Embed Size (px)

DESCRIPTION

VA Insurance Magazine

Citation preview

Certificates of Insurance –“The Ultimate Chess Match”

A Discussion of AgencyWebsite and Social Media

“Best Practices”

Social Media Time-Savers

When Good ThingsWhen Good ThingsHappen to Good Agents

BIG IOfficial Publication of the Independent Insurance Agents of Virginia

Virginia

The

Summer2011

ROLLINSRisk Placement Services, Inc.Serving The Transportation Industry Since 1946

Call 800.432.7715 or visit us at: www.RPSins.com/Rollins

RPS Rollins full page ad-910.indd 1 9/24/2010 4:34:13 PM

Summer 2011 • THE BIG “I” VIRGINIA 3

The Big I Virginia is a publication of the Independent Insurance Agents of Virginia

8600 Mayland Drive, Richmond, VA 23294Phone: 804.747.9300 / Toll-free: 800.288.IIAV (4428)

Fax: 804.747.6557 / E-mail: [email protected]: www.iiav.com

For information on advertising please contact: Jim Aitkins, Blue Water Publishers, LLC / 22727 161st Ave SE, Monroe, WA 98272phone: 360.805.6474 / fax: 360.805.6475 / [email protected]

The Big I Virginia is a publication of the Independent Insurance Agents of Virginia and is published quarterly by Blue Water Publishers, LLC. IIAV and Blue Water Publishers, LLC do not necessarily endorse any of the companies advertising in the publication or the views of its writers.

TM IIAV is an organization devoted to promoting,

enhancing, serving and assisting independent

insurance agents.

IIAV extends our appreciation to the following sponsors of this publication:

Insid

e t

his

issu

e6 Message from the Chairman of the Board - Robert A. Yergey

8 Message from the President and CEO - Bob Bradshaw

10 Message from the State National Director - James P. Bradner

12 Certificates of Insurance - “The Ultimate Chess Match”

18 Social Media Time-Savers

22 7 Tips for Selling More in a Tough Economy

26 When Good Things Happen To Good Agents

30 A Discussion of Agency Website and Social Media “Best Practices”

34 Avoid the Steamroller

38 2011 VAIA Pre-Licensing Schedule

46 IIAV Young Agents 2011 Event Schedule

Allied Insurance 45AmTrust NA 47Atlantic Specialty Lines 19Builders Mutual Insurance 35Delta Dental 11FCCI Insurance Group 37FastSnap 27GNY Insurance Cos. 17GUARD Insurance Group 33Hanover Excess & Surplus 48Harford Mutual 27JMWilson 37Jackson Sumner & Associates 41Johnson & Johnson 24, 25Keystone Insurers Group 29

Military Benefit Association 5Millers Mutual Group 2Penn National Insurance 7Preferred Property Program 23Prime Rate Premium Finance 20PROvision Underwriters 48RPS Rollins 3SIAA 17Southern Insurance Co. of Virginia 44TAPCO Underwriters 9The Iroquois Group 13U.S. Insurance Services 39Utica National Insurance Group 43WineryPak 21

SUMMER 2011

IIAV Staff

Carole Barton Accounting Assistant [email protected]

Robert N. Bradshaw, Jr., MAM President & [email protected] (804) 929-4134

Teresa Chester Executive Secretary/ [email protected]

Sherry Grubbs, AISM Chief Financial Officer [email protected]

Joe Hudgins, CPCU Vice President of Education & Technical Affairs [email protected] (804) 929-4138

Bonnie Joyce Insurance Administrative Assistant [email protected]

Melanie Kjar Communications/Website Director [email protected]

Linda Loving, CIC, AISM, AIAO IIAV Chief Operating Officer & VFSC Executive Vice President [email protected] (804) 929-4133

Danny Mitchell Membership/Marketing Director [email protected] (804) 929-4135

Susan E. C. Perkins Membership/Education Coordinator [email protected]

Kristina Preisner IIAV Education Marketing Coordinator & VAIA Executive Director [email protected]

Marie Toney Sales Associate [email protected] (804) 929-4136

4 THE BIG “I” VIRGINIA • Summer 2011

Summer 2011 • THE BIG “I” VIRGINIA 5

Protecting Those Who Protect UsMilitary Benefit Association has aproud 50-year history of promotingfinancial security to the military andfederal government communities.We sponsor a variety of group termlife insurance coverage for activeduty service members, militaryretirees, veterans, federal govern-ment employees and their families.

www.militarybenefit.orgor call our toll-free number

(800)-458-3087

Premium rates are competitive, and members can keep their coverage after they leave govern-ment employment. Additionally,MBA offers a selection of valuablebenefits that provide members with discounts for essential products and services. Contact us if you are interested in marketing MBA-sponsored life insurance.

Visit our website for more informa-tion:

Life Insurance underwritten by Government Personnel Mutual Life Insurance Company. Not available in all states. GP01 05-08

A ATT CMYK 03-08 4 10/31/09 1:32 AM Page 1

Hello again – for the last time! It is hard to believe that it’s been a full year since I became your Chairman! Time does fly when

you’re having fun…Well, this year has been full of new and

interesting issues that your association has tackled to the best of their abilities. The staff has done a great job attracting new members and working with our current members on all the services we have to offer. As you talk to members of the staff please thank them for all their hard work in making your association one of the best in this country.

The convention will be a very exciting experience this year and we hope that all have a great time. The coming year will bring new challenges to your association and we feel strongly that the incoming leadership will be able to tackle those well. John Watson and his incoming executive committee are ready and able to lead this association into the future!

I want to thank all of you that have wished me well in my term and for all the support from the staff and board this year. While we were not able to work on everything we had

hoped to cover, we did accomplish some great tasks that were facing us this year. The association has a new business plan in place as well as a plan for the upcoming years in order to keep us viable and to meet the needs and desires of the membership. We have put into place a strong plan to help members utilize Trusted Choice and other national and state programs that are available. Several committees that have not been active for some time have been re-established in order to more appropriately serve the mission of the association. All of these things have been accomplished by the hard work of the staff with the help and direction of the Board of Directors.

In addition, the Young Agents program continues to strive to produce new leaders for our organization. I hope that you continue to try to find ways to stay involved and participate in all of the wonderful events that the young agents group offers. Remember, once a young agent, always a young agent!

Thank you all again for your help and support – it has been a pleasure serving as Chairman and I look forward to continuing to assist in the future.

Chairman of the BoardRobert A. Yergey

6 THE BIG “I” VIRGINIA • Summer 2011

Summer 2011 • THE BIG “I” VIRGINIA 7

Business • Auto • Home • Surety

We don’t just create fast and simple automation solutions for our agents. We set out to delight them. From our award-winning, Real-Time commercial lines bridge for data transfer to our “wow” personal lines quoting system, we deliver seamless, simple online tools our agents want.

We’re looking for a few select agents. Find out for yourself why our agents choose Penn National Insurance as their go-to carrier. Watch a short video at www.PennNationalInsurance.com. Click on Becoming An Agent. Then give us a call.

800.877.7366 x4120

Simply delightful.Better, faster tools.

President and CEOBob Bradshaw

The economy these past couple of years has really had all of us focusing on the core functions of business and trying to keep all of the clients we can. When I speak

with members, much of the discussion is in terms of making sure that the agencies’ clients are renewed and taken care of. Renewal of current business and personal lines customers is essential.

As agencies are focused inward and making sure that they are running efficient operations, IIAV is working to take care of the external factors that serve to complicate our business, industry and profession. Clearly the legislature is our number one target. While the General Assembly meets for only a few short months at the beginning of the year, there are regular legislative meetings throughout the year where legislators can meet and discuss our industry. A couple of standing committees that meet throughout the year include the Joint Commission on Health Care, the Virginia Housing Commission and the Small Business Commission.

In addition to these legislative initiatives, IIAV regularly meets with and communicates with the Bureau of Insurance. For example, we have been having regular discussions with the Bureau on the problems you’re having with Certificates of Insurance. I hope that by the time you read this an IIAV initiated Administrative Letter on COI’s from the Bureau has been released. We have also been meeting with a number of policy holders on the COI issue – and as you may have heard, even convinced a major government agency to withdraw their policy coverage demand form and replace it with the new Acord form. Your IIAV technical committee and legislative committee will determine later in the year whether there’s a need for legislation on COI’s and we’ll

continue to meet with industry representatives.We’re also active on the health insurance

front. Virginia’s efforts to create a health insurance exchange are becoming critical as federal deadlines approach. We’re actively working with the Virginia Health Reform Initiative Advisory Council and the Secretary of Health and are seeking to actively represent our members. We may think it’s just common sense to see that what insurance agents do is essential to small businesses seeking protection for their employees, but some consumer groups just don’t agree with us. It makes you wonder whether or not some of these individuals have ever had to purchase health insurance for their employees and keep monitoring the coverage to insure that it stays comprehensive and affordable.

