Embed Size (px)

Citation preview

Sustainability transparency in financial reporting Facilitators: Terry Hudgins, Ernst & Young LLP Chris Doherty, Ernst & Young LLP

Solution Set – Session B

Sustainability transparency in financial reporting Real Estate Investment Trusts Sector Insights

Page 2

Disclaimer

► EY refers to the global organization, and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the U.S.

► This presentation is © 2015 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of U.S. and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 3

Topics

► What is sustainability (non-financial) reporting ► Real Estate sector trends and drivers

► Institutional Investors—raising the sustainability bar

► Beyond reporting – realizing value ► Shareholder Value

► “Brown discounts” & “Green premiums” reach Earnings Parody-TIAA-CREF’s Report; May-2015 ► Reduced:

► Energy, Water, Waste, Carbon ► Improved:

► Net Operating Income, Asset Valuation ► Leveraging federal, state and utility incentives

► EY – Integration of GRESB, Green Buildings & Incentives

Page 4

What is non-financial (sustainability) reporting

A sustainability report* describes a company’s non-financial performance with respect to environmental, social and governance topics relevant to internal and external stakeholders.

*Often referred to by companies as a Corporate Social Responsibility Report (CSR) or Citizenship Report

Page 5

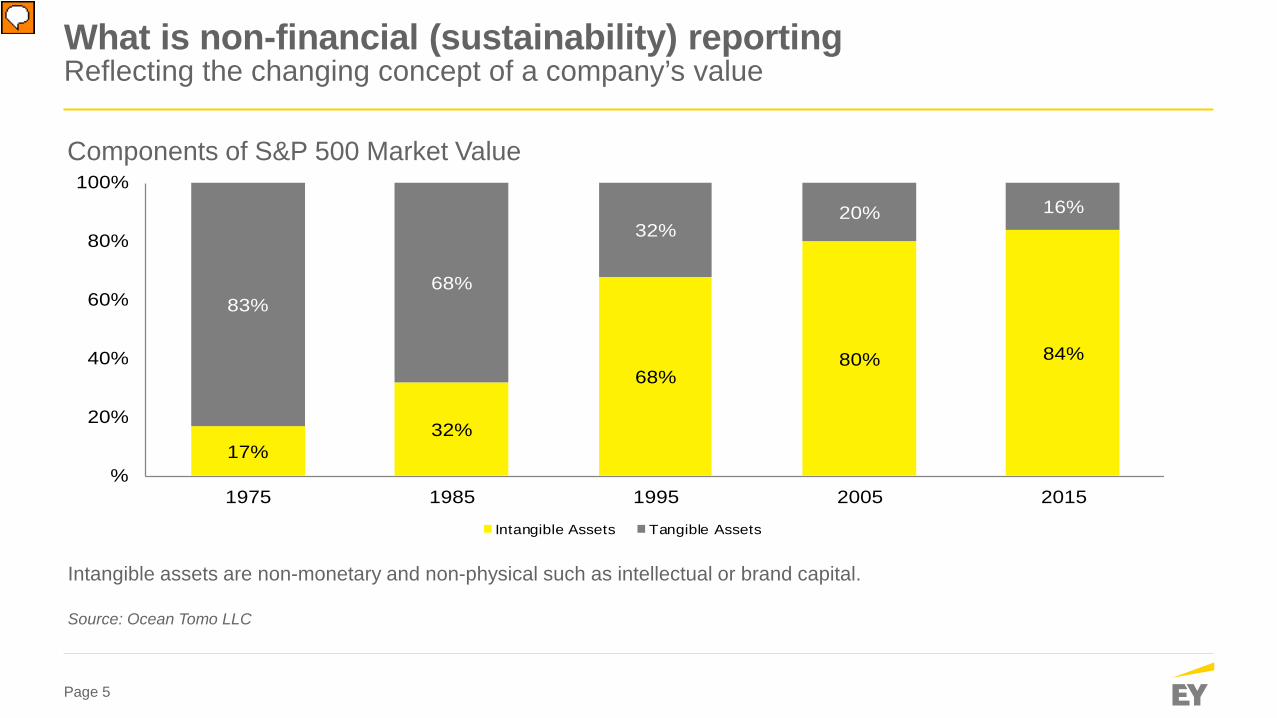

What is non-financial (sustainability) reporting Reflecting the changing concept of a company’s value

Components of S&P 500 Market Value

17%32%

68%80% 84%

83%68%

32%20% 16%

%

20%

40%

60%

80%

100%

1975 1985 1995 2005 2015

Intangible Assets Tangible Assets

Intangible assets are non-monetary and non-physical such as intellectual or brand capital. Source: Ocean Tomo LLC

Page 6

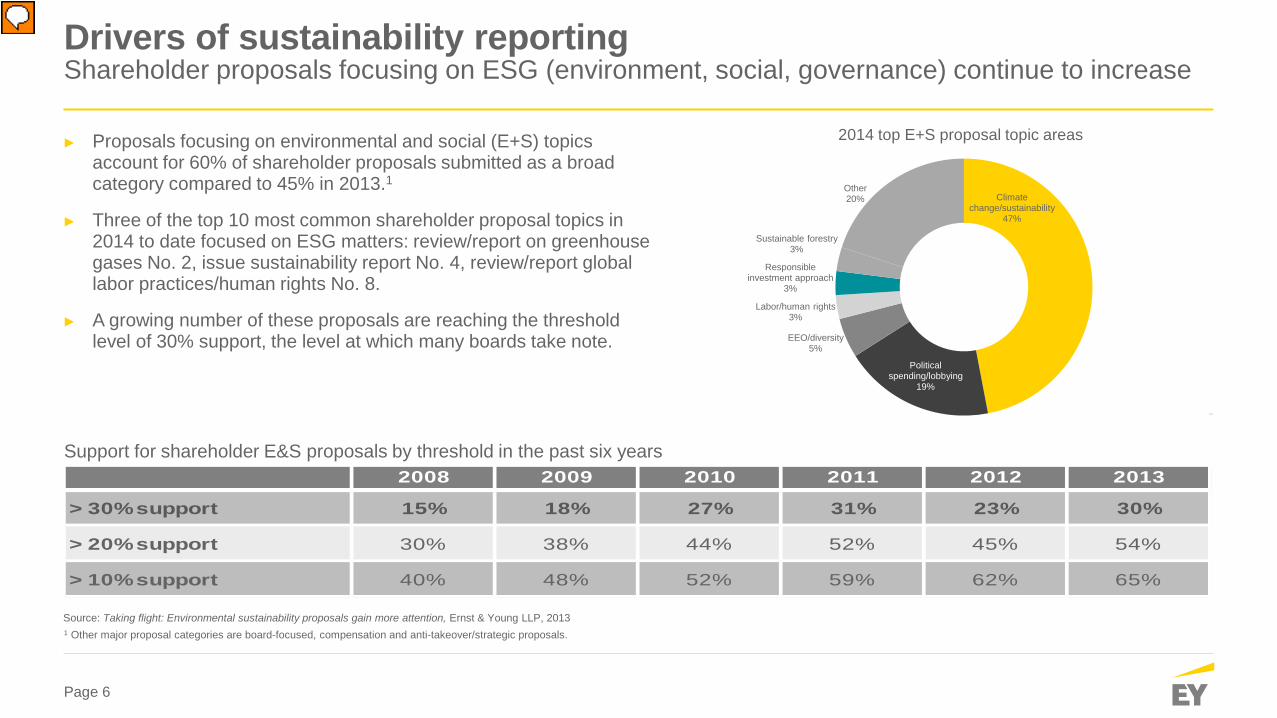

Drivers of sustainability reporting Shareholder proposals focusing on ESG (environment, social, governance) continue to increase

► Proposals focusing on environmental and social (E+S) topics account for 60% of shareholder proposals submitted as a broad category compared to 45% in 2013.1

► Three of the top 10 most common shareholder proposal topics in 2014 to date focused on ESG matters: review/report on greenhouse gases No. 2, issue sustainability report No. 4, review/report global labor practices/human rights No. 8.

► A growing number of these proposals are reaching the threshold level of 30% support, the level at which many boards take note.

Source: Taking flight: Environmental sustainability proposals gain more attention, Ernst & Young LLP, 2013 1 Other major proposal categories are board-focused, compensation and anti-takeover/strategic proposals.

