Embed Size (px)

Citation preview

Sukuk Market in Malaysia: Issues of

Structuring

By Prof Dato’ Dr. Mohd Azmi Omar and Dr Azman

bin Mohd Noor

International Islamic University Malaysia

Content

2

Introduction

Definition of Sukuk

Tradeability of sukuk

Shariah principles used in different types of sukuk

Shariah and legal issues and challenges

17 Full fledge Islamic Banks

10 Conventional banks with ‘Islamic window’

4 International Islamic Banks

Islamic Finance in Malaysia

Financial System in Malaysia Conventional

Banking

Islamic Banking

Takaful Islamic Money

Market

Islamic Capital Market

Insurance Money Market

Capital Market

Islamic Banking Takaful

12 Takaful Oprators

4 Retakaful Operators

Money Market for Islamic Banks

Daily Transactions RM 1 billion Bursa Suq Al Sila’ as a platform

for Commodity Murabahah trading

Money Market Capital Market

88% halal counters/stocks traded at Bursa Malaysia

57% of private debt securities are sukuk

14 Islamic Fund Management institutions

152 Islamic funds 36 Islamic Fund Management

Institutions with Islamic mandate

Labuan Offshore FSA

Islamic Banking – 6 Islamic Banks and 9 Conventional banks with ‘Islamic window’. 3.8% of total banking industry.

Takaful & Retakaful– 7 retakaful and 9 conventional reinsurance with ‘Islamic window’

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Average total asset growth (2001-2010): 20.3% (asset)

The Growth of Islamic Banking in Maaysia

Asset : 20.8% (RM351b)

Financing : 22.7% (RM223.3b)

Deposit: 22.6% (RM277.5b)

Average Profit of Islamic Banking 15.4%

* Sumber: BNM Sistem Statistik Institusi Kewangan

RM

‘ 0

00

mil

lio

n

Asset Financing Deposit

Total Asset, Financing & Deposit of Islamic Banks (2001- 2010)

Singapore

0.1%

UAE

4%

Bahrain

2%

Saudi Arabia

7%

others

1%

Ofshores

17%

Indonesia

4%

Malaysia

65%

(USD 96 bilion)

Growing Financial Market

Malaysia the largest

sukuk issuer in the

world

Total Immatured Global Sukuk a

USD 148 bilion

Immatured Private Debt Securitiies (as of Dec 2010)

Islamic

57%

Conventional

43%

* Source: FAST

RM 323 b (USD 96b)

Definition of Sukuk

Sukuk is defined by Accounting and Auditing Organization for

Islamic Financial Institutions (AAOFI) as

“certificates of equal value representing undivided shares in

ownership of tangible assets, usufruct and services”

6

Nature of Sukuk

A ‘Sukuk’ is a Shari'ah-compliant variant of a conventional bond -

investor returns are derived from ownership of a business/assets

rather than interest-based debt obligations.

The Sukuk holders share profits from the business/assets.

7

Nature of sukuk

Economic characteristics similar to that of a conventional bond, key difference being that a Sukuk is not a debt instrument.

It represents a proportionate ownership in the underlying asset, giving the holder the ownership and accordingly the right to the benefits of the income stream of the underlying asset.

The yield is usually linked to a return on an underlying asset through an Islamic structure e.g. lease.

8

9

Types of assets eligible for Sukuk

Issuance

The type of assets eligible for Sukuk issuance or securitized

must be Shariah compliant . These are:

Existing tangible assets

Land, building

Future tangible assets

Bai al salam/Istisna'a/Ijarah Mausufah Fi Dhimma (forward/advance lease)

10

Financial assets/instruments/Intangibles

Ordinary shares

Intellectual Property? (see Islamic Fiqh Academy resolution No.43 (5/5)

Debts – account receivables ? Lease receivables ?

