Embed Size (px)

Citation preview

JAMESTRONG PACKAGING AUSTRALIA SUPERANNUATION FUND

SUPER UPDATE – MAY 2017Presented by Simon Hussey, Willis Towers Watson

22

DISCLAIMER

The information in this presentation is general information only. It is not personal

advice. This presentation is not intended to and should not be taken as a

recommendation of any investment options and it does not take into account particular

objectives, financial circumstances or needs.

Before making any investment decisions regarding this information, you should read

the Fund’s Product Disclosure Statement or member booklet for your category of

membership, and also consider your objectives, financial situation and needs. You may

also wish to consider obtaining professional advice before making your decision.

Towers Watson Australia Pty Ltd

ABN 45 002 415 349, AFSL 229921

33

AGENDA

● Fund highlights

● Jamestrong Packaging Australia Superannuation Fund - features

● Investments and Performance

● Legislative update

● Retirement Strategies

● Centrelink Age Pension

● Questions

44

WHAT DO YOU THINK

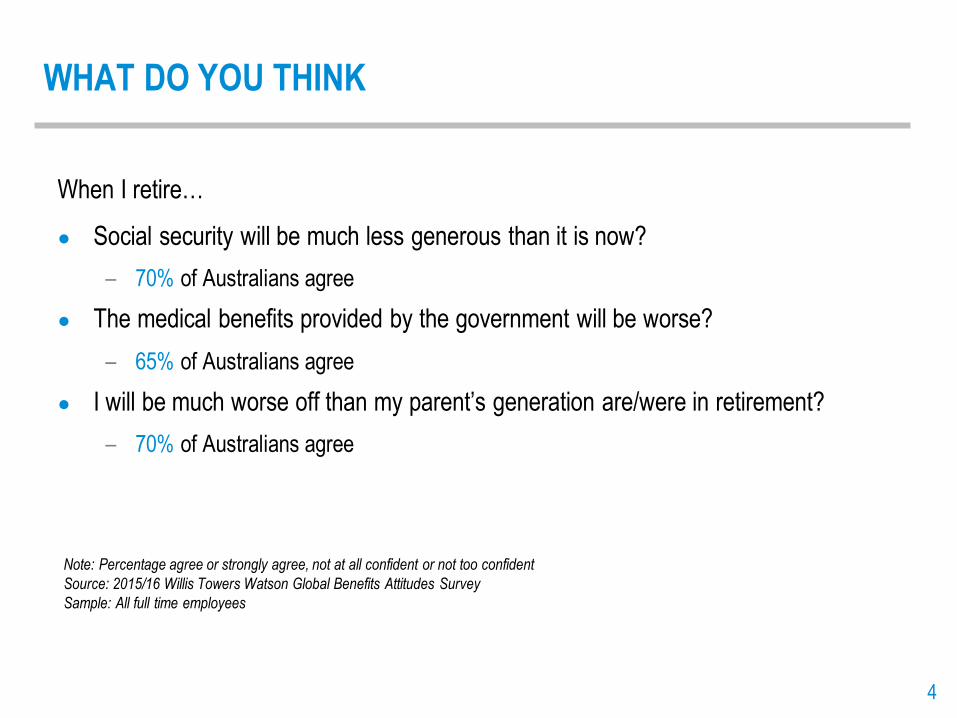

When I retire…

● Social security will be much less generous than it is now?

– 70% of Australians agree

● The medical benefits provided by the government will be worse?

– 65% of Australians agree

● I will be much worse off than my parent’s generation are/were in retirement?

