Embed Size (px)

Citation preview

Stronger growth, but risks loom large

Ángel Gurría OECD Secretary-General

Álvaro S. Pereira OECD Chief Economist ad interim

OECD ECONOMIC OUTLOOK

Paris, 30 May

Key messages • Global growth will be around 4%

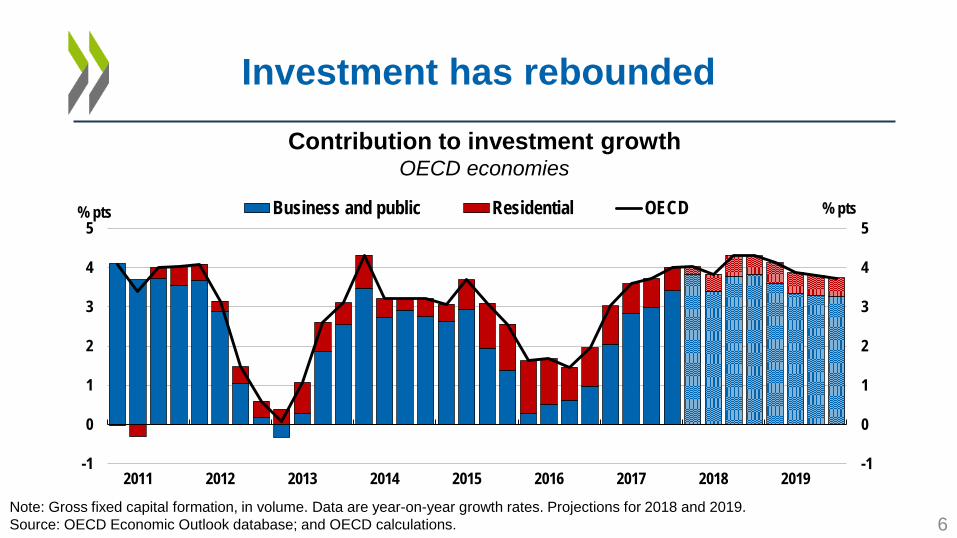

Investment and trade have rebounded

• Monetary and fiscal policies have been supportive Three quarters of OECD countries are undertaking fiscal easing

• Job growth has been strong The OECD unemployment rate will be at its lowest since 1980

• Risks loom large over the next few years: oil prices, trade tensions, financial volatility Rising interest rates will pose challenges for highly indebted countries, households and corporations.

• Now is the time to reform for sustainable and inclusive growth Invest in education, skills, digital infrastructure 2

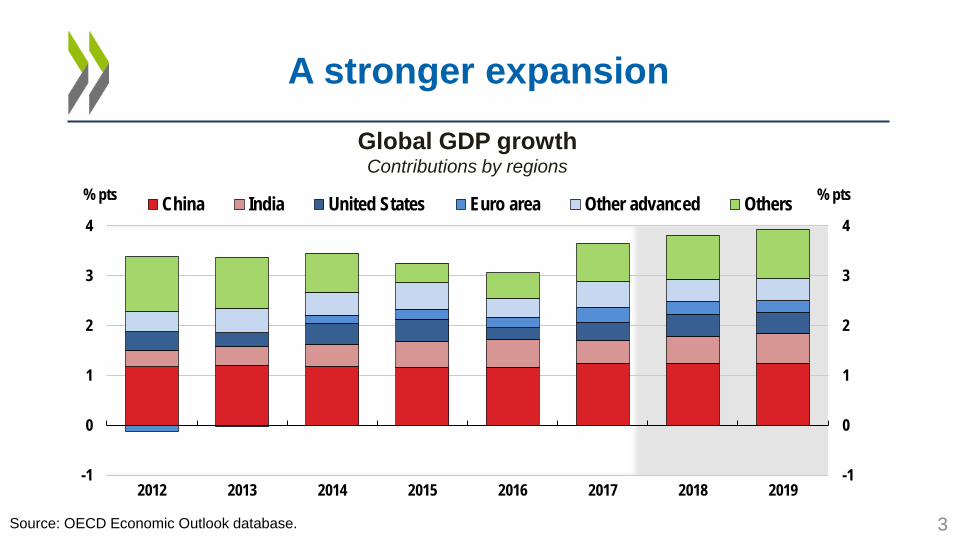

A stronger expansion

Global GDP growth Contributions by regions

Source: OECD Economic Outlook database.

-1

0

1

2

3

4

-1

0

1

2

3

4

2012 2013 2014 2015 2016 2017 2018 2019

% pts % pts China India United States Euro area Other advanced Others

3

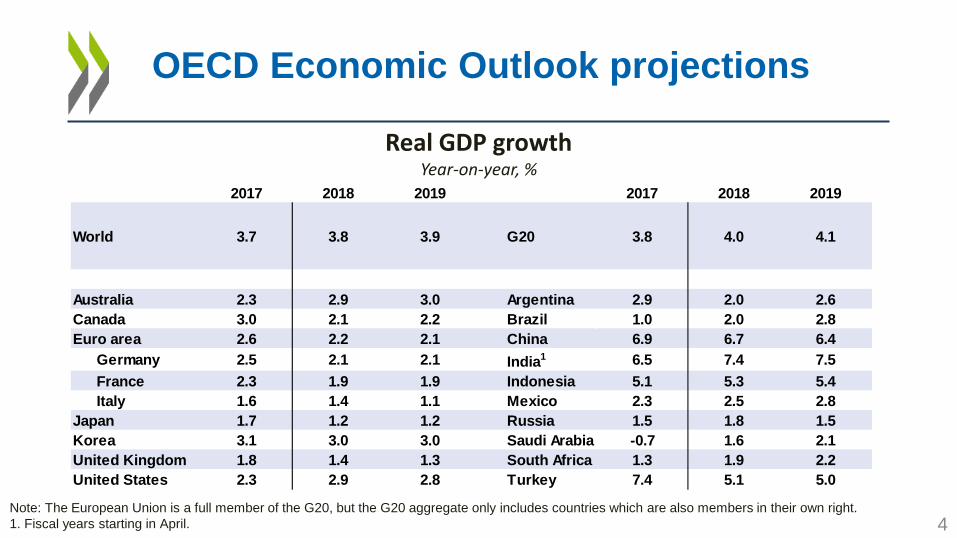

Real GDP growth Year-on-year, %

Note: The European Union is a full member of the G20, but the G20 aggregate only includes countries which are also members in their own right. 1. Fiscal years starting in April. 4