Contracts awarded by government, i.e, concession, construction, supply and

services

Usufructs/manfa`ah (financial benefits)

Note that the tangible or intangible assets or future tangible

assets may be owned or leased

Tradeability of Sukuk in secondary market

Sukuk Type Tradability

Sukuk of Freehold

Existing Assets

Acceptable

Sukuk of Existing Assets

Subject to Head Lease

Acceptable

Sukuk of Future

Tangible Assets

Can be traded only after the asset is created and identified. No

trading allowed while the asset is constructed except at par value

Sukuk of Existing

Specified Services

Acceptable prior to sub-leasing (selling) such services. Reason:

when we sub-lease, the sukuk represents rent receivables which

cannot be traded except at par value

Sukuk of Described

Future Services

Can be traded after the source of service is identified and

available. No trading allowed while the service is yet to be

available except at par value

11 Note: Adapted from (1) Adam, N and (2) Ayub, M. 2007.

Tradeability of Sukuk in secondary market

Sukuk Type Tradability

Sukuk Murabaha

Acceptable before sale of goods/commodity to the end buyer.

Once the goods are sold then trading is only accepted at par

value

Sukuk Salam Not acceptable except at par value

Sukuk Istisna'a Acceptable if funds are converted into assets and before sale to

party ordering the project

Sukuk Mudarabah,

Musharakah and

Wakalah

Acceptable after commencement of activity for which the funds

were raised

12 Note: Adapted from (1) Adam, N and (2) Ayub, M. 2007.

Types of Sukuk

13

Leased-based Sukuk – Sukuk Ijarah

Sukuk of Freehold Existing Assets

Sukuk of Existing Assets Subject to Head Lease

Sukuk of Future Tangible Assets (Mausufah Fi Dhimma (advance

lease)

