decision making we often use market values not book values.If anywhere near financial distress: capital value of pensions deficit?

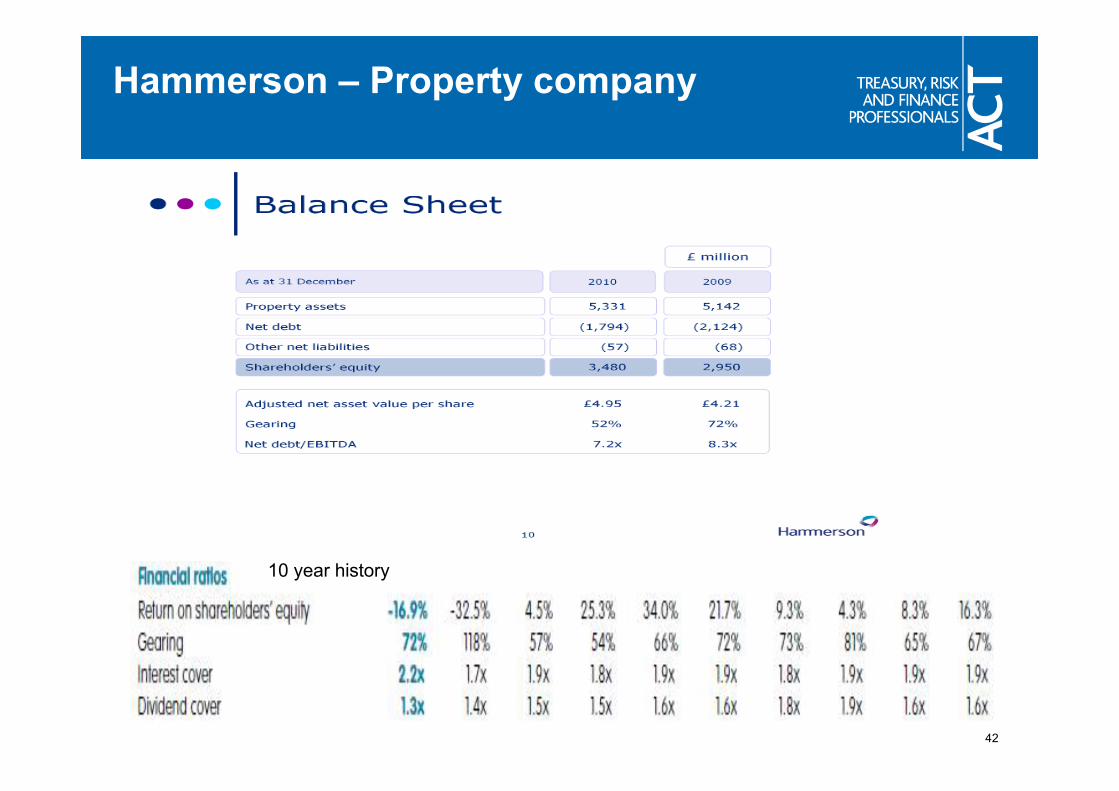

Hammerson – Property company

42

10 year history

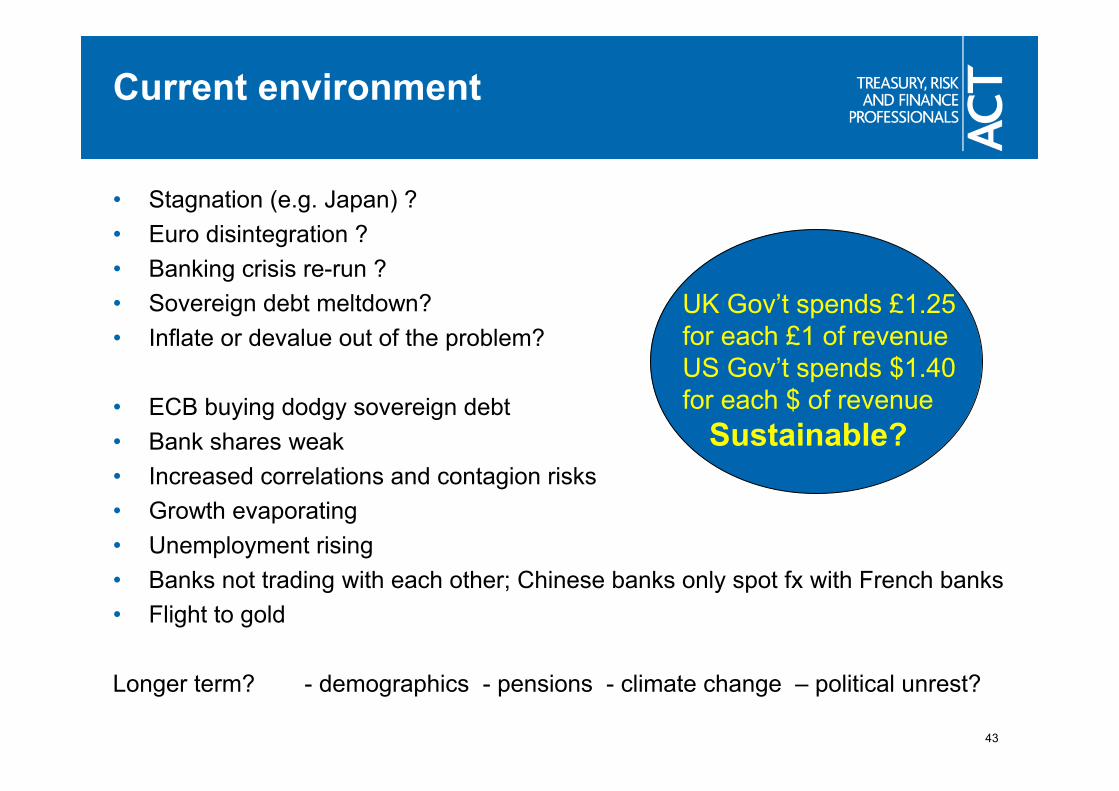

Current environment

• Stagnation (e.g. Japan) ?

• Euro disintegration ?

• Banking crisis re-run ?

• Sovereign debt meltdown?

• Inflate or devalue out of the problem?

• ECB buying dodgy sovereign debt

• Bank shares weak

• Increased correlations and contagion risks

• Growth evaporating

• Unemployment rising

• Banks not trading with each other; Chinese banks only spot fx with French banks

• Flight to gold

Longer term? - demographics - pensions - climate change – political unrest?

43

UK Gov’t spends £1.25 for each £1 of revenueUS Gov’t spends $1.40 for each $ of revenue

Sustainable?

The new paradigm

• Risk appetite of bond and equity investors reduced But some seeking risk as desperate for income

• Banks ever more risk conscious; somewhat paralysed by fear of regulation

• Cost of funding from banks up and availability down due to regulation (Basel III / CRD IV)

• More companies accessing non-bank lenders– Loans from non-banks, e.g. Hedge funds

– Selling bonds (large companies through public bonds, small through private placements) (“Retail bonds”)

• Insurance company investors seeking lower risk and shorter maturities (Solvency II )

• Companies competing with vast funding requirements by banks and Governments (especially 20013-15)

• Need to deal with Knightian uncertainty - the black swan events of Nassim Taleb – as well as computable risk.

44

Inflation and real rates

• Nominal and Real rates exceptionally low

• Inflation pressure from– Quantitative easing

– Consumption by trade surplus developing countries (eventually)

– Aging population

– Demand for commodities

eventually...

• We have had 30 years of falling real interest rates. When the panic ends, eventually, with new controls on debt availability (Basel III, CRD IV, Solvency II) and reminders of risk...

real rates are likely to riseeventually

45

OECD nominal and real rates

46

Result

• Need to build robustness into our capital structure and into the underlying business

• Robustness means operating below “optimum”capital structure and “optimum” WACC

• Need cautious capital structure and increased liquidity to hand rather than relying on access to capital or loan markets when needed