– 70% of Australians agree

Note: Percentage agree or strongly agree, not at all confident or not too confident

Source: 2015/16 Willis Towers Watson Global Benefits Attitudes Survey

Sample: All full time employees

55

BACKGROUND

● The Jamestrong Packaging Australia Superannuation Fund commenced on

1 November 2007 after Impress Australia Pty Limited acquired Amcor’s Australian

food can and Aerosols Division

● The Fund continues to provide benefits to members on the same terms and

conditions even though the employer has changed

Amcor Impress Ardagh Jamestrong Packaging

● The Fund is managed by a professional Trustee

● Investment manager adjusts asset allocations to enhance returns and/or to

reduce risk

● The Fund’s website is updated regularly – jamestrongsuper.com.au

● The Trustee issues two or three newsletters per year, along with a detailed

Annual Report

66

FUND HIGHLIGHTS

● The Fund continues to deliver competitive investment returns. Recent returns for

the Active Balanced option have been:

– 1 July 2015 – 30 June 2016 3.5%

– 1 July 2016 – 30 April 2017 9.8%

● If you are a contributory member, the full cost of insurance cover and

administration fees are met by Jamestrong Packaging

● The Fund’s new website Member Centre allows you to

– check your benefits at any time

– update your personal details

– change your beneficiaries, and

– switch investment options

77

CONTAINERS PACKAGING SECTION – FEATURES

Choice of membership categories

● Contributory – members are provided with defined benefit style benefits

● Non-contributory – members are provided with accumulation style benefits

● Changes between Contributory and Non-contributory membership can happen

annually at 1 July

88

CONTAINERS PACKAGING SECTION – FEATURES

Contributory members

● Defined benefit style benefits – final superannuation benefit is based on a formula

using years of contributory membership and final average salary

● May not be impacted by investment market performance

● Member must contribute 3.5% of salary (after tax) or 4.12% of salary (before tax)

● Can also make additional voluntary contributions

● Insurance cover provided on death, TPD and temporary disability (i.e. income

protection)

● Administration and insurance fees are paid by Jamestrong Packaging as part of its

monthly contribution

99

CONTAINERS PACKAGING SECTION – FEATURES

Non-contributory members

● Accumulation style benefits:

– Ongoing contributions by Jamestrong Packaging at Superannuation Guarantee

rate

– Positive/negative investment returns affect accounts

– Administration fees, insurance premiums and taxes deducted from member’s

account

● Benefit is impacted by investment market performance

● Members can make voluntary contributions

● Lower levels of death and TPD cover compared to Contributory membership

1010

CONTAINERS PACKAGING SECTION – FEATURES

Changing membership

● Changes between Contributory and Non-contributory membership can happen at

1 July each year

● If you transfer between Contributory and Non-contributory, you get:

– A defined benefit for the period that you contribute (i.e. multiple for that period x

FAS at date of calculation) based on most recent salaries even if you were

contributory a long time ago

– Accumulation benefit for the period that you do not contribute

● To be accepted for the higher levels of insurance cover that are available to

Contributory members, you must provide health evidence satisfactory to the Fund’s

insurer

● If you are considering changing to Contributory membership, contact the Fund

Administrator (1800 253 154) for the relevant forms

1111

INVESTMENT PERFORMANCE

Options10 months to

30 April 2017

2015/2016

Final Rates

Assertive Plus 13.87% 3.43%

Assertive 11.75% 3.68%

Active Balanced 9.80% 3.50%

Conservative 4.75% 3.93%

Cash 1.57% 1.95%

The above figures are net of investment fees, indirect costs and tax.

1212

MEDIUM TERM ASSET ALLOCATION STRATEGY

The investment manager regularly reviews markets to determine which investment

sectors it expects to outperform in the medium term.

Attractive: hedge funds; private equity; credit; cash

Neutral: Australian shares; international shares; infrastructure; property

Negative: currency (AUD); fixed interest

The investment manager’s views and themes are then applied evenly across the pre-

packaged options. For example, if there was a positive view on property, all portfolios

would have a proportionately overweight holding of property.

