Embed Size (px)

Citation preview

Sustainability Investment:Sustainability Investment: Time for Benchmarking29 May 2013Emily Chew, Senior Analyst, MSCI ESG Research

msci.commsci.com

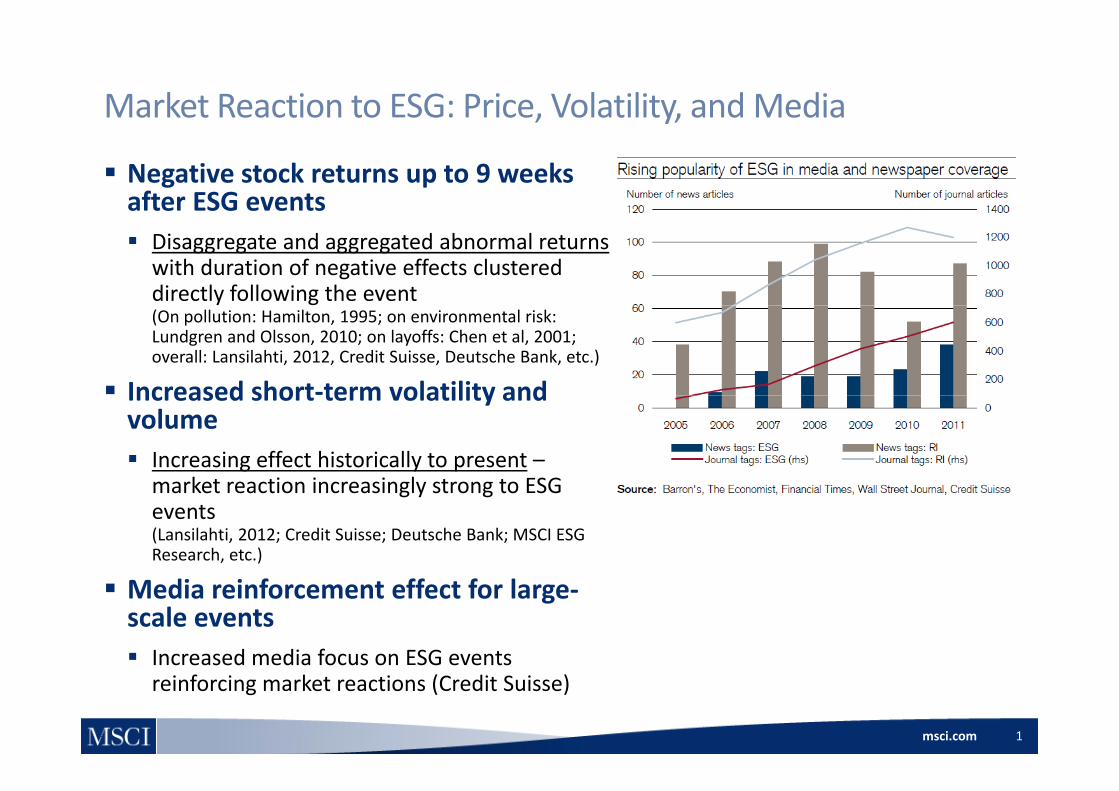

Market Reaction to ESG: Price, Volatility, and Media

Negative stock returns up to 9 weeks after ESG events Disaggregate and aggregated abnormal returns

with duration of negative effects clustered directly following the event(On pollution: Hamilton, 1995; on environmental risk: Lundgren and Olsson, 2010; on layoffs: Chen et al, 2001; overall: Lansilahti, 2012, Credit Suisse, Deutsche Bank, etc.)

Increased short‐term volatility andIncreased short term volatility and volume Increasing effect historically to present –

market reaction increasingly strong to ESGmarket reaction increasingly strong to ESG events(Lansilahti, 2012; Credit Suisse; Deutsche Bank; MSCI ESG Research, etc.)

Media reinforcement effect for large‐scale events Increased media focus on ESG events

msci.com

Increased media focus on ESG events reinforcing market reactions (Credit Suisse)