• Need to be able to cope with major financial price changes

• This all has a cost

47

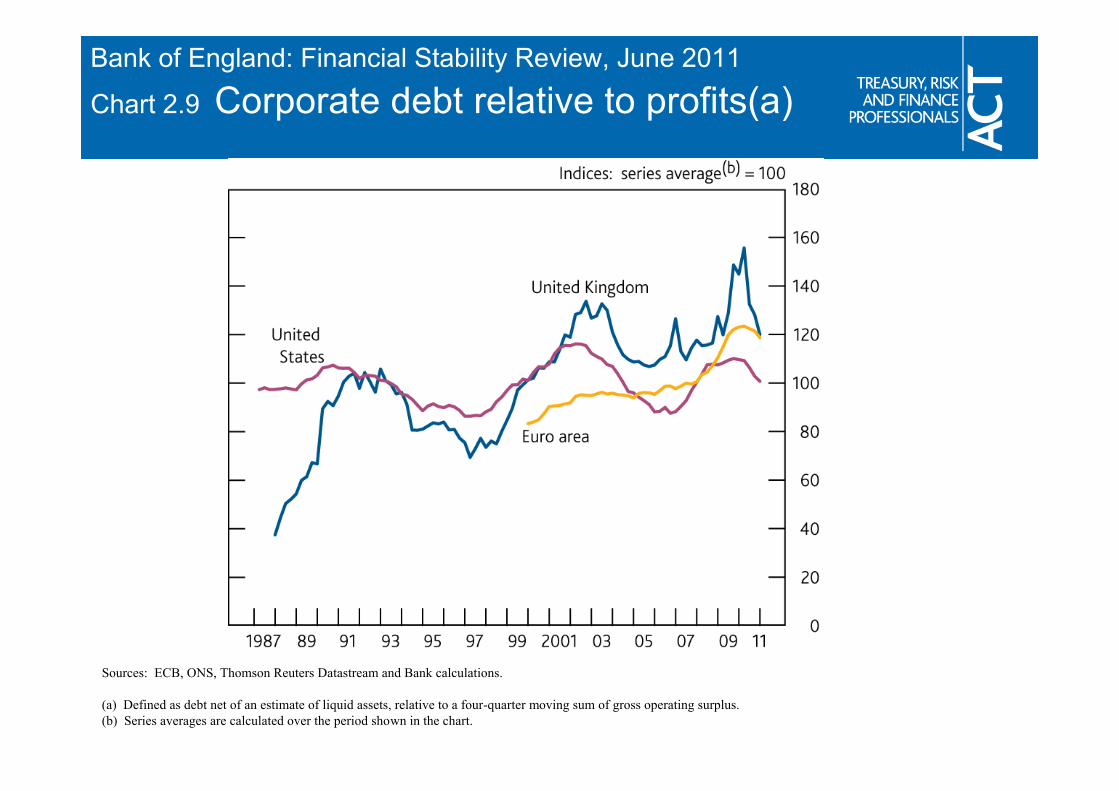

Sources: ECB, ONS, Thomson Reuters Datastream and Bank calculations.

(a) Defined as debt net of an estimate of liquid assets, relative to a four-quarter moving sum of gross operating surplus.(b) Series averages are calculated over the period shown in the chart.

Bank of England: Financial Stability Review, June 2011

Chart 2.9 Corporate debt relative to profits(a)

Source: The Deloitte CFO Survey (April 2011).

(a) CFOs were asked if their aim for the next twelve months was to raise gearing, keep it unchanged, or reduce it.(b) CFOs were asked whether it was a good time to be taking greater risk onto their balance sheets.

Bank of England: Financial Stability Review, June 2011

Chart 2.10 Attitudes of UK CFOs to risk and gearing

The changing regulatory environment

27th September 2011

Martin O’DonovanDeputy Policy & Technical [email protected]

Regulation – what’s brewing?

• Basel III = CRD IV (Capital Requirements Directive) on banks

• EMIR (European Market Infrastructure Regulation) on OTC derivatives

• MiFID review (Market in Financial Instruments Directive) on market information and processes

• Solvency II on risk for insurance companies

• Independent Commission on Banking – Vickers report on Retail banking robustness

51

Current position for OTC derivatives

• For financial derivatives (mainly interest rates, foreign exchange and credit)

– A credit line needed for trading derivatives with a bank to cover market risk and settlement risk

– Some banks (and some corporates) beginning to ask for margining or collateral

– Derivatives in pension schemes have been routinely margined for several years

• For other derivatives (e.g. commodities)

– Trading broadly done on exchanges with initial and variation margining

52

Proposed position

• Broad thrust of US / European approach includes (Dodd-Frank or EMIR)

