Embed Size (px)

Citation preview

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 1/64

INTRODUCTION

CAPITAL MARKET

Capital Market is an essential pre-requisite for industrial and commercial

development of a country. Credit is generally required and supplied on short term and long

term basis. The money market caters to the short term needs only.

Capital market refers to the institutional arrangements which facilitate the borrowings and

lending of long term funds. It consists of series of channels through which the savings of

the community are made available for industrial and commercial enterprises and public

authorities.

Capital market is further divided into three categories which are given below:

1) New Issue Market: NIM represents Primary market where new securities i.e. shares or

bonds that have never been previously offered.

2) Secondary Market: Secondary market is a place where existing securities i.e. shares

and debentures are traded.

3) Financial Institutions: Financial institutions provide medium and long term loans on

easy installments to big business houses. Such institutions help in promoting new

companies, expansion and development of existing companies.

SCENARIO OF PRIMARY MARKET

During both the earlier boons there was an availability of poor quality offerings in the

market. As issuing companies were allowed freedom to price their offerings, shares were

offered at a huge premium. Investors were left holding worthless talks as promoters

walked off with cash taking the advantage of IPO market. Numerous fly by night

operators had tapped the market and vanishing companies had become a norm.

In fact many experts opine that this loss of credibility of technology boom of 90’s,

company tapping the market for IPO often changed the name to something related to

technologies. These two left the investors bearing huge losses. Today things have

changed for better SEBI has now set up stringent eligibility criteria for companies willing

to tap the market.Its DIP (Disclosure and Investors Protection Guidelines) amended asrecently as August 2011, created a mechanism of better disclosure and increased

1

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 2/64

transparency. The process of Book Building has become the norm after the change of

rules, thus ensuring better transparency.

Primary market in India has evolved over the years. Post liberalization and after

the abolition of the office of controller of capital issues, public offers flooded the market.

The number of public offerings coming to the market and the amount raised declined over

the subsequent years. There was a brief revival thereafter which lasted for two years after

which the market languished again. From mid 2010 the market witnessed a sleeve of

initial public offers; the mobilization of funds has been definitely on masses scale.

PRIMARY MARKET

“Primary market deals with new securities which were not previously available to

the investors therefore the market makes available a new block of securities for public

subscription.”

“The new issue market is concerned with the floatation and disposal of new issue

of shares and debentures through their allotment to persons and organizations.”

“The new issue market represents the primary market where securities i.e. shares

or bonds that have never been previously issued or offered. Both the new companies andexisting one can raise capital on new issue market.”

“Primary markets are where firms raised capital through the issuance of financial

securities”.The prime function of new issue market is to facilitate the transfer of funds

from the willing investors to the entrepreneurs setting up new corporate enterprises or

going in for expansion, diversification, growth or modernization. Besides helping

corporate enterprises in securing their funds, the NIM canalizes the saving of individuals

and others into investment.

2

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 3/64

INITIAL PUBLIC OFFERING

IPO is an acronym for Initial Public Offering. This is the first sale of stock by a company

to the public. The company can raise money by either issuing debt or equity. If the company has

never issued equity to the public is known as IPO. Corporate may raise capital in primary market

by the way of an IPO, Rights Issue or Private Placement. An IPO is selling of securities to the

public in primary market. This IPO’s can be made through Book Building Method, Fixed Price

Method or combination of both.

BOOK BUILDING PROCESS

The normal method of offering shares to the investing public at a price fixed by the issuer

does not take into account the investors demand. On the other hand, the Book Building Method

takes into account the demand for shares at various prices as an important input to finalize the

offer price.

BookBuilding is basically a capital issuance process used in IPO which aids price and

demand discovery. It is a process used for marketing a public offer of equity share of a company.

It is a mechanism where, during the period for which the book for IPO is opened, bids are

collected from investors at various prices, which are above or equal to the floor price. The issue

price is then determined after the bid closing date based on certain evaluation criteria.

GREEN SHOE OPTIONA company making an IPO of Equity shares through the Book building mechanism can

avail of Green shoe option for stabilizing the post listing price of is shares. The Green shoe option

means an option of allotting shares in access of the shares in the public issue and operating a post

listing price stabilizing mechanism through a stabilizing agent.

A Green shoe option is a clause contained in an underwriting agreement of an IPO. A

Green shoe option which is also referred as over allotment provision, allows the underwriting

syndicate to buy in an additional 15 % of the shares at the offering price if public demand for shares exceeds expectations and the stock trades above its offering price.

3

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 4/64

NEED OF THE STUDY

Readers of this project can have perfect knowledge of basics of primary market.

This project can be used by researchers who want to study the trends in primary

market in post liberalization period.

Users can have thorough idea of five years area wise performance in primary

market.

People with observation and knowledge in primary market can have look on new

inclusions like Book Building Process and Green Shoe Option.

4

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 5/64

SCOPE OF THE STUDY

The study covers only corporate securities of primary market excluding Euro

Issues.

Resource mobilization part of the project covers number of issues, amount raised

sector wise distribution only and it did not cover response of public to various

Public Issues during the study period.

Book Building Process implications and its study belongs to year 2012 only.

Green Shoe Option on post distinct period is change in Central Government i.e.

May 2012.

5

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 6/64

OBJECTIVE OF THE STUDY

The objective of doing this project is mainly to make a thorough study and

performance of primary market, from 2008-2012 with special reference to

trends in primary market.

To assess primary market trends for last five years in different sectors.

To examine the factors affecting the performance of Indian primary market.

To examine positive and negative growth in different sectors of primary

market and major factors affecting it.

The purpose also includes Book Building Process and Green shoe Option

with regard to special case study.

The comparative study of different ingredients in primary market and its

performance.

6

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 7/64

METHODOLOGY OF THE STUDY

The method employed in the investigation depends on the purpose and scope of the study.

Let us try to understand methodology.

1) RESEARCH DESIGN: Research design is some statement or specification of

procedures for collecting and analyzing the information required for the solution of some

specific problem.

Here the exploratory research is used as investigation is mainly concerned with

determining the trends and positive and negative growth in different sectors in different

times in primary market .Exploratory research is generally carried out by three sources of

information

A) Study of secondary sources

B) Discussion with individuals

C) Analyzing some specific areas.2) DATA COLLECTION METHODS: The key for creating useful system are selectivity

in collection of data and linking that selectivity to the analysis and decision issue of the

action to be taken. The accuracy of collected data is of great significance for drawing

correct and valid conclusions from the investigation.

The following are the main steps in data collection process

a) Type of information required in the investigation

b) Establishing the facts that are available at present and additional facts required.

c) Identification of sources from where the information can be available.

d) Selection of appropriate information i.e. collection method.

7

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 8/64

Primary data: primary data are generated in an investigation according to the needs of

problem in head. Primary data is collected using case study methods. There are some set

of Qualitative techniques used for collection of some socio economic information about

some phenomenon.

