Embed Size (px)

Citation preview

JIU/REP/2000/9

STRENGTHENING THE INVESTIGATIONS FUNCTION INUNITED NATIONS SYSTEM ORGANIZATIONS

Prepared by

John D. FoxWolfgang Münch

Khalil Issa Othman

Joint Inspection Unit

Geneva2000

iii

CONTENTS

Paragraphs Page

Acronyms ....................................................................................................................... iv

EXECUTIVE SUMMARY: OBJECTIVE,CONCLUSIONS AND RECOMMENDATIONS........................................................ v

I. INTRODUCTION................................................................................................ 1-8 1

II. SIGNIFICANT ASPECTS OF THE INVESTIGATIONSFUNCTION IN UNITED NATIONS SYSTEM ORGANIZATIONS............. 9-24 3

A. The need for investigations ............................................................................ 9-10 3B. Scope and kinds of investigations ................................................................. 11-14 3C. Referral of cases to national authorities ......................................................... 15-16 3D. Fragmentation of responsibility for investigations......................................... 17-21 4E. Organizational arrangements for investigations units .................................... 22-24 5

III. IMPORTANT REQUIREMENTS FOR INVESTIGATIONS ........................ 25-39 6

A. Legal/procedural framework.......................................................................... 26-27 6B. Mandate ......................................................................................................... 28-31 6C. Operational independence.............................................................................. 32-33 8D. Strong support from the executive head......................................................... 34-35 8E. Qualified investigators ................................................................................... 36-39 8

IV. MAJOR ISSUES .................................................................................................. 40-78 10

A. Common standards and procedures ............................................................... 41-46 10B. The involvement of management in investigations........................................ 47-53 11C. Meeting the need for a professional investigations capability ....................... 54-66 12D. Financing investigations in small organizations ............................................ 67-70 14E. Need for preventive measures to reduce vulnerability ................................... 71-75 15F. Inter-agency cooperation................................................................................ 76-78 16

Annexes

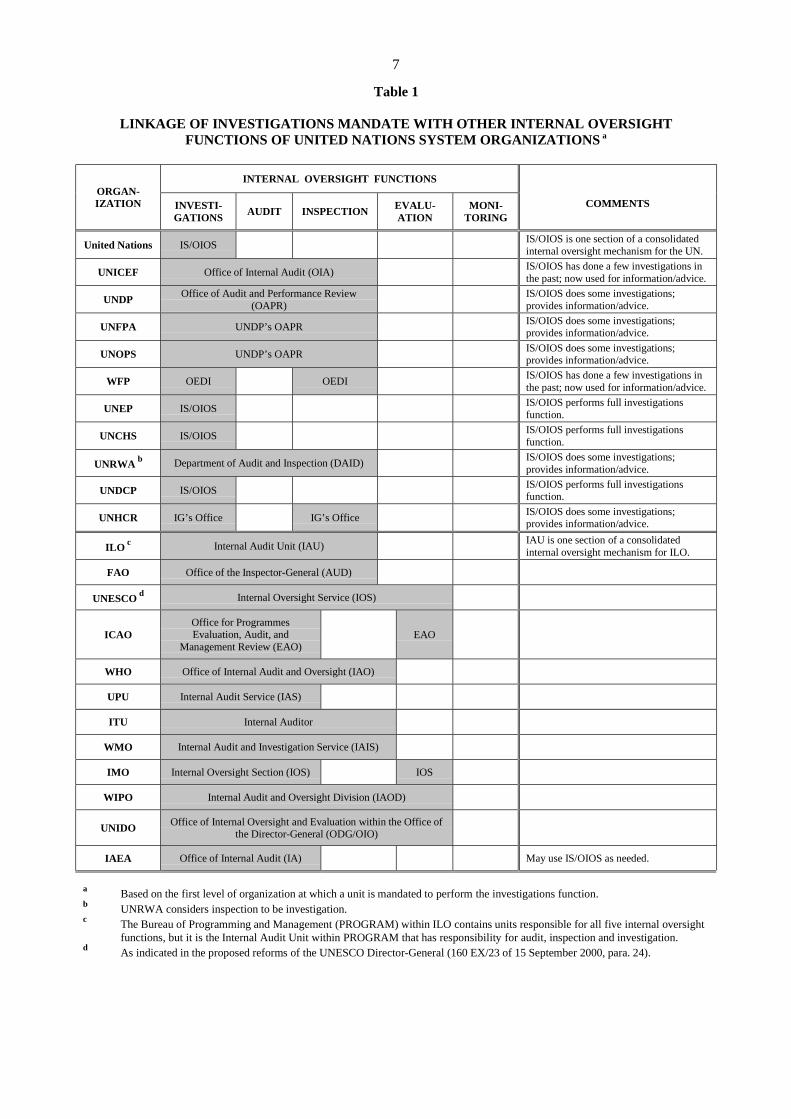

I. Brief description of investigations capabilities inorganizations of the United Nations system .................................................. 18

II. Excerpt from WMO Internal Audit Manual: principlesfor the conduct of investigations .................................................................... 24

III. World Bank Group “Quality Standards”........................................................ 25IV. Examples of unsatisfactory conduct which have been investigated

and led to disciplinary actions in UNDP/UNFPA/UNOPS ........................... 26

iv

ACRONYMS

AUD Office of Inspector-General (of FAO)DAID Department of Audit and Inspection (of UNRWA)DPKO Department of Peacekeeping OperationsEAO Office for Programmes Evaluation, Audit, and Management Review (of ICAO)FAO Food and Agriculture Organization of the United NationsFLETC Federal Law Enforcement Training CenterIA Office of Internal Audit (of IAEA)IAEA International Atomic Energy AgencyIAIS Internal Audit and Investigation Service (of WMO)IAO Office of Internal Audit and Oversight (of WHO)IAOD Internal Audit and Oversight Division (of WIPO)IAS Internal Audit Service (of UPU)IAU Internal Audit Unit (of ILO)ICAO International Civil Aviation OrganizationIES Inspection and Evaluation Service (of UNHCR)IGO Inspector General’s Office (of UNHCR)ILO International Labour OrganizationIMO International Maritime OrganizationIOS Internal Oversight Section (of IMO) and Internal Oversight Service (of UNESCO)IS/OIOS Investigations Section of the Office of Internal Oversight ServicesITU International Telecommunication UnionJIU Joint Inspection UnitOAPR Office of Audit and Performance Review (of UNDP)ODG/OIO Office of Internal Oversight and Evaluation within the Office of the Director-General (of

UNIDO)OEDI Office of Inspector General (of WFP)OHR Office of Human Resources (of UNDP)OIA Office of Internal Audit (of UNICEF)OIOS Office of Internal Oversight Services (of United Nations)UNCHS United Nations Centre for Human Settlements (Habitat)UNCTAD United Nations Conference on Trade and DevelopmentUNDCP United Nations International Drug Control ProgrammeUNDP United Nations Development ProgrammeUNEP United Nations Environment ProgrammeUNESCO United Nations Educational, Scientific and Cultural OrganizationUNFPA United Nations Population FundUNHCR United Nations High Commissioner for RefugeesUNHQ United Nations HeadquartersUNICEF United Nations Children’s FundUNIDO United Nations Industrial Development OrganizationUNOG United Nations Office at GenevaUNON United Nations Office at NairobiUNOPS United Nations Office for Project ServicesUNRWA United Nations Relief and Works Agency for Palestine Refugees in the Near EastUPU Universal Postal UnionWFP World Food ProgrammeWHO World Health OrganizationWIPO World Intellectual Property OrganizationWMO World Meteorological Organization

v

EXECUTIVE SUMMARY:OBJECTIVE, CONCLUSIONS AND RECOMMENDATIONS

Objective:To enhance the capability of United Nations system organizations for meeting the need forinvestigations.

CONCLUSIONS

A. The investigations function has become animportant component of internal oversight for mostUnited Nations organizations, but this function isrelatively new in the System and some major issuesneed to be addressed and resolved (para. 1).

B. Significant aspects of the investigations functionin United Nations system organizations include:

1. An effective investigations function is requiredto deter wrongdoing, to assure properaccountability and to maintain the confidence ofMember States and other stakeholders in theintegrity of the organizations they are supporting(paras. 9-10).

2. The investigations focus on fraud and corruptionbut include a wide variety of other cases as well,and can concern individuals who are notmembers of organization secretariats (paras. 13-14).

3. The referral of investigation cases to nationalauthorities can have a strong deterrent effect, butthere are reasons for being cautious in doing so(paras. 15-16).

4. There is a fragmentation of responsibility for theinvestigations function within the organizationsof the United Nations system (paras. 17-21).

5. Significant differences exist among theorganizations of the United Nations systemregarding the location and lines of reporting forthose units specifically mandated to conductinvestigations (paras. 22-24).

6. Opportunities for more effective inter-agencycooperation regarding the investigations functionhave been increased with the annual Conferenceof Investigators of United Nations Organizationsand Multilateral Financial Institutions, initiatedby OIOS in 1999 (paras. 76-78).