Support for shareholder environmental and social (E+S) proposals by threshold in the past six years2008 2009 2010 2011 2012 2013

> 30% support 15% 18% 27% 31% 23% 30%

> 20% support 30% 38% 44% 52% 45% 54%

> 10% support 40% 48% 52% 59% 62% 65%

Support for shareholder E&S proposals by threshold in the past six years

2014 top E+S proposal topic areas

Climate change/sustainability

47%

Political spending/lobbying

19%

EEO/diversity 5%

Labor/human rights 3%

Responsible investment approach

3%

Sustainable forestry 3%

Other 20%

Page 7

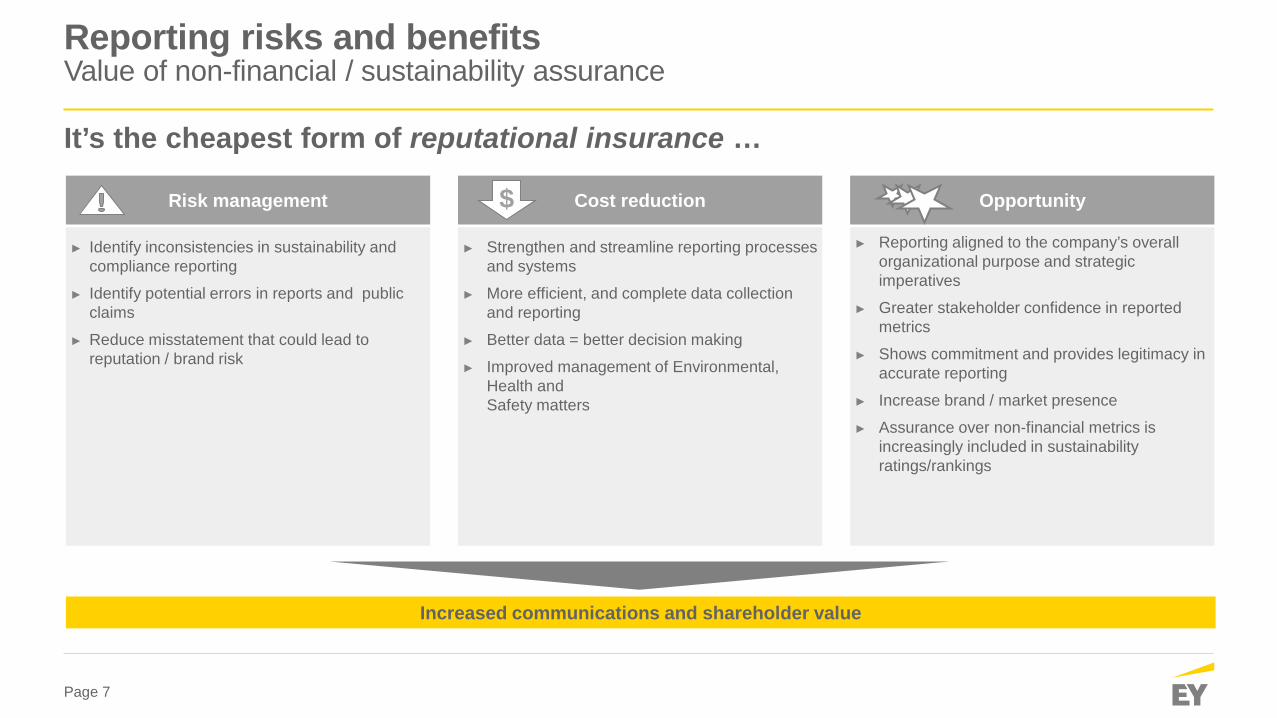

It’s the cheapest form of reputational insurance …

Reporting risks and benefits Value of non-financial / sustainability assurance

Cost reduction Opportunity Risk management

► Strengthen and streamline reporting processes and systems

► More efficient, and complete data collection and reporting

► Better data = better decision making

► Improved management of Environmental, Health and Safety matters

► Reporting aligned to the company’s overall organizational purpose and strategic imperatives

► Greater stakeholder confidence in reported metrics

► Shows commitment and provides legitimacy in accurate reporting

► Increase brand / market presence

► Assurance over non-financial metrics is increasingly included in sustainability ratings/rankings

► Identify inconsistencies in sustainability and compliance reporting

► Identify potential errors in reports and public claims

► Reduce misstatement that could lead to reputation / brand risk

Increased communications and shareholder value

$

Page 8

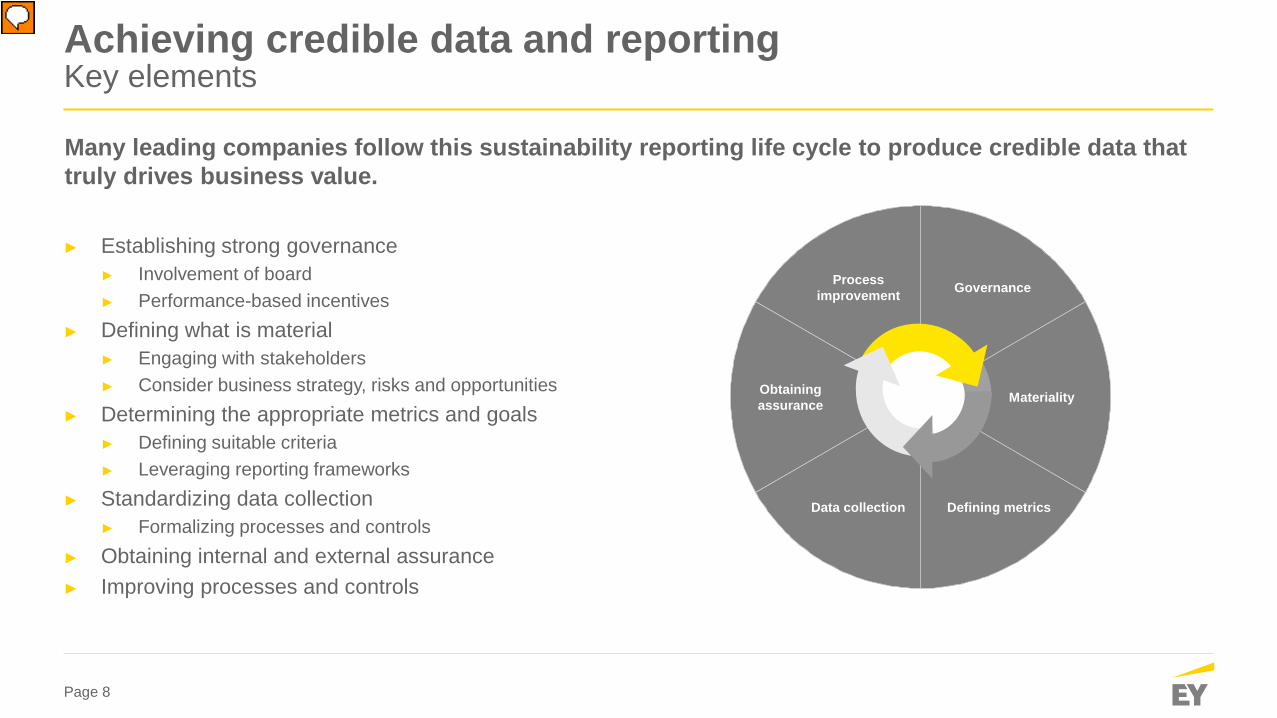

Achieving credible data and reporting Key elements

► Establishing strong governance ► Involvement of board ► Performance-based incentives

► Defining what is material ► Engaging with stakeholders ► Consider business strategy, risks and opportunities

► Determining the appropriate metrics and goals ► Defining suitable criteria ► Leveraging reporting frameworks

► Standardizing data collection ► Formalizing processes and controls

► Obtaining internal and external assurance ► Improving processes and controls

Many leading companies follow this sustainability reporting life cycle to produce credible data that truly drives business value.

Obtaining assurance Materiality

Defining metrics Data collection

Governance Process improvement

Page 9

Real Estate sector trends and drivers

Page 10

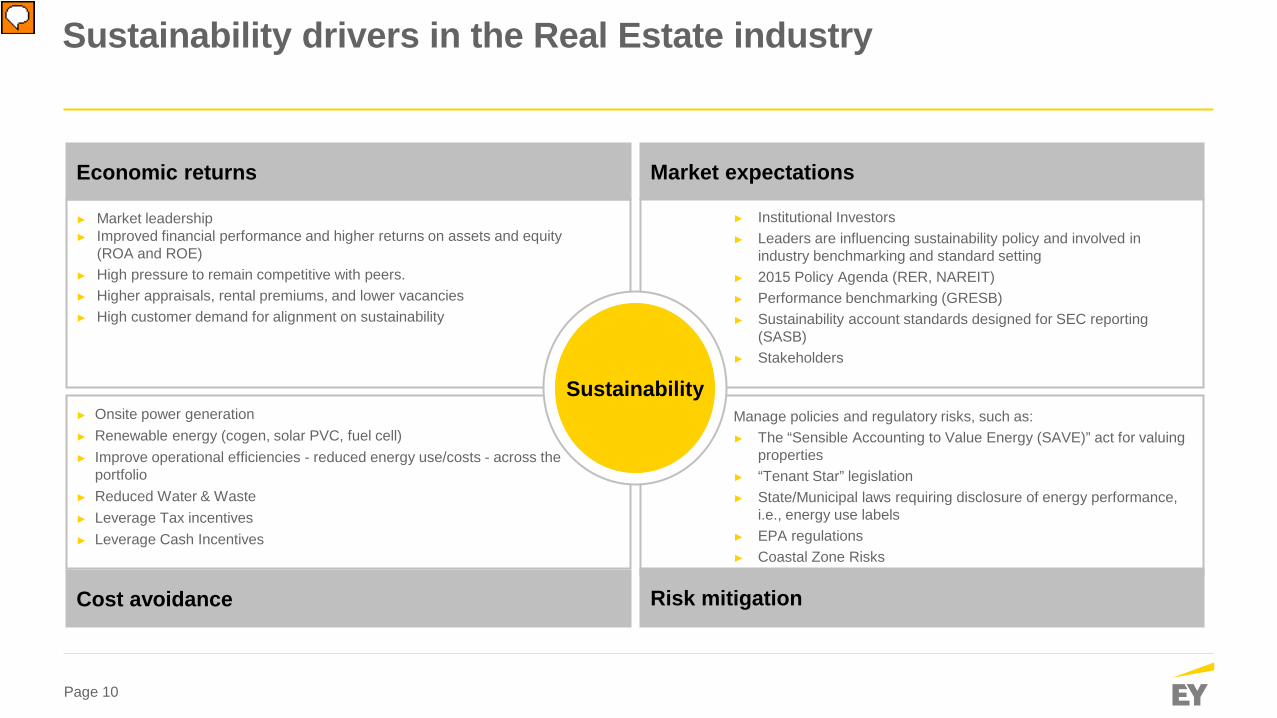

Sustainability drivers in the Real Estate industry

► Onsite power generation ► Renewable energy (cogen, solar PVC, fuel cell) ► Improve operational efficiencies - reduced energy use/costs - across the

portfolio ► Reduced Water & Waste ► Leverage Tax incentives ► Leverage Cash Incentives

