Embed Size (px)

Citation preview

Structuring Profits Interests as Equity Incentive Compensation for Key Employees and Service ProvidersDistribution Threshold, Vesting, Company Repurchase Rights, 83(b) Election, Rights of the Profits Interest Holder

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

WEDNESDAY, AUGUST 11, 2021

Presenting a live 90-minute webinar with interactive Q&A

David Howell, MBA, ASA, Principal, Plante & Moran, Chicago, IL

Joseph E. Hunt, IV, Attorney, Morse Barnes-Brown & Pendleton, Waltham, MA

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial 1-877-447-0294 and enter your Conference ID and PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the ‘Full Screen’ symbol located on the bottom right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the printer icon.

Recording our programs is not permitted. However, today's participants can order a recorded version of this event at a special attendee price. Please call Customer Service at 800-926-7926 ext.1 or visit Strafford’s website at www.straffordpub.com.

FOR LIVE EVENT ONLY

Structuring Profits Interests as Equity CompensationAugust 2021

Welcome and Introduction

• What is a profits interest?• Options and phantom arrangements• Tax, 409A, 83(b) elections, revenue rulings, safe harbor

provisions• Design, structure, and implementation• Q&A

6

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

About Our Speaker

Joe has nine years of advisory and legal experience, counseling startup, emerging, and middle-market companies throughout all stages of the entity life cycle, including formation, tax structuring, issuing equity, venture capital

financing, and mergers and acquisitions. His clients span a variety of different industries at all stages of corporate development, with a particular focus in serving technology and life sciences startup companies. Joe is a member

of the adjunct faculty at Boston University School of Law where he teaches in the Graduate Tax Program.

Joseph E. Hunt IV, J.D., LL.M.Senior Attorney

Morse

About David Howell

8

> Started career in corporate banking> Investment banking

> Valuation consulting> Valuation generalist

> Special expertise – equity compensation> PE / VC, private, public companies

•BA Economics, Northwestern University•MBA, Finance & Marketing, Kellogg, Northwestern University

•Taught undergraduate finance at Northwestern University•Published on valuation complex financial instruments

•Training and presentations•20 + years experience

David Howell, ASAPrincipal

Management ConsultingPlante Moran, Chicago

What I hope to provide

What is a profits interest?

9

10

Types of ownership interests in LLCs

• Capital interests• Profits interests• Carried interest• Options• Phantom shares• Warrants

11

What is a profits interest?

Unique form of equity ownership in private companies• Only LLCs and partnerships• Private equity, investor backed businesses, real estate• Incentive compensation – attract, retain, reward key

employees• Alternative to cash compensation• Flexible form, structure, names • Potential tax benefits• Can be complex and confusing

Characteristics of profits interests• Provided in exchange for services (no capital contribution)• Share of future value (some or all)

Income Appreciation Distributions Residual (exit value)

• Subject to safe harbor valuation threshold• Governed by shareholder, grant, plan agreements• Conditional: vesting, waterfall, other• Dilutive• Similar (but not same) economics as stock options or

appreciation rights

12

Safe Harbor Threshold:On the grant date, if the company was liquidated, the profits interests would receive no payout (value).

Example of Private Equity Waterfall

• Class A Preferred (Capital and preferred return)• Class B Preferred (Capital and preferred return)• Common Units• Derivative interests may include

Convertible interests Warrants Profits Interests

13

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Structuring Profits Interests as Equity Incentive Compensation

Joseph E. Hunt IV

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

II. Option to Acquire LLC Interests

• An LLC can issue options to a service provider to acquire either capital or profits interests; however, one may make more sense than the other.

• An LLC option is a contractual right held by the grantee to purchase an LLC interest at a fixed price in the future.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Capital Interest

• Generally, a service provider would not be subject to tax upon the grant of an option to acquire a capital interest.– The issuance of an option should not result in tax to

the service provider if the option does not have a readily ascertainable FMV at the time of grant.

– Beware though; if an option is deep in the money the Internal Revenue Service may characterize the option as ownership of the underlying LLC interest for tax purposes.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Capital Interest• Unlike corporations, LLCs taxed as partnerships cannot

issue incentive stock options (or their LLC equivalent. • Tax treatment for a compensatory non-qualified LLC option

should be like the corporate context:– Strike price at least equal to FMV on the date of grant (Yes, 409A

applies!)– Neither income to the grantee nor deduction to the LLC at grant– At exercise, grantee (1) pays the strike price to the LLC and (2)

recognizes ordinary income on the spread between the FMV of the interest received on the date of exercise and the strike price.