1

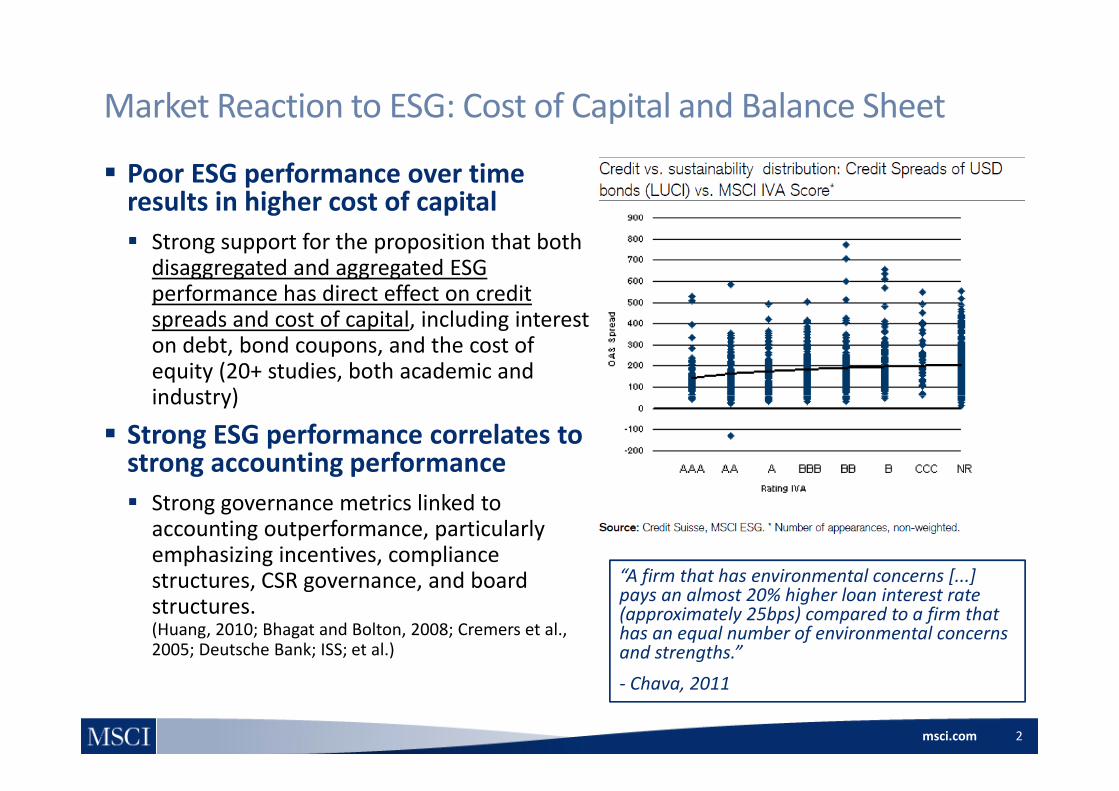

Market Reaction to ESG: Cost of Capital and Balance Sheet

Poor ESG performance over time results in higher cost of capital Strong support for the proposition that both

disaggregated and aggregated ESG performance has direct effect on credit spreads and cost of capital, including interest on debt, bond coupons, and the cost of equity (20+ studies, both academic and industry)industry)

Strong ESG performance correlates to strong accounting performance Strong governance metrics linked to

accounting outperformance, particularly emphasizing incentives, compliance t t CSR d b d “A firm that has environmental concerns [ ]structures, CSR governance, and board structures.(Huang, 2010; Bhagat and Bolton, 2008; Cremers et al., 2005; Deutsche Bank; ISS; et al.)

A firm that has environmental concerns [...] pays an almost 20% higher loan interest rate (approximately 25bps) compared to a firm that has an equal number of environmental concerns and strengths.”