Sukuk of Existing Specified Services

Sukuk of Described Future Services

Partnership-based Sukuk

Sukuk Mudaraba

Sukuk Musharaka

Sukuk Wakala

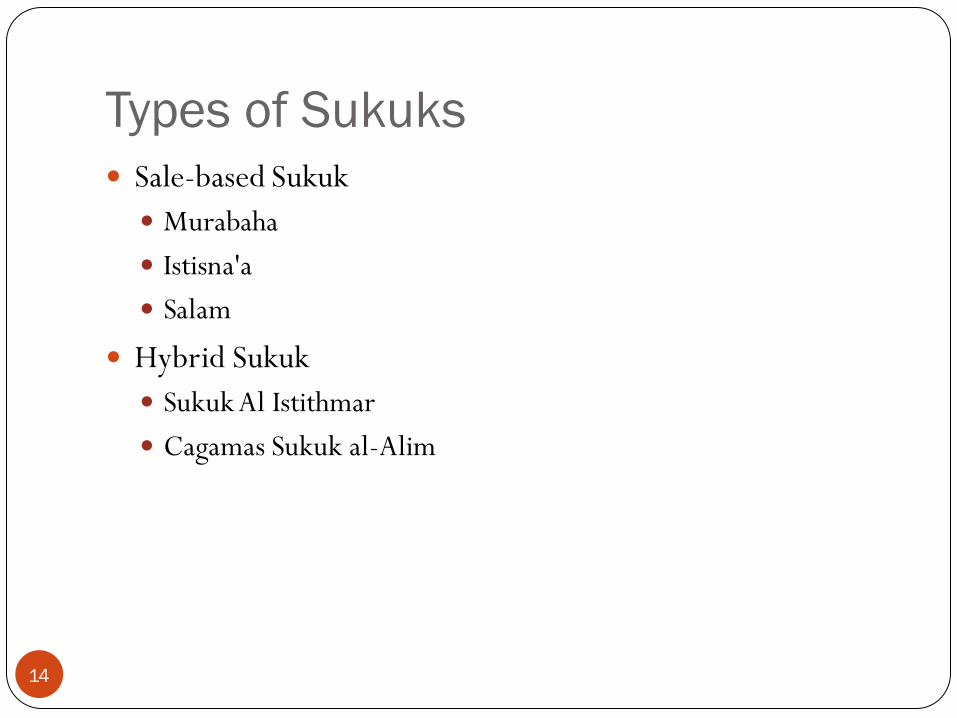

Types of Sukuks

14

Sale-based Sukuk

Murabaha

Istisna'a

Salam

Hybrid Sukuk

Sukuk Al Istithmar

Cagamas Sukuk al-Alim

Ijarah

A contract involving the transfer of the usufruct of an

underlying asset by the owner of the said asset to another

party, for an agreed tenure, at an agreed consideration

Lease period shall commence from the date on which the

underlying leased asset is delivered to the lessee

Subject matter of the lease must have valuable use and the

benefit from the lease must be lawful in Shariah

Relation between parties to Ijarah

Corpus of the leased asset remains in the ownership of the

lessor and only its usufruct is transferred to the lessee

15

Expenses

Liabilities arising from the ownership of the leased asset remains

with the lessor whilst the liabilities from the usufruct of the

leased asset shall be borne by the lessee i.e., liable to the wear

and tear of the asset normally occurs during its use

The lessee is responsible for any loss caused to the asset due to

his misuse and/or negligence

Lessor may delegate the task of performing major maintenance

and/or procurement of insurance to the lessee. However, cost

would still be borne by the lessor

Rental period within the lease tenure must be determined

clearly

16

Rental arising from the lease must be determined at the time

of contract for the whole rental period

The rental must be specified upfront, either as lump sum

amount covering the entire lease period or by installments for

parts of the duration of the lease rental period

Variable rental is allowed by way of referring the rental to a

predetermined benchmark

Security

Ijarah contract may include security arrangement allowed by

Shariah, to secure the rental payments or as security against

negligence and/or misuse of the leased asset by the lessee,

including charge over the assets, assignments of rights over the

leassee’s assets, amongst others

17

Common Ijarah Structures

Ijarah Muntahiah Bitamlik – Sale or hibah by

upon maturity,

Ijarah Mausufah Fi Dhima –

Forward/Advance Lease

Lease and Leaseback

18

Ijarah Muntahiah Bitamlik

Sale and leaseback of completed asset

3 steps process flow:

1. Financiers to purchase asset

2. Financiers to lease asset and receive lease rental

3. Financiers to sell the asset at nominal cost upon maturity of

the lease, via the Sale Undertaking (call option) and/or

Purchase Undertaking issued by the Lessor

Normally involve sale of beneficial ownership, whereby the

legal title of the asset shall remain with client at all times

Asset to be charged as security

19

Sukuk al-Ijara

20

As an owner of the leased assets, lessor could securitise

the ownership of the leased assets which could be

affected through a trust structure.

Through the securitisation of the ownership, the lease

receivables are also indirectly securitised.

The ijara backed securities are known as Sukuk al-

Ijara.

Sukuk al-Ijara

21

The issuer of these certificates is selling a proportionate

ownership of the leased asset

The subscribers are buyers of the asset.

The mobilised funds from subscription are the purchase

price of the asset, and the certificate holders become the

owners of the assets jointly with its benefits and risks.

