Embed Size (px)

Citation preview

Enrico Camerinelli is a senior analyst withCelent’s retail and business banking group,based in Europe. His current research focuseson the Single Euro Payments Area and on thefinancial supply chain. Prior to joining Celent, MrCamerinelli was an independent analyst andadviser to organisations such as the Sup-ply Chain Council and the Theory of Con-straints International Certification Organization.Mr Camerinelli has previously held the positionof VP for Enterprise Applications at the METAGroup research company. He also covered theposition of pre-sales marketing manager at J.D.Edwards, having previously worked in theindustry as a supply chain and plant manager.

ABSTRACT

In the contingent situation of extreme reductionof credit flows, enterprises try to extract liq-uidity, as much as possible, through better andmore efficient management of their operations.It becomes paramount, therefore, to understandthe sources of possible internal financing. It isabout aligning the operational flow with thefinancial flow. It is about fully evaluating theprocesses and the ‘end-to-end’ information thatdetermine the values of liquidity, of the ac-counts and of the corporate working capital.The supply chain is a network of participantswho trade goods, services and information infront of purchase and sales orders. The financialcomponent, expressed through invoices andpayments, acts as the ‘glue’ between the variousparticipants. In such a context, control passesfrom corporates to the issuing institutions, that

is, the banks. Banks also find themselves indire straits owing to the serious economic crisis.They need to innovate products and services inan ever-more competitive — and prudent —market. By mapping the operational processesin front of these as well as other financialsolutions, the supply-chain manager can guidethe finance colleague proactively to involve thebank of reference to obtain solutions andservices that positively condition the corpora-tion’s working capital.

Keywords: supply chain management,working capital, supply chain finance,payments, economic value added

INTRODUCTIONTo cover the topic of supply-chainfinance (SCF), the concept of supply-chain management (SCM) first needs tobe introduced. Supply chain managementis a disciplined blend of time-basedpractices and technologies that sustaincorporate users in the design, planning,sourcing, making, delivery, service and,eventually, return of the goods, informa-tion and services delivered to a globalisedmarket. The end game is to performsuch activities in a sustainable andprofitable way. The supply chain is,therefore, a set of physical and informa-tion flows which cross networks ofrelationships established among tradingpartners, who, from time to time, are

Supply chain finance

Enrico CamerinelliReceived: 14th October, 2008Celent, Via Agnello, 6/1, 20121 Milan, Italy.Tel: �39 039 21 00 137; e-mail: [email protected]

Journal of Payments Strategy & Systems Volume 3 Number 2

Page 114

Journal of Payments Strategy& SystemsVol. 3 No. 2, 2009, pp. 114-128,� Henry Stewart Publications,1750-1806

creased strategic relevance and importanceof SCM to the company’s economy. Theperson responsible for such operations —the supply-chain manager indeed — isnot, however, the right interlocutor withthe CFO, as the two speak on different‘wavelengths’.

The CFO measures the companyperformance in terms of cash-to-cashcycle time or working capital or cash flowof assets and of operations. Accountspayables and accounts receivables are partof his department’s daily performanceindicators.

The supply-chain manager gaugesresults in terms of production throughput,on-time delivery, work in progress,inventory turns, forecast reliability andproduction efficiency.

Part of the reason why commonsupply-chain metrics are not being usedby finance and senior members ofmanagement is that these measures do notfit in with the normal accounting-financial language of the firm. Hence, thechallenge is to provide the translationof operations outcomes to financialmeasures.

Supply chain management requires newthinking and a new approach. Theincreased levels of globalisation and in-novation which permeate the strategiesand agenda of corporate-level execu-tives of industrial production organisationsdemand tight integration between physi-cal operations, exchange of data andinformation and injections of liquidity.

Companies are gradually realising thattheir current financial supply-chain prac-tices are not sustainable. They must even-tually move from the manual quagmireto the electronic realm. The eleganceof the concept of end-to-end financialsupply-chain automation is hard to deny.The ‘one sweep’ elegance, however, getsmired in multiple departments and busi-ness processes (see Figure 1).

customers and suppliers. Therefore, theconcept of a supply ‘chain’ expands toa supply ‘network’, to incorporatealso the chains of design, commer-cial distribution, service managementand post-sales management. Logistics,manufacturing, purchasing, marketing re-search, promotion, sales, research anddevelopment, product design and totalsystems/value analysis should all beincluded in the scope of SCM.