C. Requirements for investigations include:

1. An established legal/procedural framework(paras. 26-27).

2. A clear mandate, including jurisdictions andauthorities (paras. 28-31).

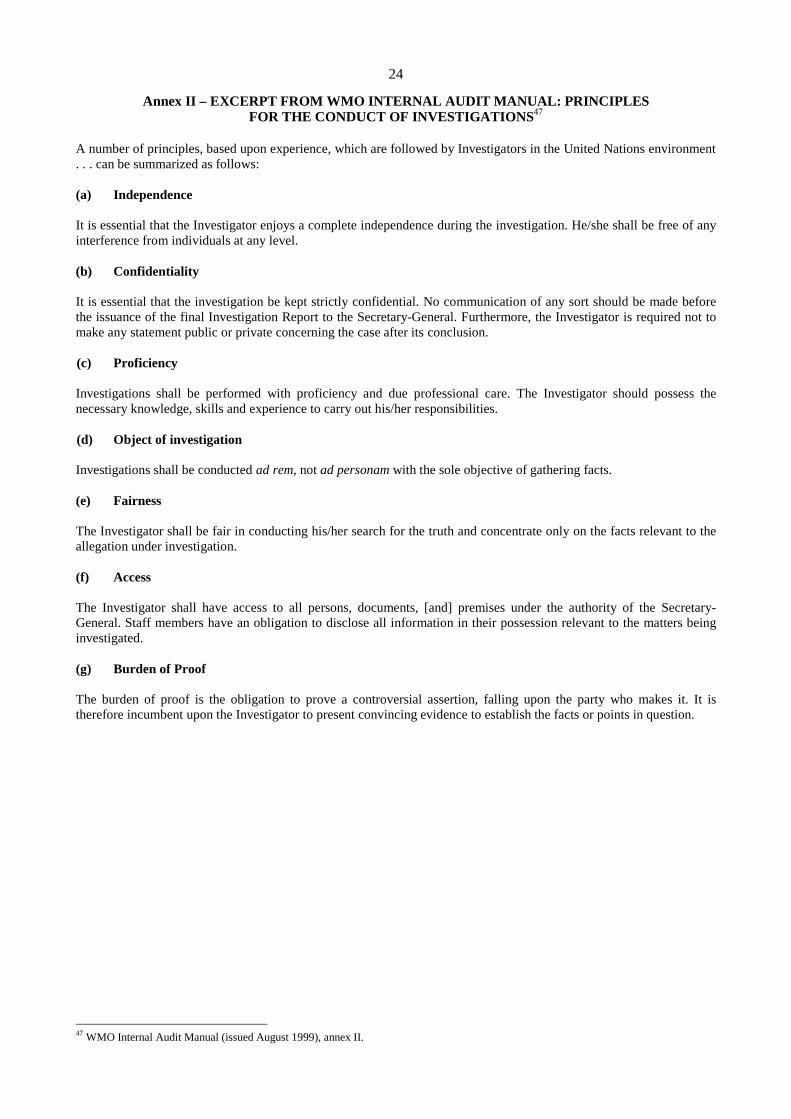

3. Operational independence (paras. 32-33).

4. Strong support from the organization’s executivehead (paras. 34-35).

5. Qualified investigators (paras. 36-39).

D. Major issues to be addressed regarding theinvestigations function in United Nations systemorganizations include:

1. Common standards and procedures forconducting investigations (paras. 41-46).

2. Training of programme and administrativesupport managers for their involvement ininvestigations (paras. 47-53).

3. Meeting the need for access to a professionalinvestigations capability (paras. 54-66).

4. Options for small organizations regarding thefinancing of access to professionally trained andexperienced investigators (paras. 67-70).

5. The need for preventive measures to reducevulnerability to wrongdoing by use of proactiveinvestigations and lessons learned fromcompleted investigations (paras. 71-75).

6. Inter-agency cooperation regarding theinvestigations function (paras. 76-78).

vi

RECOMMENDATIONS

1. Common standards and procedures

The Third Conference of Investigators ofUnited Nations Organizations andMultilateral Financial Institutions in 2001should make arrangements for developingand adopting a common set of standards andprocedures for conducting investigations inUnited Nations system organizations (paras.41-46).

2. Training for managers

Executive heads of organizations shouldensure that managers involved ininvestigations have sufficient training in theuse of established standards and proceduresfor conducting investigations (paras. 47-53).

3. Meeting the need for a professional investi-gations capability

Each executive head should conduct a riskprofile of his/her organization as an initialbasis for issuing a report to the appropriatelegislative organ on the organization’s needfor access to professionally trained andexperienced investigators. This report shouldindicate those measures that the executivehead would recommend as necessary to meetthis need (paras. 54-66).

4. Options for financing access of smallorganizations to a professional investigationscapability

Executive heads of small organizations shouldpresent to their appropriate legislative organsoptions for financing the access that may benecessary for their organizations toprofessionally trained and experiencedinvestigators such as, inter alia, the use ofcommon services and/or outsourcing(including within the United Nations system)(paras. 67-70).

5. Preventive measures based on proactiveinvestigations and lessons learned

Executive heads should ensure that workprogrammes of units responsible forinvestigations include the development ofpreventive measures based on proactiveinvestigations and lessons learned fromcompleted investigations (paras. 71-75).

6. Conferences of United Nations Investigators

Conferences of Investigators of UnitedNations Organizations and MultilateralFinancial Institutions should continue todevelop opportunities, including thoseexternal to the System, to foster inter-agencycooperation regarding the investigationsfunction in areas such as those indicated in thereport (paras. 76-78).

1

I. INTRODUCTION

1. The investigations function has become anincreasingly important component of internaloversight for most United Nations systemorganizations, but it remains very much in adevelopmental stage with a number of issues stillneeding to be resolved. The objective of this report isto address those issues and make recommendations toenhance the capability of organizations in the Systemto meet the need for investigations.

2. A previous report of the Joint Inspection Unit(JIU), entitled “More coherence for enhancedoversight in the United Nations system”,1 reviewedthe full range of oversight functions in theorganizations of the System and maderecommendations to improve the effectiveness ofthose functions. Preparation of that report indicatedthe developmental stage of the investigationsfunction in the System and the need for a more in-depth examination of it.

3. The present report is system-wide, covering theUnited Nations, its funds and programmes, and thespecialized agencies and IAEA. To gather thenecessary information, a questionnaire was sent outin early March 2000 to the organizations of theSystem.

4. The questionnaire was supplemented byextensive interviews with officials of someorganizations, which took place, for the most part, inApril and May 2000. The officials interviewedrepresented a wide spectrum of responsibilities,including legal, budget, human resources and internaland external audit, in addition to those specificallyresponsible for conducting investigations. Thoseincluded in the interviews were officials of theUnited Nations, both at Headquarters in New York(UNHQ) and at the United Nations Office at Nairobi(UNON), as well as several of the United Nationsfunds and programmes and specialized agencies inNew York, Geneva, Rome and Nairobi. As we hadexpected in planning our mission to Nairobi, gettinga field perspective on the investigations function wasof major assistance in preparing this report. Althoughthe World Bank is not a JIU participating agency,World Bank officials helpfully provided importantbackground information during interviews inWashington, D.C.

5. In gathering data on the investigation caseloadsof the organizations, we encountered significant 1 A. T. Abraszewski, J. D. Fox, S. Kuyama and K. I. Othman,“More coherence for enhanced oversight in the United Nationssystem”, JIU/REP/98/2, transmitted to the United Nations GeneralAssembly as A/53/171 of 9 July 1998.

problems. We were struck by the major differences inreported caseloads. However, our review of the datasubmitted in the questionnaire responses and ourinterviews with the oversight professionals involvedin investigations made it clear that the data had to betreated with caution, particularly for comparativepurposes. The data received were non-comparable forreasons such as:

– The jurisdiction of units conducting investi-gations differs among organizations, e.g., sexualharassment allegations are variously investigatedby human resources management professionals,by investigations professionals, or by designatedsenior managers.

– In general, the data submitted related only tocases handled by oversight units, e.g., allsubmissions except for that of the United NationsOffice at Geneva (UNOG) omitted caseloads ofthe investigations units of security and safetyservices.

– The organizations use different criteria forrecord-keeping regarding investigations, e.g.,“closed” cases may mean determination of guiltor innocence for one organization, while anothermay also include cases closed for a variety ofother reasons (referral to another office,requested information provided, insufficientinformation, etc.).

6. We concluded that there was little to be gainedfrom tabular presentations of the caseload data wecollected from the organizations and, in fact, doing sowould not be justified in view of the sensitivity of thematter. An appropriate objective in the future may befor the organizations to devise and implement areporting process that would provide sufficientlycomparable data on investigation cases, and actionstaken on them. However, attempting this now risksinvolving the already limited resources available forthe investigations function in what most likely wouldbe a time-consuming and fruitless exercise. It wouldbetter serve the interests of the System at this stage toaddress the issues identified in this report andimplement the related recommendations. This wouldalso establish a more promising basis for effectivesystem-wide reporting on investigations in the future.

7. Chapters II and III provide background for thereport by reviewing significant aspects of theinvestigations function in United Nations systemorganizations, and important requirements for beingable to conduct effective investigations. Chapter IV,the heart of the report, addresses major issuesrelevant to the development of this important

2

oversight function in the organizations of the UnitedNations system. The issues addressed in chapter IVare the basis for the recommendations presented inthe Executive Summary.

