Embed Size (px)

Citation preview

Substantially Equal Periodic Payments and

Other Strange Animals

Found in the

Internal Revenue Code

by

William J. Stecker, CPA

Second Edition © 2001

Extremely Important Notice The second edition of this text was published November 2001. From that date through October 4, 2002, everything in the text was accurate. However, on October 4, 2002, the Internal Revenue Ser-vice issued Revenue Ruling 2002-62. Although only a seven-page document, this ruling is extremely significant and literally creates a whole new set of rules regarding both in-progress as well as new sub-stantially equal periodic payment plans. In general, this new ruling is two rulings in one:

(1) It provides for new interpretations of IRC §72(t)(4), specifically what constitutes a “modification” and what does not; thus, providing a relief mechanism to taxpayers with existing SEPP plans that are prematurely running out of IRA assets. Further, a one-time method conversion is allowed to the “required minimum distribution” method.

(2) Effective, January 1, 2003, new SEPP plans will be materially limited from the current

set of rules such that the maximum amount of distributions allowed, holding the IRA balance constant, will be reduced in the range of 25% to 30%.

As a result of the new ruling, this text is undergoing a major revision which is going to take some time to accomplish—both in resolving new open issues related to the new ruling as well as a complete re-write of the text itself. Anyone purchasing this report should do several things: one, send an e-mail to [email protected] so that the author can send you, at no charge, a copy of the 3rd edition when it becomes available (anticipated in January 2003); two, should you anticipate launching a new SEPP program in the near future, please seek professional assistance from the tax accountant or tax attorney of your choice, at least, to get briefed on the contents of Revenue Ruling 2002-62 and how it may change your SEPP plans. As an interim source of information, feel free to visit www.72t.net and review both the Articles section of the web site as well as the Message Board. There are several good articles here as well as ongoing discussion of tactical SEPP issues. William J. Stecker, CPA

iii

Table of Contents

Introduction ..............................................................................................................vi Second Edition ....................................................................................................... viii Disclaimer............................................................................................................... viii Biographical Information...................................................................................... viii Chapter 1: Current Law............................................................................................1 Internal Revenue Code................................................................................................................1 Exception #1 Age 59½................................................................................................................1 Exception #2 Death.....................................................................................................................1 Exception #3 Disability...............................................................................................................2 Exception #5 Separation of Service at Age 55.............................................................................4 Exceptions #6 Through #12 ........................................................................................................5 Exception #4 Substantially Equal Period Payments .....................................................................7 Internal Revenue Service Publications ........................................................................................9 Tax Court Cases..........................................................................................................................9 Private Letter Rulings .................................................................................................................9 Chapter 2: Common Concepts ................................................................................11

Unearned Ordinary Income ....................................................................................................... 11 Age Windows ...........................................................................................................................11 The Account Concept................................................................................................................12 Individual Ownership................................................................................................................13 Relationship to Earned Income..................................................................................................14 Reversibility and Errors ............................................................................................................14 Basis in Account .......................................................................................................................15 Penalty Computations ...............................................................................................................15

Chapter 3: Other Strange Animals—Roth IRAs & NUA......................................17 Roth IRA Taxation and Penalties ..............................................................................................17 Roth Definition .........................................................................................................................17 Qualified and Unqualified Withdrawals ....................................................................................17 Application of 5-Taxable-Year Rule .........................................................................................18 Contribution and Earnings Withdrawals ....................................................................................19 Conversion Dollar Withdrawals ................................................................................................20 Net Unrealized Appreciation (NUA) .........................................................................................21 Summary ..................................................................................................................................24 Chapter 4: Computation of Substantially Equal Periodic Payments....................26

Minimum Method .....................................................................................................................27 Amortization Method................................................................................................................29 Annuity Method........................................................................................................................30

iv

Other Methods ..........................................................................................................................31 Chapter 5: Interest Rate Selection Risks ................................................................32

External Risk ............................................................................................................................32 Internal Risk .............................................................................................................................33 Internal Risk Management ........................................................................................................34 External Risk Management .......................................................................................................36 Conclusions ..............................................................................................................................37

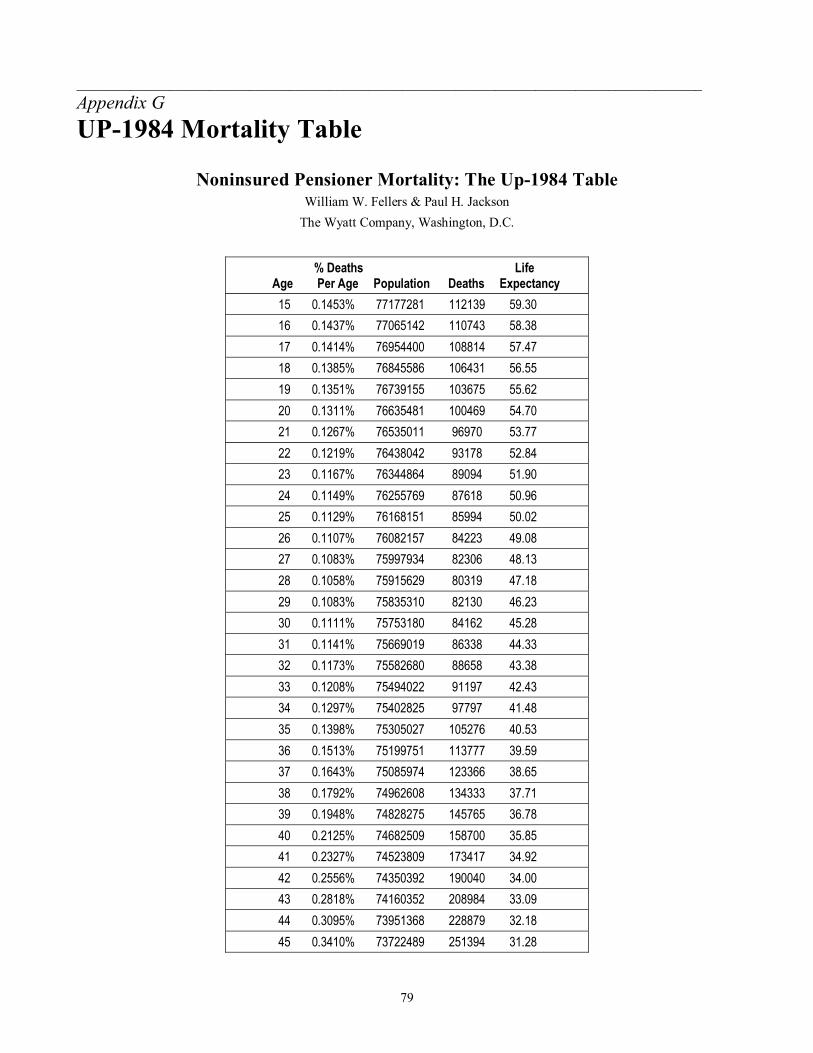

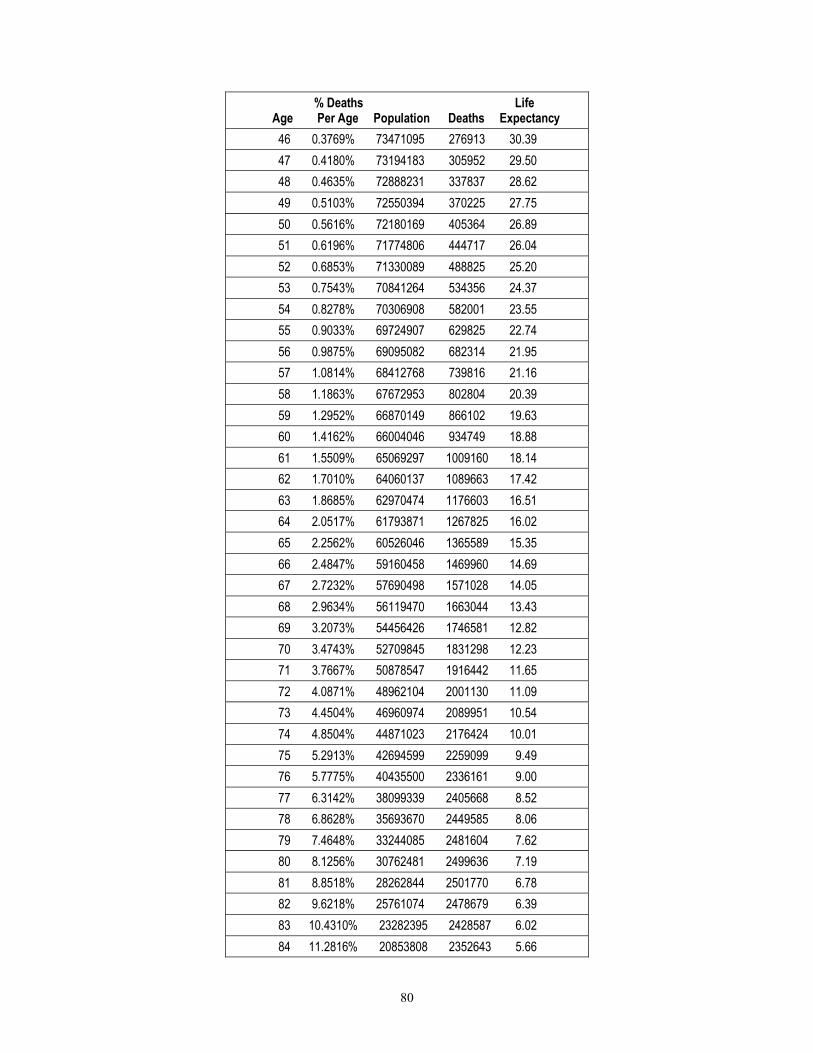

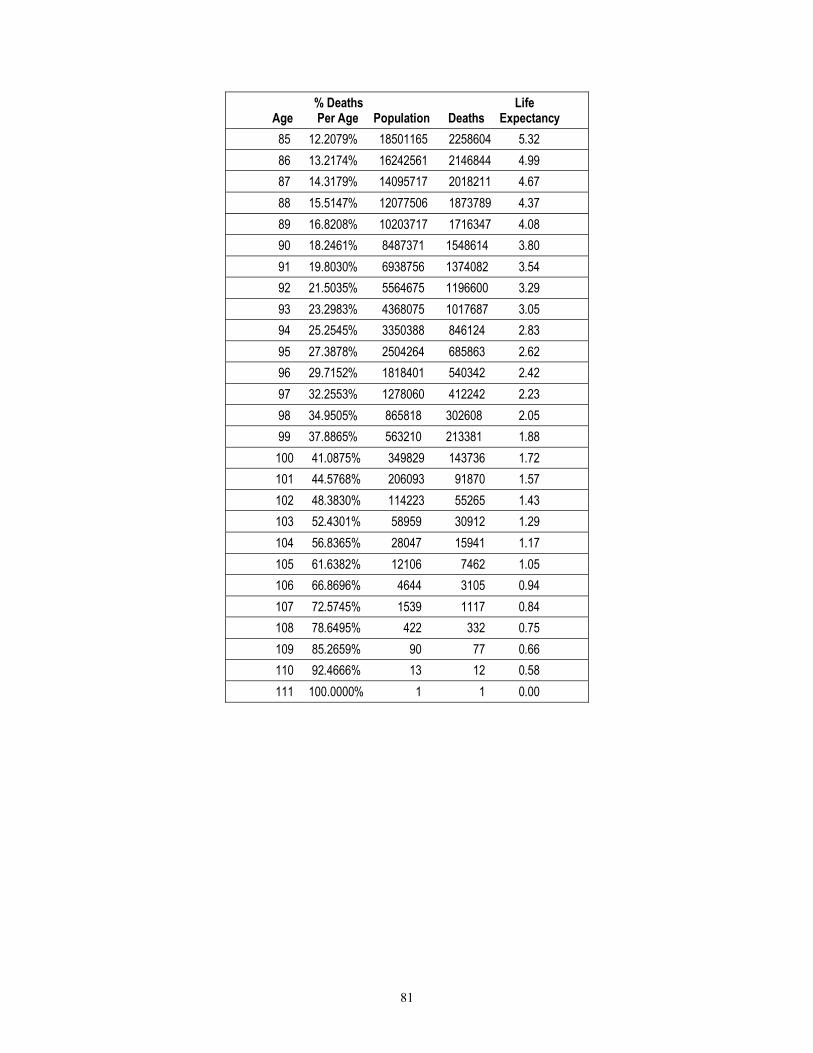

Chapter 6: Life Expectancy Table Selection ..........................................................39 Approved Mortality Tables .......................................................................................................39

