Embed Size (px)

Citation preview

$67,435,000Energy Efficiency Revenue Bonds

Series 2011

Sustainable Energy Utility, Inc.

Post Pricing Commentary August 1, 2011

Table of Contents

1. Preliminary and Final Official Statement Covers

2. Preliminary and Final Pricing Wires

3. Pricing Spreads and Comparable Transactions

4. Distribution Analysis

5. Rating Reports

6. Market Commentary

7. Marketing Materials and Media

8. Working Group

9. Final Numbers

10. Closing Memo

Section

Preliminary and Final Official Statement Covers

This

Pre

limin

ary

Offi

cial

Sta

tem

ent a

nd th

e in

form

atio

n co

ntai

ned

here

in a

re s

ubje

ct to

com

plet

ion

and

amen

dmen

t. U

nder

no

circ

umst

ance

s sh

all t

his

Prel

imin

ary

Offi

cial

Sta

tem

ent c

onst

itute

an

offe

r to

sell o

r the

sol

icita

tion

of a

n of

fer t

o bu

y, no

r sha

ll the

re b

e an

y sa

le o

f the

Bon

ds in

any

juris

dict

ion

in w

hich

suc

h of

fer,

solic

itatio

n or

sal

e w

ould

be

unla

wfu

l prio

r to

regi

stra

tion

or q

ualifi

catio

n un

der t

he s

ecur

ities

law

s of

any

suc

h ju

risdi

ctio

n. T

he Is

suer

has

dee

med

this

Pre

limin

ary

Offi

cial

Sta

tem

ent fi

nal,

as o

f its

dat

e, e

xcep

t for

info

rmat

ion

perm

itted

to b

e om

itted

by

Rul

e 15

c2‑1

2 of

the

Secu

ritie

s an

d Ex

chan

ge C

omm

issi

on.

PRELIMINARY OFFICIAL STATEMENT DATED JULY 18, 2011

NEW ISSUE-BOOK-ENTRY ONLY RATINGS: See “RATINGS herein”

In the opinion of Drinker Biddle & Reath LLP, Bond Counsel, under existing law as currently enacted and construed, interest on the Bonds is excluded from gross income for federal income tax purposes and is not a specific item of tax preference for purposes of the individual and corporate federal alternative minimum tax; but, interest on the Bonds will be included in “adjusted current earnings” in computing alternative minimum taxable income with respect to certain corporations. The Bonds, and the interest payable thereon, are exempt from taxation by the State of Delaware or any political subdivision thereof. See “CERTAIN TAX MATTERS” herein.

$62,640,000*SUSTAINABLE ENERGY UTILITY, INC.

Energy Efficiency Revenue Bonds, Series 2011Dated: Date of Issuance Due: September 15, as shown on inside cover

The Sustainable Energy Utility, Inc. Energy Efficiency Revenue Bonds, Series 2011 (the “Bonds”) are being issued by Sustainable Energy Utility, Inc. (the “Issuer”), a Delaware nonprofit corporation created by and for the benefit of the State of Delaware (the “State”) pursuant to the Delaware Energy Act, 29 Del. C. §8059 (the “SEU Authorizing Act”), under a Trust Indenture dated as of August 1, 2011, between the Issuer and Citibank N.A. Agency & Trust, New York, New York (the “Trustee”). Proceeds of the Bonds will be used to fund projects (the “Projects”) consisting of the design, construction and installation of certain energy conservation measures at facilities of certain State agencies (collectively and as further described herein, the “Agencies”). Such funds will be applied to pay the costs of the Projects on behalf of the Agencies in accordance with separate Guaranteed Energy Savings Agreements between the Agencies and the energy service companies that have contracted with the Agencies to implement the Projects (the “Contractors”). See “THE PROJECTS” herein.

The Bonds will be issued as fully registered bonds in the name of Cede & Co., as registered owner and nominee of The Depository Trust Company, New York, New York (“DTC”). DTC is securities depository for the Bonds. Purchases of the Bonds will be made in book-entry form and purchasers will not receive certificates representing their interests in the Bonds purchased. Principal and redemption price if any of, and interest on, the Bonds are payable by the Trustee to DTC which in turn will remit such principal and interest payments to participants for subsequent disbursement to the beneficial owners of the Bonds. As long as Cede & Co. is the registered owner as nominee of DTC, payments on the Bonds will be made to such registered owner, and disbursal of such payments to beneficial owners will be the responsibility of DTC and its participants. See “BOOK-ENTRY ONLY SYSTEM” herein.

The Bonds will be available to purchasers in denominations of $5,000 and any integral multiple of $5,000. Interest, at the rates set forth on the inside cover hereof, is payable on March 15, 2012 and on each September 15 and March 15 thereafter. The Bonds are subject to redemption as described herein. See “THE BONDS – Redemption” herein.

The Bonds are limited obligations of the Issuer payable solely from the Trust Estate, primarily consisting of the Installment Payments (as defined herein) to be made to the Trustee (as assignee of the Issuer) by, or on behalf of, the Agencies in consideration of the Issuer issuing the Bonds and making the proceeds thereof available to pay the costs of the Projects on behalf of the Agencies. The Agencies’ obligations to make Installment Payments are subject to appropriation by the State. See “SECURITY FOR AND SOURCES OF PAYMENT OF THE BONDS.”

EXCEPT AS DESCRIBED HEREIN WITH RESPECT TO THE PAYMENT OF MONEYS WHEN, AS AND IF APPROPRIATED TO THE AGENCIES FOR SUCH PURPOSE, NEITHER THE STATE NOR ANY POLITICAL SUBDIvISION THEREOF SHALL BE OBLIGATED TO MAKE PAYMENTS ON THE BONDS. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OR OF ANY POLITICAL SUBDIvISION THEREOF IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE INTEREST ON BONDS. THE ISSUANCE OF THE BONDS SHALL NOT DIRECTLY OR INDIRECTLY OR CONTINGENTLY OBLIGATE THE STATE OR ANY POLITICAL SUBDIvISION THEREOF TO LEvY OR TO PLEDGE ANY FORM OF TAXATION WHATEvER THEREFOR, OR TO MAKE ANY APPROPRIATION FOR THEIR PAYMENT.

The Bonds are offered when, as and if issued and accepted by the Underwriter subject to the approval of legality by Drinker Biddle & Reath LLP, Bond Counsel, and to certain other conditions. Certain legal matters will be passed upon for the Issuer by Murphy and Landon, Wilmington, Delaware, and for the State Agencies that are not institutions of higher learning by the Department of Justice, State of Delaware as counsel; for Delaware State University and Delaware Technical Community College by their respective general counsels; and for the Underwriter by Miller, Canfield, Paddock and Stone, P.L.C. The Bonds are expected to be delivered to DTC in book-entry form on or about August __, 2011.

Citi*Preliminary, subject to change.

MATURITY SCHEDULE

Due September 15

Principal Amount*

Interest Rate Yield Price

CUSIP**

2013 $1,430,000 % % 2014 1,545,000 2015 2,950,000 2016 2,900,000 2017 3,055,000 2018 1,840,000 2019 1,975,000 2020 2,080,000 2021 2,220,000 2022 2,405,000 2023 2,570,000 2024 2,745,000 2025 2,935,000 2026 3,135,000 2027 3,345,000 2028 3,565,000 2029 3,805,000 2030 4,060,000 2031 4,395,000

$9,685,000* ____% Term Bonds Due September 15, 2034, Priced @ _____% to Yield ______%

* Preliminary, subject to change.

** Copyright 2011, American Bankers Association. CUSIP data herein are provided by Standard & Poor’s CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. The CUSIP numbers listed above are being provided solely for the convenience of bondholders and neither the Issuer nor the Agencies make any representation with respect to such number or undertakes any responsibility for their accuracy. The CUSIP numbers are subject to being changed after the issuance of the Bonds as a result of various subsequent actions including, but not limited to, a refunding in whole or in part of the Bonds.

NEW ISSUE-BOOK-ENTRY ONLY RATINGS: See “RATINGS herein”

In the opinion of Drinker Biddle & Reath LLP, Bond Counsel, under existing law as currently enacted and construed, interest on the Bonds is excluded from gross income for federal income tax purposes and is not a specific item of tax preference for purposes of the individual and corporate federal alternative minimum tax; but, interest on the Bonds will be included in “adjusted current earnings” in computing alternative minimum taxable income with respect to certain corporations. The Bonds, and the interest payable thereon, are exempt from taxation by the State of Delaware or any political subdivision thereof. See “CERTAIN TAX MATTERS” herein.

$67,435,000SUSTAINABLE ENERGY UTILITY, INc.

Energy Efficiency Revenue Bonds, Series 2011

Dated: Date of Issuance Due: September 15, as shown on inside cover

The Sustainable Energy Utility, Inc. Energy Efficiency Revenue Bonds, Series 2011 (the “Bonds”) are being issued by Sustainable Energy Utility, Inc. (the “Issuer”), a Delaware nonprofit corporation created by and for the benefit of the State of Delaware (the “State”) pursuant to the Delaware Energy Act, 29 Del. C. §8059 (the “SEU Authorizing Act”), under a Trust Indenture dated as of August 1, 2011, between the Issuer and Citibank, N.A., New York, New York (the “Trustee”). Proceeds of the Bonds will be used to fund projects (the “Projects”) consisting of the design, construction and installation of certain energy conservation measures at facilities of certain State agencies (collectively and as further described herein, the “Agencies”). Such funds will be applied to pay the costs of the Projects on behalf of the Agencies in accordance with separate Guaranteed Energy Savings Agreements between the Agencies and the energy service companies that have contracted with the Agencies to implement the Projects (the “Contractors”). See “THE PROJECTS” herein.

The Bonds will be issued as fully registered bonds in the name of Cede & Co., as registered owner and nominee of The Depository Trust Company, New York, New York (“DTC”). DTC is securities depository for the Bonds. Purchases of the Bonds will be made in book-entry form and purchasers will not receive certificates representing their interests in the Bonds purchased. Principal and redemption price if any of, and interest on, the Bonds are payable by the Trustee to DTC which in turn will remit such principal and interest payments to participants for subsequent disbursement to the beneficial owners of the Bonds. As long as Cede & Co. is the registered owner as nominee of DTC, payments on the Bonds will be made to such registered owner, and disbursal of such payments to beneficial owners will be the responsibility of DTC and its participants. See “BOOK-ENTRY ONLY SYSTEM” herein.