And of course we continue to represent your interests by making sure that we have the very best options for E&O coverage for your agency and employees. In today’s litigious market, policy coverage is critical for agency protection. You tell your customers to not purchase insurance based on price - we work with our national association to make sure that we have the most comprehensive coverage options available to you and your agency and that, plus all of the other work that we do on your behalf, provides added value to our programs..

The bottom line is….IIAV works for you. We are an extension of your agency. We’re only an 800 number away (1-800-288-4428). And since we represent the agency, ALL of your employees have access to us. If any of your employees run into a situation where they need help, they should remember to call the IIAV staff and seek assistance. Remember – we work for you.

While you’re managing your business – we’re watching out for you.

8 THE BIG “I” VIRGINIA • Summer 2011

800-552-6326www.gotapco.com

• “A”-rated non-admitted carrier

• Competitive pricing

• Fast policy turnaround

• In-house financing available in most states

• Quick claims handling

• $10 credit to your personalized TAPCO EZ Bucks Visa debit card with each policy

• Visa, MasterCard and ACH payments accepted

The TAPCO Service Pledge

1,000 Strong More than 1,000 classes of P&C businesswritten under binding authority.

Real Time Service with a Real Live Underwriter.

Call. Quote. Bind. Using TAPCO’s courteous and prompt call center, you’ll speak with a real underwriter who can compare, quote, bind, and deliver coverage to your e-mail inbox quickly and accurately during one,

simple five-minute phone call. Making TAPCO The Logical Choice for all your Real Time needs.

Do you remember when Real Time meant a relationship with a real underwriter? We do!

15371 Tapco Ad - Big I VA.pdf 4/6/10 12:30:51 PM

It’s always interesting visiting Washington, DC to interact with our Congress. IIAV sent a contingent of 10 to the National Legislative Conference on April 14. We visited our legislators (actually their legislative aides - you know how that works…) and lobbied for our big issues of this current Congress: MLR, NARAB

II, State jurisdiction of insurance, flood continuity and even crop-hail. We seem to be in good position on everything but MLR for health insurance. Although there’s a house bill on our position, the big fight will be in the Senate, where there is firm opposition to removing agents’ commission from MLR’s. But I was impressed with the “friends” that our national association has on the “Hill”. Both the Speaker of the House and the Majority Leader of the House appear very close to our leaders at IIABA.

At the national level the big issues are Trusted Choice and CAP. Trusted Choice is our new logo, and it is being embraced by over 60 of our insurance company partners. As you know by now, by being a member of IIABA we are Trusted Choice agents, and have the right to advertise as such. There are funds available from TC to offset the expense of changing our stationary, business cards, signs, etc. to add the logo. Soon there will be a Trusted Choice website with a link to the Consumer Agent Portal (CAP)….which, if it works as advertised, can be a “game changer” for us in our battle with the “lizard and “Flo” for personal lines business. If at all possible you need to come to this year’s convention at the Homestead (June 19-21) to hear IIABA’s Tom Minkler, the spearhead of CAP, explain how we can make CAP our game changer. Although there won’t be a lot of costs to utilize CAP, some training and web-site adjusting will be necessary to participate.

State National DirectorJames P. Bradner [email protected]

10 THE BIG “I” VIRGINIA • Summer 2011

DD_BigI_BrkrMeetsNeeds_8.625x11.125_4C.indd 1 4/5/11 3:53 PM

Summer 2011 • THE BIG “I” VIRGINIA 11

One of my job responsibilities at IIAV is to

help our members who have technical questions regarding insurance coverage and procedures, particularly insurance statutes

and regulations. For the past year and a half I have spent a multitude of hours helping members navigate through the maze that is “certificates of insurance”. Just as background, prior to coming to IIAV, I also spent many hours dealing with this issue as vice president of underwriting for a small, regional property and casualty insurance carrier. What I plan to do in this article is to lay out what I believe to be the genesis of the “certificates” problem, the realities or day to day effect on agents, and some possible solutions.

First the genesis of the modern day certificates of insurance problem as it relates to agents. Things seemed to be relatively calm and serene until about 5 years ago. Certificates were commonplace and everyone in the insurance community seemed content with the standard array of coverage provided by the commercial property, commercial liability, commercial auto and worker’s compensation policies. Then, as if someone flipped a switch, agents and companies began to get demands from certificate holders for new and exotic policy coverages such as waiver of subrogation, that the liability coverage must be primary and non contributory, there should be no exclusions applying to vacant property, certificate holders now needed to be on the policy as an additional insured (in some cases we have seen requests that they be added as a named insured) and that non pay cancellation notices must grant a 30 – 45 day notice in lieu of the traditional 10 – 15 days (no carrier does that). I have also seen a certificate holder specific certificate of insurance that requires the agent to list on the certificate

each exclusion in the CPP. I find it hard to believe that the risk manager who mandated that requirement actually had any concept of the makeup of the standard GL policy.

The “coup de grace” (although it was not merciful) came about approximately 2 years ago when ACORD made its now famous (infamous?) revision to their Forms 24 & 25. This simple but elegant change to the cancellation wording on these two certificates set off a reaction not unlike the reactions to the firing on Fort Sumter or the sinking of the Lusitania. To be sure, there was a problem with the “endeavor to” wording in the cancellation provision of the prior certificates. There was legitimate concern that there was a “promise” that no one, in particular the insurance companies, ever intended to keep. In addition, holding all of the different policies on the certificate accountable to the same number of days of cancellation notice was problematic. The solution, simply stated, said that the policy conditions for each policy would speak for themselves. When that change settled in, the certificates of insurance issue heated up another notch. It generated serious “push back” from certificate holders. Many demanded that the new wording be lined out and the old wording be inserted in its place. Agents in states where forms had to be filed and approved by the state insurance regulatory body were insulated from this as they could easily demonstrate the illegality of that request. Not so in Virginia. The other problem this presented agents in states where ACORD was not required to file forms was that to use the old form would be a violation of copyright laws as ACORD had withdrawn the forms.

So, where does all of this bring us in April of 2011? Insurance agents are having to make choices daily between misrepresenting policy coverages or conditions or causing their clients to lose a contract. Additionally, it is common practice by certificate holders to not pay for work already completed if the certificate of insurance does not reflect their exact requests. It would appear that certificate holders either just don’t care that they

By Joe Hudgins, CPCU Independent Insurance Agents of Virginia

THE ULTIMATE CHESS MATCH

Certificatesof Insurance

12 THE BIG “I” VIRGINIA • Summer 2011

Strong Agencies Made Stronger

For over thirty years Iroquois has helped make strong, independent agencies even stronger and more independent. And it shows.

Iroquois recognizes some of its members who have recently played key leadership positions within the industry:

Kenneth E. DavelerPast President, PIA of VA & DCAlliance Insurance Services, Inc.

Marilyn J. DonohoeACSR of the Year, IIAVMcLean Insurance Agency, Inc

Michael F. FunkhouserPast President, IIAVHaun Magruder Inc.

Tyler W. HancockPast Chairman, IIAVFord & Thomas Insurance Agency, Inc.

Crystal Miller-JohnsonPast Agent of the Year, IIAVAssociated Insurance Systems Services, Inc.

Alan K. PlaceOutstanding Agent & Past Pres., PIA -VA & DCCentral Virginia Insurance Agency

Cruger S. Ragland, Jr.Immediate Past Chairman, IIAVHubbard Insurance Agency, Inc.

Jodi Street Reynolds Outstanding Agent & Past Pres., PIA -VA & DCSWVA Professional Insurance Agency, Inc.

Robert T. ShortSecond Vice Chairman, IIAVShort Insurance Associates, Ltd

Thomas WelchPast President, IIAV & DCWelch, Graham & Ogden Insurance

Dennis C. Winfree Treasurer, IIAVHorizon Insurance Services

Robert A. YergeyChairman, IIAVYergey Insurance Agency, Inc.