OECD Economic Outlook projections

2017 2018 2019 2017 2018 2019

World 3.7 3.8 3.9 G20 3.8 4.0 4.1

Australia 2.3 2.9 3.0 Argentina 2.9 2.0 2.6Canada 3.0 2.1 2.2 Brazil 1.0 2.0 2.8Euro area 2.6 2.2 2.1 China 6.9 6.7 6.4 Germany 2.5 2.1 2.1 India1 6.5 7.4 7.5 France 2.3 1.9 1.9 Indonesia 5.1 5.3 5.4 Italy 1.6 1.4 1.1 Mexico 2.3 2.5 2.8Japan 1.7 1.2 1.2 Russia 1.5 1.8 1.5Korea 3.1 3.0 3.0 Saudi Arabia -0.7 1.6 2.1United Kingdom 1.8 1.4 1.3 South Africa 1.3 1.9 2.2United States 2.3 2.9 2.8 Turkey 7.4 5.1 5.0

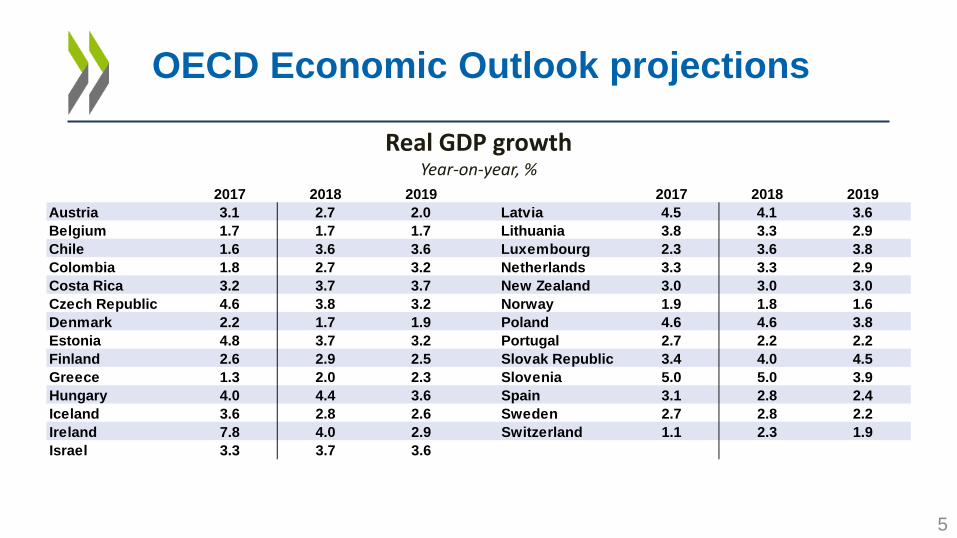

Real GDP growth Year-on-year, %

5

OECD Economic Outlook projections

2017 2018 2019 2017 2018 2019Austria 3.1 2.7 2.0 Latvia 4.5 4.1 3.6Belgium 1.7 1.7 1.7 Lithuania 3.8 3.3 2.9Chile 1.6 3.6 3.6 Luxembourg 2.3 3.6 3.8Colombia 1.8 2.7 3.2 Netherlands 3.3 3.3 2.9Costa Rica 3.2 3.7 3.7 New Zealand 3.0 3.0 3.0Czech Republic 4.6 3.8 3.2 Norway 1.9 1.8 1.6Denmark 2.2 1.7 1.9 Poland 4.6 4.6 3.8Estonia 4.8 3.7 3.2 Portugal 2.7 2.2 2.2Finland 2.6 2.9 2.5 Slovak Republic 3.4 4.0 4.5Greece 1.3 2.0 2.3 Slovenia 5.0 5.0 3.9Hungary 4.0 4.4 3.6 Spain 3.1 2.8 2.4Iceland 3.6 2.8 2.6 Sweden 2.7 2.8 2.2Ireland 7.8 4.0 2.9 Switzerland 1.1 2.3 1.9Israel 3.3 3.7 3.6

Investment has rebounded Contribution to investment growth

OECD economies

Note: Gross fixed capital formation, in volume. Data are year-on-year growth rates. Projections for 2018 and 2019. Source: OECD Economic Outlook database; and OECD calculations. 6

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2011 2012 2013 2014 2015 2016 2017 2018 2019

Business and public Residential OECD% pts % pts

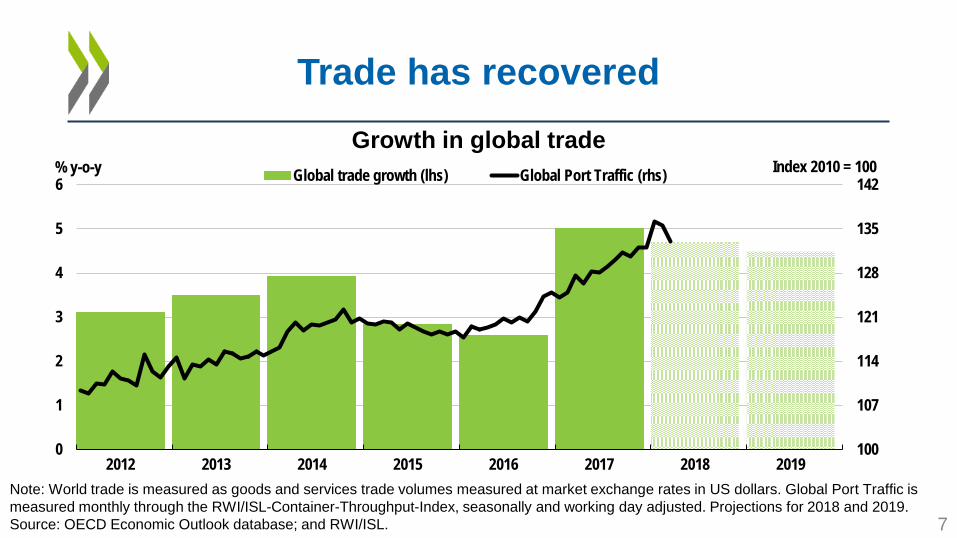

Trade has recovered Growth in global trade

Note: World trade is measured as goods and services trade volumes measured at market exchange rates in US dollars. Global Port Traffic is measured monthly through the RWI/ISL-Container-Throughput-Index, seasonally and working day adjusted. Projections for 2018 and 2019. Source: OECD Economic Outlook database; and RWI/ISL. 7