– Reporting of derivatives transactions

– Central clearing (and margining) of standardised derivatives

– Greater standardisation of derivatives

• Regulation broadly aimed at financial sector but

– Very large trading volumes will be dragged in

– Standardisation may cascade into available products, central clearing and margining (MiFID and EMIR)

– Much increased capital for un-margined deals (CRD IV)

53

Will start a trend towards collateral demands generally

Implications for corporate treasurers

• Reporting

– But likely to be handled by trading counterparty

• ACT hopeful to avoid mandatory clearing for most non financials

• Standardisation might reduce flexibility

• Liquidity

– Funding margins / dealing with hot money

• Negative pledge clauses

• Margining may be in corporate interest to reduce credit risk

• Cost of derivatives

– Will rise with Basel III issues

54

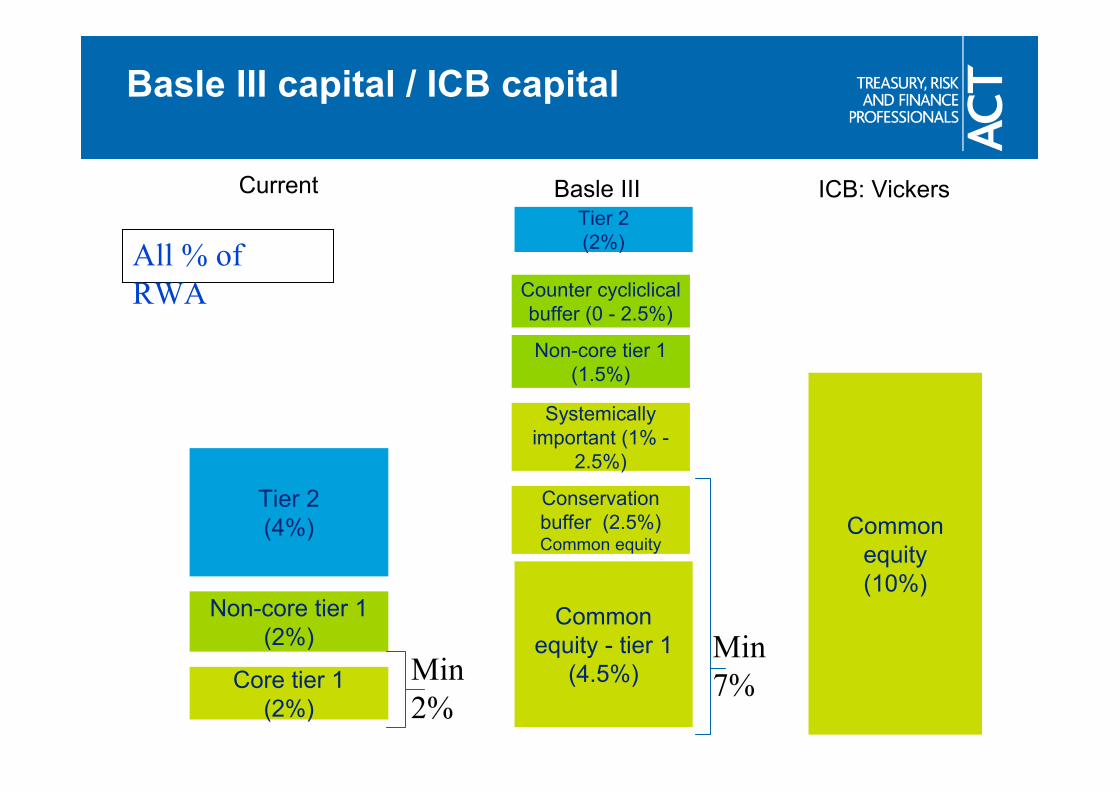

Basle III / CRD IVCapital

• Tighter definition of capital

• Much increased capital levels

• Conservation buffer which can be depleted

• Counter-cyclical buffer at national level

• Extra for systemically important banks

• New leverage measure (3% un-weighted assets)

55

- More capital means higher margins generally- Revolving credit facilities availability reduced-Undrawn facilities expensive – so need better cash forecasts -Trade finance commitments heavily hit- Derivative exposures particularly hard hit – cost up, availability down

Basle III capital / ICB capital

Tier 2(4%)

Common equity - tier 1

(4.5%)

Tier 2(2%)

Non-core tier 1(2%)

Conservation buffer (2.5%)Common equity

Non-core tier 1(1.5%)

