Embed Size (px)

Citation preview

JANUARY - MARCH 2013

RSIINTRADAYSIGNALS

a weakerBREAKOUTSTRATEGY

yen?FUNDAMENTALS AND LONG TERM FLOWS ARE MORE IMPORTANT THAN POLITICS

EUR/USDDAY TRADINGSTRATEGY

TECHNICALM O N E YMANAGEMENT

TRADER MAGAZINE

FOREX OPTION

FXCONTENTs

A weAker Yen ?Politics Are just A cAtAlYstThe Yen’s fundamentals and long-term flows are more important than politics

19

A strategy combining the opening Price Principle with technical analysis tools and risk management parameters

09

Five practical trading methods to use the rsi for intraday signals

05 EDITOR’S NOTE

MONEY MANAGEMENT:

26 The science behind technical Money Management: Using technical analysis techniques with strict money management can substantially enhance the chances of reaching growth in currency investments and funds.

BOOK EXCERPT

44 Forex Option Breakout Strategy:This excerpt from “Options in Motion” exposes an FX option strategy, which is one of the five capital growth strategies developed in the book.

FX MANAGERS:

31 Interview with Douglas Garistina, CEO of Sequoia Capital Fund Management

CURRENCY WATCH:

49 USD/INR: fundamental analysis combined with a neural network-based method.

TECHNICAL OUTLOOK:

57 Major USD rates Featured market USD/CHF

58 Majors Featured cross rate EUR/JPY

59 Emerging Markets

Featured rate EUR/RON

60 Asian Rates Featured market USD/SGD

TECHNICAL ANALYSIS:

53 Majors Report: EUR/GBP, EUR/USD, EUR/JPY, USD/JPY

INTERNATIONAL DATA:

61 FX Spot Monitor

62 Central Bank Rates

63 Economica Data - FX Poll

64 Markets View

65 ECONOMIC CALENDAR

39

FX TRADER MAGAZINE January - March 2013 3

the Art oF DAY trADing the eur/usD

using rsi As An intrADAY tool:

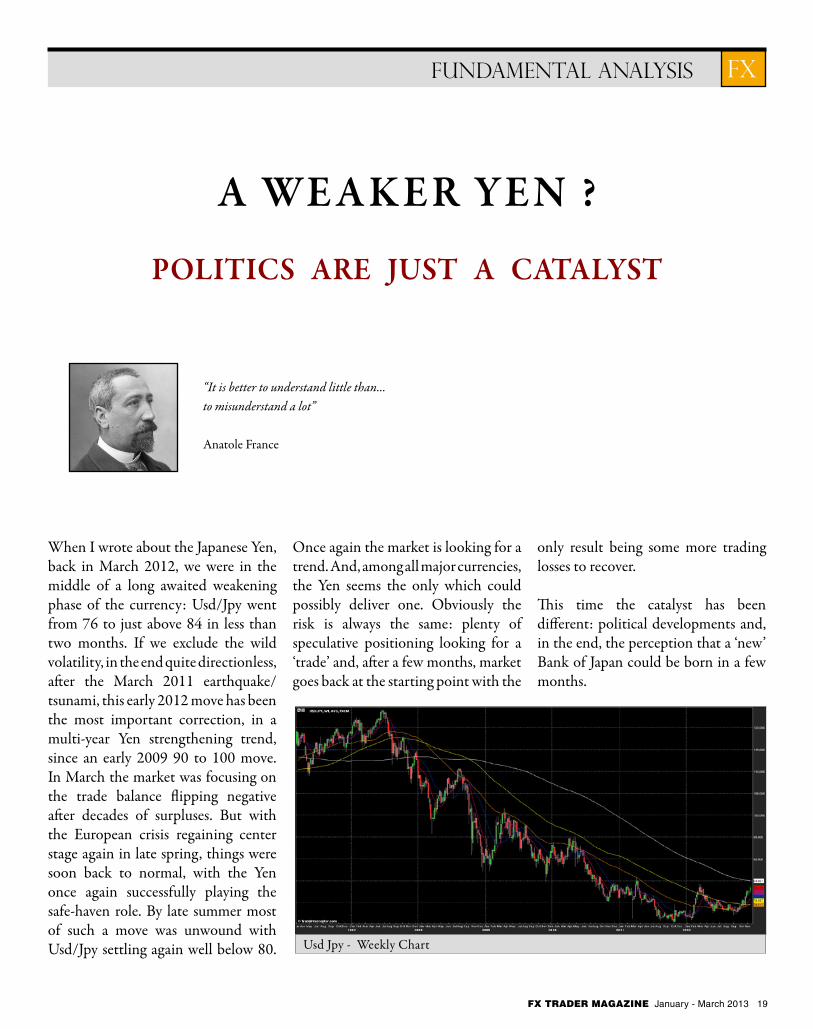

When I wrote about the Japanese Yen, back in March 2012, we were in the middle of a long awaited weakening phase of the currency: Usd/Jpy went from 76 to just above 84 in less than two months. If we exclude the wild volatility, in the end quite directionless, after the March 2011 earthquake/tsunami, this early 2012 move has been the most important correction, in a multi-year Yen strengthening trend, since an early 2009 90 to 100 move. In March the market was focusing on the trade balance flipping negative after decades of surpluses. But with the European crisis regaining center stage again in late spring, things were soon back to normal, with the Yen once again successfully playing the safe-haven role. By late summer most of such a move was unwound with Usd/Jpy settling again well below 80.

Once again the market is looking for a trend. And, among all major currencies, the Yen seems the only which could possibly deliver one. Obviously the risk is always the same: plenty of speculative positioning looking for a ‘trade’ and, after a few months, market goes back at the starting point with the

only result being some more trading losses to recover.

This time the catalyst has been different: political developments and, in the end, the perception that a ‘new’ Bank of Japan could be born in a few months.

A WE Ak ER YEN ?

POlITICS ARE JUST A CATAlYST

“It is better to understand little than...to misunderstand a lot”

Anatole France

Usd Jpy - Weekly Chart

FXFUNDAMENTAL ANALYSIS

FX TRADER MAGAZINE January - March 2013 19

A CHANGING POLITICAL LANDSCAPE

Shinzo Abe, Japan’s recently elected prime minister, has made slaying the country’s persistent deflation his top economic priority. Mr. Abe had pledged that when he would become prime minister he would manage to trigger inflation. His campaign represented a significant, and untested, shift in the focus of Japan’s policy on its twin woes of deflation and debt.

Seeking to address the debt, ex-Prime Minister Yoshihiko Noda (now in the opposition DPJ party) pushed through Parliament this summer a sales-tax increase, one reason for the unpopularity, which costed him his job in the vote. Bank of Japan Governor Masaaki Shirakawa has warned that aggressive increases in bond-buying, the central bank’s main method for easing with short-term rates essentially at zero (a.k.a. Quantitative Easing), could be seen as enabling politicians to borrow without constraint and might trigger an event that would lead to a jump in such yields. But perception is now that Mr. Noda and Mr. Shirakawa have done too little to stem the deflation that has plagued Japan in some form since the country’s asset bubble burst in 1990. Now Mr. Abe wants to shift the emphasis. “We will concentrate our policy tools to curb deflation,” he told The Wall Street Journal last month. He laid out a $2.4 trillion spending plan, and said he would consider delaying Mr.

Noda’s hard-fought tax increase “if we judge that we are not on our way out of deflation.”

Mr. Abe, leader of the Liberal Democratic Party which won elections for the Lower room by margin, has called for “unlimited” monetary easing from the BOJ until prices rise 2%. Yoshimasa Hayashi, a former economy minister who helped draft Mr. Abe’s party platform, says that despite the dangers of new deflation-fighting measures, Japan must take that chance. He compares the current situation to a man refusing to leave his house for fear of catching the flu. But just staying at home, he can’t earn a living and starts to starve. “At some point, you have to go outside and take some risks, and find some other way to prevent the virus,” he says.

With such a potential for change in the political environment, in November

the market started to focus on the recently announced and held snap general election. Rising expectations for regime change to an LDP-led government, committed to a more accomodative monetary policy, sent Usd/Jpy higher once Prime Minister Noda first hinted early election were going to be held mid-December, on November 14th. This evolution is particularly important since there is also growing interest in who will succeed BOJ Governor Masaaki Shirakawa when his term ends in April 2013. The prospect of the LDP influencing the choice after its return to power has provided ammunition for a weaker yen and for a steepening of the long and ultra-long end of the bond curve. So it could be of interest to compare the monetary policy stances of the current favorites for the job and consider the potential impact on the markets once a decision has been made.

Shinzo Abe

FX FUNDAMENTAL ANALYSIS

20 FX TRADER MAGAZINE January - March 2013