1313

ASSET ALLOCATION OF ACTIVE BALANCED OPTION

Current Long-term

26%

26%

7%

14%

8%

11%

8%

36%

24%3%

10%

5%

7%

15%

Australian Shares International Shares Growth Alternatives Property

Cash Defensive Alternatives Diversified Fixed Income

1414

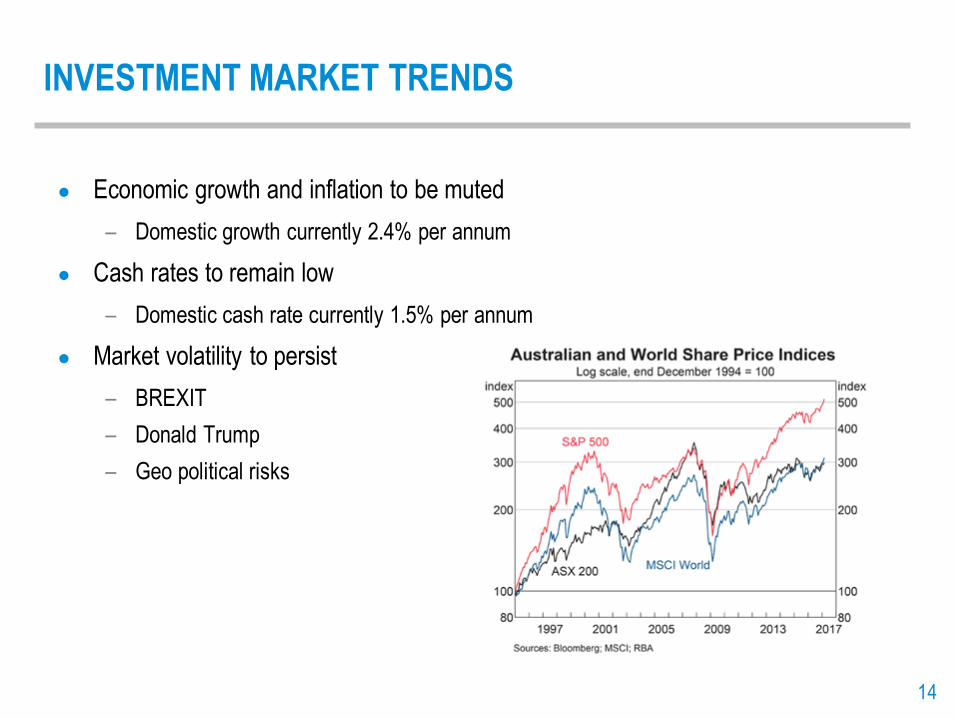

INVESTMENT MARKET TRENDS

● Economic growth and inflation to be muted

– Domestic growth currently 2.4% per annum

● Cash rates to remain low

– Domestic cash rate currently 1.5% per annum

● Market volatility to persist

– BREXIT

– Donald Trump

– Geo political risks

1515

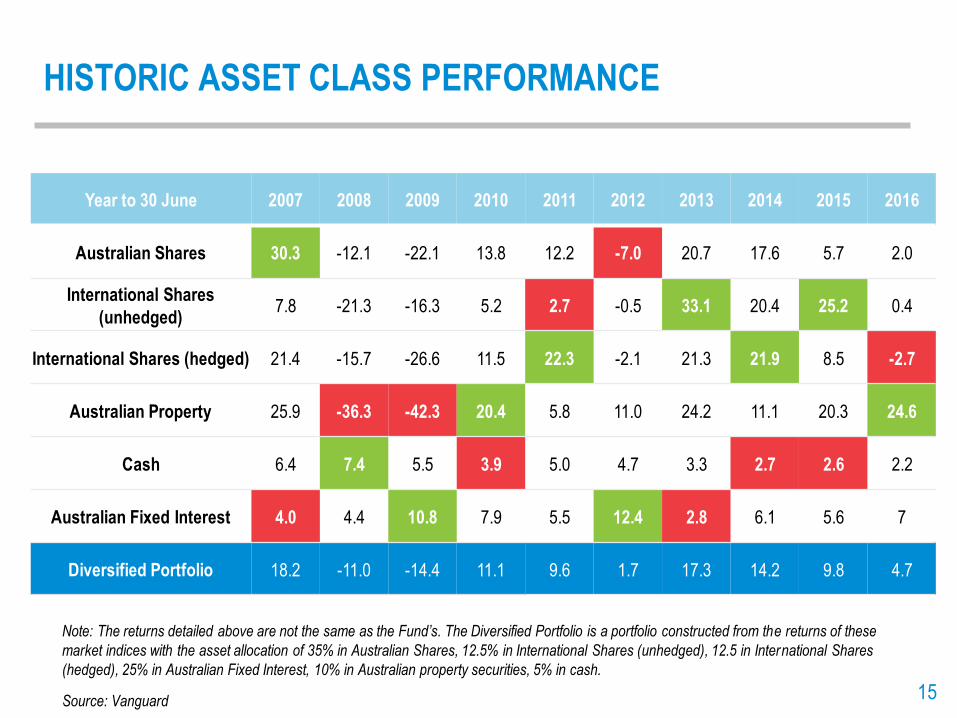

HISTORIC ASSET CLASS PERFORMANCE

Note: The returns detailed above are not the same as the Fund’s. The Diversified Portfolio is a portfolio constructed from the returns of these

market indices with the asset allocation of 35% in Australian Shares, 12.5% in International Shares (unhedged), 12.5 in International Shares

(hedged), 25% in Australian Fixed Interest, 10% in Australian property securities, 5% in cash.

Source: Vanguard

Year to 30 June 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Australian Shares 30.3 -12.1 -22.1 13.8 12.2 -7.0 20.7 17.6 5.7 2.0

International Shares

