Embed Size (px)

Citation preview

Sustainability – driven by Supplier Management

Jan Grönvall

26th of March 2014 @ CIPS

JG/26 March 2014

JG/26 March 2014 / 2

THE MOST POWERFUL

BUSINESS WOMAN

HELENA HELMERSSON

owns the most important

“future issue” in the

largest company on the

stock exchange

JG/26 March 2014 / 3

Head of Sustainability at H&M

THE MOST POWERFUL

BUSINESS WOMAN

HELENA HELMERSSON

owns the most important

“future issue” in the

largest company on the

stock exchange

JG/26 March 2014 / 4

“You are what you talk”

Who in your company is on stage when the subject

is sustainability?

Maybe we all have to take a bigger responsibility

here?

JG/26 March 2014 / 5

JG/26 March 2014 / 6

JG/26 March 2014 / 7

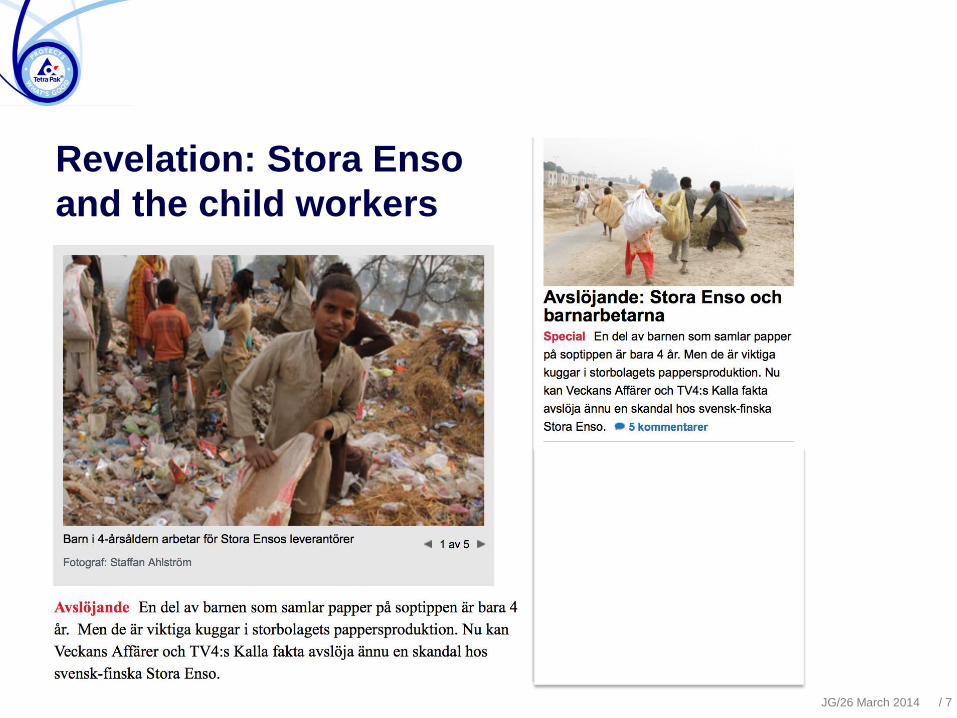

Revelation: Stora Enso

and the child workers

Questions to ask ourselves

How far up the supply chain does our responsibility go?

Do we do enough to protect our brands – and the world?

Is NOT sourcing in your biggest market sustainable?

…. etc.

JG/26 March 2014 / 8

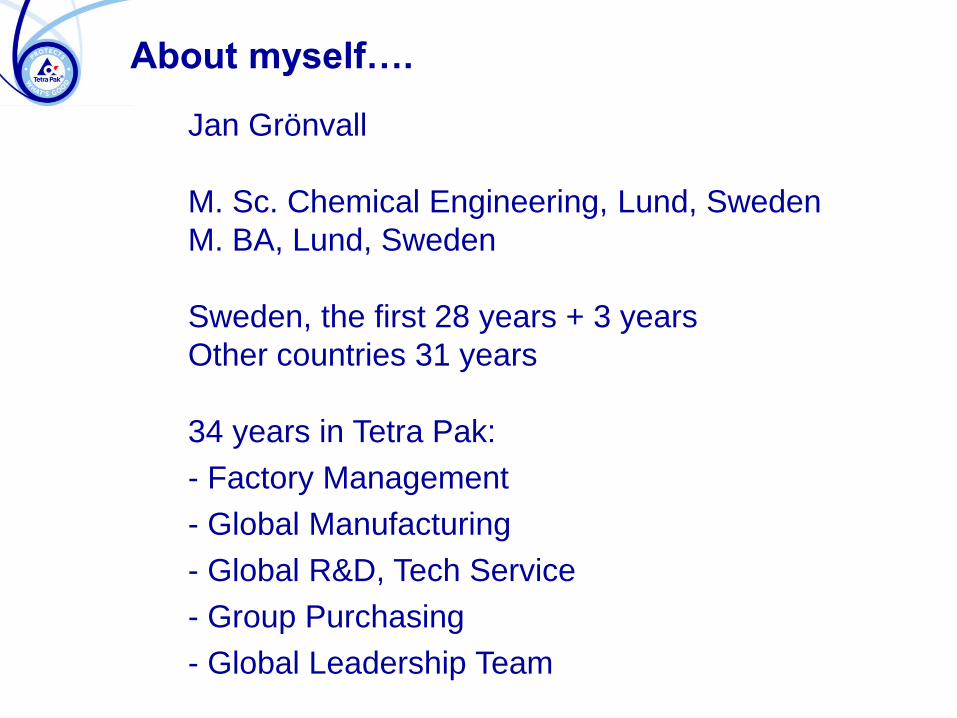

About myself….

Jan Grönvall

M. Sc. Chemical Engineering, Lund, Sweden

M. BA, Lund, Sweden

Sweden, the first 28 years + 3 years

Other countries 31 years

34 years in Tetra Pak:

- Factory Management

- Global Manufacturing

- Global R&D, Tech Service

- Group Purchasing

- Global Leadership Team

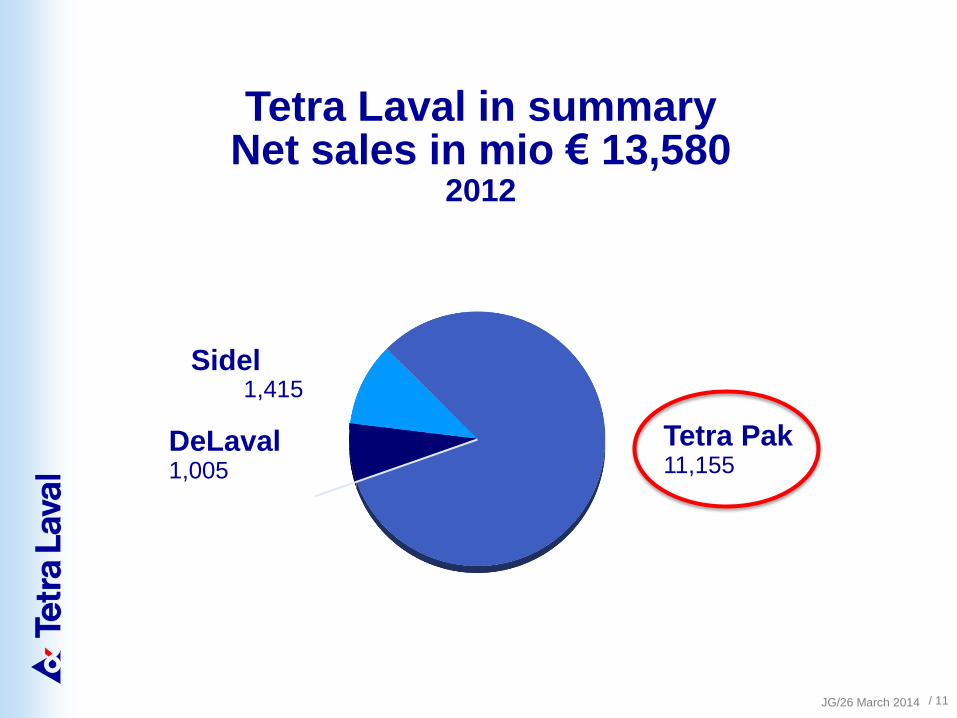

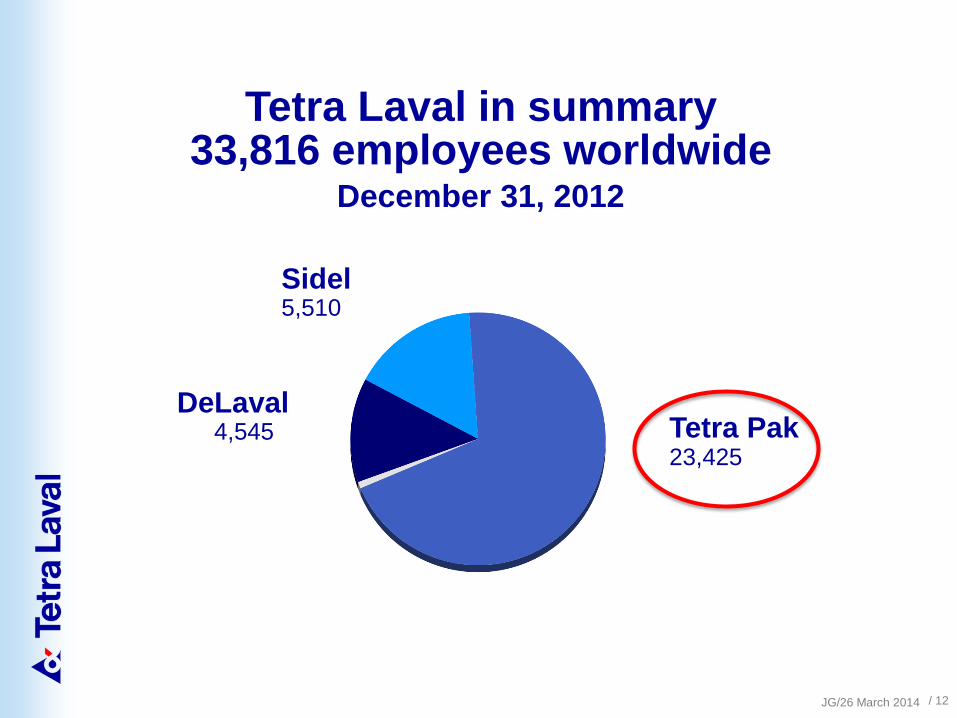

This is Tetra Pak

JG/26 March 2014

Tetra Pak 11,155

DeLaval 1,005

Sidel 1,415

Tetra Laval in summary Net sales in mio € 13,580

2012

/ 11 JG/26 March 2014

Tetra Pak 23,425

DeLaval 4,545

Sidel 5,510

Tetra Laval in summary 33,816 employees worldwide

December 31, 2012

/ 12 JG/26 March 2014

Ruben Rausing, founder of Tetra Pak

“A package should save more than it costs”

/ 13 JG/26 March 2014

1952, Lund, Sweden

The first delivery to a customer

/ 14 JG/26 March 2014

Packaging Solutions 9.9 bio €

Processing Solutions 1.3 bio €

11.2 bio € in total net sales 2012 Two distinct and complementary businesses

Product diversification – on standardized technology platforms

JG/26 March 2014 / 16

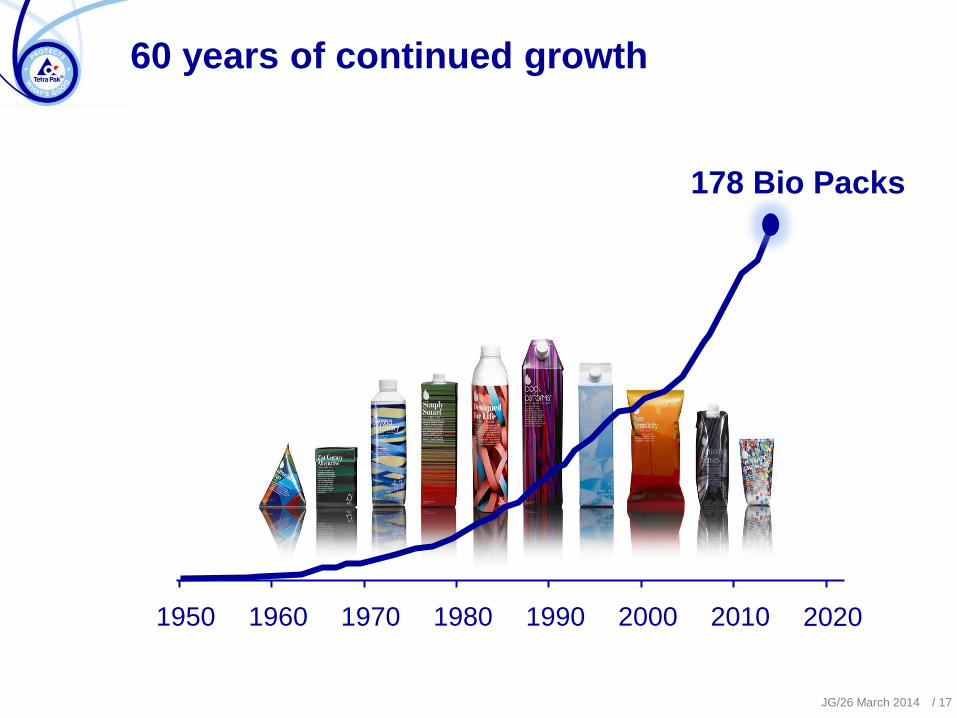

60 years of continued growth

1950 1960 1970 1980 1990 2000 2010 2020

178 Bio Packs

JG/26 March 2014 / 17

• Customers in 172 countries

• 45 packaging material plants

• Deliveries 2013:

