Embed Size (px)

Citation preview

Succeeding for generationsStories of the world’s most enduring family businesses

Succeeding for generationsStories of the world’s most enduring family businesses

Succeeding for generations2 3Succeeding for generations

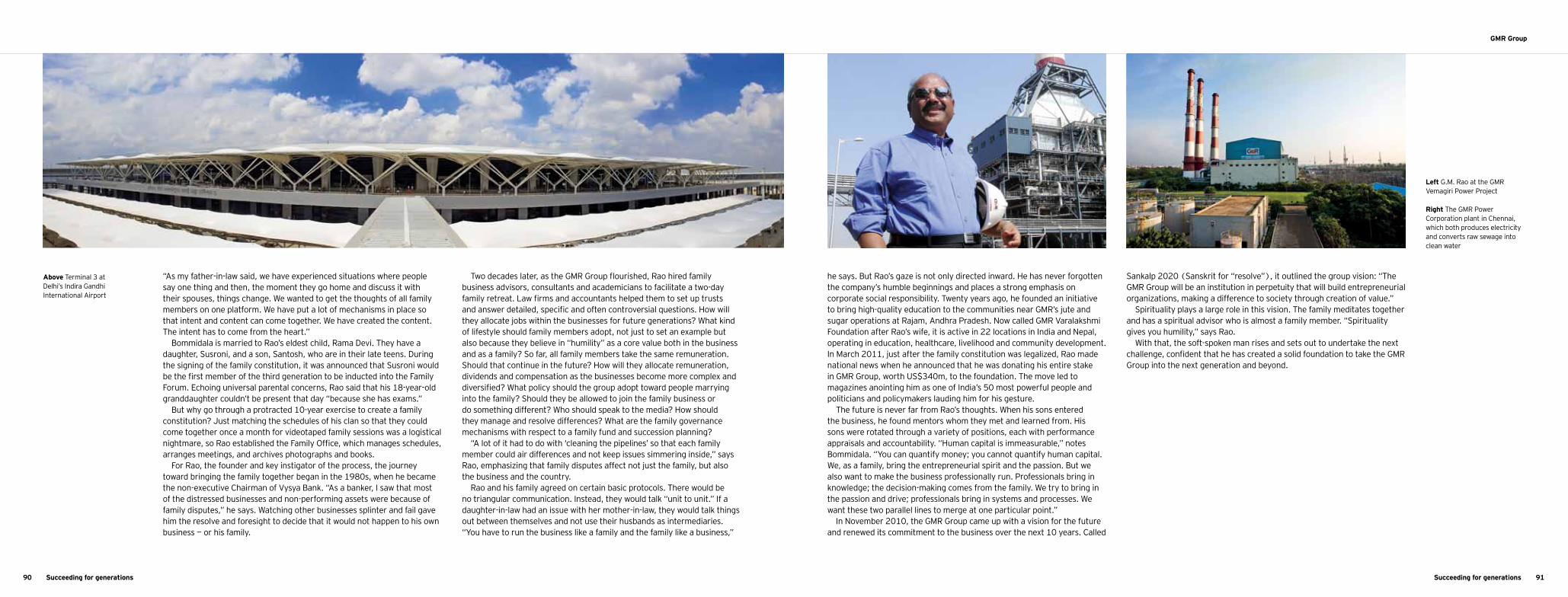

Family businesses contribute significantly to economies around the world — but they are often content to stay out of the limelight. For the

leaders of these businesses, the most important stakeholders are not shareholders or markets, but their family and the next generation. Through prudent investment and steady growth, they seek to pass on a stable, dynamic legacy to their children and grandchildren.

Succeeding for generations celebrates these exceptional companies. Through in-depth interviews and stunning photography, we trace the histories of some of the world’s most enduring family businesses as they navigate through wars, recessions and market revolutions.

By always keeping their eyes on the horizon, and with the experience of many decades — or even centuries — behind them, family businesses are better equipped than most to deal efficiently and successfully with both internal and external challenges. But while family businesses have much in common, each one is as individual as a fingerprint. The selection in Succeeding for generations reflects this.

Spanning 14 countries and 2 continents, our featured companies range from wine merchants to banks, and from manufacturers to publishers. Some maintain an all-family management board, while others have handed over the day-to-day running of the company to outsiders. Some have remained in the sector in which they were originally founded, while others have diversified into a number of different industries. Some have been passed down through many generations, while, in others, the third generation is only now making its first foray into the business.

Longevity is a key trait of family businesses — many of our featured companies have been in existence for well over a century. But these businesses are not trapped in the past. Constant innovation is crucial to surviving and competing in a rapidly globalizing world. Long-running family businesses know this better than anyone.

Ernst & Young is no stranger to the unique challenges these companies face: our global organization is the result of the merger of two long-running family businesses. We are therefore pleased to have brought you Succeeding for generations. It’s our tribute to a special breed of business.

We hope you enjoy their stories.

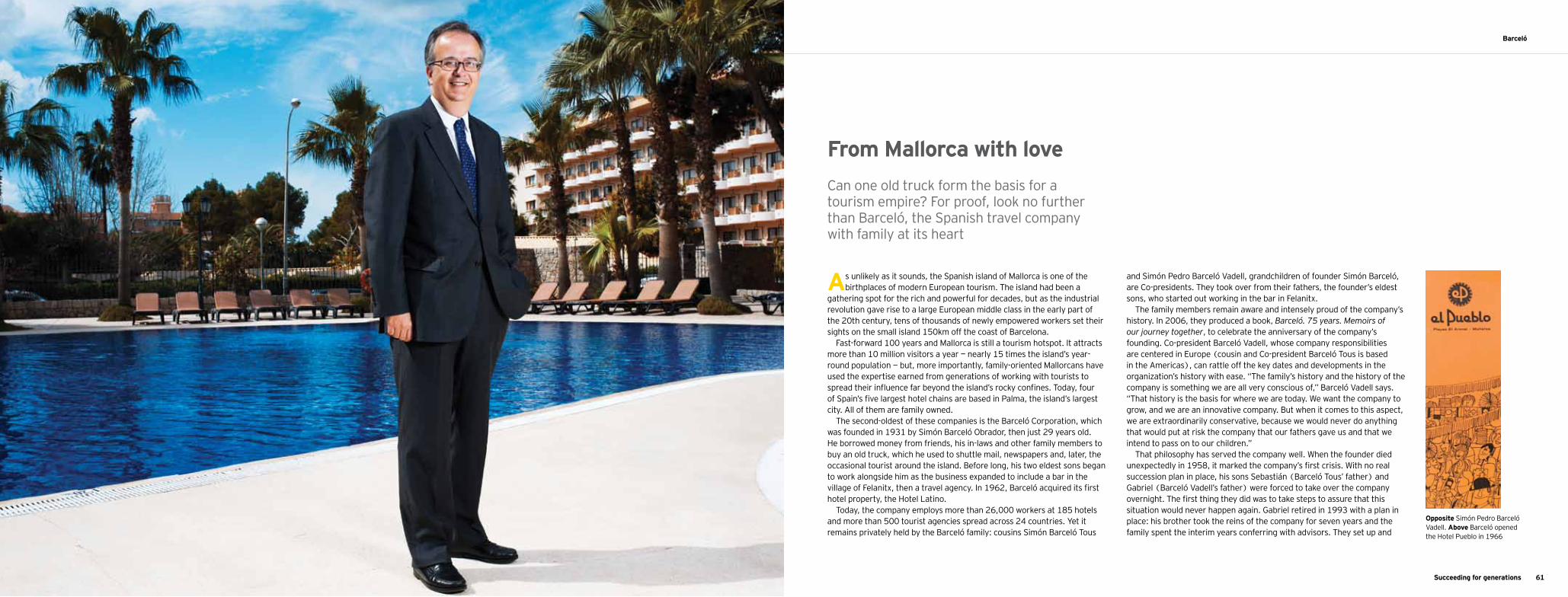

The history of Ernst & Young 4Bankhaus Spängler Austria 7Rothschild France 15Obeikan Investment Group Saudi Arabia 21 Esteve Spain 27Oras Invest Finland 31 Avantha Group India 35De Agostini Group Italy 41 Prym Group Germany 47 WICOR Switzerland 53Barceló Spain 61Berry Bros. & Rudd United Kingdom 65Papadopoulos Greece 73

Contents

Arvid Nordquist Sweden 77Van Oord The Netherlands 83GMR Group India 89The growth DNA of family business 92

Introduction

Timelines Banking 12 Cosmetics, fashion and luxury goods 24Media and publishing 38Automotive 58Food and drink 70 Shipping 80

Succeeding for generations4 5Succeeding for generations

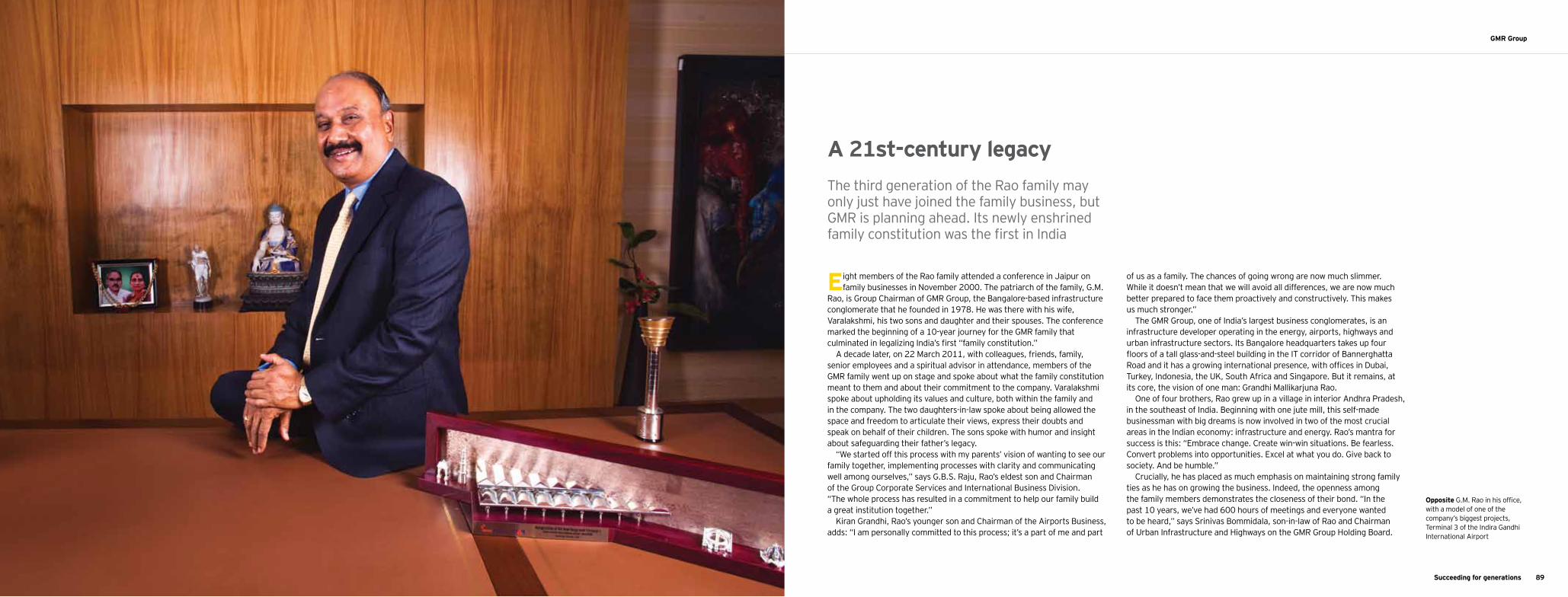

Ernst & Young

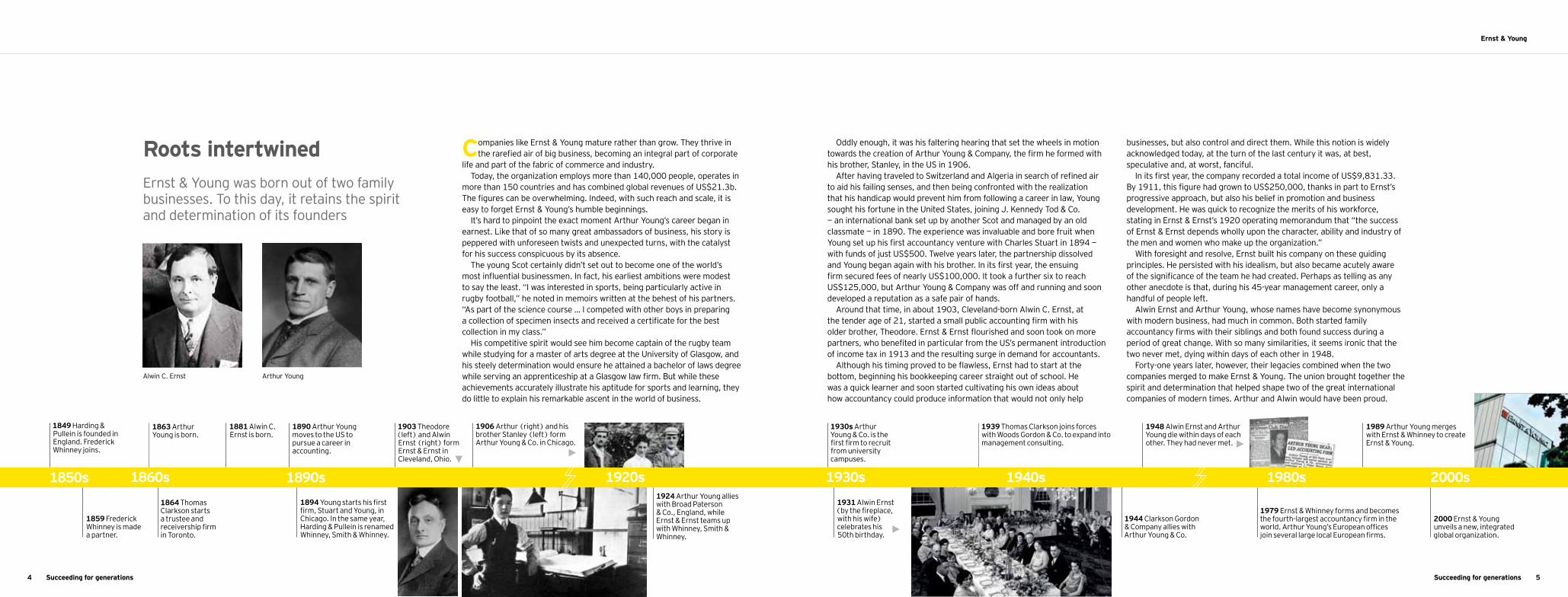

Ernst & Young was born out of two family businesses. To this day, it retains the spirit and determination of its founders

Roots intertwined Companies like Ernst & Young mature rather than grow. They thrive in the rarefied air of big business, becoming an integral part of corporate

life and part of the fabric of commerce and industry. Today, the organization employs more than 140,000 people, operates in

more than 150 countries and has combined global revenues of US$21.3b. The figures can be overwhelming. Indeed, with such reach and scale, it is easy to forget Ernst & Young’s humble beginnings.

It’s hard to pinpoint the exact moment Arthur Young’s career began in earnest. Like that of so many great ambassadors of business, his story is peppered with unforeseen twists and unexpected turns, with the catalyst for his success conspicuous by its absence.

The young Scot certainly didn’t set out to become one of the world’s most influential businessmen. In fact, his earliest ambitions were modest to say the least. “I was interested in sports, being particularly active in rugby football,” he noted in memoirs written at the behest of his partners. “As part of the science course … I competed with other boys in preparing a collection of specimen insects and received a certificate for the best collection in my class.”

His competitive spirit would see him become captain of the rugby team while studying for a master of arts degree at the University of Glasgow, and his steely determination would ensure he attained a bachelor of laws degree while serving an apprenticeship at a Glasgow law firm. But while these achievements accurately illustrate his aptitude for sports and learning, they do little to explain his remarkable ascent in the world of business.

Oddly enough, it was his faltering hearing that set the wheels in motion towards the creation of Arthur Young & Company, the firm he formed with his brother, Stanley, in the US in 1906.

After having traveled to Switzerland and Algeria in search of refined air to aid his failing senses, and then being confronted with the realization that his handicap would prevent him from following a career in law, Young sought his fortune in the United States, joining J. Kennedy Tod & Co. — an international bank set up by another Scot and managed by an old classmate — in 1890. The experience was invaluable and bore fruit when Young set up his first accountancy venture with Charles Stuart in 1894 — with funds of just US$500. Twelve years later, the partnership dissolved and Young began again with his brother. In its first year, the ensuing firm secured fees of nearly US$100,000. It took a further six to reach US$125,000, but Arthur Young & Company was off and running and soon developed a reputation as a safe pair of hands.

Around that time, in about 1903, Cleveland-born Alwin C. Ernst, at the tender age of 21, started a small public accounting firm with his older brother, Theodore. Ernst & Ernst flourished and soon took on more partners, who benefited in particular from the US’s permanent introduction of income tax in 1913 and the resulting surge in demand for accountants.

Although his timing proved to be flawless, Ernst had to start at the bottom, beginning his bookkeeping career straight out of school. He was a quick learner and soon started cultivating his own ideas about how accountancy could produce information that would not only help

businesses, but also control and direct them. While this notion is widely acknowledged today, at the turn of the last century it was, at best, speculative and, at worst, fanciful.

In its first year, the company recorded a total income of US$9,831.33. By 1911, this figure had grown to US$250,000, thanks in part to Ernst’s progressive approach, but also his belief in promotion and business development. He was quick to recognize the merits of his workforce, stating in Ernst & Ernst’s 1920 operating memorandum that “the success of Ernst & Ernst depends wholly upon the character, ability and industry of the men and women who make up the organization.”