100

107

114

121

128

135

142

0

1

2

3

4

5

6

2012 2013 2014 2015 2016 2017 2018 2019

Index 2010 = 100 % y-o-y Global trade growth (lhs) Global Port Traffic (rhs)

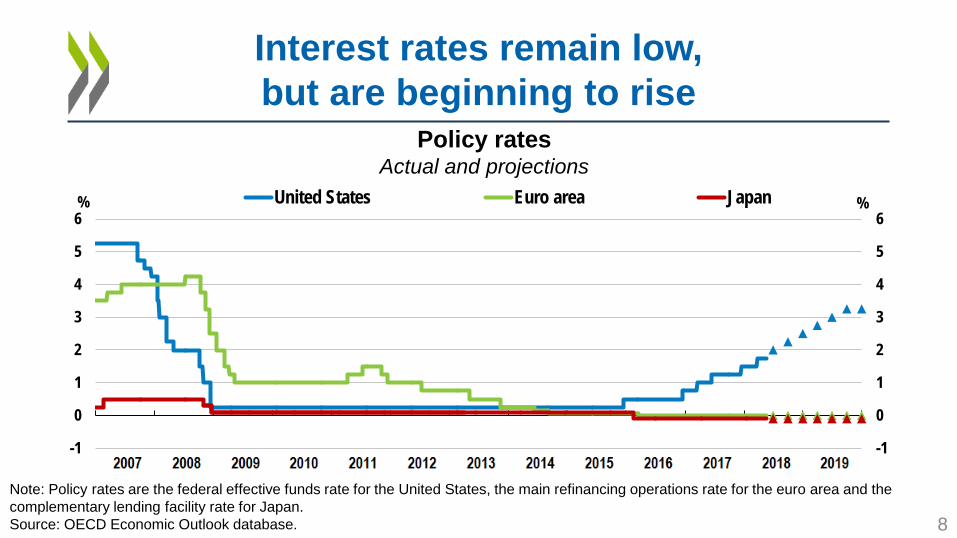

Interest rates remain low, but are beginning to rise

Policy rates Actual and projections

Note: Policy rates are the federal effective funds rate for the United States, the main refinancing operations rate for the euro area and the complementary lending facility rate for Japan. Source: OECD Economic Outlook database. 8

-1

0

1

2

3

4

5

6

-1

0

1

2

3

4

5

6United States Euro area Japan% %

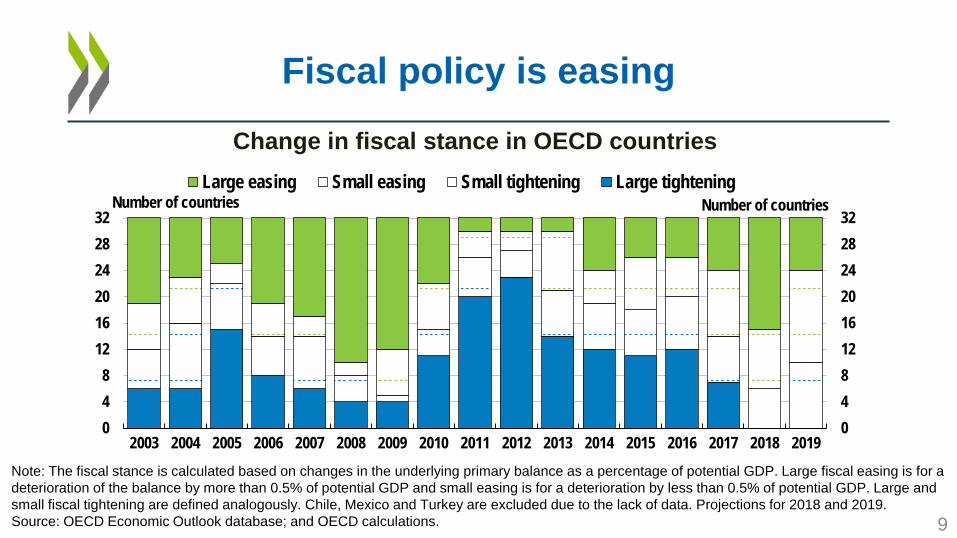

Note: The fiscal stance is calculated based on changes in the underlying primary balance as a percentage of potential GDP. Large fiscal easing is for a deterioration of the balance by more than 0.5% of potential GDP and small easing is for a deterioration by less than 0.5% of potential GDP. Large and small fiscal tightening are defined analogously. Chile, Mexico and Turkey are excluded due to the lack of data. Projections for 2018 and 2019. Source: OECD Economic Outlook database; and OECD calculations.

Change in fiscal stance in OECD countries

Fiscal policy is easing

048121620242832

048

121620242832

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Large easing Small easing Small tightening Large tighteningNumber of countries Number of countries

9

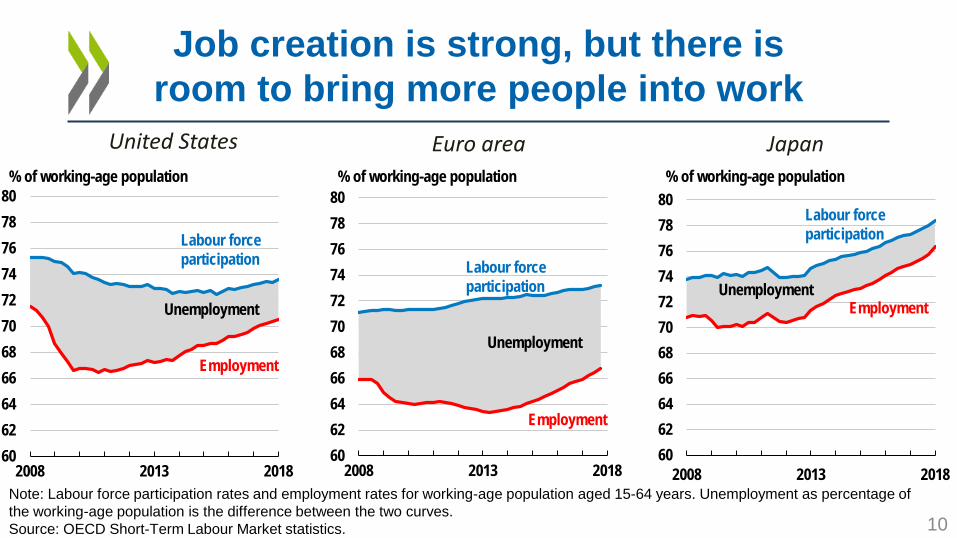

Note: Labour force participation rates and employment rates for working-age population aged 15-64 years. Unemployment as percentage of the working-age population is the difference between the two curves. Source: OECD Short-Term Labour Market statistics.