Secondary data: Secondary data can be defined as data collected by some one else for

purpose other than solving the problem being investigated. Secondary data is collected

from external sources which include information from published material of SEBI and

some of the information is collected online. The data sources also include various books,

journals, magazines, news papers, etc. The organization profile is collected from Branch

Manager.

8

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 9/64

LIMITATIONS OF THE STUDY

A good report sells the results of the study. But every project has its own

limitations. These limitations can be in terms of

No depth analysis of government securities: Only corporate securities are

studied. No depth analysis of government securities is undertaken.

Government securities are taken only for comparison.

Limited to a particular period: Data under consideration is taken from

2008-2012.Previous years are not taken into consideration.

Partial fulfillment: Project studied doesn’t fulfill all requirements because

it does not study the whole primary market due to time availability and

course requirement. It only fulfills the partial requirement as it studies only

certain important aspects of primary market.

Approximate results: The results are approximated, as no accurate data is

available.

Results of Book Building do not apply to all firms: Book Building case

study results do not apply to all firms. It is also limited to a particular

period.

9

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 10/64

INDUSTRIAL PROFILE

STOCK MARKETS IN INDIA

Stock exchanges are the perfect type of market for securities whether of

government and semi – Govt bodies or other public bodies also for shares and debentures

issued by the joint –stock companies. In the stock market, purchases and sales are

affected in conditions of free competition. Government securities are traded outside the

trading ring in the form of over the counter sales or purchase. The bargains that are struck

in the trading ring by the members of the stock exchanges are at the fairest prices

determined by the basic loss of supply and demand.

STOCK EXCHANGE

“Stock exchange means anybody individual whether incorporated or not constituted

for the purpose of assisting, regulating or controlling the business of buying and selling or

dealing in securities”. The securities include.

Shares of public company.

Government securities

Bonds.

HISTORY OF STOCK EXCHANGES

Indian Stock Markets are one of the oldest in Asia. Its history dates back to nearly

200 years ago. The earliest records of security dealings in India are meager and obscure.

The East India Company was the dominant institution in those days and business in its

loan securities used to be transacted towards the close of the eighteenth century.

10

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 11/64

By 1830's business on corporate stocks and shares in Bank and Cotton presses

took place in Bombay. Though the trading list was broader in 1839, there were only half a

dozen brokers recognized by banks and merchants during 1840 and 1850.

The 1850's witnessed a rapid development of commercial enterprise and

brokerage business attracted many men into the field and by 1860 the number of brokers

increased into 60.

In 1860-61 the American Civil War broke out and cotton supply from United

States of Europe was stopped; thus, the 'Share Mania' in India begun. The number of

brokers increased to about 200 to 250. However, at the end of the American Civil War, in

1865, a disastrous slump began (for example, Bank of Bombay Share which had touchedRs 2850 could only be sold at Rs. 87).

At the end of the American Civil War, the brokers who thrived out of Civil War in

1874, found a place in a street (now appropriately called as Dalal Street) where they

would conveniently assemble and transact business. In 1887, they formally established in

Bombay, the "Native Share and Stock Brokers' Association" (which is alternatively

known as “The Stock Exchange "). In 1895, the Stock Exchange acquired a premise in the

same street and it was inaugurated in 1899. Thus, the Stock Exchange at Bombay was

consolidation.

The only stock exchange operating in the 19 th century were those of Mumbai setup

in 1875 and Ahmadabad setup in 1894. These are organized as voluntary non-profit

marking associations of brokers to regulate and protect their interests. Before the control

on securities under the constitution in 1950, it was a state subject and the Bombay

securities contracts (control) act of 1925 used to regulate trading in securities. Under thisact, the Mumbai stock exchange was recognized in 1927 and Ahmadabad in 1937. During

the war boom, a number of stock exchanges were organized. Soon after it became a

central subject, central legislation was proposed and a committee headed by

A.D.GORWALA went to into the bill for securities regulation on the basis of the

committee’s recommendations and public discussion, the securities contract (regulation)

act become law in 1956.

11

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 12/64

VARIOUS STOCK EXCHANGES IN INDIA

Presently there are 22 stock exchanges recognized under the securities contracts act 1956.

Those are,

Ahmadabad stock exchange.

Bangalore stock exchange.

Bhubaneswar stock exchange.

Calcutta stock exchange.

Cochin stock exchange.

Coimbatore stock exchange.

Delhi stock exchange.

Geuwahati stock exchange.

Jaipur stock exchange.

Kanara stock exchange.

Ludhiana stock exchange.

Madras stock exchange.

Madhya Pradesh stock exchange.

Magadha stock exchange.

12

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 13/64

Meerut stock exchange.

Mumbai stock exchange.

National stock exchange of India.

OTC stock exchange of India.

Pune stock exchange.

Saurashtra Kutch stock exchange.

Uttar Pradesh stock exchange.

Vadodara stock exchange

Previously 23 stock exchanges are there in India. Hyderabad stock

exchange registration was cancelled so now it reached to 22.

FUNCTIONS OF STOCK EXCHANGE

Stock exchange is established into the main purpose of providing a market place for the

members to deal in securities under well laid down regulations and to protect the interest

of the investors. The main functions of stock exchange are

It brings the companies and investors together so that the investors can put risk

capital into companies and thus, companies can use the capital.

It provides an orderly regulated market for securities.

It provides continuous, ready and open market for selling and buying securities.

13

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 14/64

It promotes savings and investment in the economy by attracting funds from

the investors.

It facilitates take over’s by means of acquiring majority of shares traded on the

stock market.

It acts as a clearing house of business information.

It motivates the managers of well reputed companies, to retain their shares in ‘A’

group, to improve performance.

It induces the managers to improve performance for converting non-specified

shares into specified shares in the exchange.

It enables the investors to evaluate the net worth of their holdings.

It also allows the companies to float their shares in the market.

TRADING PATTERN OF THE INDIAN STOCK MARKET

Trading in Indian stock exchanges are limited to listed securities of public limited

companies. They are broadly divided into two categories, namely, specified securities

(forward list) and non-specified securities (cash list). Equity shares of dividend paying,

14

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 15/64

growth-oriented companies with a paid-up capital of at least Rs.50 million and a market

capitalization of at least Rs.100 million and having more than 20,000 shareholders are,

normally, put in the specified group and the balance in non-specified group.

Two types of transactions can be carried out on the Indian stock exchanges:

spot delivery transactions "for delivery and payment within the time or on the date

stipulated when entering into the contract which shall not be more than 14 days following

the date of the contract"

Forward transactions "delivery and payment can be extended by further period of 14 days

each so that the overall period does not exceed 90 days from the date of the contract". The

latter is permitted only in the case of specified shares. The brokers who carry over the

outstanding pay carry over charges (cantango or backwardation) which are usually

determined by the rates of interest prevailing.

A member broker in an Indian stock exchange can act as an agent, buy and sell

securities for his clients on a commission basis and also can act as a trader or dealer as a

principal, buy and sell securities on his own account and risk, in contrast with the practice

prevailing on New York and London Stock Exchanges, where a member can act as a

jobber or a broker only.