• 178 billion packs

• 576 Filling/Packaging Machines

• 1800 Distr. Machines

• 2000 Processing systems

Tetra Pak is global and works locally

JG/26 March 2014 / 18

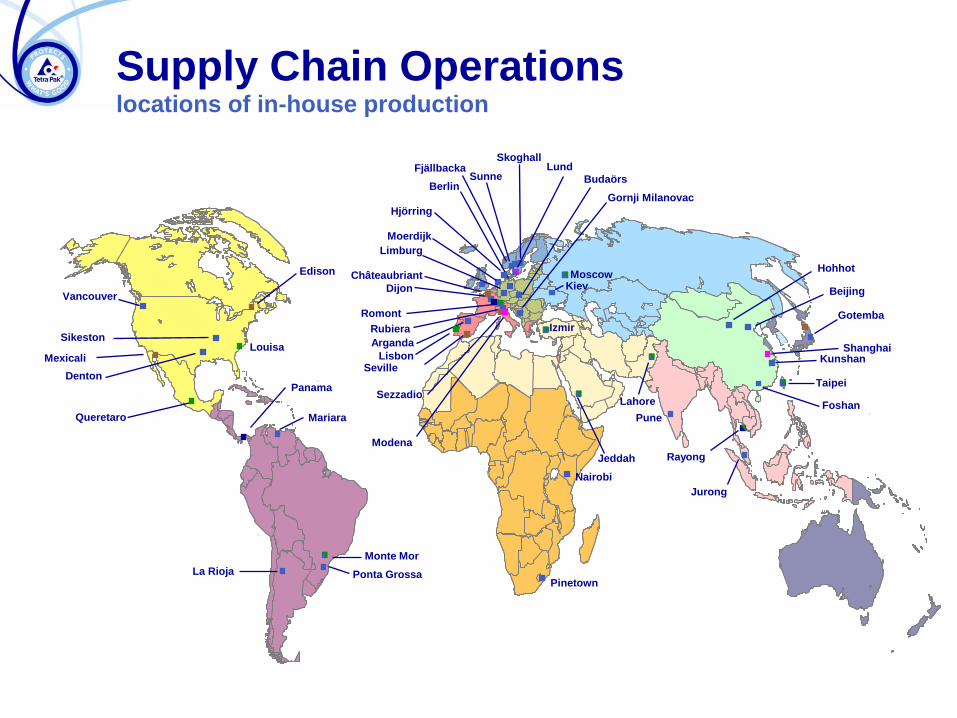

Queretaro

Denton

Mariara

Vancouver

Sikeston

Ponta Grossa

Monte Mor

La Rioja

Skoghall

Sunne

Limburg

Moerdijk

Berlin

Dijon

Romont

Rubiera

Arganda

Nairobi

Lund

Pinetown

Jeddah

Pune

Budaörs

Izmir

Lahore

Kiev Moscow

Gornji Milanovac

Taipei

Beijing

Gotemba

Kunshan

Jurong

Foshan

Hohhot

Supply Chain Operations locations of in-house production

Hjörring

Fjällbacka

Rayong

Lisbon Louisa

Mexicali

Edison

Seville

Sezzadio

Châteaubriant

Shanghai

Modena

Panama

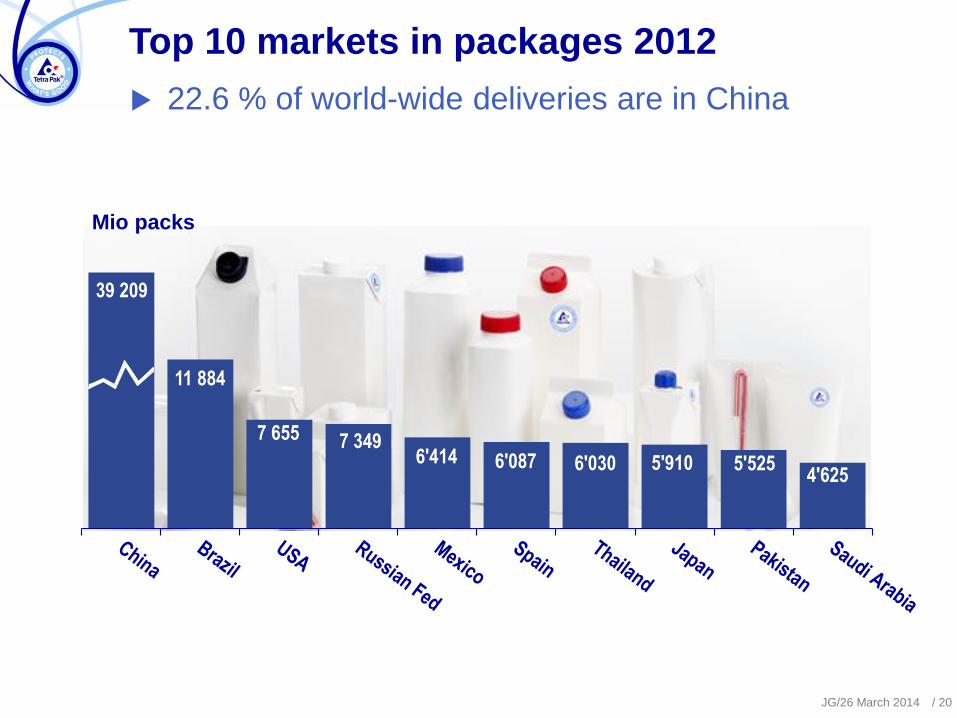

39 209

11 884

7 655 7 349 6'414 6'087 6'030 5'910 5'525

4'625

22.6 % of world-wide deliveries are in China

Top 10 markets in packages 2012

Mio packs

JG/26 March 2014 / 20

Sustainability for Tetra Pak

Environmental

Economical

Social Responsibility

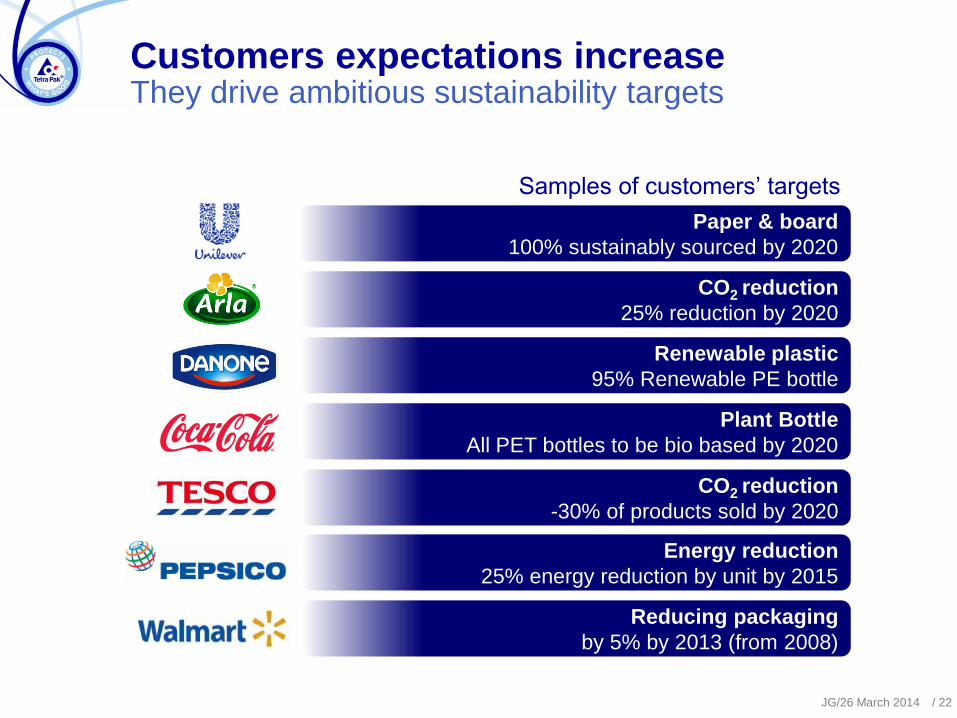

They drive ambitious sustainability targets Customers expectations increase

Plant Bottle

All PET bottles to be bio based by 2020

CO2 reduction

25% reduction by 2020

CO2 reduction

-30% of products sold by 2020

Paper & board

100% sustainably sourced by 2020

Energy reduction

25% energy reduction by unit by 2015

Renewable plastic

95% Renewable PE bottle

Reducing packaging

by 5% by 2013 (from 2008)