– The LLC will have a corresponding deduction equal to the income recognized by the grantee.

– Holding period for the grantee begins on the exercise date.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Capital Interest

• Section 721 (providing for tax free treatment to the grantee) may not apply.

• Additionally, it is unclear whether the exercise triggers a deemed transfer of cash, other assets, or some other capital shift to the grantee.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Profits Interest

• Similar to a capital interest, a service provider would not be subject to tax upon the grant of an option to acquire a profits interest.– The issuance of an option should not result in tax to

the service provider if the option does not have a readily ascertainable FMV at the time of grant.

• By definition a profits interest has a liquidation value of zero at the time of grant.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Profits Interest

• The exercise of an option to acquire a profits interest should have the same tax consequences as if the company had initially granted a profits interest.– The exercise of an option should not constitute a

taxable event for the grantee.– Since the receipt of a profits interest upon exercise of

the option should not constitute a taxable event, there should be no corresponding deduction for the LLC.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Option to Acquire Profits Interest

• While an LLC can issue an option to acquire a profits interest, just because you can doesn’t mean you should.– Why do grantees exercise options in the first

place?– Potential for a taxable capital shift.– Delayed holding period.– Availability of better alternatives

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

III. Phantom Arrangements

• What happens if an LLC wants to incentivize service providers without giving up a slice of real LLC equity? What if the LLC has elected to be taxed as an S-corporation and cannot issue a second class of equity?

• Enter the “phantom” equity arrangement.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Phantom Arrangements

• Phantom equity plan (or standalone phantom equity grants) replicate the issuance of actual equity without conferring any of the rights, privileges, and responsibilities of being a member of the LLC upon the grantee.

• Not risk free: Phantom equity plans should be designed as “unfunded, unsecured promises to pay” deferred compensation, and most comply with Section 409A.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Phantom Arrangements

• Can be structured to trigger a payment obligation only upon a liquidity event/change of control similar to a management carveout plan.

• Phantom Unit Rights– Right to payment upon a liquidity event equal to the value

of a unit of actual equity at the time of the event multiplied by the number of phantom units granted.

• Phantom Unit Appreciation Rights– Right to payment upon a liquidity event equal to the

spread between the price of actual equity at the liquidity event less the grant price, multiplied by the number of phantom units granted.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Phantom Arrangements

• Taxation for Service Provider:– Service provider not taxed upon the grant and should not

be treated as a member (no allocations of income, no rights to books and records, no voting rights, etc.)

– Upon exercise or settlement, the service provider will recognize compensation income taxable at ordinary income rates.

• Taxation for LLC:– Neither income nor gain recognized upon issuance of

phantom equity award.– LLC entitled to a corresponding deduction when the

phantom equity award is paid to the service provider.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

IV. Income Tax Consequences, Advantages, & Disadvantages

• From a tax perspective, the primary reason employers issue profits interests is that the grant of a profits interest does not result in taxable income to the grantee at the time of grant.

• The second tax reason to issue a profits interest is that since the profits interest represents true equity in an LLC, the later sale or redemption of the profits interest generally generates income taxable at favorable capital gains rates.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Income Tax Consequences, Advantages, & Disadvantages

• Unlike a capital interest, the transfer of a vested profits interest to a service provider is not a taxable event under Rev. Proc. 93-27.– By definition, a profits interest has no liquidation

value since upon grant it only entitles the service provider to share in future profits and appreciation, as opposed to a share in the existing assets of the partnership.

– However, the mere absence of a liquidation value does not imply that a profits interest is “worthless.”

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Income Tax Consequences, Advantages, & Disadvantages

• Unlike a capital interest, the transfer of a vested profits interest to a service provider is not a taxable event under Rev. Proc. 93-27.– By definition, a profits interest has no liquidation value since

upon grant it only entitles the service provider to share in future profits and appreciation, as opposed to a share in the existing assets of the partnership.

– However, the mere absence of a liquidation value does not imply that a profits interest is “worthless.”

• Rev. Proc. 2001-43 supplements Rev. Proc. 93-27 by clarifying that whether an interest granted to a service provider is a profits interest is determined as of the time of grant, even if the interest is substantially nonvested.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Income Tax Consequences, Advantages, & Disadvantages

• Taxation of a Vested Profits Interest– The receipt of a vested profits interest by a grantee in

consideration for services rendered is not a taxable event so long as the requirements of Rev. Proc. 93-27 are satisfied.