The nature of trading on Indian Stock Exchanges are that of age old conventional style of

face-to-face trading with bids and offers being made by open outcry. However, there is a

great amount of effort to modernize the Indian stock exchanges in the very recent times.

NSE (NATIONAL STOCK EXCHANGE)

The national stock exchange of India ltd has genesis in the report of high power study group on establishment of new stock exchanges, which recommended promotion of

15

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 16/64

a national stock exchange by financial institutions to provide access to investors from all

across the country on an equal footing. Based on the recommendations, NSE was

promoted by leading financial institutions at the behest of the Govt of India and was

incorporated in November 1992 as a tax – paying company unlike other stock exchanges

in the country. On its recognition as a stock exchange under the securities contract act,

1956 in April 1993, NSC commenced operations in the whole sale debt market (WDM)

segment in june1994. The capital market (equities) segment commenced operations in

November 1994 and operations in derivatives segment commences in June 2000.

NSC’s mission is setting the agenda for change in the securities market in India. The NSC

was setup with the objectives of:

Establishing a nation wide trading facility for equities and debt instruments.

Ensuring equal access to investors all over the country through an appropriate

communication network.

Providing a fair, efficient and transparent securities market to investors using

electronic trading system.

Enabling shorter settlement cycles and book entry settlement systems, and

Meeting the current international standards of securities market.

The standards set by NSE in terms of market practices and technology, have become

industry benchmarks and are being emulated by other market participants. NSE is more

than a mere market facilitator. It’s that force which is guiding the industry towards new

horizon and greater opportunities.

16

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 17/64

BSE (BOMBAY STOCK EXCHANGE)

The stock exchange Mumbai, popularly known as “BSE” was established in

1875as “The native share and stock broker association”. It is the oldest in Asia, even

older then the Tokyo stock exchange, which was established in 1878. It is a voluntary non

profit association of persons (AOP) and is currently engaged in the process of converting

itself into demutualised and corporate entity. It has evolved over the years into its present

status as the premier stock exchange in the country. It is the first stock exchange in the

country to have obtained permanent recognition in 1956 from the Govt. of India under

securities contract (regulation) act 1956. The exchange while providing an efficient and

transparent market for trading in securities, debts and derivatives upholds the interests of

the investors and ensures redresses of their grievances whether against the companies or

its own member-brokers. It also strives to educate and enlighten the investors by

conducting investor education programmers and making available to them necessary

informative inputs.

A governing board having 20 directors is the apex body, which decides the

policies and regulates the affairs of the exchange. The governing board consists of 9

elected directors, who are from the broking community (one third of them retire ever year

by rotation), three SEBI nominees, six public representatives and an executive director

&chief executive officer and a chief operating officer. The executive director as the chief

executive officer is responsible for day-to-day administration of the exchange and the

chief operating officer and other heads of department assist him.

17

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 18/64

REGULATORY FRAME WORK OF STOCK EXCHANGE

A comprehensive legal frame work was provide by the “securities contract

regulation act, 1956”and “securities exchange board of India 1952”. Three tier regulatory

structure comprising

Ministry of finance

The securities and exchange board of India

Governing body.

MEMBERS OF THE STOCK EXCHANGE

The securities contract regulation act 1956 has provided a uniform regulation for

the admission of members in the stock exchanges. The qualifications for becoming a

member of a recognized stock exchange are given below:

The minimum age prescribed for the members 21 years.

He should be an India citizen.

He should not be convicted for fraud or dishonesty.

He should be neither a bankrupt nor compound with the creditors.

He should not be engaged in other business connected with a company.

He should not be a defaulter of any other stock exchange.

The minimum required education is a pass in 12th standard examination.

18

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 19/64

COMPANY PROFILE

CD Equisearch is one of the leading brokerage houses with a strong

presence in the institutional and HNI broking segment With over 30 years of experience,

you could be sure of the best in class research, operations, backend support and above all,

a name which inspires trust. At CD Equisearch, the emphasis is on transparent and clean

dealings. This has earned us our clients' goodwill. This quality has stood the test of timeand has helped us secure business from all quarters.

At CD Equisearch, people are not weighed down by tradition. Rather, we are

inspired by the rich heritage of the company. Here, business is conducted by building

long term relationships with our clients and associates by laying emphasis on ethical and

clean dealings. Here, people practice the gentle art of finance with professionalism, skill

and transparency. At CD Equisearch, we do business quietly.

Continued growth which is so essential in today’s fast paced and ever changing capital

market has been a constant feature at CD Equisearch. With an eye on the future and in

keeping with the changing times, we at CD Equisearch have earned the investor's

goodwill our most important asset, over the years.

After having a track record of servicing Institutions and HNIs for over 3 decades, we are

planning to foray into the growing retail segment in a big way. We would be expanding

across the geography with a wide network of our regional offices, branches, franchisees

and sub-brokers. We would be offering a complete basket in financial services. We are

looking at ourselves amongst one of the top ten broking houses in India by 2014 . To

achieve that, we have very aggressive plans of expansion.

19

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 20/64

Mission & Vision

CD Equisearch is passionate about providing friendly customer services on the greens of

the investing world. Following the highest standards of ethics is entrenched in the DNA

of CD Equisearch.

At CD Equisearch, the selection and recommendations of wealth creating opportunitiesare primarily based on the 3C principle:

• Conservation of capital

• Consistent growth in value of investment over a period of time

• Continual cash inflow through handsome dividends

Our Guiding Principles...

We, at CD Equisearch believe that being on par in terms of price and quality only

satisfies the customer. It is the customized service, which delights. The core values,

which drive CD Equisearch to exceed customer service expectations, are:

• TRUST

• TRANSPARENCY

• THOUGHT LEADERSHIP

We believe that abiding by these values for over more than the past three decades

has helped us earn the goodwill that we enjoy today.

20

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 21/64

MANAGEMENT

Chairman-Non Executive Director Mr. Chandravadan Desai

Director Mr. Pranay Desai

CFO Mr. Jayesh Vora

Director (Group Companies) Mr. Nilesh Vasa

21

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 22/64

PRIMARY MARKET, BBP AND GSO

PRIMARY MARKET

This project focuses on the relatively unexplored area of primary debt and equity

markets in developing countries. Its broad goal is to begin the process of understanding

how and why primary markets develop.

Primary markets are where the firms raise capital through the issuance of financialsecurities traded after insurance. The research will examine the development of domestic

primary market, focusing on macro economic factors. With the abolition of Control over

Capital Issues prior approval of capital issue proposals by companies has been dispensed

with. The companies are required now to be fair and honest to the investing public by

disclosing all material facts along with the risk factors associated with their projects to the

public. The present practice of brochure which is circulated widely to the investors along

with application form has been replaced with abridged prospectus to be attached to the

New Issue application forms.

The word “market” can have different meanings but it is used most often as a

catchall term to denote both primary and secondary market. In fact primary market and

secondary market are both distinct terms that refers to the market where securities are

created and the one in which they are traded among investors respectively. Knowing the

functions of primary and secondary market are the key to understanding how stocks trade.

