Embed Size (px)

Citation preview

STATE COUNCIL OF EDUCATIONAL RESEARCH &TRAININGVARUN MARG, DEFENCE COLONY, NEW DELHI -24

Support Material For

PGT (Commerce)

Year 2011-12

Classes XI & XII- Accountancy

&

Business Studies

Chief Advisor

Ms. Rashmi Krishnan Director, SCERT

Advisor

Dr. Pratibha Sharma Joint Director, SCERT

Editor / Co-ordinator

Dr. Seema SrivastavaSr. Lecturer, DIET- Moti Bagh

Members / Contributors

Dr. Seema Srivastava, Sr. Lecturer, DIET- Moti Bagh

Ms. Meenakshi Yadav, Sr. Lecturer, SCERT

Dr. Meenu Nandrajog, Reader (Commerce), Deptt. Of Social Sciences, NCERT

Mr. Shruti Bodh Aggarwal, Vice Principal, Govt. Co.ed, SSS Singhu

Mr. Sanjeev Kumar, Lecturer (Commerce), RPVV, Gandhi Nagar

Ms. Jyotsna Davar, Lecturer (Commerce), RPVV, Tyagraj Nagar

Mr. Tarun Mittal, Lecturer (Commerce), RPVV, Tyagraj Nagar

Mr. Anil Kumar Deswal, Lecturer (Commerce), RPVV, Kishan Ganj

Technical Support

Sh. Mukesh Yadav, Publication Officer, SCERTAnd Radha, Support Officer

New Topics/Terms Introduced in Syllabus of C B S EClass XII - Business Studies

In Class XII-Business Studies syllabus some new terms are introduced which are common in present scenario. Business and trade witness changes in the domestic as well as international arena. New terms, approaches and processes are common to enter business world in the liberalised policies globally .This is an attempt to fill the gap and relate the text to the world of work by familiarising class XII commerce students with these. The terms given below are explained in simple words for better comprehension. You are advised to find as many examples and contexts to make it understandable to students. The Hindi version of the same is given at the end of this write-up.

Given below are new terms introduced in the above-mentioned syllabus:

I Public Private Partnership (PPP)

Public Private Partnership means an enterprise in which a project or service is financed and operated through a partnership of government and private enterprises. PPP is the long term partnership between public and private sectors.

Features of Public Private Partnership

1. Facilitates Partnership between Public Sector and Private Sector.PPP is an arrangement which facilitates partnership between Public Sector and Private Sector.2. Pertaining to High Priority Project.PPP pertains to high priority projects.

3. Suitable for Big Projects (Capital Intensive and Heavy Industries)PPP is suitable for big projects whose gestation period is very long.

4. Public WelfarePPP is used in the Government Projects targeted at Public Welfare.

5. Sharing revenue Revenue is shared between Government and Private Enterprise in the agreed ratio.

II Multiple Option Deposit Scheme/ Account (MODS)

Multiple Option Deposit account is a combination of savings account and fixed deposit account which provide specific options to the depositors. It is a type of Saving Bank Account in which excess of a particular limit gets automatically transferred to Fixed Deposit Account.

Many banks offer ‘Flexi Deposit Schemes’ to their depositors. It is to be noted that one can earn higher rate of interest from a Fixed Deposit Account than from a Saving Bank Account. The depositor also enjoys the facility of deposit encashment whenever he/she issues a cheque or withdraws through an ATM debit card, an amount higher than the existing balance in the Saving Bank Account.

III Bank Draft

A bank draft (also known as Demand Draft) is an instrument which is used for the transfer of funds. Anybody can obtain a bank draft after depositing the amount in the bank or. A bank draft is drawn by a bank branch on another branch or some other bank at the place of destination. The bank charges some commission in lieu of issuing a bank draft. Thus, a bank draft is drawn by one branch of a bank on another branch to pay a certain sum of money to the certain person, named therein or to his/her order. A bank may issue bank draft free of cost depending on the customer’s relation with the bank.

A bank draft is issued by a bank branch to any person for consideration or value received in advance. The purchaser will send the draft to the payee. The payee can present the draft on the drawee branch at his/her place and collect the money.

IV Banker’s Cheque

A banker’s cheque (also known as Pay Order) is issued to transfer money like a bank draft. It refers to that bank draft which is payable within the same city or town. A banker’s cheque is a cheque issued by a bank branch in favour of the person named therein and is payable at the same branch. Banks issue banker’s cheque for local purpose and issue bank draft for outstations. Payee can deposit the banker’s cheque in his/her account in same branch. If the payee does not have an account in the issuing branch, then the banker’s cheque will have to be collected through the clearing house. Like a bank draft it will be honoured by the drawee bank.The procedure for issue of a banker’s cheque is same as in case of a bank draft.

V Real Time Gross Settlement (RTGS)

Real Time Gross Settlement refers to a funds transfer system where transfer of funds takes place from one bank to another on a ‘Real Time’ and on ‘Gross’ basis. In this system, transactions are processed continuously throughout the RTGS business hours. The transactions are settled as soon as they are processed.Real Time Gross Settlement is available for funds transfer within India only. This is the fastest possible money transfer system through banks. Funds may be transferred through the Real Time Gross Settlement using the internet facility provided by banks.

VI National Electronic Funds Transfer (NEFT)

National Electronic Funds Transfer refers to a nationwide system that facilitates individuals and firms to electronically transfer of funds from any bank branch to any other individual

having an account with any other bank branch in the country. This scheme is at present available in the major cities. The settlement takes place at a particular time. In this system, transfer of money takes place in batches at regular time intervals. For example, National Electronic Funds Transfer settlement takes place 6 times a day during the weekdays (at 0930, 1030, 1200, 1300, 1500 and 1600) and 3 times during Saturdays (at 0930, 1030, 1200 and 1300). Account-holders can transfer funds through this system by using internet banking facility provided by the bank.

VII Knowledge Process Outsourcing (KPO)

Knowledge Process Outsourcing refers to obtaining high-end knowledge work from outside the organization in order to run the business successfully and in cost effective manner. Many organizations have been setup for the creation, use, dissemination and management of knowledge. In Knowledge Process Outsourcing the focus is on knowledge Expertise. Knowledge Process Outsourcing means outsourcing of Knowledge-based operations to an independent service providing on a contract basis. In Knowledge Process Outsourcing the companies look for individuals who are homogeneous mixes of specialized knowledge, Work Experience, English Speaking and Attitude.

VIII Indian Depository Receipt (IDRs)

An Indian Depository Receipt is an instrument denominated in Indian Rupees in the form of a depository Receipt created by an Indian Depository against the underlying equity of issuing company to enable a foreign company to raise funds from the Indian securities market. The foreign company issuing IDRs deposits shares to an Indian Depository and the depository would issue receipts to investors in India against these shares. The benefits of the underlying shares would avail by the IDR holders in India.‘Standard Chartered PLC’ the first company who issued Indian Depository Receipt in Indian securities market in June 2010.

IX Inter Corporate Deposits (ICD)

Inter corporate deposits are insecure short-term deposits made by a company with another company. The three types of Inter corporate deposits are: (i) Three months deposits; (ii) Six months deposits; (iii) Call deposits. The rate of interest on these deposits is higher than that of banks. These deposits are usually considered by the borrower company to solve problems of short term funds insufficiency.

X Micro, Small and Medium Enterprises Development Act, 2006In accordance with the provisions of Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 the Micro, Small and Medium Enterprises (MSME) are classified as under:

Classification of Enterprises (Chapter III – Unit 7)

Concept of 'Enterprises' as against 'Industries'

Enterprises are classified broadly into:

i) Enterprises engaged in the manufacture/production of goods pertaining to any industry

ii) Enterprises engaged in providing/rendering of services.