With foresight and resolve, Ernst built his company on these guiding principles. He persisted with his idealism, but also became acutely aware of the significance of the team he had created. Perhaps as telling as any other anecdote is that, during his 45-year management career, only a handful of people left.

Alwin Ernst and Arthur Young, whose names have become synonymous with modern business, had much in common. Both started family accountancy firms with their siblings and both found success during a period of great change. With so many similarities, it seems ironic that the two never met, dying within days of each other in 1948.

Forty-one years later, however, their legacies combined when the two companies merged to make Ernst & Young. The union brought together the spirit and determination that helped shape two of the great international companies of modern times. Arthur and Alwin would have been proud.

1860s 1930s1920s 1980s

1849 Harding & Pullein is founded in England. Frederick Whinney joins.

1939 Thomas Clarkson joins forces with Woods Gordon & Co. to expand into management consulting.

1881 Alwin C. Ernst is born.

1930s Arthur Young & Co. is the first firm to recruit from university campuses.

1903 Theodore (left) and Alwin Ernst (right) form Ernst & Ernst in Cleveland, Ohio.

1948 Alwin Ernst and Arthur Young die within days of each other. They had never met.

1944 Clarkson Gordon & Company allies with Arthur Young & Co.

Alwin C. Ernst Arthur Young

1859 Frederick Whinney is made a partner.

1863 Arthur Young is born.

1864 Thomas Clarkson starts a trustee and receivership firm in Toronto.

1894 Young starts his first firm, Stuart and Young, in Chicago. In the same year, Harding & Pullein is renamed Whinney, Smith & Whinney.

1890 Arthur Young moves to the US to pursue a career in accounting.

1906 Arthur (right) and his brother Stanley (left) form Arthur Young & Co. in Chicago.

2000 Ernst & Young unveils a new, integrated global organization.

1924 Arthur Young allies with Broad Paterson & Co., England, while Ernst & Ernst teams up with Whinney, Smith & Whinney.

1979 Ernst & Whinney forms and becomes the fourth-largest accountancy firm in the world. Arthur Young’s European offices join several large local European firms.

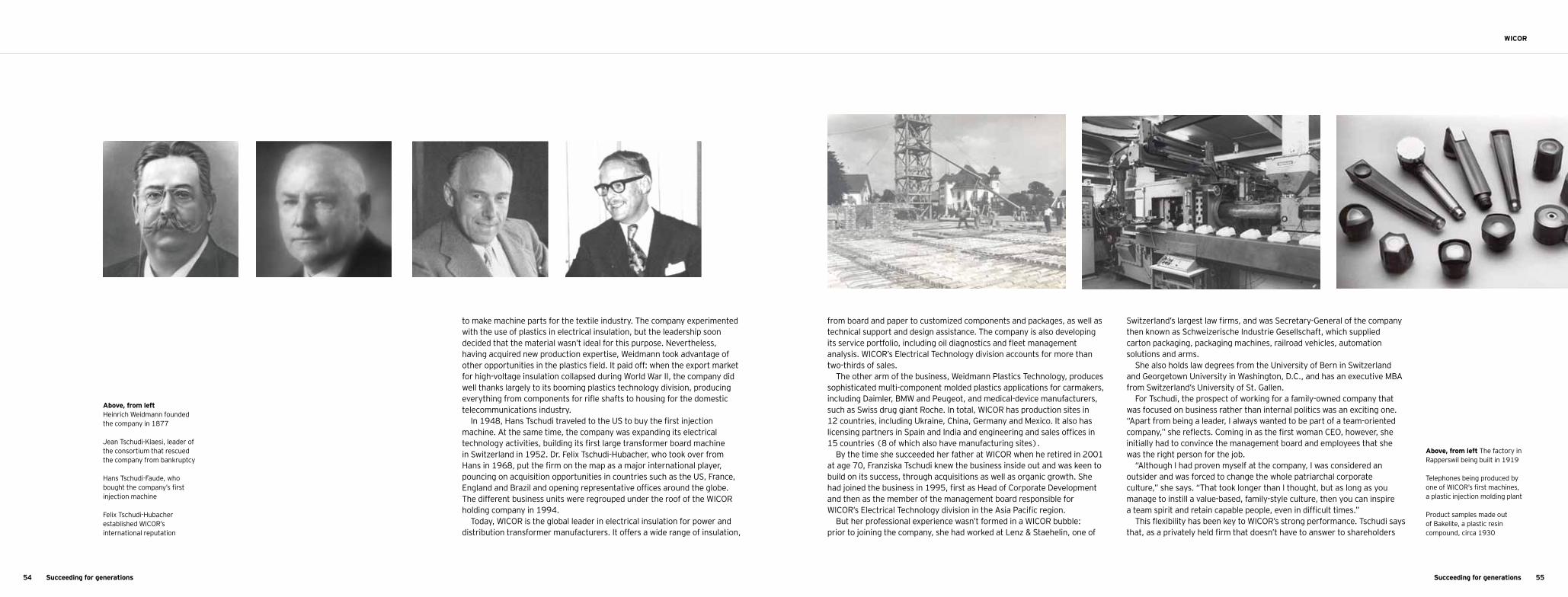

1989 Arthur Young merges with Ernst & Whinney to create Ernst & Young.

1850s 1890s 1940s 2000s1931 Alwin Ernst (by the fireplace, with his wife) celebrates his 50th birthday.

Succeeding for generations6

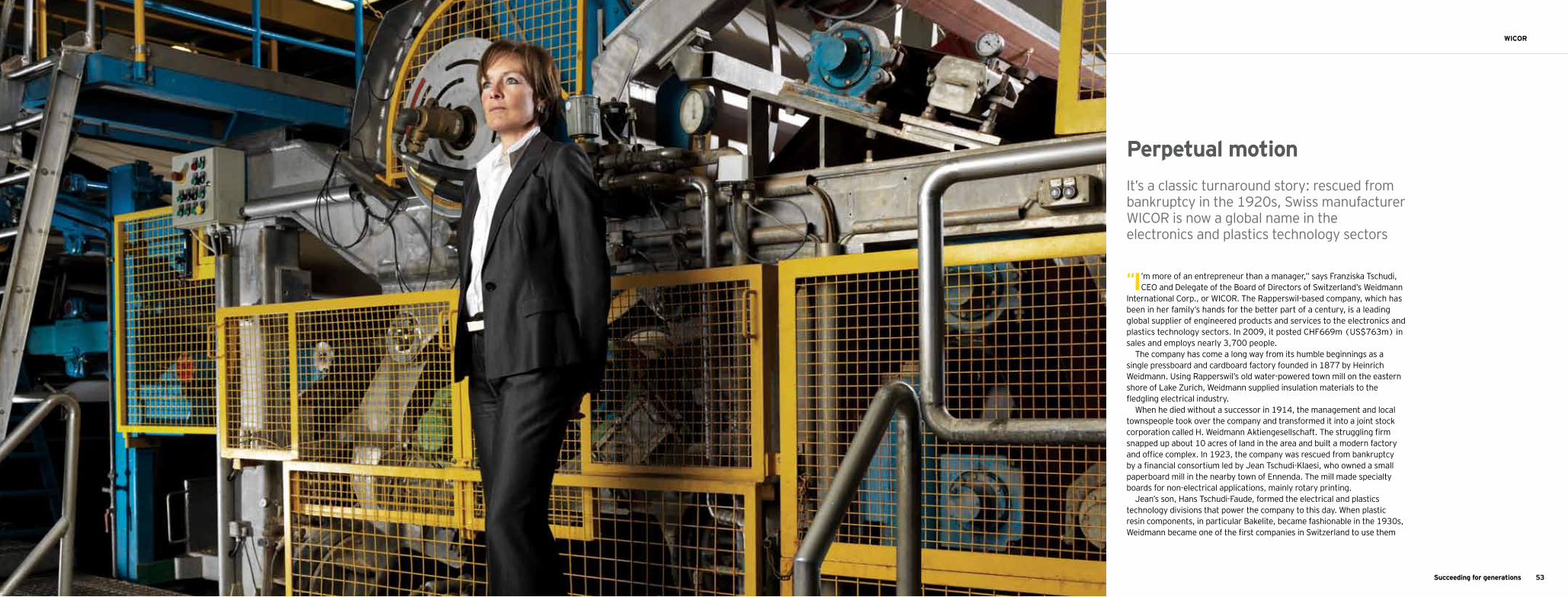

Bankhaus Spängler

7Succeeding for generations

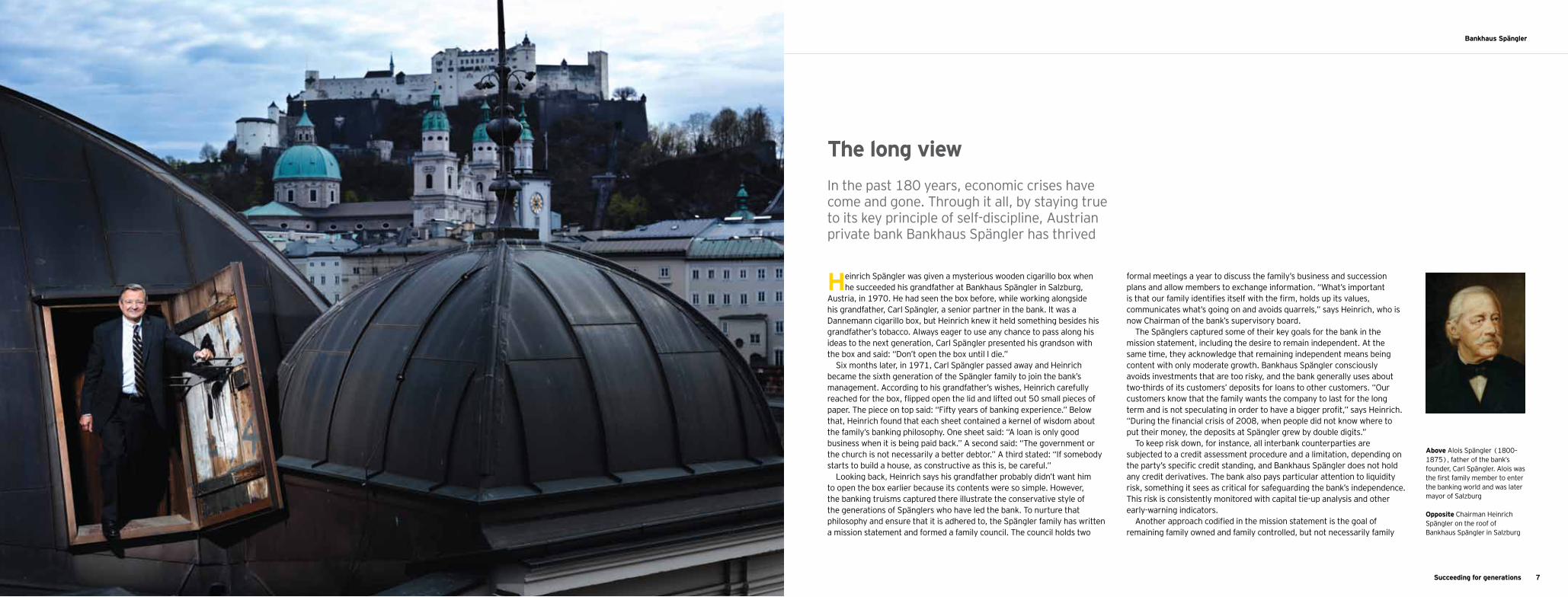

In the past 180 years, economic crises have come and gone. Through it all, by staying true to its key principle of self-discipline, Austrian private bank Bankhaus Spängler has thrived

The long view

Heinrich Spängler was given a mysterious wooden cigarillo box when he succeeded his grandfather at Bankhaus Spängler in Salzburg,

Austria, in 1970. He had seen the box before, while working alongside his grandfather, Carl Spängler, a senior partner in the bank. It was a Dannemann cigarillo box, but Heinrich knew it held something besides his grandfather’s tobacco. Always eager to use any chance to pass along his ideas to the next generation, Carl Spängler presented his grandson with the box and said: “Don’t open the box until I die.”

Six months later, in 1971, Carl Spängler passed away and Heinrich became the sixth generation of the Spängler family to join the bank’s management. According to his grandfather’s wishes, Heinrich carefully reached for the box, flipped open the lid and lifted out 50 small pieces of paper. The piece on top said: “Fifty years of banking experience.” Below that, Heinrich found that each sheet contained a kernel of wisdom about the family’s banking philosophy. One sheet said: “A loan is only good business when it is being paid back.” A second said: “The government or the church is not necessarily a better debtor.” A third stated: “If somebody starts to build a house, as constructive as this is, be careful.”

Looking back, Heinrich says his grandfather probably didn’t want him to open the box earlier because its contents were so simple. However, the banking truisms captured there illustrate the conservative style of the generations of Spänglers who have led the bank. To nurture that philosophy and ensure that it is adhered to, the Spängler family has written a mission statement and formed a family council. The council holds two

formal meetings a year to discuss the family’s business and succession plans and allow members to exchange information. “What’s important is that our family identifies itself with the firm, holds up its values, communicates what’s going on and avoids quarrels,” says Heinrich, who is now Chairman of the bank’s supervisory board.

The Spänglers captured some of their key goals for the bank in the mission statement, including the desire to remain independent. At the same time, they acknowledge that remaining independent means being content with only moderate growth. Bankhaus Spängler consciously avoids investments that are too risky, and the bank generally uses about two-thirds of its customers’ deposits for loans to other customers. “Our customers know that the family wants the company to last for the long term and is not speculating in order to have a bigger profit,” says Heinrich. “During the financial crisis of 2008, when people did not know where to put their money, the deposits at Spängler grew by double digits.”

To keep risk down, for instance, all interbank counterparties are subjected to a credit assessment procedure and a limitation, depending on the party’s specific credit standing, and Bankhaus Spängler does not hold any credit derivatives. The bank also pays particular attention to liquidity risk, something it sees as critical for safeguarding the bank’s independence. This risk is consistently monitored with capital tie-up analysis and other early-warning indicators.

Another approach codified in the mission statement is the goal of remaining family owned and family controlled, but not necessarily family

Above Alois Spängler (1800–1875), father of the bank’s founder, Carl Spängler. Alois was the first family member to enter the banking world and was later mayor of Salzburg

Opposite Chairman Heinrich Spängler on the roof of Bankhaus Spängler in Salzburg

Succeeding for generations8

Overleaf Heinrich Spängler on top of the world

9

Bankhaus Spängler

Succeeding for generations

managed. “The best-qualified members of each generation should represent the family owners on the board,” says Heinrich. “If the family cannot agree or nobody can be found from the family to take over a position, then the family should focus on its role as the company’s owners, leaving the open position to a non-family member. Being family managed is a goal, but not the most important one.”

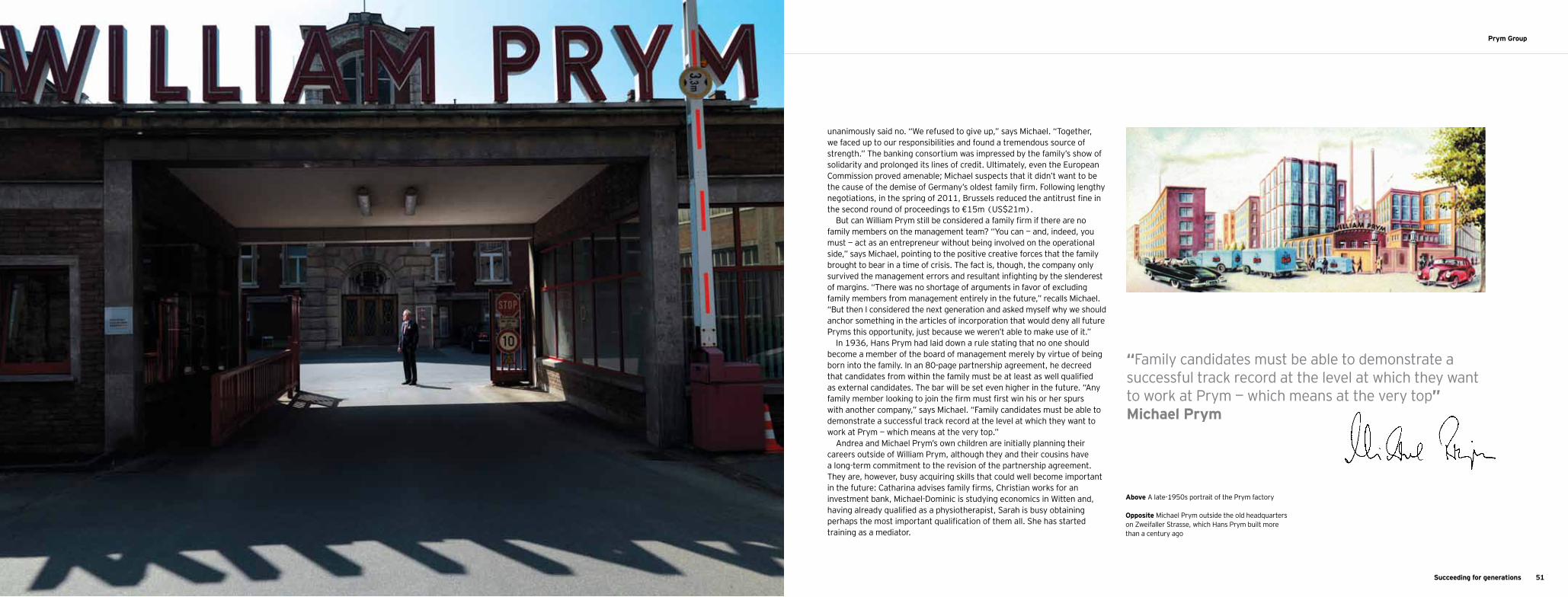

For 166 years, the bank operated as a partnership run by four family members. As of 1994, Spängler became a joint stock company with all its shares owned by the family. The corporation has since been overseen by a management board and a supervisory board, a structure typical in Austria, Switzerland and Germany. The bank’s current staffing of those positions is fully in line with the family’s mission statement. Two family members serve on the eight-member supervisory board: Heinrich Wiesmüller, the son-in-law of the late Richard Spängler, who was a senior partner with Carl Spängler; and Heinrich Spängler himself. Franz Welt, the grandson of Richard Spängler, also serves on the four-member executive board, acting as the bank’s risk manager. “This is something we learned during our decades of business,” says Heinrich. “Mixed boards are the best possible way to manage the company if you want to take advantage of both the family’s insight and the best talent available on the market.”