Table S: 80CNMST & 90CM....................................................................................................43 Chapter 7: Other Planning Issues...........................................................................45

How to Plan a SEPP..................................................................................................................45 Account Fracturing and Aggregation.........................................................................................45 Multiple SEPP Programs...........................................................................................................46 Important Dates ........................................................................................................................46 Stub Periods .............................................................................................................................47 Disbursement Frequencies and Locations..................................................................................48 Diminimus Issues......................................................................................................................48 Cost of Living Adjustments ......................................................................................................48 Recalculation in Conjunction with the Amortization or Annuity Methods .................................49 Death and Divorce ....................................................................................................................54 Simultaneous Processing of Other Exceptions...........................................................................55 Planning of the SEPP ................................................................................................................55 Tax Planning Issues for the Wealthy .........................................................................................56 Conclusions ..............................................................................................................................57

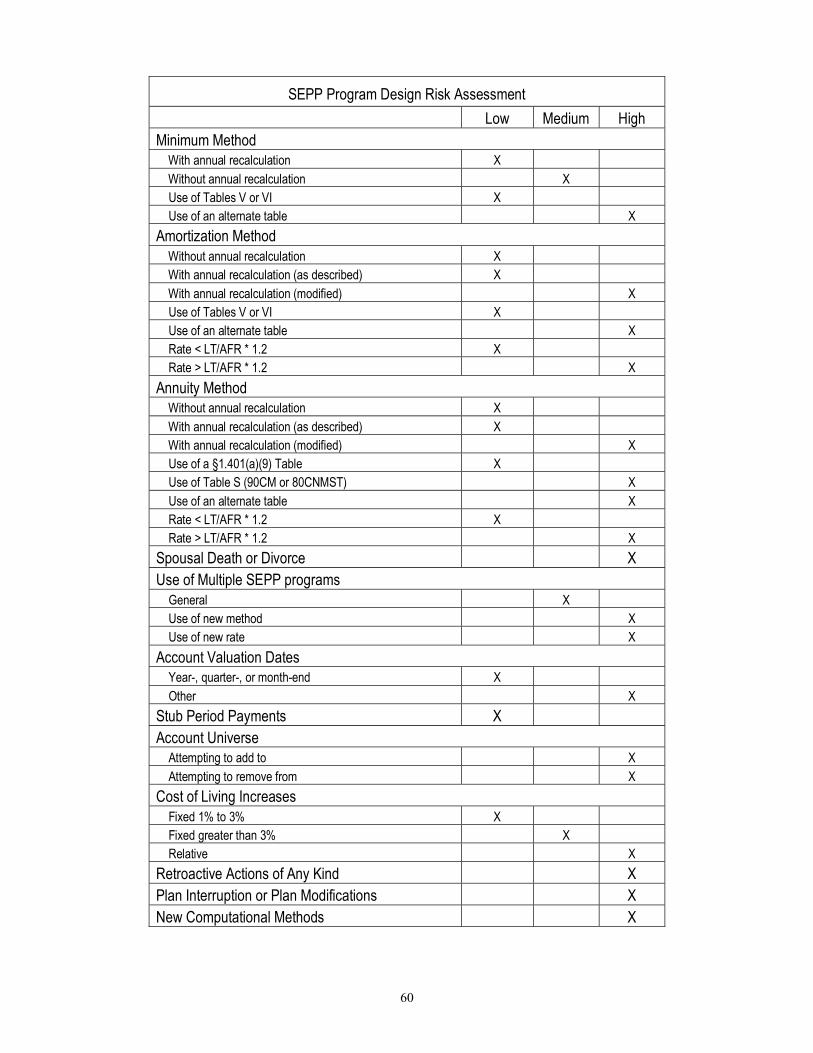

Chapter 8 Risk Analysis ..........................................................................................58

Risk Assessment .......................................................................................................................58 SEPP Program Design Risk Assessment ...................................................................................60 Individual Issues .......................................................................................................................61 Selecting a Professional ............................................................................................................61

Chapter 9 Administration .......................................................................................63

Record Keeping ........................................................................................................................63 Trustee Communications...........................................................................................................63 Tax Matters...............................................................................................................................63 State Taxation ...........................................................................................................................64

Appendices

Appendix A: Internal Revenue Code §72(t)...............................................................................65 Appendix B: IRC Reg. §1.72-17A(f) Disability.........................................................................69 Appendix C: Excerpt from Notice 89-25, 1989-1 C.B. 662 .......................................................70