Job creation is strong, but there is room to bring more people into work

Euro area United States Japan

10

6062646668707274767880

2008 2013 2018

Unemployment

Employment

Labour force participation

% of working-age population

6062646668707274767880

2008 2013 2018

Unemployment Employment

Labour force participation

% of working-age population

6062646668707274767880

2008 2013 2018

Unemployment

Employment

Labour force participation

% of working-age population

0.00.20.40.60.81.01.21.41.61.82.0

0.00.20.40.60.81.01.21.41.61.82.0

United States Euro area Japan

1995-2007 2007-2017 2017-2019 (projected) % %

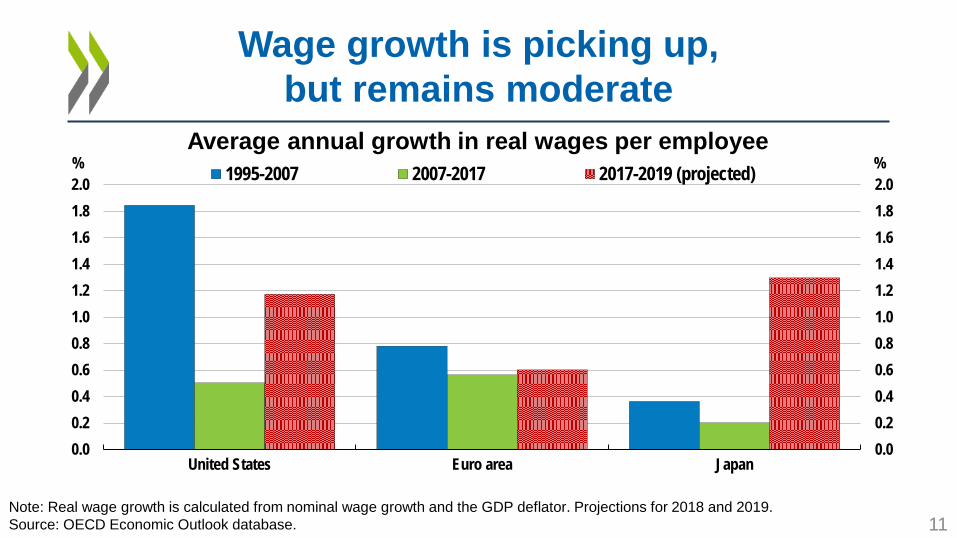

Wage growth is picking up, but remains moderate

Note: Real wage growth is calculated from nominal wage growth and the GDP deflator. Projections for 2018 and 2019. Source: OECD Economic Outlook database. 11

Average annual growth in real wages per employee

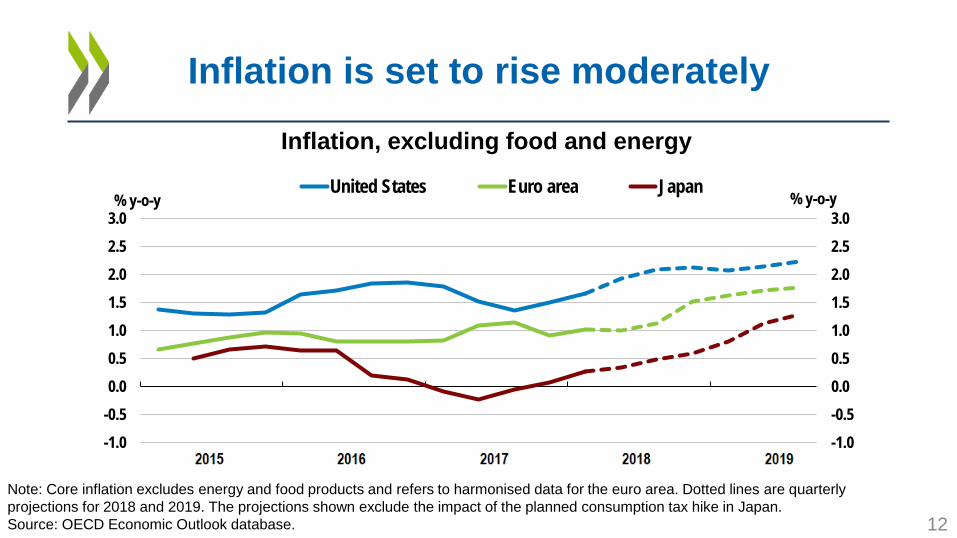

Inflation is set to rise moderately

Inflation, excluding food and energy

Note: Core inflation excludes energy and food products and refers to harmonised data for the euro area. Dotted lines are quarterly projections for 2018 and 2019. The projections shown exclude the impact of the planned consumption tax hike in Japan. Source: OECD Economic Outlook database. 12