The Bonds will be available to purchasers in denominations of $5,000 and any integral multiple of $5,000. Interest, at the rates set forth on the inside cover hereof, is payable on March 15, 2012 and on each September 15 and March 15 thereafter. The Bonds are subject to redemption as described herein. See “THE BONDS – Redemption” herein.

The Bonds are limited obligations of the Issuer payable solely from the Trust Estate, primarily consisting of the Installment Payments (as defined herein) to be made to the Trustee (as assignee of the Issuer) by, or on behalf of, the Agencies in consideration of the Issuer issuing the Bonds and making the proceeds thereof available to pay the costs of the Projects on behalf of the Agencies. The Agencies’ obligations to make Installment Payments are subject to appropriation by the State. See “SECURITY FOR AND SOURCES OF PAYMENT OF THE BONDS.”

EXCEPT AS DESCRIBED HEREIN WITH RESPECT TO THE PAYMENT OF MONEYS WHEN, AS AND IF APPROPRIATED TO THE AGENCIES FOR SUCH PURPOSE, NEITHER THE STATE NOR ANY POLITICAL SUBDIvISION THEREOF SHALL BE OBLIGATED TO MAKE PAYMENTS ON THE BONDS. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OR OF ANY POLITICAL SUBDIvISION THEREOF IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE INTEREST ON BONDS. THE ISSUANCE OF THE BONDS SHALL NOT DIRECTLY OR INDIRECTLY OR CONTINGENTLY OBLIGATE THE STATE OR ANY POLITICAL SUBDIvISION THEREOF TO LEvY OR TO PLEDGE ANY FORM OF TAXATION WHATEvER THEREFOR, OR TO MAKE ANY APPROPRIATION FOR THEIR PAYMENT.

The Bonds are offered when, as and if issued and accepted by the Underwriter subject to the approval of legality by Drinker Biddle & Reath LLP, Bond Counsel, and to certain other conditions. Certain legal matters will be passed upon for the Issuer by Drinker Biddle & Reath LLP; for the State Agencies that are not institutions of higher learning by the Department of Justice, State of Delaware as counsel; for Delaware State University and Delaware Technical Community College by their respective general counsels; and for the Underwriter by Miller, Canfield, Paddock and Stone, P.L.C. Becker Capital and Finance, New York, New York, and NW Financial Group, LLC, Jersey City, New Jersey, have served as financial advisors to the Issuer in connection with the issuance of the Bonds. The Bonds are expected to be delivered to DTC in book-entry form on or about August 1, 2011.

citi

Dated July 25, 2011

$67,435,000

Sustainable Energy Utility, Inc. Energy Efficiency Revenue Bonds, Series 2011

MATURITY SCHEDULE

Due September 15

Principal Amount

Interest Rate Yield Price

CUSIP**

2013 $1,775,000 2.000% 0.650% 102.840 86932UAA3 2014 1,845,000 3.000 1.000 106.132 86932UAB1 2015 3,325,000 3.000 1.280 106.884 86932UAC9 2016 400,000 3.000 1.640 106.654 86932UAD7 2016 2,840,000 5.000 1.640 116.441 86932UAW5 2017 300,000 4.000 2.040 111.224 86932UAE5 2017 3,135,000 5.000 2.040 116.952 86932UAX3 2018 2,285,000 4.000 2.460 110.002 86932UAF2 2019 2,405,000 5.000 2.790 115.959 86932UAG0 2020 570,000 3.000 3.060 99.523 86932UAH8 2020 2,000,000 5.000 3.060 115.336 86932UAZ8 2021 2,655,000 5.000 3.230 115.175 86932UAJ4 2022 2,805,000 5.000 3.440* 113.235 86932UAK1 2023 2,940,000 5.000 3.600* 111.784 86932UAL9 2024 3,080,000 3.500 3.770 97.222 86932UAM7 2025 3,175,000 5.000 3.900* 109.122 86932UAN5 2026 3,325,000 5.000 3.990* 108.339 86932UAP0 2027 700,000 4.000 4.080 99.057 86932UAQ8 2027 2,780,000 5.000 4.080* 107.562 86932UAY1 2028 3,630,000 5.000 4.170* 106.792 86932UAR6 2029 3,810,000 4.250 4.440 97.647 86932UAS4 2030 3,960,000 5.000 4.290* 105.775 86932UAT2 2031 4,215,000 5.000 4.370* 105.104 86932UAU9

$9,480,000 5.00% Term Bonds Due September 15, 2034, Priced @ 103.612 to Yield 4.550%*, CUSIP 86932UAV7

* Yield calculated to call date of September 15, 2021.

** Copyright 2011, American Bankers Association. CUSIP data herein are provided by Standard & Poor’s CUSIP Service Bureau, a

division of The McGraw-Hill Companies, Inc. The CUSIP numbers listed above are being provided solely for the convenience of bondholders and neither the Issuer nor the Agencies make any representation with respect to such number or undertakes any responsibility for their accuracy. The CUSIP numbers are subject to being changed after the issuance of the Bonds as a result of various subsequent actions including, but not limited to, a refunding in whole or in part of the Bonds.

Preliminary and Final Pricing Wires

********************************************************************************

Monday, July 25, 2011 10:48AM ========================================MSS Wire #273397 == Preliminary Pricing Wire ==MSS Master Message #3216512 ========================================TO: Citigroup Global Markets Inc (Manager)

RE: $67,670,000*SUSTAINABLE ENERGY UTILITY, INC. (Delaware)Energy Efficiency Revenue BondsSeries 2011

MOODY'S: Aa2 S&P: AA+ FITCH: NR

DATED:08/01/2011 FIRST COUPON:03/15/2012

DUE: 09/15

ADD'L TAKEDOWN

MATURITY AMOUNT* COUPON PRICE ( Pts )09/15/2013 1,825M 2.00% 0.70 1/4

(Approx. $ Price 102.733)09/15/2014 1,915M 3.00% 1.00 1/4 (Approx. $ Price 106.132)

09/15/2015 3,420M 3.00% 1.30 3/8 (Approx. $ Price 106.800)

09/15/2016 3,350M 3.00% 1.64 3/8 (Approx. $ Price 106.654)

09/15/2017 3,490M 4.00% 2.04 1/2 (Approx. $ Price 111.224)

09/15/2018 2,320M 4.00% 2.46 1/2 (Approx. $ Price 110.002)

09/15/2019 2,450M 5.00% 2.79 1/2 (Approx. $ Price 115.959)

09/15/2020 2,580M 3.00% 3.06 1/2 (Approx. $ Price 99.523)

09/15/2021 2,640M 5.00% 3.23 1/2 (Approx. $ Price 115.175)

09/15/2022 2,800M 5.00% 3.42 1/2

(Approx. $ Price PTC 09/15/2021 113.418 Approx. YTM 3.530 )09/15/2023 2,930M 5.00% 3.58 1/2 (Approx. $ Price PTC 09/15/2021 111.964 Approx. YTM 3.761 )

09/15/2024 3,065M 3.50% 3.72 1/2 (Approx. $ Price 97.729)

09/15/2025 3,170M 5.00% 3.85 1/2 (Approx. $ Price PTC 09/15/2021 109.560 Approx. YTM 4.101 )

09/15/2026 3,315M 5.00% 3.94 1/2

(Approx. $ Price PTC 09/15/2021 108.773 Approx. YTM 4.209 )09/15/2027 3,465M 4.00% 4.03 1/2 (Approx. $ Price 99.643)

09/15/2028 3,600M 5.00% 4.12 1/2 (Approx. $ Price PTC 09/15/2021 107.219 Approx. YTM 4.395 )

09/15/2029 3,765M 5.00% 4.19 1/2 (Approx. $ Price PTC 09/15/2021 106.621 Approx. YTM 4.463 )

09/15/2030 3,950M 5.00% 4.26 1/2

(Approx. $ Price PTC 09/15/2021 106.028 Approx. YTM 4.525 )09/15/2031 4,195M 5.00% 4.35 1/2 (Approx. $ Price PTC 09/15/2021 105.271 Approx. YTM 4.595 )

09/15/2034 9,425M 5.00% 4.58 1/2 (Approx. $ Price PTC 09/15/2021 103.366 Approx. YTM 4.758 )

---------------------------------------

CALL FEATURES: Optional call in 09/15/2021 @ 100.00

---------------------------------------

* - APPROXIMATE SUBJECT TO CHANGE

Order period until today 12:45 PM, Eastern, Monday, 07/25/11.Please use Electronic Order Entry to enter orders or call (212) 723-7093 .

The manager reserves the right to terminate or extend the order period prior to or laterthan the above-mentioned time and date and to confirm bonds at their discretion.

PRIORITY OF ORDERS AS FOLLOWS:1. Delaware Retail2. Member

The compliance addendum MSRB Rule G-11 will apply.

Delivery is firm for Monday, August 1, 2011.

This Issue is book entry. This issue is clearing through DTC.

Citigroup Global Markets Inc

By: Citigroup Global Markets Inc New York, NY

Monday, July 25, 2011 10:48AM

********************************************************************************

********************************************************************************

Tuesday, July 26, 2011 9:02AM ========================================MSS Wire #273436 == Final Pricing Wire ==MSS Master Message #3216882 ========================================TO: Citigroup Global Markets Inc (Manager)

RE: $67,435,000SUSTAINABLE ENERGY UTILITY, INC. (Delaware)Energy Efficiency Revenue BondsSeries 2011

WE HAVE RECEIVED THE WRITTEN AWARD.

DELIVERY IS FIRM FOR 08/01/2011.

CUSIP AND TRADE DATE WIRE WILL FOLLOW SHORTLY.