(unhedged)7.8 -21.3 -16.3 5.2 2.7 -0.5 33.1 20.4 25.2 0.4

International Shares (hedged) 21.4 -15.7 -26.6 11.5 22.3 -2.1 21.3 21.9 8.5 -2.7

Australian Property 25.9 -36.3 -42.3 20.4 5.8 11.0 24.2 11.1 20.3 24.6

Cash 6.4 7.4 5.5 3.9 5.0 4.7 3.3 2.7 2.6 2.2

Australian Fixed Interest 4.0 4.4 10.8 7.9 5.5 12.4 2.8 6.1 5.6 7

Diversified Portfolio 18.2 -11.0 -14.4 11.1 9.6 1.7 17.3 14.2 9.8 4.7

1616

SUPERANNUATION – CONCESSIONAL CONTRIBUTIONS

● Concessional contributions include superannuation guarantee, employer funded

insurance premiums/administration fees and salary sacrifice contributions

– For Non-Contributory members, concessional contributions are the sum of actual

SG contributions and any salary sacrifice contributions

– For Contributory members, concessional contributions are a notional contribution

relating to your defined benefit plus any additional salary sacrifice contributions

1717

SUPERANNUATION – CONCESSIONAL CONTRIBUTIONS

● From 1 July 2017, the concessional cap will reduce to $25,000 per annum

regardless of age

¹ Subject to the work test

● Concessional contributions taxed at 15%

● Up to 85% of contributions over the concessional cap can be withdrawn from super