Manufacturing Enterprises:

Defined in terms of investment in plant and machinery (excluding land & buildings) and further classified into:

• Micro Enterprises - investment up to Rs. 25 lakh.

• Small Enterprises - investment above Rs. 25 lakh & up to Rs. 5 crore.

• Medium Enterprises - investment above Rs. 5 crore& up to Rs. 10 crore.

Service Enterprises

Defined in terms of their investment in equipment and further classified into:

• Micro Enterprises - investment up to Rs.10 lakh.

• Small Enterprises - investment above Rs.10 lakh & up to Rs. 2 crore.

• Medium Enterprises - investment above Rs. 2 crore& up to Rs. 5 crore.

1

1-1-1-1-1- lkoZtfud futh Hkkxhnkjh ¼lkoZtfud futh Hkkxhnkjh ¼lkoZtfud futh Hkkxhnkjh ¼lkoZtfud futh Hkkxhnkjh ¼lkoZtfud futh Hkkxhnkjh ¼PPP½½½½½

lkoZtfud futh Hkkxhnkjh dk vfHkizk; ,sls miØeksa ls gS ftudk foÙkh;u rFkk lapkyu] lkoZtfud rFkkfuth miØeksa }kjk feydj fd;k tkrk gSA PPP lkoZtfud ,oa futh {ks=k dh nh?kZdkyhu Hkkxhnkjh gSA

lkoZtfud futh Hkkxhnkjh dh fo'ks"krk,¡

1- lkoZtfud ,oa futh {ks=k ds chp lk>snkjh dks lqyHk cukuk

lkoZtfud futh Hkkxhnkjh ,slh O;oLFkk gS tks lkoZtfud ,oa futh {ks=k dh lk>snkjh dks lqyHkcukrh gSA

2- mPp izkFkfedrk okyh ifj;kstukvksa ls lacaf/kr

lkoZtfud futh Hkkxhnkjh dk laca/k mPp izkFkfedrk okyh ifj;kstukvksa ls gksrk gSA

3- cM+h ifj;kstukvksa gsrq mi;qDr

lkoZtfud futh Hkkxhnkjh cM+h ifj;kstukvksa ds fy, mi;qDr ekuh tkrh gS] ftudk xHkZdky vf/kdyEck gksrk gSA

4- lkoZtfud dY;k.k

lkoZtfud futh Hkkxhnkjh dk iz;ksx mu ljdkjh ifj;kstukvksa esa fd;k ukrk gS ftudk mís';lkoZtfud dY;k.k gksA

5- vkxe foHkktu

vkxe dk foHkktu ljdkj ,oa futh miØeksa ds chp lger vuqikr esa fd;k tkrk gSA

2-2-2-2-2- cgq&fodYih; tek [kkrkcgq&fodYih; tek [kkrkcgq&fodYih; tek [kkrkcgq&fodYih; tek [kkrkcgq&fodYih; tek [kkrk

cgq&fodYih; tek [kkrk] cpr [kkrs ,oa lkof/k tek [kkrs dk la;kstu gS tks tekdrkZ dks fodYi miyC/k djkrk gSA ;g ,d izdkj dk cpr [kkrk gS ftlesa ,d fuf'pr lhek ls vf/kd jkf'k Lor% gh lkof/ktek [kkrs esa LFkkukarfjr gks tkrh gSA dbZ cSad vius tekdrkZvksa dks ^yphyh tek ;kstuk* miyC/k djkrsgSaA mYys[kuh; gS fd cpr [kkrs dh vis{kk lkof/k tek [kkrs ls dksbZ O;fDr vf/kd C;kt nj vftZr djldrk gSA tekdrkZ vius cpr [kkrs ds orZeku 'ks"k ls vf/kd jkf'k dk pSd Hkqukus dk lqfo/kk dk Hkhmi;ksx dj ldrk gSA

3-3-3-3-3- cS ad Mªk¶VcSad Mªk¶VcSad Mªk¶VcSad Mªk¶VcSad Mªk¶V

cSad Mªk¶V ¼ftls fMekaM Mªk¶V Hkh dgrs gSa½ ,d foÙkh; iqtkZ gS ftls /ku gLrkraj.k gsrq iz;ksx fd;k tkrkgSA dksbZ Hkh O;fDr cSad esa /kujkf'k tek djds cSad Mªk¶V izkIr dj ldrk gSA cSad Mªk¶V] cSad dh ,d 'kk[kk}kjk fdlh vU; 'kk[kk ¼tks xarO; LFkku ij fLFkr gksrh gS½ ij fy[kk tkrk gSA cSad Mªk¶V tkjh djus ijcSad }kjk dqN deh'ku pktZ dh tkrh gSA vFkkZr~ cSad Mªk¶V cSad dh ,d 'kk[kk }kjk fdlh vU; 'kk[kk ijfy[kk tkrk gS ftldk mís'; ,d fuf'pr /kujkf'k] ,d fuf'pr O;fDr vFkok mlds }kjk vknsf'kr O;fDrdks Hkqxrku djuk gSA ,d cSad fcuk deh'ku ds Hkh cSad Mªk¶V tkjh dj ldrk gS ijUrq ;g xzkgd ds cSadds lkFk laca/kksa ij fuHkZj djrk gSA

2

cSad dh dksbZ Hkh 'kk[kk fdlh Hkh O;fDr ls vfxze /kujkf'k izkIr djds cSad Mªk¶V tkjh djrh gSA Mªk¶V Ø;djus okyh O;fDr cSad Mªk¶V ml O;fDr dks Hkst nsrk gS ftls og /ku Hkstuk pkgrk gSA cSad Mªk¶V izkIrdjus okyk O;fDr bl Mªk¶V dks fu/kkZfjr cSad 'kk[kk esa izLrqr djds /kujkf'k izkIr dj ldrk gSA

4-4-4-4-4- cS adlZ pSdcSadlZ pSdcSadlZ pSdcSadlZ pSdcSadlZ pSd

cSadlZ pSd ¼ftls is vkWMZj Hkh dgrs gSa½ cSad Mªk¶V dh rjg /ku gLrkarj.k gsrq tkjh fd;k tkrk gSA ;g ,slkcSad Mªk¶V gS tks mlh uxj esa ns; gksrk gS tgk¡ ls bls tkjh fd;k x;k gSA

cSadlZ pSd fdlh cSad 'kk[kk }kjk fdlh O;fDr dks tkjh fd;k x;k ,slk pSd gS tks mlh 'kk[kk ij ns; gksrkgSA cSad LFkkuh; mís'; ds fy, cSadlZ pSd rFkk cká LFkkuksa ds fy, cSad Mªk¶V tkjh djrs gSaA Hkqxrku izkIrdjus okyk O;fDr cSadlZ pSd dks mlh 'kk[kk esa fLFkr vius [kkrs esa tek dj ldrk gSA ;fn mlh 'kk[kkesa mldk [kkrk u gks rks og lek'kks/ku x`g ds ek/;e ls /kujkf'k

¼¼¼¼¼ii½½½½½ okgu jlhn ¼okgu jlhn ¼okgu jlhn ¼okgu jlhn ¼okgu jlhn ¼Lorry Receipt½½½½½

okgu jlhn ,d ,slk izi=k gS tks ifjogu daiuh }kjk izs"kd ls mldk eky izkIr djds tkjh dh tkrh gSrkfd izs"kd ds funsZ'kkuqlkj xarO; LFkku ij eky dh lqiqnZxh dh tk ldsA bls ifjogu jlhn rFkk fcYVhHkh dgk tkrk gSA lkekU;r% izsf"kd }kjk okgu jlhn izs"k.kh dks Hkst nh tkrh gS vkSj izs"k.kh mlds i`"B Hkkxij gLrk{kj djds xarO; LFkku ij eky dh lqiqnZxh izkIr dj ysrk gSA