v

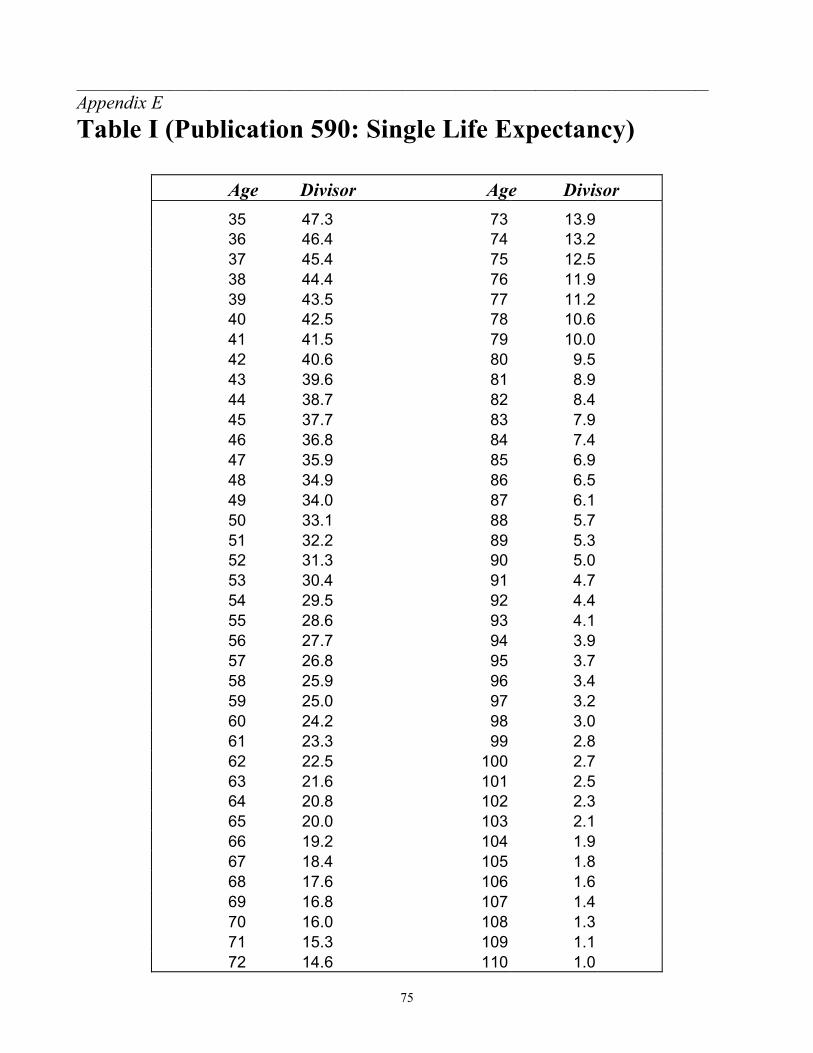

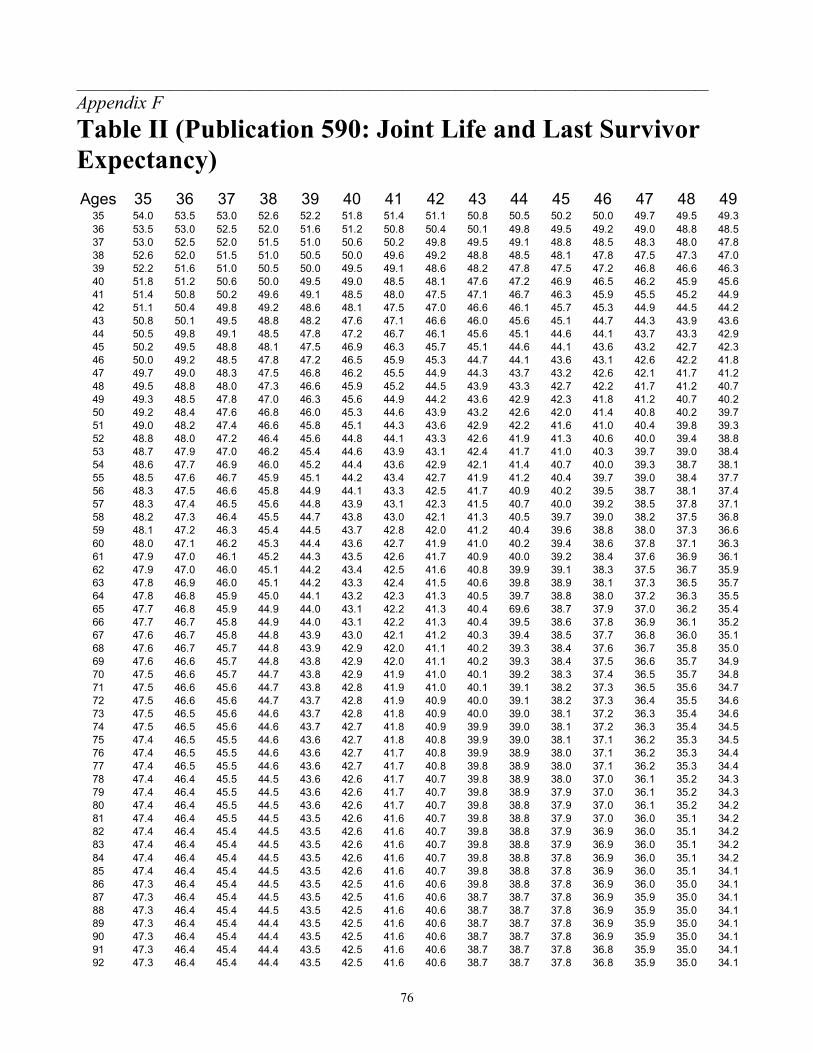

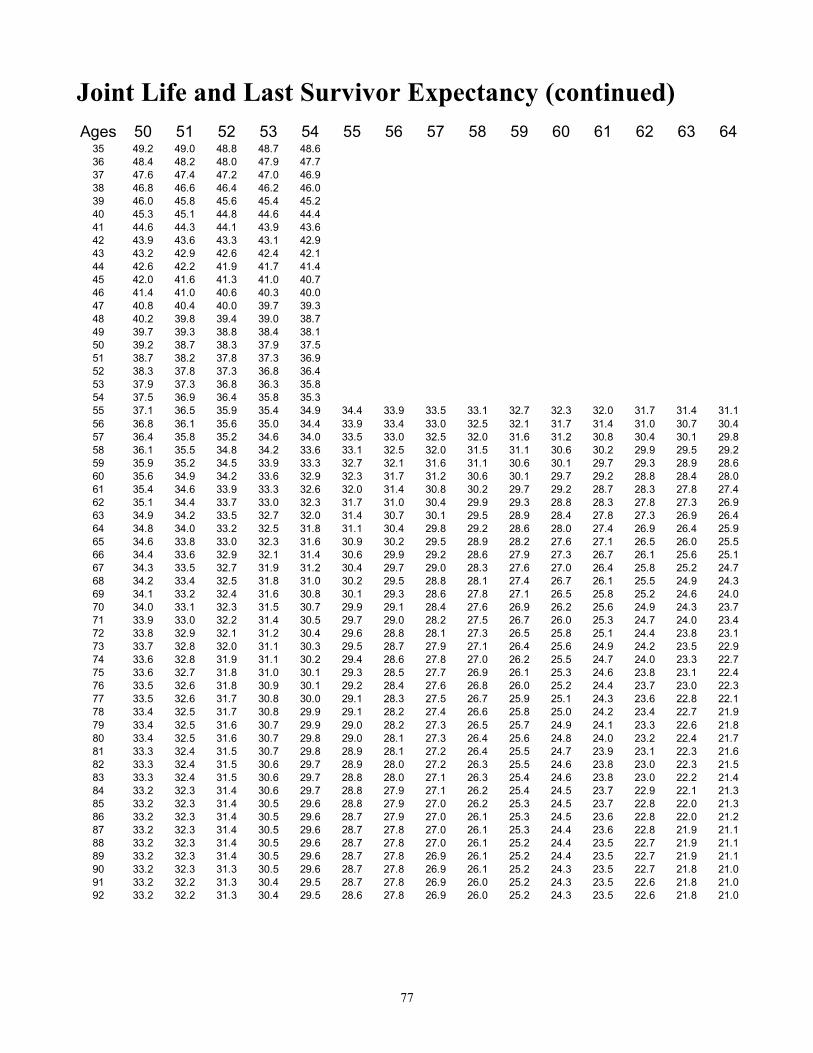

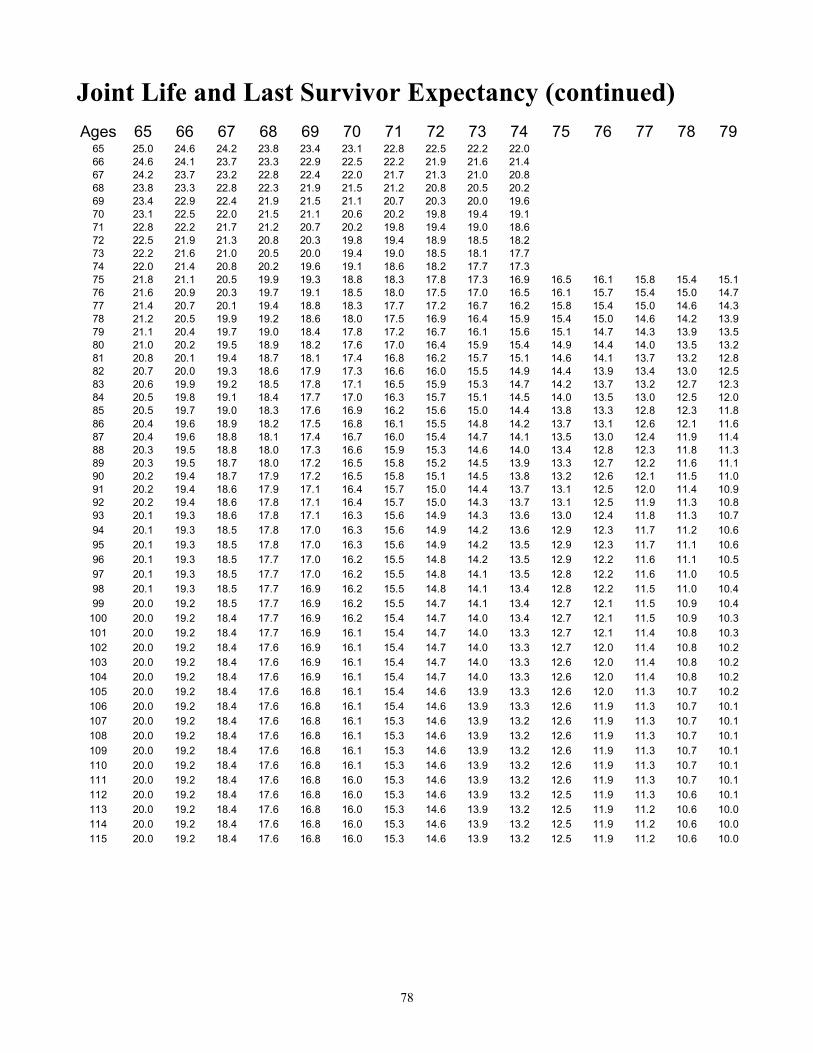

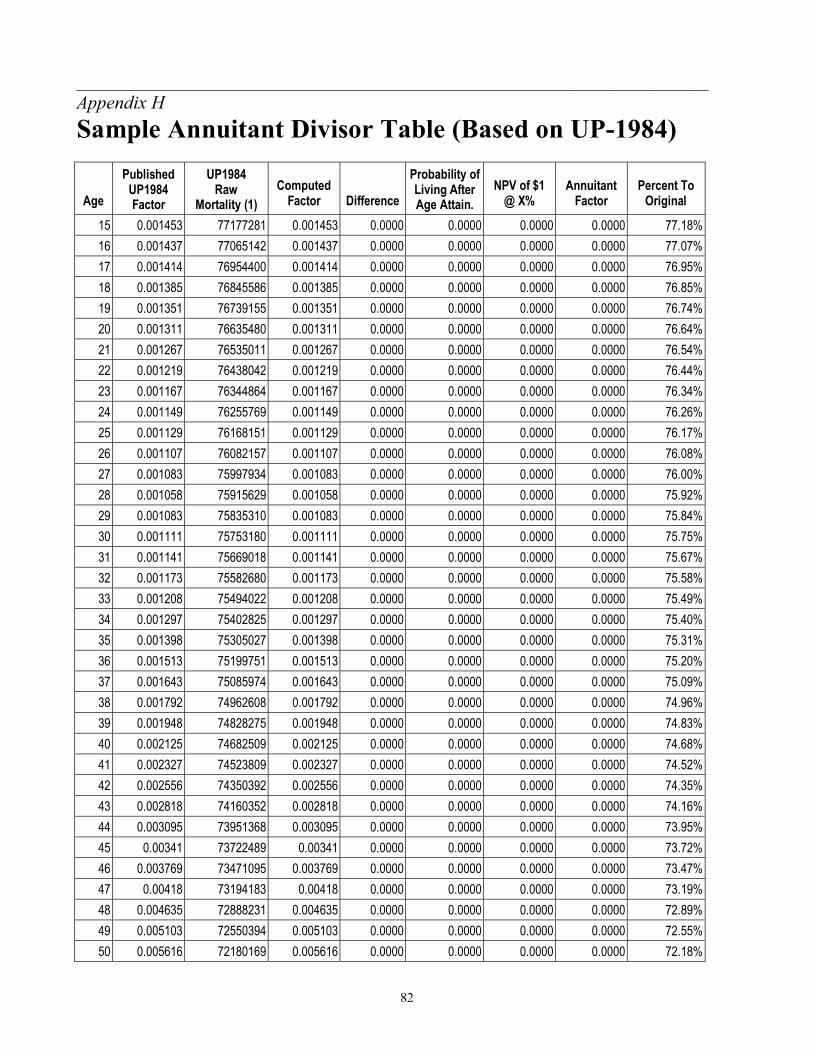

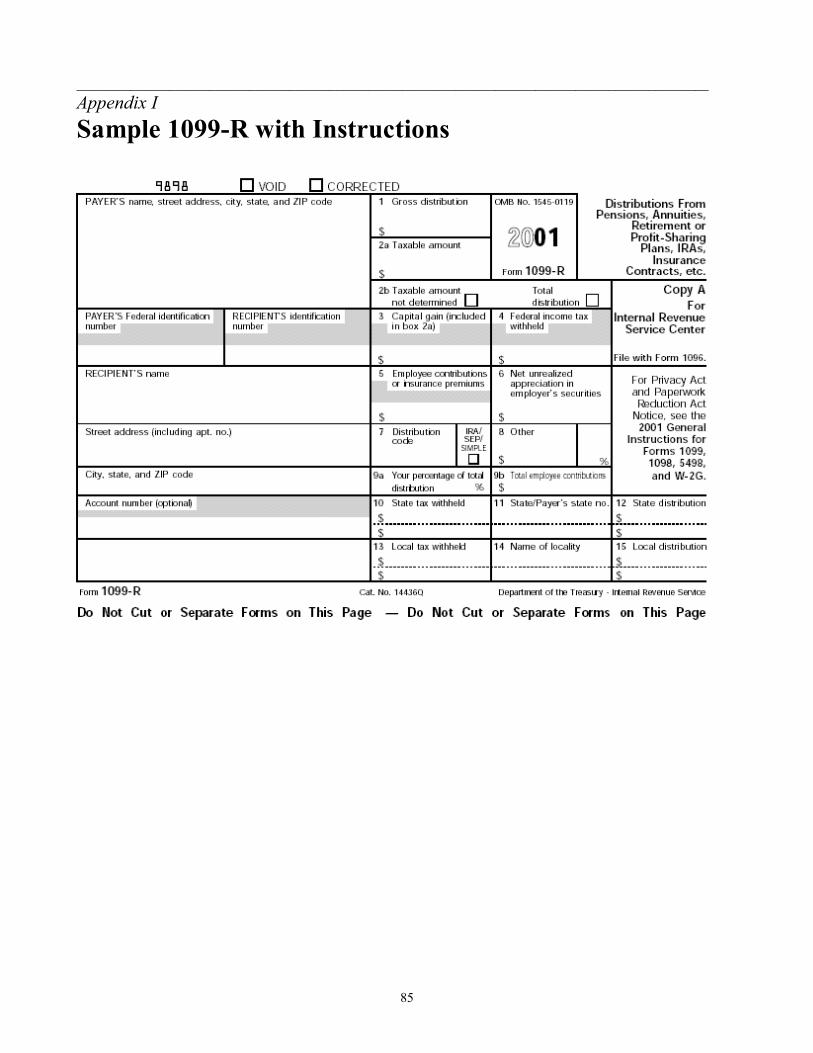

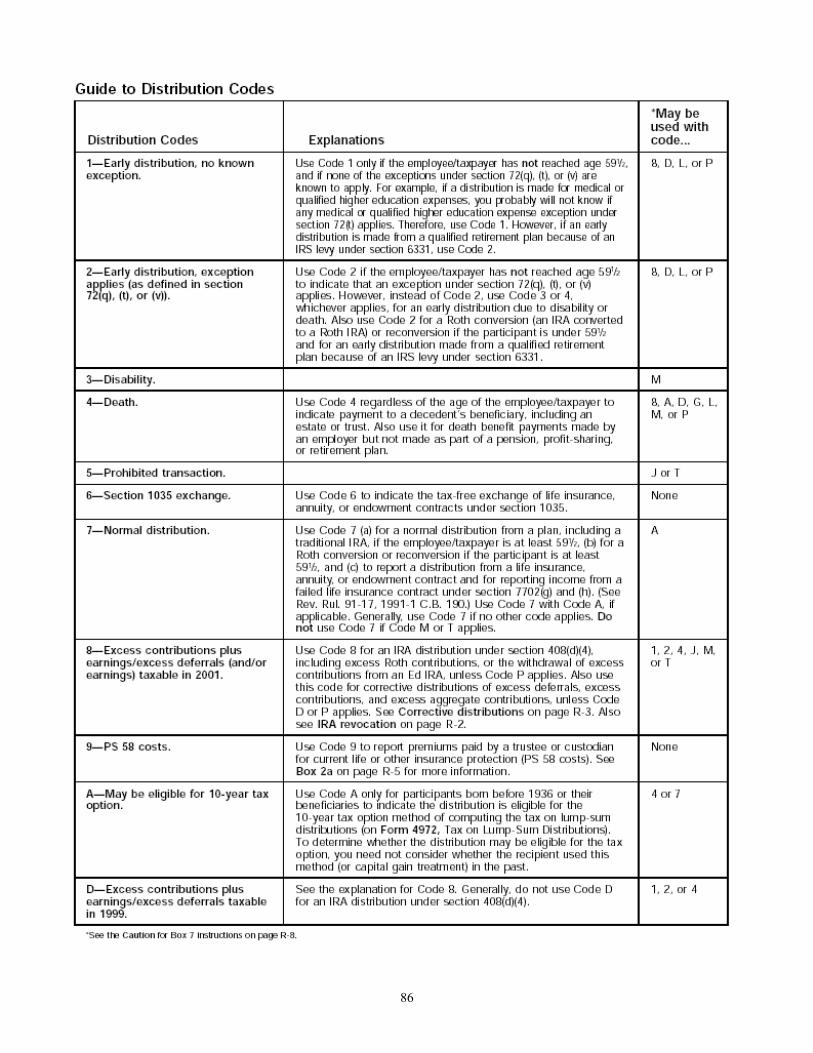

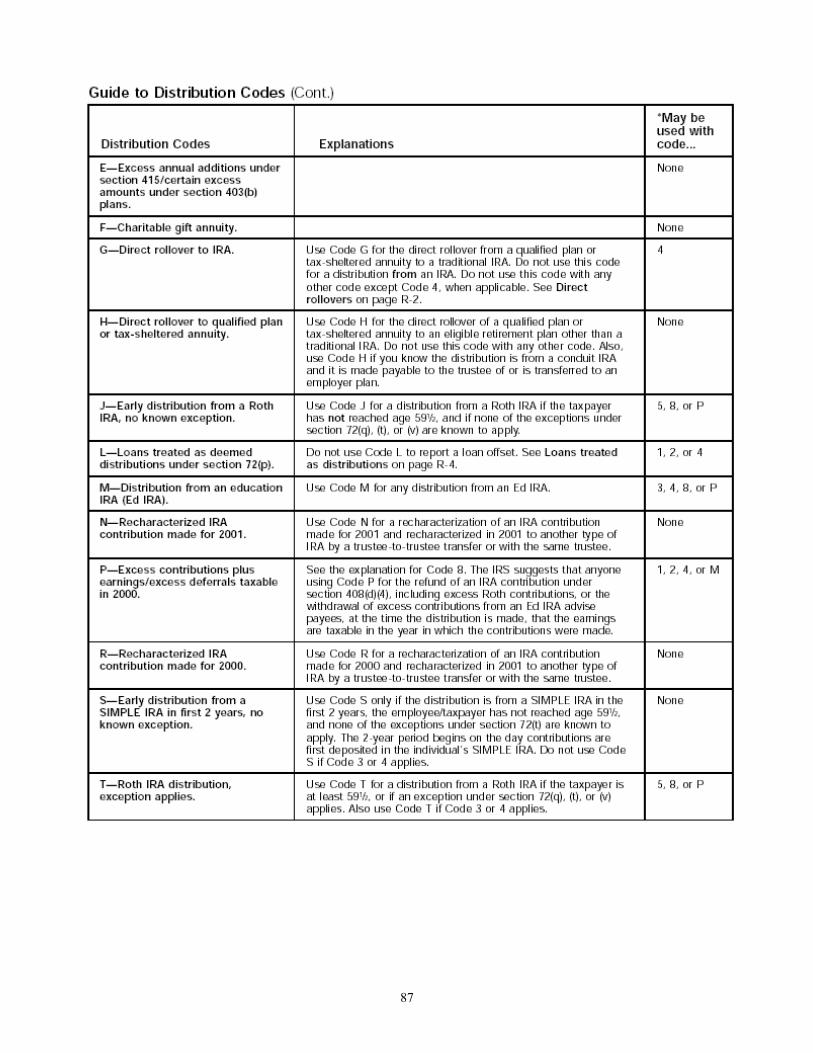

Appendix D: Excerpt from IRS Publication 590........................................................................71 Appendix E: Table I from Publication 590: Single Life Expectancy ..........................................75 Appendix F: Table II from Publication 590: Joint Life and Last Survivor Expectancy...............76 Appendix G: UP-1984 Mortality Table .....................................................................................79 Appendix H: Sample Annuitant Divisor Table (Based on UP-1984)..........................................82 Appendix I: Sample 1099-R with Instructions ...........................................................................85 Appendix J: Sample Form 5329 with Instructions .....................................................................88

Glossary ...................................................................................................................94

vi

________________________________________________________________________________________________

Introduction At the dawn of the twenty-first century, many taxpayers have acquired substantial retirement assets in a variety of tax-deferred vehicles such as:

• Employer-sponsored plans, such as profit sharing plans, 401(k) plans, and the conversion or lump-sum distribution of older defined benefit plans.

• Personally initiated traditional individual retirement accounts, (IRAs) including those funded by annual contributions and rollovers.

• Simplified employee pension accounts (SEPs).

• Recently created Roth IRA accounts, through both regular annual contributions and conver-sions from traditional IRAs.

More and more frequently, taxpayers in their thirties, forties, and early fifties are voluntarily (or involuntarily) contemplating some form of early retirement and are perplexed as to how they can ac-cess their tax-deferred assets without undue tax burden, as required by the Internal Revenue Code (IRC).

As of October 2001, IRC §72(t) now provides 12 reasons or exceptions that qualify taxpayers to withdraw monies from their 401(k)s or IRAs (collectively called “deferred accounts1”) and avoid the 10% surtax. These exceptions generically fall into two types: transaction specific and process/multi-year. There are seven transaction specific exceptions, which will be discussed briefly later on the text. As an example, exception #10 is the ability to withdraw some monies while you are unemployed and need to make health insurance premium payments2. All seven of these transaction-specific exceptions are either severely limited in scope or are present for coordination purposes with other parts of the IRC. Conversely, the focus of this text is to closely examine the other five “process” or “multi-year” exceptions. They are:

• §72(t)(2)(A)(i) Age 59½

• §72(t)(2)(A)(ii) Death

• §72(t)(2)(A)(iii) Disability

• §72(t)(2)(A)(iv) Substantially equal periodic payments (“SEPPs”)

• §72(t)(2)(A)(v) Separation of service at age 55

These five code subsections deal very specifically with how a taxpayer (or his or her estate) may commence withdrawals from 401(k)s, IRAs, and other deferred accounts and avoid the application of the 10% surtax on such distributions.

Within this text, you will find issues and solutions that the general public, professional accountants, and lawyers seldom confront. Further, due to a general absence of concise and practical information on 1 Within this context, we include all savings plan type accounts, of a “defined contribution” nature, which are qualified un-der various sections of the IRC §§401-424. As always there is an exception, that being Roth IRAs, which are separately discussed in Chapter 3 due to their unique characteristics. 2 IRC §72(t)(2)(D)

vii

this subject, many professionals periodically end up in a “reinvent the wheel” mode. Every time the wheel gets reinvented, it tends to look a little different—sometimes better, sometimes worse—than the last wheel. This is somewhat dangerous in that, as we will discover later, making a mistake in theory or practice in this area can be extremely costly. We are faced with IRC sections that are becoming more popular in their application coupled with an absence of concise authority, further coupled with an ab-sence within the IRC to correct mistakes.

The scope of this text covers a variety of what we will collectively call deferred accounts. These include all forms of §401(a), §403(b), and §401(k) plans as well as virtually all IRA types, SEPs and SIMPLEs. Although §401(a) and §403(b) cover both defined-benefit and defined-contribution plans of various types, this text deals only with defined-contribution plans and accounts3. Frequently, we will use the specific term of “IRA” in an example. The reader should assume that the example applies equally to all types of deferred accounts unless there is a notation to the contrary.

The audience for this text is twofold: individual taxpayers and professionals. More and more individuals are contemplating or working through the financial issues of early re-tirement and need to withdraw from deferred accounts before the age of 59½. This text should answer almost all your questions in this circumstance. Professionals, primarily accountants, and lawyers cur-rently have no place to go when a client presents a situation requiring the implementation of §72(t)(2)(A) issues. Similarly, this text should solve almost all of those questions. However, as is need-less to say, it is always possible for a client to present a permutation of facts that will cause the answer to become unclear.

We have attempted to make this text as thorough as possible. Unfortunately, most of the authority written on §72(t)(2)(A) is spread over a variety of document types and locations—many of which would be unfamiliar to the average taxpayer. As a result, whenever possible, we have included the lit-eral text, tables, and other computations in the appendices.