The roots of Bankhaus Spängler go back to a medieval trading business that started with the transport of salt to the south and the import of wine, silk and spices from Venice. Originally, the Spänglers were winegrowers and innkeepers in southern Tyrol. Then, two cousins set out — one to Salzburg and the other to Venice — and began to supply the archbishops who ruled Salzburg at the time with wine and silk. The bank emerged from

that trading business in 1828 and moved into its present-day headquarters on Salzburg’s Salzach River at the beginning of the 20th century. Built in 1881, the building is a former bazaar designed by Salzburg architects Valentin and Jakob Ceconi. On warm days, employees can be seen strolling between the building and the riverfront during the official lunch break, for which the bank closes.

Proud of its history as a family-owned company, Bankhaus Spängler supports other family-owned businesses with its banking services and with training sessions and discussion symposiums. A recent forum, for instance, featured Karl Weisskopf, the head of the German family-owned manufacturing group Liebherr International, speaking about the differences between listed companies and family-owned businesses. Bankhaus Spängler also teams up with the Institute for Management to offer custom-tailored courses for people running family businesses. Classes are offered on 13 days throughout the year in the rococo Leopoldskron Castle in Salzburg.

The company’s long survival was made possible because it has been carefully handed down from one generation to the next. Today, the seventh generation, represented by Markus Wiesmüller and Carl Philipp Spängler, works at the bank in its family management department, which provides personal and comprehensive service to wealthy private clients and families. It advises on challenges specific to family companies, such as the transfer of wealth, successor selection and risk management.

Officially called Bankhaus Carl Spängler & Co., the bank operates at 13 locations, has a staff of 240 and focuses on two primary areas of business: interest-bearing business such as deposits and loans, and securities, asset

management and family-office services. It also owns a capital investment company, Carl Spängler Kapitalanlagegesellschaft, which employs 30 people and has issued more than 100 investment funds. Close to half are publicly offered in Austria, Germany and Switzerland.

Of course, the banking sector has changed tremendously since Bankhaus Spängler was founded 183 years ago, but the bank’s conservative philosophy has seen it through several banking crises and two world wars. “We face new challenges and opportunities in a world changing faster than ever before, but we believe we can cope with these changes due to our manageable size, speed to market, understanding of our own goals and skillful organization,” Heinrich says. “Our business model shows that this is possible if you take the right approach, combining optimism and the necessary modesty.”

He describes the bank’s business model as one based on responsibility, business awareness, positive thinking, humanity and, above all, decency toward partners, employees and customers. And exercising these character traits is a message that Heinrich relays to the next generation of Spänglers, who will be taking over in the coming years.

So far, however, Heinrich is not planning to leave that advice in a wooden box on his desk like his grandfather did. That’s because the next generation of the family already knows the story of the cigarillo box very well. “It all goes back to what my grandfather taught me: the value of self-discipline. The next generation should stick to the bank’s philosophy, deciding on given situations with responsibility, awareness and the necessary open-mindedness,” he says. “My grandfather often quoted Gustav Mahler as saying: ‘Tradition is not to conserve the ashes, but to hold up the flame.’”

Above, from left Carl Spängler (1825–1902), the founder of Bankhaus Carl Spängler & Co.

Carl Spängler (1894–1971), grandson of the bank’s founder. He gave his grandson, Heinrich, the cigarillo box of banking truisms

Franz Welt is the grandson of Richard Spängler and serves on the four-member executive board

Markus Wiesmüller works in the bank’s family management department, which provides a service to wealthy private clients

Carl Philipp Spängler and Markus Wiesmüller represent the seventh generation of the family

Above, from left Heinrich Spängler (left), Chairman of the supervisory board, and Dr. Heinrich Wiesmüller, Honorable Chairman of the supervisory board

Members of the executive board, (from left): Dr. Rudolf Oberschneider, Dr. Helmut Gerlich, Franz Welt and Dr. Werner Zenz

Right Carl Spängler (1864–1902), son of the bank’s founder. He was married to Katharina Mayr, whose father owned the tavern Zum Goldenen Schiff in Salzburg

Succeeding for generations10

Bankhaus Spängler

Succeeding for generations 11

Succeeding for generations12 13Succeeding for generations

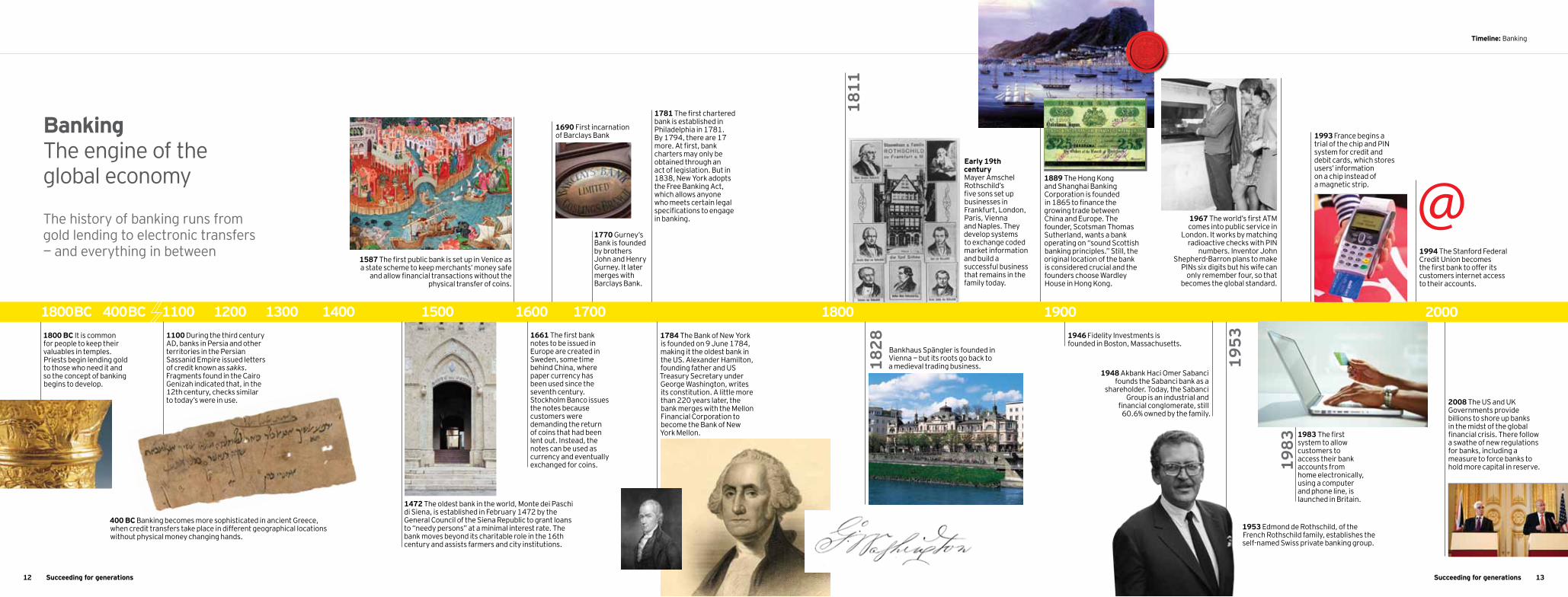

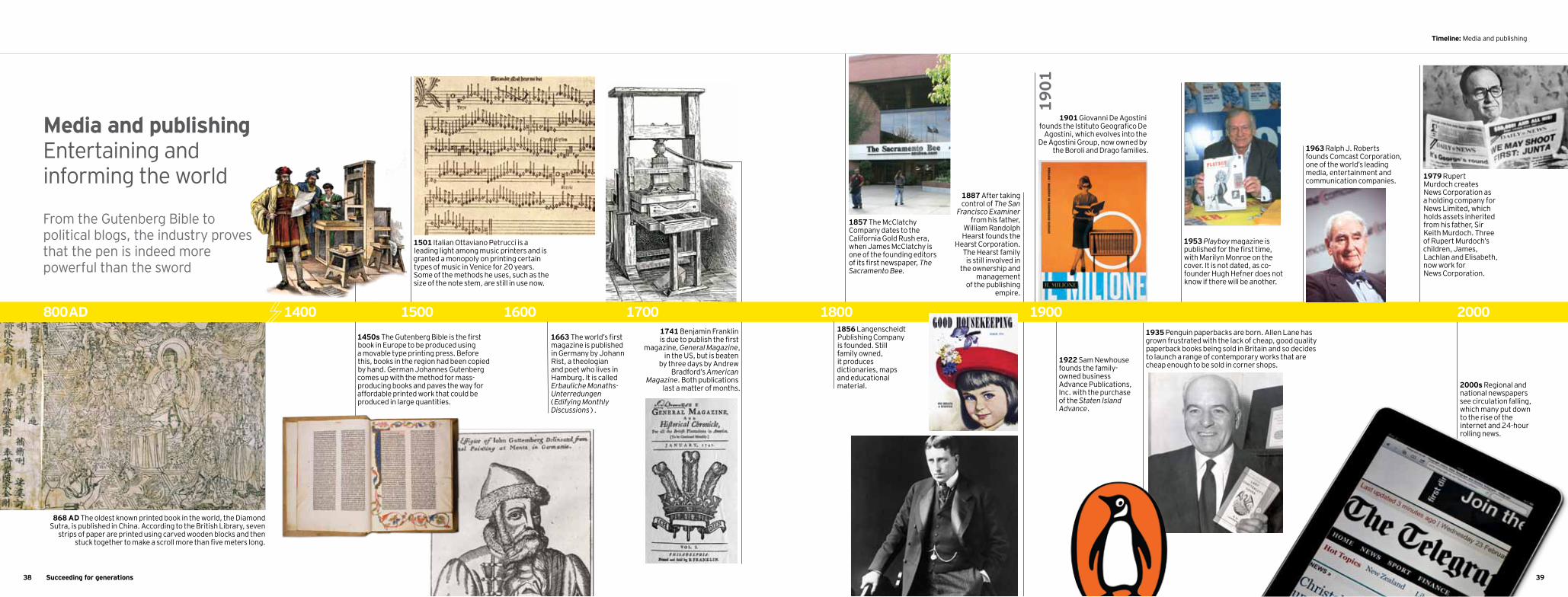

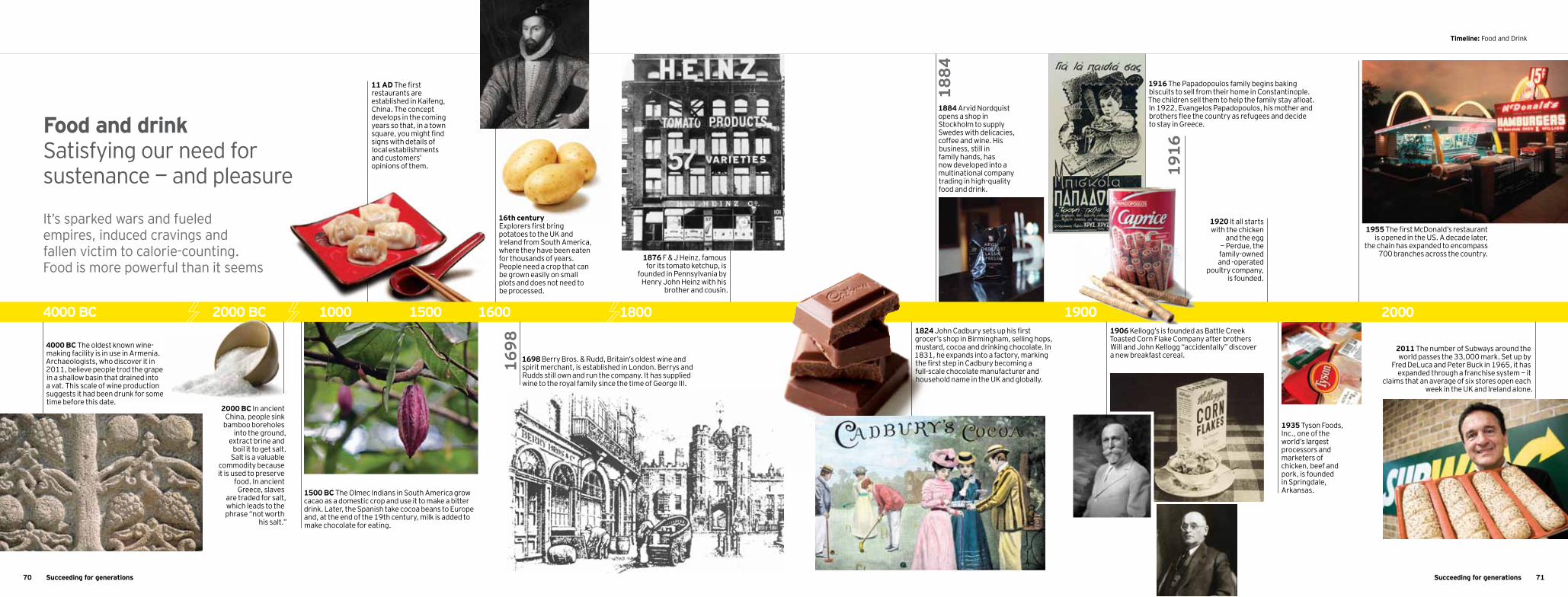

Timeline: Banking

The history of banking runs from gold lending to electronic transfers — and everything in between

BankingThe engine of the global economy

1811

1953

1828

1953 Edmond de Rothschild, of the French Rothschild family, establishes the self-named Swiss private banking group.

1889 The Hong Kong and Shanghai Banking Corporation is founded in 1865 to finance the growing trade between China and Europe. The founder, Scotsman Thomas Sutherland, wants a bank operating on “sound Scottish banking principles.” Still, the original location of the bank is considered crucial and the founders choose Wardley House in Hong Kong.

1100 1200 1300 1400 170016001500 1800 200019001800BC 400BC

1983

1948 Akbank Haci Omer Sabanci founds the Sabanci bank as a

shareholder. Today, the Sabanci Group is an industrial and

financial conglomerate, still 60.6% owned by the family.

1690 First incarnation of Barclays Bank

400 BC Banking becomes more sophisticated in ancient Greece, when credit transfers take place in different geographical locations without physical money changing hands.

Early 19th century Mayer Amschel Rothschild’s five sons set up businesses in Frankfurt, London, Paris, Vienna and Naples. They develop systems to exchange coded market information and build a successful business that remains in the family today.

1784 The Bank of New York is founded on 9 June 1784, making it the oldest bank in the US. Alexander Hamilton, founding father and US Treasury Secretary under George Washington, writes its constitution. A little more than 220 years later, the bank merges with the Mellon Financial Corporation to become the Bank of New York Mellon.

Bankhaus Spängler is founded in Vienna — but its roots go back to a medieval trading business.

1800 BC It is common for people to keep their valuables in temples. Priests begin lending gold to those who need it and so the concept of banking begins to develop.

1100 During the third century AD, banks in Persia and other territories in the Persian Sassanid Empire issued letters of credit known as sakks. Fragments found in the Cairo Genizah indicated that, in the 12th century, checks similar to today’s were in use.

1472 The oldest bank in the world, Monte dei Paschi di Siena, is established in February 1472 by the General Council of the Siena Republic to grant loans to “needy persons” at a minimal interest rate. The bank moves beyond its charitable role in the 16th century and assists farmers and city institutions.

1587 The first public bank is set up in Venice as a state scheme to keep merchants’ money safe

and allow financial transactions without the physical transfer of coins.

1661 The first bank notes to be issued in Europe are created in Sweden, some time behind China, where paper currency has been used since the seventh century. Stockholm Banco issues the notes because customers were demanding the return of coins that had been lent out. Instead, the notes can be used as currency and eventually exchanged for coins.

1770 Gurney’s Bank is founded by brothers John and Henry Gurney. It later merges with Barclays Bank.

1781 The first chartered bank is established in Philadelphia in 1781. By 1794, there are 17 more. At first, bank charters may only be obtained through an act of legislation. But in 1838, New York adopts the Free Banking Act, which allows anyone who meets certain legal specifications to engage in banking. 1967 The world’s first ATM

comes into public service in London. It works by matching

radioactive checks with PIN numbers. Inventor John

Shepherd-Barron plans to make PINs six digits but his wife can

only remember four, so that becomes the global standard.

1983 The first system to allow customers to access their bank accounts from home electronically, using a computer and phone line, is launched in Britain.

1993 France begins a trial of the chip and PIN system for credit and debit cards, which stores users’ information on a chip instead of a magnetic strip.