and taxed at your marginal tax rate

Current Legislation From 1 July 2017

Concessional

contribution cap

< age 50 $30,000

$25,00050 – 65 years$35,000

65 – 75 years¹

1818

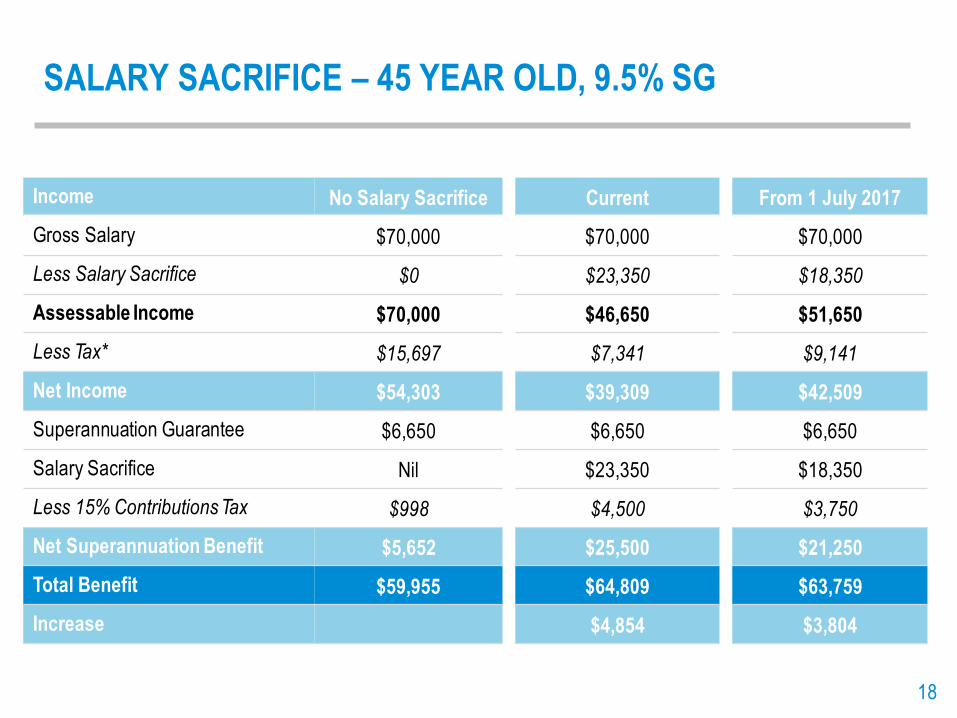

SALARY SACRIFICE – 45 YEAR OLD, 9.5% SG

Income No Salary Sacrifice

Gross Salary $70,000

Less Salary Sacrifice $0

Assessable Income $70,000

Less Tax* $15,697

Net Income $54,303

Superannuation Guarantee $6,650

Salary Sacrifice Nil

Less 15% Contributions Tax $998

Net Superannuation Benefit $5,652

Total Benefit $59,955

Increase

Current

$70,000

$23,350

$46,650

$7,341

$39,309

$6,650

$23,350

$4,500

$25,500

$64,809

$4,854

From 1 July 2017

$70,000

$18,350

$51,650

$9,141

$42,509

$6,650

$18,350

$3,750

$21,250

$63,759

$3,804

1919

SALARY SACRIFICE – 55 YEAR OLD, 9.5% SG

Income No Salary Sacrifice

Gross Salary $70,000

Less Salary Sacrifice $0

Assessable Income $70,000

Less Tax* $15,697

Net Income $54,303

Superannuation Guarantee $6,650

Salary Sacrifice Nil

Less 15% Contributions Tax $998

Net Superannuation Benefit $5,652

Total Benefit $59,955

Increase

Current

$70,000

$28,350

$41,650

$5,541

$36,109

$6,650

$28,350

$5,250

$29,750

$65,859

$5,904

From 1 July 2017

$70,000

$18,350

$51,650

$9,141

$42,509

$6,650

$18,350

$3,750

$21,250

$63,759

$3,804

2020

WHY SHOULD I CONSIDER SALARY SACRIFICE?

● For each $1,000 salary sacrificed to superannuation within the concessional cap,

the net benefit is $850 (net of 15% contribution tax)

● Compared to personal income taxed at marginal rates:

¹ Rates quoted include Medicare and Budget Repair Levies. Budget Repair Levy ceases on 30 June 2017

● Division 293 income threshold reduces to $250,000 from 1 July 2017

Taxable Income Marginal Rate¹ Net Income Difference Required Return

< $18,200 Nil $1,000 - $150 - 15.0%

$18,201 - $37,000 21% $790 $60 7.6%

$37,001 - $87,000 34.5 $655 $195 29.8%

$87,001 - $180,000 39% $610 $240 39.3%

$180,001 - $300,000 49% $510 $340 66.7%

> $300,000 49% $510 $190 37.3%

2121

SUPERANNUATION – NON-CONCESSIONAL

CONTRIBUTIONS

● Made on an after tax basis, contribution tax does not apply

● From 1 July 2017 the non-concessional contribution cap will reduce to $100,000 per

annum, with a two year bring forward of up to $300,000 available prior to age 65

● Transitional arrangements apply to two year bring forward

● Non-concessional contributions not permitted once total superannuation benefits

exceed $1.6 million

● Full bring forward not available if total superannuation benefits exceed $1.4 million

Current legislation From 1 July 2017

Non-

concessional

contribution cap

< age 65$180,000 or $540,000 two

year bring forward

$100,000 or $300,000 two

year bring forward

65 – 75 years¹ $180,000 $100,000

2222

LEGISLATIVE UPDATE

Tax offsets from 1 July 2017

● Low Income Superannuation Tax Offset (LISTO)