Certificates of ownership of usufructs of existing assets

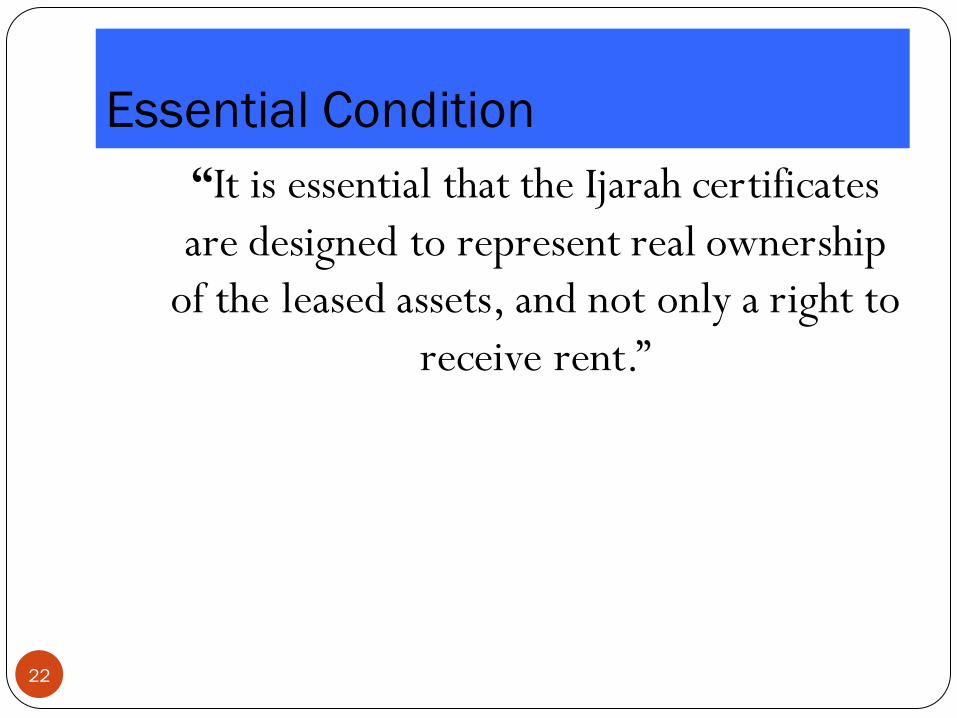

Essential Condition

22

“It is essential that the Ijarah certificates

are designed to represent real ownership

of the leased assets, and not only a right to

receive rent.”

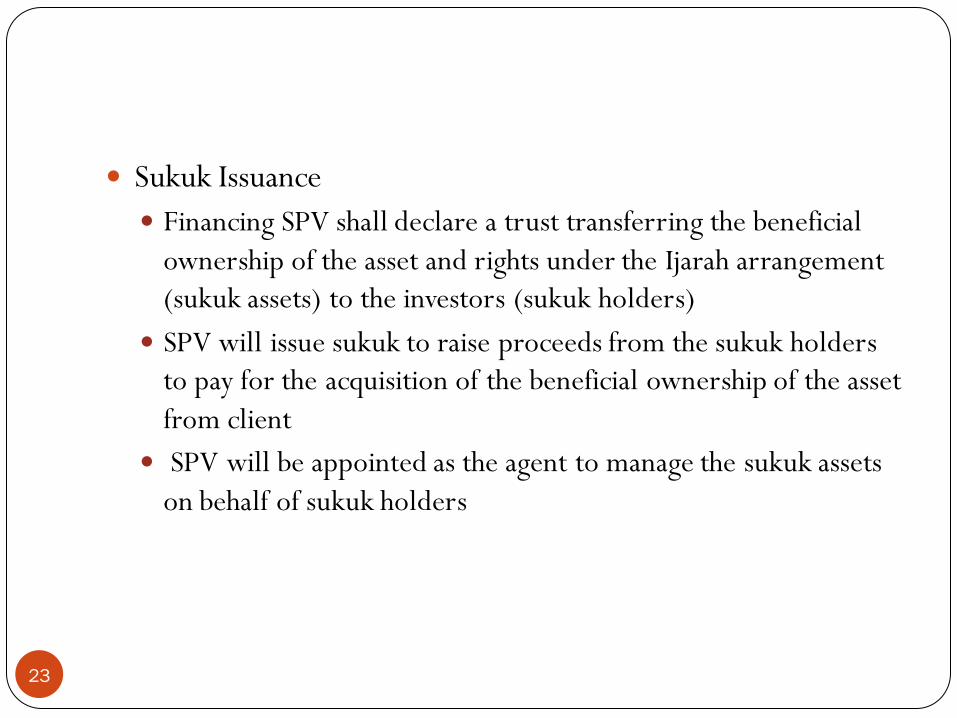

Sukuk Issuance

Financing SPV shall declare a trust transferring the beneficial

ownership of the asset and rights under the Ijarah arrangement

(sukuk assets) to the investors (sukuk holders)

SPV will issue sukuk to raise proceeds from the sukuk holders

to pay for the acquisition of the beneficial ownership of the asset

from client

SPV will be appointed as the agent to manage the sukuk assets

on behalf of sukuk holders

23

Why Shari'ah Compliance ?