8. We would like to thank the many people who sowillingly contributed their expertise to thepreparation of this report. Those who found the timein their busy schedules to respond to ourquestionnaire and/or to meet with us for interviewshave earned our gratitude. We are especially indebted

to the investigations professionals of the Office ofInternal Oversight Services (OIOS) and the WorldFood Programme (WFP), who provided much usefuladvice in the planning for this report, and then tookthe time to review and comment on the draftquestionnaire. The JIU focal points in theorganizations and the head of administration inUNON were most effective and helpful in makingarrangements for our interviews, for which we aregrateful.

3

II. SIGNIFICANT ASPECTS OF THE INVESTIGATIONS FUNCTION INUNITED NATIONS SYSTEM ORGANIZATIONS

A. The need for investigations

9. A senior official we interviewed for this reportnoted his surprise when he took office that so littlewas being done about a whole range ofmisdemeanours by staff, and the only risk they facedby committing wrongful acts was that of losing theirjobs. Fortunately, there has been in the Systemincreasing recognition of and concern about thepossibility of an organization being subject towrongdoing by staff members and by those externalto the organization who provide goods and servicesto it. Hence there is now a greater recognition of theneed for an effective investigations capability to bothdetect and deter such wrongdoing.

10. The recognition of this need for an investigationscapability has been an integral part of the increasedconcern for effective oversight witnessed over thepast several years in the United Nations system. Thisreflects a new realism about the need for activemeasures to ensure proper accountability and deterwrongdoing. It also reflects a practical requirementfor maintaining the confidence of Member States andother stakeholders in the integrity of theorganizations they are called upon to supportfinancially, politically and substantively.

B. Scope and kinds of investigations

11. Investigations, as considered in this report, maybe either reactive or proactive. Reactiveinvestigations are instigated in response toallegations, reports or incidents. The mandate forreactive investigations can be seen, for example, inUnited Nations General Assembly resolution 48/218B, of 12 August 1994, which calls for the Office ofInternal Oversight Services, inter alia, to “investigatereports of violations of United Nations regulations,rules and pertinent administrative issuances…”.2

Proactive investigations entail analysis and testing ofsituations and operations to identify areas of risk forthe purpose of developing or improving measuresand systems of control that would pre-empt wrongfulacts. Again relating to the United Nations, a mandatefor such proactive investigations is found in theSecretary-General’s Bulletin on “Establishment ofthe Office of Internal Oversight Services”.3 This callsfor investigations of the “potential within programmeareas for fraud and other violations” as a basis for

2 “Review of the efficiency of the administrative and financialfunctioning of the United Nations”, A/RES/48/218 B, 12 August1994, para. 5 (c) (iv).

3 ST/SGB/273 of 7 September 1994, para. 17.

recommendations for “corrective action to minimizethe risk of commission of such violations”.

12. In the organizations of the United Nationssystem, both types of investigations are undertaken,but the major emphasis is on reactive investigations.This report accordingly focuses on reactiveinvestigations, but it does address, also, the need forproactive investigations and recommends thatattention be given to this need (see recommendation5 in the Executive Summary and paras. 71-75 below).

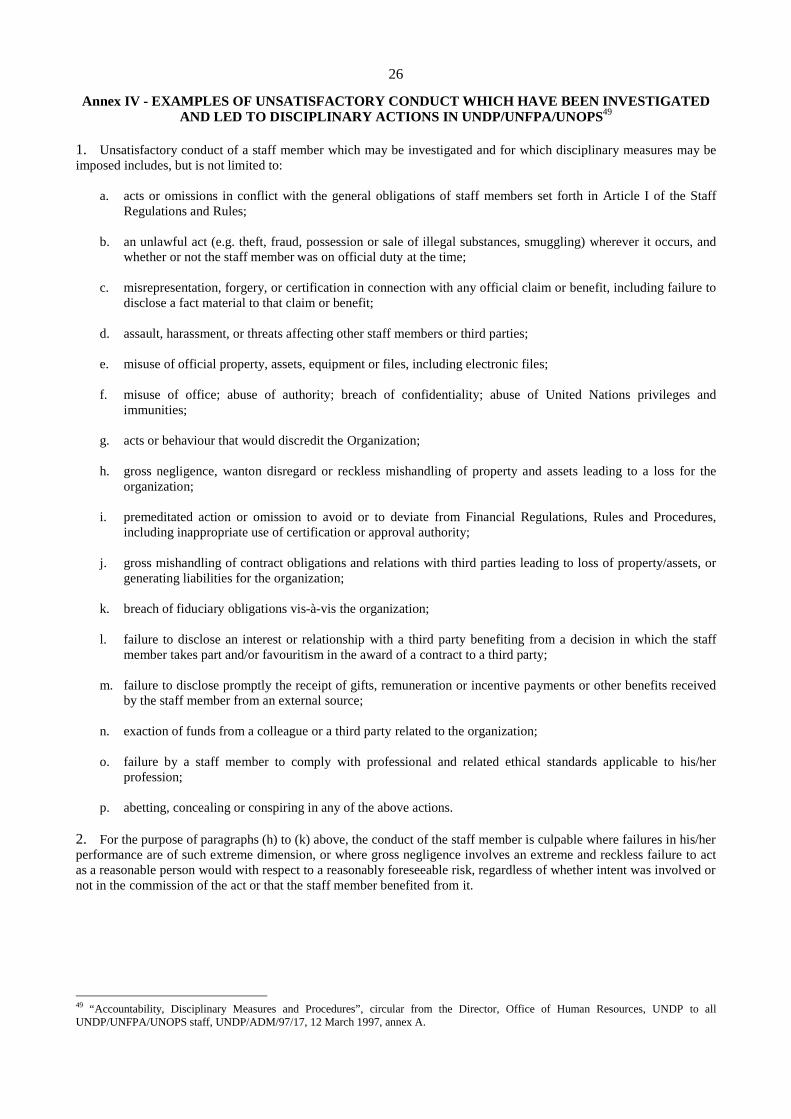

13. While the main focus of investigations in theorganizations of the United Nations system is onfraud and corruption, investigations also cover a widerange of wrongdoing without direct financialimplications, such as theft of personal property,abuse of authority, violations of ethical behaviour,sexual harassment, assault, and even murder. Thedocument at annex IV illustrates the wide variety ofinvestigations possible in an organization.

14. The scope of investigations in the United Nationssystem is not limited to staff of organizationsecretariats. Investigations can extend also to externalparties, such as contractors or consultants performingservices and companies supplying goods. This, inturn, means that investigations can be conductedwithin the framework of the national legal system,both civil and criminal, of the relevant host countryin addition to the regulations, rules and pertinentadministrative issuances of United Nationsorganizations.

C. Referral of cases to national authorities

15. We found varying practices among theorganizations, and a wide diversity of opinion amongthe officials concerned, regarding the referral of casesto national authorities. Many organizations are veryhesitant about such referrals for a number of reasons:

− the bad publicity that such action can engender,especially when the significance of the case isnot great;

− the related costs, which may be substantial, interms of staff time spent developing andproviding evidence and testimony;

− the requirement to make public possiblyconfidential and/or embarrassing information;

4

− severe delays in a national jurisdiction’s judicialprocesses which could block internal action byan organization on a case that may be urgentlyrequired;

− the uncertainties of judicial processes in somenational jurisdictions which could lead to anacquittal for an accused staff member andthereby compromise the ability to succeed with agood case against that staff member for summarydismissal within an organization’s administrationof justice process;4

− sharp differences in the severity of the penalcode among national jurisdictions; and

− just making the threat of criminal prosecutionindirectly through diplomatic channels, withoutactual referral of the case to national authorities,may better assist in the recovery of losses forsome cases.5

16. However, while not disputing the need to givecareful consideration to such possible negativeeffects of referring cases to national authorities, manyofficials are emphatic that the deterrent effect ofmaking such referrals normally outweighs thepossible negative consequences. In someorganizations, generally those with a major fieldpresence, that is the opinion reportedly held stronglyby the executive heads. Those supporting this viewstress the importance of sending a message to staffand those who do business with United Nationsorganizations that corrupt acts will not be toleratedand will be prosecuted to the fullest extent of the law.Other benefits they cite are recovery of assets and/orreimbursement for losses, transparency of purpose,clear determination of guilt or innocence and often aswifter process than the internal justice system.

D. Fragmentation of responsibility for investi-gations

17. Except for IAEA and the World MeteorologicalOrganization (WMO), no United Nations systemorganization places full responsibility for theinvestigations function in a single internal entity.6

4 It should be noted, however, that the United NationsAdministrative Tribunal has ruled that acquittal in a national courtis not sufficient basis for a successful appeal by a staff memberagainst his/her summary dismissal. United Nations AdministrativeTribunal Judgement No. 436 (Case No. 457: Wiedl Against: TheSecretary-General of the United Nations, 9 November 1988).

5 In this regard, it should be noted that conviction in a nationaljurisdiction may be required to gain recovery of losses throughattachment of the assets of the guilty party.