2008 The US and UK Governments provide billions to shore up banks in the midst of the global financial crisis. There follow a swathe of new regulations for banks, including a measure to force banks to hold more capital in reserve.

1994 The Stanford Federal Credit Union becomes the first bank to offer its customers internet access to their accounts.

1946 Fidelity Investments is founded in Boston, Massachusetts.

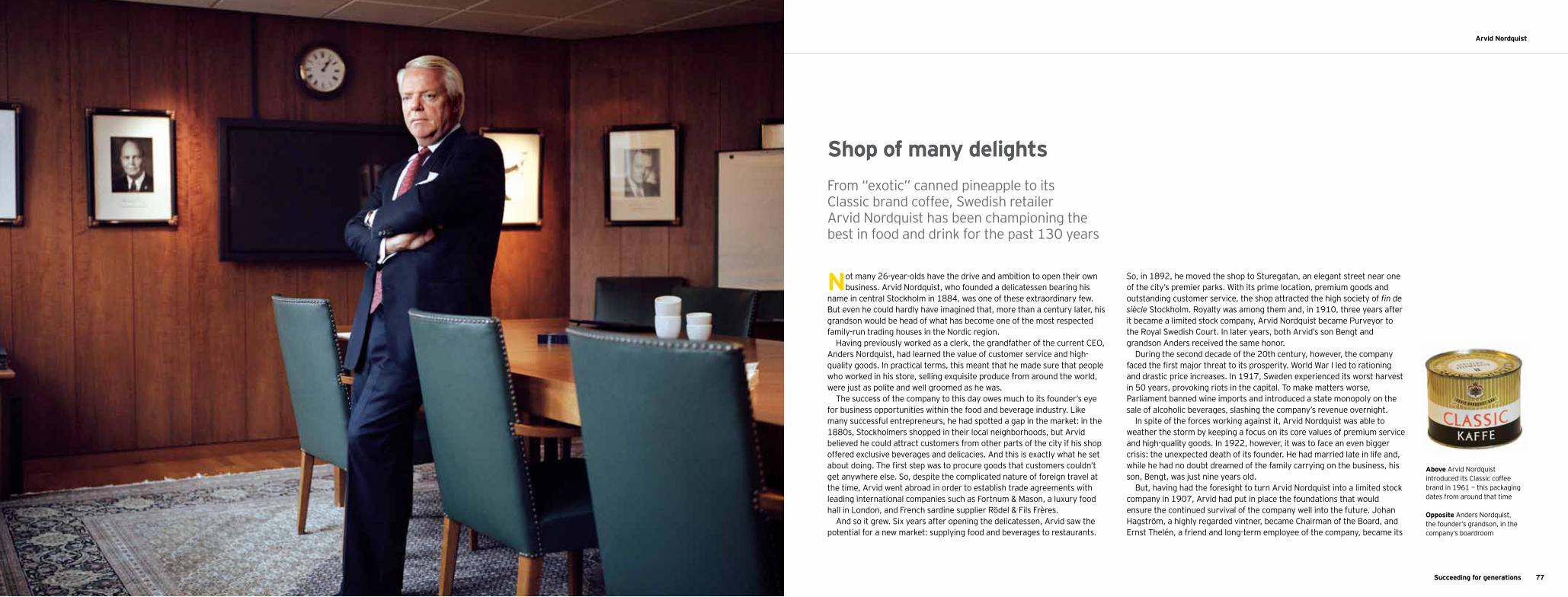

Succeeding for generations14 15Succeeding for generations

Rothschild

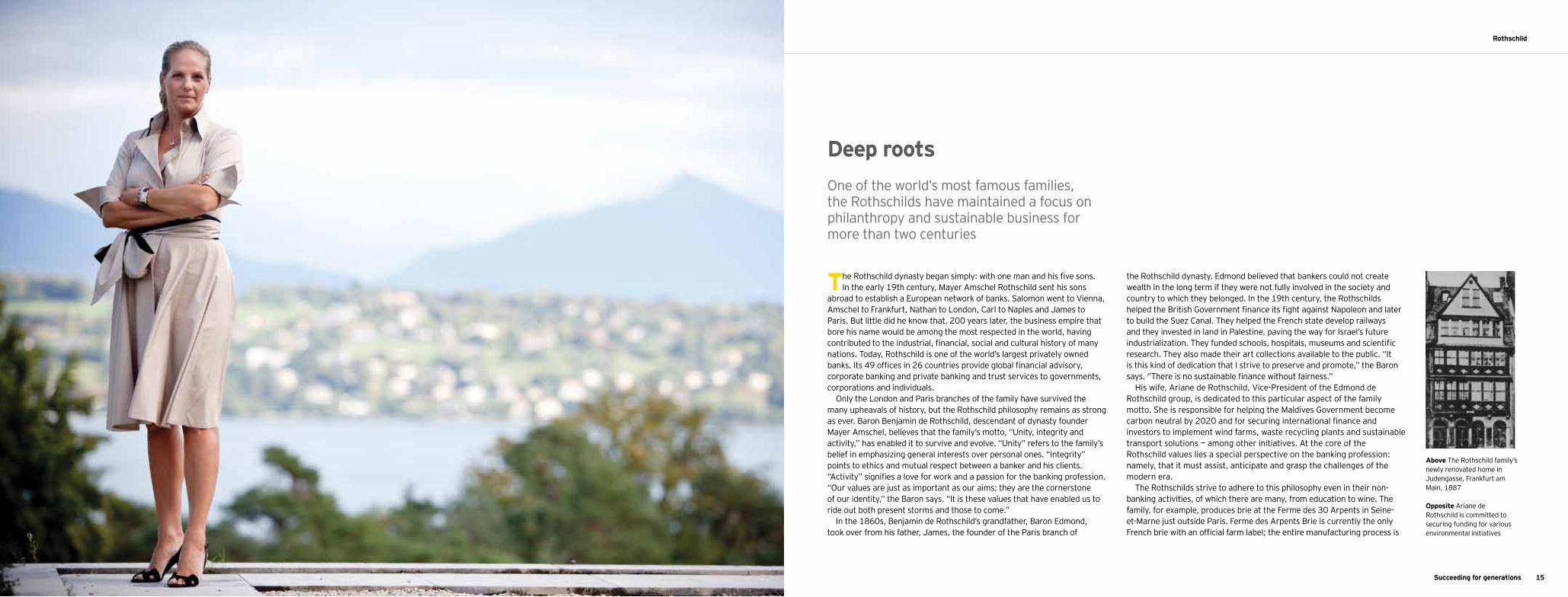

One of the world’s most famous families, the Rothschilds have maintained a focus on philanthropy and sustainable business for more than two centuries

Deep roots

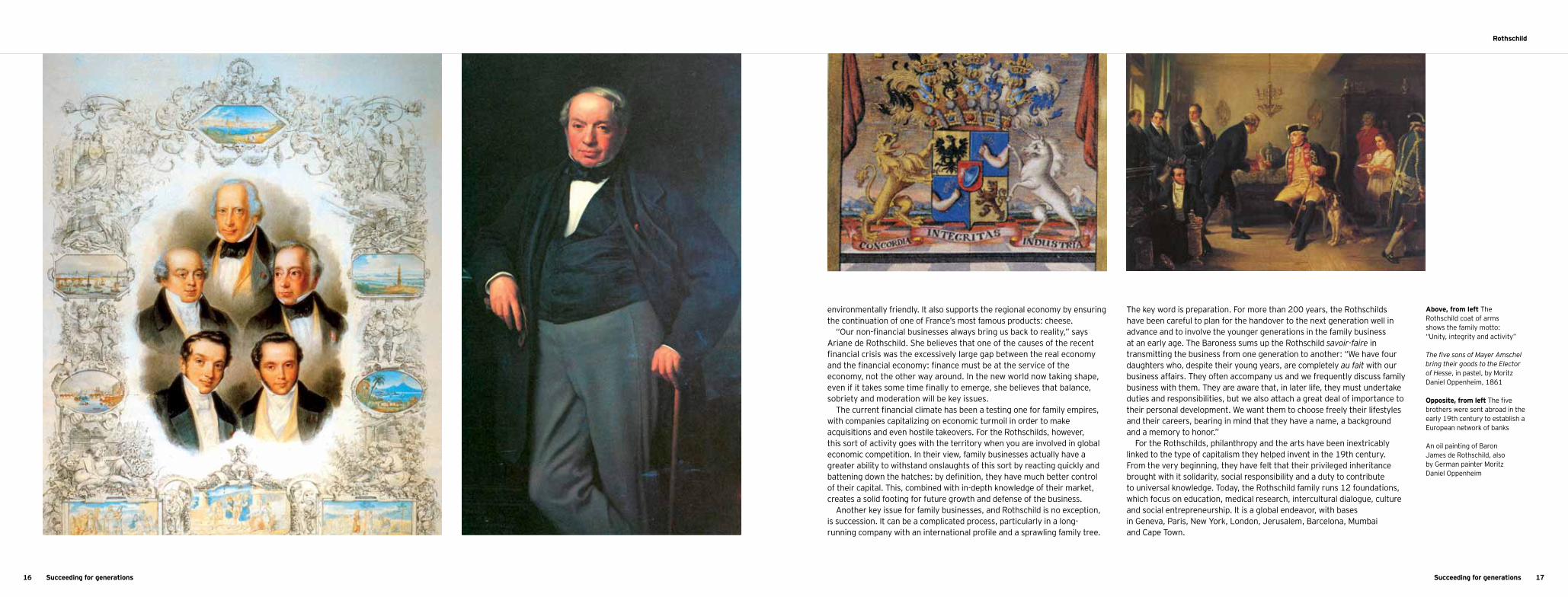

The Rothschild dynasty began simply: with one man and his five sons. In the early 19th century, Mayer Amschel Rothschild sent his sons

abroad to establish a European network of banks. Salomon went to Vienna, Amschel to Frankfurt, Nathan to London, Carl to Naples and James to Paris. But little did he know that, 200 years later, the business empire that bore his name would be among the most respected in the world, having contributed to the industrial, financial, social and cultural history of many nations. Today, Rothschild is one of the world’s largest privately owned banks. Its 49 offices in 26 countries provide global financial advisory, corporate banking and private banking and trust services to governments, corporations and individuals.

Only the London and Paris branches of the family have survived the many upheavals of history, but the Rothschild philosophy remains as strong as ever. Baron Benjamin de Rothschild, descendant of dynasty founder Mayer Amschel, believes that the family’s motto, “Unity, integrity and activity,” has enabled it to survive and evolve. “Unity” refers to the family’s belief in emphasizing general interests over personal ones. “Integrity” points to ethics and mutual respect between a banker and his clients. “Activity” signifies a love for work and a passion for the banking profession. “Our values are just as important as our aims; they are the cornerstone of our identity,” the Baron says. “It is these values that have enabled us to ride out both present storms and those to come.”

In the 1860s, Benjamin de Rothschild’s grandfather, Baron Edmond, took over from his father, James, the founder of the Paris branch of

the Rothschild dynasty. Edmond believed that bankers could not create wealth in the long term if they were not fully involved in the society and country to which they belonged. In the 19th century, the Rothschilds helped the British Government finance its fight against Napoleon and later to build the Suez Canal. They helped the French state develop railways and they invested in land in Palestine, paving the way for Israel’s future industrialization. They funded schools, hospitals, museums and scientific research. They also made their art collections available to the public. “It is this kind of dedication that I strive to preserve and promote,” the Baron says. “There is no sustainable finance without fairness.”

His wife, Ariane de Rothschild, Vice-President of the Edmond de Rothschild group, is dedicated to this particular aspect of the family motto. She is responsible for helping the Maldives Government become carbon neutral by 2020 and for securing international finance and investors to implement wind farms, waste recycling plants and sustainable transport solutions — among other initiatives. At the core of the Rothschild values lies a special perspective on the banking profession: namely, that it must assist, anticipate and grasp the challenges of the modern era.

The Rothschilds strive to adhere to this philosophy even in their non-banking activities, of which there are many, from education to wine. The family, for example, produces brie at the Ferme des 30 Arpents in Seine-et-Marne just outside Paris. Ferme des Arpents Brie is currently the only French brie with an official farm label; the entire manufacturing process is

Above The Rothschild family’s newly renovated home in Judengasse, Frankfurt am Main, 1887

Opposite Ariane de Rothschild is committed to securing funding for various environmental initiatives

Succeeding for generations16 17Succeeding for generations

Rothschild

environmentally friendly. It also supports the regional economy by ensuring the continuation of one of France’s most famous products: cheese.

“Our non-financial businesses always bring us back to reality,” says Ariane de Rothschild. She believes that one of the causes of the recent financial crisis was the excessively large gap between the real economy and the financial economy: finance must be at the service of the economy, not the other way around. In the new world now taking shape, even if it takes some time finally to emerge, she believes that balance, sobriety and moderation will be key issues.

The current financial climate has been a testing one for family empires, with companies capitalizing on economic turmoil in order to make acquisitions and even hostile takeovers. For the Rothschilds, however, this sort of activity goes with the territory when you are involved in global economic competition. In their view, family businesses actually have a greater ability to withstand onslaughts of this sort by reacting quickly and battening down the hatches: by definition, they have much better control of their capital. This, combined with in-depth knowledge of their market, creates a solid footing for future growth and defense of the business.

Another key issue for family businesses, and Rothschild is no exception, is succession. It can be a complicated process, particularly in a long-running company with an international profile and a sprawling family tree.

The key word is preparation. For more than 200 years, the Rothschilds have been careful to plan for the handover to the next generation well in advance and to involve the younger generations in the family business at an early age. The Baroness sums up the Rothschild savoir-faire in transmitting the business from one generation to another: “We have four daughters who, despite their young years, are completely au fait with our business affairs. They often accompany us and we frequently discuss family business with them. They are aware that, in later life, they must undertake duties and responsibilities, but we also attach a great deal of importance to their personal development. We want them to choose freely their lifestyles and their careers, bearing in mind that they have a name, a background and a memory to honor.”

For the Rothschilds, philanthropy and the arts have been inextricably linked to the type of capitalism they helped invent in the 19th century. From the very beginning, they have felt that their privileged inheritance brought with it solidarity, social responsibility and a duty to contribute to universal knowledge. Today, the Rothschild family runs 12 foundations, which focus on education, medical research, intercultural dialogue, culture and social entrepreneurship. It is a global endeavor, with bases in Geneva, Paris, New York, London, Jerusalem, Barcelona, Mumbai and Cape Town.

Above, from left The Rothschild coat of arms shows the family motto: “Unity, integrity and activity”

The five sons of Mayer Amschel bring their goods to the Elector of Hesse, in pastel, by Moritz Daniel Oppenheim, 1861

Opposite, from left The five brothers were sent abroad in the early 19th century to establish a European network of banks

An oil painting of Baron James de Rothschild, also by German painter Moritz Daniel Oppenheim

Succeeding for generations18 19Succeeding for generations

Rothschild

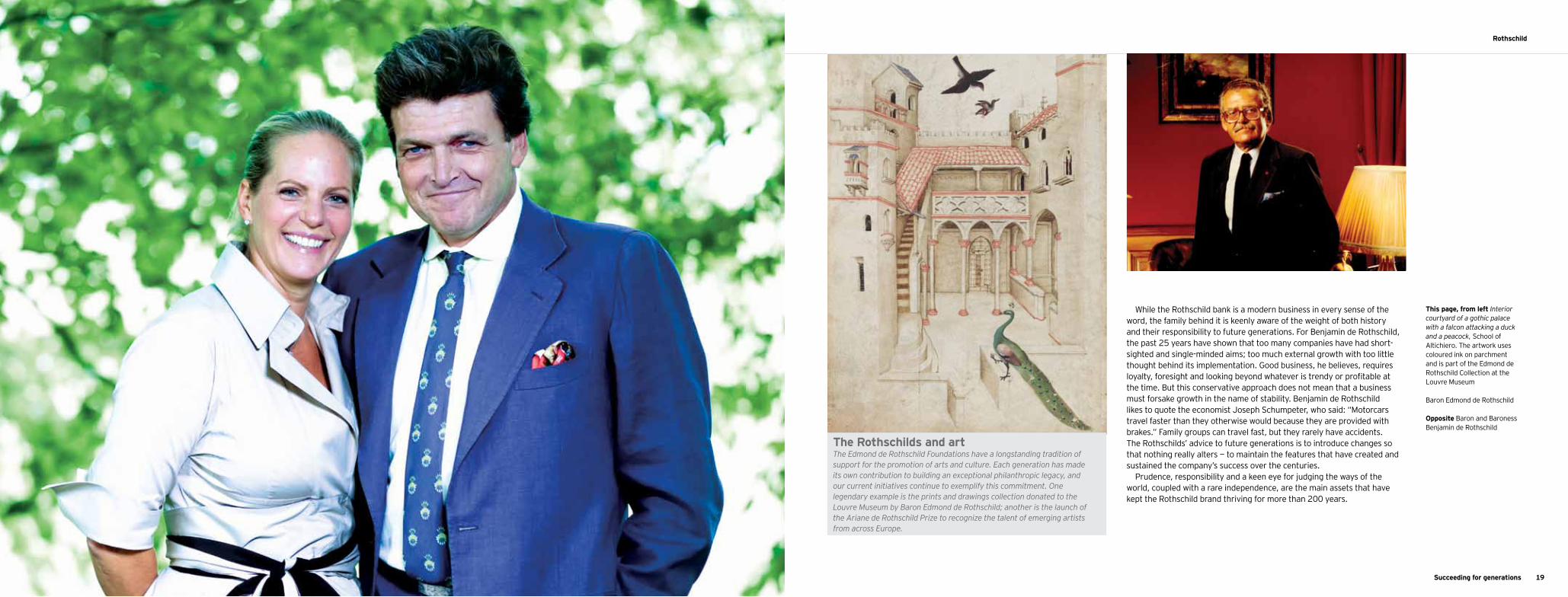

While the Rothschild bank is a modern business in every sense of the word, the family behind it is keenly aware of the weight of both history and their responsibility to future generations. For Benjamin de Rothschild, the past 25 years have shown that too many companies have had short-sighted and single-minded aims; too much external growth with too little thought behind its implementation. Good business, he believes, requires loyalty, foresight and looking beyond whatever is trendy or profitable at the time. But this conservative approach does not mean that a business must forsake growth in the name of stability. Benjamin de Rothschild likes to quote the economist Joseph Schumpeter, who said: “Motorcars travel faster than they otherwise would because they are provided with brakes.” Family groups can travel fast, but they rarely have accidents. The Rothschilds’ advice to future generations is to introduce changes so that nothing really alters — to maintain the features that have created and sustained the company’s success over the centuries.