¼¼¼¼¼iii½½½½½ jsyos jlhn %jsyos jlhn %jsyos jlhn %jsyos jlhn %jsyos jlhn %

jsyos jlhn ,d izi=k gS tks jsy iz'kklu }kjk izs"kd dks tkjh fd;k tkrk gS rkfd izs"kd ds eky dks cqfdaxLVs'ku ls izkIr djds izs"kd ds funsZ'kkuqlkj xarO; LVs'ku ij Hkstk tk ldsA ;g bl ckr dk izek.k gS fdeky jsyos iz'kklu }kjk izs"kd ls izkIr dj fy;k x;k gSA

izkIr dj ldrk gSA cSad Mªk¶V dh rjg gh bldk Hkqxrku vo'; izkIr gksrk gSA

cSadlZ pSd tkjh djus dh dk;Zfof/k fcYdqy cSad Mªk¶V tSth gh gSA

5-5-5-5-5- okLrfod le; ldy fuLrkj.k ¼okLrfod le; ldy fuLrkj.k ¼okLrfod le; ldy fuLrkj.k ¼okLrfod le; ldy fuLrkj.k ¼okLrfod le; ldy fuLrkj.k ¼RTGS½½½½½

okLrfod le; ldy fuLrkj.k ,d ,slh iz.kkyh gS ftlesa ,d cSad ls /ku dk gLrkarj.k ^okLrfod le;*rFkk ̂ ldy vk/kkj* ij gksrk gSA bl iz.kkyh esa RTGS O;kolkf;d ?kaVksa ds nkSjku /ku dk gLrkarj.k fujarjgksrk jgrk gSA ysu&nsuksa dks rHkh fuLrkfjr dj fn;k tkrk gS tc os izfØ;k esa vkrs gksaA

okLrfod le; ldy fuLrkj.k ds ek/;e ls /ku dk gLrkarj.k dsoy Hkkjr ds Hkhrj gh fd;k tk ldrkgSA ;g cSad ds ek/;e ls /ku gLrkarj.k dh rhozre iz.kkyh gSA RTGS ds ek/;e ls /ku dk gLrkarj.k cSadksa}kjk baVjusV ds }kjk fd;k tkrk gSA

6-6-6-6-6- jk"Vªh; bysDVªkfud dks"k gLrkarj.k ¼jk"Vªh; bysDVªkfud dks"k gLrkarj.k ¼jk"Vªh; bysDVªkfud dks"k gLrkarj.k ¼jk"Vªh; bysDVªkfud dks"k gLrkarj.k ¼jk"Vªh; bysDVªkfud dks"k gLrkarj.k ¼NEFT½½½½½

jk"Vªh; bysDVªkfud dks"k gLrkarj.k ,d ,slh jk"VªO;kih iz.kkyh gS tks O;fDr;ksa ,oa Qeks± dks fdlh cSad 'kk[kkls fdlh vU; O;fDr vFkok QeZ ¼ftldk ns'k esa fdlh cSad 'kk[kk esa [kkrk gks½ dks dks"kksa ds bysDVªkfud

3

ek/;e ls gLrkarj.k dh lqfo/kk nsrh gSA orZeku esa ;g ;kstuk dsoy egkuxjksa esa miyC/k gSA fuiVku dk;Z,d fo'ks"k le; ij fd;k tkrk gSA NEFT O;ogkjksa dks lewgksa esa ,d fu;fer le; varjky ij fuiVk;ktkrk gSA mnkgj.kkFkZ] jk"Vªh; bysDVªkfud dks"k gLrkarj.k ds varxZr lkseokj ls 'kqØokj rd izR;sd fnu 6ckj ¼09%30] 10%30] 12%00] 13%00] 15%00 o 16%00½ rFkk 'kfuokj dks 3 ckj ¼09%30] 10%30 o 12%00cts½ fuiVku fd;k tkrk gSA [kkrk&/kkjd cSadksa }kjk miyC/k djkbZ tkus okyh baVjusV cSafdax lqfo/kk dkiz;ksx djds bl iz.kkyh }kjk dks"kksa dk gLrkarj.k dj ldrs gSaA

7-7-7-7-7- Kku izfØ;k ckádj.k ¼Kku izfØ;k ckádj.k ¼Kku izfØ;k ckádj.k ¼Kku izfØ;k ckádj.k ¼Kku izfØ;k ckádj.k ¼KPO½½½½½

Kku izfØ;k ckádj.k dk vFkZ gS fd O;olk; dks U;wure ykxrksa ij lQyrkiwoZd pykus ds fy, ,sls dk;ks±dks ckgj ls djk;k tk, ftuds fy, mPp&Lrjh; Kku dh vko';drk iM+rh gSA Kku dh jpuk] mi;ksx]izlkj rFkk izca/k gsrq dbZ laLFkkvksa dh LFkkiuk gqbZ gSA Kku izfØ;k ckádj.k esa Kku fuiq.krk ij ladsUnz.kgksrk gSA

fdlh Lora=k lsok iznkrk ls vuqcU/k vk/kkj ij Kku vk/kkfjr izpkyu dk;Z djokuk gh Kku izfØ;kcká;dj.k gSA Kku izfØ;k dk ckádj.k esa daifu;k¡ ,sls O;fDr;ksa dks [kkstrh gSa] ftuesa fof'k"V Kku]dk;Z&vuqHko] vaxzsth cksyus esa l{kerk rFkk O;ogkj dq'kyrk dk leku feJ.k gksrk gSA

8-8-8-8-8- Hkkjrh; fMiksftVjh fjlhV ¼Hkkjrh; fMiksftVjh fjlhV ¼Hkkjrh; fMiksftVjh fjlhV ¼Hkkjrh; fMiksftVjh fjlhV ¼Hkkjrh; fMiksftVjh fjlhV ¼IDR½½½½½

Hkkjrh; fMiksftVjh fjlhV ,d ,slk foÙkh; iqtkZ gS ftls fdlh fons'kh daiuh ds varfuZfgr lerk va'kksa dsfo#) Hkkjrh; fMiksftVjh daiuh }kjk] Hkkjrh; #i;s esa ewY;kafdr djrs gq, Hkkjr esa tkjh fd;k tkrk gSAfons'kh daiuh ¼tks Hkkjrh; fMiksftVjh fjlhV tkjh djuk pkgrh gS½ fdlh Hkkjrh; fMiksftVjh daiuh dks va'ktkjh djrh gS vkSj Hkkjrh; fMiksftVjh daiuh] Hkkjr esa fuos'kdksa dks bu va'kksa ds fo#) Hkkjrh; fMiksftVjhfjlhV tkjh djrh gSA Hkkjrh; fMiksftVjh fjlhV ds /kkjdksa }kjk buesa varfuZfgr va'kksa ds ykHk feyrs gSaA

^LVSaMMZ pkVZMZ ih-,y-lh-* izFke fons'kh daiuh gS ftlus twu 2010 esa Hkkjrh; iw¡th cktkj esa Hkkjrh;fMiksftVjh fjlhV tkjh dh gSA

9-9-9-9-9- vUr% fuxfer fu{ksi ¼vUr% fuxfer fu{ksi ¼vUr% fuxfer fu{ksi ¼vUr% fuxfer fu{ksi ¼vUr% fuxfer fu{ksi ¼Inter-corporate Deposits (ICD)½½½½½

vUr% fuxfer fu{ksi ,d daiuh }kjk fdlh vU; daiuh esa fd;s x;s vYidkyhu vlqjf{kr fu{ksi gksrs gSaA;s rhu izdkj ds gksrs gSa%&