Finally, we have made every attempt to explain the relevant theory and then bring that theory down to a practical level such that all readers should be comfortable with the basic concepts as well as the computational nuances. Ninety-nine percent of all published literature on “deferred accounts” is either persuasive in na-ture—meaning a focus on why you should have an IRA or why you should contribute to your em-ployer sponsored 401(k) plan—or it is focused on how you should manage these deferred assets during their accumulation years, e.g. should you buy stocks, bonds, mutual funds, etc. To the best of this au-thor’s knowledge, there is no other comprehensive literature or writing available on getting your money out; particularly on getting your money out early. That is what this text is all about. Those read-ers specifically interested in SEPP mathematics can jump forward to Chapters 4 through 7, all other readers are encouraged to read each chapter. The author is the first to admit that in-depth discussions on §72(t)(2)(A) are, on a scale of one to 10, a 13 in the dry reading department. As a result, we have occasionally inserted some humor, so eve-ryone can stay awake. On the other hand, humor can be dangerous, as someone can always be of-fended. We mean no offense, malice, or harm in this regard. 3Defined-benefit plan payments and annuities are ineligible for treatment under §72(t). Instead, these plan types are handled by IRC §72(q)(2) and are outside the scope of this text. However, as a general comment, almost all of the exceptions found in §72(t) are repeated in §72(q) to afford the same tax treatment for taxpayers making withdrawals from defined-benefit plans.

viii

________________________________________________________________________________________________

Second Edition This is the second edition of the text. The first was published September 2000. The second edition reflects all changes in the IRC during the intervening period. Further, the second edition has new or expanded sections on all 12 exceptions for avoidance of the 10% surtax, a new chapter covering Roth IRA penalty tax circumstances and the mechanics of implementing the “Net Unrealized Appreciation” method, and updates for private letter rulings issued in the last 16 months that periodically give us ad-ditional or new insights into IRS thinking on specific tactics. In addition, the author has attempted to incorporate many of the reader suggestions from the first edition, typically in the area of attempting to make some of the more technical passages a little easier to understand.

Unfortunately, the second edition grew in size to almost one hundred pages compared to the first edition size around seventy-five pages. Readers, don’t despair; the subject matter did not get 33% more difficult over the past year; rather, the breadth of material covered has been materially expanded as noted above. Further, our objective (in both editions) has always been to treat this subject exhaustively, primarily because readers have no place else to go. As a result, it is unlikely that anyone needs this whole text because of its dictionary or reference book like nature.

________________________________________________________________________________________________

Disclaimer In a way, it is unfortunate that books of this nature require disclaimers, but such is today’s legal environment. We have made every effort to be accurate and believe that to be the case as of October 2001. Unfortunately, the IRC and related documents of authority are ever-changing. As a result, in some small fashion, this text has a high probability of being out-of-date within several months to a year. As a result, we can offer no prospective promises regarding accuracy beyond the date of publica-tion. Recognizing that this does not really help the reader, we suggest that serious readers intent on im-plementing one or more of the strategies outlined in this text should confirm to themselves that they are in fact dealing with the most current set of facts and applicable law. The easiest way to do this is to hire the expertise of a tax accountant or a tax attorney who is conversant on these topics. ________________________________________________________________________________________________

Biographical Information William J. Stecker, (Bill), earned a bachelor’s degree in Finance and Applied Mathematics in 1971 and a Masters of Science in Accounting from DePaul University (Chicago, Illinois) in 1983. He is a Certified Public Accountant since 1980 and a member of American Institute of Certified Pubic Ac-countants as well as a member of both the Illinois and Colorado State Societies. Bill has spent 30 years in accounting, finance and related fields. Further, he has particular in-depth knowledge on this subject, having made multiple and successful private letter ruling requests and determination letter requests to the Internal Revenue Service.

ix

Bill and his wife, Mary, own The Marble Group, Ltd., an accounting, tax, and financial consulting group based in Colorado. Bill devotes most of his time to tax issues, specializing in retirement plan and participant issues—primarily §72 and §§401-424 of the IRC. You can send your inquires to: The Marble Group, Ltd., 30671 Bearcat Trail, Conifer, Colorado 80433 or [email protected] or [email protected].

1

________________________________________________________________________________________________ Chapter 1 Current Law In this chapter, we present the currently available resources that offer guidance on IRA withdraw-als that are not subject to penalties. These sources create something of a rule book. To help clarify these technical passages, we’ve added a brief explanation of each citation. Further, this chapter will cover all 12 exceptions and conclude with an introduction to Substantially Equal Periodic Payments, (SEPPs), exception #4.

Internal Revenue Code Internal Revenue Code (IRC) §72(t)(1) imposes a 10% surtax on all withdrawals from deferred ac-counts. Immediately following, however, IRC §72(t)(2) grants a variety of exceptions to §72(t)(1). It is important to remember that this is one of those sections of the IRC that was intentionally drafted in re-verse, e.g. a 10% surtax will always apply unless the taxpayer fully meets one of the exceptions identi-fied in §72(t)(2)(A) or elsewhere within §72(t). As a result, if the taxpayer does not fully satisfy an ex-ception, then the 10% surtax is re-applied by the Internal Revenue Service (IRS) without any need for further statutory action.

Exception #1 Age 59½ The best known exception is achieved by attaining the age of 59½4. This exception would appear, on its face, to be rather easy to apply, e.g. make a withdrawal after you are 59½ and you will not be subject to the 10% surtax. However, there are two very specific rules that apply:

• The IRS is required to make a literal age interpretation here because it is the IRC which spe-cifically says, “made on a day on or after the date on which the employee attains the age 59½.” So when do you have your 59th and ½ birthday? Exactly 183 days after your 59th birthday. As an example, if your birth date is April 26, 1946, your 59½ birthday is October 26, 2009. A withdrawal made on this date or later will be fine; a withdrawal made on October 25, 2009, or earlier will be subject to the 10% penalty5.