6 The new mandates for investigations in some organizationsappear to centralize responsibility, but other documents assignresponsibility for aspects of the investigations function to other

Furthermore, the division of responsibilities amongthe different entities vested with this function is notalways clear. A good example of this fragmentationcan be seen in the United Nations HighCommissioner for Refugees (UNHCR). Althoughthere is an Inspector General, who is the designatedfocal point for investigations, investigations may beconducted also by the heads of the concerned offices,by the heads of the various administrative supportdivisions, by both the UNHCR Audit Section and theInvestigations Section of OIOS (IS/OIOS), and byuse of “other resources as appropriate”.7

18. The mandates of the security and safety servicesof United Nations organizations certainly do notfocus on the investigations function, but they donevertheless have a role in this regard. Weinterviewed senior officials of the security and safetyservices at UNHQ, UNON and the Food andAgriculture Organization of the United Nations(FAO) in Rome to ascertain to what extent securityand safety services are involved in investigations.While the major purpose of such services is to ensurethe physical security of people and property in apreventive sense, they also carry out investigationsinto incidents of wrongdoing, and at least some havededicated investigations units for that purpose. Theincidents investigated are, for the most part, thefts ofproperty, but the services are also involved in at leastsome investigations of fraud and corruption.

19. At UNHQ in New York, the dividing linebetween the Security and Safety Service andIS/OIOS regarding investigations is relatively clear,as is the case for the equivalent entities in FAO. TheSecurity and Safety Service in UNON, however,appears to have a broader role than that of other suchservices in the United Nations system. Owing to thesecurity situation in the Nairobi area, theirresponsibilities extend beyond the UNON complex,and entail regular liaison with, and support of, thelocal police. Especially regarding thefts, they havebeen involved in investigations. Moreover, inaddition to serving the United Nations, they alsoprovide services for the many other United Nationsorganizations with offices in Nairobi, and some ofthem have requested assistance for cases involvingfraud and corruption. Nevertheless, even with regardto Nairobi, the relationship between the security andsafety services and other units with responsibility forinvestigations appears to be mutually supportive and

units as well, e.g., United Nations, WHO (see footnotes 19 and 22respectively).

7 “Focal Point for Investigation”, Inter-Office and Field OfficeMemorandum from the High Commissioner to all staff membersat headquarters and in the field, UNHCR/IOM/77/97-FOM/84/97,14 November 1997; and UNHCR brochure “Inspector General’sOffice” (undated).

5

works well in practice, despite some overlap inactivities regarding investigations.

20. For most United Nations system organizations,management officials – including the concernedprogramme managers and those managersresponsible for administrative support functions,especially human resources management – areauthorized, and even mandated, to conductinvestigations. While the role of the variousmanagement officials in conducting investigationsmay be proper and unavoidable, this presents an issuethat will be addressed separately in section B ofchapter IV.

21. An additional factor leading to fragmentation ofresponsibility for the investigations function is therequirement in many organizations for the specialhandling, often by those responsible for humanresources management, of investigations regardingalleged sexual harassment. This is because theproblem of sexual harassment has often been dealtwith in specific legislative instruments andadministrative issuances.

E. Organizational arrangements for investi-gations units

22. Separate investigations units, staffed byprofessionally trained and experienced investigators,are the exception rather than the rule in theorganizations of the United Nations system (table 1).The Investigations Section of OIOS is the only clearexample of a separate unit, although it can be arguedthat the Office of the Inspector General (OEDI) ofWFP is essentially a separate investigations unit aswell.8 In most other organizations, responsibility forthe investigations function is assigned to an internaloversight unit which has responsibility also for someor all of the other internal oversight functions (audit,inspection, evaluation, monitoring). This is the casefor all of the specialized agencies and IAEA. AmongUnited Nations funds and programmes, this is alsothe case in the United Nations DevelopmentProgramme (UNDP), UNHCR, the United NationsChildren’s Fund (UNICEF), and the United NationsRelief and Works Agency for Palestine Refugees inthe Near East (UNRWA). The remaining funds andprogrammes make use of IS/OIOS.9

23. In all cases, the officials or units responsible forinvestigations report either directly to the executive

8 The Inspector General of WFP is responsible for both investi-gations and inspections. However, the inspections conducted bythe Inspector General appear to serve primarily as proactiveinvestigations.

9 The role of IS/OIOS regarding the funds and programmes withtheir own internal investigations capabilities is a matter still underconsideration in the United Nations General Assembly.

head of the organization or to an overall head ofinternal oversight, e.g., an Inspector General, whoreports directly to the executive head. In manyorganizations, relevant provisions of mandates callfor Member States in the appropriate legislativeorgan and/or other Member States to receive eitherdirectly, or unchanged from the executive head of theorganization, both an annual summary report oninternal oversight activities and reports on individualmatters prepared by the head of internal oversight.10

In FAO, the World Health Organization (WHO) andthe International Labour Organization (ILO), forexample, the mandates for the directors of therelevant units call for these officials to submit annualsummary reports on internal oversight activities aswell as to send any reports on their work that theymay deem appropriate to their respective legislativeorgans and, in the case of FAO, to other interestedMember States as well.11

24. The investigations units/officials in the Systemare mostly centralized and situated at headquarters,although their staff must travel frequently to fieldlocations to carry out their work, e.g., WFP,UNHCR and UNICEF. However, IS/OIOS has asmall staff located in Nairobi, largely to minimize thecosts of investigations regarding the manyorganizations that have operations in Nairobi andother parts of Africa. Nevertheless, the direction ofIS/OIOS remains centralized in UNHQ. The Officeof Inspector-General in FAO (AUD) maintains anintegrated approach, but there are four auditors (withvarying degrees of investigative experience) locatedin major regions away from Headquarters. WHO hastwo auditors located in Washington, D.C., to coverthe Regional Office for the Americas, but they reportdirectly to the Chief of Internal Audit and Oversightat Headquarters.

10 The release of internal oversight reports on individual matters iscommon practice in the United Nations, but it has not been thepractice of the heads of internal oversight in other organizations torelease such reports to legislative organs on their own initiative.The WHO Chief of Internal Audit and Oversight did release a1999 report on “Evaluation of the management support units”, butthis was in response to a request in a resolution of the ExecutiveBoard (EB 103.R6).

11 For the mandate of the WHO Chief of Internal Audit andOversight, see WHO Information Circular No. 69 on “Office ofInternal Audit and Oversight (IAO)” (IC/96/69 of 12 December1996) and WHO Financial Rule 117.4. For the mandate of theILO Chief Internal Auditor, see ILO Financial Rule 14.10. Therelevant wording in the Charter for the Office of the Inspector-General in FAO is as follows: “The Office of the Inspector-General shall report the results of its work and makerecommendations to management for action with a copy to theDirector-General and the External Auditor. At the discretion ofthe Inspector-General, any such report may also be submitted tothe Finance Committee together with the Director-General’scomments thereon and be made available to other interestedmember states [emphasis added].”. See FAO, Director-General’sBulletin, No. 2000/11, 1 February 2000, para. 13.

6

III. IMPORTANT REQUIREMENTS FOR INVESTIGATIONS

25. In considering the investigations capabilities ofUnited Nations system organizations, it is useful toreview briefly some important requirements that mustbe met in order for the investigations function to becarried out effectively. To the extent that some ofthese requirements are not being met, they areconsidered further in the following chapter.

A. Legal/procedural framework

26. Investigation is in many ways a legal undertakingand, as such, must be conducted within anappropriate legal framework. This requirement iswell met in the United Nations system. The necessarylegal framework is defined by the United NationsCharter – and the equivalent basic instruments of theother organizations – as well as relevant resolutionsand decisions of legislative organs, regulations, rulesand pertinent administrative issuances. Alsocontributing to this legal framework are theapplications and interpretations of these documentsthat occur in specific cases through the functioning ofthe processes for the administration of justice in theorganizations. In addition, the organizations mayhave recourse to the judicial systems of MemberStates, which have their own defined legalframeworks.

27. A legal framework is necessary but not sufficientfor the proper conduct of investigations; anestablished and recognized set of standards andprocedures is also required, to form a basis foravoiding arbitrary practices so that investigations areconducted in a consistent, professional, impartial,thorough and timely manner.12 There are currently noformally agreed common standards and proceduresfor the conduct of investigations in the organizationsof the United Nations system. The need for such is anissue addressed in section A of the following chapter.

B. Mandate

28. In order to have the legitimacy required to beeffective, and to ensure proper accountability, thoseresponsible for conducting the investigations functionmust have a mandate for doing so from a recognizedsource, and this mandate must be widely understoodwithin the organizations. The usefulness of suchmandates is increased by including a clear indicationof specific authorities to be used in conductinginvestigations, e.g., initiation of investigationswithout hindrance, free access to staff members and 12 This useful set of objectives for investigations is included inWorld Bank Group, Business Ethics and Integrity Office,“Standards and procedures for inquiries and investigations”, DraftRev. 1.1, 29 May 2000, p. 1.

full cooperation from them, rights to inspectcomputer and other files, the use of surveillancemeasures, specification of due process requirements.There should also be an indication of the jurisdictions– e.g., geographical, organizational, types of cases –within which these authorities exist, and under whatconditions.

29. While investigations are not new to UnitedNations organizations, it was not until the mid-1990sthat significant attention began to be paid to theinvestigations function within the System. With thisnew focus on it, the investigations function hasincreasingly been seen as a necessary and importantpart of internal oversight. As a result, this function isnow included in the mandates of the internaloversight mechanisms for all of the organizations.However, reflecting the still developmental stage ofthe investigations function in the System, thearticulation of mandates for it in documents, andimplementation of those mandates, vary greatlyamong the organizations, especially in regard to thespecification of related authorities and jurisdictions.