2010 Best Practices Agencies

Short Insurance Associates, LtdCharlottesville, VA

Towne Insurance Agency, LLCChesapeake, VA

Welch, Graham & Ogden InsuranceManassas, VA

The Ware CompanyVirginia Beach, VA

LEADERSHIP

Independent agents with premium from $500,000 to $50 million join The Iroquois Group® for market optimization and strategies to increase their revenue, profits and agency value—without giving up their independence.

The IROQUOIS Group

®

To learn more about how Iroquois could further strengthen your agency, contact Matt Ward at 804-320-6984 or [email protected] and visit our website at www.iroquoismidatlantic.com

are, in essence, asking insurance agents to violate state insurance statutes or they are just ignorant of the insurance process. It is clear based on writings received from some certificate holders that some believe the insurance statutes just do not apply to them or the certificate process. They just want what they want. And, unfortunately, due to the current state of the economy, they have been getting what they have requested. It is almost as if the risk managers of the world huddled together in some clandestine location and decided to create an insurance coverage “wish list” and to use certificates of insurance as their method of making it happen.

As all of this began to unfold, we (the IIAV) became increasingly alarmed. It was evident from the phone calls and emails we were receiving that insurance agents in Virginia, as I said earlier, were being put at risk on a daily basis because of this change in the certificate of insurance process. Agents are at risk both financially and legally. First, agency employees are spending a great deal of time dealing with the problems posed by certificate demands. This computes to lost revenue and higher expenses as it diverts agency personnel away from productive activities that lead to growth and profitability. Second, it creates a dramatic increase in an agent’s exposure to an E&O claim. Third, it puts the agency in the position of legal consequences due to the violation of state insurance statutes.

So, what to do? We (the IIAV) began to engage the Virginia Bureau of Insurance in discussions about this serious problem. We then decided to convene a meeting of our technical committee to discuss the issue and compare notes. We set a date for the meeting and, in addition to the committee, invited the Virginia Bureau of Insurance. Their response was fantastic! They sent Mary Bannister, Deputy Commissioner Property & Casualty; Brian Gaudiose, Deputy Commissioner Agent Regulation & Administration; George Lyle, Principal Insurance Market Examiner; Mike Beavers, Principal Insurance Market Examiner and Joanne Scott, Principal Market Examiner to participate. We held the meeting at IIAV’s office the morning of March 9, 2011. The meeting consisted of a roundtable discussion where the agency members recounted their particular certificate of insurance “horror” stories. There was also general discussion about legalities and procedural issues. During the meeting the BOI staff listened, contributed and asked probing questions. After the “horror” stories, we discussed what could be done to bring some sanity (my word) back to the certificate of insurance process. The BOI staff stated that they felt an “advisory letter” discussing the proper and legal use of certificates of insurance was needed. True to their word, the letter was written and signed by Commissioner Cunningham. As I write this article on April 15, the advisory letter is to be sent to all licensed insurance

carriers in the state of Virginia the week of April 18; insurance carriers are then required to distribute it to all of their appointed agents. We have reprinted the Bureau’s advisory letter and put it at the end of this article.

What will be the next step? Our hope is that by the time you read this article the advisory letter will have had a positive effect and will have curtailed the certificate holder’s penchant for requesting insurance agents to certify both the illegal and outrageous. Currently 41 states (including Virginia) have taken steps directed at certificates of insurance; that number alone is a testament to the pervasiveness of the problem. The steps range from very specific, detailed legislation to regulations to advisory letters. The typical legislative solution includes four very basic elements. First, and probably most important, the statute states that the certificate of insurance confers no rights upon the certificate holder. Second, the certificate of insurance must be filed with the state insurance regulatory authority for approval. Third, a certificate holder cannot request that a certificate be changed from the filed version. Fourth, a certificate holder cannot request the issuance of a certificate that contains any false or misleading information concerning the policies being certified.

At this point (April 15) we are not actively advocating a legislative remedy in Virginia; we are willing to wait and see the results of the Bureau’s advisory letter. Our plan is to reconvene the technical committee and discuss how we can get a positive affect from it. We ask that you continue to make us aware of any situations where a certificate holder has demanded a certificate that misrepresents policy coverage or conditions. We also ask that you make us aware of situations where a certificate holder has refused to pay one of your clients for work already performed. We will reach out to certificate holders, in particular government entities, and try to educate them regarding the proper use of certificates of insurance. If all else fails, we will actively pursue a legislative remedy at the 2012 Virginia General Assembly.

In the meantime we urge you to educate your clients and your agency staff on the proper use and completion of certificates of insurance. It is important that agency staff communicate with one another, particularly at the agency’s regular staff meetings, if they are having a problem with a particular certificate holder or with certificates of insurance in general. It is equally important that your staff be consistent in how they process certificates. To help the education process, we have a new certificates of insurance course which is approved for 2 CE hours P&C credit. It is scheduled to be taught in our office in Richmond on July 21; please check our online education calendar for more details. We will add additional dates for this course in Richmond and in other cities.

Stay tuned. m

14 THE BIG “I” VIRGINIA • Summer 2011

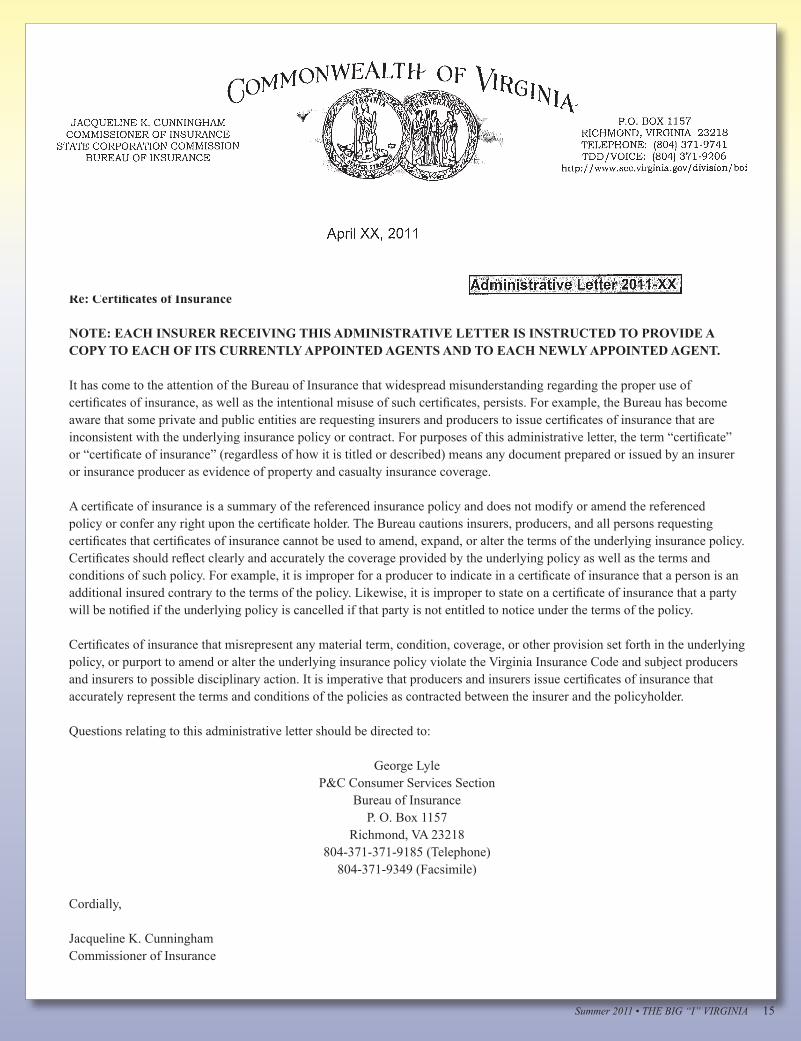

To: All Insurers Licensed to Write Property and Casualty Insurance in Virginia and All Interested Parties

Re: Certificates of Insurance

NOTE: EACH INSURER RECEIVING THIS ADMINISTRATIVE LETTER IS INSTRUCTED TO PROVIDE A COPY TO EACH OF ITS CURRENTLY APPOINTED AGENTS AND TO EACH NEWLY APPOINTED AGENT.