• As we will learn later, if you are making substantially equal periodic payment distributions sub-ject to IRC §72(t)(2)(A)(iv), exception #1 may be held in abeyance for some amount of time until all of the requirements of exception #4 are fully satisfied.

Exception #2 Death6 Death, although never really a desirable outcome, is usually a fairly straight-forward event; some one either is or is not deceased. This exception, however, is a good time to raise two topics: one, the IRC versus the IRS, and two, the concept of playing audit lottery. 4 IRC §72(t)(2)(A)(i). 5 Many other sections of the IRC are written in a manner that examines a taxpayer’s “highest attained age” within a particu-lar tax or calendar year. This is not one of those situations. Instead, the IRS is required to and does measure to the day. 6 IRC §72(t)(2)(A)(ii).

2

• By the time the reader reaches the end of this text, it will become apparent that there is often considerable latitude in the implementation of these exceptions but in other circumstances it will appear as if the rules switch around and become unduly harsh and restrictive. The reason for this lies in determining who or what is the prevailing authority on an issue. When the words are embodied in the IRC, then the IRS has no alternative but to take a very literal interpretation of the law—thus, this whole stickiness on when does some one truly turn age 59½.

Conversely, there are many circumstances where the IRC is vague or may embody language like, “based on regulations as issued by the Commissioner.” In this later case, decision-making authority is actually transferred from Congress to the IRS on the belief that the IRS is better at examining the details of a situation and is better qualified to issue appropriate regulations and opinions. In these later cases, we will find considerable additional flexibilities afforded to the taxpayer.

• Everyone would like to win the Powerball lottery, but this is about as likely as being struck by lightning three times on the same day. On the other hand, no one wants to win in the IRS lot-tery. Further, should your Social Security number magically turn up7, it is very important to know which lottery you are in. In the arena of auditable issues on §72(t) there are really two different lotteries: the congres-sional lottery and the IRS lottery. In same context as above, if you are audited and the central issue to be resolved lies in the interpretation of the IRC as drafted by Congress, YOU WILL LOSE! The IRS as well as tax courts and federal district courts will take a literal and restrictive construct of the IRC language. In short, there is zero maneuvering room. Conversely, if the central issue to be resolved lies in the interpretation of the IRC through the IRS’s issuance of regulations, rules, notices, etc., you may then stand a chance greater than zero of prevailing; that chance, however, is still relatively small. Sometimes the temptation to venture into “audit land and gray areas of the IRC” may appear to be a good business decision. This is not one of them. As we will discuss later in the text, the body of knowledge is not in the taxpayer’s favor, and in this particular section of tax law, there are virtually no corrective measures available to the taxpayer when the IRS prevails. There is no way to put back the improper distributions and amend your tax returns. Further, there isn’t even any negotiating room in the computation of the penalties and statutory interest due. In summary, §72(t) is not the place to push the envelope as the downside risks are substantial and almost always, non-negotiable.

The second exception, embodied in §72(t)(2)(A)(ii) says in part, “made to a beneficiary…on or af-ter the death of the employee.” If you are audited, simply make sure to take a copy of the signed death certificate with you to the examination.

Exception #3 Disability8 The full text of exception #3 says, “attributable to the employee’s being disabled within the mean-ing of subsection (m)(7).”

7 There is absolutely no evidence that taking early withdrawals from your deferred-asset account(s) in any way influences or increases your likelihood of an audit. However, should you be audited, there is a virtual 100% probability that your with-drawals will be closely examined to insure full compliance with the law. 8 IRC §72(t)(2)(A)(iii).

3

“Attributable” means that in order to use this exception, you, personally, must be physically and/or mentally disabled according to the following definition:

What does the preceding mean? First, with certainty, if you choose to use this exception and are subsequently audited, you will be required to present external proof and evidence that you are disabled. Second, the IRS has issued a fairly in-depth regulation on this subject. It says in part:

The above Code and regulation language imply several tests or hurdles that must both be met or exceeded in order to qualify for this exception. They are:

• Effectively, the disability must be total as opposed to partial. As an example, some one may be disabled in all outward appearance; however, if that person were capable of (irrespective of whether he does or not) returning to work on a part-time basis; then that person would not be considered disabled under this definition.

• The disability is always measured in context to the individual’s pre-disability occupation. As an example, two brothers are in a vehicular accident resulting in both brothers becoming para-plegic; however, both subsequently fully recover but for the use of their legs. One brother is a professional football player and the other is a surgeon. The former is disabled; the later is not.

The IRS will consider any and all external evidence you produce but is not necessarily bound or obligated to honor that evidence in making its determination. Such evidence might include doctor statements, employer statements, proof that you are already collecting private disability insurance, and Social Security disability proceeds—Social Security being the most persuasive evidence. Further, be-ing disabled has been classified as a “facts and circumstances” test by the IRS; accordingly, they will not rule in advance on this issue for individual taxpayers. As result, this author believes that using ex-ception #3 is a fairly dangerous strategy unless the disability is beyond a shadow of a doubt. With any lesser disability, the taxpayer is well advised to seek the professional opinion of an attorney who spe-cializes in disability matters.

“In determining whether an individual’s impairment makes him unable to engage in any substantial gainful activity [emphasis added], primary consideration shall be given to the nature and severity of his impairment. Consideration shall also be given to other factors such as the individual’s education, training, and work experi-ence. The substantial gainful activity to which section (m)(7) refers is the activity, or comparable activity, in which the individual customarily engaged prior to the arising of the disability….”

IRC Reg. §1.72-17A(f)

“…an individual shall be considered to be disabled if he is unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment which can be expected to result in death or to be of long-continued or indefinite duration. An individual shall not be considered to be disabled unless he furnishes proof of the existence thereof in such form and manner as the Secretary may require.”

IRC §72(m)(7)

4

Exception #5 Separation of Service at Age 55 Wait a minute, what happened to exception #4? Number 4—substantially equal periodic pay-

ments—is by far the most difficult of the process/multi-year exceptions to understand and is the most difficult of all of the exceptions to implement correctly. As a result, we are going to skip #4 for the time being and finish the discussion of the remaining exceptions first.

In almost all cases in this text, we treat “deferred-plan assets” (e.g. assets accumulated within plans qualified under §401(a), §401(k), §403(b), and IRAs) and IRAs as being the same and accordingly re-ceive the same treatment under §72(t)(2)(A). IRC §72(t)(2)(A)(v) is an exception to the general rule. Subsection (v) provides an ability for a separated employee to commence withdrawals provided he is 55 or older when separated from the employer who is the plan sponsor from which the now terminated employee wishes to make withdrawals. Unfortunately, §72(3)(A) says in part that §72(t)(2)(A)(v) “does not apply to distributions from an individual retirement plan.9” This simple sentence effectively forces a split between plan assets and IRA assets and makes subsection (v) available only to plan assets and disallows the same treatment for IRAs. Notice 87-13 provides a further amplification of how to interpret §72(t)(2)(A)(v) by saying:

Finally some reasonably clear language. As we will learn when we get into the approved methods and mathematics of SEPPs, SEPPs by their nature are restrictive. Here, we can skip all of the SEPP rules if the taxpayer can comply with the rules enumerated in Notice 87-13. What are those rules? 1. The taxpayer must terminate employment from his or her employer in the same tax year as he or

she attains the age 55 or greater. This is not the same as being 55 when you quit. Instead, one need only reach age 55 anytime in the same year, even if attaining age 55 occurs six months after termi-nation. Thus a theoretical minimum age exists of 54 years and two days. If your birthday is De-cember 31, you could quit on January 2 of the year you turn 55.

2. The assets withdrawn must be withdrawn from the plan sponsored by the employer from which the employee has just terminated. This is critical. Further, there are two subsidiary issues of equal im-portance:

• If the taxpayer terminates employment with the employer/plan sponsor and immediately rolls the plan assets into an IRA; the IRA assets, though they did originate from the qualified plan become ineligible for treatment under §72(t)(2)(A)(v). The assets absolutely must remain in the plan. Thus, as a caution, taxpayers should resist the sales pitches from various financial advo-cates that ex-employees should quickly roll over their plan assets into IRAs in order to take ad-vantage of all the investment vehicles that are available through an IRA and might not have been available inside the plan. If you are 35, go ahead; if you are 54½, this can be a disaster.

9 Why this distinction is made between plan assets and IRA (definitionally not a qualified plan) assets remains a mystery.

“Section 72(t) (as added by TRA '86) applies an additional tax equal to 10 percent of the portion of any ‘early distribution’ from a qualified retirement plan...that is includible in the taxpayer’s gross income.... A distribution to an employee from a qualified plan will be treated as within section 72(t)(2)(A)(v) if (i) it is made after the em-ployee has separated from service for the employer maintaining the plan and (ii) such separation from service occurred during or after the calendar year in which the employee attained age 55.”

IRC Notice 87-13

5

• Working for a single employer for thirty or more years is pretty much an event of the past. As a result, it is not uncommon for a taxpayer to have three, four, or even five 401(k) plans and/or related conduit IRA accounts10. Further, it tends to be the oldest accounts that are the biggest because they have had the longest time to grow. Nonetheless, Notice 87-13 tells us that we can make withdrawals only from the plan account from the employer through which the employee just separated. How do we get at the plan assets from the prior employers? The easiest solution is to perform a series of rollovers. Roll the assets from either prior employer plans or conduit IRAs forward into your current employer’s plan. Further, these rollovers need to made before you terminate, as rollovers are often prohibited for terminated plan participants. On its face, this does appear a little illogical. How can it make a material difference if all the money is in the current plan versus spread out in four different plans. Unfortunately, this is one of those situations where form does govern substance.

Thus, taxpayers who are 55 (or will be 55 during the current tax year) and are separating from ser-vice from their employers11 should pause and think very carefully about this issue. There is no clear-cut obvious or winning decision here, as there are pros and cons to each decision path. The biggest ad-vantage is that the taxpayer need not pay any attention to SEPPs and instead can withdraw any amount at any time12. The biggest disadvantage is that most 401(k) plans limit investment choice (often to mu-tual funds only), which the taxpayer may not like. Any taxpayer in the 54½ to 59½ age window leav-ing employment should seek professional help before automatically rolling over 401(k) assets into an IRA.

Exceptions #6 Through #12 These exceptions are referred to as the transaction exceptions in that they tend to be very limited in scope and are often one-time events.

• #6 §404(k) Stock Dividends13. This will likely occur whenever you are member of an older §401(a) plan in which the plan sponsor/employer contributes employer stock to the plan. Fur-ther, the plan was drafted in a manner that requires that when the corporation declares a divi-dend, the dividend must be paid on the securities held in the plan. Strangely enough, the actual dividend dollars cannot be paid into the plan itself but must instead be paid directly to plan par-ticipants. In short, almost all readers need not concern themselves about this exception. If you are subject to it, your plan administrator will let you know how to declare the dividends re-ceived as income and specifically how to avoid the 10% surtax.

10 We use the term “conduit IRA” account here to mean a temporary IRA account housing the assets of a prior employer’s qualified plan, usually waiting to become eligible to participate in a new employer’s 401(k) plan. 11 In today’s economic environment, many taxpayers are being offered “early retirement” packages from their employers. Often, an employer will be willing to structure severance pay for an early retiree such that the periodic severance pay and therefore employment extends until the first weeks of January of the tax year in which the taxpayer will turn age 55 thus making this exception a viable alternative. 12 This is all predicated on being a participant in a qualified plan that provides both for periodic payments to participants and a reasonable and cooperative plan administrator. Each taxpayer facing this situation should check with his or her re-spective plan administrator as soon as possible to have a detailed discussion regarding plan provisions, particularly the abil-ity to support and process periodic payments. 13 IRC §72(t)(2)(A)(vi).

6

• #7 Tax Levies14. Should you be unfortunate enough to be subjected to a federal tax levy15, Congress has graciously determined that the 10% surtax will not be due. However, there are several catches: one, regular federal income tax will still be due upon the distribution of the IRA; and two, the distribution of the IRA must be pursuant to a court ordered levy and the dis-tribution must be made directly to the IRS. Conversely, if the IRS sends you a deficiency notice or otherwise obtains a judgment against you and you voluntarily cash in an IRA to satisfy the deficiency or judgment, this exception will not apply.