msci.com 2

‐ Chava, 2011

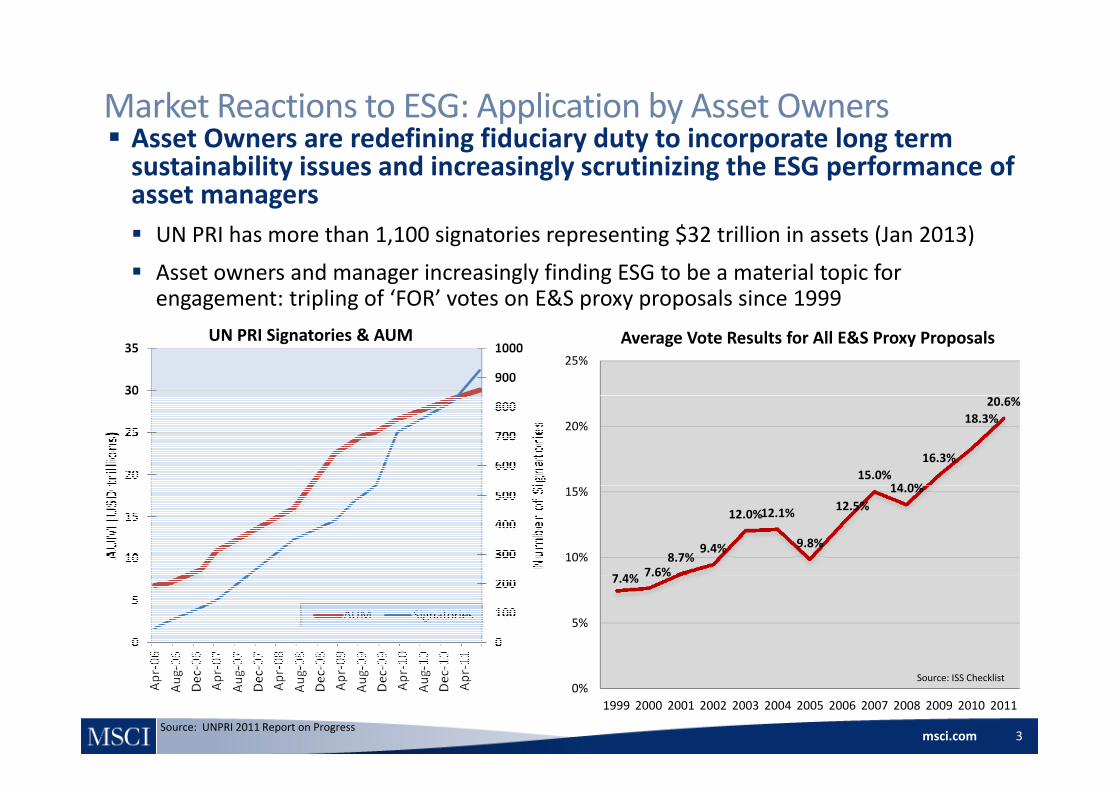

Market Reactions to ESG: Application by Asset Owners Asset Owners are redefining fiduciary duty to incorporate long term sustainability issues and increasingly scrutinizing the ESG performance of asset managers UN PRI has more than 1,100 signatories representing $32 trillion in assets (Jan 2013)

Asset owners and manager increasingly finding ESG to be a material topic for engagement: tripling of ‘FOR’ votes on E&S proxy proposals since 1999g g p g p y p p

25%

Average Vote Results for All E&S Proxy ProposalsUN PRI Signatories & AUM

15.0%14 0%

16.3%

18.3%20.6%

20%

7 4% 7.6%8.7%

9.4%

12.0%12.1%

9.8%

12.5%14.0%

10%

15%

7.4% 7.6%

5%

msci.com 3

0%1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: ISS Checklist

Source: UNPRI 2011 Report on Progress

Two Types of Risk: Event Risk

e.g.Unanticipated Costs:

Negative Externality

E t

Company generates

toxic waste

Costs:•Penalties•Litigation

•Operational Costs•License to

Company A

Event Risk

waste•License to Operate

Trigger Tipping Point Contaminates

major river

•Investigations•Protests

•Change in gRegulations

Which companies are at risk of breaching a tipping point?