Common perception still limits SCMto product logistics, materials handlingand warehouse management. A few en-lightened thinkers also include productionplanning and sales distribution in theSCM domain.

The consequence of such a lackof uniformity is that the supply-chainmanager is often forced to share decisionsand responsibilities with a number ofdepartmental managers who keep verytight control over their offices. Thisconfines the supply-chain manager to aroutine series of operational supervisions,practically impeding an overall high-levelperspective and ‘jurisdiction’.

Conversely, the manager is faced withquantitative operational and financial ob-jectives that are difficult to manage anddifficult to predict. Thousands of differentparameters and financial variables, includ-ing production or service costs, dynamicinventory levels, targeted sales levels,pricing changes, inflation rates, exchangerates, taxation rules, dynamic competitivepressures, new threats in the marketplace,changes in raw material costs, macro-economic implications and any changes inthem eventually affect the corporatefinancial performance and the corporateconsolidated financial statement.

Current research shows that an ever-growing number of chief financial officers(CFOs) are put in control of the resultsof the company supply-chain operations.This is an acknowledgement of the in-

Camerinelli

Page 115

Moreover, different economic argu-ments resonate with each stakeholder. Forexample, procurement may care relativelylittle about discount capture because,historically, only a small percentage oftheir suppliers have offered it, andbecause they are accustomed to beingrewarded via rebates from purchasing cardusage. Accounts receivable may be takingcriticism from sales and customers for anantiquated billing/invoicing system andwant to focus solely on that point.Treasurers are increasingly interested inthe big picture (end-to-end automation),because the resulting transaction visibility

and cycle time reduction facilitate theircash-flow forecasting.

Treasury services could rise inprominence if banks drew new maps andexplored uncharted territories along thesupply chain. Moreover, unlike credit,which has mapped nearly all availableterritories, treasury services havenumerous green fields to enter. The greenfields lie in working capital andsupply-chain financial optimisation.Increasingly, companies and their banksare recognising that working-capitaloptimisation is inextricably linked to theautomation and integration of thefinancial supply chain.

THE FINANCIAL SUPPLY CHAINMarket globalisation entails even longerchains. The chains are, in reality, relation-ship networks. Each node is linked to theothers through connections of trade ex-changes, ie purchase and sales of goodsand services.

Quality of goods and services is thebasic assumption to ensure the continua-

Figure 1 Processstakeholdersoperate inseparatedenvironments

Figure 2 Physical,information andmonetary flows aretightly intertwined

Supply chain finance

Page 116

DSO, days sales outstanding; DPO, days payable outstandingSource: Celent

Source: Celent

cient management of their operations. Itbecomes paramount, therefore, to un-derstand the sources of possible internalfinancing, not so much as pure cost cut-ting but, rather, as recovery of flow ofa typical financial nature that can helpovercome the current difficult conditionscreated by the economic conjuncture.

It is about aligning the operational flowwith the financial flow. It is about fullyevaluating the processes and the ‘end-to-end’ information that determine thevalues of liquidity, of the accounts and ofthe corporate working capital.

The set of these value chains is calledthe ‘financial supply chain’, to un-derline the tight correlation betweenthe physical/information management ofgoods and services and the correspondingmonetary (and therefore financial) flow.

The financial supply chain at mostcompanies — particularly those in theGlobal 500 — is fraught with in-efficiencies which cut across multiplesubsidiaries, departments and financial

tion of the trade relationship. This is whatcorporates focus on. With significant ef-forts, they introduce continuous improve-ment practices that help improve thecompany’s internal efficiency. Larger cor-porates, in particular, adopt policies tohelp their own partners introduce thesame methods of improvement.

The problem resides when approachingthe third component required to managea supply network: the management offunds (ie monetary flow; see Figure 2).

The dynamics of an ever-globalisedmarket, and the constant need to innovateto compete, lead corporate managers togo beyond the concept of cost reductionas the primary objective. They must con-centrate on how they can ensure con-tinuous and stable growth of profit. Toaccomplish such an objective, they seeksupport from the CFO.