Manage policies and regulatory risks, such as: ► The “Sensible Accounting to Value Energy (SAVE)” act for valuing

properties ► “Tenant Star” legislation ► State/Municipal laws requiring disclosure of energy performance,

i.e., energy use labels ► EPA regulations ► Coastal Zone Risks

► Market leadership ► Improved financial performance and higher returns on assets and equity

(ROA and ROE) ► High pressure to remain competitive with peers. ► Higher appraisals, rental premiums, and lower vacancies ► High customer demand for alignment on sustainability

► Institutional Investors ► Leaders are influencing sustainability policy and involved in

industry benchmarking and standard setting ► 2015 Policy Agenda (RER, NAREIT) ► Performance benchmarking (GRESB) ► Sustainability account standards designed for SEC reporting

(SASB) ► Stakeholders

Market expectations Economic returns

Risk mitigation Cost avoidance

Channel 2 Prospects

Sustainability

Page 11

RE sector sustainability initiatives

► Began in 2005 ► Annual selection program of NAREIT members who show

exemplary sustainability practices ► Presented across 8 categories: Diversified, Global, Health

Care, Industrial, Lodging/Resorts, Office, Residential, and Retail

► Criteria takes into consideration GRESB scores

► Began in 2006 ► UN initiative of investors dedicated to bringing the financial

materiality of ESG issues into mainstream investment decision making and ownership practices

► Allows signatories to demonstrate their commitment to ESG investment, and implement the PRI’s Six Principles

► Mandatory reporting and assessment for asset owners and investment manager signatories

► Began in 2009 ► Annual benchmarking survey for property companies and funds

to disclose sustainability performance of portfolios to investors ► Participants ranked as Green Starters, Green Talk, Green Walk,

or Green Stars ► In 2014, acquired by GBCI, the certification administrator for

LEED ► First GRESB debt survey issued in 2015

► First issued in 2011 (GRI began in 1997) ► Sector-specific disclosures for the Construction and Real

Estate industry designed to be additional to the general GRI G4 Guidelines

► Used in the development of Sustainability Reports to disclose key aspects of sustainability performance

► Began in 2011 ► Devoted to creating accounting standards for 80

industries in 10 standards to disclose material sustainability information in SEC filings such as the 10-K and 20-F

► Developing disclosure standards for the Infrastructure sector to be released in March 2016

► Began in 1998 ► USGBC’s certification and rating system for sustainable

buildings at the property level ► Measures the environmental design and performance of new

and existing, commercial, residential and neighborhood developments and properties

► LEED Volume certification measures at a portfolio-level ► Four levels of certification: Certified, Silver, Gold, and Platinum

Page 12

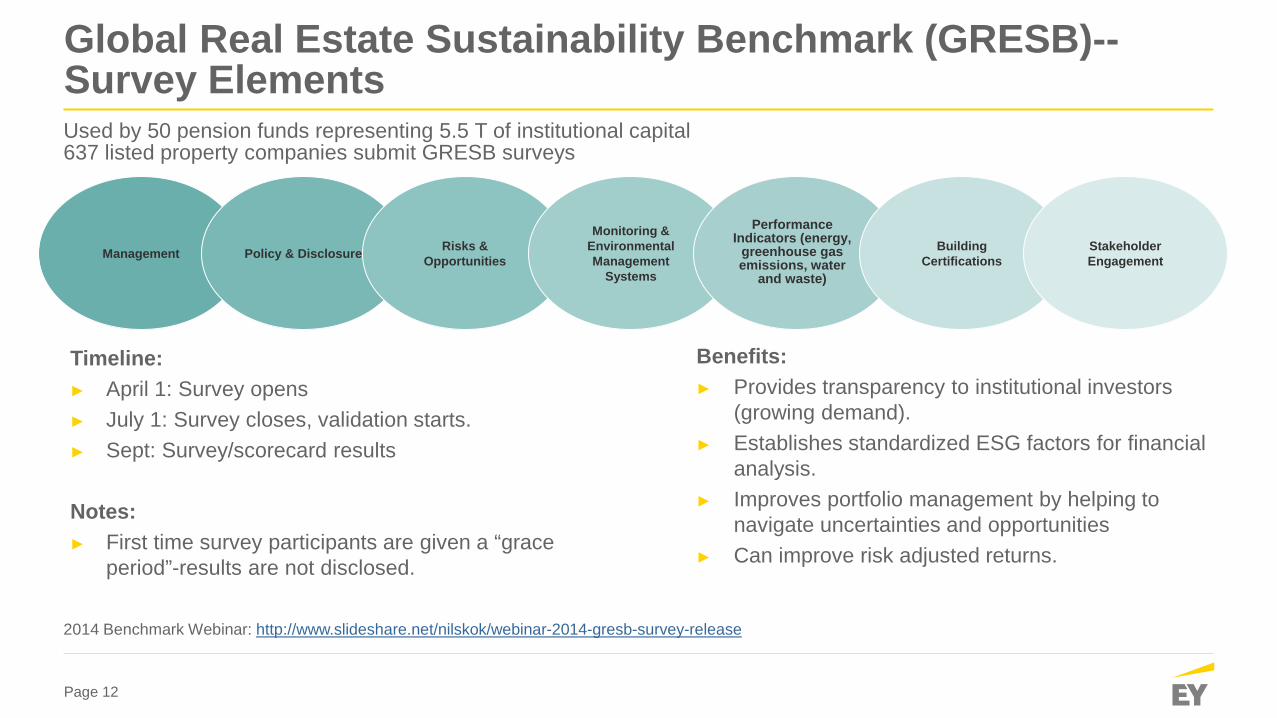

Management

Global Real Estate Sustainability Benchmark (GRESB)-- Survey Elements

Benefits: ► Provides transparency to institutional investors

(growing demand). ► Establishes standardized ESG factors for financial

analysis. ► Improves portfolio management by helping to

navigate uncertainties and opportunities ► Can improve risk adjusted returns.

Used by 50 pension funds representing 5.5 T of institutional capital 637 listed property companies submit GRESB surveys

Timeline: ► April 1: Survey opens ► July 1: Survey closes, validation starts. ► Sept: Survey/scorecard results

Notes: ► First time survey participants are given a “grace

period”-results are not disclosed.

2014 Benchmark Webinar: http://www.slideshare.net/nilskok/webinar-2014-gresb-survey-release

Policy & Disclosure Risks & Opportunities

Monitoring & Environmental Management

Systems

Building Certifications

Stakeholder Engagement

Performance Indicators (energy,

greenhouse gas emissions, water

and waste)