msci.com 4

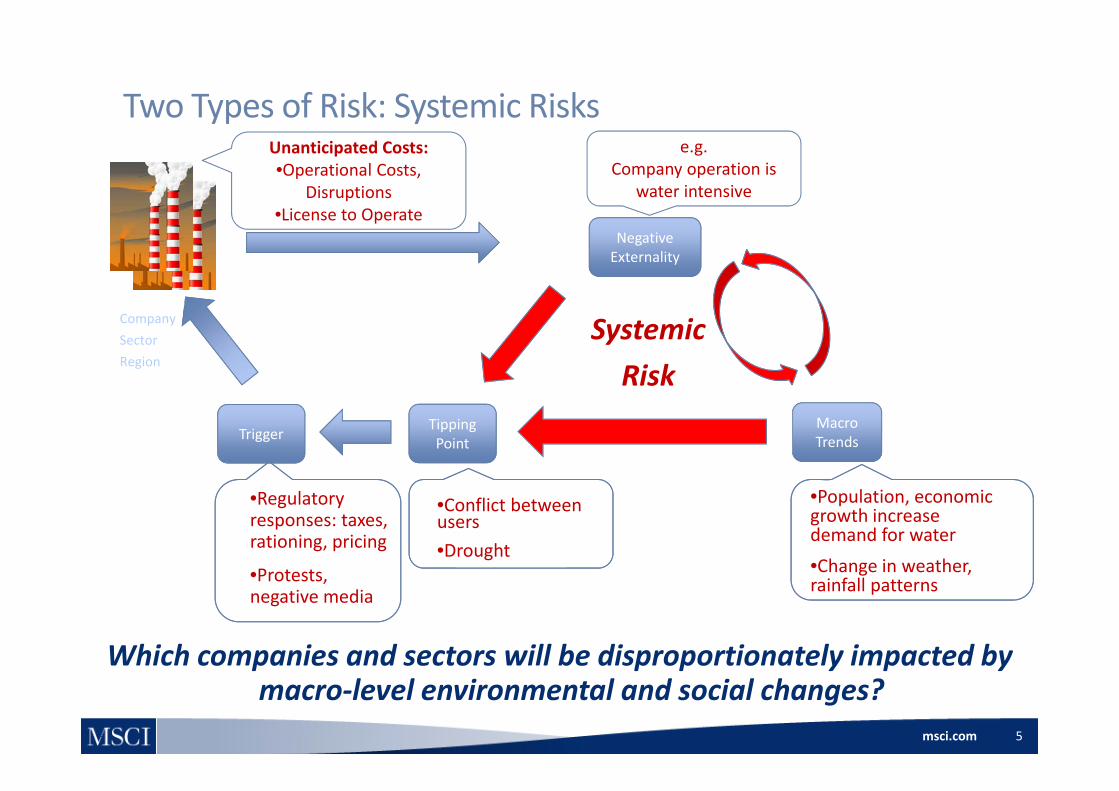

Two Types of Risk: Systemic Riskse.g.

Company operation is water intensive

Unanticipated Costs:•Operational Costs,

Disruptions•License to Operate

Negative Externality

•License to Operate

SystemicRisk

Company SectorRegion

Trigger Tipping Point

Macro Trends

•Conflict between users•Drought

•Population, economic growth increase demand for water•Change in weather,

•Regulatory responses: taxes, rationing, pricing

•Protests grainfall patterns •Protests,

negative media

Which companies and sectors will be disproportionately impacted by

msci.com 5

Which companies and sectors will be disproportionately impacted by macro‐level environmental and social changes?

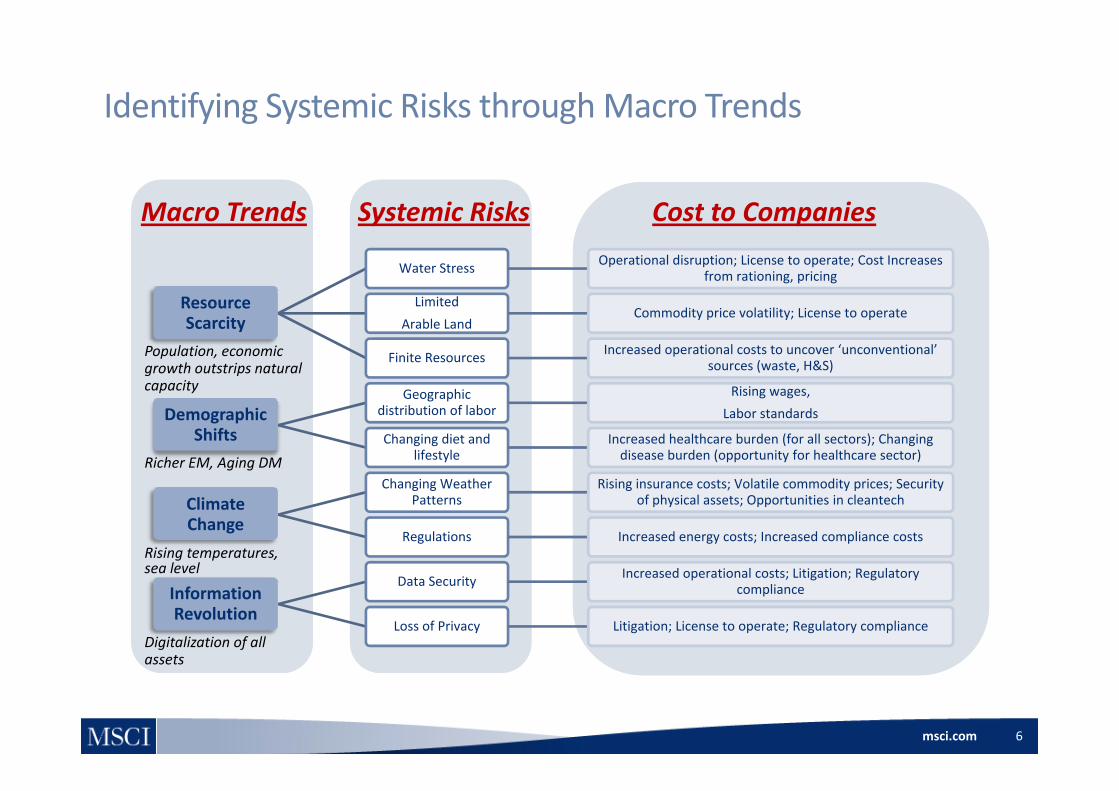

Identifying Systemic Risks through Macro Trends

Macro Trends Systemic Risks Cost to Companies

Resource

Water Stress Operational disruption; License to operate; Cost Increases from rationing, pricing