In particular, in the contingent situationof extreme reduction of credit flows,enterprises try to extract liquidity, as muchas possible, through better and more effi-

Figure 3 Paymentdurations are quitescattered in Europe

Camerinelli

Page 117

Source: Celent

institutions. The order-to-cash processconsumes significant time and resources:30 days is typically a minimum, while 120days is common if there is a dispute. Ifone considers the huge price variations inbasic payment services in Europe, sucharguments are indeed very sensitive.Research shows that prices of managing abank account vary between member statesby a factor of 1:8 (eg from c34 a year forthe average customer in the Netherlandsto c252 in Italy). It is not only on pricethat large differences are seen. Forexample, in some member states, pay-ments are executed in real time or on thesame day, but in others 20 days, or evenlonger, is the rule (see Figure 3).

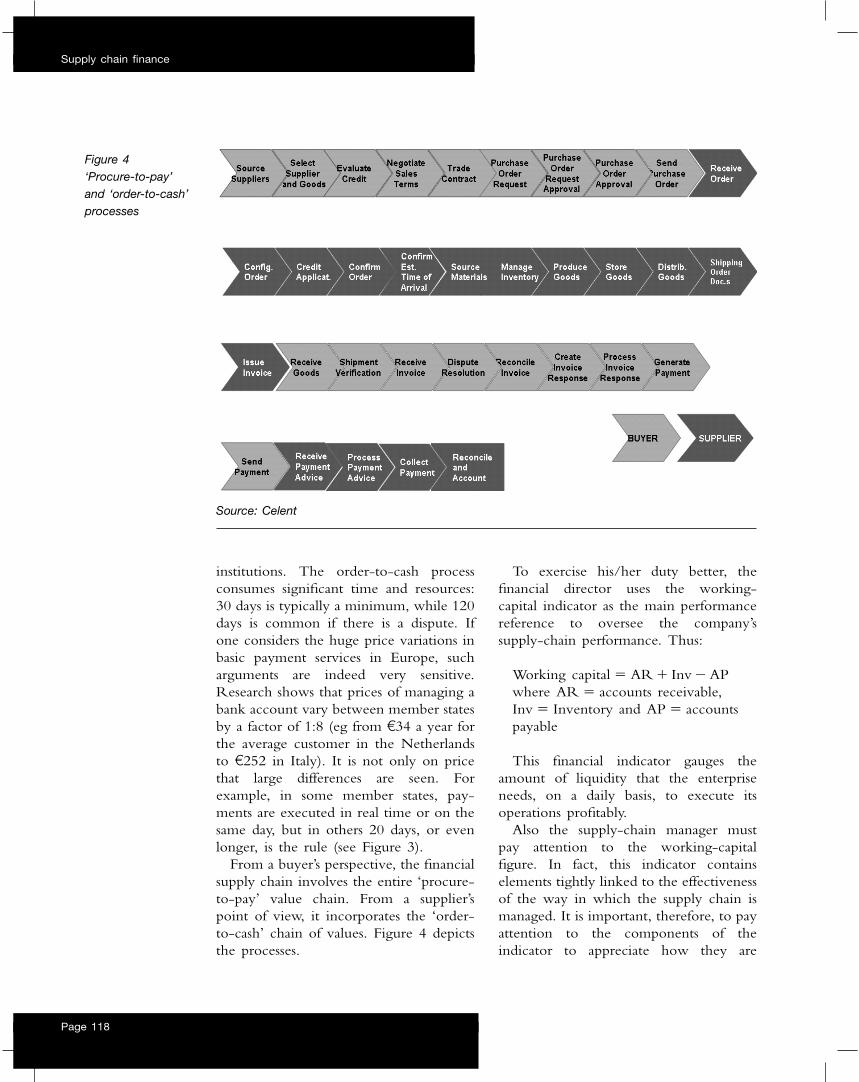

From a buyer’s perspective, the financialsupply chain involves the entire ‘procure-to-pay’ value chain. From a supplier’spoint of view, it incorporates the ‘order-to-cash’ chain of values. Figure 4 depictsthe processes.

To exercise his/her duty better, thefinancial director uses the working-capital indicator as the main performancereference to oversee the company’ssupply-chain performance. Thus:

Working capital � AR � Inv � APwhere AR � accounts receivable,Inv � Inventory and AP � accountspayable

This financial indicator gauges theamount of liquidity that the enterpriseneeds, on a daily basis, to execute itsoperations profitably.