Prudence, responsibility and a keen eye for judging the ways of the world, coupled with a rare independence, are the main assets that have kept the Rothschild brand thriving for more than 200 years.

This page, from left Interior courtyard of a gothic palace with a falcon attacking a duck and a peacock, School of Altichiero. The artwork uses coloured ink on parchment and is part of the Edmond de Rothschild Collection at the Louvre Museum

Baron Edmond de Rothschild

Opposite Baron and Baroness Benjamin de Rothschild

The Rothschilds and artThe Edmond de Rothschild Foundations have a longstanding tradition of support for the promotion of arts and culture. Each generation has made its own contribution to building an exceptional philanthropic legacy, and our current initiatives continue to exemplify this commitment. One legendary example is the prints and drawings collection donated to the Louvre Museum by Baron Edmond de Rothschild; another is the launch of the Ariane de Rothschild Prize to recognize the talent of emerging artists from across Europe.

Succeeding for generations20 21Succeeding for generations

Obeikan Investment Group

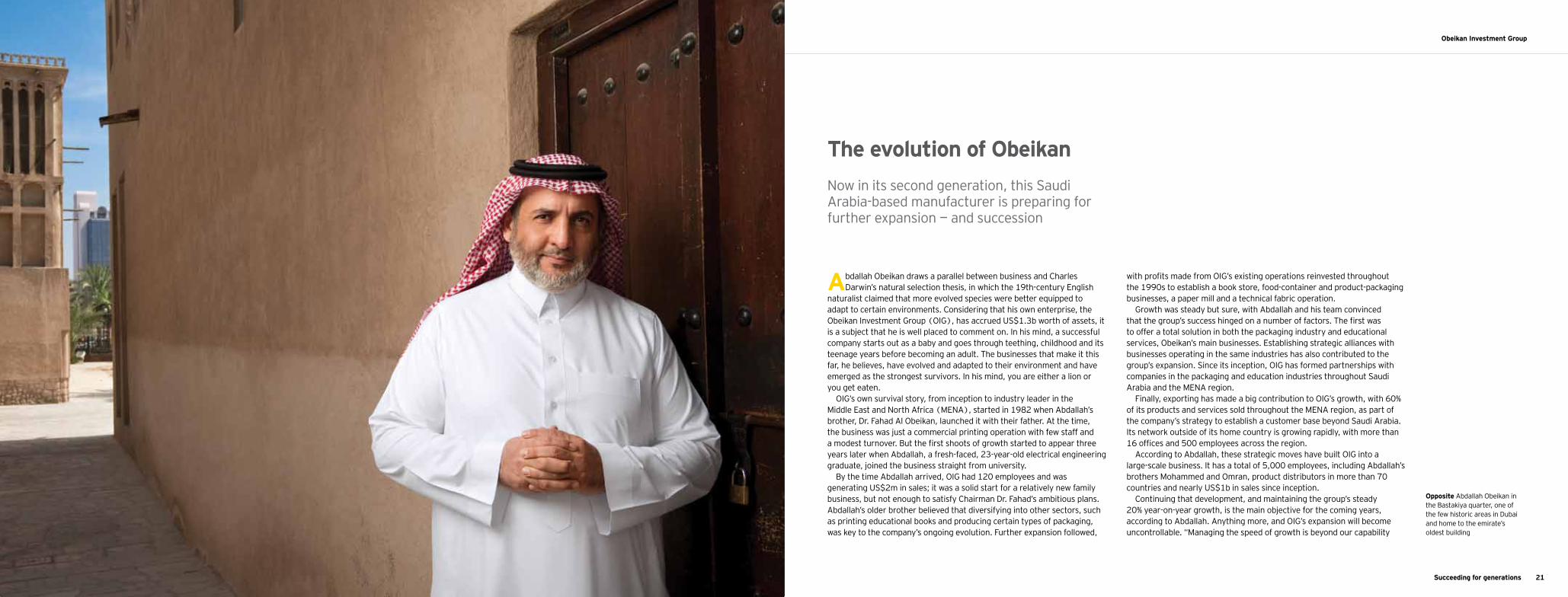

Now in its second generation, this Saudi Arabia-based manufacturer is preparing for further expansion — and succession

The evolution of Obeikan

Abdallah Obeikan draws a parallel between business and Charles Darwin’s natural selection thesis, in which the 19th-century English

naturalist claimed that more evolved species were better equipped to adapt to certain environments. Considering that his own enterprise, the Obeikan Investment Group (OIG), has accrued US$1.3b worth of assets, it is a subject that he is well placed to comment on. In his mind, a successful company starts out as a baby and goes through teething, childhood and its teenage years before becoming an adult. The businesses that make it this far, he believes, have evolved and adapted to their environment and have emerged as the strongest survivors. In his mind, you are either a lion or you get eaten.

OIG’s own survival story, from inception to industry leader in the Middle East and North Africa (MENA), started in 1982 when Abdallah’s brother, Dr. Fahad Al Obeikan, launched it with their father. At the time, the business was just a commercial printing operation with few staff and a modest turnover. But the first shoots of growth started to appear three years later when Abdallah, a fresh-faced, 23-year-old electrical engineering graduate, joined the business straight from university.

By the time Abdallah arrived, OIG had 120 employees and was generating US$2m in sales; it was a solid start for a relatively new family business, but not enough to satisfy Chairman Dr. Fahad’s ambitious plans. Abdallah’s older brother believed that diversifying into other sectors, such as printing educational books and producing certain types of packaging, was key to the company’s ongoing evolution. Further expansion followed,

with profits made from OIG’s existing operations reinvested throughout the 1990s to establish a book store, food-container and product-packaging businesses, a paper mill and a technical fabric operation.

Growth was steady but sure, with Abdallah and his team convinced that the group’s success hinged on a number of factors. The first was to offer a total solution in both the packaging industry and educational services, Obeikan’s main businesses. Establishing strategic alliances with businesses operating in the same industries has also contributed to the group’s expansion. Since its inception, OIG has formed partnerships with companies in the packaging and education industries throughout Saudi Arabia and the MENA region.

Finally, exporting has made a big contribution to OIG’s growth, with 60% of its products and services sold throughout the MENA region, as part of the company’s strategy to establish a customer base beyond Saudi Arabia. Its network outside of its home country is growing rapidly, with more than 16 offices and 500 employees across the region.

According to Abdallah, these strategic moves have built OIG into a large-scale business. It has a total of 5,000 employees, including Abdallah’s brothers Mohammed and Omran, product distributors in more than 70 countries and nearly US$1b in sales since inception.

Continuing that development, and maintaining the group’s steady 20% year-on-year growth, is the main objective for the coming years, according to Abdallah. Anything more, and OIG’s expansion will become uncontrollable. “Managing the speed of growth is beyond our capability

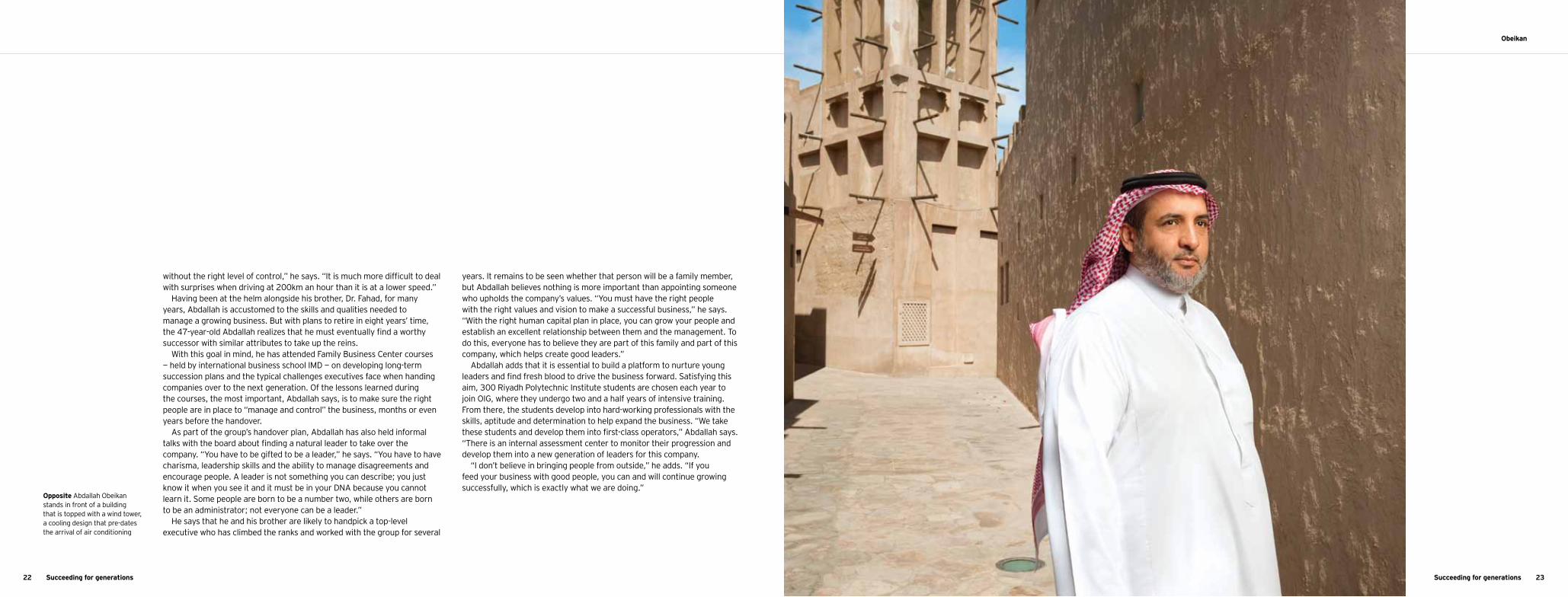

Opposite Abdallah Obeikan in the Bastakiya quarter, one of the few historic areas in Dubai and home to the emirate’s oldest building

Succeeding for generations22 23Succeeding for generations

Obeikan

without the right level of control,” he says. “It is much more difficult to deal with surprises when driving at 200km an hour than it is at a lower speed.”

Having been at the helm alongside his brother, Dr. Fahad, for many years, Abdallah is accustomed to the skills and qualities needed to manage a growing business. But with plans to retire in eight years’ time, the 47-year-old Abdallah realizes that he must eventually find a worthy successor with similar attributes to take up the reins.

With this goal in mind, he has attended Family Business Center courses — held by international business school IMD — on developing long-term succession plans and the typical challenges executives face when handing companies over to the next generation. Of the lessons learned during the courses, the most important, Abdallah says, is to make sure the right people are in place to “manage and control” the business, months or even years before the handover.

As part of the group’s handover plan, Abdallah has also held informal talks with the board about finding a natural leader to take over the company. “You have to be gifted to be a leader,” he says. “You have to have charisma, leadership skills and the ability to manage disagreements and encourage people. A leader is not something you can describe; you just know it when you see it and it must be in your DNA because you cannot learn it. Some people are born to be a number two, while others are born to be an administrator; not everyone can be a leader.”

He says that he and his brother are likely to handpick a top-level executive who has climbed the ranks and worked with the group for several

years. It remains to be seen whether that person will be a family member, but Abdallah believes nothing is more important than appointing someone who upholds the company’s values. “You must have the right people with the right values and vision to make a successful business,” he says. “With the right human capital plan in place, you can grow your people and establish an excellent relationship between them and the management. To do this, everyone has to believe they are part of this family and part of this company, which helps create good leaders.”

Abdallah adds that it is essential to build a platform to nurture young leaders and find fresh blood to drive the business forward. Satisfying this aim, 300 Riyadh Polytechnic Institute students are chosen each year to join OIG, where they undergo two and a half years of intensive training. From there, the students develop into hard-working professionals with the skills, aptitude and determination to help expand the business. “We take these students and develop them into first-class operators,” Abdallah says. “There is an internal assessment center to monitor their progression and develop them into a new generation of leaders for this company.

“I don’t believe in bringing people from outside,” he adds. “If you feed your business with good people, you can and will continue growing successfully, which is exactly what we are doing.”

Opposite Abdallah Obeikan stands in front of a building that is topped with a wind tower, a cooling design that pre-dates the arrival of air conditioning

Succeeding for generations24 Succeeding for generations 25

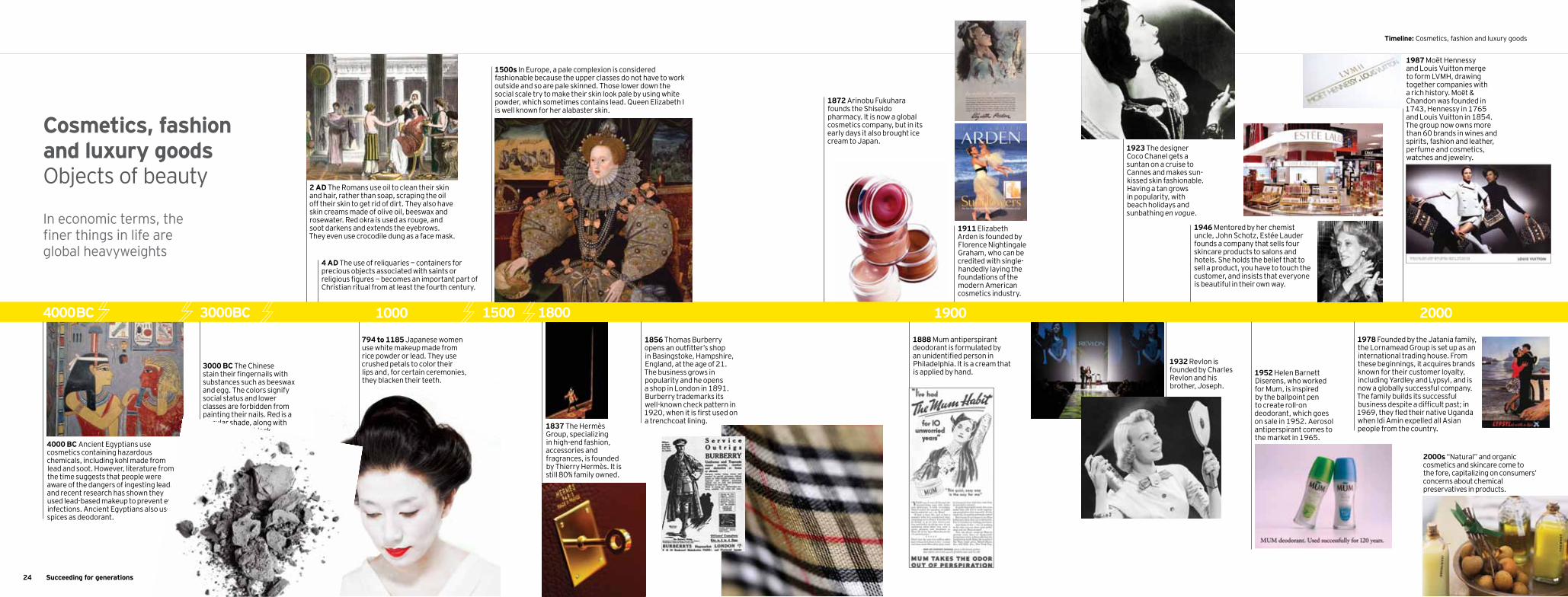

Timeline: Cosmetics, fashion and luxury goods

In economic terms, the finer things in life are global heavyweights

Cosmetics, fashion and luxury goodsObjects of beauty

1932 Revlon is founded by Charles Revlon and his brother, Joseph.

1872 Arinobu Fukuhara founds the Shiseido pharmacy. It is now a global cosmetics company, but in its early days it also brought ice cream to Japan.

4000BC 18001500 1900 2000

1923 The designer Coco Chanel gets a suntan on a cruise to Cannes and makes sun-kissed skin fashionable. Having a tan grows in popularity, with beach holidays and sunbathing en vogue.

2 AD The Romans use oil to clean their skin and hair, rather than soap, scraping the oil off their skin to get rid of dirt. They also have skin creams made of olive oil, beeswax and rosewater. Red okra is used as rouge, and soot darkens and extends the eyebrows. They even use crocodile dung as a face mask.

3000 BC The Chinese stain their fingernails with substances such as beeswax and egg. The colors signify social status and lower classes are forbidden from painting their nails. Red is a popular shade, along with gold, silver and black.

1500s In Europe, a pale complexion is considered fashionable because the upper classes do not have to work outside and so are pale skinned. Those lower down the social scale try to make their skin look pale by using white powder, which sometimes contains lead. Queen Elizabeth I is well known for her alabaster skin.