Limited

Macro Trends Systemic Risks Cost to Companies

Resource Scarcity

Limited Arable Land

Commodity price volatility; License to operate

Finite Resources Increased operational costs to uncover ‘unconventional’ sources (waste, H&S)

Geographic Rising wages,

Population, economic growth outstrips natural capacity

Demographic Shifts

Geographic distribution of labor

Rising wages, Labor standards

Changing diet and lifestyle

Increased healthcare burden (for all sectors); Changing disease burden (opportunity for healthcare sector)

Changing Weather Rising insurance costs; Volatile commodity prices; SecurityRicher EM, Aging DM

Climate Change

Changing Weather Patterns

Rising insurance costs; Volatile commodity prices; Security of physical assets; Opportunities in cleantech

Regulations Increased energy costs; Increased compliance costs

Increased operational costs; Litigation; RegulatoryRising temperatures, sea level

Information Revolution

Data Security Increased operational costs; Litigation; Regulatory compliance

Loss of Privacy Litigation; License to operate; Regulatory complianceDigitalization of all assets

msci.com 6

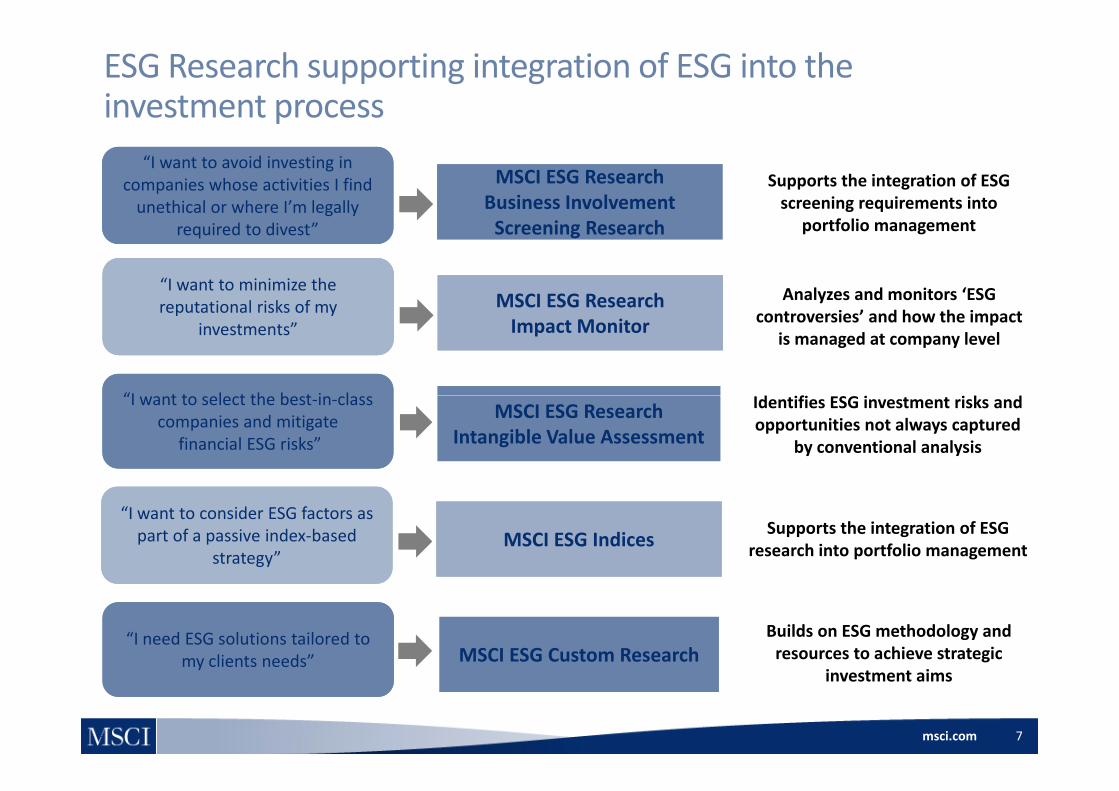

ESG Research supporting integration of ESG into the investment process

MSCI ESG Research Business Involvement MSCI ESG Research

Business Involvement

“I want to avoid investing in companies whose activities I find unethical or where I’m legally