Page 13

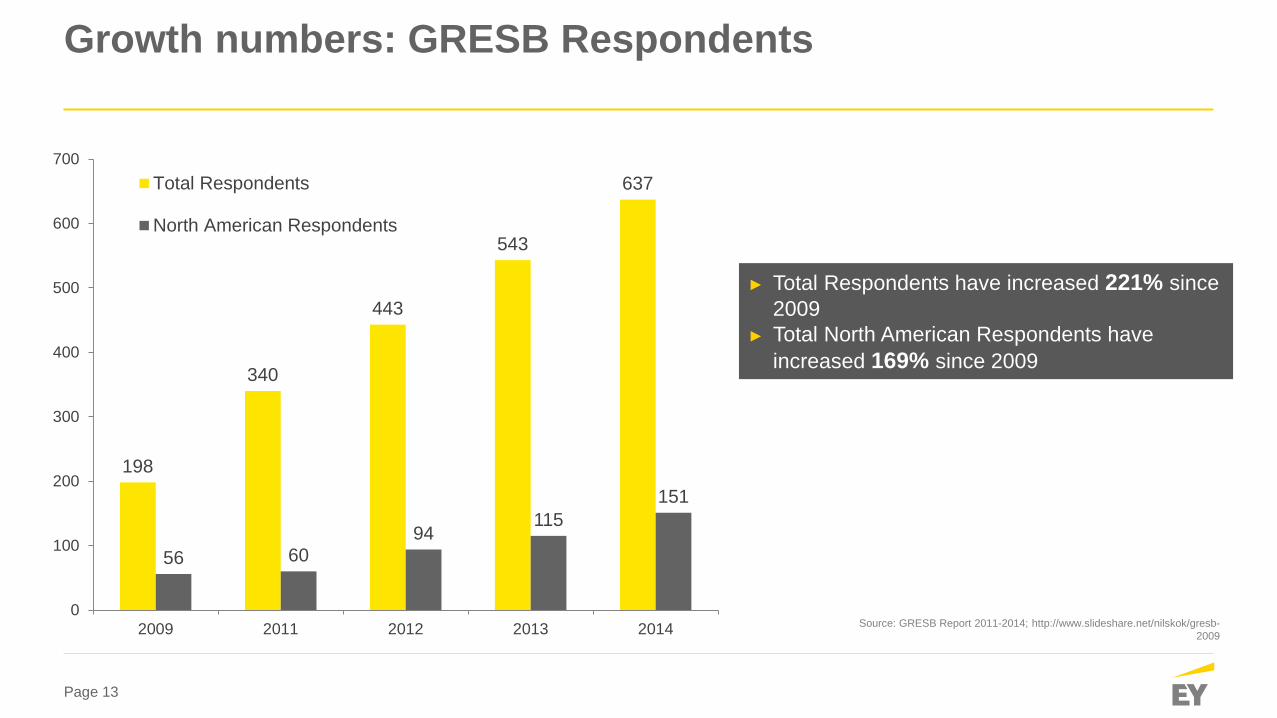

Growth numbers: GRESB Respondents

Source: GRESB Report 2011-2014; http://www.slideshare.net/nilskok/gresb-2009

198

340

443

543

637

56 60 94

115 151

0

100

200

300

400

500

600

700

2009 2011 2012 2013 2014

Total Respondents

North American Respondents

► Total Respondents have increased 221% since 2009

► Total North American Respondents have increased 169% since 2009

Page 14

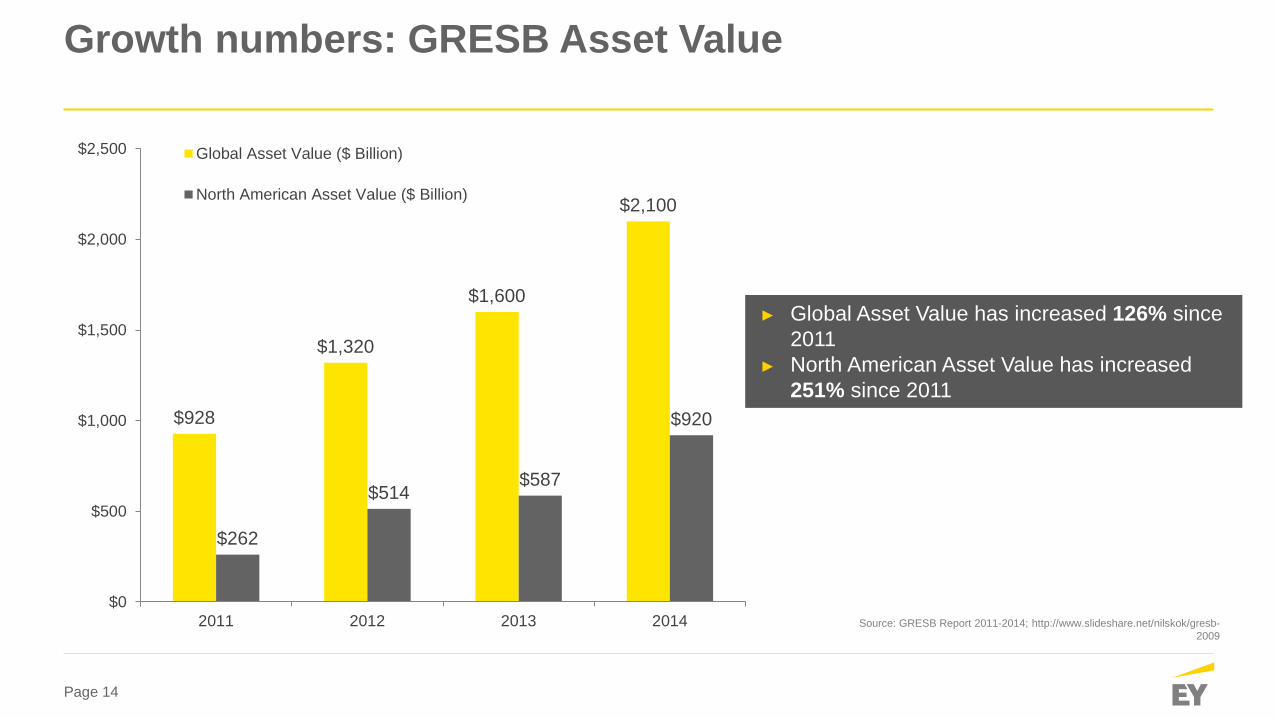

Growth numbers: GRESB Asset Value

$928

$1,320

$1,600

$2,100

$262

$514 $587

$920

$0

$500

$1,000

$1,500

$2,000

$2,500

2011 2012 2013 2014

Global Asset Value ($ Billion)

North American Asset Value ($ Billion)

► Global Asset Value has increased 126% since 2011

► North American Asset Value has increased 251% since 2011

Source: GRESB Report 2011-2014; http://www.slideshare.net/nilskok/gresb-2009

Page 15

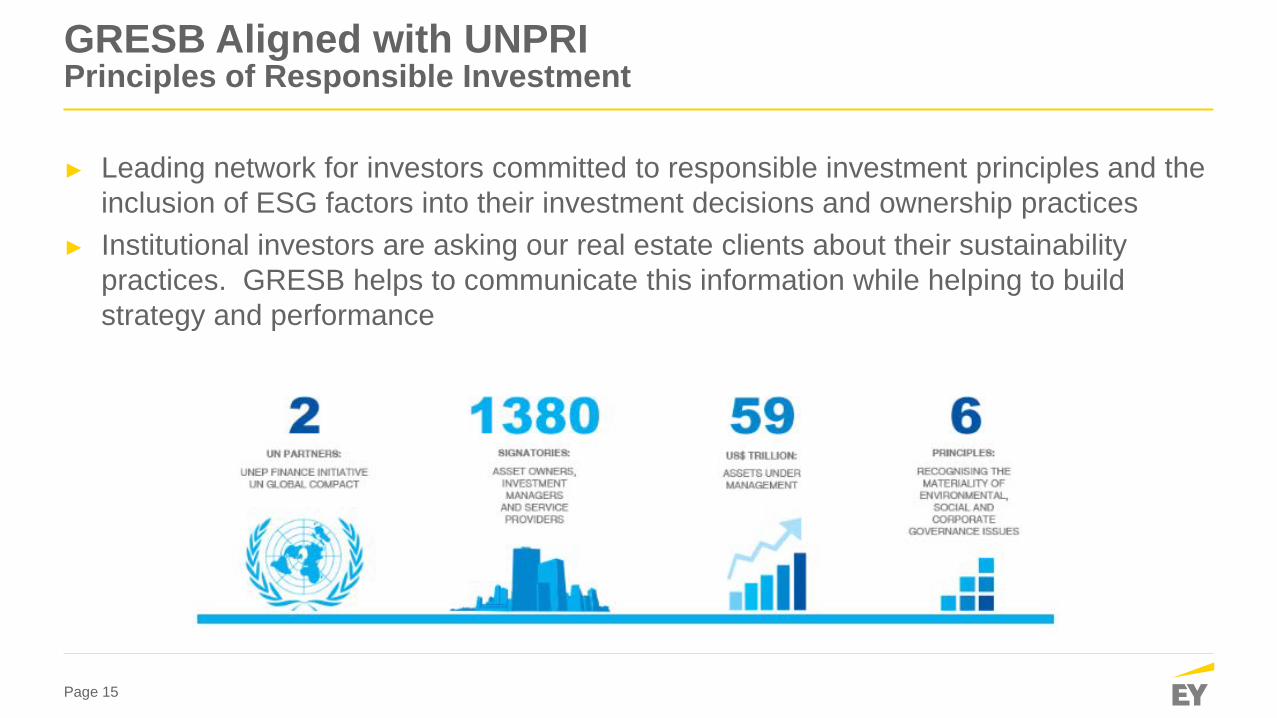

GRESB Aligned with UNPRI Principles of Responsible Investment

► Leading network for investors committed to responsible investment principles and the inclusion of ESG factors into their investment decisions and ownership practices

► Institutional investors are asking our real estate clients about their sustainability practices. GRESB helps to communicate this information while helping to build strategy and performance