Samples of customers’ targets

JG/26 March 2014 / 22

Sustainability for Tetra Pak

Environmental

Economical

Social Responsibility

- Beverage Carton

- Plastic

- Other

Competitors

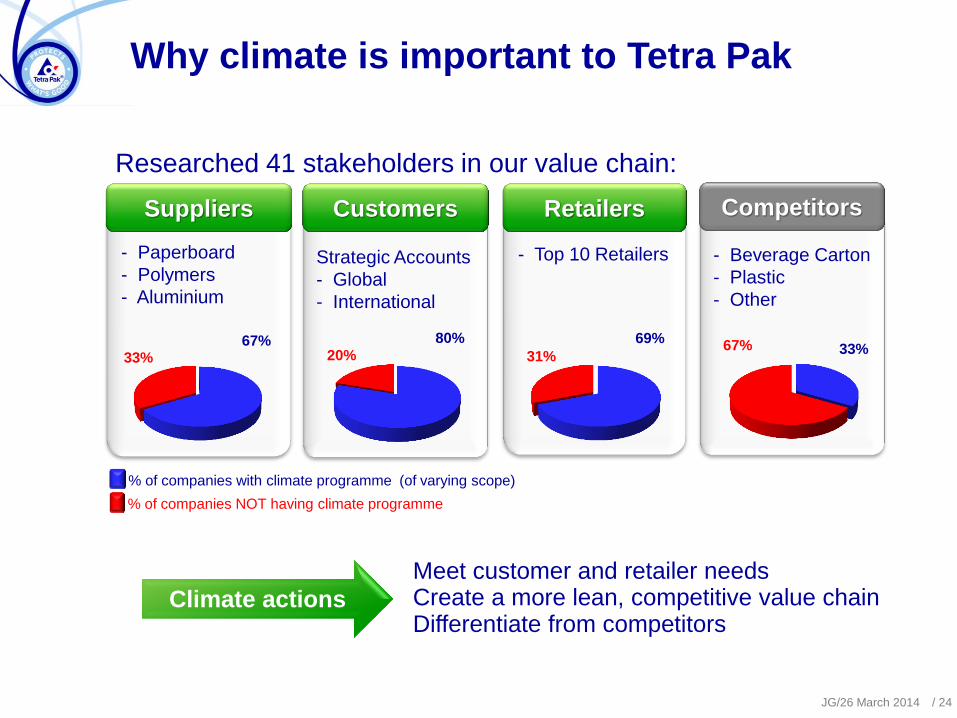

Why climate is important to Tetra Pak

Meet customer and retailer needs Create a more lean, competitive value chain Differentiate from competitors

Researched 41 stakeholders in our value chain:

- Paperboard

- Polymers

- Aluminium

Strategic Accounts

- Global

- International

- Top 10 Retailers

Customers Retailers Suppliers

67% 33%

33% 67% 69%

31%

80%

20%

% of companies with climate programme (of varying scope)

% of companies NOT having climate programme

Climate actions

JG/26 March 2014 / 24

Tetra Pak early mover to drive environmental performance

1970s 1980s 1990s 2000s

1-way vs. returnables

Waste efficient

Energy recovery Efficiency

LCA

Factory emissions

Design for environment

Recycling

Environment reporting

Climate goal

LCA target setting

Partnering & commitments

JG/26 March 2014 / 25

1-way vs. returnables

Waste efficient

Energy recovery Efficiency

LCA

Factory emissions

Design for environment

Recycling

Environment reporting

Climate goal

LCA target setting

Partnering & commitments

Environment is a core driver of our business today

2010s

Raw materials

Transparency

Water

Food waste

Supply chain integration

Certification and labelling

JG/26 March 2014 / 26

Environment is a strategic priority for Tetra Pak

Sustainable, profitable growth

JG/26 March 2014 / 27

We have clear focus to drive environmental excellence

Reduce environmental footprint

across the value chain

Develop sustainable products

Increase recycling

Objectives

JG/26 March 2014 / 28

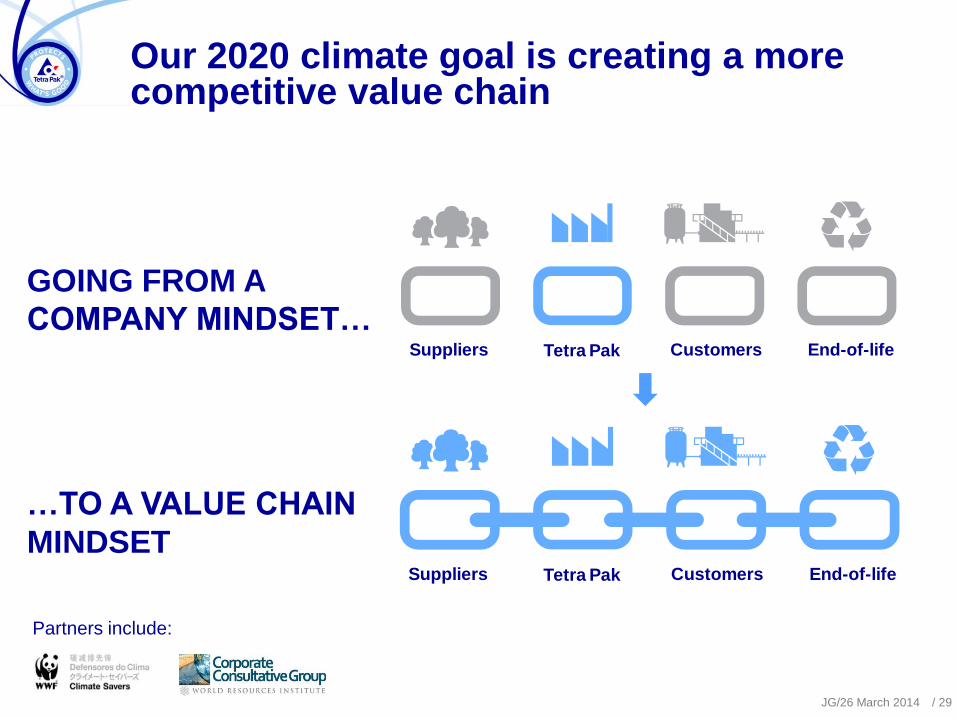

Tetra PakSuppliers Customers End-of-life

Our 2020 climate goal is creating a more competitive value chain

GOING FROM A

COMPANY MINDSET…

…TO A VALUE CHAIN

MINDSET

Tetra PakSuppliers Customers End-of-life

Partners include:

JG/26 March 2014 / 29

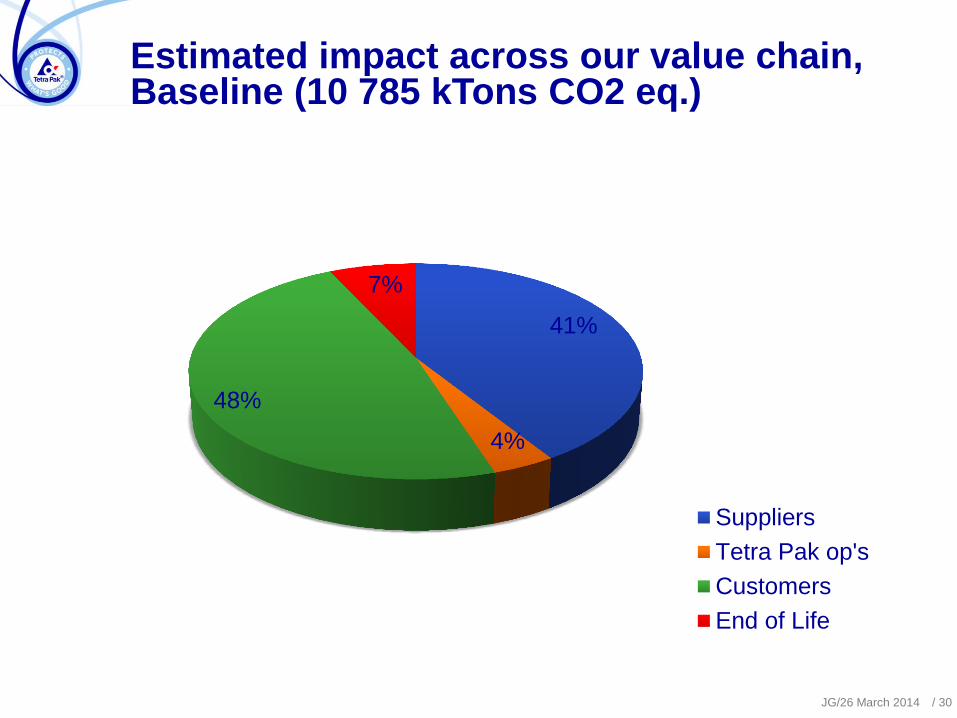

Estimated impact across our value chain, Baseline (10 785 kTons CO2 eq.)