30. Responsibility for this mandate is handleddifferently within internal oversight mechanisms forthe organizations of the System. A graphicpresentation of these differences can be seen in table1. The role of IS/OIOS for many, but not all, UnitedNations funds and programmes should be noted. Alsoof note is that all of the specialized agencies andIAEA assign the investigations function to the unitprimarily responsible for internal audit, which alsohas responsibility for various other internal oversightfunctions depending on the agency. A briefdescription of how the investigations function isassigned among internal oversight units for each ofthe United Nations system organizations can befound in annex I.

31. As noted in the preceding chapter, there is afragmentation of responsibility for the investigationsfunction within most organizations of the UnitedNations system. In addition to being assigned to aninternal oversight unit, responsibility forinvestigations is often assigned also to the securityand safety services, to programme managers andadministrative support managers, and to Boards ofEnquiry. This fragmentation of responsibility, whichappears to be unavoidable and even necessary, canpresent a problem that will be addressed in section Bof the following chapter.

7

Table 1

LINKAGE OF INVESTIGATIONS MANDATE WITH OTHER INTERNAL OVERSIGHTFUNCTIONS OF UNITED NATIONS SYSTEM ORGANIZATIONS a

INTERNAL OVERSIGHT FUNCTIONSORGAN-IZATION INVESTI-

GATIONSAUDIT INSPECTION EVALU-

ATIONMONI-

TORINGCOMMENTS

United Nations IS/OIOSIS/OIOS is one section of a consolidatedinternal oversight mechanism for the UN.

UNICEF Office of Internal Audit (OIA)IS/OIOS has done a few investigations inthe past; now used for information/advice.

UNDPOffice of Audit and Performance Review

(OAPR)IS/OIOS does some investigations;provides information/advice.

UNFPA UNDP’s OAPRIS/OIOS does some investigations;provides information/advice.

UNOPS UNDP’s OAPRIS/OIOS does some investigations;provides information/advice.

WFP OEDI OEDIIS/OIOS has done a few investigations inthe past; now used for information/advice.

UNEP IS/OIOSIS/OIOS performs full investigationsfunction.

UNCHS IS/OIOSIS/OIOS performs full investigationsfunction.

UNRWA b Department of Audit and Inspection (DAID)IS/OIOS does some investigations;provides information/advice.

UNDCP IS/OIOSIS/OIOS performs full investigationsfunction.

UNHCR IG’s Office IG’s OfficeIS/OIOS does some investigations;provides information/advice.

ILO c Internal Audit Unit (IAU)IAU is one section of a consolidatedinternal oversight mechanism for ILO.

FAO Office of the Inspector-General (AUD)

UNESCO d Internal Oversight Service (IOS)

ICAOOffice for ProgrammesEvaluation, Audit, and

Management Review (EAO)EAO

WHO Office of Internal Audit and Oversight (IAO)

UPU Internal Audit Service (IAS)

ITU Internal Auditor

WMO Internal Audit and Investigation Service (IAIS)

IMO Internal Oversight Section (IOS) IOS

WIPO Internal Audit and Oversight Division (IAOD)

UNIDOOffice of Internal Oversight and Evaluation within the Office of

the Director-General (ODG/OIO)

IAEA Office of Internal Audit (IA) May use IS/OIOS as needed.

a Based on the first level of organization at which a unit is mandated to perform the investigations function.b UNRWA considers inspection to be investigation.c The Bureau of Programming and Management (PROGRAM) within ILO contains units responsible for all five internal oversight

functions, but it is the Internal Audit Unit within PROGRAM that has responsibility for audit, inspection and investigation.d As indicated in the proposed reforms of the UNESCO Director-General (160 EX/23 of 15 September 2000, para. 24).

8

C. Operational independence

32. It is well recognized that those responsible forinternal oversight must have operationalindependence in order to fulfil their duties. This isespecially true for those with responsibility forinvestigations in view of the sensitive matters ofteninvolved. Key elements of operational independencefor an investigations unit would include:

− autonomy in establishing a work plan, although itmay accept requests for investigations fromsenior management;

− the authority to initiate and carry out anyinvestigations it considers necessary to fulfil itsresponsibilities, without any hindrance or needfor prior clearance;

− the clear identification of the human andfinancial resources of the unit in the budget ofthe organization, with delegated authority tomanage those resources subject to overallpolicies and procedures of the organization;

− the right to direct and prompt access to allpersons engaged in activities under the authorityof the organization, and to their full cooperation;

− full, free and prompt access to all accounts,records, property, operations and functionswithin the organization that it believes arerelevant to the subject being investigated;

− authorization to encourage staff of theorganization to communicate directly with it on aconfidential basis regarding complaints orallegations of wrongdoing, irregularities orwaste, and to ensure that the staff would not besubject to reprisals provided there is no intentionto misinform; and

− the right to send copies of reports oninvestigations to the executive head and to theexternal auditor, and to the pertinent legislativeorgans when the unit deems appropriate.

33. There is a general understanding that thoseresponsible for internal oversight must not assumeoperational responsibilities for activities they areoverseeing, in order to avoid an actual or perceivedthreat to their objectivity.13 Application of this well-accepted standard for internal auditors to all of thoseconducting investigations in organizations of the

13 See Standards for the Professional Practice of InternalAuditing, The Institute of Internal Auditors (Altamonte Springs,Florida: 1997), p. 16.

United Nations system presents a problem, in view ofthe involvement of programme and administrativesupport managers in investigations, which isconsidered in section B of the following chapter.

D. Strong support from the executive head

34. As noted previously (paras. 9 and 10), there hasbeen a growing recognition of the need for aneffective investigations capability in United Nationsorganizations. Executive heads have shared in thiscultural change in the System and many are stronglysupportive of the role of internal oversight, and theinvestigations function in particular, for addressingthis need. For example, executive heads in someorganizations have sought to strengthen the role ofinternal oversight by creating an Office of InspectorGeneral, including the investigations function.14

Other executive heads, without establishing anInspector General, have made clear their personalsupport for an effective investigations function.

35. There was frequent reference by thoseinterviewed to the supportive attitude of theirexecutive heads regarding internal oversight servicesgenerally, and often the investigations functionespecially. In some cases this was manifest inbudgetary support for these services at a time ofactual budget reductions and/or zero nominal growthbudgets (e.g., United Nations, FAO, WFP, UNICEF).In some instances, however, recent funding crises andthe urgent need to revitalize programmes (e.g.,UNEP, UNCHS) have meant that internal oversighthas been accorded lower priority in the budgetaryprocess. Unless it is clear to all in an organizationthat the executive head believes in and supports theinvestigations function, it will be difficult forinvestigators to be effective.

E. Qualified investigators

36. Another important requirement is thatorganizations should employ, or at least have accessto, qualified investigators. For professionalinvestigator posts in United Nations systemorganizations, an advanced university degree in lawwould seem to be an optimal requirement, combinedwith further professional studies which might includespecific training in investigation skills andtechniques, attendance at courses such as those thatUnited Nations system staff have arranged at relevant

14 Offices of Inspector General have been created as follows:UNESCO, 1989 (changed to Internal Oversight Service in 2000);WFP, 1994; FAO, 1997; UNIDO, 1998 (changed to Office ofInternal Oversight and Evaluation in 2000); and UNHCR, 1999.In most cases, these dates mark the reorganization and/orenhancement of former oversight structures/offices.

9

national training facilities, participation in seminarsfor updating and refreshing skills, qualification as aCertified Fraud Examiner, etc. Formal trainingqualifications should be supported by several years ofinvestigatory experience, preferably in lawenforcement activities, and, for senior level posts,managerial and supervisory experience in aninvestigations environment. 37. Very few of the professional staff members whoconduct investigations in the organizations of theUnited Nations system have qualifications andexperience as outlined above. In the manyorganizations where the investigations function is notclearly separated from other internal oversightfunctions, job descriptions and/or classificationsmake only passing reference to the investigationsfunction and the requirement for some investigatoryexperience may be stated as “desirable”, if it is statedat all.

38. Within United Nations system internal oversightservices, use of the functional title "Investigator" (orsimilar) in job descriptions and/or classifications islimited to a small number of organizations(UN/OIOS, UNHCR, IAEA), and in these cases therequirements appear to have been met satisfactorily.

While the range of university degree subjectsrequired for these professional investigator posts isquite broad, the need for formal training in lawenforcement type investigation and/or forprofessional experience in investigatory work(prolonged at the senior levels) is clearly stipulated.In IS/OIOS, formal training in investigativetechniques is also required for the General Serviceinvestigation assistant.

39. In the other organizations, the oversightprofessionals who conduct investigations are, for themost part, qualified and experienced senior auditorswho are also, in some cases, Certified FraudExaminers. While some of these auditors haveparticipated in investigatory training, e.g., at theFederal Law Enforcement Training Center (FLETC),investigatory training and/or investigatory experiencedo not, in general, appear as prerequisites in their jobdescriptions and/or classifications. Meeting the needfor access to professionally trained and experiencedinvestigators is addressed further in section C of thechapter that follows.