• #8 Medical Expenses16. You may make distributions from your IRA up to the amount of your qualifying medical expenses17 and escape payment of the 10% penalty remembering that regu-lar federal income tax will still be due on the amount distributed. However, the amount one can withdraw using this exception is limited to those qualifying medical expenses that are in excess of 7½% of your adjusted gross income.

• #9 Qualified Domestic Relations Orders18, (QDROs). A QDRO is a court order signed by a judge typically as a result of a divorce proceeding. With respect to your IRA, the judge can conceivably sign two different types of QDROs. The judge may sign an order requiring the di-vision of your IRA into two IRAs; one for you, and one for your spouse, where the character of the newly created IRA remains the same simply changing the name on the new account. This type of IRA division is governed by IRC §414(p) and is a nontaxable event. Or, the judge may order a payment stream (thus creating a taxable event) from your qualified plan19 to one or more alternate payees—typically, an ex-spouse and/or children. In this case a taxable event has occurred requiring that income tax be paid on the amounts distributed each year. Fortunately, the 10% surtax is excused, irrespective of your age.

• #10 Payment of Health Insurance Premiums While Unemployed20. If you have been or were unemployed for 12 or more weeks, you can make withdrawals from your IRA up to the amount of your health insurance premiums for the period during which you were unemployed.

• #11 Higher Education21. Generally speaking, distributions from your IRA can be made to pay for post-secondary qualifying educational expenses for yourself, your spouse, and your chil-dren. Seeking professional assistance is advised as the “qualifying” expenses part of this rule does get a little tricky.

14 IRC §72(t)(2)(A)(vii). 15 This is tantamount to the IRS performing asset seizure, where it will typically take your residence, your cars, your jew-elry, and, by the way, your IRA as well—all pursuant to court order. 16 IRC §72(t)(2)(B). 17 See IRC §213; typically the same medical expenses you would place on Schedule A -- Itemized Deductions. 18 IRC §72(t)(2)(C). 19 Please note the change in language here to “qualified plan.” IRAs are not eligible for this exception. 20 IRC §72(t)(2)(D). 21 IRC §72(t)(2)(E).

7

• #12 First Home Purchases22. Generally, you may withdraw up to $10,000, per lifetime, to purchase a principal residence—provided that you have not owned a home in the last 24 months. The detail rules here can get very complex.

A word of caution. Exception rules #6 through #12 all vary in complexity, each in its own right. Above is a brief synopsis simply to let taxpayers know that they exist and may be used when the proper conditions present themselves. Exceptions can generally be used independent of another; how-ever, there is always one right way and usually a dozen wrong ways to implement an exception. Al-though some of these exceptions appear to be fairly generous, particularly for distressed circumstances, it is advisable to seek professional assistance on any and all of these because an exception, incorrectly implemented, will be disallowed and the 10% surtax plus interest will be re-imposed. Further, as with all of the exceptions in §72(t), there are no corrective measures that can be taken once an exception has been improperly implemented.

Exception #4 Substantially Equal Periodic Payments IRC §72(t)(2)(A)(iv) introduces us to a lesser known and the least understood exception—the con-cept of a “substantially equal periodic payment” (SEPP). Of particular importance is what the IRC says about this concept:

Note: A complete excerpt of IRC §72(t) is included in Appendix A. We can learn a lot about SEPPs from just this one sentence. It is actually easiest to take the term “substantially equal periodic payments” and deal with each word in reverse order. PAYMENTS in this case mean a dollar23 withdrawal from a deferred account. Further, because of the plural, we can infer that there will need to be more than one payment. PERIODIC implies that each withdrawal will occur over some set of defined intervals. Immedi-ately following we find the language “not less frequently than annually.” As a result, we know the out-side limit with certainty—a minimum of once a year. However, there is no guidance about more fre-quently than annually. As we will learn later, monthly and quarterly withdrawals are fine as well. EQUAL implies that the withdrawals from the deferred account will be of equal dollar amounts.

SUBSTANTIALLY is potentially the most interesting word in the sentence. It becomes a modifier to the word “equal.” If Congress had intended for these payments to be literally equal, it would not have used the adjective “substantially.” As a result, we now have “sort of” or “almost” equal payments because we do not yet know how to interpret the word “substantially.”

22 IRC §72(t)(2)(F). 23Actually, withdrawals can be “in kind” as well as cash. All of our examples will focus on cash withdrawals or disburse-ments from one or more deferred accounts.

“…part of a series of substantially equal periodic payments (not less frequently than annually) made for the life (or life expectancy) of the employee or the joint lives (or joint life expectancies) of such employee and his desig-nated beneficiary.”

IRC §72(t)(2)(A)(iv)

8

The remainder of the definition is devoted to time span; namely the life or life expectancy of the employee24 or employee and beneficiary. We can interpret this to mean that there is an outside parame-ter at which time payments will stop. Next we need to turn our attention to IRC §72(t)(4)(A)(ii)25, which gives us some rule modifiers as follows:

Essentially, this says that, barring death or disability, if the taxpayer modifies or discontinues these SEPPs before the passage of at least five years and attaining the age of 59½, then the 10% surtax plus interest will be reimposed. As we will learn later, the word “modified” will become critical in our thinking and strategy. As a result, we can now develop a preliminary working definition of SEPPs as follows: A series of payments or withdrawals from deferred accounts that can be either exactly equal or potentially some-what dissimilar, that occur annually or more frequently, and continue for a minimum time period of five years or until the taxpayer reaches age 59½ , whichever is greater. So, if we set up a payment stream that meets all these criteria, we should be able to implement that payment stream and avoid the 10% surtax. The only other modifiers or rules to be found in the IRC are some rather obvious ones:

1. The 10% penalty, if applied, applies only to that portion of the distribution that is includible in gross income.

2. An employee must have separated from service in order to commence SEPPs that include dis-bursements from an employer plan26.

Virtually all of the remainder of this text is devoted to avoidance of the 10% penalty tax. Unfortu-nately, regular income tax (both federal and often state) is always due. After all, both contributions by employees to 401(k) plans and deductible IRAs and employer contributions to various plans as well as all of the earnings accrued through the intervening years have never been taxed. Thus, we tend to call all of these accounts and assets as “deferred asset accounts,” not “tax-free accounts.” Taxes have been 24 Frequently, the IRC uses the term “employee” in the context of one being employed and therefore a participant in a quali-fied plan. The reader can also conceptually substitute the word “owner” in the context of an IRA. 25 IRC §72(t)(4)(A) is pretty clear in the circumstance when a taxpayer, aged 50, commences SEPPs and modifies them before age 59½; he will owe back taxes and interest on 100% of the distributions. What about a taxpayer, aged 56½ who makes SEPP distributions to 59½ (3 years) and then modifies those SEPPs after age 59½? Our taxpayer is more than 59½ but has failed the five-year test. In this case, the surtax and interest will be imposed only on the three early year’s worth of SEPPs. See Pub 575, page 29, 2000 edition. 26 In order to remain “qualified” virtually all plans have “separation of service” language in them to prevent withdrawals from the plan while still employed. Some plans, however, will permit “in-service hardship withdrawals” under certain spe-cific conditions.

“ [If]...the series of payments under such paragraph are subsequently modified (other than by reason of death or disability)… before the close of the 5-year period beginning with the date of the first payment and after the em-ployee attains age 59½, or… before the employee attains age 59½, [then]...the taxpayer’s tax for the 1st taxable year in which such modification occurs shall be increased by an amount... equal to the tax which...would have been imposed plus interest for the deferral period.”

IRC §72(t)(4)(A)

9

deferred on these accounts during their accumulation or building years. Now that the taxpayer wants to commence withdrawals, the tax-deferral period ends and Congress, through the arm of the Internal Revenue Service, is standing at the door, ready to collect. Thus, we are willing to (although begrudg-ingly) to pay regular federal income tax on those distributions; however, we are unwilling to pay a 10% surtax or penalty just because we are withdrawing assets before the age of 59½.

Internal Revenue Service Publications Next on our document list is Notice 89-2527, which gives us one page of information as to what the IRS believes constitutes a “series of substantially equal periodic payments.” Finally, we start to get down to some specifics with this notice in that it provides us with three detailed methods of how SEPPs may be computed. These three methods are called the minimum, amortization, and annuity methods. Rather than get into the specifics of each here, we later devote a full chapter to these methods and the computational specifics of each. We can also take a look at Publication 59028, the IRS’s seminal text on IRAs. The relevant portion of Publication 590 is included in Appendix D. Of particular relevance is the section that is titled “An-nuities” commencing in the middle of the second page of Appendix D. Unfortunately, this reference in Publication 590 sends us right back to Notice 89-25 for detailed guidance29, which is discussed above.

Tax Court Cases Where else can we look for authority on this issue? Our next stop is the courts. Fortunately, here we find some new information in the case of Arnold v. Commissioner30. The real issue decided in this case was a precise definition of the five-year rule embodied in §72(t)(4)(A)(ii). The Arnolds contended that “five years” meant “five tax years;” the Commissioner contended that “five years” meant a literal interpretation of the calendar, e.g. if your first withdrawal was on 5/1/92, then five years later is 5/1/97 or 1826 days later. The Commissioner prevailed. There are other tax court cases that cite or make ref-erence to §72(t) but are not relevant in refining our definition of SEPPs.

Private Letter Rulings Our last source of authority lies in the private letter rulings (PLRs) issued by the IRS; of which there are approximately 75. We face a bit of a dilemma, however, when delving into PLRs. Every PLR issued by the IRS starts with “This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code.” There is actually good reason for this language. PLRs are a response of law (or at least the IRS’s position of the law to which they are essentially bound) to a particular fact set from a particular taxpayer. Rarely are circumstances identical, and it would be much too easy for tax- 27 1989-1 Cumulative Bulletin 662. The relevant portion is contained in full text in Appendix C. 28 Every individual and practitioner should keep a copy of Publication 590 handy. It is a comprehensive text on IRAs and other retirement issues. 29 As we will ultimately learn, the IRS thinks “detailed guidance” is the logical equivalent of providing some one a map of the solar system in order to help locate North Platte, Nebraska. 30 111 TC 250; 1998 U. S. Tax Ct. Further, what appears to be of significance is the IRS’s very stringent interpretation of the IRC; versus its somewhat relaxed interpretations of IRS-originated documents on other §72(t) issues.

10

payer number two to use taxpayer number one’s PLR with a slightly modified fact set. Unfortunately, it can be that slight modification in the fact set that nullifies or reverses the essence of the PLR.

In addition to the obvious benefit of the submitting taxpayer, PLRs are published and are therefore the IRS’s method of providing other taxpayers and practitioners a “peek in the box” as to how the IRS is thinking on an issue, without the IRS being bound by its thinking (other than to the submitting tax-payer). Thus, at one level, PLRs are worthless to us. We can never pick a PLR or two and present them as a defense to the IRS in or out of a court of law31. At another level, PLRs become extremely impor-tant. It is in PLRs that we find almost all of the meat we need to make effective tactical decisions on SEPPs. Often we can find the same issue repeating itself across multiple PLRs resulting in the same decision by the IRS. This, at least, can provide us with some comfort in our analysis.

Further, as we will see in the risk assessment chapter, there are certain basic interpretations on SEPPs that are very safe, and PLRs simply provide an affirmation of our thinking. In other areas there may be one or at most two PLRs indicating that possibilities exist in this area, but the risks are higher. Also, there are several negative PLRs32 that represent very high risk levels. Moreover, it is always pos-sible to frame the question in a manner or with a fact set for which no ruling exists. When this occurs we at least know that we are treading in virgin country, which usually represents the highest of risk environments. Based on all that we know, from the IRC down to the PLRs, we will develop a risk as-sessment profile of SEPP programs and classify those SEPP programs as either below or above a sub-jective threshold where making a new private letter ruling request may be advisable.

31 This is not entirely true. While an individual PLR cannot be admitted into evidence as a defense, a group of PLRs—treated as a group—can be admitted into evidence where the purpose of doing so is to abstract the theory espoused and its consistency throughout the sum of the PLRs while ignoring or discarding the transactional details, facts, and circumstances. 32 95% of all PLRs issued in this arena are “positive” meaning in favor of the taxpayer. Negative PLRs are unusual in that a submitting taxpayer is afforded the opportunity to withdraw or modify the PLR submission instead of receiving a negative reply. Then again, some taxpayers are simply stubborn.