It has come to the attention of the Bureau of Insurance that widespread misunderstanding regarding the proper use of certificates of insurance, as well as the intentional misuse of such certificates, persists. For example, the Bureau has become aware that some private and public entities are requesting insurers and producers to issue certificates of insurance that are inconsistent with the underlying insurance policy or contract. For purposes of this administrative letter, the term “certificate” or “certificate of insurance” (regardless of how it is titled or described) means any document prepared or issued by an insurer or insurance producer as evidence of property and casualty insurance coverage.

A certificate of insurance is a summary of the referenced insurance policy and does not modify or amend the referenced policy or confer any right upon the certificate holder. The Bureau cautions insurers, producers, and all persons requesting certificates that certificates of insurance cannot be used to amend, expand, or alter the terms of the underlying insurance policy. Certificates should reflect clearly and accurately the coverage provided by the underlying policy as well as the terms and conditions of such policy. For example, it is improper for a producer to indicate in a certificate of insurance that a person is an additional insured contrary to the terms of the policy. Likewise, it is improper to state on a certificate of insurance that a party will be notified if the underlying policy is cancelled if that party is not entitled to notice under the terms of the policy.

Certificates of insurance that misrepresent any material term, condition, coverage, or other provision set forth in the underlying policy, or purport to amend or alter the underlying insurance policy violate the Virginia Insurance Code and subject producers and insurers to possible disciplinary action. It is imperative that producers and insurers issue certificates of insurance that accurately represent the terms and conditions of the policies as contracted between the insurer and the policyholder.

Questions relating to this administrative letter should be directed to:

George LyleP&C Consumer Services Section

Bureau of InsuranceP. O. Box 1157

Richmond, VA 23218804-371-371-9185 (Telephone)

804-371-9349 (Facsimile)

Cordially,

Jacqueline K. CunninghamCommissioner of Insurance

Summer 2011 • THE BIG “I” VIRGINIA 15

Summer 2011 • THE BIG “I” VIRGINIA 17

• CompleteIndependence• TopTierProfitSharing• StableMarkets

Call Dan Kernsin Western VA888-371-6879www.blueridgeagents.com

Call Lee Millsin Central & Southeast VA910-455-7576www.siaofnc.com

Call Jon Pappasin Northern VA / DC area443-692-4000www.pinsiaa.com

Call Beth Roein North Central VA423-612-0683www.meaa4u.com

PotomacInsurance Network

www.siaa4u.com

18 THE BIG “I” VIRGINIA • Summer 2011

As a Marketing Process Manager for Progressive, I speak with independent agents across the country about the importance of social media. For most, finding time in their

busy schedule is one of the biggest concerns.But you don’t have to dedicate hundreds of hours to see a return from social media. A well-defined strategy (and a few time-saving tools) can help you strike a balance between the time you invest and the value your investment adds.

When it comes to social media planning, there’s no right or wrong level of involvement. The most important factor is consistency. Start by setting goals for your agency’s participation. Whether it’s regular interaction with customers on Facebook, a tweet every few days, or a weekly blog post, you can strengthen your social media presence by having clear goals in sight.Here are three levels of social media involvement to consider based on the time you want to commit and the goals you set:

Listen (1-2 hours a week)This should be the first step of any social media

strategy. After you’ve set up your agency’s accounts on sites like Facebook, Twitter and LinkedIn, study what

people are saying on the platform. Check sites like Google Places or Yelp! for customer reviews of your agency. Friend your customers and follow their updates, track your competitors’ tweets, and watch how people respond. Note what’s working, record the questions and topics that dominate the conversation, and think through how you’d respond.

By first using social media as a listening tool, you’ll learn best practices for status updates, tweets and blog posts before creating your own. Plus, you can apply what you’re learning from online chatter to shape quoting and in-person conversations with your customers.

Time-savers• Clearly outline actions and responsibilities within

your agency to prevent redundancy, maintain focus and meet your social media goals. For example, you could assign a single person in your agency to review Facebook, Twitter and LinkedIn for one hour, twice a week.

• “Like” competitor Facebook pages from your personal profile to more easily follow their updates when you’re online.

• Search Twitter and third party directories like WeFollow and Twellow to identify popular profiles

This article outlines three levels of involvement for agencies with social media, depending upon the agency’s objectives and the amount of time it wants to dedicate. With each level of involvement, the author recommends specific time-savers that will help agency employees get the greatest impact from the time they spend working on the social web.

By Matt Marko

in the event of a natural disaster or emergency,

Hard to place risk?Simple Solution.

Call Toll Free 877-SMPL-R8Sor 877-767-5787.www.simple-rates.com

With just a few questions, we can provide you with an Instant Quote for:

Personal Lines■ Personal Umbrella■ Excess Personal Liability■ Excess Umbrella Liability■ Comprehensive Personal Liability■ Dwelling Package■ Home Based Business

Professional Lines■ Non Profit Directors & Officers Liability■ Employment Practices Liability

Specialty Products■ Special Events

(General Liability/Liquor Liability)

Commercial Lines■ Artisan Contractors – 60 classes

(including roofers & welders)■ 1-4 Family Dwelling■ Apartments■ Beauty/Nail Salon/Barber shop■ Convenience Stores/Deli’s■ Child Care (Commercial and Residental)■ Fitness Centers■ Janitoral Services■ Mobile Home Parks■ Restaurants■ Truckers■ Vacants

Ocean Marine■ Marine Artisan Contractors■ Boat Winterization

Independently Owned • Reliable & Experienced Underwriters • Local Virginia Company

the “A” way — Attitude, Assistance, Adaptability

Independently Owned | Reliable & Experienced Underwriters | Local Virginia Company

All of ASL’s servers are located off site in a bunker that has back up power and

diesel generators.

AtlAntic SpeciAlty lineS

don’t weAther the Storm ALone! look no further than your own backyard.

LindSey hArriSASL Claims CoordinatorO: 800.368.2095 x1701

Continue to support your local Virginia broker.

800.368.2095 | www.AtlanticSpecial.com

DAVE ADCOCkCommercial LinesO: 804.474.1571C: 804.398.0998

GREG PROVEnzOSenior Vice President

O: 804.474.1568 C: 804.338.2221

nick SmithPersonal Lines

O: 804.474.1570C: 804.310.4928

we have an offsite location in Richmond, VA with backup generator power, should our home office be inaccessible

two back up internet connections are available for

access to our servers from anywhere in the world.

All policies and file documents are imaged (paperless), thus we can immediately access all files for

you and your clients.

ASL_BigIVA_June2011_FullPg1Ad_FINAL.indd 1 4/13/11 9:37:24 PM

20 THE BIG “I” VIRGINIA • Summer 2011

associated with insurance. Create Twitter lists to organize the people you follow by category (customers, competitors, etc.), and use programs like Hootsuite or Tweetdeck to monitor your Twitter lists at a glance.

• Use a reputation management tool to monitor what people are saying about your agency. Consider using free services like SocialMention and Google Alerts, or more robust paid services like ChatMeter, LocationMonitor, or Trackur.

• Create a Google Reader account for one-stop monitoring of key insurance blogs and publications. Content hubs can save you hours a week by better organizing content for quick review.

Respond (2-5 hours a week)After taking some time to listen, join the conversation

by responding to questions, posts, and comments with a helpful link or thoughtful answer. Note that while answering questions or directing people to another online resource builds goodwill and trust, “hijacking” an online conversation to explicitly promote your agency can undermine your efforts.

Provide helpful advice over time and associate comments with your agency through hyperlinks or a

simple signature with contact information. Remember, showing your value doesn’t require you to give “pro bono” advice. Asking the right questions and outlining relevant points customers should consider can demonstrate the value of an independent agent, and lead to a follow-up phone call.

Time-savers• Focus on a few active online communities rather

than jumping around looking for every opportunity to respond. You’ll get to know the members better and your participation will build credibility that can lead to references across the social network.

• Develop a FAQ of common topics, your responses, and online resources you can share. Using these responses as a starting point can save time when responding to similar questions or comments.

Publish (5+ hours a week)The final level of social media engagement is

proactively communicating to your audience. Although most businesses prefer to jump right into engagement, by listening and responding first, you’ll be more comfortable with the medium and your audience. By starting slow,

Summer 2011 • THE BIG “I” VIRGINIA 21

you’ll also have a better understanding of the time you have for social media, and you’ll be more likely to provide the consistent presence necessary to build trust.