Page 16

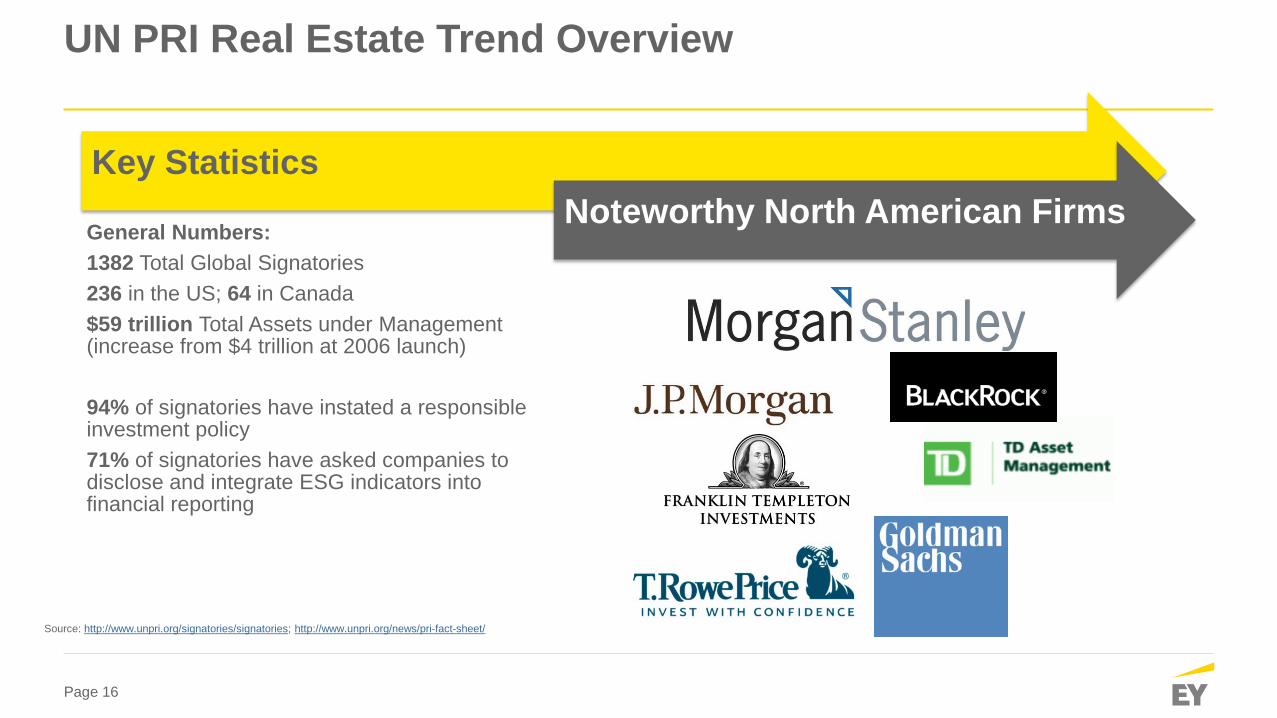

UN PRI Real Estate Trend Overview

Key Statistics

General Numbers: 1382 Total Global Signatories 236 in the US; 64 in Canada $59 trillion Total Assets under Management (increase from $4 trillion at 2006 launch) 94% of signatories have instated a responsible investment policy 71% of signatories have asked companies to disclose and integrate ESG indicators into financial reporting

Noteworthy North American Firms

Source: http://www.unpri.org/signatories/signatories; http://www.unpri.org/news/pri-fact-sheet/

Page 17

Beyond reporting – realizing value

Page 18

REITs continue to invest in sustainability and realize returns

► Real estate organizations are becoming more focused when it comes to energy management, making smarter investments in energy efficiency projects in order to maximize their returns over the life-cycle of the project or equipment

► More than half of all investment in 2014 was directed to heating, ventilation and air conditioning (HVAC). Previously, lighting-related projects had attracted the greatest share of investment.

► Respondents are continuing to strategically target investments with the intent of maximizing returns

Source: 2014 Leader in the Light Award Entries & Trend Analysis https://www.reit.com/sites/default/files/media/PDFs/2014NAREITLeaderLightAward_Trend%20Analysis_RF.pdf

Investment in energy efficiency projects

30%

Between 2011 and 2013

Savings from sustainability projects

ROI 2011-2013 av. ROI 2014 av.

96% In 2014 over 2011-2013 average

26%

40%

Page 19

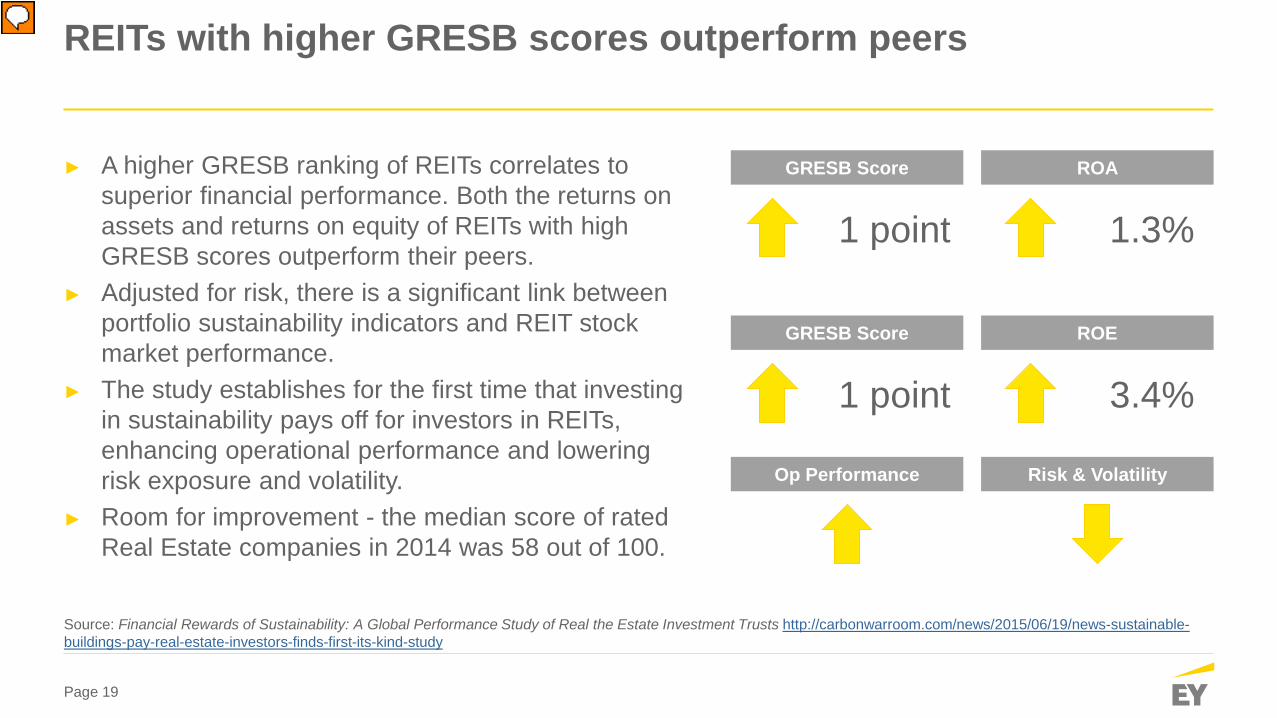

REITs with higher GRESB scores outperform peers

► A higher GRESB ranking of REITs correlates to superior financial performance. Both the returns on assets and returns on equity of REITs with high GRESB scores outperform their peers.

► Adjusted for risk, there is a significant link between portfolio sustainability indicators and REIT stock market performance.

► The study establishes for the first time that investing in sustainability pays off for investors in REITs, enhancing operational performance and lowering risk exposure and volatility.

► Room for improvement - the median score of rated Real Estate companies in 2014 was 58 out of 100.

Source: Financial Rewards of Sustainability: A Global Performance Study of Real the Estate Investment Trusts http://carbonwarroom.com/news/2015/06/19/news-sustainable-buildings-pay-real-estate-investors-finds-first-its-kind-study

GRESB Score ROA

1 point

1.3%

GRESB Score ROE

1 point

3.4%

Op Performance Risk & Volatility

Page 20

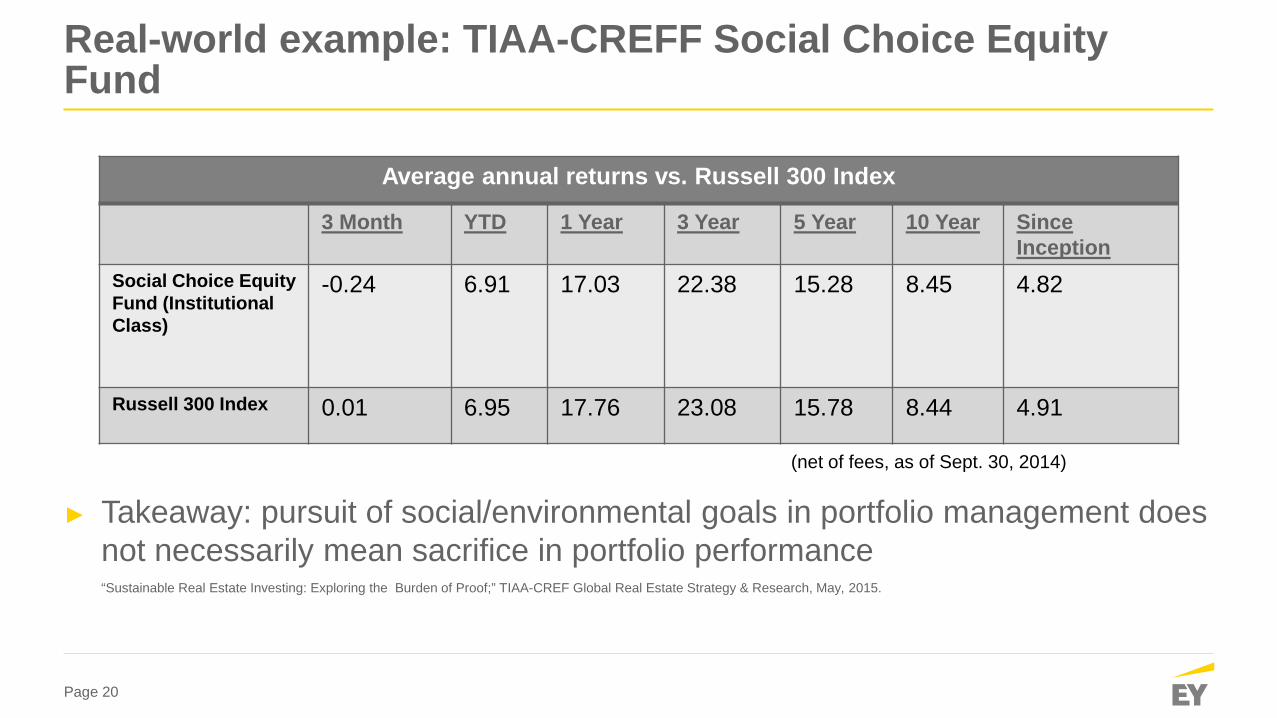

Real-world example: TIAA-CREFF Social Choice Equity Fund

Average annual returns vs. Russell 300 Index

3 Month YTD 1 Year 3 Year 5 Year 10 Year Since Inception

Social Choice Equity Fund (Institutional Class)

-0.24 6.91 17.03 22.38 15.28 8.45 4.82

Russell 300 Index 0.01 6.95 17.76 23.08 15.78 8.44 4.91

► Takeaway: pursuit of social/environmental goals in portfolio management does not necessarily mean sacrifice in portfolio performance “Sustainable Real Estate Investing: Exploring the Burden of Proof;” TIAA-CREF Global Real Estate Strategy & Research, May, 2015.