11

________________________________________________________________________________________________

Chapter 2 Common SEPP Concepts Before we delve into the intricacies of individual SEPP programs, we should spend some time on the basics and concepts common to all SEPP programs. Central to all deferred accounts is the concept of timing. In exchange for the tax deferral granted in earlier years, each of us implicitly agreed to live by Congress’s implied definition of the word “retirement.” It does not matter if we like or dislike the congressional definition or are financially able to retire early; we signed on the first day we opened an IRA or made a contribution to a 401(k) plan.

Unearned Ordinary Income Congress has effectively legislated that withdrawals from deferred accounts are the logical equiva-lent of retirement33 and that retirement is essentially a time period or periods during which a taxpayer’s unearned income replaces earned income. Earned income is easy to understand; it is those monies re-ceived, typically from an employer, for your personal services, e.g. wages, salary, bonuses, and the like. Further, each taxpayer was taxed on this earned income when earned except for the contributions to deferred account savings vehicles, like 401(k) plans and deductible IRAs. By law, all the contribu-tions you and maybe your employer made to these deferred accounts as well as all earnings and in-vestment asset appreciation are reclassified as unearned income. As a result, some years later, the con-tents of your deferred account(s) are as yet untaxed34. Neither the manner or original source of the con-tributions nor the manner in which asset appreciation occurred is of significance. All withdrawals from all deferred accounts are treated as unearned ordinary income35 and are accordingly taxed at the then present graduated tax rates for ordinary income.

Age Windows In concert with indirectly defining the word “retirement,” Congress has created three time win-dows:

• Before age 59½

• Between ages 59½ and 70½

• After age 70½

33 This is not entirely true in that §72(t)(2)(A), (B), (C), and (D), as discussed in Chapter 1 contain a variety of “bad” and “good” specific/emergency situations, e.g. death, disability, education, first home purchase, etc. where the 10% surtax is waived; however, our main thrust of §72(t) is to deal with retirement situations. 34 The term “untaxed” in this context is referring to federal income tax. Conversely, if you examine your pay stub or year-end W-2 carefully, you will see that your contributions to your 401(k) plan were not federally taxed, but they were taxed for FICA/Medicare. Because contributions were taxed for FICA/Medicare on the way in, they are not taxed again on the way out. 35 There are two potential exceptions here: net unrealized appreciation (NUA) on employer securities discussed later and taxpayer basis in a deferred account. These topics are discussed later in the text.

12

Before age 59½ is called “early retirement.” During this period, Congress intentionally makes it difficult to make deferred-account withdrawals. It matters not that you were professionally successful or started a personal savings program early in life. Congress has deemed that individuals leaving the earned income workforce and substituting unearned income before age 59½ are early retirees. Con-gress further says, by implication, that this should not happen. Therefore it imposes extra taxes (namely the 10% surtax) on those individuals who make these early withdrawals. Fortunately, Con-gress did give us some narrow windows of opportunity. That is what this text is all about. Stage two, from ages 59½ to age 70½ is typically called “normal retirement.” During this period taxpayers have virtually unlimited freedom in deferred account withdrawals36. The only requirement is that the taxpayer pay ordinary income taxes on those withdrawals because the withdrawal dollars have not been previously taxed. Stage three really doesn’t have a formal name, but it starts at age 70½. At this point Congress re-verses course and, instead of making it difficult to make withdrawals, Congress mandates withdraw-als37, essentially forcing you to make withdrawals even though you might not want to. These are called minimum distribution requirements, and not meeting them is painful to the tune of a 50% excess ac-cumulations tax38.

The entire focus of this text is on early retirement withdrawals and the use of the few windows of opportunity Congress left open. Nonetheless, it is equally important to remember that your deferred accounts will live with you through each of these three different stages of tax treatment.

The Account Concept A taxpayer (or taxpayer and spouse) is almost always treated as a single taxable entity. Thus, if you think about IRS Form 1040, it starts to make a lot of sense. Through the use of a blizzard of subsidiary forms (e.g. one for interest and dividends, another for capital gains, and another for farm income) all taxpayer income eventually flows upward and lands somewhere on Form 1040. It is on this form that the whole taxpayer’s income situation is revealed and a tax is assessed. IRC §72(t) and SEPPs work in the exact opposite manner. Instead of treating the taxpayer as a sin-gle taxable entity, the taxpayer is fragmented into pieces. As we will later learn, this will often work to our advantage. SEPPs are structured, evaluated, and used on an account-by-account basis; not on an aggregate “taxpayer” basis.

For example: It is quite conceivable that a taxpayer might have three or six or nine separate de-ferred accounts. To commence SEPPs, the taxpayer will have two fundamental choices:

1. Select one of those nine deferred accounts and commence the withdrawal of SEPPs from that, and only that, account. The other eight accounts are held on the sidelines for future use at future dates.

Or 2. Select more than one of nine—up to selecting all nine—and define a SEPP universe; let’s say ac-

counts A, B, and C. SEPPs are then computed on the sum total value of all three accounts, and SEPP withdrawals can be made in any proportion from any of the three accounts defined in the

36 Previously, §4980A(c) imposed an excess distribution tax equal to 15% of the amount distributed in excess of an indexed value approximating $150,000. Fortunately, this section of the IRC was repealed effective 12/31/96. 37 See IRC §401(a)(9)(C). 38 See IRC §4974(a).

13

universe. Once a universe is defined, however, and the first SEPP withdrawal has occurred, the contents or membership of the universe is frozen and cannot change. For example, after a with-drawal has been made, deferred account X cannot be added into the mix of accounts A, B, and C.

This concept of fracturing the taxpayer’s deferred accounts applies only before the taxpayer reaches age 59½ and will work to our advantage in ultimately designing multiple SEPP programs that can run concurrently. Between the ages of 59½ and 70½, this concept becomes irrelevant. When the taxpayer reaches age 70½, Congress reverses course and requires that all deferred accounts be aggre-gated together for purposes of measurement and computation of minimum mandatory distributions.

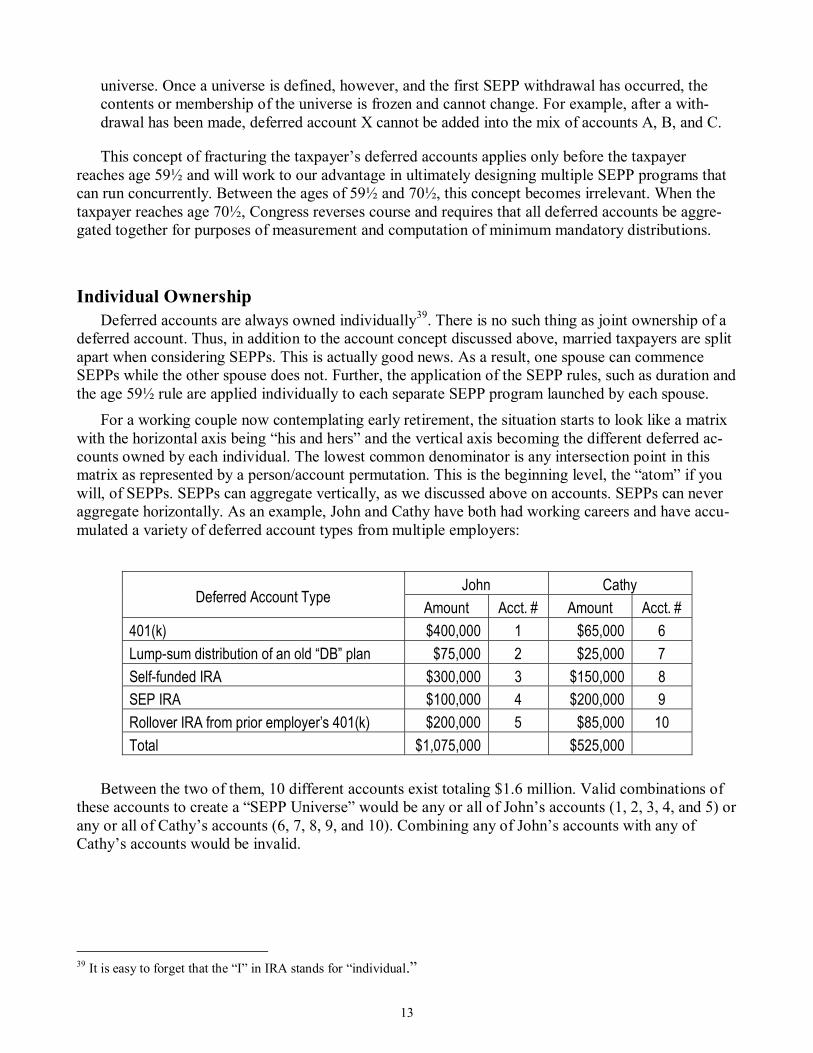

Individual Ownership Deferred accounts are always owned individually39. There is no such thing as joint ownership of a deferred account. Thus, in addition to the account concept discussed above, married taxpayers are split apart when considering SEPPs. This is actually good news. As a result, one spouse can commence SEPPs while the other spouse does not. Further, the application of the SEPP rules, such as duration and the age 59½ rule are applied individually to each separate SEPP program launched by each spouse. For a working couple now contemplating early retirement, the situation starts to look like a matrix with the horizontal axis being “his and hers” and the vertical axis becoming the different deferred ac-counts owned by each individual. The lowest common denominator is any intersection point in this matrix as represented by a person/account permutation. This is the beginning level, the “atom” if you will, of SEPPs. SEPPs can aggregate vertically, as we discussed above on accounts. SEPPs can never aggregate horizontally. As an example, John and Cathy have both had working careers and have accu-mulated a variety of deferred account types from multiple employers:

John Cathy Deferred Account Type Amount Acct. # Amount Acct. #

401(k) $400,000 1 $65,000 6 Lump-sum distribution of an old “DB” plan $75,000 2 $25,000 7 Self-funded IRA $300,000 3 $150,000 8 SEP IRA $100,000 4 $200,000 9 Rollover IRA from prior employer’s 401(k) $200,000 5 $85,000 10 Total $1,075,000 $525,000

Between the two of them, 10 different accounts exist totaling $1.6 million. Valid combinations of these accounts to create a “SEPP Universe” would be any or all of John’s accounts (1, 2, 3, 4, and 5) or any or all of Cathy’s accounts (6, 7, 8, 9, and 10). Combining any of John’s accounts with any of Cathy’s accounts would be invalid.

39 It is easy to forget that the “I” in IRA stands for “individual.”

14

Relationship to Earned Income During your working career, you more than likely received earned income in the form of a pay-check from your employer. Conversely, deferred-account withdrawals are classified as unearned40 in-come. These two types of income are unrelated in that neither prohibits the creation or receipt of the other. Thus, it is perfectly okay to begin receiving distributions from your IRA in the form of a SEPP and at the same time continue to be gainfully employed (or self-employed) as you so choose.

Reversibility and Errors In many cases the IRC provides methods for a taxpayer to reverse course, sometimes years after an initial tax decision has been made. This is NOT one of those cases. Within our general context of dis-cussion, SEPPs are never reversible. However, if we broaden our scope momentarily, there are two circumstances where SEPPs can be reversed. They are:

Annual rollover—A taxpayer can always make a withdrawal from a deferred account and replace those withdrawn funds within 60 calendar days. This is then classified as a rollover, and each tax-payer is allowed one per year per account. It is not our intent to make use of this feature, but can potentially provide a limited ability to correct mistakes41.

Surtax—A taxpayer can always stop the SEPP withdrawals at any time and suffer the wrath of §72(t)(4); namely the application of the 10% surtax plus statutory interest. Again, it is not our in-tent to take advantage of this feature; further, it is pretty hard to conceive of this as any kind of ad-vantage at all. However, in subsequent chapters we will find a unique circumstance or two when it is actually in the taxpayer’s best interest to invoke §72(t)(4) early in some “pay me now or pay me even more later” scenarios.

However, the issues just discussed above are really exceptions. The point here is that each taxpayer should view the commencement of a SEPP program as irreversible. Further, the IRC does not differen-tiate between a change in taxpayer circumstance42 and errors. Errors can be mistakes in theory as well as practice. A taxpayer may believe he or she has properly interpreted how to apply one of the ap-proved methods. The taxpayer may be wrong resulting in a “theory error.” Or, a taxpayer may have theory down pat and properly interpreted but may make a date or math computational error. This then becomes a “practice error.” In any event, the IRC treats changes in taxpayer desire or circumstance, theory errors, and practice errors equally. All three events are unfortunately treated as “modifications” resulting in the application of §72(t)(4), the 10% surtax plus interest.