1856 Thomas Burberry opens an outfitter’s shop in Basingstoke, Hampshire, England, at the age of 21. The business grows in popularity and he opens a shop in London in 1891. Burberry trademarks its well-known check pattern in 1920, when it is first used on a trenchcoat lining.

4000 BC Ancient Egyptians use cosmetics containing hazardous chemicals, including kohl made from lead and soot. However, literature from the time suggests that people were aware of the dangers of ingesting lead, and recent research has shown they used lead-based makeup to prevent eye infections. Ancient Egyptians also use spices as deodorant.

1837 The Hermès Group, specializing in high-end fashion, accessories and fragrances, is founded by Thierry Hermès. It is still 80% family owned.

1911 Elizabeth Arden is founded by Florence Nightingale Graham, who can be credited with single-handedly laying the foundations of the modern American cosmetics industry.

1888 Mum antiperspirant deodorant is formulated by an unidentified person in Philadelphia. It is a cream that is applied by hand. 1952 Helen Barnett

Diserens, who worked for Mum, is inspired by the ballpoint pen to create roll-on deodorant, which goes on sale in 1952. Aerosol antiperspirant comes to the market in 1965.

1946 Mentored by her chemist uncle, John Schotz, Estée Lauder founds a company that sells four skincare products to salons and hotels. She holds the belief that to sell a product, you have to touch the customer, and insists that everyone is beautiful in their own way.

1987 Moët Hennessy and Louis Vuitton merge to form LVMH, drawing together companies with a rich history. Moët & Chandon was founded in 1743, Hennessy in 1765 and Louis Vuitton in 1854. The group now owns more than 60 brands in wines and spirits, fashion and leather, perfume and cosmetics, watches and jewelry.

1978 Founded by the Jatania family, the Lornamead Group is set up as an international trading house. From these beginnings, it acquires brands known for their customer loyalty, including Yardley and Lypsyl, and is now a globally successful company. The family builds its successful business despite a difficult past; in 1969, they fled their native Uganda when Idi Amin expelled all Asian people from the country.

2000s “Natural” and organic cosmetics and skincare come to the fore, capitalizing on consumers’ concerns about chemical preservatives in products.

4 AD The use of reliquaries — containers for precious objects associated with saints or religious figures — becomes an important part of Christian ritual from at least the fourth century.

3000BC 1000

794 to 1185 Japanese women use white makeup made from rice powder or lead. They use crushed petals to color their lips and, for certain ceremonies, they blacken their teeth.

Succeeding for generations26

Esteve

Succeeding for generations 27

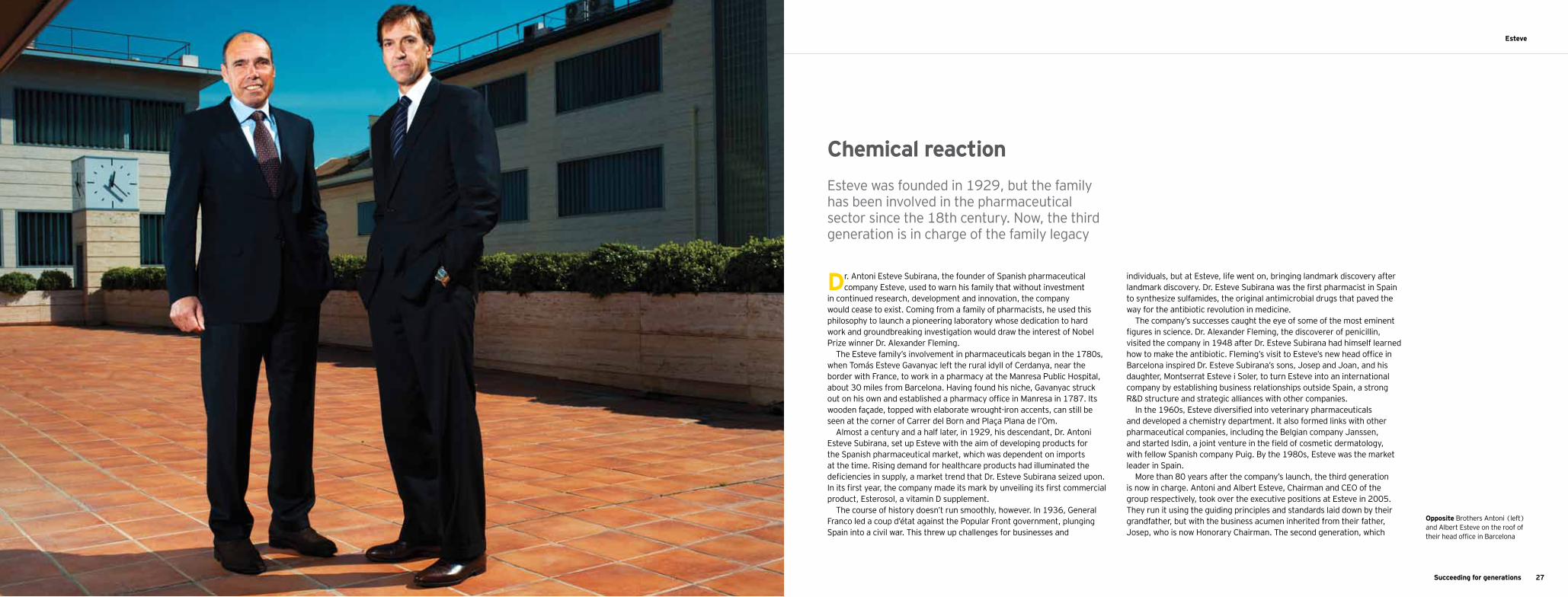

Esteve was founded in 1929, but the family has been involved in the pharmaceutical sector since the 18th century. Now, the third generation is in charge of the family legacy

Chemical reaction

Dr. Antoni Esteve Subirana, the founder of Spanish pharmaceutical company Esteve, used to warn his family that without investment

in continued research, development and innovation, the company would cease to exist. Coming from a family of pharmacists, he used this philosophy to launch a pioneering laboratory whose dedication to hard work and groundbreaking investigation would draw the interest of Nobel Prize winner Dr. Alexander Fleming.

The Esteve family’s involvement in pharmaceuticals began in the 1780s, when Tomás Esteve Gavanyac left the rural idyll of Cerdanya, near the border with France, to work in a pharmacy at the Manresa Public Hospital, about 30 miles from Barcelona. Having found his niche, Gavanyac struck out on his own and established a pharmacy office in Manresa in 1787. Its wooden façade, topped with elaborate wrought-iron accents, can still be seen at the corner of Carrer del Born and Plaça Plana de l’Om.

Almost a century and a half later, in 1929, his descendant, Dr. Antoni Esteve Subirana, set up Esteve with the aim of developing products for the Spanish pharmaceutical market, which was dependent on imports at the time. Rising demand for healthcare products had illuminated the deficiencies in supply, a market trend that Dr. Esteve Subirana seized upon. In its first year, the company made its mark by unveiling its first commercial product, Esterosol, a vitamin D supplement.

The course of history doesn’t run smoothly, however. In 1936, General Franco led a coup d’état against the Popular Front government, plunging Spain into a civil war. This threw up challenges for businesses and

individuals, but at Esteve, life went on, bringing landmark discovery after landmark discovery. Dr. Esteve Subirana was the first pharmacist in Spain to synthesize sulfamides, the original antimicrobial drugs that paved the way for the antibiotic revolution in medicine.

The company’s successes caught the eye of some of the most eminent figures in science. Dr. Alexander Fleming, the discoverer of penicillin, visited the company in 1948 after Dr. Esteve Subirana had himself learned how to make the antibiotic. Fleming’s visit to Esteve’s new head office in Barcelona inspired Dr. Esteve Subirana’s sons, Josep and Joan, and his daughter, Montserrat Esteve i Soler, to turn Esteve into an international company by establishing business relationships outside Spain, a strong R&D structure and strategic alliances with other companies.

In the 1960s, Esteve diversified into veterinary pharmaceuticals and developed a chemistry department. It also formed links with other pharmaceutical companies, including the Belgian company Janssen, and started Isdin, a joint venture in the field of cosmetic dermatology, with fellow Spanish company Puig. By the 1980s, Esteve was the market leader in Spain.

More than 80 years after the company’s launch, the third generation is now in charge. Antoni and Albert Esteve, Chairman and CEO of the group respectively, took over the executive positions at Esteve in 2005. They run it using the guiding principles and standards laid down by their grandfather, but with the business acumen inherited from their father, Josep, who is now Honorary Chairman. The second generation, which

Opposite Brothers Antoni (left) and Albert Esteve on the roof of their head office in Barcelona

Succeeding for generations28 29Succeeding for generations

Esteve

included their uncle and aunt, Joan and Montserrat, also placed an emphasis on professional management; former Group CEO Joaquim Targa was key to Esteve’s growth. “The skills of our family’s second generation lie in their ability to generate trust in others and go on to establish business agreements after gaining that trust,” says Antoni.

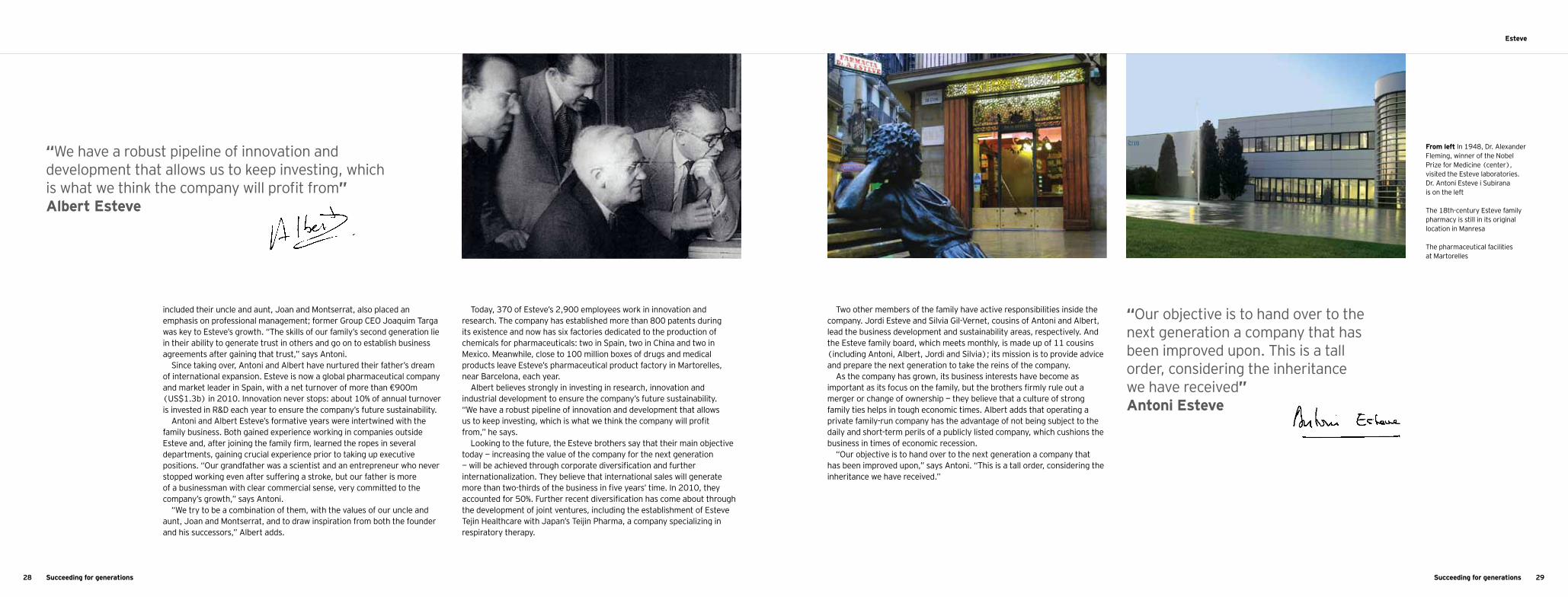

Since taking over, Antoni and Albert have nurtured their father’s dream of international expansion. Esteve is now a global pharmaceutical company and market leader in Spain, with a net turnover of more than €900m (US$1.3b) in 2010. Innovation never stops: about 10% of annual turnover is invested in R&D each year to ensure the company’s future sustainability.

Antoni and Albert Esteve’s formative years were intertwined with the family business. Both gained experience working in companies outside Esteve and, after joining the family firm, learned the ropes in several departments, gaining crucial experience prior to taking up executive positions. “Our grandfather was a scientist and an entrepreneur who never stopped working even after suffering a stroke, but our father is more of a businessman with clear commercial sense, very committed to the company’s growth,” says Antoni.

“We try to be a combination of them, with the values of our uncle and aunt, Joan and Montserrat, and to draw inspiration from both the founder and his successors,” Albert adds.

Today, 370 of Esteve’s 2,900 employees work in innovation and research. The company has established more than 800 patents during its existence and now has six factories dedicated to the production of chemicals for pharmaceuticals: two in Spain, two in China and two in Mexico. Meanwhile, close to 100 million boxes of drugs and medical products leave Esteve’s pharmaceutical product factory in Martorelles, near Barcelona, each year.

Albert believes strongly in investing in research, innovation and industrial development to ensure the company’s future sustainability. “We have a robust pipeline of innovation and development that allows us to keep investing, which is what we think the company will profit from,” he says.

Looking to the future, the Esteve brothers say that their main objective today — increasing the value of the company for the next generation — will be achieved through corporate diversification and further internationalization. They believe that international sales will generate more than two-thirds of the business in five years’ time. In 2010, they accounted for 50%. Further recent diversification has come about through the development of joint ventures, including the establishment of Esteve Tejin Healthcare with Japan’s Teijin Pharma, a company specializing in respiratory therapy.

Two other members of the family have active responsibilities inside the company. Jordi Esteve and Silvia Gil-Vernet, cousins of Antoni and Albert, lead the business development and sustainability areas, respectively. And the Esteve family board, which meets monthly, is made up of 11 cousins (including Antoni, Albert, Jordi and Silvia); its mission is to provide advice and prepare the next generation to take the reins of the company.

As the company has grown, its business interests have become as important as its focus on the family, but the brothers firmly rule out a merger or change of ownership — they believe that a culture of strong family ties helps in tough economic times. Albert adds that operating a private family-run company has the advantage of not being subject to the daily and short-term perils of a publicly listed company, which cushions the business in times of economic recession.

“Our objective is to hand over to the next generation a company that has been improved upon,” says Antoni. “This is a tall order, considering the inheritance we have received.”

From left In 1948, Dr. Alexander Fleming, winner of the Nobel Prize for Medicine (center), visited the Esteve laboratories. Dr. Antoni Esteve i Subirana is on the left

The 18th-century Esteve family pharmacy is still in its original location in Manresa

The pharmaceutical facilities at Martorelles

“We have a robust pipeline of innovation and development that allows us to keep investing, which is what we think the company will profit from”Albert Esteve

“Our objective is to hand over to the next generation a company that has been improved upon. This is a tall order, considering the inheritance we have received”Antoni Esteve

Succeeding for generations30 31Succeeding for generations

Oras Invest

The Paasikivis are one of Finland’s most successful families, having turned a small metal workshop into a US$1b business. Now it’s the third generation’s turn to shine

Portrait of a family

Owning a company is worlds apart from investing in one, at least for the Paasikivis. One of Finland’s most successful families, they are

second- and third-generation entrepreneurs turned industrial owners. Their company, Oras Invest, has some of Finland’s finest under its wings.

Modest beginnings marked the birth of the Paasikivi family business. In 1945, Erkki Paasikivi founded Oras Ltd. with his wife, Irja, née Oras, in his father-in-law Kosti’s basement. It started out as a small metal workshop producing pretty much anything people needed. Kosti Oras was a firm believer in the younger generation’s skills and knew Erkki and Irja could achieve a lot. Be that as it may, there is no way Kosti could have guessed that Erkki and Irja’s decision to name their little company after him would eventually make his surname an international brand.

The small basement operation took its first steps toward serial production when Erkki managed to get his hands on a batch of surplus grenade shells, which he manufactured into radiator pipe connectors. It seems that once the Paasikivi family was introduced to the winning combination of metal and water, nothing could stop them.

In the 1950s, the business grew in parallel with Finland, a country that was rebuilding itself with unmatched vigor after the war. Water-related foundry products soon formed the core of the business and, by the 1970s, Oras was a synonym for faucets. High-quality, consistent innovation and design collaboration with the likes of Alessi have made the company the Nordic market leader, one of the largest manufacturers of faucets in Europe and an internationally known brand.

Yet today the family business is about much more than this. Oras Invest is an industrial owner with a mission. For the Paasikivis, industrial ownership means never investing mere money in a company. Being part of the family’s portfolio of companies means that the Paasikivis will also invest their time, talent and expectations in a company. They plan on being part of its history.

In addition to owning 100% of the original company, Oras, the family business owns a quarter of Uponor and 18% of both Kemira and Tikkurila — all three are major listed companies on the Finnish stock exchange. All of Oras Invest’s companies operate in water technology, housing solutions or both. At the end of 2010, Oras Invest’s net asset value was more than €650m (US$940m). Not bad for a family business.

“We aim to be the largest owner in our listed companies and majority owner in our unlisted ones,” explains Annika Paasikivi, granddaughter of the founders and board member of Oras Invest since 2006. This is in line with the Paasikivi outlook on business. First and foremost, they are a family business, fully family owned and family run. Second, they are responsible industrial owners. The Paasikivis see nothing wrong with short-term investors; they simply want to make it clear that their approach to business is different.