Without them, the stock market would be much harder to navigate and much less

profitable. We will help you to understand how these markets work and how they relate to

individual investors.

The primary market is that part of capital markets that deals with issuance of new

securities. Companies, government or Public sector institutions can obtain funding

through the sale of new stock or bond issue. This is typically done through a syndicate of

securities dealers .The process of selling new issues to the investors is called

Underwriting. In the case of new stock issue, this sale is called an IPO (Initial public

22

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 23/64

offering). Dealers earn a commission that is built into the price of the security, though it

can be found in the prospectus.

The market in which investors have the first opportunity to find a newly issued

security. After the first purchases, subsequent trading is said to occur in secondary

market.

The primary market is where securities are created. It is in this market that firms

sell (float) new stock and bonds to the public for the first time. For our purposes, you can

think of a primary market as being synonymous with an IPO. Simply put, an IPO occurs

when a private company sells stocks to the public for the first time.

METHODS OF FLOATING NEW ISSUES

The various methods which are used in floatation of new securities in the new issue

market are

1) Public Issue / Offer through Prospectus

2) Offer for sale

3) Private Placement

4) Right Issues

5) Stock Exchange Pricing

6) Subscription by inside coteries

1) PUBLIC ISSUES:This is the most common method followed by joint stock companies

to raise capital through the issue of new securities. Under this method, the issuing

company directly offers to the general public or institutions a fixed number of shares at a

stated price through a document called prospectus. The purpose of raising the new capital

is to finance some capital expenditure, it is usual for companies to issue a prospectus

inviting the public to take up the new securities. Legally no public limited company can

raise capital from public without issuing prospectus.

2) OFFER FOR SALE: Under this method the company sells the shares /securities to the

issue house / brokers at an agreed price. The issue house/brokers sell their shares /

securities to the investors at a higher price. The company are relieved from the problem of

23

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 24/64

printing and advertisement of prospectus and making allotment of shares. Offer for sale is

not common in India

3) PRIVATE PLACEMENT: The promoters sell their shares to their friends, relatives and

well wishers to obtain the minimum subscription which is a precondition for issue of

shares to the public. Once this precondition for issue of shares is met, the issue

house/brokers buy the securities out right with the intention of placing them with their

clients afterwards. The issue house/brokers maintain their own list of clients and through

customer contact sell the securities. The main disadvantage of this method is that the

securities are not widely distributed to the large section of investors.

4) RIGHT ISSUES: Rights issue is a method of raising funds in the market by an existing

company. A right means an option to buy certain securities at a certain privileged price

within a specified period. Shares so offered to the existing shareholders are called Right

shares. Right shares are offered to the existing shareholders in a particular proportion to

their existing shareholders. The company should abide with section 81 of the companies

act. If the shareholders fail to take the Right shares within a specified period, the balance

is to be equally distributed among applicants for additional shares. Any balance still left

over may be disposed off in the market.

5) STOCK EXCHANGE PLACING: This method has been discontinued in India due to

strict regulations and statutory rules for listing of securities. According to it, “A company

used to place its shares privately with the aid of brokers, and then secured permission for

dealing on stock exchange”. This method involved little cost but often led to

concentration of new shares in few hands.

6) SUBSCRITION BY INSIDE COTERIES: When a company goes to the new issue

market a certain percentage of the capital is kept in reserve for subscription by inside

coteries.

24

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 25/64

SEBI GUIDELINES FOR NEW ISSUE MARKET

The SEBI guidelines for different category of companies are as follows

NEW COMPANY: A new company is a company which has not completed twelve months

of production. These companies have to issue shares only at par.

PRIVATE AND CLOSELY HELD COMPANIES: Those companies having a track record

of consistent profitability for last three years are permitted to price their issues freely.

EXISTING LISTED COMPANIES:The existing limited companies will be allowed to

raise fresh capital by freely pricing its shares provided the promoter’s contribution is 50%

on first 100 crores of issue.

DIFFERENTIAL PRICING: Issue to the public can be priced differentially as compared

to issue to right shareholders justification for the price difference should be mentioned in

the offer document.

LOCK IN PERIOD: Lock in period is five years for promoters contribution from the date

of allotment or from commencement of commercial production whichever is later.

GUIDELINES FOR PUBLIC ISSUE:

Every application should be accompanied with an abridged prospectus.

The risk factors should be highlighted in the abridged prospectus.

Company’s management, past history and present business of the firm

should be highlighted in the prospectus.

Justification for premium should be stated

The public issues should be kept open for a minimum of three days and a

maximum of ten working days.

The quantum of issue should not exceed amount given in the prospectus

Compliance report in the prescribed form should be submitted to SEBI

within forty five days from the date of closure of issue.

The gap between the closure date of various issues i.e. rights and public

should not exceed thirty days.

25

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 26/64

RECENT TRENDS AND DEVELOPMENTS IN NEW ISSUE

MARKET

The recent economical changes i.e. privatization, liberalization, foreign private

participation, disinvestment in public sector have given a new direction to the capital

market.

The number of issues made and the amount of capital raised from the market has been

phenomenal in the last decade. The public sector organizations like financial institutions,

public sector undertaking have started dominating the primary market. In 1996-97, all

public financial institutions including IDBI, IFCI, ICICI and many public sector backs

have mobilized resources through public issue route. There is a major decline in the

equity at premium issues over the years.

CAPITAL MOBILISED THROUGH DEBT: The late 90’s have witnessed the bent of

capital market for the issue of debt as that period is characterized with high interest rates

and negative returns from the secondary market.

MUTUAL FUNDS: New mutual funds were set up during the last decade. Many investors

are turning towards mutual funds to take the advantage of expertise in investments and

lowering of investment risk.

SEBI has dispensed with the requirement of a minimum promoters contribution and

lock in for listed companies with a three year dividend track record in the past five years

The market reforms include the introduction of electronic trading with the setting

up of OCTEI and NSE. The process of Book building was encouraged and IPO through

Book building has picked up.

Credit rating was made mandatory for some issues. This step has built the customer

confidence in the market. Qualitative changes included the introduction of new innovative

financial instruments. Certain innovative financial instruments were designed to suit the

investor’s requirement. With the globalization of business, foreign markets have

welcomed Indian companies. The Indian companies have issued GDR (global depository

receipts) and ADR (American depository receipts), foreign currency bonds, euro currency

bonds etc.

26

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 27/64

PROBLEMS OF NEW ISSUE MARKET

The problems of new issue market can be summarized as follows:

The new issue market failed to mobilize adequate savings from

the household sector. Only 10 % of the financial savings was mobilized. One reason

for such failure is lack of awareness among these sector and private placement of

capital by the companies.

The new issue market has failed to communicate to the public the

benefits of investing in new instruments.

Merchant banks have failed to bridge the gap between the

investors and the companies. They have failed to evaluate the projects taken up by

companies, credentials of promoters, technical and managerial aspects, etc. this has

led to customers being duped by companies. SEBI has now brought out stringent

guidelines for companies and merchant bankers.