¼i½ rhu ekg okys fu{ksi

¼ii½ N% ekg okys fu{ksi

¼iii½ ek¡x fu{ksi

bu fu{ksiksa ij C;kt dh nj] cSad ls vf/kd gksrh gSA daifu;k¡] lkekU;r% viuh vYidkyhu dks"kvi;kZIrrk dh leL;k lqy>kus ds fy, bu fu{ksiksa dk iz;ksx djrh gSaA

4

10-10-10-10-10- lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ¼lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ¼lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ¼lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ¼lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ¼Micro, Small and Medium

Enterprises Development Act, 2006½½½½½

lw{e] y?kq rFkk e/;e m|e fodkl vf/kfu;e] 2006 ds vuqlkj lw{e] y?kq rFkk e/;e m|eksa dk oxhZdj.kbl izdkj gS %

m|eksa dk oxhZdj.k ¼v/;k;&III&7½

^m|ksx* ds LFkku ij ^m|e* 'kCn dk iz;ksx fd;k x;k gSA

m|eksa dks eq[;r% nks Hkkxksa esa ck¡Vk x;k gS %

¼i½ oLrqvksa ds [email protected] esa layXu m|eA

¼ii½ lsok iznku djus okys m|eA

fuekZ.kh m|e %fuekZ.kh m|e %fuekZ.kh m|e %fuekZ.kh m|e %fuekZ.kh m|e %

IykaV ,oa e'khujh esa fuosf'kr /kujkf'k ds vk/kkj ij ifjHkkf"kr fd, x, gSa] vkSj fuEu izdkj ls oxhZd`rfd, x, gSa %

lw{e m|e% 25 yk[k #i;s rd dk fuos'kA

y?kq m|e % 25 yk[k #i;s ls vf/kd vkSj 5 djksM+ #i;s rd dk fuos'kA

e/;e m|e % 5 djksM+ #i;s ls vf/kd vkSj 10 djksM+ #i;s rd dk fuos'kA

lsok m|e %lsok m|e %lsok m|e %lsok m|e %lsok m|e %

midj.kksa esa fuosf'kr /kujkf'k ds vk/kkj ij ifjHkkf"kr fd, x, gSa o fuEu izdkj ls oxhZd`r fd, x, gSa%

lw{e m|e% 10 yk[k #i;s rd dk fuos'kA

y?kq m|e % 10 yk[k #i;s ls vf/kd vkSj 2 djksM+ #i;s rd dk fuos'kA

e/;e m|e % 2 djksM+ #i;s ls vf/kd vkSj 5 djksM+ #i;s rd dk fuos'k

11-11-11-11-11- vkarfjd O;kikj esa iz;ksx gksus okys izeq[k izi=kvkarfjd O;kikj esa iz;ksx gksus okys izeq[k izi=kvkarfjd O;kikj esa iz;ksx gksus okys izeq[k izi=kvkarfjd O;kikj esa iz;ksx gksus okys izeq[k izi=kvkarfjd O;kikj esa iz;ksx gksus okys izeq[k izi=k

¼i½ izksQkWekZ chtd ¼Pro-forma Invoice½

izs"kd }kjk izs"k.kh dks Hksts x, eky ds fooj.k dks izksQkWekZ chtd dgk tkrk gSA izksQkWekZ chtd ,slkchtd gS tks dsoy lwpuk ds fy, gksrk gS] blhfy, bls izksQkWekZ chtd dgk tkrk gSA D;ksafd izs"k.k]fcØh ugha gS vkSJ u gh izs"k.kh Øsrk gSA blhfy, blh izksQkWekZ chtd dgrs gSaA :i ,oa fo"k; oLrqesa ^izksQkWekZ chtd* fcYdqy chtd tSlk gh gksrk gSA

Accountancy-XI

International Financial Reporting Standards (IFRS)

Introduction

In the present scenario of globalisation and liberalisation the whole world has become one

economic unit. A number of multinational companies are establishing their businesses in various

countries. There is more and more of international trade, foreign direct investment and flow of

capital to other nation.

Different Countries follow different accounting standards which are affected by political, legal,

economic and cultural system of that particular nation. The use of different accounting

frameworks in different countries results in inconsistent treatment and presentation of the same

underlying economic transactions create confusion for the users of financial statements. Therefore

there is a need for single set of accounting standards that can make the presentation and

preparation of accounting information worldwide in a unified manner. This would facilitate inter-

nation investment and other economic decision.

For this purpose, International Accounting Standards Committee (IASC) was established in 1973,

which issued 41 accounting standards known as International Accounting Standards. (IAS), out of

which 12 IAS have been withdrawn or replaced. IASC was replaced by International Accounting

Standards Board (IASB) in 2001 which adopted the IAS issued by IASC and new accounting

standards issued after 2001 by IASB are known as International Financial Reporting Standards

(IFRS). Now, International Accounting Standards issued by IASB and IFRS are collectively

referred to as IFRS’s.

Meaning

International Financial Reporting Standards (IFRS) refer to the accounting standards issued by

International Accounting Standard Board (IASB). IFRS also cover IAS issued by IASC.

Objectives of IFRS

1. To develop and implement a single set of high quality comparable and globally enforceable Accounting

Standards.

2. To provide high quality transparent and comparable information in Financial Statements.

Advantages of IFRS

The formation of International Standards enables investors, government and organisations to compare

various financial statements supported by IFRS with greater ease that are given below:

(a) Unifies Business Transactions

One of the major aims of IFRS is simply to place all economies/business in the whole world at one level

when it comes to making financial statements. It will enable domestic firms to display their Financial

Statements on similar levels as their foreign competitor. In addition to that organisations with various

Subsidiaries in other countries are also able to prepare their financial statements in a universal

accounting language that is understood by everyone.

(b) Saves Cost

Because many companies are new adopting IFRS, this is going to be a great advantage for companies

with foreign operations. IFRS enables internal consistency with regards to preparing financial reports.

This means that the cost will be reduced since all the reports are going to be prepared in a uniform

manner in all the different branches of the company.

(c) Provide Consistency

It allows companies having different subsidiaries to streamline their training, auditing, reporting

standards and operation standards as well as development standards.

Financial Statements to be prepared under IFRS

1. Statement of financial position

2. Statement of comprehensive income

3. Statement of Charges in Equity

4. Statement of Cash Flow

5. Notes and Significant Accounting Policies

Components of Financial Statements

I Position Statement

(a) Assets

An asset is a resource controller by the enterprise as a result of past events from which future

economic benefits are expected to flow to the enterprise.

(b) Liability

A liability is a present obligation of the enterprise arising from the past events, the settlement of

which is expected to result in an outflow from enterprise resources i.e. assets.

(c) Equity

Equity is the residual interest in the assets of the enterprise after deducting all the liabilities.

Equity is also known as Owner’s Equity.

II Income Statements

(a) Revenues

These are Increase in economic benefits during an accounting period as a result of business operations

or increase in value of assets or decrease in liabilities. However it does not include the contributions

made by equity participants i.e. proprietor, partners and shareholders.

(b) Expenses

It decreases the economic benefits during an accounting period in the form of outflows as a result of

business operations or decrease in value of assets or increase in liabilities.

Presentation in IFRS based Financial Statements

A number of different measurement basis are employed to different degrees and various combinations in

financial statements.

These bases are as under:

(a) Historical Cost

Assets are recorded at the amounts of cash or cash equivalents paid or the fair value of the

consideration given to acquire them at the time of their acquisition. Liabilities are recorded at the

amount of proceeds received in exchange for the obligations.

(b) Current Cost

Assets are carried at the amount of Cash or Cash Equivalents that would have to be paid if the

same or equivalent assets were acquired currently. Liabilities are carried at undiscounted value

that would be required to settle the obligations.