(net of fees, as of Sept. 30, 2014)

Page 21

Quantitative evidence:

► TIAA-CREF: “The high winning percentage of the LEED portfolio and the non-LEED portfolio’s low winning percentage are interesting; both are statistically significant. These results validated the LEED portfolio’s tendency to outperform over NCREIF office performance and the non-LEED portfolio’s propensity to underperform.”

“Sustainable Real Estate Investing: Exploring the Burden of Proof”; TIAA-CREF Global Real Estate Strategy & Research, May, 2015

Page 22

Case Study: TIAA-CREF’s Global Real Estate Sustainability Initiative (GRESI)

► TIAA’s GRESI incorporates the pursuit of economic returns, environmental returns, risk mitigation and meeting market expectations

► During 2014, TIAA-CREF’s GRESI benefitted their portfolios: ► Over $14 million in energy costs saved ► Over 118 million kilowatt-hours of energy consumption avoided ► Greenhouse gas emissions reduced by over 47,700 metric tons of carbon dioxide

equivalent

► Potentially improving Net Operating Income and Asset Valuation, while meeting shareholder value and stakeholder transparency

“Sustainable Real Estate Investing: Exploring the Burden of Proof”; TIAA-CREF Global Real Estate Strategy & Research, May, 2015

Page 23

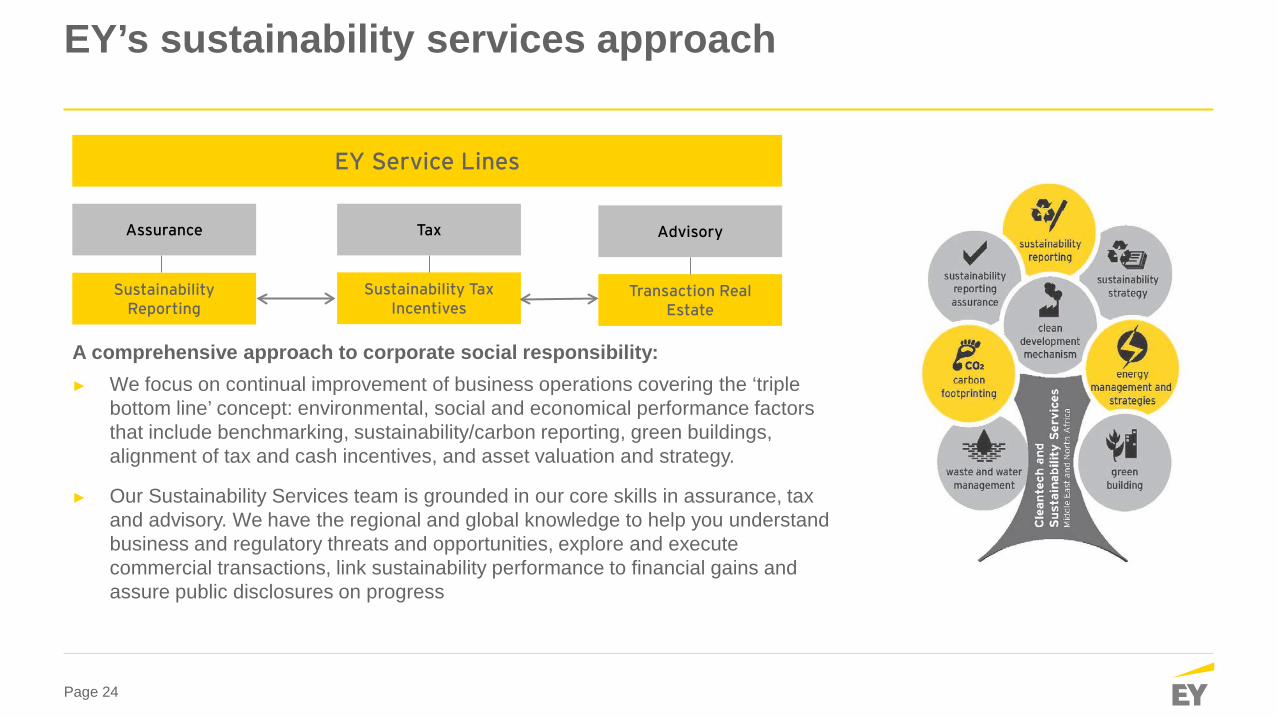

EY – Integration of GRESB, Green Buildings and Incentives

Page 24

A comprehensive approach to corporate social responsibility: ► We focus on continual improvement of business operations covering the ‘triple

bottom line’ concept: environmental, social and economical performance factors that include benchmarking, sustainability/carbon reporting, green buildings, alignment of tax and cash incentives, and asset valuation and strategy.

► Our Sustainability Services team is grounded in our core skills in assurance, tax and advisory. We have the regional and global knowledge to help you understand business and regulatory threats and opportunities, explore and execute commercial transactions, link sustainability performance to financial gains and assure public disclosures on progress

EY’s sustainability services approach

EY Service Lines

Assurance Advisory Tax

Sustainability Tax Incentives

Transaction Real Estate

Sustainability Reporting

Page 25

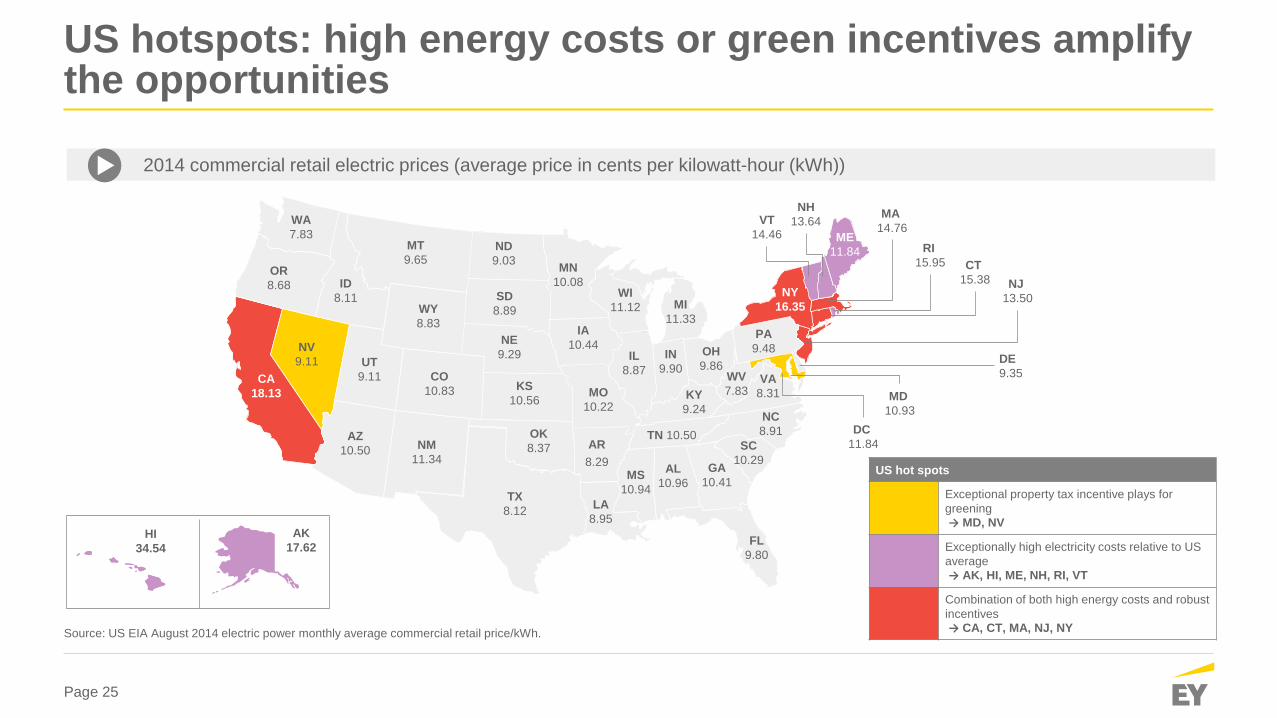

US hotspots: high energy costs or green incentives amplify the opportunities

2014 commercial retail electric prices (average price in cents per kilowatt-hour (kWh))

Source: US EIA August 2014 electric power monthly average commercial retail price/kWh.