Investment in capital markets are considered to be risky. So the

risk adverse attitude of customer has diverted the investment from shares to fixed

deposits and debentures.

Abnormally high cost of flotation has kept away small companies

from the primary market.

NIM has not reached to the semi urban and rural areas. An

investor from this region has to spend additional cost for post and bank charges to

access the NIM.

Delay in allotment of shares, refunding of application money,

posting of share certificates etc are common anomalies in NIM

New companies failed to gain the favor of underwriter. Caution

investors have stayed away from new companies, which led to devolution on

underwriters.

Timing of an issue is very important. But companies failed to

keep an eye on the other issues which are made during the same time. Thus crowding

of new issues at one time has made the investor to select the one which he considered

to be worthy.

27

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 28/64

INITIAL PUBLIC OFFERING

IPO is an acronym for initial public offering. This is the first sale of stock by a

company to the public. A company can raise money by issuing either debt or equity. If the

company has never issued equity to the public, it is known as an IPO. Corporate may

raise capital in the primary market by way of an IPO, right issue or private placement.

Companies fall into two broad categories private and public. A privately held

company has fewer shareholders. Anybody can come out and incorporate a private

company, put in some money file the right legal documents and follow the reporting

rules. Most small businesses are privately held, but large companies can be private too.

IKEA, Domino’s pizza and Hallmark cards are all privately held. It usually is not possible

to buy shares in private company. The shares of private company are not offered to

general public.

On the other hand public companies can sell at least a portion of themselves to the

public and trade on stock exchange. This is why doing an IPO is also referred to as going

public. Public companies have thousands of share holders and are subjected to strict rules

and regulations.

WHY GO PUBLIC?

Going public raises cash , being publicly traded also opens many financial

doors .Because of increased scrutiny public companies can usually get better rates when

they issue debt. As long as there is a market demand a public company can always issue

more stock.

Trading in open market means liquidity. Being on a major stock exchange carries

a considerable amount of prestige. In past companies with strong fundamentals could

28

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 29/64

only qualify for an IPO, but Internet boom changed all this. Firms no longer needed

strong financial and a solid history to go public. Instead, IPO’s were done by smaller start

ups seeking to expand their business. There is nothing to worry for expansion of IPO but

most of these firms had never made a profit and didn’t plan on being profitable any time.

In cases like this companies might be suspected of doing an IPO just to make the founders

rich. The IPO then becomes the end of the road rather than beginning.Howcan this

happen? Remember an IPO is just selling stock; it is all about the sales job. If you can

convince people to buy stock in your company, you can raise a lot of money. In our

opinion IPO’s came just to collect money are extremely risky and should be avoided.

IPO BASICS: HOW TO GET INTO AN IPO?

UNDERWRITING PROCESS: Getting a piece of a hot IPO is very difficult, if not

impossible. To understand why we need to know how an IPO is done, a process known as

underwriting.

When a company wants to go public, the first thing it does is hire an investment

bank. A company could theoretically, sell its shares on its own but realistically, an

investment bank is required. Underwriting is the process of raising money by either debt

or equity. Underwriter acts as middlemen between companies and the investing public.

The company and the investment bank will first meet to negotiate the deal. Items

usually discussed includes the amount of money company will raise, the types of

securities to be issued and all details in underwriting agreement. The deal can be

structured in a variety of ways. For example, in a “firm commitment” deal the underwriter

guarantees that a certain amount will be raised by buying the entire offer and then

reselling to the public. In a “best effort” deal the underwriter sells the securities, but

doesn’t guarantee the amount rose.

Once all sides agree to deal, the investment bank puts together a registration

statement to be filed with SEC, governing bodies. This document contains information

about offering as well as company information such as financial statements, management

background, legal problems and insider holdings. The SEC then requires a “cooling off

period” in which they investigate and make sure all material information has been

disclosed. Once SEC approves the offering, a date is set when the stock will be offered to

the public.

29

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 30/64

During the cooling off the period the underwriters put together what is known as

red herring. This is an initial prospectus containing all information about the company

except for the offer price and effective date , which aren’t known at the time with the red

herring in hand , the underwriter and the company attempt to hype and build up interest

for the issue. They go on a road show also known as “the dog and pony show” where the

big institutional investors are courted.

As an effective date approach the underwriter and company sit down and decide

on the price. This is not an easy decision; it depends on the company, the success of the

road show and most importantly current market conditions. Of course it is in both parties

interest to get as much as possible. Finally the securities are sold on the stock market and

money is collected from investors.

INDIVIDUAL INVESTOR: As you can see, the road to an IPO is an long and complicated

one. You may have noticed that individual investors are not involved until the very end,

because small investors are not the target market. They do not have more cash and

therefore hold little interest for the underwriters. If the underwriters think that an IPO will

be successful they will usually pad the pockets of their favorite institutional client with

shares at IPO price. The only way for individual investor to get shares is to have an

account with one of the investment banks that is part of the underwriting syndicate. But

an individual cannot expect to open an account with $1000 and be showered with an

allocation. He has to be frequently trading client with a large account to get into a hot

IPO.

POINTS TO BE CONSIDERED TO GET INTO AN IPO

NOHISTORY: It’s hard enough to analyze the stock of an established company. An IPO

company is even trickier to analyze since there won’t be a lot of historical information.

The main source of data is Red herring prospectus, so make sure you examine this

document carefully. Look for the usual information but also pay special attention to the

management team and how they plan to use the funds generated from an IPO.

LOCK UP PERIOD: If you look at the charts following many IPO’s, you will notice that

after few months the stock takes a sleep downturn, this is often because of lockup period.

30

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 31/64

When a company goes public, the underwriters make company officials and

employees sign a lock up agreement. Lock up agreements are legally binding contracts

between underwriters and insiders of the company, prohibiting them from selling any

shares of stock for a specified period of time. The period can be anything from 3 to 24

months. 90 days is minimum period stated under rule, but lockup specified by the

underwriters can last much stronger. The problem is when lockups expire all the insiders

are permitted to sell their stock. The result is a rush of people trying to sell their stock to

realize their profit. This excess supply can put severe downward pressure on the stock

price.

FLIPPING: Flipping is reselling a hot IPO stock in the first few days to earn a good

profit. This is not easy to do and you will be strongly discouraged by your broker. The

reason behind this is that, the companies want long term investors who hold their stock,

not traders. There are no laws that prevent flipping, but your broker may black list you

from future offering or just smile less when you shake hands.

Of course, institutional investors flip stocks all the time and make big money. The double

standard exists and there is nothing we can do about it as they have buying power.

Because of flipping, it is a good rule not to buy shares of an IPO if you don’t get in on the

initial offering. Many IPO’s that have big gains on the first day will come back to earth as

the institutions take their profits.

AVOID THE HYPE-It’s important to understand that underwriters are salesmen. The

whole underwriting process is intentionally hyped up to get as much attention as possible.