10

IV. MAJOR ISSUES

40. The Executive Summary of this report containsrecommendations for dealing with a number of issuesthat need to be addressed in developing theinvestigations function within the United Nationssystem. These issues, some of which were flagged inchapter III, and the related recommendations, areexplained in this chapter.

A. Common standards and procedures

41. The lack of recognized standards and proceduresfor the conduct of investigations in United Nationsorganizations is a key issue to be resolved in thedevelopment of this important internal oversightfunction for the System. Fortunately, this is a matterof concern to the relevant officials and it wasdiscussed at the Second Conference of Investigatorsof United Nations Organizations and MultilateralFinancial Institutions in Rome, June 2000. At theconference, there was general acceptance of the needfor such standards and procedures, and for them to beharmonized or made common throughout the System.

42. Member State concern about an important aspectof this matter was expressed most recently in UnitedNations General Assembly resolution 54/244 of 31January 2000. This resolution stressed the need forprotecting the individual rights of staff, includingthose making reports to the investigators, and forensuring due process and fairness for all partiesconcerned in investigations. The General Assemblyrequested the Secretary-General to submit for itsconsideration and action “rules and procedures to beapplied for the investigation functions performed bythe Office of Internal Oversight Services, in order toensure fairness and avoid possible abuse in theinvestigation process”.15

43. Formally establishing – and issuing publicly –standards and procedures for conductinginvestigations would be an important step to take inthe development of the investigations function. Thiswould help to:

− improve the quality of investigations;

− ensure more consistency and rigour in theinvestigative process;

− set criteria for the use of outsourcing forinvestigations, making use of other organizationsas well as the private sector;

15 “Review of the implementation of General Assembly resolution48/218 B”, A/RES/54/244, 31 January 2000, paras. 16 and 17.

− increase throughout the organizations, includingmanagement, staff and Member States, anunderstanding of, and support for, the role andresponsibilities of those conductinginvestigations;

− give recognized legitimacy to investigativeactivities;

− provide a basis for evaluating the performance ofthe investigations function, and for holdinginvestigators accountable for their actions; andthereby

− ease resistance to the investigations functionamong staff members by giving reassuranceregarding its professionalism, and safeguardsagainst possible abuse in the investigativeprocess.

44. Having common standards and proceduresshared by all organizations of the System wouldcompound their value within each organization bygiving them a more generally recognized status. Thiswould also improve the effectiveness of inter-agencycooperation regarding specific investigations, andadd to the further development of the investigationsfunction overall within the System. Furthermore,since the Member States of all organizations in theSystem are essentially the same, the application ofsuch common standards and procedures throughoutthe System would enhance the governance process bybetter allowing Member States to make meaningfulcomparisons among organizations regarding theperformance of this internal oversight function andthe related resource requirements. Just one practicalexample of how the governance process would beimproved would be the development of a commonterminology regarding investigations among thedifferent organizations.

45. At the present time, reflecting the developmentalstage of the investigations function within theSystem, the approach to standards and procedures forinvestigations remains piecemeal. However, someorganizations have made significant initial efforts atdefining standards and procedures.16 In addition, the

16 In this regard, particular note should be taken of annex II, whichcontains an excerpt from the WMO Internal Audit Manual (issuedin August 1999) setting out principles followed by investigators inthe United Nations environment. Also relevant are: the sectionregarding the investigations function in the United Nationscontained in the Secretary-General’s Bulletin that establishedOIOS (ST/SGB/273 of 7 September 1994); the OIOSInvestigations Section Manual (which was first issued in February1997 and is now being updated); “Terms of reference and code of

11

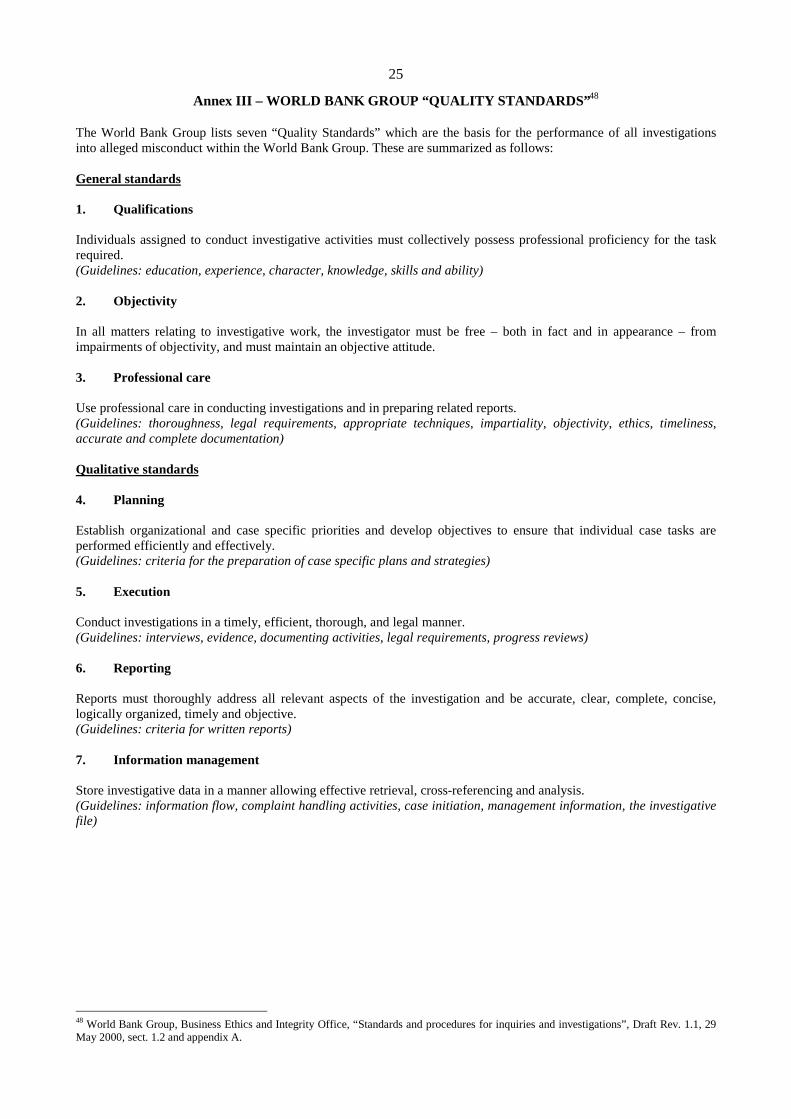

World Bank Group has recently published anextensive draft manual on standards and proceduresfor investigations, which was presented fordiscussion at the June 2000 conference ofinvestigators.17 Participants at the conference agreedthat the World Bank draft would be a helpful tool inefforts to adopt common standards, and the Bankagreed to facilitate the process. To prepare fordiscussion of proposed common standards at its nextsession, there was agreement at the conference thatsub-groups on this topic would be hosted by WMOand UNHCR for European-based organizations andby IS/OIOS for organizations based in the Americasand elsewhere.

46. Thus a good basis exists for formulating commonstandards and procedures for conductinginvestigations in United Nations systemorganizations, and there has been agreement on doingthis, at least in principle, among the professionalsresponsible for the function. Recommendation 1calls for a formal request to the 2001 conference ofinvestigators to make the necessary arrangements forgetting the job done, e.g., establishment of a workinggroup to prepare an agreed text for consideration andapproval at the following conference. Approval bythe conference would follow the model ofestablishing standards for the professional practice ofinternal auditing in United Nations organizations thatwere adopted in 1990 at the 20th Meeting ofRepresentatives of Internal Audit Services of theUnited Nations Organizations and MultilateralFinancial Institutions.18

B. The involvement of management in investi-gations

47. In discussing in section D of chapter II thefragmentation of responsibility for the investigationsfunction, attention was called to the fact thatmanagement officials of most United Nations

conduct of the Office of Inspector General” in the “InformationPackage” (undated) of the WFP Office of Inspector General(OEDI), paras. 13-19.

17 See World Bank Group “quality standards” in annex III.

18 It should be noted that it may be more difficult to reachagreement on procedures than on standards due to differing legalbases among the organizations. For example, an organization mayhave a regulation requiring that anyone suspected of wrongdoingbe informed immediately, which would preclude the practice ofmany organizations of conducting a preliminary investigation.However, while it may be necessary to separate agreement onstandards from agreement on procedures, agreement on bothshould still be the ultimate goal. Difficulties in reachingagreement on procedures would serve to point out differences inlegal bases among the organizations that it might be useful toharmonize.

organizations are authorized, and even mandated, toconduct investigations. While, as indicated below,this can risk compromising the effectiveness andprofessional quality of investigations, it is notpossible, or even desirable, fully to avoid theinvolvement of managers in conductinginvestigations. Thus, the issue here is not whethermanagement officials should be involved, but theneed for arrangements to reduce resulting problems.

48. Despite the prominence regarding investigationsin the United Nations now given to the InvestigationsSection of OIOS, documents that both predate(although still remaining in effect) and postdate theestablishment of OIOS make it clear thatmanagement officials also have responsibility forconducting investigations.19 In fact, even whenIS/OIOS conducts an investigation in the UnitedNations or its funds and programmes, it is alwaysconsidered to be “preliminary”20 in the sense thatdecisions on how then to proceed rest with theresponsible manager. The preliminary nature ofOIOS investigations was stressed to us in interviewsfor this report, by both the professional investigatorsof OIOS and the programme and administrativemanagers to whom OIOS submits the reports of itspreliminary investigations.