“Our aim is to act in the best interests of the company,” she adds. “We are not after fast returns, or in it for a three- to eight-year stretch. We are looking for steady profit, healthy growth and a solid foundation for sustainable development. We only seek ownership in companies that we

Opposite Kaj, Annika and Eerik Paasikivi, grandchildren of the founders

Succeeding for generations32 Succeeding for generations 33

Oras Invest

can literally grow old with and then pass to the next generation; companies that will benefit and prosper from the know-how we bring in as owners.”

In 2011, the third generation of Paasikivis, of which Annika is part, is preparing to take the lead. Living up to the success associated with the family name is by no means simple, but it takes only a few moments in their presence to be convinced that this pack will hold their own. Annika, Kaj and Eerik Paasikivi represent the new generation on Oras Invest’s board. Kaj is also a member of the board at Oras Ltd, along with his brother, Risto.

The third generation comprises seven cousins in total, and they meet up regularly to discuss the family business. More cousins may well join Annika, Kaj and Eerik on the board in the future, but no one is forced to take part in the operative business. However, if the rest of the cousins share even a portion of the enthusiasm these three show, it is likely we will be seeing more Paasikivis on the Oras Invest board and in operative roles in the years to come. Admittedly, it is not an easy challenge. Working with your entire family is one thing. Joining a group with decades of unflappable business success is an entirely different matter.

The Paasikivis have the reputation of not having a reputation. Rarely in the public eye, they go from one success to another without so much as a whiff of failure. A track record so good might even be a burden to future generations. Is a family member allowed to make mistakes? “Of course, but preferably in their youth while working for somebody else,” Annika says with a stern face. It takes a moment to grasp that she is kidding. “Seriously speaking, we all share the family’s strong values, which for us

represent a way of life: ownership, vitality, commitment and endurance,” she says. “Together, they spell out the respect we feel toward work. We always live up to these values, whether we are employed by the family or by someone else.”

For Oras Invest, as for any family business, the generation gap is something to be overcome. Some claim a family should not consider a change in generation until everyone — including the older generation — is old enough to respect the rest, regardless of age. “We definitely have mutual respect,” says Annika. “I think I am starting to resemble my father more and more each year. Or perhaps I always did and was not willing to admit it earlier on!

“Even though you are someone’s child or niece or nephew, it does not mean anyone is allowed to treat you as a child after you’ve reached a certain position,” she adds. “This is vital in order to keep the business running, although I must admit that I have one exception to this rule. My grandmother, solid as a rock and one of the smartest people I know, is in her 90s now. She is allowed to tell me off, tell me what to do and treat me as if I still have a lot of living and learning to do before she deems me a grownup. From her perspective, I gather I still do have a thing or two to learn about life.”

Oras Invest could make a full generation shift at any point, but the family is in no particular hurry. There is a large enough age difference between Pekka, Jukka and Jari — Annika’s father and his two brothers — to keep things running smoothly. Annika and her cousins hope that Jari,

who is the youngest brother and CEO of Oras Invest, will stay with the company for a good 10 years after Jukka and Pekka retire.

“Not that I believe my father or any of his brothers would ever actually retire,” Annika laughs. “Mark my word, all three will be in and out of here, pottering about, for as long as they live. This business is a part of who they are. I would say that this is one of the best things about being in a family business. It is virtually impossible to lose knowledge due to key people leaving or retiring. We’re in this for life.”

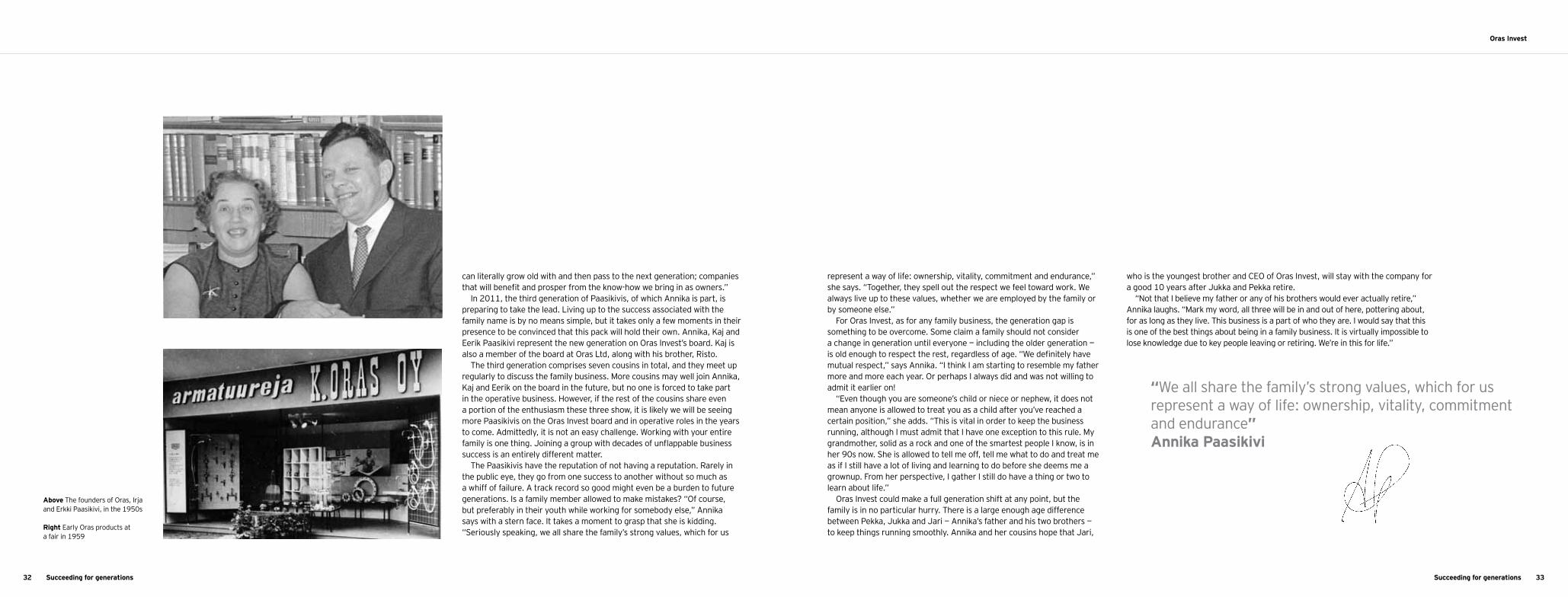

Above The founders of Oras, Irja and Erkki Paasikivi, in the 1950s

Right Early Oras products at a fair in 1959

“We all share the family’s strong values, which for us represent a way of life: ownership, vitality, commitment and endurance”Annika Paasikivi

Succeeding for generations34 35Succeeding for generations

Avantha Group

The Thapar family has been in business for nearly a century. A split in the second generation paved the way for Avantha, now one of India’s biggest conglomerates

Future gazing

Hanging on the walls of the Avantha Group’s headquarters at Thapar House in New Delhi is an art installation of large clocks. Somewhere

in the middle, there is one that purports to tell the time in Pataal (“netherworld” in Hindi). “This one goes anti-clockwise,” explains Gautam Thapar, Chairman and CEO of the US$4b Avantha Group.

So let’s go back in time to 1919, when Thapar’s grandfather, Karam Chand Thapar, founded what would become the Thapar Group. He started out in the coal-trading business in the early 1920s and, over time, built up assets and entered into manufacturing. He made forays into industries ranging from textiles and chemicals to sugar, banking, insurance and paper. He had four sons and eventually passed the Thapar Group to his third son and Gautam’s uncle, Lalit Mohan Thapar. When it came time to think about the third generation, Lalit had been grooming his nephew, Vikram, to take over the business — but ended up choosing Gautam as the successor instead.

It’s a situation that family businesses dread: how do you solve the problem of two or more family members competing for the top spot? There is the potential for hurt feelings, endless mediation and even court battles.

But not in the Thapar Group’s case. Gautam had never expected to become leader of the group; in the 1980s, he was studying chemical engineering in the US. He returned to India in 1985 to join the family business, and had risen in Lalit’s estimation after turning around the fortunes of group companies such as Andhra Pradesh Rayons, Ballarpur Industries (BILT) and Crompton Greaves (CG). Therefore, Lalit, who

Opposite Gautam Thapar at Avantha’s New Delhi headquarters. One of the clocks in this installation runs backwards, purporting to tell the time in the netherworld

Succeeding for generations36

Avantha Group

Succeeding for generations 37

never married, left his share of the businesses to Gautam in 2005 when he retired.

The Thapar empire divided in its second generation, unlike most family conglomerates, which tend to split in the third. A four-way division of the family’s assets in 1999 was followed by a separation between Gautam and his older sibling Karan in 2005. Unlike other splits, however, the Thapar Group partition was a rather amicable one. Instead of fighting with his cousins over the family name, Gautam Thapar decided to drop the baggage of the past and rebrand his group businesses as Avantha in 2007.

But no matter how amicable the split, a change of that magnitude was never going to be without its difficulties, particularly in the immediate aftermath. It took time to financially consolidate the holdings and resolve pending issues. “We lost time,” admits Thapar.

And so a new era began. Yet Thapar feels that Avantha and the original Thapar Group have a lot in common. “My grandfather was someone who relied on professionals. That culture is still there,” he says. “Moreover, he was a risk-taker. But then, he learned his lessons rather quickly. That quality lives on in the group.”

In practice, Thapar puts decisions into two categories: those that are good for the individual businesses and those that are good for the group. He takes the lead on the latter, looking strategically at what will drive growth in the group, and leaves the day-to-day running of the individual businesses to their respective CEOs. His strategy is working. In recent years, he has globalized the group’s operations, made acquisitions and

expanded capacities. The group has manufacturing facilities in more than 10 countries and a worldwide customer base. Its businesses include BILT, the largest manufacturer of writing and printing paper in India; CG, an engineering company dealing in the management and application of electrical energy; the Global Green Company, Avantha’s foods division; Solaris ChemTech Industries; Avantha Power and Infrastructure; Builtech Building Elements, which is focused on green building materials; and Salient Business Solutions and Avantha Technologies, which both deal in IT and IT-enabled services. BILT and CG together account for nearly 65% of the group’s revenues.

All this growth has resulted in a fourfold increase in Avantha’s turnover — from US$1b in 2003 to US$4b today — and it is on track to achieve a turnover of US$10b by 2015. “In a country that is growing at 9% per annum, there are opportunities emerging every day,” says Thapar.

And the company is quick to capitalize on these opportunities. Its overseas acquisitions began in 2005, with CG taking over Belgium-based power-transformer maker Pauwels. Since then, CG has made five global acquisitions in the US, France, Hungary, Ireland and the UK.

Other group companies have also grown inorganically, with Global Green acquiring Belgium-based Intergarden in 2006 and Hungarian food company Puszta Konzerv in 2008. Similarly, in 2007, BILT acquired Malaysia-based Sabah Forest Industries and, recently, Bangalore-based Premier Tissues India. In the IT sector, the Avantha Group acquired Pyramid Healthcare Solutions, based in Florida in the US.

Globalization initiatives have exposed the group to a plethora of risks, however, which has necessitated a risk and governance framework. Thapar has already put an Avantha management board structure in place to manage the group companies better. The primary purpose of the board is to prepare the group for future growth and create a global Avantha. It focuses on financial matters, talent, R&D, technology and sustainability. It reviews each of the group businesses along these parameters and advises Thapar on issues such as investment, disinvestment and diversification.

Talent is another key area for the group. According to Thapar, companies today need to make themselves attractive to global talent. “The best talent will not join you if they know that they have to be subservient to the promoter in any way,” he says. He believes strongly in giving professionals in all his group companies the freedom to manage as they see fit.

Avantha may have a new name, but its roots are intertwined with those of the Thapar family. Thapar himself has two daughters, aged 11 and 13, but isn’t making any predictions about whether they will join him at Avantha. Some time back, he and his wife decided that they would not press them to join the family business. While he’s not closing any route to his children, Thapar wants them to be clear about the difference between ownership and management of a business. “It’s one thing to understand the nitty-gritty of a company and quite another to understand your role as a shareholder,” he says. Even if his daughters decide to go down that route, Thapar insists that the day-to-day running of the companies will be left to the professionals. “Talent is not genetic,” he says. “Globally, there are several professionally managed, family-owned businesses where both the management and the board are headed by a professional, non-family person.”

Whether Thapar’s daughters play a leading role in the business or not, it’s clear that it will always have professionalism at its heart. For him, there are three things that will keep Avantha ahead of its competitors: the fact that it gives its people freedom to operate in the way they see fit; the fact that it is very good at the basic skill of manufacturing and getting margins out of manufacturing; and the fact that, as the company grows, its skills base grows too. This is one family business that is always looking ahead.

“Our secrets to success are that we give our people freedom to operate, we have a strong understanding of manufacturing and we add skills as we grow”Gautam Thapar

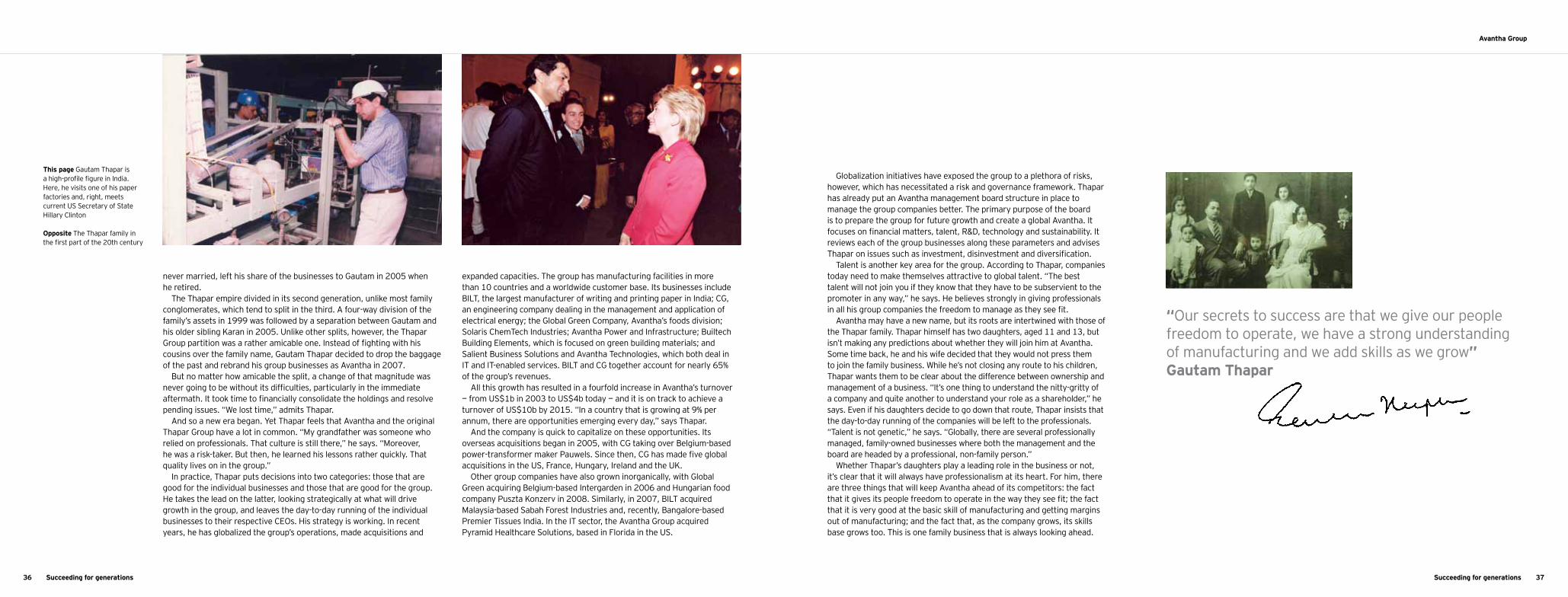

This page Gautam Thapar is a high-profile figure in India. Here, he visits one of his paper factories and, right, meets current US Secretary of State Hillary Clinton

Opposite The Thapar family in the first part of the 20th century

Succeeding for generations38 39

Timeline: Media and publishing

1935 Penguin paperbacks are born. Allen Lane has grown frustrated with the lack of cheap, good quality paperback books being sold in Britain and so decides to launch a range of contemporary works that are cheap enough to be sold in corner shops.

1901

1901 Giovanni De Agostini founds the Istituto Geografico De

Agostini, which evolves into the De Agostini Group, now owned by

the Boroli and Drago families.

800AD 1400 18001600 19001500 1700 2000

1953 Playboy magazine is published for the first time, with Marilyn Monroe on the cover. It is not dated, as co-founder Hugh Hefner does not know if there will be another.

1501 Italian Ottaviano Petrucci is a leading light among music printers and is granted a monopoly on printing certain types of music in Venice for 20 years. Some of the methods he uses, such as the size of the note stem, are still in use now.

1450s The Gutenberg Bible is the first book in Europe to be produced using a movable type printing press. Before this, books in the region had been copied by hand. German Johannes Gutenberg comes up with the method for mass-producing books and paves the way for affordable printed work that could be produced in large quantities.

1741 Benjamin Franklin is due to publish the first

magazine, General Magazine, in the US, but is beaten

by three days by Andrew Bradford’s American

Magazine. Both publications last a matter of months.

1663 The world’s first magazine is published in Germany by Johann Rist, a theologian and poet who lives in Hamburg. It is called Erbauliche Monaths-Unterredungen (Edifying Monthly Discussions).

1856 Langenscheidt Publishing Company is founded. Still family owned, it produces dictionaries, maps and educational material. 2000s Regional and

national newspapers see circulation falling, which many put down to the rise of the internet and 24-hour rolling news.