Since IPO’s only happen once for each company, they are often presented as “once in a

lifetime” opportunities. Of course some IPO soar high and keep soaring. But many end up

selling below their offering prices within the year. Don’t buy a stock because it is an IPO

do it because it is a good investment.

31

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 32/64

BOOK BUILDING PROCESS

The abolition of the capital issues control act, 1947 has brought a new era in the

primary market in India. The control over the pricing of the issues, designing and tenure

of capital issues were abolished. The issuers at present are free to make the price of issue.The main drawback of pricing was the process of pricing of issues. The issue price was

determined around 60 to 70 days before the opening of the issue and the issuer had no

clear idea abut the market perception of the price determined. The traditional fixed price

method of tapping individual investor from two defects

Delay in initial public process.

Under pricing/over pricing of issues.

In fixed price method, public offers do not have any flexibility in terms of prices

as well as number of issues. From experience it can be stated that a majority of the public

issues come through fixed price method are either under priced or over priced. Retail

investors are unable to distinguish good issues from bad one. That is why book building

mechanism, a new (product) process of price discovery has been introduced to overcome

this limitation and determine issue price effectively.

SEBI guidelines defines book building as a process undertaken by which a

demand for the securities proposed to be issued by a corporate body is elicited and build

up and the price for such securities is assessed for the determination of the quantum of

such securities to be issued by means of a notice, circular, advertisement, document or

information memoranda or offer document.

Book building is basically a capital issuance process used in IPO which aids price

and demand discovery. It is a process used for marketing a public offer of equity shares of

a company. It is a mechanism where during a period fro which a book for IPO is open,

32

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 33/64

bids are collected from the investors at various prices, which are above or equal to the

floor price. The process aims at tapping both wholesale and retail investors. The

offer/issue price is then determined after the bid closing date based on certain evaluation

criteria.

FEATURES OF BOOK BUILDING PROCESS

Public offers in fixed price method involves a pre issue cost of 2-3 percent and

carry the risk of failure if it does not receive 90 percent of total subscription. In

Book building such cost and risk can be avoided because Issuer Company can

withdraw the market if demand for security does not exist.

Institutional investor like to participate largely in book built transactions as in this

process the time taken for completion of entire process is less than the fixed price

issues

Here the price is determined on the basis of the demand received or at the price

above or equal to the floor price whereas in fixed price option the price of issues is

fixed first and then securities are offered to the investors.

Book is built by book running lead manager to know the everyday demand

whereas in case of fixed price of public issues, the demand is known at the close

of the issue.

Book should remain open for minimum of 5 days.

33

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 34/64

BOOK BUILDING PROCESS IN INDIA

The main parties who are directly associated with book building process are issuer

company. BRLM (Book Running Lead Managers) and the syndicate members. The

BRLM (merchant banker) and the syndicate members who are the intermediaries are both

eligible to act as underwriters. The steps involved in book building process are as under:

The issuer company proposing an IPO appoints a lead merchant banker as BRLM.

Initially the issuer company consults with the book running lead manager in drawing

up a draft prospectus which does not mention the price of the issues but includes other

details about the size of the issues, past history of a company and a price band. The

securities available to the public are separately identified as net offer to the public.

The draft prospectus is filed with SEBI which gives it a legal standing.

A definite period is fixed as a bid period and BRLM conducts awareness campaign

like advertisements, road shows etc.

The BRLM appoints a syndicate member, a SEBI register intermediary who

underwrites the issues to the extent of net offer to the public.

The BRLM is entitling to remuneration for conducting the book building process.

The copy of draft prospectus may be circulated by BRLM to the institutional investors

as well as to the syndicate members.

34

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 35/64

The syndicate members create demand and ask each investor for the number of shares

and offer price.

The BRLM receives the feedback about the investors bid through syndicate members.

The prospective investors may revise their bids at any time during the bid period.

The BRLM on receipt of feedback from the syndicate embers about the bid price and

quantity of share apply has to build up an order book showing the demand for the

shares of the company at various prices. The syndicate members must also maintain a

record book for orders received from institutional investors for subscribing to the

issue of private portion.

12) On receipt of above information, the BRLM and the issuer company decides the

issue price. This is known as market clearing price.

13) The BRLM then closes the book in consultation with the issuer company and

determine the issue size of placement portion and public offer portion.

Once the final price is determined the allocation of securities should be made by

BRLM based on prior commitment, investors quality, price aggression, earliness of

bids etc. the bid of an institutional bidder, even if he has paid full amount may be

rejected without being assigned any reason as the book building portion of

institutional investors is left entirely at the discretion of issuer company and the

BRLM

The final prospectus if filed with the registrar of companies within 2 days of

determination of issue price and receipts of acknowledgement card from SEBI.

Two different accounts for collection of application money, one for the private

placement portion and the other for the public subscription should be opened by

Issuer Company.

The placement portion is closed a day before the opening of public issue through

faxed price method. The BRLM is required to have the application forms along with

application money from the institutional buyers and underwriters to the private

placement portion.

35

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 36/64

The allotment for the private placement portion shall be made on the second day from

the closure of the issue and the private placement portion is ready to be listed.

The allotment and listing of issues under the public portion i.e. fixed price portion

must be as per the existing statuary requirements.

Finally the SEBI has the right to inspect such records and books which are maintained

by BRLM and the intermediaries involved in the Book building process.

BOOK BUILDING ISSUES IN INDIA

The practice of Book building is new to Indian capital market and the procedure is

still evolving. When Book building was introduced in India the main objective was that

Book building would help discover the right price for a public issue, which in turn would

eliminate unreasonable issue pricing by greedy promoters. ICICI first used book building

method for its Rs.1000 crores- bond issue in April 2007 followed Larsen & Toubro,

TISCO, Hughes software, ONGC, TCS, NTPC etc in recent times

Sl.

No.

Name of the

issue

Book Running

Lead Manager

Date of

issue

Price

Band

Issue size

(Lakh

shares)

01

SAL Steel

Limited

1) SBI Capital Market Ltd.

2)IL&FS Invest smart Ltd.

01.11.2012

to

05.11.2012

Rs.12

to

Rs.14 420.00

36

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 37/64

02 NTPC

Limited

1) ICICI Securities Ltd.

2) Enam Financial consults.

3) Kotak Mahindra Capital.

07.10.2012

to

14.10.2012

Rs.52

to

Rs.628658.30

03

India bulls

Financialservices Ltd

1) SBI Capital Markets Ltd.

2) DSP Merrill Lynch Ltd.

06.09.2012

to10.09.2012

Rs.16

toRs.19

271.87

04

Tata

consultancy

services Ltd

1) J.M.Morgan Stanley.

2) DSP Merrill Lynch.

3) JP Morgan India Pvt. Ltd.

29.07.2012

to

05.08.2012

Rs.775

to

Rs.900554.52

05 NDTV Ltd.

1) J.M.Morgan Stanley.

2)Kotak Mahindra Capital

3) ICICI Securities Ltd.