(c) Realisable (Settlement) Value

Assets are carried at the amount of cash or Cash Equivalents that could be realised by selling the

assets in an orderly disposal. Assets are carried at the present discounted value to generate in the

normal course of business. Liabilities are carried at the present discounted value of the future net

cash outflows that are expected to be required to settle the liabilities in the normal course of

business.

Qualitative Characteristics of Financial Statements

(a) Understandability

(b) Reliability

(c) Comparability

(d) Relevance

(e) True Fair View/Fair Presentation

Assumptions in IFRS

The underlying assumptions in IFRS are:

(1) Account Basis

The effect of transactions and other events are recognised when they occur, not as cash is realized

or paid.

(2) Going Concern

It is assumed that the life of the business is infinite i.e. the entity will continue for an indefinite

period.

(3) Stable measuring Unit Assumption

Measuring unit for valuation of capital is the current purchasing power. It means assets should be

reflected at current i.e. fair value.

(4) Units of constant purchasing power

Constant purchasing power means value of capital be adjusted to inflation in the economy at the

end of the financial year.

Status of IFRS in India

Government of India has opted for a four stage implementation of IFRS.

In the first stage, starting April 1, 2011 companies that are Part of the NIFTY or SENSEX or those

with shares listed overseas or with a net worth of over Rs. 1,000 Crore are expected to move to IFRS.

In the second stage, starting April 1, 2012, IFRS would be applicable to insurance companies.

In the third stage, starting April 1, 2013, companies with a net worth of over Rs. 500 Crore and large

non-banking finance companies are expected to adopt IFRS.

In the Fourth stage, starting April 1, 2014, listed companies with a net worth of less than Rs. 500

Crore, non-banking finance companies with a net worth of over Rs. 500 Crore and urban cooperative

banks with net worth of Rs. 200 Crore would be required to shift to IFRS.

The Government has also clarified that unlisted companies with a net worth of under Rs. 500 Crore and urban cooperative banks with a net worth of under Rs. 200 Crore won’t be required to adopt IFRS.

Project work

Project work on Accountancy Class-XI

Topic Bank Reconciliation Statement.

You are employed by sunshine Garments Ltd. as their cashier. Your main responsibility is to maintain the firm’s Cash Book and to prepare a Bank Reconciliation Statement at the end of the month. The Cash Book of sunshine garments (Bank Column Only) is set out below together with a copy of bank statement for March, 2011

You are required to make entries in Cash Book to update it and Reconcile the Cash Book with Bank Statement.

Sun Shine GarmentCash Book (Bank Column Only)

Dr.

Date Particulars Rs. Date Particulars Rs.

2011March 1 To balance bld 5,000 March 5 By Pooja (514241) 6,000March 1 To Kapil and Sons 10,000 March 7 By Meena (514242) 8,000March 4 To Nikhil 20,000 March 8 By Surya Ltd. (514243) 7,000

March 15 To Suraj a Co. 15,000 March 15 By Insurance Co. (DD) 10,000March 28 To Mohit Ltd. 20,000 March 17 By New Computers (514244) 15,000

March 18 By Petty Cash (514245) 5,000March 20 By Anil & Co. (514246) 10,000March 21 By Balance cld 9,000

70,000 70,000

Sun Shine Ltd.ABC Bank Statement

Account No. 004654923Date March 31, 2011

Date Details Withdrawl (Dr.) Deposits (Cr.) Balance2011

March 1 Balance 5,000 (Cr.)March 3 Kapil & Sons 10,000 15,000 (Cr.)March 7 Nikhil 20,000 35,000 (Cr.)March 8 Pooja (514241) 6,000 29,000 (Cr.)March 10 Sumit 10,000 39,000 (Cr.)March 10 Surya Ltd. (514243) 7,000 23,000 (Cr.)March 17 Insurance Co. (DD) 10,000 22,000 (Cr.)March 18 Self (514245) 5,000 17,000 (Cr.)March 22 Anil & Co. (514246) 10,000 7,000 (Cr.)March 29 Bank Charges 200 6,800 (Cr.)March 31 Bank Interest 100 6,900 (Cr.)

SolutionStep I - Tick the items which are found both in Cash Book and Bank Statement. Put () Sign before such

items. These items will neither be recorded in amended Cash Book nor in Bank Reconciliation Statement.

Step II - The unticked items on the Bank Statement are those items which have not been entered in Cash Book because of Lack of information These are :-(i) Directly deposited by Sumit Rs. 10,000(ii) Bank Charges Rs. 200(iii) Interest Credited by Bank Rs. 100These items need to be entered in the Cash Book to update it

Sun Shine GarmentsAmended Cash Book

Dr. Date Particulars Rs. Date Particulars Rs.

March 31March 31March 31

To balance bldTo Sumit (Directly eposited)To Interest

9,00010,000

100

March 31March 31

By bank ChargesBy balance cld

20018,900

19,100 19,100

Step III - The Balance of Bank Column of Cash Book is Rs. 18,900 but - the Bank statement shows a balance of Rs. 6,900. Thus a difference of Rs. 12,000 still exists (Rs. 18,900 - Rs. 6,900)

Step IV - Identify the unticked items in the Cash Book on both debit & Credit Side these are:-Cheques paid into bank for collection but not yet collected :-Suraj & Co. Rs. 15,000Mohit Ltd. Rs. 20,000Cheques issued for payment but not yet presented for payments :-Meena Rs. 8,000New Computers Ltd. Rs. 15,000these items should appear on next month’s bank statement as these are timing differences. These items will be required to be considered in the preparation of Bank Reconciliation Statement.

Bank Reconciliation Statement As on 31 March 2011

Particulars (+) Items (-) ItemsBalance as per amended Cash Book

Less : Cheques deposited but not cleared (Suraj - 15,000, Mohit - 20,000)

Add : Cheques issued but not presented (Meera - 8,000, New Computers - 15,000)

Balance as per Pass Book

18,900

23,000

35,000

6,90041,900 41,900

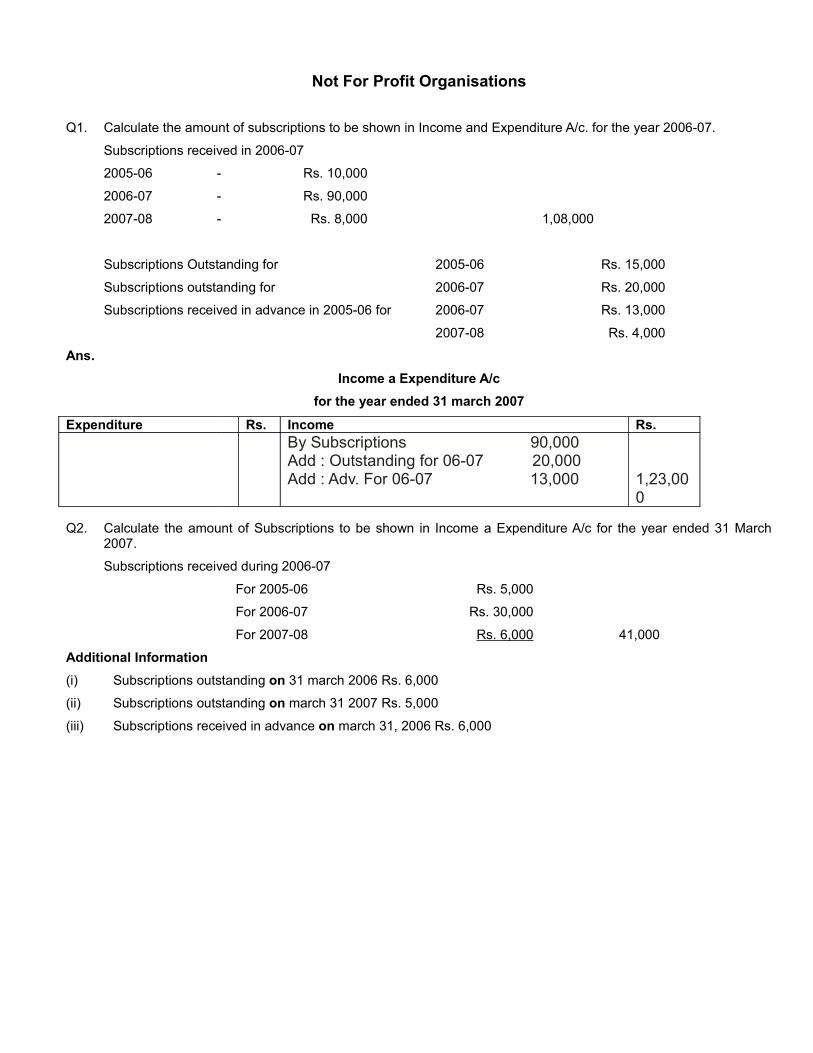

Not For Profit Organisations

Q1. Calculate the amount of subscriptions to be shown in Income and Expenditure A/c. for the year 2006-07.