Current Basle III

Core tier 1(2%)

Counter cycliclicalbuffer (0 - 2.5%)

Min 7%Min

2%

Common equity (10%)

Systemically important (1% -

2.5%)

ICB: Vickers

All % of RWA

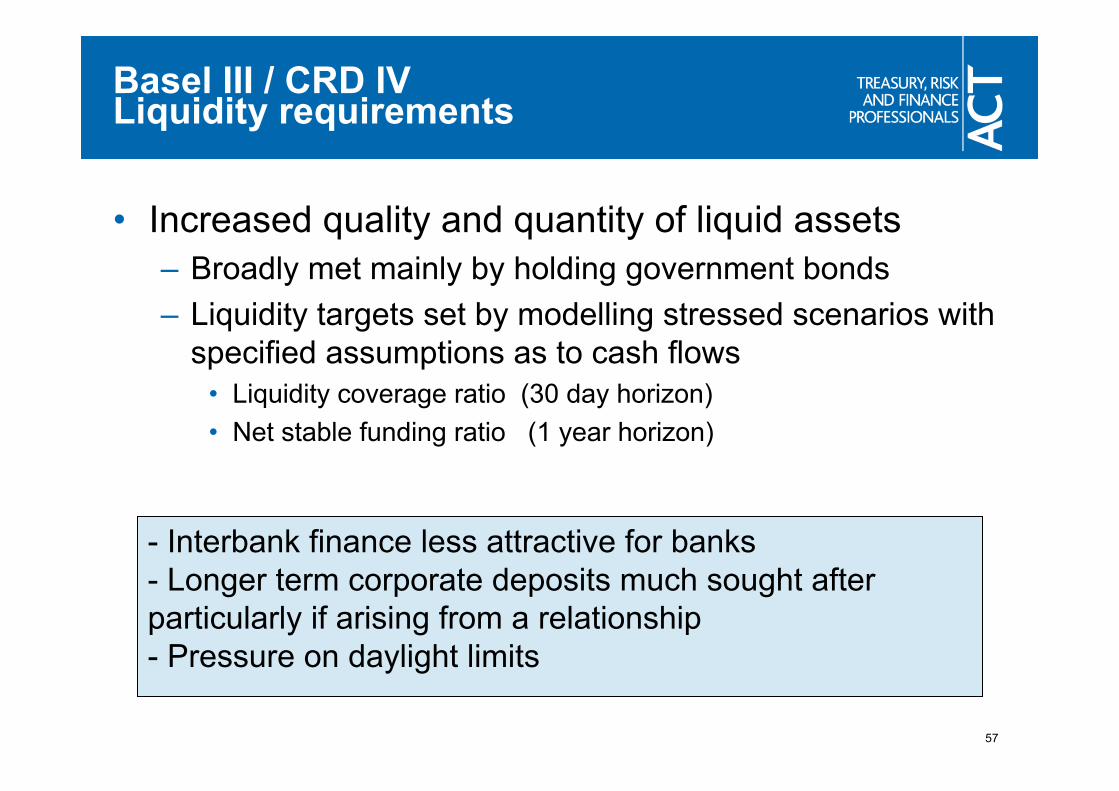

Basel III / CRD IVLiquidity requirements

• Increased quality and quantity of liquid assets

– Broadly met mainly by holding government bonds

– Liquidity targets set by modelling stressed scenarios with specified assumptions as to cash flows

• Liquidity coverage ratio (30 day horizon)

• Net stable funding ratio (1 year horizon)

57

- Interbank finance less attractive for banks- Longer term corporate deposits much sought after particularly if arising from a relationship- Pressure on daylight limits

Independent Commission on Banking - Implications

• Retail side theoretically lower risk therefore lower rates on customer deposits

• Vice-versa for non retail banks therefore higher lending margins too

• Retail can sell / introduce wholesale side so assess credit standing of each separate legal entity

• Overall additional cost of 13bp for all borrowings by customers (ICB figure)

• Balance of competitive position vs foreign banks?

58

Independent Commission on Banking: Vickers report

Capital and Loss absorbency

• Retail bank - capital 10% of RWA (Basel III = 9.5% for SIFIs)

• Non risk adjusted leverage up to 4.06% (size dependent) vs3% in Basel III

• Loss absorbing capacity 17% to 20% (dependent on size and complexity).