MOODY'S: Aa2 S&P: AA+ FITCH: NR

DATED:08/01/2011 FIRST COUPON:03/15/2012

DUE: 09/15

ADD'L

TAKEDOWNMATURITY AMOUNT COUPON PRICE ( Pts )09/15/2013 1,775M 2.00% 0.65 1/4 (Approx. $ Price 102.840)

09/15/2014 1,845M 3.00% 1.00 1/4 (Approx. $ Price 106.132)

09/15/2015 3,325M 3.00% 1.28 3/8 (Approx. $ Price 106.884)

09/15/2016 400M 3.00% 1.64 3/8 (Approx. $ Price 106.654)

09/15/2016 2,840M 5.00% 1.64 3/8 (Approx. $ Price 116.441)

09/15/2017 300M 4.00% 2.04 1/2 (Approx. $ Price 111.224)

09/15/2017 3,135M 5.00% 2.04 1/2 (Approx. $ Price 116.952)

09/15/2018 2,285M 4.00% 2.46 1/2 (Approx. $ Price 110.002)

09/15/2019 2,405M 5.00% 2.79 1/2 (Approx. $ Price 115.959)

09/15/2020 570M 3.00% 3.06 1/2 (Approx. $ Price 99.523)

09/15/2020 2,000M 5.00% 3.06 1/2 (Approx. $ Price 115.336)

09/15/2021 2,655M 5.00% 3.23 1/2 (Approx. $ Price 115.175)

09/15/2022 2,805M 5.00% 3.44 1/2 (Approx. $ Price PTC 09/15/2021 113.235 Approx. YTM 3.549 )

09/15/2023 2,940M 5.00% 3.60 1/2

(Approx. $ Price PTC 09/15/2021 111.784 Approx. YTM 3.779 )09/15/2024 3,080M 3.50% 3.77 1/2 (Approx. $ Price 97.222)

09/15/2025 3,175M 5.00% 3.90 1/2 (Approx. $ Price PTC 09/15/2021 109.122 Approx. YTM 4.140 )

09/15/2026 3,325M 5.00% 3.99 1/2 (Approx. $ Price PTC 09/15/2021 108.339 Approx. YTM 4.247 )

09/15/2027 700M 4.00% 4.08 1/2

(Approx. $ Price 99.057)09/15/2027 2,780M 5.00% 4.08 1/2 (Approx. $ Price PTC 09/15/2021 107.562 Approx. YTM 4.342 )

09/15/2028 3,630M 5.00% 4.17 1/2 (Approx. $ Price PTC 09/15/2021 106.792 Approx. YTM 4.429 )

09/15/2029 3,810M 4.25% 4.44 1/2 (Approx. $ Price 97.647)

09/15/2030 3,960M 5.00% 4.29 1/2

(Approx. $ Price PTC 09/15/2021 105.775 Approx. YTM 4.544 )09/15/2031 4,215M 5.00% 4.37 1/2 (Approx. $ Price PTC 09/15/2021 105.104 Approx. YTM 4.608 )

09/15/2034 9,480M 5.00% 4.55 1/2 (Approx. $ Price PTC 09/15/2021 103.612 Approx. YTM 4.741 )

---------------------------------------

CALL FEATURES: Optional call in 09/15/2021 @ 100.00

---------------------------------------

Sinking Fund Schedule

2034 Term Bond

09/15/2032 4,32509/15/2033 2,63509/15/2034 2,520

PRIORITY OF ORDERS AS FOLLOWS:1. Delaware Retail2. Member

The compliance addendum MSRB Rule G-11 will apply.

The Award is expected on Monday, July 25, 2011 at 8:24PM Eastern .

Delivery is firm for Monday, August 1, 2011.

This Issue is book entry. This issue is clearing through DTC.

Award: 07/25/2011Award Time: 8:24PM EasternDelivery: 08/01/2011 (Firm)Initial trade:Date of Execution:Time of Execution:

MATURITY CUSIP COUPON ---------- --------- ------ 09/15/2013 86932UAA3 2.000 09/15/2014 86932UAB1 3.000 09/15/2015 86932UAC9 3.000 09/15/2016 86932UAD7 3.000

09/15/2016 86932UAW5 5.000 09/15/2017 86932UAE5 4.000 09/15/2017 86932UAX3 5.000 09/15/2018 86932UAF2 4.000 09/15/2019 86932UAG0 5.000 09/15/2020 86932UAH8 3.000 09/15/2020 86932UAZ8 5.000 09/15/2021 86932UAJ4 5.000 09/15/2022 86932UAK1 5.000

09/15/2023 86932UAL9 5.000 09/15/2024 86932UAM7 3.500 09/15/2025 86932UAN5 5.000 09/15/2026 86932UAP0 5.000 09/15/2027 86932UAQ8 4.000 09/15/2027 86932UAY1 5.000 09/15/2028 86932UAR6 5.000 09/15/2029 86932UAS4 4.250 09/15/2030 86932UAT2 5.000 09/15/2031 86932UAU9 5.000 09/15/2034 86932UAV7 5.000

Citigroup Global Markets Inc

By: Citigroup Global Markets Inc New York, NY

Tuesday, July 26, 2011 9:02AM

********************************************************************************

Pricing Spreads and Comparable Transactions

SEU Comparable TransactionsThe SEU financing priced favorably to other appropriation backed deals because of the strength of the State of Delaware.

5

Issuer: Sustainable Energy Utility, Inc. Tobacco Settlement Financing Corp (NY) New York State Housing Finance AgencySeries: Energy Efficiency Revenue Bonds, Series 2011 Series 2011B (Appropriation) 2011 Series A (Appropriation)Size: $67.435 million $543.595 million $71.015 million

Ratings: Aa2 / AA+ / NR NR / AA‐ / AA‐ NR / AA‐ / AA‐Call Date: 9/15/2021 Non‐Call Non‐CallSale Date: 7/25/2011 6/28/2011 6/23/2011

Year Par CouponSpread

to MMD Par CouponSpread

to MMD Par CouponSpread

to MMD

2012 16,320 2.50% Sealed2013 1,775 2.00% 25 81,595 4.00% 51 12,600 5.00% 40 2014 1,845 3.00% 35 85,000 5.00% 73 12,600 5.00% 55 2015 3,325 3.00% 38 89,000 5.00% 83 7,705 5.00% 65 2016 3,240 3%/5% 45 94,000 5.00% 85 8,060 3.00% 75 2017 3,435 4%/5% 50 98,000 5.00% 85 8,475 5.00% 78 2018 2,285 4.00% 53 96,000 5.00% 85 900 5.00% 80 2019 2,405 5.00% 53 1,875 5.00% 79 2020 2,570 3%/5% 55 2,480 5.00% 80 2021 2,655 5.00% 55 2022 2,805 5.00% 57 2023 2,940 5.00% 57 2024 3,080 3.50% 60 2025 3,175 5.00% 60 2026 3,325 5.00% 60 2027 3,480 4%/5% 60 2028 3,630 5.00% 60 2029 3,810 4.25% 78 2030 3,960 5.00% 54 2031 4,215 5.00% 52 203220332034 9,480 5.00% 41

*2029 maturity priced with discount structure

SEU Comparable Transactions (Cont’d)

Given the relative scarcity of the Delaware name, the SEU’s bonds were in high demand.

6

Issuer: Sustainable Energy Utility, Inc. City of Jacksonville, Florida The Turnpike Authority of KentuckySeries: Energy Efficiency Revenue Bonds, Series 2011 Series 2011B (Appropriation) 2011 Series A (Appropriaton)Size: $67.435 million $86.600 million $115.175 million

Ratings: Aa2 / AA+ / NR Aa2 / AA‐ / AA Aa2 / AA+ / AA‐Call Date: 9/15/2021 Non‐Call 7/1/2021Sale Date: 7/25/2011 6/9/2011 4/6/2011

Year Par CouponSpread

to MMD Par CouponSpread

to MMD Par CouponSpread

to MMD

20122013 1,775 2.00% 25 650 3.00% 76 2014 1,845 3.00% 35 1,100 4.00% 79 2015 3,325 3.00% 38 9,200 5.00% 82 2016 3,240 3%/5% 45 9,425 5.00% 84 13,170 5.00% 52 2017 3,435 4%/5% 50 14,675 5.00% 90 13,780 4.00% 59 2018 2,285 4.00% 53 10,275 5.00% 87 14,420 5.00% 67 2019 2,405 5.00% 53 11,675 5.00% 86 15,115 5.00% 68 2020 2,570 3%/5% 55 14,175 5.00% 82 3,785 5.00% 68 2021 2,655 5.00% 55 15,425 5.00% 79 3,960 5.00% 66 2022 2,805 5.00% 57 4,135 5.00% 66 2023 2,940 5.00% 57 4,295 4.13% 66 2024 3,080 3.50% 60 4,455 5.00% 66 2025 3,175 5.00% 60 4,615 5.00% 68 2026 3,325 5.00% 60 4,920 5.00% 70 2027 3,480 4%/5% 60 5,175 5.00% 70 2028 3,630 5.00% 60 5,435 5.00% 70 2029 3,810 4.25% 78 5,685 5.00% 70 2030 3,960 5.00% 54 5,945 5.00% 68 2031 4,215 5.00% 52 6,285 4.88% 64 203220332034 9,480 5.00% 41

*2029 maturity priced with discount structure

Distribution Analysis

Sustainable Energy Utility, Inc.

Energy Efficiency Revenue Bonds, Series 2011

Orders and Allotments by Order Type (000’s)

Member63%

Retail5%Citi

Underwritten32%

Allotment % Breakdown by Order Type

Order Type Orders Allotments

Retail: 3,365$ 3,265$ Member: 79,175 42,760 Citi Underwritten: - 21,410

Total: 82,540$ 67,435$

Sustainable Energy Utility, Inc.