41%

4%

48%

7%

Suppliers

Tetra Pak op's

Customers

End of Life

JG/26 March 2014 / 30

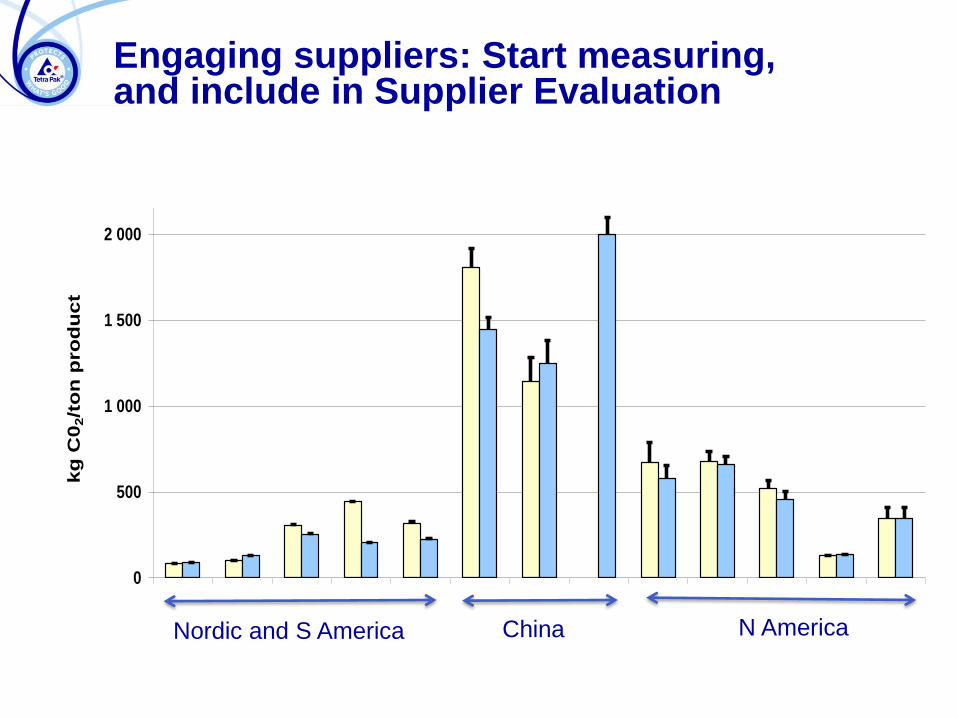

Engaging suppliers: Start measuring, and include in Supplier Evaluation

CO2 emission from suppliers

0

500

1 000

1 500

2 000

Kors

näs

Gäv

le

Kors

näs

Frö

vi

Sto

ra E

nso

Tainio

nko

ski

Sto

ra E

nso

Sko

ghall

Klabin

IP S

veto

gors

k

IP A

ugust

a

IP C

hin

a

Mea

dW

estv

aco E

vadale

Eve

rgre

en

Wey

erhae

use

r

Biller

ud

Potla

tch

kg

C0

2/t

on

pro

du

ct

2005 2010

T=extra emissions

due to higher

grammage than

benchmark

Nordic and S America China N America

What is needed to make it happen?

Buy less – innovation at Tetra Pak and at suppliers

Engage suppliers to improve their performance

Optimise supplier mix/volumes

But……Many paradoxes and dilemmas to work on − Shall we buy paperboard in China and USA?

− How can we get big polymer companies interested?

− Is the aluminium industry interested?

JG/26 March 2014 / 32

We have clear focus to drive environmental excellence

Reduce environmental footprint

across the value chain

Develop sustainable products

Increase recycling

Objectives Goals Objectives

2020 climate goal:

Cap climate impact across value

chain at 2010 levels

Renewable packaging goals:

100% FSC-certified paperboard,

A 100% renewable package

2020 recycling goal:

40% global recycling rate

JG/26 March 2014 / 33

FSC certification and stamp –on-pack Tetra Pak buys > 2 mio tons of board/year

FSC™ forest certification ensures responsible forest management

Key elements of the FSC forest certification scheme

- Forest Management (FM): = responsible forestry practices

- Chain of Custody (CoC) : = traceability from forest to store

- Logo/Trademark: = identifies certified products

- Control mechanisms: = certification and accreditation

FM certificate

CoC certificate

CoC certificate

FSC-labelled product

JG/26 March 2014 / 35

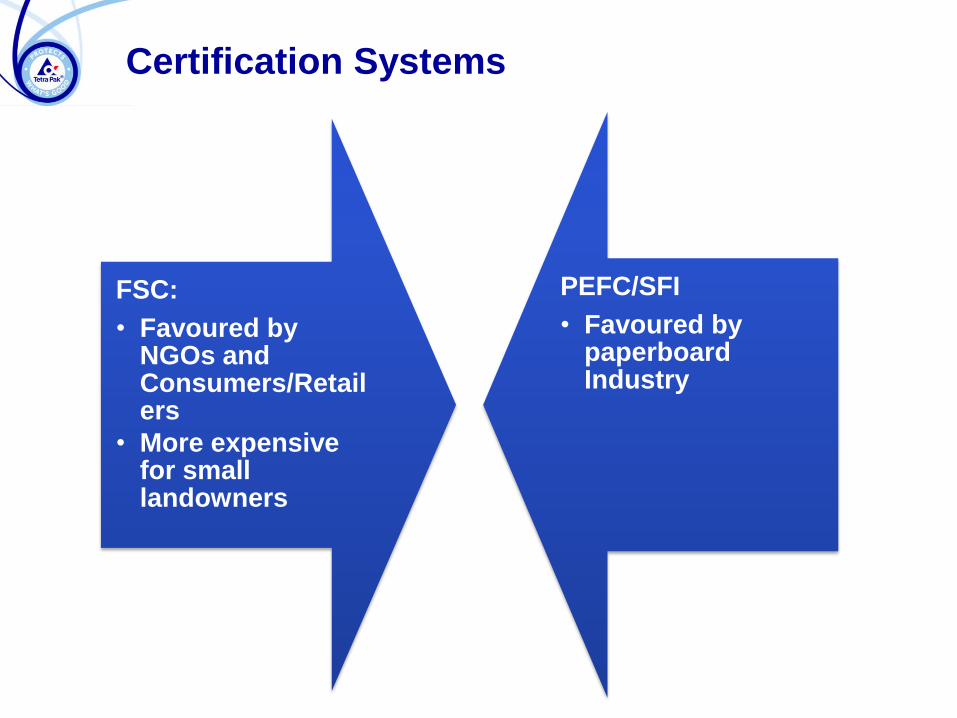

Certification Systems

FSC:

• Favoured by NGOs and Consumers/Retailers

• More expensive for small landowners

PEFC/SFI

• Favoured by paperboard Industry

JG/26 March 2014

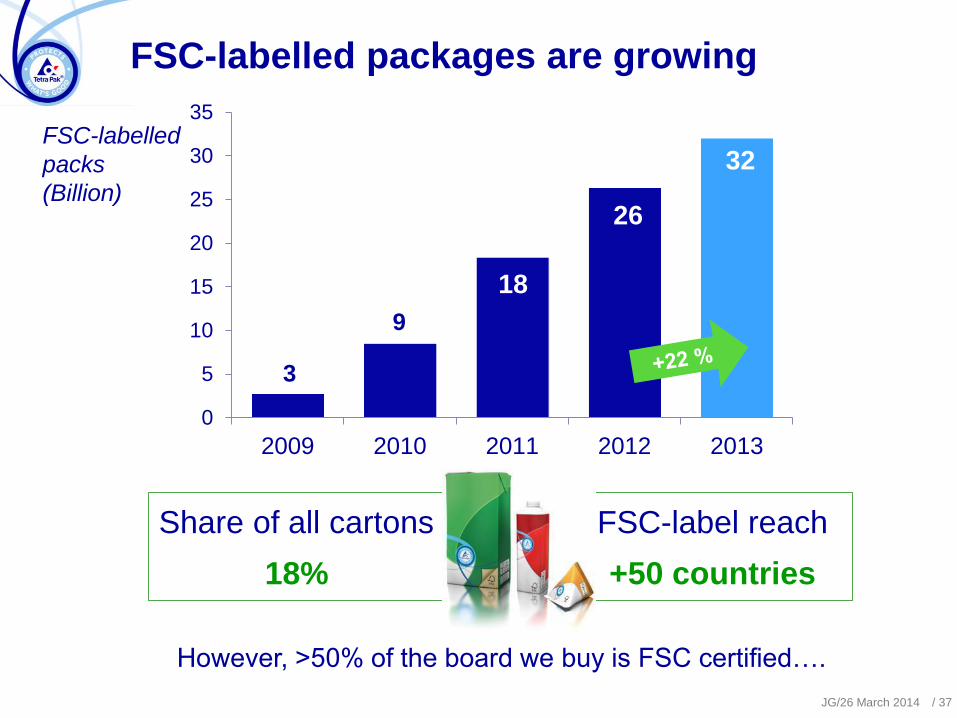

3

9

18

26

32

0

5

10

15

20

25

30

35

2009 2010 2011 2012 2013

FSC-labelled

packs

(Billion)

FSC-labelled packages are growing

Share of all cartons

18%

FSC-label reach

+50 countries

/ 37

However, >50% of the board we buy is FSC certified….