Subscriptions received in 2006-07

2005-06 - Rs. 10,000

2006-07 - Rs. 90,000

2007-08 - Rs. 8,000 1,08,000

Subscriptions Outstanding for 2005-06 Rs. 15,000

Subscriptions outstanding for 2006-07 Rs. 20,000

Subscriptions received in advance in 2005-06 for 2006-07 Rs. 13,000

2007-08 Rs. 4,000

Ans.

Income a Expenditure A/c

for the year ended 31 march 2007

Expenditure Rs. Income Rs.By Subscriptions 90,000Add : Outstanding for 06-07 20,000Add : Adv. For 06-07 13,000 1,23,00

0

Q2. Calculate the amount of Subscriptions to be shown in Income a Expenditure A/c for the year ended 31 March 2007.

Subscriptions received during 2006-07

For 2005-06 Rs. 5,000

For 2006-07 Rs. 30,000

For 2007-08 Rs. 6,000 41,000

Additional Information

(i) Subscriptions outstanding on 31 march 2006 Rs. 6,000

(ii) Subscriptions outstanding on march 31 2007 Rs. 5,000

(iii) Subscriptions received in advance on march 31, 2006 Rs. 6,000

Solution

Income & Expenditure A/c for the year ended 31 march 2007

Expenditure (Dr.)Rs. Income (Cr.)Rs.By Subscriptions 30,000Add : Outstanding for 2006-07 4,000(5,000-1,000)Add : Advance for 2006-07 6,000

40,000

Q3. Show how would you deal with the following items appearing in the books of a not for profit organisations :

Rs.

(a) Receipts from Tournament Fund 15,000

Tournament Expenses 7,000

(b) Prize Fund 40,000

Prize Fund Investments 40,000

Donations for prize fund 20,000

Income from prize fund Investments 5,000

Prizes awarded 10,000

Interest accrued on prize fund Investments 2,000

Solution (a)

Balance Sheet

Liabilities Rs. Assets Rs.Tournament Fund (15,000)

(-) Tournament Expenses (7,000) 8,000

Balance Sheet

Liabilities Rs. Assets Rs.Prize Fund 40,000 Prize Fund Investments 40,000(+) Donations for Prize fund 20,000

Accrued Interest 2,000

(+) Income fromPrize fund Investments 5,000

(-) Prizes Awarded (10,000)(+) Accrued Interest on Prize Fund Investments 2,000 57,000

Q4. On the basis of the following information calculate the amount that will appear against the item stationery Account, in the income a expenditure A/c for the year ended 31 march 2011

As at 01.04.2010

As at 31.03.2011

Creditors for stationery 4,600 11,800

Stock of stationery 15,000 30,400

During 2010-11, the payment made to the creditors amounted to Rs. 56,800. Some stationery were purchased on cash, which was 20% of the total purchase of stationery.

Solution

Income a Expenditure A/c

Expenditure Rs. Income Rs.To Stationery purchasedCash 64,000Credit 16,000 80,000(+) Opening Stock 15,000(-) Closing Stock 30,400

64,600

Creditors for Stationery A/c

Particulars Rs. Particulars Rs.To Cash A/c 56,800 By balance 4,600

By Purchase 64,000To balance aid 11,800 (Balancing Figure)

68,600 68,600

Credit Purchase Rs. 64,000

Cash Purchase = 20% of Total Purchase

Let Total Purchase = x

∴

Cash Purchase =

20 1

100 5x x× =

Total purchases = cash purchase + Credit purchase

So

164,000

5x x+ =

464,000

5x =

80,000x = (Total Purchases)

Cash Purchase = 80,000 - 64,000 = 16,000

Q5. Following is the Receipt and Payments Account of Sun Shine club for the year ended 31 December 2010

Receipts Rs. Payments Rs.Balance bld. 7,250 Salary 12,500Subscriptions 81,750 Stationery 1,700Donations 3,000 Electricity Charges 9,550Grant from Government 15,000 Insurance 7,500Sale of Newspapers 300 Equipments 30,000Proceeds of Charity Show 16,500 Petty Expenses 500Interest on Investments 7,000 Expenses on Charity Show 12,900(@ 10% for full year) Newspapers 1,000Sundries Income 400 Lecturers Fees 16,500

Honorarium to Secretary 12,000balance bld. 27,050

1,31,200 1,31,200

Additional Information

01.01.2010 31.12.2010Rs. Rs.

Outstanding Salary 1,200 1,800Insurance Prepared 700 300Subscriptions Outstanding 3,750 2,500Subscriptions Received in Advance 1,750 1,000Electricity Charges Outstanding - 1,250Stock of Stationery 2,250 700Equipments 25,600 50,200Buildings 1,20,000 1,14,000

Prepare Income & expenditure A/c for the year ended 31 Dec. 2010 & Balance Sheet as on that date.

Solution

Income & Expenditure A/c of Sun Shine Club for the year ended 31 Dec. 2010Dr. Cr.

Expenditure Rs. Income Rs.To Salary 12,500 By Subscriptions 81,750Add : Outstanding of the end 1,800 Add : Outstanding at the end 2,500Less : Outstanding the Beg. (1,200) 13,100 Less : Outstanding (3,750)To Stationery 1,700 in the BeginningAdd : Opening Stock 2,250 Add : Advance at Beginning 1,750Less : Closing Stock (700) 3,250 Less : Advance at End (1,000) 81,250To Electricity Charges 9,550 By Donations 3,000Add : Outstanding at the End 1,250 10,800 By Grant from Government 15,000To Petty Expenses 500 By Sale of Newspapers 300To Insurance 7,500 By Proceeds of charity show 16,500Add : Prepaid in the Beginning 700 By interest on Investments 7,000Less : Prepaid at the end (300) 7,900 By Sundries Income 400To Expenses on Charity Show 12,900To Newspapers 1,000To Lectures Fees 16,500To Honorium to Secretary 12,000To depreciation on Equipments 5,400To Depreciation on Buildings 6,000To Surplus 34,100

1,23,450

1,23,450

Balance Sheet

as in 31.12.2010

Liabilities Rs. Assets Rs.Outstanding Salary 1,80 Insurance Prepaid 300Subscriptions received in advance 1,000 Subscriptions Outstanding 2,500Electricity Charges Outstanding 1,250 Stock of Stationery 700Capital Fund 2,23,600 Equipment 50,200Add : Surplus 34,100 2,60,700 Buildings 1,14,000

Investments 70,000Cash 27,050

2,64,750 2,64,750

Balance Sheet as on 01.01.2010

Liabilities Rs. Assets Rs.Outstanding Salaries 1,200 Insurance Prepaid 700Subscriptions received in Advance 1,750 Subscriptions Outstanding 3,750Capital Find (Balancing Figure) 2,26,600 Stock of Stationery 2,250

Equipments 25,600Buildings 1,20,000Cash 7,250Investments 70,000

2,29,550 2,29,550

Value of Investments =

7,000 100

7

×

Depreciation on Equipments = 25,600 + 30,000 - 50,200

= Rs. 5,400

Depreciation on Buildings = 1,20,000 - 1,14,000

= Rs. 6,000

Q6. Following is the Receipt and Payments account of cricket club for the year ended 31 March, 2008

Receipt & Payments A/c

Receipts Rs. Payments Rs.To balance bld 1,82,000 By Salaries 1,66,000To Subscriptions 1,80,000 By Stationery 32,000To Tournament Fund 1,64,000 By Rent 48,000To Interest (Investments) 65,000 By Telephone Expenses 8,000To Donations 1,12,000 By Sports material 78,000To Sale of Concert Tickets 2,47,000 By 6% Investments 5,00,000

By Miscellaneous Expenses 24,000By Concert Expenses 58,000By balance 36,000

9,50,000 9,50,000

Following additional information is provided :

(i) Subscriptions include Rs. 12,000 for 2006-07 and Rs. 18,000 for 2008-09.