Energy Efficiency Revenue Bonds, Series 2011

Orders and Allotments by Maturity(000’s)

*Coverage Factors <1.0x indicate maturities underwritten by Citi

Maturity Orders Allotments Coverage

9/15/2013 7,325$ 1,775$ 4.1x 9/15/2014 2,640 1,845 1.4x 9/15/2015 7,340 3,325 2.2x 9/15/2016 700 3,240 0.2x 9/15/2017 300 3,435 0.1x 9/15/2018 2,820 2,285 1.2x 9/15/2019 4,900 2,405 2.0x 9/15/2020 585 2,570 0.2x 9/15/2021 5,530 2,655 2.1x 9/15/2022 2,805 2,805 1.0x 9/15/2023 2,980 2,940 1.0x 9/15/2024 2,005 3,080 0.7x 9/15/2025 - 3,175 - 9/15/2026 450 3,325 0.1x 9/15/2027 700 3,480 0.2x 9/15/2028 - 3,630 - 9/15/2029 3,810 3,810 1.0x 9/15/2030 3,960 3,960 1.0x 9/15/2031 4,215 4,215 1.0x 9/15/2034 29,475 9,480 3.1x

Total: 82,540$ 67,435$ 1.2x

Sustainable Energy Utility, Inc.

Energy Efficiency Revenue Bonds, Series 2011

Orders and Allotments by Buyer(000’s)

Unfilled orders are typically the result of oversubscribed maturities:– Serial Bonds: 2013 – 2015, 2018 – 2019, 2021 – 2034 Term Bond

Buyers Orders Allotments

Citi Underwritten -$ 21,410$ Definitive Capital 22,690 9,580 Lord Abbet 11,745 6,315 Gannett 5,735 5,695 First New York Securities 3,810 3,810 Merrill TOB 9,425 3,750 Retail 3,365 3,265 Breckenridge Capital 2,450 2,405 Sterling Asset Management 3,740 1,545 Wells Fargo 1,500 1,485 Cutwater Asset Management 3,420 1,425 Neuberger Berman 4,465 1,425 Wilmington Trust 3,420 1,400 RBC Wealth Management 1,000 1,000 Edward Jones 1,000 900 Lee Munder Investments 875 875 Wells Capital Management 1,825 450 JP Morgan Asset Management 1,825 450 Columbia Management 250 250

Total: 82,540$ 67,435$

Ratings Reports

New Issue: MOODY'S ASSIGNS INITIAL RATING OF Aa2 TO APPROXIMATELY $70 MILLION DELAWARE SUSTAINABLE ENERGY UTILITY, INC. ENERGY EFFICIENCY REVENUE BONDS

Global Credit Research - 14 Jul 2011

OUTLOOK IS STABLE

Delaware (State of) State DE

Moody's Rating

Opinion

NEW YORK, Jul 14, 2011 -- Moody's Investors Service has assigned an initial rating of Aa2 to the Delaware Sustainable Energy Utility, Inc., Energy Efficiency Revenue Bonds, Series 2011, expected to be issued with a par amount of approximately $70 million. Proceeds will be used to finance projects for five state agencies or entities consisting of the design, construction and installation of certain energy efficiency measures, and to fund capitalized interest on the bonds. The bonds are paid by appropriations made from the State of Delaware's General Fund to those agencies or entities, and therefore the rating on the bonds is based on the general obligation rating of the State of Delaware (rated Aaa/Stable).

RATING RATIONALE

The rating reflects the strong legal structure; the involvement of several entities in the transaction, including state agencies, contractors, and a non-profit corporation; the potential for future legislative action reducing the revenue stream from which debt service payments are made; the lack of any other appropriation debt issued by the state; and some relative weakness regarding essentiality of the project. The rating is two notches off the state's rating of Aaa, reflecting both the need for legislative appropriation and the factors listed above.

CREDIT STRENGTHS

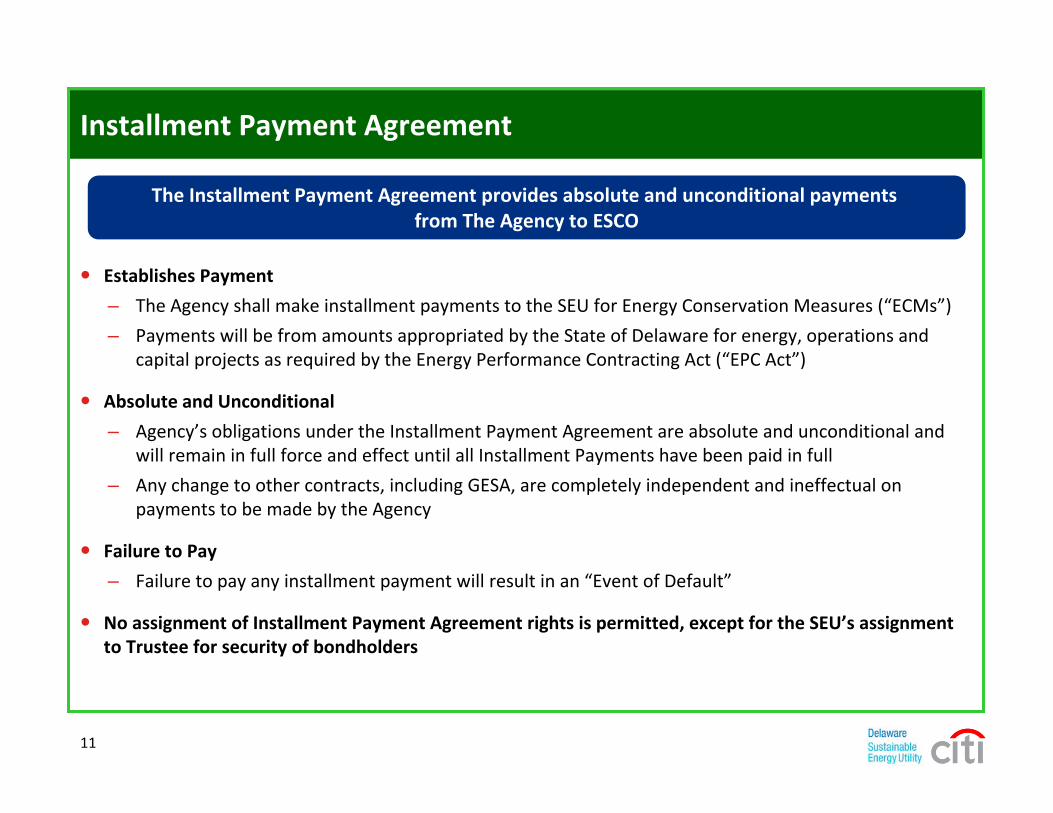

--Payments for debt service are absolute and unconditional obligations of agencies to pay under the Installment Payment Agreement

--The MOU strengthens flow of funds from state directly to trustee

--State has long history of strong and conservative management

CREDIT CHALLENGES

--This is a new and untested credit for the state, which has not previously issued appropriation-backed debt

--Distance from the state, with various agencies and other entities responsible for making installment payments (rather than the state appropriating for debt service), and the bonds issued by a non-profit corporation

--The involvement of private contractors and a non-profit corporation presents risks, although small, around potential bankruptcy situations

DETAILED CREDIT DISCUSSION

THE BONDS

The Sustainable Energy Utility, Inc. (SEU) is issuing approximately $70 million in bonds to finance energy efficiency projects. The bonds will have a maximum final maturity of 20 years after the end of the construction period, and will be fixed rate bonds. There will be capitalized interest through the construction period. No debt service reserve fund will be available for the bonds.

ISSUE RATINGEnergy Efficiency Revenue Bonds, Series 2011 Aa2 Sale Amount $70,000,000 Expected Sale Date 07/19/11 Rating Description Lease Appropriation

Page 1 of 4

7/18/2011http://www.moodys.com/research/MOODYS-ASSIGNS-INITIAL-RATING-OF-Aa2-TO-APPR...