“I want to avoid investing in companies whose activities I find unethical or where I’m legally

Supports the integration of ESG screening requirements into

Screening ResearchScreening Researchg y

required to divest”g y

required to divest”

Analyzes and monitors ‘ESG

portfolio management

MSCI ESG ResearchMSCI ESG Research“I want to minimize the reputational risks of my“I want to minimize the reputational risks of my

“I t t l t th b t i l“I t t l t th b t i l d f k d

controversies’ and how the impact is managed at company level

MSCI ESG Research Impact Monitor

MSCI ESG Research Impact Monitor

reputational risks of my investments”

reputational risks of my investments”

MSCI ESG Research Intangible Value Assessment

MSCI ESG Research Intangible Value Assessment

“I want to select the best‐in‐class companies and mitigate

financial ESG risks”

“I want to select the best‐in‐class companies and mitigate

financial ESG risks”

Identifies ESG investment risks and opportunities not always captured

by conventional analysis

MSCI ESG IndicesMSCI ESG Indices“I want to consider ESG factors as part of a passive index‐based

strategy”

“I want to consider ESG factors as part of a passive index‐based

strategy”

Supports the integration of ESG research into portfolio management

“I need ESG solutions tailored to my clients needs”

“I need ESG solutions tailored to my clients needs” MSCI ESG Custom ResearchMSCI ESG Custom Research

Builds on ESG methodology and resources to achieve strategic

msci.com 7

my clients needsmy clients needsinvestment aims

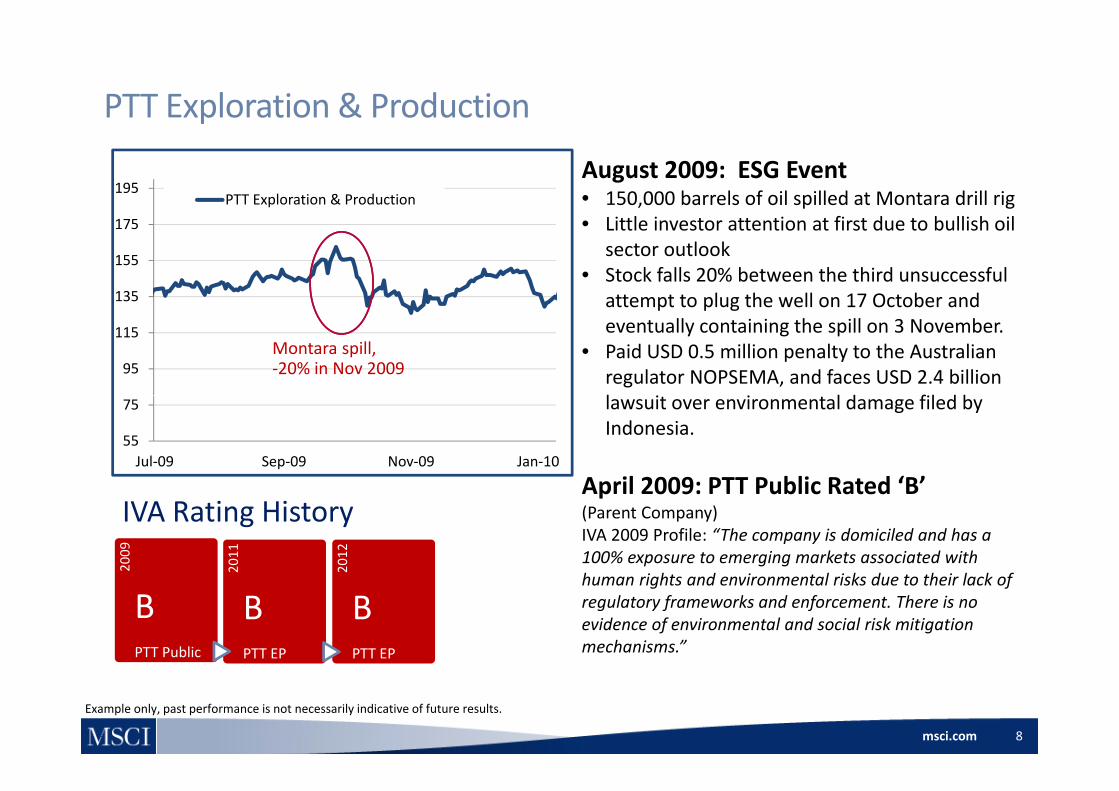

PTT Exploration & Production

195PTT Exploration & Production

August 2009: ESG Event• 150,000 barrels of oil spilled at Montara drill rig

l f d b ll h l

135

155

175 • Little investor attention at first due to bullish oil sector outlook

• Stock falls 20% between the third unsuccessful attempt to plug the well on 17 October and

95

115

attempt to plug the well on 17 October and eventually containing the spill on 3 November.