(ii) Stock of Stationery on 31 march 2007 and 2008 was Rs. 7,200 and Rs. 5,400 respectively.(iii) Stock of Sports material in the beginning and at the end of the year was Rs. 12,000 and Rs. 21,000 respectively.

(iv) Rent include Rs. 4,000 paid for march 2007. Rent of march 2008 is outstanding.

(v) Telephone expenses include Rs. 3,000 as quarterly rent up to 31 may, 2008.

(vi) The value of Buildings on 31 march 2007 was Rs. 8,00,000 and is to be depreciated by 10%.

(vii) The value of Investments on 31 march 2007 was Rs. 10,00,000 and the club made similar additional Investments during the year on 1st October, 2007.

You are required to prepare the Income & Expenditure Account of the club for the year ended 31st march, 2008.

Solution

Income & Expenditure A/c for the year ended 31st march, 2008

Dr. Cr.

Expenditure Rs. Income Rs.To Salaries 1,66,000 By Subscriptions 1,80,00

0To Stationery 3,200 Less : Subscriptions for

Add : Opening Stock 7,200 2006-07 12,000

Less : Closing Stock (5,400) 33,800 2008-09 18,000 (30,000) 1,50,000

To Rent 48,000 By interest on Investments 65,000

Less : Paid for march 2007 (4,000) Add : Accrued Interest 10,000 75,000

Add : Outstanding for march 08 4,000 48,000 By Sale of Concert Tickets 2,47,000

To Telephone Expenses 8,000 Less Concert Expenses (58,000) 1,89,000

Less : Prepaid (3,000 x) (2,000) 6,000 By Donations 1,12,000

To Sports Materials 78,000

Add : Opening Stock 12,000

Less : Closing Stock 21,000 69,000

To Miscellaneous Expenses 24,000

To Depreciation on Buildings 80,000

To Surplus 99,200

5,26,000 5,26,000

Working Notes :

Calculation of Interest on InvestmentsRs.

610,00,000

100× = 60,000

6 65,00,000

100 12× × = 15,000

Total Interest earned 75,000

Less : Interest received 65,000

Accrued Interest 70,000

Q7. From the following Receipt & Payment A/c of Royal club show how Subscriptions would appear in Income & Expenditure A/c for the year ended 31st march 2011 and in Balance Sheet as at that date.

Receipt & Payments A/c

Dr. Cr.

Receipts Rs. Payments Rs.To Subscriptions2009-2010 5,0002010-2011 25,0002011-2012 4,000 34,000

Additional Information :

Club has 300 members each paying an annual subscription of Rs. 100. Subscriptions received in advance in 2009-10 for 2010-11 were Rs. 2,000 and for 2011-12 Rs. 1,000.

Subscriptions Outstanding as on 31 March 2010 were Rs. 6,000

SolutionIncome & Expenditure A/c

Dr. Cr.

Expenditure Rs. Income Rs.By Subscriptions 25,000Add : Received in advance for 2010-11 2,000Add : Outstanding for 2010-11 3,000 30,000

Balance Sheet as at 31 march 2011

Liabilities Rs. Assets Rs.Subscriptions received in advance

5,000

Subscriptions outstanding2009-10 1,0002010-11 3,000

4,000

Balance Sheet as at 31 march 2010

Liabilities Rs. Assets Rs.Subscription in advance for

2009-10 1,0002010-11 3,000

3,000

Subscriptions Outstanding

6,000

* Likewise similar projects can be taken up by students.

Project Work in Commerce

GROUP PROJECT WORK IN BUSINESS STUDIES AND ACCOUNTANCY

.

Abstract

Project work has been part of curriculum of Business Studies for class XI and

in Accountancy for Class XII. From this session 2011-12 CBSE has introduced

project work in Accountancy for Class XI and Business Studies for class XII

(session 2012-13). But it has not been taken up as seriously and methodically

as it should be done to bring out desirable behavioral/constructive outcomes.

If planned and executed methodically it is a source of joyful learning and

brings a long lasting benefit.

In our classes, taking up Individual Projects are regular feature but Group

Projects have been neglected. Group projects should be taken up seriously for

desirable outcomes of Cooperative and Team Learning. The present write –up

gives you insights as to how this can be taken up and executed in the areas of

both Business Studies and Accountancy effectively.

Introduction

Project work is an important component of curriculum of Business Studies and

Accountancy. Let us first look at the prescribed components of the syllabi in these two

subjects before discussing how group projects can be used in the curriculum transaction.

WHY GROUP PROJECT WORK?

Group project work fulfils certain important educational objectives namely

1. It teaches the value of team work. Teamwork is very important for any

successful execution of group projects.

2. It develops Cooperative Learning.

3. It equips them with Leadership Skills.

4. It develops Communication Skills.

5. It develops the skill of Conflict resolution and managing disagreements.

6. It enables student of different abilities to work together to complete a

given task.

SUGGESTIVE STEPS IN GROUP PROJECT WORK

Group project work can be organized by taking the following steps:

1. Formation of Groups: These can be formed on any basis like on the basis of roll numbers, by student themselves out of their own choice, by common interest of students or on any other suitable basis.

2. Assignment of project to the group.

3. Project Planning: Formulation of Synopsis based on the selected theme of project

4. Making Group Leaders.

5. Assigning task and coordinating to members of the group by Group Leader.

6. Peer - review of the work.

7. Modification (if any) after the Peer -review.

8. Execution of the project and Finalization of Report Writing.

9. Presentation of results by the team and review by the teacher and the entire class.

10. Presentations by different Group Leaders.

* Selected good projects can be documented for future reference and can be placed in the library.

.

CURRICULUM

ACCOUNTANCY (CLASS XI)

Unit 12: Project Work (Any One) Periods- 22, Marks-10

1. Collection of Source Documents, Preparation of Vouchers, Recording of Transactions with the help of vouchers.

2. Preparation of Bank Reconciliation Statement with the help of given Cash book and Pass book.

3. Project Work on any Windows based Accounting package: Installing & starting the package, setting up a new Company, Setting up account heads, voucher entry, viewing and editing data.

ACCOUNTANCY (CLASS XII)

In this component of curriculum two units namely Ratio Analysis and Cash Flow

Statement are covered. It carries a weightage of 20 marks break up of which is as

under:-

1. Marks for Report File = 04

2. Marks for Viva = 04

3. Written examination = 12

I BUSINESS STUDIES CLASS XI 10 Marks

The project work consists of Projects such as:

1. Auxiliaries to Trade: Find out the names of five companies each related to

different auxiliaries, i.e. Banking, Insurance, Warehousing, Transportation,

Communication and Advertising from real life.