= bail-in bonds that are written off or convert to equity if regulator says bank not viable

• Depositor preference for deposits covered by FSCS

• Secondary bail-in power – regulator could impose losses on all unsecured liabilities

59

Independent Commission on Banking: Vickers report

Retail Ring Fence

• Must be in retail side

– Retail and SME deposit taking and payments systems

• Must be outside retail

– Derivatives, prop trading, underwriting

• On either side

– Large corporate loans and deposits

Retail may introduce services and products from non retail side

Retail may hedge its own activities

Retail dealings with non retail side at arms length and limited,and restricted on services to financial institutions

60

Be ready to adjust to circumstances

61

Source: Bank of England Inflation report May 2011

Consequences

• Deal with uncertainty through cautious capital structure

• Hold extra liquidity or committed funding - but costly therefore work on more accurate cash forecasts

• Seek out new funding markets and lenders

• Make your company attractive to lenders

– Prudent capital structure

– Decent plans and forecast

– Upside and downside scenarios including mitigations

• Consider bank relationships and ‘share of wallet’

• Adjust business model to changed environment

62

The NED Perspective

Thames Water

September 2011

64

Thames Water – the Business

UK's largest water and wastewater services company based on customers served

Over 2010 – 2015 Thames Water will invest nearly £5bn on essential work to improve ageing

water pipes, sewers and the network and will incur operating costs (excluding depreciation

measures) of £600m annually. Thames Water’s capital programme represents the biggest-ever

investment programme in the UK water industry

WaSCs Water Waste Water

Area of supply 8,000 km2 13,300 km2

Population Served 8.7 million 13.8 million

Length of mains 31,000 km 68,000 km

Key volumes2,080 mega litres per day of water delivered

3,000 mega litres per day of waste water collected

Produces 187 gigawatt hours of ‘green’ electricity

Other assets

98 water treatment plants

214 service reservoirs

27 raw water reservoirs

31 water towers

347 pumping stations

349 sewage treatment works

34 sludge treatment facilities

2,590 pumping stations

Thames Water Service Area

Reservoirs

Principal Water Treatment Works

Groundwater Sources

Principal Sewerage Treatment Works

Water Region Boundary

Sewage Region Boundary

Water Companies

Grimsbury

Farmoor

Reading

Shalford

Walton

HamptonKempton

CoppermillsMaple Lodge

Oxford

Mogden

Beckton

Crossness

Long Reach

River Cherwell

River Thames

River Kennet

River Wey

River Colne

River Lee

Deephams

Axford

Gatehampton

Medmenham

South East Water

North Surrey Water

Sutton and East Surrey Water

Three Valleys Water

Banbury

Cirencester

Swindon

Newbury

Basingstoke

Haslemere

Crawley

Sevenoaks

Dartford

Bishop’s Stortford

Stevenage

Luton

Slough

Waltham Cross

LONDON

65

Importance of Strategy

The scale of capital programme led to a £3bn funding requirement over the 5 year

regulatory period 2010-15

In the period since acquisition by the Kemble consortium in late 2006, over £4.2bn

raised in the debt capital markets at different levels in the capital structure and

across a range of markets and maturities

Have been able to access markets in a range of circumstances, including when

markets have been open during periods of market distress/crisis

The “credit story” has undoubtedly been supported by the defensive nature of the

sector and a stable regulatory regime, which has underpinned strong investment

grade credit ratings

TW’s position has been enhanced by the establishment of a clear strategy to enable

the management team to act as and when market opportunities present themselves

66

Key Pillars of Strategy

Maintenance of target credit ratings

Maintain a strong liquidity position

Management of counterparty credit risk

Diversify sources of funding

Define clear risk management parameters

Establish the appropriate governance structure

67

Key Pillars of Strategy

Maintenance of target credit ratings

– For entities with significant borrowing requirements the focus is to ensure the widest possible access to capital markets; ensure an understanding of key drivers (such as liquidity, ability to maintain key ratios, management focus and operational performance)

Maintain a strong liquidity position

– To underpin credit rating and demonstrate to markets the ability to borrow when able to rather than when need to; Thames Water maintains over £1bn of undrawn committed bank facilities to support its liquidity position