JG/26 March 2014 / 38

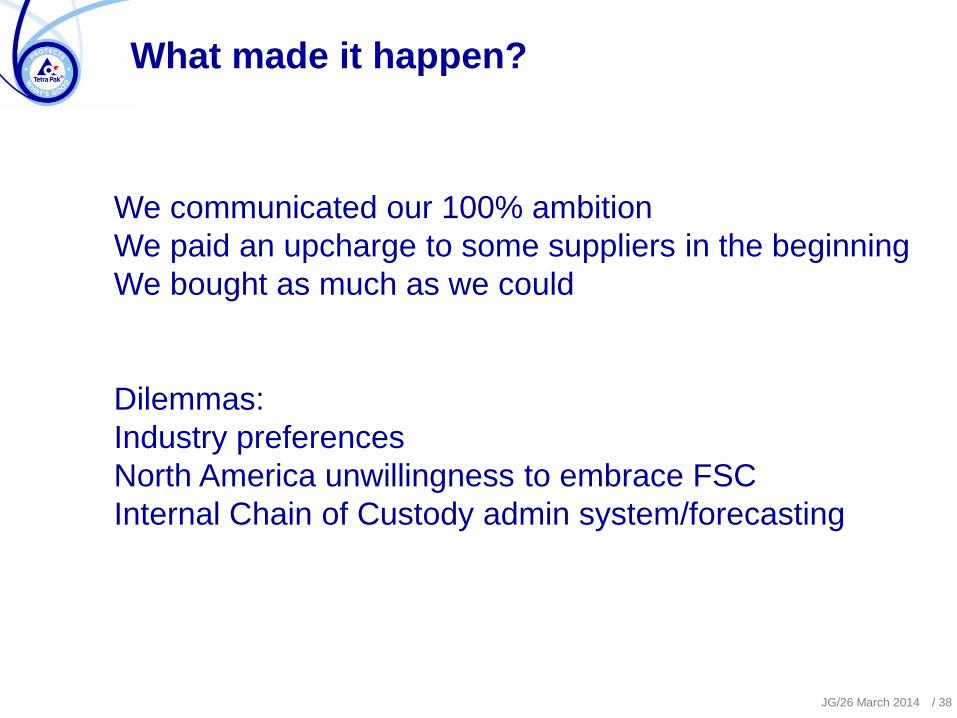

What made it happen?

We communicated our 100% ambition

We paid an upcharge to some suppliers in the beginning

We bought as much as we could

Dilemmas:

Industry preferences

North America unwillingness to embrace FSC

Internal Chain of Custody admin system/forecasting

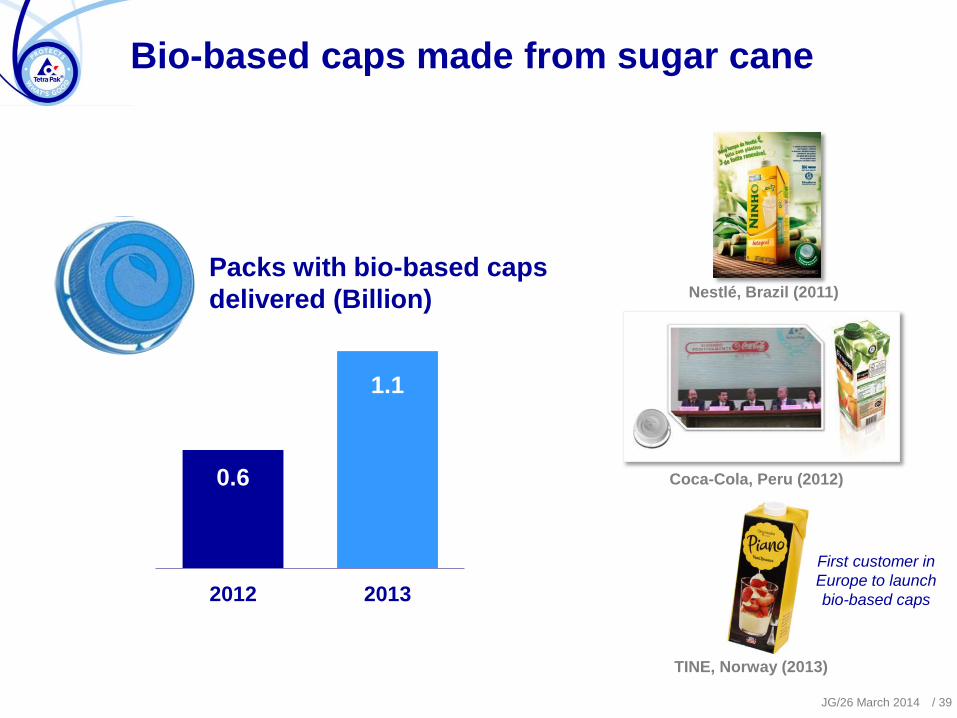

Bio-based caps made from sugar cane

Nestlé, Brazil (2011)

Packs with bio-based caps

delivered (Billion)

0.6

1.1

2012 2013

Coca-Cola, Peru (2012)

First customer in

Europe to launch

bio-based caps

TINE, Norway (2013)

JG/26 March 2014 / 39

We have clear focus to drive environmental excellence

Reduce environmental footprint

across the value chain

Develop sustainable products

Increase recycling

Objectives Goals Objectives

2020 climate goal:

Cap climate impact across value

chain at 2010 levels

Renewable packaging goals:

100% FSC-certified paperboard,

A 100% renewable package

2020 recycling goal:

40% global recycling rate

JG/26 March 2014 / 40

JG/26 March 2014

Recycling is not our own business…

Market …but it’s our business to make recycling work

/ 41

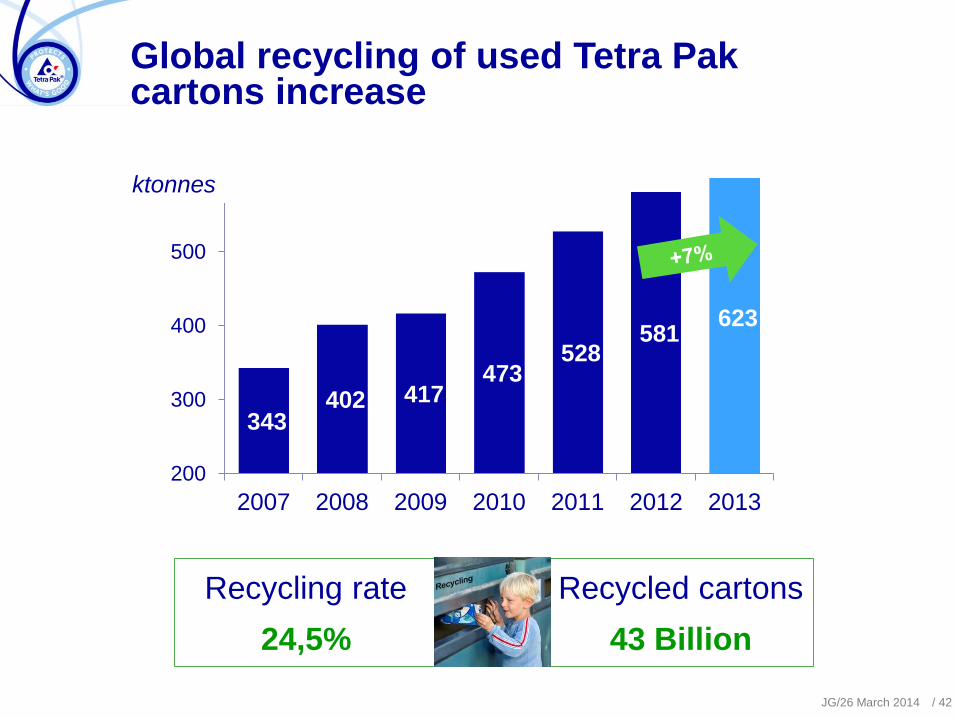

343 402 417

473 528

581 623

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013

ktonnes

Global recycling of used Tetra Pak cartons increase

Recycling rate

24,5%

Recycled cartons

43 Billion

JG/26 March 2014 / 42

Sustainability for Tetra Pak

Environmental

Economical

Social Responsibility

Customer focus & Long-Term

View

Symmetry & Balance

Trust & Mutual Advantage

Integrity & Respect

Openness & Responsiveness

Supplier Relation Cornerstones The Values

Economic sustainability

Be the best Customer

Mandatory procedure of how to manage Strategic Suppliers,

with the aim to have a long term relation

Short and medium term risk management

Risk Management

• Yearly process

• 6-weekly process to get early warnings

Assisting a supplier early is always cheaper

than doing it late – or too late

Sustainability for Tetra Pak

Environmental

Economical

Social Responsibility

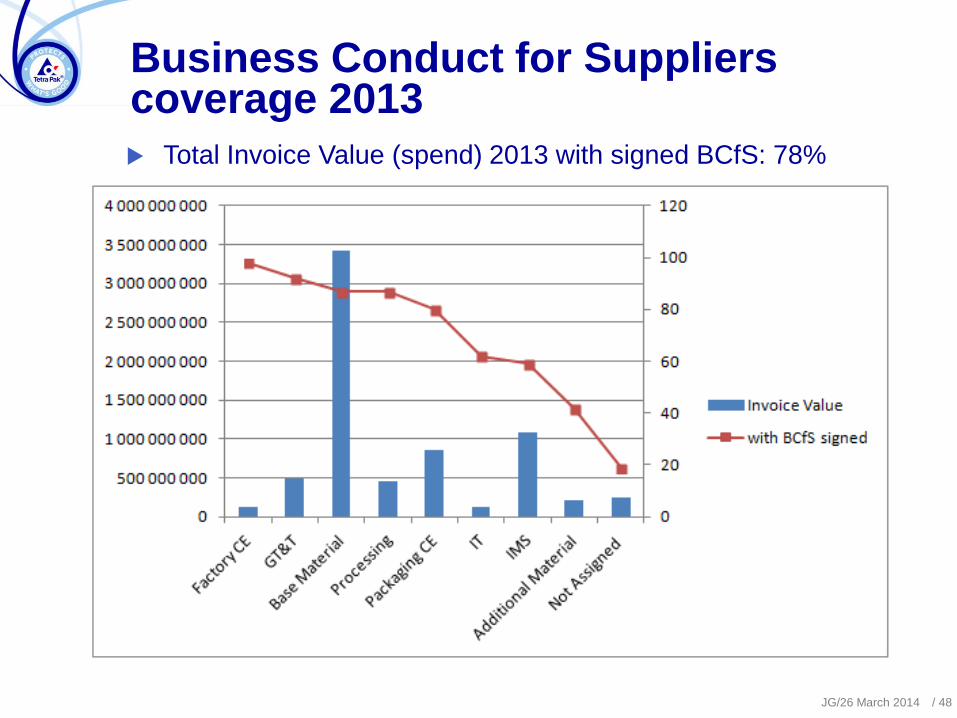

Business Conduct for Suppliers coverage 2013

Total Invoice Value (spend) 2013 with signed BCfS: 78%

JG/26 March 2014 / 48

We have many pieces in place

Policies, Business Code of Conduct, …

Self declaration and internal audits

Business Conduct for Suppliers

Risk management process and guideline

Training

x Verification

JG/26 March 2014 / 49

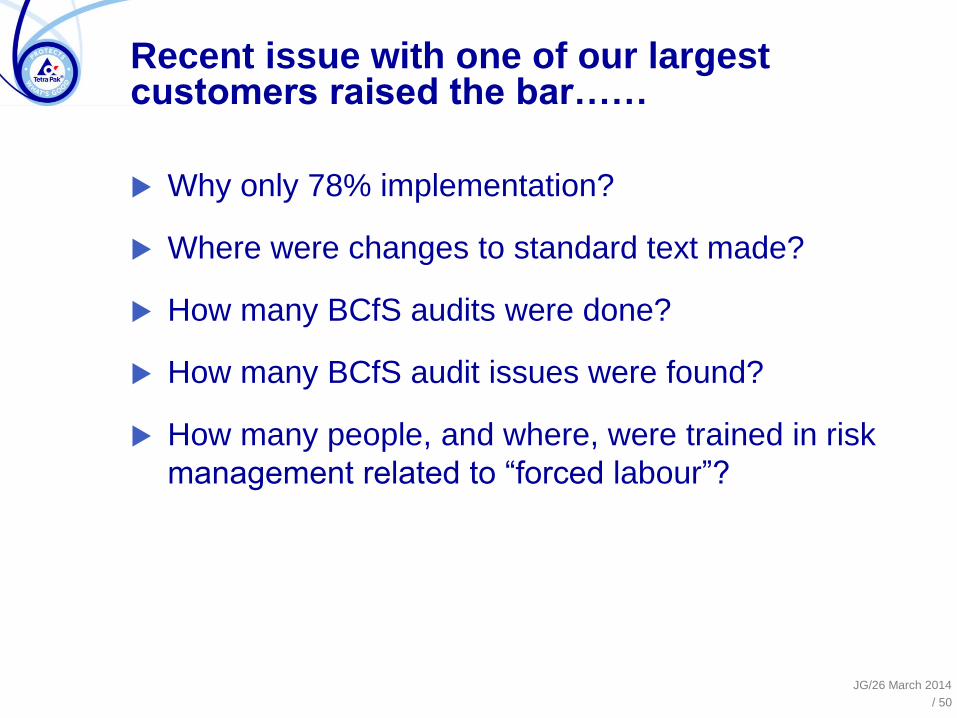

Recent issue with one of our largest customers raised the bar……

Why only 78% implementation?

Where were changes to standard text made?

How many BCfS audits were done?

How many BCfS audit issues were found?

How many people, and where, were trained in risk

management related to “forced labour”?

