Embed Size (px)

Citation preview

WOODSTOCK INSTITUTE | OCTOBER 2014

October 9, 2014

Student debt: what’s the

problem?

Katie Buitrago | Senior Policy and Communications Associate

Woodstock Institute | Chicago, Illinois

P 312.368.0310 | F 312.368.0316

@woodstockinst

WoodstockInstitute

Why does student loan debt matter?

• It’s not just a debt problem—it’s a repayment problem

• Return on investment in education and credentials

• The difference between a surgeon with $200,000 of

debt and a nursing school dropout with $15,000 of debt

• Student debt without credentials and skills

un- and underemployment + unmanageable debt burden

WOODSTOCK INSTITUTE | OCTOBER 2014

Why does student loan debt matter?

• Impact on the broader economy

Unaffordable student debt

Low discretionary

income

Delayed household formation

WOODSTOCK INSTITUTE | OCTOBER 2014

Why does student loan debt matter?

• Impact on long-term future well-being

Unaffordable student debt

Low savings Retirement

disaster

WOODSTOCK INSTITUTE | OCTOBER 2014

Threat on the horizon:

Growing racial wealth gap

• Limited wealth-building options beyond home equity

and retirement savings

•Homeownership rate for adults under 35 is at lowest

level since 1982 (36.2%)

•Adults 40 and younger lost 30% of net wealth in Great

Recession

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit colleges particularly problematic

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit market overview

• Percent of undergraduates enrolled in for-profit

colleges:

• 2000: 4.6 percent

• 2012: 10.3 percent

• Revenues of 4-year for-profit schools grew nearly 800

percent from 2000 to 2012

• Student body:

•24.2 percent African American, 15.7 percent Latino;

50 percent low income

WOODSTOCK INSTITUTE | OCTOBER 2014

Cost of for-profit colleges

• On average, a year of college at for-profit school cost

$15,130 in 2013-2014

• Tuition and fees at public two-year school:

21 percent of for-profit T&F

• Tuition and fees at public four-year school:

59 percent of for-profit T&F

WOODSTOCK INSTITUTE | OCTOBER 2014

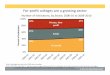

For-profit colleges cost more for low-income

students

$8,065

$11,854

$19,359

$24,173

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Public two-year Public four-year Private non-profit Private for-profit

Net cost of attendance for students in lowest income quartile, 2011-2012

WOODSTOCK INSTITUTE | OCTOBER 2014

Students are more likely to borrow at for-

profit colleges than at other colleges

1.32% 1.98% 4.08% 9.93%

35.76%

62.81%

58.84%

25.28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

All other colleges Private for-profit

Proportion of students who received federal and private loans at for-profit and other colleges, 2011-2012 academic year

No loans received

Non-private loans only

Both non-private and private loans

Private loans only

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

African American students most likely to

borrow relative to other racial groups

72.7

7%

78.0

1%

76.0

9%

68.6

6%

42.3

5%

48.5

4%

31.5

8%

32.6

0%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

White African American

Latino Asian

Percentage of students at for-profit and other colleges who borrow, by race, 2011-2012 academic year

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

Students at private for-profits are more likely

to take out private student loans

10.9

1%

11.4

6%

14.3

1%

12.8

7%

6.0

9%

4.6

0%

3.6

7%

4.3

9%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

White African American

Latino Asian

Percentage of students at for-profit and other colleges who take out private loans, by race, 2011-2012 academic year

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit students of all races are more likely

to have borrowed during their college career

85.8

0%

90.6

7%

89.2

9%

93.7

6%

66.3

0%

86.2

7%

72.2

8%

55.6

4%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

White African American

Latino Asian

Percentage of graduating seniors pursuing a BA in 2011-2012 who borrowed during their programs

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit students are more likely to borrow non-

federal loans at some point in their college career

38.1

9%

45.7

4%

43.2

3%

45.5

8%

28.8

7%

30.1

0%

29.6

3%

22.3

4%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

White African American

Latino Asian

Percentage of graduating seniors who borrowed non-federal loans during their programs

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

Students of all races borrow more money over the

course of their college career at private for-profits

$40,0

14

$39,3

40

$39,7

22

$40,7

41

$27,6

06

$31,5

21

$28,7

84

$20,7

87

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

White African American

Latino Asian

Cumulative amount borrowed for graduating seniors pursuing a BA who borrow, by for-profit attendance and race