OBLIGATION TO MAKE PAYMENTS IS GOVERNED BY INSTALLMENT PAYMENT AGREEMENT

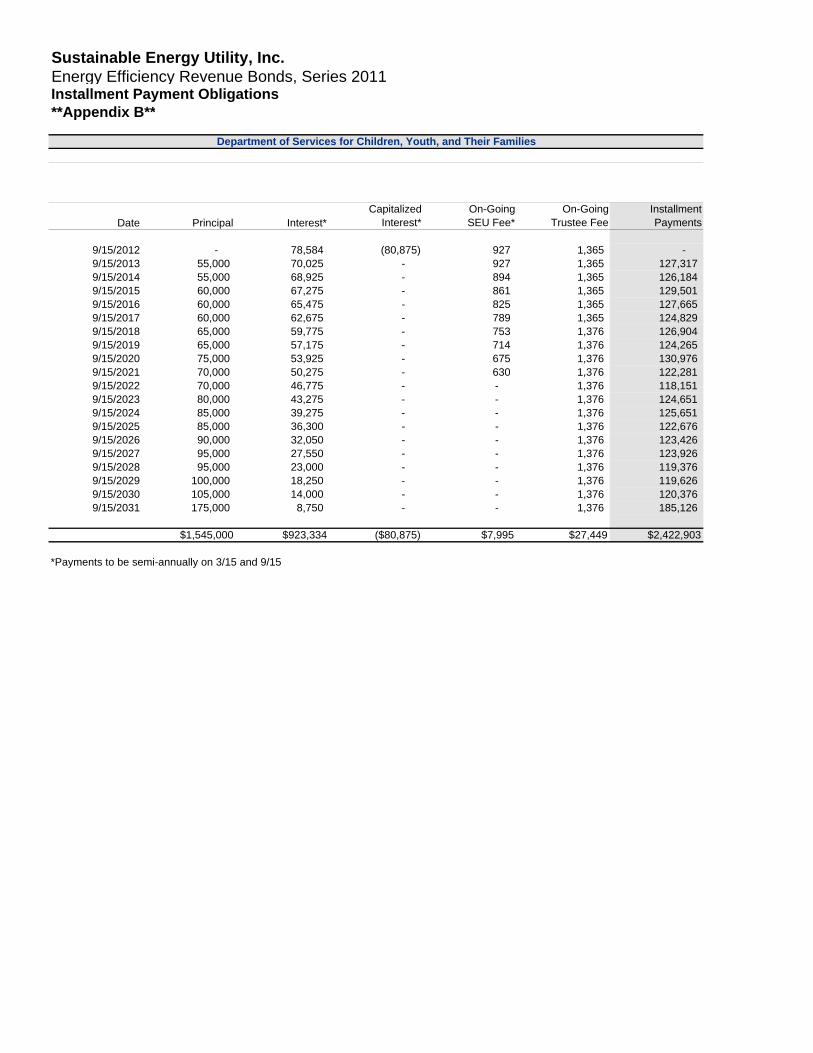

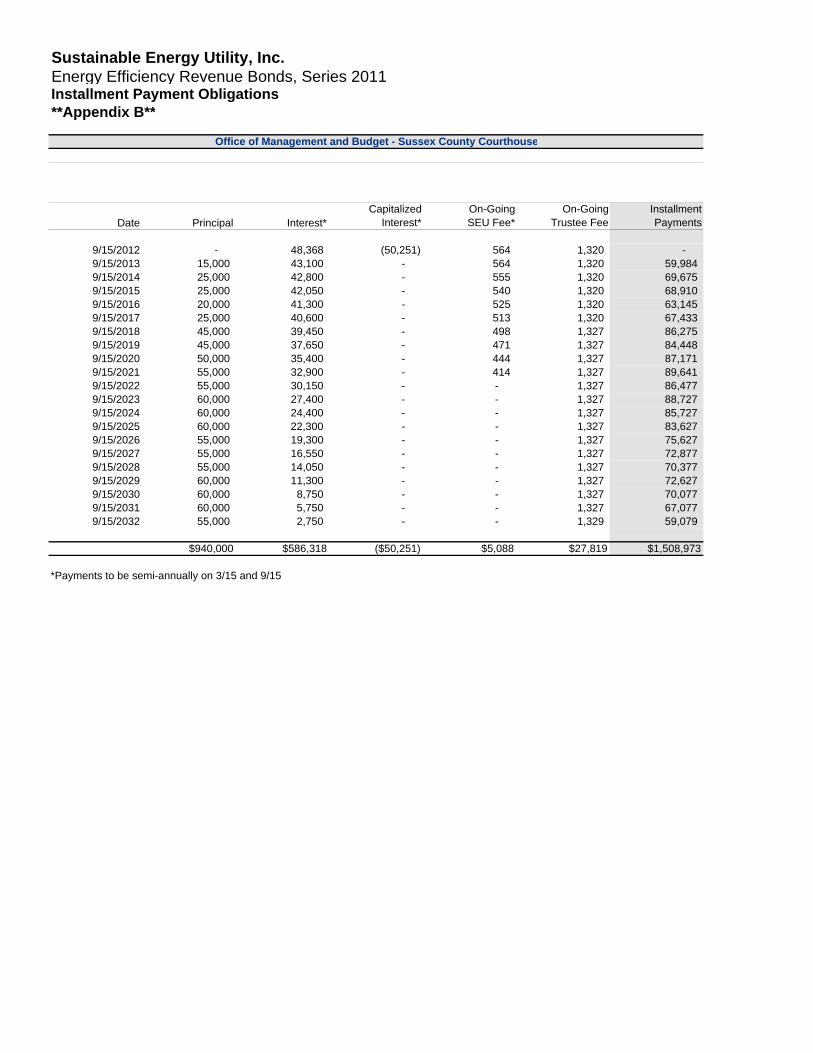

The State of Delaware created the Sustainable Energy Utility, Inc. (SEU) on June 28, 2007, as a non-profit tax-exempt 501(c)(3) organization to realize the state's legislated target of a 30% reduction in energy use by 2020. SEU expects to enter into a Construction Funding Agreement with a contractor and each agency involved in this transaction, whereby the SEU agrees to pay for energy efficiency investments. The agencies involved in this transaction are the Department of Corrections, the Department of Services for Children, Youth, and Their Families, the Office of Management and Budget, Delaware State University, and Delaware Technical and Community College.

After the issuance of these bonds, the contractor will use the proceeds to complete energy efficiency projects. The bonds are secured by payments under Installment Payment Agreements signed by the agencies and the SEU. In the agreements, the agencies pledge to make annual payments for installation of energy efficiency upgrades (and the SEU in turn assigns those payments to the trustee in the trust indenture). The obligation of each agency to make payment is absolute and unconditional, subject to appropriation. Installment payments are limited obligations of the agency payable from amounts appropriated by the state that are eligible for payment of the installment payments pursuant to the Energy Performance Contracting Act (Del Code Ann. Tit. 29 section 6974). The act states that "a governmental unit may use funds designated for operating, energy, or capital expenditures for any performance contract, including, without limitation, for purchases on an installment payment or lease purchase basis." We note that the revenues from which the installment payments are made are governed by the act, and could therefore be changed by a further act.

MEMORANDUMS OF UNDERSTANDING WITH STATE BUDGET OFFICE ADD STRENGTH

Each of the agencies involved is expected to enter into a Memorandum of Understanding (MOU) with the state Office of Management and Budget. The state in the MOU recognizes that the agency is obligated to make payments under the Installment Payment Agreement. It recognizes that pursuant to statute, payments from the state to an agency shall not be reduced as a result of a performance contract during the life of the contract. Further, the agency agrees to request the Installment Payment Agreement amounts in its annual budget request, and OMB agrees to work with the agency and the legislature to ensure appropriate levels of funding are received. Finally, the agency agrees it will transfer sufficient funds to make its payments at the beginning of each year, and OMB agrees it will initiate the transfer and make payments directly to the trustee, out of appropriated funds available to make the payments.

Each contractor is expected to enter into a Guaranteed Energy Savings Agreement (GESA) with the agencies, guaranteeing a targeted annual savings level for the term of the agreement. Each agency is therefore guaranteed to receive energy efficiencies and savings, unless the contractor declares bankruptcy. Each agency's obligations under its Installment Payment Agreement are absolute and unconditional, whether or not the guaranteed energy savings levels are achieved under its Guaranteed Energy Savings Agreement, provided that the Installment Payments are limited obligations of the agency, payable only from amounts appropriated by the state that are eligible for payment of the Installment Payments pursuant to the Energy Performance Contracting Act.

THE SEU

The SEU is a not-for-profit corporation formed by and for the benefit of the state pursuant to the SEU Authorizing Act, with full lawful power and authority to enter into the Indenture and to issue bonds. The SEU was created in 2007 for the purpose of, among other things, developing energy efficiency services. As such, the SEU plans to issue the bonds to pay the costs of projects which consist of the design, construction and installation of certain energy conservation measures at certain facilities operated by the agencies. The SEU is not limited to acting solely as a shell corporation facilitating financings, and we note that were the SEU to expand its operations, this could present additional risk.

The State of Delaware created the SEU to coordinate and promote the sustainable use of energy in the state. The SEU's statutory charge includes the use of competitive markets and leveraged private-financing to deliver cost-effective energy services. The SEU Authorizing Act creates an Oversight Board to ensure that the SEU meets responsibilities and performance targets enumerated in its contract with the Energy Office and to serve as the SEU's board of directors. This Act further establishes initial performance targets for the SEU as well as evaluation and monitoring mechanisms to ensure that energy savings are verifiable.

STRONG COVERAGE FROM STATE APPROPRIATIONS TO AGENCIES

The agencies and entities involved in the transaction could withstand severe budget cuts and still have no trouble making their installment payments. The Department of Corrections, for example, received $30 million in fiscal 2011 budgetary appropriations for energy, supplies and materials, contractual services, and capital outlay (the line items from which the installment payment can be made), providing over 8 times coverage of a likely annual installment payment of approximately $3.6 million. The other agencies and entities report even stronger coverage of installment payments by fiscal 2011 appropriated amounts available for installment payments to the trustee.

Outlook

As the rating on this transaction is notched off the state's general obligation rating, the outlook is the state's stable outlook, which reflects our belief that the combination of the state's strong structural governance features, speedy actions to deal with downward revenue revisions, the use of recurring solutions to solve gaps, a low-risk debt profile and high pension funding ratio will result in the state coming out of this recession in a strong position relative to its peers.

What could change the rating-DOWN

Page 2 of 4

7/18/2011http://www.moodys.com/research/MOODYS-ASSIGNS-INITIAL-RATING-OF-Aa2-TO-APPR...

--Significant decline in state appropriations available for debt service

--Any legislative changes that weaken the structure of the security

The principal methodology used in this rating was The Fundamentals of Credit Analysis for Lease-Backed Municipal Obligations published in October 2004. Please see the Credit Policy page on www.moodys.com for a copy of this methodology.

REGULATORY DISCLOSURES

For ratings issued on a program, series or category/class of debt, this announcement provides relevant regulatory disclosures in relation to each rating of a subsequently issued bond or note of the same series or category/class of debt or pursuant to a program for which the ratings are derived exclusively from existing ratings in accordance with Moody's rating practices. For ratings issued on a support provider, this announcement provides relevant regulatory disclosures in relation to the rating action on the support provider and in relation to each particular rating action for securities that derive their credit ratings from the support provider's credit rating. For provisional ratings, this announcement provides relevant regulatory disclosures in relation to the provisional rating assigned, and in relation to a definitive rating that may be assigned subsequent to the final issuance of the debt, in each case where the transaction structure and terms have not changed prior to the assignment of the definitive rating in a manner that would have affected the rating. For further information please see the ratings tab on the issuer/entity page for the respective issuer on www.moodys.com.

Information sources used to prepare the rating are the following: parties involved in the ratings, parties not involved in the ratings, and public information.

Moody's considers the quality of information available on the rated entity, obligation or credit satisfactory for the purposes of issuing a rating.

Moody's adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources Moody's considers to be reliable including, when appropriate, independent third-party sources. However, Moody's is not an auditor and cannot in every instance independently verify or validate information received in the rating process.

Please see ratings tab on the issuer/entity page on Moodys.com for the last rating action and the rating history.

The date on which some Credit Ratings were first released goes back to a time before Moody's Investors Service's Credit Ratings were fully digitized and accurate data may not be available. Consequently, Moody's Investors Service provides a date that it believes is the most reliable and accurate based on the information that is available to it. Please see the ratings disclosure page on our website www.moodys.com for further information.

Please see the Credit Policy page on Moodys.com for the methodologies used in determining ratings, further information on the meaning of each rating category and the definition of default and recovery.