JG/26 March 2014

/ 50

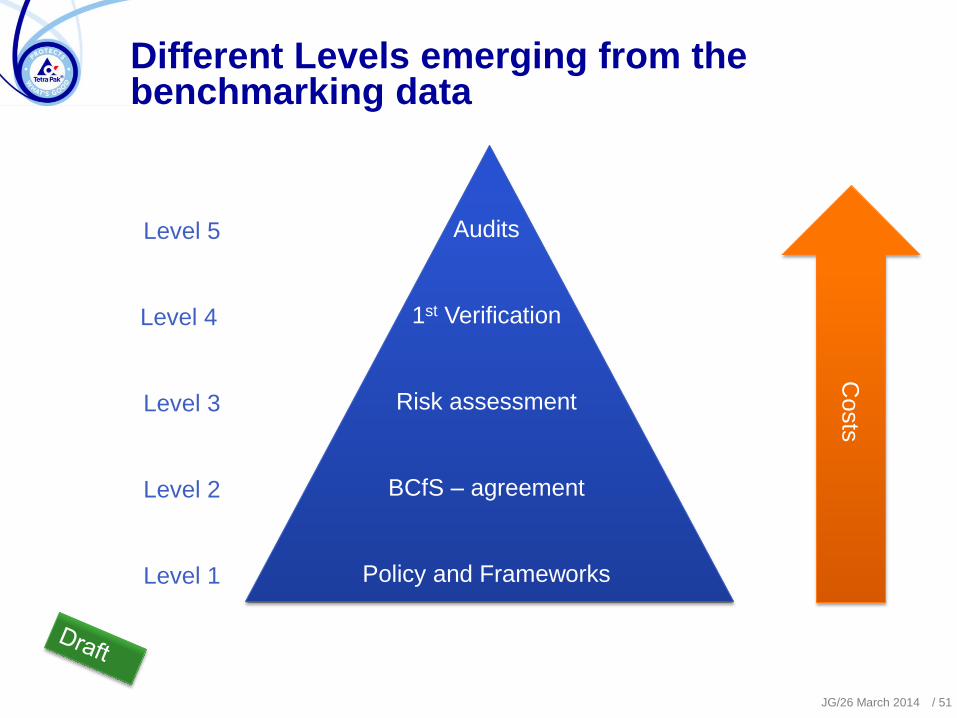

Different Levels emerging from the benchmarking data

JG/26 March 2014 / 51

Audits

1st Verification

Risk assessment

BCfS – agreement

Policy and Frameworks

Level 5

Level 4

Level 3

Level 2

Level 1

Costs

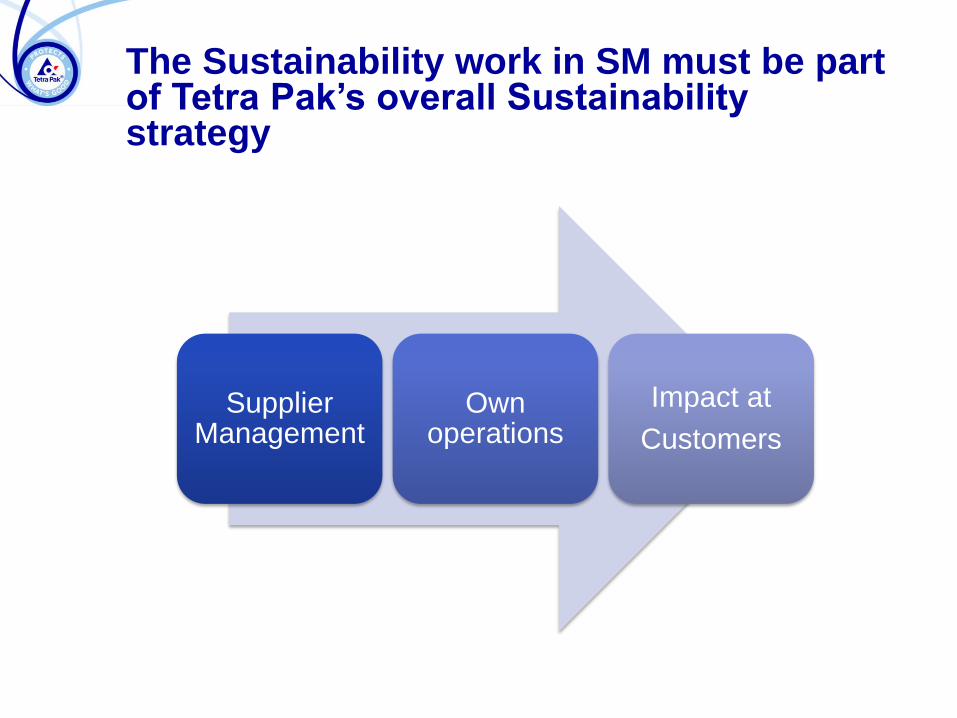

The Sustainability work in SM must be part of Tetra Pak’s overall Sustainability strategy

Supplier Management

Own operations

Impact at

Customers

Must do’s for sustainability in supplier management:

1. Supplier Management activities must be fully aligned

2. One voice to suppliers!

3. A clear Key Supplier Management role is needed to

coordinate all the activities with each supplier. “Common

agenda” - approach

4. Long term approach, with continuity.

5. There must be something in it for the supplier.

6. Suppliers must understand and be committed to their role in

our sustainability strategy.

7. The SM staff must be well selected and well trained, so that

they understand the big picture.

8. The performance must be measured.

JG/26 March 2014 / 53

We collaborate extensively with stakeholders to find the best solutions

Business partners

FSC

(Forest Stewardship

Council )

UN Global Compact

WWF

(on Forestry & Climate)

WRI

(World Resource

Institute)

Nutrition and feeding

JG/26 March 2014 / 54

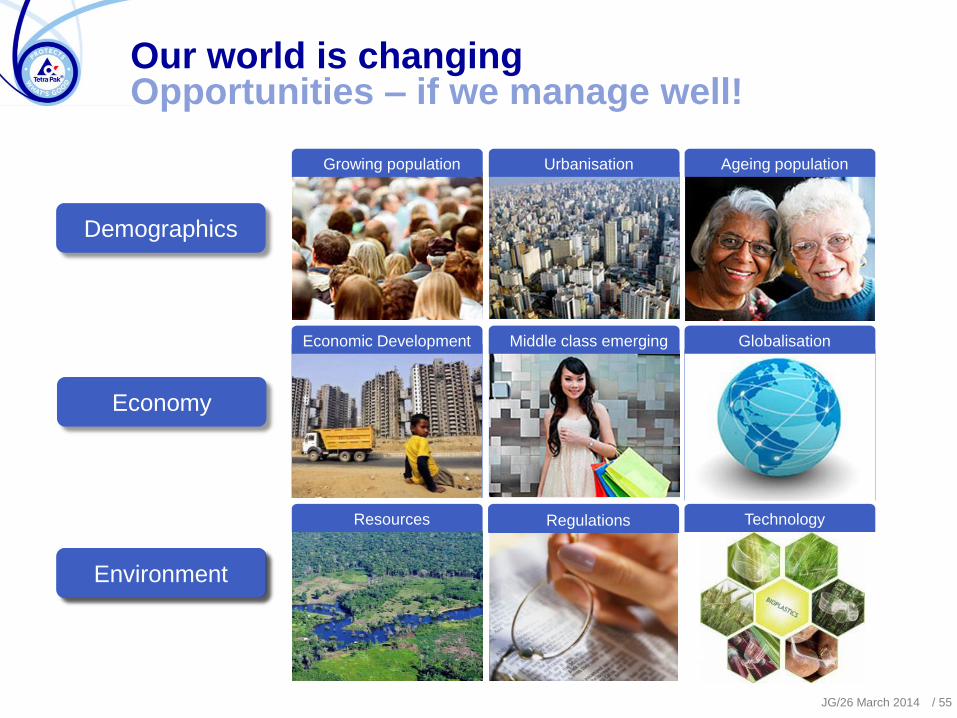

Our world is changing Opportunities – if we manage well!

Growing population Urbanisation Ageing population

Demographics

Environment

Sustainability

Globalisation Middle class emerging

Economy

Economic Development

Environment

Regulations Technology Resources

JG/26 March 2014 / 55

We commit to making food safe and available, everywhere

3

![Supplier Sustainability Guidelines and Expectationssuppliers.safeway.com/docs/supplier_sustainability...Supplier Sustainability Expectations [7] 2/18/2020 Where feasible and applicable](https://img.pdfslide.net/doc/110x75/5f3f28a287ed1c305f46070b/supplier-sustainability-guidelines-and-e-supplier-sustainability-expectations.jpg)

![Supplier sustainability assess[1]](https://img.pdfslide.net/doc/110x75/5551cee6b4c905922b8b4f69/supplier-sustainability-assess1.jpg)