Management of counterparty credit risk

– Define clear policies and ensure systems in place to facilitate effective management of counterparty credit risk; need to consider a range of credit metrics including ratings, and set defined limits for each approved counterparty

68

Key Pillars of Strategy

Diversify sources of funding

– Seek to utilise the widest possible range of capital markets and forms of transaction, as and when pricing is competitive; understand credit requirements if considering use of derivatives

Define clear risk management parameters

– Thames Water maintains 85% of debt in either fixed rate or RPI form and maintains a balanced debt maturity profile with no more than 20% of debt maturing in any 2-years and 40% of debt within any 5-year period

Establish the appropriate governance structure

– to ensure flexibility exists to take advantage of market opportunities, but with necessary controls to ensure management discipline and alignment with the risk appetite of the business

69

Thames Water Financing Activity

Our framework has created the platform to deliver the financing requirements of the business and

has provided the flexibility to meet objectives despite periods of market closure:

– Debt capital markets were effectively closed between October 2008 and March 2008

– August 2011 no new corporate bond issuance in the Sterling market

Between 2007 and March 2010:

– over £2.5bn of senior debt (“Class A”) obligations across a range of maturities including

fixed rate public bond market issuance in Sterling and Euro markets, Sterling RPI private

placements, US Dollar and Japanese Yen private placements

April 2010 onwards:

– Over £1bn of new Class A debt across Sterling and Euro public and private bond markets

– £850m of new subordinated debt (“Class B”) in the Sterling bond market

– £825m subordinated debt refinancing programme including a debut £400m High Yield bond

70

Thames Water Governance

Board annually approves the treasury governance framework including strategy,

policy and operating procedures

Board grants delegated authorities to defined board directors, (including CEO and

CFO), to take forward financing transactions within defined limits and time-frame

maintains debt issuance programmes at both operating and holding company levels

utilised for all debt financing transactions, a common approach for frequent issuers,

reducing the time required to move to deal execution

maintains a strong relationship banking group to provide credit support and access to

a wide range of financing opportunities

Sub-committees of the Board with appropriate delegated authorities appointed to

take forward specific financing projects (used in 2007 for whole business

securitisation and 2010/11 for subordinated debt refinancing programme)

71

Financing in a Changing World

Markets will remain extremely nervous as we witness continued economic crises and

deterioration of sovereign credit quality – event risk is high and there will undoubtedly

be periods when bond markets are closed to new issuance

Lenders are developing an increased sensitivity to risk and an increased reluctance

to lend or provide credit lines

The developing regulatory framework (Basle III, Solvency II, UK bank reform), will

reduce further the capacity to obtain credit at a competitive cost

Treasury and financing strategies need to be flexible and respond to changing

market conditions

72

Appendices

TWUL Debt Portfolio

TWUL Debt Maturity Profile

73

42%

3%6%

49%

Bonds

EIB

Leasing

Index Linked43%

51%

6%Floating

Fixed

Index Linked

Financing the BusinessTWUL debt portfolio

Class A debt rated A3 by Moody’s and A- by S&P, Class B debt rated Baa3/BBB

Average debt maturity of 20 years with 8.5% of debt maturing over the next four years

Total debt £7.6bn as at 31 March 2011

£970m Class A issued, £850m Class B issued in 2010/11

Debt Split By Instrument Debt Split By Rate Type (after derivatives)

31-Mar-11 31-Mar-12 31-Mar-13 31-Mar-14 31-Mar-15 Total

Debt refinanced (£m) 402 19 564 12 152 1,149

Incremental debt (£m) 1417 481 461 582 380 3,321

Total (£m) 1819 500 1,025 594 532 4.470

Actual/to date 1819 100

TWUL Issuance

74

Financing the BusinessDebt maturity profile

Debt to be refinanced shall not exceed 20% of asset value (RCV) in any 24 month period or 40% of

RCV within any 5-year regulatory period

Figures all in Sterling Current Maturity Profile

Figures all in Sterling Debt Issuance Headroom

-

400,000

800,000

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050 2052 2054 2056 2058 2060 2062 2064

Existing Debt

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050 2052 2054 2056 2058 2060 2062

Head

roo

m (

£)

Panel discussionQ&A session

Conclusions Charles MayoPartnerSimmons & Simmons