24

Sukuk do not represent debt owned by the issuer/

certificate holder.

Sukuk do not issue for a pool of receivables.

As such, it distinguishes sukuk from shares and bonds.

Since Sukuk al Ijara evidence the undivided pro-rata

ownership of the underlying asset, it is freely tradedable

at par, premium or discount.

Malaysia Global Sukuk

Issuer Malaysia Global Sukuk Inc (“SPV”) in June 2002

Obligor Government of Malaysia (as lessee of Leased Assets)

Issue size US$600 mil

Leased assets Selayang Hospital, Tengku Ampuan Rahimah Hospital, Jalan Duta Government living quarters, Jalan Duta Government Office Complex

Issue rating BBB (S&P) / Baa2 (Moody) in line with the sovereign ceiling

Maturity 5 years with bullet payment (June 2007)

Yield Benchmarked on 6-month USD Libor plus credit spread

Listing Luxembourg SE, Bahrain SE & Labuan IFE

25

Malaysia Global Sukuk

26

GOM

Malaysia Global

Sukuk Inc

Secondary

Market

Primary

Subscribers Assets Sukuk

1. The Federal Land Commissioner sells

beneficial interest in land parcels to SPV for

USD600 m

2. SPV enters into a Master Ijara Agreement

with GOM

3. SPV declares a trust transferring the

beneficial ownership of the assets & rights

under the Ijarah agreement to the investors.

SPV issues Sukuk representing undivided

proportionate ownership in the leased

assets which gives rise to rights to share

the rental payments in the Master Ijara

arrangement (this satisfies the Shari'ah

requirement for ownership)

Purchase

Undertaking Sale undertaking

Malaysia Global Sukuk -Documentation

Document Parties Purpose

1. Asset Sale Agreement GOM & SPV To transfer the beneficial ownership of

the Assets from GOM to SPV.

2. Asset Lease Agreement SPV & GOM To lease the Assets to GOM.

3. Purchase Undertaking From GOM to SPV GOM undertakes to buy the Assets at

maturity or if it defaults under the lease.

4. Sale Undertaking From SPV to GOM SPV undertakes to sell the Assets to

GOM at maturity.

5. Service Agency Agreement Between SPV and GOM SPV appoints GOM as the Service Agent

for the Assets.

6. Trust Deed By SPV SPV declares a trust over the Leased

Assets in favour of the Sukuk-Holders.

Issues Sukuk to the Primary Subscribers.

7. Security Trust Deed Between the SPV and a

Professional Trustee

SPV appoints a Professional Trustee to

hold and manage the Trust Assets for the

Sukuk-Holders.

27

Document Parties Purpose

1. Asset Sale Agreement GOM & SPV To transfer the beneficial ownership of the

Assets from GOM to SPV.

2. Asset Lease Agreement SPV & GOM To lease the Assets to GOM.

3. Purchase Undertaking From GOM to SPV GOM undertakes to buy the Assets at

maturity or if it defaults under the lease.

4. Sale Undertaking From SPV to GOM SPV undertakes to sell the Assets to GOM

at maturity.

5. Service Agency Agreement Between SPV and GOM SPV appoints GOM as the Service Agent

for the Assets.

6. Trust Deed By SPV SPV declares a trust over the Leased Assets

in favour of the Sukuk-Holders. Issues

Sukuk to the Primary Subscribers.

7. Security Trust Deed Between the SPV and a

Professional Trustee SPV appoints a Professional Trustee to

hold and manage the Trust Assets for the

Sukuk-Holders.