Time-savers• Put a process in place to keep your involvement

consistent and efficient. Assign a producer, CSR, or a marketing intern from a local college as your social media manager to ensure a single point of contact. Make sure they work alongside everyone in your agency to get questions answered and develop content without bottlenecks. Remember that effective social media engagement is timely and human. Delayed responses and overly-corporate language limit your effectiveness online.

• Share any quality information you think followers may be interested in—it doesn’t always need to be about insurance. Not only can this save you time developing your own content, it provides value to fans, followers and readers and increases the chance that others will share your content with their communities.

• Distribute the work among a few employees to keep it manageable. This adds variety to your

posts, and prevents disruption due to vacation, job changes, or illness.

• Mix up your content. A thought-provoking question can be as effective as a blog post, and takes a fraction of the time to compose. Discussing community events or commenting on your favorite sports team can also engage your audience without the research and writing time longer posts may require. Plus, consumers will appreciate seeing the personality of your agency and its employees.

Please visit the “Websites & Social Media” quick link at www.iiaba.net/act for more articles and recorded webinars on social media issues.

Matthew Marko is a Marketing Process Manager for Progressive Insurance. He works to provide local marketing strategies, tools and co-branded collateral to help independent agencies grow their businesses. E-mail him at [email protected]. Matt prepared this article for ACT. For more information about ACT, contact Jeff Yates, ACT Executive Director at [email protected]. This article reflects the views of the author and should not be construed as an official statement by ACT. m

INSURANCE PROGRAMS.®

WINERYPAK

YOUR TOTAL WINERY INSURANCE SOLUTION.

Your business. Our specialty.

888-386-5701 • www.WineryPak.com© 2010 WineryPak, LLC. All rights reserved.UNDERWRITTEN BY MEMBER COMPANIES OF GREAT AMERICAN INSURANCE GROUP.

If you’re an insurance professional targeting the winemaking or distilled spirits in-dustries, now you can provide more of the coverages your clients and prospectsneed, in one inclusive program.

WineryPak® offers coverage for:• WINERY AND VINEYARD OPERATIONS • SPECIAL EVENTS & HOSPITALITY• FARM & RANCH COVERAGES • BONDS • CROP INSURANCE • CYBER RISK

22 THE BIG “I” VIRGINIA • Summer 2011

You hear it everywhere you go: “Sales are down because of

the economy. My customers simply aren’t buying as much.” There are some people out there saying the economy doesn’t matter, it’s what’s going on in your own head that matters. While it’s true that what goes on in your brain is always more important than outside circumstances, the economy is still what’s affecting many businesses. If yours is one of them, put the following seven ideas into practice and you’ll find that the effect on you will be minimal, and in fact, you may notice no change or even a positive one.

1) Don’t let the economy be your excuse.After a tough day or some difficult sales calls, it’s

easy to use the economy as an excuse. If you do, people will hear it in your voice and you’ll sell less. This attitude also leads to working less. In a down economy, when salespeople should be increasing their calls and activity level, the average salesperson cuts calls by 37%. The answer? Use the down economy as a warning and motivation to work harder and smarter, not as an excuse to back off. If you back off, business will go down; if you work harder and smarter, business will improve. As the saying goes “When the going gets tough, the tough get going.”

2) Get better at selling.When there are fewer sales opportunities and

prospects, you must do better with the ones you have. The way to do this is to get better at selling. Read books, listen to tapes and CDs, watch DVDs, become a sponge and absorb everything you can get your hands on. Using this strategy has helped many salespeople improve to the point where they actually sold more in a so-called down economy than they sold when times were good. Now is the

time to improve your skills; constant and

consistent learning is the best way to grow your

sales.

3) Keep a good attitude.Your attitude is the most important

sales tool in your arsenal; you have to keep it sharp. Now is not time to read the front page of every newspaper and watch every newscast. Our brains are like computers “Garbage in, garbage out.” What you should be doing is putting as many good ideas as possible into your brain. Pick up anything that is inspirational, motivational, positive, and upbeat and use it to keep a good attitude and stay focused. Be positive and persistent. In addition to putting good ideas into your brain, surround yourself with positive people and stay away from negative people.

4) Prepare for the price objection and build value.People are focused on price more than ever these

days. Prospects and customers will do everything they can to commoditize vendors and simply go with the lowest price. Thus it is very important that you build value. What are your primary benefits? How are you, your company, and your product better than the competition? Are you local? Is your long-term cost less? Can you respond to service calls faster? You need to accentuate your primary benefits, make them as powerful as possible, and provide proof in ROI Models, testimonials, and the like. Finally, come up with some solid responses to the price objection.

5) Build relationships.The relationship with the salesperson is the number

one reason people give for doing business with a particular company. We’ve all seen it happen, you make an overwhelming case for your product versus the competition and yet, the prospect still buys from your competitor

By John Chapin

7Tips for Selling More in a Tough Economy

Summer 2011 • THE BIG “I” VIRGINIA 23

because they’re golf buddies. Relationships are extremely important, in most cases more than anything else, so you need to focus on not only staying in touch with and keeping your name in front of customers and prospects, but also on taking that next step and building solid relationships.

6) Go back to the basics.Now is the time to increase the personal touch. Make

more face-to-face visits to customers, send handwritten notes, stop by occasionally simply to say “hello”, and drop off the proposal in person instead of mailing or e-mailing it. Your objective is to touch the customer more often on a more personal level at a time when your competitors are calling less and being less personal.

7) You are completely responsible for your success.Five years from now you and your career will arrive

somewhere; the question is: Where? If you decide that something outside of you, such as the economy, is responsible for your success or failure, you give away control of your destiny and your ultimate success. The way to change that is to remember that your success is up to you, you own it, and you control it. Provided you have solid goals and strong enough reasons why you need to get there, you will arrive where you decide to

arrive, regardless of the economy, or anything else for that matter. Reminding yourself that you are 100% responsible for your success keeps your success under your control and within reach.

If you put the above tips to work, you will see an improvement in business, perhaps a significant one. Many people have found that as a result of the above tips they are doing more business now than they were when the economy was good. What are you capable of if you really set your mind to it and get to work? The sky is the limit, so stay positive, work hard, work smart, and dream big.

John Chapin is an award winning speaker, sales trainer, coach, and co-author of the gold-medal winning “Sales Encyclopedia”, a comprehensive how-to guide on selling. “Sales Encyclopedia” is written for sales professionals in all industries at any level of experience. Utilizing more than 21 years of sales experience and as a number one salesperson in three industries, John co-founded Complete Selling Incorporated, a company helping salespeople significantly increase their sales results.

If you would like access to John’s free white paper on what it takes to be successful in sales along with a monthly newsletter, you can visit John’s website at http://www.completeselling.com For permission to reprint, or to reach John, email him at [email protected]. m

Summer 2011 • THE BIG “I” VIRGINIA 25

It’s Monday, December 21, and an agency owner (let’s call him Bob) is trying to get things wrapped up before the holidays so he can

be ready for a nice vacation. He’ll be back after the first of the year. At about 3:00 pm his assistant tells him he has a call from someone named Frank. He asks who Frank is and she says she doesn’t know. Think-ing it might be one of his old college buddies, he takes the call. Frank says he’s an attorney and he wants to talk to Bob about Kenny, a former insur-ance customer of Bob’s. Frank then tells him that they have a trial start-ing on December 28 and he wants to discuss Kenny with him.

Immediately, Bob’ heart sinks and things start to race through his mind: Will his vacation be ruined? But one thing pops into his mind that he remembers from a Swiss Re loss control seminar he went to a few months earlier. The instructor there said: “If an attorney calls you and wants to talk, remember, unless he’s your attorney he’s not your friend. And you don’t have to talk to him. Instead, ask what he wants to talk

about and don’t volunteer any infor-mation. Instead, politely tell him you can’t talk to him and immediately call the claims department at Swiss Re or your E&O carrier.”

Bob knows that Kenny has always been a challenging customer (late premium payments, unreason-able requests, failing to report chang-es, etc). What does this lawyer want? Why is he calling Bob?

So Bob tells Frank the lawyer:”I’m sorry, but I can’t talk to you about Kenny,” and hangs up. He immedi-ately calls his state E&O administra-tor who gives him the number for the Swiss Re claims department. Bob calls and speaks with one of Swiss Re’s professional claims staff, Sarah, who goes over everything with Bob, and she tells him that if anyone calls him or if he receives any letters or documents - including a subpoena - to immediately call her. Sure enough, the next morning the attorney delivers a subpoena for him to testify at his deposition on Thursday, December 24. Merry Christmas!