• Paid USD 0.5 million penalty to the Australian regulator NOPSEMA, and faces USD 2.4 billion l i i l d fil d b

Montara spill,‐20% in Nov 2009

55

75

Jul‐09 Sep‐09 Nov‐09 Jan‐10

lawsuit over environmental damage filed by Indonesia.

April 2009: PTT Public Rated ‘B’IVA Rating History

April 2009: PTT Public Rated B (Parent Company)IVA 2009 Profile: “The company is domiciled and has a 100% exposure to emerging markets associated with h i ht d i t l i k d t th i l k f

2009

2011

2012

human rights and environmental risks due to their lack of regulatory frameworks and enforcement. There is no evidence of environmental and social risk mitigation mechanisms.”

B PTT Public

BPTT EP

BPTT EP

msci.com 8

Example only, past performance is not necessarily indicative of future results.

Yum! Brands

80

90Yum! Brands

December, 2012: ESG Event• Inquiry launched by China’s health officials

regarding KFC purchase of raw chicken with

60

70

g g phigher‐than‐permitted levels of antibiotics

• Share price drop of 4.2% following publicity associated with the controversy; Yum! Brands d i 44% f it t t l f Chi

0

50

60Publicity on food safety problems, Dec 2012:‐4.2%

derives 44% of its total revenues from China and expects KFC’s 2012 Q4 sales to fall by 6%

September 2012: Rated ‘CCC’4001‐Sep‐12 01‐Nov‐12 01‐Jan‐13

IVA Rating

September, 2012: Rated CCCBottom quartile ranking on ‘Product Safety & Quality’IVA 2012 Profile: “The company does not appear to have

IVA Rating microbiological testing programs for its raw materials or finished products; [...the company faces] ongoing challenge of overseeing such an enormous number of restaurants, particularly its franchised locations, where 20

10

2011

2012

the degree of operational control is less but the impact on reputation just as great in the event of quality problems.”BB CCC CCC

msci.com 9

Example only, past performance is not necessarily indicative of future results.