– Effectively eliminates tax on superannuation contributions for low income earners

– Annual cap of $500

– To qualify, your adjusted taxable income must not be greater than $37,000 per annum

– ATO will determine eligibility and pay offset to superannuation fund directly

● Extension of spouse contribution tax offset

– Tax offset of 18% of contributions made by a contributing spouse, up to $540

– Spouse income thresholds will increase substantially from 1 July 2017

Current From 1 July 2017

Lower Threshold Upper Threshold Lower Threshold Upper Threshold

$10,800 $13,800 $37,000 $40,000

2323

GOVERNMENT CO-CONTRIBUTION

● Provides an incentive for individuals to make after tax contributions to

superannuation

● At least 10% of assessable income must be from employment and a tax return

must be submitted

● The maximum annual Government Co-contribution is $500 per annum based on a

member contribution of $1,000 per annum

● Entitlement decreases by 3.333 cents per $1 of income above the following income

thresholds:

2016/17 2017/18

Lower Threshold Upper Threshold Lower Threshold Upper Threshold

$36,021 $51,021 $36,813 $51,813

2424

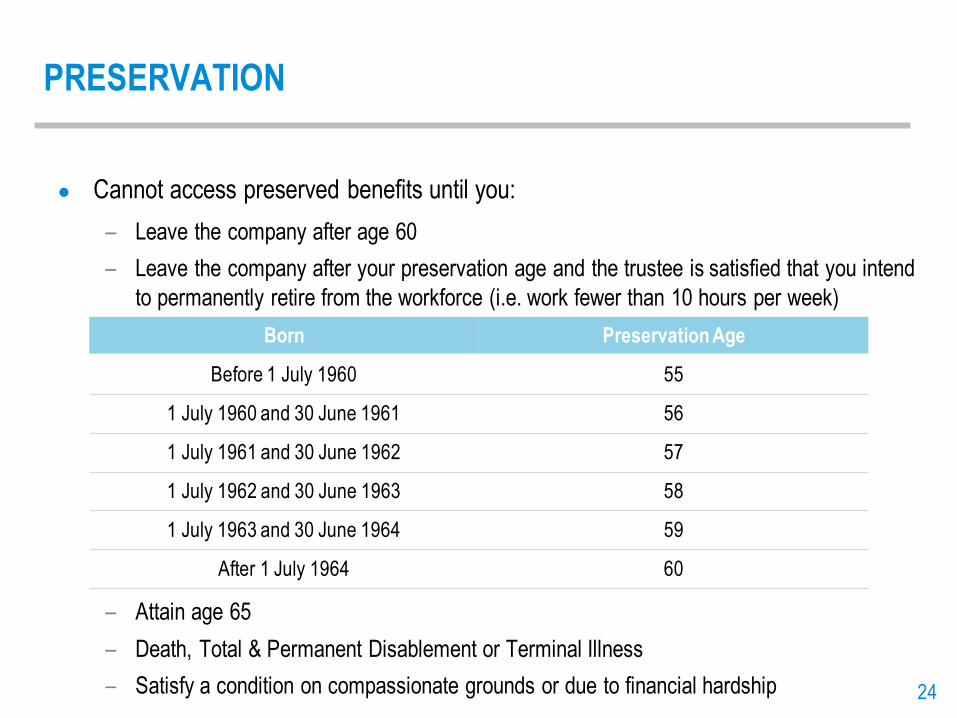

PRESERVATION

● Cannot access preserved benefits until you:

– Leave the company after age 60

– Leave the company after your preservation age and the trustee is satisfied that you intend

to permanently retire from the workforce (i.e. work fewer than 10 hours per week)