Bob immediately calls Sarah the claims handler who tells him to fax

the subpoena to her right then, which Bob does. In the next two days, an at-torney has been retained to represent Bob and the attorney contacts the attorney who issued the subpoena. They talk and the subpoena is with-drawn.

The key to this is not that Bob’s vacation was saved, (although that’s nice too) but more importantly he remembered what he’d learned at a Swiss Re/IIABA endorsed loss control seminar: that any time he is con-tacted by anyone who wants to talk to him about one of his customers, he should assume that they are not wanting to help him and he should contact his E&O claims department. But be careful, if there has been a problem with your customer’s policy or a claim and you receive a call from your customer, a representative from the insurance company or even someone from your state department of insurance, then you may want to call your E&O carrier’s claims staff to get some advice as well.

Here are a few other examples of what happens when agents do the right thing:

happen to good agents

By Richard F. Lund, J.D., Vice President, Senior Underwriter, Swiss Re*

When

THINGS

26 THE BIG “I” VIRGINIA • Summer 2011

An agent receives a subpoena for his customer’s records. He con-tacts his E&O claims department who contact the attorney who issued the subpoena and ask what they want. It’s determined they only want a copy of the customer’s policy. The claims handler obtains that from the agent and forwards it to the attorney.

An agent receives a call from the carrier of a policy of a former customer of the agent and they want to see his file. The agent asks why and they tell him there is a ques-tion about the information that was contained in the application. They tell the agent they just want to help him. The agent hangs up and im-mediately contacts his E&O claims department and the claims handler calls the carrier and asks specifically what information they want. They say they don’t know of anything in particular, they just want to see the agent’s file to see if they find any-thing in his notes. The claims handler tells them that if they can tell her anything specific, they’ll see what they can locate, but unless they have a specific request, they can’t provide anything. They never hear back from the carrier.

An agent receives a call from an upset former customer who has a claim that was denied by the carrier because the policy expired due to non-payment of the premium. The customer tells the agent they’re go-ing to sue them and hangs up. The agent immediately contacts his E&O claims department. They discuss what happened and the claims han-dler asks if the agent has any docu-mentation about the cancellation. The agent says yes, he has a copy of the letter from the carrier notifying the customer of the cancellation. The claims handler helps the agent draft a letter to the customer and provides a copy of the cancellation notice. The agent sends the letter and the notice

Summer 2011 • THE BIG “I” VIRGINIA 27

28 THE BIG “I” VIRGINIA • Summer 2011

to the customer and the agent never hears from the cus-tomer again.

An agent receives a notice of complaint from the state department of insurance and contacts the Swiss Re claims department. The claims handler reviews the complaint, discusses it with the agent, contacts the DOI investigator and helps the agent prepare a formal re-sponse refuting the allegations in the complaint. In some limited instances, an attorney is retained to help the agent respond to the complaint. In most cases, the complaints are resolved in the agent’s favor without further action. But if the complainant pursues it further including filing a lawsuit, the groundwork to defend the agent has already been laid. In each one of these cases, as soon as the agent was aware that there might be a problem that could lead to a claim the agent immediately contacted their E&O claims department. The claims department then gathered information from the agent and took steps to avert a claim. In many instances, by taking immediate action with the claims department before an actual lawsuit arises, the claim can be averted.

So you see, not all E&O claim situations have a bad outcome. Many times, good things happen to good agents.

This article is intended to be used for general infor-mational purposes only and is not to be relied upon or used for any par-ticular purpose. Swiss Re shall not be held respon-sible in any way for, and specifically disclaims any liability arising out of or in any way connected to, reliance on or use of any of the information con-tained or referenced in this article. The informa-tion contained or refer-enced in this article is not intended to constitute and should not be considered legal, accounting or pro-fessional advice, nor shall it serve as a substitute for the recipient obtaining such advice. The views

expressed in this article do not necessarily represent the views of the Swiss Re Group (“Swiss Re”) and/or its sub-sidiaries and/or management and/or shareholders.

Insurance products underwritten by Westport Insurance Corporation, Overland Park, Kansas, a member of the Swiss Re group.

Copyright 2010 Swiss Re America Holding Corporation

*Richard F. Lund, JD, is a Vice President and Senior Underwriter of Swiss Re/Westport, underwriting insurance agents errors and omissions coverage. He has also been an insurance agents E&O claims counsel and has written and presented numerous E&O risk management/ loss control seminars, mock trials and articles nationwide since 1992. m

Contact IIAV Today to Register! Independent Insurance Agents of Virginia-8600 Mayland Dr. Richmond, VA 23294

800-288-4428-www.iiav.com

What You Will Learn:

Effective Communication Skills Best Practices in Customer Service Time Management Business Writing Skills E&O reduction techniques Maximizing company relationships Why politics matter Building partnerships through sales Negotiation tactics Etiquette and the Spoken Word Ethics Leadership skills Stress Management

Professional Skills That Will Last A Lifetime

Associate in Insurance Account Management (AIAM)

Overview:

Six Days of Class over 3 months National Designation Interactive class and learning model

©2011 Keystone Insurers Group®. All Rights Reserved. This does not constitute an offer to sell a franchise in any state in which the Keystone Insurers Group franchise is not registered.

• Increasing Agency Value for Over 200 Partners in Seven States

• Perpetuating & Strengthening the Independent Agency System

• Individually Owned & Operated

Partner with the best and distance yourself from the competition.

Bringing the Best Together

Partners in Pennsylvania, North Carolina, Virginia, Indiana, Ohio, Kentucky & Tennessee

Ben, Brett, Kenan & Bud Schultheis, Evansville, IN

John Frankenfield, Telford, PA

Mark Bates, Crown Point, IN

Rick Spreng, Ashland, OH

Neil Annas, Granite Falls, NC

Craig Katzman & David Swimmer, Charlotte, NC Bill Talley, III V & IV, Petersburg, VA

David Priest, Richmond, VA

David & Bob Fenner, Columbus, OH

Bob Seltzer, Orwigsburg, PA

Ronnie Bagwell, Raleigh, NC

Cloyce Anders, Raleigh, NC

Todd Roadman, Bedford, PA

IN VIRGINIA

Call Cheryl Brooks [email protected]

804.201.1395 Or visit www.keystoneinsgrp.com

Social Media“Best Practices”

A Dicussion ofAgency Website

and

30 THE BIG “I” VIRGINIA • Summer 2011

At the Fall ACT meeting, there was a lively “break out” that focused on the latest thinking on websites and social media in the insurance industry and what value agents and carriers

were finding through their “digital” presence. The conversation uncovered behavior and tactics that the group felt were “best practices” and helpful in achieving a successful “social” implementation.

I served as moderator of the breakout session, which had 18-20 participants. The following is a brief overview of the discussion.

Websites and BloggingConsidering the increased functionality of Facebook

Pages, which Facebook previously called Fan Pages, some actually questioned the need for a website. Most agreed, however, that a website is still a very important component in a “social” strategy. Yet, it’s important to note that the website talked about is not the static brochure-ware of a 1990s website. Rather, it is a 2010 blog or website built on a blog platform – for example, a website created using a product like WordPress or TypePad.

New tools make it easy to keep content fresh and relevant. A website is a company’s “home” – it is where they humanize their brand and it is the core of their digital existence. It was suggested that a successful strategy is to become a curator of information on a specific subject – that is, become the resource customers and prospects go to for subject matter expertise.

At our session, discussion took place concerning the quality of blog content, as well as the time needed to keep a blog updated and fresh. One agent participant offered this: “I was ready to hire someone to do our blog, but one of our employees said she could do it, so I decided to

let her try. It helped me realize that a good blog doesn’t require a professional writer. Writing in the first person is okay. In fact, this seems to be the best practice. I did review the posts at first, but now I have full confidence and trust in her and no longer review them.”

Another agent mentioned that he typically uses his blog to write testimonials about his clients.

Best Practice Tips: ● Keep blogs short – Two paragraphs or about 300

words. What drives more interest is good concise information.

● Build an “editorial calendar” for your blog posts and share the responsibility for writing them with your colleagues.

● Consistency is more important than frequency.● Blogging is very good for search engine

optimization (getting found through search engines such as Google.com). One said, “Every time we blog, page views go up.”