-1.0-0.50.00.51.01.52.02.53.0

-1.0-0.50.00.51.01.52.02.53.0

United States Euro area Japan% y-o-y % y-o-y

RISKS LOOM LARGE

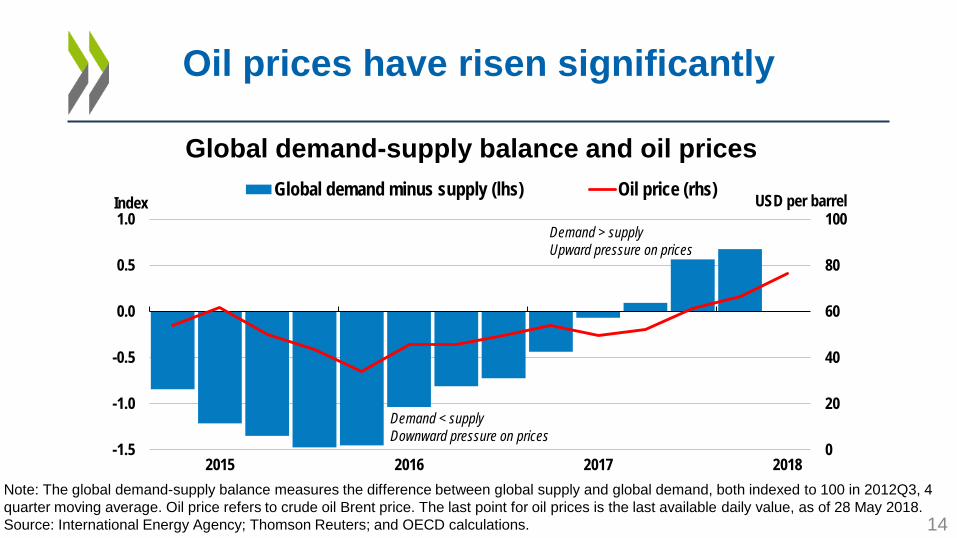

Global demand-supply balance and oil prices

Oil prices have risen significantly

Note: The global demand-supply balance measures the difference between global supply and global demand, both indexed to 100 in 2012Q3, 4 quarter moving average. Oil price refers to crude oil Brent price. The last point for oil prices is the last available daily value, as of 28 May 2018. Source: International Energy Agency; Thomson Reuters; and OECD calculations. 14

0

20

40

60

80

100

-1.5

-1.0

-0.5

0.0

0.5

1.0

2015 2016 2017 2018

Global demand minus supply (lhs) Oil price (rhs) USD per barrel Index

Demand < supply Downward pressure on prices

Demand > supply Upward pressure on prices

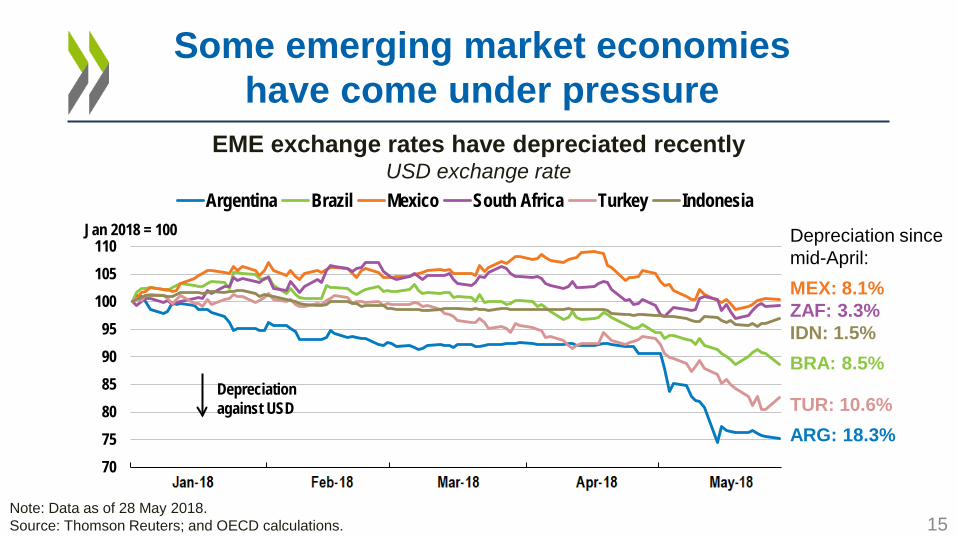

Some emerging market economies have come under pressure

EME exchange rates have depreciated recently USD exchange rate

Note: Data as of 28 May 2018. Source: Thomson Reuters; and OECD calculations.

Depreciation since mid-April: MEX: 8.1% ZAF: 3.3% IDN: 1.5% BRA: 8.5% TUR: 10.6% ARG: 18.3%

15

707580859095

100105110

Argentina Brazil Mexico South Africa Turkey IndonesiaJan 2018 = 100

Depreciation against USD

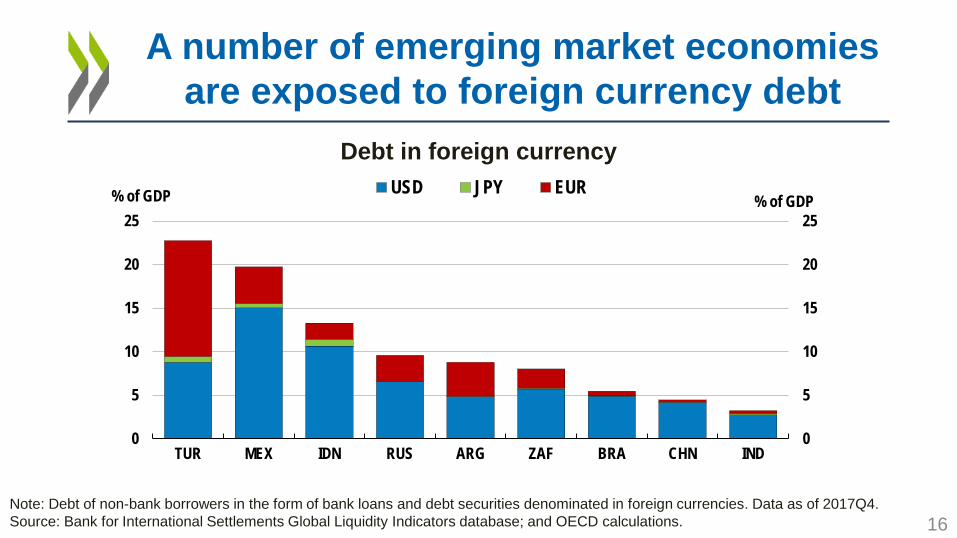

Debt in foreign currency

Note: Debt of non-bank borrowers in the form of bank loans and debt securities denominated in foreign currencies. Data as of 2017Q4. Source: Bank for International Settlements Global Liquidity Indicators database; and OECD calculations.