US hot spots

Exceptional property tax incentive plays for greening → MD, NV

Exceptionally high electricity costs relative to US average → AK, HI, ME, NH, RI, VT

Combination of both high energy costs and robust incentives → CA, CT, MA, NJ, NY

AK 17.62

HI 34.54

WA 7.83

OR 8.68

CA 18.13

NV 9.11

ID 8.11

MT 9.65

WY 8.83

UT 9.11

AZ 10.50

CO 10.83

NM 11.34

TX 8.12

ND 9.03

SD 8.89

NE 9.29

KS 10.56

OK 8.37 AR

8.29

LA 8.95

MS 10.94

AL 10.96

GA 10.41

FL 9.80

SC 10.29

NC 8.91 TN 10.50

VA 8.31

WV 7.83 KY

9.24 MO

10.22

PA 9.48 OH

9.86 IN

9.90 IL

8.87

IA 10.44

MN 10.08

WI 11.12 MI

11.33

NY 16.35

ME 11.84

VT 14.46

NH 13.64 MA

14.76

RI 15.95 CT

15.38 NJ 13.50

DE 9.35

MD 10.93

DC 11.84

Page 26

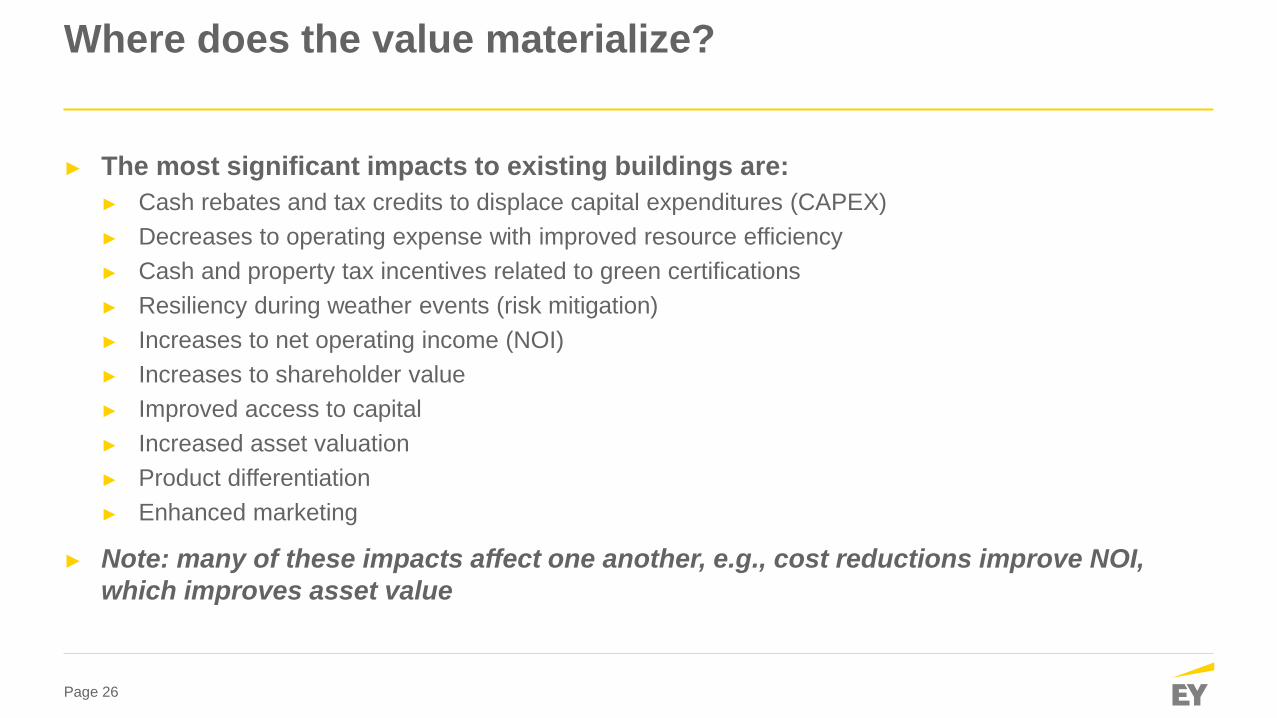

► The most significant impacts to existing buildings are: ► Cash rebates and tax credits to displace capital expenditures (CAPEX) ► Decreases to operating expense with improved resource efficiency ► Cash and property tax incentives related to green certifications ► Resiliency during weather events (risk mitigation) ► Increases to net operating income (NOI) ► Increases to shareholder value ► Improved access to capital ► Increased asset valuation ► Product differentiation ► Enhanced marketing

► Note: many of these impacts affect one another, e.g., cost reductions improve NOI, which improves asset value

Where does the value materialize?

Page 27

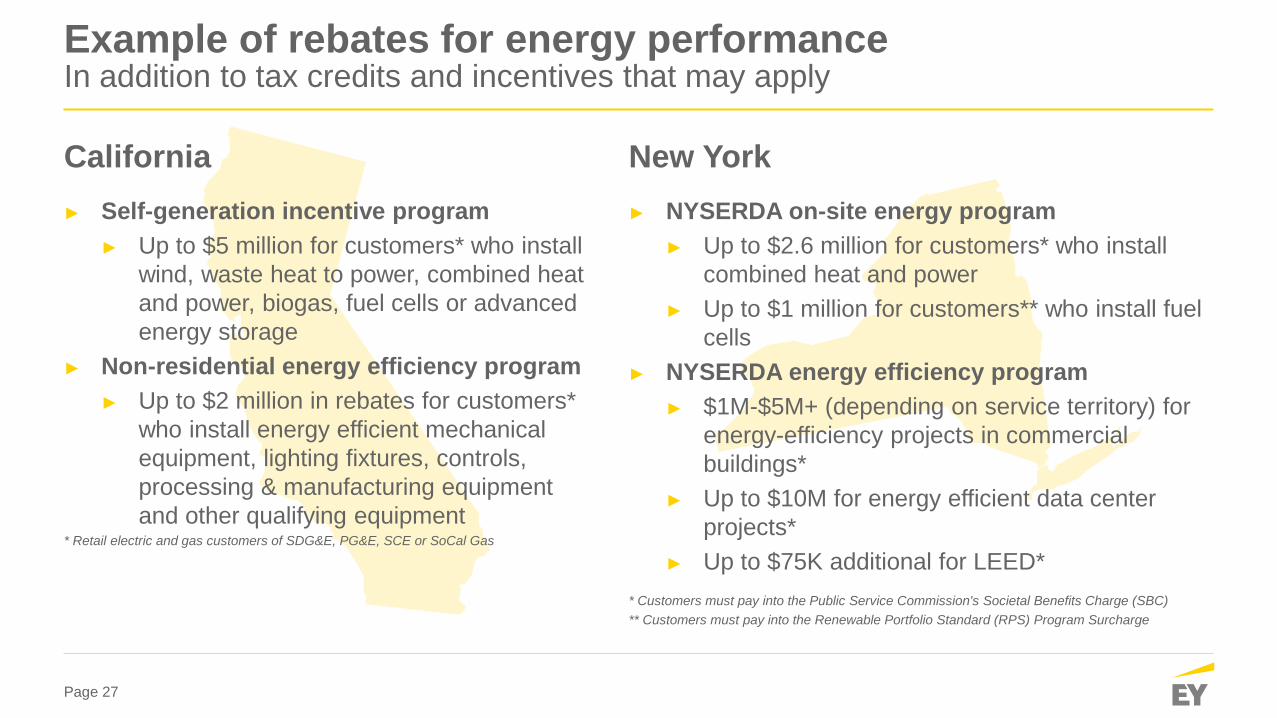

► Self-generation incentive program ► Up to $5 million for customers* who install

wind, waste heat to power, combined heat and power, biogas, fuel cells or advanced energy storage

► Non-residential energy efficiency program ► Up to $2 million in rebates for customers*

who install energy efficient mechanical equipment, lighting fixtures, controls, processing & manufacturing equipment and other qualifying equipment

* Retail electric and gas customers of SDG&E, PG&E, SCE or SoCal Gas

► NYSERDA on-site energy program ► Up to $2.6 million for customers* who install

combined heat and power ► Up to $1 million for customers** who install fuel

cells ► NYSERDA energy efficiency program

► $1M-$5M+ (depending on service territory) for energy-efficiency projects in commercial buildings*

► Up to $10M for energy efficient data center projects*

► Up to $75K additional for LEED* * Customers must pay into the Public Service Commission's Societal Benefits Charge (SBC) ** Customers must pay into the Renewable Portfolio Standard (RPS) Program Surcharge

California New York

Example of rebates for energy performance In addition to tax credits and incentives that may apply