● Use Google Analytics to monitor your site. It is a free, easy way to track hits to your web page.

● Consider adding a disclaimer.

Facebook “Fan” PageThe discussion started with the assumption that

every agent and broker should have such a page. All participants agreed that, “you want (need) to be where your prospects and customers are.” The “inbound” and permission-based marketing model of today will work only if you can be found. With more than 500,000,000 users, Facebook is a place where you must have a presence. It was felt that having a Facebook Fan page is an important component of a firm’s overall “social” strategy.

A group of 18-20 Internet savvy agent, carrier and vendor executives gathered at the latest ACT meeting to discuss their experiences and lessons with their websites and uses of social media. What emerged was a consensus on several “best practice” tips for using these online tools, which will be helpful to additional agencies as they seek to build their online presence and brand.

By Rick Morgan

Summer 2011 • THE BIG “I” VIRGINIA 31

32 THE BIG “I” VIRGINIA • Summer 2011

Best Practice Tips:

● Think of Facebook as a way to keep your “fans” updated on agency activity and/or events. For example, a sports team you sponsor or participation in a cancer walk is news you can share with your community.

● Think of your page as an online civic club meeting or cocktail party – a place to introduce yourself and build your online persona.

● Use customized tabs to create a “Welcome” landing page.

● Consider using Facebook Ads to promote your blog and grow your fan base. These ads are very cost effective and can be “laser” focused. Facebook provides good metrics and the ads are easy to create and revise as needed. Some of the comments: “If nothing is working, change it.” “You are not selling a product with a Facebook ad.” “It’s cheap and easy. Play with it.”

● Some carriers are using co-op advertising dollars to help agents with Facebook Ads.

LinkedInFor many in the breakout session, use of LinkedIn

“felt” less threatening and more “comfortable” than many of the other social media applications. We agreed that LinkedIn has become more than a place to post an online resume. For example, it can be used to do research on potential prospects. Also, engaging in conversation on Linkedin groups can be an effective way to demonstrate subject matter expertise.

Best Practice Tips:● Be sure you have a good and complete profile.● Take advantage of its strong search capability

when looking for prospects or researching existing customers.

● Join groups focused on your firm’s sweet spot. For example, if you write restaurants or contractors, be sure to join corresponding groups.

TwitterThe value and business use of Twitter continues

to be elusive for many insurance agents. For others, it has become one of their most effective research and communication tools. For some agents, Twitter, like Facebook, is used to “humanize” and personalize their corporate brand. They use Twitter to broadcast news and events in “real time.” For example, one agent uses Twitter

to track local weather and report on tornado sightings and provide location updates.

Best Practice Tips:● Use Twitter search.● Use Twitter to monitor local news events.● Use Twitter to follow areas of interest – For

example, #insurance.

Social Networking – Getting StartedWhen asked what steps should be taken by someone

just getting started with social networking, the group offered this advice:

● Create a “connected” digital presence by using tools such as Hootsuite, TweetDeck and/or FriendFeed to link and manage all of your social activity. While these tools allow you to replicate posts across all of your social sites, you need to consider whether you should actually do this. It is important to consider the different audiences and deliver relevant messaging on your various social sites to each.

● Make sure you have a good policy or social web guide in place that outlines and defines appropriate behavior for your company and employees when using the social web.

● Have a good, comprehensive strategy in place that is part of the firm’s business plan. Be sure to communicate that plan with all employees.

● Decide what you want to measure and how to measure it. You will want to know what success looks like.

● Don’t delay. This is not a fad or an experiment. Pick one thing and do it now.

● Let tools like GetListed.org help you with Local Search.

● Consider using video and YouTube. Using a Flip video camera is a very easy and effective way to create your own video.

● Use Google Alerts to track “mentions” of not only your firm but also to track your key customers and even your competition.

● Blog, blog and blog some more.● Pay attention to the details. Make sure your brand

image is consistent across all of your online touch points.

Biggest MistakeWhen asked what mistakes they made, the group

responded with:

Summer 2011 • THE BIG “I” VIRGINIA 33

● Sitting on the sideline waiting for it to mature.● Don’t use these tools as a sales or self-promotion

megaphone. ● Thinking that if you build it they will come and

your bottom line will magically grow. It takes work to build relationships and gain trust – online and off. Be patient and sales will come.

Other Comments● One agent is discontinuing chat. He felt that most

were useless chats.● Some agents have abandoned the Yellow Pages.

Instead, they spend the money on improving their website and developing their social sites. One agent also commented that the type of inquiries that came from their social sites were more solid and qualified than the calls they previously had received from the Yellow Pages.

● It is important to be in all of these “social” places, because prospective customers are searching for you there.

Under the heading of “What’s Next,” the group universally expected to make more effective use of video.

Many were also interested in creating iPhone apps for their agency and saw “mobile’ and location-based applications as emerging trends for 2011.

Editor’s Note: The ACT website contains a wealth of additional information related to effective use of agency websites and social media. For example, you will find prototype website disclaimers in the article “Don’t Get Caught in the Web,” examples of agency social media policies, ACT’s “Creating a Social Web Policy for Your Independent Agency,” and several other informative articles and recorded webinars. Go to www.iiaba.net/act and click on “Websites & Social Media” in the gray shaded area on the left.

Rick Morgan is a consultant with four decades of experience in innovative technology, marketing, and publishing in the independent agency system. He chairs ACT’s Social Web Work Group. ([email protected]; http://www.rickmorganconsulting.com/blog) Rick produced this article for ACT (www.iiaba.net/act ). It reflects his views and should not be construed as an official statement by ACT. m

becauseWe want your business.

We’ll work hard to get your business.

We’ll work even harder to keep your business!

Rated A- (”Excellent”) by A.M. Best

Let us convince you. Visit www.guard.com or call 800-673-2465, ext. 4567!

Property and casualty insurance for small- to mid-sized employers – workers’ compensation coverage is our traditional specialty.

34 THE BIG “I” VIRGINIA • Summer 2011

STEAMROLLERAvoid the

By now, it’s no surprise to anyone that we’re in dire need of new blood in the insurance industry. Although we continuously cite the average age

of an agency principal as 55, those birthdays keep coming, and that average age creeps up every year. According to a recent study of more than 3,000 insurance and risk management professionals by the National Alliance Research Academy, the average age of a non-retired industry professional is 56. And although 59 percent said they plan to continue working part-time after retiring, 41 percent claim they will retire from all forms of employment by age 66. This gives the industry 14 years to prepare for the departure of an entire generation of seasoned insurance professionals. The Alliance survey reports that 87 percent of respondents have more than 20 years of industry

experience—a resource that will be gone in a little over a decade.

Luckily, that resource is renewable—if we do some smart planning right now. Until recently, the industry’s reaction to this oncoming juggernaut has been to pretty much keep doing things the way it always has. Although most producer trade associations have long-standing programs targeting younger agents, the term “young” was often pretty relative.

But as Gen Y grows into an increasing presence in the workforce, the old rules—look for an older mentor, expect to put in years before you see a payoff, dress for success, follow the rules and keep your mouth shut—are suddenly irrelevant. The new generation, weaned on the Internet, social networking and instant information access, doesn’t have time to do things the traditional way.

Dealing with the oncoming wave of agency retirements is like getting run over by a steamroller: You know it will happen if you don’t move, but its occurring so slowly you think there is time to escape.

By Laura Mazzuca ToopsPropertyCasualty360.com

working with builders mutual is just that easy.We’re always looking for ways to help our agents offer better

service and coverage to their customers. By attending our

exclusive training, using our online resources and exploring our

increased appetite, you’ll become—and stay—the “go to” agent

for residential, commercial and trade contractors

If you’re in construction, the insurance choice is simple.

(800) 809.4859 buildersmutual.com

Typical agenT workday

1 2LogIn to bob 2.0 quote and wrIte poLIcy

Summer 2011 • THE BIG “I” VIRGINIA 35

36 THE BIG “I” VIRGINIA • Summer 2011

“We as agencies can’t continue to do business or expect young people to do business like we did in the past,” said Joey O’Conner, sales vice president for Insurance Underwriters Ltd. in Metairie, La., and past national chair of the IIABA Young Agents Council (YAC). “Young people have access to tools that help them do their job much faster than veteran agents. If you’re not aware of what their hot buttons are and how they work collectively, it can be frustrating for both the agency and the young people coming in.”