A number of emerging market economies are exposed to foreign currency debt

0

5

10

15

20

25

0

5

10

15

20

25

TUR MEX IDN RUS ARG ZAF BRA CHN IND

USD JPY EUR% of GDP % of GDP

16

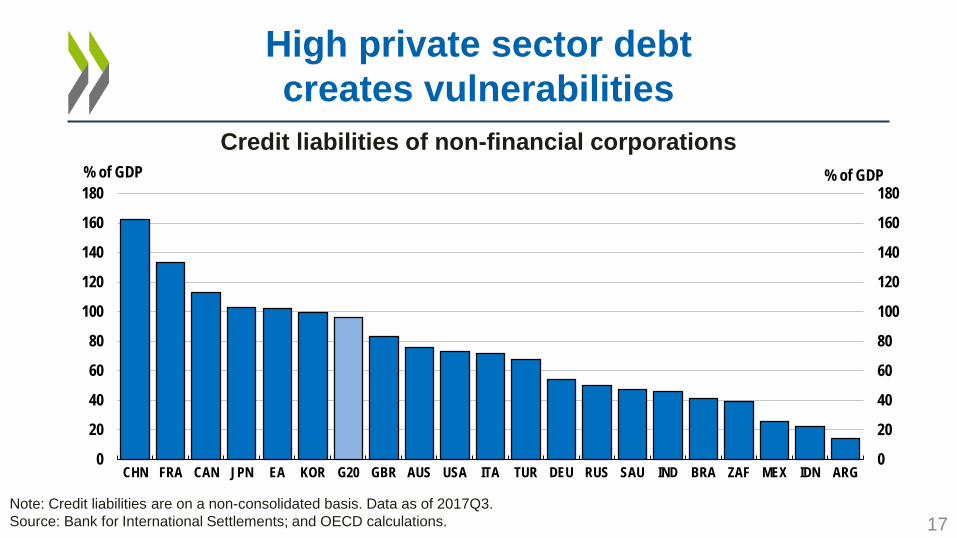

Note: Credit liabilities are on a non-consolidated basis. Data as of 2017Q3. Source: Bank for International Settlements; and OECD calculations.

High private sector debt creates vulnerabilities

Credit liabilities of non-financial corporations

17

0

20

40

60

80

100

120

140

160

180

0

20

40

60

80

100

120

140

160

180

CHN FRA CAN JPN EA KOR G20 GBR AUS USA ITA TUR DEU RUS SAU IND BRA ZAF MEX IDN ARG

% of GDP % of GDP

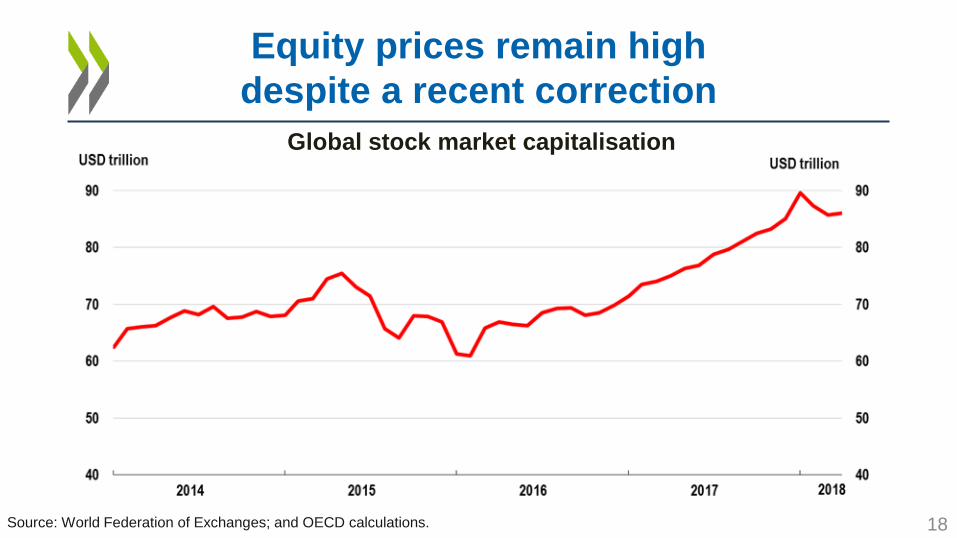

Global stock market capitalisation

Source: World Federation of Exchanges; and OECD calculations.

Equity prices remain high despite a recent correction

18

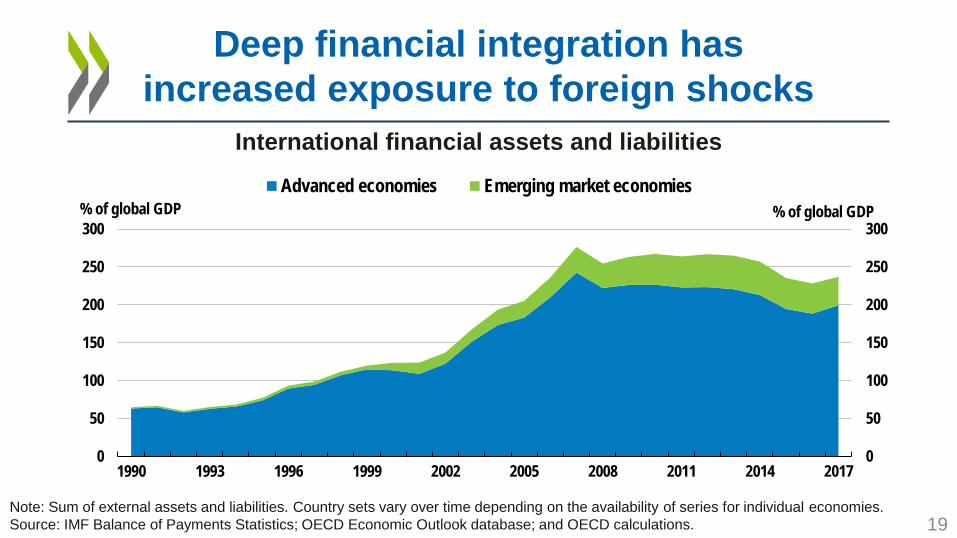

Deep financial integration has increased exposure to foreign shocks

International financial assets and liabilities

Note: Sum of external assets and liabilities. Country sets vary over time depending on the availability of series for individual economies. Source: IMF Balance of Payments Statistics; OECD Economic Outlook database; and OECD calculations. 19

0

50

100

150

200

250

300

0

50

100

150

200

250

300

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Advanced economies Emerging market economies% of global GDP % of global GDP