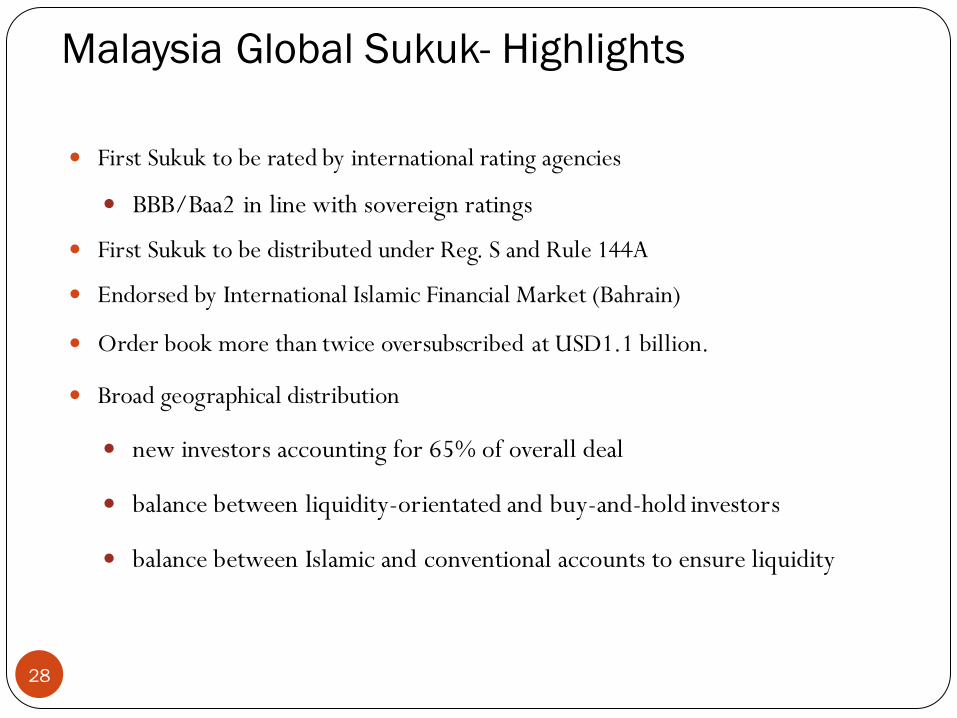

Malaysia Global Sukuk- Highlights

28

First Sukuk to be rated by international rating agencies

BBB/Baa2 in line with sovereign ratings

First Sukuk to be distributed under Reg. S and Rule 144A

Endorsed by International Islamic Financial Market (Bahrain)

Order book more than twice oversubscribed at USD1.1 billion.

Broad geographical distribution

new investors accounting for 65% of overall deal

balance between liquidity-orientated and buy-and-hold investors

balance between Islamic and conventional accounts to ensure liquidity

Malaysia Global Sukuk- Highlights

29

The transaction was announced on 10 June 2002 with the release of preliminary offering circulars to investors on that day.

Roadshow was conducted in East Asia, Middle East and Europe

Conventional accounts required more guidance on the transaction structure

Middle Eastern credits required more guidance on the Malaysian credit

Initial price guidance released on 20 June 2002 at US$LIBOR + 95 bps

Interest from Asia grew to US$600 million on same day

Price guidance revised to US$LIBOR + 95 - 98 bps due to market volatility

Deal was priced on 25 June 2002 at US$LIBOR + 95 bps

Deal closed oversubscribed at US$1.1 billion in orders from 51 accounts

Deal upsized to US$600 million

Source: Arshad Ismail

Why Sukuk Al-Ijarah is Highly Demanded?

30

Elimination of Bay Al-Inah & Bay A-Dayn elements in sukuk issuance. These 2 elements are regarded as non-Shari'ah compliant (trading debt paper or debt obligation - riba based financing) by most of scholars particularly Middle Easterns.

Shari'ah compliance - sukuk do not represent debt owned by the issuer/ certificate holder & sukuk do not issue for a pool of receivables.

The strength of the Malaysian sovereign credit and opportunity for stable risk diversification the BBB-rated deal will offer Middle Eastern-based accounts.