– Attain age 65

– Death, Total & Permanent Disablement or Terminal Illness

– Satisfy a condition on compassionate grounds or due to financial hardship

Born Preservation Age

Before 1 July 1960 55

1 July 1960 and 30 June 1961 56

1 July 1961 and 30 June 1962 57

1 July 1962 and 30 June 1963 58

1 July 1963 and 30 June 1964 59

After 1 July 1964 60

2525

LEGISLATIVE UPDATE

Transition to Retirement Pensions

● From 1 July 2017, the tax exemption applicable to investment earnings on

Transition to Retirement Pensions will be removed

● Depending on individual circumstances it may still be appropriate for individuals to

maintain a transition to retirement pension after 1 July 2017

● Note: the Fund does not offer Account-Based Pensions, including Transition to

Retirement Pensions

Current Legislation From 1 July 2017

Income

Tax-free

A maximum of 15%, can be reduced by deductions

and other offsets such as imputation credits

Capital Gains15% for assets held less than 12 months

10% for assets held more than 12 months

2626

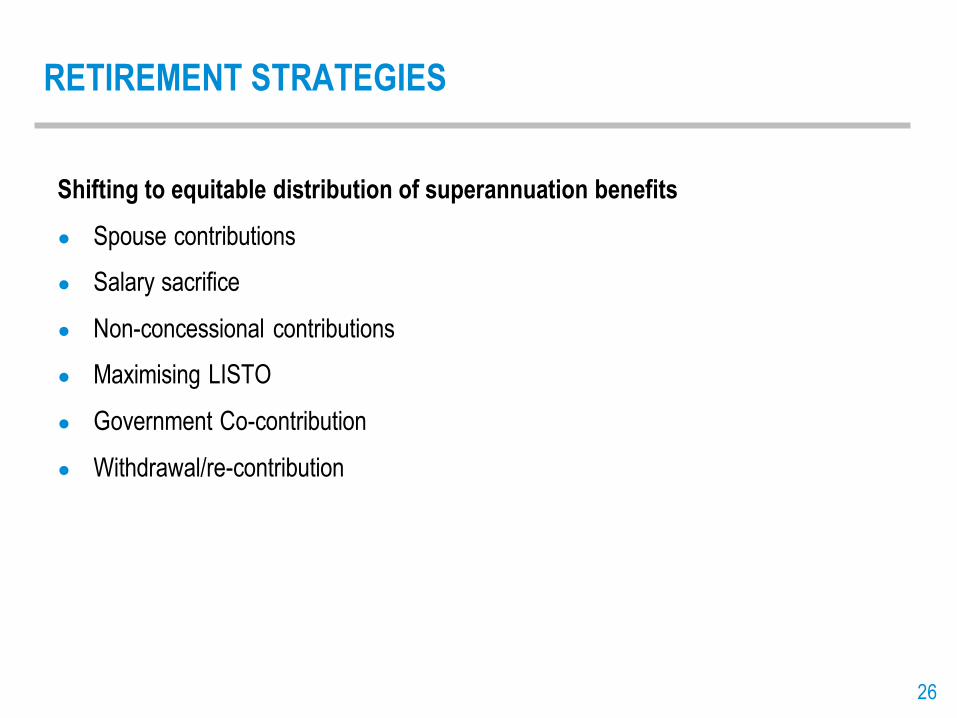

RETIREMENT STRATEGIES

Shifting to equitable distribution of superannuation benefits

● Spouse contributions

● Salary sacrifice

● Non-concessional contributions

● Maximising LISTO

● Government Co-contribution

● Withdrawal/re-contribution

2727

CENTRELINK – AGE PENSION

● Eligibility

Date of Birth Male Female

1 July 1947 – 31 December 1948 65 years 64.5 years

1 January 1949 – 30 June 1952 65 years

1 July 1952 – 31 December 1953 65.5 years

1 January 1954 – 30 June 1955 66 years

1 July 1955 – 31 December 1956 66.5 years

After 31 December 1956 67 years

2828

CENTRELINK – AGE PENSION

● Means test as at 20 March 2017

* Inclusive of Pension and Clean Energy Supplements

● Excludes family home, superannuation assets prior to attaining age pension

eligibility age and up to $250 of employment income per fortnight

● Above the lower threshold, pension entitlement reduces by:

– Asset test: $3 per fortnight per $1,000 of assessable assets

– Income test: $0.50 per fortnight for singles and $0.25 for each member of a couple, for

each $1,000 of assessable income

Homeowners Lower threshold Upper threshold Maximum pension*

SingleAsset test $250,000 $546,250 $888.30 pf

($23,095.80 pa)Income test $4,264 $50,455.60

CoupleAsset test $375,000 $821,500 $669.60 each pf

($34,819.20 pa

combined)Income test $7,592 $77,230.40

2929

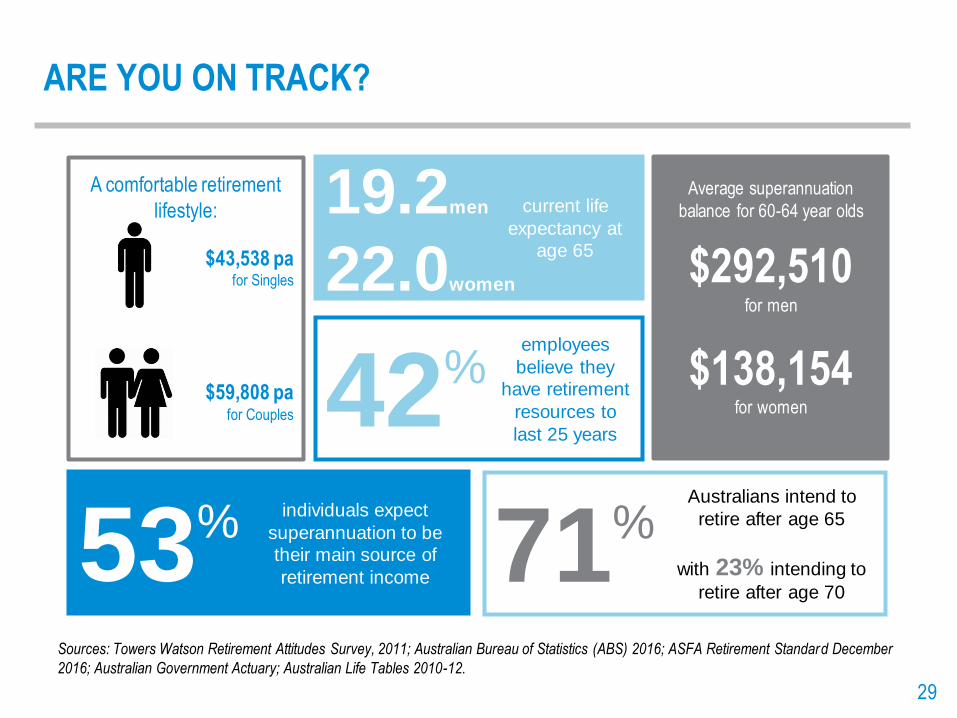

ARE YOU ON TRACK?

Sources: Towers Watson Retirement Attitudes Survey, 2011; Australian Bureau of Statistics (ABS) 2016; ASFA Retirement Standard December

2016; Australian Government Actuary; Australian Life Tables 2010-12.

employees

believe they

have retirement

resources to

last 25 years 42%

Australians intend to

retire after age 65

with 23% intending to

retire after age 7071%individuals expect

superannuation to be

their main source of

retirement income53%

Average superannuation

balance for 60-64 year olds

$292,510for men

$138,154 for women

current life

expectancy at

age 65

19.2men

22.0women

A comfortable retirement

lifestyle:

$43,538 pa for Singles

$59,808 pa for Couples

3030

YOUR ACTION PLAN

Have you…

● Reviewed your superannuation contribution strategy

– Pre and post 1 July 2017 salary sacrifice contributions

– Eligibility for Government Co-contribution

– Spouse contributions

● Assessed the appropriateness of your current investment choice

● Considered whether your insurance cover is sufficient

● Got a valid superannuation death benefit nomination, Will and Power of Attorney

Questions?

31

More information on the Jamestrong Packaging

Australia Superannuation Fund can be found at:

jamestrongsuper.com.au

Jamestrong Packaging Australia Superannuation Fund

Fund Administrator

Phone 1800 253 154

Email [email protected]

Willis Towers Watson – Financial Planning

Phone 03 9655 5421

Email [email protected]