21.04.2012

to

28.04.2012

Rs.63

to

Rs.70173.01

06DatamaticsTech. Ltd

1) Enam Financial Consults. 12.04.2012to

19.04.2012

Rs.101to

Rs.110103.00

07

Pharmaceuti

cals and

chemicals

1) Enam Financial Consults.

2) IL&FS Invest smart Ltd.

29.03.2012

to

07.04.2012

Rs.155

to

Rs.17534.33

08

ICICI Bank

Ltd.

1) DSP Merrill Lynch Ltd.

2) J.M.Morgan Stanley.

3) Kotak Mahindra Capital.

02.04.2012

to

07.04.2012

Rs.255

to

Rs.2951196.07

DIFFERENCE BETWEEN SHARE OFFERED THROUGH

BOOKBUILDING AND THROUGH NORMAL PUBLIC ISSUE

In normal public issue method the price at which the securities are offered/allotted

is known in advance to the investor whereas the price at which these securities

will be offered/allotted is not known in advance to the investor in book building

process. Only indicative price range is known.

In normal public issue method demand for the securities offered is known only

after the closure of the issue whereas in book building method demand for the

securities offered can be known everyday as the book is built

In normal issue method payment is made at the time of subscription wherein

refund is given after allocation whereas in book building method payment is made

only after allocation.

37

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 38/64

In book building securities are offered a t prices above or equal to the floor prices,

whereas securities are offered at a fixed price in case of normal public issues.

OFFER TO THE PUBLIC THROUGH BOOK BUILDING PROCESS

The oxford dictionary of business jumps from “bonus shares to book keeping” and

then on “book of primary entry” without devoting an entry for book building. Book

building is the process by which an underwriter attempts to offer an IPO based on

demand form institutional investors.

An underwriter “builds a book” by accepting orders from fund managers,

indicating the number of shares they desire and the price they are willing to pay. Book

maker is not the same as the book builder. The former takes bets and pays out money to

the people who win. The IPO can be made through fixed price method, book building

method or a combination of both. In case the issuer choose to issue securities through

book building route then as per SEBI guidelines, an issuer company can issue securities

in the following manner.

A) 100 percent of the net offer to the public through book building route

B) 75 percent of the net offer to the public through the book building process and 25

percent through fixed price portion.

C) Under 90 percent scheme this percentages will be 90 and 10 respectively.

A) 100 % THROUGH BOOK BUILDING PROCESS: In the 100 percent of the net offer to

the public, entire issue is made through book building process. In case of 100 percent

book building process, the bidding centers should be at all the places where recognized

stock exchanges are situated.

B) 75 % THRUOGH BOOK BUILDING PROCESS: The option of 75 percent book

building is available through the book building process are indicated as placement portion

category and securities available to public are identified as net offer to the public. In this

38

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 39/64

option, underwriting is mandatory to the extent of net offer to the public. The issue price

for placement portion and offers to public are required to be same.

C) 90 % THROUGH BOOK BUILDING PROCESS: This option is not available in India.

TYPES OF INVESTORS

There are three kinds of investors in book building issue. The retail individual

investor (RII), the non-institutional investor (NII) and the qualified institutional buyers

(QIB).

RII is an investor who applies for stocks for a value of not more than rupees

100000. Any bid exceeding this amount is considered in the NII category. NIIs are

commonly referred to as high net worth individuals. On the other hand QIBs are

institutional investors who posses the expertise and the financial muscle to invest in

securities markets.

Mutual funds, financial institutions, scheduled commercial banks, insurance

companies, provident funds, state industrial development corporations fall under the

definition of being a QIB. Each of these is allotted a certain percentage of total issue. The

total allotment of RII category has to be at least 35 percent of the total issue. RII alsohave an option of applying at cut-off price. This option is not available to other classes of

investors. NIIs are to be given at least 15 percent of the total issue and QIBs are to be

issued not more than 50 percent of the total issue

REVERSE BOOK BUILDING PROCESS

The reverse book building is a mechanism provided for capturing the sell orders

online basis from the shareholders through respective BRLMs which can be used by thecompanies intending to delist its shares through buy back process. In reverse book

building scenario, the acquirer/company offers to buy back shares from the shareholders.

The reverse book building is basically a process used for efficient price discovery. It is a

mechanism where during the period for which the reverse book building is open offers are

collected from the shareholders at various prices, which are above or equal to the floor

price. The buy back price is determined after the offer closing date.

Business process for delisting through book building is as follows

39

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 40/64

The acquirer shall appoint designated BRLM for accepting offers form the

shareholders

The company/acquirer intending to delist its shares through book building process

is identified by way of a symbol assigned to it by BRLM.

Orders for the offer shall be placed by the shareholders only through the

designated trading members, duly approved by the exchange.

The designated trading members shall ensure that the security/shareholder deposit

the securities offered with the trading members prior to the placement of an order.

The offer shall be open for number of days

The BRLM shall intimate the final acceptance price and provide the valid

accepted order file to the National Securities Clearing Corporation Limited

(wholly owned securities of NSE carrying out clearing and responsible for

settlement operation.).

SEBI guidelines shall be applicable to delisting of securities of companies and

specifically apply to:

Voluntary delisting being sought by the promoters of a company.

Any acquisition of shares of the company (either by a promoter or by any other

person)or scheme or arrangement, by whatever name referred to, consequent to

which the public shareholding falls below the minimum limit specified in the

listing conditions or listing agreement that may result in delisting of securities.

Promoters of the company who voluntarily seek to delist their securities from all

or some of the stock exchanges.

Case where a person in control of the management is seeking to consolidate hishol ding in a company in a manner which would result in the public share

40

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 41/64

holdings or in the listing agreement that may have affect of company being

delisted.

The companies which may be compulsorily delisted by stock exchanges

Advantages of reverse book building provides following advantages

It provides a fair, efficient and transparent method for collecting offer using latest

electronic trading systems.

The NSE system offers a nationwide bidding facility in securities.

Cost involved in issue is far less than those in a normal IPO.

RED HERRING PROSPECTUS

A preliminary registration statement that must be filed with the SEC describing a

new issue of stock and the prospects of the issuing company.

"Red Herring Prospectus" is a prospectus which does not have details of either

price or number of shares being offered or the amount of issue. This means that in case

the price is not disclosed, the number of shares and the upper and lower price bands are

disclosed. On the other hand, an issuer can state the issue size and the number of shares

are determined later. An RHP for and FPO can be filed with the ROC without the price

band and the issuer, in such a case will notify the floor price or a price band by way of an

advertisement one day prior to the opening of the issue. In the case of book-built issues, it

is a process of price discovery and the price cannot be determined until the bidding

process is completed. Hence, such details are not shown in the Red Herring prospectus

filed with the ROC in terms of the provisions of the Companies Act.

Only on completion of the bidding process, the details of the final price are

included in the offer document. The offer document filed thereafter with ROC is called a

prospectus.