Also the supply-chain manager mustpay attention to the working-capitalfigure. In fact, this indicator containselements tightly linked to the effectivenessof the way in which the supply chain ismanaged. It is important, therefore, to payattention to the components of theindicator to appreciate how they are

Figure 4‘Procure-to-pay’and ‘order-to-cash’processes

Supply chain finance

Page 118

Source: Celent

the analysis of a number of supply-chaininefficiencies that combine to increase theaccounting value of the inventory and,therefore, negatively influence the valueof the working-capital figure:

• too long a waiting time at goodsinwards;

• too long a time to move goods withinthe plant;

• delays in managing purchases and sales;• too long a time spent in preparing the

goods for shipment;• low efficiency of the distribution

channel;• bad forecasting capability;• poor planning;• non-optimal selection of stock-balance

parameters;• purchase of goods based on volume

discounts rather than on real needs;• adoption of ‘push’ rather than ‘pull’

models;• inventories of purchased, in process and

finished goods all created too early.

It is the supply-chain manager’s duty tofind solutions that postpone the comple-tion of a product, in order to minimisethe total amount of stock.

As for the third component of work-ing capital, AP, it is advisable to usethe time-related equivalent: ‘days payableoutstanding’ (DPO).

‘Chocking’ suppliers by forcing themto accept prolonged payment terms doesnot prove to be a winning strategy. Suchan extension of terms can be negotiatedonly if the supplier foresees a valuablereturn.

A clear determination of the parametersused to manage materials — be it theminimum or maximum daily deliveryvolumes or the delivery time windows, aswell as quality assurance protocols — areall steps that provide better and morereliable visibility to the supplier. This

influenced — positively or not — by theoperational supply-chain practices.

The first element is AR. To evaluatebetter how the supply-chain operationsaffect this item, it is advisable to refer tothe ‘time’ factor that so heavily permeatesthe activities of the function, transformingthe AR indicator into the equivalent ‘dayssales outstanding’ (DSO). This figure rep-resents the time it takes to collect andcash-in payments. It therefore measuresthe speed (hence the ‘time’ factor) withwhich the clients receive the invoice andexecute the payment. The crucial pointresides in how the operations, tied to thesales of goods and services, are conducted.By investigating the way in which thebad functioning of supply-chain opera-tions affects the sales process, it becomesevident which areas affect DSO and,consequently, AR.

The most evident of the supply-chainproblems emerges when the product isnot delivered or is delivered in the wrongquantity, with the wrong specifications orin the wrong package. The consequence,in any case, is that the payment is notexecuted.

Moreover, insufficient management ofthe invoicing process, due to wrong in-formation on the shipping documents,will, per se, extend the period between theshipping of the goods and the collectionof the funds.

It becomes evident that projects focusedon improving the defects just illustratedwill determine an improvement (ie reduc-tion) in the DSO indicator. Consequently,the company will benefit from fastercollection of payments and a greateravailability of funds.

‘Inventory’ is the second component ofworking capital. Applying the time factorto this indicator (as was done for DSO),it turns into ‘days in inventory’ (DII). Itis now possible to measure how supply-chain activities affect its value, through

Camerinelli

Page 119

effort can positively affect the way inwhich the supplier manages its ownproduction flows and, consequently, setsthe foundation for better negotiation (iedelay) of the payment terms.

The subject of working capital assumessignificant and indispensable relevance forSCM strategic choices. All this becomesevident when taking into consideration atopic of stringent actuality in SCM prac-tices: outsourcing decisions.

The fact that these decisions must beexamined from all aspects and not onlyfrom considerations related to logisticalaspects (ie limited to the flow of goodsand information) becomes evident as soonas the effects of working capital are as-sessed against the overall economic resultstied to the decision.

Indeed, when comparing the coststructure related to local production(‘Made in Europe’ in Figure 5) versus anoutsourcing option (‘Made in LCC’ —low cost country), the purely physicalsupply-chain costs (eg raw materials,

transport, labour) would make the deci-sion propend in favour of the LCCsupplier. In reality, however, the dailypractice involves other aspects that cannotbe captured by the analysis of the sole‘physical’ costs: for instance, the tendencyto force LCC suppliers to keep goods instock to ensure a continuous supply,offsetting the geographical distance; simi-larly, the imposition on these suppliers —usually with a low negotiating power —to accept extremely extended paymentterms; and, moreover, the contingentsituation of a geographical distance thatputs time deliveries at risk; lastly, thequality guarantee of the delivered goods,not always in line with the expected andcontracted standards.