– No gain, loss, or deduction for either the LLC or the existing members is allowed upon the grant of a vested profits interest.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Income Tax Consequences, Advantages, & Disadvantages

• Taxation of an Unvested Profits Interest– Neither the grant nor subsequent vesting of a profits

interest is taxable to the grantee, so long as the requirements of Rev. Proc. 2001-43 are satisfied.

– Many practitioners recommend making a “protective” 83(b) election in the event the intended profits interest grant is later determined to be a capital interest or if there is risk that the requirements of Rev. Proc. 2001-43 and 93-27 will not be satisfied.

– No gain, loss, or deduction for either the LLC or the existing members is allowed upon the grant or vesting of an unvested profits interest.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Profits Interests – Exit Taxation• A profits interest is a capital asset (even if not a capital interest)

in the partnership.• The holding period for a profits interest begins on the date the

interest is no longer subject to a substantial risk of forfeiture (or the date an IRC Section 83(b) election is made).

• Partnerships are “passthrough” entities – not only do items of income and loss pass through the entity to the partners, but the passthrough items retain the character that they would have had in the hands of the entity.– This can produce situations where gain on the sale of partnership

interest does not result produce long term capital gains (“LTCG”) with respect to the sale amount.

– In a sale of a partnership where the partner is selling his ratable portion of hot assets (such as unrealized receivables, inventory, or depreciation recapture), a portion of the proceeds are OI instead of CG.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

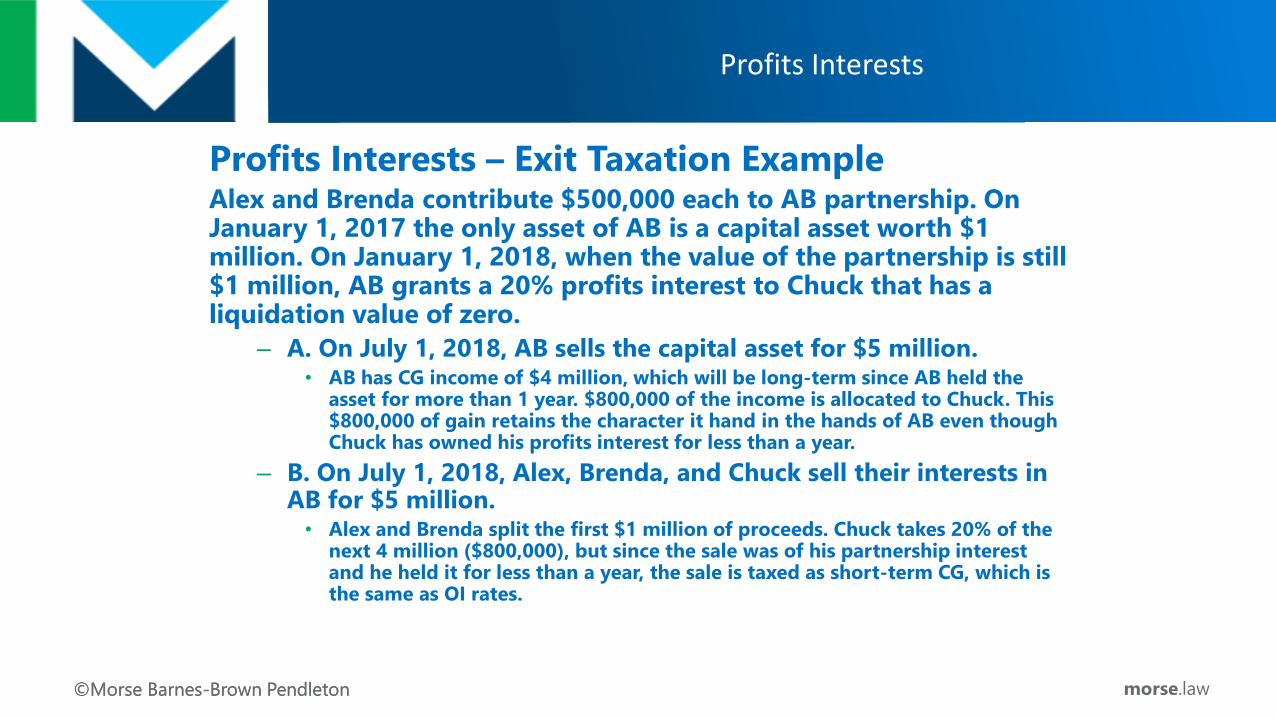

Profits Interests – Exit Taxation ExampleAlex and Brenda contribute $500,000 each to AB partnership. On January 1, 2017 the only asset of AB is a capital asset worth $1 million. On January 1, 2018, when the value of the partnership is still $1 million, AB grants a 20% profits interest to Chuck that has a liquidation value of zero.