1979 Rupert Murdoch creates News Corporation as a holding company for News Limited, which holds assets inherited from his father, Sir Keith Murdoch. Three of Rupert Murdoch’s children, James, Lachlan and Elisabeth, now work for News Corporation.

868 AD The oldest known printed book in the world, the Diamond Sutra, is published in China. According to the British Library, seven

strips of paper are printed using carved wooden blocks and then stuck together to make a scroll more than five meters long.

1963 Ralph J. Roberts founds Comcast Corporation, one of the world’s leading media, entertainment and communication companies.

1922 Sam Newhouse founds the family-owned business Advance Publications, Inc. with the purchase of the Staten Island Advance.

1887 After taking control of The San

Francisco Examiner from his father,

William Randolph Hearst founds the

Hearst Corporation. The Hearst family is still involved in

the ownership and management

of the publishing empire.

1857 The McClatchy Company dates to the California Gold Rush era, when James McClatchy is one of the founding editors of its first newspaper, The Sacramento Bee.

From the Gutenberg Bible to political blogs, the industry proves that the pen is indeed more powerful than the sword

Media and publishingEntertaining and informing the world

Succeeding for generations40 41Succeeding for generations

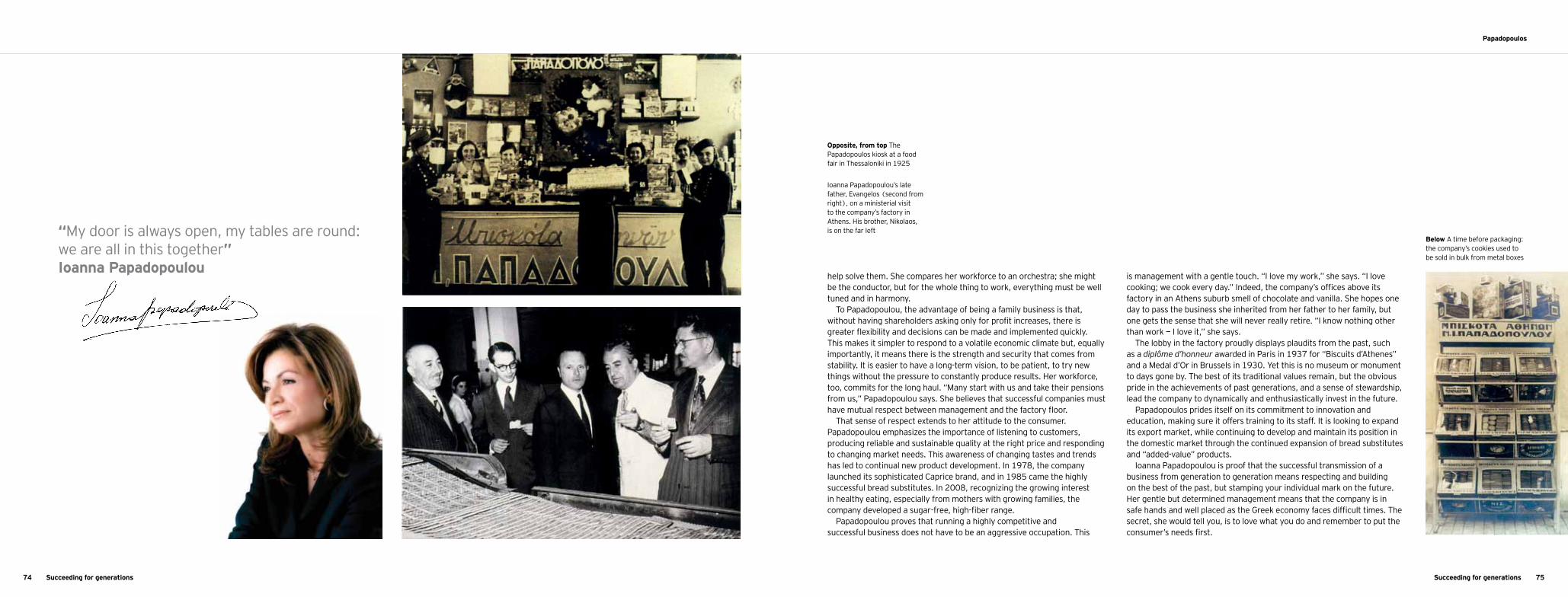

De Agostini Group

Long famous for its publishing activities, De Agostini is still controlled by the Drago and Boroli families. Now its interests extend far beyond the written word

A broad canvas

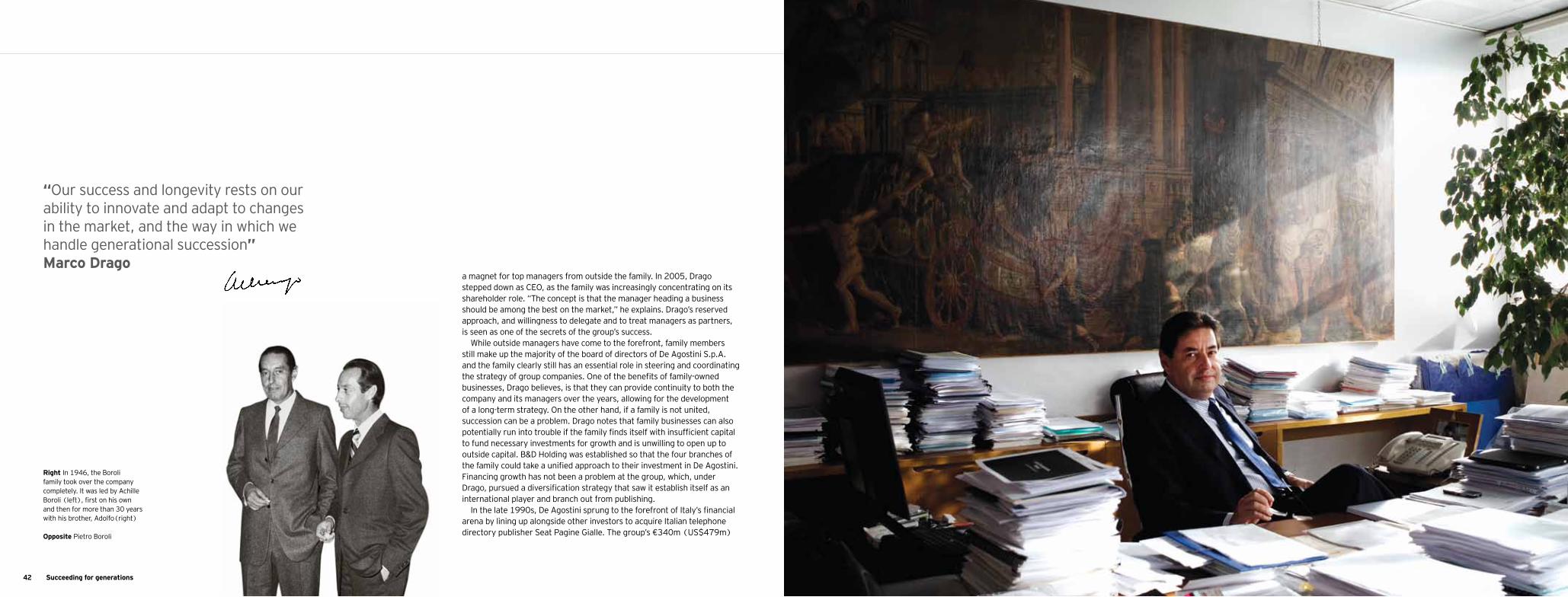

Marco Drago seemingly had little choice but to join the family business. One day in 1969, not long after receiving an economics degree from

Milan’s Bocconi University, his uncle, Adolfo Boroli, told him to report for work the following Monday at the family’s company, Istituto Geografico De Agostini. Drago, whose mother, Giuliana Boroli, was one of Adolfo’s sisters, willingly complied.

He had other job offers, but felt drawn to the publishing sector. “I certainly couldn’t have imagined everything that has taken place since then,” he says. “It’s made a great story.”

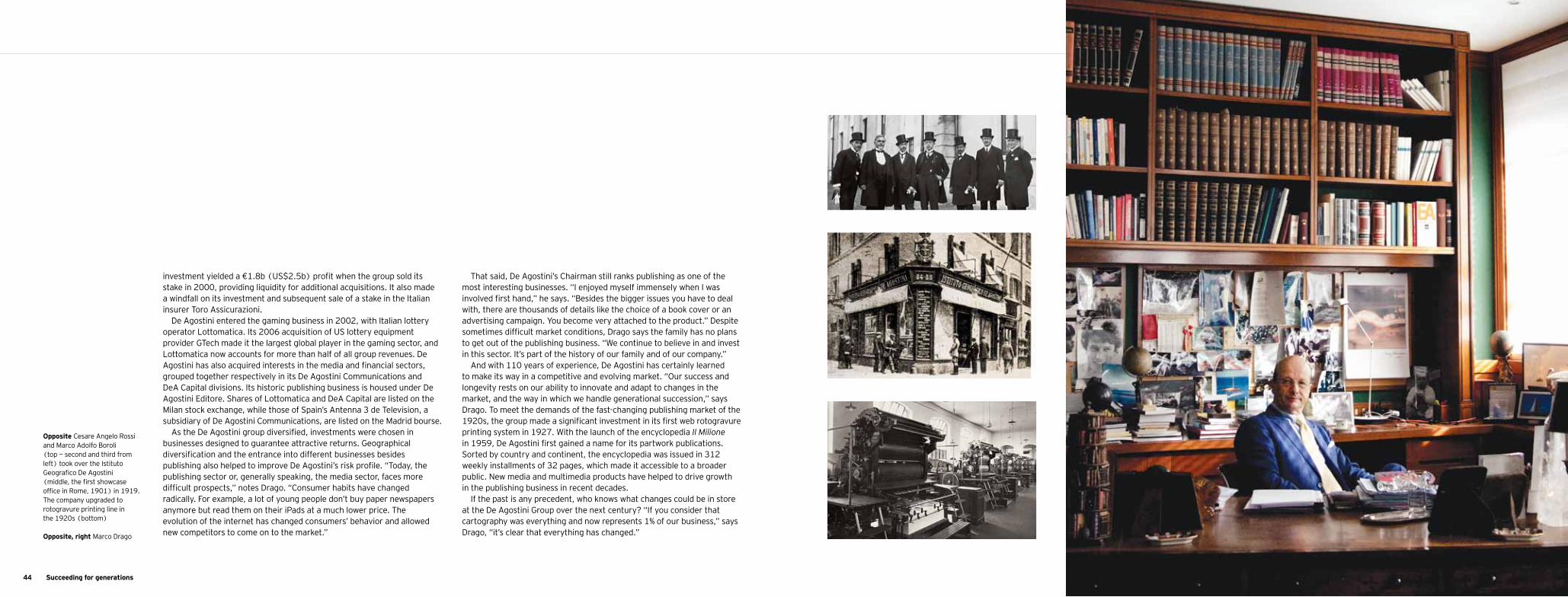

Drago worked his way up in the company, becoming a manager in 1975 and spearheading domestic and international growth as CEO of the De Agostini Group’s publishing business in the 1980s and 1990s. The current chapter of the De Agostini story sees the 65-year-old Drago as Chairman of De Agostini S.p.A., the group holding company that now comprises not only the historic publishing work of the Boroli and Drago families, but also media, gaming and services, and financial activities. Today, the De Agostini Group is an international force, with group revenues of more than €4b (US$5.6b) and a presence in 66 countries.

De Agostini’s history dates back to 1901, when the geographer Giovanni De Agostini set up a mapmaking business in Rome. Just a few years later, he moved the company to Novara in northern Italy, not far from Milan. Marco Drago’s maternal grandfather, Marco Boroli, and Boroli’s business partner, Cesare Rossi, acquired De Agostini in 1919, with the Boroli family taking full control of the group in 1946. It was initially Marco Boroli’s son,

Achille, subsequently accompanied by his brother Adolfo, who built up the company’s publishing business in the decades after World War II.

Beginning in the 1960s, more than a dozen members of the third generation of the family, including Marco Drago himself, took on operational positions in the group. Today, two members of the fourth generation of the company have management roles in group companies and two others sit on the board of directors of the holding company, De Agostini S.p.A.

Drago expects more family members from the fourth generation to take an increasingly active role in De Agostini companies to help pave the way for succession in B&D Holding, the limited partnership of the Boroli and Drago families that controls the De Agostini Group. “For this, we must train the fourth generation of shareholders to take our place when the time comes,” he says. As Chairman of B&D Holding, he wants to leave behind a solid and sustainable company for the next generation.

While family members seeking a job in the De Agostini Group were once welcomed with open arms, today they must meet strict requirements and demonstrate they can stack up well against outside competition. Requisites include at least five years’ experience in another company, knowledge of languages and a solid degree. The company’s board of directors has devised official criteria for family members looking to enter the company; there is also a special committee that evaluates the qualifications and career development of the fourth-generation shareholders. This stringent personnel selection policy has helped to make the De Agostini Group

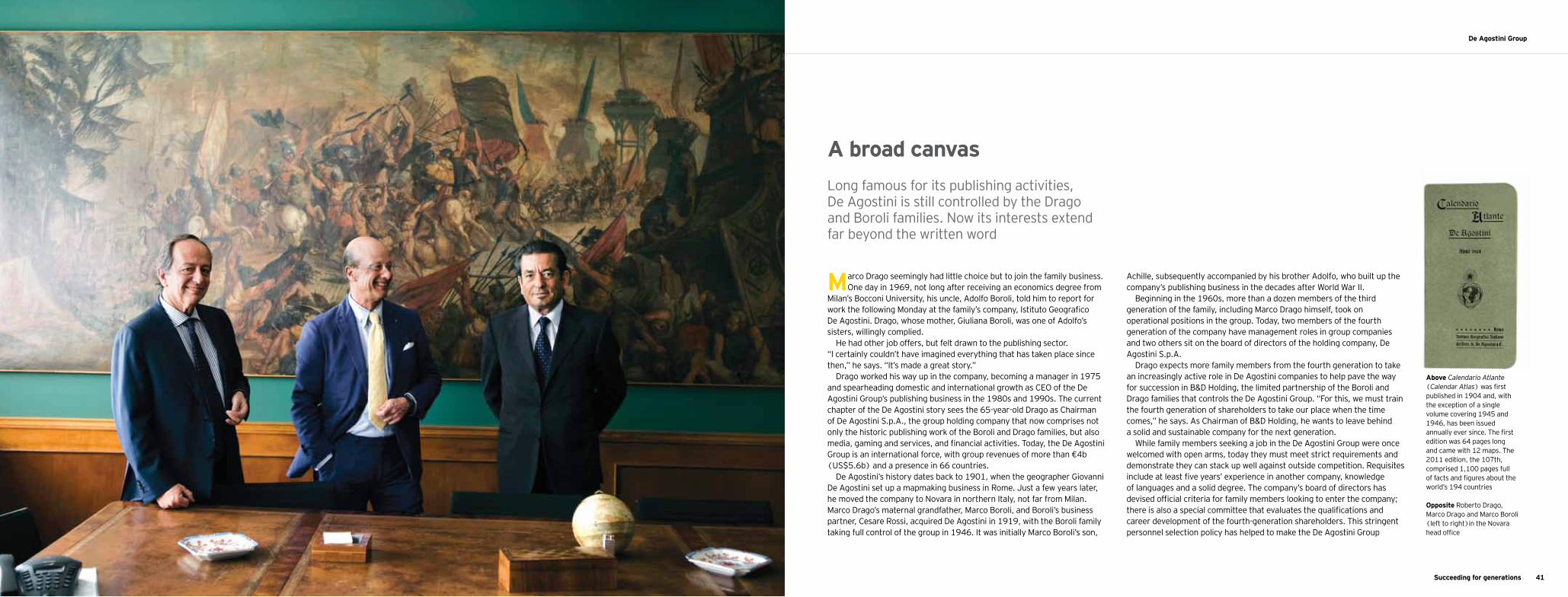

Above Calendario Atlante (Calendar Atlas) was first published in 1904 and, with the exception of a single volume covering 1945 and 1946, has been issued annually ever since. The first edition was 64 pages long and came with 12 maps. The 2011 edition, the 107th, comprised 1,100 pages full of facts and figures about the world’s 194 countries

Opposite Roberto Drago, Marco Drago and Marco Boroli (left to right)in the Novara head office

Succeeding for generations42

De Agostini Group

Succeeding for generations 43

a magnet for top managers from outside the family. In 2005, Drago stepped down as CEO, as the family was increasingly concentrating on its shareholder role. “The concept is that the manager heading a business should be among the best on the market,” he explains. Drago’s reserved approach, and willingness to delegate and to treat managers as partners, is seen as one of the secrets of the group’s success.

While outside managers have come to the forefront, family members still make up the majority of the board of directors of De Agostini S.p.A. and the family clearly still has an essential role in steering and coordinating the strategy of group companies. One of the benefits of family-owned businesses, Drago believes, is that they can provide continuity to both the company and its managers over the years, allowing for the development of a long-term strategy. On the other hand, if a family is not united, succession can be a problem. Drago notes that family businesses can also potentially run into trouble if the family finds itself with insufficient capital to fund necessary investments for growth and is unwilling to open up to outside capital. B&D Holding was established so that the four branches of the family could take a unified approach to their investment in De Agostini. Financing growth has not been a problem at the group, which, under Drago, pursued a diversification strategy that saw it establish itself as an international player and branch out from publishing.

In the late 1990s, De Agostini sprung to the forefront of Italy’s financial arena by lining up alongside other investors to acquire Italian telephone directory publisher Seat Pagine Gialle. The group’s €340m (US$479m)