Case in point: the way young producers at his own agency approach sales. Of the agency’s 11 young agents, 5 of them Millennials, it’s evident that one of their generational traits is a preference for working in groups, O’Conner said. “When they go on sales calls, they tackle it as a team. If an agency wasn’t flexible, that approach and their enthusiasm could be disrupted. If you tell them to go out by themselves, and don’t adapt, you could be frustrating them and losing out on great talent.”

His agency has adapted to this new approach and established an internal structure on how to divide or share revenue with two producers who go on account calls together, something typically rare for veteran agents, O’Conner said.

“We also don’t interfere with how they should service the account; they work it out as a team,” he said. “It would be foolish of us to divide it up or try to micromanage that job description. We’ve had great success encouraging them to work in teams.”

The industry reactsThe industry’s young agent programs are sitting up

and taking notice, with most pushing aggressive new initiatives to boost membership, increase outreach to high schools and colleges, and otherwise ramp up their efforts to make insurance a relevant career choice for a new generation of employees. We spoke with the leaders of five producer trade association young agent groups on how they were tackling the generational transition challenge. Here are their responses:

Joey O’Connor, sales vice president, Insurance Underwriters Limited, Metairie, La. past national chair, IIABA Young Agents Council (YAC)

As part of the organization that sponsors Project InVEST, Big I’s 40-year-old initiative to educate high school and college-aged students on the viability of a career in insurance, YAC made history last year by joining

Give the Gift of Knowledge to Future GenerationsGive the Gift of Knowledge to Future Generations

Help Virginia Association of Insurance Agents educate future generations on: How to be insurance

literate consumers The career possibilities in

the insurance industry Training programs available

to start a career in insurance

Get Involved By: Volunteering Donating to VAIA Programs Attending VAIA Events

Virginia Association of Insurance Agents 8600 Mayland Dr. Richmond, VA 23294 800-288-4428—www.vaia.info

Summer 2011 • THE BIG “I” VIRGINIA 37

“Volunteerism is a rewarding commitment. This same feeling of gratifi cation comes from my 16-year career in the insurance industry, working with experienced managers and underwriters and assisting our agents in being successful.”

Chuck CraycraftBranch Manager in Westerville, Ohio —and Habitat for Humanity volunteer

Connect with Chuck on LinkedIn!

800.388.8178 jmwilson.com

Managing General Agency Since 1920

Property/Casualty • Professional Liability • Surety Commercial Transportation • Personal Lines • Premium Finance

COMMITMENTA PROMISE WE DON’T TAKE LIGHTLY

38 THE BIG “I” VIRGINIA • Summer 2011

2011 VAIA Pre-Licensing Schedule

Richmond

8600 Mayland Dr. 23294

July 11-15: Life & Health July 18-22: Property & Casualty

Aug. 8-12: Life & Health Aug. 15-19: Property & Casualty

Sept.12-16: Life & Health Sept.19-23: Property & Casualty

Oct. 3-7: Property & Casualty Oct. 11-14: Life & Health

Oct.31-Nov. 4: Property & Casualty Nov. 14-18: Life & Health

Dec. 5-9: Property & Casualty Dec. 12-16: Life & Health

Chesapeake

911 Live Oak Dr. 23320

Aug. 22-26: Property & Casualty Oct. 31-Nov. 4: Property & Casualty

Newport News

12363 Hornsby Ln. 23602

June 20-24: Property & Casualty Sept. 26-30: Property & Casualty

8600 Mayland Dr. Richmond, VA 23294

1-800-288-4428

www.vaia.info

Self-Study Options &

In-House Classes are available .

forces with InVEST to help foster the national growth of the program through promotion, fundraising and taking the industry’s message and the InVEST program to members’ home communities, O’Connor said. They’re working at the high school and community college level to reach students for recruiting future employees.

If the industry had a problem in the past with recruitment, it was probably simply complacency and failing to toot its own horn about how great an insurance career can be, O’Connor said. “I always tell independent agents of all ages that we do a great job when we’re all together at a function talking about the industry and how we do so much good for the public; what we don’t do well is talking to young people coming out of high school and college about what a great career it can be. We must promote what we’re proud of.”

That’s why the YAC and InVEST alignment is important—”to bring forces together and speak with one voice about how great the industry is.”

The first step is for individuals to identify if InVEST already has a presence in their area, because they can provide a list of names of young people taking uniquely developed program for young people. “By the time they’re finished, they can do an internship at an agency, get to know them, and they may be a fit,” he said. “Part of the strategy of YAC and InVEST joining forces is to cover all the bases of what we should be doing as agencies and companies to attract new employees.”

YAC membership runs “a few hundred,” with an age range of 22 to around 45. As with most of the association groups, YAC’s major benefit is to provide networking opportunities for young agents across the country and the opportunity to develop relationships with insurance company personnel. “We have done everything from motivational seminars to professional development sessions

aimed at making them better agents to sales classes, or even had company partners come and talk about a specific product,” he said.

The biggest business challenge by far for young agents is a lack of experience: “When you’re a new young agent, you must remain patient and be willing to give yourself time to grow professionally in the industry,” O’Connor said. “This is a challenge for any young person who comes in eager and motivated, no matter what career you’re pursuing. There’s a learning curve you must be willing to go through.”

However, this doesn’t mean that young people must follow the same slow career path that older generations

Summer 2011 • THE BIG “I” VIRGINIA 39

did. “When I graduated from college years ago, the advice I got from counselors and other adults was to seek out the most successful person in your field, usually someone in excess of a 25-year career, ask them how they got there and imitate what they did,” O’Connor said. “Today, a lot of 25-year-olds can’t see themselves working that long to get to that level. It’s important for us to start identifying highly successful 28-to-32-year-olds in our industry, including those on the company side. This closes the age gap and shows that it doesn’t have to take 35 years for them to succeed with the proper work ethic.”

David “Moose” Bulloch, Speed-Stiel Insurance Services, Hammond, La., national chairman, PIA Young Insurance Professionals (YIP)

As the leader of a relatively new national group of young agents, David Bulloch is keen to recreate the success of the Louisiana chapter of the Young Insurance Professionals (YIP) on a nationwide basis. Although YIP has been around, starting in New York and New Jersey, for more than 20 years, and the Louisiana chapter is 12 years old, YIP national is only 5 years old. “Our initiative for 2011 is to get into all states by contacting PIA associations in each state,” Bulloch said. “Some are too small to support a full board, and we’re not asking them

to do that; we’re just asking them to get young people involved, to send them to D.C. for a legislative summit, so when they’re older and running an agency, they’re already involved and know the players.”

The major benefit to members is the opportunity to get involved in state and national legislative issues and educational programs, including continuing education classes, designation programs and sales classes.

For agents already selling business, YIP is useful because of the opportunity to network with peers in other states or regions. “If I want to know about a risk, I can call a fellow agent,” Bulloch said. “And I’ve had agents from South Carolina, Florida and New York call and ask me about a Louisiana risk they want me to place because they’re not licensed here.”

Although the Louisiana chapter doesn’t currently have a formal recruitment program, this is something they “absolutely” need to target, Bulloch said. To encourage college student members, the group offers annual membership priced at only $5, compared with $45 for working members. For the price, members get to attend 3 to 4 continuing education sessions and an annual state conference.

While Bulloch concedes that

40 THE BIG “I” VIRGINIA • Summer 2011

the average agency skews toward baby boomers, he is seeing more agency employees under age 35 in areas like Baton Rouge and southeast Louisiana, compared with New Orleans, where many of the agencies have been around for more than 100 years. “For some of these places, it’s their way or the highway, but they have to understand that things change,” Bulloch said. “If you look at the way all businesses function these days, it’s a lot different than just 15 years ago, when the big question was, ‘do you have a fax machine?,’” he said. “Ten years ago, it was, ‘Do you have an e-mail address?’ Now we get faxes, e-mails with attachments and can search the web from our smart phones.”

A big part of the recruitment challenge is that well-known industries with more financial clout are cherry-picking the best and brightest with high salaries and bonuses, and insurance can have a tough time competing with them. “What pharmaceutical companies or others that guarantee big salaries and bonuses don’t say is that in 10 years, that hire may be making the same amount he did when he was hired,” he said. “It’s hard for agency owners to say, ‘You may not make much in your first year, but as your book grows, you’ll be making more.’ Many young people can’t see the big picture, and that’s probably the hardest thing about attracting new talent.”