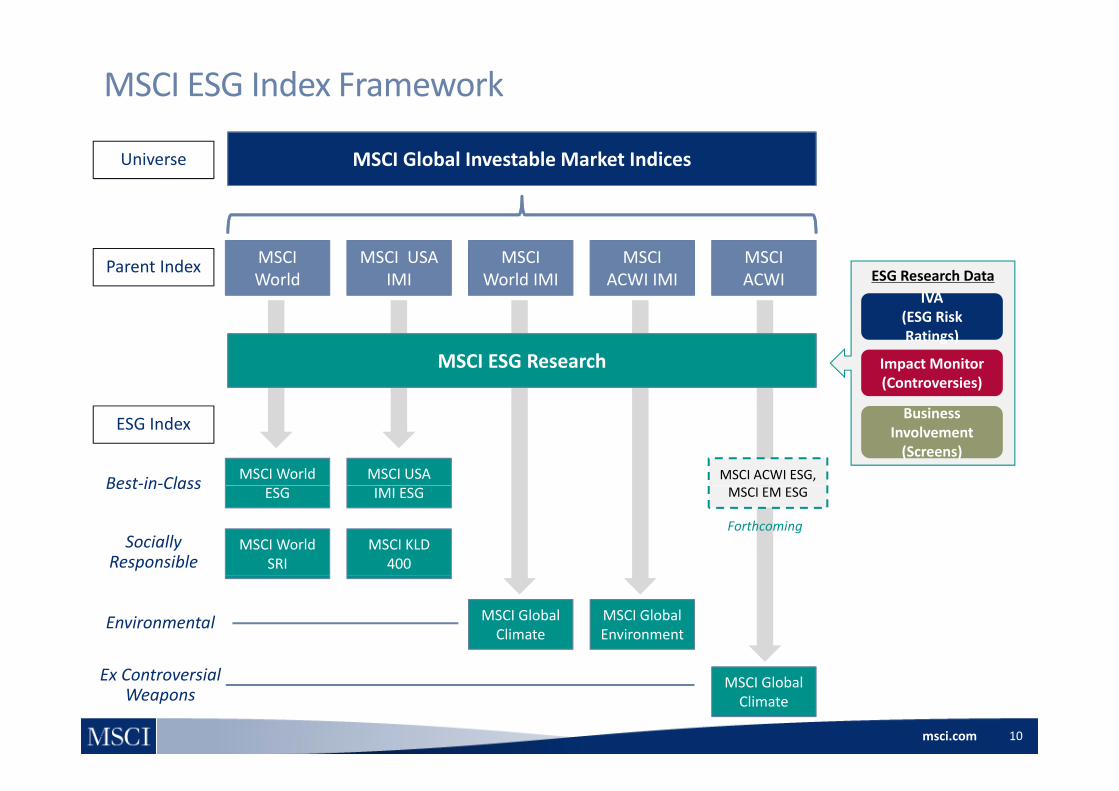

MSCI ESG Index Framework

MSCI Global Investable Market IndicesUniverse

Parent Index MSCI World

MSCI USA IMI

MSCI World IMI

MSCI ACWI IMI

MSCI ACWI ESG Research Data

IVA

MSCI ESG Research

(ESG Risk Ratings)

Impact Monitor (Controversies)

ESG Index

MSCI World MSCI USA MSCI ACWI ESG, Best‐in‐Class

Business Involvement (Screens)

ESG

MSCI World SRI

IMI ESG

MSCI KLD 400

MSCI EM ESGBest in Class

SociallyResponsible

Forthcoming

MSCI Global Climate

MSCI Global Environment

Environmental

msci.com 10

MSCI Global Climate

Ex Controversial Weapons

MSCI ESG Global Client Service

A i 1 212 804 5299Americas + 1.212.804.5299

Asia Pacific + 612.9033.9339

Europe, Middle East and Africa + 44.207.618.2510

www.msci.com/esg

msci.com 12msci.com

Notice and Disclaimer This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the “Information”) is the property of MSCl

Inc. or its subsidiaries (collectively, “MSCI”), or MSCI’s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”) and is provided for informational purposes only. The Information may not be reproduced or redisseminated in whole or in part without prior written permission from MSCI.

The Information may not be used to create derivative works or to verify or correct other data or information. For example (but without limitation), the Information may not be used to create indices, databases, risk models, analytics, software, or in connection with the issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services.

The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information. NONE OF THE INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING WITHOUT LIMITATION ANY IMPLIED WARRANTIES OF ORIGINALITY ACCURACY TIMELINESS NON INFRINGEMENTIMPLIED WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE INFORMATION.

Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent that such injury results from the negligence or wilful default of itself, its servants, agents or sub-contractors.

Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. Past performance does not guarantee future results.

None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment vehicle or any trading strategy. You cannot invest in an index.

MSCI’s indirect wholly-owned subsidiary Institutional Shareholder Services Inc. (“ISS”) is a Registered Investment Adviser under the Investment Advisers Act of 1940. Except with respect to any applicable products or services from ISS (including applicable products or services from MSCI ESG Research which are provided by ISS)Except with respect to any applicable products or services from ISS (including applicable products or services from MSCI ESG Research, which are provided by ISS), neither MSCI nor any of its products or services recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments or trading strategies and neither MSCI nor any of its products or services is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

The MSCI ESG Indices use ratings and other data, analysis and information from MSCI ESG Research. MSCI ESG Research is produced by ISS or its subsidiaries. Issuers mentioned or included in any MSCI ESG Research materials may be a client of MSCI, ISS, or another MSCI subsidiary, or the parent of, or affiliated with, a client of MSCI, ISS, or another MSCI subsidiary, including ISS Corporate Services, Inc., which provides tools and services to issuers. MSCI ESG Research materials,client of MSCI, ISS, or another MSCI subsidiary, including ISS Corporate Services, Inc., which provides tools and services to issuers. MSCI ESG Research materials, including materials utilized in any MSCI ESG Indices or other products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body.

Any use of or access to products, services or information of MSCI requires a license from MSCI. MSCI, Barra, RiskMetrics, ISS, CFRA, FEA, and other MSCI brands and product names are the trademarks, service marks, or registered trademarks or service marks of MSCI or its subsidiaries in the United States and other jurisdictions. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS)” is a service mark of MSCI and Standard & Poor’s.

msci.com 13msci.com

© 2013 MSCI Inc. All rights reserved.Jan 2013