High Yield – 6 month USD Libor + credit spread.

Why Sukuk Al-Ijarah is Highly Demanded?

31

Listed on established International Exchanges i.e. Luxembourg,

Bahrain & Labuan.

Competitive pricing in line with conventional bond issues.

Ability to trade at premium – data show more buyers than sellers in

the market.

Priority in liquidation, similar to Secured Creditors as it is backed by

assets.

Sukuk holders have pro-rata undivided beneficial ownership of the

leased assets held in trust, as such entitled to the income streams from

the leased assets.

Hybrid Sukuk- Sukuk Istithmar

In a hybrid Sukuk, the underlying pool of assets can comprise

of Istisna'a, Murabaha receivables as well as Ijara. Having a

portfolio of assets comprising of different classes allows for a

greater mobilization of funds.

However, as Murabaha and Istisna'a contracts cannot be

traded on secondary markets as securitised instruments at

least 51 percent of the pool in a hybrid Sukukmust comprise

of Sukuk tradable in the market such as an Ijara Sukuk. Due

to the fact the Murabaha and Istisna'a receivables are part of

the pool, the return on these certificates can only be a pre-

determined fixed rate of return.

32

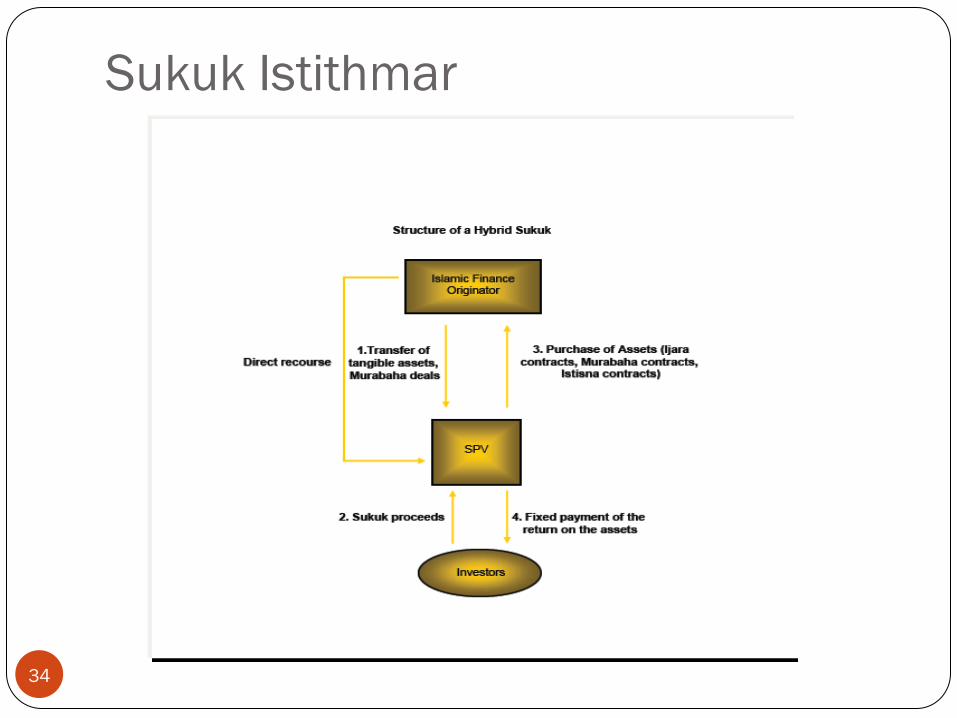

Sukuk Istithmar structure

1.Islamic finance originator transfers tangible assets as well as

Murabaha deals to the SPV.

2.SPV issues certificates of participation to the Sukuk holders

and receive funds. The funds are used by the Islamic finance

originator.

3.Islamic finance originator purchase these assets from the

SPV over an agreed period of time.

4.Investors receive fixed payment of return on the assets.