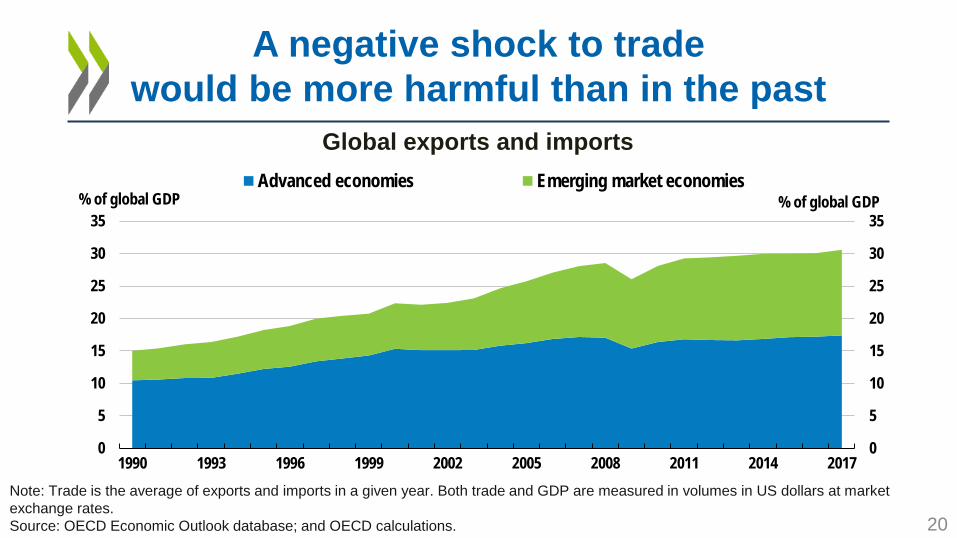

A negative shock to trade would be more harmful than in the past

Global exports and imports

Note: Trade is the average of exports and imports in a given year. Both trade and GDP are measured in volumes in US dollars at market exchange rates. Source: OECD Economic Outlook database; and OECD calculations. 20

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Advanced economies Emerging market economies% of global GDP % of global GDP

POLICIES TO MAKE GROWTH MORE SUSTAINED

AND INCLUSIVE

051015202530354045

05

1015202530354045

2011-12 2013-14 2015-16 2017 2011-12 2013-14 2015-16 2017

% %

In process of implementation

In process of implementation

Emerging market economies Advanced economies

Note: The estimated take-up of reforms is captured by the Going for Growth indicator of reform responsiveness. Fully coloured bars refer to the share of fully implemented reforms. For 2017, reforms in process of implementation are shown to ensure comparability with previous 2-year periods. Emerging market economies include Argentina, Brazil, Chile, China, Colombia, Costa Rica, Indonesia, India, Mexico, Russia, Turkey and South Africa. Advanced economies include all non-emerging OECD member countries and Lithuania. Source: OECD Going for Growth.

Step up structural reform ambition

22

Implementation of Going for Growth recommendations

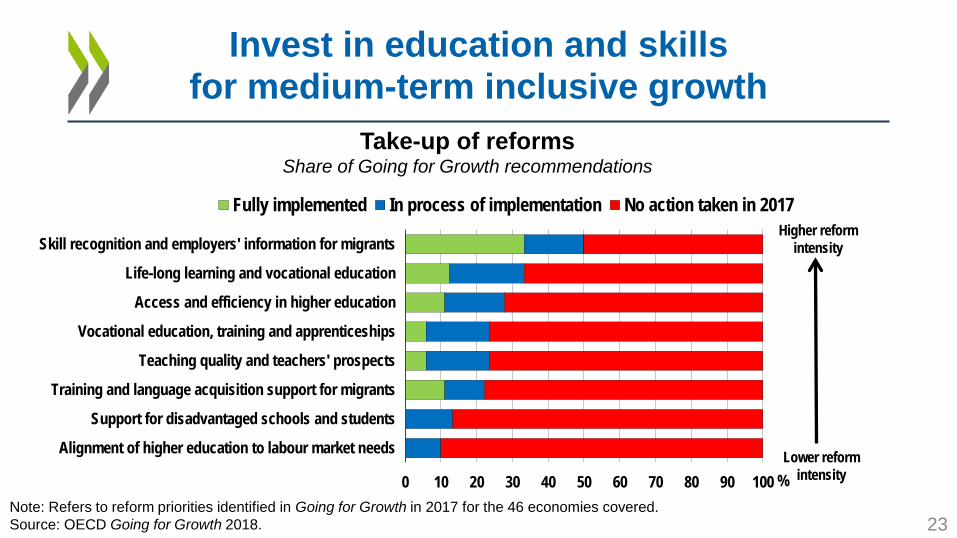

Invest in education and skills for medium-term inclusive growth

23 Note: Refers to reform priorities identified in Going for Growth in 2017 for the 46 economies covered. Source: OECD Going for Growth 2018.

Take-up of reforms Share of Going for Growth recommendations

0 10 20 30 40 50 60 70 80 90 100

Alignment of higher education to labour market needs

Support for disadvantaged schools and students

Training and language acquisition support for migrants

Teaching quality and teachers' prospects

Vocational education, training and apprenticeships

Access and efficiency in higher education

Life-long learning and vocational education

Skill recognition and employers' information for migrants

%

Fully implemented In process of implementation No action taken in 2017Higher reform