Analysts

Emily Raimes Analyst Public Finance Group Moody's Investors Service

Edward Hampton Backup Analyst Public Finance Group Moody's Investors Service

Contacts

Journalists: (212) 553-0376 Research Clients: (212) 553-1653

Moody's Investors Service, Inc. 250 Greenwich Street New York, NY 10007 USA

Page 3 of 4

7/18/2011http://www.moodys.com/research/MOODYS-ASSIGNS-INITIAL-RATING-OF-Aa2-TO-APPR...

© 2011 Moody's Investors Service, Inc. and/or its licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ARE MOODY'S INVESTORS SERVICE, INC.'S ("MIS") CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MIS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS DO NOT CONSTITUTE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS ARE NOT RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. CREDIT RATINGS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MIS ISSUES ITS CREDIT RATINGS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources Moody's considers to be reliable, including, when appropriate, independent third-party sources. However, MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall MOODY'S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY'S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY'S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading "Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Any publication into Australia of this document is by MOODY'S affiliate, Moody's Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001.

Notwithstanding the foregoing, credit ratings assigned on and after October 1, 2010 by Moody's Japan K.K. (“MJKK”) are MJKK's current opinions of the relative future credit risk of entities, credit commitments, or debt or debt-like securities. In such a case, “MIS” in the foregoing statements shall be deemed to be replaced with “MJKK”. MJKK is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO.

This credit rating is an opinion as to the creditworthiness or a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be dangerous for retail investors to make any investment decision based on this credit rating. If in doubt you should contact your financial or other professional adviser.

Page 4 of 4

7/18/2011http://www.moodys.com/research/MOODYS-ASSIGNS-INITIAL-RATING-OF-Aa2-TO-APPR...

Research

Summary:

Sustainable Energy Utility Inc., Delaware; Appropriations

Rationale

The strong general credit quality of the State of Delaware (AAA/Stable);

The state's demonstrated commitment, within both the administrative and legislative branches, to repaying its appropriation-backed debt;

The strong contractual provisions, which include an absolute and unconditional payment provision upon annual appropriation; and

Annual payments that are date certain and not subject to acceptance.

The Department of Correction;

The Department of Services for Children, Youth and Their Families;

The Office of Management and Budget (OMB);

Delaware State University; and

Delaware Technical Community College.

Credit Profile

US$81.455 mil energy efficiency rev bnds (Delaware) ser 2011 Long Term Rating AA+/Stable New

RatingsDirect

18-Jul-2011

Current Ratings

Standard & Poor's Ratings Services assigned its 'AA+' long-term rating, and stable outlook, to the Sustainable Energy Utility Inc., Del.'s (SEU) energy efficiency revenue bonds, series 2011.

The rating reflects what we view as:

The bonds are being issued by SEU, a Delaware not-for-profit corporation created by and for the benefit of the State of Delaware pursuant to the Delaware Act, Del. Code Tit. 29 §8059 under a Trust Indenture between the SEU and Citibank N.A. Agency & Trust, New York, N.Y., as trustee.

We understand that bond proceeds will be used to fund projects consisting of the design, construction, and installation of certain energy conservation measures (ECM) at facilities of a number of state agencies inclusive of Delaware State University (the agencies). The funds will be used by various energy service companies that have contracted with the state through these agencies to implement the projects under the guaranteed energy savings agreements. The agencies that have entered these contracts for this issue are:

The bonds are limited obligations of the SEU payable solely from the trust estate. The trust estate includes installment payments made by OMB through a memorandum of understanding (MOU) between OMB and the various agencies. The installment payments are provided through an installment payment agreement with each agency and are subject to annual appropriations from the state. The SEU is a signatory and beneficiary of the MOU. The bonds are equally and ratably secured by the trust estate, and the failure of the state to appropriate sufficient funds to each of the agencies to make the installment payments will cause insufficient funds to be available to provide full debt service payments on the

Page 1 of 3[18-Jul-2011] Summary: Sustainable Energy Utility Inc., Delaware; Appropriations

7/18/2011https://www.globalcreditportal.com/ratingsdirect/showArticlePage.do?rand=7Uo1dWPt3n&article...

Outlook

Related Criteria And Research

Primary Credit Analyst: Richard J Marino, New York (1) 212-438-2058;[email protected]

Secondary Contact: Robin Prunty, New York (1) 212-438-2081; [email protected]

bonds. To insure sufficient funds are provided to the agencies the MOU provides that each agency will include in its annual budget request an amount, which fully satisfies its annual obligation under its installment payment agreement. Each agency will transfer the amount of its annual installment payments to OMB at the beginning of each fiscal year, and OMB will make payments directly to the trustee on behalf each agency.

Each agency's obligations under its installment payment agreement are absolute and unconditional, and not subject to counterclaim or offset. The installment payments do not depend upon guaranteed energy savings being achieved. The lack of a debt service reserve fund is offset by debt service payments not being made until two-and-a-half months have elapsed in the state's fiscal year. The SEU's interest in the MOU is assigned to the trustee and full assignment of all installment payments that cover debt service on the bonds has also been given to the trustee.

The state enacted the Energy Performance Contracting Act to encourage agencies to conserve energy by authorizing them to enter into guaranteed energy performance contracts for the design and installation of ECMs at their facilities. The act provides that the contract can be structured as an installment payment contract and that the financing of the ECMs might be implemented through a third party, such as SEU. Each agency participating in the program selected a pre-qualified contractor to perform an investment-grade energy audit of its facilities and recommend ECMs. The act requires an agency to allocate sufficient monies for each fiscal year to pay amounts payable under a performance contract, including a performance contract structured as an installment payment contract and permits an agency to use funds designated for operating, energy, or capital expenditures for any performance contract, including for purchases on an installment payment basis. The installment payment agreements are substantially the same for each agency, and we understand are date certain and not subject to project completion.

(For further information, see the full analysis on Delaware, published May 11, 2011, on RatingsDirect on the Global Credit Portal.)

The stable outlook on SEU reflects the stable outlook on Delaware's long-term general obligation bonds.

USPF Criteria: Appropriation-Backed Obligations, June 13, 2007

Complete ratings information is available to subscribers of RatingsDirect on the Global Credit Portal at www.globalcreditportal.com. All ratings affected by this rating action can be found on Standard & Poor's public Web site at www.standardandpoors.com. Use the Ratings search box located in the left column.

No content (including ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P. The Content shall not be used for any unlawful or unauthorized purposes. S&P, its affiliates, and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions, regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold, or sell any securities or to make any investment decisions. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P's opinions and analyses do not address the suitability of any security. S&P does not act as a fiduciary or an investment advisor. While S&P has obtained information from sources it believes to

Page 2 of 3[18-Jul-2011] Summary: Sustainable Energy Utility Inc., Delaware; Appropriations

7/18/2011https://www.globalcreditportal.com/ratingsdirect/showArticlePage.do?rand=7Uo1dWPt3n&article...

be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

Any Passwords/user IDs issued by S&P to users are single user-dedicated and may ONLY be used by the individual to whom they have been assigned. No sharing of passwords/user IDs and no simultaneous access via the same password/user ID is permitted. To reprint, translate, or use the data or information other than as provided herein, contact Client Services, 55 Water Street, New York, NY 10041; (1) 212-438-7280 or by e-mail to: [email protected].

Copyright © 2011 Standard & Poor’s, a division of The McGraw-Hill Companies. All Rights Reserved.

Page 3 of 3[18-Jul-2011] Summary: Sustainable Energy Utility Inc., Delaware; Appropriations

7/18/2011https://www.globalcreditportal.com/ratingsdirect/showArticlePage.do?rand=7Uo1dWPt3n&article...

Market Commentary

Citi Investment Research & Analysis is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Citigroup Global Markets

North America

22 July 2011 │ 21 pages

Municipal Market Comment Issuance Could be Dampened by Market Volatility

Uncertainty surrounding the debt ceiling battle has yet to be resolved and the Treasury market has been highly volatile, but range-bound.

Despite the uncertainties surrounding these issues, the municipal bond market stayed in an even narrower track while handling the heaviest calendar of 2011.

There are three sets of most likely potential outcomes for the debt ceiling/deficit reduction crisis: no deal, a small deal with likely Treasury downgrades, and a larger deal that could lead to major spending cuts.

Each of these scenarios presents different challenges for the municipal market though the larger deal presents the greatest challenge as access to the tax-exempt bond market for new issues could be curtailed or eliminated at some point in the process.

We discuss some of the key myths and realities surrounding the muni market that ought to be considered as the process moves forward.

BABs continue to perform well, showing their defensive characteristics. MCDS spreads have widened, as if investors are forgetting about the Lehman overhang.

Crossover high-grade and derivatives investors are unlikely to get out of their muni positions, but high-yield investors could certainly start angling for an exit.

Current Recommendations in this issue:

– BAB credit OAS curves are inverted; buy 10-20-YR bonds versus the long end

– Overweight high-grade taxable university bonds versus Treasuries

– Overweight high-quality revenue bonds versus Treasuries

Municipals

See Appendix A-1 for Analyst Certification, Important Disclosures and non-US research analyst disclosures.