– A. On July 1, 2018, AB sells the capital asset for $5 million.• AB has CG income of $4 million, which will be long-term since AB held the

asset for more than 1 year. $800,000 of the income is allocated to Chuck. This $800,000 of gain retains the character it hand in the hands of AB even though Chuck has owned his profits interest for less than a year.

– B. On July 1, 2018, Alex, Brenda, and Chuck sell their interests in AB for $5 million.

• Alex and Brenda split the first $1 million of proceeds. Chuck takes 20% of the next 4 million ($800,000), but since the sale was of his partnership interest and he held it for less than a year, the sale is taxed as short-term CG, which is the same as OI rates.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Profits Interests – Forfeiture Considerations• Rev. Proc. 2001-43 does not address the

forfeiture of an unvested profits interest.• Treas. Reg. Sec. 1.83-2(a) limits a service

provider’s loss upon the forfeiture of property following an IRC Section 83(b) election to the excess of the amount paid for the interest over any amount realized on forfeiture.– Consider that since a profits interest has a liquidation

value of zero, if a service provider makes a protective Section 83(b) election and forfeits the interest, the forfeiture loss limitation is likely to be zero.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Profits Interests – Other Considerations• The receipt of a profits interest causes the

service provider to cease being classified as an employee.– Amounts paid as compensation to a partner are

reported on Schedule K-1 as guaranteed payments rather than Form W-2 employment income.

– Amounts paid as compensation to a partner are no longer subject to income tax withholding by the entity but are instead subject to self-employment tax paid by the partner through estimated quarterly tax payments.

Profits Interests

©Morse Barnes-Brown Pendleton morse.law©Morse Barnes-Brown Pendleton

Profits Interests – Other Considerations• LLCs taxed as S-corporations cannot issue

profits interests.– An S-corporation is only allowed to have one class of stock (with

the same economic rights).– Since a profits interest only grants the recipient the right to share

in future profits and appreciation of the equity, a profits interest would grant a different economic right and violate the restriction against more than one class of equity.

– Attempting to grant a profits interest in an LLC taxed as an S-corporation can have nasty side effects, such as the service provider recognizing OI on the grant of what would be construed as a capital interest, or…

– …a blown S election.

Profits Interests

Design, structure, implementation

36

Design Considerations

37

• Business objectives and goals: income and value creation

• Participation – narrow or broad• Long term vs. short term incentive• Coordinate with cash comp (salary, bonus, perks)

strategy• Dilution / reasonableness / fairness• Vesting conditions• Departures from service, put/call, buy/sell, transfers• Thresholds Key Action: Establish and

document the threshold for each grant

Surprise!

38

• Financial reporting (GAAP) requirements• Equity or liability treatment• Income statement• Balance sheet• Footnote disclosures

• Fair market value (tax) versus fair value (accounting)

• Valuation requirements• Methods

The fair value of a profits interest for financial

reporting is almost never $0

Financial reporting requirements

39

• Valuation and reporting requirements• Issuance date• Ongoing

• One and done, or• Liability: mark to market until settled

• Valuation• Tax $0 (if comply with safe-harbor

provisions)• GAAP – almost never zero• GAAP does not impact tax

Financial reporting for profits interests impact net income, EBITDA, balance

sheet, loan covenants, disclosures, GAAP

compliance.

40

Professional Guidance – Financial Reporting for Profits Interests

Accounting• ASC 718 (f/k/a 123R) – share based payments

Valuation• “AICPA -Valuation of Privately-Held-Company

Equity Securities Issued as Compensation” issued 2013

• “AICPA - Valuation of Portfolio Company Investments of Venture Capital and Private Equity Funds and Other Investment Companies” issued 2019 Define requirements,

methods, and best practices

Professionally accepted methods to value profits interests

• Option methods address uncertainty, risk, potential future value Black Scholes Monte Carlo

• Scenario based methods• Intrinsic method

41

Financial reporting considers the potential for future value creation that is the goal of

equity based compensation

Q&A

42