intensity

Lower reform intensity

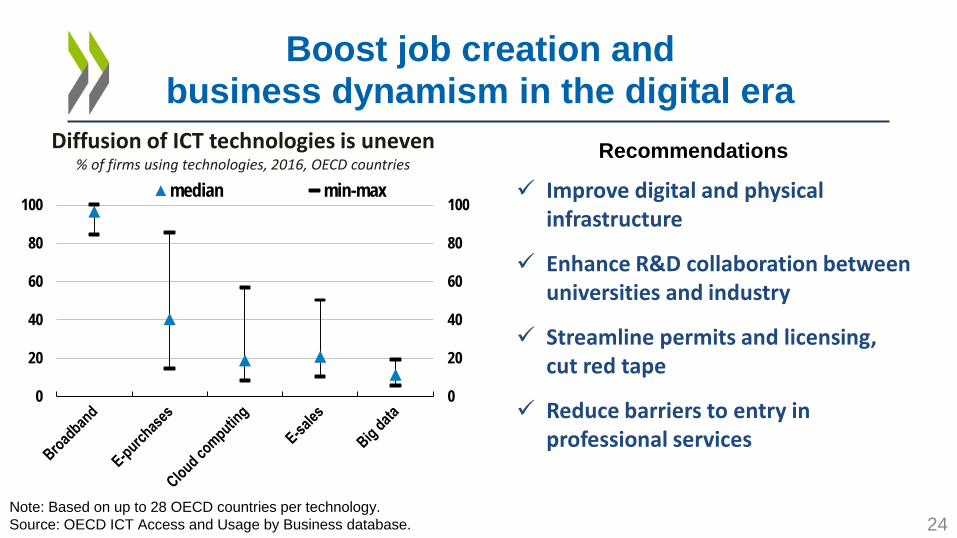

Boost job creation and business dynamism in the digital era

Note: Based on up to 28 OECD countries per technology. Source: OECD ICT Access and Usage by Business database.

Diffusion of ICT technologies is uneven % of firms using technologies, 2016, OECD countries

Improve digital and physical infrastructure

Enhance R&D collaboration between universities and industry

Streamline permits and licensing, cut red tape

Reduce barriers to entry in professional services

24

Recommendations

0

20

40

60

80

100

0

20

40

60

80

100median min-max

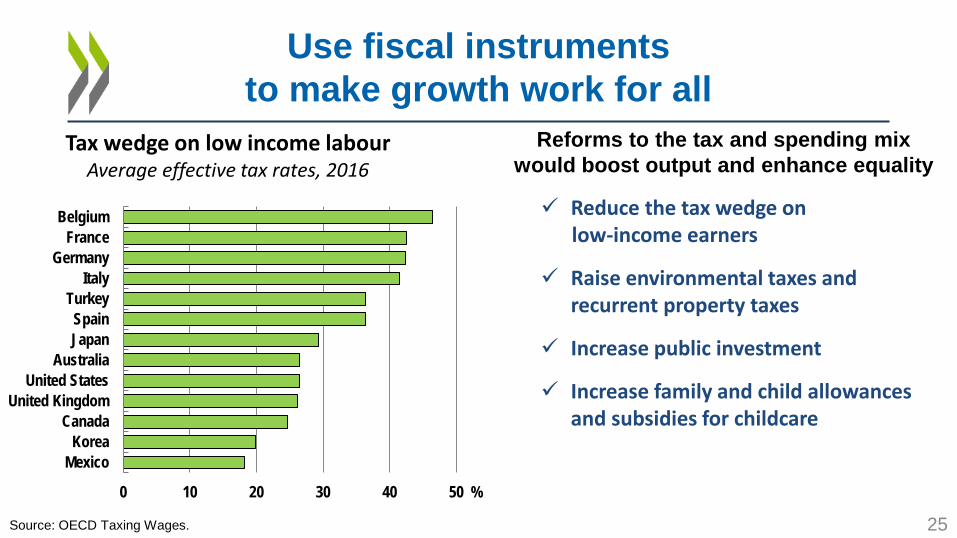

Source: OECD Taxing Wages.

Tax wedge on low income labour Average effective tax rates, 2016

Use fiscal instruments to make growth work for all

Reforms to the tax and spending mix would boost output and enhance equality

25

Reduce the tax wedge on low-income earners

Raise environmental taxes and recurrent property taxes

Increase public investment

Increase family and child allowances and subsidies for childcare

MexicoKorea

CanadaUnited Kingdom

United StatesAustralia

JapanSpain

TurkeyItaly

GermanyFrance

Belgium

0 10 20 30 40 50 %

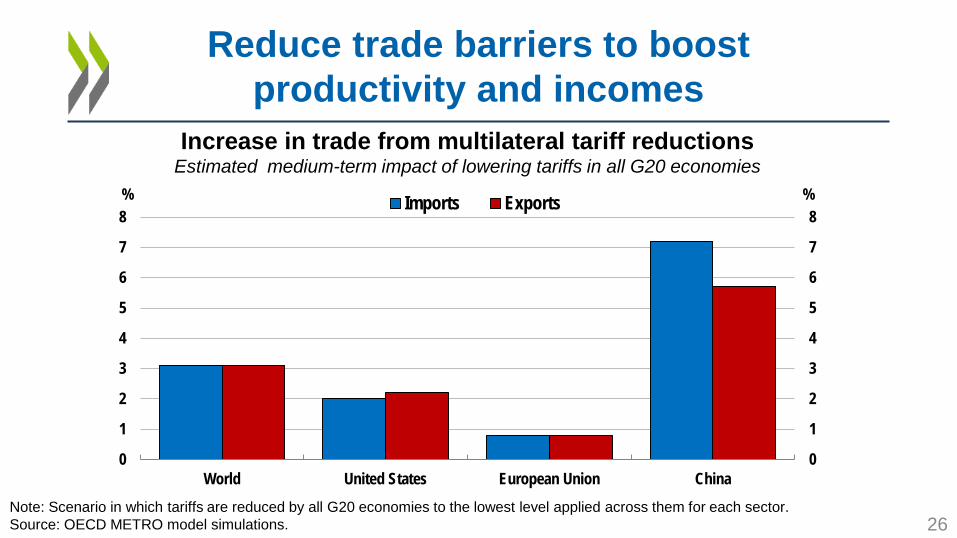

Reduce trade barriers to boost productivity and incomes

Note: Scenario in which tariffs are reduced by all G20 economies to the lowest level applied across them for each sector. Source: OECD METRO model simulations.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

World United States European Union China

% % Imports Exports

Increase in trade from multilateral tariff reductions Estimated medium-term impact of lowering tariffs in all G20 economies

26

Key messages • Global growth will be around 4%

Investment and trade have rebounded

• Monetary and fiscal policies have been supportive Three quarters of OECD countries are undertaking fiscal easing

• Job growth has been strong The OECD unemployment rate will be at its lowest since 1980

• Risks loom large over the next few years: oil prices, trade tensions, financial volatility Rising interest rates will pose challenges for highly indebted countries, households and corporations.

• Now is the time to reform for sustainable and inclusive growth Invest in education, skills, digital infrastructure 27