49. The role of managers in conductinginvestigations is also evident in the specializedagencies. Some examples are:

− ILO: the responsibility for initiatinginvestigations lies with the Treasurer andFinancial Comptroller, calling on the resourcesof the Financial Services Department, theRegional Administrative Services and theInternal Audit Unit.21

19 For example, para. 2 of “Revised disciplinary measures andprocedures”, Administrative Instruction to members of the stafffrom the Under-Secretary-General for Administration andManagement (ST/AI/371 of 2 August 1991) assigns investigationresponsibility to “the head of office or responsible officer” when astaff member appears to have engaged in conduct subject to adisciplinary measure. Also, para. 12 of “Follow-up report onmanagement irregularities causing financial losses to theOrganization”, Report of the Secretary-General (A/54/793 of 13March 2000), issued long after the establishment of OIOS,indicates that heads of departments/offices should investigateallegations of gross negligence since they are familiar withconducting investigations of misconduct.

20 The use of the word “preliminary” in this context certainly doesnot mean “superficial” or “casual”; a “preliminary” investigationby IS/OIOS will be as much in depth as required.

21 ILO’s written response to the JIU questionnaire, 5 July 2000. Inaddition, ILO has a Committee on Accountability, which, interalia, examines investigation cases referred to it by the Treasurerand Financial Comptroller, establishes the facts, and gives

12

− WHO: the mandate for the Office of InternalAudit and Oversight (IAO) says it “is the soleunit which will perform or authorize others toperform internal audits and oversightinvestigations”, but other documents assignresponsibility for investigations to a number ofmanagement officials as well.22

− WIPO: the Director General will designate theappropriate senior staff member to carry out aninvestigation and this is done on a case-by-casebasis.23

50. Since they usually lack professional training andexperience in investigative techniques, thisinvolvement of managers in conductinginvestigations could seriously risk problems such as:

− overlooking or losing significant evidence;

− improper handling of evidence so that it wouldbe inadmissible in a court or tribunal;

− violation of due process requirements; and/or

− compromising of efforts to gain recovery of lostfinancial assets.

51. In addition, there must always be a questionabout the independence and impartiality of a managerconducting an investigation in his or her own area ofresponsibility. There would be a natural inclinationfor managers to downplay the significance of anallegation and the loss to the organization in order tojustify taking care of problems on their own. Thiswould allow them to avoid disruptions to theirprogrammes that could result from calling in theinvestigators, as well as the associated negativepublicity that is likely to reflect badly on theirreputations as competent managers. At a more opportunity for all responsible officials to provide explanations.This Committee reports to the Director-General through theTreasurer and Financial Comptroller. It is chaired by the Directorof the Financial Services Department and includes onerepresentative each from the Financial Services Department, theOffice of the Legal Adviser and the Personnel Department, withthe Chief Internal Auditor or his representative attending in aconsultative capacity. See Circular No. 223, Series 2 of 17February 1998.

22 The IAO mandate is attached to WHO Information Circular No.69 on “Office of Internal Audit and Oversight (IAO)” (IC/96/69of 12 December 1996). For assignment of investigationresponsibility to other officials see paras. 310-345 and 490 of theWHO Manual and para. 12 of Information Circular No. 28 on‘Sexual Harassment” (IC/96/28 of 14 May 1996).

23 WIPO’s written response to the JIU questionnaire, 30 March2000.

serious level, of course, a manager who is implicatedin wrongdoing would endeavour to block enquiriesby professional investigators.

52. As noted previously, the involvement ofmanagers in conducting investigations at least in partpredates the new emphasis in the United Nationssystem on the need for a professional investigationscapability. Nevertheless, it is hard simply to divorcethe addressing of misconduct or wrongdoing from amanager’s overall responsibility and accountabilityfor the performance of staff assigned to his/her unit.When allegations arise, at least their initialinvestigation could be seen as a proper managementresponsibility. While all allegations must beaddressed, a senior manager would certainly beexpected to determine whether the allegedmisconduct and/or loss to the organization aresignificant enough to justify calling in investigatorsin view of the associated resource commitment.

53. Since there is inevitably a role for managers ininvestigations, they must be sufficiently trained in therecognized standards and procedures for conductinginvestigations in order to help minimize the risks tothe investigative process that could result from theirinvolvement in it. This is what is called for inRecommendation 2. Professional investigators withexperience in conducting investigations in UnitedNations organizations should be used for providingthis training so that it would be tailored to reflect thespecial environment and circumstances in whichUnited Nations organizations operate.

C. Meeting the need for a professional investi-gations capability

54. In assessing the adequacy of its investigationscapability, and deciding whether and whatimprovements should be made, an organization mustdetermine its need for professionally trained andexperienced investigators among its staff.Alternatively, it could consider other means (e.g.,inter-agency agreements, outsourcing) for gaining theaccess it requires to such a capability. A startingpoint for addressing this issue would be to conduct arisk profile of the organization to clarify its need foran investigations capability. This would provide aninitial basis for informed judgement, in view of theresource implications, about alternative institutionalarrangements for handling the investigationsfunction.

55. There are two important aspects to consider inpreparing a risk profile of an organization. Oneconcerns the risk factors of the organization, and theother concerns the quality of its internal controls.

13

56. How the organization is structured and the natureof its work would define the risk factors of anorganization. Potential risk factors to be consideredwould include the following:

− size of budget and staff;

− extensiveness of field operations;

− activities which entail large-scale and/or highvalue procurement by the organization;

− activities which, while not necessarily involvingsignificant expenditures by the organization, doentail major financial consequences for otherparties;

− engagement in emergency/crisis operations;

− degree of decentralization;

− extent of delegation of authority;

− programme delivery through implementingpartners.

57. Such risk factors tend to be more pronouncedand/or clustered together for some organizations,especially UNICEF, UNHCR, WFP and the UnitedNations Department of Peacekeeping Operations(DPKO). However, to varying degrees, at least someof these are important factors in the work andstructure of most other organizations of the System aswell.

58. It would be a mistake to feel complacent aboutthe need for an investigations capability inorganizations that are very much headquarters based,with no or only minimal field presence. Furthermore,while the nature of field operations may make themmore vulnerable to wrongdoing, the need also to payattention to headquarters must not be ignored. A caserecently concluded by IS/OIOS in UNCTADdemonstrates clearly that large-scale fraud can beperpetrated from headquarters.24 Indeed, as one highlevel official stressed in our interviews, there is aneed for an investigations capability at headquartersbecause that is where “the money” is in UnitedNations system organizations. Of course, investi-gations at headquarters could be required as well forother wrongdoing not directly related to “the money”,such as harassment, gross negligence, breach of

24 “Allegations of theft of funds by a United Nations Conferenceon Trade and Development staff member”, Note by the Secretary-General, A/53/811 of 28 January 1999.

confidentiality, failure to comply with professionalethical standards, etc.

59. Regarding the status of internal controls in anorganization, interviews for this report suggested thattheir quality would be enhanced by the extent towhich an organization is marked by elements such asthe following:

− a strong and widespread culture in theorganization of observing and practising internalcontrols;

− good and consistent internal audit of internalcontrols;

− effective examination by the external auditors ofthe internal audit of internal controls; and

− active concern by legislative bodies regarding theadequacy of internal controls.

60. Organizations with high-quality internal controlsand a low level of risk factors would obviously bemuch less vulnerable to wrongdoing than those withthe opposite characteristics. And organizations withboth characteristics high or both low would have adegree of vulnerability in between the extremes,although the vulnerabilities would be quite different.

61. However, human nature being what it is, it wouldclearly be unrealistic to believe that any organizationcould have such effective internal controls and such alow level of risk factors as simply to eliminate theneed for an investigations capability. Nevertheless,bearing this caution in mind, how an organizationrates itself in this regard would be relevant to itschoice of institutional arrangements for handling theinvestigations function.

62. For example, one high level official weinterviewed indicated the belief that, except for hisorganization’s participation in one inter-agency fieldprogramme, it has minimal exposure to risk factorssuch as those indicated above. He also stressed theeffectiveness of the organization’s internal controlmechanisms because of the extent to which it ismarked by the elements indicated above. As a result,he is sure that possibilities for wrongdoing in theorganization are quite restricted. Such a risk profilegives him confidence that the internal auditors in hisoffice have sufficient investigative skills to handlethe few cases (generally entitlements fraud) whicharise each year in the organization.

14

63. In this regard, that organization is consistent withthe practice of most others in the United Nationssystem which, as noted above, vest the mandate forinvestigations in their internal audit services.Whether this does appropriately reflect the actualsituation regarding risk factors and internal controlsis a judgement to be made for each organization.

64. There is at least some apparent overlap in theroles of internal auditors and investigators. Inparticular, both share a concern for fraud andcorruption, and both make use of much the sameinformation in pursuing this concern. However, inconsidering the use of auditors for the investigationsfunction, it is important to be aware of what somebelieve to be important differences between internalauditors and investigators:25

− Auditors are concerned with controls andsystems; Investigators are concerned with thebehaviour of individuals, seeing intent as the key.