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit students borrow a greater amount of

federal loans over course of college careers

$35,5

11.8

9

$32,6

79.6

7

$36,1

37.7

9

$35,0

85.6

2

$22,3

75.3

0

$27,8

58.1

3

$22,1

32.0

4

$19,2

21.2

4

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

$35,000.00

$40,000.00

White African American

Latino Asian

Cumulative federal loans borrowed ever for graduating seniors (BA) who borrow federal loans, by for-profit attendance and race

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

Amounts of non-federal loans borrowed vary by

race and for-profit attendance

$10,1

44.9

1

$13,2

76.4

5

$10,2

04.7

2

$11,6

34.2

6

$13,8

72.9

7

$11,5

93.9

9

$17,8

00.6

1

$6,3

99.6

8

$0.00

$2,000.00

$4,000.00

$6,000.00

$8,000.00

$10,000.00

$12,000.00

$14,000.00

$16,000.00

$18,000.00

$20,000.00

White African American

Latino Asian

Cumulative non-federal loans borrowed ever for graduating seniors pursuing a BA who borrow non-federal loans, by for-profit

attendance and race

Attends private for-profit

Does not attend private for-profit

Source: Woodstock Institute analysis of 2012

National Postsecondary Student Aid Survey

WOODSTOCK INSTITUTE | OCTOBER 2014

Outcomes of for-profit college students

55.7

64.6

54.8

33.6

37.4

44

37.2

27.3

48.3

60.2

45.6

42.8

60

67.4

58.3

39.4

0

10

20

30

40

50

60

70

80

Total 4 year-institutions

Private nonprofit Public Private for-profit

Graduation rates of full-time, first-year students by race/ethnicity and institution type (cohorts: 2006 and 2009)

Overall

African American

Latino

White

WOODSTOCK INSTITUTE | OCTOBER 2014

Source: College Board

For-profit college students are more likely to

default on their loans

• For-profit institutions accounted for:

• 11% of all students enrolled in 2009-10

• 32% of those who entered repayment in 2010-11

• 43% of those who defaulted by the end of September

2012

WOODSTOCK INSTITUTE | OCTOBER 2014

For-profit problems in Illinois

• Westwood College

• Sued by Attorney General Lisa Madigan in 2012

• Broken promises about law enforcement job

opportunities

• Students accumulate debt loads of $50,000 - $70,000

• Misrepresented costs of attendance, terms of in-

house loans

WOODSTOCK INSTITUTE | OCTOBER 2014

Potential Solutions

• Loan reforms

• Bankruptcy discharge

• Allow refinances at current federal rate

• Repayment options for students struggling to repay

private student loans

• School certification of private student loan need

WOODSTOCK INSTITUTE | OCTOBER 2014

Potential Solutions

• School reforms

• Reduce revenue schools can obtain through federal

aid from 90 to 85 percent

• Establish strong rules limiting federal aid to schools

who produce students unable to repay their loans

• Separate grants and scholarships from work, student

loans, and parent loans on costs sheets

WOODSTOCK INSTITUTE | OCTOBER 2014

Potential Solutions

• Enact and enforce consumer protections from debt

settlement and financial aid vendors, student loan

servicers

• Enforcement actions from AG, CFPB

• Consent orders from prudential regulators

• Servicing standards

• We need better data

•Children’s savings accounts

WOODSTOCK INSTITUTE | OCTOBER 2014

WOODSTOCK INSTITUTE | OCTOBER 2014

October 9, 2014

Student debt: what’s the

problem?

Katie Buitrago | Senior Policy and Communications Associate

Woodstock Institute | Chicago, Illinois

P 312.368.0310 | F 312.368.0316

@woodstockinst

WoodstockInstitute

![All India Private Colleges Pre-Medical Test [PC-PMT - … of Private Medical & Dental Colleges of Rajasthan All India Private Colleges Pre-Medical Test [PC-PMT - 2015] ACADEMIC YEAR](https://img.pdfslide.net/doc/110x75/5aa11f937f8b9a80378b48be/all-india-private-colleges-pre-medical-test-pc-pmt-of-private-medical-dental.jpg)