Page 28

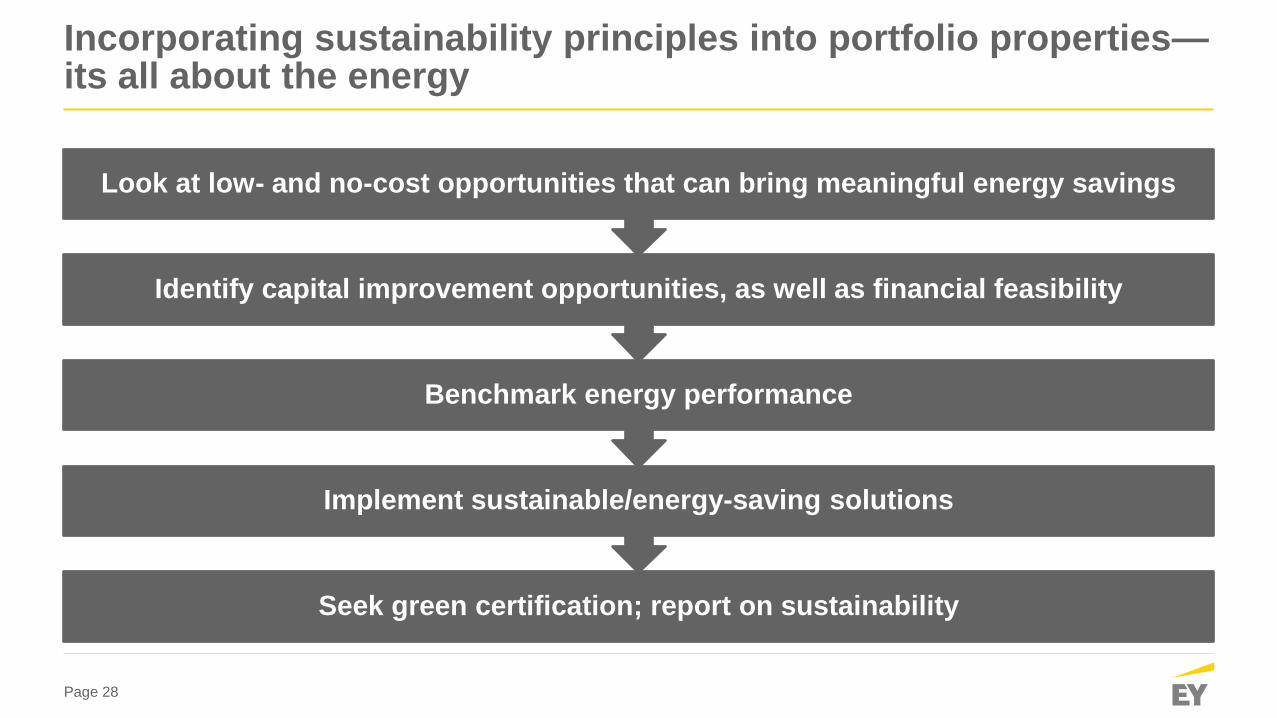

Incorporating sustainability principles into portfolio properties—its all about the energy

Seek green certification; report on sustainability

Implement sustainable/energy-saving solutions

Benchmark energy performance

Identify capital improvement opportunities, as well as financial feasibility

Look at low- and no-cost opportunities that can bring meaningful energy savings

Page 29

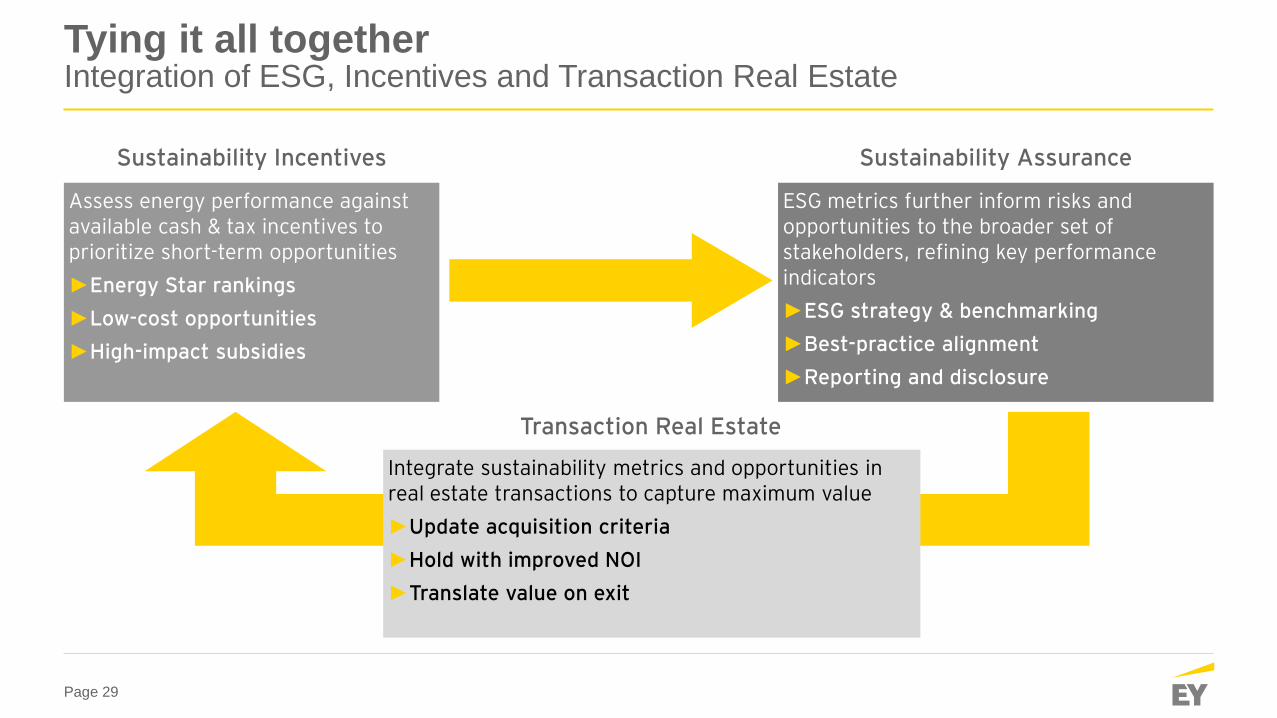

Tying it all together Integration of ESG, Incentives and Transaction Real Estate

Assess energy performance against available cash & tax incentives to prioritize short-term opportunities ►Energy Star rankings ►Low-cost opportunities ►High-impact subsidies

ESG metrics further inform risks and opportunities to the broader set of stakeholders, refining key performance indicators ►ESG strategy & benchmarking ►Best-practice alignment ►Reporting and disclosure

Integrate sustainability metrics and opportunities in real estate transactions to capture maximum value ►Update acquisition criteria ►Hold with improved NOI ►Translate value on exit

Sustainability Incentives Sustainability Assurance

Transaction Real Estate

Page 30

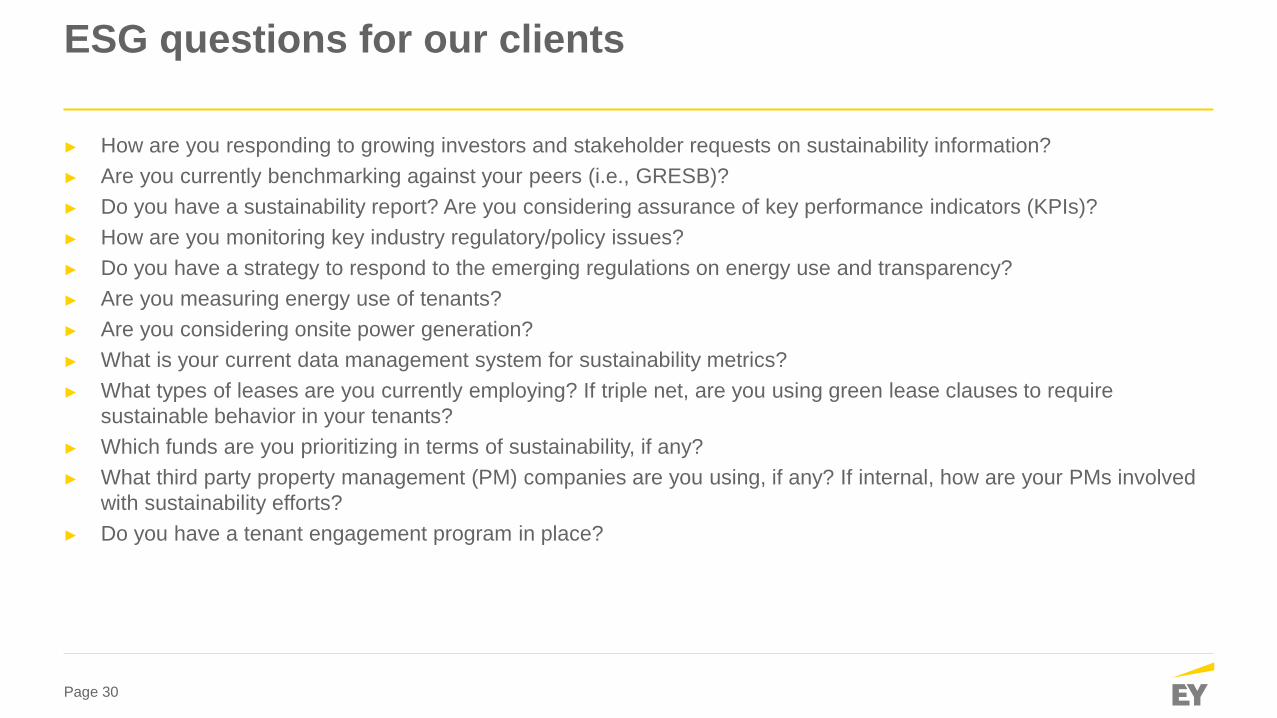

ESG questions for our clients

► How are you responding to growing investors and stakeholder requests on sustainability information? ► Are you currently benchmarking against your peers (i.e., GRESB)? ► Do you have a sustainability report? Are you considering assurance of key performance indicators (KPIs)? ► How are you monitoring key industry regulatory/policy issues? ► Do you have a strategy to respond to the emerging regulations on energy use and transparency? ► Are you measuring energy use of tenants? ► Are you considering onsite power generation? ► What is your current data management system for sustainability metrics? ► What types of leases are you currently employing? If triple net, are you using green lease clauses to require

sustainable behavior in your tenants? ► Which funds are you prioritizing in terms of sustainability, if any? ► What third party property management (PM) companies are you using, if any? If internal, how are your PMs involved

with sustainability efforts? ► Do you have a tenant engagement program in place?

Page 31 Page 31

For additional information please contact:

Terry Hudgins Senior Manager, LEED-AP®

Green Building & Incentives Ernst & Young LLP ► +1 (480) 620-4795 ► [email protected]

Chris Doherty Senior Manager Sustainability Services Ernst & Young LLP ► +1 (415) 769-7918 ► [email protected]