33

Sukuk Istithmar

34

35

Islamic Development Bank (IDB) Trust

Certificates – Sukuk Al Istithmar (2003)

US$400 million issued in 2003 with maturity in 2008

Securitization of Sukuk Ijara (65.8%), murabaha

receivables (30.73%) and Sukuk Istisna'a (3.4%)

contracts of IDB with a minimum of 51% of Ijara assets

The certificate holders will be entitled to receive

periodic profit distribution

Challenges

Fully subscribe, become “illiquid.”

Resemblances of conventional bonds in generating fixed income.

Non-completion risk and remedies

(a) Istisna'a’, (b) Musharakah (c) Mudarabah

Securitization of asset/project vis-à-vis securitization of receivables.

Force majure position and what constitutes force majure in commercial

perspective.

Collateral and securities

(a) Charge

(b) Assignment

(c) Put option

(d) Purchase undertaking

(e) Sale Undertaking 36

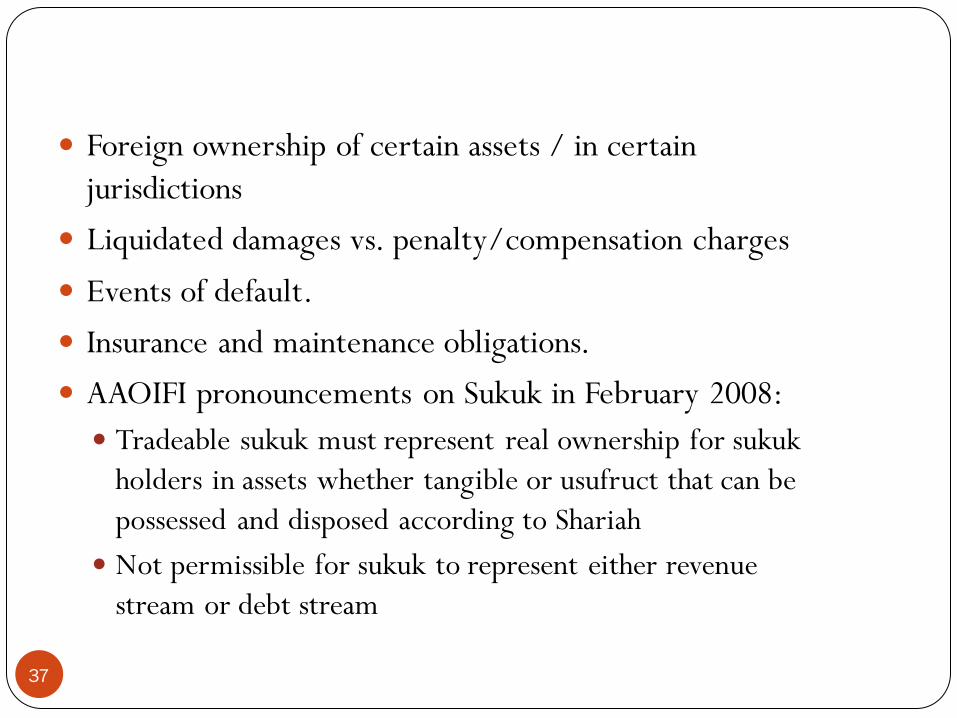

Foreign ownership of certain assets / in certain

jurisdictions

Liquidated damages vs. penalty/compensation charges

Events of default.

Insurance and maintenance obligations.

AAOIFI pronouncements on Sukuk in February 2008:

Tradeable sukuk must represent real ownership for sukuk

holders in assets whether tangible or usufruct that can be

possessed and disposed according to Shariah

Not permissible for sukuk to represent either revenue

stream or debt stream

37

Not permissible for manager of the Sukuk to offer loans to

sukuk holders when actual earnings fall short from expected

earnings

Not permissible for the issuer to promise to purchase assets

from the sukuk holders at a nominal value at the end of the

sukuk tenor

Permissible for the lessee in a Sukuk Ijarah to agree to purchase

the leased assets when the sukuk are extinguished for their

nominal value, as long as the lessee is also not an investment

partner, mudarib, or agent

38