“Abridged Prospectus” means contains all the salient features of a prospectus. It

accompanies the application form of public issues.

GREEN SHOE OPTION

41

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 42/64

In most of the case it is experienced that IPO through book building method in

India turns out to be over priced or under priced after their listing and ultimately the small

investor becomes the net loser. If the prices in open market fall below the issue price,

small investors may start selling their securities to minimize losses. Therefore there was a

vital need of a market stabilizer to smoothen swing in the open market price of newly

listed shares after an IPO. Market stabilization is the mechanism by which stabilizing

agent acts on behalf of the issuer company, buys a newly issued securities for the limited

purpose of preventing a decline in the new securities in open market price in order to

facilitate its distribution to the public. It can prevent the IPO from huge price fluctuation

and save investors from potential loss. Such mechanism is known as Green Shoe Option.

Green Shoe Option can rectify the demand and supply imbalances and can stabilize the

price of the stock. It owes its origin to the green shoe option company, which used this

option for the first time in the world.

SEBI recognized GSO system of initial public 2004 August. According to SEBI

Guidelines “A company desirous of availing GSO shall pass the resolution in the general

body meeting authorizing the public issue, seek authorization, also for possibility of

allotment of further shares to the stabilizing agent. The company shall appoint one of the

Lead book runners among the issue management team as stabilizing agent, will beresponsible for price stabilization process if required.

The stabilizing agent shall enter into an agreement with the promoters who will

lend their share, specifying the maximum number of shares that may be borrowed from

the promoters, which shall not be in excess of fifteen percent of the total issue size. The

stabilization mechanization shall be available for the period disclosed by the company in

the prospectus, which shall not exceed 30 days from the date when trading permission

was given by the exchanges.

Ideally, with the intervention of the stabilizing agent the share price should not fall

below the issue price for a period of 30 days from the listing date. Due to this option, the

investor has a time period of 30 days up to which he is safe and his chances of incurring

the losses are minimum.

A GSO is a clause contained in the underwriting agreement of IPO. The GSO is

also referred to as an overallotment provision, allows the underwriting syndicate to buy

42

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 43/64

up an additional 15 % of the shares at the offering price if public demand for the shares

exceeds expectations and the stock trades above its offering price.

The GSO provides extra incentive for the underwriters of a new stock offering. In

addition this investment banks, brokerages and other financing parties also often exercise the

GSO the cover some of the short position. They may have created an effort to maintain a stable

market after a new stock begins to trade as well as to meet after market demand.

AN INTERESTING FACT

The Green shoe company was the first issuer to allow the overallotment option to its

underwriters, hence the name. The provision that has become standard in firm

commitment underwriting is the overallotment option or green shoe option. Where thecompany and other sellers of securities grant and option to the underwriters to purchase

additional shares (around 15 % in total offerings) on the same term as the original shares

offer to the underwriters. The GSO allows the underwriters to exercise significant market

clout in stabilizing activities during a 30 day period immediately following a public

offering. The over allotment gives the underwriters buying power to cover their short

position in order to stem a falling stock price, without the risk of having to buy stock at

higher prices to cover their short position is the stock price increases

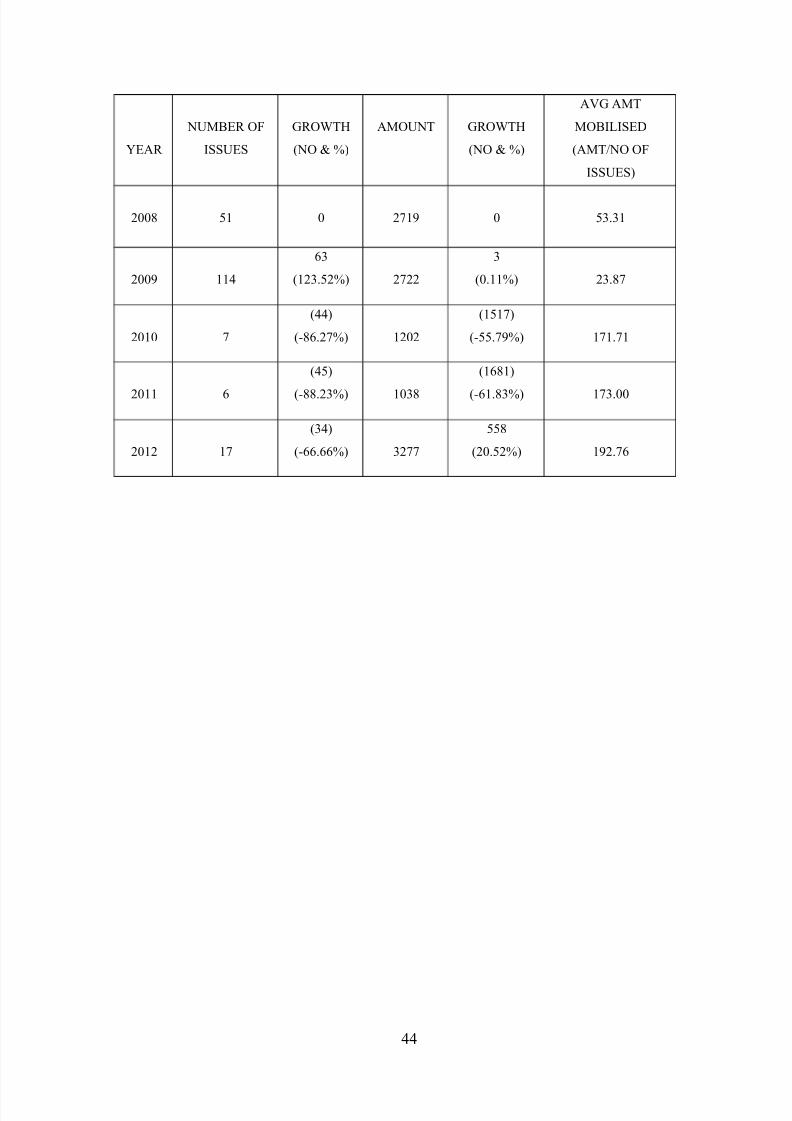

RESOURCE MOBILIZATION FROM PUBLIC ISSUES (IPO’S)

(2008-2012)

(TABLE: 1) (Rs. In crores)

43

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 44/64

YEAR

NUMBER OF

ISSUES

GROWTH

(NO & %)

AMOUNT GROWTH

(NO & %)

AVG AMT

MOBILISED

(AMT/NO OF

ISSUES)

2008 51 0 2719 0 53.31

2009 114

63

(123.52%) 2722

3

(0.11%) 23.87

2010 7

(44)

(-86.27%) 1202

(1517)

(-55.79%) 171.71

2011 6

(45)

(-88.23%) 1038

(1681)

(-61.83%) 173.00

2012 17

(34)

(-66.66%) 3277

558

(20.52%) 192.76

44

8/22/2019 study on primary market with reference to CD equi search.doc

http://slidepdf.com/reader/full/study-on-primary-market-with-reference-to-cd-equi-searchdoc 45/64

INTERPRETATION