Figure 5 shows that the introduction ofa new element — working capital —drastically changes the perspective of amere (and more traditional) profit-and-loss view. Suddenly, the indicator capturesthe effect of the ‘bad’ practices previouslydescribed. It is clear, in fact, that any kind

Figure 5 Workingcapital makes thedifference

Supply chain finance

Page 120

Profit 10%

Fixed overheads 10%

Equipment depreciation

20%

Direct labour 40%

Raw materials 20%

Working capital

Made in Europe

Profit 10%

Fixed overheads 12%

Equipment depreciation

15%

Direct labour 6�8%

Raw materials 20%

Working capital

Made in LCC

Logistics 15%

Potential savings

Source: ABN AMRO

Physical supply

chain

SUPPLY-CHAIN FINANCE AND THEROLE OF BANKSThe supply chain is a network ofparticipants that trade goods, services andinformation in front of purchase and salesorders. The financial component, ex-pressed through invoices and payments,acts as the ‘glue’ between the variousparticipants. In such a context, controlpasses from corporates to the issuinginstitutions, that is, the banks.

In effect, banks also find themselves indire straits owing to the serious economiccrisis. They need to innovate productsand services in an ever-increasing com-petitive — and prudent — market.

Corporate customers are in search ofintegrated solutions rather than discreteproducts. The relations manager mustassume a consulting role rather thanbeing a mere expert in the offeredservices/products. Banks have to revisittheir distribution channel, creating aportfolio of solutions that better adapt tothe expectations of their corporateclients, who are involved daily inmanaging the physical, information andfinancial flow of their own supplychain.

To this purpose, some of the largestinternational financial institutions (JPMorgan; ABN-Royal Bank of Scotland;Deutsche Bank; Citi; HSBC) some timeago proposed SCF solutions to themarket. That is, solutions that will financethe typical processes of a corporate’ssupply chain.

Even though the difference between‘financial supply chain’ and ‘supply-chainfinance’ might appear subtle, and merelyacademic, it becomes extremely impor-tant to understand the nature of the twoterms.

The financial supply chain is, as alreadydescribed, the set of processes and informa-tion that determines the value of liquidity,of the accounts and of the company’s

of imposition that affects the financialperformance of the LCC supplier (egreceivables, inventory) will reflect in anincrease in the final price of the goodsdelivered.

The final scenario is quite differentfrom the purely logistical situation, forwhich the flows examined are exclusivelyrelated to goods and information. Theadvantages of the lower costs of thephysical chain can be offset by the higherfinancial costs of a worsened workingcapital.

The need to factor in working capitalis due to two major factors that shapethe ecosystem of current supply chains:the nature of the business conditions ofemerging countries; and the effect of timedelays in the management of geographi-cally dispersed and distant nodes in thesupply and demand networks.

Factors that affect business conditionsare most likely to be country and liquidityrisk. These determine the higher value ofthe cost of capital (typically, by almost fivepercentage points) that burdens all invest-ments made in emerging countries.

Time delays (which characterisegeographically dispersed supply chains)have a significant effect on indicators suchas DSO, DPO and DII. These representthe fundamental components of thecash-to-cash cycle — the time-basedtranslation, in days, of working capital:

C2C � DSO � DII � DPO

The existence of these new factors incurrent SCM decision making is in directcorrelation with the emergence of morecomplex supply networks. More complexnetworks imply an increased number ofpoints of disconnect, which highlightsthe need to balance timely requirementsand processes with the corporate-widestrategic objective to create shareholdervalue and sustainable growth.

Camerinelli

Page 121

working capital. Supply-chain finance, onthe other hand, is the set of products andservices that a financial institution offers tofacilitate the management of the physicaland information flows of a supply chain.

As an example, the issue of an invoiceis a typical financial supply-chain process.It is, in effect, a process generated by thephysical management of the supplies, andtends to modify the value of liquidity, ofthe accounts, and of the working capitalof the issuing company. A correspondingSCF solution, to stay with the example, is‘factoring’. With such a financial instru-ment, a supplier can ‘sell’ to its bank or toits factoring partner its own credit, ac-tually represented by the invoice, andcash-in the payment in advance of thenatural expiration date.

The enterprise pays the financial institu-tion for the service provided in the formof a ‘discount’ on the invoice’s nominalvalue. It will be the institution’s dutyto exact the amount from the invoicereceiver (ie the buyer) once the collectionterm has matured.