George Friedlander +1-212-723-4451 [email protected]

Mikhail Foux +1-212-723-9353 [email protected]

Vikram Rai +1-212-723-1834 [email protected]

Municipal Market Comment 22 July 2011

Citigroup Global Markets 2

Issuance Could be Dampened by Market Volatility 3 Summary and Opinion 3 Munis Face Up to Volume and Confusion 3 Demand Patterns 5 The Debt Ceiling Crisis: Three Distinct Scenarios 6 Deficit Reduction Could Curtail New Tax-Exempt Issuance 8 Special Focus: Myths That Magnify the Threat to Tax Exemption for Newly Issued Bonds 9

Introduction 9 Myth #1: The muni market provides an inefficient subsidy 9 Myth #2: Taxable tax credit bonds could effectively replace tax-exempt bonds as a form of support for state and local issuers. 10 Myth #3: Subsidies for state and local issuance are dangerous because low borrowing costs lead issuers to "overspend." 10 Myth #4: Taxable Build America Bonds could never provide an efficient subsidy for state and local projects because the buyers of taxable munis are primarily non-taxed entities. 10 Myth #5: Funding for state and local projects is ample, whether they are subsidized or not. 11 Myth #6: Anything that can be done to reduce the federal deficit will ultimately auger to the benefit of state and local governments as well. 11

Quantitative Municipal Strategies 12 Crossover Investors Not Running for an Exit 12 Recommend 10-20-YR BABs 14 US Municipals Strategy Portfolio 15

MMD Rate and Curves 15 Derivatives 16

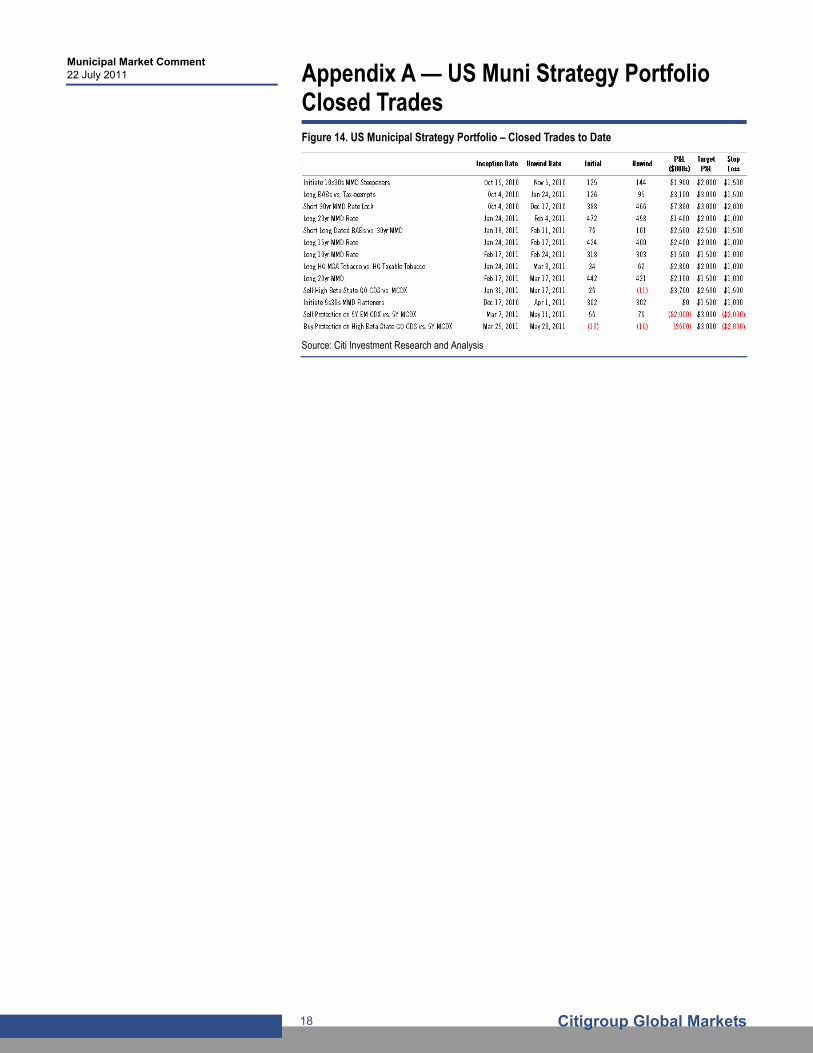

Trades Opened Since Last Publication 17 Trades Closed Since Last Publication 17 Appendix A — US Muni Strategy Portfolio Closed Trades 18 Appendix A-1 19

Contents

Municipal Market Comment 22 July 2011

Citigroup Global Markets 3

Summary and Opinion

Municipal bond investors surely cannot ignore the ongoing battles over the debt ceiling and deficit reduction. The worst case, which we continue to classify as an unlikely outcome, would be that no deal can be achieved to increase the debt ceiling by August 2, throwing the capital markets into chaos and creating new credit risks associated with a sharply weaker economy.

There appear to be two other potential scenarios, both with implications for munis. The first is that a very modest deficit reduction package is the best that can be achieved and that at least one agency, Standard & Poor's, goes ahead with its threat to reduce the rating on US debt to the double-A range in the absence of meaningful long-term deficit reduction. The second alternative scenario is that Congress and the administration get serious about achieving meaningful deficit reduction, either as part of a deal to raise the debt ceiling or shortly thereafter.

It is this latter case that has some important implications for tax-exempt bond investors: Under this scenario, there is a more-than-zero possibility that issuance of new tax-exempt municipal bonds could be sharply curtailed. This possible outcome, in our view, plays strongly into the case for extending maturity within tax-exempt portfolios: If this outcome occurs, the value of existing long-term munis could increase substantially, as shortages of new tax-exempt debt rapidly develop. Under this scenario, long-term bonds, particularly in sectors viewed as "essential service" or as important stand-alone transportation facilities, would appear to be particularly attractive purchases. There are, of course, a number of less-extreme potential outcomes, none of which contradict our view that there is attractive value in:

Longer intermediate maturities (8-16-YR or so);

High-coupon callable bonds, known as "cushion" or "kicker" bonds; and

Highly rated zero-coupon bonds, including some issued for California school districts, which yield 100bp more than longer-maturity current-coupon bonds.

Munis Face Up to Volume and Confusion

Municipal bond market participants would justified about feeling nervous coming into the past week. Volume for the week was the highest so far in 2011, at $8.3 billion, according to preliminary Bond Buyer estimates. The Treasury market was caught in a tug-of-war between the dueling crises provided by the debt ceiling mess in Washington and the concerns about other sovereign credits emanating from Europe. And yet, the muni market was largely unchanged for most of the week, before edging very slightly higher in yield on Thursday.

Figure 1. AAA General Obligation Yields

Source: Citi Investment Research and Analysis

Issuance Could be Dampened by Market Volatility

George Friedlander

+1-212-723-4451

Vikram Rai

+1-212-723-1834

Volume for the week was the highest so

far in 2011, at $8.3 billion, according to

preliminary Bond Buyer estimates.

Municipal Market Comment 22 July 2011

Citigroup Global Markets 4

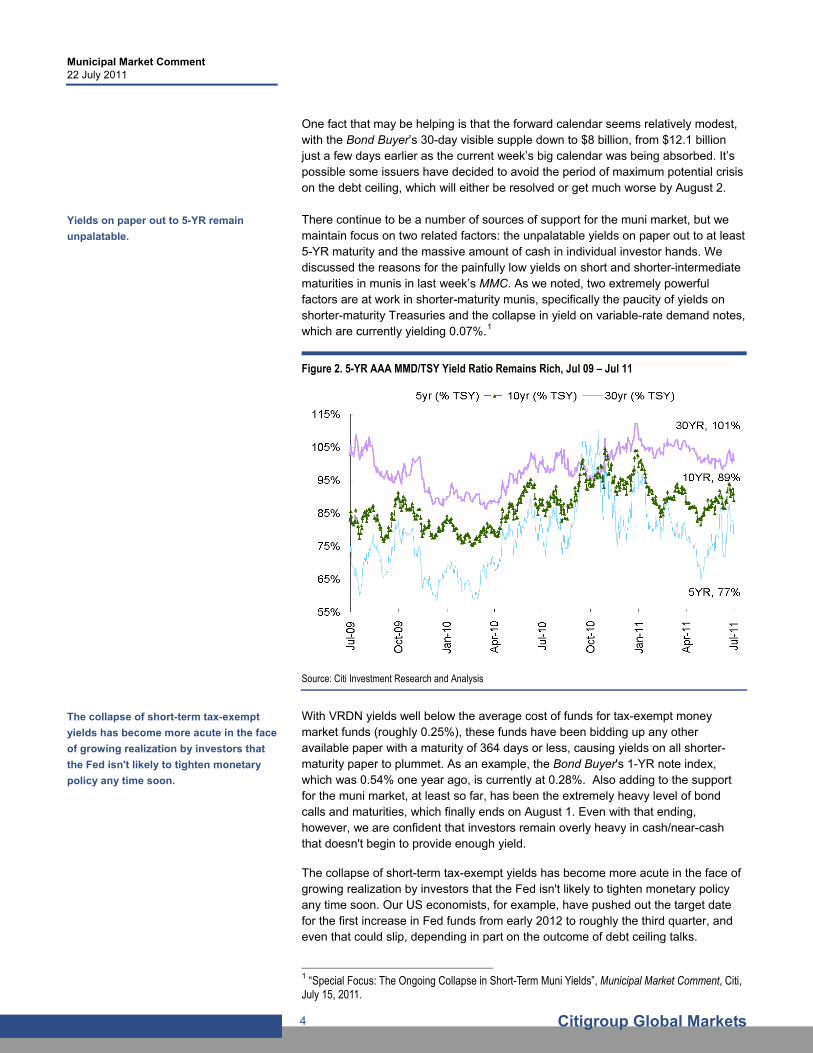

One fact that may be helping is that the forward calendar seems relatively modest, with the Bond Buyer’s 30-day visible supple down to $8 billion, from $12.1 billion just a few days earlier as the current week’s big calendar was being absorbed. It’s possible some issuers have decided to avoid the period of maximum potential crisis on the debt ceiling, which will either be resolved or get much worse by August 2. There continue to be a number of sources of support for the muni market, but we maintain focus on two related factors: the unpalatable yields on paper out to at least 5-YR maturity and the massive amount of cash in individual investor hands. We discussed the reasons for the painfully low yields on short and shorter-intermediate maturities in munis in last week’s MMC. As we noted, two extremely powerful factors are at work in shorter-maturity munis, specifically the paucity of yields on shorter-maturity Treasuries and the collapse in yield on variable-rate demand notes, which are currently yielding 0.07%.1

Figure 2. 5-YR AAA MMD/TSY Yield Ratio Remains Rich, Jul 09 – Jul 11

Source: Citi Investment Research and Analysis

With VRDN yields well below the average cost of funds for tax-exempt money market funds (roughly 0.25%), these funds have been bidding up any other available paper with a maturity of 364 days or less, causing yields on all shorter-maturity paper to plummet. As an example, the Bond Buyer's 1-YR note index, which was 0.54% one year ago, is currently at 0.28%. Also adding to the support for the muni market, at least so far, has been the extremely heavy level of bond calls and maturities, which finally ends on August 1. Even with that ending, however, we are confident that investors remain overly heavy in cash/near-cash that doesn't begin to provide enough yield.