40 There is really no prejudice intended in the words “unearned” versus “earned.” If you have it, of course you earned it; it is simply a matter of which asset you employed: your time versus your other financial assets. Thus, these terms are really just titles for us to keep clear as to how current period or future period taxation will take place. Further, it is a common oc-currence for a taxpayer who commences SEPPs to wish also to make an IRA contribution. This is not permitted. Instead a taxpayer must have earned income from some other source and then make an IRA contribution based on that earned in-come. 41 There is also a strategy wherein a taxpayer creates seven different IRA accounts of approximately equal size and makes overlapping withdrawals starting on the 1st day, 54th day, 108th day, etc.; e.g. make a withdrawal on day 1 of $10,000 from IRA A; make a second withdrawal from IRA B of $10,000 on 54th day placing that money back in IRA A to satisfy the 60 day rollover rule. In this manner, a taxpayer can essentially lend oneself approximately 1/7th of the sum total IRAs value. This strategy does work, but this author thinks that it is a bit too much work involved compared to the gain received. 42 You might win the lotto after two years of SEPPs and desire to suspend those SEPPs or modify them to a smaller amount for the foreseeable future.

15

What should we take away from this? There are probably several points. First, a taxpayer should think long and hard before commencing SEPPs to insure that the SEPP program fits correctly with both upside and potential downside changes in personal finances. Further, this implies a great deal of thought as well as preplanning in advance of SEPP commencement. Second, a taxpayer who is the least bit hesitant should purchase some insurance against committing an error. The easiest way to do this is to hire a competent tax accountant and/or tax attorney43 who is insured and who is capable of performing or at least reviewing the taxpayer’s assumptions and computations. Thus, in the event an error occurs, the taxpayer can rely upon the professional’s errors and omissions insurance coverage.

Basis in Account So far, our entire conversation about SEPPs has assumed that the entire deferred-account balance is taxable as unearned ordinary income. This is not always the case. The most common exception is the individual who has made a number of nondeductible IRA contributions to the deferred account in prior years. Thus, we now have an account that has a mixture of taxed and untaxed monies in it. In this situation, the taxpayer has “basis” in the account, which are those contribution dollars that have al-ready been taxed.

For example: Assume a taxpayer wishes to commence SEPPs on an IRA with a current total valuation of $100,000, of which $20,000 was originally from after-tax contributions. The basis in this account is $20,000. Further, let’s assume that the SEPP amount for the first year is computed to be $5,000. Only $4,000 is includible in the gross income of the taxpayer; $1,000 is excluded as a ratable return of basis in the account.

This return of basis issue can get considerably more complex in year two when accounting for ad-ditional account appreciation or when a taxpayer selects a multiple-account SEPP universe. Since IRS Publication 590 does an excellent job of covering most of these situations, we will not repeat them here. However, the basic concept continues into future years—that being a mathematical computation to arrive at a percentage or dollar amount representing a ratable return of basis, e.g. prior-year previ-ously taxed contributions that are not re-taxed when distributed.

Penalty Computations Almost all of this text is explicitly devoted to avoiding penalties. Nonetheless, a common charac-teristic of all SEPP programs is the danger that, for some reason, penalties will be enforced. IRC §72(t)(4) says in part that if a taxpayer modifies the SEPPs:

What does this mean? This is essentially a “look back” tax that says that if a modification occurs, then an additional tax is going to be immediately due in and for the same tax year in which the modifi-cation occurs. 43 We will discuss how to hire competent professional assistance in the risk assessment chapter.

“The taxpayer’s tax for the 1st taxable year in which such modification occurs shall be increased by an amount...equal to the tax which...would have been imposed, plus interest for the deferral period .”

IRC §72(t)(4)

16

This additional tax is computed by going back to the first year in which the SEPPs started and for that year and every intervening year recomputing the tax due for each year applying the 10% surtax. Thus, we wind up with an additional tax due by year since the commencement of SEPPs. Secondly, for each year in which additional tax is due and it is not the current year, compute the statutory interest due for all intervening years as a penalty for not having originally paid the tax when it was due.

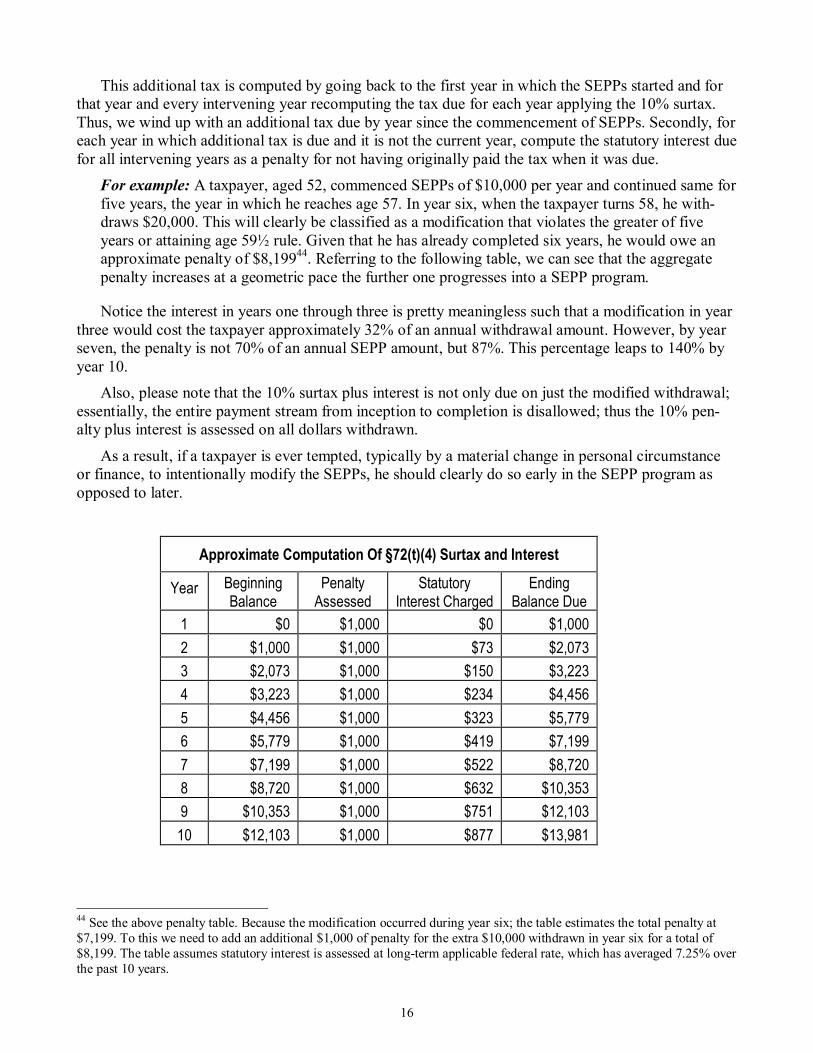

For example: A taxpayer, aged 52, commenced SEPPs of $10,000 per year and continued same for five years, the year in which he reaches age 57. In year six, when the taxpayer turns 58, he with-draws $20,000. This will clearly be classified as a modification that violates the greater of five years or attaining age 59½ rule. Given that he has already completed six years, he would owe an approximate penalty of $8,19944. Referring to the following table, we can see that the aggregate penalty increases at a geometric pace the further one progresses into a SEPP program.

Notice the interest in years one through three is pretty meaningless such that a modification in year three would cost the taxpayer approximately 32% of an annual withdrawal amount. However, by year seven, the penalty is not 70% of an annual SEPP amount, but 87%. This percentage leaps to 140% by year 10. Also, please note that the 10% surtax plus interest is not only due on just the modified withdrawal; essentially, the entire payment stream from inception to completion is disallowed; thus the 10% pen-alty plus interest is assessed on all dollars withdrawn.

As a result, if a taxpayer is ever tempted, typically by a material change in personal circumstance or finance, to intentionally modify the SEPPs, he should clearly do so early in the SEPP program as opposed to later.

Approximate Computation Of §72(t)(4) Surtax and Interest Year Beginning

Balance Penalty

Assessed Statutory

Interest Charged Ending

Balance Due 1 $0 $1,000 $0 $1,000 2 $1,000 $1,000 $73 $2,073 3 $2,073 $1,000 $150 $3,223 4 $3,223 $1,000 $234 $4,456 5 $4,456 $1,000 $323 $5,779 6 $5,779 $1,000 $419 $7,199 7 $7,199 $1,000 $522 $8,720 8 $8,720 $1,000 $632 $10,353 9 $10,353 $1,000 $751 $12,103 10 $12,103 $1,000 $877 $13,981

44 See the above penalty table. Because the modification occurred during year six; the table estimates the total penalty at $7,199. To this we need to add an additional $1,000 of penalty for the extra $10,000 withdrawn in year six for a total of $8,199. The table assumes statutory interest is assessed at long-term applicable federal rate, which has averaged 7.25% over the past 10 years.

17

________________________________________________________________________________________________ Chapter 3 Other Strange Animals—Roth IRAs & NUA

Roth IRA Taxation and Penalties Thus far, our entire focus has been the elimination of the 10% surtax imposed by IRC §72(t) by searching for and implementing one or more of the available exceptions. In each of these cases, when properly implemented, the 10% surtax is avoided, but, more often than not, regular federal income tax (and potentially state income tax) is still imposed. Further, in this context, essentially all accounts (§401(a), §403(b), §401(k) plan balances and §408 IRAs) are treated as deferred accounts; the implica-tion being that taxation of the account proceeds is deferred to some point in the future, not eliminated or forgiven.

Roth Definition In the Taxpayer Relief Act of 1997, Senator William Roth championed a new type of IRA, accord-ingly called the Roth IRA45. For brevity purposes, we are going to shorten this to a “Roth.” The rules for Roths are completely different from all other types of IRAs. Roths have the following general char-acteristics:

• Unlike regular IRAs, no deduction is ever afforded for making a contribution. Further, the abil-ity to contribute to a Roth is generally limited to $2,000 per year46 for those taxpayers with less than $110,000 or $160,000 of adjusted gross income for single and married filing jointly tax-payers, respectively.

• Taxpayers with less than $100,00047 of adjusted gross income can also elect to convert some or all of their regular IRAs into Roths; however, this does create a taxable event on which regular income tax (but no penalty) is due48.

• Distributions from Roths are categorized as either qualified or unqualified. If the distribution is qualified, it is a tax-free distribution, irrespective of the composition or source of the distribu-tion dollars. If a distribution is unqualified, it is potentially taxable depending on a new set of special ordering rules discussed following.

Qualified and Unqualified Withdrawals Since there are many fine texts written all about Roth contributions, conversions, and recharacteri-

zations, we will skip past all of these issues and instead take a hard look at the distribution side of the

45 See IRC §408A and related regulations. 46 Commencing in 2002, IRA contribution limits, including Roth IRAs, will be increased $3,000; $4,000 in 2003; $5,000 in 2004 and indexed to inflation thereafter. 47 A Taxpayer may have AGI of less than $100,000 but may wish to convert IRAs of such size that their resultant AGI ex-ceeds the $100,000 limit. This is okay in that the AGI limit; imposed by IRC §408A(c)(3)(B) ignores the amount of the rollover or conversion in computing the taxpayer’s AGI. 48 On its face, a conversion from a regular IRA to a Roth is a withdrawal from the IRA and therefore subject to the 10% under §72(t). However, IRC §408A(d)(3)(A)(ii) gives us a break by saying that “§72(t) shall not apply”.

18

equation. Our objectives are, first and foremost, to completely avoid taxation and, second, if forced into a taxable event, to avoid the 10% surtax as imposed by §72(t). To do this we need to first under-stand the differences between qualified and unqualified distributions.

A qualified distribution is one that is BOTH:

• Made after a 5-taxable-year period, and

• Made on or after the date on which the taxpayer attains the age of 59½ , or made to a benefici-ary or the estate of the owner on or after the date of the owner’s death, or attributable to the owner’s being disabled, or for a first-time home purchase49.

An unqualified distribution is any distribution that is not qualified according to the rules above.

Application of 5-Taxable-Year Rule Based on the permissible types of transactions for a Roth, we potentially create three classes of as-