− Auditors may uncover fraud and suspect thewrongdoer; Investigators have the skills,training, experience and mind-set to collect theevidence and prepare a case for presentation to atribunal or court.

− Auditors have limited flexibility since they facepredetermined audit plan commitments;Investigators are expected to be more reactive todevelopments, although they may still have toprioritize heavy caseloads.

− Auditors are increasingly seeking a more “user-friendly” image with participative audits andconsultant services for clients, which would beundermined if they were seen as potential“policemen”; Investigators can maintain a moredetached stance with both witnesses andsuspects.

− Auditors focus on matters involving financialimplications; Investigators are concerned withmany types of wrongdoing that have no financialimplications and fall outside the normal purviewof auditors (e.g., gross negligence, harassment,abuse of authority).

65. The assignment of the investigations function tointernal auditors was a matter addressed at the

25 The following are drawn in part from a table on “The differencebetween audit, inspection and investigation” presented by OIOS atthe Second Conference of Investigators of United NationsOrganizations and Multilateral Financial Institutions, Rome, 8-9June 2000.

conference of United Nations system investigatorsmentioned above. While some participants arguedthat the investigations function should be assigned tointernal auditors, it was indicated also that thiscombination of responsibilities just reflects in somecases the lack of other means within currentbudgetary constraints to meet the now increasedconcern in organizations for having an investigationscapability. There were also participants who arguedthat audit and investigation are quite differentfunctions, and that combining the two could have adetrimental effect on internal audit. In summarizingdiscussion of this item, the conference chairmanincluded the point that, regardless of the particularinstitutional arrangements, it was recognized thateach organization should have a professionalinvestigator capacity.

66. Within the context of the existing differences ofopinion about the matter, Recommendation 3 callsfor determining the institutional arrangements withineach organization to meet this agreed need for aprofessional investigations capability. Based on anorganization’s risk profile, again noting the cautionindicated in paragraph 61, each executive head wouldbe requested to issue a report to the appropriatelegislative organ on the organization’s need foraccess to professionally trained and experiencedinvestigators and to recommend measures necessaryto meet that need. While there will be differencesamong organizations regarding their needs for aprofessional investigations capability, and the bestway to meet those needs, these are issues that shouldbe clearly and openly examined by Member States ineach organization.

D. Financing investigations in small organi-zations

67. A major problem faced by small organizations –among both the specialized agencies and the UnitedNations funds and programmes – is that of budgetingfor the episodic nature of their need for a professionalinvestigations capability to deal with complicatedcases that are beyond the capacity of in-houseofficials. How can they justify the costs of having afull professional investigations capability alwaysavailable when the need for one is likely to be veryirregular compared with the more steady level ofneed that can be expected in large organizations?

68. The smaller United Nations funds andprogrammes make use of the Investigations Sectionof OIOS for meeting their need for access to aprofessional investigations capability. However, thereare problems in these current arrangements:

15

− Incomplete reimbursement. Since the UnitedNations regular budget is supposed to financeonly OIOS investigations related to regularbudget activities, services provided to the fundsand programmes should be reimbursed fromextra-budgetary funds.26 In practice, however,such reimbursements cover only the travel andper diem costs of OIOS investigators, with noreimbursement for direct salary and overheadcosts. 27

− Competing priorities. Especially since salary andoverhead costs are not reimbursed, the limitedresources and growing caseload of IS/OIOSmean that they may not be able to give thepriority to a request from a fund or programmethat the fund or programme believes is required.The resulting delay in response could lead to aloss of evidence and an undermining of thedeterrent effect of the investigations function.

− Reduced accountability of executive heads.Being subject to the priorities of an external unitregarding the handling of a matter that could beof critical importance to a fund or programmedetracts from the full accountability of theexecutive head for that fund or programme.28

− Limited independence. The need to negotiatereimbursement provisions for each case inadvance with fund or programme officials mustlimit the normal independence of IS/OIOS indetermining what cases to investigate, and whatarrangements to make for conducting suchinvestigations (e.g., sites to visit, staff to use).

69. Alternatives, not all mutually exclusive, for thefinancing by small organizations of access to aprofessional investigations capability could include:

26 Rather than reimbursement, direct allotments were made toOIOS from the budgets of the International Criminal Tribunal forRwanda and the International Criminal Tribunal for Yugoslaviafor travel related to investigations requested by the GeneralAssembly in 1996 and 1997.

27 In fact, not all funds and programmes have made such limitedreimbursement payments, e.g., UNEP. Regarding this, a seniorUNEP official observed that if the Programme were required toreimburse OIOS for investigation services, it would considersetting up its own in-house investigations capability, although itprobably did not have the required critical mass of cases to justifydoing so.

28 UNHCR officials especially stressed in interviews that it wouldbe wrong for the High Commissioner to rely entirely on OIOS forconducting investigations and hence to lose control over theprioritization of cases. They indicated that this is an importantreason why they established an investigations post in-house.

− Continued use of IS/OIOS by the small fundsand programmes, despite the problems indicatedin paragraph 68 above.

− The use of IS/OIOS also by the small specializedagencies through special contractualarrangements, again despite those problemsindicated above.

− Small agencies and funds and programmesjoining together, with the required critical massof cases, to establish an arrangement for sharedadvanced funding, rather than reimbursement.Mitigating the problems above, this would allowoptions such as:

• establishing a separate division of IS/OIOS,perhaps located in Geneva;

• creating an inter-agency investigations unitindependent of IS/OIOS;

• contracting out to the private sector for aprovider of investigation services.

− Establishing a roster of investigative experts inorganizations of the System to be called on asnecessary.

− Establishing a clearing-house of externalinvestigation services with which organizationshave had good experience.

70. Alternatives such as the above are what isexpected from Recommendation 4, which calls forthe executive heads of the small organizations topresent to their appropriate legislative organs optionsto ensure the access to professionally trained andexperienced investigators needed by theirorganizations.

E. Need for preventive measures to reducevulnerability

71. A distinction between reactive and proactiveinvestigations was noted earlier in paragraph 11. Onecannot dispute the need for proactive investigationsleading to the timely development andimplementation of preventive measures that wouldhelp avoid significant losses for an organization,disruptions to its operations, and the oftenconsiderable costs of conducting a reactiveinvestigation. In practice, however, the urgent toooften pre-empts the important, and thus priority isnormally given to reactive investigations whichcannot be ignored. For example, since IS/OIOS iscommitted to following up on all allegations ofwrongdoing reported to it, and the number of suchcases has risen sharply, IS/OIOS was able to

16

undertake only two proactive investigations in 1998-1999.

72. In smaller organizations, the caseload of reactiveinvestigations may be less onerous, allowing moretime for proactive work. The need for reactiveinvestigations within a specific unit is, by its nature,episodic. Thus, proactive investigations could beused by smaller organizations to fill relative lowpoints in activity and this may help them justify thecreation of an in-house professional investigationscapability. The Office of Inspector General of WFP(OEDI) provides a good example in this regard: it isestimated that about two thirds of OEDI’s efforts arefor reactive investigations and one third for proactiveinvestigations.

73. The distinction between reactive and proactiveinvestigation is by no means universal – or even clear– in the United Nations system. Definitions differ,and there may be a blurring at the edges betweenproactive investigation and the mandates of both theinspection function and the audit function. In WFP,for example, proactive examination of situations topre-empt risk is regarded as inspection, but inUNHCR, an inspection is a broad and systematicreview of performance that does not include the riskprofiling functions of a proactive investigation. Forseveral organizations (UNICEF, UNDP, ILO, FAO,IAEA and ICAO), the pertinent distinction isbetween proactive audit and reactive investigation,with the findings of the former, on occasion,triggering the latter. However, overlapping – orconflicting – definitions are not the real issue. Whatcounts is that processes are in place to assessvulnerabilities and profile risk, and to suggestcorrective actions in order to prevent incidents ofwrongdoing from occurring in the first place.

74. Closely related to this is the need for follow-up atthe conclusion of a reactive investigation to identify“lessons learned” regarding measures that should betaken to avoid similar incidents in the future. Everyinvestigation should result in the development oflessons learned regarding preventive measures for thefuture as well as regarding possible changes orimprovements in investigative techniques andmethodologies.29

75. Recommendation 5 calls for ensuring that thework programmes of investigations units include thedevelopment of preventive measures based on

29 In this regard, UNIDO places lessons learned frominvestigations on its INTRANET and this will soon be linked withsoftware to fulfil needs for tracking follow-up of all oversightrecommendations.

proactive investigations and lessons learned fromcompleted investigations.

F. Inter-agency cooperation

76. As noted previously, investigation is a relativelynew internal oversight function in the United Nationssystem, and provision for this function varies widelyamong the different organizations. A useful way toadvance its development would be through inter-agency cooperation. This is already being facilitatedactively through the annual Conference ofInvestigators of United Nations Organizations andMultilateral Financial Institutions, initiated by OIOSin 1999. The wider attendance at the secondconference indicates a growing interest in the subject,and is a mark of the success of the conferences. Alsoimportant are the regular contacts maintained by theprofessionals concerned with the investigationsfunction.

77. Some examples of areas for inter-agencycooperation would include:

− The development of common standards andprocedures for conducting investigations, ascalled for in Recommendation 1.