Factoring is one of the SCF solutionsoffered by banks. Among the many avail-able, more or less sophisticated, are: theletter of credit, reverse factoring and pre-shipment financing.

Letter of creditA letter of credit is a document issued,mostly, by financial institutions, whichusually provides a payment undertaking toa beneficiary against complying docu-ments, as stated in the letter of credit.It is often used in import-export trade,when the buyer puts at the disposal ofthe seller an established amount for theprovisioning of goods and services. Suchan amount will be available to the selleronly under established and contractualconditions agreed upfront, and that thebank (ie confirming bank) is obliged tohonour.

Reverse factoringWhile in ‘traditional’ factoring it is theseller who asks for an anticipated credit tothe financial institution, with reverse fac-toring it is the bank that promotes theinitiative (hence, the term ‘reverse’). Inthis case, the bank, which has visibilityof the trade transaction between buyerand seller, evaluates the financial risk as-sociated with the buyer — usually anestablished customer. Once the institutionis certain that the buyer will honour itscommitment to the seller, it will an-ticipate to the latter the amount to beinvoiced, at a discount rate significantlyattractive if compared with how much theseller could achieve from its local bank.

This instrument of SCF is usually of-fered to supplying companies in emergingmarkets, in which the financing cost is notcompetitive when compared with howmuch can be offered by a bank that seesthe insolvency risk of the buyer mini-mised.

Pre-shipment financingThis is a rather advanced form of SCF.The document used as guarantee is notthe invoice but the purchase order. Thelevel of risk is high and, therefore, thesolution is offered to consolidated andwell-established buyer-seller circuits.

The financing is once again establishedon the buyer’s level of risk, and ensuresan advance of liquidity of absolute ad-vantage for the seller. This form of SCFis applied, generally, concomitantly with anew product launch, for which the sup-plier has to finance new production linesand new machinery to respond to thebuyer’s requirements.

It must be said that the solutionsdescribed have been present on thefinancial markets for many years; indeed,reverse factoring, which was called ‘con-firming’ in Spain, has been present formany decades. Corporate managers, how-

Supply chain finance

Page 122

desired result in a sustainable andresponsible way, and translate that intoaction. That is, instructions and practicesthat the operators on the shop-floor, inthe warehouses, in the distributioncentres, in the purchasing departmentsand in the planning offices can properlyexecute and measure with a more familiarset of metrics.

Accounts receivable is certainly not an‘out of bounds’ zone and can be positivelyaffected through supply-chain activities,such as providing more reliable transittimes and shorter lead times. In order toaffect AR positively, the supply chainplays a role by delivering products in theright quantity and with the right specs.Improving an otherwise bad invoicingprocess due to incorrect information ondelivery documents can also have a posi-tive effect on the reduction of the ARvalue.

Better forecast accuracy and demandreliability represent a practical way inwhich supply-chain practices affect AP. Astudy by EyeOn cites a 2 per cent poten-tial reduction in purchase prices as adirect consequence of improved demandreliability.1

Reliable production planning andscheduling, together with agreed qualityassurance protocols, can surely improvethe quality of the relationship withsuppliers. That enables the purchasingdepartment to close better deals once awin-win and trustworthy collaborativeenvironment has been established.

EVA modelSupply chain management decisions can-not help determine which financial leversto pull, but they can give an organisationmore confidence in its operation, whichwill give it greater flexibility whenmaking financial decisions. Operationaldecisions can provide visibility into earn-ings, which may allow the company to

ever, must not be deceived. The noveltyresides in the form in which the guaranteedocument is being used. While, up to thistime, the guarantee documents were onlypaper-based, with all the correlated conse-quences and inefficiencies, the new in-ternet technologies allow for completedocument dematerialisation, with theconsequent automation of all the ad-ministrative and operational processes,according to what is commonly defined as‘straight-through processing’.

WHAT CAN CORPORATEMANAGERS DO?The levers for achieving a positive resultof working capital lie in both reducingAR and inventory, and increasing AP. Themost common belief among supply-chainoperators is that AR is almost ‘untouch-able’, as it is tightly linked to sales and,therefore, it is on the sales managers’‘turf ’. Inventory is certainly an item underthe direct control of SCM. Many tech-niques and practices exist to size it, op-timise it and reduce it. Accounts payableis a purchasing manager’s ‘job’, which isimmediately accomplishable by ‘seizing’the supplier with a ‘take it or leave it’proposal, aimed at extending paymentterms by contract. What was previouslypaid after 30 days is now paid in 60.