The collapse of short-term tax-exempt yields has become more acute in the face of growing realization by investors that the Fed isn't likely to tighten monetary policy any time soon. Our US economists, for example, have pushed out the target date for the first increase in Fed funds from early 2012 to roughly the third quarter, and even that could slip, depending in part on the outcome of debt ceiling talks.

1 “Special Focus: The Ongoing Collapse in Short-Term Muni Yields”, Municipal Market Comment, Citi, July 15, 2011.

Yields on paper out to 5-YR remain

unpalatable.

The collapse of short-term tax-exempt

yields has become more acute in the face

of growing realization by investors that

the Fed isn't likely to tighten monetary

policy any time soon.

Municipal Market Comment 22 July 2011

Citigroup Global Markets 5

Demand Patterns

Bond fund flows remained slightly positive this week, with long-term funds showing outflows once again. Nevertheless, we are at least a bit optimistic about the results from Lipper/AMG. All weekly reporting funds showed inflows of $123 million for the week ended 7/20, down from $367 million the prior week. Flows in intermediate funds dropped fairly sharply, to $98 million, from $382 million. Long-term funds had outflows of $137 million, down from $157 million the week before. And high-yield funds remained in modestly positive territory, at $97 million, versus $67 million the prior week.

Figure 3. All Muni Bond Fund Flows (Four Week Average), Inching Up Figure 4. Weekly Long Term Muni Bond Flows Remain Dismal

Source: Citi Investment Research and Analysis Source: Citi Investment Research and Analysis

The reasons for our cautious optimism are threefold. First, we believe that fund investors, in particular, were spooked by the ongoing confusion in Washington and by the Euro crises. According to Lipper, both taxable bond funds and equity funds saw a substantial decline in inflows this week versus the prior two weeks. Any settling down of the external crises may lead to better data, we suspect. Second, outflows now appear to be limited largely to one or two fund families. And third, during this week's heavy calendar, funds were among the buyers for a number of the major new deals.

In the meantime, buying by direct retail investors remains solid in three ways. First, the net buys of odd-lots from the MSRB daily feed has declined modestly from recent peaks but remains extremely solid. Second, we continue to see a willingness to do extension swaps out of our least-favored 1-5-YR range into longer, higher-yielding maturities. Finally, bona fide retail orders taken during the retail order periods for this week's heavy new issue calendar saw very solid demand on nearly all deals. Clearly, had direct retail not been active over the past week, the $8.3 billion or so of new issues would have caused a substantial upward adjustment in yields, but that was not the case. And all of this happened in the midst of the twin crises over Greece and the European Union and the still-extant crisis over the need to raise the debt ceiling.

Clearly, had direct retail not been active

over the past week, the $8.3 billion or so

of new issues would have caused a

substantial upward adjustment in yields.

Municipal Market Comment 22 July 2011

Citigroup Global Markets 6

The Debt Ceiling Crisis: Three Distinct Scenarios

Both Standard & Poor's and Moody's have responded aggressively to the ongoing risks and complexities generated by the need to raise the debt ceiling by August 2, give or take a day. On July 13, Moody’s had warned that the United States could lose its Aaa rating if there is a default due to failure to raise the debt ceiling by August 2. (The agency also suggested that it might act before the actual "drop dead" date of August 2, but it is not certain that it would do so.)

On Tuesday, July 19, Moody’s said that five states — Maryland, New Mexico, South Carolina, Tennessee and Virginia, totaling about $24 billion in GO debt outstanding — of the 15 currently rated triple-A were targeted for a potential downgrade due to their fiscally sensitive relationship with the US sovereign credit. “Should the U.S. government’s rating be downgraded to Aa1 or lower, these five states’ ratings would likely be downgraded as well,” Moody’s said.

A Moody's analyst was quoted in the Bond Buyer as saying that the risk factors tying these five states, in particular, to the federal triple-A are macroeconomic sensitivity, capital markets reliance and dependence on federal revenues. The agency, however, noted that these five states remain strong credits, as a result of financial resources available to counteract those risks.

In our view, however, Standard & Poor's has taken a more aggressive and comprehensive approach to this particular crisis because:

1. S&P has made it clear that there is a substantial risk of a downgrade of US Treasury debt even if a debt ceiling deal is reached, if that deal does not incorporate a substantial down payment toward reducing the size of the US's current and projected annual deficit.

The agency parsed the outlook for US Treasury debt into three distinct sets of potential outcomes:

A worst case, under which Congress does not reach a deal to raise the debt ceiling by August 2;

An intermediate case, under which there is an agreement to raise the debt ceiling on a timely basis but no substantial progress made to put an agreement in place to cut future deficits through a combination of spending cuts and revenue increases; and

A better case, under which substantial progress is made toward reducing future deficits. Earlier S&P reports explicitly put the magnitude of cuts needed to achieve this best case at $4 trillion over 10 years, but the most recent reports simply spoke about the need for the administration and Congress to achieve an agreement to raise the debt ceiling and successfully collaborate on a long-term framework for fiscal consolidation.

Only under this third scenario, according to the agency, would the triple-A rating of Treasury and related debt be confirmed. Under the first scenario, Treasury soon misses a payment, resulting in an SD (Selective Default) rating, followed by a confirmation in the double-A range once the ceiling is raised and debt repayment restarts. Under the second scenario, the rating would be lowered to the double-A range, but the timing is more uncertain.

Moody’s has also suggested that it might

act before the actual "drop dead" date of

August 2.

In the worst case scenario, the Treasury

misses a payment, resulting in an SD

(Selective Default) rating, followed by a

confirmation in the double-A range once

the ceiling is raised and debt repayment

restarts.

Municipal Market Comment 22 July 2011

Citigroup Global Markets 7

2. S&P has parsed the outcome for a wide range of capital market credits under the three potential scenarios. For the municipal bond market in particular, S&P published a special report, titled "Where U.S. Public Finance Ratings Could Head in the Wake of the Federal Fiscal Crisis."2 While the report is far too detailed to summarize comprehensively here, we believe that it is important to make a few observations. These include the following:

The better case scenario, under which Congress and the administration get serious about the need to sharply reduce the size of projected annual deficits, is not uniformly good news for municipal issuers in terms of the ratings outlook, even though only under this scenario would the US debt rating be confirmed at triple-A. This outcome could, ironically, be the most negative for the ratings of some public finance issuers over the near term because of the potential sharp cut in outlays that affect their operations. The agency notes, however, that impact differs depending upon which outlays are cut (Social Security versus Medicare versus military). Nevertheless, after having publicly embraced this scenario, the agency concedes that it could slow growth for years to come, causing lower ratings in some sectors to occur over time.

Under the intermediate case, the rating implications for state and local issuers over the near-term appear to not be as severe as under the "better case," even though under this case, according to the agency, the rating on US debt is very likely to be downgraded to the double-A range.

S&P is more emphatic about the negative implications of the worst case, under which no agreement is reached by August 2 and the Treasury misses payments on some of its debt. According to the Agency, the Treasury soon misses a payment and rating goes to SD (Selective Default). World credit markets seize up, and equity markets fall sharply. When the credit markets reopen, interest rates are significantly higher. The dollar loses 10% or more of its value. When the debt payment recommences in full, the US ratings drop to AA/A-1+/negative outlook. Investors seek new, risk-free alternatives (including possibly some munis). Under this scenario, there would be many state downgrades and, at the local level, concerns about variable-rate demand notes and more questions about ability to pay.

S&P notes that, in many sectors, under all three scenarios, ratings would have to be examined on a case-by-case basis. However, one pattern stands out in looking at the Agency’s views on implications of all three scenarios: The sectors that appear to be in the least jeopardy for rating reductions are essential service utility revenue bonds and important stand-alone transportation facilities.

The bottom line is that, with the series of reports published in conjunction with its examination of the debt ceiling crisis, S&P has begun to articulate a view that the federal/state/local "compact" is under pressure, regardless of how the federal government begins to deal with the challenges created by massive projected federal deficits, with credit implications for many issuers on a case-by-case basis as a consequence.

2 “Where U.S. Public Finance Ratings Could Head In The Wake Of The Federal Fiscal Crisis”, Steven J Murphy et. al., Standard & Poor’s, July 21, 2011.

The better case scenario could ironically,

be the most negative for the ratings of

some public finance issuers over the

near term.

S&P notes that, in many sectors, under

all three scenarios, ratings would have to

be examined on a case-by-case basis.

Municipal Market Comment 22 July 2011

Citigroup Global Markets 8

Deficit Reduction Could Curtail New Tax-Exempt Issuance

It is important to begin our discussion of this topic by stressing that absolutely nothing is being considered by Congress or the administration as part of deficit reduction that would eliminate or curtail the tax-exempt status of interest on state and local bonds that were initially issued as tax-exempt. Indeed, the scenario we will be describing below substantially strengthens the case for purchasing longer-maturity tax-exempt bonds, including but not limited to the two sectors noted above — essential service utilities and strong stand-alone transportation facilities.

Having said that, we believe that it is important to note that, in our view, the tax-exempt status for some or all newly issued municipal bonds, after some future date, is in the most jeopardy than it has been since the 1986 tax reform bill, which curtailed a number of types of issuance and made other types of new issues subject to the Alternative Minimum Tax for the first time. The reason for our concern about the tax exemption stems from several sources.

First, the "Gang of Six" plan to reduce the deficit had significant bipartisan support, even though we do not expect it to be enacted for a variety of reasons, including the artificial nature of some of its assumptions regarding tax cuts. This plan was modeled in large part on the Bowles-Simpson plan developed by The National Commission on Fiscal Responsibility and Reform.3 Under this plan, all newly issued state and local debt would come as taxable bonds, but without the subsidy provided for Build America Bonds issued in 2009-2010 as part of the stimulus bill. The elimination of this tax exemption would, in effect, be a source of revenue under the Commission’s deficit reduction package.