2. Cooperative Society: Find out names of five different types of Co-operative

Societies around you. Also give details of business activities of any one of

them.

3. Private, Public and Global Enterprises: Give five names each of different

types of Public Sector enterprises (including all 3 types), Global enterprises,

Joint Ventures and Public Private Partnerships. Also give details of business

activities of any one of them.

4. Banking-SB Account: Visit a nearby bank to find out the procedure for

opening a Saving Bank Account. Collect the required documents and prepare a

report on the same.

5. Banking-Remittance: Visit a bank and remit Rs. 100 to any of your

relatives. Write the formalities completed by you for the same.

6. E-Banking: Write the procedure for transferring funds through RTGS or NEFT.

7. External Trade: Imagine yourself to be an exporter or importer. Collect

documents used in your trade. Fill them up and present in a file.

8. Insurance: Compare life insurance policies targeting children of any two

insurance companies.

9. Social Responsibilities: Select any two companies/firms and give an

account of the steps taken by them for discharging their social responsibilities.

II BUSINESS STUDIES- CLASS XII 10 MARKS

1. Consumer Protection File at least 10 complaints of consumer exploitation

of different types (defective goods and deficient services). Also, mention the

decisions thereof.

2. Marketing-Objectionable Advertisements: Collect information related to

five objectionable advertisements presented through any media and explains

the objections.

3. Marketing-Useful Advertisements: Collect five printed advertisements and

interpret their message.

4. Marketing-Physical Distribution: Observe the marketing plan of any two

companies and find the levels adopted by them for distribution of their

products.

5. Consumer Protection- Role of NGO’s: As a consumer, contact an NGO for

a complaint against any defective good or deficient service and report the

assistance provided by them.

6. Marketing- Sales Promotion: - Select any two famous firms/companies and

find out the sales promotion techniques generally adopted by them.

GROUP PROJECT WORK IN BUSINESS STUDIES

In Business Studies Project Work can be made very interesting if group

method is used. One of the benefits is that the group project work covers a

larger area. Let us take the example of group project work on Insurance. The

work can be assigned to the group as under to cover the following topics

assigning one to each member of the group:-

1. General Principles of Insurance and need for Insurance

2. Life Insurance: - Types of life insurance policies and their salient

features.

3. Comparison of policies offered by LIC and other companies.

4. Fire Insurance

5. Marine Insurance

6. Careers in Insurance Industry

7. Role of IRDA (Insurance Regulatory and Development Authority) in

regulating and promoting Insurance business in India.

8. Insurance Planning for a family: - How much Insurance does one

need and how to decide on the same for different types of

Insurance -Life and General.

It is evident that this group project will cover nearly all aspects of

Insurance. When the project is presented to the entire class is

done then it should result in a fairly comprehensive understanding

of the topic.

GROUP PROJECT WORK IN ACCOUNTANCY

In accountancy also group project work can result in all the benefits listed above.

Let us take an example of ‘COLLECTION OF SOURCE DOCUMENTS, PREPARATION

OF VOUCHERS AND RECORDING OF TRANSACTIONS WITH THE HELP OF

VOUCHERS’. The task can be divided among the students as under:-

1. Collection of source documents related to Bank like Pass book,

pay in slips and cheques etc.

2. Collection of other source documents like cash memos,

Invoices, debit note, credit notes, railway receipts and delivery

challans etc.

3. Collection of blank accounting vouchers- debit voucher, credit

voucher and transfer vouchers

4. Model transactions of banks on source documents.

5. Model transactions on other source documents like cash

memos. Invoices, debit and credit notes.

6. Preparation of accounting vouchers based on source

documents.

7. Recording of transactions based on accounting vouchers.

Thus we can notice that seven students can be assigned tasks in this group project. More students can be associated with presentation of the results and class discussion at that stage. This will result in constructivist and experiential learning where the students would be benefitted the most.

PRECAUTIONS TO MAKE GROUP PROJECT WORK SUCCESSFUL

Students get many benefits when working in groups. But it is also essential to take some

steps to make the group project work successful. Some of them are:-

1. Discuss the skills needed to work in groups with the students like listening skills, being tolerant to other members of the group and managing disagreements etc.

2. The method of grading the project should also be made clear to the students.

3. Give time to the members of groups to meet together and plan their work, discuss their roles etc. This will increase their cohesiveness and increase coordination.

4. If there are some problems in the group then they can be redesigned by transferring the students to other groups etc. This flexibility will increase group effectiveness.

5. If the group members develop enough understanding then they can be used or other constructivist curriculum transaction activities also like discussing a case study in Business Studies and presenting the solution in class, group tests and group problem solving etc. All this will make teaching learning process more joyful and effective.

EVALUATING AND GRADING A GROUP PROJECT

The work of each student needs to be assessed and also the work of a group as a whole

should be evaluated. This can be done by various ways and a combination thereof:-

1. Evaluation by peers i.e. group members.2. Evaluation by the students of the class when presentation of the project

and question answer session is taking place.3. Evaluation by the teacher.

*It would be good if grades are assigned by all the above three ways and a

cumulative grade is given based on the average of the three grades. This

process will make evaluation more objective and effective.

CONCLUDING NOTE

There should be no doubt in the minds of all stake holders that if group project work is

done in the ways described above it will result in effective curriculum transaction which

will make teaching learning process more joyful.

Be creative and think out of box while guiding students for taking up Group

Projects. Newspapers, Magazines, various Search Engines and other sources

will enable Teachers and Students to take up projects which expose them to

the World of Work which is the spirit behind National Curriculum Framework’

2005.

* Please communicate through email on address mentioned below the areas

where you need our academic intervention and support. We would appreciate

your valuable suggestions.

PROJECT WORK IN ACCOUNTANCY CLASS XI

Voucher –Based Approach in Accountancy

In Accountancy, it is for the first time that the Project work is introduced in class XI for 10 marks. Voucher Based Accounting can be a good project which will practically expose thestudents the importance of maintaining receipts and vouchers supporting the occurrence of business transactions and also how books of accounts are prepared with the help of these vouchers.

What is a Voucher?

Voucher is any document or evidence (e.g. receipts or bills) supporting the occurrence of any accounting transaction and it supports the authentic basis for preparing the book of accounts following the double entry system of accounting.

At this level, the accountancy teachers are required to help the students in the project in the following ways:

1. By providing knowledge to the students about Accounting Process,2. Give the imaginary transactions data.3. Show the original Source Document (Which is easily available).4. Training the students for preparing vouchers.5. Show and demonstrate the students how to record transaction from vouchers.6. To motivate and guide students to collect various Source Documents.7. To encourage students to prepare books of accounts with the help of vouchers.

So, the commerce teachers play an important role in preparation of project in class XI . The teacher may provide various transactions to the students. Some examples of transactions are given below:

Ayan started business under the name AYAN & BROTHERS at NOIDA on April 1, 2011 to deal in Books and Stationary material. He introduced `Rs. 5, 00,000 as capital out of which ` Rs. 1, 00,000 was in cash and balance by cheque. He enclosed the original papers relating to his business transactions for the month of April, 2011.

Students should analyze the transaction on the basis of these papers and process the information through-

Various stages of accounting cycle.

Preparation of vouchers for each financial transaction.

Recording in the journal & subsidiary books.

Posting them into ledger & balancing.

Preparing Trial Balance.

Preparing Final Accounts on the basis of Trial Balance made.

* Based on the vouchers of M/s. AYAN & BROTHERS, the preparation of the Books of Accounts using the vouchers are given in the in the PART –II, Microsoft Excel Sheet . You are requested to go through the process consulting the exemplar GIVEN IN PART –II (Project based on Voucher Based Approach in Accounting), and guide students to collect the vouchers from different source of various companies and try to formulate and execute the project on the same.