If collaboration is a practice that goesbeyond pure academic exercise, to bepractically implemented and executedacross all supply-chain constituents, thesupply-chain manager certainly cannotaccept the prospect of getting involved inpractices that reduce the level of trust andcredibility of his/her function, in favourof short-term, short-sighted and poten-tially counterproductive results.

This means that the supply-chainmanager who is on the same ‘wavelength’as the CFO has the responsibility tounderstand what it takes to achieve the

Camerinelli

Page 123

take on more interest risk. Improvedoperations resulting from supply-chainpractices and technologies can also gener-ate additional cash flow to pay off debt,while a higher quality of earnings enablesorganisations to negotiate better interestrates or receive a better bond rating.Together, these factors lower the cost ofdebt.

Among the most accepted models usedto link performance to the creationof shareholder value is economic-valueadded (EVA) established by Stern-Stewart.Empirical evidence indicates that increas-ing shareholder value does not conflictwith the long-term interests of othershareholders.

Specific to the EVA model, the totalshareholder value is calculated by deter-mining a performance spread, ie the ex-cess of the return on invested capitalabove the cost of capital, and by mul-tiplying it by the invested capital toproduce the EVA for the period underconsideration.

The way EVA is calculated can be betterrepresented in a graphical format, typicallycalled the ‘EVA tree’ (see Figure 6).

To support the corporate executives’decision over what actions to take inorder to achieve the expected return, themodel breaks down the EVA value asthe result of the difference between twocomponents:

Figure 6 The EVA‘tree’

Supply chain finance

Page 124

Source: Celent

case, is that the path is indeed taking us fromhigh-level financial performance targetstowards more operational tasks, expressedin the language of the people responsiblefor performing those tasks. The samecomments apply to the other two branchesof the value tree, directed at reducingworking capital and fixed capital.

A first set of ‘leaves’ of the value treelead to the actions needed to increasesales and reduce costs. Supply-chainoperators must focus on improving mar-gins, rationalising network costs, leverag-ing freight procurement, working onlabour arbitrage and incurring lowerairfreight costs.

The ‘leaves’ related to fixed and work-ing capital provide additional insight intohow the actions pursued to improve theseindicators reflect in the final financialvalue of the enterprise’s EVA figure.

Actually, the model breakdown sug-gests the following actionable items thatwill improve the components of workingcapital:

• perfect order fulfilment;• order fulfilment cycle time;• return on working capital;• forecast accuracy;• capacity utilisation.

One company case will prove that theseare not pure academic lucubration, butreal practices.

Case study at DHLDHL uses this model to link the com-pany’s financial result (‘TRS’ value atthe far left in Figure 7) with the ac-tions required from the supply chain.Moving from left to right, the modeldecomposes the TRS figure into moregranular elements, down to the ‘leaves’of the model. One can see that the‘leaves’ of this tree enlist elements suchas ‘reduce costs’ or ‘working capital

• net operating profit after taxes(NOPAT);

• cost of capital.

This means that, only after the value ofthe cost of capital is deducted from theoperating margin — thus obtaining the‘economic profit’ — can the companyeffectively establish whether it still has freecash to be reinvested (positive value forEVA) and therefore generate value, orwhether it is destroying value (whereEVA is negative).

The EVA model adds the component of‘cost of capital’ to the equation, providingclear evidence of the value generated bythe company. In fact, the cost of capital isdefined as the weighted cost sustained bythe enterprise to remunerate its equity (iethe projected return expected by investorsand shareholders) and its debt (ie theinterest rate paid to creditors and banks).

Shown graphically in Figure 6, this isthe cost of capital split into:

• weighted average cost of capital(WACC);

• net invested capital.

On the NOPAT ‘branch’, the model goesbeyond this initial correlation of factors,to break down the NOPAT figure furtherinto its structural elements:

• earning before income taxes (EBIT);• tax rate.

By recursively applying the decomposi-tion rules, the model breaks down theprincipal components of the EVA valueinto the final elements of what resemblesthe picture of a tree rotated 90 degrees,with its roots on the left, the branches inthe middle, and the leaves on the right.

Of course, each component can bebroken down into sub-tasks with moregranular detail. What counts most, in this

Camerinelli

Page 125

reduction’, which are tightly connectedto SCM practices. And, indeed, DHL hasidentified what practices (bullet points inthe figure) must be performed by itssupply-chain resources to most likelybring the corresponding financial resultsto the TRS figure.

DHL has also established clear perfor-mance targets, quantified in the percent-age values shown in the arrow symbols atthe far right of the figure.

The ability to translate operational ac-tions into financial performance has al-lowed DHL to quantify the direct impactof supply-chain improvements on firmvalue.

E-PAYMENTS: THE POSSIBLESOLUTION?Most companies have, at best, automatedonly fragments of the financial sup-ply chain, and only the largest cor-porations have established buyer-supplierconnectivity via electronic data inter-

change (EDI). Consequently, companiesare saddled with excess working capitalgenerating low or no return (eg Fortune500 companies have upwards of a bil-lion dollars each in working capital).Moreover, the interests of suppliers andbuyers are at odds: suppliers want toshrink DSO, while buyers want to extendtheir DPO.

The migration to electronic paymentsfor business-to-business transactions hasbeen far from a gold rush. Conceptually,e-payments make good sense along theoperational efficiency and financial fronts.In reality, however, they do not makeenough sense to generate a gold rush.There is good news and bad news in thee-payments migration story.

The good news is that companies areincreasing their use of e-payments. Theslope of the business-to-business e-pay-ments adoption curve is steepening. By2012, the scale will tip in favour ofe-payments.

The bad news is that the pace is

Figure 7 EVAconcept in practiceat DHL

Supply chain finance

Page 126

Source: DHL

Traditional thinking around tradefinance (especially buyer-centric finance)is increasingly being challenged bycorporates’ growing expectations of thebanking community. The future perspec-tive of a bank’s SCF offer is, as IBM callsit, an event-driven financial chain.

As soon as the financial institution isable to pinpoint when the accountingtransaction is triggered by the supply-chain process (see ‘trigger points’ inFigure 8), it will be able to offervalue-added services. Again, using theexample from the figure, from the ‘triggerpoint’ of the issue invoice, the bankcould offer corresponding services (‘in-voice issuance’), such as a service ofelectronic invoicing, of dematerialisationand management of the related paperdocuments, and of invoice financing.

As the illustration shows, there aremany ‘trigger points’ that can activatevalue-added financial services. The bankcan intercept them — and therefore in-

extremely slow, encumbered by manualprocesses, legacy systems, proprietary for-mats and other priorities.

On the frontier is the developmentof standard, open platforms and service-oriented architecture. The role of tech-nology and third-party providers in adop-tion of e-payments is profound.

Pioneer companies share several traits.First and foremost is a willingness tochange. Electronic payments adoption atcompanies equates to major change.Consequently, any discussion around theadoption of e-payments must begin withan examination of the changes requiredby companies, not only technological butalso organisational and process-related.Second is a desire to alleviate the pain, ateither the operational or financial level,caused by manual processes and papercheques. Third is a desire to add arevenue stream to a cost centre (egprocurement earns a rebate when it usesa purchasing card).

Figure 8 Physicaland financial chainslinked through‘trigger points’

Camerinelli

Page 127

Source: Celent

crease its offer — by integrating theprocesses of the physical chain upon atechnological platform capable of recog-nising them and, consequently, activatethe proper ‘triggers’.

Instead of managing the transactionsmanually, the presence in the market ofenterprise resource planning systems, ofnew communication protocols (eg XML)and of new standards of data transmission(eg ISO 20022) enables, from a purelytechnological standpoint, total visibility ofthe trade processes, and provides a com-plete and functioning predisposition of anecosystem that handles the physical, infor-mation and financial flows of the supply-chain processes.

By mapping the operational processesin front of these as well as other financialsolutions, the supply-chain manager canguide their finance colleague proactivelyto involve the bank of reference to

obtain solutions and services that posi-tively condition the corporate’s workingcapital.

The barrier against these forms of moreefficient and sophisticated forms of financ-ing sit, as always, in the culture andmaturity of each enterprise. For thisreason, the author believes that bankshave a clear responsibility to provideclarity in the business landscape, con-tributing to the understanding and accept-ance by companies through incisiveaction of education, information andpresentation of the value connected withmore modern and mature management ofthe financial supply chain.

REFERENCES

(1) EyeOn (2005) ‘Improved ForecastAccuracy Does Pay Back!’, available at:http://www.eyeon.nl/index.php?id=68&id2=363

Supply chain finance

Page 128